EXECUTIVE SUMMARY Title of the study: “The study of Venture Capital Financing – The right process of reaching a Venture Capitalist and factors effecting the capital decisions” As a part of Curriculum, I have done an internship project for the period of two months at Funding Solutionz, and by working in the organization I have been able to study venture capital financing and prepare this project report on the factors involved while taking capital decisions on a potential project by a venture capitalist. (present financial condition, potential of the venture, Cost of financing, ownership, organization structure and management, existing customer base, size and tenure). It involves the reliability and innovation in the business idea, companies earning stability (CMR ratios), quality of management, the corporate governance and structure, investment structure and exit plans. Most of the entrepreneurs fail to forecast these factors in a required manner that is demanded by the venture capitalist for their analysis, thereby losing their chances of getting approved by a VC and missing the opportunity of funding their potential venture idea. This study will cover : Page | 1

Transcript

EXECUTIVE SUMMARY

Title of the study:

“The study of Venture Capital Financing – The right process of reaching a Venture Capitalist and

factors effecting the capital decisions”

As a part of Curriculum, I have done an internship project for the period of two months at Funding

Solutionz, and by working in the organization I have been able to study venture capital financing and

prepare this project report on the factors involved while taking capital decisions on a potential project by a

venture capitalist. (present financial condition, potential of the venture, Cost of financing, ownership,

organization structure and management, existing customer base, size and tenure). It involves the reliability

and innovation in the business idea, companies earning stability (CMR ratios), quality of management, the

corporate governance and structure, investment structure and exit plans.

Most of the entrepreneurs fail to forecast these factors in a required manner that is demanded by the

venture capitalist for their analysis, thereby losing their chances of getting approved by a VC and missing

the opportunity of funding their potential venture idea.

This study will cover :

1. Preparation of documentations as per required by the VC i.e

a. Investment Teaser

b. Business plan(Business idea, Market, Competitor Study, Financial and Marketing Plan,

Exit Plan etc)

c. Information memorandum (a presentation having summary on all dimensions) d. Financial

Plan

2. The detail study will further be supported by crucial factors that play major role for the business

plan to get sanctioned by the venture capitalist.

Page | 1

3. And the process of venture capital financing:

a. Deal origination

b. Screening

c. Evaluation

d. Deal structuring

e. Post investment activity

f. Exit plan

Page | 2

CHAPTER 1: INTRODUCTION

1.1 VENTURE CAPITAL FINANCING

Business requires capital, and getting it at the right time is very important. There are several alternatives to

fund the business. A brief heading to name a few would be :

• Owner or proprietor’s capital

• Equity partner • Debt Finance

These can be further be branched to many options giving entrepreneur several options to choose among. In

this study the focus would be more on venture capital which comes under equity partner as well as under

debt financing.

Venture capital is a risk financing in the form of equity or quasi-euity. It gives the business funds based on

their potential and their interest as perceived by the investor. Funds might be required for seed stage

funding, expansion/development funding or for acquisition financing. Venture capital is established

among developed countries and is developing in third world countries because of its impact on

encouraging entrepreneurial activities within a nation. Venture Capital firms invest funds on any business

with a professional outlook, they focus on their primary segment which vary among different

The number of venture capital firms are raising in India due to the well-developed avenues for buying and

selling of shares within SME’s, huge tax benefits for the venture capitalist and support from government

policies. Venture capital plays a strategic role to build potential business/enterprises to reach a level where

they can reap their capital gains and can cash out these gains by leading directing their financed venture to

any of the following exit routes:

• Initial public offerings (IPO)

• Acquisition by other company

• Purchase of venture capitalist’s share by other investors or promoters

This is done when the Venture capitalist realizes the required return of return on his primary capital

invested on the business to take the exit route. Venture capital financing helps both the entrepreneurs as

well as the venture capitalist to realize their goals.

With venture capital financing, the venture capitalist acquires an agreed proportion of the equity of the

company in return for the funding that he offers.

This could be summarized as follows :

1 “Loughborough University Institutional Repository: Venture Capital Financing in India: a Study of Venture Capitalist’s Valuation, Structuring, and Monitoring Practices,” accessed March 30, 2013, https://dspace.lboro.ac.uk/dspacejspui/handle/2134/6819.

Page | 4

• Equity participation

• Long term investment

• Participation in management

The rate of return on this capital lies within the success of the business venture. Venture capital Equity

finance thereby offers the advantage of having no interest charges. It is "patient" capital that seeks a return

through long-term capital gain rather than immediate and regular interest payments, as in the case of debt

financing. Given the nature of equity financing, venture capital investors are therefore exposed to the risk

of the company failing. As a result the venture capitalist must look to invest in companies which have the

ability to grow very successfully and provide higher than average returns to compensate for the risk.

2

Venture capitalist’s management approach differ to that of a lender or a bank. The bank does not

participate with the management and keeps its ties away from the venture’s management, operations and

other decision making. When venture capitalists invest in a business they typically direct and guide the

venture so as to lead it towards capital gains. They are a crucial part of the company's decision making

and occupy a place in board of directors. These professional venture capitalists act as mentors and aim to

provide support and advice on a range of management, sales and technical issues to assist the company to

develop its full potential.3

1.2 BACKGROUND OF THE STUDY:

2 “About Venture Capital (VC),” accessed March 30, 2013, http://indiavca.org/about-venture-capital-vc.html.

Page | 5

Today due to the economic crisis and the change in job market. Entrepreneurship has gained market. A

number of technocrats in India today plan to setup their own shops and capitalize this opportunities. In

today’s highly dynamic economic climate with regular technological inventions, few traditional business

models may survive but margin lies more towards more innovative business ideas. Today it is not the

conglomerates that fuel economic growth but are the new SMEs and other innovative businesses.

The bright reason for global economic growth today lies in the hand of the small and medium enterprises.

For example, in India SMEs alone contribute to almost 40% of the gross industrial value added in the

Indian economy.

Whereas in the United States 55% of their global exports are supported by very SMEs with not more than

50 employees and 10% exports are generated by companies with 800 or more employees.

There is a paradigm shift from the earlier physical production and economies of scale model to new

ventures with technological advancements providing services and under process industry.

However, staring an enterprise has its own risk and is never easy. There are number of parameters that

contribute to its success or downfall. That is why entrepreneurs find it difficult to find the right venture

capitalist and miss the right way to approach them. However, there are methods and a right protocol for

any entrepreneur to reach out his investor in a right way and thereby get the funding and that is our topic

of study here.

1.3 NEED FOR THE STUDY

• The study has been conducted for gaining the practical knowledge about Venture capital finance

and various operations to reach them in a right manner.

3 “Venture Capitalist,” accessed March 30, 2013, http://techaloo.com/venture-capitalist/.

Page | 6

• The study has been undertaken as a part of PGDM_MBA curriculum from 1st jan.to Feb 28th 2013

for the fulfilment of the requirement of PGDM_ MBA degree.

The study covers the domain of conditions checked by the VC firms before heading towards funding the

venture, This is the link where the entrepreneur miss their chance due to not having the know-how of how

to approach a potential VC for his funding needs.

The Venture capitalist on the other hand will have a specific format in their requirement sheet which the

entrepreneur has to add maximum value, to gain his attention and thereby to get evaluated for his venture

funding

1.4 OBJECTIVE OF THE STUDY

• To understand the right method to reach to a venture capital firm with the required financial

presentation and business plan.

• To understand about the working of Venture Capital Financing and data required by them.

• To study the sources and allocation of Venture Capital Financing.

Page | 7

1.5 SCOPE OF THE STUDY

The scope of the study was to realize the funding lifecycle in a practical format, by preparing business

case for entrepreneurs and help them seek a VC. To realize the theoretical aspect of the study into real life

work experience by analyzing the financials of the venture and guiding business finance to them. The

study of financials and possible funding that could be approved is based on the tools such as Size wise

analysis and Ratios. The study is based on the last 5 years Annual Reports of venture capital firms and

fund seeking ventures.

1.6 LIMITATIONS OF THE STUDY

• All the data presented for the venture capital financing are limited to few firms and for the last 5

years. The information provided to the researcher may be over simplifications of facts over

generalization from insufficient data.

• Financial analysis of fund seeking ventures does not measure the qualitative aspects of the

business. It does not show the skills, technical know-how and the efficiency of its employees and

managers

• It does not reveal the fairness of selection criteria by a venture capital firm.

