Page 1

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 1/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

The 3 basic business activitiesThe 3 basic business activities

The subject of financial accounting & reporting:

Page 2

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 2/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

Equity

Financing

Debt

Financing

Investment

in Producing

Assets

Goods &

Services

Net

EarningsOperating

Activities

Investing

Activities

Financing

Activities

Reinvested

DebtPayment

Dividends

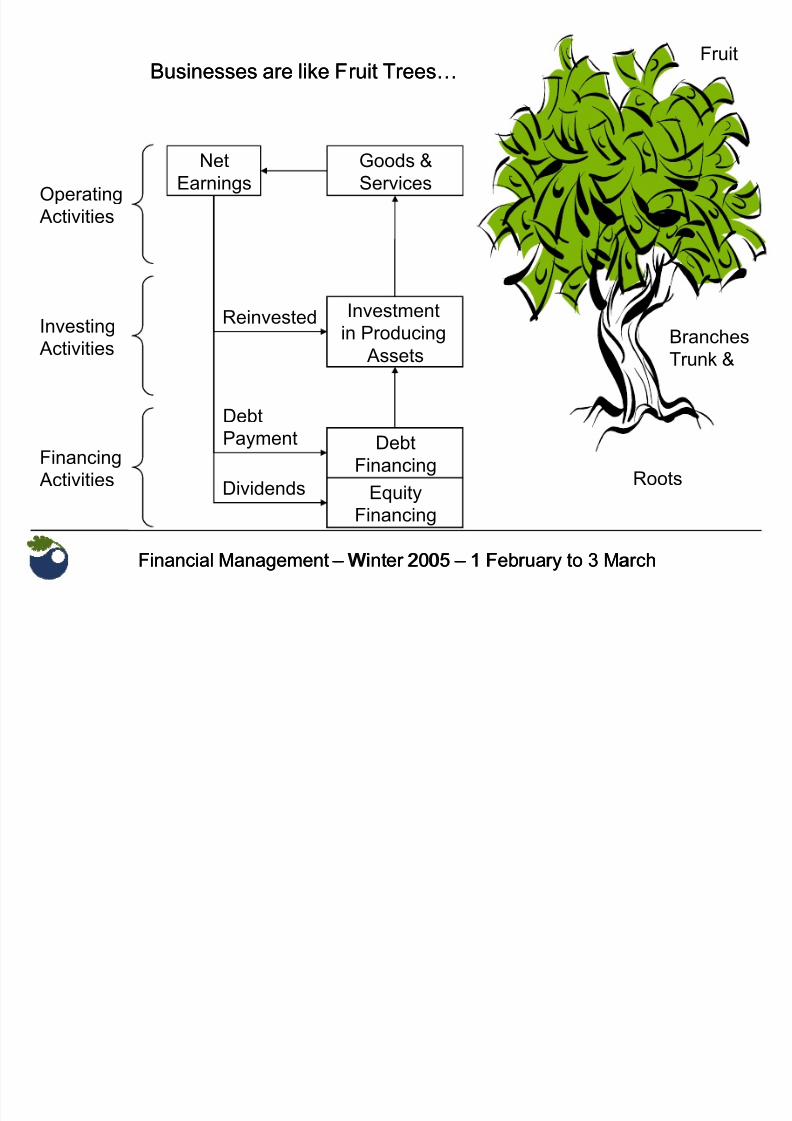

Businesses are like Fruit Trees«Businesses are like Fruit Trees«

Roots

Branches

Trunk &

Fruit

Page 3

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 3/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

The 3 basic activities involved in conducting a business are:The 3 basic activities involved in conducting a business are:

Financing activities (Roots):Financing activities (Roots):

- Owners contribute cash and receive equity shares in return.- Creditors loan cash in return for the promise of interest and principal payments.

Investing activities (Trunk and branches):Investing activities (Trunk and branches):

Once the capital is collected it is invested in producing assets, like buildings,

equipment, machinery and vehicles.

Operating activities (Fruit):Operating activities (Fruit):

The assets are operated to produce goods & services which are sold to customers.

The Net IncomeNet Income of these sales can be used in three ways:

1. Reinvested in the producing assets

2. Returned to the creditors in the form of debt payments

3. Returned to the owners in the form of dividends

Page 4

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 4/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

