141

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL (A GOVT. OF INDIA UNDERTAKING UNIT) SUMMER INTERNSHIP PROJECT FOREX MANAGEMENT- IMPORT AND EXPORT IN VIDHI ( IPER PGDM ) Page 1

| Date post: | 24-Oct-2014 |

| Category: |

Documents |

| Upload: | shreyansh-jain |

| View: | 45 times |

| Download: | 4 times |

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

(A GOVT. OF INDIA UNDERTAKING UNIT)

SUMMER INTERNSHIP PROJECT

FOREX MANAGEMENT-

IMPORT AND EXPORT IN

BOKARO STEEL PLANT (BSL)

VIDHI ( IPER PGDM ) Page 1

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

ACKNOWLEDGMENT

I am neither expert nor a trend spotter. I am a management student with foundations of management principles and theories who is keen in different industries, it’s happening mainly in SAIL-BSL.

I am highly obliged to Mr. Dharmendra Kumar- Assistant Manager (F & A-Purchase) SAIL-BSL, my prime internal guide for his invaluable support; guidance and knowledge that he shared with me thereby aiding me in making this project a success along with different guides as Sri S.KUMAR-Sr. Manager (F&A-Sales Invoice), MS MEENA BAKLA,(sr. manager)- (F& A PURCHASE SECTION) of each sections who provided their utmost working knowledge, which has broaden my area of interest and benefited mostly in completing the project. Their guidance and suggestions without which it was a difficult step to complete the project alone.

This provided me some experience not only in practical aspects of industry but also in human relation, group work , individual work and provided great insights into the actual working of an industry . Definitely I can’t ignore the technology with internet as a backbone in building the project.

I am obliged to DR. A.S.KHALSA (Director), my guide and other staff members, for their inspiring presence and blessings for going ahead and fulfilling the project report.

I hereby also declare that the contents in the report are true to the best of my knowledge.

Lastly I thank to INSTITUTE OF PROFESSIONAL EDUCATION AND RESEARCH,BHOPAL and BOKARO STEEL PLANT –SAIL which gave me an opportunity regarding training purpose and helped me in building some experience in my career.

Vidhi

IPER PGDM

VIDHI ( IPER PGDM ) Page 2

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

CERTIFICATE

This is to certify that the project entitled “FOREX MANAGEMENT –IMPORT AND EXPORT”

at SAIL- BOKARO STEEL PLANT has been carried out by Ms. VIDHI from 09ND MAY 2011

to 02TH JULY 2011, under my supervision in partial fulfillment of his PGDM

Programme at INSTITUTE OF PROFESSIONAL EDUCATION AND RESEARCH

(IPER), BHOPAL.

I am satisfied with her sincere performance and study conducted by her in SAIL-BOKARO

STEEL PLANT. The project is hereby approved as a bonafied work carried out and

presented in a manner satisfactory to its acceptance area to the post graduate degree for

which it has been submitted.

I recommend submitting the project report. I wish her all success in life.

This is also certified that the project work is original and has not been submitted to any other

place.

Project Guide(SAIL) Project GuideIPER)

Mr. .Dharmendra Kumar DR. A.S.KHALSAAssistant Manager -Purchase (F & A) DirectorBSL (SAIL). IPER PGDM

BHOPAL

VIDHI ( IPER PGDM ) Page 3

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

DECLARATION

I hereby declare that the following documented project report titled “FORGIEN EXCHANGE

MANAGEMENT IN SAIL-BSL “is an authentic work done by me as a part of my study on

Finance.

I also further state that the project has been prepared by my own with the secondary data

provided in the reports of the company, which were essential for the completion of the

project. The project was undertaken as a part of the course curriculum of PGDM

Programme, INSTITUTE OF PROFESSIONAL EDUCATION AND RESEARCH, (IPER),

BHOPAL, MP. This has not been submitted to any other Examination body earlier.

VIDHI

PGDM 3RD TRIM

IPER PGDM

BHOPAL,MP

VIDHI ( IPER PGDM ) Page 4

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

EXECUTIVE SUMMARY

Steel Authority of India Limited (SAIL) is the leading steel making company in India. It has

got one of the prestigious honors i.e. a”MAHARATNA COMPANY”. It is fully integrated iron

and steel maker, producing both basic and special steel for domestic construction

engineering, power, railway automotive and defense industries and for safe in export

markets. Bokaro Steel Plant – The fourth integrated plant in the public sector taking shape in

1965 in collaboration with the Soviet Union.

It was originally incorporated as a limited company on 29thJanuary 1964, and was later

merged with SAIL first as a subsidiary and then as a unit through the public sector iron &

steel companies act1978. Foreign Exchange management is concerned with import

and export procedure, mode of import payments along with export payments.

The foreign policy of this large scale company is an obligation by the Government of India,

as there will be more flow of the foreign currency. The exports are to be looked as a more

prime area because revenue is generated from it.

In today’s world no economy is self sufficient, so there is need for exchange of goods

services amongst the different countries. So in this global village, unlike in the primitive age

the exchange of goods and services is no longer carried out on barter basis. Every

sovereign country in the world has a currency that is legal tender in its territory and this

currency does not act as money outside its boundaries. So whenever a country buys or sells

goods and services from or to another country, the parties of both countries have to

exchange currencies. So we can imagine that if all countries have the currency then there is

no need for foreign exchange. Importing is an importing tool for increasing our production as

lower labour costs or a different tax regime may mean one country’s prices for a particular

product are significantly lower than those in the other country moreover a higher-quality of

finished products or raw materials with upgrades the quality level of of the goods produced.

VIDHI ( IPER PGDM ) Page 5

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Exports are a part of its revenue but the plant does not fully depend on it as its customers

are more of domestic area than the foreigners.

In short it can be said that this project mainly deals with :

Procedure of payment of foreign exchange to the importers and exporters through LC, CAD , WIRE TRANSFER and PURCHASE ORDER AS WELL AS HOW FOREIGN EXCHANGE REMIT IS DONE .

VIDHI ( IPER PGDM ) Page 6

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

CONTENTS:

1) A) HISTORY OF SAIL

B) CURRENT POSITION OF STEEL INDUSTRY

2) COMPANY’S PROFILE

a) HISTORY OF SAIL

b) MANAGEMENT

3) FINANCE DEPARTMENT OF SAIL

4) IMPORT AND EXPORT OBLIGATION OF SAIL

5) DATA AND INTERPRETATION

6) FOREIN EXCHANGE MANAGEMENT AND DOCUMENTATION IN SAIL

7) PROBLEM IN FOREIN EXCHANGE MANAGEMENT

8) SUGGESTION AND CONCLUSION

9) BIBLIOGRAPHY

10) ANNEXTURE

VIDHI ( IPER PGDM ) Page 7

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

CHAPTER-1

A. History of Steel Industry In India

The antiquity of man’s use of iron attested by references to that metal both in

fragmentary writing & inscriptions that survived ancient civilization of Babylon, Mexico,

Egypt, China, India, Greece & Rome. However, it is believed that most of the iron used

by pre–historic people might have been obtained by fragment of meteorites and it

remained a rare metal for many centuries.

For many years after man learned how to extract iron from its ores, the product probably was so relatively soft and unpredictable, that bronze continued to be preferred for many tools and weapons. Eventually iron replaced the non–ferrous metal for these purposes when man learned how to master the difficult arts of smelting, forging, hardening and tempering iron. Archeological findings in Mesopotamia and Egypt have proved that iron or steel has been in the service o mankind for nearly 6000 years. The origin of the methods used by early man for

Extracting iron from its ores is unknown. Some have suggested that many learned the

method accidentally.

Iron, in the beginning was smelted by charcoal made from wood. Later coal was discovered

as a great source of heat. Subsequently, it was converted into coke, which was found to be

ideal for smelting of iron. Iron kept its dominant place for 200 or more years after the Saugus

works that was the first successful Iron Works in America founded in 1646, with the advance

of Industrial Revolution, iron formed the rails for newly invented railroad trains. It was also

used to amour the sides of the fighting ships. About the mid 19th century the new age of

steel began with the invention of Bessemer process (1856) making steel available in large

quantities at reasonable cost.

Indian history is also replete with references to the usage of iron and steel. Some of the

ancient monuments like the famous iron pillar near New Delhi or the massive beams used in

the Sun Temple at Konark bear ample testimony to the technological excellence of the

Indian metallurgists.

VIDHI ( IPER PGDM ) Page 8

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

The history of iron in India goes back to the ancient era. Our ancient literary sources like Rig

Veda, the Atbara Veda, the Puranas and other Epics are full of references to iron and its

uses in peace and war. According to one of the studies, iron has been produced in India for

over 3000 years.

B.Current Position of Steel Industry

Steel industry has a major role to play in the economic growth of India. With new global acquisitions by Indian steel giants, setting up of new state-of-the-art steel mills, modernisation of existing plants, improving energy efficiency and backward integration into global raw material sources, India is now on the centre of the global steel map. Consumption of steel in the construction sector, industrial applications, and transport sector has been on the rise and special steel usage in engineering industries such as power generation, petrochemicals and fertiliser industry is also growing.

