42

Report on Financial Statements

| Date post: | 09-Dec-2015 |

| Category: |

Documents |

| Upload: | blaahkugan-kun |

| View: | 50 times |

| Download: | 5 times |

Report on Financial Statements and financial position of Reliance Industries Ltd.

Prepared by : Sumeet BaidJonny PaulSamyak JainPranav Garg

Batch: PGP Mumbai2014-2016

Report on Financial Statements and financial position of Reliance Industries Ltd.

Sumeet Baid 55Jonny Paul 22Samyak Jain 43Pranav Garg 40

PGP Mumbai2014-2016

Reliance Industries Ltd.

Company >> Finance >> Balance SheetReliance Industries Ltd

Industry :Refineries(Rs in Crs)

3,232.00 1.13 3,229.00 1.28193,842.00 67.53 176,766.00 70.02

0 0.00 0 0.0017 0.01 25 0.01

197,091.00 68.66 180,020.00 71.3111,203.00 3.90 6,626.00 2.6278,765.00 27.44 65,801.00 26.0789,968.00 31.34 72,427.00 28.69

0 0.00 0 0.00287,059.00 100.00 252,447.00 100.00287,059.00222,565.00 77.53 213,154.00 84.44113,159.00 39.42 103,406.00 40.96

0 0.00 0 0.00109,406.00 38.11 109,748.00 43.47

0 0.00 0 0.0041,716.00 14.53 19,116.00 7.5786,062.00 29.98 52,509.00 20.80

0.00 0.0042,932.00 14.96 42,729.00 16.9310,664.00 3.71 11,880.00 4.7136,624.00 12.76 49,547.00 19.6311,743.00 4.09 11,454.00 4.54

101,963.00 35.52 115,610.00 45.800.00 0.00

64,142.00 22.34 49,523.00 19.624,167.00 1.45 4,348.00 1.72

68,309.00 23.80 53,871.00 21.3433,654.00 11.72 61,739.00 24.46

0 0.00 0 0.00161 0.06 100 0.04

12,376.00 4.31 12,293.00 4.87-12,215.00 -4.26 -12,193.00 -4.8328,436.00 9.91 21,528.00 8.53

287,059.00 100.00 252,447.00 100.0050,645.00 17.64 47,403.00 18.78

Year Mar 14 Mar 13 SOURCES OF FUNDS : Share Capital Reserves Total Equity Share Warrants Equity Application Money Total Shareholders Funds Secured Loans Unsecured Loans Total Debt Other Liabilities Total Liabilities APPLICATION OF FUNDS : Gross Block Less : Accumulated Depreciation Less:Impairment of Assets Net Block Lease Adjustment Capital Work in Progress Investments Current Assets, Loans & Advances Inventories Sundry Debtors Cash and Bank Loans and Advances Total Current Assets Less : Current Liabilities and Provisions Current Liabilities Provisions Total Current Liabilities Net Current Assets Miscellaneous Expenses not written off Deferred Tax Assets Deferred Tax Liability Net Deferred Tax Other Assets Total Assets Contingent Liabilities http://www.capitaline.com

3,271.00 1.39 3,273.00 1.49 3,270.37 1.64 1,642.78 0.82162,825.00 69.42 148,267.00 67.65 133,900.24 67.06 124,730.19 62.28

0 0.00 0 0.00 0 0.00 0 0.001 0.00 10 0.00 1.36 0.00 1.42 0.00

166,097.00 70.82 151,550.00 69.15 137,171.97 68.70 126,374.39 63.1010,013.00 4.27 10,104.00 4.61 11,670.50 5.84 10,697.92 5.3458,434.00 24.91 57,499.00 26.24 50,824.19 25.45 63,206.56 31.5668,447.00 29.18 67,603.00 30.85 62,494.69 31.30 73,904.48 36.90

0 0.00 0 0.00 0 0.00 0 0.00234,544.00 100.00 219,153.00 100.00 199,666.66 100.00 200,278.87 100.00

205,493.00 87.61 221,253.00 100.96 215,864.71 108.11 149,628.70 74.7191,770.00 39.13 78,546.00 35.84 62,604.82 31.35 49,285.64 24.61

0 0.00 0 0.00 0 0.00 0 0.00113,723.00 48.49 142,707.00 65.12 153,259.89 76.76 100,343.06 50.10

0 0.00 0 0.00 0 0.00 0 0.007,754.00 3.31 12,228.00 5.58 12,138.82 6.08 69,043.83 34.47

54,008.00 23.03 37,652.00 17.18 23,228.62 11.63 21,606.49 10.790.00 0.00 0.00 0.00