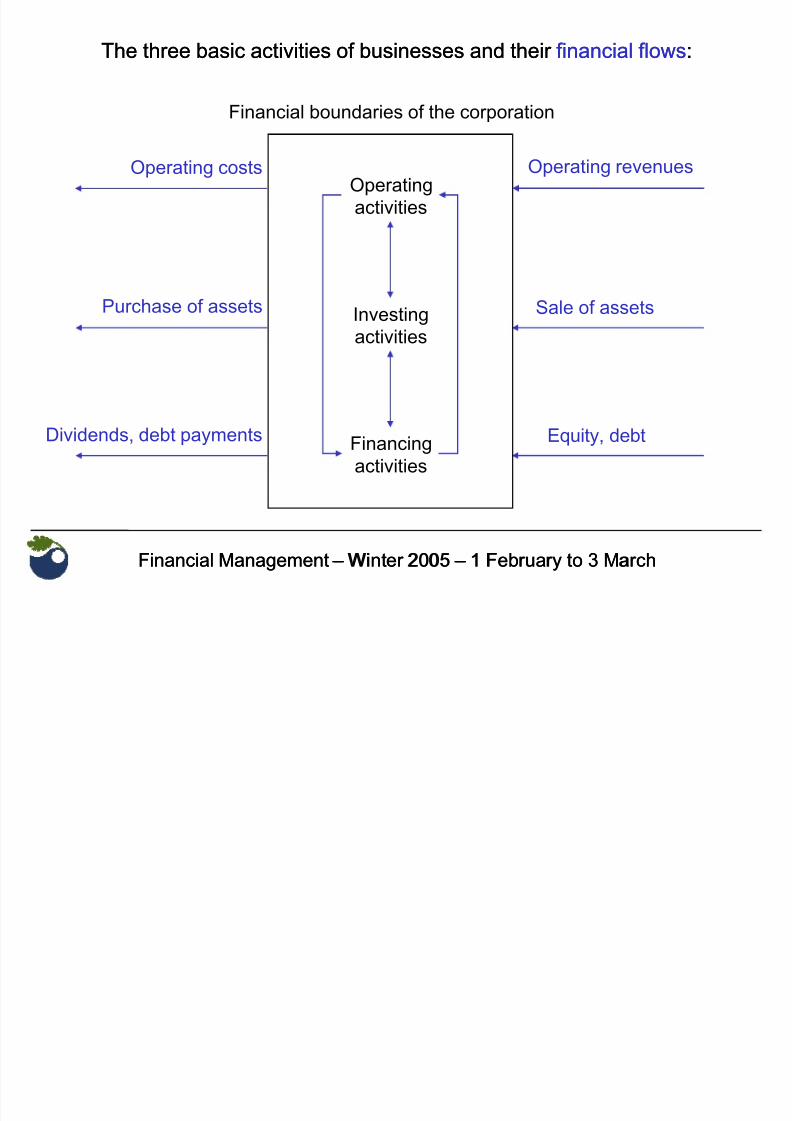

The three basic activities of businesses and their The three basic activities of businesses and their financial flowsfinancial flows::

Operating revenuesOperating costs

Sale of assetsPurchase of assets

Operating

activities

Investing

activities

Financing

activities

Equity, debtDividends, debt payments

Financial boundaries of the corporation

Page 5

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 5/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