Page | 8

1.7 DATA COLLECTION

• Primary sources include surveys done across 100 respondents across different sectors from SMEs

and VC firms and further discussion with the managers at Funding Solutionz.

• Secondary Sources were case studies, journals, financial records, books.

• Sampling Size:-Last 5 years Financial Statements

1.9 TOOLS USED

SPSS (17) and Microsoft Office Excel 2007 Cross tabulation and chi-square statistics

Page | 9

CHAPTER 2 : INDUSTRY PROFILE

2.1 VC INDUSTRY PROFILE IN INDIA

India currently has more than about 400 Venture capital firms. 4

The Venture Capital industry has shown a exponential upward curve from investments of

about USD 0.5 billion (56 deals) in 2003 to USD 14 billion (439 deals) in 2007. In the year 2008, there

was a decline to about USD 11 billion (382 deals).

Unlike before as observed in the early stages of the industry’s growth the investments were inclined

largely towards the IT sector, but within 8 years of success stories now in 2009 Venture cvapital firms are

now interested in nearly all sectors.

4 “Microsoft Word - The VC Handbook -- _Chapter 0-26_ - PVI.A02_Venture.Capital.Industry.in.India.pdf,” accessed March 16, 2013, http://smoothridetoventurecapital.com/PVI.A02_Venture.Capital.Industry.in.India.pdf.

Page | 10

With developing Indian entrepreneurship standards, government support , policies and globalisation

policies there are vast opportunities for private equity investors to capitalize on.

Preferred regions for VC investments are Mumbai, Delhi and NCR, followed by Bangalore. Although

companies in South India attracted a higher number of investments, in value terms Western India

did much better. Among cities, Mumbai-based companies retained the top slot with 108 private equity

investments totalling almost US $6 billion in 2007, followed by Delhi/NCR with 63 investments (US

$2.7 billion) and Bangalore with 49 investments aggregating US $700 million.

2.2 INTRODUCTION TO THE VENTURE CAPITAL INDUSTRY

Initiative in India:

Indian tradition of venture capital for industry starts with a history of more than 150 years. Back then

many of the managing agency houses acted as venture capitalists providing both finance and management

skill to risky projects. It was the managing agency system through which Tata iron and Steel and Empress

Mills were able to raise equity from the investing public. The Tata’s also initiated a managing agency

system, named Investment Corporation of India in 1937, which by acting as venture capitalists,

successfully provided hi-tech enterprises such as CEAT tyres, associated bearings, national rayon etc. The

early form of venture capital enabled the entrepreneurs to raise large amount of funds and yet retain

management control. After the abolition of managing agency system, public sector term lending

institutions met a part of venture capital requirements through seed capital and risk capital for hi-tech

industries which were not able to meet promoter’s contribution. However all these institutions supported

only proven and sound technology while technology development remained largely confident to

government labs and academic institutions.

Many hi-tech industries, thus found it impossible to obtain financial assistance from banks and other

financial institutions due to unproven technology, conservative attitude, risk awareness and rigid security

parameters. Venture capitals growth in India passed through various stages. In 1973, R.S. Bhatt committee

recommended formation of Rs. 100 crore venture capital funds. The seventh five year plan emphasized

the need for developing a system of funding venture capital. The Research and Development Cess Act

Page | 11

was enacted in May 1986, which introduced a cess of 5 percent on all payments made for purchases of

technology from abroad. The levy provides the source for the venture capital fund. Formalized venture

capital took roots when comptroller of capital issues venture capital guidelines in Nov 1988.5

2.3 GROWTH OF VENTURE CAPITAL INDUSTRY

Up to 1996: The Early Years:

• Funds that were mobilized for venture investment were small in value.

• The venture capitalists in those times were mostly from a banking background.

• Banks approached the subject of venture funding much likely they approached debt financing of a

project.

• The accent was on the asset-side of the balance sheet. And the focus on innovation and business

building was low.

• Value creation as a focus had not yet been fully discovered, and exit strategies were being thought

more around the life-term of the fund.

• Valuations were low.

• No competition between VCs.

• Indian entrepreneurs had not yet discovered the venture capital route to funding and growth and it

reflected in the small amounts that were invested.

• There was little or no active participation of venture capitalists in entrepreneurial activities such as

financial structuring, business strategy.

• Business enhancement through networks.

1997 to 2000: The Rock ‘n’ Roll Years:

• The SEBI guidelines of 1996 acted as huge incentive for institutional acked MNC venture capital

companies to focus their attention on India.

5 “VENTURE CAPITAL - ManagementParadise.com Forums - Your MBA Online Degree Program and Management Students Forum for MBA,BMS, MMS, BMM, BBA, Students & Aspirants.,” accessed March 30, 2013, http://www.managementparadise.com/forums/miscellaneous-project-reports/11182-venture-capital.html.

Page | 12

• The range of venture capitalists now spanned incubators, ingents, classic venture capitalists and

even private equity players. And the lines between them had begun to blur.

• Venture capitalists were instrumental in introducing risk taking too many, members of the

professional class.

• Innovation was the key, and idea flows equaled doer flows at a frantic pace never before seen. 2001 Onwards: The Reality Years:

• The number of people who had got in to venture capital game was truly impressive.

• In addition to the seasoned players, there were finance and noon finance professionals of different

hues entering the industry and people with little or no experience running the companies.

• Venture capital community is finally recognizing that the evolution and business is an on-going

process. This added to the return of the business maturation cycle of five to seven years, portends a

less frenetic and more sustained pace of venture activity.

2.4 PROBLEMS IN THE VCs IN THE INDIAN CONTEXT:

One can ask why venture funding is so successful in USA but faced a number of problems in India. The

biggest problem was a mind set change from ‘collateral funding’ to high risk high return funding. Most of

the pioneers in the industry were people with credit background and exposure to manufacturing industries.

Exposure to fast growing intellectual property business and services sector was almost zero.

All combined to a slow start to the industry. The other issue that led to such a situation includes:

2.5 LICENSE RAJ AND THE IPO BOOM:

Till early 1990s, under the license raj regime, only commodity centric businesses thrived in a deficit

situation.

To fund a cement plant, venture capital is not needed. What was needed was ability to get a license, and

then get the project funded by the banks and DFIs. In most cases, the promoters were well established

Page | 13

industrial houses, with no apparent need for funds. Most of these entities were capable of raising funds

from conventional sources, including term loans from institutional and equity markets.

2.6 SCALABILITY:

The Indian software segment has recorded an impressive growth over the last few years and earns large

revenues from its export earnings, yet our share in the global market is less than 1 per cent. Within the

software industry the value chain ranges from body shopping at the bottom to strategic consulting at the

top. Higher value addition and profitability as well as significant market presence take place at the higher

end of the value chain. If the industry has to grow further and survive the flux it would only be through

innovation. For any venture idea to succeed there should be a product that has a growing market with a

scalable business model. The IT industry (which is most suited for venture funding because of its ideas

nature) in India till recently had a service centric business model. Products developed for Indian markets

lack scale.

2.7 MINDSETS :

Venture capital as an activity was virtually non existence in India. Most venture capital companies went to

provide capital on a secured debt basis, to established businesses with profitable operating histories. Most

of the venture capital units were off-shoots of financial institutions and banks and the lending mindset

continued. True venture capital is capital that is used to help launch products and ideas of tomorrow.

Abroad, this problem is solved by the presence of angel investors. They are typically wealthy individuals

who not only provide venture finance but also help entrepreneurs to shape their business and make their

venture successful.6

6 “Legal - Venture Capital-overview.pdf,” accessed March 30, 2013,

There is a multiplicity of regulators like SEBI and RBI. Domestic venture funds are set up under the

Indian Trusts Act of 1882 as per SEBI guidelines, while offshore funds routed through Mauritius follow

RBI guidelines. Abroad, such funds are made under the Limited Partnership Act, which brings advantages

in the terms of taxation. The government must allow pension funds and insurance companies to invest in

venture capitals as in USA where corporate contributors to venture funds are large.

