Seeding the College Dream Final Report: An EvaluaƟon of the Child Support for College Asset-Building IniaƟve December 2013 The University of Texas at AusƟn Lyndon B. Johnson School of Public Affairs

Transcript

Seeding the College Dream

Final Report: An Evalua on of the Child Support for College Asset-Building Inia ve

December 2013

The University of Texas at Aus nLyndon B. Johnson School of Public Affairs

Final Report: An Evaluation of the Child Support for College Asset-Building Initiative

CS4C: Final Evaluation Report December 2013 Page 2 of 164

EXECUTIVE SUMMARY

The importance of a college education has risen dramatically in recent decades. Individuals with a college degree have higher paying jobs, increased career flexibility, and are less likely to be unemployed; meanwhile, broad shifts in the U.S. economy continue to trim the number of jobs available to those without a college degree, further amplifying the significance of higher education. Though many parents recognize the importance of sending their children to college, financing a college education has also become increasingly difficult. Tuition costs continue to climb, raising the barrier to entry and saddling many low- and middle-income students with substantial student loan debt. This report presents evaluation outcomes from the Child Support for College (CS4C) pilot program, an innovative collaboration between public and private entities developed to promote college savings and attendance among those in the Texas child support system through incentivized college savings accounts. Throughout the 18-month pilot, CS4C encountered a number of successes and challenges. Though the program struggled to attract the interest of potential participants, over one-third of individuals who inquired about the program received at least one financial coaching session, and two-thirds of these individuals opened college savings accounts. Over the course of the pilot, significant changes were made to the incentive structure and participation requirements. These changes resulted in considerable increases in the number of account openings, as well as a reduced lag between inquiry and account opening. For many of those who opened accounts, CS4C also marked the beginning of college savings, a process which research indicates may carry important psychological benefits for account openers who now believe their child will go to college – a vital element to college success. Participants were motivated to participate in CS4C primarily by a desire for their children to pursue higher education and a commitment to helping their children achieve this goal; in addition, participants cited the importance of CS4C savings incentives as a catalyst in their decision to open an account. Participants were not significantly motivated, however, by the receipt of a lump sum child support payment as originally hypothesized. In fact, participants who failed to open accounts often cited inconsistent child support and insufficient money as substantial barriers to participation, and those who opened accounts tended to have higher income and education than those who did not. The CS4C program also revealed several programmatic lessons that will advance the field of asset building as a strategy for college savings. For example, through the pilot, program partners learned the limits to the guidance that financial coaches can provide clients, leading to a push for new policies around financial coaching. Moreover, CS4C revealed the importance of carefully aligning the program design with the core principles of asset building. Although the program aligned with the basic tenets of asset building in many respects, CS4C also inadvertently incorporated adverse incentive structures and a number of barriers to account opening. As these barriers were removed, more accounts were opened. Finally, this pilot highlights the need to ensure consistency between program goals and the existing goals of participating institutions to facilitate long-term sustainability.

CS4C: Final Evaluation Report December 2013 Page 3 of 164

Introduction

In recent decades, college has become increasingly important to earnings potential, upward mobility, and a host of positive life outcomes. At the same time, college has also become increasingly expensive, fueling a rapid escalation in student loan debt and borrower default rates. These developments have significantly raised the barrier to entry for many low- to middle-income students, prompting a national conversation around alternative methods of bringing a college education within reach of today’s low-income families. Alongside these trends, the U.S. Department of Health and Human Services (HHS) developed the ASSET Initiative to integrate financial education and asset-building strategies into the core functions of partner agencies and organizations—a measure aimed at strengthening the long-term financial stability of low-income families, including their ability to save for post-secondary education. This initiative gave rise to several demonstration waiver projects funded by the Office of Child Support Enforcement (OCSE); as part of one of these projects, the Child Support for College (CS4C) pilot program is an innovative collaboration between state-level partners, local nonprofits, private entities, and the Texas Office of the Attorney General, Child Support Division (OAG). The CS4C program applies the incentives of asset building to lump sum transfers within the child support population, a largely untapped intersection that helps marry the twin goals of boosting college savings and promoting educational advancement and self-sufficiency among a traditionally lower-income population. Because the program has little precedent, program partners contracted with the Child and Family Research Partnership (CFRP) at The University of Texas at Austin to evaluate the influence of the program on a range of outcomes related to college savings and financial literacy. This report presents research findings from the 18-month pilot of CS4C, and addresses four overarching questions in connection with the goals of the program: 1) Who participated in CS4C?, 2) What were the motivations and barriers to program participation?, 3) What are the benefits to participating in CS4C?, and 4) What lessons can be learned from the program design and implementation? In addition, CFRP addresses several related topics, including the development of CS4C’s program and incentive structures, how these structures appeared to impact account opening and savings outcomes, characteristics of participants at various program stages, whether the program is associated with increases in financial literacy, whether participants made progress toward meeting their financial goals, and lessons for program replication on a larger scale. PRIMARY FINDINGS

Overall, the CS4C program was successful in many respects. Of the 298 individuals who inquired about the program, one-third (99) received at least one financial coaching session, and nearly two-thirds of those receiving financial coaching (63) opened college savings accounts. Moreover, CS4C marked the beginning of college savings for most account openers. Although the dollar amount that many families deposited was relatively low, the mere act of opening an account generated psychological benefits for many account openers who now believe their child will go to college and have made a financial commitment, however small, toward realizing that goal. The psychological impact of saving for college is underlined by prior research, which suggests that the act

CS4C: Final Evaluation Report December 2013 Page 4 of 164

of setting aside designated college savings—even in very small amounts—yields a belief in the attainability of college and is linked to significantly higher rates of enrollment and graduation. The CS4C program also revealed several programmatic lessons learned that will advance the field of asset building as a strategy for college savings. For example, through the pilot, program partners learned the limits to the guidance that financial coaches can provide clients, and this knowledge has led to a push for new policies for financial coaches. Moreover, CS4C revealed the importance of carefully aligning the program design with the core principles of asset building. Although the program aligned with the basic tenets of asset building in many respects, CS4C also inadvertently incorporated adverse incentive structures and a number of barriers to account opening. As these barriers were removed, more accounts were opened. Finally, this pilot highlights the need to ensure consistency between program goals and the existing goals of participating institutions to facilitate long-term sustainability. OUTLINE

The remainder of this report is organized as follows. First, we highlight several relevant trends in the domain of higher education, including changes in tuition costs, savings behavior, student loan debt, and borrower default rates. The subsequent section explores the use of asset-building strategies as an additional option for promoting college savings among low-income savers, with particular emphasis on the proliferation of college savings incentives by state-level policymakers and organizations. In the following section, we discuss the theoretical motivations behind CS4C, including the impetus to capitalize on lump sum transfers within the child support population as a point of intervention for promoting college savings. We also outline the program’s basic elements, including program partners, program stages, how the program evolved over time, and the evaluation strategy employed by CFRP. The subsequent section presents findings of the evaluation, followed by a discussion of lessons learned and relevant considerations for the broader work of asset-building policy.

Background

COLLEGE IS IMPORTANT

College has become increasingly vital to individual earnings potential, social mobility, and a wide range of life outcomes. In 2002, individuals with a bachelor’s degree earned an average of 75 percent more than those with a high school diploma over the course of their lifetimes. By 2011, that premium had grown to 84 percent, or a full $1 million difference in lifetime earnings.1 Other studies suggest this growing gap in earnings is accompanied by a host of other benefits, including lower levels of unemployment, improved access to health insurance and pension benefits, higher job satisfaction, healthier lifestyles, and increased civic participation.2 Structural changes in the economy also highlight the growing importance of a college degree. In 2010, workers with at least some postsecondary education and training held 59 percent of U.S. jobs.3 By 2020, these workers will hold 65 percent of jobs, leaving an increasingly narrow share of employment for those with a high school diploma or less.4

CS4C: Final Evaluation Report December 2013 Page 5 of 164

DISPARITIES IN COLLEGE ENROLLMENT AND COMPLETION

Despite the growing importance of college, only 41 percent of all 18- to 24-year-olds were enrolled in postsecondary education in 2012.5 Moreover, these rates are not uniform across demographic groups; minority and low-income youth enroll in college at significantly lower rates than their white and high-income counterparts. The racial gap in college enrollment between white and black students, as well as between white and Hispanic students, has been well-documented throughout the literature.6 Despite the decades-long persistence of these racial disparities, recent trends suggest the racial gap in enrollment may be narrowing. Among 18- to 24-year-olds in 2012, 42.1 percent of white youth, 35.8 percent of black youth, and 37.5 percent of Hispanic youth were enrolled in college. This 5-6 point discrepancy is an improvement over previous years when the racial gap in college enrollment stood at 12-18 percentage points7; still, these numbers obscure two related trends that suggest racial disparities in higher education are yet to be solved. One such trend is the enduring discrepancy between the types of institutions where white and minority students enroll. Minority enrollment continues to be concentrated in the lower tiers of postsecondary education, at two-year community colleges and technical schools, rather than four-year institutions.8 Moreover, even where minority groups do attend four-year institutions, they are less likely to graduate. Among full-time students enrolled at four-year institutions, minority students lag behind whites in bachelor’s degree attainment by a margin of roughly 20 percentage points—a gap that has persisted for over two decades.9 Many of the racial inequities in college enrollment are mirrored in comparisons of enrollment by income level. Studies focused on enrollment rates at four-year institutions, for example, show the gap in college enrollment by income group is widening as low-income students forgo bachelors programs in favor of more affordable two-year colleges.10 Low-income high school graduates are also less likely to immediately enroll in college than their high-income counterparts, a gap that has exceeded 20 percentage points since at least 1972.11 Recent developments, however, show signs of improvement; the gap in immediate college enrollment rates between youth in the top and bottom income quintiles contracted from 41 percentage points in 1995 to 25 percentage points in 2008.12 Yet even where low-income students enroll, they continue to graduate at only half the rate of their high-income counterparts—a stubborn rift in college completion that continues to grow.13 Theories vary on the mechanisms underlying these persistent gaps; one early theory, that these gaps can be explained by differing levels of educational preparation, appears incomplete. Prior literature shows that accounting for students’ cognitive abilities and academic achievement in estimates of college enrollment rates lessens, but does not eliminate, the gap in college entry between top and bottom income quartiles.14 As a result, several researchers have identified the expense of college as one substantial barrier to minority and low-income students’ enrollment—an expense that has risen substantially in recent decades.15

CS4C: Final Evaluation Report December 2013 Page 6 of 164

COLLEGE IS EXPENSIVE

Since 1978, college tuition and fees have increased by 1,120 percent, more than four times the rate of the consumer price index.16 Perhaps not surprisingly, this surge in cost has disproportionately impacted low-income families; in the early 1970s, a family in the lowest income quintile would have to contribute 42 percent of their income to pay for the cost of a public four-year institution. By the 2000s, that family would need to contribute 60 percent of their income for the same degree. In contrast, the amount that a family in the highest income quintile would need to contribute increased by just 1 percentage point, from 5 to 6 percent.17 Though tuition costs in Texas are still relatively affordable by national standards, they too have been on the rise. For the 2012-2013 school year, the average published tuition and fees at Texas four-year public institutions was $8,354, fully 18 percent higher than five years before.18 The acceleration was similar at public two-year institutions, which climbed 17 percent to an average cost of $2,131 for the 2012-2013 school year.19 PARENTS WANT TO SAVE BUT MANY DO NOT

Despite the rising costs, most parents still believe in the importance of college. Overall, more than 8 in 10 parents agree that college is an investment in their child’s future, that college is part of the American dream, and that a college degree is more important now than it used to be.20 These attitudes are especially common among low-income parents. Households making less than $35,000 per year are consistently more likely than wealthier households to strongly agree on questions related to the importance of college.21 Low-income parents also cite saving for college as their number one savings priority,22 and are more likely than any other income group to say they would be willing to stretch themselves financially to obtain the best opportunity for their child’s future.23 In spite of these laudable goals, only 37 percent of low-income families have started saving for their child’s education.24 In 2012, these families saved 6 percent of their incomes, double the proportion saved by middle- and high-income families. Still, projections show this is not likely to be enough. On average, low-income parents expect to pay 22 percent of total college costs from their own savings and income (not including the student’s savings and income). This expectation is remarkably close to reality; low-income parents currently pay 21 percent of total college costs from their own savings and income.25 At a four-year public college this expected cost would translate to a total of $30,586, yet based on current savings habits, low-income parents are projected to save less than one-third of that amount ($9,432).26 These projected shortfalls are not unique to low-income parents. Despite rising tuition costs, the percentage of parents saving for their child’s college education slipped from 60 percent in 2010, to 50 percent in 2012.27 Only one-third of parents have a plan to pay for college, and when asked to describe their feelings on the subject, many parents report feeling overwhelmed, frustrated, scared, or that they do not like thinking about it at all.28 Among low-income parents not saving for college, 7 in 10 cite not having enough money as a major (55%) or minor (15%) reason. And half of these parents report an expectation that their child will qualify for enough in scholarships and financial aid to cover the costs.29

CS4C: Final Evaluation Report December 2013 Page 7 of 164

Unfortunately however, scholarship and aid receipt may not bridge this savings gap for many parents. Though roughly 6 in 10 students received some type of scholarship or grant in academic year 2011-12, those grants covered an average of just 29 percent of total college costs.30 Low-income students tend to receive higher grant awards than their wealthier peers; during the 2007-2008 school year nearly 9 out of 10 full-time dependent students with parental incomes under $40,000 received an average grant amount of $8,600 compared to $4,900 for the student population at large.31 Though hugely beneficial to grant recipients, these amounts are unlikely to cover college costs by themselves. In fact, according to some estimates, only 0.3 percent of students enrolled full time at four-year colleges receive enough money from grants (including federal, state, institutional, and private) to cover the full cost of attendance.32 TRENDS IN STUDENT LOAN DEBT AND BORROWER DEFAULT RATES

