CHAPTER 1 – FRAMEWORK OF FINANCIAL MANAGEMENT 1.1 INTRODUCTION: Finance can be defined as the art and science of managing money. Virtually all individuals and organizations earn or raise money and spend or invest money. Finance is concerned with the process, institutions, markets and instruments involved in the transfer of money among and between individuals, businesses and governments. Finance consists of three interrelated areas: i) Money and capital markets, which deals with securities markets and financial institutions. ii) Investments, which focuses on the decisions of both individuals and institutional services as they choose securities for their investment portfolios. iii) Financial management or managerial finance, which is concerned with the duties of the financial manager in the business firm. Financial managers actively mange the financial affairs of many types of business- financial and non-financial, private and public, large and small, profit- seeking and not-for-profit. Relationship to Economics: The field of finance is closely related to economics. Financial managers must understand the economic framework and be alert to the consequences of varying levels of economic activity and changes in economic policy. They must also be able to use economic theories as guidelines for efficient business operations. Examples include supply and demand analysis, profit maximizing strategies and price theory. A basic knowledge of economics is therefore necessary to understand both the environment and the decision techniques of managerial finance. Relationship to accounting: The firm’s finance and accounting activities are closely related and generally overlap. Indeed managerial finance and accounting are not often easily distinguishable. In small firms the accountant often carries out the finance function, and in large firms many accountants are closely involved in various finance functions. However, there are two basic differences between finance and accounting: i) Emphasis on cash flows. The accountant’s function is to develop and provide data for measuring the performance of the firm, assessing its financial position, and paying 1

Transcript

CHAPTER 1 – FRAMEWORK OF FINANCIAL MANAGEMENT

1.1 INTRODUCTION:Finance can be defined as the art and science of managing money. Virtually all individuals and organizations earn or raise money and spend or invest money. Finance is concerned with the process, institutions, markets and instruments involved in the transfer of money among and between individuals, businesses and governments.Finance consists of three interrelated areas:

i) Money and capital markets, which deals with securities markets and financial institutions.

ii) Investments, which focuses on the decisions of both individuals and institutional services as they choose securities for their investment portfolios.

iii) Financial management or managerial finance, which is concerned with the duties of the financial manager in the business firm. Financial managers actively mange the financial affairs of many types of business- financial and non-financial, private and public, large and small, profit-seeking and not-for-profit.

Relationship to Economics:The field of finance is closely related to economics. Financial managers must understand the economic framework and be alert to the consequences of varying levels of economic activity and changes in economic policy. They must also be able to use economic theories as guidelines for efficient business operations. Examples include supply and demand analysis, profit maximizing strategies and price theory. A basic knowledge of economics is therefore necessary to understand both the environment and the decision techniques of managerial finance.

Relationship to accounting:The firm’s finance and accounting activities are closely related and generally overlap. Indeed managerial finance and accounting are not often easily distinguishable. In small firms the accountant often carries out the finance function, and in large firms many accountants are closely involved in various finance functions. However, there are two basic differences between finance and accounting:

i) Emphasis on cash flows. The accountant’s function is to develop and provide data for measuring the performance of the firm, assessing its financial position, and paying taxes. Using certain standardized and generally accepted principles, the accountant prepares financial statements that recognize revenue at the point of sale and expenses when occurred is accrual basis of accounting.

The financial manager, on the other hand, places primary emphasis on cash flows. He or she maintains the firm’s solvency by planning the cash flows necessary to satisfy its obligations and to acquire assets needed to achieve the firm’s goals. The financial manager uses this cash basis to recognize the revenues and expenses only with respect

1

to actual inflows and outflows of cash. Regardless of its profit or loss, a firm must have sufficient cash flows

ii) Decision-making: whereas accountants devote most of their attention to the collection and presentation of financial data, financial managers evaluate the accounting statements, develop additional data, and make decisions based on their assessment of the associated returns and risks. Accountants provide consistently developed and easily interpreted data about the firm’s past, present and future operations. Financial managers use these data, either in raw form or after adjustments and analysis, as inputs to the decision making process.

1.2 THE FINANCIAL MANAGER’S RESPNSIBILITIES:The manager’s task is to acquire and use funds so as to maximize the value of the firm. The financial manager’s primary responsibilities include:

i. Financial analysis and planning: this is concerned with monitoring the firm’s financial condition, evaluating the need for increased (or reduced) productive capacity, and determining what financial is required.

ii. Investment decisions: the financial manager must determine the mix of current and fixed assets and attempts to maintain optimal levels for reach type of current asset. The financial manager also decided which fixed assets to acquire and when existing fixed assets need to be modified, replaced or liquidated.

iii. Financing decisions: financing decisions involve two major areas. First, the most a[appropriate mix of short term and long term financing must be established. A second and equally important concern is which individual short term or long term sources of financing are the best at a given point in time. Many of these decisions are dictated by necessity but some require in depth analysis of the financing alternatives, their costs, and their long run implications.

iv. Dealing with the financial markets: the financial manager must deal with the money and capital markets where funds are raised, the firm’s securities are traded and its investors either make or lose money.

v. Risk management. All businesses face risks, including natural disasters, uncertainties in commodity and security prices, volatile interest rates and fluctuating exchange rates. The financial manager is usually responsible for the firm’s overall risk management, including identifying the risks that should be hedged and them in the most efficient manner.

In summary, financial managers make decisions regarding which assets their firms should acquire, how those assets should be financed, and how the firm should manage its existing resources.

GOALS OF FINACIAL MANAGEMENT

Shareholder wealth maximization:The goal of the firm, and therefore of all managers and employees, is to maximize the wealth of the owners for whom it is being operated. The wealth of corporate owners is measured by the share price of the stock, which in turn is based on the timing of returns (cash flows), their magnitude and their risk. When considering each financial decision alternative or possible action in terms of its impact on the share price of the firm’s stock, financial managers should accept only those actions that are

2

expected to increase share price. Because share price represents the owners’ wealth in the firm, share price maximization is consistent with owner-wealth maximization.

What about stakeholders?Although shareholder wealth maximization is the primary goal, in recent years many firms have broadened their focus to include the interests of stakeholders as well as shareholders. Stakeholders are groups such as employees, customers, suppliers, creditors, owners and others who have a direct economic link to the firm. Employees are paid for their labour, customers purchase the firm’s products or services, suppliers are paid for the materials and services they provide, creditors provide debt financing that is to be repaid subject to specified terms, and owners provide equity financing for which they expect to be compensated. A firm with a stakeholder focus consciously avoids actions that would prove detrimental to stakeholders. The goal is not to maximize stakeholders well being but to preserve it.

The stakeholder view does not alter the shareholder wealth maximization goal. Such a view is often considered part of the firm’s social responsibility and is expected to provide maximum long-run benefit to shareholders by maintaining positive stakeholder relationships. Such relationships should minimize stakeholder turnover, conflicts and litigation. Clearly, the firm can better achieve its goal of shareholder wealth maximization with cooperation of-rather than conflict with-its stakeholders.

Profit maximization.To achieve the goal of profit maximization, the financial manager takes only those actions that are expected to contribute to the firm’s overall profits. For each alternative being considered, the financial manager would select the one that is expected to result in the highest monetary return. Corporations normally measure profits in terms of EPS, which is calculated by dividing the period’s total earnings available for the firm’s common stockholders by the number of shares of common stock outstanding.

But, is profit maximization a reasonable goal? No; it fails for a number of reasons. It ignores the following

i. Timing: because the firm can earn a return on funds it receives, the receipt of funds sooner rather than later is preferred.

ii. Cash flows: profits do not necessarily result in cash flows available to stockholders. Owners receive cash flow either in the form of cash dividends or proceeds from selling their shares for a higher price than initially paid. A greater EPS does not necessarily mean that a firm’s board of directors will vote to increase dividend payments. Also, a higher EPS does not necessarily translate into a higher stock price. Firms sometimes experience earnings increases without any correspondingly favorable change in stock price.

iii. Risk; profit maximization also disregards risk-the chance that actual outcomes may differ from those expected. A basic premise in managerial finance is that a trade-off exists between return (cash flow) and risk. Cash flow and risk affect share prices differently: Higher cash flows are generally associated with higher share prices. Higher risk tends to result in a lower share price because the stockholder must be compensated for the greater risk. In general, stockholders are risk averse- i.e. they avoid risk. When risk is involved, stockholders expect to earn higher rates of return on investments of higher risk and lower rates on lower-risk investments. Thus, differences in risk can significantly affect the value of an investment.

3

Social responsibility:Another issue that deserves consideration is social responsibility: should businesses operate strictly in their stockholder’s best interests, or are firms also partly responsible for the welfare of their employees, customers and communities in which they operate? Certainly, firms have ethical responsibility to provide a safe working environment for their employees, to ensure that their production processes are not endangering the environment, to engage in fair hiring practices, and produce products that are safe to consumers. However, socially responsible actions such as these have costs to businesses, and are questionable whether businesses would incur these costs voluntarily. It is clear, however, that if some forms act in a socially responsible manner while other firms do not, then the socially responsible firms will be at a disadvantage in attracting investors because of the extra costs involved.

Does this mean that firms should not exercise socially responsibility? Not at all, but it does mean that most significant cost-increasing actions will have to be put on a mandatory rather a voluntary basis to ensure that the burden falls uniformly on all businesses. In spite of the fact that many socially responsible actions must be mandated by the government, in recent years numerous forms have been voluntarily taking actions, especially in the area of environmental protection, because these actions help sales. For some firms, socially responsible actions may not even be very costly, because the companies often heavily advertise such actions, and many consumers prefers to by from socially responsible companies rather than from companies that shun social responsibility.

The role of Ethics.Ethics are standards of conduct or moral behavior. Business ethics can be thought of as a company’s attitude and conduct towards its employees, customers, community and stakeholders. Today, the business community in general and the financial community in particular are developing and enforcing ethical standards. The goal of these ethical standards is to motivate businesses and market participants to adhere to both the letter and the spirit of laws and regulations concerned with business and professional practice. A firm’s commitment to business ethics can be measured by the tendency of the firm and its employees to adhere to laws and regulations relating to such factors as product safety and quality, fair employment practices, fair marketing and selling practices, the use of confidential information for personal gain, community involvement, bribery, and illegal payments to foreign governments to obtain businesses.

The implementation of a proactive ethics program is believed to enhance corporate value. An ethics program can produce a number of positive benefits: reduce potential litigation and judgment costs; maintain a positive corporate image; build shareholder confidence; and gain the loyalty, commitment and respect of all of the firm’s shareholders. Such actions, by maintaining and enhancing cash flows and reducing perceived risk (as a result of greater investor confidence) are expected to positively affect the firm’s share price. Ethical behavior is there viewed as necessary for achievement of the firm’s goal of shareholder wealth maximization.

1.3 AGENCY RELATIONSHIPS

An agency relationship can be defined as a contract under which one or more people (the principals) hire another person (the agent) to perform some service on their behalf, and delegate some decision-making authority to that agent. Within the financial management framework, agency relationships exist between shareholders and managers and between shareholders and creditors.

4

Shareholders versus managers.

We have seen that the goal of the financial manager should be to maximize the wealth of the owners of the firm. Thus management can be viewed as agents of the owners who have hired and given them decision-making authority to manage the firm for the owners benefit. Technically, any manager who owns less than 100% of the firm is to some degree of the owners.

In theory, most financial managers would agree with the goal of shareholder wealth maximization. In practice, however, managers are also concerned with their personal wealth, job security, lifestyle, and fringe benefits, such as posh offices, country club memberships, and limousines, all provided at company expense. Such concerns may make managers reluctant or unwilling to take mote than moderate risk if they perceive that too much risk may result of such a ‘satisfying’ approach (a compromise between satisfaction and maximization) is a less than a maximum return and a potential loss of wealth to the shareholders. For example, the manager may decide to lead a more relaxed lifestyle and not work as hard to maximize shareholder wealth, because less of this wealth will accrue to him/her. Also, the manager may decide to consume more perquisites, because the costs will be borne by the shareholders. The potential conflict of interest is referred to as the agency problem- the lokihood that managers may place personal goals ahead of corporate goals.

RESOLVING THE AGENCY PROBLEM

Market forcesIn recent years, institutions such as mutual funds, insurance companies and pension funds that hold large blocks of a firm’s stock have become more active in management. To ensure management competence and minimize agency problems, these institutions shareholders have actively used their votes to oust under-performing managers and replace them with more competent managers. In addition to their legal voting rights, large shareholders are able to communicate with an exert pressure on management to perform **

Another market force that has in recent years threatened management to perform in the best interest of shareholders is the possibility of a hostile takeover. A hostile takeover is the acquisition of the firm (the target) by another firm or a group of firms (the acquirer) that is not supported by management. Hostile takeovers typically occur when the acquirer feels that the target firm is being poorly managed and, as a result, is undervalued in the market place. The constant threat of a takeover motivates management to act in the best interests of the shareholders.

Agency costs:Agency costs include all costs borne by shareholders to encourage managers to maximize the firm’s stock price rather than act in their own self-interests. Agency costs are of several types:

(i) Monitoring expenditures to prevent ‘satisficing’ (rather than share price maximizing) behaviors by management. These outlays pay for auditors and control procedures that are used to assess and limit managerial behavior to those actions that tend to be in the best interests of the shareholders.

5

(ii) Expenditures to structure the organization in a way that will limit undesirable managerial behavior, such as appointing outside investors to the board of directors.

(iii) Opportunity costs resulting from the difficulties that large organizations typically have in responding to new opportunities. The firm’s necessary organizational structure, decision hierarchy, and control mechanism may cause profitable opportunities to be forgone because of management’s inability to seize upon them quickly.

Managerial incentives.These are the most powerful, popular and expensive agency costs incurred by firms. They result from structuring managerial compensation to correspond with share price maximization. The objective is to give managers incentives to act in the best interests of the shareholders and to compensate them for such actions. In addition, the resulting compensation packages allow firms to compete for and hire the best managers available. Compensation plans can be divided into two groups- incentive plans and performance plans.

Incentive plans tend to tic management compensation to share price. The most popular incentive plan is the granting of executive stock options to management. These options allow managers to purchase stock at stock at some time in the future at a given price; the options would be valuable if the market price of the stock rises above the option purchase price. The firms using these plans believe that allowing managers to purchase stock at a fixed price would provide an incentive for them to take actions which would maximize the stock’s price. Although in theory these options should motivate, they are sometimes criticized because positive management performance can be masked in a poor stock market in which share prices in general have declined due to economic and behavioral ‘market forces’ outside of management’s control.

The use of performance plans has grown in popularity in recent years due to their relative independence from market forces. These plans compensate managers on the basis of their proven performance measured by earnings per share (EPS), growth in EPS, return on assets, return on equity, and so on. Performance shares often uses in these plans. Another form of performance based compensation is cash bonuses, cash payments tied to the achievement of certain performance goals. Under performance plans, management understands in advance the formula used to determine the amount of performance shares of cash bonus it can earn during the period.

The current view:

Although experts agree that an effective way to motivate management is to tie compensation to performance, the execution of many compensation plans has been closely scrutinized in recent years. Stockholders- both individuals and institutions have publicly questioned the appropriateness of the heavy compensation packages (including salary, bonus, and long-term compensation) that many corporate executives receive. Although these sizeable compensation packages may be justified by significant increases in shareholder wealth, recent studies have failed to find a strong relationship between CEO compensation packages (without corresponding share price performance) is expected to drive down executive compensation in the future.

Shareholders and creditors

6

A second agency problem arises because of potential conflicts between stockholders and creditors. Creditors lend funds to the firm at rates that are based on:

(i) The riskiness of the firm’s existing assets.

(ii) Expectations concerning the riskiness of future assets additions

(iii) The firm’s existing capital structures (i.e. the amount of debt financing it uses)

(iv) Expectations concerning future capital structure changes

These are the factors that determine the riskiness of the firm’s cash flows and hence the safety pf its debt issues, so creditors base their required rates of return on expectations regarding these factors.

Now, suppose the stockholders, acting through management, cause the firm to take on new projects that have grater risks than were anticipated by the creditors. This increases risk will cause the required rate of return on the firm’s debt to increase, which in turn will cause the value of the outstanding debt to fall. If the riskier capital investments turn out to be successful, all of the benefits will go out to the stockholders, because the creditors get only a fixed return, but if things go sour, the bondholders will have to share the losses. Similarly, if the firm increases its level of debt effort to boost profits, the value of the old debt will decrease, because the old debt’s bankruptcy protection will be lessened by the issuance of the new debt. In both of these situations, stockholders will be gaining at the expense of the firm’s creditors.

Can and should stockholders, through their managers, agents, try to exprotriate wealth from the firm’s creditors? In general, the answer is no. first, as such attempts are made, creditors will protect themselves against such stockholders actions though restrictions in credit agreements. Second, if creditors perceive that managers are trying to take advantage of them in unethical ways, they will either refuse to deal further with them or else will require a much higher than normal rate of interest to compensate for the risks of such possible exploitation. Thus, firms, which try to deal unfairly with creditors, either loose access to the debt markets or are saddled with higher interest rates, both of which can lead to a decrease in the long run value of the stock.

In view of these constraints, it follows that the goal of maximizing shareholder wealth requires fair play with creditors: stockholders wealth depends on fair play abiding by both the letter and spirit of credit agreements. Therefore, the managers, as agents of both the creditors and the shareholders, must act in a manner which is fairly balanced between the interests of these two classes of security holders. Similarly, because of other constraints and sanctions, management actions would expropriate wealth form the firm’s employees, customers, suppliers, or community will ultimately be to the detriment of shareholders. Thus, the goal of shareholder wealth maximization requires the fair treatment of all parties, or stakeholders, whose economic position is affected by managerial actions.

OVERVIEW OF FINANCIAL MARKETS AND INSTITUTIONS:

THE FINACIAL MARKETS:

7

Financial markets provide a forum in which suppliers of funds and demanders of funds can transact business. People and organizations needing money are brought together with those having surplus funds in the financial markets. The following are some of the major types of markets:

(i) Physical (real) asset markets are those for tangible assets e.g. commodities, real estate, machinery etc. financial asset markets deal with securities eg stocks, bonds, mortgages and other claims on real assets. As well as derivative securities e.g. options, futures and others whose values are derived from changes in the prices of other financial assets.

(ii) Spot markets and future markets are terms that refer to whether the assets are being bought or sold for on the ‘spot delivery’ (within a few days) or for delivery at some future date.

(iii) Money markets are the markets for short term highly liquid debt securities. Capital markets are the markets for long-term debt and corporate stocks.

