53

| Date post: | 10-Apr-2018 |

| Category: |

Documents |

| Upload: | jointariqaslam |

| View: | 219 times |

| Download: | 0 times |

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 1/53

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 2/53

Finance Bill 2010

This Memorandum summarizes an overview of economy for the year 2009-2010 and the important

changes proposed through the Finance Bill, 2010. It contain comments on the budget and on the

Finance Bill 2010, including Highlights, on the changes brought through the Income Tax Ordinance,

2001, the Sales Tax Act, 1990, the Federal Excise Act, 2005, the Custom Act, 1969, the Finance Act,

1989 and the Petroleum Products (surcharge) Ordinance, 1961. The amendments proposed through

the Income Tax Ordinance, 2001 and through other laws are intended to be effective once the

parliament has accorded it’s assent and thereafter, would be effective from July 01, 2010 i.e. tax

year 2011 unless otherwise indicated. Whereas certain provisions relating to income tax, custom duty,

excise duty and sales tax have been made applicable from June 05, 2010.

This Memorandum is intended to provide general guidance to the readers on the important changesbrought through the Bill and should not be considered as a substitute for specific advice relating to a

particular enactment. For considering the precise effect of a proposed change, reference should be

made to the appropriate wordings in the relevant statute and the notifications issued where relevant.

The Memorandum has been prepared exclusively for the use of our clients and staff , based

on information available with us till the time giving it for printing. Printing of this Memorandum, in any

manner, is strictly prohibited without seeking a written permission from the firm.

Anjum Asim Shahid Rahman

Chartered Accountants

June 06, 2010

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 3/53

Table of Contents

Budget at a glance 1

Overview of Economy 2009-2010 2

The Finance Bill 2010 – Highlights 7

Summary of changes in:

The Income Tax Ordinance, 2001 11

The Sales Tax Act, 1990 36

The Federal Excise Act, 2005 40

The Custom Act, 1969 43

The Petroleum Products (surcharge) Ordinance, 1961 46

Other laws 48

The Provisional collection of Taxes Act, 1931 49

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 4/53

Budget at a Glance

1

(Rupees in billion)2010-2011 2009-2010 2010-2011 2009-2010

% %RECEIPTS

RevenueTax 1,779 1,513 64% 61%Non tax 632 514 23% 21%Gross 2,411 2,027 87% 82%Less: Provincial share 1,034 655 37% 26%Net revenue receipts 1,377 1,372 50% 56%

OtherNet capital receipts 325 190 12% 7%External receipts 387 510 14% 20%

Self financing of PSDP by provinces 342 173 12% 7%Changes in provincial cash balance 167 73 6% 3%Privatization proceeds - 19 - 1%Bank borrowings 167 145 6% 6%

1,338 1,110 50% 44%TOTAL RECEIPTS 2,765 2,482 100% 100%

EXPENDITURES

CurrentGeneral public service 1,388 1,189 50% 48%Defence affairs and services 442 343 16% 14%Public order safety affair 51 35 2% 1%Economic affairs 67 85 2% 3%Environment protection - - - -Housing and community 2 1 0% 0%Health affairs and services 7 7 0% 0%Recreational and culture services 4 4 0% 0%Education affairs services 35 31 1% 1%Social protection 2 4 0% 0%Total current expenditures 1,998 1,699 71% 68%

Development

PSDPFederal government 290 446 11% 18%Provincial government 373 200 14% 8%Estimated operational shortfall (20) (20) (1)% (1%)Other development expenditures 124 157 5% 6%Total development expenditures 767 783 29% 32%

TOTAL EXPENDITURES 2,765 2,482 100% 100%

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 5/53

Overview of Economy 2009-2010

2

Economic Review

GDP Growth Rate – growth despite downturn

• Pakistan’s economic growth experienced a significant slowdown in previous years however marked improvement witnessed in 2009-10 with significant increase in growth rate on the back of effective economic measures

• Major challenges to sustain growth trends continue to be :

Cumulative policy-induced macro-economic imbalances

Deterioration in Pakistan’s net external terms of trade

Continuation of global financial crisis more particularly Europe resulting in reduced externaldemand for exports

Non-availability of external capital to finance its current account and fiscal deficits

• The Government continues to proactively seek external assistance to support Pakistan’s economywith both military and economic aid as well as seeking better terms with multilateral financialinstitutions

• Per capita income trends reflecting similar patterns of growth and improvement on the back of improved economic growth rates

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 6/53

Overview of Economy 2009-2010

3

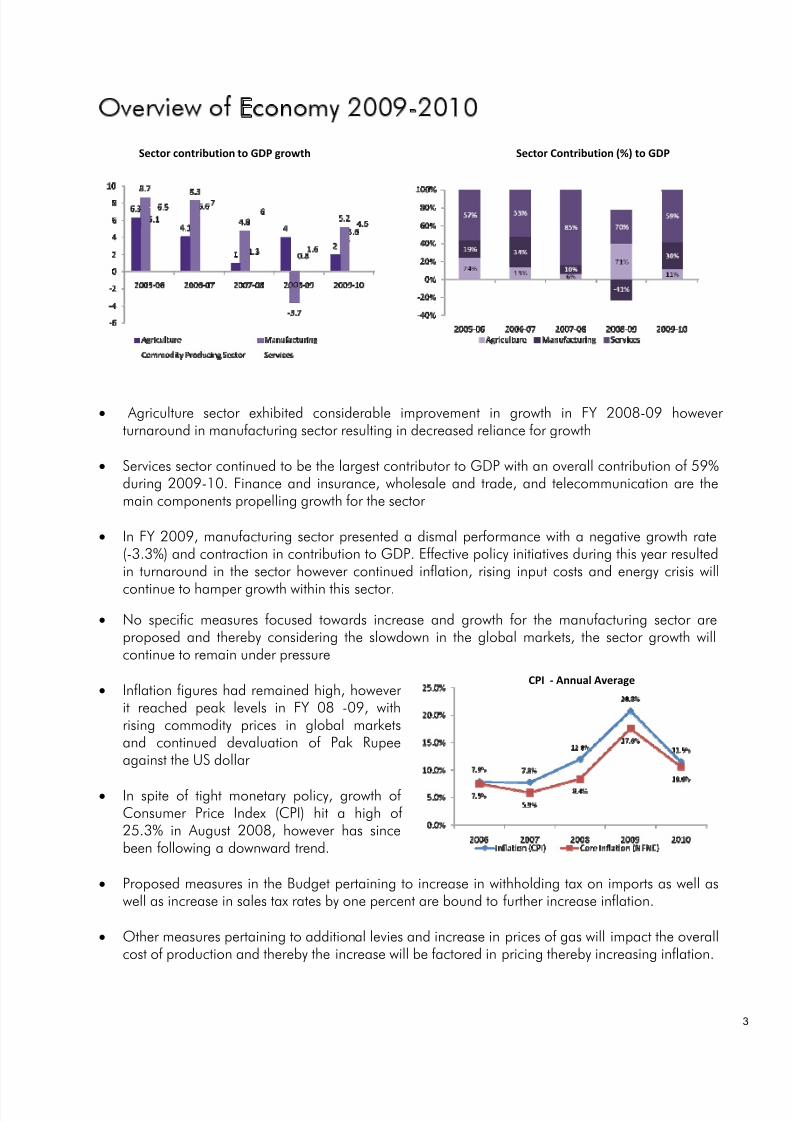

• Agriculture sector exhibited considerable improvement in growth in FY 2008-09 however turnaround in manufacturing sector resulting in decreased reliance for growth

• Services sector continued to be the largest contributor to GDP with an overall contribution of 59%during 2009-10. Finance and insurance, wholesale and trade, and telecommunication are themain components propelling growth for the sector

• In FY 2009, manufacturing sector presented a dismal performance with a negative growth rate(-3.3%) and contraction in contribution to GDP. Effective policy initiatives during this year resultedin turnaround in the sector however continued inflation, rising input costs and energy crisis will

continue to hamper growth within this sector.• No specific measures focused towards increase and growth for the manufacturing sector are

proposed and thereby considering the slowdown in the global markets, the sector growth willcontinue to remain under pressure

• Inflation figures had remained high, however it reached peak levels in FY 08 -09, withrising commodity prices in global marketsand continued devaluation of Pak Rupeeagainst the US dollar

• In spite of tight monetary policy, growth of Consumer Price Index (CPI) hit a high of 25.3% in August 2008, however has sincebeen following a downward trend.

• Proposed measures in the Budget pertaining to increase in withholding tax on imports as well aswell as increase in sales tax rates by one percent are bound to further increase inflation.

• Other measures pertaining to additional levies and increase in prices of gas will impact the overallcost of production and thereby the increase will be factored in pricing thereby increasing inflation.

Sector contribution to GDP growth Sector Contribution (%) to GDP

CPI ‐ Annual Average

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 7/53

Overview of Economy 2009-2010

4

• The current account after having shown

continuous expansion in previous years,contracted considerably in FY 09 and FY 10.Improvement in trade balance supported bystrong growth in remittances allowedcontraction in current account deficit.

• With economic activity showing gradualrecovery, imports are expected to rise with apick up in domestic demand, revival of largescale manufacturing sector and resolution of circular debt problem would supportproduction activities in energy sector.

• Current Account balance is expected toremain negative in near future with exportsbeing expected to grow at an anemic ratehowever improvements in global markets mayhelp ease pressure of the current accountbalance .

• Continued increase in external debt in pasttwo years implies an increase in the currentaccount and fiscal deficit.

• Proactive seeking of external funding by thegovernment for the stabilization program,both from the IMF, other IFIs and bilateralsources, has also raised the external debt.

• Moreover, reliance on external funding isfurthered by lack of privatization initiatives bythe government. The futile attempts of privatization of strategic assets by the previousgovernment at unfavorable terms, was being

used for funding the current account balanceby the previous government.