India has retained its position as the 5th largest producer in 2010 and recorded a growth of 11.3 per cent as compared to 2009. India has also emerged as the largest sponge iron/direct reduced iron (DRI) producing country in the world in 2010, a rank it has held on since 2002. Sponge iron production grew at a CAGR of 11 per cent to reach a level of 20.74 million tonne (MT) in 2009-10 as compared to 14.83 MT in 2005-06. India is expected to become the second largest producer of steel in the world by 2015-16, on account of growing steel demand, rich resources base of iron ore, skilled manpower and vast experience of steel making and the huge capacity expansion planned and being executed in the steel sector.With the expanding consumer market, Indian steel industry is likely to receive huge domestic and foreign investments. Nearly 222 memorandums of understandings (MoUs) for planned capacity of around 276 MT have been signed between the investors and various State Governments, mostly in Orissa, Jharkhand, Chhattisgarh and West Bengal.

India has recorded a growth of over 8.6 per cent, producing 6.35 MT of steel in March 2011 as against 5.85 MT in the corresponding month in 2010, according to World Steel Association (WSA).

Steel exports has increased by 17.3 per cent as it reached an estimated 2.46 MT, while steel imports were at an estimated 5.36 MT, a growth of 2.8 per cent in 2010.

VIDHI ( IPER PGDM ) Page 9

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Production-

Crude steel production was registered at 51.57 MT during April-Dec 2010 in the country as per Joint Plant Committee (JPC). The production is expected to be nearly 110 MT by 2012-13.

Crude steel production grew at a compound annual growth rate (CAGR) of 8.4 per cent during the five years, 2005-06 to 2009-10. The crude steel performance accounted for 31 per cent of the total crude steel production in the country during 2009-10, contributed largely by the strong trends in growth of the electric route of steel making, particularly the induction furnace route, which was a key driver in the growth of the segment. In case of total finished steel (alloy + non-alloy), production for sale was recorded at 47.30 MT, a growth of 7.9 per cent during Apr-Dec 2010.

Steel Authority of India (SAIL) Ltd has planned to enhance its hot metal production capacity from the level of 13.82 million tones per annum (MTPA) to 23.46 MTPA under its current phase of expansion and modernization which is expected to be completed by financial year 2012-13. In the next phase, SAIL would increase its capacity further to 26.18 MTPA.The indicative investment for current phase is about US$ 13.28 billion. Additionally, approximately US$ 2.21 billion has been earmarked for modernisation and expansion of SAIL Mines.

NMDC Ltd plans to increase the production of iron ore from the present level of about 24 MT to 40 MT by 2014-15. Besides, setting up a 3 MTPA Integrated Steel Plant at Nagarnar in Chhattisgarh. The environmental clearance for the plant has been accorded by Ministry of Environment and Forests (MoEF).

Consumption-

The Indian steel industry has been on a high-growth trajectory led by buoyancy in sectors such as infrastructure and construction, oil and gas and automobiles. The demand for steel is expected to further increase with major international automobile manufacturers setting manufacturing facilities in India.

The consumption of steel domestically was recorded at 44.28 MT, indicating further strengthening of demand during Apr-Dec 2010. The consumption of steel in the country has shown an increase of 10.3 per cent during April 2010 to January 2011 as compared to the same period of previous year.

VIDHI ( IPER PGDM ) Page 10

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

CHAPTER-2

COMPANY PROFILE

A. History of SAIL

A Rich Heritage

The Precursor

SAIL traces its origin to the formative years of an emerging nation - India. After

independence the builders of modern India worked with a vision - to lay the infrastructure for

rapid industrialisaton of the country. The steel sector was to propel the economic growth.

Hindustan Steel Private Limited was set up on January 19, 1954. The President of India

held the shares of the company on behalf of the people of India.

Expanding Horizon (1959-1973)

Hindustan Steel (HSL) was initially designed to manage only one plant that was coming up

at Rourkela. For Bhilai and Durgapur Steel Plants, the preliminary work was done by the

Iron and Steel Ministry. From April 1957, the supervision and control of these two steel

plants were also transferred to Hindustan Steel. The registered office was originally in New

Delhi. It moved to Calcutta in July 1956, and ultimately to Ranchi in December 1959.

A new steel company, Bokaro Steel Limited, was incorporated in January 1964 to construct

VIDHI ( IPER PGDM ) Page 11

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

and operate the steel plant at Bokaro. The 1 MT phases of Bhilai and Rourkela Steel Plants

were completed by the end of December 1961. The 1 MT phase of Durgapur Steel Plant

was completed in January 1962 after commissioning of the Wheel and Axle plant. The crude

steel production of HSL went up from .158 MT (1959-60) to 1.6 MT. The second phase of

Bhilai Steel Plant was completed in September 1967 after commissioning of the Wire Rod

Mill. The last unit of the 1.8 MT phase of Rourkela - the Tandem Mill - was commissioned in

February 1968, and the 1.6 MT stage of Durgapur Steel Plant was completed in August

1969 after commissioning of the Furnace in SMS. Thus, with the completion of the 2.5 MT

stage at Bhilai, 1.8 MT at Rourkela and 1.6 MT at Durgapur, the total crude steel production

capacity of HSL was raised to 3.7 MT in 1968-69 and subsequently to 4MT in 1972-73.

Holding Company

The Ministry of Steel and Mines drafted a policy statement to evolve a new model for

managing industry. The policy statement was presented to the Parliament on December 2,

1972. On this basis the concept of creating a holding company to manage inputs and

outputs under one umbrella was mooted. This led to the formation of Steel Authority of India

Ltd. The company, incorporated on January 24, 1973 with an authorized capital of Rs. 2000

crore, was made responsible for managing five integrated steel plants at Bhilai, Bokaro,

Durgapur, Rourkela and Burnpur, the Alloy Steel Plant and the Salem Steel Plant. In 1978

SAIL was restructured as an operating company.

Since its inception, SAIL has been instrumental in laying a sound infrastructure for the

industrial development of the country. Besides, it has immensely contributed to the

development of technical and managerial expertise. It has triggered the secondary and

tertiary waves of economic growth by continuously providing the inputs for the consuming

industry.

VIDHI ( IPER PGDM ) Page 12

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

JOINT VENTURES

SAIL has promoted joint ventures in different areas ranging from power plant to e-

commerce. The important joint ventures of the company, among others, are:-

COMPANY LOCATION JV PARTNER EQUITY PROFILE

NTPC-SAIL

Power

Company Pvt.

Ltd

NEW DELHI NTPC 50:50 Operates & manages the

captive power plants of

durgapur, Rourkela & Bhilai

Bokaro Power

supply

company Pvt.

Ltd

BOKARO DVC 50:50 Manages 302MW power

generation 660tonnes per hour

steam generation facilities at

Bokaro steel plant.

M- Junction

services Ltd.

KOLKATA TATA Steel 50:50 Promotes e-commerce

activities in steel and related

areas.

SAIL & MOIL

Ferro Alloys

Pvt. Ltd.

BHILAI MANGANESE

ORE (INDIA)

LIMITED

50:50 Production of ferro -

manganese and silicon –

Manganese at Bhilai with

furnace operation at Nandini/

Bhalai

Bhilai jaypee

cement limited

SANTNA &

BHILAI

Jaiparkash

Associates Ltd.

26:74 To set up and operate a

cement plant of 2.2 million

tones per annum capacity at

split location at satna & Bhilai ,

using slag generated during

VIDHI ( IPER PGDM ) Page 13

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

blast furnace .

Bokaro jaypee

cement Ltd.

BOKARO Jaiparkash

Associates Ltd.

26:74 To set up and operate a

cement plant of 2.1 million

tones per annum capacity,

utilizing generated slag during

Blast furnace operation at BSL.

MEMORANDUM OF UNDERSTANDINGS

Larsen & Toubro Ltd.

to set up, develop, manage and own captive/independent power plant (s) at suitable location/s to meet future power requirements of SAIL. The scope of agreement also includes exploration of opportunities to own captive thermal coal blocks to cater to the power plant requirements.

Shipping corporation of India.

to promote a Joint Venture Company, which shall primarily provide shipping related services to SAIL for imported coking coal and also participate in world wide dry bulk shipping trade.

Government of Kerala

to increase production from the existing facilities at Steel Complex Limited (SCL), Calicut and also set up, develop & manage a 50,000 TMT Rolling Mill along with its balancing facilities and auxiliaries at SCL, Calicut.

POSCO to collaborate in a wide range of strategic business and commercial areas of mutual interest.

Rashtriya Ispat Nigam Ltd. (RINL)

to jointly explore and develop low silica limestone mines in the Sultanate of Oman.

Mineral Exploration Corporation Ltd. (MECL)

for exploration by MECL at all SAIL mines for assessing the reserves and quality of ore available. It has already started exploratory work in Gua and Chiria mines.

Heavy Engineering Corporation (HEC)

for equipment/spares required for modernization/expansion.

VIDHI ( IPER PGDM ) Page 14

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Bharat Earth Movers Limited (BEML)

for supply of crucial equipment.

Rajasthan State Mines & Minerals Limited (RSMML)

for long-term supply of low-silica limestone.

IIM, Ahmedabad and Management Development Institute (MDI), Gurgaon

knowledge sharing.

Indian Railways

for procurement of high power locomotives

HistoryBokaro steel plant brings out before one’s eyes the vision of a massive giant in the making. Bokaro Steel Plant - the fourth integrated plant in the Public Sector - started taking shape in 1965 in collaboration with the Soviet Union. It was originally incorporated as a limited company on 29th January 1964, and was later merged with SAIL, first as a subsidiary and then as a unit, through the Public Sector Iron & Steel Companies (Restructuring & Miscellaneous Provisions) Act 1978. The construction work started on 6th/April/1968.