(iv) Mortgage markets deal with loans on residential, commercial, and industrial real estate, and on farmland, while consumer credit markets involve loans on appliances, education, vacation etc.

(v) Primary markets are the markets in which corporations raise new capital ie where companies sell new issues of common stock to raise capital. Secondary markets are markets in which existing, already outstanding securities are traded among investors.

FINANCIAL INSTITUTIONS

Transfer of capital between savers and those who need capital take place in three different ways:

i. Direct transfers of money and securities, which occur when a business sells its securities directly to savers, without going through any type of financial institution. The business delivers its securities to savers, who in turn give the firm the money it needs.

ii. Transfers may also go through an investment bank, which serves as a ‘middleman, and facilitates the issuance of securities. The company sells its stocks or bonds to the investment bank, which in turn sells these same securities to savers.

iii. Transfers can also be made through a financial intermediary such as a bank or mutual fund. The intermediary obtains funds from savers, issuing its own securities in exchange, and then uses the money to purchase and then hold a business’s securities. Since the intermediaries are generally large, they gain economies of scale in analyzing the creditworthiness of potential borrowers, in processing and collecting loans, and in pooling risks and thus helping individual savers diversify. Examples of intermediaries include:

a) Commercial banks

8

b) Investment banks

c) Insurance companies

d) SACCOS

e) Pension funds which are retirement plans by corporations or government agencies for their workers.

f) Mutual funds. These are companies which accept money from savers and then use these funds to buy securities issued by businesses or governmental units. They pool funds and thus reduce risks through diversification. They also achieve economies of scale, which lower the costs of analyzing securities, managing portfolios, and buying and selling securities.

SECURITIES EXCCHANGES:

Securities exchange provide the market place in which firms can raise funds through the sale of new securities and purchasers of securities can maintain liquidity by being able to resell them when necessary. Securities exchanges are commonly called stock markets, although bonds, common stock, preferred stock, and a variety of other investment vehicles are all traded on these exchanges. The two key types of securities exchanges are the organized exchange and over-the-counter exchange.

Organized securities exchanges are tangible organizations that act as secondary markets where outstanding securities are resold. Each of the larger ones occupies its own building, has specifically designated members, and has elected governing body-its board of governors.

The over-the-counter (OTC) exchange is an intangible market for the purchase and sale of securities not listed by the organized exchanges. The OTC traders, known as dealers, are linked with purchasers and sellers of securities through telecommunications networks that provide current bid and ask prices of the actively mark-up or profit. The OTC market thus included the relatively few dealers who hold inventories of OTC securities and are said to ‘make a market’ in these securities, the several brokers who act as agents in bringing these dealers together with investors, and the computers, terminals and electronic network that provide a communications link between dealers and brokers.

Securities exchanges, thus, create continuous liquid markets in which firms can obtain needed financing. They also create efficient markets that allocate funds to their most productive uses. This is especially true for securities that are actively traded on major exchanges, where the competition among wealth-maximizing investors determines and publicizes prices that are believed to be close to their true value. The competitive market created by the major securities exchanges provided a forum in which share price is continuously adjusted to changing demand and supply conditions.

EFFICIENT MARKETS

9

An efficient capital market is one in which security prices adjust rapidly to the arrival of new information and therefore, the current prices of securities reflect all information about the security.

The efficient market is defined as “A market having a large number of rational profit maximisers, actively competing with each trying to predict future market values of individual securities, and where important current information is almost freely available to all participants”.The Efficient Market Hypothesis states that at any given time, security prices fully reflect all available information. The implications of the efficient market hypothesis are truly profound. Most individuals that buy and sell securities (stocks in particular), do so under the assumption that the securities they are buying are worth more than the price that they are paying, while securities that they are selling are worth less than the selling price. But if markets are efficient and current prices fully reflect all information, then buying and selling securities in an attempt to outperform the market will effectively be a game of chance rather than skill

Securities markets are flooded with thousands of intelligent, well-paid, and well-educated investors seeking under and over-valued securities to buy and sell. The more participants and the faster the dissemination of information, the more efficient a market should be.

The debate about efficient markets has resulted in hundreds and thousands of empirical studies attempting to determine whether specific markets are in fact "efficient" and if so to what degree. Many novice investors are surprised to learn that a tremendous amount of evidence supports the efficient market hypothesis. Early tests of the EMH focused on technical analysis and it is chartists whose very existence seems most challenged by the EMH. And in fact, the vast majority of studies of technical theories have found the strategies to be completely useless in predicting securities prices. However, researchers have documented some technical anomalies that may offer some hope for technicians, although transactions costs may reduce or eliminate any advantage.

Researchers have also uncovered numerous other stock market anomalies that seem to contradict the efficient market hypothesis. The search for anomalies is effectively the search for systems or patterns that can be used to outperform passive and/or buy-and-hold strategies. Theoretically though, once an anomaly is discovered, investors attempting to profit by exploiting the inefficiency should result its disappearance. In fact, numerous anomalies that have been documented via back-testing have subsequently disappeared or proven to be impossible to exploit because of transactions costs.

The paradox of efficient markets is that if every investor believed a market was efficient, then the market would not be efficient because no one would analyze securities. In effect, efficient markets depend on market participants who believe the market is inefficient and trade securities in an attempt to outperform the market.

In reality, markets are neither perfectly efficient nor completely inefficient. All markets are efficient to a certain extent, some more so than others. Rather than

being an issue of black or white, market efficiency is more a matter of shades of gray. In markets with substantial impairments of efficiency, more knowledgeable investors can strive to outperform less knowledgeable ones. Government bond markets for instance, are considered to be extremely efficient. Most researchers consider large capitalization stocks to also be very efficient, while small capitalization stocks and international stocks are considered by some to be less efficient. Real estate and venture capital, which don't have fluid and continuous markets, are considered to be less efficient because different participants may have varying amounts and quality of information.

Market efficiency is a description of how prices in competitive markets respond to new information.. Very soon the meat is gone, leaving only the worthless bone behind, and the water returns to normal. Similarly, when new information reaches a competitive market there is much turmoil as investors buy and sell securities in response to the news, causing prices to change. Once prices adjust, all that is left of the information is the worthless bone. No amount of gnawing on the bone will yield any more meat, and no further study of old information will yield any more valuable intelligence."

There are three forms of the efficient market hypothesis

1. The "Weak" form asserts that all past market prices and data are fully reflected in securities prices. In other words, technical analysis is of no use.

2. The "Semistrong" form asserts that all publicly available information is fully reflected in securities prices. In other words, fundamental analysis is of no use.

3. The "Strong" form asserts that all information is fully reflected in securities prices. In other words, even insider information is of no use.

"

The Value of an Efficient Market It is important that stock/share markets are efficient for at least three reasons:To encourage share buying – accurate pricing is required if individuals are going to be encouraged to invest in private enterprise. If shares are incorrectly priced many savers will refuse to invest because of a fear that when they come to sell the price may be perverse and may not represent the fundamental attractions of the firm. This will seriously reduce the availability of funds to companies and inhibit growth. Investors need to know they are paying a fair price and that they will be able to sell at a fair price – that the market is a “fair game”.To give correct signals to company managers – Since the maximization of shareholder wealth can be represented by the share price in an efficient market, sound financial decision-making relies on the correct pricing of the company’s shares. In implementing a shareholder wealth-enhancing decision the manager will need to be assured that the implication of the decision is accurately signalled to shareholders and to management through a rise in the share price. It is important that managers receive feedback on their decisions from the share market so that they are encouraged to pursue shareholder wealth strategies.To help allocate resources – allocation efficiency requires both operating efficiency and pricing efficiency. If a poorly run company in a declining industry has highly valued shares because the stock market is not pricing correctly then this firm will be able to issue new shares, and thus attract more of society’s savings for use within its business. This would be wrong for society as the funds would be better used elsewhere.

CHAPTER 2- RISK AND RETURN2.1 INTRODUCTIONTo maximize share price, the financial manager must learn to assess two key determinants: risk and return. Each financial decision presents certain risk and return characteristics, and the unique combination of these characteristics has an impact on share price.

In the most basic sense, risk is the chance of financial loss. Assets having greater chances of loss are viewed as more risky than those with lesser chances of loss. More formally, the term risk is used interchangeably with uncertainty to refer to the variability of returns associated with a given asset.

12

The return is the total gain or loss experienced on an investment over a given period of time. It is commonly measured as the change in value plus any cash distributions during the period, expressed as a percentage of the rate of return earned on any asset over period t, is commonly defined as:

Kt = P t – P t-1 + Ct Pt-1

Where K is the actual or expected rate of return during period t Pt Is the price (value) of an asset at time t Pt-1 Is the price of an asset at time t-1

Ct Is the cash flow received from the asset investment in the time period t-1 to t.

RISK PREFERENCEFeelings about risk differ among managers and firms. The three basic risk preference behaviours are:

For the risk – indifferent manager, the return does not change as risk increases. In essence, no change in return would be required for the increase in risk clearly, this attitude is nonsensical in almost any business context.

For the risk – averse manager, the required return increase in risk because they shy away from risk, these managers require higher expected returns to compensate them for taking greater risk.

For the risk – seeking manager, required return decreases for an increase in risk. Theoretically, because they enjoy risk, these managers are willing to give up some return to take more risk. However, such behaviour would not be likely to benefit them.

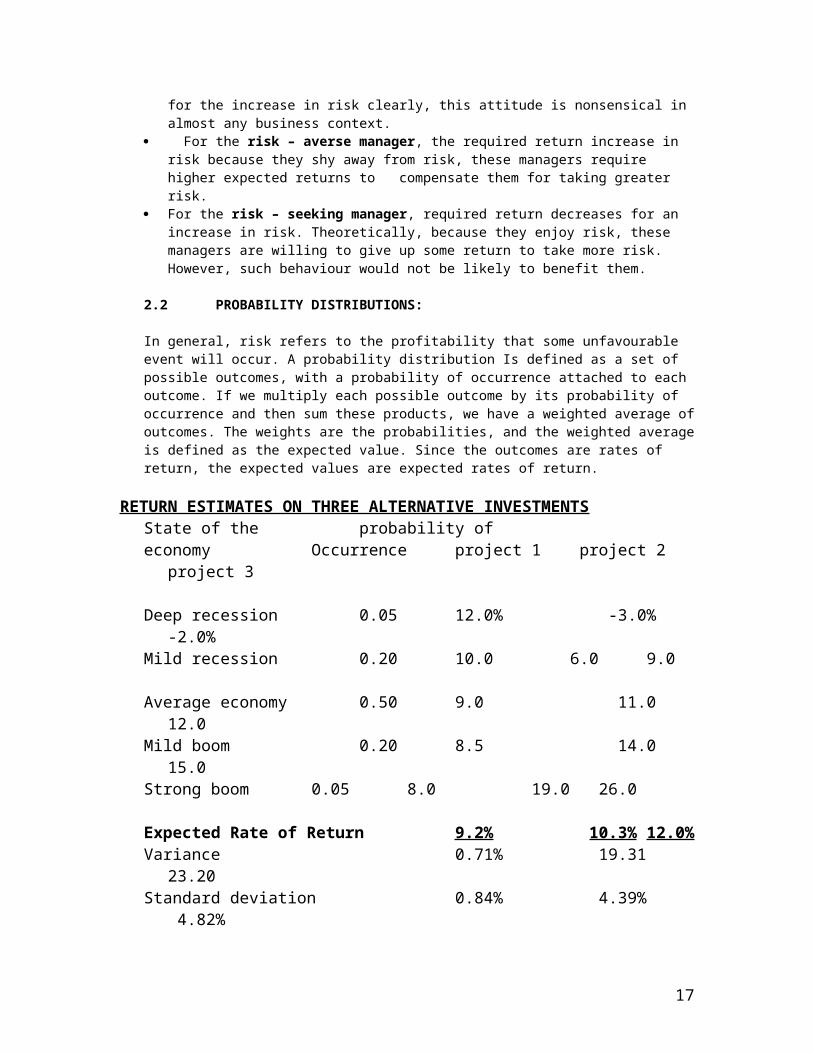

2.2 PROBABILITY DISTRIBUTIONS:

In general, risk refers to the profitability that some unfavourable event will occur. A probability distribution Is defined as a set of possible outcomes, with a probability of occurrence attached to each outcome. If we multiply each possible outcome by its probability of occurrence and then sum these products, we have a weighted average of outcomes. The weights are the probabilities, and the weighted average is defined as the expected value. Since the outcomes are rates of return, the expected values are expected rates of return.

RETURN ESTIMATES ON THREE ALTERNATIVE INVESTMENTSState of the probability ofeconomy Occurrence project 1 project 2 project 3

The expected rates of return on the other two investment alternatives can be similarly calculated and are shown in the table above.

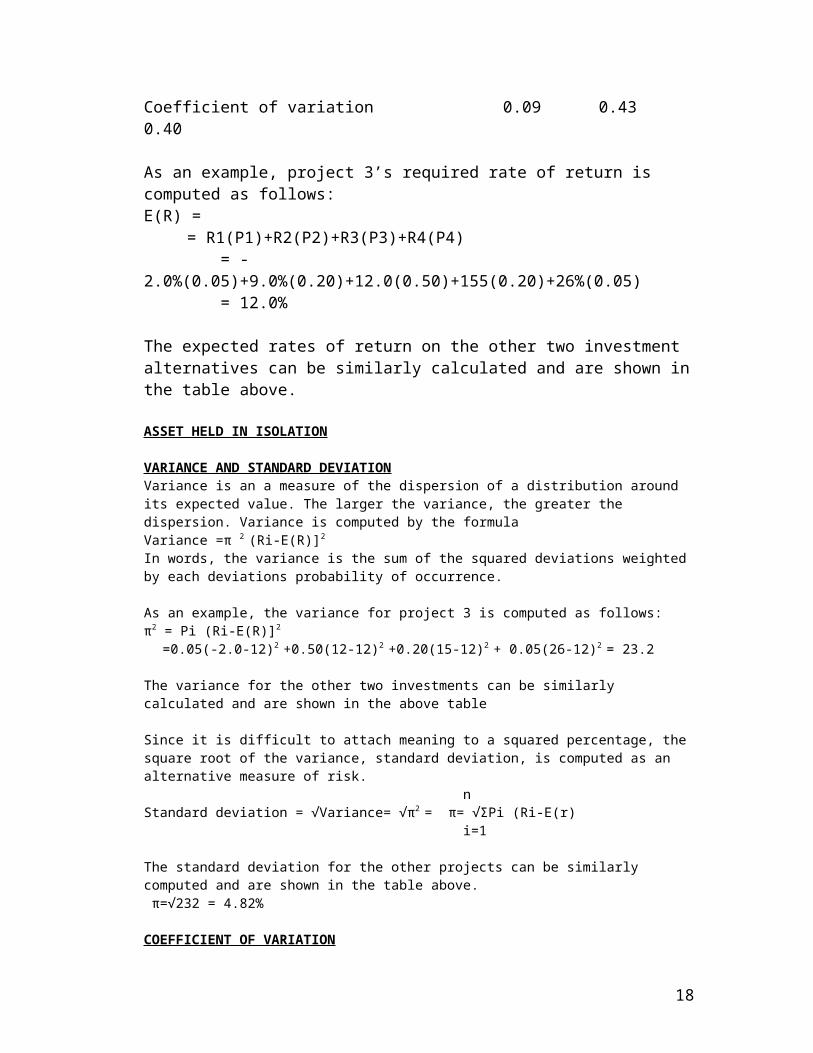

ASSET HELD IN ISOLATION VARIANCE AND STANDARD DEVIATIONVariance is an a measure of the dispersion of a distribution around its expected value. The larger the variance, the greater the dispersion. Variance is computed by the formula Variance =π 2 (Ri-E(R)]2

In words, the variance is the sum of the squared deviations weighted by each deviations probability of occurrence.

As an example, the variance for project 3 is computed as follows:π2 = Pi (Ri-E(R)]2

The variance for the other two investments can be similarly calculated and are shown in the above table

Since it is difficult to attach meaning to a squared percentage, the square root of the variance, standard deviation, is computed as an alternative measure of risk.

The standard deviation for the other projects can be similarly computed and are shown in the table above. π=√232 = 4.82%

COEFFICIENT OF VARIATION

The coefficient of variation, CV, is a measure of relative risk that is useful in comparing the risk of assets with different expected returns.

CV=Standard deviation = π Expected return E(R)

The CV shows the risk per unit of return, and provides a more meaningful basis for comparison when the expected returns on two alternatives are not the same.

The CV of project 3 is calculated as:CV= 4.82% = 0.40

12.0%

The CV for the other two investments can be similarly computed and are shown in the table above.

14

THE MEAN –VARIANCE CRITERION: The mean –variance criterion is one possible decision rule that can be used to choose among possible investment alternatives. This criteria is based on two assumptions:

1. The decision maker is risk averse.2. The distributions being evaluated are approximately normal distribution.

The first assumption is certainly true for the average investor: the second condition generally holds well for securities such as stocks and bonds, but it does not always hold for physical asset investments. The mean – variance criterion is based on a comparison of expected returns and standard deviations and can be stated symbolically as follows:

Alternative X is preferred to alternative Y if and only if either E(R)X > E(R)Y AND SD(X)< SD(Y) E(R)= Expected ReturnORE(R)>E(R)Y AND SD(X)SD(Y) <SD = Standard Deviation

Applying this criterion to the three investments above, we find that no one alternative is necessarily preferred to any other alternative, because the alternatives with the higher variances also have higher expected rates of return.

However, application of the mean – variance criterion to non – normal distributions may result in an anomaly called the mean variance paradox, a situation in which the mean variance criterion leads to incorrect decisions. For example, we have concluded that neither project 2 nor 3 is preferred under the mean variance criterion. But, project 3 is clearly preferred to 2 because it has a higher outcome for each possible state of economy. Thus, regardless of which state of economy occurs we would always get a higher rate of return from project 3 than from 2 i.e. project 3 dominates 2 as an investment.

What about a choice between projects 1 and 3?Theoretically, the choice should be made on the basis of risk aversion of the owners of the firm. However, financial managers generally cannot measure stockholders’ risk aversion, so managers often substitute their own preferences, along with other more tangible factors. For example, project 3 has a probability, albeit low, of rate of return of – 20% i.e. a loss. Perhaps, the financial manager is unwilling to accept any chance of a loss, and hence would reject that alternative. Also, the financial manager must consider his or her confidence in the estimated rates of return. Is he/ she equally confident of the accuracy of the probability distributions of all three alternatives or is there reason to be more confident in one alternative or another? If the decision maker “doesn’t trust the numbers”, then he/she may well reject what seems on paper to be the best alternative.

