46

Finance & Accounting Training: Prudential Planning, Budgeting & Forecasting August 2, 2012 9:30 – 12:00 PM

Finance & Accounting Training: Prudential

Planning, Budgeting & Forecasting

August 2, 2012 9:30 – 12:00 PM

Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

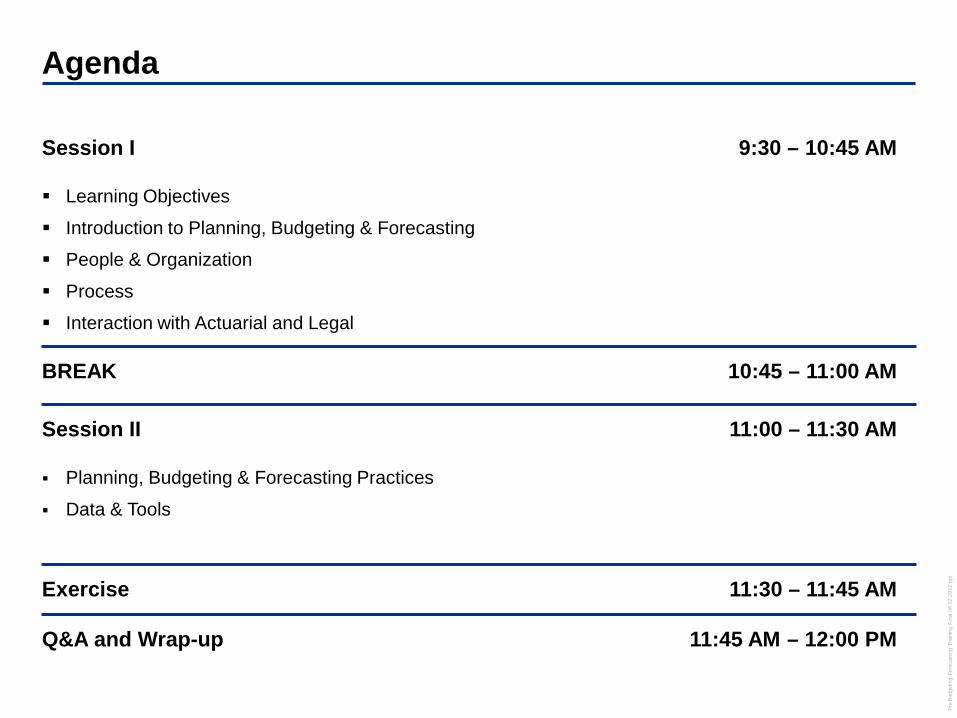

Agenda

Session I 9:30 – 10:45 AM

Learning Objectives

Introduction to Planning, Budgeting & Forecasting

People & Organization

Process

Interaction with Actuarial and Legal

BREAK 10:45 – 11:00 AM

Session II 11:00 – 11:30 AM

Planning, Budgeting & Forecasting Practices

Data & Tools

Exercise 11:30 – 11:45 AM

Q&A and Wrap-up 11:45 AM – 12:00 PM

Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

Learning Objectives

1. Understand planning, budgeting and forecasting processes and their importance

2. Understand how planning, budgeting, and forecasting fit within the broader corporate strategy of an organization

3. Understand the typical planning, budgeting and forecasting process, people and tools used in the planning, budgeting and forecasting processes

4. Understand the role of actuarial and legal in this process

5. Understand data structure and tools used in planning, budgeting, and forecasting

Learning Objectives

By the end of this module, you will have a firm foundation of planning, budgeting, and forecasting (PBF) processes, an exposure to the typical issues organizations experience around planning, budgeting and forecasting

Introduction to Planning, Budgeting & Forecasting

- 5 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

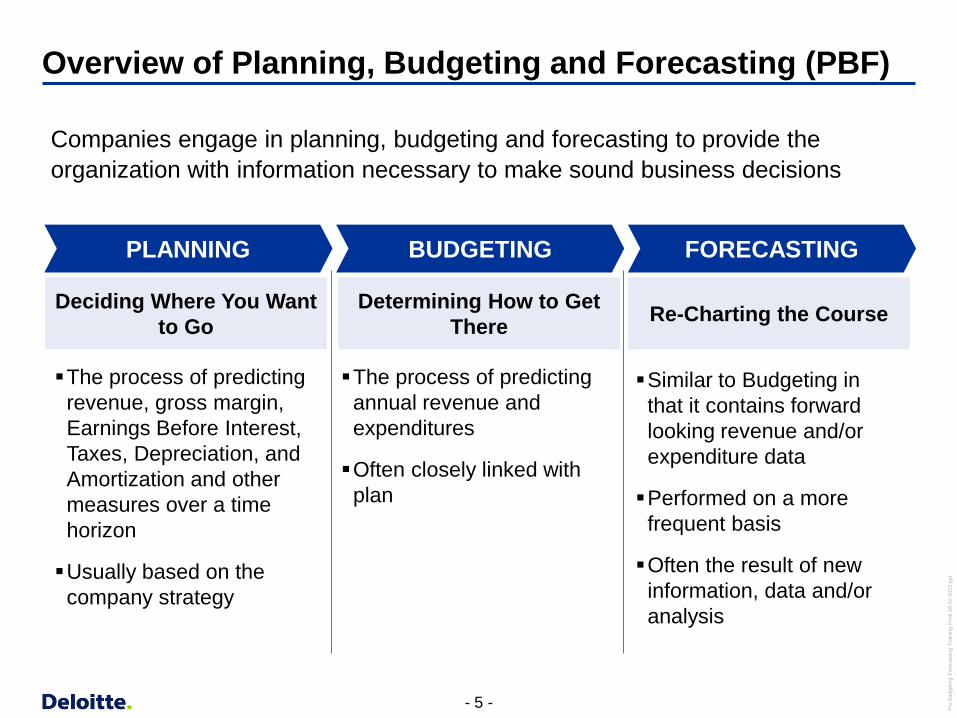

Overview of Planning, Budgeting and Forecasting (PBF)

PLANNING BUDGETING FORECASTING

Deciding Where You Want to Go

The process of predicting revenue, gross margin, Earnings Before Interest, Taxes, Depreciation, and Amortization and other measures over a time horizon

Usually based on the company strategy

Re-Charting the Course Determining How to Get There

The process of predicting annual revenue and expenditures

Often closely linked with plan

Similar to Budgeting in that it contains forward looking revenue and/or expenditure data

Performed on a more frequent basis

Often the result of new information, data and/or analysis

Companies engage in planning, budgeting and forecasting to provide the organization with information necessary to make sound business decisions