The Bokaro Steel Plant is hailed as the country’s first Swadeshi steel plant, built with maximum indigenous content in terms of equipment, material and know-how. Its first Blast Furnace started on 2nd October 1972 and the first phase of 1.7 MT ingots steel was completed on 26th February 1978 with the commissioning of the third Blast Furnace. All units of 4 MT stage have already been commissioned and the 90s' modernization has further upgraded this to 4.5 MT of liquid steel.

Bokaro Steel Plant (BSL) situated in the coal belt of the eastern region, symbolize India’s advancement in the design, engineering & equipment suppliers & construction of steel plants. It is the 4th integrated steel plants in the public sector conceived in 1959; it actually started taking shapes in 1965, with the collaboration of “SOVIET UNION”. It was initially set up with a capacity of 1.7 million tones (MT) of flat products per annum with a provision to expand up to 4 million tones .It was incorporated as a limited company. The plant was conceived as the country’s 1st “SWADESHI” steel plant to be built with maximum indigenization going into the equipments, materials & know-how.

VIDHI ( IPER PGDM ) Page 15

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

The Bokaro Steel Plant is an integrated metallurgical unit engaged in the production of ingots, plates, sheets and coils. In the process, it also produce a number of by -products crude tar, Ammonium sulphate, Benzene, Xylene, Toluene, Coal Tar , Cresols.

Medical FacilitiesThe township has a modern 1100-bed Bokaro General Hospital (BGH) with specialized units like Critical Care Unit, Intensive Coronary Care Unit, Nuclear Medicine Laboratory, Ultra modern operation theatre complex and eye operation theatre. The child care unit of the hospital has been recognized as baby friendly hospital by the UNICEF. The blood bank has been given the status of regional training center by the central government, the only one in the Jharkhand. To take care of the employees working in plant, an occupational health service center has been provided within the plant premises. BGH has been granted the status of one of the training centers for students of nursing. The medical team boasts of around 200 doctors and 1000 paramedic staff.

B. Management

The Government of India owns about 86% of SAIL's equity and retains voting control of the company. However, SAIL, by virtue of its ‘Navratna’ status, enjoys significant operational and financial autonomy. SAIL has created its own Central Marketing Organization (CMO) and the International Trade Division to take care of its international and marketing operations

The steel products manufactured by SAIL include:

Hot and cold rolled sheets and coils Galvanized sheets Electrical sheets Railway products Plates, bars and rods Stainless steel and other alloy steels

Integrated Steel Plants

Bhilai Steel plant (BSP) in Chhattisgarh Durgapur Steel Plant (DSP) in West Bengal Rourkela Steel Plant (BSL) in Jharkhand IISCO Steel Plant (ISP) in West Bengal Bokaro Steel limited (BSL) in Jharkhand

CHAPTER-3

VIDHI ( IPER PGDM ) Page 16

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Finance Department of SAIL

Finance is described as ‘science of money’ and involves the process of conversion of accumulated funds to productive use .The essence of the effective financial management is that the income generated should be greater than the cost of procuring and processing the raw materials by optimum utilization of the same.

In the recent changed business scenario which is the outcome of changed Indian economic policy from command economy to free economy to integrate the Indian economy to the world economic order .The role of financial manager has become a crucial one since the factor of efficiency in all productivity field has become paramount.

In a multi process industry like an integrated steel plant like this one where some processes remain involved in certain endothermic behavior of cost one finds it difficult to prepare the cost benefit analysis ,hence in deciding the optimum level of activity because each level of activity can be attained with the various number of alternative resources available at a particular point in time.

F&A is an important department of BSL headed by ED .There are 34 production cost centers, 24 service centers and 18 job costing centers of engineering shops : Cost and budget section allows process costing systems for its production and service centers job costing method for its engineering shops for maintaining its cost record like production and consumption of RM,power,fuel,stores, spares etc. .In production and service cost per unit is determined upon output and in engineering shop cost is determined upon machine hour rate .Monthly and annual cost is prepared on actual basis and derivations are reported to higher management through MIS report.

The reporting of actual business performance and analysis of reason for variance with planned one is done by use of management accounting techniques like variance analysis, ratio analysis and sensitivity analysis .Cost reduction activity is being monitored by cost and budget section and performance in this stage is brought to the notice of higher management.

Organizations like SAIL which has various units and subsidiaries, finance and accounts plays an important role.

3.1) Sections in Finance and Accounts

VIDHI ( IPER PGDM ) Page 17

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

CODE-01 PAY SECTION

It deals with the accounting of employee’s related salary slip .Basically deals with any activity related to pay .Loan, Bonus

Any monthly payments taken once in a year

CODE-02 MAIN ACCOUNTS SECTION

It deals with the consolation of accounts with each quarter along with the final close. It prepares a main ledger, assets ledger, section ledger and trial balance etc...It prepares and maintains assets register of the company .It facilitates the inter plant reconciliation, coordination with the various auditors.

CODE-03 PURCHASE ACCOUNTS

It basically deals with the payments and accountings of all the goods against which purchase order has been placed. Its work starts when goods are received and verified with GRN (goods and returned notes).They receive and verify the bill.

CODE-04 CASH ACCOUNT

It deals with the disbursement and receipt of cash as per the bills passed by the officers of various sections .Its main function includes monitoring of cash deposit ,liasioning with banks .They generally prepare the bank reconciliation statements(BRS).They deal with Rs 350-380 crores of expenditure on monthly basis. Whereas the revenue side consists of lease, rent etc.

CODE-05 PROJECT FINANCE

It deals with the project accounting (not with the project calculation).Basically it deals with the payments to parties related to different projects.

CODE-06 ESTATE ACCOUNTS

It deals with the accounting of IPU cases.IPU is investment in planning unit and is related to projects.

CODE-08 STORE ACCOUNTS

It deals with the accounting and maintenance of stores ledger .receipt, balance of inventories etc. . .Stores department has the custody of around two lakh items. The document raised by the stores department is:

Issue notes

VIDHI ( IPER PGDM ) Page 18

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Material return notes

Dispatch notes

Goods receipt notes

Stock transfer voucher

Stock adjustment voucher

Provisional voucher

Book transfer voucher

CODE-09 PROVIDENT FUNDS

It deals with the accountings of employee’s provident funds along with the loans taken against provident funds balance.

CODE-10 FREIGHT ACCOUNTS

It deals with the payments and accounting of freight bills related to raw materials .This section generally deals with the freight inward whereas outward is dealt by the invoicing section(which is not the part of sales accounts).

CODE-11 INSURANCE SETION

It deals with the accounting of sales tax matters which are related to steel goods

CODE -12 OPERATIONAL PAYMENTS SECTION

It deals with the payments of those expenditures which are generally not related with any particular department like

Telephone bills

Water bills-15 crores

Township management bills

Aviation

Miscellaneous payments

City park (horticulture)

In plant scrape recovery-15 crores

Railways-10 crores

VIDHI ( IPER PGDM ) Page 19

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Sports

CMO

CODE-14 SALES ACCOUNTS

It deals with the preparation of invoice and accounting thereof.

CODE-15 COST AND BUDGET

There are 77 cost centers .They prepares the budget on monthly, quarterly and annual basis .They deal with daily profits. They prepare the MIS reports .They make the valuation of finished /semi finished stock of plant .Actually this section decides the rate of each output.

CODE -16 RAW MATERIAL

It deals with the accounting of raw material consumption including Ferro and non Ferro items.It deals with evaluation of raw materials as well as payment of bills related to raw material.

CODE-17 EXCISE ACCOUNTS

It deals with the CENVAT, Excise duty.

CODE -18 VAT

It deals with the accounting and payments of VAT to central governments.

3.2) Finance and Accounts Department

Organization Chart

VIDHI ( IPER PGDM ) Page 20

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

VIDHI ( IPER PGDM ) Page 21

ERPKolkata A/C

Sales & Excise ,Service Tax ,Indirect Taxes –Report & Return

Purchase & Stores A/C,RM A/C, Railway Freight & Claim, Opas, Direct Taxes Report & Return

C&B, Main A/C, Stock Verification,MIS, Govt. Audit and Internal Audit

Pay A/C,PF & Pension, Time Office, Estate A/C, BGH

OF,Project Finance, A/C admin, Cash A/C, Insurance&Claims, Hindi Cell,Quality Circle & Suggestion Scheme

DGM (F&A)

DGM (F&A)

DGM (F&A)

DGM(F&A)

DGM (F&A)

DGM (F&A)

DGM (F&A)

GM (F&A)

ED (F&A)

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

CHAPTER 4

Import and Export obligation of SAIL

The Indian steel industry have entered into a new development stage from 2005-06, riding high on the resurgent economy and rising demand for steel. Rapid rise in production has resulted in India becoming the 7th largest producer of steel.

India’s steel consumption will continue to grow at nearly 16% rate annually, till 2012, fuelled by demand for construction projects worth US$ 1 trillion.

The National Steel Policy has envisaged steel production to reach 110 million tones by 2019-20. However, based on the assessment of the current ongoing projects, both in Greenfield and Brownfield, Ministry of Steel has projected that the steel capacity in the county is likely to be 124.06 million tones by 2011-12.