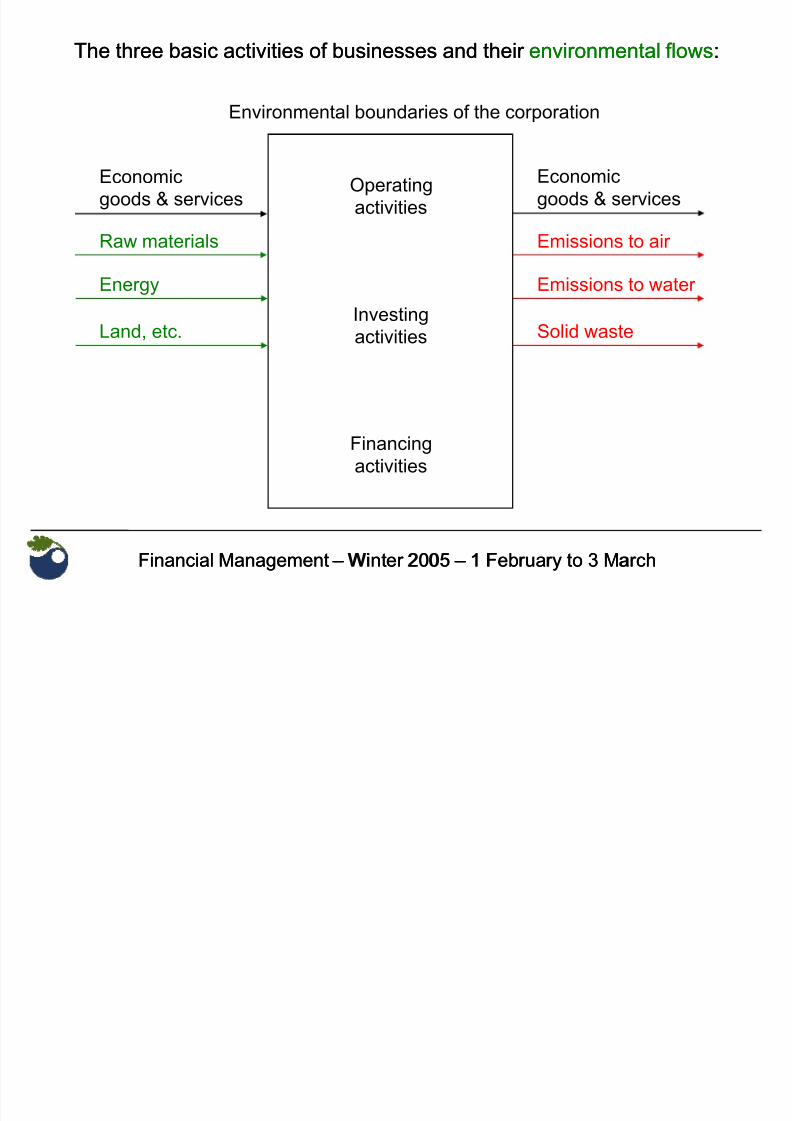

The three basic activities of businesses and their The three basic activities of businesses and their environmental flowsenvironmental flows::

Emissions to air

Economic

goods & services

Energy

Operating

activities

Investing

activities

Financing

activities

Solid wasteLand, etc.

Environmental boundaries of the corporation

Emissions to water

Raw materials

Economic

goods & services

Page 6

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 6/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

What information is contained in the 4 financial statementsWhat information is contained in the 4 financial statements

How are the financial flows of the 3 basic business activitiesHow are the financial flows of the 3 basic business activitiesreflected in the 4 financial statements?reflected in the 4 financial statements?

The 4 Financial Statements:

Page 7

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 7/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

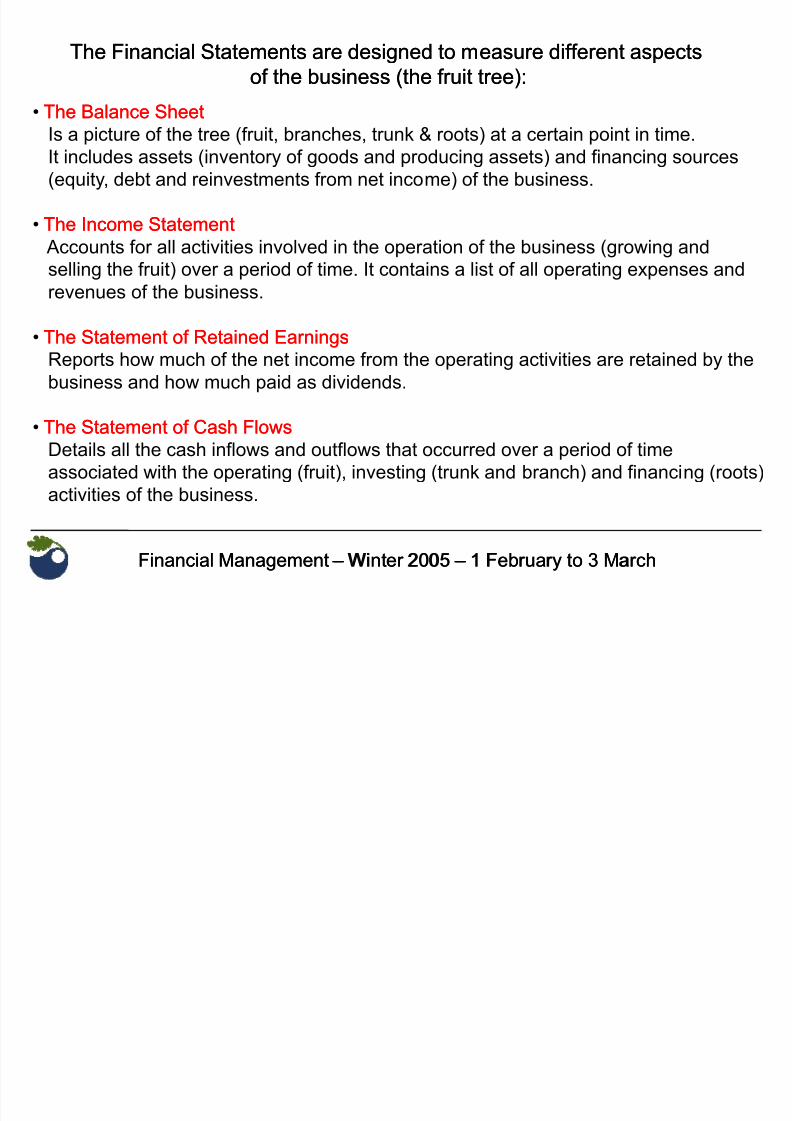

The Financial Statements are designed to measure different aspectsThe Financial Statements are designed to measure different aspects

of the business (the fruit tree):of the business (the fruit tree):

The Balance SheetThe Balance Sheet

Is a picture of the tree (fruit, branches, trunk & roots) at a certain point in time.It includes assets (inventory of goods and producing assets) and financing sources

(equity, debt and reinvestments from net income) of the business.