- 6 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

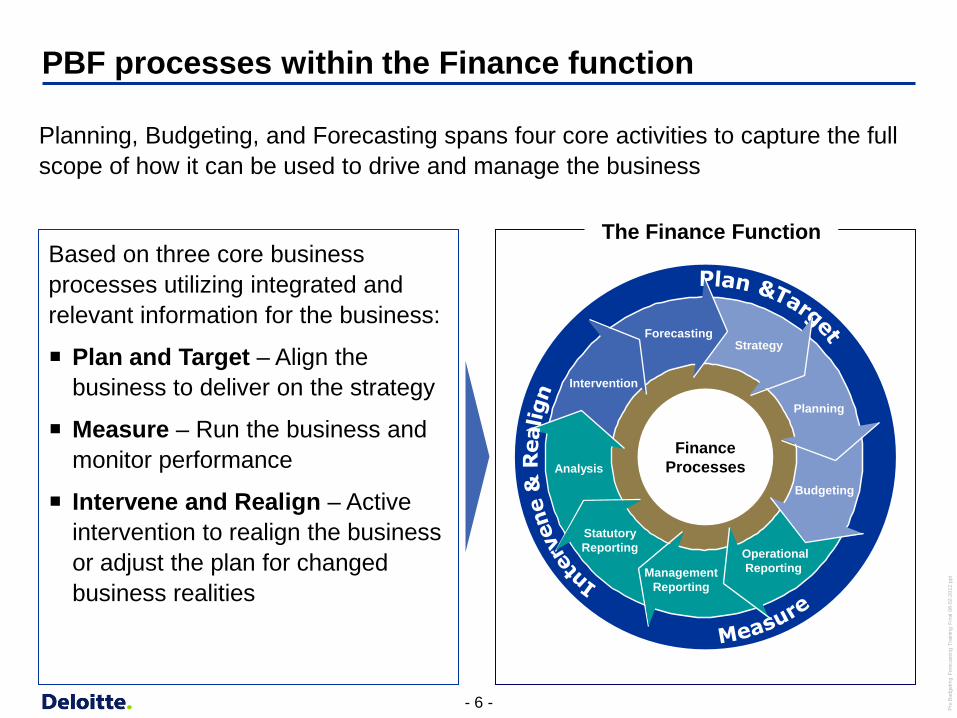

Based on three core business processes utilizing integrated and relevant information for the business:

Plan and Target – Align the business to deliver on the strategy

Measure – Run the business and monitor performance

Intervene and Realign – Active intervention to realign the business or adjust the plan for changed business realities

PBF processes within the Finance function

Planning, Budgeting, and Forecasting spans four core activities to capture the full scope of how it can be used to drive and manage the business

Strategy

Planning

Budgeting

Operational Reporting Management

Reporting

Statutory Reporting

Analysis

Intervention

Finance Processes

Forecasting

The Finance Function

- 7 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

PBF and company Strategy and Performance Management

Business Strategy

Strategic Plan

Action Results

Change

Operating Plans

Budgets

Forecast

Performance Management

Individual performance measures and metrics (KPIs)

Actuals from ERP, business systems, or other sources

Reporting and analysis of KPIs and intervention process

High-level strategic targets

Business unit performance targets

Devise strategy

Implement strategy

Measures

Execute strategy

Performance

Strategic direction is established

cascade down

cascade down

cascade down

- 8 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

PBF begins with the Strategic Plan…

The strategic plan provides direction with objectives and strategies. A company sets a long-term vision and works backwards to translate this into tangible strategies and initiatives that can be used to drive alignment of efforts and resources

Goa

l

Regional dominance? Geographic expansion? Product innovation? Etc.

Time

Company X Today

Translating Backward

Where do we need to be in the future?

Company X Today

Action Plans

How are we going to get there?

Goa

l

Time

Strategic Direction Strategies

- 9 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

… and drives Business Planning

Vision and Mission

Goal

Strategic Plan

Strategic initiatives Targets Communication

Business Planning, Budgeting and forecasting

Actual results

Strategic levers of long term shareholder

value

Internal analysis External analysis

Feedback loop – Results tailored to strategic input

requirement specifications

The planned investment, savings, costs and incremental revenues associated with strategic initiatives are included in the budget and forecasts and are tracked and disclosed in a manner that allows for separate identification of benefits and costs

• The targets set by Client Strategic planning drive the budgeting, and hence the forecasting, process. These targets should include the effect of strategic initiatives

• A mechanism is in place for the communication of and consideration in of strategic imperatives in the planning and budget process

- 10 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

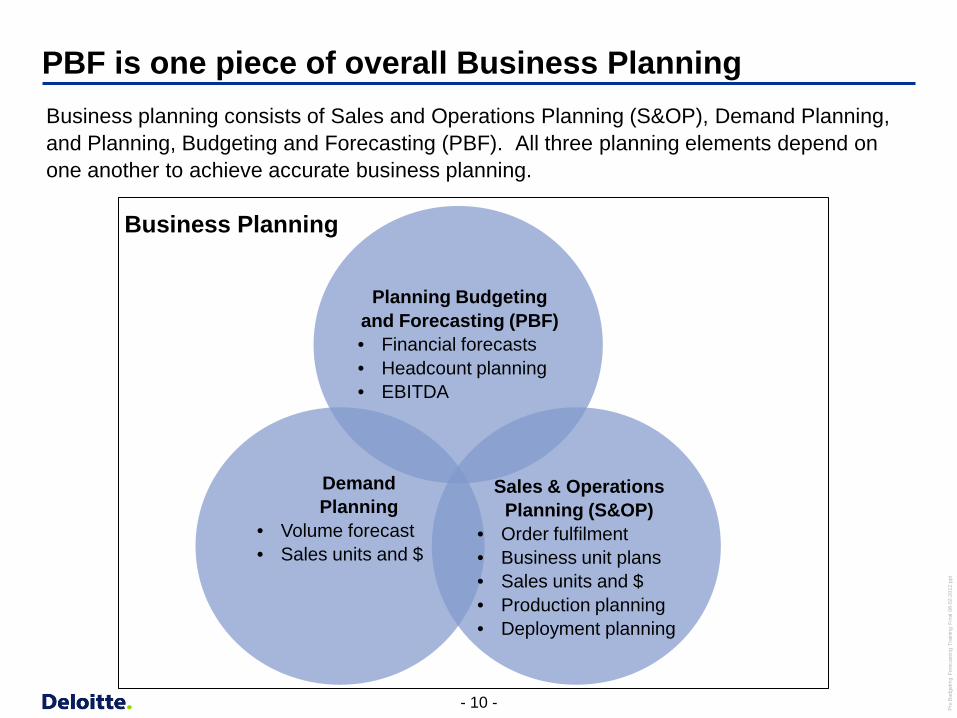

PBF is one piece of overall Business Planning Business planning consists of Sales and Operations Planning (S&OP), Demand Planning, and Planning, Budgeting and Forecasting (PBF). All three planning elements depend on one another to achieve accurate business planning.

Demand Planning

• Volume forecast • Sales units and $

Sales & Operations

Planning (S&OP) • Order fulfilment • Business unit plans • Sales units and $ • Production planning • Deployment planning

Planning Budgeting and Forecasting (PBF) • Financial forecasts • Headcount planning • EBITDA

Business Planning

- 11 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

Polling Question

1) Which of the following is not an element of Planning, Budgeting, and Forecasting?