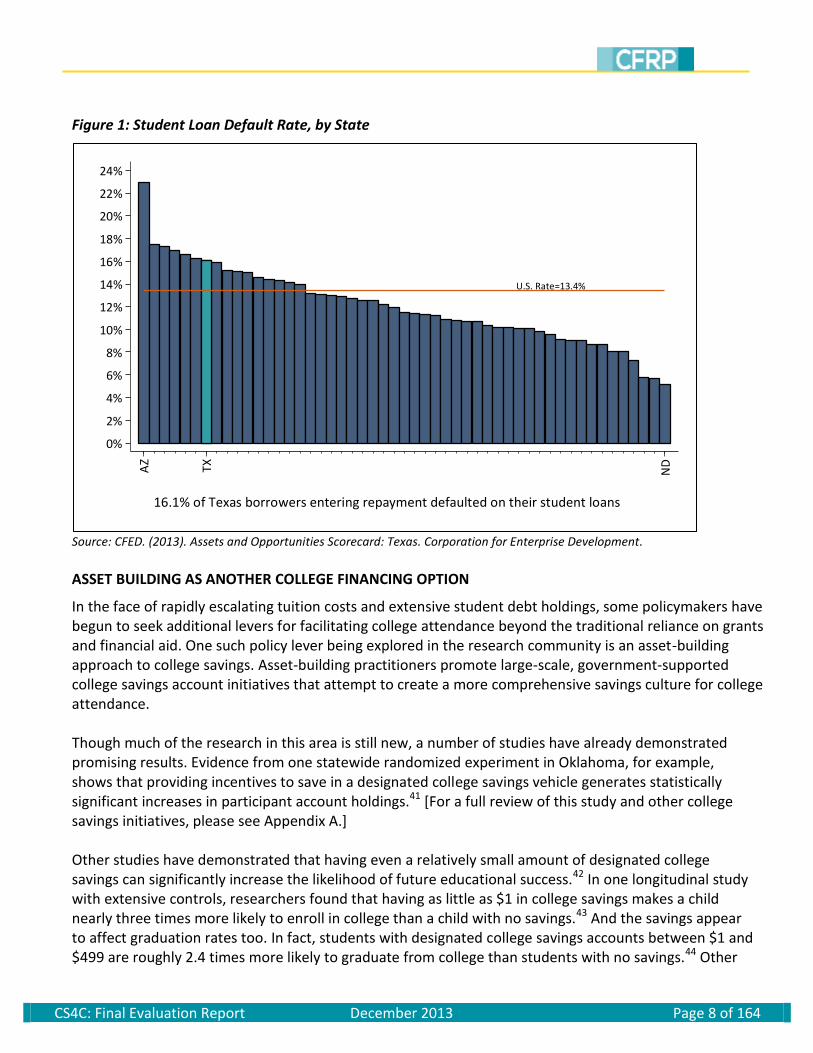

For students who have not amassed enough in savings and grants, loans increasingly make up the difference. Nationally, 67 percent of bachelor’s degree recipients used student loans to pay for their education.33 In 2005, the average U.S. student loan debt totaled $17,233. By 2012, that number had climbed to $27,253—an increase of 58 percent in just seven years.34 Naturally, the increase in debt has been paralleled by a rise in the delinquency rate on student loans, which rose almost 22 percent between 2007 and 2012.35 Today, nearly 1 in 7 borrowers defaults on his or her student loans.36 Trends in Texas have followed a similar pattern. Roughly 56 percent of Texas college graduates carry student loan debt, with the average liability totaling $22,140.37 To pay off this debt under the standard repayment plan, an individual would need to make monthly payments of $254.79 over 10 years for a total of $30,574.54 (including interest). a38 Graduates on a monthly repayment plan who fail to make a loan repayment for 270 days go into default.39 With a 16.1 percent borrower default rate, Texas ranks 45th in the U.S. on student loan defaults [Figure 1].40

a Calculation assumes borrower has an unsubsidized federal loan with an interest rate of 6.8%. For a subsidized loan with an

interest rate of 3.4%, monthly payments would be slightly lower at $217.90 over 10 years for a total of $26,147.72.

CS4C: Final Evaluation Report December 2013 Page 8 of 164

Figure 1: Student Loan Default Rate, by State

Source: CFED. (2013). Assets and Opportunities Scorecard: Texas. Corporation for Enterprise Development.

ASSET BUILDING AS ANOTHER COLLEGE FINANCING OPTION

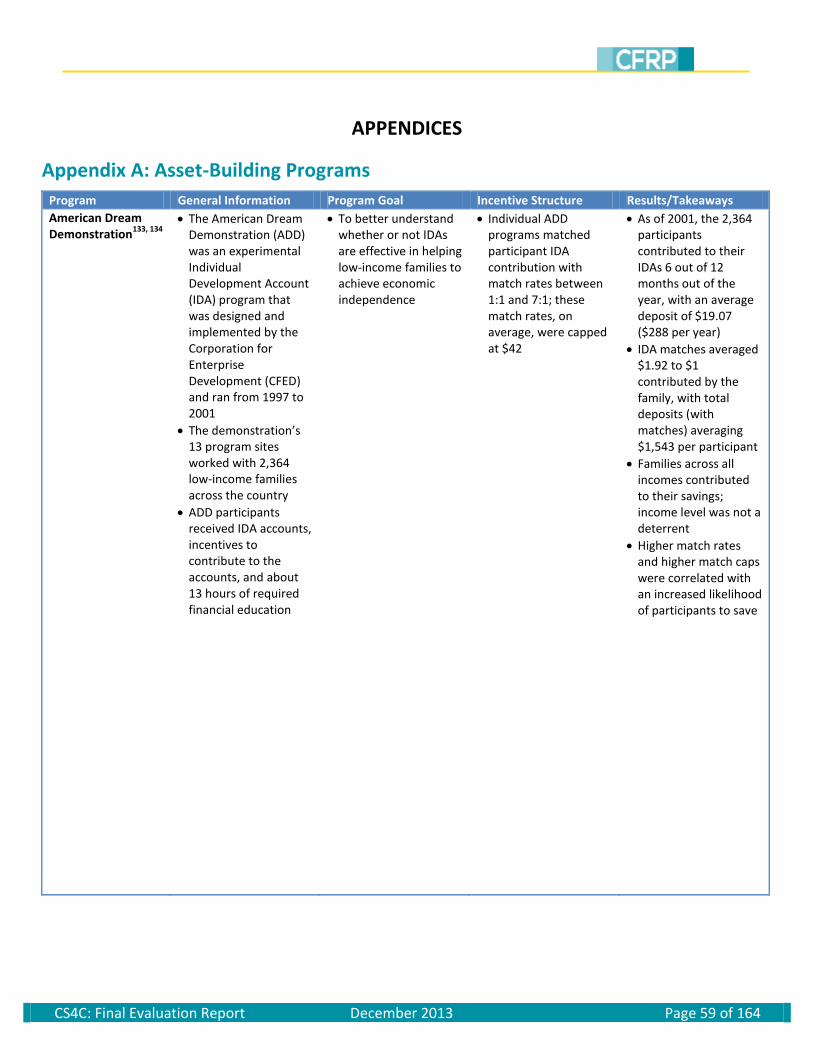

In the face of rapidly escalating tuition costs and extensive student debt holdings, some policymakers have begun to seek additional levers for facilitating college attendance beyond the traditional reliance on grants and financial aid. One such policy lever being explored in the research community is an asset-building approach to college savings. Asset-building practitioners promote large-scale, government-supported college savings account initiatives that attempt to create a more comprehensive savings culture for college attendance. Though much of the research in this area is still new, a number of studies have already demonstrated promising results. Evidence from one statewide randomized experiment in Oklahoma, for example, shows that providing incentives to save in a designated college savings vehicle generates statistically significant increases in participant account holdings.41 [For a full review of this study and other college savings initiatives, please see Appendix A.] Other studies have demonstrated that having even a relatively small amount of designated college savings can significantly increase the likelihood of future educational success.42 In one longitudinal study with extensive controls, researchers found that having as little as $1 in college savings makes a child nearly three times more likely to enroll in college than a child with no savings.43 And the savings appear to affect graduation rates too. In fact, students with designated college savings accounts between $1 and $499 are roughly 2.4 times more likely to graduate from college than students with no savings.44 Other

U.S. Rate=13.4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

AZ

TX

ND

16.1% of Texas borrowers entering repayment defaulted on their student loans

CS4C: Final Evaluation Report December 2013 Page 9 of 164

studies have found that among young people who expect to graduate from a four-year college, those who have designated college savings account are approximately three times more likely to attend than those with no account when controlling for a range of demographic, socioeconomic, and academic characteristics.45 Much of the research in this area suggests the link between college savings and college attendance may be largely psychological—that the simple act of having a designated college savings account changes how students think about college. Researchers call this a shift in the student’s “college-bound identity.”46 By actualizing the intention for children to go to college, designated college savings accounts may yield not only superior educational outcomes, but also a more lasting range of collateral benefits traditionally associated with higher education. These early studies suggest that developing programs to encourage college savings may bring about a joint set of consequences. In the most immediate sense, college savings programs may act as a lever for increasing the dollar amount of individuals’ college savings, thereby providing a valuable addition to the mix of college financing options. What is more, such programs also appear to generate a psychological impact that seeds a belief in the attainability of a college degree. Importantly, this psychological impact seems to operate largely independently of the size of individual account holdings, implying that college savings accounts may carry inherent value in and of themselves. COLLEGE SAVINGS INCENTIVES

Motivated by this line of research, many states and organizations have begun to explore the use of college savings incentives as a means of boosting families’ financial capacity to send their children to college. In 2013, Texas was one of fifteen states offering financial incentives to save in a 529 college savings plan. Though some of these states offer tax credits based on a percentage of 529 contributions, the vast majority operate a matching grant or scholarship program.47 Matching programs tend to be structured such that families under a given income threshold are matched on contributions into 529 savings accounts at a specified rate, subject to an annual match limit (e.g. $500) and up to a lifetime maximum (e.g. $2,500), or for a maximum number of years (e.g. 5 years). Examples of states with variations on this design are Arkansas, Colorado, Kansas, Missouri, Nevada, North Dakota, Rhode Island, Utah, and West Virginia. A number of states also include a variable match rate tied to household income level. Arkansas and Rhode Island, for example, match 2:1 for low-income savers and 1:1 for middle-income savers.48 In Texas, matching grants are administered by the Texas Match the Promise Foundation, a 501(c)(3) public charity established by the Texas Comptroller to direct the Texas Save and Match program.49 In 2007, the Texas Legislature created the Save and Match program under HB 3900 with the aim of incentivizing college saving through matched purchases of prepaid college tuition units. The program was officially launched in September 2012, and now provides matching scholarships to participants in the Texas Tuition Promise Fund (TTPF) who meet certain eligibility requirements and have been selected through a competitive application process. To be eligible, students must be in grades 5 through 9, have family incomes below $100,000, have a Promise Fund account, and meet a $100 contribution requirement.50 Each year, matching scholarships are provided to the top 150 applicants based on a scoring of career essays, grade averages, income levels, and the number of dependents claimed by the

CS4C: Final Evaluation Report December 2013 Page 10 of 164

student’s parents. Funded primarily by individual contributions, these scholarships match up to $500 of participant tuition unit purchases with the same number and type of tuition unit. In addition, the top five applicants each year are awarded a one-time scholarship worth $2,000 of current tuition units.51 Because the Save and Match program is very new, participant data, savings rates, and other evaluation outcomes are not yet available. Prior to the launch of the Save and Match program, enrollment in TTPF accounts had been steadily declining for four years.52 Though more than 30,000 prepaid tuition plans were opened between 2008 and March of 2012, only 6 percent of these enrollees came from households with below median incomes ($50,000). Families with household incomes over $100,000 were four times more likely to enroll in a prepaid fund than families earning less than this amount. Moreover, recent declines in enrollment have been most pronounced among families with household incomes below $75,000, as well as African American and Hispanic families.53 Beyond creating the Save and Match program, the Texas legislature has taken one other important step toward reversing the trend of declining college enrollment, especially among disadvantaged groups. In 2011, Texas passed HB 3708 exempting college savings accounts from asset limit tests in determining eligibility for public assistance or state financial aid.54 For additional information on how college savings accounts impact public benefits and financial aid in Texas, see Box 1.

CS4C: Final Evaluation Report December 2013 Page 11 of 164

Box 1: College Savings, Public Benefits, and Financial Aid

Do College Savings Affect Public Benefits and Financial Aid?

One concern held by some low-income families is whether or not assets held in college savings accounts will impact any government benefits that they may be receiving. Because some public assistance programs are administered at the state level, while others operate at the federal level, rules regarding the applicability of assets held in college savings accounts vary. The Supplemental Nutrition Assistance Program (SNAP), for example, is a federal program and sets a nationwide asset limit at $2,000. Individual states have the flexibility to modify this asset limit, however; thirty-six states have eliminated the SNAP asset limit entirely, and Texas has raised it to $5,000.55 Following the adoption of the 2008 Farm Bill, Federal law exempts education savings accounts, including 529s, from the asset limit test for SNAP assistance.56 Supplemental Security Income (SSI) is also a federally administered program. The current asset limit on unrestricted assets – which includes money held in 529s – is $2,000.57 For programs administered at the state level such as TANF, Medicaid, or CHIP, individual states maintain broad discretion in setting their own eligibility criteria.58 In Texas, assets held in 529 and prepaid tuition accounts are exempt from counting toward asset limits for TANF, Medicaid, and CHIP. Another concern held broadly across income groups is that college savings may negatively influence financial aid eligibility. Overall, 3 in 10 parents who are not saving for college express a belief that saving for college may prevent their child from getting financial aid.59 Generally, financial aid awards are based on a student’s financial need or ability to pay. Ability to pay is determined by a federal formula known as the expected family contribution (EFC), which calculates the net worth of both student and parental assets expected to be used for college expenses. For dependent students, the formula stipulates that between 2.64 and 5.64 percent of assets held in a 529 count toward a family’s EFC.60 Though a larger EFC reduces the overall amount of financial aid eligibility, most families do not have an EFC because of savings and asset protection allowances. For example, assets are not considered in EFC calculations for those with a total household income below $50,000/year.61 Allowances like this one preclude most families from being impacted by 529 holdings. In 2008, only 13 percent of FAFSA filers had enough assets to count toward their EFC.62 At the state level, Texas has taken additional measures to prevent educational savings accounts from impacting state financial aid eligibility with the passage of HB 3708.63 Under Section 56.007 of the bill, assets held under these plans “may not be considered an asset of the person, or otherwise included in the person’s household income or other financial resources, for purposes of determining the person’s eligibility for a TEXAS grant or any other state-funded student financial assistance.”64