Current Account Balance

Total External Debt

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 8/53

Overview of Economy 2009-2010

5

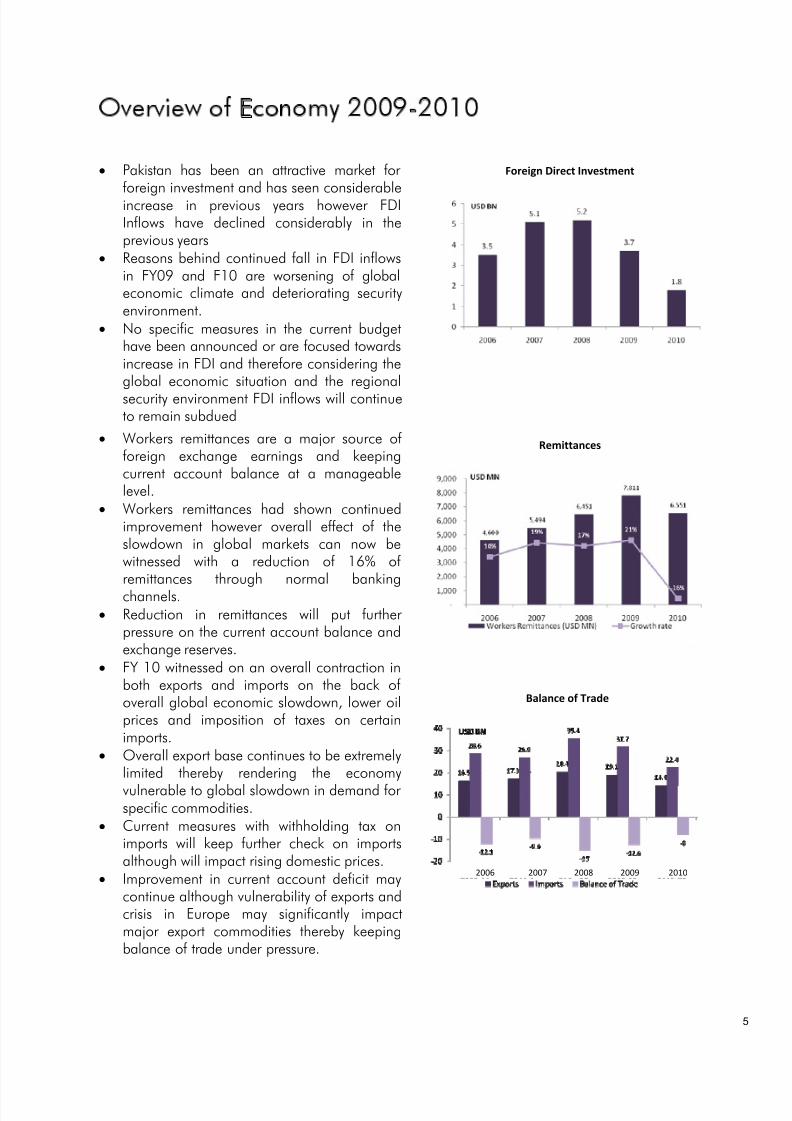

• Pakistan has been an attractive market for

foreign investment and has seen considerableincrease in previous years however FDIInflows have declined considerably in theprevious years

• Reasons behind continued fall in FDI inflowsin FY09 and F10 are worsening of globaleconomic climate and deteriorating securityenvironment.

• No specific measures in the current budgethave been announced or are focused towardsincrease in FDI and therefore considering theglobal economic situation and the regionalsecurity environment FDI inflows will continueto remain subdued

• Workers remittances are a major source of foreign exchange earnings and keepingcurrent account balance at a manageablelevel.

• Workers remittances had shown continuedimprovement however overall effect of theslowdown in global markets can now bewitnessed with a reduction of 16% of remittances through normal bankingchannels.

• Reduction in remittances will put further pressure on the current account balance andexchange reserves.

• FY 10 witnessed on an overall contraction inboth exports and imports on the back of overall global economic slowdown, lower oilprices and imposition of taxes on certainimports.

• Overall export base continues to be extremelylimited thereby rendering the economyvulnerable to global slowdown in demand for specific commodities.

• Current measures with withholding tax onimports will keep further check on importsalthough will impact rising domestic prices.

• Improvement in current account deficit maycontinue although vulnerability of exports andcrisis in Europe may significantly impactmajor export commodities thereby keepingbalance of trade under pressure.

Balance of Trade

Foreign Direct Investment

Remittances

2006 2007 2008 2009 2010

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 9/53

Overview of Economy 2009-2010

6

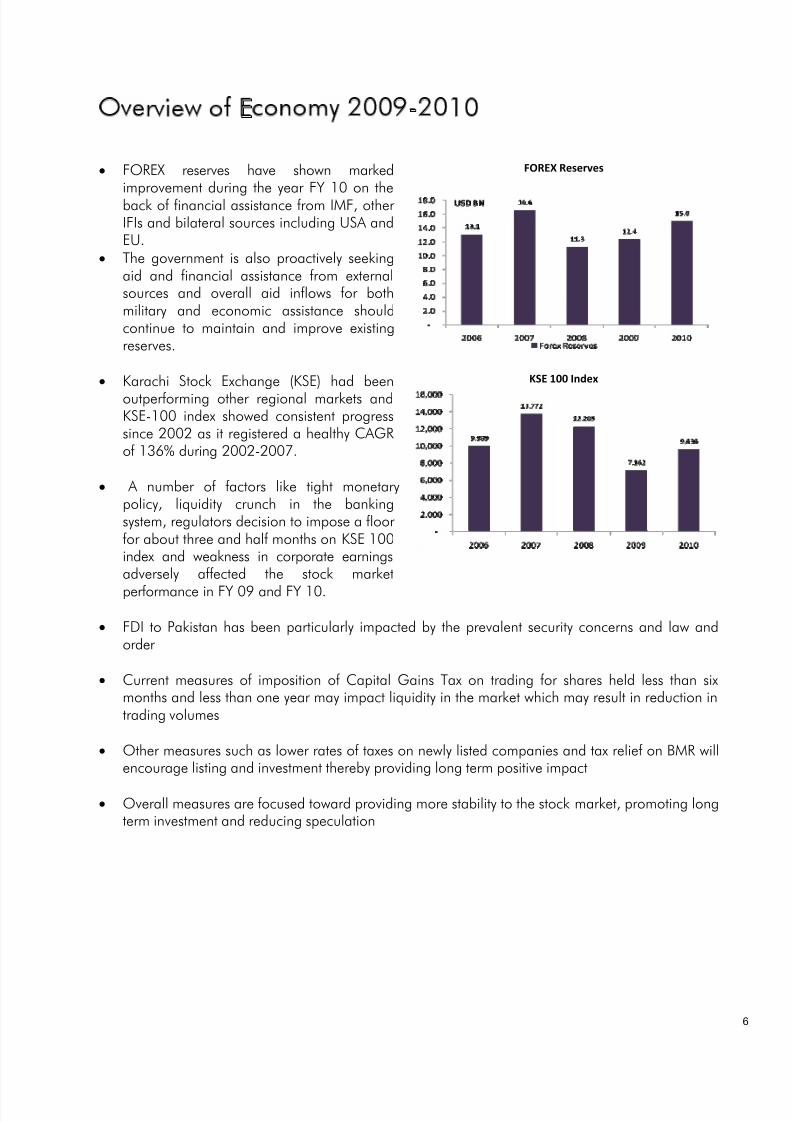

• FOREX reserves have shown marked

improvement during the year FY 10 on theback of financial assistance from IMF, other IFIs and bilateral sources including USA andEU.

• The government is also proactively seekingaid and financial assistance from externalsources and overall aid inflows for bothmilitary and economic assistance shouldcontinue to maintain and improve existingreserves.

FOREX Reserves

• Karachi Stock Exchange (KSE) had beenoutperforming other regional markets andKSE-100 index showed consistent progresssince 2002 as it registered a healthy CAGRof 136% during 2002-2007.

• A number of factors like tight monetarypolicy, liquidity crunch in the bankingsystem, regulators decision to impose a floor for about three and half months on KSE 100index and weakness in corporate earningsadversely affected the stock marketperformance in FY 09 and FY 10.

KSE 100 Index

• FDI to Pakistan has been particularly impacted by the prevalent security concerns and law andorder

• Current measures of imposition of Capital Gains Tax on trading for shares held less than sixmonths and less than one year may impact liquidity in the market which may result in reduction intrading volumes

• Other measures such as lower rates of taxes on newly listed companies and tax relief on BMR willencourage listing and investment thereby providing long term positive impact

• Overall measures are focused toward providing more stability to the stock market, promoting longterm investment and reducing speculation

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 10/53

Finance Bill 2010 - Highlights

7

Income Tax

• The basic threshold of total income not liable to tax is proposed to be enhanced from the presentlimit of Rs.200,000 to Rs.300,000 in respect of salaried taxpayers whereas in respect of non-salaried taxpayers, such limit is proposed to be increased from Rs.100,000 to Rs.300,000

• The rate of advance tax deductible from monthly electricity bills of commercial or industrialconsumers is proposed to be reduced from 10% to 5%

• The income of senior citizens of the age of 60 years or more are currently enjoying reduction intax liability by 50% provided their total income does not exceed Rs.750,000. This threshold isproposed to be increased to Rs.1,000,000. However, this relief shall not be available on incomewhich is subject to final tax regime

• In pursuance of Prime Minister’s Relief Package to rehabilitate the economy of Khyber Paktunkhwa, FATA and PATA, some amendments are proposed to be introduced in the IncomeTax Ordinance. These measures provide following reliefs to industrial and commercial taxpayershailing from most and moderately affected areas, which are summarized as under:

waiver of entire amount of default surcharge & penalties till June 30, 2010 subject to paymentof the principal dues;

exemption from withholding tax on electricity bills for the tax years 2010 and 2011;

exemption from withholding tax on exports; and

exemption from advance tax on import of plant and machinery up to June 30, 2011;

However these concessions shall not be available to the manufacturers and suppliers of cement,sugar, beverages and cigarettes industries

• It is proposed not to tax perquisites on account of loan availed at concessional rates where theemployee does not take interest on deposit with the employer.

• A tax credit @ 10% of the tax payable is proposed to be allowed to a listed company in thepurchase of a plant and machinery for installation or for the purposes of BMR in an industrialundertaking upto the year June 30, 2015;

• A tax credit equal to 5% of the tax payable is proposed to be allowed to a company in the taxyear of its enlistment in any registered stock exchange in Pakistan as a measure of encouragement.

• A 10% withholding tax deducted on government securities, PIBs and other debt instrument isproposed to be a final tax on such income including in the hands of companies.

• For providing incentive to foreign lenders for tax-free repatriation of profits earned on foreignindustrial loans, Clause 72(iii) of Part-IV of Second Schedule to the Income Tax Ordinance 2001is proposed to be re-introduced.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 11/53

Finance Bill 2010 - Highlights

8

• The maximum rate of withholding tax on payments made to the non-resident taxpayers which arenot subject to Avoidance of Double Taxation Treaties (other than payments made on account of royalty, fee for technical services and payment subject to withholding of tax u/s 152 of theOrdinance is proposed to be reduced to @ 20% as against@ 30% currently applicable.

• The rate of withholding tax @ 20% currently applicable on cross-word puzzles, prizes, raffle andwinnings on quiz is proposed to be reduced to 10%;

• A flat rate of tax for AOPs is proposed to be @ 25% of their taxable income. AOPs were earlier taxed at progressive rates with a maximum rate of tax @ 25% of total income.

• Advance tax deductible on imports made by commercial importers is proposed to be increased to@5% as against 4% earlier being final tax liability.