a) Financial forecasts

b) Headcount planning

c) EBITDA

d) Order fulfillment

People and Organization

- 13 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

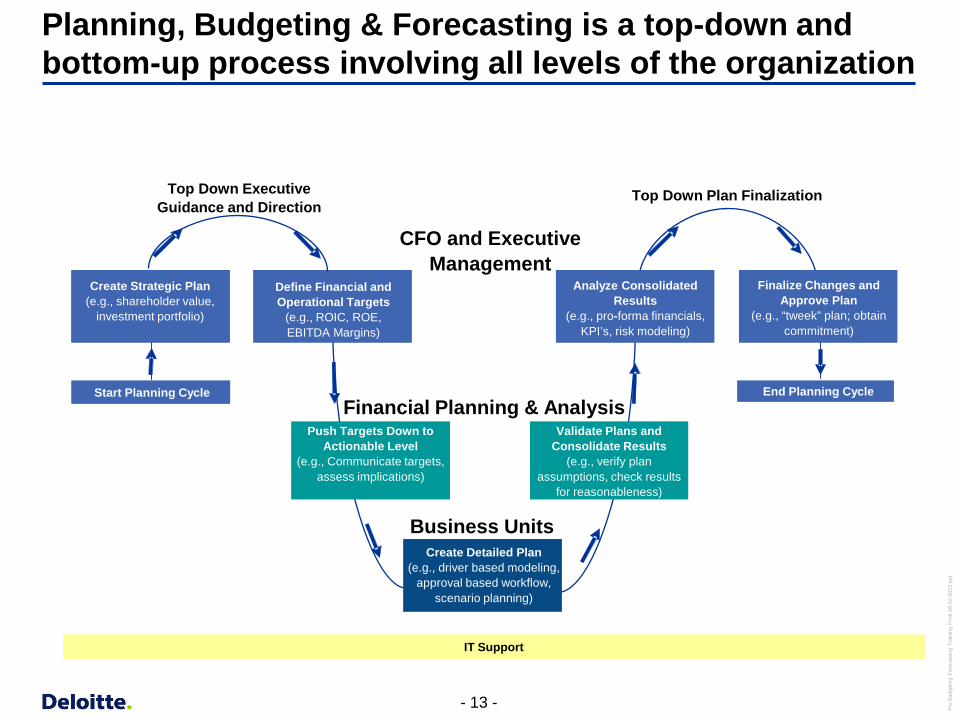

Planning, Budgeting & Forecasting is a top-down and bottom-up process involving all levels of the organization

Start Planning Cycle

Push Targets Down to Actionable Level

(e.g., Communicate targets, assess implications)

Create Detailed Plan (e.g., driver based modeling,

approval based workflow, scenario planning)

Validate Plans and Consolidate Results

(e.g., verify plan assumptions, check results

for reasonableness)

Analyze Consolidated Results

(e.g., pro-forma financials, KPI’s, risk modeling)

End Planning Cycle

Finalize Changes and Approve Plan

(e.g., “tweek” plan; obtain commitment)

Financial Planning & Analysis

CFO and Executive Management

Top Down Executive Guidance and Direction

Top Down Plan Finalization

Define Financial and Operational Targets

(e.g., ROIC, ROE, EBITDA Margins)

Create Strategic Plan (e.g., shareholder value,

investment portfolio)

Business Units

IT Support

- 14 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

The process includes many stakeholders

Stakeholders Role/Responsibilities How Information is Used

CFO and Executive Management

Define strategy and strategic goals Approve targets from FP&A, and budget,

plan or forecast from business units

Communicate forecasted performance to the investor community

Corporate FP&A (Financial Planning

and Analysis)

Translate strategy into measurable targets

Monitor progress against those targets Ensure that the company manages risks

associated with achieving the strategic objectives

Understand the company’s forecasted performance

Business Units Execute the process Construct the budget based on spending

needs Responsible for corporate strategy

development and integration with the operational planning process

Understand their revenue targets and spend for the fiscal year

Information Technology and

Accounting

Support the company-wide budgeting process enabled by network software that shares assumptions and captures targets

Enable availability, processing, analysis and accuracy of information

Process

- 16 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

The PBF process includes multiple steps and sign-offs

The budget process begins with the setting of targets (e.g., operational, financial) by executive management and corporate strategy, followed by the development of the plan

Primary stakeholders, including revenue generating business units, regions or shared services and other cost centers develop their components of the budget, often using prior year actuals as a starting point

Following initial review and approval, the budget is submitted to and consolidated by the Corporate Financial Planning & Analysis

Financial Planning & Analysis finalizes the budget and reviews with executive management (CFO, CEO)

After approval by the board of directors, the annual budget is loaded into the budgeting and/or accounting tool for comparison against actual results during the year

- 17 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

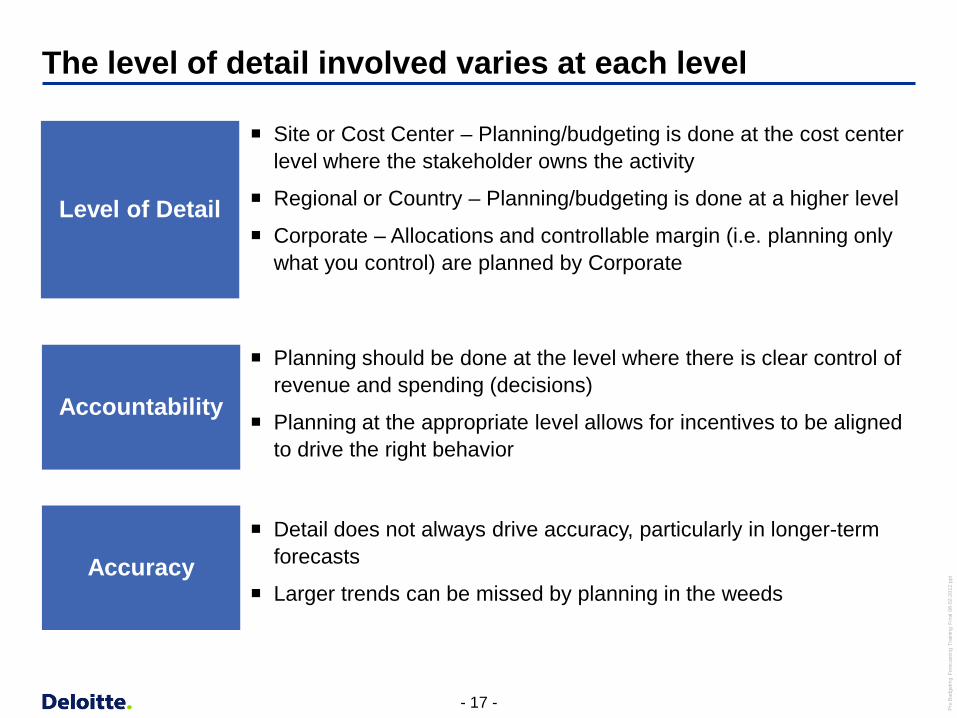

The level of detail involved varies at each level

Level of Detail

Accuracy

Accountability

Site or Cost Center – Planning/budgeting is done at the cost center level where the stakeholder owns the activity

Regional or Country – Planning/budgeting is done at a higher level

Corporate – Allocations and controllable margin (i.e. planning only what you control) are planned by Corporate

Detail does not always drive accuracy, particularly in longer-term forecasts

Larger trends can be missed by planning in the weeds

Planning should be done at the level where there is clear control of revenue and spending (decisions)

Planning at the appropriate level allows for incentives to be aligned to drive the right behavior

- 18 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

The resulting information can take many forms

The reporting generated from the budgeting, planning, and forecasting process varies by organization. Some typical reports include:

Budgeting and Planning Reports – Financial Statements – Total Revenue – Revenue by product – Expenses

Forecasting Reports – Budget to Actual Variance Analysis – Actual Expense Analysis