The Income StatementThe Income Statement

Accounts for all activities involved in the operation of the business (growing and

selling the fruit) over a period of time. It contains a list of all operating expenses andrevenues of the business.

The Statement of Retained EarningsThe Statement of Retained Earnings

Reports how much of the net income from the operating activities are retained by the

business and how much paid as dividends.

The Statement of Cash FlowsThe Statement of Cash Flows

Details all the cash inflows and outflows that occurred over a period of time

associated with the operating (fruit), investing (trunk and branch) and financing (roots)

activities of the business.

Page 8

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 8/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

The Income StatementThe Income Statement

measures operating performance over a particular period of time.

Operating Revenues

í Operating Expenses

= Operating Income

+ Other Revenues

í Other Expenses

= Net Income before Taxes

í Income Taxes

= Net Income after Taxes

/ Number of Shares

= Income per Share

Net incomeNet income is the most important number disclosed on the financial statements.

Page 9

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 9/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

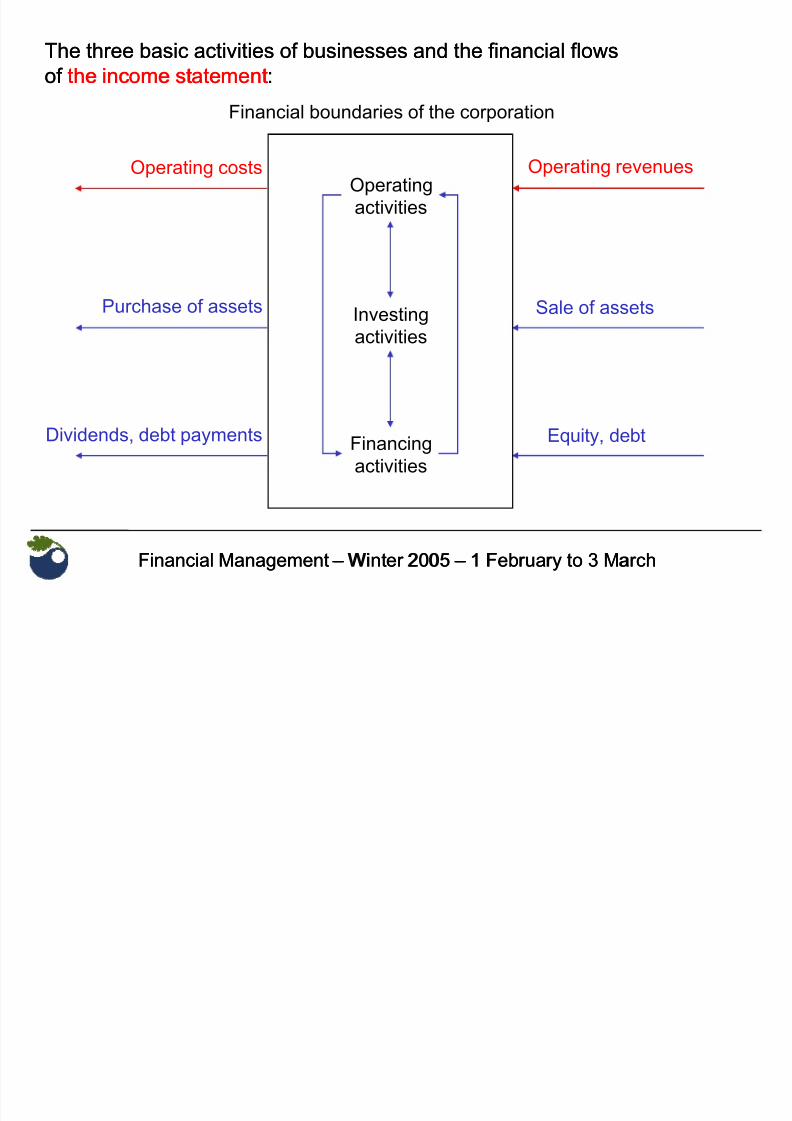

The three basic activities of businesses and the financial flowsThe three basic activities of businesses and the financial flows

of of thethe income statementincome statement::

Operating revenuesOperating costs

Sale of assetsPurchase of assets

Operating

activities

Investing

activities

Financing

activities

Equity, debtDividends, debt payments

Financial boundaries of the corporation

Page 10

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 10/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