2.9 EXIT:

The exit routes available to the venture capitalists were restricted to the IPO route. Before deregulation,

pricing was dependent on the erstwhile CCI regulations. In general all issues were under period. Even

now SEBI guidelines make it difficult for pricing issues for an easy exit. Given the failure if the OTCEI

and the revised guidelines, small companies could not hope for a BSE / NSE listing. Given the dull market

for mergers and acquisitions, strategic sale was also not available.

2.10 VALUATION:

The recent phenomenon is valuation mismatches. Thanks to the software boom, most promoters have sky

high valuation expectations. Given this, it is difficult for deals to reach financial closure as promoters do

not agree to a valuation. This coupled with the fancy for software stocks in the bourses means that most

companies are proponing their IPOs. Consequently, the number and quality of deals available to the

venture funds gets reduced.7

7 “VENTURE CAPITAL - ManagementParadise.com Forums - Your MBA Online Degree Program and Management Students Forum for MBA,BMS, MMS, BMM, BBA, Students & Aspirants.”

Page | 15

2.11 CONTRIBUTORS TO THE VENTURE FUND:

• Foreign Institutional Investors.

• All India Financial Institutions.

• Multilateral Dev Agencies.

• Other Banks.

• Other Public.

• Private Sector.

• Public Sector.

• Nationalized Banks.

• State Financial Institutions.

• Insurance Companies.

• Mutual Funds.

Page | 16

CHAPTER 3 : COMPANY PROFILE

Funding Solutionz is a boutique investment advisory firms offering services in preparing business plans to

raising capital resources for companies in Bangalore, Founded on February 17, 2012 with branches across

Bangalore and headoffice located in Jayanagar Bangalore. The company has a well-qualified and

experienced management team with ex bankers and other finance professionals to help entreprenuers with

raising capital through

a. Private Equity

b. Venture capital

c. Angel Investments

d. Crowd Funding

e. Structured Finance through Debt and Equity capital

The company has a wide client base, and a huge network among all venture capital firms and young

business firms

They also support clients with business consulting and business finance

Page | 17

OVERVIEW3.1

3.2 OBJECTIVES OF THE STUDY:

We shall discuss here these following requirements by a VC firm that helps them judge the right venture

they wish to invest in.

• Investment Teaser : Executive summary

It holds the summary of the business plan and is a smart persuasive, yet realistic. Its a two

page of your business plan holding the venture idea and covering all its key elements.

• Investor Memorandum : covering aspects as shown below

Background of venture

The parent company profile for the VC to be sure of the brand strength

Product services offered

This part should cover all details of the product or service offered from its competitive

edge, USP to the development stages for even a non-specialist to understand. This should

also hold details of patents, or any other legal protection pending or required.

Market analysis

The plan should describe about the market traction towards your venture’s services and

products, It should be strong enough to convince the VC firm to seek a real commercial

opportunity in your business.

• Size of the market

• Competitor

• How developed is the market

• Strategic Positioning • Strength and weaknesses if any

• Projections for company and the market

Page | 18

Marketing and Business operations

• The marketing aspect i.e o Sales and distribution strategy o Strategies for

different sales force o Pricing strategy o Promotions

• The operations aspects o Suppliers o Labour requirements

o Logistics and other daily working resources

Management team

• Quality and depth in the management team

• Strong records of being involved with successful businesses

Exit plan

The routes available for the VC to exit the investment and make a return.

• Floating on a stock exchange

• Selling the share to other trade buyer

Funds required

A clear statement of how much funds are required with its source. The purpose for the funding

required with its clear break up for the VC to understand and analyse

• Financial projections

Ratios that describe all important business financial status for last 5 to 6 years, the capital allocation,

cash flow statements, profit n Loss statements, Balance sheets, cost analysis and yearly graphical

presentations for the expenses and earnings forecasted in for the coming years with this new venture.

Page | 19

This holds the most important part and will be examined again with few examples later in our study .The

Financial should produce a pro forma profit n loss statement and balance sheet and ensure that these are

realistic and could be updated or adjusted if need arises. It should also hold the company’s present

financial outlook that shows their margin and earning stability. It should forecast the prospective future

margins keeping the competition in mind.

• Company growth prospect

• Debt to Shareholder fund ratio

• Budgets allocated to each units

And to prove the consistency of the company of meeting the financial projections

relevant historical financials should be presented.

The second objective is to find the factors that are most crucial and are taken into consideration by a

venture capitalist for providing capital to a new company. We focus on a few sets of predefined factors.

The process to find these factors is necessary to understand as to how to implement these into the

documentation in proper manner so that the venture capitalist seeks the right interest for the proposed

venture.

Page | 20

We here will measure the factors

• Business Idea

• Financials

• Management

• IRR Conditions

• Pay Back period

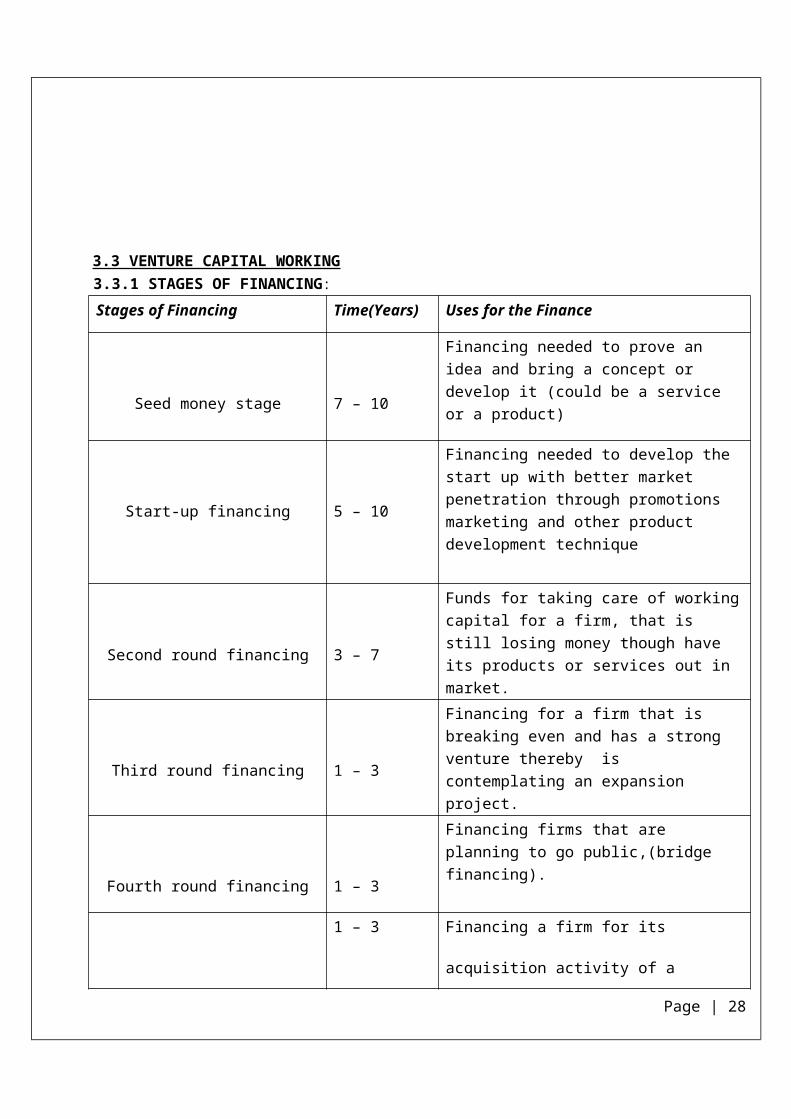

3.3 VENTURE CAPITAL WORKING 3.3.1 STAGES OF FINANCING:

Stages of Financing Time(Years) Uses for the Finance

Seed money stage

7 – 10

Financing needed to prove an idea and bring a concept or develop it (could be a service or a product)

Page | 21

Start-up financing

5 – 10

Financing needed to develop the start up with better market penetration through promotions marketing and other product development technique

Second round financing

3 – 7

Funds for taking care of working capital for a firm, that is still losing money though have its products or services out in market.

Third round financing

1 – 3

Financing for a firm that is breaking even and has a strong venture thereby is contemplating an expansion project.

Fourth round financing

1 – 3

Financing firms that are planning to go public,(bridge financing).

Buy-out

1 – 3 Financing a firm for its acquisition activity of a

product line or service business.

Turnaround 3 – 5 Re-establishing a business

• 3.3.2 STAGES IN VENTURE FINANCING :

Early Stage Financing:

• Seed financing for supporting a concept or idea.