- 19 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

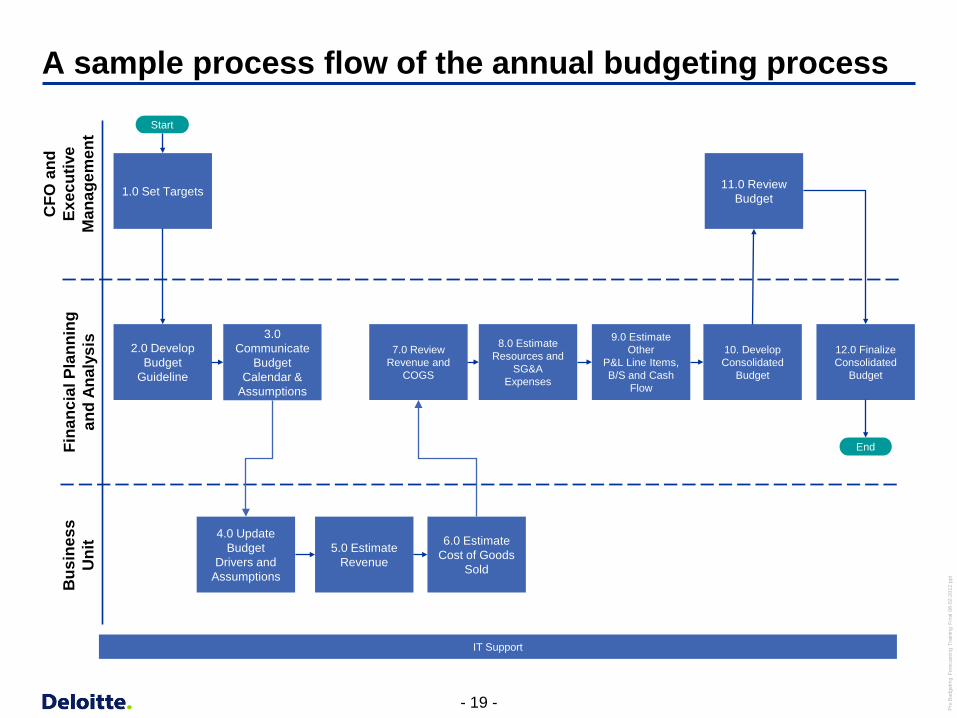

A sample process flow of the annual budgeting process C

FO a

nd

Exec

utiv

e M

anag

emen

t Fi

nanc

ial P

lann

ing

and

Anal

ysis

Start

11.0 Review Budget

End

3.0 Communicate

Budget Calendar &

Assumptions

2.0 Develop Budget

Guideline

4.0 Update Budget

Drivers and Assumptions

5.0 Estimate Revenue

6.0 Estimate Cost of Goods

Sold

Bus

ines

s U

nit

1.0 Set Targets

9.0 Estimate Other

P&L Line Items, B/S and Cash

Flow

8.0 Estimate Resources and

SG&A Expenses

10. Develop Consolidated

Budget

7.0 Review Revenue and

COGS

12.0 Finalize Consolidated

Budget

IT Support

Interaction with Actuarial and Legal

- 21 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

Planning Budgeting Forecasting

Interaction of Actuarial and Legal with Finance

Strategic Planning Gather Data Prepare Budget Consolidate and Sign-Off

Periodic Forecasting

Updates

• Actuarial provides input into the Reinsurance and Insurance strategic planning process including loss reserve and IBNR

• Legal provides guidance to the strategic planning process on the impact of current and projected statutory, regulatory and compliance requirements

• Actuarial and Legal receive standard budget template from Corporate

• Actuarial gathers data and Actuarial department budget

• Legal gathers data for Legal department budget

• Actuarial provides guidance in Reinsurance and Insurance UW budget preparation on loss reserves and IBNR

• Legal provides guidance in Insurance and Reinsurance budget preparation on areas such as regulatory, compliance and capital reserves

• Actuarial prepares budget for the department using data gathered

• Legal prepares budget for the department using data gathered

• Actuarial reviews the consolidated Insurance and Reinsurance UW budget for accuracy and provides sign-off

• Legal reviews the consolidated Insurance and Reinsurance budgets to ensure compliance and provides sign-off

• Actuarial performs valuation and analysis on loss reserves and IBNR and prepares projections for Insurance and Reinsurance forecasts

• Actuarial reviews and signs-off on Insurance and Reinsurance forecasts

• Legal analyzes impact of legal and regulatory and provides input to the forecasting process

• Actuarial and Legal prepare departmental forecasts

- 22 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

Actuarial and Legal Roles in Finance

Key Activities:

Actuarial Reviews and provides sign-off on the budgets on insurance and reinsurance sections of planning,

budgeting & forecasting

Performs valuation and projection work for forecasting and close processes (e.g., IBNR)

Produces management reports (e.g. Global Premium Report for Actuarial)

Creates of supporting schedules (e.g. Schedule P for Statutory Reporting)

Legal Reviews and communicates loss reserves to Finance as part of the forecasting process

Provides advice on and ensures compliance with regulatory requirements (e.g., Solvency II)

, Impact on the Planning, Budgeting and Forecasting Process Actuarial valuation and projection work may be performed using a combination of vendor systems, in-

house systems and spreadsheets which may lead to a long financial forecasting and close

Changes in regulatory and compliance environments, particularly around capital and reserve requirements can have a major impact in the planning, budgeting and forecasting process, making Legal a critical partner in the planning, budgeting and forecasting process

BREAK

PBF Practices

- 25 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

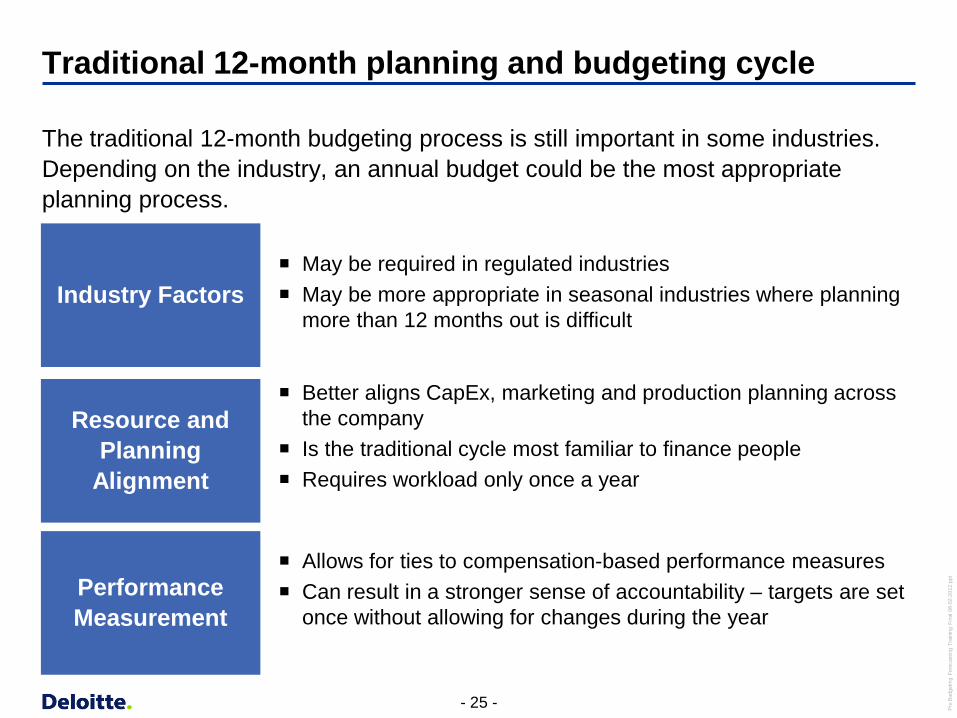

Traditional 12-month planning and budgeting cycle

The traditional 12-month budgeting process is still important in some industries. Depending on the industry, an annual budget could be the most appropriate planning process.