Production

Steel industry was relicensed and decontrolled in 1991 & 1992 respectively. Today, India is the 7th largest crude steel producer of steel in the world. In 2008-09, production of Finished (Carbon) Steel was 59.02 million tones. Production of Pig Iron in 2008-09 was 5.299 Million Tons. Last 5 year's production of pig iron and finished (carbon) steel is given below:

(in million tons)

Category 2004-05 2005-06 2006-07 2007-08 2008-09

Pig Iron 3.228 4.695 4.993 5.314 5.289

Finished Carbon Steel 40.055 44.544 55.416 58.233 59.02

Imports of Iron & Steel

Iron & Steel are freely importable as per the extant policy. Last five years import of Finished (Carbon) Steel is given below:-

Year Qty. (In Million Tons)

2004-2005 2.109

2005-2006 3.850

2006-2007(Partly estimated)

4.436

2007-08 6.581

2008-2009(Partly estimated)

5149

VIDHI ( IPER PGDM ) Page 22

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Exports of Iron & Steel

Exports (Qty. in Million Tonnes)

Year Finished (Carbon) Steel Pig Iron

2004-2005 4.381 0.393

2005-2006 4.478 0.440

2006-2007(Prov. estimated)

4.750 0.350

2007-2008 4.627 0.560

2008-2009(Prov. estimated)

3.482 0.350

India has also emerged as the largest sponge iron/direct reduced iron (DRI) producing country in the world in 2010, a rank it has held on since 2002. Sponge iron production grew at a CAGR of 11 per cent to reach a level of 20.74 million tonne (MT) in 2009-10 as compared to 14.83 MT in 2005-06. India is expected to become the second largest producer of steel in the world by 2015-16, on account of growing steel demand, rich resources base of iron ore, skilled manpower and vast experience of steel making and the huge capacity expansion planned and being executed in the steel sector.

India has recorded a growth of over 8.6 per cent, producing 6.35 MT of steel in March 2011 as against 5.85 MT in the corresponding month in 2010, according to World Steel Association (WSA).

Steel exports has increased by 17.3 per cent as it reached an estimated 2.46 MT, while steel imports were at an estimated 5.36 MT, a growth of 2.8 per cent in 2010.

Crude steel production was registered at 51.57 MT during April-Dec 2010 in the country as per Joint Plant Committee (JPC). The production is expected to be nearly 110 MT by 2012-13.

The steel industry in India is likely to receive huge domestic and foreign investments.

Posco, South Korea, plans to set up a 12 MT integrated steel plant in Orissa. Mittal Group's announced plans to set up their 12 MT integrated steel unit in Orissa. Bhilai Steel Plant (BSP), the flagship entity of the Steel Authority of India Limited

(SAIL), has secured a fresh order of exporting rails to Sri Lanka. The order of about 14,000 tonnes is for the UIC-60 grade of rails. Earlier, the company had received an order to supply 6,500 tonnes of rails to Sri Lanka.

Tata Steel Ltd (TSL) and Nippon Steel Corporation (NSC) have signed a joint venture (JV) agreement to setup India's first continuous annealing and processing line

VIDHI ( IPER PGDM ) Page 23

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

(CAPL) for the production of 600,000 tonnes per annum of automotive cold-rolled steel at Jamshedpur, India. The project will be set up at a capital cost of approximately US$ 509.08 million and is expected to come on stream in 2013.

IMPORT

Importing of goods was for a long period of time. As the goods which were unavailable in one country was too imported from the other sourced country. Before it was similar to the barter system but as the year passes as the world changes to a growth stage, these importing of goods becomes a business and of course of a more profitable one.

Now many big organizations do importing of goods and raw materials which enhanced their production to a high margin.

Sail basically imports.

There are a number of benefits to be gained by opting for an overseas supplier.

o Lower priced goods: Lower labour costs or a different tax regime may mean one country’s prices for a particular product are significantly lower than those in the UK.

o Higher-quality finished products: Every country has its specialties and strengths. If you want the very best, it could be to your advantage to import from a particular country.

o Traditional skills and raw materials: It makes sense to take advantage of traditional crafts and skills that have been carried on for generations in some cultures.

o Original products: Originality and authenticity are important in some markets

if you want to keep ahead of your competitors

Since the payments are done by conversion from currency to the another. There may be some type of risk as fluctuating exchange rates can affect the price of the product and your profitability. A forward exchange contract is one way to protect you. This is a binding obligation to buy or sell a certain amount of foreign currency at a pre-agreed rate of exchange, on or before a certain date. This enables you to budget at a guaranteed rate of exchange.

Payment options

How you choose to pay your supplier depends on a number of factors, not least the level of trust between the two..

Open Account-Orders placed with organizations may be dealt with on an open account basis. The supplier trusts your ability to pay them against their invoice within, say, 30 days. Clearing banks offer fast money electronic transfer systems for such transactions. Or you could open a euro currency account allowing you to trade with countries in the Euro zone using just one account.

VIDHI ( IPER PGDM ) Page 24

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Letters of credit

These offer both buyer and seller security and are honored through the banking system. The conditions are stated on the letter of credit, including the amount to be paid, a description of the goods and what documents the exporter must present to receive payment. The importer’s bank guarantees the exporter that payment will be made if those conditions are met.

Documentary collections

Documents relating to the goods imported are sent by the supplier via their own bank to your bank. Your bank receives all the shipping documents and the invoices, which state the methods of payment. The bank will notify you when it has all the documents. The advantage of this system is that you, as the importer, don’t have to make payment for your goods until you have accepted the documents relating to them from your bank.

Terms of delivery and means of transport

Although some suppliers may want to quote for their goods including the transport or freight charges, importer may take responsibility for goods early in the supply chain. This allows choosing the carrier, routing and point of entry into the imported country. Always inspect goods as soon as they are received.

FOB – Free on board Named port of shipment – Maritime and inland waterway transport only

The seller delivers the goods, cleared for export, when they pass the ship’s rail at the named port of shipment.

CFR – Cost and freight Named port of destination – Maritime and inland waterway transport only

The seller delivers the goods when they pass the ship’s rail in the port of shipment and must pay the costs and freight necessary to bring the goods to the named port of destination.

CIF – Cost insurance and freight Named port of destination – Maritime and inland waterway transport only

The same as CFR except the seller must also procure insurance against the buyer’s risk of loss or damage during carriage.

CPT – Carriage paid to Named place of destination – Any mode of transport

VIDHI ( IPER PGDM ) Page 25

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

The seller delivers the goods to the nominated carrier and must also pay the cost of carriage necessary to bring the goods to the named destination.

IMPORT PROCEDURE

PROCEDURE CUM PAYMENT FACILITATED AT BOKARO STEEL PLANT (SAIL)

MODE OF PAYMENT

A letter of credit makes a bank's promise to pay the exporter to that of the foreign buyer provided that the exporter has complied with all the terms and conditions of the letter of credit. The foreign buyer applies for issuance of a letter of credit from the buyer's bank to the exporter's bank and therefore is called the applicant; the exporter is called the beneficiary.

Payment under a documentary letter of credit is based on documents, not on the terms of sale or the physical condition of the goods. The letter of credit specifies the documents that are required to be presented by the exporter, such as an ocean bill of lading (original and several copies), consular invoice, draft, and an insurance policy. The letter of credit also contains an expiration date. Before payment, the bank responsible for making payment, verifies that all document conform to the letter of credit requirements. If not, the discrepancy must be resolved before payment can be made and before the expiration date.

A letter of credit may either be irrevocable and thus, unable to be changed unless both parties agree; or revocable where either party may unilaterally make changes. A revocable letter of credit is inadvisable as it carries many risks for the exporter.

A change made to a letter of credit after it has been issued is called an amendment. Banks also charge fees for this service. It should be specified in the amendment if the exporter or the buyer will pay these charges. Every effort should be made to get the letter of credit right the first time since these changes can be time-consuming and expensive.

To expedite the receipt of funds, wire transfers may be used. Exporters should consult with their international bankers about bank charges for such services.

VIDHI ( IPER PGDM ) Page 26

CAD- CASH AGAINST DOCUMENT LC – LETTER OF CREDIT TT - TELEGRAPHIC TRANSFER

LETTER OF CREDIT

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

PROCEDURE

The following procedures include a flow of events that follow the decision to use a Commercial Letter of Credit.

After a contract is concluded between buyer and seller, buyer's bank supplies a letter of credit to seller.

Seller consigns the goods to a carrier in exchange for a bill of lading.

VIDHI ( IPER PGDM ) Page 27

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Seller pays bill of lading for payment from buyer's bank. Buyer's bank exchanges bill of lading for payment from the buyer.

Buyer provides bill of lading to carrier and takes delivery of goods.

PROCEDURE OF BSL

1. On receipt of advice from respective department (Purchase department) along with relevant information (Bank details etc.) we proceed for opening of Letter of Credit (LC).

2. Checking of “Terms & conditions” of Purchase Order (PO) in line with requisite information required for LC opening. LC cannot be opened unless Bank Guarantee is CONFIRMED or, relevant Bank details etc not provided.

VIDHI ( IPER PGDM ) Page 28

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

3. LC opening advice sends to Bank in separate format in the form of “FD SWIFT-700 APPLICATION & GUARANTEE FOR ISSUE OF DOCUMENTARY CREDIT” along with relevant Po. LC has been opened thereafter.

4. After opening of LC, if respective department asked for amendment in LC, we do the relevant amendment by giving advice in respective format for amendment.

5. On receipt of documents for payment by our Banker, if any, discrepancy is to be sought by bank, we need to reply instantly to Bank about respective discrepancy, if any, exist, otherwise Bank will retire the document within relevant frame of time as thinks fit.

6. Properly endorsed document by Bank has to be retired and handed over to us for further communication to our Sales & Tax Department (S&T), Kolkata office.