A portfolio is a combination or collection of assets or securities.

EXPECTED RETURN FOR A PORTFOLIO

The expected rate for a portfolio is simply the weighted average of the expected rates of Return for the individual investments in the portfolio. The weights are the proportions of the total value of the investment. E(Rp) = Σ Wi Ri

i=1

15

Where W1 = is the percent of the portfolio invested in asset I Ri – is the expected rate of return for asset i

2.3 RISK OF A PORTFOLIOTwo basic concepts in statistics, co-variance and correlation, must be understood in order to understand portfolio risk.

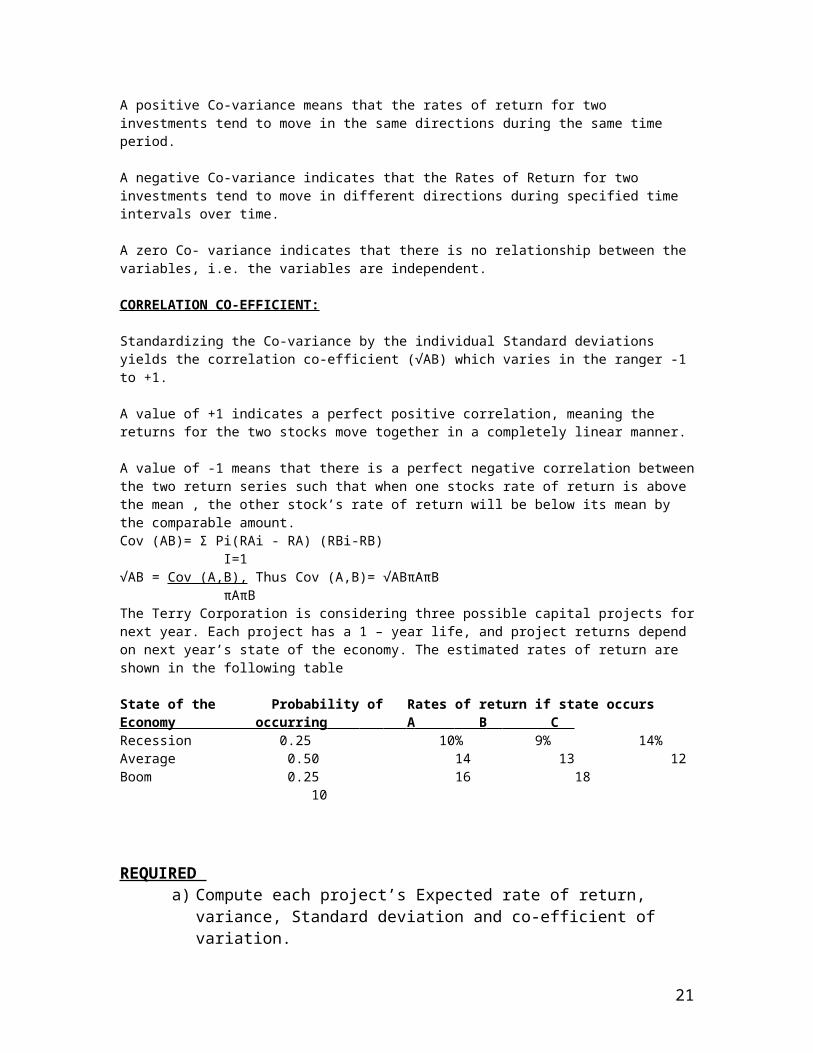

CO- VARIANCE of Returns:Co-Variance is a measure of the degree to which two variables “move together” over time. In portfolio analysis, we are usually concerned with co-Variance of rates of Return.A positive Co-variance means that the rates of return for two investments tend to move in the same directions during the same time period. A negative Co-variance indicates that the Rates of Return for two investments tend to move in different directions during specified time intervals over time.

A zero Co- variance indicates that there is no relationship between the variables, i.e. the variables are independent.

CORRELATION CO-EFFICIENT:

Standardizing the Co-variance by the individual Standard deviations yields the correlation co-efficient (√AB) which varies in the ranger -1 to +1.

A value of +1 indicates a perfect positive correlation, meaning the returns for the two stocks move together in a completely linear manner.

A value of -1 means that there is a perfect negative correlation between the two return series such that when one stocks rate of return is above the mean , the other stock’s rate of return will be below its mean by the comparable amount.Cov (AB)= Σ Pi(RAi - RA) (RBi-RB) I=1√AB = Cov (A,B), Thus Cov (A,B)= √ABπAπB πAπBThe Terry Corporation is considering three possible capital projects for next year. Each project has a 1 – year life, and project returns depend on next year’s state of the economy. The estimated rates of return are shown in the following table

State of the Probability of Rates of return if state occursEconomy occurring A B C Recession 0.25 10% 9% 14%Average 0.50 14 13 12Boom 0.25 16 18 10

REQUIRED a) Compute each project’s Expected rate of return, variance, Standard deviation

and co-efficient of variation.b) Apply the Mean – Variance criterion to the alternative projects. Do any of the

projects dominate any of the others according to this criterion?

16

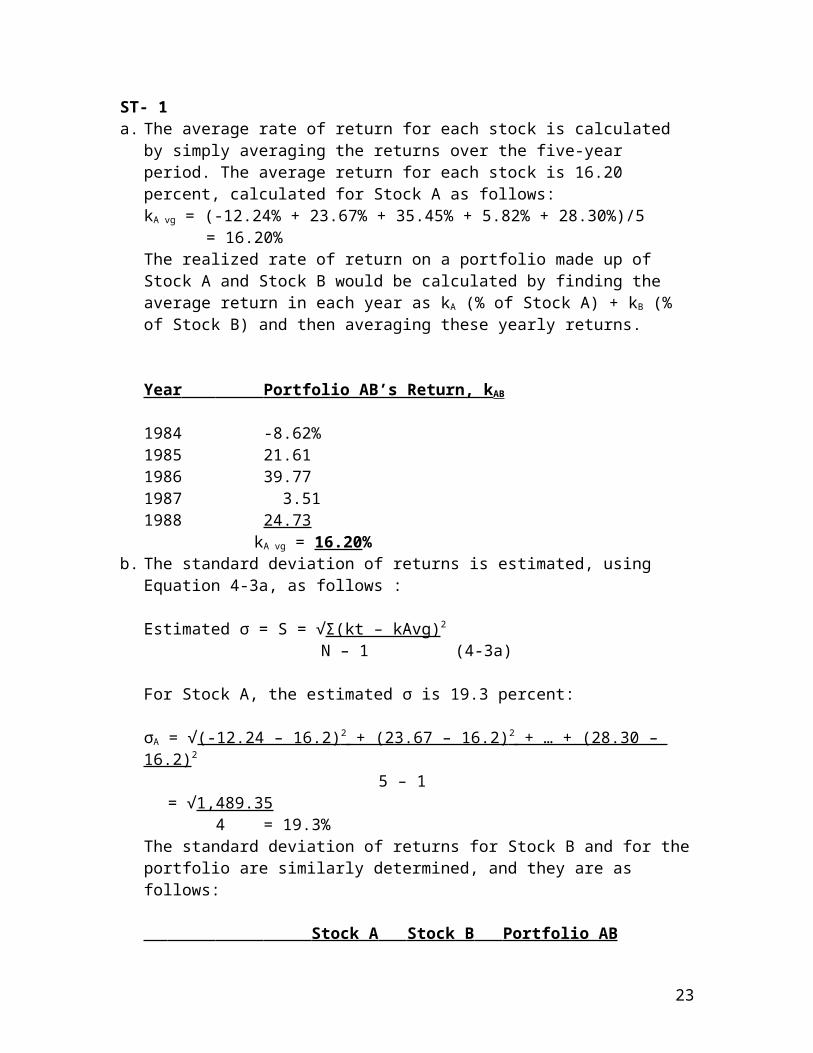

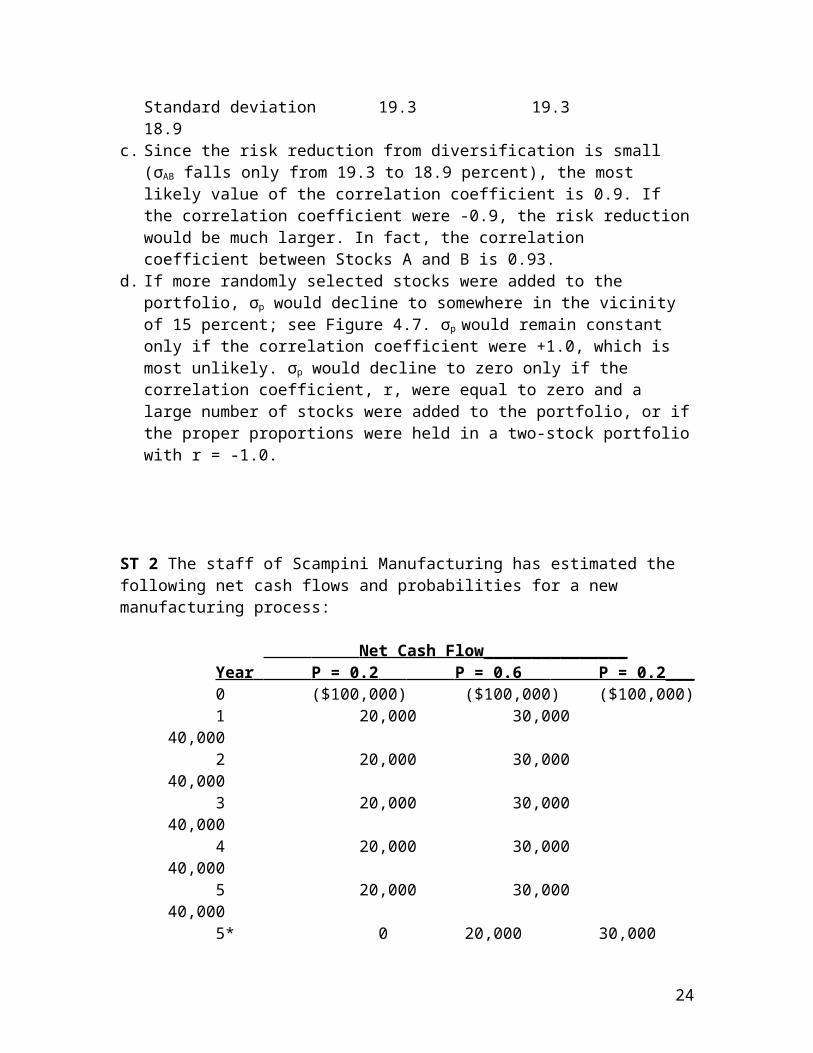

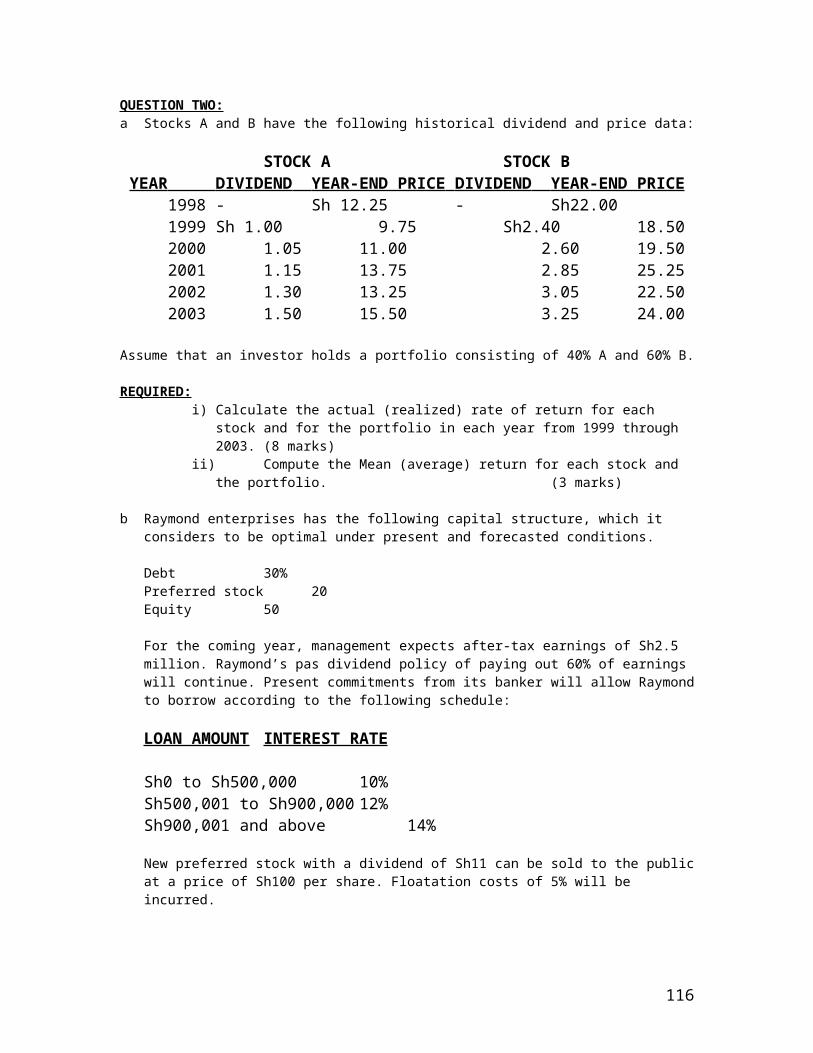

QUESTIONS AND ANSWERSST-1 Stocks A and B has the following historical returns:

Calculate the average rate of return for each stock during the period 1984 through 1988. Assume that someone held a portfolio consisting of 50 percent of Stock A and 50 percent of Stock B. What would have been the realized rate of return on the portfolio in each year from 1984 through 1988? What would have been the average return on the portfolio during this period?Now calculate the standard deviation of returns for each stock and for the portfolio.On the basis of the extent to which the portfolio has a lower risk than the stocks held individually, would you guess that the correlation coefficient between returns on the two stocks is closer to 0.9 or to -0.9?If you added more stocks at random to the portfolio, what is the most accurate statement of what would happen to σp?

σp would remain constant.σp would decline to somewhere in the vicinity of 15 percent.σp would decline to zero if enough stocks were included

SOLUTION ST- 1a. The average rate of return for each stock is calculated by simply

averaging the returns over the five-year period. The average return for each stock is 16.20 percent, calculated for Stock A as follows:kA vg = (-12.24% + 23.67% + 35.45% + 5.82% + 28.30%)/5

= 16.20%The realized rate of return on a portfolio made up of Stock A and Stock B would be calculated by finding the average return in each year as kA (% of Stock A) + kB (% of Stock B) and then averaging these yearly returns.

Year Portfolio AB’s Return, k AB

1984 -8.62%

17

1985 21.611986 39.771987 3.511988 24.73

kA vg = 16.20%b. The standard deviation of returns is estimated, using Equation 4-3a,

4 = 19.3%The standard deviation of returns for Stock B and for the portfolio are similarly determined, and they are as follows:

Stock A Stock B Portfolio AB Standard deviation 19.3 19.3 18.9

c. Since the risk reduction from diversification is small (σAB falls only from 19.3 to 18.9 percent), the most likely value of the correlation coefficient is 0.9. If the correlation coefficient were -0.9, the risk reduction would be much larger. In fact, the correlation coefficient between Stocks A and B is 0.93.

d. If more randomly selected stocks were added to the portfolio, σp would decline to somewhere in the vicinity of 15 percent; see Figure 4.7. σp would remain constant only if the correlation coefficient were +1.0, which is most unlikely. σp would decline to zero only if the correlation coefficient, r, were equal to zero and a large number of stocks were added to the portfolio, or if the proper proportions were held in a two-stock portfolio with r = -1.0.

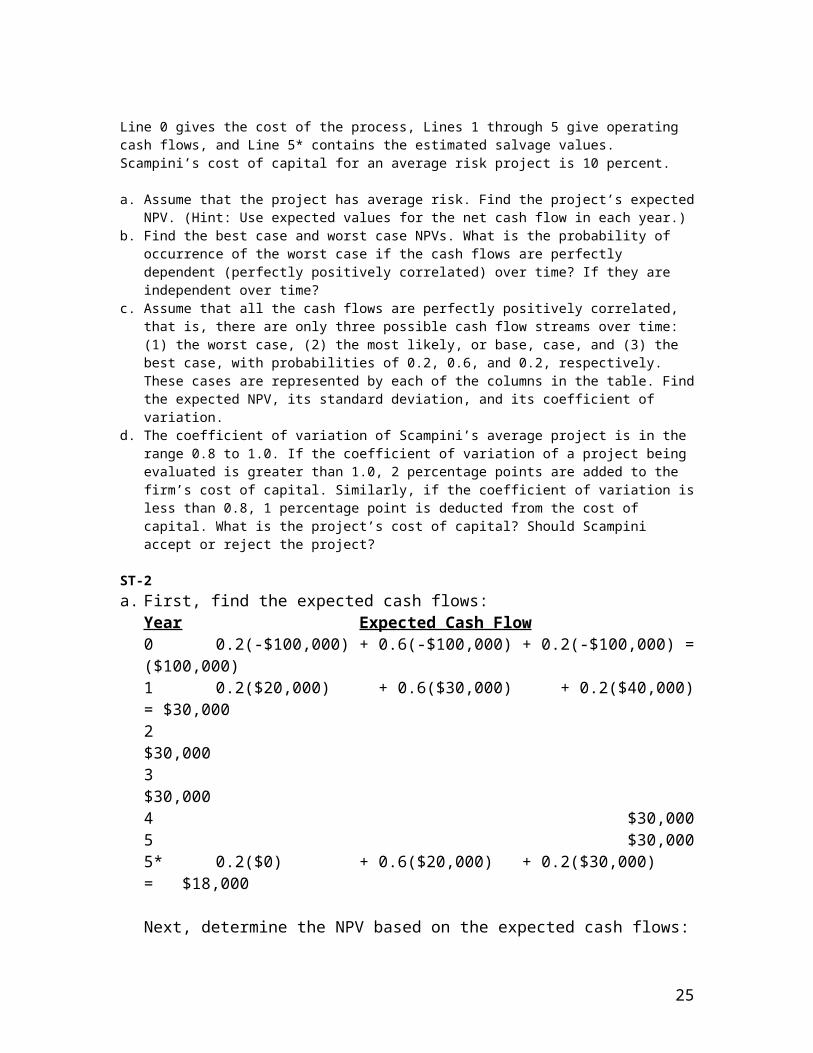

ST 2 The staff of Scampini Manufacturing has estimated the following net cash flows and probabilities for a new manufacturing process:

Net Cash Flow_______________ Year P = 0.2 P = 0.6 P = 0.2___ 0 ($100,000) ($100,000) ($100,000)1 20,000 30,000 40,0002 20,000 30,000 40,000

Line 0 gives the cost of the process, Lines 1 through 5 give operating cash flows, and Line 5* contains the estimated salvage values. Scampini’s cost of capital for an average risk project is 10 percent.

