61

FINANCIAL AID NIGHT 2015 – 2016 1

| Date post: | 16-Dec-2015 |

| Category: |

Documents |

| Upload: | karla-baskerville |

| View: | 212 times |

| Download: | 0 times |

FINANCIAL AID NIGHT

2015 – 2016

1

Understanding the College and Financial Aid Application Process

• Be patient, thorough, and organized as you go through the college admission and financial aid application process

• The steps are fairly similar, regardless of college

• It will be toward the end of your senior year when you will finally know what your out-of-pocket costs will be to attend a particular college(s).

2

Senior Year College Process

Apply for admission and merit-based scholarships for all colleges you likeFile the 2015-16 FAFSA by March 10Apply for private, outside scholarshipsFinancial Aid Notification Letters come from colleges,

likely between March 15-April 15Compare your aid offers Make final college decision by May 1 Return all required forms to your chosen college

3

Sources of Aid

•Colleges

•State of Indiana

•Federal government

•Schools, churches, clubs, businesses, foundations, parents’ employers, etc.

Types of Aid

•Scholarships - “gift aid” based on student’s merit

•Grants - “gift aid” based on financial need

•Student Loans - student repays after graduation •Work-study - campus job

Financial Aid “Package”

• Ultimately, you may have a financial aid “package” that is comprised of many different types of financial aid from several sources.

• Tonight we’ll discuss how to apply for all types of aid from all sources.

5

Applying for Admission is the key!

Student must be accepted for admission by the college(s) before any formal offer of scholarship or financial aid is made.

6

APPLY FOR MERIT-BASED SCHOLARSHIPS FROM COLLEGES

• These may be based on academics, talents, athletics, or affiliations.

• Follow the steps and deadlines dictated by each college.

• Colleges decide criteria and amounts.

7

APPLY FOR PRIVATE SCHOLARSHIPS

• Good info from Guidance Office about these!

• Private scholarships can be funded by community groups, churches, foundations, parents’ employers, businesses, etc.

• Don’t pay a person or service to do this for you!

• Good Online Scholarship search resources: https://bigfuture.collegeboard.org/scholarship-searchhttps://mycollegedollars.hyfnrsx1.com/

8

WHAT IS THE FAFSA?

• The Free Application for Federal Student Aid (FAFSA) collects demographic and financial information about the student and family.

• It is the ONLY way to apply for federal and state of Indiana financial aid and is the primary application used by most colleges to distribute their own need-based funds.

• Some colleges may ask you for a supplemental financial aid application, in addition to the FAFSA. Example of one such form is the “CSS Profile.”

9

www.fafsa.gov• Beware of www.fafsa.COM --- They will charge a fee!

Official FAFSA is free.

• File the 2015-16 FAFSA -- NOT 2014-15 (it is for current year)

• Filing by March 10 is a MUST for Indiana residents

• You can direct your FAFSA to multiple colleges at once by listing their code.

10

Why file the FAFSA even if you don’t think you will qualify for aid?

• The FAFSA must be filed in order to use federal student or parent loans, which typically have more favorable terms than private educational loans.

• Some families place a value on requiring the student to partner with them in funding college. Student can do this by using student loans.

• If you have more than one child in college at the same time, you may qualify for more aid.

11

• It is dangerous to make assumptions that you make too much money. Myths abound about the FAFSA and aid.

• It may allow college to re-evaluate eligibility in the event of unforeseen changes in family circumstances. College can more quickly assist you if things change mid-year.

Why file the FAFSA?

13

14

BEFORE YOU BEGIN:

Parent and student PINs may be created at PIN site prior to

starting the FAFSA - recommended

AFTER FAFSA HAS BEEN SUBMITTED: You can log back in to make corrections, etc. SAR may be printed after FAFSA has

been processed.

PINs for FAFSA• Student AND one parent must each create a PIN at www.pin.ed.gov.

• PIN serves as a “signature” for the online FAFSA; may submit without, but FAFSA will not be fully processed until “signed” with PINs.

• PIN will be needed to change/correct FAFSA; both PINs (student + parent) must be applied each time FAFSA is updated.