• Research and Development financing for product development.

• Start-up capital for initiating operations and develop a prototypes.

• First stage financing for production and marketing.

Page | 22

Expansion Financing:

• Second stage financing for working capital and initial expansion.

• Development financing for major expansion.

• Bridge or mezzanine financing for facilitating public issue.

Acquisition/Buy-out Financing:

• Acquisition financing for acquiring another firm for further growth

• Management Buy-out financing for enabling operating group to acquire the firm or part of its

business.

• Turnaround financing.

3.4 ADVANTAGES OF VENTURE CAPITAL

• It injects long term equity finance which provides a solid capital base for future growth.

• The venture capitalist is a business partner, sharing both the risks and rewards. Venture

capitalists are rewarded by business success and the capital gain.

• The venture capitalist is able to provide practical advice and assistance to the company

based on past experience with other companies which were in similar situations.

• The venture capitalist also has a network of contacts in many areas that can add value to

the company, such as in recruiting key personnel, providing contacts in international

Page | 23

markets, introductions to strategic partners, and if needed co-investments with other

venture capital firms when additional rounds of financing are required.

• The venture capitalist may be capable of providing additional rounds of funding should it

be required to finance growth.

3.5 DISADVANTAGES OF GOING TO VENTURE CAPITAL FINANCE

• The agreement of funding is passed on a contract which could be partial ownership or other

profit sharing which if not properly negotiated by the entrepreneur he might lose ownership of

his whole business or idea and future to them.

• Intrusion and control : the VC gets the right to drive the firm thereby can take strategic

decision or can drive them to his advantage if the deal is not guided properly.

3.6 VENTURE CAPITALISTS GENERALLY:

Finance new and rapidly growing companies.

Purchase equity securities.

Assist in the development of new products or services.

Add value to the company through active participation.

Take higher risks with the expectation of higher rewards.

Have a long term orientation.

When considering an investment, venture capitalists carefully screen the technical and business merits of

the proposed company. Venture capitalists only invest in a small percentage of the businesses they review

and have a long term perspective. They also actively work with company’s management, especially with

contacts and strategy formulation8.

8 “MomentumVC | About Venture Capital,” accessed March 30, 2013, http://www.momentumvc.com.au/docs/3100_f.htm.

Page | 24

Venture capitalists mitigate the risk of investing by developing a portfolio of young companies in a single

venture fund. Many times they co-invest with other professional venture capital firms. In addition, many

venture partnerships manage multiple funds simultaneously. For decades, venture capitalists have nurtured

the growth of America’s high technology and entrepreneurial communities resulting in significant job

creation, economic growth and international competitiveness. Companies such as Digital

Equipment Corporation, Apple, Federal Express, Compaq, Sun Microsystems, Intel, Microsoft and

Genetic are famous examples of companies that received venture capital early in their development.

In India these funds are governed by the Securities and Exchange Board of India (SEBI) guidelines.

According to this venture capital fund means a fund established in the form of a company or trust, which

raises money through loans, donations, issue of securities or units as the case may be, and makes or

proposes to make investments in accordance with these regulations.

(Source: SEBI (Venture Capital Funds), Regulations, 1996).

3.7 FACTORS DETERMINING THE VENTURE CAPITAL REQUIREMENTS

• Nature of business: The requirements of working is very limited in public utility

undertakings such as electricity, water supply and railways because they offer cash sale

only and supply services not products, and no funds are tied up in inventories and

receivables. On the other hand the trading and financial firms requires less investment

in fixed assets but have to invest large amt. of working capital along with fixed

investments.

• Size of the business: Greater the size of the business, greater is the requirement of

working capital.

• Length of production cycle: The longer the manufacturing time the raw material and

other supplies have to be carried for a longer in the process with progressive increment

of labor and service costs before the final product is obtained. So working capital is

directly proportional to the length of the manufacturing process.

• Seasonal variations: Generally, during the busy season, a firm requires larger working

capital than in slack season.

Page | 25

• Working capital cycle: The speed with which the working cycle completes one cycle

determines the requirements of working capital. Longer the cycle larger is the

requirement of working capital.

• Business cycle: In period of boom, when the business is prosperous, there is need for

larger amt. of working capital due to rise in sales, rise in prices, optimistic expansion of

business, etc. On the contrary in time of depression, the business contracts, sales

decline, difficulties are faced in collection from debtor and the firm may have a large

amt. of working capital.

CHAPTER 4 : PROJECT DESING AND METHODOLOGY

4.1.1 TITLE OF THE PROJECT: - A study on factors effecting capital decisions by Venture Capitalist

4.1.2 OBJECTIVE OF THE STUDY:-

• To understand about the process of Venture Capital Financing.

• To understand relevance of different factors effecting capital decisions

• To study the expected IRR by a VC

• To study the right method to reach to a potential VC with his preferred choice of documents.

4.1.3 SCOPE OF THE STUDY:-

The scope of the study was to put the theoretical aspect of the business plan study into real life work

experience by working with a investment banker. The data on preference of factors by venture capitalist

are analysed through a survey method consisting of Small and Medium Enterprises.

Page | 26

4.2 RESEARCH METHODOLOGY:-

Field study was carried out across different VC and capital seeking entrepreneurs, It was analysed

through SPSS (17) and Microsoft Office Excel 2007 Cross tabulation and chi-square statistics were

utilized to verify the interrelationships between the different respondents and the responses they provided.

To find the correlation among the factors Regression Analysis was also done. Pearson correlation

coefficient was found to be positive at a significance level over 0.5 which indicates a strong correlation.

4.2.1 DATA COLLECTION:-

Primary sources includes survey with the a sample of 100 respondents is collected from Bangalore

region. The population is without any sectorial differentiation.

Secondary Sources were articles, journals, past records from Funding Solutionz, books and internet

sources.

4.2.2 RESEARCH DESIGN: - The research or study conducted at Funding Solutionz is a descriptive

research in nature. This design is an attempt to know the preferred factors considered by the venture

capitalist before financing a firm..

4.2.3 LIMITATION OF THE STUDY:-

All the data presented for the study is for a small sample size only in Bangalore. The information

provided to the researcher may be over simplifications of facts over generalization from

insufficient data.

The study does not measure the qualitative aspects of the factors towards the decision making of a

Venture Capitalist. It does not show the skills, technical know-how of a VCs final decision call

Page | 27

4.2.4 SAMPLING DESIGN

Sampling Unit:-Respondents include VCs and fund seeking entrepreneurs Sampling

Size:-100

4.2.5 TOOLS USED

MS-EXCEL and SPSS (17)

4.3 : HOW TO REACH INVESTORS AND PREPARE DOCUMENTS AS PER

THEIR REQUIREMENT

The major issue though after knowing the important factors of decision making by a VCs remains the

same, how to reach them in a right manner with the documents they wish to study.

The current scenario of Venture Capital Firms show how critical it is to set the right documentation for the

analysis and processing of any new venture plan by a VC firm.

Through this experience I learned how to prepare the whole set of documents required by a VC as defined

below:

• Investment Teaser

• Business plan(Business idea, Market, Competitor Study, Financial and Marketing Plan, Exit Plan

etc)

• Information memorandum (a presentation having summary on all dimensions) • Financial Plan

1. Investment Teaser:

This covers the necessary summary and aspects of the new venture proposed, topics like:

Page | 28

o Investment Summary o

About the Company o The

Need o The current Gap o

The opportunity o ROI

and Sustainability o The

Capability and the current

state o The Competition o

The USP o The Revenue

Model o Funding Needs o

End note

2. Business plan :

This holds the whole information in a detailed manner regarding the venture plan, financials, its market

characteristics, and every details from the ownership to capital utilisation.

Such details are only inferred to the investor once they seek interest in the venture after having the view at

the investment teaser

3. Information Memorandum:

This is presentation the investee would show the investor, with clear details on the outline of all features

like the Venture Idea, Market analysis, Business model, Marketing plan, Financial Plan, Entrant barrier,

Management, Current services, Exit Plan, Risk Involved.

4. Financial Plan:

Ratios that describe all important business financial status for last 5 to 6 years, the capital allocation, cash

flow statements, profit n Loss statements, Balance sheets, cost analysis and yearly graphical presentations

for the expenses and earnings forecasted in for the coming years with this new venture.