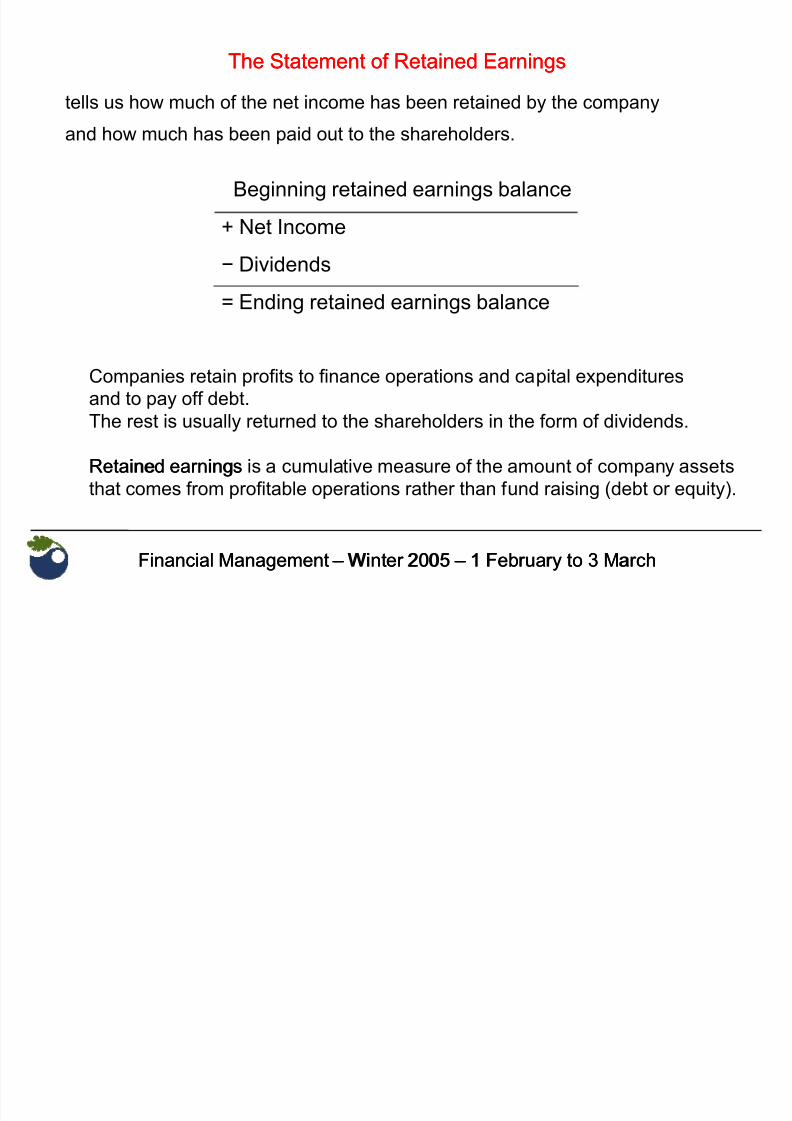

The Statement of Retained EarningsThe Statement of Retained Earnings

Beginning retained earnings balance

+ Net Income

í Dividends

= Ending retained earnings balance

tells us how much of the net income has been retained by the company

and how much has been paid out to the shareholders.

Companies retain profits to finance operations and capital expenditures

and to pay off debt.

The rest is usually returned to the shareholders in the form of dividends.

Retained earningsRetained earnings is a cumulative measure of the amount of company assets

that comes from profitable operations rather than fund raising (debt or equity).

Page 11

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 11/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