Industry Factors

Performance Measurement

Resource and Planning

Alignment

May be required in regulated industries May be more appropriate in seasonal industries where planning

more than 12 months out is difficult

Allows for ties to compensation-based performance measures Can result in a stronger sense of accountability – targets are set

once without allowing for changes during the year

Better aligns CapEx, marketing and production planning across the company

Is the traditional cycle most familiar to finance people Requires workload only once a year

- 26 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

Issues with traditional 12-month planning and budgeting

Jack Welch, former Chief Executive Officer (CEO) of General Electric, has called the annual budgeting process the “bane of corporate America” and Bob Lutz, Vice Chairman of Chrysler, has referred to it as a “tool of repression”

Too Historically

Focused

Treated as an Isolated Event

Provides Limited Visibility

Issues with a Typical 12-Month Planning Cycle

Annual budgets have a very short shelf life and are overly focused on the past

Rolling forecasts focus on creating a realistic view of the future, allowing leadership to quickly react to changing environments

Annual budgets create an artificial barrier at year-end, and there is little insight gained beyond the current year. This limited view can lead to unproductive actions management to hit numbers or spend budget

Rolling forecasts continually provide an updated assessment of progress the against medium term goals that drive firm value

Traditional budget processes consume significant leadership headspace in the 3rd quarter, but are rarely evaluated more than once per year

Rolling forecasts are typically refreshed at least once per quarter, allowing managers to learn from their forecast record, and to refine forecasting techniques and assumptions

- 27 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

Other planning, budgeting & forecasting practices

PBF Practice Key Feature Benefits

1 Rolling Forecasts

Expansion of forecast horizon beyond current fiscal year

Better insights into market conditions and expected performance

2 Driver Based Planning

Development of planning models based on major internal and external drivers that impact performance

More accurate plans and better insight into performance drivers

3 Capital Budgeting

Focuses capital spend on projects or initiatives that drive value

Better return on investment for key initiatives

4 Scenario Analysis

Using various assumptions to gauge bottom line impact

Better decision-making that includes consideration of all business scenarios

- 28 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

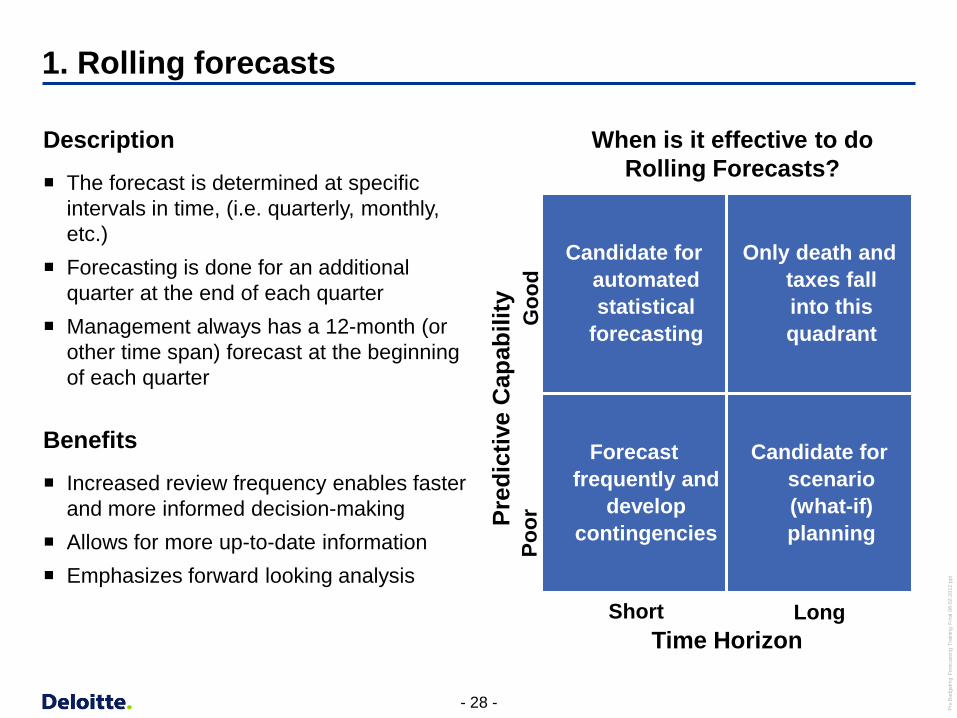

1. Rolling forecasts

Description

The forecast is determined at specific intervals in time, (i.e. quarterly, monthly, etc.)

Forecasting is done for an additional quarter at the end of each quarter

Management always has a 12-month (or other time span) forecast at the beginning of each quarter

Benefits

Increased review frequency enables faster and more informed decision-making

Allows for more up-to-date information Emphasizes forward looking analysis

Candidate for automated statistical

forecasting

Only death and taxes fall into this quadrant

Forecast frequently and

develop contingencies

Candidate for scenario (what-if) planning

When is it effective to do Rolling Forecasts?

Pred

ictiv

e C

apab

ility

Time Horizon Short Long

Goo

d Po

or

- 29 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

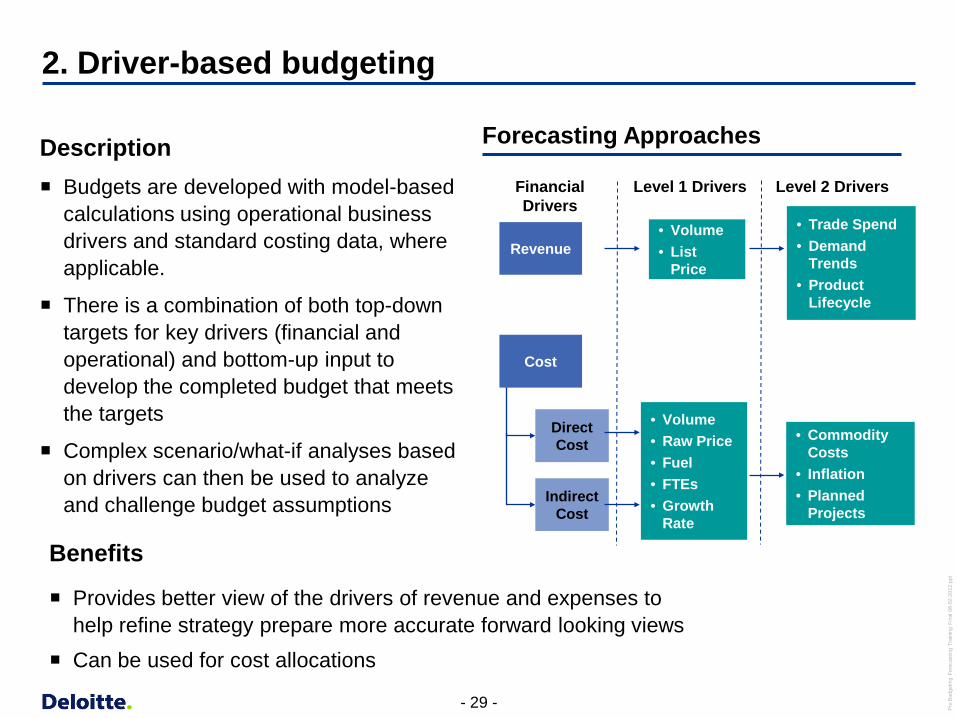

2. Driver-based budgeting

Revenue

Direct Cost

Indirect Cost

Financial Drivers

Level 1 Drivers Level 2 Drivers

• Volume • List

Price

• Volume • Raw Price • Fuel • FTEs • Growth

Rate

• Trade Spend • Demand

Trends • Product

Lifecycle

• Commodity Costs

• Inflation • Planned

Projects

Cost

Description Budgets are developed with model-based

calculations using operational business drivers and standard costing data, where applicable.