Page | 29

Example shown in appendix

CHAPTER 5 : DATA ANALYSIS

5.1 : FACTORS EFFECTING THE CAPITAL DECISIONS Descriptive Characteristics The survey covers all factors with a scale of one to five.

One been the least and five been the maximum.

The survey is done to check the rank of factors effecting the decision making of an investor.

Here the respondents rank

• Business Idea

• Financials

• Management

• IRR Conditions

• Pay Back period

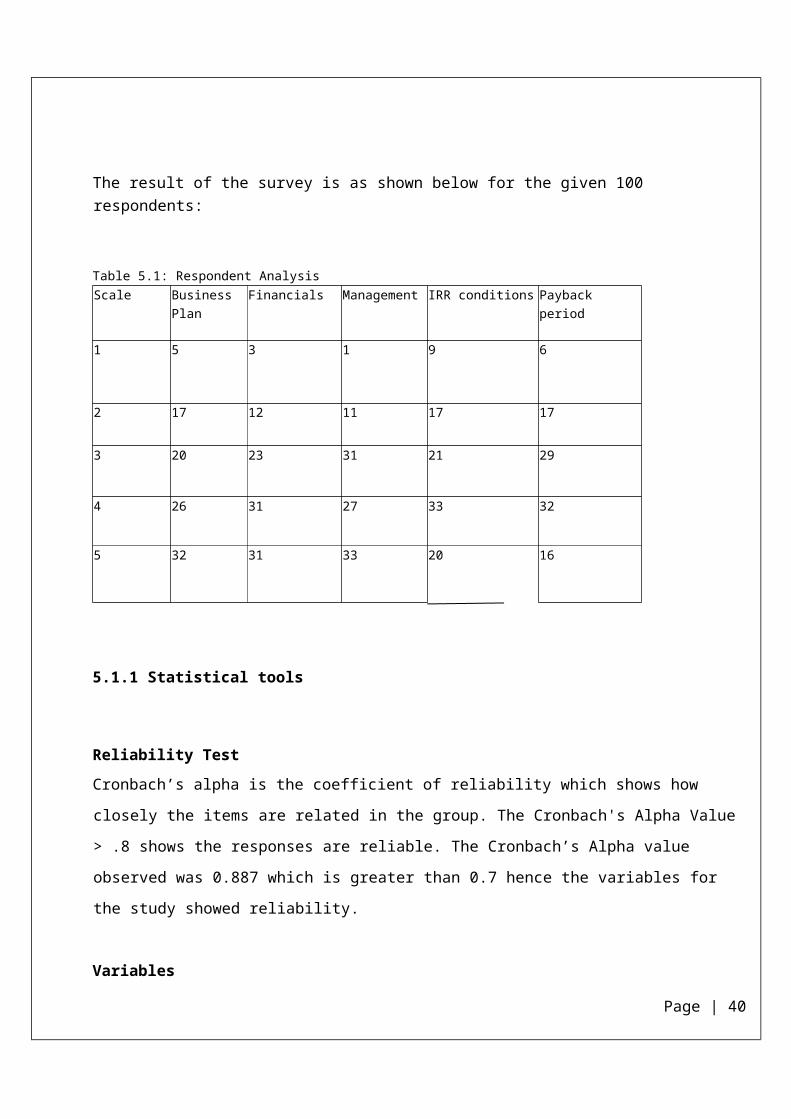

The result of the survey is as shown below for the given 100 respondents:

Table 5.1: Respondent Analysis Scale Business Plan Financials Management IRR conditions Payback period

1 5 3 1 9 6

2 17 12 11 17 17

3 20 23 31 21 29

Page | 30

4 26 31 27 33 32

5 32 31 33 20 16

5.1.1 Statistical tools

Reliability Test

Cronbach’s alpha is the coefficient of reliability which shows how closely the items are related in the

group. The Cronbach's Alpha Value > .8 shows the responses are reliable. The Cronbach’s Alpha value

observed was 0.887 which is greater than 0.7 hence the variables for the study showed reliability.

Variables

The independent variables used here are Business plan, Financials, Management, IRR Conditions,

Payback period and dependent variable is Venture Capitalist financing decision

Hypothesis

H0: Business plan, Financials, Management, IRR Conditions, Payback period does not affect the Venture

Capitalist financing decision.

H1: Business plan, Financials, Management, IRR Conditions, Payback period does affect the Venture

Capitalist financing decision.

Confidence Interval The confidence associated with an interval estimate is at 95%. Decision Rule

Page | 31

Since Observed value is less than Critical value (at 95% confidence interval value alpha is .05) Ho is rejected. Hence the hypothesis is proved that the venture capital financing is dependent on the factors like Business

Initial Eigenvalues Extraction Sums of Squared Loadings

Total % of Variance Cumulative % Total % of Variance Cumulative %

1 3.899 77.986 77.986 3.899 77.986 77.986

2

3

4

5

.837

.212

.051

1.311E-16

16.744

4.250

1.020

2.622E-15

94.730

98.980

100.000

100.000

Extraction Method: Principal Component Analysis.

Factor Analysis

Factor analysis is a collection of methods used to examine how underlying constructs influence the

responses on a number of measured variables. Factor analyses are performed by examining the pattern of

correlations (or covariance’s) between the observed measures. Measures that are highly correlated (either

positively or negatively) are likely influenced by the same factors, while those that are relatively

uncorrelated are likely influenced by different factors. (Decoster, 1998)

TABLE 5.1.3 Communalities

Initial Extraction

Timeline 1.000 .691

Business idea 1.000 .566

Financials 1.000 .965

Management 1.000 .875

IRR 1.000 .803

Extraction Method: Principal Component

Analysis.

Page | 32

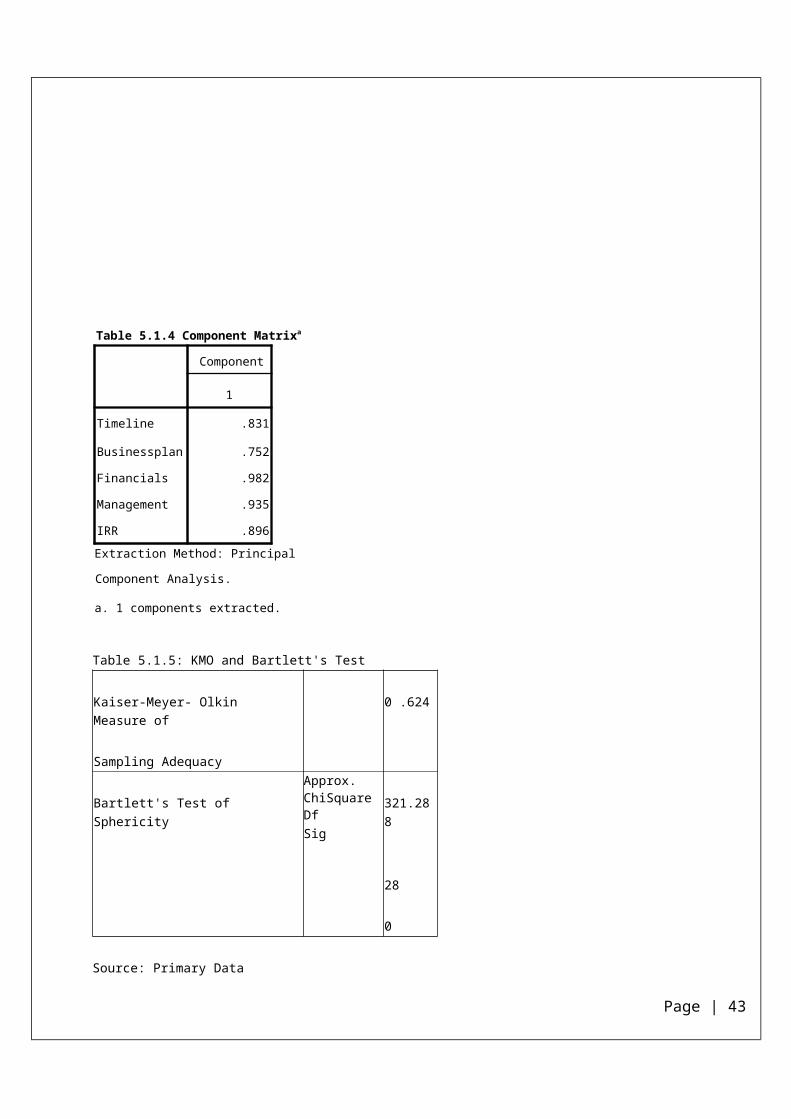

Table 5.1.4 Component Matrixa

Component

1

Timeline .831

Businessplan .752

Financials .982

Management .935

IRR .896

Extraction Method: Principal

Component Analysis.

a. 1 components extracted.