35,955.00 15.33 29,825.00 13.61 26,981.62 13.51 14,836.72 7.4118,424.00 7.86 17,442.00 7.96 11,660.21 5.84 4,571.38 2.2839,598.00 16.88 27,135.00 12.38 13,462.65 6.74 22,176.53 11.0711,338.00 4.83 7,032.00 3.21 10,274.62 5.15 13,127.64 6.55

105,315.00 44.90 81,434.00 37.16 62,379.10 31.24 54,712.27 27.320.00 0.00 0.00 0.00

44,216.00 18.85 49,403.00 22.54 36,848.04 18.45 32,689.58 16.324,258.00 1.82 4,601.00 2.10 3,565.43 1.79 3,010.90 1.50

48,474.00 20.67 54,004.00 24.64 40,413.47 20.24 35,700.48 17.8356,841.00 24.23 27,430.00 12.52 21,965.63 11.00 19,011.79 9.49

0 0.00 0 0.00 0 0.00 0 0.0085 0.04 181 0.08 242.95 0.12 247.51 0.12

12,207.00 5.20 11,743.00 5.36 11,169.25 5.59 9,973.81 4.98-12,122.00 -5.17 -11,562.00 -5.28 -10,926.30 -5.47 -9,726.30 -4.8614,340.00 6.11 10,698.00 4.88 0 0.00 0 0.00

234,544.00 100.00 219,153.00 100.00 199,666.66 100.00 200,278.87 100.0045,104.00 19.23 48,700.68 22.22 17,650.06 8.84 19,278.00 9.63

Mar 12 Mar 11 Mar 10 Mar 09

1,453.39 1.23 1,453.35 1.58 1,393.17 1.94 1,393.09 2.3578,312.81 66.41 62,513.78 68.10 48,411.09 67.55 39,010.23 65.91

1,682.40 1.43 0 0.00 0 0.00 0 0.000 0.00 0 0.00 0 0.00 0 0.00

81,448.60 69.07 63,967.13 69.69 49,804.26 69.49 40,403.32 68.266,600.17 5.60 9,569.12 10.42 7,664.90 10.69 7,972.90 13.47

29,879.51 25.34 18,256.61 19.89 14,200.71 19.81 10,811.69 18.2736,479.68 30.93 27,825.73 30.31 21,865.61 30.51 18,784.59 31.74

0 0.00 0 0.00 0 0.00 0 0.00117,928.28 100.00 91,792.86 100.00 71,669.87 100.00 59,187.91 100.00

104,229.10 88.38 99,532.77 108.43 84,970.13 118.56 55,125.82 93.1442,345.47 35.91 35,872.31 39.08 29,253.38 40.82 24,872.83 42.02

0 0.00 0 0.00 0 0.00 0 0.0061,883.63 52.48 63,660.46 69.35 55,716.75 77.74 30,252.99 51.11

0 0.00 0 0.00 0 0.00 0 0.0023,005.84 19.51 7,528.13 8.20 6,957.79 9.71 4,829.29 8.1622,063.60 18.71 16,251.34 17.70 5,846.18 8.16 17,051.46 28.81

0.00 0.00 0.00 0.0014,247.54 12.08 12,136.51 13.22 10,119.82 14.12 7,412.88 12.52

6,227.58 5.28 3,732.42 4.07 4,163.62 5.81 3,927.81 6.644,280.05 3.63 1,835.35 2.00 2,146.16 2.99 3,608.79 6.10

18,130.67 15.37 12,209.07 13.30 8,144.85 11.36 13,503.03 22.8142,885.84 36.37 29,913.35 32.59 24,574.45 34.29 28,452.51 48.07

0.00 0.00 0.00 0.0021,045.47 17.85 16,865.53 18.37 12,563.50 17.53 13,659.72 23.08

2,992.62 2.54 1,712.87 1.87 3,890.98 5.43 3,471.80 5.8724,038.09 20.38 18,578.40 20.24 16,454.48 22.96 17,131.52 28.9418,847.75 15.98 11,334.95 12.35 8,119.97 11.33 11,320.99 19.13

0 0.00 0 0.00 0 0.00 0 0.00310.53 0.26 297.64 0.32 121.7 0.17 366.64 0.62

8,183.07 6.94 7,279.66 7.93 5,092.52 7.11 4,633.46 7.83-7,872.54 -6.68 -6,982.02 -7.61 -4,970.82 -6.94 -4,266.82 -7.21

0 0.00 0 0.00 0 0.00 0 0.00117,928.28 100.00 91,792.86 100.00 71,669.87 100.00 59,187.91 100.00