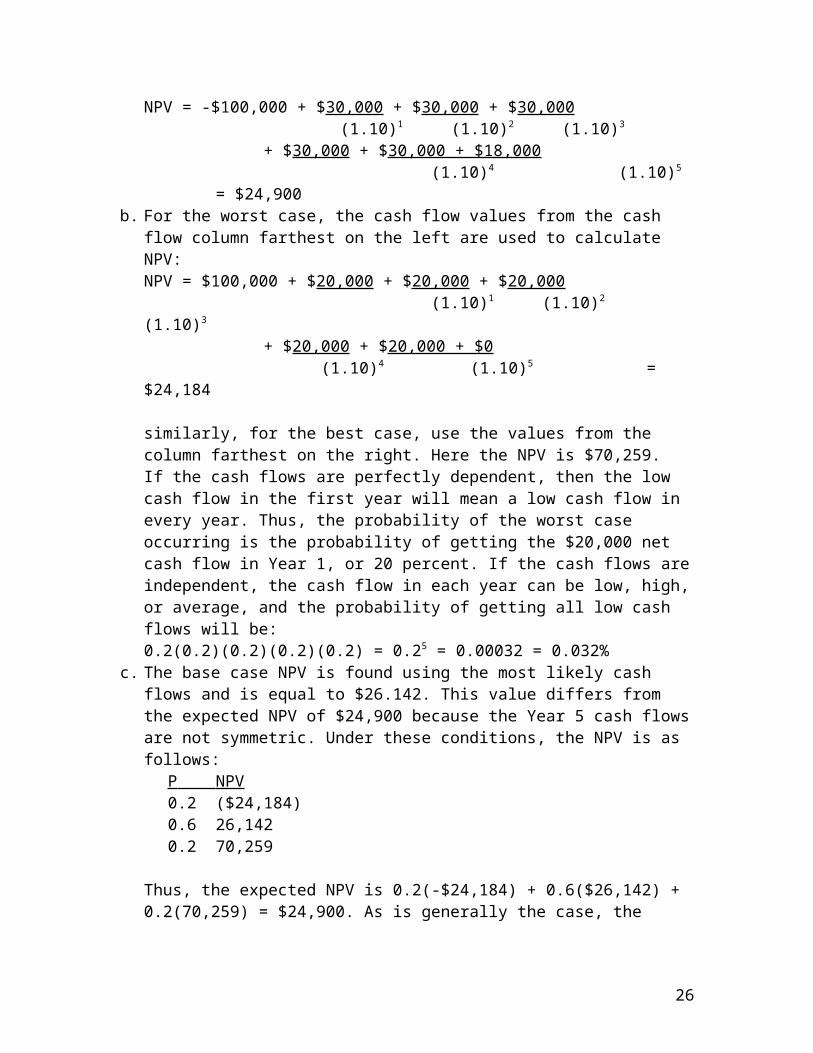

a. Assume that the project has average risk. Find the project’s expected NPV. (Hint: Use expected values for the net cash flow in each year.)

b. Find the best case and worst case NPVs. What is the probability of occurrence of the worst case if the cash flows are perfectly dependent (perfectly positively correlated) over time? If they are independent over time?

c. Assume that all the cash flows are perfectly positively correlated, that is, there are only three possible cash flow streams over time: (1) the worst case, (2) the most likely, or base, case, and (3) the best case, with probabilities of 0.2, 0.6, and 0.2, respectively. These cases are represented by each of the columns in the table. Find the expected NPV, its standard deviation, and its coefficient of variation.

d. The coefficient of variation of Scampini’s average project is in the range 0.8 to 1.0. If the coefficient of variation of a project being evaluated is greater than 1.0, 2 percentage points are added to the firm’s cost of capital. Similarly, if the coefficient of variation is less than 0.8, 1 percentage point is deducted from the cost of capital. What is the project’s cost of capital? Should Scampini accept or reject the project?

similarly, for the best case, use the values from the column farthest on the right. Here the NPV is $70,259.If the cash flows are perfectly dependent, then the low cash flow in the first year will mean a low cash flow in every year. Thus, the probability of the worst case occurring is the probability of getting the $20,000 net cash flow in Year 1, or 20 percent. If the cash flows are independent, the cash flow in each year can be low, high, or average, and the probability of getting all low cash flows will be:0.2(0.2)(0.2)(0.2)(0.2) = 0.25 = 0.00032 = 0.032%

c. The base case NPV is found using the most likely cash flows and is equal to $26.142. This value differs from the expected NPV of $24,900 because the Year 5 cash flows are not symmetric. Under these conditions, the NPV is as follows:

P NPV 0.2 ($24,184)0.6 26,1420.2 70,259

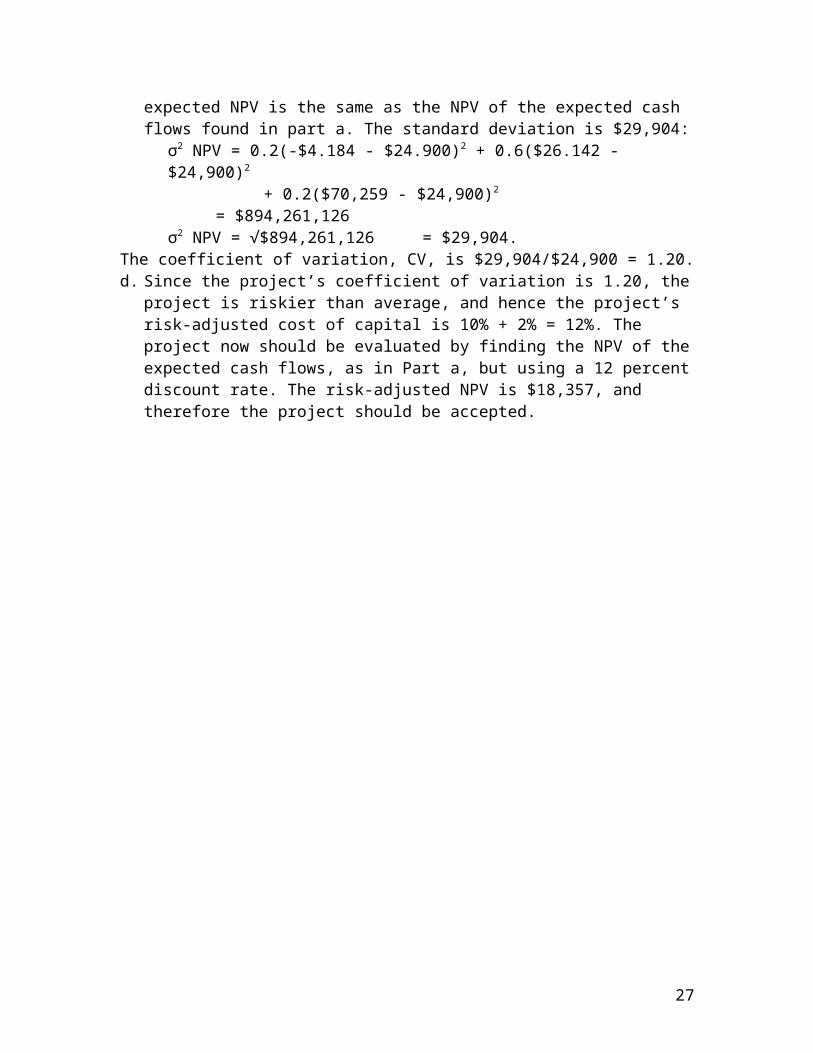

Thus, the expected NPV is 0.2(-$24,184) + 0.6($26,142) + 0.2(70,259) = $24,900. As is generally the case, the expected NPV is the same as the NPV of the expected cash flows found in part a. The standard deviation is $29,904:

The coefficient of variation, CV, is $29,904/$24,900 = 1.20.d. Since the project’s coefficient of variation is 1.20, the project is

riskier than average, and hence the project’s risk-adjusted cost of capital is 10% + 2% = 12%. The project now should be evaluated by finding the NPV of the expected cash flows, as in Part a, but using a 12 percent discount rate. The risk-adjusted NPV is $18,357, and therefore the project should be accepted.

20

CHAPTER 3 - INVESTMENT DECISIONS - CAPITAL BUDGETING

3.1 INTRODUCTIONCapital budgeting is vital in marketing decisions. Decisions on investment, which take time to mature, have to be based on the returns which that investment will make. Unless the project is for social reasons only, if the investment is unprofitable in the long run, it is unwise to invest in it now. Often, it would be good to know what the present value of the future investment is, or how long it will take to mature (give returns). It could be much more profitable putting the planned investment money in the bank and earning interest, or investing in an alternative project.

The time value of money Recall that the interaction of lenders with borrowers sets an equilibrium rate of interest. Borrowing is only worthwhile if the return on the loan exceeds the cost of the borrowed funds. Lending is only worthwhile if the return is at least equal to that which can be obtained from alternative opportunities in the same risk class. The interest rate received by the lender is made up of: i) The time value of money: the receipt of money is preferred sooner rather than later. Money can be used to earn more money. The earlier the money is received, the greater the potential for increasing wealth. Thus, to forego the use of money, you must get some compensation. ii) The risk of the capital sum not being repaid. This uncertainty requires a premium as a hedge against the risk, hence the return must be commensurate with the risk being undertaken. iii) Inflation: money may lose its purchasing power over time. The lender must be compensated for the declining spending/purchasing power of money. If the lender receives no compensation, he/she will be worse off when the loan is repaid than at the time of lending the money.a) Future values/compound interest Future value (FV) is the value in dollars at some point in the future of one or more investments. FV consists of: i) the original sum of money invested, andii) the return in the form of interest.The general formula for computing Future Value is as follows: FVn = Vo (l + r)n

where Vo is the initial sum investedr is the interest raten is the number of periods for which the investment is to receive interest.Thus we can compute the future value of what Vo will accumulate to in n years when it is compounded annually at the same rate of r by using the above formula. Exercise 6.1 Future values/compound interest i) What is the future value of $10 invested at 10% at the end of 1 year?ii) What is the future value of $10 invested at 10% at the end of 5 years?We can derive the Present Value (PV) by using the formula: FVn = Vo (I + r)n By denoting Vo by PV we obtain: FVn = PV (I + r)n by dividing both sides of the formula by (I + r)n we derive:

21

Rationale for the formula: As you will see from the following exercise, given the alternative of earning 10% on his money, an individual (or firm) should never offer (invest) more than $10.00 to obtain $11.00 with certainty at the end of the year.

Exercise 6.2 Present value i) What is the present value of $11.00 at the end of one year?ii) What is the PV of $16.10 at the end of 5 years?b) Net present value (NPV) The NPV method is used for evaluating the desirability of investments or projects.

where: Ct = the net cash receipt at the end of year tIo = the initial investment outlayr = the discount rate/the required minimum rate of return on investmentn = the project/investment's duration in years.The discount factor r can be calculated using:

Examples:

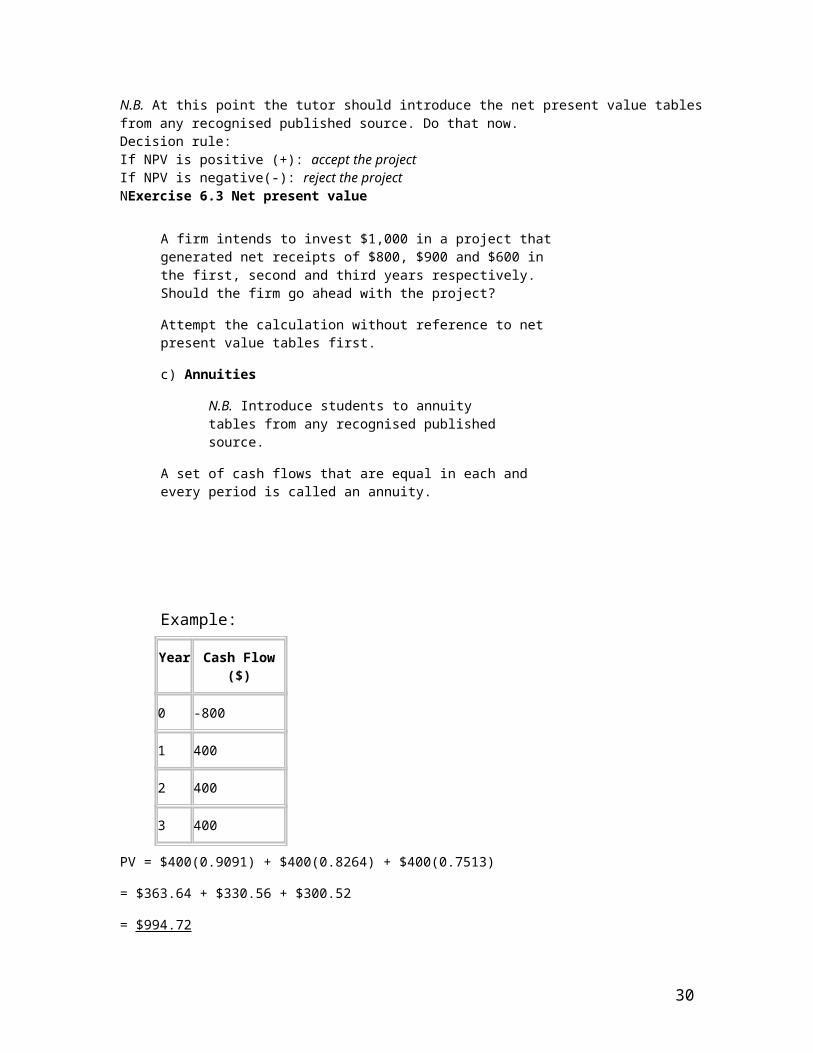

N.B. At this point the tutor should introduce the net present value tables from any recognised published source. Do that now.Decision rule: If NPV is positive (+): accept the projectIf NPV is negative(-): reject the projectNExercise 6.3 Net present value

A firm intends to invest $1,000 in a project that generated net receipts of $800, $900 and $600 in the first, second and third years respectively. Should the firm go ahead with the project?

Attempt the calculation without reference to net present value tables first.

c) Annuities

N.B. Introduce students to annuity tables from any recognised published source.

22

A set of cash flows that are equal in each and every period is called an annuity.

Example:

Year Cash Flow ($)

0 -800

1 400

2 400

3 400

PV = $400(0.9091) + $400(0.8264) + $400(0.7513)

= $363.64 + $330.56 + $300.52

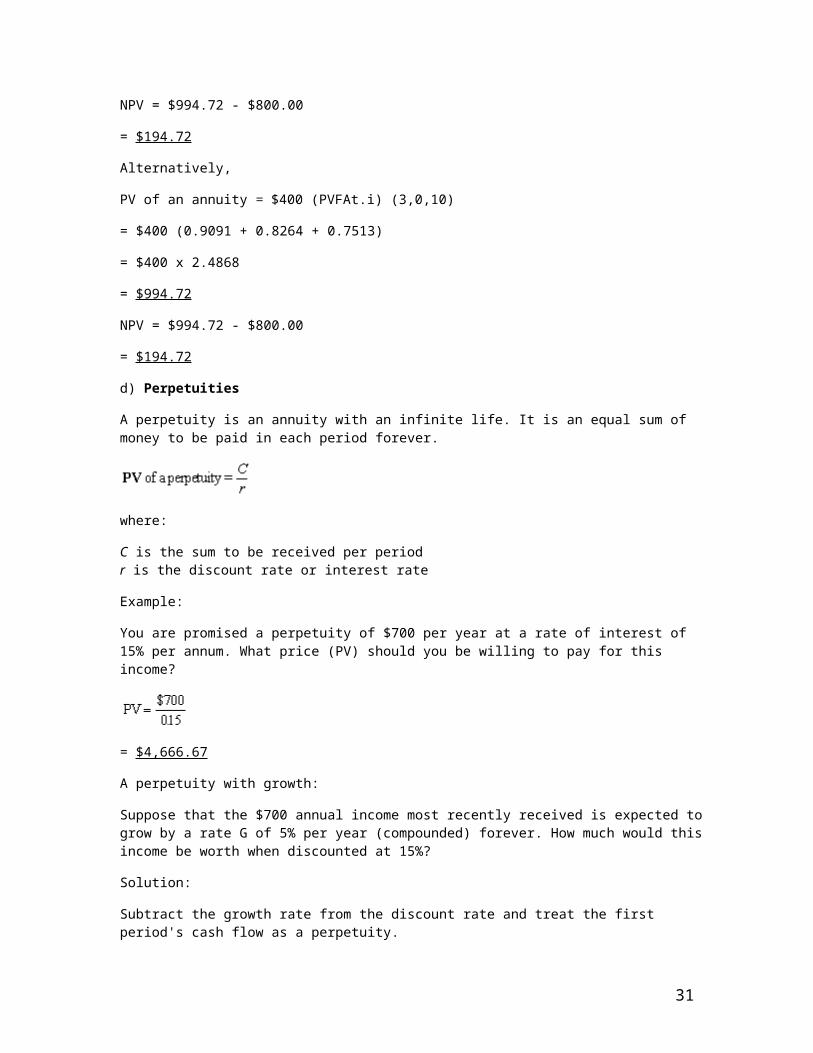

= $994.72

NPV = $994.72 - $800.00

= $194.72

Alternatively,

PV of an annuity = $400 (PVFAt.i) (3,0,10)

= $400 (0.9091 + 0.8264 + 0.7513)

= $400 x 2.4868

= $994.72

NPV = $994.72 - $800.00

= $194.72

d) Perpetuities

A perpetuity is an annuity with an infinite life. It is an equal sum of money to be paid in each period forever.

where:

23

C is the sum to be received per periodr is the discount rate or interest rate

Example:

You are promised a perpetuity of $700 per year at a rate of interest of 15% per annum. What price (PV) should you be willing to pay for this income?

= $4,666.67

A perpetuity with growth:

Suppose that the $700 annual income most recently received is expected to grow by a rate G of 5% per year (compounded) forever. How much would this income be worth when discounted at 15%?