There is a combination of both top-down targets for key drivers (financial and operational) and bottom-up input to develop the completed budget that meets the targets

Complex scenario/what-if analyses based on drivers can then be used to analyze and challenge budget assumptions

Forecasting Approaches

Benefits

Provides better view of the drivers of revenue and expenses to help refine strategy prepare more accurate forward looking views

Can be used for cost allocations

- 30 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

2. Driver-based budgeting (contd.)

Cost Driver Cost Category

Total Subscribers

Gross Adds Deactivations

Handset Exchanges

Minutes of Use (MOUs)

Handset Upgrades

Calls to Care (Internal)

Service Plan Revenue

Long Distance MOUs

Cell Sites Calls to Care (Outsourced)

Equi

pmen

t Pro

gram

s (L

aker

u)

Cos

t: 50

%

Rev

enue

: 49%

Bad

Deb

t Exp

ense

(Kirk

patri

ck)

Cos

t of L

D &

Tol

l (R

ay)

CC

Out

sour

cing

(Nok

es)

Cre

dit C

ard

Fees

(Kirk

patri

ck)

Bank

Fee

s (K

irkpa

trick

)

Nat

iona

l Net

wor

k (R

ay)

Usa

ge –

Var

iabl

e (R

ay)

Usa

ge R

ecip

roca

l Com

p (R

ay)

Dire

ctor

y As

sist

ance

(Ray

)

Upg

rade

Pro

gram

s (B

utle

r)

Dat

a C

onte

nt E

xpen

se (B

rodm

an)

Varia

ble

Equi

pmen

t Los

s R

etai

l: 91

%

Dea

ler/V

AR: 8

09%

C

onsu

mer

Dire

ct: 6

4%

Nat

iona

l Ret

ail:

75%

Bu

sine

ss: 7

0%

Ret

entio

n C

omm

issi

ons

(Inza

)

Line

Ser

vice

Fix

ed (R

ay)

Util

ities

(Ray

)

Leas

es &

Ren

t (R

ay)

Parts

, Sup

plie

s, L

abor

& M

aint

(Ray

)

Mis

cella

neou

s C

ust S

uppo

rt (N

okes

)

Cus

tom

er C

are

Telc

o (S

trick

land

)

Billi

ng S

ervi

ces

(Stri

ckla

nd)

Dire

ct C

omm

issi

ons

(Nok

es)

Coo

p/M

DF

Expe

nse

(Nok

es)

Agen

t Com

mis

sion

s (N

okes

)

Mis

cella

neou

s –

Activ

atio

ns (N

okes

)

Dire

ct A

ct F

ees

(Nok

es)

CC

/FS

Payr

oll (

Nok

es)

Call Center FTEs

Handsets Sold

Example:

- 31 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

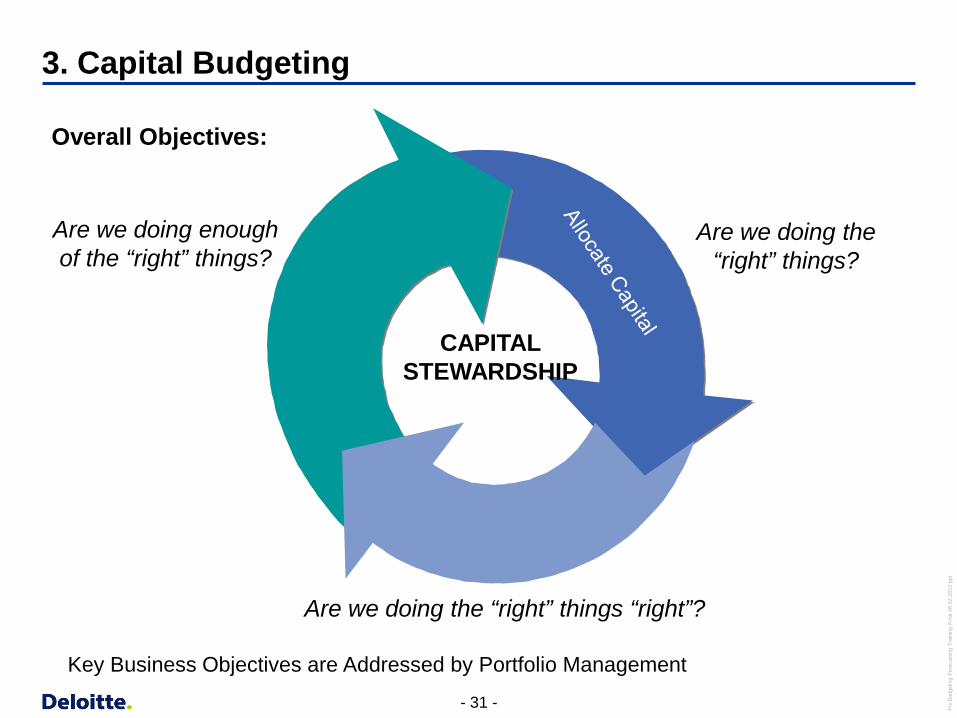

Are we doing the “right” things?

Are we doing the “right” things “right”?

Are we doing enough of the “right” things?

3. Capital Budgeting

Manage Capital

Outlay

CAPITAL STEWARDSHIP

Overall Objectives:

Key Business Objectives are Addressed by Portfolio Management

- 32 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

With finite resources, capital, and time, how can an organization better manage the capital allocation and alignment of work with strategic imperatives?

Manage Capital Outlay • Gain visibility to project portfolio • Manage project execution

2

Allocate Capital • Align your investments with

business strategy • Make the right choices when

prioritizing investments

1

Optimize Capital Outlay • Review and reprioritize projects • Reallocate and redistribute

resources and capital

3

3. Capital Budgeting (contd.)

- 33 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

4. Scenario Analysis

Description

Involves the ability to adjust the budget or forecast based on different assumptions and drivers

Executive management or Financial Planning and Analysis will request additional versions of the budget or forecast

Drivers and assumptions are updated and the resulting budget/forecast is analyzed

Benefits

Automated budgeting and planning tools allow for quickly consolidating results. Many applications are built to support this need with multiple versions and associated naming convention

Multiple scenarios allow management to see the bottom line impact of different assumptions and drivers, allowing them to make better decisions and set priorities

Data and Tools

- 35 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

A data structure exists to support PBF

Chart of Accounts

The accounts used for budgeting, planning, and forecasting can be at a summarized level (i.e. 75 accounts)

The accounts can also be the entire chart of accounts from the ERP ledger

Dimensions

Various dimensions can be used to build data calculations at many levels of detail.