• Capital gains on the sale of shares of listed companies held for less than one year are proposedto be brought under the tax regime at varied rates.

• Advance tax deductible on goods transport vehicles is proposed to be charged to tax @ Re.1 per kilogram of the laden weight capacity of goods transport vehicle instead of subject to tax at slabrates.

• In addition to cash withdrawals from banks, various banking transactions including modes likewithdrawals through Demand Draft, Pay Order, Online Transfer, Telegraphic Transfer, TDR, CDR,STDR and RTC, are proposed to be subject to withholding of tax with an enhanced rate of withholding @ 0.3%.

• Turnover tax on loss making companies is proposed to be enhanced to @ 1% as against @0.5%earlier. Individuals and AOP having turnover of Rs. 50,000,000 or more are also proposed to besubject to levy of minimum tax @1% of the turnover.

• Withholding tax on gross value of inland air ricket is proposed @ 5% adjustable in nature.

• The mandatory requirement of filing of wealth statement along with its reconciliation thereof isproposed by the taxpayers being assessed under the fixed tax regime with yearly tax increasing toRs.35, 000 as against a threshold of Rs. 20,000 earlier

• In order to enhance the categories of withholding tax agents, persons made responsible towithhold tax at source being ‘Prescribed Persons’. Individuals with turnover of Rs.50 millions or above is also proposed to be included in the category of prescribed person responsible towithhold tax at source.

• Income from rental income is proposed to be outside the ambit of final tax regime. The tax rateson rental income, however, remained unchanged

• Advance tax on capital gains is proposed to be payable on the transactions of listed securities ona quarterly basis.

• Monthly withholding tax reporting are proposed to be substituted with e-filing of quarterly

statements.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 12/53

Finance Bill 2010 - Highlights

9

On merger of Investment Corporation of Pakistan with Industrial Development Bank, the exemptionavailable to ICP on dividend income is proposed to be withdrawn.

• Exemption under clause (52) of Part-IV of the Second Schedule to the Income Tax Ordinance2001 available to Vanaspati Ghee or Oil is proposed to be withdrawn, in view of demise of SRO.593(I) 1991 Dated 30 th June 1991.

Sales Tax Act, 1990

• Enhancement in the general rate of sales tax from 16% to 17%

• Increase in tax rate on import of soyabean seed by solvent extraction industries from 6% to 7%

• Enhancement in rate of tax on import of rapeseed by solvent extraction industries from 14% to

15%• Automatic enhancement of rate of tax on supply of natural gas by gas companies from existing

25% to 26%

• Withdrawal of powers of Commissioner to delegate his authority to subordinate officers

• Commissioner, in addition to Board, is authorized to appoint a chartered accountant, a costaccountant to conduct audit. Similarly, Commissioner can also authorize any officer to have freeaccess to business premises

Federal Excise Act, 2005

• Increase in rate of Federal Excise Duty on Natural Gas from Rs. 5.09 per MMBTu to Rs. 10 per MMBTu

• Upward revision of Federal Excise Duty on cigarettes

• Levy of Federal Excise Duty @ Rs. 1 per filter rod of cigarettes

• Levy of 10% Federal Excise Duty on electricity intensive home appliances

• Withdrawal of restriction on adjustment of Federal Excise Duty paid on beverage concentrateenforced through notification

Customs Act, 1969

• Reduction of customs duty on crude palm oil from Rs.9,000 MT to Rs.8,000 MT

• Exemption of customs duty on import of photographic plates and film for X-ray to reduce the costof medical diagnoses for general public

• Reduction of duty to 5% on pharmaceutical raw materials and drugs

• Reduction of duty on equipment for dedicated use of renewable energy to encourage use of

renewable energy resources

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 13/53

Finance Bill 2010 - Highlights

1 0

• Reduction of duty on raw materials for laundry soap and detergent

• Concession of customs duty on import of Road Sweeping Lorries to increase efficiency of municipal and local governments

• Exemption of customs duty on import of fully dedicated LPG buses and dispensing equipment toencourage use of cheaper environment friendly fuel

• Exemption of customs duty on import of raw materials/components for energy saving lamps tosupport local manufacturers

• Exemption of customs duty and sales tax on rice processing machinery to boost value additionand export of rice

• Reduction of duty on raw materials of leather and glass industries

• Reduction of duty on secondary quality tin mill black plate for manufacturers of tin plate to reducetheir manufacturing cost

• Exemption of duty on milk filters to support dairy industry

• Rationalization of duty on glucose and glucose syrup, adhesives and. prepared industrial colours,

• Inclusion of LED T.V. in industry specific concessionary regime to encourage local manufacturing

• Levy of 5% concessionary duty on copper & aluminum tubes and electro galvanized steel sheets

• Valuation formula for export simplified by including regulatory duty instead of export duty insection 25

• The value determined by custom officer to be applicable until and unless the same is revised,superseded or rescinded by the competent authority

• Concept of review application before Director General Valuation introduced against valuesdetermined by Director Valuation or Collector of Customs. Application is required to be filedwithin time period of 30 days from the date of determination of customs value. Such review order is subject to appeal before Appellate Tribunal

• To curb the tendency of misdeclaration in self assessment, appropriate measures introduced

• Facility of filing of goods declaration after examining the goods is now restricted to used goodsonly

• Time limit imposed to finalize the cases of provisional assessment within three months

• General penalty rate enhanced to Rs.50,000

• Enhancement of penalty to the extent of twice the value of the offending goods besides theconfiscation of goods for violation of Section 128 and 129 of Customs Act, 1969

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 14/53

Summary of changes in theIncome Tax Ordinance, 2001

1 1

Section

Tax Administration

Through Presidential Ordinance, Internal Revenue Services (IRS) has been created.The Federal Board of Revenue (FBR) is undergoing a comprehensive program of taxadministration reforms. The tax reforms program envisaged a functionally integratedtax administration of Sales Tax, Federal Excise and Direct Tax.

2, 205, 207,208, 209,210, 211,215, 217,239, 239B

With this background, the Finance Amendment Ordinance, 2009 was Promulgatedon October 28, 2009 by the President of Pakistan. As the same could not beapproved by the National Assembly, it expired after four months. After its expiry, theFederal Government has intended to re-promulgate the Finance Ordinance, 2010but failed. Instead of presenting this Ordinance separately for approval andadoption by the National Assembly, the changes stipulated thereon, are nowproposed to be made as part of this bill. The changes relate to, wherever considerednecessary, renaming institutions as well as re-designating the tax authorities given inthe Income Tax Ordinance, 2001. These are now proposed to be modified with aview to harmonize functions whereby an Officer of Inland Revenue is able toexercise powers under the aforementioned laws.

Existing Proposed(i) Bodies

Income Tax Appellate Tribunal

(ii) Tax Authorities

Appellate Tribunal Inland Revenue

Central Board of Revenue Board

Regional Commissioner of IncomeTax

Chief Commissioner Inland Revenue

Commissioner of Income Tax Commissioner Inland Revenue

Commissioner of Income Tax(Appeals)

Commissioner Inland Revenue(Appeals)

Additional Commissioner InlandRevenueDeputy Commissioner InlandRevenue

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 15/53

Summary of changes in theIncome Tax Ordinance, 2001

1 2

Section

Existing Proposed

Assistant Commissioner InlandRevenue

Taxation Officer Officer Inland Revenue

Special Officer Inland Revenue.

Inspector Inland Revenue

(iii) Terminology

Additional tax Default surcharge

A new clause is proposed to be inserted in section 2 which provides for thedefinition of ‘Officer of Inland Revenue’. This is to mean any AdditionalCommissioner Inland Revenue, Deputy Commissioner Inland Revenue, AssistantCommissioner Inland Revenue, Officer Inland Revenue, Special Officer InlandRevenue or any other officer, however designated, or appointed by the Board.

2(38 A)

To give effect to the above substitutions and insertions, consequential amendmentsare also proposed in the various relevant sections of the Income Tax Ordinance,2001 to effect the change in the existing nomenclature of the taxation authorities.

Further through section 239B, it is proposed to insert modifications which providesfor making reference to the tax authorities as appearing in the notifications, orders,circulars or clarifications or any other instruments to be construed as reference to thetax authorities as appearing after the proposed substitutions.

Definition of “industrial undertaking”

The bill seeks to fine tune the definition of ‘industrial undertaking’ in a more clear and descriptive manner.

2(29C)

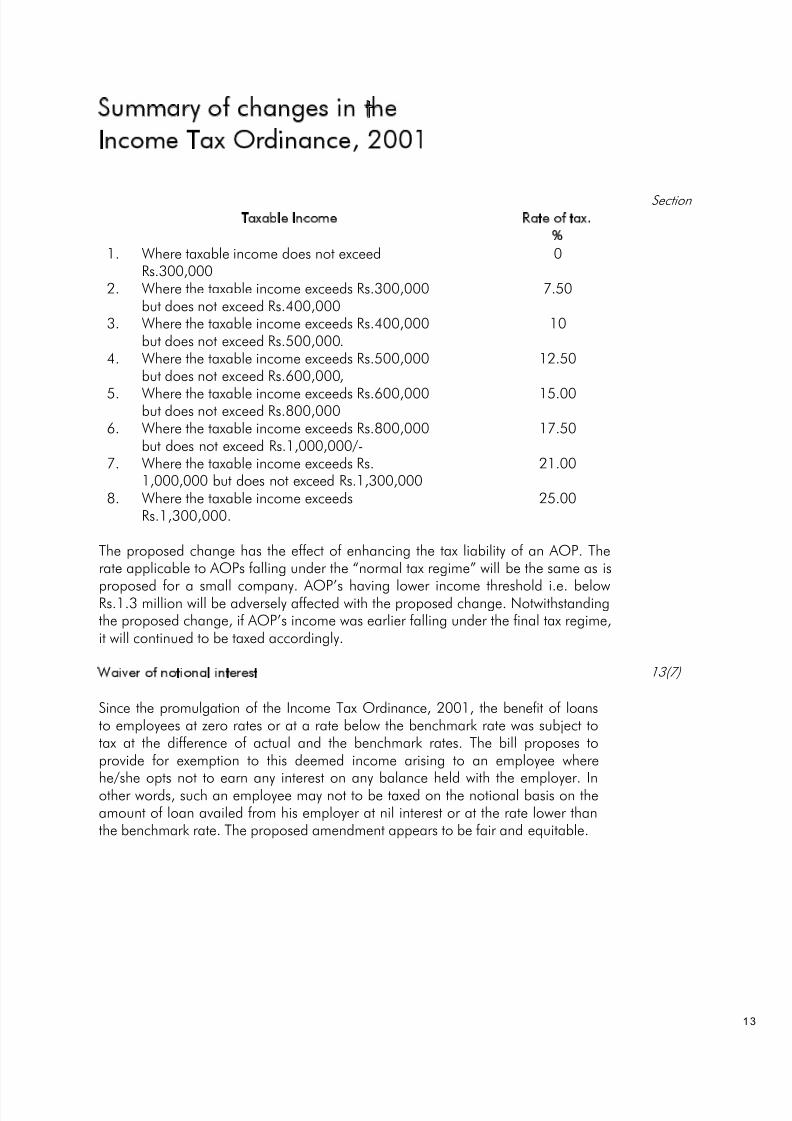

Association of persons (AOP’s) are to be taxed differently

The proposed amendment seeks to tax an Association of Persons at a flat rate of 25% instead of progressive slabs as earlier. These slab rates are now applicable tothe’ individual taxpayers only:

4, Division 1B,Part 1 of First

Schedule

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 16/53

Summary of changes in theIncome Tax Ordinance, 2001

1 3

Section

Taxable Income Rate of tax.%

1. Where taxable income does not exceedRs.300,000

0

2. Where the taxable income exceeds Rs.300,000but does not exceed Rs.400,000

7.50

3. Where the taxable income exceeds Rs.400,000but does not exceed Rs.500,000.

10

4. Where the taxable income exceeds Rs.500,000but does not exceed Rs.600,000,

12.50

5. Where the taxable income exceeds Rs.600,000but does not exceed Rs.800,000

15.00

6. Where the taxable income exceeds Rs.800,000but does not exceed Rs.1,000,000/-

17.50

7. Where the taxable income exceeds Rs.1,000,000 but does not exceed Rs.1,300,000

21.00

8. Where the taxable income exceedsRs.1,300,000.

25.00

The proposed change has the effect of enhancing the tax liability of an AOP. Therate applicable to AOPs falling under the “normal tax regime” will be the same as is

proposed for a small company. AOP’s having lower income threshold i.e. belowRs.1.3 million will be adversely affected with the proposed change. Notwithstandingthe proposed change, if AOP’s income was earlier falling under the final tax regime,it will continued to be taxed accordingly.

Waiver of notional interest 13(7)

Since the promulgation of the Income Tax Ordinance, 2001, the benefit of loansto employees at zero rates or at a rate below the benchmark rate was subject totax at the difference of actual and the benchmark rates. The bill proposes toprovide for exemption to this deemed income arising to an employee wherehe/she opts not to earn any interest on any balance held with the employer. Inother words, such an employee may not to be taxed on the notional basis on theamount of loan availed from his employer at nil interest or at the rate lower thanthe benchmark rate. The proposed amendment appears to be fair and equitable.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 17/53

Summary of changes in theIncome Tax Ordinance, 2001

1 4

Section

Capital gains on trading of listed securities brought under tax

Presently capital gains of unlisted companies are subject to tax at three/fourth of the amount of the gains, if held for more than one year. The proposedamendment seeks to restrict this concession in respect capital gains of unlistedshares by inserting words “other than shares of public companies includingvouchers of Pakistan Telecommunication Corporation, Modaraba certificates or instruments of redeemable capital”, The shares of listed securities are nowproposed to be taxed as a separate block of income taxable at varied ratessubject to period of holding.

It is for the first time tax on capital gains on the sale of shares of publiccompanies, vouchers of Pakistan Telecommunication Corporation, Modarabacertificates or instruments of redeemable capital is proposed to be introduced. Theproposed rates of tax are as under:-

37(3)&37A & Division VII of Part I of First

Schedule

Tax Year. ProposedRate of tax.

%1. Where holding period of a security is

less than six months.2010 10

2011 102012 12.52013 152014 17.5

2. Where holding period of a security ismore than six months but less thantwelve months.

2010 7.5

2011 82012 8.52013 92014 9.52015 10

Capital gains arising to the long term investors, holding securities for over one year,shall continue to be exempt from tax. The gains net of all capital losses andexpenditure incurred in earning such gains, in particular the financial charges,brokerage and commission paid or any other expenditure wholly and exclusivelyincurred in earning such gains, shall be allowed in arriving at the capital gains as aseparate block of income.

The capital losses shall also be available for set-off against the capital gains.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 18/53

Summary of changes in theIncome Tax Ordinance, 2001

1 5

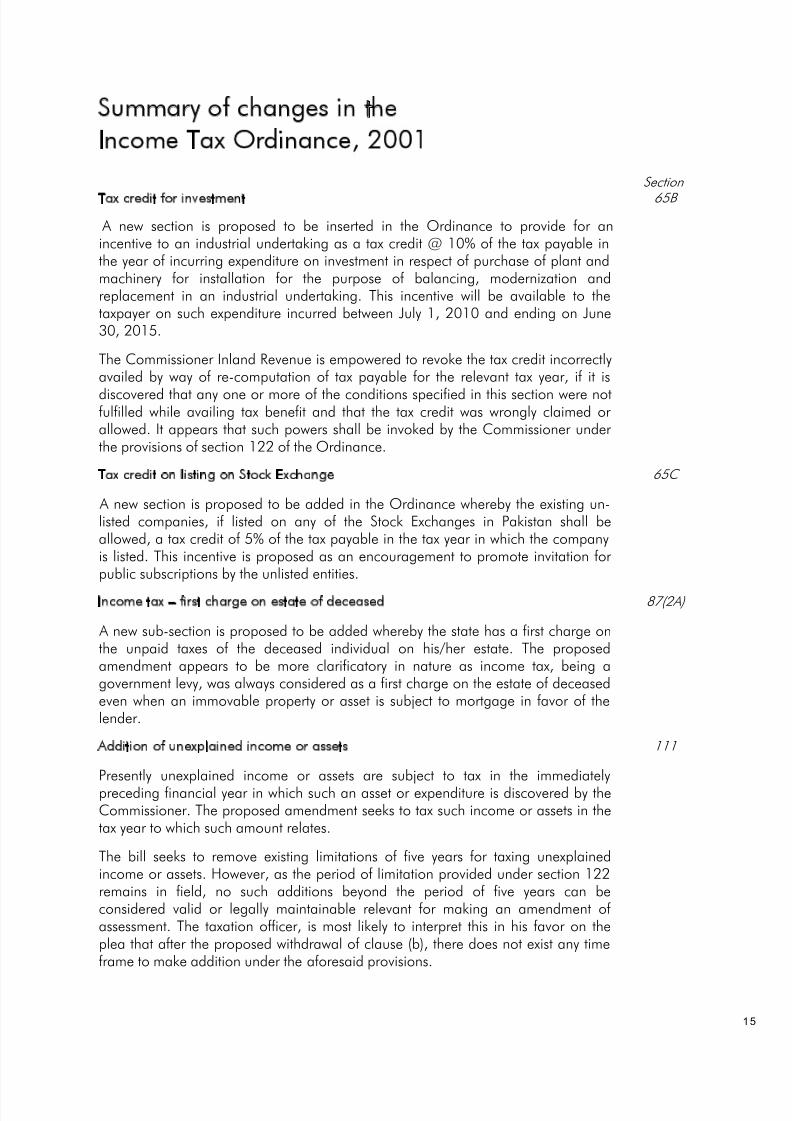

Section Tax credit for investment 65B

A new section is proposed to be inserted in the Ordinance to provide for anincentive to an industrial undertaking as a tax credit @ 10% of the tax payable inthe year of incurring expenditure on investment in respect of purchase of plant andmachinery for installation for the purpose of balancing, modernization andreplacement in an industrial undertaking. This incentive will be available to thetaxpayer on such expenditure incurred between July 1, 2010 and ending on June30, 2015.

The Commissioner Inland Revenue is empowered to revoke the tax credit incorrectlyavailed by way of re-computation of tax payable for the relevant tax year, if it isdiscovered that any one or more of the conditions specified in this section were notfulfilled while availing tax benefit and that the tax credit was wrongly claimed or allowed. It appears that such powers shall be invoked by the Commissioner under the provisions of section 122 of the Ordinance.

Tax credit on listing on Stock Exchange 65C

A new section is proposed to be added in the Ordinance whereby the existing un-listed companies, if listed on any of the Stock Exchanges in Pakistan shall beallowed, a tax credit of 5% of the tax payable in the tax year in which the companyis listed. This incentive is proposed as an encouragement to promote invitation for public subscriptions by the unlisted entities.

Income tax – first charge on estate of deceased 87(2A)

A new sub-section is proposed to be added whereby the state has a first charge onthe unpaid taxes of the deceased individual on his/her estate. The proposedamendment appears to be more clarificatory in nature as income tax, being agovernment levy, was always considered as a first charge on the estate of deceasedeven when an immovable property or asset is subject to mortgage in favor of thelender.

Addition of unexplained income or assets 111

Presently unexplained income or assets are subject to tax in the immediatelypreceding financial year in which such an asset or expenditure is discovered by theCommissioner. The proposed amendment seeks to tax such income or assets in thetax year to which such amount relates.

The bill seeks to remove existing limitations of five years for taxing unexplainedincome or assets. However, as the period of limitation provided under section 122remains in field, no such additions beyond the period of five years can beconsidered valid or legally maintainable relevant for making an amendment of assessment. The taxation officer, is most likely to interpret this in his favor on theplea that after the proposed withdrawal of clause (b), there does not exist any timeframe to make addition under the aforesaid provisions.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 19/53

Summary of changes in theIncome Tax Ordinance, 2001

1 6

Section Minimum tax 113(1)(e) & (2)

The rate of minimum tax is proposed to be enhanced from the current one-half percent of turnover to one percent of turnover. The following taxpayers are proposedto be included in the list of persons for the purpose of levy of minimum tax:

a) an individual who has turnover up to Rs. 50 million or above for the tax year 2009 or in any subsequent tax year; and

b) an Association of Person having turnover of Rs. 50 million or above in thetax year 2007 or in any subsequent tax year.

The aforementioned tax years of 2009 and 2007 for individuals and AOPsrespectively is for the purpose of levy of minimum tax from the tax year 2011.

Revision of return 114(6)(6A)

Under the provisions of the Income Tax Ordinance, 2001, a taxpayer had the rightto revise the return without any condition. However, through the Finance Act, 2009,three conditions for revision of the return were stipulated whereby (i) tax payer hadto furnish alongwith the revised return revised audited accounts; (ii) reason of revision of return and (iii) revision of return could only be made before issuance of

the show-notice for making amendment of an assessment.

The bill proposes further amendment in section 114(6) by retaining two conditionsfor revising, the return of income i.e. furnishing of revised accounts or auditedaccounts with the revised return and the reason for revision. However, the conditionof revising return after issuance of show-cause notice has been removed with certainpenalties such as:

a) where tax payer revises his / her return of income, after receipt of show-cause notice under section 177 but before issuance of notice for amendment of an assessment under Section 122(9) he shall be required to

make payment of difference of tax, default surcharge and 25% of applicablepenalties under the Ordinance; or

b) where a tax payer revises his / her return of income after receipt of shownotice for making amendment of assessment under section 122(9) butbefore passing of an amendment order, he shall make payment of difference of tax, default surcharge and 50% of leviable penalties under theOrdinance.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 20/53

Summary of changes in theIncome Tax Ordinance, 2001

1 7

Section

With the aforesaid changes, an anomaly has been created as the word “leviablepenalties” has not been explained as to which particular penalty is voluntarilyrequired to be paid by the tax payer. With the proposed change in section 182,several provisions for imposition of penalty have been provided.