Solution:

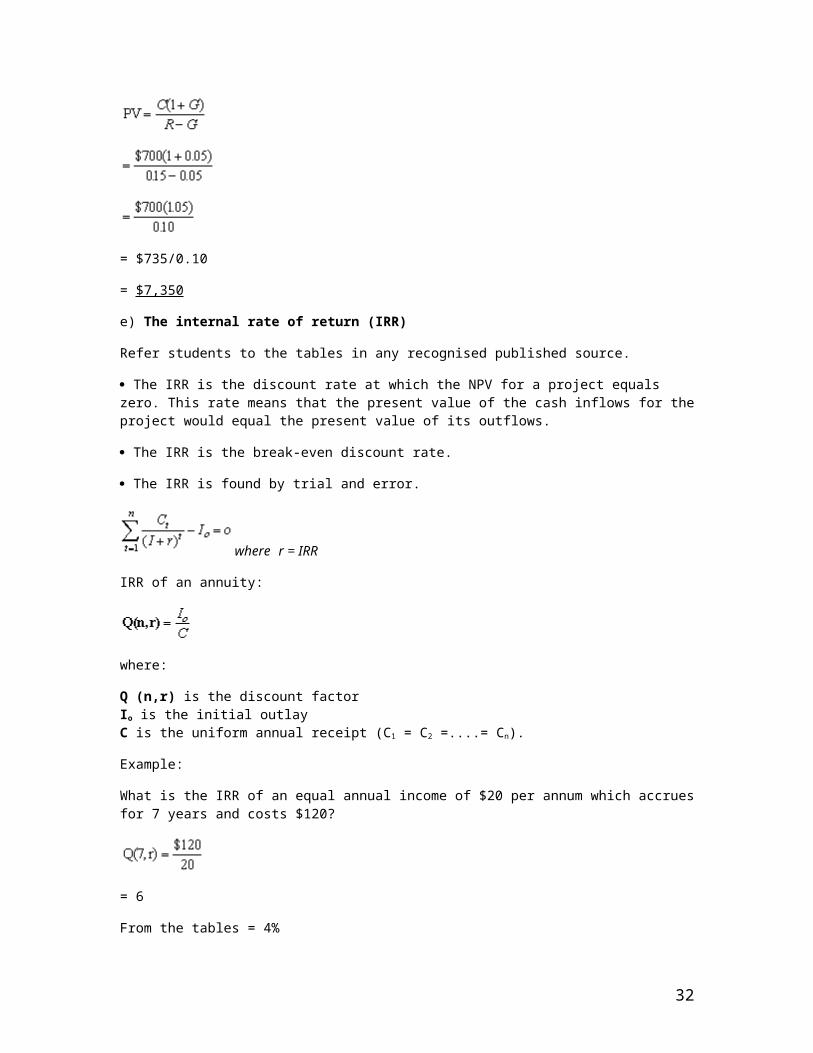

Subtract the growth rate from the discount rate and treat the first period's cash flow as a perpetuity.

= $735/0.10

= $7,350

e) The internal rate of return (IRR)

Refer students to the tables in any recognised published source.

The IRR is the discount rate at which the NPV for a project equals zero. This rate means that the present value of the cash inflows for the project would equal the present value of its outflows.

The IRR is the break-even discount rate.

The IRR is found by trial and error.

where r = IRR

IRR of an annuity:

24

where:

Q (n,r) is the discount factorIo is the initial outlayC is the uniform annual receipt (C1 = C2 =....= Cn).

Example:

What is the IRR of an equal annual income of $20 per annum which accrues for 7 years and costs $120?

= 6

From the tables = 4%

Economic rationale for IRR:

If IRR exceeds cost of capital, project is worthwhile, i.e. it is profitable to undertake. Now attempt exercise 6.4

Exercise 6.4 Internal rate of return

Find the IRR of this project for a firm with a 20% cost of capital:

YEAR CASH FLOW

$

0 -10,000

1 8,000

2 6,000

a) Try 20%b) Try 27%c) Try 29%

Net present value vs internal rate of return

Independent vs dependent projects

NPV and IRR methods are closely related because:

i) both are time-adjusted measures of profitability, andii) their mathematical formulas are almost identical.

So, which method leads to an optimal decision: IRR or NPV?

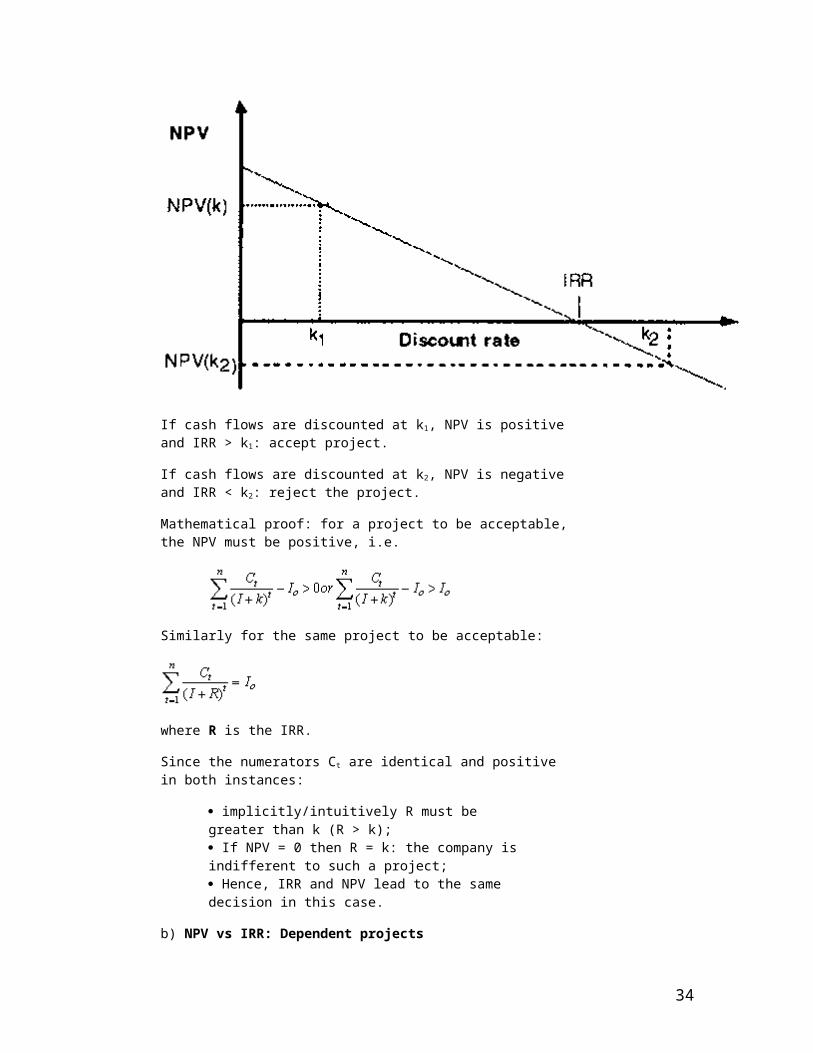

a) NPV vs IRR: Independent projects

25

Independent project: Selecting one project does not preclude the choosing of the other.

With conventional cash flows (-|+|+) no conflict in decision arises; in this case both NPV and IRR lead to the same accept/reject decisions.

Figure 6.1 NPV vs IRR Independent projects

If cash flows are discounted at k1, NPV is positive and IRR > k1: accept project.

If cash flows are discounted at k2, NPV is negative and IRR < k2: reject the project.

Mathematical proof: for a project to be acceptable, the NPV must be positive, i.e.

Similarly for the same project to be acceptable:

where R is the IRR.

Since the numerators Ct are identical and positive in both instances:

implicitly/intuitively R must be greater than k (R > k); If NPV = 0 then R = k: the company is indifferent to such a project; Hence, IRR and NPV lead to the same decision in this case.

26

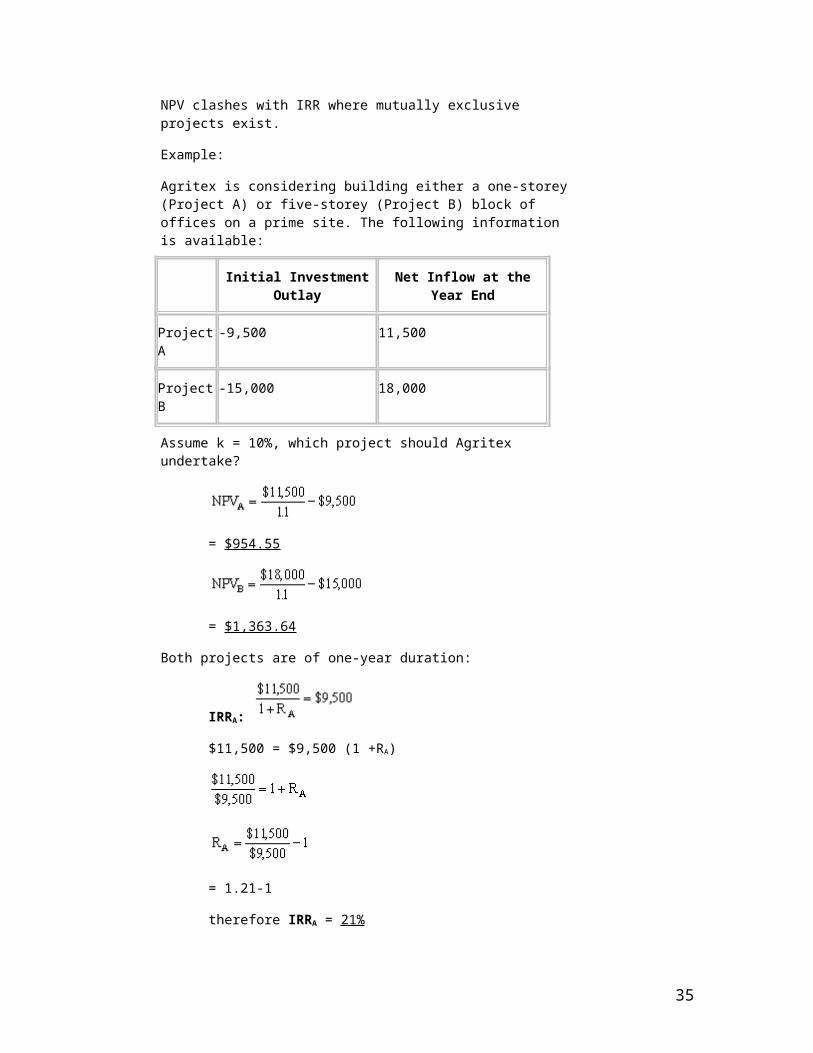

b) NPV vs IRR: Dependent projects

NPV clashes with IRR where mutually exclusive projects exist.

Example:

Agritex is considering building either a one-storey (Project A) or five-storey (Project B) block of offices on a prime site. The following information is available:

Initial Investment Outlay Net Inflow at the Year End

Project A -9,500 11,500

Project B -15,000 18,000

Assume k = 10%, which project should Agritex undertake?

= $954.55

= $1,363.64

Both projects are of one-year duration:

IRRA:

$11,500 = $9,500 (1 +RA)

= 1.21-1

therefore IRRA = 21%

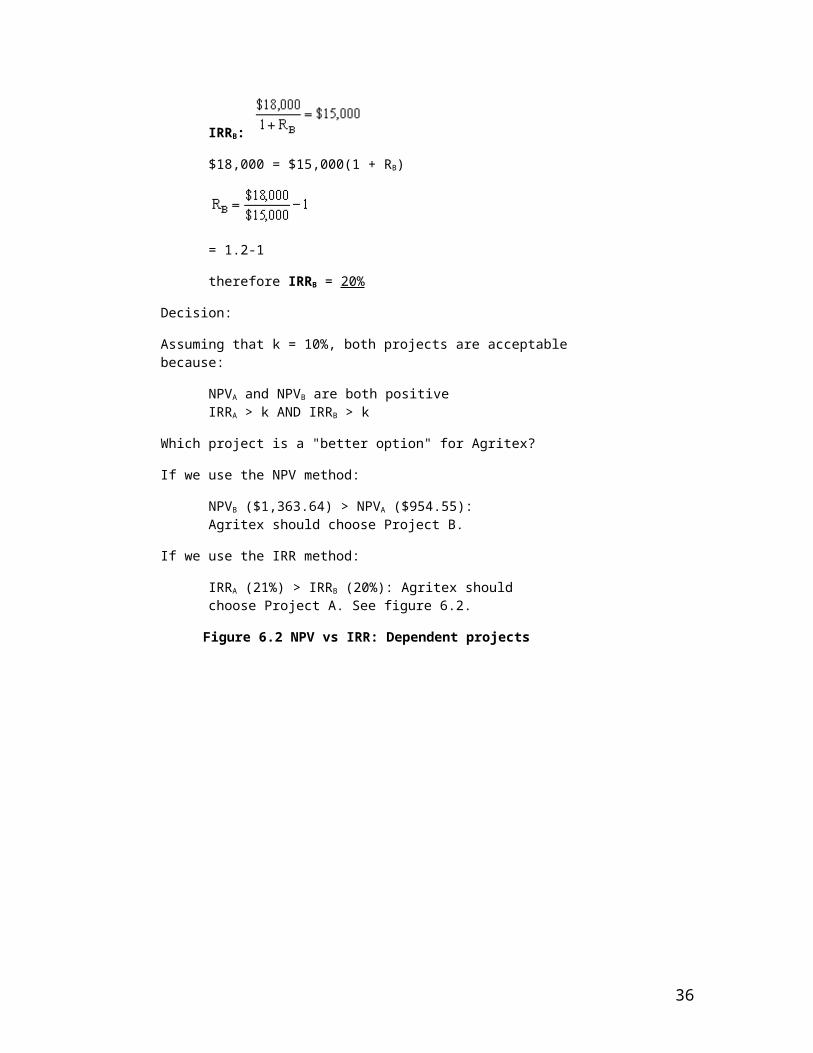

IRRB:

$18,000 = $15,000(1 + RB)

27

= 1.2-1

therefore IRRB = 20%

Decision:

Assuming that k = 10%, both projects are acceptable because:

NPVA and NPVB are both positiveIRRA > k AND IRRB > k

Which project is a "better option" for Agritex?

If we use the NPV method:

NPVB ($1,363.64) > NPVA ($954.55): Agritex should choose Project B.

If we use the IRR method:

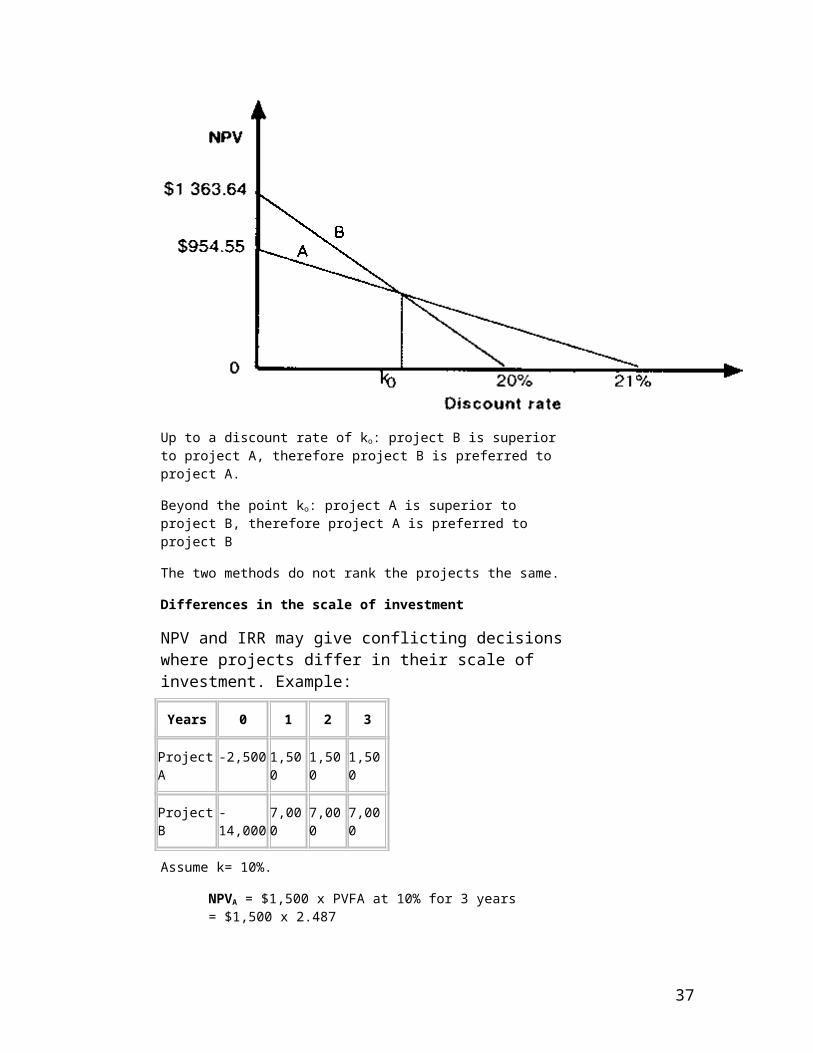

IRRA (21%) > IRRB (20%): Agritex should choose Project A. See figure 6.2.

Figure 6.2 NPV vs IRR: Dependent projects

Up to a discount rate of ko: project B is superior to project A, therefore project B is preferred to project A.

Beyond the point ko: project A is superior to project B, therefore project A is preferred to project B

The two methods do not rank the projects the same.

Differences in the scale of investment

28

NPV and IRR may give conflicting decisions where projects differ in their scale of investment. Example:

Years 0 1 2 3

Project A -2,500 1,500 1,500 1,500

Project B -14,000 7,000 7,000 7,000

Assume k= 10%.