15

FAFSA ID (new in Spring 2015)

• In late spring 2015, users who access FAFSA with their PINs will be prompted to create a FAFSA ID

• FAFSA ID will replace the PIN

• Purpose is to enhance security of personal information and identity

16

17

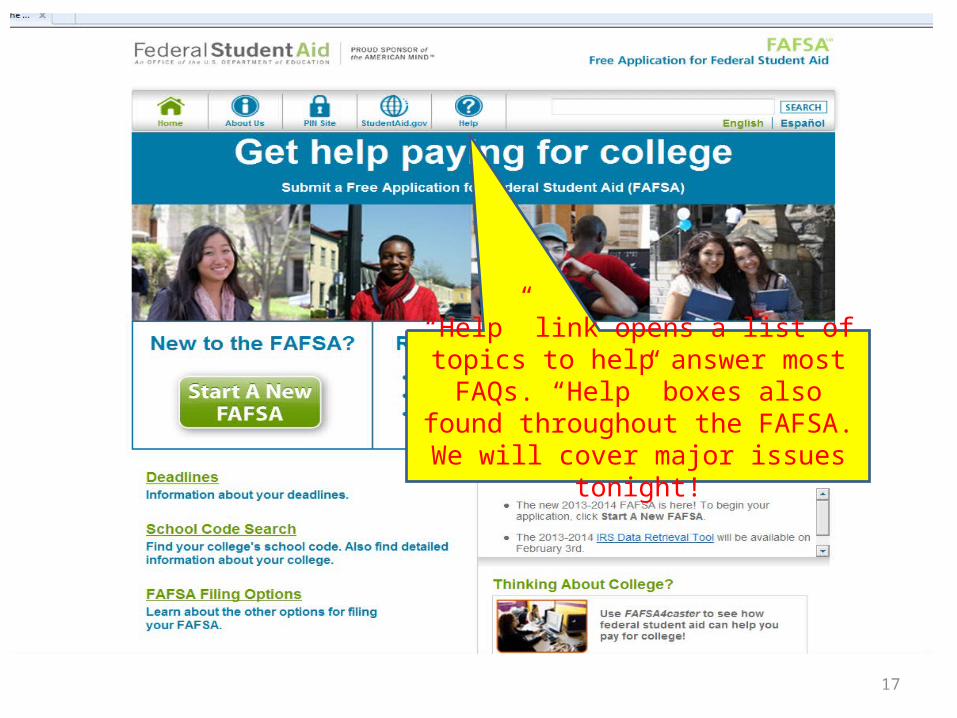

“Help” link opens a list of topics to help answer most FAQs. “Help” boxes also found throughout the FAFSA. We will

cover major issues tonight!

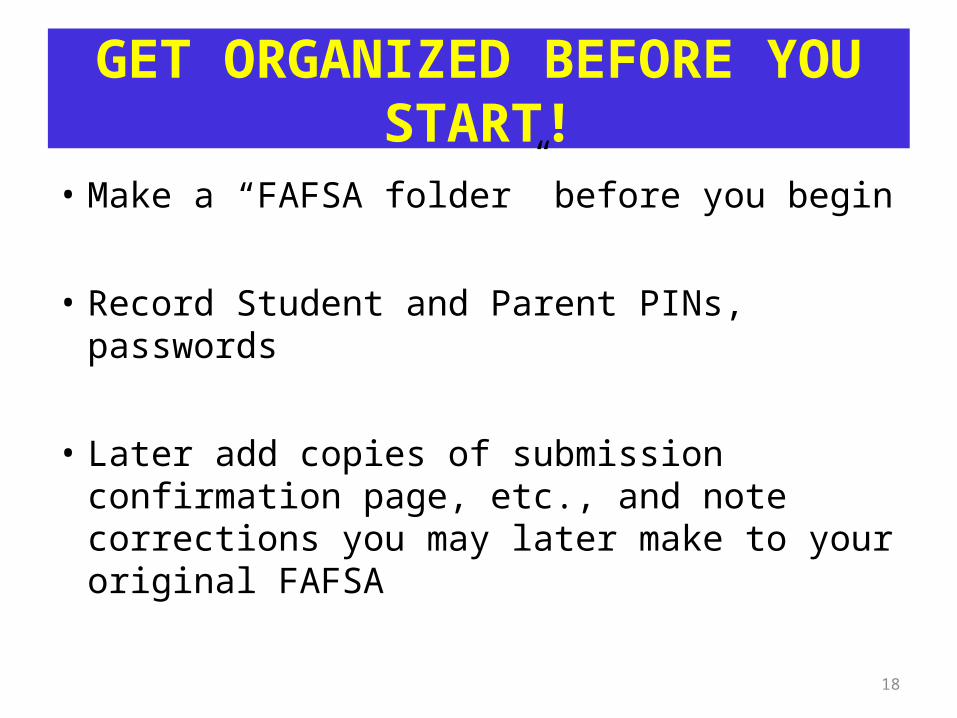

GET ORGANIZED BEFORE YOU START!