CS4C: Final Evaluation Report December 2013 Page 12 of 164

CHALLENGES TO COLLEGE SAVINGS INCENTIVES

Despite growing interest in asset-building policy and a handful of promising studies, the field of asset building has occasionally struggled to generate the desired outcomes in practice. There is inconclusive evidence, for example, that asset-building programs actually increase savings among target populations.65 Though some matched savings programs have demonstrated substantive increases in enrollment and contributions among low-income individuals, others have yielded mostly insignificant effects on assets, net worth, or poverty rates.66 Many other asset-building programs have been ill-suited to evaluation, lacking the resources or capacity to conduct large-scale experiments with control groups and longitudinal data collection.67 In cases where rigorous evaluation has been possible, the impact of asset-building programs aimed at incentivizing college savings have also been somewhat underwhelming—especially among those with the lowest incomes. SEED OK, the matched college savings program in Oklahoma with perhaps the most rigorous evaluation to date, has shown substantial success with automatic enrollment, but only limited success in increasing private account openings or generating meaningful differences in deposit amounts.68 A partial explanation for the limited success of some matched college savings programs may lie in the imperfect marriage between asset building and 529 college savings accounts. Indeed, the potential success of asset-building strategies paired with 529 college savings accounts may be attenuated by the 529 vehicle itself, which is not widely used by families saving for college—especially low-income families who tend to save through general savings accounts or CDs.69 A recent report from the GAO reveals that in 2010, less than 3 percent of U.S. families were saving in a 529 plan.70 Even among those with major educational expenses on the horizon, only 7 percent reported saving in a 529 plan.71 Moreover, families who do use 529s are disproportionately high-income; data from the GAO reveal that families using 529 plans have approximately 25 times the median financial assets of those not using 529 plans.72 One reason for this imbalance is the plan’s features; studies show the tax benefits of 529s accrue predominantly to high-income earners, and give disproportionate advantage to those in the top income brackets when considered alongside potential reductions in financial aid eligibility.73 Furthermore, even where asset-building strategies succeed in increasing the asset holdings of low-income families, there may also be drawbacks. Though asset accumulation has been linked to a number of positive outcomes in social and economic wellbeing, scholars of asset building caution that especially under weak economic conditions, asset holding by low-income individuals may be detrimental given the potential for risky investments, low or negative appreciation of assets, constrained mobility, neglect of current needs, a lack of savings to weather crises, and higher levels of stress associated with maintaining assets.74

CS4C: Final Evaluation Report December 2013 Page 13 of 164

BEST PRINCIPLES OF ASSET BUILDING

In light of these considerations, many researchers contend that the most important determinants of success lie in the way asset-building programs are designed.75 Research shows that rates of account opening in college savings programs cannot be explained by differences in the personal characteristics of participants, implying that programmatic elements may be the primary drivers of participation rates. When given the opportunity to open an incentivized college savings account, for example, there is no difference between low-income individuals who open the account and those who do not on measures of economic strain, personal mastery (feeling of control over one's life), and parental stress.76 Moreover, prior studies find little evidence of a reliable association between account opening and a wide range of demographic variables, including gender, race, marital status, poverty status, credit card ownership, baseline savings, and others.77 Scholars maintain that the tenuous connection between individual characteristics and the propensity to open an incentivized savings account squares well with the theoretical underpinnings of asset building itself. In particular, much of the research underlines the notion that the success of asset-building programs is determined primarily by institutional factors such as characteristics of the organizations that administer the programs and how the accounts are designed, rather than by individual or household factors.78 For those with a limited capacity to save, the most appropriate asset-building strategies have both less demanding savings requirements and more generous financial incentives.79 In particular, researchers across the field emphasize the importance of automatic enrollment, default account opening, generous seed deposits, clear account statements, committed staff, and strong outreach and recruitment.80 Other considerations include lower initial deposit requirements, fewer restrictions on the allowable uses of funds, a higher match rate, and “higher touch” interventions involving financial coaches and one-on-one assistance.81 Asset-building initiatives have also begun to incorporate lessons from the field of social psychology and behavioral economics.82 One line of research indicates that the timing of cash flows may be an important consideration in facilitating savings among low income individuals. Several studies, for example, suggest that individuals may prefer to save income received as a lump sum.83 Field studies show the lump sum may be more attractive in part because it acts as a “forced savings mechanism,” effectively providing individuals with an opportunity to save they may not have taken otherwise.84 We expand on the logic underpinning the use of lump sum transfers as a target for incentivized college savings in the description of the CS4C program structure.

CS4C: Final Evaluation Report December 2013 Page 14 of 164

College Savings Incentives and the Child Support System

As researchers and policymakers continue to explore the impact of asset-building initiatives on college savings and the potential for long-term gains in the domain of higher education, one intersection that has remained largely untapped is that between college savings and the child support system. Investigating how the child support system might leverage existing infrastructure to boost college savings among the child support population may prove advantageous for a number of reasons. One motivating factor in exploring the union of child support and college savings initiatives is the vast scale and reach of state child support systems. In Texas, roughly $3.4 billion dollars flow from noncustodial to custodial parents each year; transfers which may offer a natural point of entry for programs promoting college savings.85 This far-reaching transfer system includes nearly 1.4 million cases, and supports 1.6 million—or almost 1 in 4—Texas children.86b In cases where the custodial parent is not paid the full amount of child support, arrears or past-due obligations accrue. In July 2013, there were 820,410 cases in which the custodial parent was owed arrears; the median amount owed for these cases was $6,995.c Custodial parents often receive arrears payments in a lump sum transfer; the average lump sum payment was $2,444 in August 2011. This particular aspect of the child support system provided much of the impetus for CS4C, and is discussed further under the program design section. In addition to the volume of transfers made within the Texas child support system, parents in the child support system show a keen interest in saving for college. In a 2012 study conducted by the Texas OAG, 81.5 percent of custodial parents and 61.5 percent of noncustodial parents indicated an interest in saving for their children’s education through a shared education savings account. Custodial parents also rated saving for their children’s future education expenses as their most important financial goal.87 Moreover, the child support system is characterized by a lower-income population, and offers a ready-made avenue for targeting those most in need of college savings supports.

Finally, college savings incentives support the broad goals of the Texas Child Support Division. Although the primary mission of the OAG is to perform child support establishment, modification, and enforcement, the Child Support Division has also adopted a more comprehensive approach to child support that includes the provision of family-centered support and the promotion of economic stability. This mission is carried out by the OAG’s Family Initiatives section, whose primary responsibility is to administer special projects and programs that aim to “respond compassionately and effectively to the changing needs of families and children in Texas.”88 These programs tend to work in

b According to OAG Administrative Records, there are 1,376,368 active child support cases in Texas that involve at least one

child under 18 (some of these cases involve only medical support). These cases include 1,598,032 children under the age of

18. In 2012, 26.8% of Texas’s population of 26.06 million was under the age of 18. Of the nearly 7 million Texans under the

age of 18, 1.6 million—or 23%—is in the child support system. c Calculation based on July 2013 OAG Administrative Records; only arrears owed to custodial parents, not to the state, are

included in this calculation. Only cases with a balance greater than 0 of arrears owed to custodial parents are included. The

average arrears owed on case was higher, at $13,868. Custodial parents may be associated with multiple cases; in July 2013,

the median amount owed a custodial parent was $7,890, and the average amount was $15,331.

CS4C: Final Evaluation Report December 2013 Page 15 of 164

collaboration with community and faith-based organizations, courts, schools, and other public agencies to promote and encourage stable family formation. The Family Initiatives section also acts as the administrator of the Building Assets for Fathers and Families (BAFF) grant, a federally-funded initiative aimed at strengthening families’ long-term financial stability through asset-building services.89 Helping to set families on a trajectory towards college completion aligns well with the goals of the BAFF initiative, as well as the broader work of the OAG’s Family Initiatives section. Despite the potential for collaboration between the child support system and asset-building initiatives, the two areas have little history of partnership. Child Support for College represents one of the first programs to marry these ideas with the purpose of cultivating college savings among the child support population. Because the program has little precedent, CS4C has met with both successes and challenges in each phase of its execution. This report details some of the program’s core achievements and shortcomings. We conclude with a synthesis of lessons learned and offer considerations for the broader work of asset-building research.

CS4C Program Design

This section describes the design of the CS4C program, including program partners, an overview of the program structure, and how the program design evolved over time. We establish the motivating logic to develop CS4C, and detail program modifications to outreach, incentive structures, and financial coaching during the 18-month program period. Program Partners

The CS4C program is an innovative collaboration between private, public, nonprofit, and academic institutions. RAISE Texas, a statewide network of nonprofit organizations, for-profit corporations, and public institutions, promotes policies and programs to advance the financial success and economic stability of low- and moderate-income Texans. The CS4C program aligned well with the existing goals of RAISE Texas, who viewed the program as an opportunity to work with a target population that may have the potential for large-scale implementation, as well as a chance to learn lessons for the broader field of asset building. RAISE Texas acted as the fiscal agent for CS4C, disbursing program funds to the implementing nonprofits and incentive payments to participants. The Office of the Attorney General (OAG) led the design of the CS4C program. The OAG saw CS4C as an innovation with the potential for increasing long-term self-sufficiency among Texas child support customers, as well as a way to provide lump sum recipients with additional financial options beyond those such as using check cashing establishments to manage money. In addition, the OAG conducted outreach activities for CS4C, including identifying and advertising to customers who had recently received lump sum child support payments. Citi Community Development works with nonprofit and public agencies across the United States to expand access to financial services and forge innovative partnerships to achieve financial inclusion and economic empowerment for underserved individuals, families, and communities. Citi regarded the CS4C program as

CS4C: Final Evaluation Report December 2013 Page 16 of 164

an opportunity to foster an original idea that could yield large-scale benefits for Texas families. As one of the more innovative pilots in the field of asset building, CS4C also aligned with Citi’s investment in promoting children’s savings accounts and college success among the economically disadvantaged. Citi played an integral role in the early conceptualization of CS4C, and provided funding for the program in hopes that, if successful, it might be taken to scale. Three local nonprofits implemented the pilot program. The Brazos Valley Affordable Housing Corporation provides first time homebuyer seminars, credit counseling, and other housing assistance to families in the Brazos Valley, including Bryan-College Station, TX and surrounding counties. Brazos Valley provided an opportunity to pilot the program in a rural location, an important consideration for program partners who sought to take the program to scale in the future. United Way of San Antonio and Bexar County focuses on improving early care and education for children and provides a free tax preparation program for low- to moderate-income families. In Austin, TX Foundation Communities provides support services to low-income families, including affordable housing, adult education, financial coaching, and tax services. Foundation Communities also administers a number of programs intended to improve college access, making CS4C particularly well-aligned with the existing mission and goals of the organization. Program Structure

The CS4C program provided matched contributions and financial coaching services to encourage college savings among eligible parents in the child support system. Many of the program’s core elements were modeled on the basic principles of asset building, including the provision of a savings match, which has been linked to increased participation rates—especially among low-income individuals;90 financial coaching services, which research shows are a valuable tool in helping people to save;91 a focus on leveraging lump sum income, which has been linked to increased odds of saving;92 and the use of statewide college savings vehicles, a common feature of other college savings programs due to their institutional structure and restrictions on access and use of funds.93 In an effort to generate college savings among a broad-based, low-income population, CS4C leveraged a unique element of the child support system as its core innovation. Instead of tapping into savers’ existing income streams, the CS4C program attempted to capitalize on an existing structural component of the child support system—lump sum payments—to promote the accumulation of assets among child support customers. Lump sum payments occur when a noncustodial parent makes a large arrears, or “catch-up,” payment to the child support system which is passed through to the custodial parent. Program partners hypothesized that the sudden windfall provided by a lump sum payment would present an opportunity to encourage college savings among child support customers—a notion supported by prior literature suggesting that the marginal propensity to save from a lump sum payment is greater than that of regular income.94 This concept stems from research showing that individuals have separate mental accounts, and are more likely to build assets from money they view as “wealth” than current income;95 since an unexpected influx of cash is likely to be viewed as “irregular” income, it is less likely to be pre-assigned to future expenditures and more likely to be earmarked for savings.96 Other research shows that when low-income individuals receive a sudden windfall of cash, they benefit from a brief mental reprieve or “reset” moment during which their attention may shift from the routine