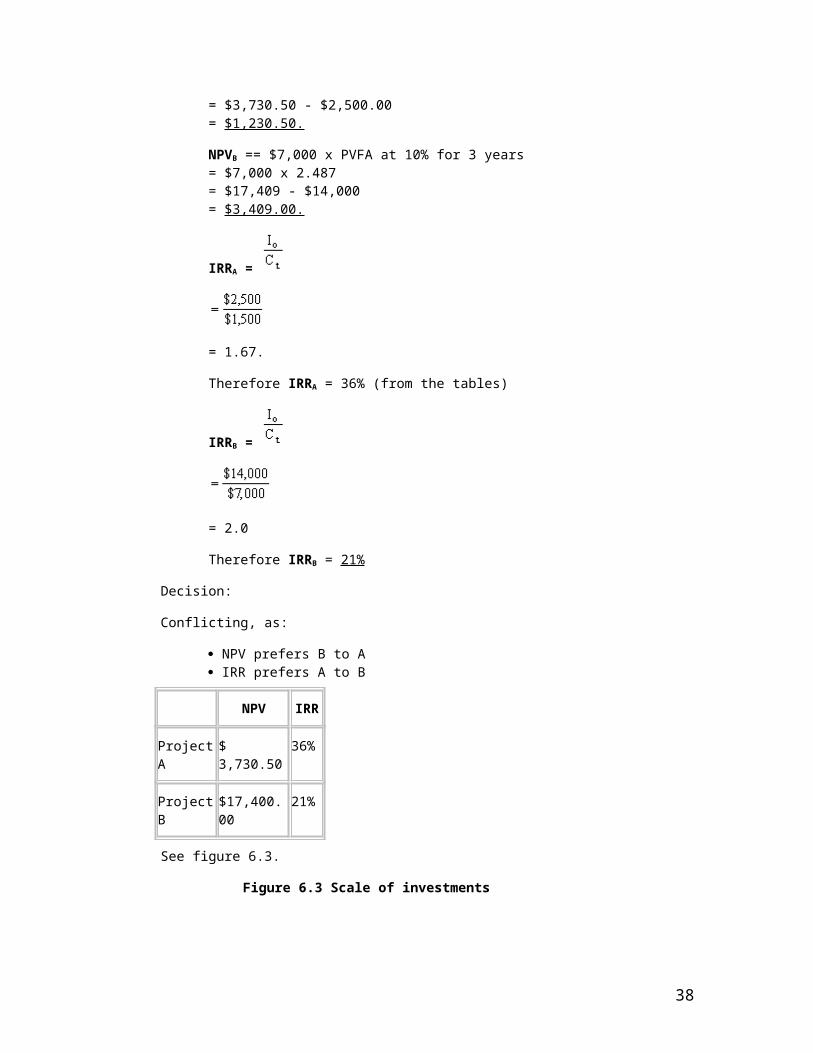

NPVA = $1,500 x PVFA at 10% for 3 years= $1,500 x 2.487= $3,730.50 - $2,500.00= $1,230.50.

NPVB == $7,000 x PVFA at 10% for 3 years= $7,000 x 2.487= $17,409 - $14,000= $3,409.00.

IRRA =

= 1.67.

Therefore IRRA = 36% (from the tables)

IRRB =

= 2.0

Therefore IRRB = 21%

Decision:

Conflicting, as:

NPV prefers B to A IRR prefers A to B

NPV IRR

Project A $ 3,730.50 36%

29

Project B $17,400.00 21%

See figure 6.3.

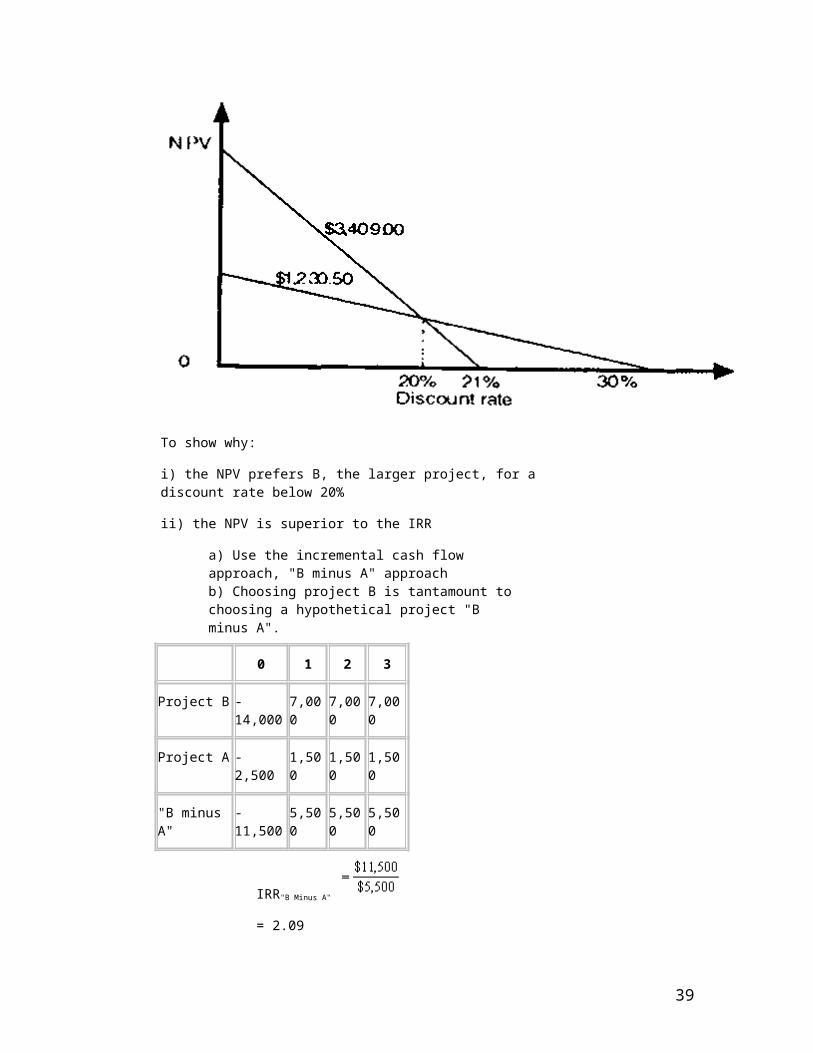

Figure 6.3 Scale of investments

To show why:

i) the NPV prefers B, the larger project, for a discount rate below 20%

ii) the NPV is superior to the IRR

a) Use the incremental cash flow approach, "B minus A" approachb) Choosing project B is tantamount to choosing a hypothetical project "B minus A".

0 1 2 3

Project B - 14,000 7,000 7,000 7,000

Project A - 2,500 1,500 1,500 1,500

"B minus A" - 11,500 5,500 5,500 5,500

IRR"B Minus A"

= 2.09

= 20%

30

c) Choosing B is equivalent to: A + (B - A) = B

d) Choosing the bigger project B means choosing the smaller project A plus an additional outlay of $11,500 of which $5,500 will be realised each year for the next 3 years.

e) The IRR"B minus A" on the incremental cash flow is 20%.

f) Given k of 10%, this is a profitable opportunity, therefore must be accepted.

g) But, if k were greater than the IRR (20%) on the incremental CF, then reject project.

h) At the point of intersection,

NPVA = NPVB or NPVA - NPVB = 0, i.e. indifferent to projects A and B.

i) If k = 20% (IRR of "B - A") the company should accept project A.

This justifies the use of NPV criterion.

Advantage of NPV:

It ensures that the firm reaches an optimal scale of investment.

Disadvantage of IRR:

It expresses the return in a percentage form rather than in terms of absolute dollar returns, e.g. the IRR will prefer 500% of $1 to 20% return on $100. However, most companies set their goals in absolute terms and not in % terms, e.g. target sales figure of $2.5 million.

3.2 THE TIMING OF THE CASH FLOW

The IRR may give conflicting decisions where the timing of cash flows varies between the 2 projects.

Note that initial outlay Io is the same.

0 1 2

Project A - 100 20 125.00

Project B - 100 100 31.25

"A minus B" 0 - 80 88.15

Assume k = 10%

31

NPV IRR

Project A 17.3 20.0%

Project B 16.7 25.0%

"A minus B" 0.6 10.9%

IRR prefers B to A even though both projects have identical initial outlays. So, the decision is to accept A, that is B + (A - B) = A. See figure 6.4.

Figure 3.4 Timing of the cash flow

The horizon problem

NPV and IRR rankings are contradictory. Project A earns $120 at the end of the first year while project B earns $174 at the end of the fourth year.

0 1 2 3 4

Project A -100 120 - - -

Project B -100 - - - 174

Assume k = 10%

NPV IRR

32

Project A 9 20%

Project B 19 15%

Decision:

NPV prefers B to AIRR prefers A to B.

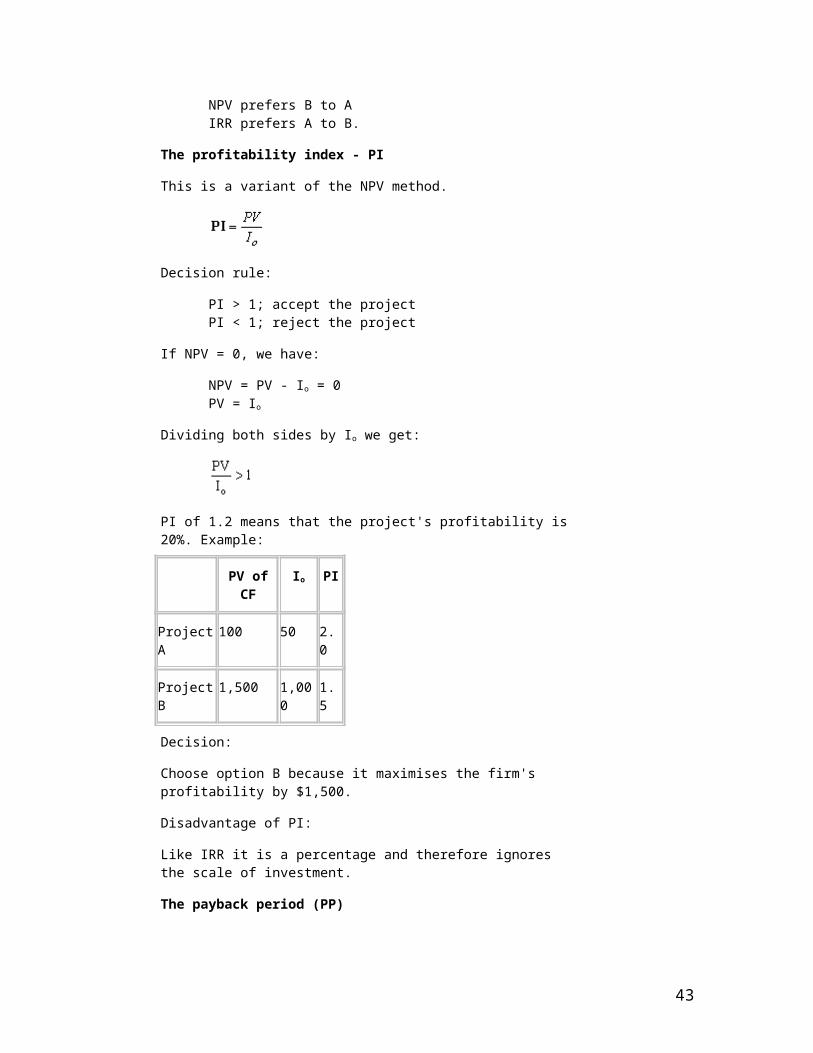

The profitability index - PI

This is a variant of the NPV method.

Decision rule:

PI > 1; accept the projectPI < 1; reject the project

If NPV = 0, we have:

NPV = PV - Io = 0PV = Io

Dividing both sides by Io we get:

PI of 1.2 means that the project's profitability is 20%. Example:

PV of CF Io PI

Project A 100 50 2.0

Project B 1,500 1,000 1.5

Decision:

Choose option B because it maximises the firm's profitability by $1,500.

Disadvantage of PI:

Like IRR it is a percentage and therefore ignores the scale of investment.

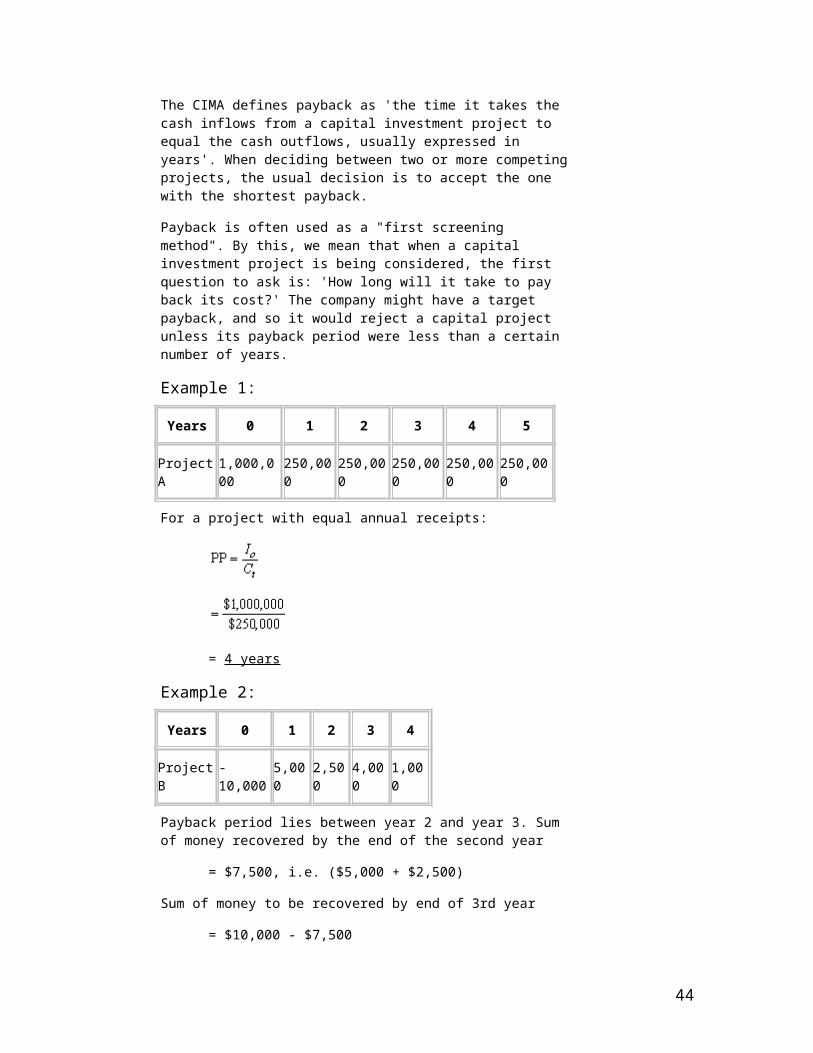

The payback period (PP)

The CIMA defines payback as 'the time it takes the cash inflows from a capital investment project to equal the cash outflows, usually expressed in years'. When deciding between two or more competing

33

projects, the usual decision is to accept the one with the shortest payback.

Payback is often used as a "first screening method". By this, we mean that when a capital investment project is being considered, the first question to ask is: 'How long will it take to pay back its cost?' The company might have a target payback, and so it would reject a capital project unless its payback period were less than a certain number of years.

Example 1:

Years 0 1 2 3 4 5

Project A 1,000,000 250,000 250,000 250,000 250,000 250,000

For a project with equal annual receipts:

= 4 years

Example 2:

Years 0 1 2 3 4

Project B - 10,000 5,000 2,500 4,000 1,000

Payback period lies between year 2 and year 3. Sum of money recovered by the end of the second year

= $7,500, i.e. ($5,000 + $2,500)

Sum of money to be recovered by end of 3rd year

= $10,000 - $7,500

= $2,500

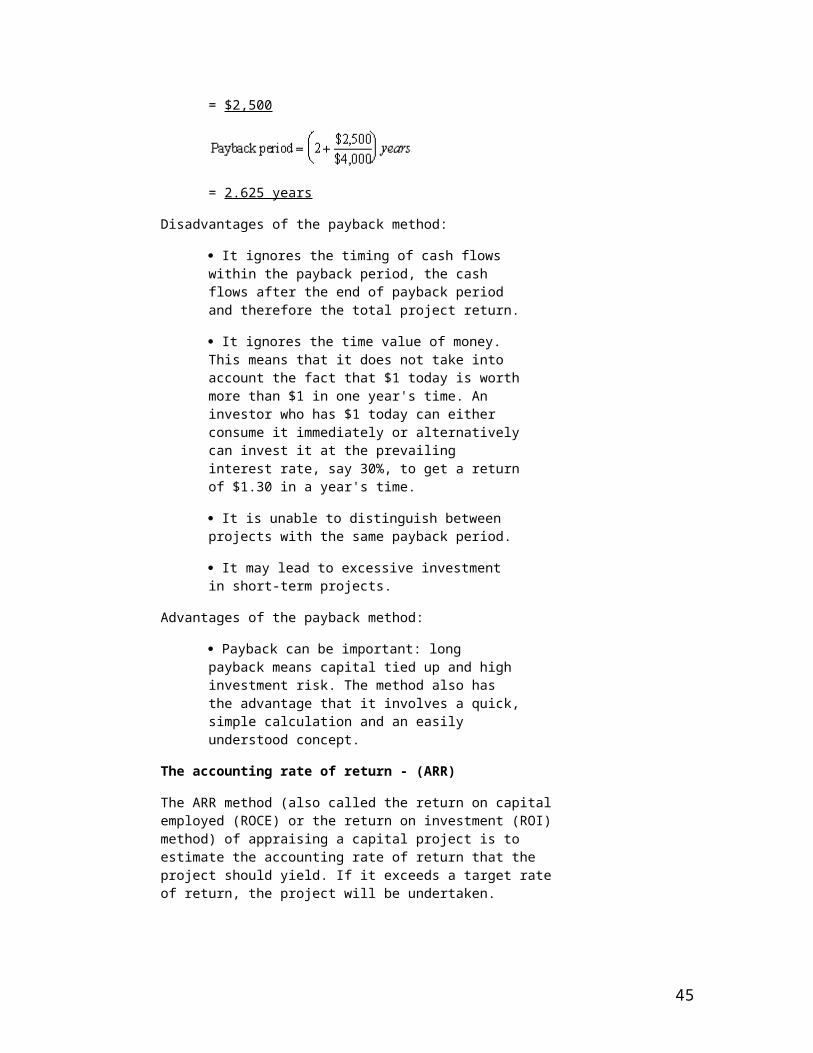

= 2.625 years

Disadvantages of the payback method:

It ignores the timing of cash flows within the payback period, the cash flows after the end of payback period and therefore the total project return.

34

It ignores the time value of money. This means that it does not take into account the fact that $1 today is worth more than $1 in one year's time. An investor who has $1 today can either consume it immediately or alternatively can invest it at the prevailing interest rate, say 30%, to get a return of $1.30 in a year's time.

It is unable to distinguish between projects with the same payback period.

It may lead to excessive investment in short-term projects.

Advantages of the payback method:

Payback can be important: long payback means capital tied up and high investment risk. The method also has the advantage that it involves a quick, simple calculation and an easily understood concept.