• Make a “FAFSA folder” before you begin

• Record Student and Parent PINs, passwords

• Later add copies of submission confirmation page, etc., and note corrections you may later make to your original FAFSA

18

FAFSA can be done in stages• Student can begin FAFSA and enter all demographic information;

parents can complete their pages at another time

• Each page is saved when completed

• FAFSA can be reopened and continue to be completed prior to submission.

• You MUST know PIN and Passwords to reopen and continue to work on a saved FAFSA!!

• FAFSA can be corrected after submission

19

20

Begin here for initial FAFSA

Access your FAFSA here after first time, whether submitted or just saved. Must

know PIN.

File the 2015-16 FAFSA

Watch carefully if “Student“ or “Parent” info is needed on each screen.

STUDENT is the applicant, not the parent

Help and Hints - lists question numbers and offers detailed explanation.

The system automatically saves the application at the end of each step.

22

Most questions

have detailed

help as you go along.

FAFSA will be saved after each click of

“next”

Must correct obvious errors

before going to next page

Dependency Status

• The FAFSA narrowly defines the situations that make a student “independent” according to the FAFSA

• “My parents don’t plan to pay for my college” does NOT make the student independent

• “What if my parents don’t claim me on their taxes?” - NO -- still not independent for the FAFSA.

Dependency Status

• Include parent information on the FAFSA, unless you can officially answer “yes” to one of the questions defining your Dependency Status

25

PARENT INFORMATION

• Who is considered a parent? “Parent” refers to a biological or adoptive parent. Grandparents, foster parents, legal guardians, older siblings, and uncles or aunts are not considered parents for the FAFSA unless they legally adopted you.

• In case of divorce or separation give information about the parent you live with the most. If your divorced or widowed parent has remarried, your FAFSA household is your custodial parent + stepparent and all who live there and receive support.

26

Household for FAFSA

Figure out home base • Filling out the FAFSA is NOT

connected to who pays the bill in the end

• It is OK to get aid based upon one parent’s income, even if a different parent will pay the bill

• Child support being received or paid has a place to be reported on the FAFSA

• Does NOT matter who claims child as dependent on taxes

How many in college?

• Count all dependent siblings as long as they will enroll for at least ½ time (6 credits per semester) in the UPCOMING school year

• Parents are NOT supposed to be counted. This should be discussed with college if parent is full-time and family is incurring expense.