24,308.69 20.61 28,356.90 30.89 18,339.06 25.59 9,153.89 15.47

Mar 08 Mar 07 Mar 06 Mar 05

Company >> Finance >> Profit & LossReliance Industries Ltd

Industry :Refineries(Rs in Crs)

401,302.00 100.67 371,119.00 99.8711,185.00 2.81 10,822.00 2.91

390,117.00 97.86 360,297.00 96.968,936.00 2.24 7,998.00 2.15

-412 -0.10 3,317.00 0.89398,641.00 100.00 371,612.00 100.00

0.00329,837.00 91.92 306,629.00 82.51

10,153.00 2.83 7,166.00 1.933,370.00 0.94 3,354.00 0.906,778.00 1.89 6,359.00 1.718,548.00 2.38 8,755.00 2.36

857 0.24 662 0.18715 0.20 98 0.03

358,828.00 100.00 332,827.00 89.5639,813.00 11.10 38,785.00 10.44

3,206.00 0.89 3,036.00 0.8236,607.00 10.20 35,749.00 9.62

8,789.00 2.45 9,465.00 2.5527,818.00 7.75 26,284.00 7.07

5,812.00 1.62 5,244.00 1.410 0.00 0 0.00

22 0.01 37 0.0121,984.00 6.13 21,003.00 5.65

1,810.53 0.50 1,286.52 0.3520,173.47 5.62 19,716.48 5.31

0 0.00 1,116.00 0.308,610.00 2.40 7,609.00 2.05

0 0.00 0 0.0021,268.00 5.93 21,118.00 5.68

9,326.00 2.60 8,610.00 2.322,793.00 0.78 2,628.00 0.71

0 0.00 0 0.0095 0.03 90 0.02

66.55 0.02 63.66 0.020.00 0.00

609.76 0.17 554.17 0.15

Year Mar 14(12) Mar 13(12) INCOME : Sales Turnover Excise Duty Net Sales Other Income Stock Adjustments Total Income EXPENDITURE : Raw Materials Power & Fuel Cost Employee Cost Other Manufacturing Expenses Selling and Administration Expenses Miscellaneous Expenses Less: Pre-operative Expenses Capitalised Total Expenditure Operating Profit Interest Gross Profit Depreciation Profit Before Tax Tax Fringe Benefit tax Deferred Tax Reported Net Profit Extraordinary Items Adjusted Net Profit Adjst. below Net Profit P & L Balance brought forward Statutory Appropriations Appropriations P & L Balance carried down Dividend Preference Dividend Equity Dividend % Earnings Per Share-Unit Curr Earnings Per Share(Adj)-Unit Curr Book Value-Unit Curr http://www.capitaline.com

339,792.00 100.84 258,651.00 101.65 200,399.79 100.77 146,328.07 101.249,888.00 2.93 10,481.00 4.12 7,938.77 3.99 4,369.07 3.02

329,904.00 97.90 248,170.00 97.53 192,461.02 96.78 141,959.00 98.226,192.00 1.84 3,052.00 1.20 2,460.32 1.24 2,148.40 1.49

872 0.26 3,243.00 1.27 3,947.89 1.99 427.56 0.30336,968.00 100.00 254,465.00 100.00 198,869.23 100.00 144,534.96 100.00

0.00 0.00 0.00 0.00276,255.00 81.98 194,698.00 76.51 150,915.03 75.89 107,010.32 74.04

4,094.00 1.21 2,255.00 0.89 2,706.71 1.36 3,355.98 2.322,862.00 0.85 2,624.00 1.03 2,307.73 1.16 2,357.40 1.636,309.00 1.87 6,600.00 2.59 5,578.24 2.80 3,704.00 2.566,925.00 2.06 6,807.00 2.68 5,549.74 2.79 4,619.24 3.20

749 0.22 333 0.13 -11.48 -0.01 1,379.92 0.9537 0.01 30 0.01 1,217.92 0.61 3,265.65 2.26

297,157.00 88.19 213,287.00 83.82 165,828.05 83.39 119,161.21 82.4439,811.00 11.81 41,178.00 16.18 33,041.18 16.61 25,373.75 17.56

2,667.00 0.79 2,328.00 0.91 1,997.21 1.00 1,745.23 1.2137,144.00 11.02 38,850.00 15.27 31,043.97 15.61 23,628.52 16.3511,394.00 3.38 13,608.00 5.35 10,496.53 5.28 5,195.29 3.5925,750.00 7.64 25,242.00 9.92 20,547.44 10.33 18,433.23 12.75