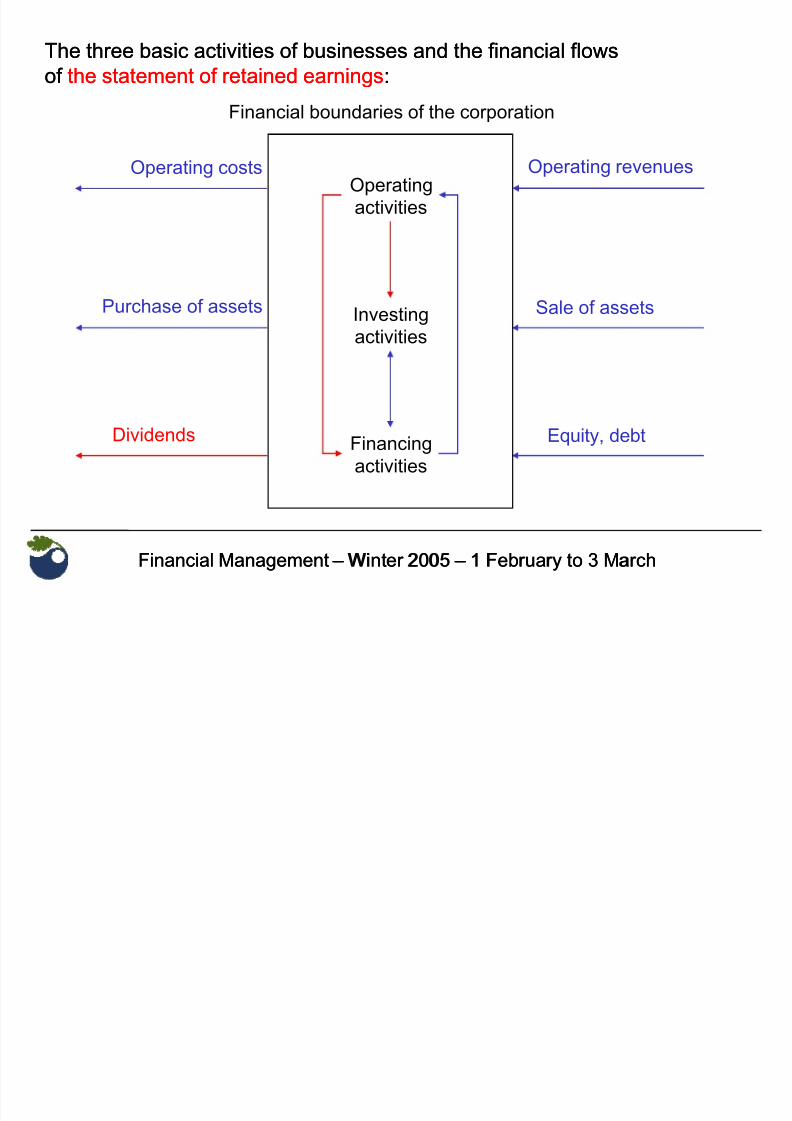

The three basic activities of businesses and the financial flowsThe three basic activities of businesses and the financial flows

of of the statement of retained earningsthe statement of retained earnings::

Operating revenuesOperating costs

Sale of assetsPurchase of assets

Operating

activities

Investing

activities

Financing

activities

Equity, debtDividends

Financial boundaries of the corporation

Page 12

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 12/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

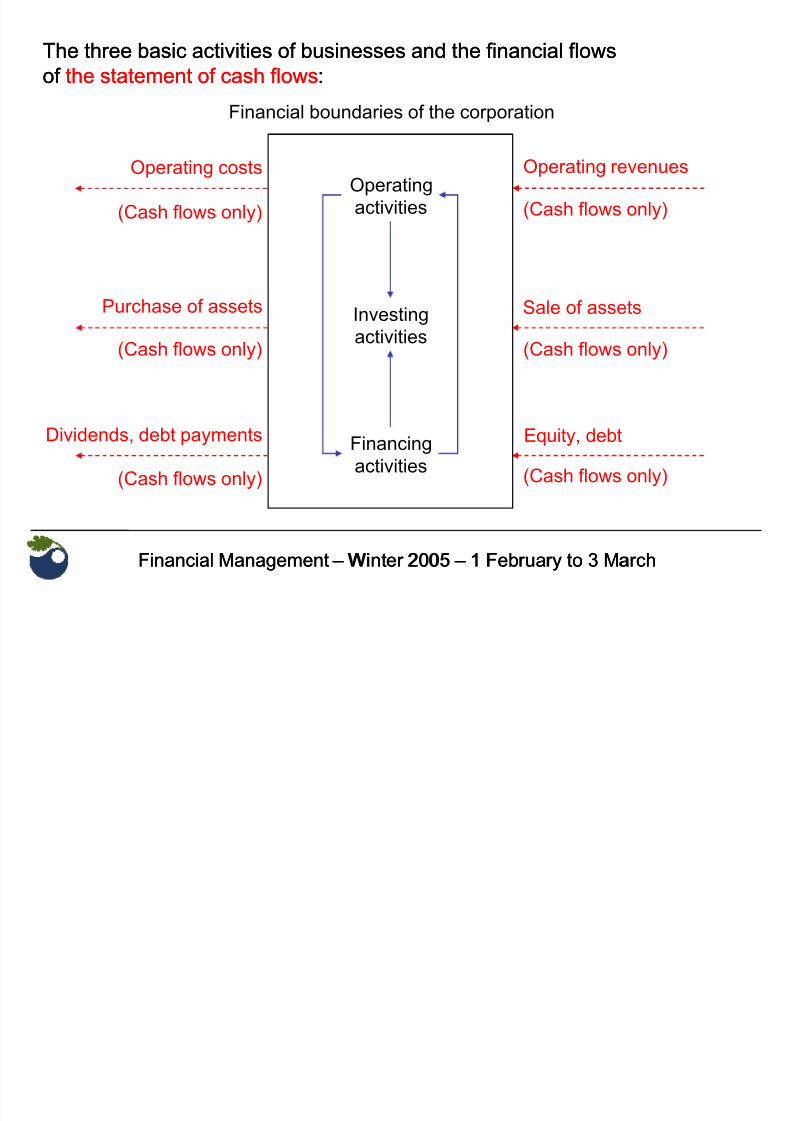

The Statement of Cash FlowsThe Statement of Cash Flows

The statement of cash flows is a summary of the financial flows into and out of a

company¶s cash account. (Note that accounting flows are not necessarily cash flows)

Operating activities + Cash collection

í Cash paid

= Net cash increase (decrease) from operating activities (1)

Investing activities í Purchases of securities or property

+ Sales of securities or property

= Net cash increase (decrease) from investing activities (2)

Financing activities + raised capital from issuing equity or entering debt

í Dividends or debt payments

= Net cash increase (decrease) from financing activities (3)

(1) + (2) + (3) = Increase (decrease) in cash balance

+ Beginning cash balance

= Ending cash balance

The cash balance provides important information on a company¶s solvency.