Dimensions can support robust and transparent reporting of data

Roll-ups and Hierarchies

The entity structure of an organization (i.e. cost centers and departments) shapes the structure of the entity hierarchy used in budgeting, planning, and forecasting

The components that make up the data structure of planning, budgeting, and forecasting are:

Attributes

An attribute is a ‘flag’ on a dimension that allows for additional information to be captured

The use of attributes greatly increases the robustness of reporting

- 36 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

The chart of accounts is dictated by several factors

The chart of accounts from the ERP system is often used as a starting point for the chart of accounts in the budgeting/forecasting tool

Below is a high-level example of an online travel services firm:

Business Unit

20000 – Online Hotel

20001 – Online Flight Reservations

20002 – Hotel Reservations Network

Department

400 – Customer Care

401 – Hotel Processing

402 – Corporate Travel Account

50001 – Salaries

50002 – Commissions

50003 – Bonus

- 37 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

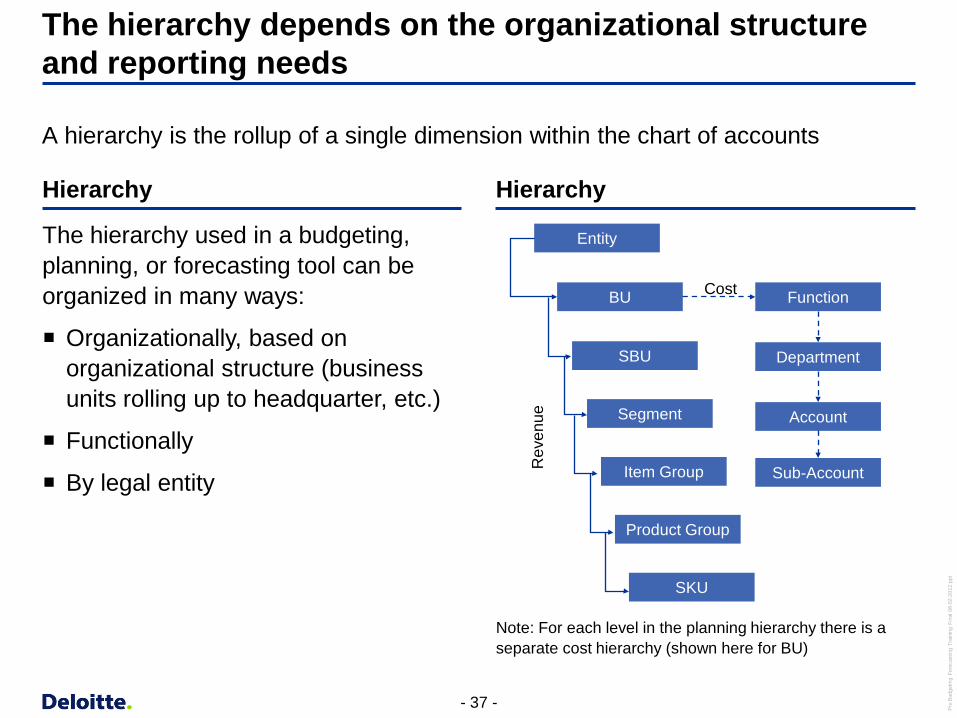

The hierarchy depends on the organizational structure and reporting needs

Hierarchy

The hierarchy used in a budgeting, planning, or forecasting tool can be organized in many ways:

Organizationally, based on organizational structure (business units rolling up to headquarter, etc.)

Functionally

By legal entity

A hierarchy is the rollup of a single dimension within the chart of accounts

Entity

BU

SBU

Segment

Item Group

Product Group

SKU

Function

Department

Account

Sub-Account

Cost

Rev

enue

Note: For each level in the planning hierarchy there is a separate cost hierarchy (shown here for BU)

Hierarchy

- 38 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

Dimensions are a core part of the data structure

Dimensions Description

Entity Stores cost center data

Product Includes products at which an organization budgets

Channel Stores distribution and sales channels

Customer Includes customers for which an organization budgets

Years Measures time by year

Time Periods Measures time by week, month, or quarter

Currency Stores currency of financial data

Scenarios Can be used to differentiate between budgets, forecasts, or historic actuals

Versions Supports multiple versions of the budget or forecast

Account Holds numeric amounts to store and calculate data. Includes statistical accounts that can be used for driver-based calculations

A sample list of dimensions:

- 39 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

The dimensions intersect to provide meaningful data

The intersection of all dimensions is where data is stored and calculated. For example, viewing the combination of the following dimensions gives the Budget version 2 January sale in US dollars for the Music Download Service sold to Jane Smith through the Direct Online channel

Entity: Premium Services

Product: Music Download Service

Channel: Direct Online

Customer: Jane Smith

Year: FY08

Time Period: January

Currency: USD

Scenario: BUD08

Version: v2

Account: Subscription Revenue

Other Performance Equipment

Sports Apparel Foot ware

base

ball

Hoc

key

Run

ning

Bas

ketb

all

Gol

f

Cha

nnel

s

Other Voice Services

Data Services Music Download

Com

pany

Sto

res

Ret

ail P

artn

ers

Kio

sks

Onl

ine

Part

ners

Dire

ct O

nlin

e

- 40 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

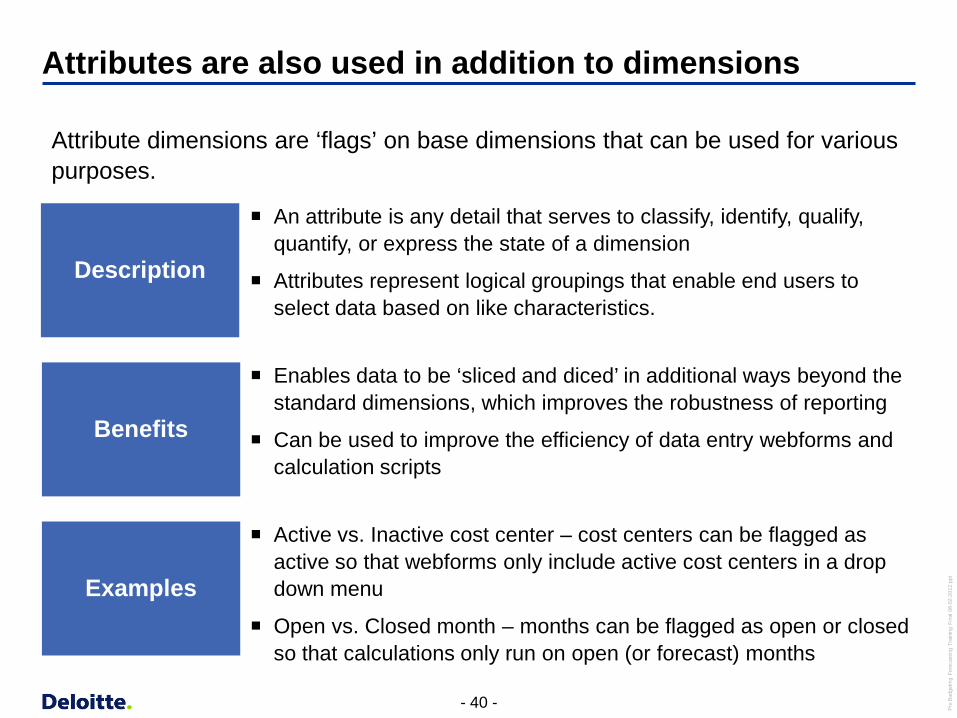

Attributes are also used in addition to dimensions

Description

An attribute is any detail that serves to classify, identify, qualify, quantify, or express the state of a dimension

Attributes represent logical groupings that enable end users to select data based on like characteristics.