5,150.00 1.53 4,320.00 1.70 3,111.77 1.56 1,206.50 0.830 0.00 0 0.00 0 0.00 56.87 0.04

560 0.17 636 0.25 1,200.00 0.60 1,860.54 1.2920,040.00 5.95 20,286.00 7.97 16,235.67 8.16 15,309.32 10.59

1,233.53 0.37 224.22 0.09 187.8 0.09 40.61 0.0318,806.47 5.58 20,061.78 7.88 16,047.87 8.07 15,268.71 10.56

0 0.00 0.55 0.00 0 0.00 0 0.006,514.00 1.93 4,999.45 1.96 5,384.19 2.71 4,363.29 3.02

0 0.00 0 0.00 0 0.00 0 0.0018,945.00 5.62 18,772.00 7.38 16,620.41 8.36 14,288.42 9.89

7,609.00 2.26 6,514.00 2.56 4,999.45 2.51 5,384.19 3.732,531.00 0.75 2,385.00 0.94 2,084.67 1.05 1,897.05 1.31

0 0.00 0 0.00 0 0.00 0 0.0085 0.03 80 0.03 70 0.04 130 0.09

60.01 0.02 60.8 0.02 48.59 0.02 95.24 0.070.00 0.00 0.00 0.00

498.22 0.15 446.3 0.18 392.51 0.20 727.78 0.50

Mar 12(12) Mar 11(12) Mar 10(12) Mar 09(12)

139,269.46 100.52 118,353.71 104.89 89,124.46 106.49 73,164.10 109.20365,463.68 3.94 6,654.68 5.90 8,246.67 9.85 7,245.27 10.81418

133,805.78 96.57 111,699.03 99.00 80,877.79 96.64 65,918.83 98.389466,615.62 4.77 478.28 0.42 682.92 0.82 1,603.38 2.393181

-1,867.16 -1.35 654.6 0.58 2,131.19 2.55 -524.35 -0.782637138,554.24 100.00 112,831.91 100.00 83,691.90 100.00 66,997.86 100

0.00 0.00 0.00 096,311.56 69.51 78,692.94 69.74 58,342.31 69.71 45,931.87 68.55722

2,052.84 1.48 2,261.69 2.00 1,146.26 1.37 907.94 1.3551782,049.95 1.48 2,045.95 1.81 932.09 1.11 791.21 1.1809483,951.40 2.85 3,486.87 3.09 2,217.72 2.65 1,937.13 2.8913314,882.01 3.52 5,342.31 4.73 5,765.46 6.89 2,826.38 4.218612

547.3 0.40 588.85 0.52 461.19 0.55 352.09 0.525524175.46 0.13 111.21 0.10 155.14 0.19 9.6 0.014329

109,619.60 79.12 92,307.40 81.81 68,709.89 82.10 52,737.02 78.7144828,934.64 20.88 20,524.51 18.19 14,982.01 17.90 14,260.84 21.28552

1,077.36 0.78 1,188.89 1.05 877.04 1.05 1,468.66 2.192127,857.28 20.11 19,335.62 17.14 14,104.97 16.85 12,792.18 19.09342

4,847.14 3.50 4,815.15 4.27 3,400.91 4.06 3,723.50 5.5576423,010.14 16.61 14,520.47 12.87 10,704.06 12.79 9,068.68 13.53578

2,604.96 1.88 1,617.10 1.43 900 1.08 705 1.05227247 0.03 40.34 0.04 30.72 0.04 0 0

899.89 0.65 919.63 0.82 704 0.84 792 1.18212719,458.29 14.04 11,943.40 10.59 9,069.34 10.84 7,571.68 11.30138

4,111.75 2.97 -312.17 -0.28 74.91 0.09 31.94 0.04767315,346.54 11.08 12,255.57 10.86 8,994.43 10.75 7,539.74 11.2537

48.1 0.03 0.51 0.00 0 0.00 -4.17 -0.0062242,765.37 2.00 3,029.09 2.68 8,967.86 10.72 5,592.06 8.346625

0 0.00 0 0.00 0 0.00 0 017,908.47 12.93 12,207.63 10.82 15,008.11 17.93 4,191.71 6.256483

4,363.29 3.15 2,765.37 2.45 3,029.09 3.62 8,967.86 13.385291,631.24 1.18 1,440.44 1.28 1,393.51 1.67 1,045.13 1.559945