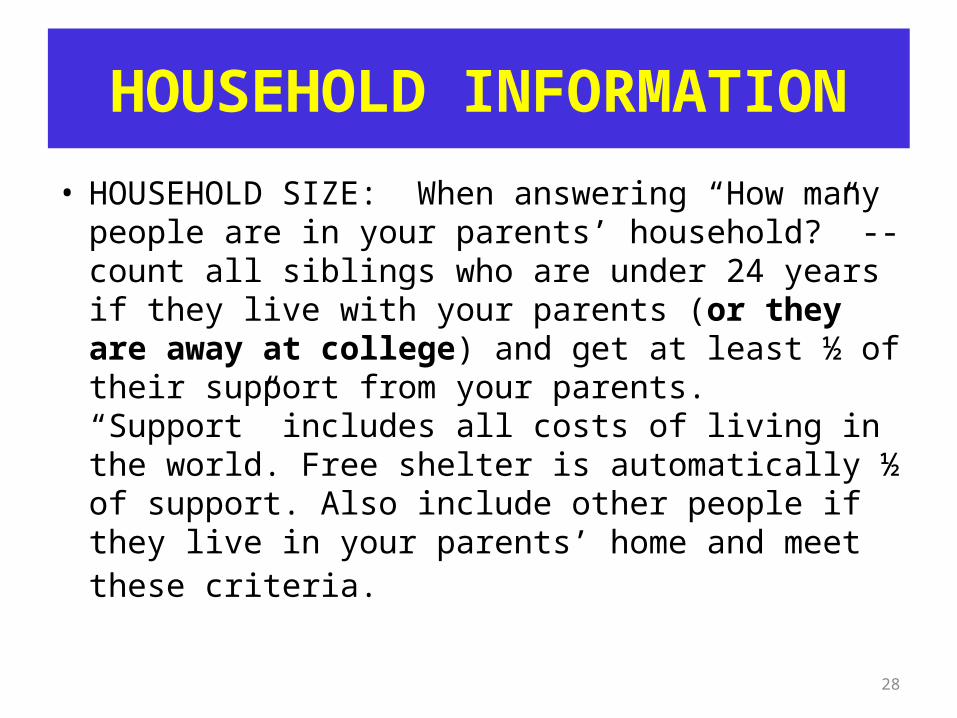

HOUSEHOLD INFORMATION

• HOUSEHOLD SIZE: When answering “How many people are in your parents’ household?” -- count all siblings who are under 24 years if they live with your parents (or they are away at college) and get at least ½ of their support from your parents. “Support” includes all costs of living in the world. Free shelter is automatically ½ of support. Also include other people if they live in your parents’ home and meet these criteria.

28

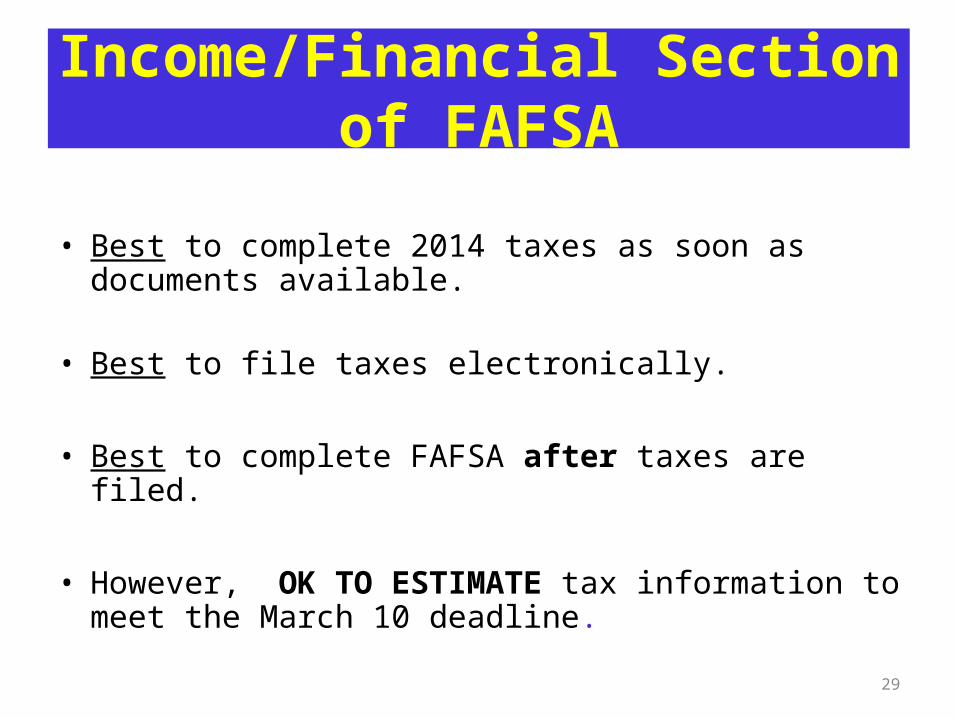

Income/Financial Section of FAFSA

• Best to complete 2014 taxes as soon as documents available.

• Best to file taxes electronically.

• Best to complete FAFSA after taxes are filed.

• However, OK TO ESTIMATE tax information to meet the March 10 deadline.

29

IRS Data Retrieval for Tax info

• Allows transfer of IRS data into FAFSA. Available for electronic filers after about 3 weeks; mail-in filers must wait approx. 8-11 weeks.

• May use to initially provide tax info , OR….

• Update later as a “correction” if estimated tax info used when filing FAFSA initially

• May be used for BOTH student AND parent tax information

Indicate if taxes are “already

completed” or “Will file”

Try to use the IRS Data

Retrieval Tool if conditions

allow. Otherwise, put

tax info in manually and correct later

using IRS Data Retrieval.