Examples

Active vs. Inactive cost center – cost centers can be flagged as active so that webforms only include active cost centers in a drop down menu

Open vs. Closed month – months can be flagged as open or closed so that calculations only run on open (or forecast) months

Benefits

Enables data to be ‘sliced and diced’ in additional ways beyond the standard dimensions, which improves the robustness of reporting

Can be used to improve the efficiency of data entry webforms and calculation scripts

Attribute dimensions are ‘flags’ on base dimensions that can be used for various purposes.

- 41 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

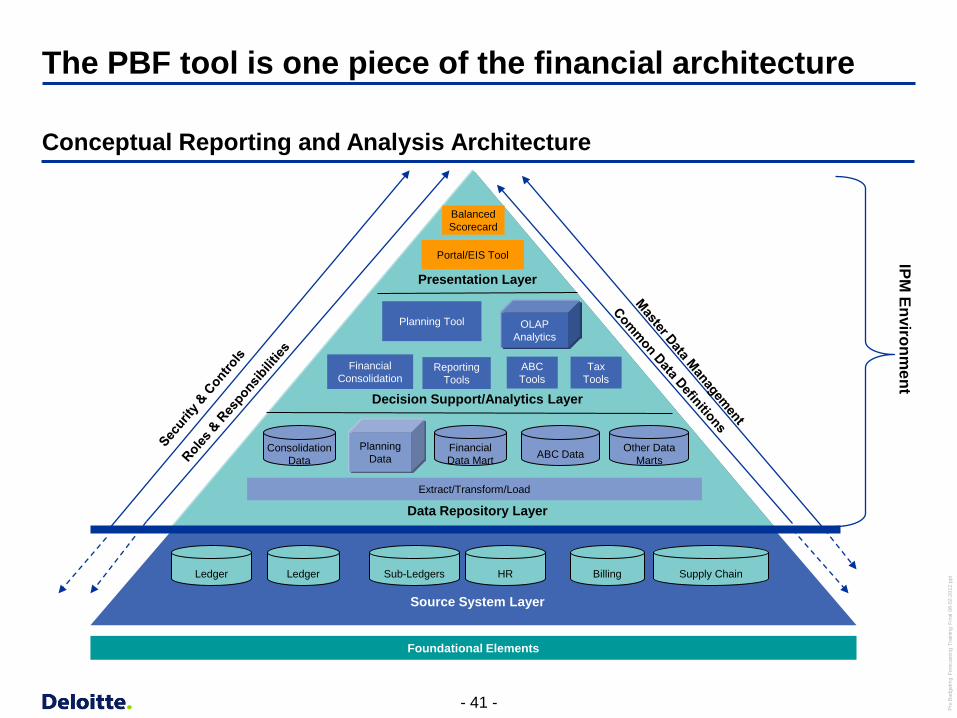

The PBF tool is one piece of the financial architecture

OLAP Analytics

Ledger Sub-Ledgers Billing Supply Chain Ledger

Planning Tool

Portal/EIS Tool

Financial Consolidation

Reporting Tools

Presentation Layer

Source System Layer

Data Repository Layer

Decision Support/Analytics Layer

HR

Extract/Transform/Load

Balanced Scorecard

Financial Data Mart

Other Data Marts ABC Data Consolidation

Data Planning

Data

ABC Tools

Foundational Elements

Tax Tools

IPM Environm

ent

Conceptual Reporting and Analysis Architecture

- 42 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

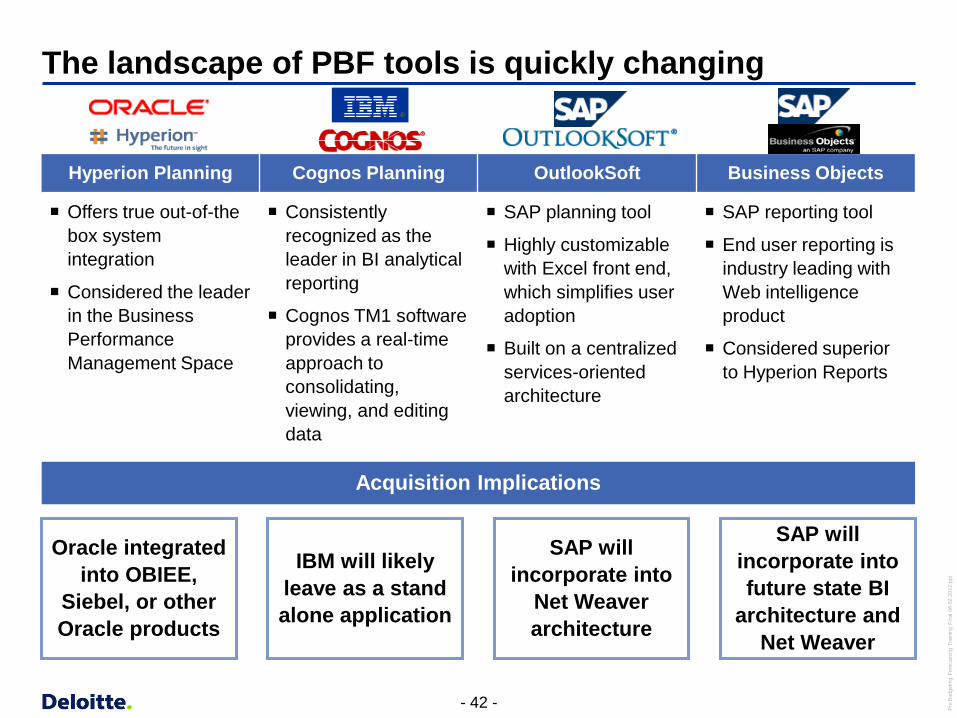

The landscape of PBF tools is quickly changing

Hyperion Planning Cognos Planning OutlookSoft Business Objects

Offers true out-of-the box system integration

Considered the leader in the Business Performance Management Space

Consistently recognized as the leader in BI analytical reporting

Cognos TM1 software provides a real-time approach to consolidating, viewing, and editing data

SAP planning tool

Highly customizable with Excel front end, which simplifies user adoption

Built on a centralized services-oriented architecture

SAP reporting tool

End user reporting is industry leading with Web intelligence product

Considered superior to Hyperion Reports

IBM will likely leave as a stand alone application

SAP will incorporate into

Net Weaver architecture

Oracle integrated into OBIEE,

Siebel, or other Oracle products

SAP will incorporate into future state BI

architecture and Net Weaver

Acquisition Implications

- 43 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

Exercise

- 44 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

Budget to Actuals Analysis

Instructions

Now that you understand the fundamentals of the PBF process, think about the information generated from the process.

Review the budget to actual variance handout. This is a sample variance analysis from a telecom company

Review the three highlighted variances

Consider the causes of the variances between budgeted and actual amounts. Consider all factors (internal and external), including the underlying driver of the revenue/cost

After five minutes, discuss your thoughts on the variances with the class

- 45 - Pru

Bud

getin

g Fo

reca

stin

g Tr

aini

ng F

inal

08-

02-2

012.

ppt

Q&A

Copyright © 2008 Deloitte Development LLC. All rights reserved.