7. We have to submit declaration in the form of “Form A1” to bank for foreign remittance against supply of imported Plant & Equipment, materials etc as per PO.

8. Endorsed document has to be sent immediately to our S&T department Kolkata office for further processing like release of material, payment of duty, etc.

9. On payment to Foreign Beneficiary, Banker has been debited our current A/C which has to be booked into our section with respective PO though accounting in SAP.

10. After releasing of material & payment of duty by our S&T department, Kolkata office, and triplicate copy of Bill of Entry (B/E) send to us for further submission to it to our Banker.

VIDHI ( IPER PGDM ) Page 29

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

CAD ( CASH AGAINST DOCUMENTS)

Cash against documents is a type of transaction in which the title for purchased goods is released to the buyer after the total sale price is paid using cash. Often, a commission house or a similar financial institution upon verification of the cash payment handles the actual transfer of title. Usage of the cash against document method is commonly employed with transactions that involve the purchase of exports.

The process for CAD, or cash against documents, in an export environment is fairly straightforward. After accepting an order from an international customer, the exporter prepares the export documents required by both the country of origin and the destination. Among the documents is a form that is normally referred to as an Export Collection Form. This form, along with other manifests and copies of shipping documents, is forwarded to the bank used by the exporter. While it is not always necessary, many exporters choose to prepare a bill of exchange, and include that document with the other forms.

As the next step in a purchasing using the cash against documents method, the exporter’s bank forwards the necessary documents to the bank designated by the purchaser or importer. The documents are provided with a proviso that they are not to be released to the importer until payment for the shipment is made in full. Until the payment is received by the exporter’s bank, the transaction is not considered complete.

Once the importer’s bank receives authorization to honor the exporter’s invoice, cash payment is electronically transferred to the exporter’s financial institution. After receiving confirmation that the payment was executed and posted properly, the importer’s bank releases all documents pertaining to the transaction to the buyer.

Many banks charge fees for executing cash against documents transaction. In some instances, the seller covers all bank charges. However, it is more common for buyers to cover any charges issued by the banks at each end of the transaction. Typically, the seller adds the bank charges from the point of origin onto the invoice, while the importer’s bank normally debits the account used to issue the cash against documents payment.

VIDHI ( IPER PGDM ) Page 30

CASH AGAINST DOCUMENT

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

A telegraphic transfer is a method of transferring money by telegram, cable or telex issued

by a bank in one centre to another in a foreign centre. Transfers of large sum of money are

generally done by TT. If money is to be sent urgently, the bank may be requested for

telegraphic transfers on payment of a nominal charges and telegram charges. In case both

telegraphic transfer and mail transfer, money can also be made payable to a beneficiary on

identification.

Sometimes depositors/clients want to remit funds immediately on an urgent need and at

their request the funds by using of various mode like telegraph/telephone/Telex/Fax etc.

duly attested by secret Test Number. On receipt of which paying branch pay amount to the

payee crediting his account or payment order as the case may be is called telegraphic

transfer (TT). It is a quickest mode for remittance of fund from one place to another.

Procedure of issue TT (at the Issuing Office):

1) Fill up the TT application form.

2) Realized required fund, Commission, VAT & Telephone charge.

3) Required information:

4) Name of the issuing branch

5) Name of the paying branch

6) Amount in figure & words

7) Payee’s name and account number

8) Date, Test Number

9) Voucher to be prepared

10)Dr. Party’s Account/ Cash

11)Cr. General Account by issuing IBCA

12)Commission Account

13)VAT Account

VIDHI ( IPER PGDM ) Page 31

TELEGRAPHIP TRANSFER

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Procedure for payment of TT(at the Paying Office):

1) At first verify the Test Number of message

2) Confirm the Test Number of message.

3) Entry the particular of TT to the “TT Payable Resister”.

4) Dr. General Account (by responding IBCA for TT)

5) Cr. TT Payble A/c

6) Dr. TT Payble A/c

7) Cr. Party A/c

Payment OrderPayment Order is meant for making payment of the banker’s own or of the customer’s dues

locally and not for effecting and remittance to an outstation. In a sense, the payment order is

used for making a remittance to the local creditor. It is not a negotiable instrument and can

not be endorsed.

VIDHI ( IPER PGDM ) Page 32

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

1. Total Import Value from Bokaro Steel Plant

(From 1-Oct-2010 to 31-Mar-2011)

MONTH USD INR EURO INR JPY INR GBP INR

Oct-10 1201945.13 53428289 4457955.22 275650254 - - - -

Nov-10 14822796 154480964 2711216 166763932 - - 64,999 4678191

Dec-10 5,49,688 6,59,40,645 6596479.44 487411382 - - - -

Jan-11 3778613 170699836 3837695.75 169571210 1038000 552865 20,459 14,89,208

Feb-11 2405822.71 109789056 1537607.21 94713421 - - 1550.21 1156.22

Mar-11 12,32,753 5,53,57,341 864726.11 103437149 - - - -

TOTAL 22209176.84 488398145 20005679.73 1297547348 1038000 552865 87,008 4679347.22

MONTH TOTAL(INR)10-Oct 32907854310-Nov 32592308710-Dec 55335202711-Jan 34231311911-Feb 15879449011-Mar 158794490

VIDHI ( IPER PGDM ) Page 33

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

OCT NOV DEC JAN FEB MAR0

100000000

200000000

300000000

400000000

500000000

600000000

TOTAL IMPORT VALUE (INR)

INTERPRETATION:

As in the above figure showing the total import value of Bokaro steel plant it shows a declining trend in this six months period from October 2010 to march 2011.

The declining trend may be due to the less import orders from the company so the payment value is also less of the other can be that the currency when converted in INR in later months gives less value as compared to previous months.

VIDHI ( IPER PGDM ) Page 34

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

1000000

2000000

3000000

4000000

5000000

6000000

7000000

TOTAL IMPORT VALUE (EURO)

INTERPRETATION:

The total import value of euro that is European currency has a declining trend. Whereas its maximum lies in December month. The reason can be that export from country accepting euro is maximum in December.

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

2000000

4000000

6000000

8000000

10000000

12000000

14000000

16000000

TOTAL IMPORT VALUE (USD)

INTERPRETATION:

Total import value of USD is also declining in this graph and has maximum in the month of November. This month has maximum payment in terms of USD

VIDHI ( IPER PGDM ) Page 35

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

200000

400000

600000

800000

1000000

1200000

TOTAL IMPORT VALUE(JPY)

JPYLinear (JPY)

INTERPRETATION:

JPY is only visible in month of January and thus has highest.

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

10000

20000

30000

40000

50000

60000

70000

TOTAL IMPORT VALUE(GBP)

INTERPRETATION:

Total import value of GBP is maximum in month of November and has declining trend in six month from November 2010 to march 2011.

A GRAPH OF FOREIGN CURRENCY TOGETHER OF TOTAL IMPORT VALUE:

VIDHI ( IPER PGDM ) Page 36

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Oct-10

Nov-10

Dec-10

Jan-11

Feb-11

Mar-11

0 5000000 10000000 15000000 20000000

TOTAL IMPORT VALUE ( FC )

GBYJPYMoving average (JPY)EUROMoving average (EURO)USDMoving average (USD)

INTERPRETATION:

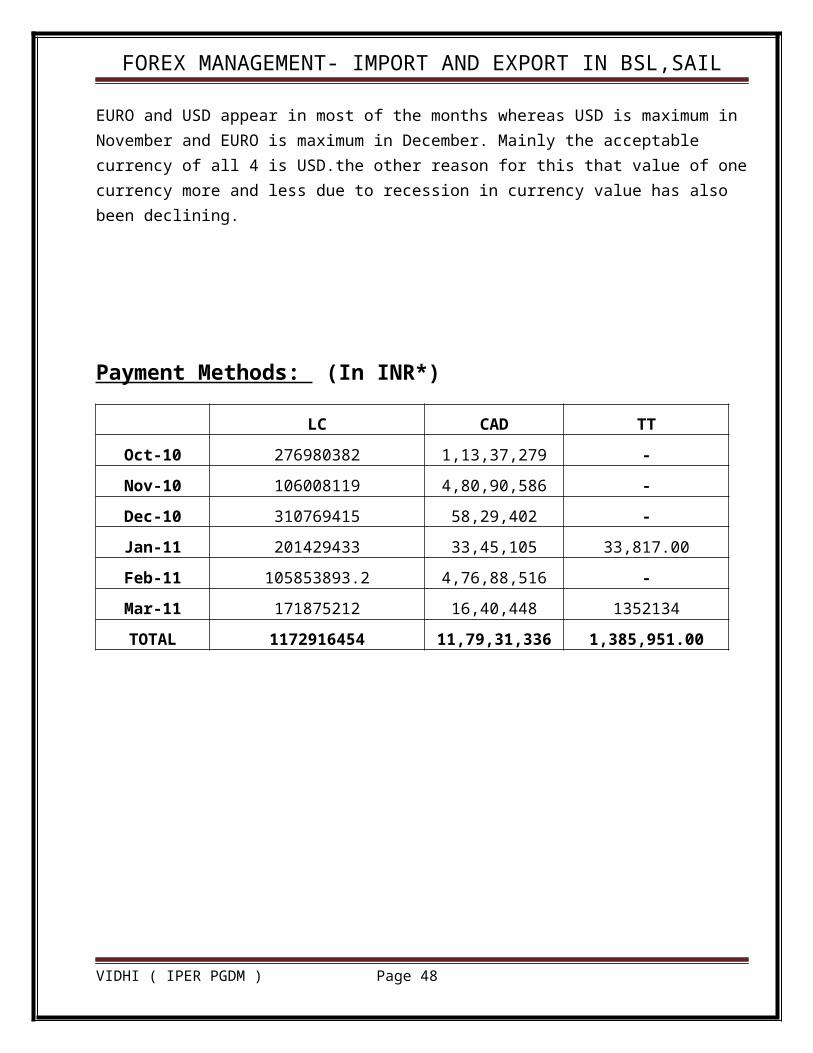

EURO and USD appear in most of the months whereas USD is maximum in November and EURO is maximum in December. Mainly the acceptable currency of all 4 is USD.the other reason for this that value of one currency more and less due to recession in currency value has also been declining.