CS4C: Final Evaluation Report December 2013 Page 17 of 164

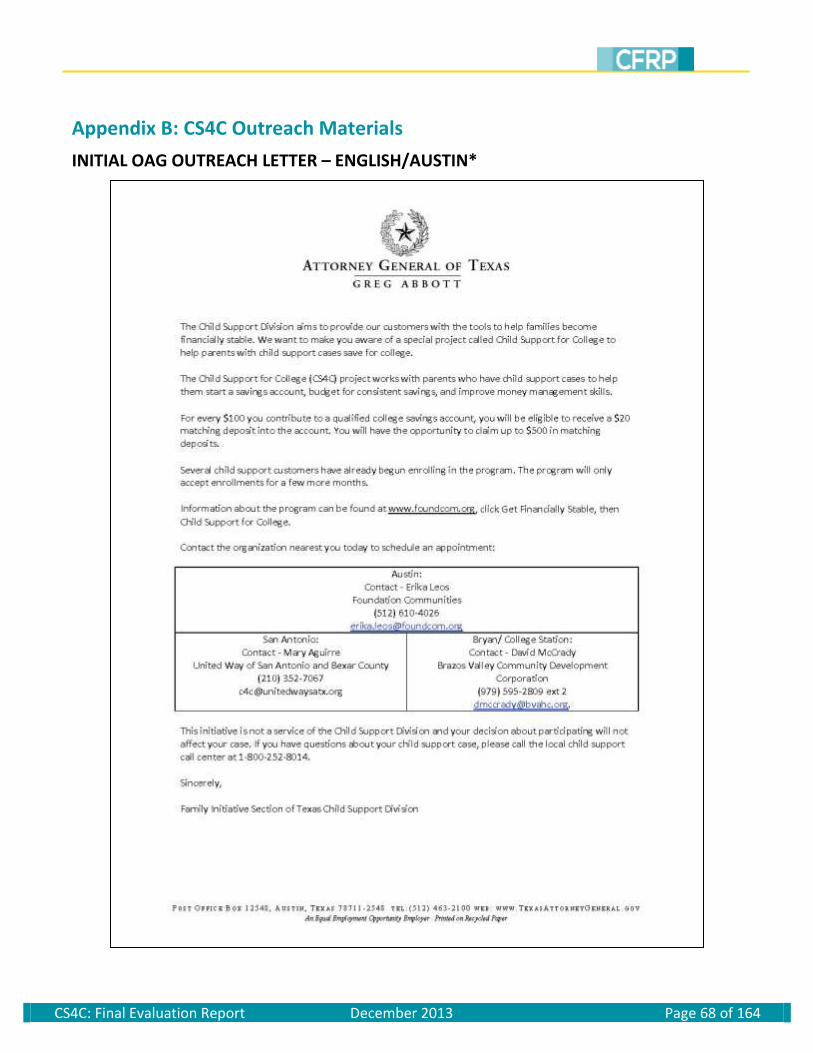

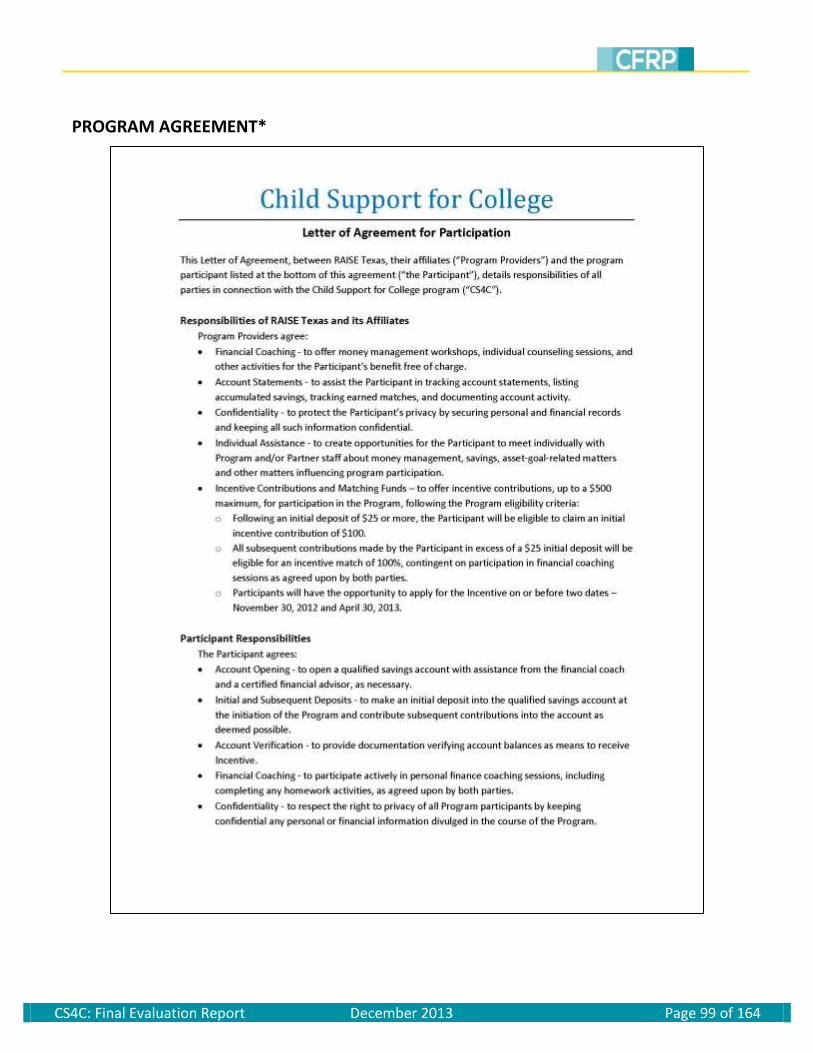

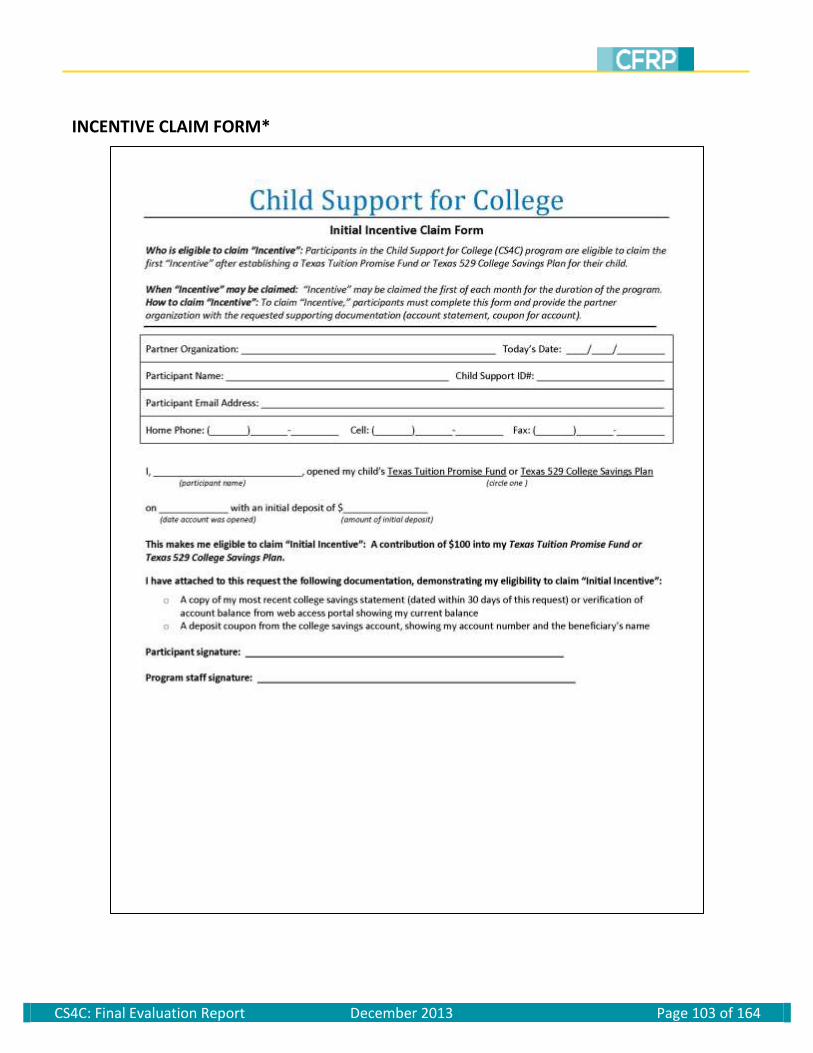

management of day-to-day life toward taking advantage of opportunities to make investments for the future.97 Child support customers in the three Texas regions of the program who were due to receive a lump sum payment were actively contacted through outreach activities from the OAG and program partners. The primary channel of recruitment was through email and direct mail, though additional outreach materials were displayed in child support offices and at child support court [outreach materials available in Error! Reference source not found.]. Though CS4C was originally targeted toward custodial parents receiving lump sum arrears payments, any child support customer residing within the service area of one of the participating nonprofits was eligible to participate in the program. Child support customers who expressed an interest in the program first contacted one of the three local nonprofits to inquire about CS4C. Staff at the local nonprofits collected basic contact and demographic information from each of these inquirers, and offered to set up an initial meeting to discuss the program further. A portion of these inquirers then attended an initial meeting to learn more about CS4C, and were asked to complete an intake form. This form acted as the baseline survey instrument, and collected detailed information on demographic and financial characteristics, as well as financial and educational goals. In addition, these participants received an initial financial coaching session. Over the course of several additional coaching sessions, participants discussed their financial status and decided whether to open a college savings account through CS4C. Participants who chose to open a college savings account through CS4C selected from two different savings vehicles—the Texas College Savings Plan (529) and the Texas Tuition Promise Fund. In the traditional 529 account, participants also elected specific investments packages from a menu of savings options. After opening a college savings account through the CS4C program, program partners monitored participant deposits and distributed incentive payments according to a specified match structure.

CS4C: Final Evaluation Report December 2013 Page 18 of 164

Evolution of Program Design: Outreach, Incentives, and Financial Coaching

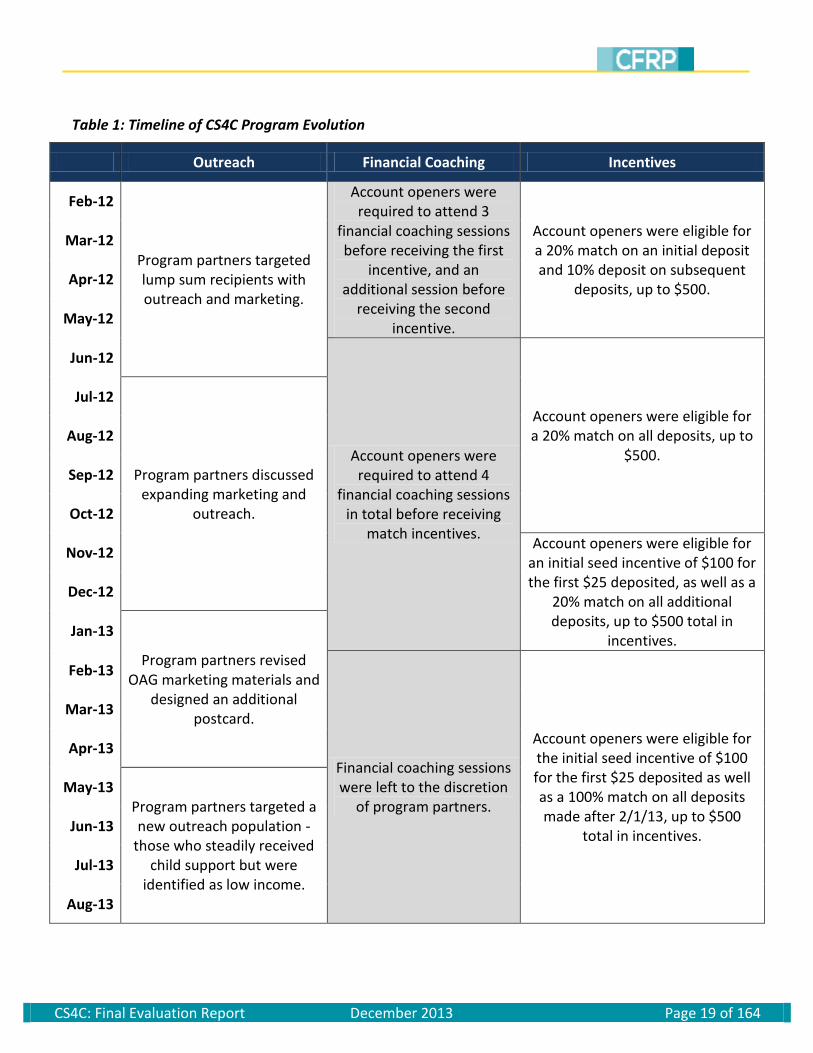

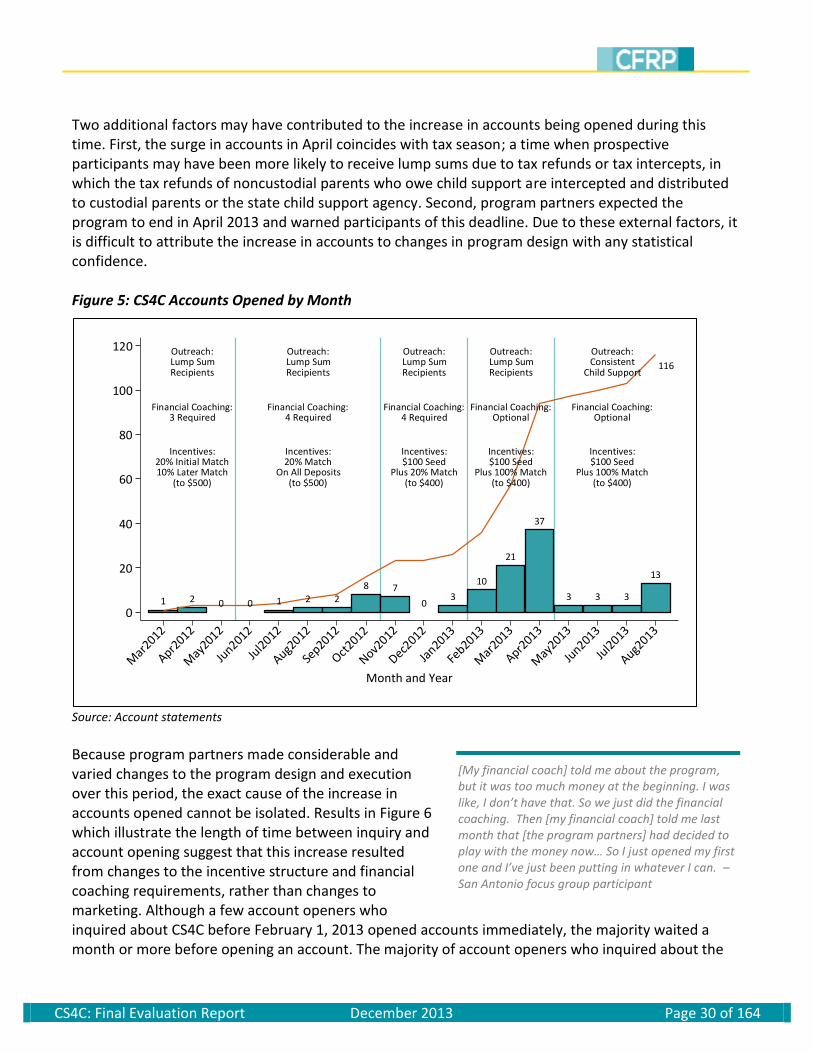

Given the innovative nature of the CS4C program, program administrators had little in the way of a road map for the optimal program design and implementation strategy. In addition, the program was launched quickly before all logistical decisions could be settled. Though the original program structure was designed with the core principles of asset building in mind, CS4C also inadvertently incorporated adverse incentive structures and a number of barriers to participation. As the program went into effect, program partners learned what was most effective and modified the program accordingly. This section provides an overview of changes in the outreach, financial coaching, and incentive structures of the CS4C program. Table 1 outlines the evolution of the program from program launch in February 2012 to program close in August 2013. At the outset of the program, direct outreach focused on families who were receiving lump sum payments under the presumption that the unexpected windfall of cash would provide an opportunity to save for college. Lump sum recipients who enrolled in the program received a 20 percent match on an initial deposit after six months and three financial coaching sessions. Participants could receive an additional 10 percent match on subsequent deposits following a fourth financial coaching session. In May of 2012, the match rate was changed to a constant 20 percent on all deposits and participants were required to attend a total of four financial coaching sessions before receiving match incentives. This modification was made in response to the tendency of participants to delay their initial deposits in order to save more and maximize the initial match. This delay was believed to decrease the number of people opening accounts. By standardizing the match, program partners hoped to eliminate the incentive to delay and increase the number of accounts. During this time, program partners also began to discuss expanding outreach beyond lump sum recipients. In November 2012, an additional incentive was added to encourage account opening among prospective participants. Participants opening an account with a $25 deposit were provided with an initial seed incentive of $100. All deposits were also matched at the existing 20 percent match rate once participants had completed four financial coaching sessions. In January 2013, program partners revised the marketing materials and designed an additional postcard in an effort to boost enrollment. February 2013 saw the greatest modifications to the CS4C program. Two companion changes were made, one intended to boost incentives and the other intended to reduce barriers. The match rate was raised to 100 percent on all deposits, and financial coaching requirements were waived. Participants seeking to open accounts were no longer required to complete four financial coaching sessions; however, financial coaching services were still provided on a voluntary basis. Finally, in April of 2013 the CS4C program altered its outreach. The new marketing strategy targeted a different population of child support recipients – those who were identified as low income families steadily receiving child support. The program concluded at the end of August 2013.

