34

ISSUE OF SHARES Presented by, K. Nagaveni 2 nd year MHA J.N. Medical college Belgaum 4/4/2015 1 K.Nagaveni

| Date post: | 14-Jul-2015 |

| Category: |

Business |

| Upload: | nagaveni-kandagal |

| View: | 58 times |

| Download: | 0 times |

ISSUE OF SHARES

Presented by,

K. Nagaveni

2nd year MHA

J.N. Medical college

Belgaum

4/4/2015 1K.Nagaveni

INTRODUCTION

As we are aware finance is the life blood of business. It

is of vital significance for modern business which

requires huge capital. Funds required for a business may

be classified as long term and short term. we have learnt

about short term finance. Finance is required for a long

period also. It is required for purchasing fixed assets like

land and building, machinery etc..

4/4/2015 2K.Nagaveni

Even a portion of working capital, which is required to

meet day to day expenses, is of a permanent nature. To

finance it we require long term capital. The amount of

long term capital depends upon the scale of business and

nature of business.

4/4/2015 3K.Nagaveni

Sources of long term finance

The main sources of long term finance are as follows:

1. Shares

2. Debentures

3. Public Deposits

4. Retained earnings

5. Term loans from banks

6. Loan from financial institutions

4/4/2015 4K.Nagaveni

SHARES

Definition: shares can be defined as one of the units into which

the share capital of a company has been divided.

According to section 2 (46) of the companies Act, “a share is the

share in the capital of a company and includes stock except where

a distinction between stock and share is expressed or implied.”

The person holding the share is known as shareholder . He

receives dividend from the company as a consideration for

investing his money into the company.

4/4/2015 5K.Nagaveni

4/4/2015 K.Nagaveni 6

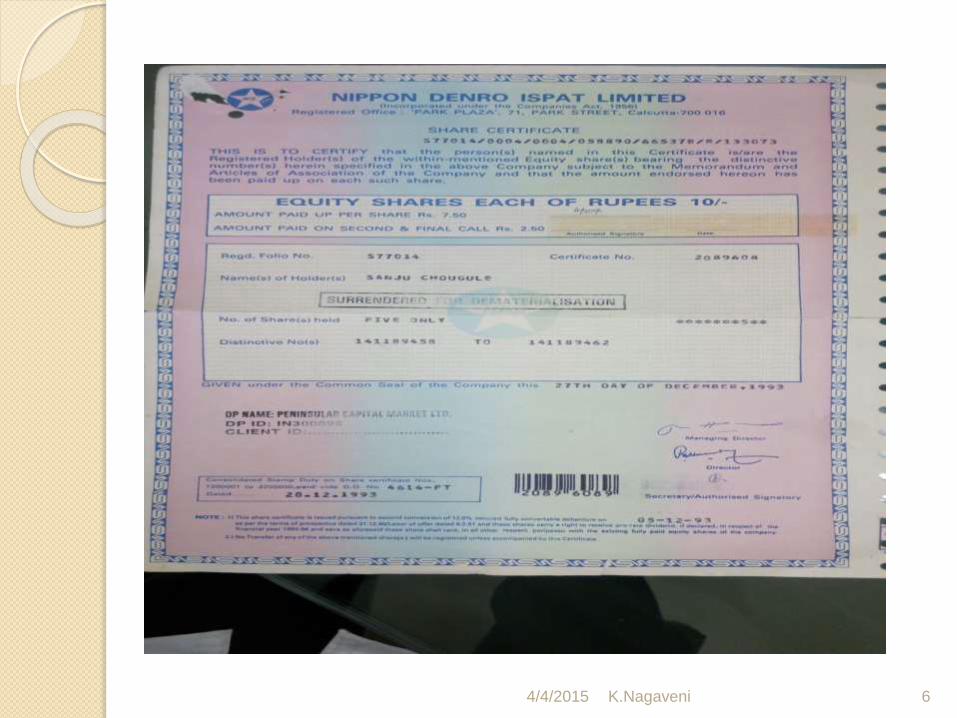

Sealing and Signing of Certificate.-

Every share certificate shall be issued under the seal of the

company, which shall be affixed in the presence of

(i) two directors or persons acting on behalf of the directors

under a duly registered power-of-attorney ; and

(ii) the secretary or some other person appointed by the

Board for the purpose. The two directors or their attorneys

and the secretary or other person shall sign the share

certificate.