It is not clear whether all the aforesaid penalties are voluntarily required to be paidor only any one or two of the above would suffice. This requires clarity in theFinance Act 2010 by way of an explanation otherwise unnecessary tax litigation willtrigger as the taxation officers, in the interest of raising revenue, will not accept therevised returns on the basis that such revised returns do not qualify for acceptance

as deemed order under section 120 of the Ordinance.

Provisional assessment

A new Section 122C is proposed to be added which empowers the Commissioner tomake a provisional assessment on the basis of available information or partialinformation according to the best of his judgment. In the Repealed Ordinance, 1979similar provision existed where a person who failed to furnish the return of income, inresponse to issuance of a notice, may receive a provisional assessment. Thisprovision was however, not included in the Income Tax Ordinance, 2001.

This proposed insertion empowers the tax authority to raise the tax demand on aperson, who in the opinion of the Commissioner, is liable to tax but has not compliedwith the provisions of law. However, where a person, within sixty days of passing of the provisional assessment, files the tax return along with wealth assessment andwealth reconciliation statement, then in such a case provisional assessment shall notbe treated as final assessment and return filed by the person would constitutedeemed assessment order under section 120 of the Income Tax Ordinance, 2001.Therefore the tax demand raised as a result of provisional assessment will not bepressed by the tax department under the proposed proviso in section 137 of theIncome Tax Ordinance, 2001.

Consequently 121(1) (a) is also proposed to be omitted which provides for finalization of assessment where a person fails to furnish a return of income incompliance to notice under sub-section (3) or (4) of Section 114. However, after proposed insertion of section 122(c), this sub-section would become redundant.

116(2A),121A,122C, 122(3) &

137(6)

Power to amend assessments which were subjected to appeals 122(5AA)

The proposed insertion of new sub-section seeks to provide retrospective powerseffective July 01, 2003 to the Commissioner to amend or further amend anassessment order under the provision of section 122(5A) where appeals have beenfiled or decided against the amended order of the Commissioner in respect of anypoint or issue which was not the subject matter of the appeal.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 21/53

Summary of changes in theIncome Tax Ordinance, 2001

1 8

Section

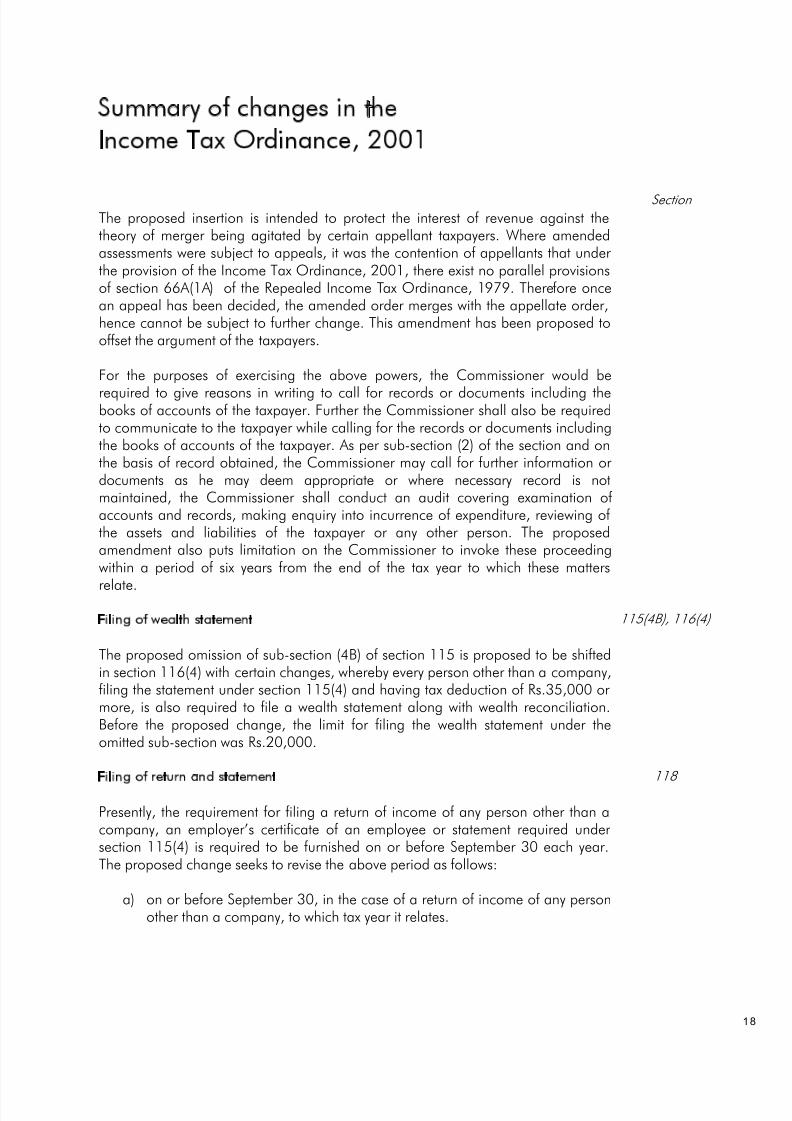

The proposed insertion is intended to protect the interest of revenue against thetheory of merger being agitated by certain appellant taxpayers. Where amendedassessments were subject to appeals, it was the contention of appellants that under the provision of the Income Tax Ordinance, 2001, there exist no parallel provisionsof section 66A(1A) of the Repealed Income Tax Ordinance, 1979. Therefore oncean appeal has been decided, the amended order merges with the appellate order,hence cannot be subject to further change. This amendment has been proposed tooffset the argument of the taxpayers.

For the purposes of exercising the above powers, the Commissioner would be

required to give reasons in writing to call for records or documents including thebooks of accounts of the taxpayer. Further the Commissioner shall also be requiredto communicate to the taxpayer while calling for the records or documents includingthe books of accounts of the taxpayer. As per sub-section (2) of the section and onthe basis of record obtained, the Commissioner may call for further information or documents as he may deem appropriate or where necessary record is notmaintained, the Commissioner shall conduct an audit covering examination of accounts and records, making enquiry into incurrence of expenditure, reviewing of the assets and liabilities of the taxpayer or any other person. The proposedamendment also puts limitation on the Commissioner to invoke these proceedingwithin a period of six years from the end of the tax year to which these matters

relate.

Filing of wealth statement 115(4B), 116(4)

The proposed omission of sub-section (4B) of section 115 is proposed to be shiftedin section 116(4) with certain changes, whereby every person other than a company,filing the statement under section 115(4) and having tax deduction of Rs.35,000 or more, is also required to file a wealth statement along with wealth reconciliation.Before the proposed change, the limit for filing the wealth statement under theomitted sub-section was Rs.20,000.

Filing of return and statement 118

Presently, the requirement for filing a return of income of any person other than acompany, an employer’s certificate of an employee or statement required under section 115(4) is required to be furnished on or before September 30 each year.The proposed change seeks to revise the above period as follows:

a) on or before September 30, in the case of a return of income of any personother than a company, to which tax year it relates.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 22/53

Summary of changes in theIncome Tax Ordinance, 2001

1 9

Section b) August 31 each year in case of a annual statement of deduction filed by an

individual, return of income through e-portal in case of a salaried personand statement required under Section 115(4).

In other words, a period of one month is shortened for filing particulars of salariedclass of tax payers as well as for persons filing statements under section 115(4) of the Ordinance on income falling under the final tax regime.

Qualification for appointment of accountant member 130 (4)

The proposed amendment seeks to substitute sub-section (4) by stipulating the

qualification of an accountant member of an appellate tribunal in addition to aRegional Commissioner, the rank of Commissioner Inland Revenue(Appeals) havingexperience of at least 5 five years as Commissioner or Collector. It is interesting tonote that there is no position of Regional Commissioner in the Income TaxOrdinance 2001 as the bill seeks to change this designation as Chief Commissioner Inland Revenue.

Estate in bankruptcy 138B

A new sub-section is proposed to be inserted whereby if a taxpayer declaresbankruptcy, the tax liability under the Ordinance shall pass on to the estate in

bankruptcy. If the tax liability is incurred as estate in bankruptcy the tax shall deemedto be current expenditure in the operation of the estate in bankruptcy and shall bepaid before the claims preferred by other creditors.

Advance Tax 147

The following changes are proposed for the purposes of payment of advance tax:

a) individuals – the minimum threshold for payment of advance tax byindividuals is proposed to be enhanced from Rs 200,000 to Rs. 500,000

b) exemption on payment of advance tax on capital gains is proposed to bewithdrawn

c) the basis for payment of advance tax by AOPs are proposed to be same asapplicable for companies

d) the dates for payment of advance tax for companies and AOPs areproposed to be 25 th day for September, December and March quarters, of each respective month whereas for the quarter ended June, the date isproposed to be 15th June.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 23/53

Summary of changes in theIncome Tax Ordinance, 2001

2 0

Section e) advance tax on gain on sale of securities will be paid as follows:

i) where holding period of security is six month, @2%ii) where the holding period of security is more than six months and less

than year, 1.5%.

The dates of payment for advance tax will be seven days after the close of eachquarter. It appears that there is inadvertent mistake that the bill does not specify onwhat basis advance tax will be paid by the taxpayer earning the capital gains.

Import of edible oil and packing materials outside in final tax regime 148 (7)

The above proposed change is a clarificatory amendment to remove an ambiguitythat the importers of edible oil and packing material do not fall under the final taxregime rather tax collected at source will be advance tax adjustable against the finaltax liability.

Profit on debt under FTR 151(4)

A new sub-section is proposed whereby final tax regime is stipulated in respect of profit on debt, other debt instruments, government securities and PakistanInvestment Bonds. At present, return on such securities are taxed @ 10% as full and

final discharge of tax liability in the hands of a taxpayer other than a companyexcept return on Federal Government, Provincial Government or Local Authoritysecurities. Now this distinction is proposed to be eliminated and all categories of taxpayers are eligible to fall under FTR on such income.

Individuals prescribed as withholding tax agents 153(9)(h)

The bill seeks to propose individuals having turnover Rs. 50 million or above in taxyear 2009 or in any subsequent tax years as withholding tax agents. In previousyears, such an attempt was also made for individuals having turnover of Rs.25million on but were not made part of the Act when bill was enacted.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 24/53

Summary of changes in theIncome Tax Ordinance, 2001

2 1

Section

Income from property

The proposed amendment seeks to exclude income from property from final taxregime. The rates of tax on income from property continue to be same as providedin Division VI, Part I of the First Schedule to the Ordinance at the gross value of the rent.