CS4C: Final Evaluation Report December 2013 Page 19 of 164

Table 1: Timeline of CS4C Program Evolution

Outreach Financial Coaching Incentives

Feb-12

Program partners targeted lump sum recipients with outreach and marketing.

Account openers were required to attend 3

financial coaching sessions before receiving the first

incentive, and an additional session before

receiving the second incentive.

Account openers were eligible for a 20% match on an initial deposit and 10% deposit on subsequent

deposits, up to $500.

Mar-12

Apr-12

May-12

Jun-12

Account openers were required to attend 4

financial coaching sessions in total before receiving

match incentives.

Account openers were eligible for a 20% match on all deposits, up to

$500.

Jul-12

Program partners discussed expanding marketing and

outreach.

Aug-12

Sep-12

Oct-12

Nov-12 Account openers were eligible for

an initial seed incentive of $100 for the first $25 deposited, as well as a

20% match on all additional deposits, up to $500 total in

incentives.

Dec-12

Jan-13

Program partners revised OAG marketing materials and

designed an additional postcard.

Feb-13

Financial coaching sessions were left to the discretion

of program partners.

Account openers were eligible for the initial seed incentive of $100 for the first $25 deposited as well as a 100% match on all deposits made after 2/1/13, up to $500

total in incentives.

Mar-13

Apr-13

May-13 Program partners targeted a new outreach population -

those who steadily received child support but were

identified as low income.

Jun-13

Jul-13

Aug-13

CS4C: Final Evaluation Report December 2013 Page 20 of 164

Evaluation Strategy

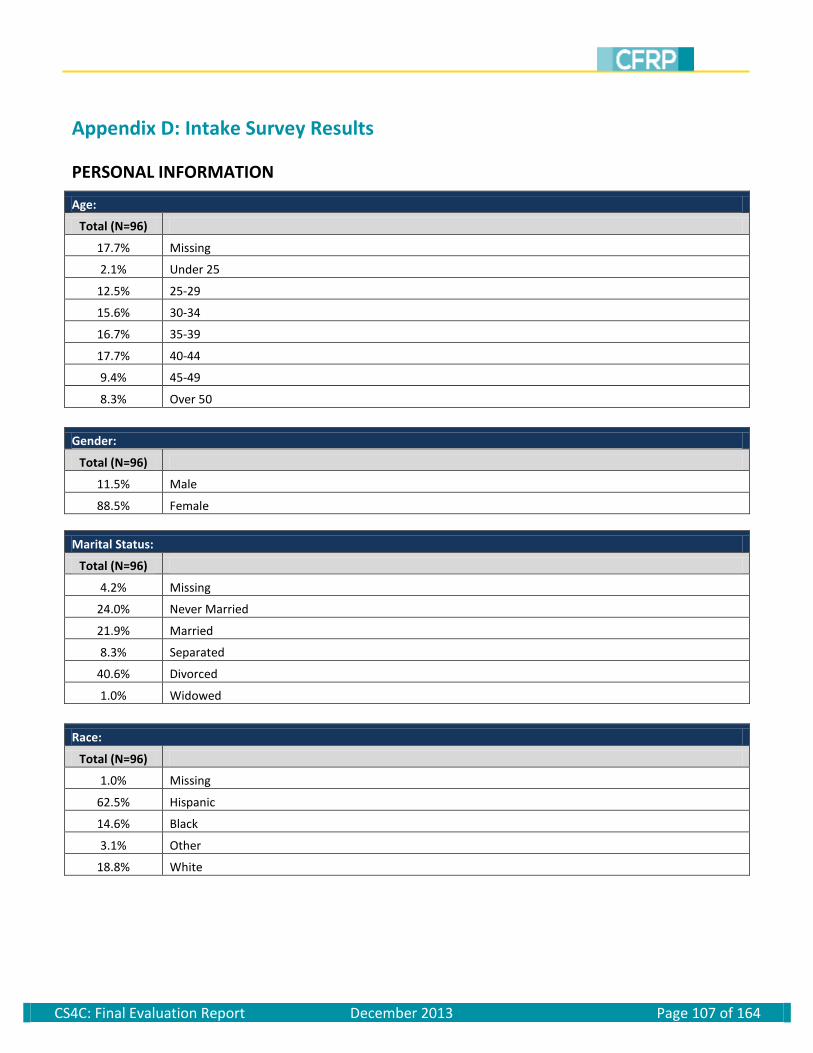

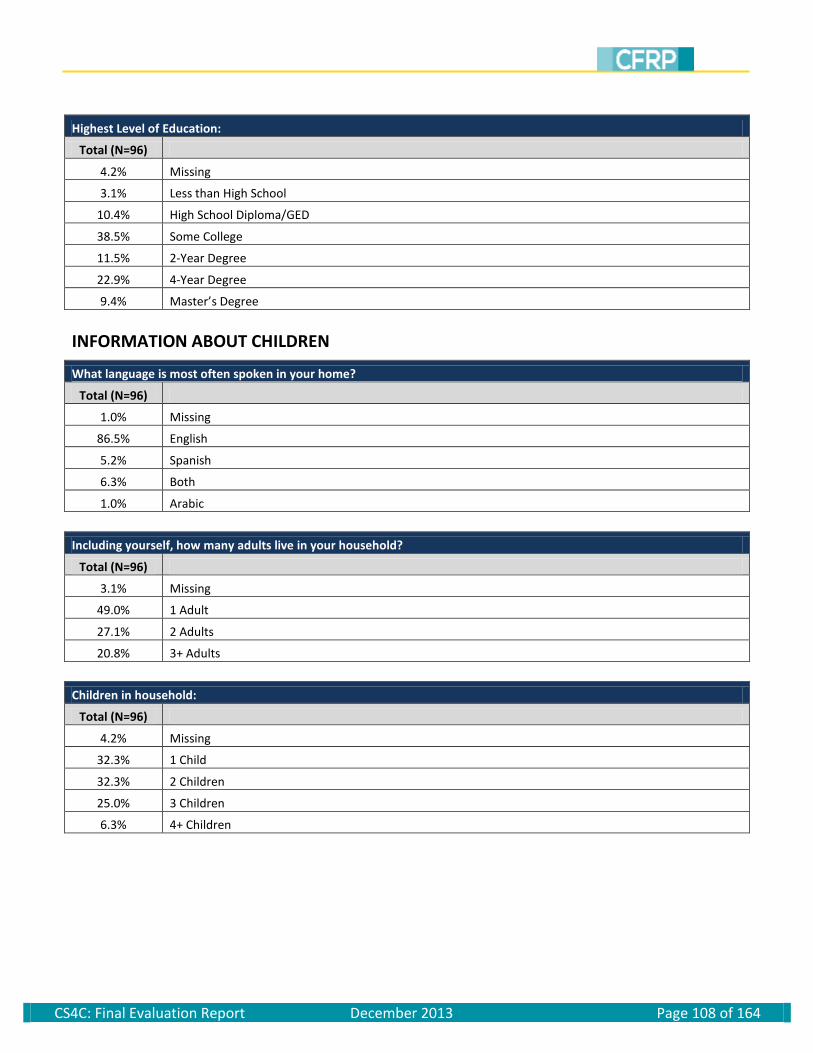

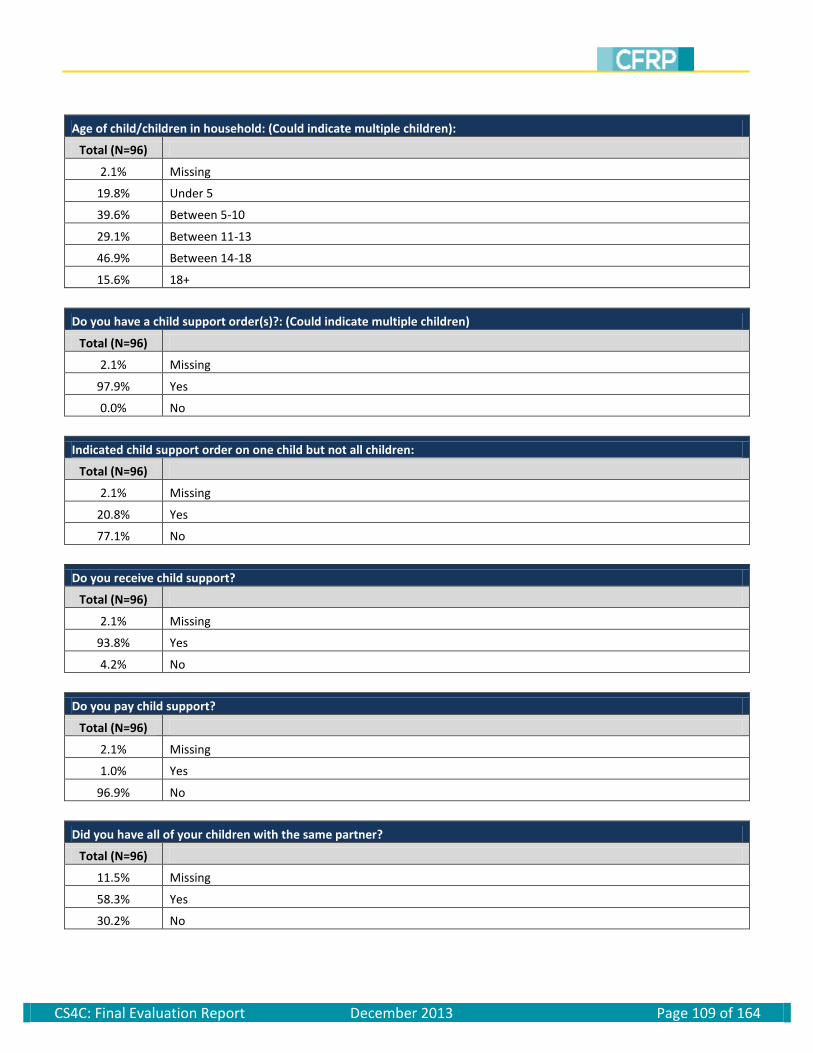

The evaluation of the CS4C program relies on a mixed methods approach, integrating both quantitative and qualitative analyses throughout the evaluation process. The use of multiple evaluation strategies helps to contextualize elements of the program that may not be well-suited to quantitative or qualitative data alone. In particular, the relatively small number of participants and numerous changes made to the program introduce challenges to statistical analyses. In these cases, qualitative data supplement the discussion and provide a more comprehensive understanding of program dynamics. This evaluation seeks to address three broad research questions: 1) Who participated in CS4C?, 2) What were the motivations and barriers to program participation?, and 3) What are the benefits to participating in CS4C? Each of these research topics is discussed in the findings section. In addition, this evaluation aims to identify relevant programmatic lessons in the areas of program design and implementation, which are detailed in the policy considerations section. DATA COLLECTION