Payment Methods: (In INR*)

LC CAD TT

Oct-10 276980382 1,13,37,279 -

Nov-10 106008119 4,80,90,586 -

Dec-10 310769415 58,29,402 -

Jan-11 201429433 33,45,105 33,817.00

Feb-11 105853893.2 4,76,88,516 -

Mar-11 171875212 16,40,448 1352134

TOTAL 1172916454 11,79,31,336 1,385,951.00

VIDHI ( IPER PGDM ) Page 37

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

50000000

100000000

150000000

200000000

250000000

300000000

350000000

PAYMENT METHOD (LC)

INTERPRETATION:

In the graph above x axis shows month and y axis shows amount in INR letter of credit as a payment method is mostly accepted by company so in that case the graph is higher and so it first increases and then decreases.

The trend is like of V upside down.

Maximum is in month of December.

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

10000000

20000000

30000000

40000000

50000000

60000000

11337279

48090586

58294023345105

47688516

1640448

PAYMENT METHODS (CAD)

VIDHI ( IPER PGDM ) Page 38

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

INTERPRETATION:

In this graph x axis shows month and y axis shows amount in INR and then it is v shaped as November and December has highest of CAD as payment methods and others are relatively less hence CAD and LC are preferable.

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

200000

400000

600000

800000

1000000

1200000

1400000

33817

1352134

PAYMENT METHODS (TT)

INTERPRETATION:

Telegraphic transfer or Performa invoice is very less in number as many companies do not find it promising and hence the number is less as compared to letter of credit and cash against documentation.

TOTAL IMPORT DATA (In FC**)

MONTH USD EURO JPY GBP TOTAL

Oct-10 1201945 4457955.7 - - 5659900.72

Nov-10 2417736.2 2711176 - 64,999 5193911.2

Dec-10 5,49,688 6596479.4 - - 6596479.44

Jan-11 3778613 3837695.8 1038000 20,459 8674767.75

Feb-11 2405822.7 1537607.2 - 1550.2 3944980.13

Mar-11 4229815.5 1686969.1 - - 5916784.61

TOTAL 14033932 20827883 1038000 87,008

VIDHI ( IPER PGDM ) Page 39

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

1000000

2000000

3000000

4000000

5000000

6000000

7000000

TOTAL IMPORT DATA(EURO)

INTERPRETATION:

This graph is total import data of EURO and x axis shows month and y axis shows amount in EURO itself , that how much import has been done in case of EURO. It has declining trend and from October onwards it has gone to decline.

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

200000

400000

600000

800000

1000000

1200000

TOTAL IMPORT DATA(JPY)

INTERPRETATION:

VIDHI ( IPER PGDM ) Page 40

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

In this graph x axis shows month and y axis shows the amount in JPY and it has only one months transaction so it can be said that in month of January itself material has been bought in JPY currency.

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

10000

20000

30000

40000

50000

60000

70000

TOTAL IMPORT DATA(GBP)

INTERPRETATION:

In this graph x axis shows month and y axis shows amount in GBP.it has only 2 month transaction. In which November is having highest and January is less so it has a declining trend

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

TOTAL IMPORT DATA(USD)

INTERPRETATION:

VIDHI ( IPER PGDM ) Page 41

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

In this above graph the data is in USD and x axis shows month and y axis shows amount in USD . it has rising trend .import in month of October and December is less because materials were more bought in other currency.

TOTAL TRAGET FOR THE MONTH OF OCTOBER 2010 – MARCH 2011 (IMPORTS) INR

FC OCT NOV DEC JAN FEB MAR

USD 4,61,60,050 14,17,89,562 6,59,40,645 6,57,50,736 9,29,86,041 5,53,57,341EURO 1,63,55,698 8,74,35,553 18,51,88,105 8,03,74,738 1,40,16,498 2,33,63,770

JPY - - - - - -

GBP - - - 14,89,208 - - TOTAL 6,25,15,748 23,25,04,968 25,11,28,750 14,76,14,682 10,70,02,539 7,87,21,111

IMPORTS MONTHS WISE-( figure in Rs)

MONTHS INR

OCT'106,25,15,748

NOV'1023,25,04,968

DEC'1025,11,28,750

JAN'1114,76,14,682

FEB'1110,70,02,539

MAR'117,87,21,111

VIDHI ( IPER PGDM ) Page 42

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

OCT'10 NOV'10 DEC'10 JAN'11 FEB'11 MAR'110

500

1000

1500

2000

2500

3000

625.15748

2325.049682511.28749999997

1476.14682

1070.02539

787.21111

TOTAL IMPORT PAYMENT(INR)

INTERPRETATION:

In this graph there is x axis showing month and y axis showing amount in INR, it has a trend of inverse u and it is quite visible with December having highest and October with lowest.

It can be said that the total import payment in INR is presented of different month and from the graph itself it can be said that imports have been less in 3 monthsi.e January, February, and March. And due to this production may have hampered or else it can be said that materials were not needed as production of that particular products were needed whose raw material were not bought.

PAYMENT MONTHY THROUGH LC AND CAD-(figure in lakhs)

MONTH LC CADOct-10 104.17587 113.37279Nov-10 165.72764 480.90586Dec-10 85.46138 58.29402Jan-11 67.30996 33.45105Feb-11 83.52799 476.88516Mar-11 17.52641 16.40448

VIDHI ( IPER PGDM ) Page 43

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

100

200

300

400

500

600

PAYMENT THROUGH LC AND CAD

LCMoving average (LC)Moving average (LC)CADMoving average (CAD)Moving average (CAD)

INTERPRETATION:

In the graph above x axis shows month and y axis shows amount in INR. This graph shows a comparison of both LC (letter of credit) and CAD (cash against documentation) and can be seen that LC is more than CAD. LC is far from x axis but declining and on the other hand CAD is more towards x axis and it is also declining.

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

20

40

60

80

100

120

140

160

180

104.17587

165.72764

85.46138

67.3099683.52799

17.5264099999998

LETTER OF CREDIT

MONTH

RUPEES

INTERPRETATION:

VIDHI ( IPER PGDM ) Page 44

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

In this graph x axis shows month and y axis shows amount in INR and it has a declining trend or can say that it was maximum in November and then started declining.

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

100

200

300

400

500

600

113.372789999999

480.90586

58.2940233.45105

476.885159999997

16.40448

CAD

MONTH

RUPEESIN (CRORES)

INTERPRETATION:

In this graph x axis shows month and y axis shows amount in INR.,in this graph it has increasing and decreasing trend as from October it is rising and then declined in December and again highest in February and march with lowest.

VIDHI ( IPER PGDM ) Page 45

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

EXPORTS

PROCEDURE OF EXPORTS IN BSL

EXPORT PROCEDURE DESCRIPTION

VIDHI ( IPER PGDM ) Page 46

INTERNATIONAL BUYER

SAIL (ITD)

CMO (ITD)

PPC (BSL)

BSL SALES & INVOICE

SHOP

FOREIGN COUNTRY

CMO (BSL)

TRAFFIC DEPT. RLY

INDIAN

BANK

AT BORDER SALES OFFICE

CUSTOM DEPT.

R & C

BSL CENTRALEXCISE DEPT.

1

2

3

4

5

6

13

14

15

11

11. A

9

7

8

10

16

17

18

12

12. A

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

International buyer sends an order enquiry letter to SAIL (ITD).

SAIL- makes enquiry within its units makes a confirmation for the materials.

International buyer puts a purchase order against the CMO (ITD).

CMO (ITD) sends the order specification to PPC-BSL. E.g.-HR Coil-200 tons, CR Coil-220 tons, SLABS-300 tons etc

PPC places an order copy to sales section. Here based on the order specification sales &Invoice makes an invoice.

PPC puts one more order copy to the concerned authority for manufacturing of the finished goods for the export.

After the manufacturing done the material sent to R&C department. Here in R&C department testing of material is done according to the order.

R&C department passes the goods to PPC with test certificate.

PPC get in touch with the traffic department of Indian Railways.BSL makes DA –goods loaded to wagons.Railways provide a RR receipt for freight charges to the border.

PPC provide one copy of DA,RR,TC to Invoice section.Invoice section prepares a commercial Invoice .

BSL Sales &Invoice passes the commercial invoice to Sales &Excise.Sales & Excise prepares an Export Invoice – ARE1, NEPAL INVOICE.