0 0.00 0 0.00 0 0.00 0 0130 0.09 110 0.10 100 0.12 75 0.111944

131.97 0.10 84.28 0.07 63.7 0.08 53.3 0.0795550.00 0.00 0.00 0

542.83 0.39 439.67 0.39 324.11 0.39 270.43 0.40364

Mar 08(12) Mar 07(12) Mar 06(12) Mar 05(12)

Solvency position

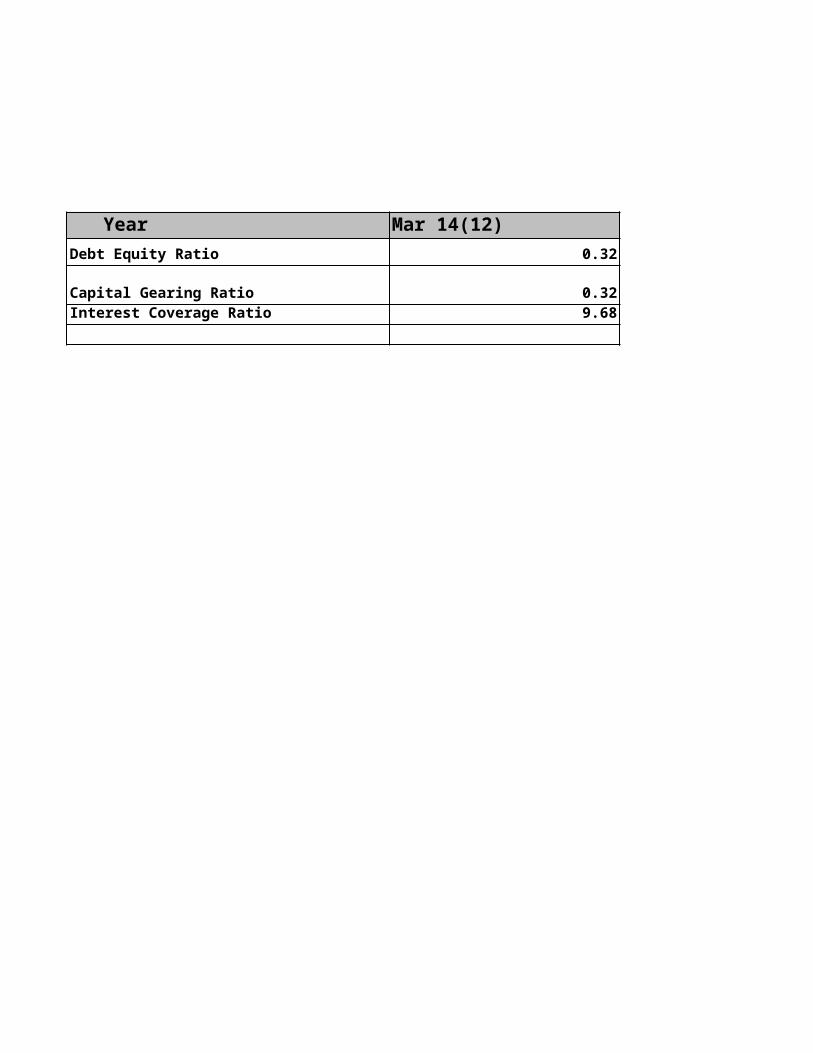

Interest Coverage Ratio

Comment

Debt equity Ratio

Comment

Capital Gearing Ratio

Comment

Solvency position of a company is measured by the solvency ratios such as Interest Coverage Ratio, Debt-Equity Ratio, Total Solvency position of a company is measured by the solvency ratios such as Interest Coverage Ratio, Debt-Equity Ratio, Total Assets to Debt Ratio etc. These ratios are used by money lenders and investors to check whether the company will be able to repay the loan or not

Interst Coverage Ratio = EBIT / Interest Expenses

Interest Coverage Ratio measures the number of times a company could make the interest

payments on its debt with its EBIT. It determines how easily a company can pay interest expenses on outstanding debt. RIL has a good Interest Coverage Ratio which

means that it is solvent enough to pay off its interest expenses on its outstanding

debtSince the current ratio of Reliance Industries Limited is very close to Rs. 1.5, we

can say that the company is in a good position to pay off its short term liabilities

Debt Equity Ratio = Long term Debt / Shareholders funds

As the value of the acid-test ratio is less than but close to 1, the company is stable in paying

off its short term obligations in time

Capital geraring ratio = Long term debt+ Preference share holders/ Equity Share

holders Fund

Since deployment of debt is cheaper than equity as interst on debt is tax deductable,

unlike dividend on equity shares which attract corporate dividend tax. Deployment of debt in

the capital structure of the company incereases EPS. RIL has don e the same thing

by deploying more of debt and thereby increasing EPS. It is visible in increse of

Capital Gearing Ratio from 0.24 to 0.32

Interest Coverage Ratio

Comment

Interst Coverage Ratio= EBIT/Interest expense

It measures the number of times by which interest expense of the company is covered by

the earnings of the company. In RIL, interst coverage ratio is 9.68 which signifies that the earnings are 9.68 times the interest obligatipn

which in turn implieas that the company is financially fit to serve its interest obligations.