Table 5.1.5: KMO and Bartlett's Test Kaiser-Meyer- Olkin Measure of Sampling Adequacy

0 .624

Bartlett's Test of Sphericity

Approx. ChiSquare Df Sig

321.288 28 0

Source: Primary Data

Decision Rule:

Page | 33

Barlett’s Test of sphericity tests the null hypothesis that the correlation matrix is an identity matrix KMO

should be greater than 0.6 in orders to reject null hypothesis. The results for KMO and Bartlett’s Test

showed that factor analysis was success.

Variables Used:

The variables used for the study are Business plan, Financials, Management, IRR Conditions, Payback

period. These variables were used to examine the pattern of correlations. Out of these 5 factors only 2

components were found to be highly correlated.

Decision Rule:

Based on the rotated component matrix two important variables were identified which are Financials,

Management. Chi-square testing was done to prove the main hypothesis using these three variables.

Conclusion: The advantage of using factor analysis is that it results in reduction of number of variables,

by combining two or more variables into a single factor but the limitation of this tool is its interpretation.

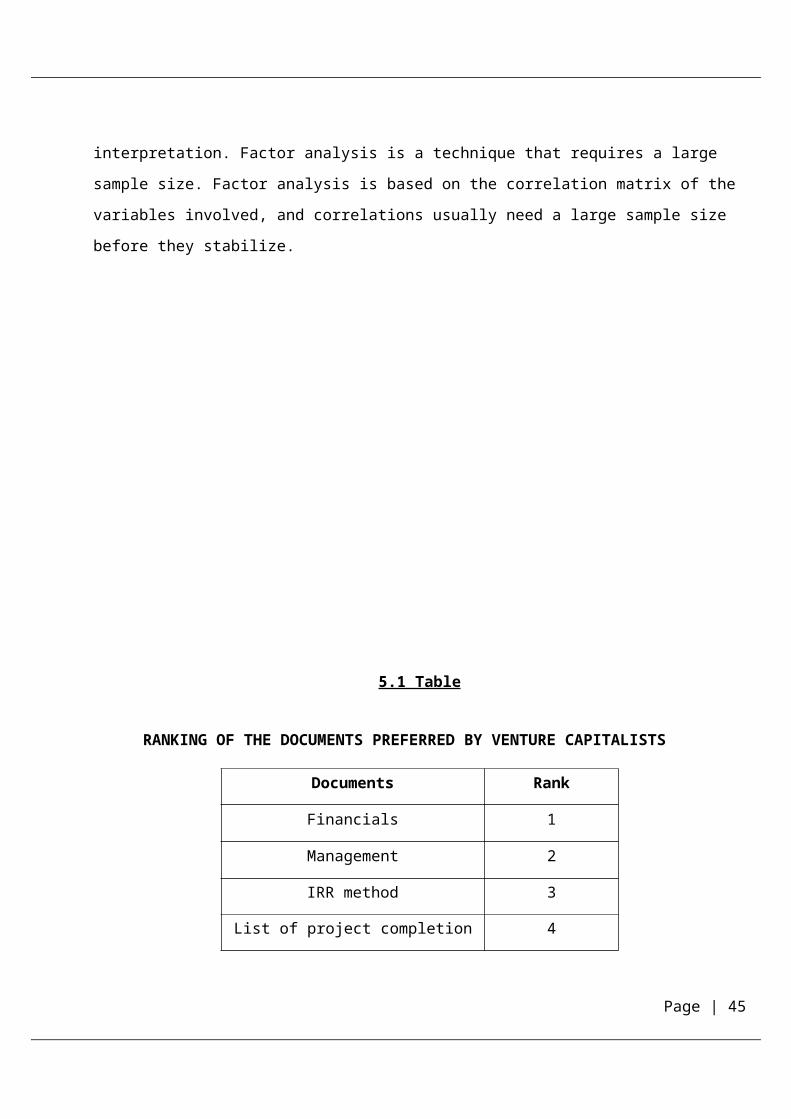

Factor analysis is a technique that requires a large sample size. Factor analysis is based on the correlation

matrix of the variables involved, and correlations usually need a large sample size before they stabilize.

Page | 34

5.1 Table

RANKING OF THE DOCUMENTS PREFERRED BY VENTURE CAPITALISTS

Documents Rank

Financials 1

Management 2

IRR method 3

List of project completion 4

CRITERIA FOR INVESTING IN START-UP COMPANIES:

The criteria for investing in start-up companies are based on the following factors.

• Nature of the venture team • Project / Product / Service.

• Market characteristics.

• Financial consideration.

• Entrepreneurial and management experience.

Depending on the critical and analytical evaluation of the above mentioned factors, the decision as to

whether to accept or reject the project / proposal will be taken.

Chart-5.1

Page | 35

RANKING OF THE DOCUMENTS PREFERRED BY VENTURE CAPITALIST

5.1.2 INTERPRETATION:

In the list of order of preference of required documents, the financials including previous year’s income

statement and forecasted cash flow occupies the first slot as more respondents gave it the first preference.

Financials:

Page | 36

Factor Importance

TimelineIRRManagementFinancials

1.2

1

0.8

0.6

0.4

0.2

0

Financial plan is preferred by more respondents because it helps to evaluate how well do the firm utilise

the fund both for the investor and the consultant early a project will yield returns and based on that

investment decision are made.

Cash flow projection helps respondents to know how the funded cash will be utilized to give best

profitable returns. This helps to analyse the company’s ability to utilize the given funds for the optimum

results.

Balance Sheet, helps to evaluate company’s price earning ratio and debt coverage ratio in order to assess

whether the company is meeting external debts or not.

Management:

A strong leadership and an experience of past success venture projects gives venture capitalist an

assurance that they are investing money in the right firm and will be utilised for the right purpose.

IRR Conditions:

Internal rate of return and its share towards the investor further help him make a faster decision on a

venture project.He seeks his share of advantage and capital gain through his investment and would only

agree to go forwards if that is clear and also achievable for the timeline planned Timeline:

A investor will like faster IRR and for that he requires a project with a shorter timeline with greater

revenues and profits. His decision making factors would thereby lie on the timeline feature of the desired

venture. If the timeline is defined well with achievable targets and acceptable risk conditions an Investor

will find it more comfortable in investing in such Venture ideas.

5.1.3 FINDINGS:

• Innovative nature of the project and its strong financial outlook with forecasted cash flow

statement and proper allocation stated well in the investor documentation becomes the

foremost amongst the major criteria in decision making.

• Entrepreneurial personality and experience, is given second importance by the respondents.

Page | 37

• IRR expected and one that can be achieved is given next importance after the entrepreneurial

personality and experience.

• Timeline, a most crucial decision making factor as it justifies the time for the ROI invested by

the venture capitalist.

• An International Market and market Characteristics criterion is given fifth position by the

respondent.