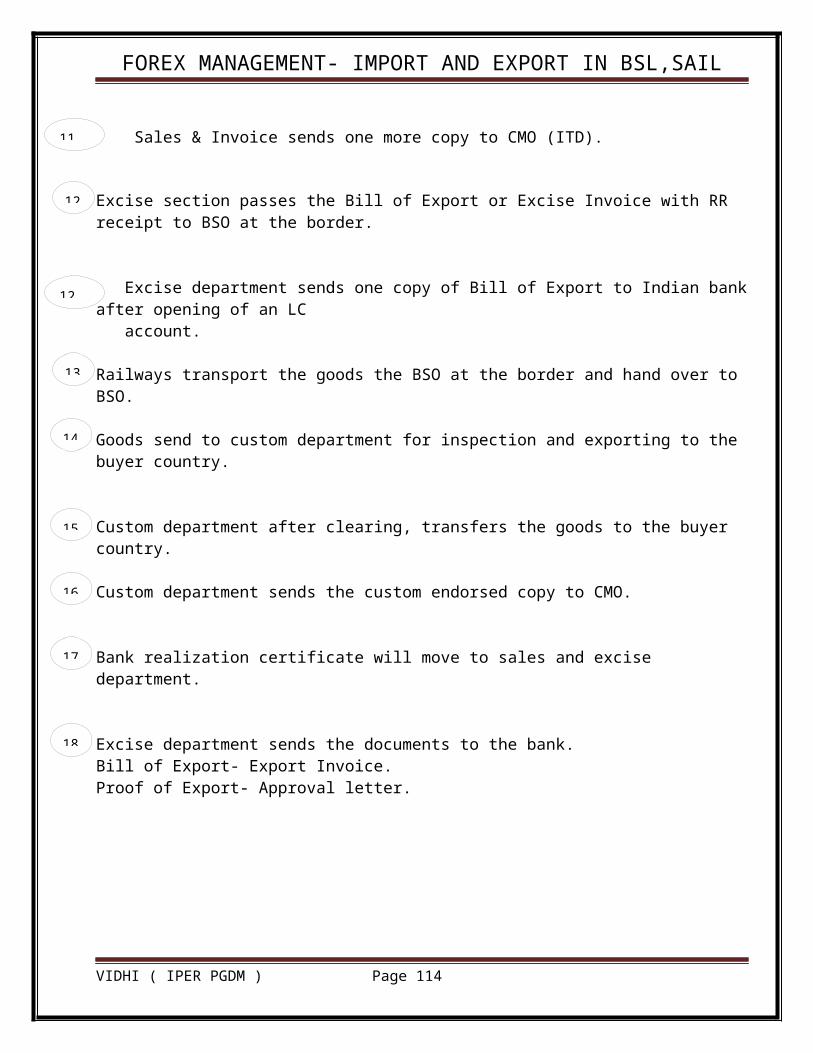

Sales & Invoice sends one more copy to CMO (ITD).

Excise section passes the Bill of Export or Excise Invoice with RR receipt to BSO at the border.

Excise department sends one copy of Bill of Export to Indian bank after opening of an LC account.

Railways transport the goods the BSO at the border and hand over to BSO.

Goods send to custom department for inspection and exporting to the buyer country.

VIDHI ( IPER PGDM ) Page 47

1

2

3

4

5

6

7

8

9

10

11

11. A

12

13

14

12. A

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Custom department after clearing, transfers the goods to the buyer country.

Custom department sends the custom endorsed copy to CMO.

Bank realization certificate will move to sales and excise department.

Excise department sends the documents to the bank.Bill of Export- Export Invoice.Proof of Export- Approval letter.

VIDHI ( IPER PGDM ) Page 48

15

16

17

18

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

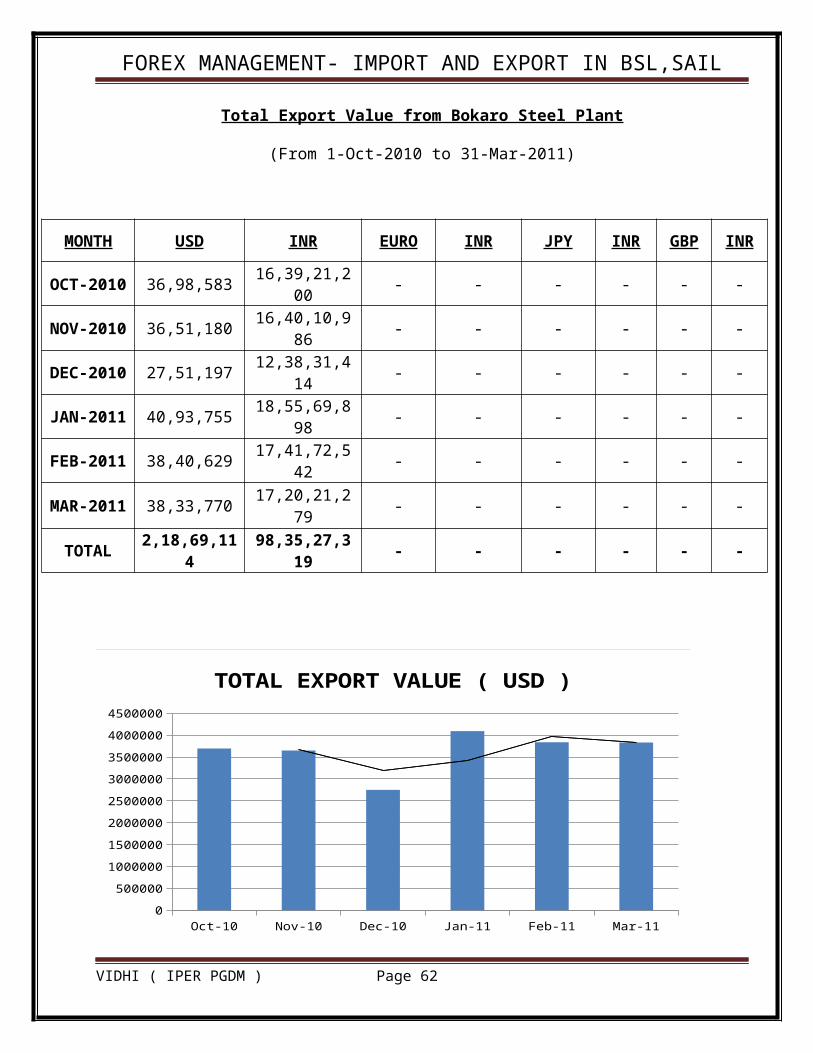

Total Export Value from Bokaro Steel Plant

(From 1-Oct-2010 to 31-Mar-2011)

MONTH USD INR EURO INR JPY INR GBP INR

OCT-2010 36,98,583 16,39,21,200 - - - - - -

NOV-2010 36,51,180 16,40,10,986 - - - - - -

DEC-2010 27,51,197 12,38,31,414 - - - - - -

JAN-2011 40,93,755 18,55,69,898 - - - - - -

FEB-2011 38,40,629 17,41,72,542 - - - - - -

MAR-2011 38,33,770 17,20,21,279 - - - - - -

TOTAL 2,18,69,114 98,35,27,319 - - - - - -

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

TOTAL EXPORT VALUE ( USD )

VIDHI ( IPER PGDM ) Page 49

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

INTERPRETATION:

In the graph above x axis shows month and y axis shows amount in INR and It can be because of 1 reason that most of the countries accept USD and so it has highest. January has the highest and December has the lowest.

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

20000000

40000000

60000000

80000000

100000000

120000000

140000000

160000000

180000000

200000000

TOTAL EXPORT VALUE ( INR )

MONTH

amount(INR)

INTERPRETATION:

The graph shows the total export value in INR and x axis shows month while y axis shows amount in INR.it can be seen that January has highest of all and December shares lowest.

This value is the conversion of all the foreign currency in INR so to make it simpler.

VIDHI ( IPER PGDM ) Page 50

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Receipts Methods: (In INR*)

MONTH LC CAD TT

OCT-2010 10,87,64,236 5,51,56,964 -

NOV-2010 14,04,48,405 2,35,62,581 -

DEC-2010 11,01,71,588 1,36,59,826 -

JAN-2011 15,89,71,772 2,65,98,126 -

FEB-2011 14,14,76,706 3,26,95,836 -

MAR-2011 11,98,56,384 5,21,64,895 -

TOTAL 77,96,88,491 20,38,38,228 -

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

20000000

40000000

60000000

80000000

100000000

120000000

140000000

160000000

180000000

RECEIPT METHOD(LC)

INTERPRETATION:

In this graph above shows receipt method through LC and x axis shows month and y axis shows amount in INR. it is very clear that January month has highest and December and October with lowest , a slightly upward moving trend line.

VIDHI ( IPER PGDM ) Page 51

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

10000000

20000000

30000000

40000000

50000000

60000000

RECEIPT METHOD(CAD)

INTERPRETATION:

In this method of receipt that is CAD x axis shows month and y axis shows amount in INR and October has highest while December share lowest. And looking towards the trend line it is almost constant.

TOTAL EXPORT DATA (In INR*)

MONTH LC PAYMENT CAD PAYMENT TOTAL PAYMENT

OCT 2010 10,87,64,236 5,51,56,964 16,39,21,200

NOV 2010 14,04,48,405 2,35,62,581 16,40,10,986

DEC 2010 11,01,71,588 1,36,59,826 12,38,31,414

JAN 2011 15,89,71,772 2,65,98,126 18,55,69,898

FEB 2011 14,14,76,706 3,26,95,836 17,41,72,542

MAR 2011 11,98,56,384 5,21,64,895 17,20,21,279

TOTAL 77,96,88,491 20,38,38,228 98,35,27,319

VIDHI ( IPER PGDM ) Page 52

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

20000000

40000000

60000000

80000000

100000000

120000000

140000000

160000000

180000000

200000000

TOTAL PAYMENT(INR)

INTERPRETATION:

In the graph above x axis shows month and y axis shows amount in INR. It is the month wise payment of the export in INR value and it is quite clear that January has highest and December has lowest. It is combination of both LC and CAD and can be said that many of countries to whom SAIL is exporting products like to accept payment of LC and CAD and not TT as they are promising.