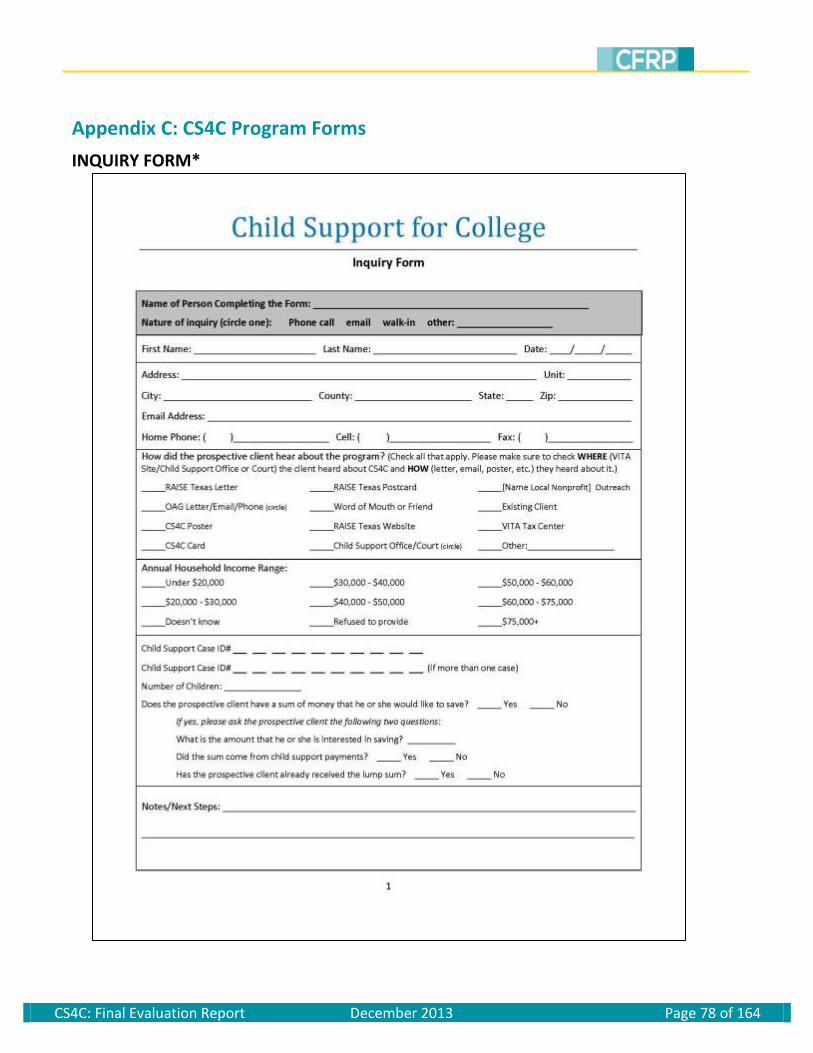

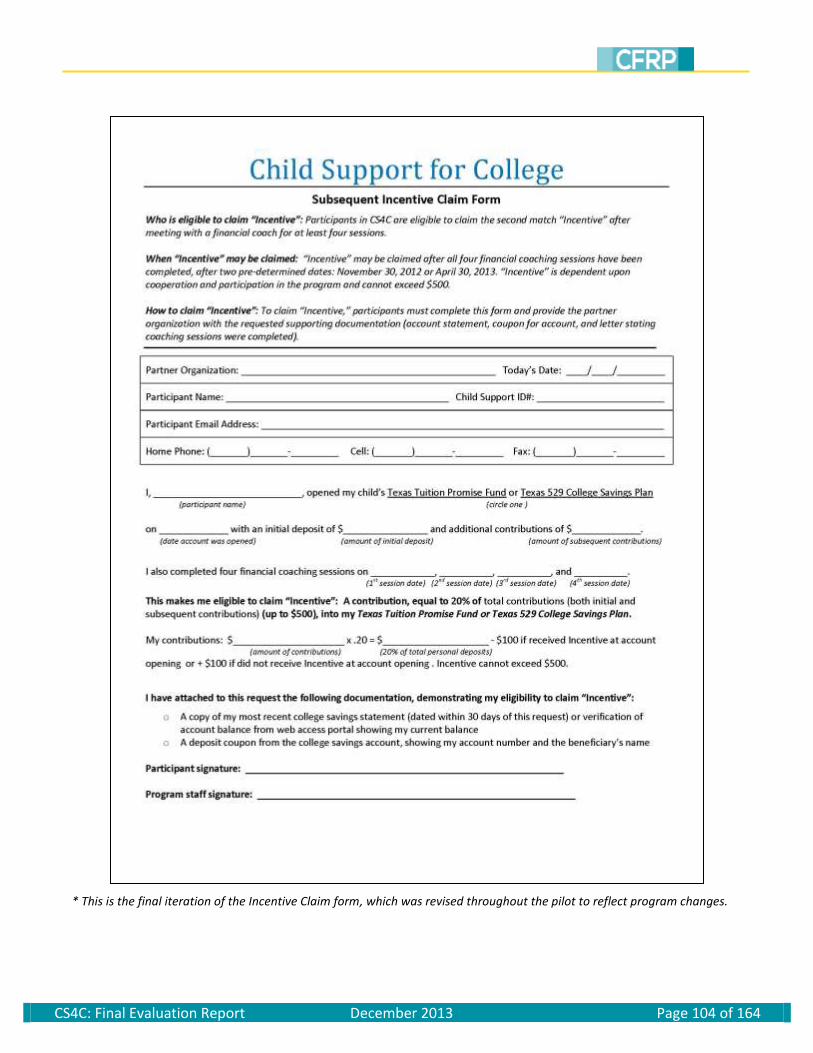

To evaluate CS4C, CFRP collected data from a variety of sources. Program forms completed by the local nonprofits made up one of the largest sources of information. These forms include an inquiry form, which program partners completed for every inquiry made about CS4C; a financial coaching form, which financial coaches completed following every coaching session; and several forms related to the incentive claim process [program forms available in Appendix C]. Additionally, CFRP received account statements from account openers as part of the incentive claim process.d To collect more detailed information about inquirers, non-openers, and account openers, CFRP fielded two larger surveys for CS4C. First, CFRP asked program participants to complete intake surveys during their first financial coaching session; out of 99 participants, 96 began intake surveys. This survey collected detailed demographic and financial characteristics, as well as participants’ financial and educational goals [full results available in Appendix D]. Second, CFRP conducted an online exit survey of all CS4C inquirers, non-openers, and account openers in June 2013, to which 110 individuals responded [full results available in Appendix E]. Of the 110 respondents, at the time of the exit survey, 57 were individuals who inquired about CS4C (inquirers). Another 15 individuals had met with a representative from the local nonprofit but did not open an account (non-openers). Finally, 38 individuals had opened an account with CS4C (account openers).e CFRP also used information collected by program partners and on surveys to match inquirers and participants with administrative data from the OAG. CFRP was able to match 215 (out of 298) inquirers and participants to active child support cases. These case records provide detailed information on child

d It is important to note that participants were not required to submit “final” account statements to program evaluators. As a

result, CFRP does not have access to final account balances for participants who received the maximum match and may have

continued to make deposits thereafter. Reported deposits are unlikely to reflect all participant contributions into college

savings accounts during the pilot. e After taking the exit survey, one inquirer and one non-opener went on to become account openers.

CS4C: Final Evaluation Report December 2013 Page 21 of 164

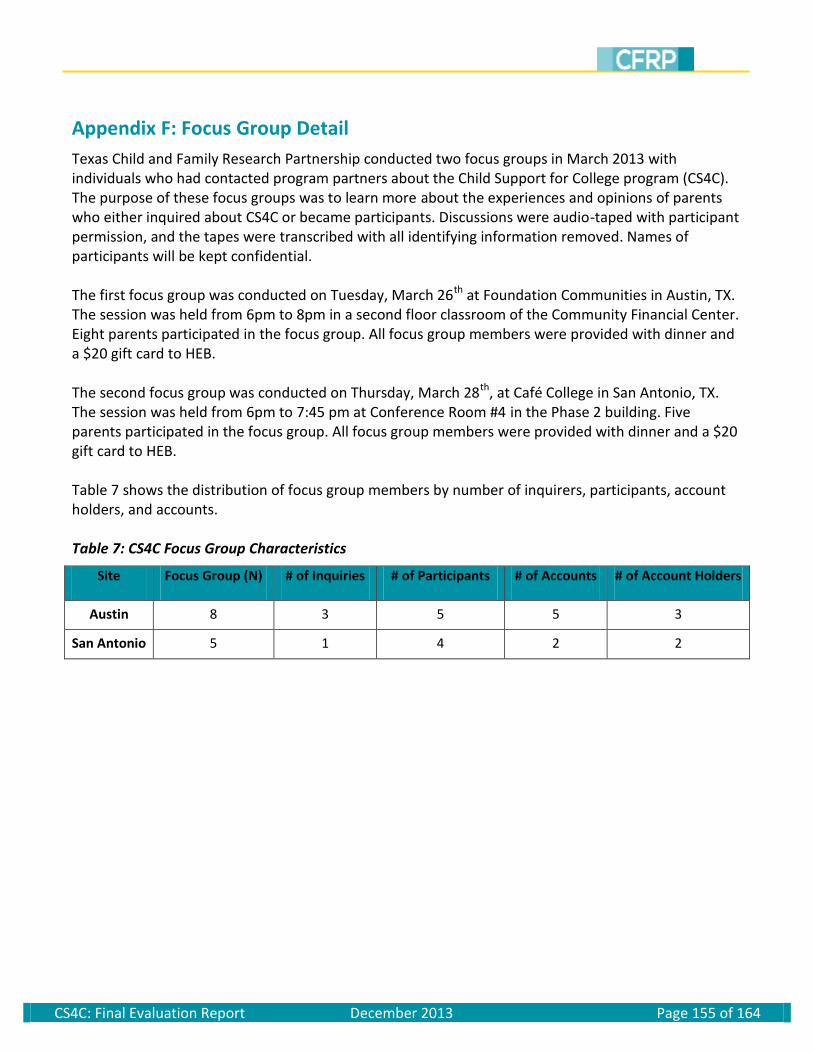

support payment histories. Additionally, the OAG provided CFRP with marketing records on all individuals contacted throughout the course of the program. To supplement information from quantitative data sources, CFRP also conducted two focus groups in Austin and San Antonio during March 2013. Individuals who had contacted local nonprofits about CS4C were invited to participate: eight parents participated in the Austin focus group, and five parents participated in the San Antonio focus group. Focus group results were transcribed and coded for recurring themes. [For more information on CS4C focus groups, please see Appendix F.] In addition, CFRP gathered programmatic information from interviews and meetings with program partners. The perspectives collected from these sources offer additional context for helping to understand many of the program’s dynamics, and help to inform recommendations made at the end of the report. DATA ANALYSIS

As noted previously, CS4C experienced a quick launch. Because not all decisions about the program design had been settled, program partners made numerous revisions to the structure of the program as the pilot progressed, in part due to results from CFRP’s implementation evaluation. Importantly, program partners often made multiple modifications to the program structure simultaneously, increasing the difficulty of linking subsequent outcomes to any single program modification. Under these circumstances, the CS4C pilot had no uniform treatment, and no impact evaluation of the program was possible. To compare differences between inquirers, non-openers, and account openers, CFRP uses results from inquiry forms, intake surveys, and exit surveys to construct as large of a sample as possible from each of these groups. Binomial tests, appropriate with smaller sample sizes, are used to determine whether these groups differ statistically on various demographic characteristics. Although CFRP has mostly complete demographic results from non-openers and account openers, some inquirers provided very little information to local nonprofits, and only one-quarter of inquirers participated in the exit survey. The potential for systematic differences between inquirers who participated in the exit survey and those who did not introduces the possibility of selection bias into inquirers’ exit survey data; however, this survey also provides the most detailed portrait of this group available. To determine the motivations and barriers to program participation, CFRP presents descriptive results of exit survey data, as well as calculations of inquiry, participation, and account opening rates over time. Combined with data from focus groups, these results provide compelling evidence on the reasons inquirers chose to participate in CS4C, or were unable or unwilling to participate. Because of the small number of inquirers, non-openers, and account openers, as well as multiple incidences of item non-response on both the intake and exit surveys, CFRP did not exclude respondents with incomplete surveys.

CS4C: Final Evaluation Report December 2013 Page 22 of 164

Finally, to examine the benefits of program participation, CFRP cites descriptive analyses from intake and exit surveys; again, because of the small number of inquirers, non-openers, and account openers, along with multiple incidences of item non-response on both surveys, CFRP includes all survey respondents. In addition, CFRP conducts several pre-post binomial tests on intake and exit survey results for account openers, i.e. those who were exposed to the “treatment” of opening a college savings account through CS4C; only account openers completing both an intake survey and exit survey, as well as completing the same questions on both surveys, are included in these analyses. Throughout this section, CFRP also relies on focus group results to supplement the discussion of benefits accrued through program participation.

CS4C Program Findings

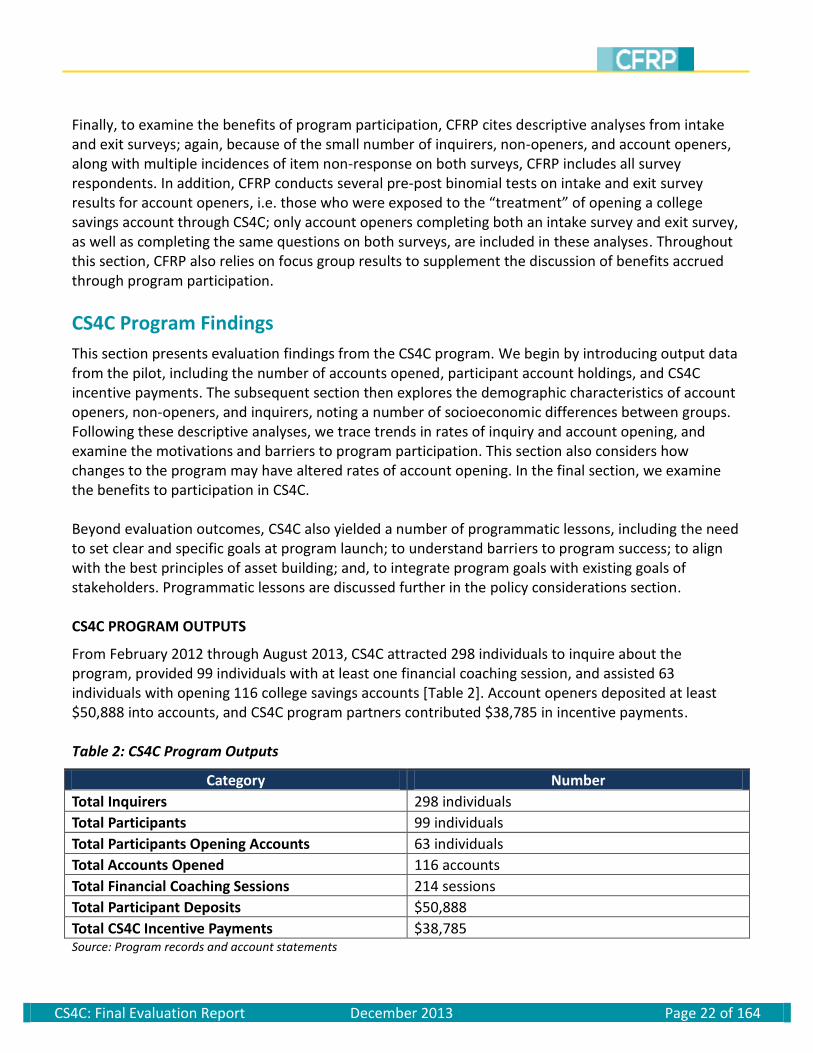

This section presents evaluation findings from the CS4C program. We begin by introducing output data from the pilot, including the number of accounts opened, participant account holdings, and CS4C incentive payments. The subsequent section then explores the demographic characteristics of account openers, non-openers, and inquirers, noting a number of socioeconomic differences between groups. Following these descriptive analyses, we trace trends in rates of inquiry and account opening, and examine the motivations and barriers to program participation. This section also considers how changes to the program may have altered rates of account opening. In the final section, we examine the benefits to participation in CS4C. Beyond evaluation outcomes, CS4C also yielded a number of programmatic lessons, including the need to set clear and specific goals at program launch; to understand barriers to program success; to align with the best principles of asset building; and, to integrate program goals with existing goals of stakeholders. Programmatic lessons are discussed further in the policy considerations section. CS4C PROGRAM OUTPUTS

From February 2012 through August 2013, CS4C attracted 298 individuals to inquire about the program, provided 99 individuals with at least one financial coaching session, and assisted 63 individuals with opening 116 college savings accounts [Table 2]. Account openers deposited at least $50,888 into accounts, and CS4C program partners contributed $38,785 in incentive payments. Table 2: CS4C Program Outputs

Category Number

Total Inquirers 298 individuals

Total Participants 99 individuals

Total Participants Opening Accounts 63 individuals

Total Accounts Opened 116 accounts

Total Financial Coaching Sessions 214 sessions

Total Participant Deposits $50,888

Total CS4C Incentive Payments $38,785 Source: Program records and account statements

CS4C: Final Evaluation Report December 2013 Page 23 of 164

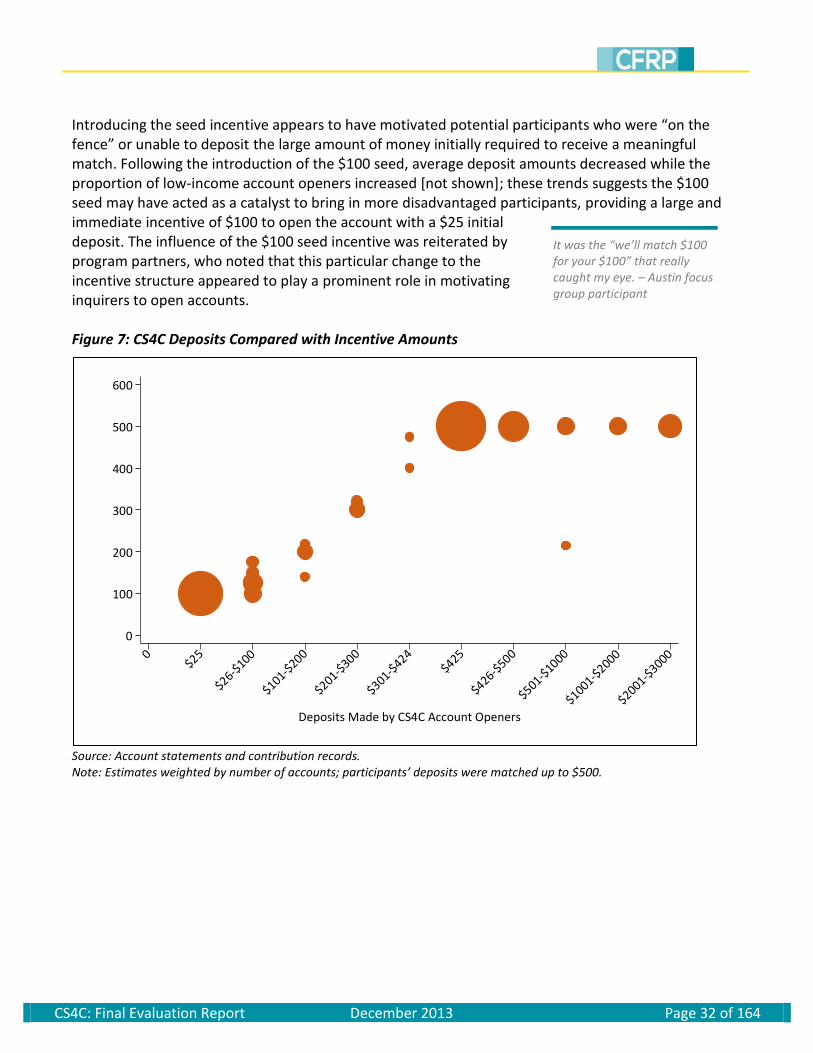

Table 3 presents information on the amount of money contributed to participant accounts. Though the average initial deposit was $224, most participants deposited substantially less than this amount when opening an account through CS4C. In fact, the median initial deposit was just $25, the minimum amount required to open an account.f The median amount of total deposits made by participants was $425, the amount needed to maximize the savings matched incentives under the final program design. Exactly one quarter of accounts received deposits totaling more than $425, with some participants, especially those opening accounts early in the program, depositing substantially more than this amount. Nearly half of accounts (47 percent), however, received less than $425 in deposits, and nearly a quarter of accounts (24 percent) only received $25 in deposits. Table 3: CS4C Account Data

Final Account Balances $773.04 $925 $125 $3500 $89,673 Source: Account statements and contribution records Note: Initial deposits based on first known deposit from participant.