Page 13

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 13/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

The three basic activities of businesses and the financial flowsThe three basic activities of businesses and the financial flows

of of the statement of cash flowsthe statement of cash flows::

Operating revenuesOperating costs

Sale of assetsPurchase of assets

Operating

activities

Investing

activities

Financing

activities

Equity, debtDividends, debt payments

Financial boundaries of the corporation

(Cash flows only)

(Cash flows only)

(Cash flows only) (Cash flows only)

(Cash flows only)

(Cash flows only)

Page 14

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 14/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

The balance sheet provides a picture of the company¶s financial situation at one point

in time. It is based on the fundamental accounting equation:

Assets = Liabilities + Equity Assets = Liabilities + Equity

The shareholders own the company. It¶s net worth is (Assets ± Liabilities) = Equity.

This is called book value of the company and different from its stock market value.

Assets:

Items and right acquired through objectively measurable transactions that can be usedin the future to generate economic benefits.

Liabilities:

Primarily a firm¶s debt and payables. The total amount of liabilities is the portion of

assets that a firm has borrowed and must repay.

Stockholders¶ Equity

consists of contributed capital and retained earnings.

The balance sheet is called classifiedclassified if assets and liabilities are grouped into

classifications, and consolidatedconsolidated if it contains all divisions and subsidiaries of the firm.

The Balance SheetThe Balance Sheet

Page 15

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 15/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