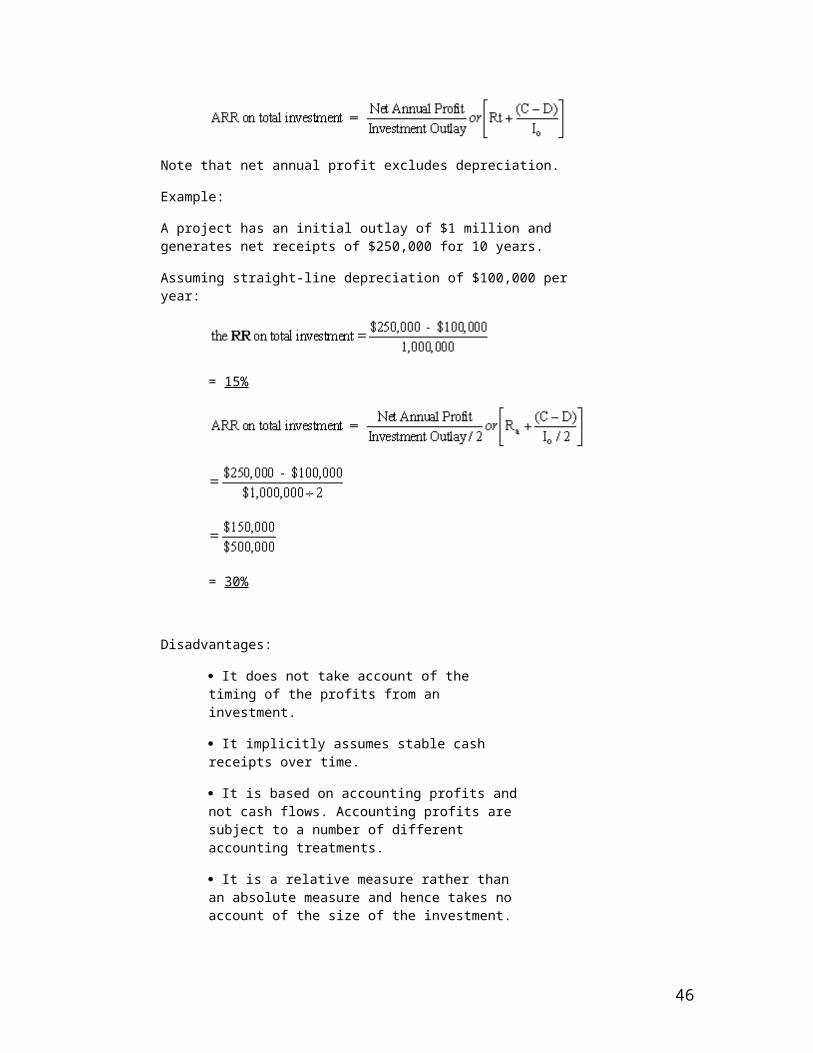

The accounting rate of return - (ARR)

The ARR method (also called the return on capital employed (ROCE) or the return on investment (ROI) method) of appraising a capital project is to estimate the accounting rate of return that the project should yield. If it exceeds a target rate of return, the project will be undertaken.

Note that net annual profit excludes depreciation.

Example:

A project has an initial outlay of $1 million and generates net receipts of $250,000 for 10 years.

Assuming straight-line depreciation of $100,000 per year:

= 15%

35

= 30%

Disadvantages:

It does not take account of the timing of the profits from an investment.

It implicitly assumes stable cash receipts over time.

It is based on accounting profits and not cash flows. Accounting profits are subject to a number of different accounting treatments.

It is a relative measure rather than an absolute measure and hence takes no account of the size of the investment.

It takes no account of the length of the project.

it ignores the time value of money.

The payback and ARR methods in practice

Despite the limitations of the payback method, it is the method most widely used in practice. There are a number of reasons for this:

It is a particularly useful approach for ranking projects where a firm faces liquidity constraints and requires fast repayment of investments.

It is appropriate in situations where risky investments are made in uncertain markets that are subject to fast design and product changes or where future cash flows are particularly difficult to predict.

The method is often used in conjunction with NPV or IRR method and acts as a first screening device to identify projects which are worthy of further investigation.

it is easily understood by all levels of management.

It provides an important summary method: how quickly will the initial investment be recouped?

QUESTIONS AND ANSWERS – INVESTMENT DECESIONSST-1 You have been asked by the president of Ellis Construction Company,

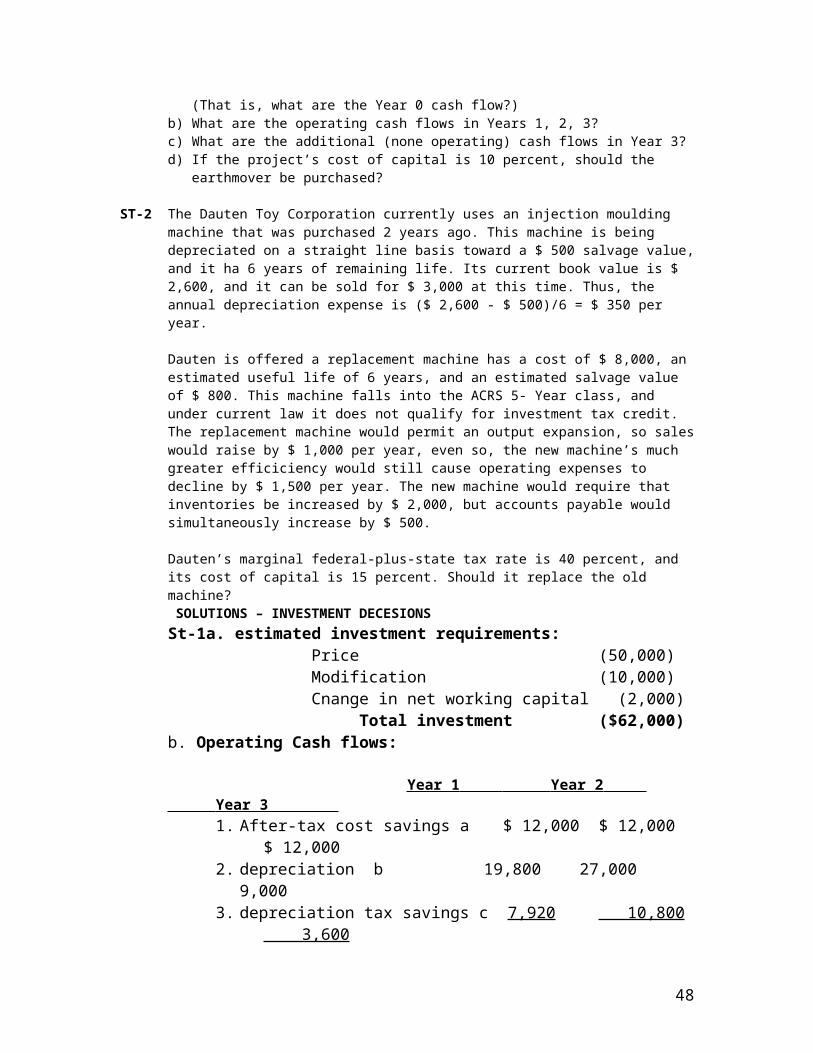

headquartered in Toledo, to evaluate the proposed acquisition of new earthmover. The mover’s basic price is $ 50, 000, and it will cost another $10,000 to modify it for special use by Ellis Construction. Assume that the mover falls into the ACRS 3-year class. It will be sold after 3 years for $ 20,000, and it will require an increase in net working capital (spare parts inventory) of $2,000. The earthmover purchase will have no effect on revenues, but it is expected to save Ellis $ 20,000 per year in before tax operating costs, mainly labor. Elli’s marginal federal–plus–state tax rate is 40 percent.

a) What is the company’s net investment if it acquires the earthmover?

36

(That is, what are the Year 0 cash flow?)b) What are the operating cash flows in Years 1, 2, 3?c) What are the additional (none operating) cash flows in Year 3?d) If the project’s cost of capital is 10 percent, should the earthmover be

purchased?

ST-2 The Dauten Toy Corporation currently uses an injection moulding machine that was purchased 2 years ago. This machine is being depreciated on a straight line basis toward a $ 500 salvage value, and it ha 6 years of remaining life. Its current book value is $ 2,600, and it can be sold for $ 3,000 at this time. Thus, the annual depreciation expense is ($ 2,600 - $ 500)/6 = $ 350 per year.

Dauten is offered a replacement machine has a cost of $ 8,000, an estimated useful life of 6 years, and an estimated salvage value of $ 800. This machine falls into the ACRS 5- Year class, and under current law it does not qualify for investment tax credit. The replacement machine would permit an output expansion, so sales would raise by $ 1,000 per year, even so, the new machine’s much greater efficiciency would still cause operating expenses to decline by $ 1,500 per year. The new machine would require that inventories be increased by $ 2,000, but accounts payable would simultaneously increase by $ 500.

Dauten’s marginal federal-plus-state tax rate is 40 percent, and its cost of capital is 15 percent. Should it replace the old machine? SOLUTIONS – INVESTMENT DECESIONSSt-1a. estimated investment requirements:

Price (50,000)Modification (10,000)Cnange in net working capital (2,000)

Total investment ($62,000)b. Operating Cash flows:

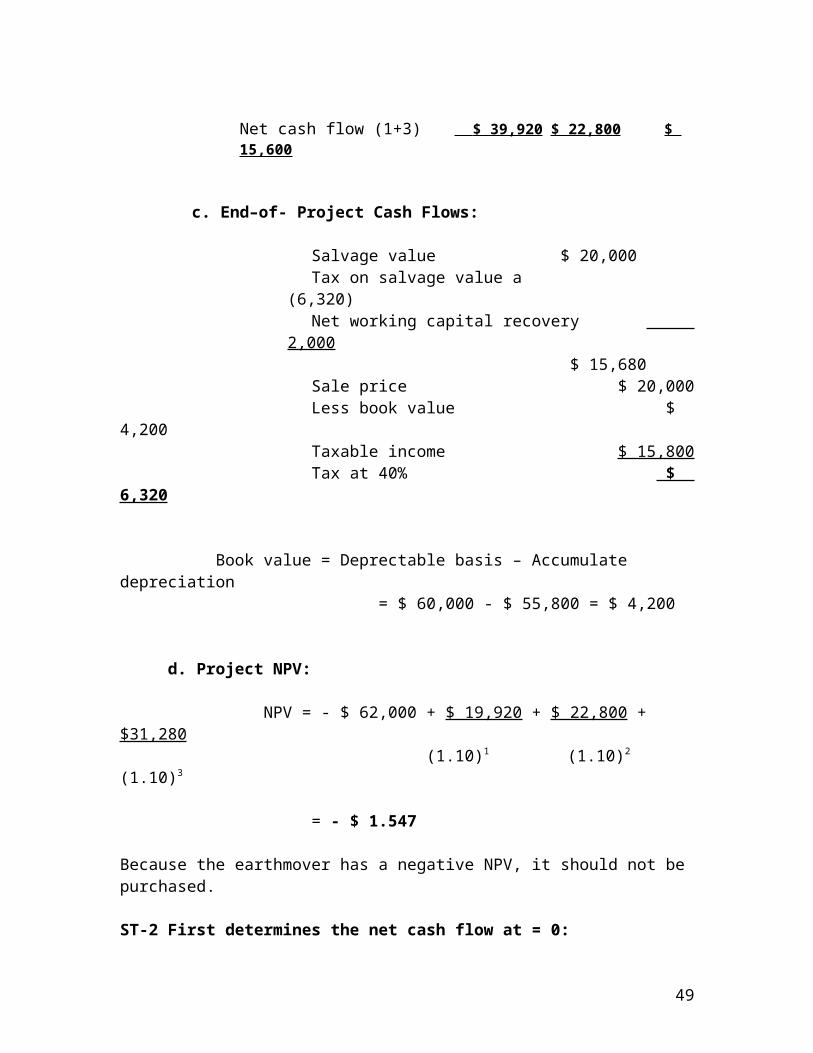

Because the earthmover has a negative NPV, it should not be purchased.

ST-2 First determines the net cash flow at = 0:

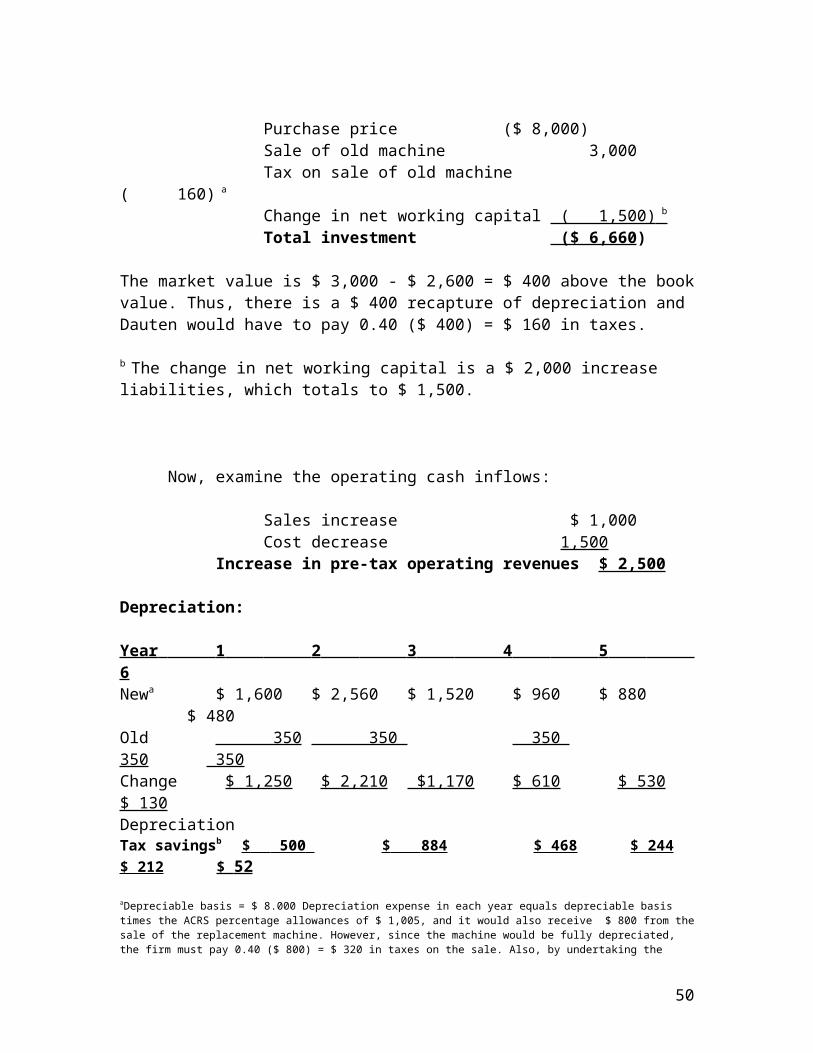

Purchase price ($ 8,000)Sale of old machine 3,000Tax on sale of old machine ( 160) a

Change in net working capital ( 1,500) b Total investment ($ 6,660)

The market value is $ 3,000 - $ 2,600 = $ 400 above the book value. Thus, there is a $ 400 recapture of depreciation and Dauten would have to pay 0.40 ($ 400) = $ 160 in taxes. b The change in net working capital is a $ 2,000 increase liabilities, which totals to $ 1,500.

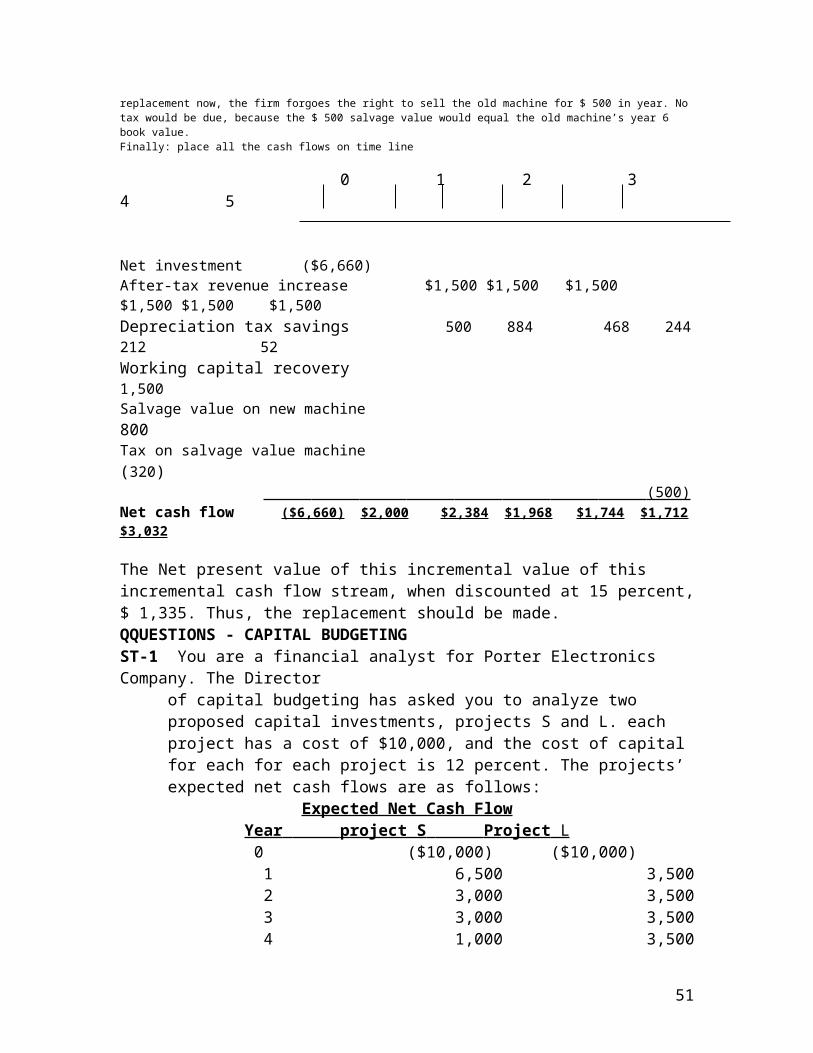

aDepreciable basis = $ 8.000 Depreciation expense in each year equals depreciable basis times the ACRS percentage allowances of $ 1,005, and it would also receive $ 800 from the sale of the replacement machine. However, since the machine would be fully depreciated, the firm must pay 0.40 ($ 800) = $ 320 in taxes on the sale. Also, by undertaking the replacement now, the firm forgoes the right to sell the old machine for $ 500 in year. No tax would be due, because the $ 500 salvage value would equal the old machine’s year 6 book value.Finally: place all the cash flows on time line

0 1 2 3 4 5

Net investment ($6,660)After-tax revenue increase $1,500 $1,500 $1,500 $1,500 $1,500 $1,500Depreciation tax savings 500 884 468 244 212 52Working capital recovery 1,500Salvage value on new machine 800Tax on salvage value machine (320)