Debt Equity Ratio

Capital Gearing RatioInterest Coverage Ratio

Year

0.32 0.24

0.32 0.249.68 9.66

Mar 14(12) Mar 13(12)

Liquidity position

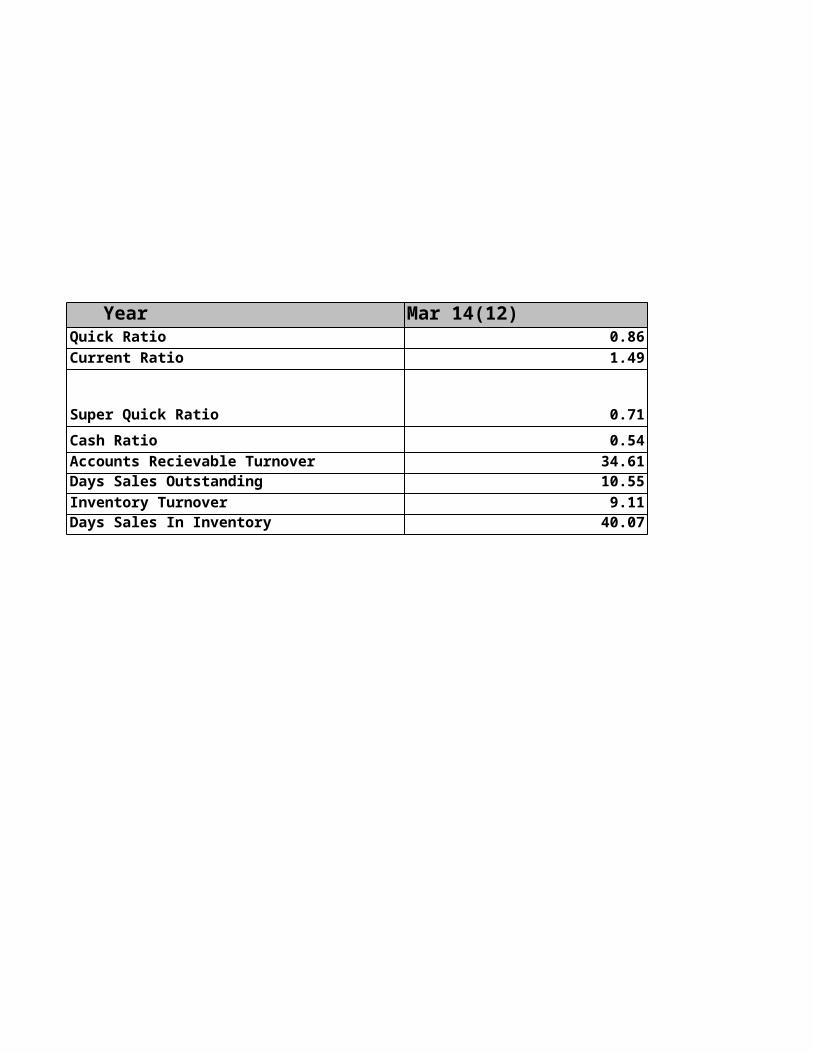

Quick Ratio

Acid-Test Ratio = 0.86

Comment

Current Ratio

Current Ratio = Current Assets / Current Liabilities

Comment

Super Quick Ratio

Comment

Cash Ratio

Comment

Liquidity ratios are the ratios that measure the ability of a company to meet its short term debt obligations. These ratios measure the ability of a company to pay off its short-term liabilities when they fall due. The liquidity ratios are a result of dividing cash and other liquid assets by the short term borrowings and current liabilities. They show the number of times the short term debt obligations are covered by the cash and liquid assets. If the value is greater than 1, it means the short term obligations are fully covered. Generally, the higher the liquidity ratios are, the higher the margin of safety that the company poses to meet its current liabilities. Liquidity ratios greater than 1 indicate that the company is in good financial health and it is less likely fall into financial difficulties.