4/4/2015 K.Nagaveni 7

Common Seal

The company Act 1960 (revised) requires affixation of the common

seal on certain documents, share certificates and share warrants issued

by the company.

The common seal should be adopted by a resolution of the Board.

The impression of the common seal should be made part of the minutes

of the meeting in which it is adopted.

The common seal should be made of metal and capable of being

manually operated.

The common seal should have the name of the company and state in

which the registered office is situated engraved in legible characters.

4/4/2015 K.Nagaveni 8

Terms of issues

Shares can be issued at par or at a premium or

at a discount.

Shares are said to be issued at par when a

shareholder is required to pay the face value of

the shares of the company.

For ex: when shares of Rs .10 are issued at Rs

.10 ,these are said to be issued at a face value.

4/4/2015 K.Nagaveni 9

Shares are said to be issued at a premium when shareholder

is required to pay more than the face value to the company.

For ex: if shares of Rs.10 are issued at Rs.12, then

shares are said to be issued at a premium.

Shares are said to be at discount when the shareholder is

required to pay less amount than the face value of the shares

to the company.

For ex: when the shares of RS.10 are issued at Rs.9,

the shares are said to be issued at a discount.

4/4/2015 K.Nagaveni 10

The issue of share amount can be received in one

instalment or it can be spread over different

instalment. The amount when received in different

instalments may be paid on application, allotments or

in different calls.

The amount which received on application called the

application money and the amount which becomes

due on allotment is called allotment money.

4/4/2015 K.Nagaveni 11

Issue of shares

Issue of shares is the main source of long term finance.

Shares are issued by joint stock companies to the public.

A company divides its capital into units of a definite face

value, say of Rs. 10 each or Rs. 100 each. Each unit is

called a share. A person holding shares is called a

shareholder.

4/4/2015 12K.Nagaveni

Shares can be issued at par, premium or discount. There are

no restrictions regarding issue of shares at par. However , for

issue of shares t premium or discount , a company has to

follow the restrictions imposed by the Companies Act ,1956 .

These restrictions are as follows:

Issue of shares at premium: a company can always issue a

shares at a premium i.e. for a value higher than the face

value of shares whether for cash or for consideration other

than cash . However , according section 78 of the companies

act , the amount of such premium shall have to be transferred

by the company to the securities premium account.

4/4/2015 K.Nagaveni 13

Securities of the premium can be used by the company only

for the following purposes:

a)For the issue fully paid bonus shares to the members of the

company,

b)For writing off preliminary expenses of the company,

c)For writing off the expenses of, or the commission paid or

discount allowed, on any issue of shares or debentures of the

company.

d) For providing premium payable on the redemption of any

redeemable preference shares or debentures of the company.

4/4/2015 K.Nagaveni 14

Issue of shares at discount: A company can issue shares at a discount , subject

to the following conditions laid down by section 79 of the companies act .

A)Shares to be issued at a discount must be of a class already issued.

B) Issue of shares at a discount must be authorised by an ordinary resolution of

the company;

c)Issue must be sanctioned by the company Law board;

d)Resolution must specify the maximum rate of discount.

e)One year must have passed since the date on which the company was allowed to

commence business.

f)Every prospectus relating to the issue of shares shall disclose particulars of the

discount allowed on the issue of shares or that amount which has not been

written at the date of the issue of prospectus.

4/4/2015 K.Nagaveni 15

Characteristics of shares

1. It is a unit of capital of the company

2.Each share is of a definite face value.

3. A share certificate is issued to a shareholder indicating

the number of shares and the amount.

4. Each share has a distinct number.

5. The face value of a share indicates the interest of a

person in the company and the extent of his liability.

6. Shares are transferable units

4/4/2015 16K.Nagaveni

Investors are of different habits and temperaments.