5.2 Table

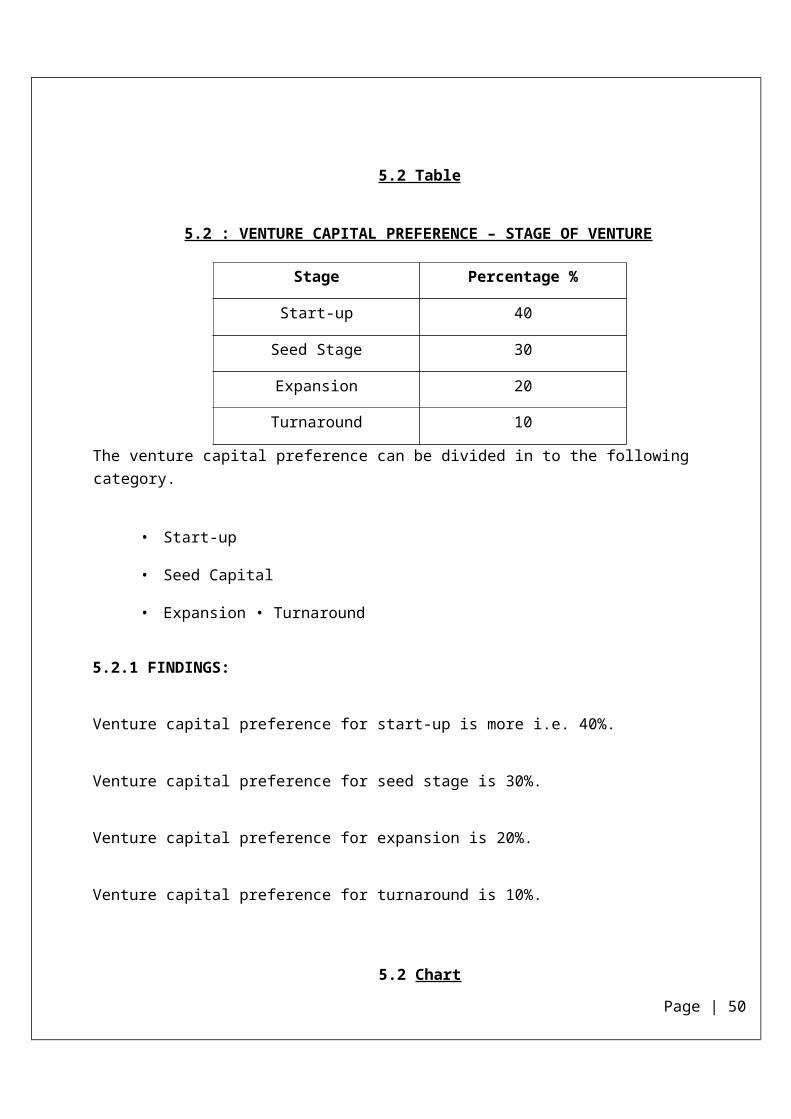

5.2 : VENTURE CAPITAL PREFERENCE – STAGE OF VENTURE

Stage Percentage %

Start-up 40

Seed Stage 30

Expansion 20

Turnaround 10

The venture capital preference can be divided in to the following category.

• Start-up

• Seed Capital

• Expansion • Turnaround

5.2.1 FINDINGS:

Venture capital preference for start-up is more i.e. 40%.

Page | 38

Venture capital preference for seed stage is 30%.

Venture capital preference for expansion is 20%.

Venture capital preference for turnaround is 10%.

5.2 Chart

5.2 : VENTURE CAPITAL PREFERENCE – STAGE OF VENTURE

5.2.2 : INTERPRETATION:

Majority of venture capitalists in India and as observed from literature records on internet prefer providing

finance to start-ups with a seeding stage though providing finance involves high risks, but never the less

promises high returns.

Page | 39

TurnaroundExpansionSeed StageStart-up

Percentage %

TurnaroundExpansionSeed StageStart-up

45

40

35

30

25

20

15

10

5

0

Seed stage financing is difficult to execute as it involves great effort not for making the project take-off.

The management further also is responsible for constant monitoring and supporting the project.

Expansion and Turnaround stage covers 20% and 10% respectively, as at these stages conventional

finance is available and even there is a very limited exit option for venture capitalists.

5.3 Table

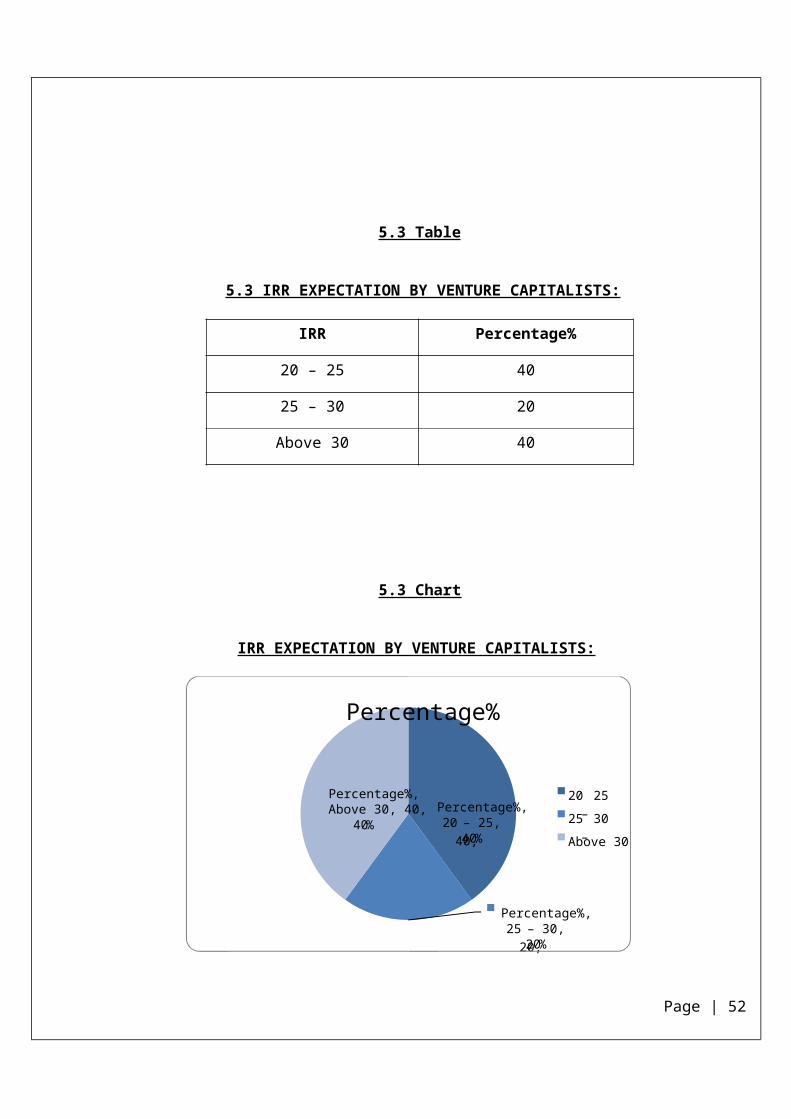

5.3 IRR EXPECTATION BY VENTURE CAPITALISTS:

IRR Percentage%

20 – 25 40

25 – 30 20

Above 30 40

5.3 Chart

IRR EXPECTATION BY VENTURE CAPITALISTS:

Page | 40

5.3.1 INTERPRETATION: The percentage of the required minimum IRR preferences by venture

capitalists turns out to be more than that demanded by the banking companies or other financial firms

backed by banks due to several reason :

• Opportunity cost when compared is high by private firms is more.

• Exchange risk in financing and raising funds is more, country’s constraints and economic risk

faced by private venture capitalist is more.

Page | 41

Above 30

30 –25

20 25 –

Percentage%

%40Above 30, 40, Percentage%,

%20 – 30, 20, 25

Percentage%,

%4020 – 25, 40,

Percentage%,

CHAPTER 6 : FINDINGS & CONCLUSION

6.1 INTERPRETATION FOR FACTORS PREFFERED BY VC BEFORE INVESTING IN A

VENTURE:

• An innovative project is essential but within realistic and logical area, venture capitalists seeks any

project which promises immense growth potential and competitive ability to succeed and sustain

in the market.

• Entrepreneurial personality, experience and his management team contribute towards the

execution and success of the project, since they utilise the VC’s fund the venture capitalist make

sure of their major role with managing, working, guiding and co-coordinating the team towards

the right path.

• International markets for the project also assumes importance in the present situation where no

barriers exits for entry all can complete in one place and the success of the

• Project depends on facing competition not just in the local market but also in the global market.

• Good Team work, the mantra for modern success stories in the market, holds good for venture

capital funding too.

Page | 42

• Market Characteristics covers the marketability of the product and the competition it faces from

other competitors. Returns in the short period depend on the market characteristics of the

projecthence it is importance as a major criterion in decision making for capital funding.

6.2 FINDINGS AND CONCLUSION:

• Venture capital has become a part of the popular business in India. Venture capital has also

become synonymous with investing in high risk technology businesses, that could be majorly IT

and can spread across further domains like healthcare, agriculture etc.

• The VC’s final decision on a proposed venture is based on many criteria and also it differs from

one to other. All seek one common thing the right and proper way of documentation for them to

analyse the projects faster and easily.