Acid-Test Ratio = (Current Assets - Inventory) / Current Liabilities

As the value of the acid-test ratio is less than but close to 1, the company is stable in paying off its short term

obligations in time

Ideally, Current ratio should be 2, while Current Ratio value of 1.5 is also acceptable. It implies that to pay off a current liability of Re. 1, the company has a current asset of Rs. 1.5. Since the current ratio of Reliance Industries Limited is very close to Rs. 1.5, we can say that the company is in a good

position to pay off its short term liabilities

Super Quick Ratio= (Current Assets- Inventory - Receivables)/Current Liabilities

While the super quick ratio has decreased from 1.13 to 0.71, so the ability to pay off highly liquid assets for current

liabilities has decreased which is not a favourable sign.

Cash Ratio= Cash + Marketable Securities/Current Liabilities

Accounts Recievable urnover

Comment

Days Sales Outstanding

Comment

Inventory Turnover

Inventory Turnover= Net sales/Average Inventory

Comment

Days Sales In InventoryDays Sales In Inventory=365/Inventory Turnover

Comment

Since the Cash Ratio is applicable to very high liquid assets, the fall in its value to almost half has been phenomenal

and thus hampering cash flow for the company.

Accounts Recievable Turnover=Net Credit Sales/Average Debtors

As the Accounts Receivable turnover has increased from 23.78 to 34.61 which shows that the debtors have paid

more debt compared to last year and is a positive sign for the company.

Days Sales Outstanding= 365/Accounts Recievable Turnover

As the Days Sales Outstanding has decreased from the past year, so it shows that at the end of the day, the amount which remains to be sold has decreased by almost one

third;again a good sign for the company.

The inventory turnover is almost the same with a very slight decrease in it value which is not very significant. A high

Inventory Turnover is favourable as it shows inventories are getting converted to sales faster.

Likewise, the day sales in inventory doesn’t show appreciable changes apart from the fact that it shows a

slight increase in the inventory that is left at the end of the day. It is suppose to be as low as possible.

Quick RatioCurrent Ratio

Super Quick Ratio

Cash RatioAccounts Recievable TurnoverDays Sales OutstandingInventory TurnoverDays Sales In Inventory

Year

0.86 1.351.49 2.15

0.71 1.13

0.54 0.9234.61 23.7810.55 15.35

9.11 9.1640.07 39.86

Mar 14(12) Mar 13(12)

ROE 10.70 11.39ROA(%) 7.48 8.10Profit 30795.00 30505.00Capital Employed 287059.00 252447.00ROI(%) 10.73 12.08

ROI

ROI = Net Profit after Interest and Tax / Total Investment

Comment

Year Mar 14(12) Mar 13(12)

Return on Investment(ROI) is performane measure used to evaluate the efficiency of investment. It is one of the most commonly used appoaches for evaluating the feasibility and viability of investment.

RIL has an ROI of 10.73 % which means that on every 100 Rupees of investment, it is earning Rs. 10.73. But ROI has fallen from 12.08% in the previous year to 10.73% in the current year which shows worse utilisation of invested funds

Profitability Position

Net Profit Ratio Return On Capital Employed

Comment Comment

Gross Profit Ratio Price Earning Ratio

Comment Comment

Operating Profit Ratio Return On Equity(ROE)

ROE=PAT/Shareholders' Equity

Comment

Return On Total Assets

Profitability position of a company is measured by the profitability ratios such as Net Profit Ratio, Return on Capital Employed etc.

Net Profit Ratio = (Net profit after tax * 100/ Net

Sales)

Return On Capital Employed =(EBIT * 100 / Total Capital)

Net Profit Ratio of 5.03% is higher than other firms in petrochemicals industry

which varies from 0.83% to 3.45%. It means that the company is earning good profit as a percentage of

sales revenue

Net Profit Ratio of 5.03% is higher than other firms in petrochemicals industry which varies from 0.83%

to 3.45%. It means that the company is earning good profit as a

percentage of sales revenue

GrossProfit Ratio = (Gross Profit * 100/ Net

Sales)

Price Earning Ratio= Market Price/Earning per Share

Net Profit Ratio of 5.03% is higher than other firms in petrochemicals industry

which varies from 0.83% to 3.45%. It means that the company is earning good profit as a percentage of

sales revenue

The P/E ratio is a valuation ratio of a company's current price per

share compared to its earnings per share.A higher P/E ratio means that the market is more willing to pay for the earnings of the company

which is the case here.

Operating Profit Ratio = EBIT*100/Sales

Operating Ratio indicates how much profit a company

makes after paying for variable cost of production

such as wages, raw materials etc. Since it has fallen as compared to the

previous year, it means the profitability of the company

has come down

It measures the efficiency of utilisation of shareholder's fund. There hasn’t been a significant

change in it but it has decreased slightly and a decrease in ROE is

not favourable s it shows that shareholder's equity is not getting

properly utilised.