Some want to take lesser risk and are interested in a

regular income. There are others who may take greater

risk in anticipation of huge profits in future. In order to

tap the savings of different types of people, a company

may issue different types of shares. These are:

1. Preference shares, and

2. Equity Shares.

4/4/2015 17K.Nagaveni

Preference Shares

Preference Shares are the shares which carry preferential

rights over the equity shares. These rights are

Receiving dividends at a fixed rate,

Getting back the capital in case the company is wound-

up.

Investment in these shares are safe, and a preference

shareholder also gets dividend regularly.

4/4/2015 18K.Nagaveni

Types of preference shares

1. Cumulative preference shares: if the company does not earn

adequate profit in any year, dividends on preference shares

may not be paid for that year . But if the preference shares are

cumulative such unpaid dividends are treated as arrears and

can b carried and forward to subsequent years.

2. Non – cumulative preference shares: The holders of these

shares no doubt will get a preferential right in getting a fixed

capital dividend before it is distributed to equity share holders

4/4/2015 19K.Nagaveni

3.Redeemable preference shares: capital raised through

the issue of redeemable preference shares is to be paid

back by the company to such shareholders after the

expiry of a stipulated period, whether the company is

wound up or not.

4/4/2015 20K.Nagaveni

4.Particiapting or non participating preference shares: the

preference shares which are entitled to share in the surplus

profit of the company in addition to the fixed rate of

preference dividend are known as participating preference

shares.

The participating preference shareholders obtain return on their

capital in two forms: 1)fixed dividend

2)share in excess of profits.

Those preference shares which don’t carry the rights of share

in excess profits are known as non participating preference

shares.

4/4/2015 21K.Nagaveni

Equity Shares

Equity shares are shares which do not enjoy any

preferential right in the matter of payment of dividend or

repayment of capital. The equity shareholder gets

dividend only after the payment of dividends to the

preference shares. There is no fixed rate of dividend for

equity shareholders. The rate of dividend depends upon

the surplus profits.

4/4/2015 22K.Nagaveni

In case of winding up of a company, the equity share

capital is refunded only after refunding the preference

share capital. Equity shareholders have the right to take

part in the management of the company. However,

equity shares also carry more risk.

4/4/2015 23K.Nagaveni

Merits of equity shares

(A) To the shareholders

1. In case there are good profits, the company pays

dividend to the equity shareholders at a higher rate.

2. The value of equity shares goes up in the stock market

with the increase in profits of the concern.

3. Equity shares can be easily sold in the stock market.

4. Equity shareholders have greater say in the management

of a company as they are conferred voting rights by the

Articles of Association.

4/4/2015 24K.Nagaveni

To the Management:

1. A company can raise fixed capital by issuing equity shares

without creating any charge on its fixed assets.

2. The capital raised by issuing equity shares is not required to

be paid back during the life time of the company. It will be

paid back only if the company is wound up.

3. There is no liability on the company regarding payment of

dividend on equity shares. The company may declare

dividend only if there are enough profits.

4. If a company raises more capital by issuing equity shares, it

leads to greater confidence among the investors and creditors.

4/4/2015 25K.Nagaveni

Demerits

A)To the shareholders

1)Uncertainly about payment of dividend:

Equity share-holders get dividend only when the

company is earning sufficient profits and the Board of

Directors declare dividend.

If there are preference shareholders, equity shareholders

get dividend only after payment of dividend to the

preference shareholders.

4/4/2015 26K.Nagaveni

2)Speculative:

Often there is speculation on the prices of equity shares.

This is particularly so in times of boom when dividend

paid by the companies is high.

3)Danger of over– capitalization:

In case the management miscalculates the long term

financial requirements, it may raise more funds than

required by issuing shares. This may amount to over-

capitalization which in turn leads to low value of shares

in the stock market.

4/4/2015 27K.Nagaveni

4)Ownership in name only :

Holding of equity shares in a company makes the holder

one of the owners of the company. Such shareholders

enjoy voting rights. They manage and control the

company. But then it is all in theory. In practice, a

handful of persons control the votes and manage the

company. Moreover, the decision to declare dividend

rests with the Board of Directors.