Consequential amendment has also been made in section 169. However, noconsequential changes have been made in section 15(6) read with Division VI of Part I of the First Schedule.

There appears to be an inadvertent error as proposed insertion of reference of section 15 in sub-sections (3) of section 169 whereas property income is proposedto be excluded from sub-section (1) of section 169.

With the proposed changes, we are of view that if the person has loss, propertyincome can be set-off against such loss under any other head of income other than capital loss and speculation loss.

155(2),169(1)(b) & 169(3)

Quarterly withholding tax statement 165

The proposed amendment seeks to withdraw the requirement of filing of monthlyand annual statements and in lieu thereof requires the withholding agents to filequarterly statements on:

a) for September quarter on or before, 20 th day of October

b) for December quarter on or before 20 th day of January

c) for March quarter, on or before 20 th day of April; and

d) for June quarter on or before the 20 th days o July

The bill further seeks to cast an obligation on withholding agents to file “nil”

statements for the period where no withholding tax deduction was made.Clarification of deemed assessment 169

The proposed insertion of an explanation seeks to clarify the existing expression “anassessment shall be treated to have been made under section 120” means:

a) the Commissioner shall be taken to have made an assessment of income for that tax year, and the tax due thereon equal to those respective amountsspecified in the return or statement under sub-section (4) of section 115;and

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 25/53

Summary of changes in theIncome Tax Ordinance, 2001

2 2

Section b) the return or the statement under sub-section (4) of section 115 shall be

taken for all purposes of this Ordinance to be an assessment order.

Retention period of record 174

The proposed amendment seeks to enhance the retention period of record from fiveto six years and a proviso is proposed to be inserted to make it mandatory on thetaxpayer to maintain the record till the proceedings pending before any authority or Court are concluded.

Pending proceeding have also been stipulated to include proceedings for assessment or amendment of assessment, appeal, revision, reference, petition or prosecution and any proceedings before an alternative dispute resolutioncommittee.

Appointment of firm of chartered accountants by the Board or Commissioner 176(1C)

The proposed amendment seeks to empower the Commissioner, in addition to theBoard, to appoint a firm of chartered accountants to conduct audit under section177. Such a firm is also empowered, with the prior approval of the Commissioner,to enter the business premises of the auditee taxpayer to obtain any information,require production of any record on which the required information is stated and

also to examine the same in the premises of the auditee taxpayer.

Audit 177(1)(2) (10)

Various sections relating to audit of tax affairs of a taxpayer are proposed to beamended. Changes are also proposed in sub-sections (1) and (2) by way of substitution whereas sub-sections (3), (4) and (5) are proposed to be omitted. A newsub-section (10) is also proposed to be inserted in the statute book.

Presently sub-section (1) provides that the Board may lay down criteria for selectionof any person for audit and the Commissioner is empowered to select the person for the purpose of audit on the basis of criteria laid down by the Board. After proposedsubstitution concept of “selection of audit” is being done away with and replacedwith the concept of “conduct of audit” of the income tax affairs of a person.Unbridled powers are proposed to be given to the Commissioners whereby he maycall for any record or documents or books of accounts for the conduct of the auditof the income tax affairs of any person. The Commissioner has express power tohave access to the electronic data where such records or documents have been kepton electronic data. The taxpayer shall allow access to Commissioner or the officer authorized by him for use of machine or software. Further the said officials are alsoauthorized to take into possession such machine and duly attested hard copies of such information or data for purposes of investigation and proceedings under thetax laws of any such person or any other person.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 26/53

Summary of changes in theIncome Tax Ordinance, 2001

2 3

Section

However, for the purposes of the above the Commissioner would be required togive reasons in writing to call for records or documents including the books of accounts of the taxpayer. Further the Commissioner shall also be required tocommunicate to the taxpayer while calling records or documents included in booksof accounts of taxpayer. And as per sub-section (2) on the basis of record obtained,the Commissioner may call for further information or documents as he may deemappropriate or where necessary record is not maintained, the Commissioner shallconduct an audit of the income tax affairs covering examination of accounts andrecords, enquiry into expenditure, assets and liabilities of the taxpayer or any other person. The proposed amendment also puts limitation on Commissioner to invokethese proceedings i.e. expiry of six years from the end of the tax year to which they

relate.

Therefore, after the proposed amendments, the concept of selection of cases for “audit” has been done away with. It is now at the entire discretion of theCommissioner to select any case. No regard will be made to considerations such asperson’s history of compliance or non compliance, amount of tax payable or classof business conducted by the person. In the prevalent environment it is apprehendedthat this power will be misused in an arbitrary manner keeping in view the contentsof section 210 of the Income Tax Ordinance, 2001 whereby Commissioner candelegate his power to the Officers of Inland Revenue, hence, power of section 177is apprehended to be invoked by the junior officers. Therefore judicious application

of this section will become questionable and will adversely affect the concept of deemed assessment under section 120 of the Income Tax Ordinance.

The insertion of sub section (10) provides that in case of non-compliance, theCommissioner may also proceed to make best judgment assessment under section121 of the Ordinance and the assessment treated to have been made under section120 on the basis of return or revised return filed by the taxpayer shall be of no legaleffect.

Selection of a Audit through computer ballot 214C

With the proposed insertion, the Board is also being empowered to select anyperson or classes of persons for audit of the income tax affairs through computer ballot which may be random or parametric as the Board may consider deemed fit.

Such audits by the income tax officers shall be conducted as per procedure providedfor audit in section 177 and all the provisions of the Income Tax Ordinance, 2001shall apply except the first proviso to section 177(1). These enabling powers areproposed with retrospective effect as sub-section (3) states that:

“The Board shall be deemed always to have had the power toselect any person or classes of persons for audit of income taxaffairs”.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 27/53

Summary of changes in theIncome Tax Ordinance, 2001

2 4

Section

Active taxpayers’ list 181A

The new section is proposed to be inserted whereby the Board is empowered toinstitute active taxpayers list which shall be regulated as may be prescribed from timeto time.

Offences and penalties 182

The proposed amendment seeks to enlist all the penalties under one section whichwere presently under separate sections. From bare perusal of the proposedamendment, it appears that harsh penalties are being imposed and in certain casesfor a single default several penalties are to be attracted simultaneously. Also anattempt is being made by the Board to ensure compliance of laws with theimposition of harsh penalties. These penalties are listed as under:

S.No. Offences Penalties

1 Where any person fails to furnisha return of income or a statementu/s 115 or wealth statement or reconciliation thereof or statement u/s 165 within the duedate.

A penalty equal to 0.1% of the taxpayable for each day of defaultsubject to a minimum penalty of Rs.5,000 and a maximum penalty of 25% of the tax payable in respect of that tax year.

114, 115,116 and 165

2 Any person who fails to issuecash memo or invoice or receipt A penalty of Rs.5,000 or 3% of theamount of the tax involved,whichever is higher.

174 and Chapter VII of the Income Tax

Rules

3 Required to apply for registrationbut fails to make an application.

A penalty of Rs.5,000 181

4 Fails to notify the changes of material nature in the particularsof registration.

A penalty of Rs.5,000 181

5 Fails to deposit the amount of tax

due or any part thereof in thetime or manner laid down under this Ordinance or rules madethereunder.

A penalty of Rs.5,000 of the amount

of the tax in default.

For the 2nd default an additionalpenalty of 25% of the amount of taxin default.

For the third and subsequent defaultsan additional penalty of 50% of theamount of tax in default.

137

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 28/53

Summary of changes in theIncome Tax Ordinance, 2001

2 5

S.No. Offences Penalties Section

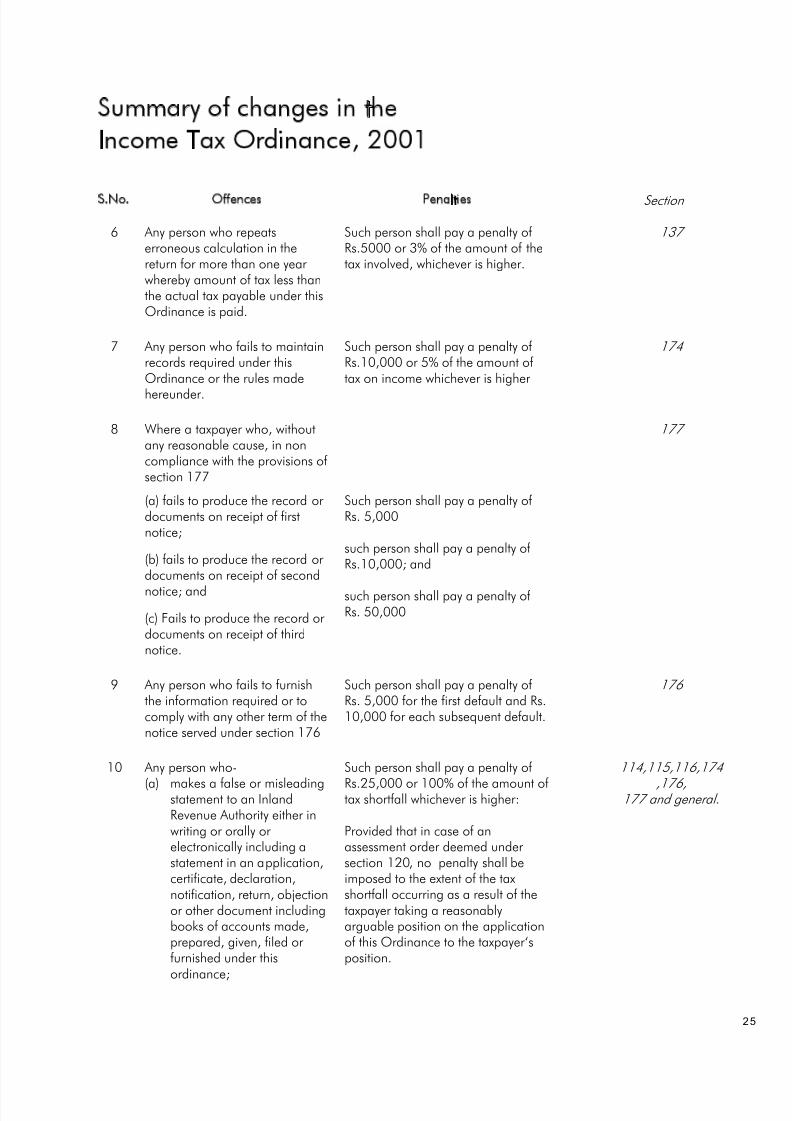

6 Any person who repeatserroneous calculation in thereturn for more than one year whereby amount of tax less thanthe actual tax payable under thisOrdinance is paid.