Because the CS4C program did not track participant deposits once account openers achieved the maximum match, it is difficult to know the amount participant deposited to their accounts after meeting this maximum. Exit survey results suggest most participants plan to continue making regular deposits to their accounts. The CS4C program itself distributed an average of $334 in incentives to each account, though slightly more than half of accounts (52 percent) received a total of $500 in incentives—the maximum savings match. Another quarter of accounts (26%) received exactly $100 in incentives, indicating that participants only received the initial seed incentive. The other quarter of accounts received incentive amounts varying between $105 and $495. These results suggest that participants were very responsive to match limits: half contributed enough to receive the $500 match. Nearly one-quarter of participants, however, deposited only enough to receive the seed incentive. These participants may have been less responsive to the match limit because they did not have enough funds to deposit more than $25.

fThroughout this section, CFRP discusses participant deposits into accounts. Participants could open multiple accounts (one

for each child), and many of them took advantage of this policy. However, all discussion should be interpreted as happening

at the account-level.

CS4C: Final Evaluation Report December 2013 Page 24 of 164

DEMOGRAPHIC CHARACTERISTICS

Table 4 below presents demographic characteristics of inquirers, non-openers, and account openers. These three groups are markedly similar on some demographic characteristics, but differ substantially on others. Members of all three groups are likely to be female and Hispanic; approximately 9 out of 10 are female, and nearly two-thirds are Hispanic. Account openers are slightly less likely to be Hispanic, though this difference does not reach statistical significance. Account openers differ greatly from both inquirers and non-openers on several demographic and socioeconomic characteristics, however. Account openers are significantly less likely than non-openers to be married, and significantly more likely than both inquirers and non-openers to be divorced. In fact, account openers are roughly twice as likely to be divorced as those who only inquired about CS4C. Table 4: Selected Demographic Characteristics

Inquirers Non-Openers Account Openers Total

N=45 N=30 N=57 N=132

Gender

Male 6.7% 10.0% 10.5% 9.1%

Female 93.3% 90.0% 89.5% 90.9%

Race

Hispanic 66.7% 70.0% 57.9% 66.7%

Black 13.3% 10.0% 17.5% 13.3%

Other 0.0% 3.3% 3.5% 0.0%

White 20.0% 16.7% 21.1% 20.0%

Marital Status

Never Married 31.1%b 13.3%a 31.6% 27.3%

Married 28.9% 36.7%a 17.5% 25.8%

Separated 13.3%a 16.7%a 3.5% 9.8%

Divorced 24.4%a 33.3%a 47.4% 36.4%

Widowed 2.2% 0.0% 0.0% 0.8%

Education Level

Less than High School 11.1%a 10.0%a

0.0% 6.1%

High School Diploma/GED 17.8% 16.7% 8.8% 13.6%

Some College 37.8% 46.7% 36.8% 39.4%

2-Year Degree 13.3% 6.7% 14.0% 12.1%

4-Year Degree or More 20.0%a 20.0%a

40.4% 28.8%

Completed Your Own Education Goals

No 82.2%a 80.0%a

56.1% 70.5%

Yes 17.8%a 20.0%a

43.9% 29.5% Source: CS4C intake and exit survey results a

Significantly different from account openers (p≤0.05) b

Significantly different from non-openers (p≤0.05)

CS4C: Final Evaluation Report December 2013 Page 25 of 164

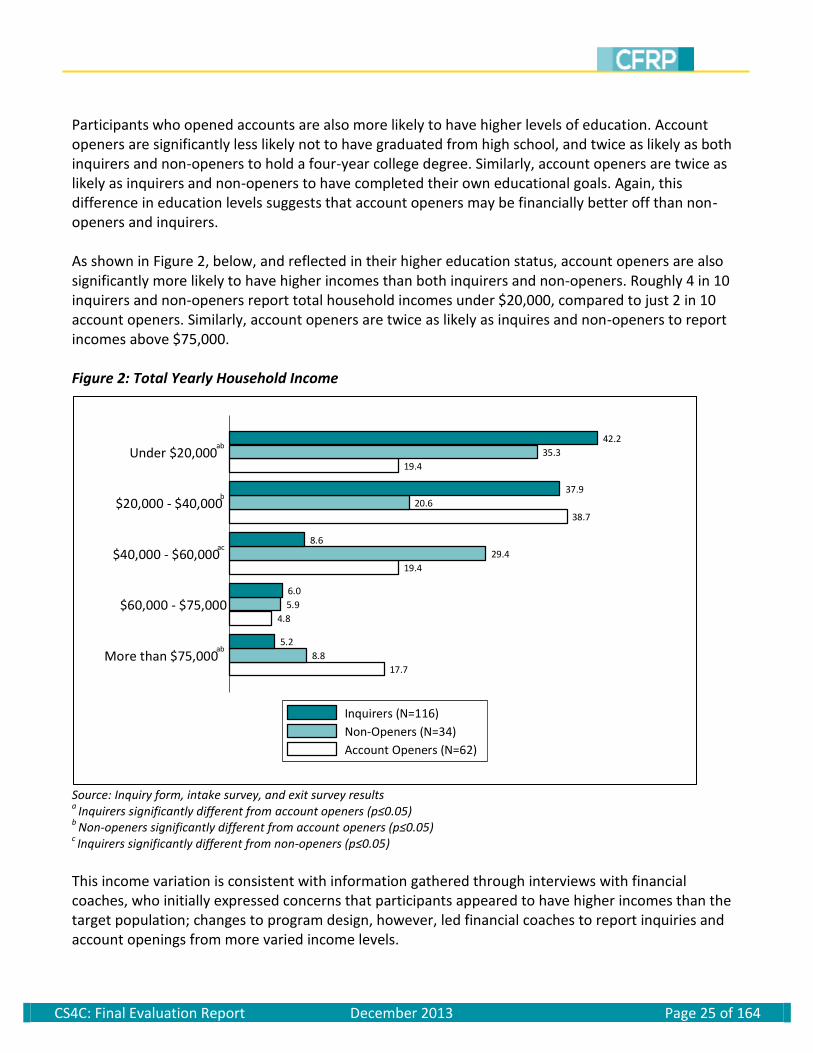

Participants who opened accounts are also more likely to have higher levels of education. Account openers are significantly less likely not to have graduated from high school, and twice as likely as both inquirers and non-openers to hold a four-year college degree. Similarly, account openers are twice as likely as inquirers and non-openers to have completed their own educational goals. Again, this difference in education levels suggests that account openers may be financially better off than non-openers and inquirers. As shown in Figure 2, below, and reflected in their higher education status, account openers are also significantly more likely to have higher incomes than both inquirers and non-openers. Roughly 4 in 10 inquirers and non-openers report total household incomes under $20,000, compared to just 2 in 10 account openers. Similarly, account openers are twice as likely as inquires and non-openers to report incomes above $75,000. Figure 2: Total Yearly Household Income

Source: Inquiry form, intake survey, and exit survey results a

Inquirers significantly different from account openers (p≤0.05) b

Non-openers significantly different from account openers (p≤0.05) c Inquirers significantly different from non-openers (p≤0.05)

This income variation is consistent with information gathered through interviews with financial coaches, who initially expressed concerns that participants appeared to have higher incomes than the target population; changes to program design, however, led financial coaches to report inquiries and account openings from more varied income levels.

17.7

8.8

5.2

4.8

5.9

6.0

19.4

29.4

8.6

38.7

20.6

37.9

19.4

35.3

42.2

More than $75,000ab

$60,000 - $75,000

$40,000 - $60,000ac

$20,000 - $40,000b

Under $20,000ab

Inquirers (N=116)

Non-Openers (N=34)

Account Openers (N=62)

CS4C: Final Evaluation Report December 2013 Page 26 of 164

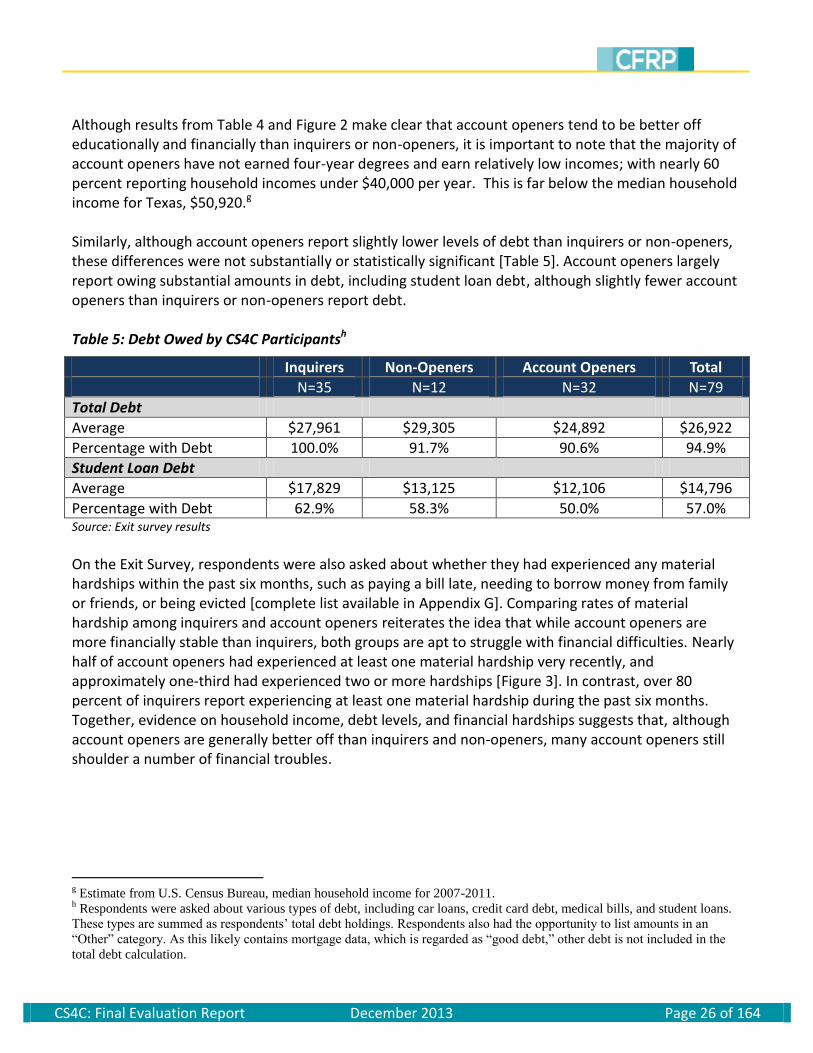

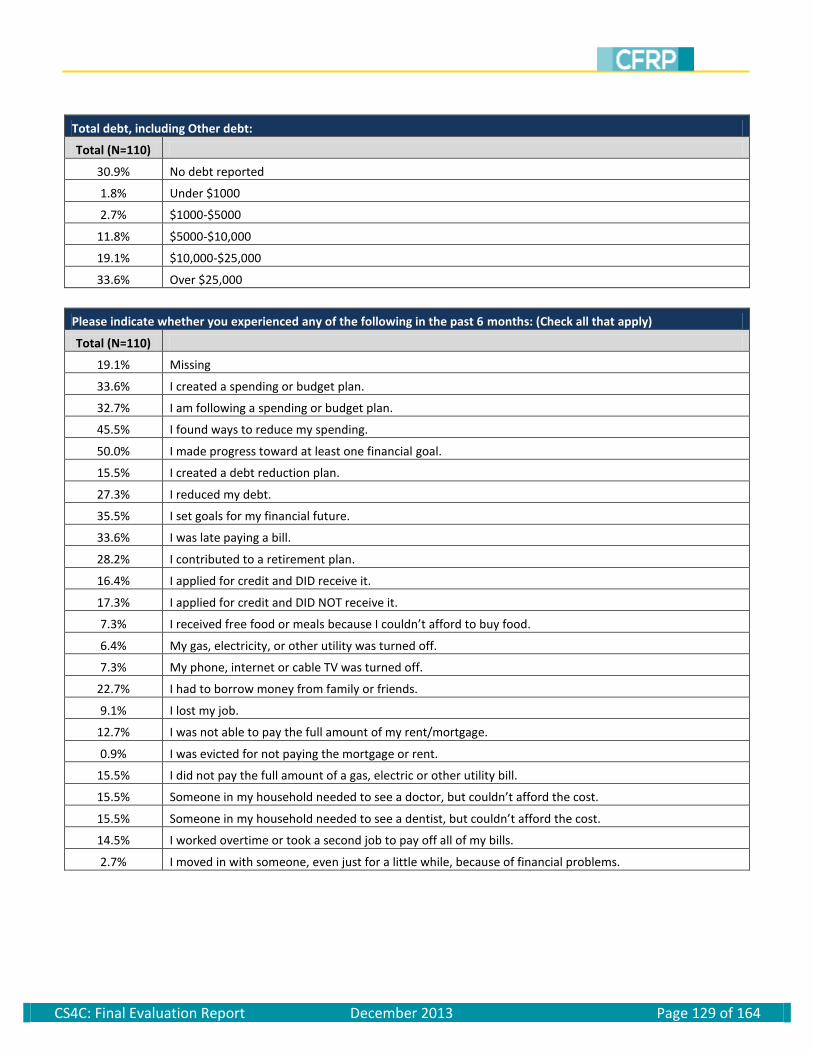

Although results from Table 4 and Figure 2 make clear that account openers tend to be better off educationally and financially than inquirers or non-openers, it is important to note that the majority of account openers have not earned four-year degrees and earn relatively low incomes; with nearly 60 percent reporting household incomes under $40,000 per year. This is far below the median household income for Texas, $50,920.g Similarly, although account openers report slightly lower levels of debt than inquirers or non-openers, these differences were not substantially or statistically significant [Table 5]. Account openers largely report owing substantial amounts in debt, including student loan debt, although slightly fewer account openers than inquirers or non-openers report debt. Table 5: Debt Owed by CS4C Participantsh