TOTAL EXPORT DATA (In FC**)

MONTH USD EURO JPY GBP TOTAL

OCT-2010 36,98,583 - - - 36,98,583

NOV-2010 36,51,180 - - - 36,51,180

DEC-2010 27,51,197 - - - 27,51,197

JAN-2011 40,93,755 - - - 40,93,755

FEB-2011 38,40,629 - - - 38,40,629

MAR-2011 38,33,770 - - - 38,33,770

TOTAL 2,18,69,114 - - - 2,18,69,114

VIDHI ( IPER PGDM ) Page 53

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

TATOL EXPORT (USD)

INTERPRETATION:

In the graph above it can be clearly seen that total export data in USD is decreasing till December and rising in January and then again declining. It can be due to change in currency where the material are being sold.

*INR- Indian Rupees

**FC- Foreign Currency

TIME PERIOD- 1 ST OCTOBER 2010 TO 31 ST MARCH 2011

EXPORT VOLUME -24,963 TONS

EXPORT VALUE -Rs 98, 35, 27,319

PRODUCT WISE -HOT ROLLED PRODUCTS

ITEMS QUANTITY( TONS)

Rs per TONS VALUE(Rs)

Coil 19850 38287 76,02,05,180Plate 45 392938 1,76,82,210

-COLD ROLLED PRODUCTS

ITEMS QUANTITY( TONS)

Rs per TONS VALUE(Rs)

Coil 3610 42623 15,38,72,187

VIDHI ( IPER PGDM ) Page 54

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

-GC

ITEMS QUANTITY( TONS)

Rs per TONS VALUE(Rs)

Sheet 1048 49396 5,17,67,742

TIME PERIOD- 1 ST APRIL 2010 TO 31 ST MARCH 2011

EXPORT VOLUME -54,579 TONS

EXPORT VALUE -Rs 2,14,56,98,130

PRODUCT WISE -HOT ROLLED PRODUCTS

ITEMS QUANTITY( TONS)

Rs per TONS VALUE(Rs)

Coil 41941 38198 1,60,20,73,945Plate 2792 39004 10,88,99,700Sheet 47 38852 18,26,055

-COLD ROLLED PRODUCTS

ITEMS QUANTITY( TONS)

Rs per TONS VALUE(Rs)

Coil 6190 4297 26,22,98,896

-GC

ITEMS QUANTITY( TONS)

Rs per TONS VALUE(Rs)

Sheet 3609 47270 17,05,99,534

VIDHI ( IPER PGDM ) Page 55

MATERIAL EXPORTED BETWEEN 1ST APRIL 2010 TO 31ST MARCH 2011

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

HR COIL

HR PLATE

HR SHEET

CR COIL

GC SHEET

0 2000 4000 6000 8000 10000 12000 14000 16000 18000

16020

1088

18

2622

1705

MATERIALS EXPORTED (INR- CR)

AMOUNT IN INR

PRODUCTS

INTERPRETATION:

In this graph x axis shows amount in INR and y axis shows materials which are exported and from that HR COIL is maximum in comparison to CR COIL and other.

COMPARISON ( EXPOTS AND IMPORTS )

VIDHI ( IPER PGDM ) Page 56

MATERIAL EXPORTED INR

HR COIL1,60,20,73,945

HR PLATE 10,88,99,700HR SHEET 18,26,055CR COIL 26,22,98,896GC SHEET 17,05,99,534

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

RECEIPT AND PAYMENT METHOD IN INR ( DATA)

MONTH

LC( RECEIPT)LC

( PAYMENTS)Oct-10 108764236 276980382Nov-10 140448405 106008119Dec-10 110171588 310769415Jan-11 158971772 201429433Feb-11 141476706 105853893.2Mar-11 119856384 171875212

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

50000000

100000000

150000000

200000000

250000000

300000000

350000000

RECEIPT AND PAYMENT METHOD THROUGH LC

LC( RECEIPT)LC ( PAYMENTS)

INTERPRETATION:

In the graph above x axis shows the month and y axis shows INR value and it is clearly visible from above that the LC payments are more in comparison to LC receipt in every month it can be so that the company in abroad rely on LC more

MONTH CAD( RECEIPT) CAD ( PAYMENT)Oct-10 55156964 11337279Nov-10 23562581 48090586Dec-10 13659826 5829402Jan-11 26598126 3345105Feb-11 32695836 47688516Mar-11 52164895 1640448

VIDHI ( IPER PGDM ) Page 57

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-110

10000000

20000000

30000000

40000000

50000000

60000000

RECEIPT AND PAYMENT METHOD THROUGH CAD

CAD( RECEIPT)CAD ( PAYMENT)

INTERPRETATION:In the above graph it is visible that CAD receipt is more that CAD payments so it can be said that in case of CAD , BSL has more of CAD method of receiving and payment more in LC

VIDHI ( IPER PGDM ) Page 58

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

CHAPTER 5

Foreign Exchange Mgt. and Documentation in SAIL

FOREIGN EXCHANGE MGT. -OVERVIEW

In today’s world no economy is self sufficient, so there is need for exchange of goods and

services amongst the different countries. So in this global village, unlike in the primitive age

the exchange of goods and services is no longer carried out on barter basis. Every

sovereign country in the world has a currency that is legal tender in its territory and this

currency does not act as money outside its boundaries. So whenever a country buys or sells

goods and services from or to another country, the residents of two countries have to

exchange currencies. So we can imagine that if all countries have the same currency then

there is no need for foreign exchange.

NEED FOR FOREIGN EXCHANGE

Let us consider a case where Indian company exports HR COILS to USA and invoices the

goods in US dollar. The American importer will pay the amount in US dollar, as the same is

his home currency. However the Indian exporter requires rupees means his home

currency for procuring raw materials and for payment to the labor charges etc. Thus he

would need exchanging US dollar for rupee. If the Indian exporters invoice their goods in

rupees, then importer in USA will get his dollar converted in rupee and pay the exporter.

From the above example we can infer that in case goods are bought or sold outside the

country, exchange of currency is necessary.

Sometimes it also happens that the transactions between two countries will be settled in the

currency of third country. In that case both the countries that are transacting will require

converting their respective currencies in the currency of third country. For that also the

foreign exchange is required.

VIDHI ( IPER PGDM ) Page 59

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

About foreign exchange market.

Particularly for foreign exchange market there is no market place called the foreign

exchange market. It is mechanism through which one country’s currency can be exchange

i.e. bought or sold for the currency of another country. The foreign exchange market does

not have any geographic location.

Foreign exchange market is describe as an OTC (over the counter) market as there is no

physical place where the participant meet to execute the deals, as we see in the case of

stock exchange. The largest foreign exchange market is in London, followed by the new

york, Tokyo, Zurich and Frankfurt. The market are situated throughout the different time

zone of the globe in such a way that one market is closing the other is beginning its

operation. Therefore it is stated that foreign exchange market is functioning throughout 24

hours a day.

In most market US dollar is the vehicle currency, viz., the currency sued to dominate

international transaction. In India, foreign exchange has been given a statutory definition.

Section 2 (b) of foreign exchange regulation ACT,1973 states:

Foreign exchange means foreign currency and includes

All deposits, credits and balance payable in any foreign currency and any draft, traveler’s

cheques, letter of credit and bills of exchange expressed or drawn in India currency but

payable in any foreign currency.

Any instrument payable, at the option of drawer or holder thereof or any other party thereto,

either in Indian currency or in foreign currency or partly in one and partly in the other.

In order to provide facilities to members of the public and foreigners visiting India, for

exchange of foreign currency into Indian currency and vice-versa. RBI has granted to

various firms and individuals, license to undertake money-changing business at seas/airport

and

VIDHI ( IPER PGDM ) Page 60

FOREX MANAGEMENT- IMPORT AND EXPORT IN BSL,SAIL

tourism place of tourist interest in India. Besides certain authorized dealers in foreign

exchange (banks) have also been permitted to open exchange bureaus.

Following are the major bifurcations

Full fledge moneychangers – they are the firms and individuals who have been authorized to take both, purchase and sale transaction with the public.

Restricted moneychanger – they are shops, emporia and hotels etc. that have been authorized only to purchase foreign currency towards cost of goods supplied or services rendered by them or for conversion into rupees.

Authorized dealers – they are one who can undertake all types of foreign exchange transaction. Bank is only the authorized dealers. The only exceptions are Thomas cook, western union, UAE exchange which though, and not a bank is an AD.

Even among the banks RBI has categorized them as followes:

Branch A – They are the branches that have nostro and vostro account.

Branch B – The branch that can deal in all other transaction but do not maintain nostro and vostro a/c’s fall under this category.

For Indian we can conclude that foreign exchange refers to foreign

money, which includes notes, cheques, bills of exchange, bank balance

and deposits in foreign currencies.

PARTICIPANTS IN FOREIGN EXCHANGE MARKET

The main players in foreign exchange market are as follows:

1. CUSTOMERS

The customers who are engaged in foreign trade participate in foreign exchange market by