4/4/2015 28K.Nagaveni

5)Higher Risk :

Equity shareholders bear a very high degree of risk. In

case of losses they do not get dividend. In case of

winding up of a company, they are the very last to get

refund of the money invested. Equity shares actually

swim and sink with the company.

4/4/2015 29K.Nagaveni

B)To the Management:

1)No trading on equity :

Trading on equity means ability of a company to raise funds

through preference shares, debentures and bank loans etc. On such

funds the company has to pay at a fixed rate. This enables equity

shareholders to enjoy a higher rate of return when profits are large.

The major part of the profit earned is paid to the equity

shareholders because borrowed funds carry only a fixed rate of

interest. But if a company has only equity shares and does not

have either preference shares, debentures or loans, it cannot have

the advantage of trading on equity.

4/4/2015 30K.Nagaveni

2)Conflict of interests :

As the equity shareholders carry voting rights, groups

are formed to corner the votes and grab the control of

the company. There develops conflict of interests

which is harmful for the smooth functioning of a

company.

4/4/2015 31K.Nagaveni

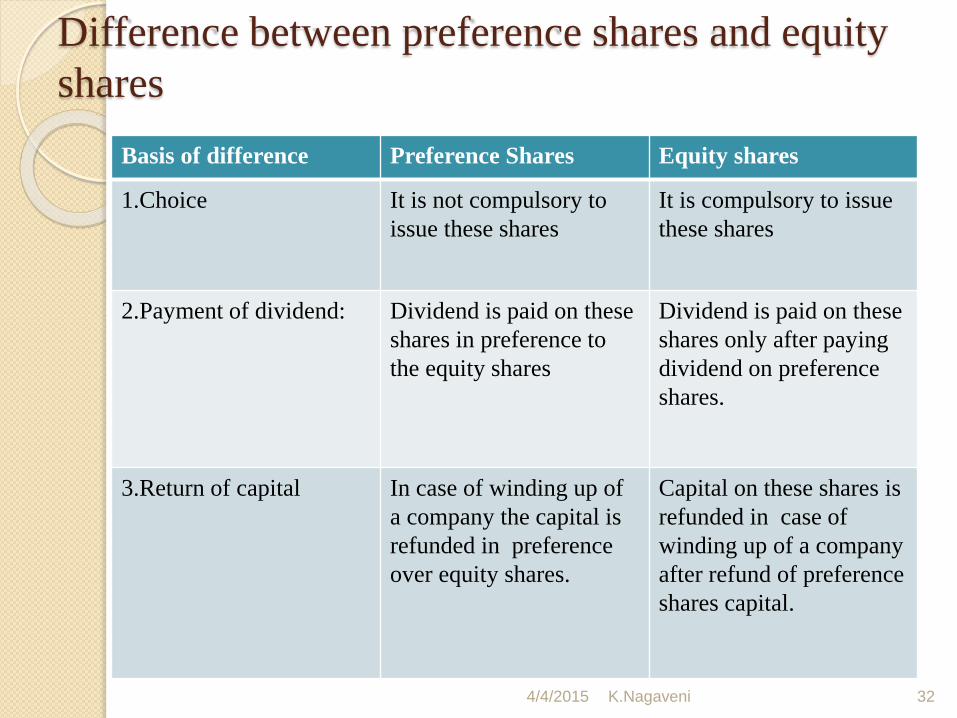

Difference between preference shares and equity

shares

Basis of difference Preference Shares Equity shares

1.Choice It is not compulsory to

issue these shares

It is compulsory to issue

these shares

2.Payment of dividend: Dividend is paid on these

shares in preference to

the equity shares

Dividend is paid on these

shares only after paying

dividend on preference

shares.

3.Return of capital In case of winding up of

a company the capital is

refunded in preference

over equity shares.

Capital on these shares is

refunded in case of

winding up of a company

after refund of preference

shares capital.

4/4/2015 32K.Nagaveni

References:

Sources of Long-term Finance –pdf

Financial management - Dr.S.N Maheshwari

Advanced accountancy – S.P.jain , K.L.Narang

4/4/2015 33K.Nagaveni

THANK YOU…..

4/4/2015 34K.Nagaveni