• If the project is new, promising and has innovative features then VC’s seek to have more interest

and are ready to help with more amounts because of its wide market characteristics and its ability

to capture the market.

• Many SME’s usually lack the right method and technique to approach the suitable VC and thereby

they seek consultants to seek funds in the startup stage through financial institution.

• SME firms in India believed that ownership of the company is compromised with the price paid

for VC funds

• The preference for investing venture capital is given to start-up stage may be because of

innovativeness of the project and a good team. It is found that less preferences is given for

expansion and turnaround stage of the venture.

Page | 43

• Due to the formal structure of the VC operation and more stringent evaluation process, complete

business plans are compulsory.

• The Internal Rate of Return is more when risk is high. 40 percent of the people don’t want to take

high risk and hence they are satisfied with moderate returns of 20-25 percent. Only 20 percent of

the people are taking risk expecting high returns.

Page | 44

•

•

•

•

The venture capital investment is made adequate on IT, Banking, Media and construction but

investment is inadequate in Telecom, Energy, Resorts and Healthcare. For overall development

adequate investments must be made in all the sectors.

The money invested in late stage is more utilized as compared to any other stage. The reason is, in

late stage the firm will be well established, has good brand name and loyal customers and hence the

money invested is used to promote the product and is fully utilized.

The risk is more in the early stage as the product is new to the market and requires huge capital to

promote the product. Similarly the risk is less in the late stage where the firm is well established

and risk of losses moderate in the growth stage.

Equity shares are much preferred since high returns can be earned. It also ensures active

participation in management and also ownership. Equity shares are preferred since no fixed interest

is given to shareholders; the dividend depends on the profit of the firm. Preference shares are less

preferred because a fixed amount is to be paid irrespective of the condition of the firm.

Page | 47

•

•

•

•

•

•

•

CHAPTER 7 : BIBLIOGRAPHY

“About Venture Capital (VC).” Accessed March 30, 2013. http://indiavca.org/about-venturecapital-vc.html. “Legal - Venture Capital-overview.pdf.” Accessed March 30, 2013. http://ganga.iiml.ac.in/~mishra/Test/mfsmakg/vcapital/Venture%20Capital-overview.pdf. “Loughborough University Institutional Repository: Venture Capital Financing in India: a Study of Venture Capitalist’s Valuation, Structuring, and Monitoring Practices.” Accessed March 30, 2013. https://dspace.lboro.ac.uk/dspace-jspui/handle/2134/6819. “Microsoft Word - The VC Handbook -- _Chapter 0-26_ - PVI.A02_Venture.Capital.Industry.in.India.pdf.” Accessed March 16, 2013. http://smoothridetoventurecapital.com/PVI.A02_Venture.Capital.Industry.in.India.pdf. “MomentumVC | About Venture Capital.” Accessed March 30, 2013. http://www.momentumvc.com.au/docs/3100_f.htm. “VENTURE CAPITAL - ManagementParadise.com Forums - Your MBA Online Degree Program and Management Students Forum for MBA,BMS, MMS, BMM, BBA, Students & Aspirants.” Accessed March 30, 2013. http://www.managementparadise.com/forums/miscellaneous-project-reports/11182-venturecapital.html. “Venture Capitalist.” Accessed March 30, 2013. http://techaloo.com/venture-capitalist/.

Page | 48

•

•

•

APPENDIX

Investment Teaser

Information memorandum

Financial Plan

Page | 49

INVESTMENT TEASER

New- ABC Services Company

Location: Bangalore, India Investment

Summary:

Our company is a one year old Technology Services firm with over 20+ member team and has acquired

few Fortune 500 companies as clients and have built a strong pipeline of prospects from across the Globe

which include USA and Europe. Company will be achieving revenue of US$ 500,000 during the financial

year 2012-13. We are now seeking US$ 5 Million investment to be used for Working capital. Based on

our projections the turnover of the company is expected to touch US$ 100 Million by 2017 proving a

healthy return for the investors.

About the Company:

The Company is promoted by 2 Technology professionals with experience in the IT & ITe Technology

domain for over 20 years. The company is currently focusing on markets in USA, Europe, India and has

plans to operate from other countries as well. "Our company specializes in new-age services like

Cloud Computing, Enterprise Mobility, Enterprise Applications, Information Management and ITe

Consulting." using unique ITe methods”.

The Need:

Across the world, the business needs are changing faster compared to a decade ago due to shorter product

cycles, consumer behavior and more competition. Traditional waterfall model of IT delivery is not

suitable to support changing business anymore; IT has to support business in an 'ITe' way. ITe IT means a

new specialized way of software engineering that requires different skills and expertise

The current Gap: Indian vendors are struggling to support this demand for ITe (due to shortage of ITe skills and knowhow,

difficulty to change the current factory models). Outsourced IT providers are asked by clients to provide

Page | 51

more value (time to market and better quality) as opposed to volume and cheap resources. These days, at

least one in 3 large RFPs is specifically demanding ITe delivery.

The opportunity:

Industries like Banking and Finance, Healthcare, Retail, Manufacturing, Telecom are shifting towards ITe

. Apart from the shift in the current market, a new market for ITe is also emerging due to emerging trends

like e-retail, e-governance, cloud and mobility. ITe is the way forward; Gartner predicts that in the next

few years, 80% of the IT will move to ITe. Current IT service companies are not geared up to support this

demand. There are no pure-play ITe IT providers from India. The size of the target market is at least USD

40 billion by 2017. We are positioning ourselves as India's first pure-play ITe company, offering ITe at

large scale from offshore.

ROI and Sustainability:

The cost of an ITe developer in the west is twice than a regular developer. Customers are willing to pay

higher for this niche and scarce skill, so the ROI is higher. ITe is a unidirectional shift and a strong

sustainable delivery model for the future.

The Capability and the current state:

We have evangelized and transformed ITe delivery setup in the past for a large international Bank’s IT in

India, so we can establish this model in the Indian services industry as the new service benchmark. We

have started small-scale operations from India from October 2011 with a completely operational ITe

facility. We need to enter the ITe savvy target markets of US and Europe to exploit the strong demand.

The Competition: The only pure play competition is a US based company called ThoughtWorks owned 97% by an

individual. They have 23 offices in 9 countries with a workforce of less than 2000 people making revenue

Page | 52

more than USD 250 million. The success of the model clearly shows that there is a good demand for the

service willing to pay above the market rates.

The USP:

We have already marketed and positioned ourselves to be the leading 'ITe thought leaders' from India

(popularity on social and professional networking sites). We will give a face-lift to the Indian IT

outsourcing scene by providing high-end business value through ‘ITe’. A new entrant would require

similar ITe image, thought leadership and subject matter expertise, and large scale ITe implementation

background to enter this arena.

The Revenue Model:

Our business model is a mix of ITe consulting and ITe delivery. In this short time, we have managed to

attract some known names like Fidelity, Barclays, HP, Monsanto etc. among others with very minimal

investments on sales. We have open pipeline on clients like Goldman Sachs, GE Healthcare, RBS, PwC,

FirstData etc. that need to convert and needs more investment on account management and sales.

Funding Needs:

We need funding of USD 5 million to invest in establishing offices in the US and Europe, setup strong

sales team, strengthening the management structure and board of directors, setup ITe infrastructure and to

groom ITe skills from the market through the ITe university model.

Our target is to reach minimum revenue of USD 101 million by 2017 which would be a faction (0.05%) of

the projected ITe market.

End note:

We have a full business plan available on request. We are very passionate about our business and we

would invite any interested investors to contact our Advisors now to discuss this investment proposal

further with us now.

Financial Plans

Financial Plan

Page | 53

Start-up Funding Table: Start-up Funding

Start-up Funding Start-up Expenses to Fund R2,000,000 Start-up Assets to Fund R115,000,000 Total Funding Required R117,000,000

Assets Non-cash Assets from Start-up

R75,000,000

Cash Requirements from Start-up R40,000,000 Additional Cash Raised R23,000,000 Cash Balance on Starting Date R63,000,000 Total Assets R138,000,000

Liabilities and Capital Liabilities Current Borrowing

R0 Long-term Liabilities R0 Accounts Payable (Outstanding Bills) R0 Other Current Liabilities (interest-free) R0 Total Liabilities R0