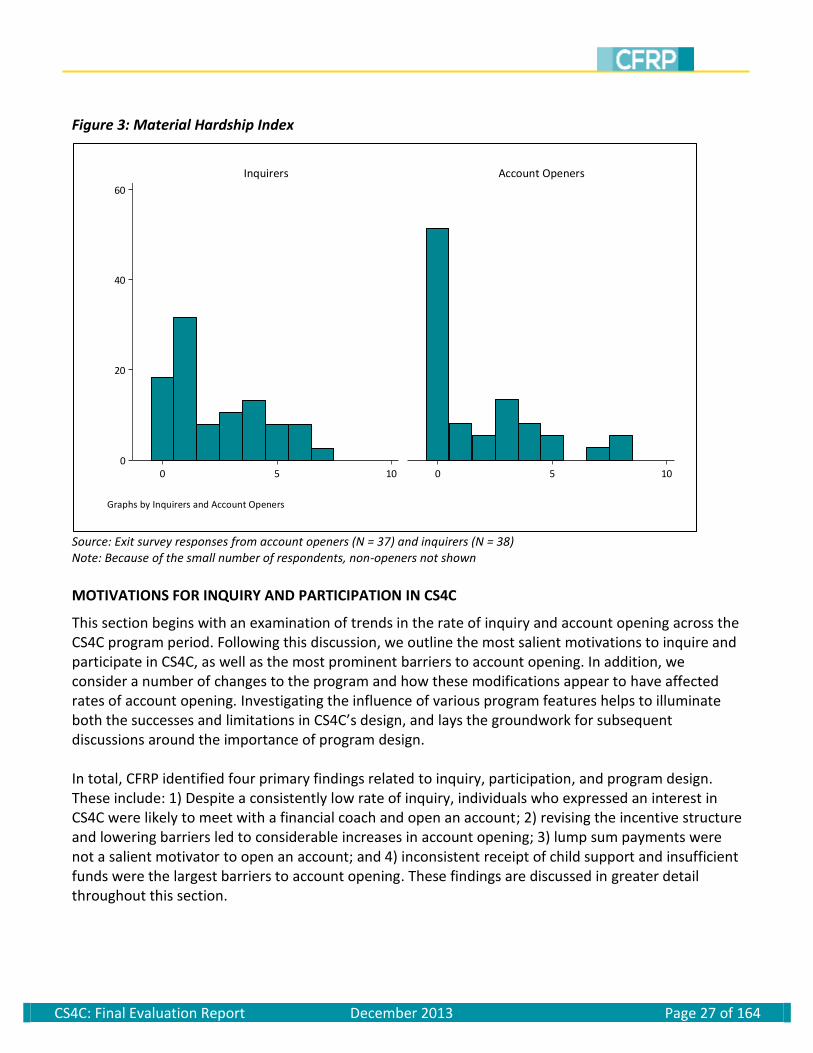

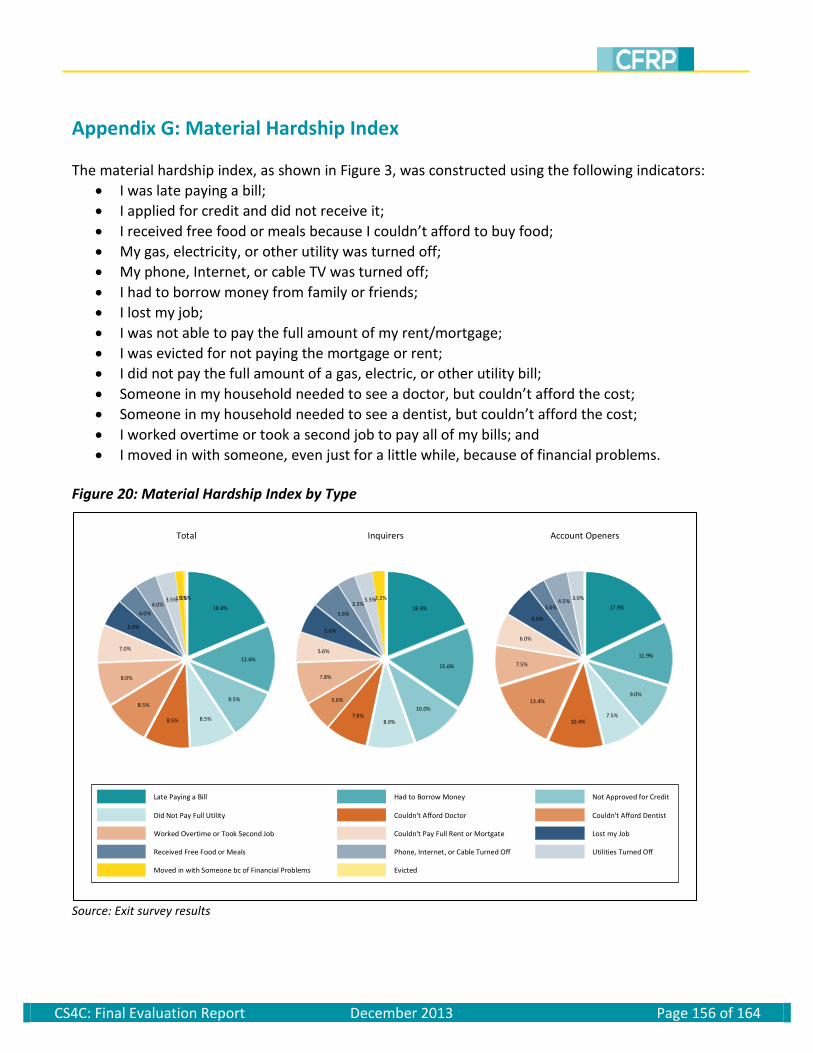

On the Exit Survey, respondents were also asked about whether they had experienced any material hardships within the past six months, such as paying a bill late, needing to borrow money from family or friends, or being evicted [complete list available in Appendix G]. Comparing rates of material hardship among inquirers and account openers reiterates the idea that while account openers are more financially stable than inquirers, both groups are apt to struggle with financial difficulties. Nearly half of account openers had experienced at least one material hardship very recently, and approximately one-third had experienced two or more hardships [Figure 3]. In contrast, over 80 percent of inquirers report experiencing at least one material hardship during the past six months. Together, evidence on household income, debt levels, and financial hardships suggests that, although account openers are generally better off than inquirers and non-openers, many account openers still shoulder a number of financial troubles.

g Estimate from U.S. Census Bureau, median household income for 2007-2011.

h Respondents were asked about various types of debt, including car loans, credit card debt, medical bills, and student loans.

These types are summed as respondents’ total debt holdings. Respondents also had the opportunity to list amounts in an

“Other” category. As this likely contains mortgage data, which is regarded as “good debt,” other debt is not included in the

total debt calculation.

CS4C: Final Evaluation Report December 2013 Page 27 of 164

Figure 3: Material Hardship Index

Source: Exit survey responses from account openers (N = 37) and inquirers (N = 38) Note: Because of the small number of respondents, non-openers not shown

MOTIVATIONS FOR INQUIRY AND PARTICIPATION IN CS4C

This section begins with an examination of trends in the rate of inquiry and account opening across the CS4C program period. Following this discussion, we outline the most salient motivations to inquire and participate in CS4C, as well as the most prominent barriers to account opening. In addition, we consider a number of changes to the program and how these modifications appear to have affected rates of account opening. Investigating the influence of various program features helps to illuminate both the successes and limitations in CS4C’s design, and lays the groundwork for subsequent discussions around the importance of program design. In total, CFRP identified four primary findings related to inquiry, participation, and program design. These include: 1) Despite a consistently low rate of inquiry, individuals who expressed an interest in CS4C were likely to meet with a financial coach and open an account; 2) revising the incentive structure and lowering barriers led to considerable increases in account opening; 3) lump sum payments were not a salient motivator to open an account; and 4) inconsistent receipt of child support and insufficient funds were the largest barriers to account opening. These findings are discussed in greater detail throughout this section.

0

20

40

60

0 5 10 0 5 10

Inquirers Account Openers

Pe

rce

nt

Graphs by Inquirers and Account Openers

CS4C: Final Evaluation Report December 2013 Page 28 of 164

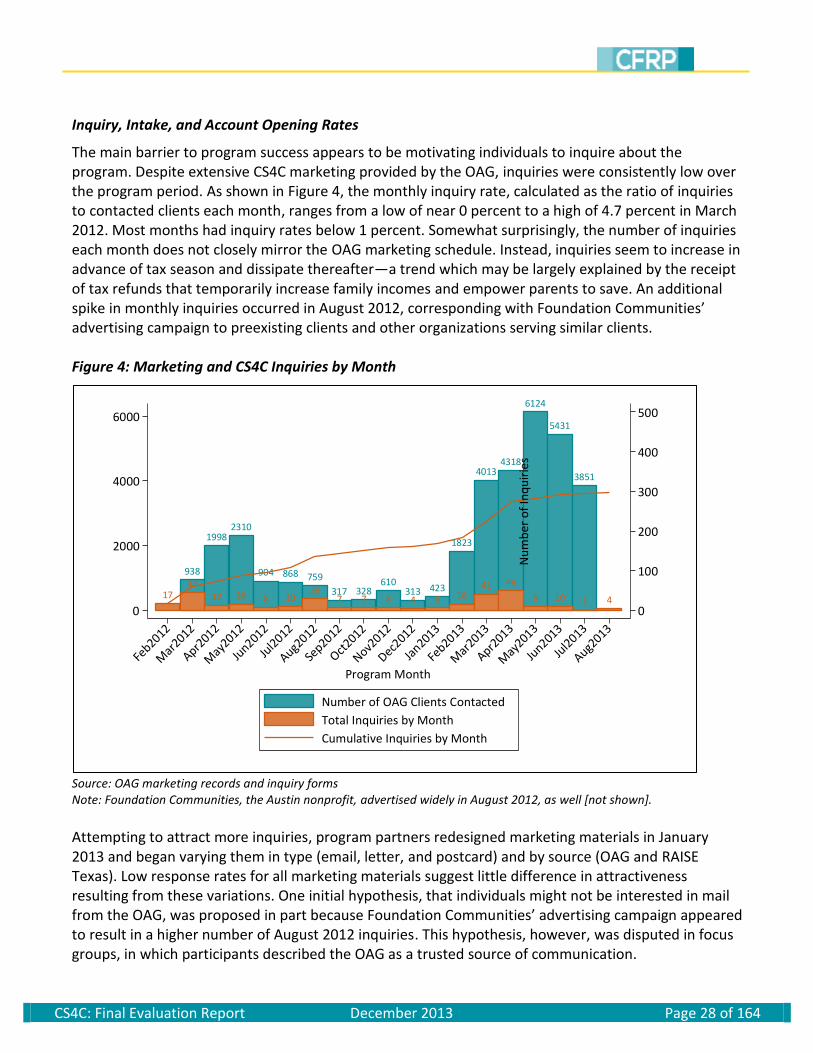

Inquiry, Intake, and Account Opening Rates

The main barrier to program success appears to be motivating individuals to inquire about the program. Despite extensive CS4C marketing provided by the OAG, inquiries were consistently low over the program period. As shown in Figure 4, the monthly inquiry rate, calculated as the ratio of inquiries to contacted clients each month, ranges from a low of near 0 percent to a high of 4.7 percent in March 2012. Most months had inquiry rates below 1 percent. Somewhat surprisingly, the number of inquiries each month does not closely mirror the OAG marketing schedule. Instead, inquiries seem to increase in advance of tax season and dissipate thereafter—a trend which may be largely explained by the receipt of tax refunds that temporarily increase family incomes and empower parents to save. An additional spike in monthly inquiries occurred in August 2012, corresponding with Foundation Communities’ advertising campaign to preexisting clients and other organizations serving similar clients. Figure 4: Marketing and CS4C Inquiries by Month

Source: OAG marketing records and inquiry forms Note: Foundation Communities, the Austin nonprofit, advertised widely in August 2012, as well [not shown].

Attempting to attract more inquiries, program partners redesigned marketing materials in January 2013 and began varying them in type (email, letter, and postcard) and by source (OAG and RAISE Texas). Low response rates for all marketing materials suggest little difference in attractiveness resulting from these variations. One initial hypothesis, that individuals might not be interested in mail from the OAG, was proposed in part because Foundation Communities’ advertising campaign appeared to result in a higher number of August 2012 inquiries. This hypothesis, however, was disputed in focus groups, in which participants described the OAG as a trusted source of communication.

938

19982310

904 868 759

317 328610

313 423

1823

40134318

6124

5431

3851

1744

12 16 8 1029

7 7 8 4 6 1641 49

9 10 1 40

100

200

300

400

500

Nu

mb

er

of

Inq

uir

ies

0

2000

4000

6000

Nu

mb

er

of

OA

G C

lien

ts C

on

tact

ed

Feb2012

Mar

2012

Apr2012

May

2012

Jun2012

Jul2

012

Aug2012

Sep2012

Oct2012

Nov2012

Dec2012

Jan2013

Feb2013

Mar

2013

Apr2013

May

2013

Jun2013

Jul2

013

Aug2013

Program Month

Number of OAG Clients Contacted

Total Inquiries by Month

Cumulative Inquiries by Month

CS4C: Final Evaluation Report December 2013 Page 29 of 164

Whenever I see something [from the OAG] I open it immediately, because it’s important! – San Antonio focus group participant

[The OAG are] next to the IRS to me…whenever they send me [anything]…it’s very important. I read it because it has to do with my income. – San Antonio focus group participant