Such person shall pay a penalty of Rs.5000 or 3% of the amount of thetax involved, whichever is higher.

137

7 Any person who fails to maintainrecords required under thisOrdinance or the rules madehereunder.

Such person shall pay a penalty of Rs.10,000 or 5% of the amount of tax on income whichever is higher

174

8 Where a taxpayer who, withoutany reasonable cause, in noncompliance with the provisions of section 177

177

(a) fails to produce the record or documents on receipt of firstnotice;

(b) fails to produce the record or documents on receipt of secondnotice; and

(c) Fails to produce the record or documents on receipt of thirdnotice.

Such person shall pay a penalty of Rs. 5,000

such person shall pay a penalty of Rs.10,000; and

such person shall pay a penalty of Rs. 50,000

9 Any person who fails to furnishthe information required or tocomply with any other term of thenotice served under section 176

Such person shall pay a penalty of Rs. 5,000 for the first default and Rs.10,000 for each subsequent default.

176

10 Any person who-

(a) makes a false or misleadingstatement to an InlandRevenue Authority either inwriting or orally or electronically including astatement in an application,certificate, declaration,notification, return, objectionor other document includingbooks of accounts made,prepared, given, filed or furnished under thisordinance;

Such person shall pay a penalty of

Rs.25,000 or 100% of the amount of tax shortfall whichever is higher:

Provided that in case of anassessment order deemed under section 120, no penalty shall beimposed to the extent of the taxshortfall occurring as a result of thetaxpayer taking a reasonablyarguable position on the applicationof this Ordinance to the taxpayer‘sposition.

114,115,116,174

,176,177 and general.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 29/53

Summary of changes in theIncome Tax Ordinance, 2001

2 6

S.No. Offences Penalties Section

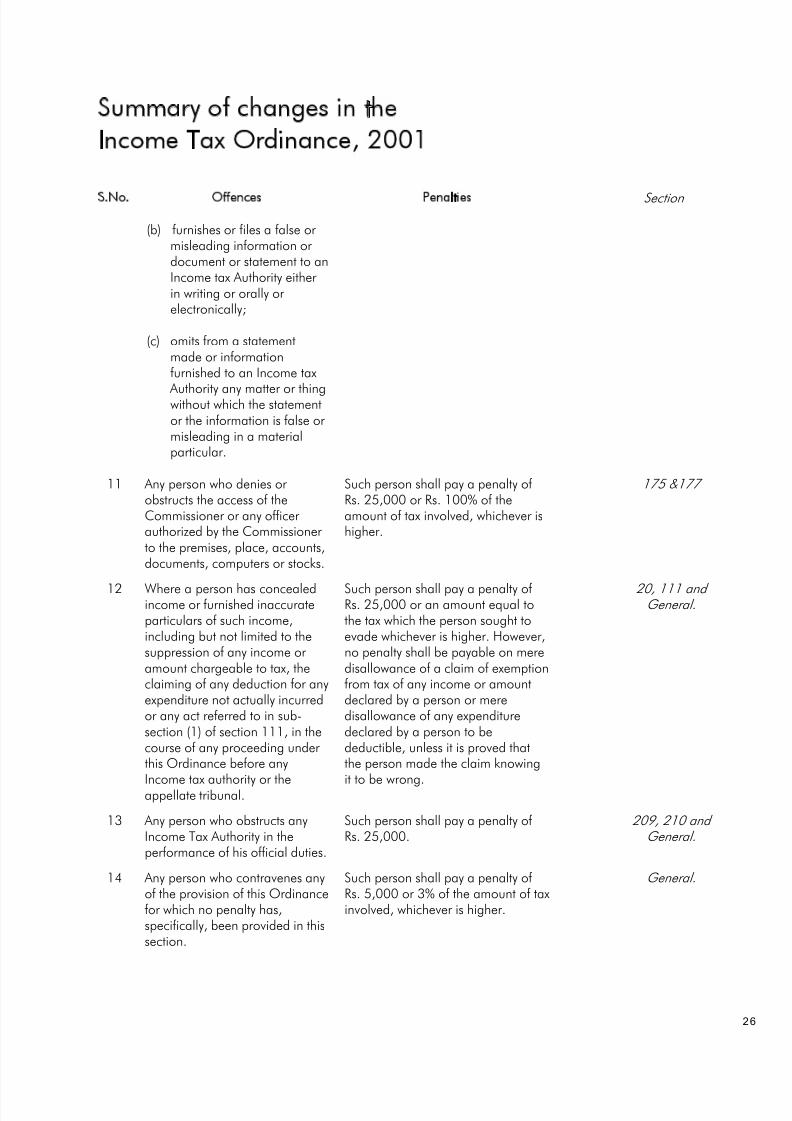

(b) furnishes or files a false or misleading information or document or statement to anIncome tax Authority either in writing or orally or electronically;

(c) omits from a statementmade or informationfurnished to an Income tax

Authority any matter or thingwithout which the statementor the information is false or misleading in a materialparticular.

11 Any person who denies or obstructs the access of theCommissioner or any officer authorized by the Commissioner to the premises, place, accounts,documents, computers or stocks.

Such person shall pay a penalty of Rs. 25,000 or Rs. 100% of theamount of tax involved, whichever ishigher.

175 &177

12 Where a person has concealedincome or furnished inaccurateparticulars of such income,including but not limited to thesuppression of any income or amount chargeable to tax, theclaiming of any deduction for anyexpenditure not actually incurredor any act referred to in sub-section (1) of section 111, in thecourse of any proceeding under this Ordinance before any

Income tax authority or theappellate tribunal.

Such person shall pay a penalty of Rs. 25,000 or an amount equal tothe tax which the person sought toevade whichever is higher. However,no penalty shall be payable on meredisallowance of a claim of exemptionfrom tax of any income or amountdeclared by a person or meredisallowance of any expendituredeclared by a person to bedeductible, unless it is proved thatthe person made the claim knowing

it to be wrong.

20, 111 and General.

13 Any person who obstructs anyIncome Tax Authority in theperformance of his official duties.

Such person shall pay a penalty of Rs. 25,000.

209, 210 and General.

14 Any person who contravenes anyof the provision of this Ordinancefor which no penalty has,specifically, been provided in thissection.

Such person shall pay a penalty of Rs. 5,000 or 3% of the amount of taxinvolved, whichever is higher.

General.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 30/53

Summary of changes in theIncome Tax Ordinance, 2001

2 7

S.No. Offences Penalties Section

15 Any person who fails to collect or deduct tax as required under anyprovision of this Ordinance or fails to pay the tax collected or deducted as required under section 160.

Such person shall pay a penalty of Rs. 25,000 or the 10% of theamount of tax whichever is higher.

148,149,150,151,152, 153, 153A,154, 155, 156,

156A, 156B, 158,160, 231A, 231B,233, 233A, 234,234A, 235, 236,

236A.It is incumbent upon the Commissioner, Commissioner (Appeals) or the AppellateTribunal to pass an order in writing before the penalty is levied on the taxpayer. Theprinciple of natural justice of providing an opportunity of being heard is alsoprovided for in the proposed amendment.

It would be better if the Board should have initiated educative program for thetaxpayers before proposing harsh and severe penal provisions. It should berecognized that the state of documentation in the country has still not attainedmaturity for which in a way the Board is also responsible as in the past, lack of documentation got promoted with the introduction of PRT or FTR schemes.

The Commissioner Appeals or the Appellate Tribunal shall immediately forward thecopy of the order to the Commissioner in respect of imposing any penalty on the

taxpayer and such order shall be considered as having been made by theCommissioner.

Exemption from penalty and default surcharge 183

It is proposed that power to exempt any person or class of person from payment of penalty and default surcharge shall rest with the Federal Government or the Board.In such an order, the reasons are to be recorded in writing for granting of theexemption and the same are to be published in the official gazette.

Special Judges 203(1)

The sub-section (1) is proposed to be substituted whereby the Federal Governmentmay appoint special judges to be notified in the official gazette, if may beconsidered necessary, and where more than one special judge is appointed, thesame shall be specified in notification with their territorial limits within which each of them can exercise their jurisdiction.

The new sub-sections (1A) and (1B) are proposed to be inserted which specify thequalification of special judge and their qualifications, terms and conditions andterritorial jurisdiction.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 31/53

Summary of changes in theIncome Tax Ordinance, 2001

2 8

Section

Computation of limitation period 226B

The proposed amendment seeks to provide for that no limitation shall apply even for a period for which any proceedings remain pending before any court, appellatetribunal or any other authority. Presently such limitations period was relevant onlywhere such proceedings were stayed by any court, appellate tribunal or any other authority.

Bar of investigation against employees of the Board 227

A new sub-section is proposed to be inserted to provide for protection to theemployees of the Board against the possible investigation or inquiry initiated by anygovernment agency for anything done in official capacity under the provisions of theOrdinance rules, instructions or directions. However, in order to initiate such inquiry,prior approval of the Board is necessary.

Directorate General of Training and Research 229

The new section is proposed to be inserted consisting of a Director General, Additional Director General and as many Directors and Additional Directors, DeputyDirectors, Assistant Directors and such officers Board may appoint to be notified inthe official gazette. The Board has obtained powers to specify functions, and powersof the Director General of Training and Research and its officers which is to benotified in the official gazette.

Advance tax on transactions in a bank

A new sub-section is proposed to be inserted making it obligatory on every bankingcompany to deduct 0.3% if the payment or withdrawal is made through any modeof banking transaction through draft , payment order, online transfer, TelegraphicTransfer, CDR, STDR, RTC or some total of the payment for the transactions in aday exceeding Rs 25,000.

231AA, Division VIA of part 4 of

first schedule

The following are the persons who are exempt from the applicability of aboveprovisions:

a) Federal or Provincial Government

c) Foreign diplomat or diplomatic mission of Pakistan

d) A person who produces a certificate from Commissioner that his incomeduring the year is exempt for tax

The intention behind the proposed amendment is to bring all transactions towithholding tax net to raise revenue and further to document the economy. In thismanner, transactions being undertaken through the banking system, if remainedunrecorded in the books of the person undertaking such transaction, the same canbe crossed checked from the statement of withholding tax submitted by the bankingcompanies. It will help the Board to track tax evasion.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 32/53

Summary of changes in theIncome Tax Ordinance, 2001

2 9

Section

Government may seek another benefit to identify purchase and sale transaction of properties will also be subjected to scrutiny with the introduction of this mechanism.This tax has a nature of advance tax and adjustable against advance tax liability of the person on whose behalf the tax has been deducted.

Collection of tax by Stock Exchanges 233A (2)

The proposed amendment seeks to make withholding tax adjustable against final taxliability. Presently such tax was collected from members of the Stock Exchanges onpurchase and sales of shares in lieu of commission earned by such members andalso in respect of trading of shares which was minimum tax.