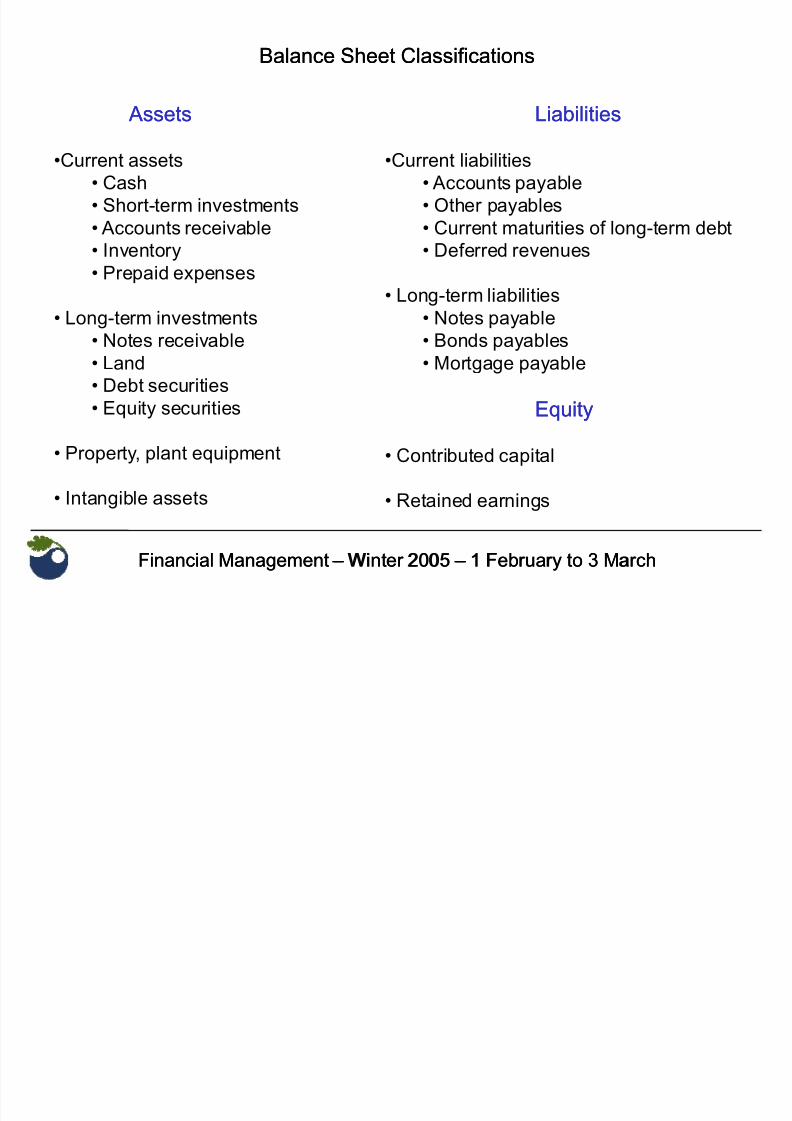

Assets Assets

Current assets

Cash

Short-term investments

Accounts receivable

Inventory

Prepaid expenses

Long-term investments

Notes receivable

Land

Debt securities

Equity securities

Property, plant equipment

Intangible assets

LiabilitiesLiabilities

Current liabilities

Accounts payable

Other payables

Current maturities of long-term debt

Deferred revenues

Long-term liabilities

Notes payable

Bonds payables

Mortgage payable

EquityEquity

Contributed capital

Retained earnings

Balance Sheet ClassificationsBalance Sheet Classifications

Page 16

8/8/2019 Financial Accounting n Reporting

http://slidepdf.com/reader/full/financial-accounting-n-reporting 16/16

Financial ManagementFinancial Management ± ± Winter 2005Winter 2005 ± ± 1 February to 3 March1 February to 3 March

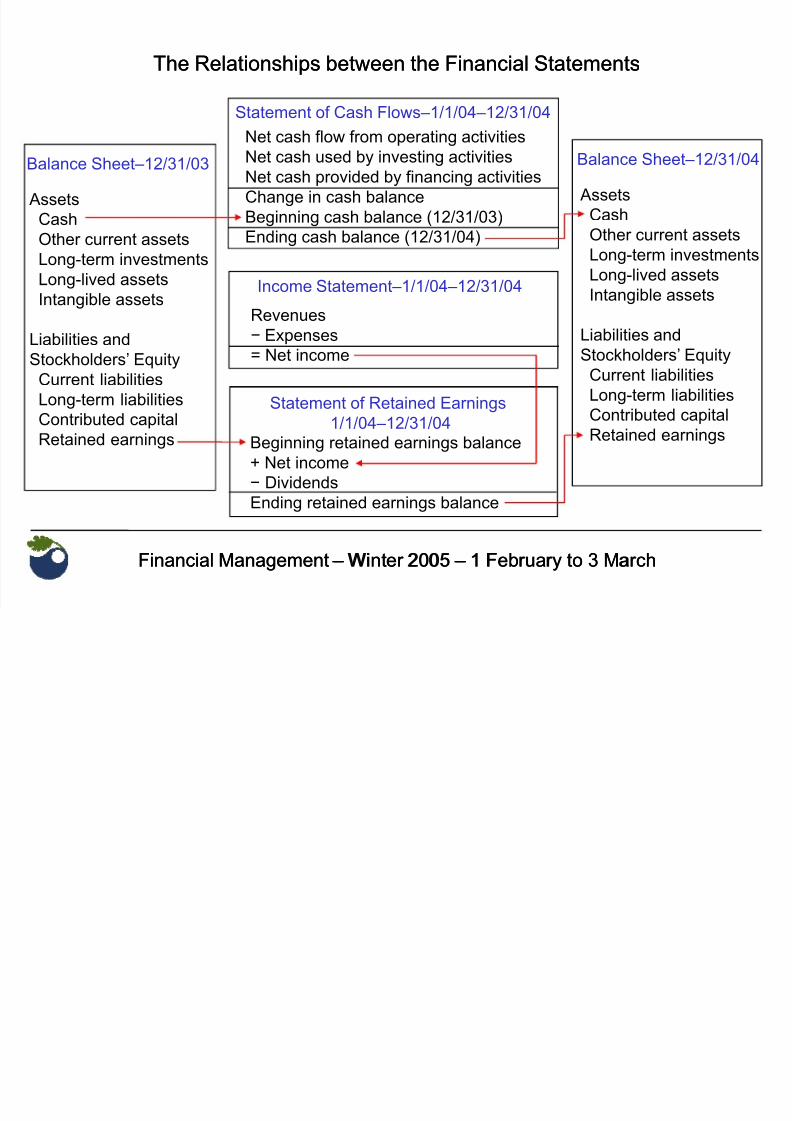

The Relationships between the Financial StatementsThe Relationships between the Financial Statements

Balance Sheet±12/31/03

Assets

Cash

Other current assets

Long-term investments

Long-lived assetsIntangible assets

Liabilities and

Stockholders¶ Equity

Current liabilities

Long-term liabilities

Contributed capitalRetained earnings

Balance Sheet±12/31/04

Assets

Cash

Other current assets

Long-term investments

Long-lived assetsIntangible assets

Liabilities and

Stockholders¶ Equity

Current liabilities

Long-term liabilities

Contributed capitalRetained earnings

Statement of Cash Flows±1/1/04±12/31/04

Net cash flow from operating activitiesNet cash used by investing activities

Net cash provided by financing activities

Change in cash balance

Beginning cash balance (12/31/03)

Ending cash balance (12/31/04)

Income Statement±1/1/04±12/31/04

Revenues

í Expenses

= Net income

Statement of Retained Earnings

1/1/04±12/31/04Beginning retained earnings balance

+ Net income

í Dividends

Ending retained earnings balance