Return On Total Assets=EBIT*100/Total

Assets

Return on Assets (ROA) is a financial ratio that shows the

percentage ofprofit that a company earns in relation to its overall resources. It has decreased from last

year.

Net Profit Ratio 5.03 5.31Return On Capital Employed 11.94 20.36

Gross profit Ratio 11.111794666728 11.1416414791Price Earning RatioOperating Ratio 7.9524860490571 8.13773081652

Return on Equity 10.235611976194 10.9523830685Return on Total Assets 8.7301051304563 9.57175223134

Year Mar 14(12) Mar 13(12)

Price to Sales Ratio

Comment

Price to Book Value

Comment

Price to Earnings

Comment

Price To Sales ratio= Market Capitalisation/ Net Sales

This ratio implies the amount whiich investor has to invest for unit of sales

revenue. Aratio lower than 1 is cosidered one. Since RIL s Price to Sales ratio

is .64, the investor has to invest Rs. 64 per unit of sales revenue

Price to Book Value=Market Price/Book Value Price

This is the ratio between market value and intrinsic value of a share.a ratio

more than one implies that investors are optimistic abut the growth of the

company in the future. Price to Book Value of RIL is 1.52, which shows the

optimism of the investors and positive sentiments in the market about the

company

Price to Earnings=Market Price per share/Earnings per share

It is the ratio between market value of a share and the earning per share. Hogher the PE ratio, better it is. RILs PE ratio of

13.97 again signifies the positive sentiment in the market.

Price to sales 0.64 0.70

Price to Book Value 1.52 1.40Price to Earning 13.97 12.22

No of shares in current year 3231901858

No of shares in previous year 3228663382Book Value/Share 609.83 557.57Market Price 929.50 778.15

Year Mar 14 Mar 13

Economic Value Added = NOPAT-Cost of Capital Mar-14 Mar-13

NOPAT (Net Operating Profit After Tax)+ Profit After Tax + Finance Cost 23,379.47 22,752.48Cost of Capital Assumed to be 12%

Capital employed = Shareholders Funds + Long term Borrowings 259,802.00 242,731.00EVA -7,796.77 -6,375.24

Market Value Added= Market Capitalisation-Book Value of Capital Employed

Mar-14 Mar-131033142777011 7.1218E+11

Comment on overall performance of the company

Solvency position of Reliance Industries Limited is good because of low share of debt funds in the capital structure and high interest coverage ratio which in turn signifies that the company is financially stable to pay of its interest obligation as and when they fall due. But as far as the liquidity is concerned, a quick ratio less than one impies that the liquid assets are not sufficient to satisfy the current liabilities. An analysis of debtors turnover ratio tells us that the average collection period has fallen down from 15.35 in the previous

year to 10.55 in the current year. Which means the company is now able to convert its debtors into cash with a greater efficiency. ROI has fallen from 12.08% in the previous year to 10.73% in the current year which shows worse utilisation of invested funds.

Return on Equity as well as Return on assets has fallen down significantly, which in turn shows the worse utilisation of funds. But still the market sentiments are positive toward the company and investors are optimistic about the growth of the company. It can be

observed from price to book value ratio of 1.52 as well as price to earning ratio at 13.97. As the CFO of the company, I would advice the company to concentrate on the operational efficiency of the company by putting more efforts to increase the sales revenue or

increase profitability by pairing some indirect expenses.

Comment on overall performance of the company

Solvency position of Reliance Industries Limited is good because of low share of debt funds in the capital structure and high interest coverage ratio which in turn signifies that the company is financially stable to pay of its interest obligation as and when they fall due. But as far as the liquidity is concerned, a quick ratio less than one impies that the liquid assets are not sufficient to satisfy the current liabilities. An analysis of debtors turnover ratio tells us that the average collection period has fallen down from 15.35 in the previous

year to 10.55 in the current year. Which means the company is now able to convert its debtors into cash with a greater efficiency. ROI has fallen from 12.08% in the previous year to 10.73% in the current year which shows worse utilisation of invested funds.

Return on Equity as well as Return on assets has fallen down significantly, which in turn shows the worse utilisation of funds. But still the market sentiments are positive toward the company and investors are optimistic about the growth of the company. It can be

observed from price to book value ratio of 1.52 as well as price to earning ratio at 13.97. As the CFO of the company, I would advice the company to concentrate on the operational efficiency of the company by putting more efforts to increase the sales revenue or

increase profitability by pairing some indirect expenses.