Telephone users 236(1) (C) & (3)(A)

The proposed insertion of clause (C) seeks to enlarge tax net by bringing sale of units through an electronic medium or whatever form along with telephone bills for subscribers and prepaid telephone cards already subject to withholding tax under clauses (a) and (b) of section 236 (1).

Such tax shall be collected by the person issuing or selling units through electronicmode from the purchaser at time of sale of units. The rate of advance tax shallcontinue to be 10 %.

Advance tax on sale by auction 236(A)

The proposed insertion in sub-section (1) seeks to levy tax on property or goodsconfiscated or attached into the withholding tax net at the time of auction. Suchconfiscated or attached goods, when auctioned, shall be subject to 5% tax atsource.

Advance tax on purchase of air tickets 236(B)

A new section is proposed to be inserted to bring domestic air tickets into thewithholding tax net @ 5%. This is a revenue measure intended to enhance taxcollection at the cost of passengers who are already feeling brunt of higher cost of domestic travelling. This tax is adjustable against the final tax liability of the person.The existing taxpayer may not feel the burden, but non-taxpayer passenger woulddefinitely feel the heat.

Removal of difficulties 240

The proposed amendment seeks to remove the sub-section (2) from the statue whichhas already become redundant as has restricted the Board’s powers to issuenotifications after June 30, 2004.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 33/53

Summary of changes in theIncome Tax Ordinance, 2001

3 0

First Schedule Clause

Minimum taxable threshold and tax benefit

The bill proposes to increase the minimum threshold for the purposes of levy of taxon the taxable income to Rs.300,000 for all individuals without any gender discrimination. The separate preferential threshold for women has been done awaywith.

Part I,Division-I

Clause(1) & (1A)

Non salaried persons

The taxable income threshold for non-salaried persons is also proposed to beenhanced to Rs.300,000 thus proposing relief of tax liability on income fallingbetween Rs. 110,000 to Rs. 300,000.

The substituted tax tariff will provide relief to the extent indicated below.

Taxable income up to Proposedslab

Previousslabs Tax saving

Rupees Rate Rate Rupees% %

110,000 0 0.50 550125,000 0 1.00 1,250150,000 0 2.00 3,000175,000 0 3.00 5,250200,000 0 4.00 8,000300,000 0 5.00 15,000

Salaried persons

The substituted tax tariff while providing relief to income earners up to Rs.300,000seeks to apply the maximum rate of tax @ 20% for persons earning incomeexceeding Rs.4,550, 000. Previously this rate was applicable to income exceedingRs.8,650, 000. The impact of the proposed changes is as under:

Gross incomeupto

Proposedslab

Previousslab

TaxImpact

Rupees Rate Rate Rupees% %

300,000 0 0.75 (2,250)325,000 0.75 0.75 -

4,800,000 20 19 48,0008,650,000 20 19 86,500

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 34/53

Summary of changes in theIncome Tax Ordinance, 2001

3 1

Rate of small companies

The bill proposes to enhance the tax rate for small companies from 20% to 25%.

Part-I Division-II Clause (iii)

Tax at import stage

The Finance Act, 2008 reduced the rate of collection of tax to 2% and withdrew thepower of the Commissioner to issue an exemption certificate. The Finance Act,2009 increased the rate of collection to 4% which is now proposed to be increasedto 5%. The power of the Commissioner to issue exemption certificate needs to berestored to facilitate liquidity position of manufacturers importing material for ownconsumption.

Part-II

Payment to non-residents

The rate of withholding tax applicable on payments other than those specifiedunder section 152 to non-residents is proposed to be reduced to 20% instead of existing rate of 30%.

Part-III Division-II Clause (2)

Prizes and winnings

The bill proposes to reduce the rate of tax on winners of cross word puzzles to 10%as against the existing rate of 20%.

Part-III Division-VI

Tax on motor vehicles

The bill proposes to decrease the existing slab rate to Re.1 per kilogram ladenweight of goods transport vehicles.

Part-IV Division-III Clause (i)

Electricity consumption

The bill proposes to reduce the rate of collection of tax to 5% instead of the existingrate of 10% providing relief to industrial and commercial consumer whose billingexceeded Rs.20,000.

Part-IV Division-IV

Second Schedule – Part IExemption from total income

Interest to non-residents for approved projects

The bill proposes to extend the scope of exemption to the profit on debts payableto foreign individuals, company, firm or association of persons in respect of foreignloan utilized for industrial investments in Pakistan where the loan agreement wasconcluded on or before first day of February, 1991 and duly registered with theState Bank of Pakistan. This exemption was earlier withdrawn by the Finance Act,2008.

Clause (72) sub-clause

(iii)

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 35/53

Summary of changes in theIncome Tax Ordinance, 2001

3 2

Pursuant to the Prime Minister’s relief package to rehabilitate to economy of Khyber Pakhtunkhwa, FATA and PATA, the bill proposes to grant exemption to educationalinstitutions for a period of two years ending on June 30, 2011 and income of taxpayers other than manufacturers and suppliers of cement, sugar, beverages andcigarettes for a period of three years starting from tax year 2010 established /located in the most affected and moderately affected areas. Most affected areasmean district Peshawar, Malakand Division, district of Swat, Buner, Shangla, Upper Dir, Lower Dir, Hangu, Bannu, Tank, Kohat and Chitral while moderately affectedareas are districts of Charsadda, Nowshera, DI Khan, Batagram, Lakki Marwat,Swabi and Mardan.

Clauses (92A), (126F)

& Part IV Clause (10A)

Dividend received by ICP

Exemption granted to ICP on account of dividend from any company is proposedto be withdrawn by omission of the said clause.

Clause (102)

Second Schedule – Part IIReduction in tax rates

Clause (24A)

The clause provides for reduction in the rate of withholding tax provided in section153 on account of supplies of goods by distributors of cigarettes andpharmaceuticals products to 1%. The bill proposes to extend the facility to large

distribution houses fulfilling the conditions prescribed in sub-section (7) of section148 for large import houses.

Second Schedule – Part IIIReduction in tax liability

Clause (1A)

Taxpayers aged 60 years or more whose income does not exceed Rs.750,000 areentitled to the benefit of reduction in their tax liability by 50%. This benefit was alsobeing availed in respect of income subject to final taxation thereby claiming refundof tax withheld to the extent of 50%. The bill proposes to restrict the benefit toincome other than that subject to final taxation while increasing the limit of incometo Rs.1,000,000.

Second Schedule – Part IVExemption from specific provisions

Clause (10A

In line with the Prime Minister’s relief package to rehabilitate the economy of Khyber Pakhtunkhwa, FATA and PATA following additional benefits are beingprovided to persons in most affected and moderately affected areas.

• exemption from penal provisions and default surcharge in terms of sections182 and 205 respectively provided the principal amount of tax due is paid by

June 30, 2010.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 36/53

Summary of changes in theIncome Tax Ordinance, 2001

3 3

• exemption from application of section 235 that is collection of advance taxon electricity bills to commercial and industrial consumers till June 30, 2011

• exemption from application of withholding tax provisions on export of goodsby exporters based in the above mentioned areas

• exemption from application of provision of section 148 on import of plantand machinery till June 30, 2011 for business other than manufacturers andsuppliers of cement, sugar, beverages and cigarettes.

Clause

The bill proposes to exempt income of foreign experts if acquired with prior approval of Ministry of Textile Industry.

(73)

Third Schedule – Part IDepreciation

Sub-clause (V)

By this insertion bill seeks to allow 100% depreciation on cost of construction f aramp with cost not exceeding Rs.250,000 built to provide access to disabledpersons.

Fifth Schedule – Part I

Rules for the computation of the profit and gainsfrom the exploration and production of petroleum

Rule (4A)

Petroleum exploration and production companies consider provision for decommissioning cost to be an allowable expense while the revenue authoritiesdisputed the claim on the basis that the expenditure have not been actuallyincurred and provisions are not allowable under the Ordinance. The longoutstanding dispute and consequential litigation was resolved with the concurrenceof the Ministry of Petroleum and Natural Resources by signing of a Memorandumof Understanding between FBR and representatives of Pakistan PetroleumExploration and Production Companies Association in March this year. To

formalize the agreed principle, facilitate tax compliance and flow of revenues,necessary amendments in law were agreed to be incorporated through the FinanceBill, 2010.

The bill by insertion of the new rule proposes to allow de-commissioning cost dulycertified by a Chartered Accountant or a Cost Accountant in the manner prescribedover a period of ten years or the life of the development and production or mininglease whichever is earlier, starting from the year of commencement of commercialproduction or commenced prior to the first day of July 2010. Such deduction shallbe allowed from the tax year 2010 and onwards.

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 37/53

Summary of changes in theIncome Tax Ordinance, 2001

3 4

Seventh Schedule – Part IRules for the computation of the profit and gainsof banking company and tax payable thereon

A proposed amendment in Rule 1(c) is intended to provide relief to the bankingcompanies whereby the provision for bad and doubtful advances and off balancesheet items are proposed to be allowed @ 5% of the total advances for consumersand Small and Medium Enterprise (SME) (as defined under the State BankPrudential Regulation). In other words, banking companies would be allowed theprovision for bad and doubtful debts under the two types of advances which are asfollows:

a) consumer loans and SME advances which shall be allowed @5% of suchadvances; and

b) other than consumer loans and SME advances, which will be allowed @ 1%of the total advances’ portfolio except (a) above.

The proposed change would provide some relief to the banking companies as 1%of total advances for bad and doubtful debts as well as off balance sheetobligation was not considered appropriate considering the fact that in practiceactual bad debts far exceed the 1% threshold. The existing limit of 1% is considered

meager and is suggested to be enhanced to make the provision more reasonableand pragmatic for the banking companies.

8A Transactional provision

The bill seeks to insert transactional provisions in respect of bad and doubtful debtsas under:

a) a banking company will be entitled to claim, over and above the provisionfor bad and doubtful debts and off balance sheet obligation for the tax year 2009, on the basis of actual write-off amounts which were provided for in thetax year 2008 and prior thereto but were not claimed nor allowed as taxdeductible in any tax year. In that event, the relevant provisions of section 29and 29A would apply to claim to actual bad debts written off.

b) amounts written back which were provided for in tax year 2008 or beforeagainst the reversal of doubtful advances which were neither claimed nor allowed as tax deductible in any tax year would not constitute income in theyear of write back.

c) the provision of the Seventh Schedule shall not apply to any assets given or acquired on finance lease by a banking company up to the tax year 2008and recognition of income and deductions in respect of such assets shall be

8/8/2019 financebill2010-2011

http://slidepdf.com/reader/full/financebill2010-2011 38/53

Summary of changes in theIncome Tax Ordinance, 2001

3 5