The Net present value of this incremental value of this incremental cash flow stream, when discounted at 15 percent, $ 1,335. Thus, the replacement should be made. QQUESTIONS - CAPITAL BUDGETINGST-1 You are a financial analyst for Porter Electronics Company. The Director

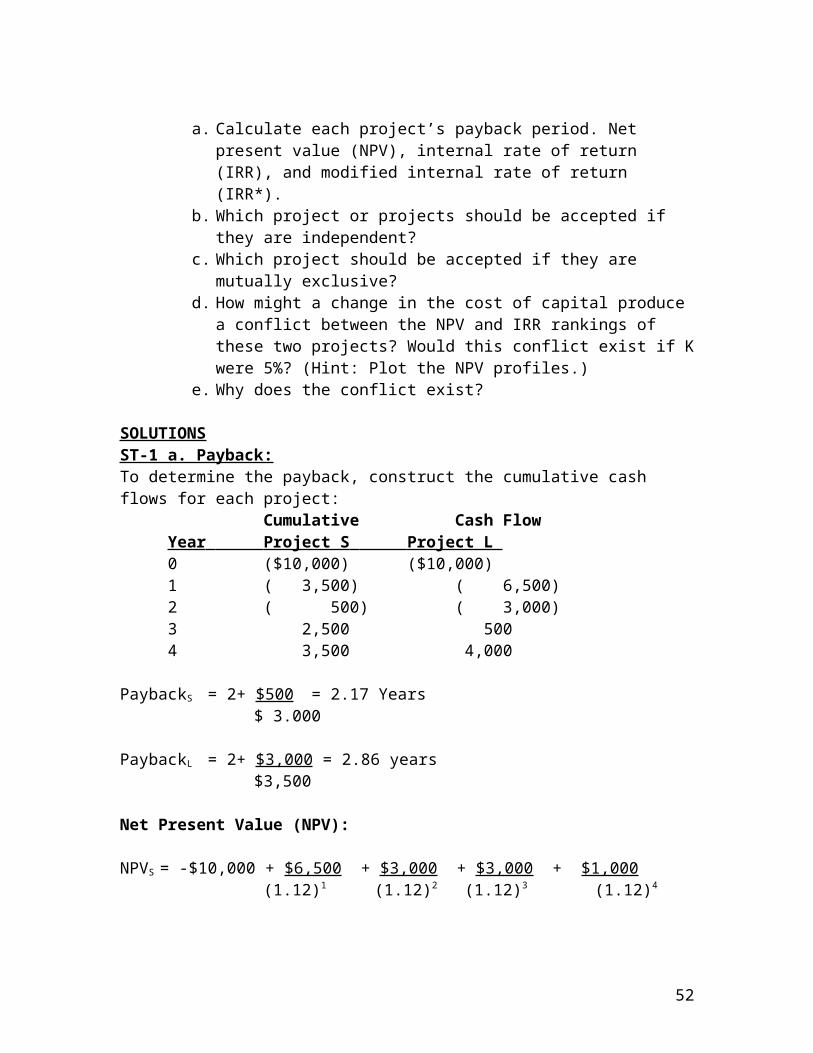

of capital budgeting has asked you to analyze two proposed capital investments, projects S and L. each project has a cost of $10,000, and the cost of capital for each for each project is 12 percent. The projects’ expected net cash flows are as follows:

Expected Net Cash FlowYear project S Project L

0 ($10,000) ($10,000) 1 6,500 3,500

2 3,000 3,500 3 3,000 3,500 4 1,000 3,500

39

a. Calculate each project’s payback period. Net present value (NPV), internal rate of return (IRR), and modified internal rate of return (IRR*).

b. Which project or projects should be accepted if they are independent?

c. Which project should be accepted if they are mutually exclusive?

d. How might a change in the cost of capital produce a conflict between the NPV and IRR rankings of these two projects? Would this conflict exist if K were 5%? (Hint: Plot the NPV profiles.)

e. Why does the conflict exist?

SOLUTIONSST-1 a. Payback:To determine the payback, construct the cumulative cash flows for each project:

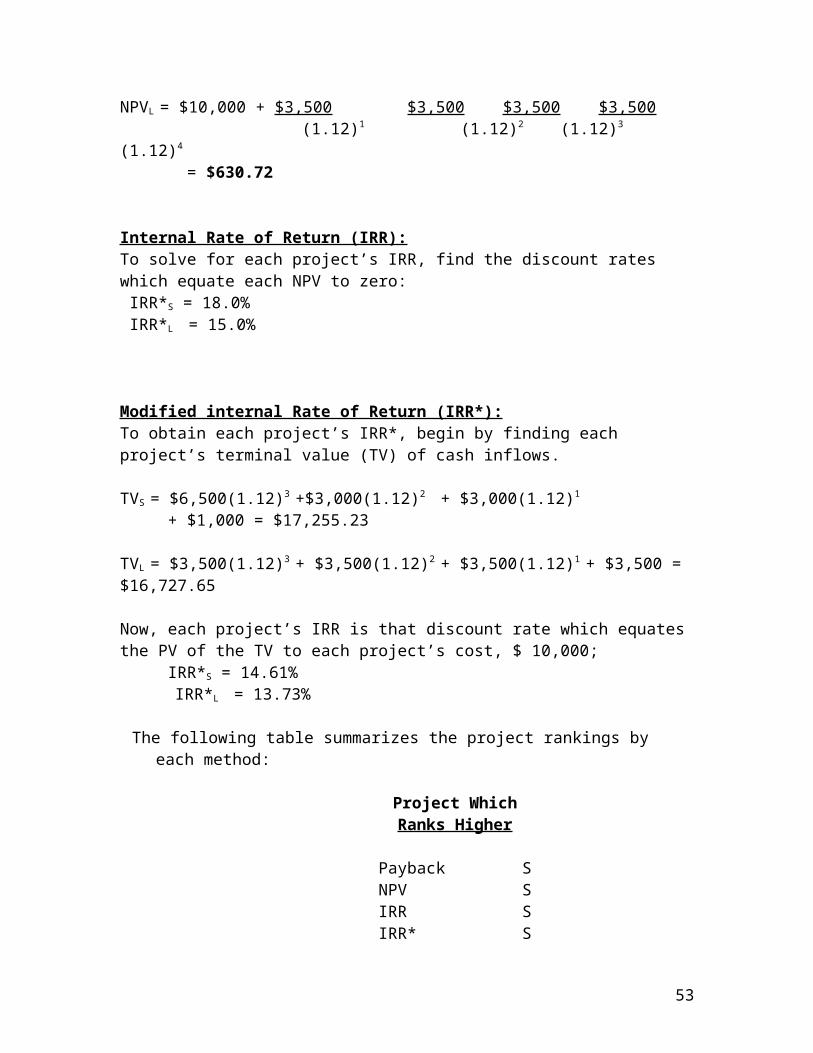

Now, each project’s IRR is that discount rate which equates the PV of the TV to each project’s cost, $ 10,000;

IRR*S = 14.61% IRR*L = 13.73%

The following table summarizes the project rankings by each method:

Project WhichRanks Higher

Payback SNPV SIRR SIRR* S

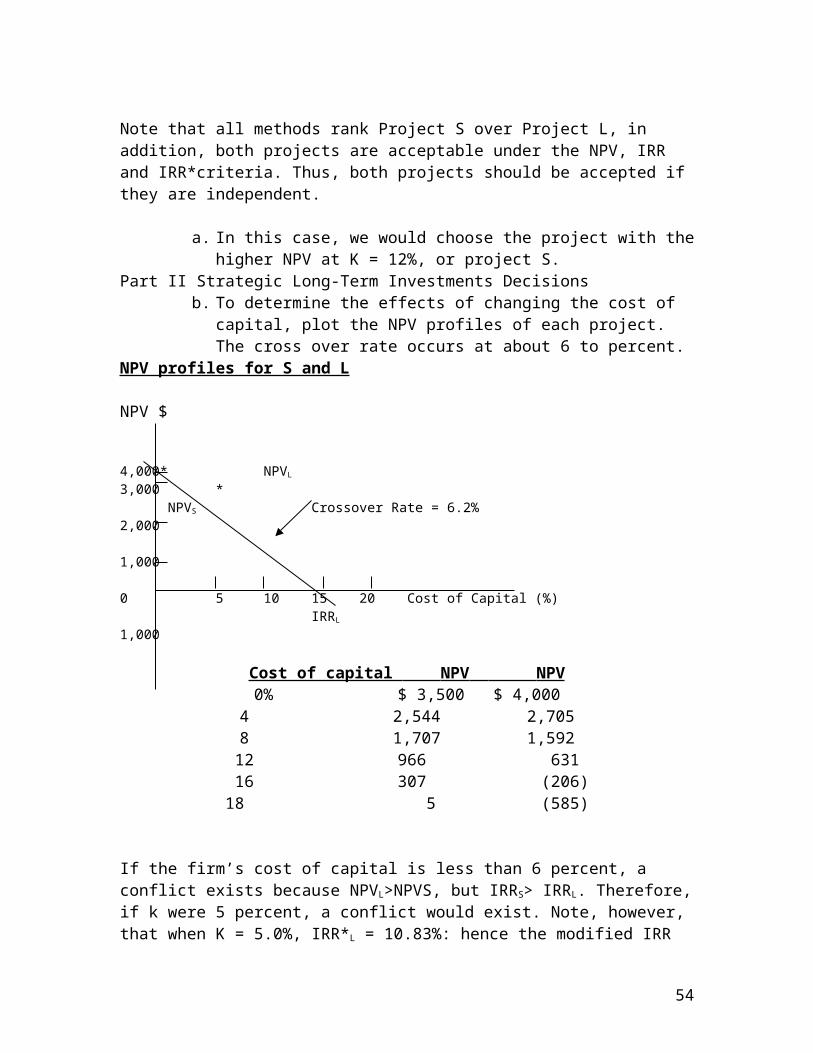

Note that all methods rank Project S over Project L, in addition, both projects are acceptable under the NPV, IRR and IRR*criteria. Thus, both projects should be accepted if they are independent.

a. In this case, we would choose the project with the higher NPV at K = 12%, or project S.

Part II Strategic Long-Term Investments Decisionsb. To determine the effects of changing the cost of capital,

plot the NPV profiles of each project. The cross over rate occurs at about 6 to percent.

NPV profiles for S and L

NPV $

4,000* NPVL

3,000 *

41

NPVS Crossover Rate = 6.2%2,000

1,000

0 5 10 15 20 Cost of Capital (%)IRRL

1,000

Cost of capital NPV NPV 0% $ 3,500 $ 4,000

4 2,544 2,7058 1,707 1,592

12 966 631 16 307 (206)18 5 (585)

If the firm’s cost of capital is less than 6 percent, a conflict exists because NPVL>NPVS, but IRRS> IRRL. Therefore, if k were 5 percent, a conflict would exist. Note, however, that when K = 5.0%, IRR*L = 10.83%: hence the modified IRR ranks the projects correctly, even if K is to the left of the crossover point. c) The basic cause of the conflict is differing reinvestment rate

assumptions between NPV and IRR. NPV assumes that cash flow can reinvested at the cost of capital, while IRR assumes reinvestment at the (generally) higher IRR. The high reinvestment rate assumption under IRR makes early cash flows especially valuable and hence short – term projects look better under IRR.

42

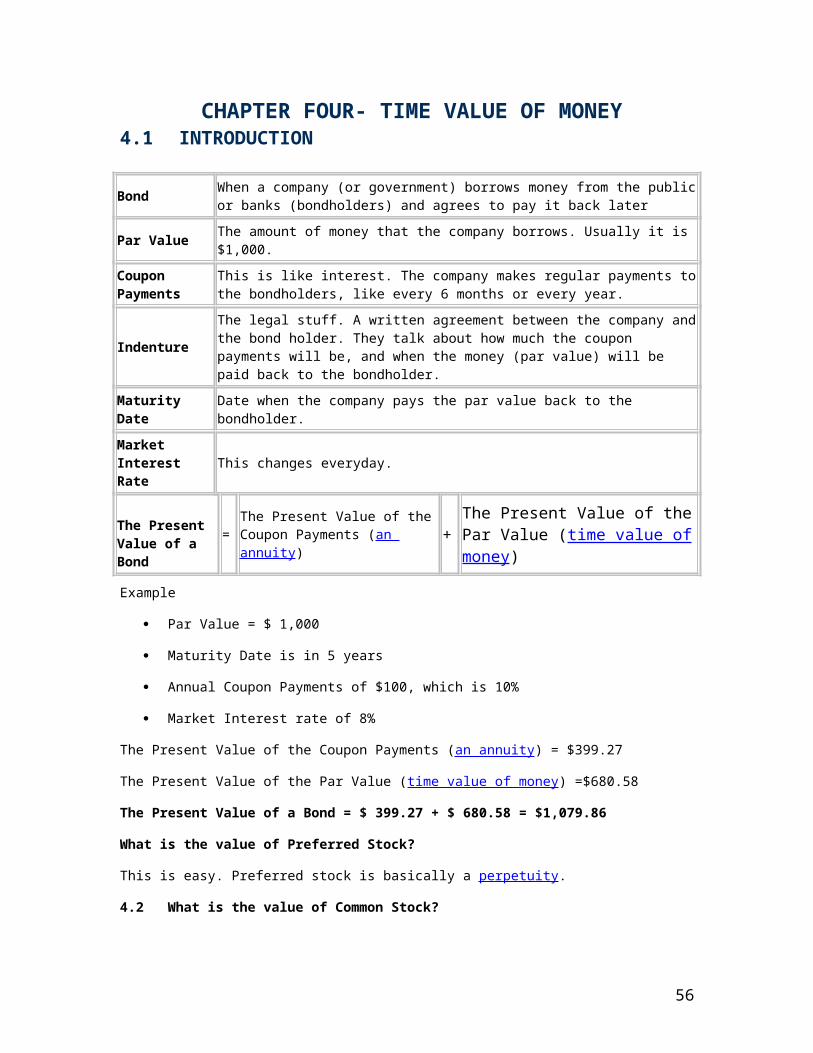

CHAPTER FOUR- TIME VALUE OF MONEY4.1 INTRODUCTION

BondWhen a company (or government) borrows money from the public or banks (bondholders) and agrees to pay it back later

Par Value The amount of money that the company borrows. Usually it is $1,000.

Coupon Payments

This is like interest. The company makes regular payments to the bondholders, like every 6 months or every year.

IndentureThe legal stuff. A written agreement between the company and the bond holder. They talk about how much the coupon payments will be, and when the money (par value) will be paid back to the bondholder.

Maturity Date Date when the company pays the par value back to the bondholder.

Market Interest Rate

This changes everyday.

The Present Value of a Bond

=The Present Value of the Coupon Payments (an annuity) +

The Present Value of the Par Value (time value of money)

Example

Par Value = $ 1,000

Maturity Date is in 5 years

Annual Coupon Payments of $100, which is 10%

Market Interest rate of 8%

The Present Value of the Coupon Payments (an annuity) = $399.27

The Present Value of the Par Value (time value of money) =$680.58

The Present Value of a Bond = $ 399.27 + $ 680.58 = $1,079.86

What is the value of Preferred Stock?

This is easy. Preferred stock is basically a perpetuity.

4.2 What is the value of Common Stock?

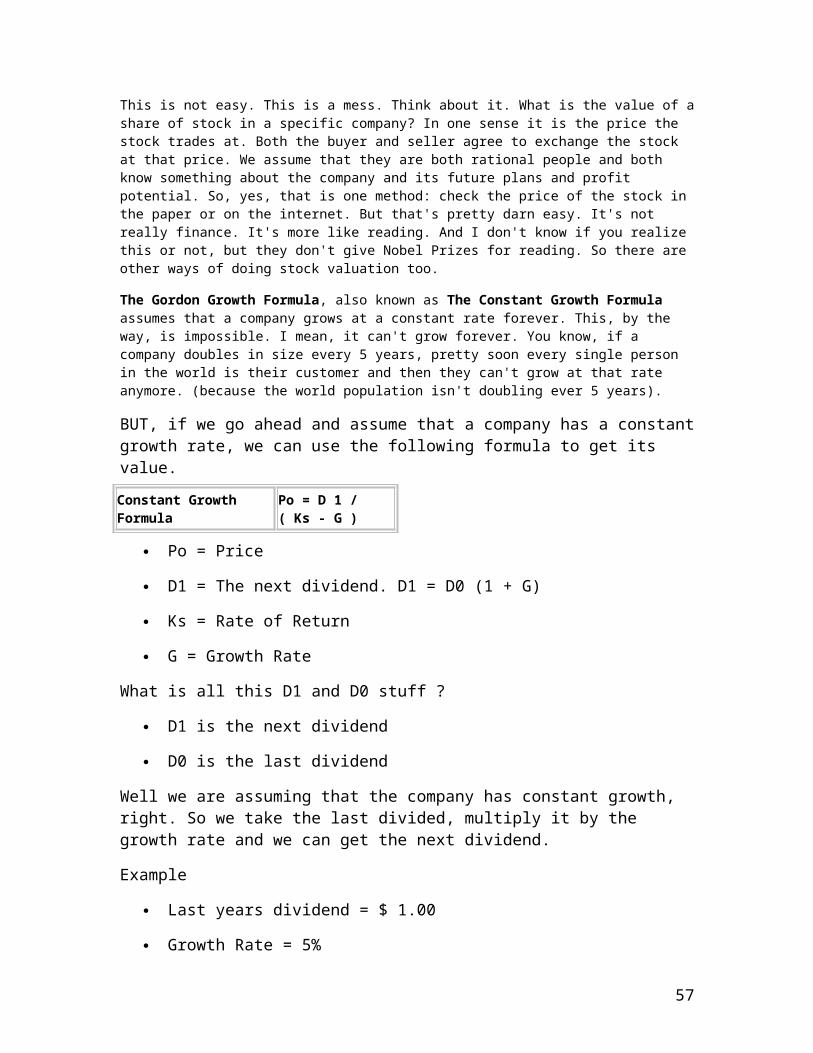

This is not easy. This is a mess. Think about it. What is the value of a share of stock in a specific company? In one sense it is the price the stock trades at. Both the buyer and seller agree to exchange the stock at that price. We assume that they are both rational people and both know something about the company and its future plans and profit potential. So, yes, that is one method: check the price of the stock in the paper or on the internet. But that's pretty darn easy. It's not really finance. It's more like reading. And I don't know if you realize this or not, but they don't give Nobel Prizes for reading. So there are other ways of doing stock valuation too.