31

32

33

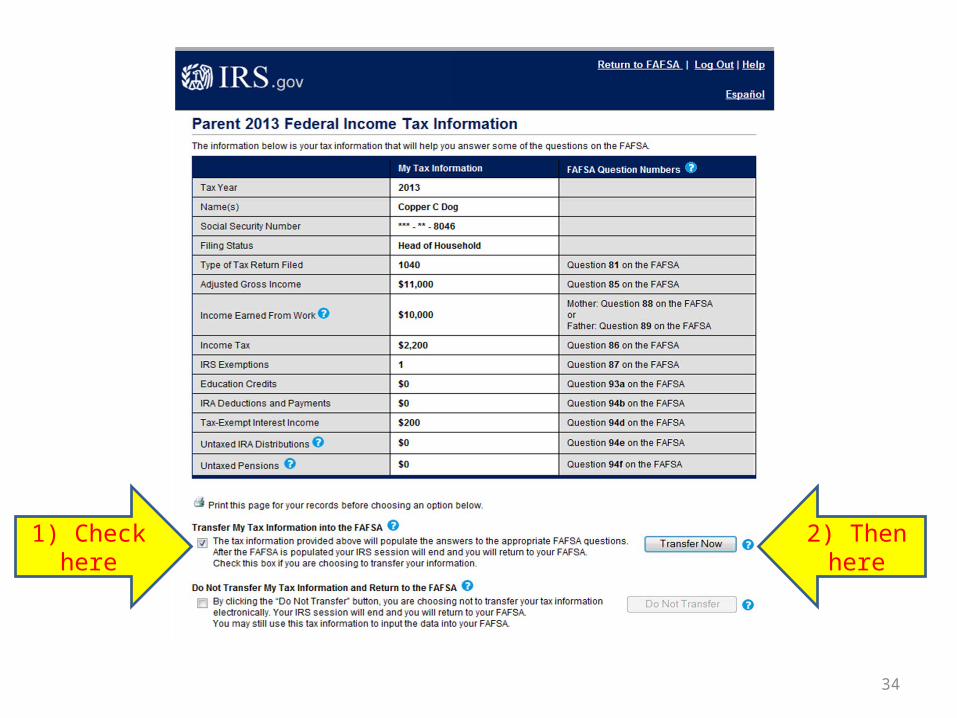

First screen in IRS Data Retrieval Tool will ask you to fill in

filing status and address (must be

exactly as shown on tax return.

If a match is found, it displays the

actual tax numbers.

34

1) Check here

2) Then here

35

Successful IRS D/R will show messages

on FAFSA

Do NOT change any information that says “Transferred

from the IRS”

If Required to Report Assets

• If asked to report assets – carefully read instructions about what to report and what is NOT to be included

• NOT included: Home in which you live, cars, life insurance, amount accumulated in retirement plans (for example 401K, etc.)

• Detailed instructions re: assets are found online while filing FAFSA and on page 2 of paper FAFSA

Business Value/Assets

• Note that family-owned businesses with fewer than 100 employees is EXCLUDED (see definition on page 2 of paper FAFSA or via online instructions)

FARM

• Note that a family farm that family lives on and operates is EXCLUDED as an asset (see definition on page 2 of paper FAFSA or via online instructions)

How much aid did I receive?

• Aid notification does not come from the FAFSA processor.

• Each college listed on your FAFSA will notify you about your financial aid in the spring, as long as you have been admitted

• Aid types and amounts can be different from each college

39

40

41

“Disagree” will be the default. Must change to “Agree” to continue.

Student and one parent will “sign” with PIN.

42

Short-cut to second child’s

FAFSA

Initial EFC index

displays here.

Colleges will use to calculate

aid.

FAFSA is not officially

submitted until you see Confirmation

page

VERIFICATION OF FAFSA

• Some FAFSAs are selected for review in a process called “verification” by the FAFSA processor or the college.

• College must confirm accuracy of FAFSA information before disbursing aid. Must follow college’s instructions to comply.

• Using IRS Data Retrieval assists you in complying with requests for verification of your FAFSA.

• Offer of aid is an estimate until verification process is completed.

43

SPECIAL CIRCUMSTANCES

• There is no way to explain special things on the FAFSA. Unusual circumstances must be discussed with a financial aid officer at the college(s) the student is considering.

• Examples include: – Recent job loss– Death of parent in prior or current year– Recent divorce or separation of parents– Large medical bills – Private school tuition for younger siblings

44

Direct Costs vs. Cost of Attendance

Direct Costs• These are costs that are

billed by the university.

• May include tuition, student fees, room, and meal plan.

• Understand each colleges direct costs and how they may be paid.

“Cost of Attendance”• This is a figure used to

calculate financial aid eligibility. Includes direct costs plus allowances for other educational expenses such as books, personal expenses, transportation.

• Maximum aid that student can receive.

45

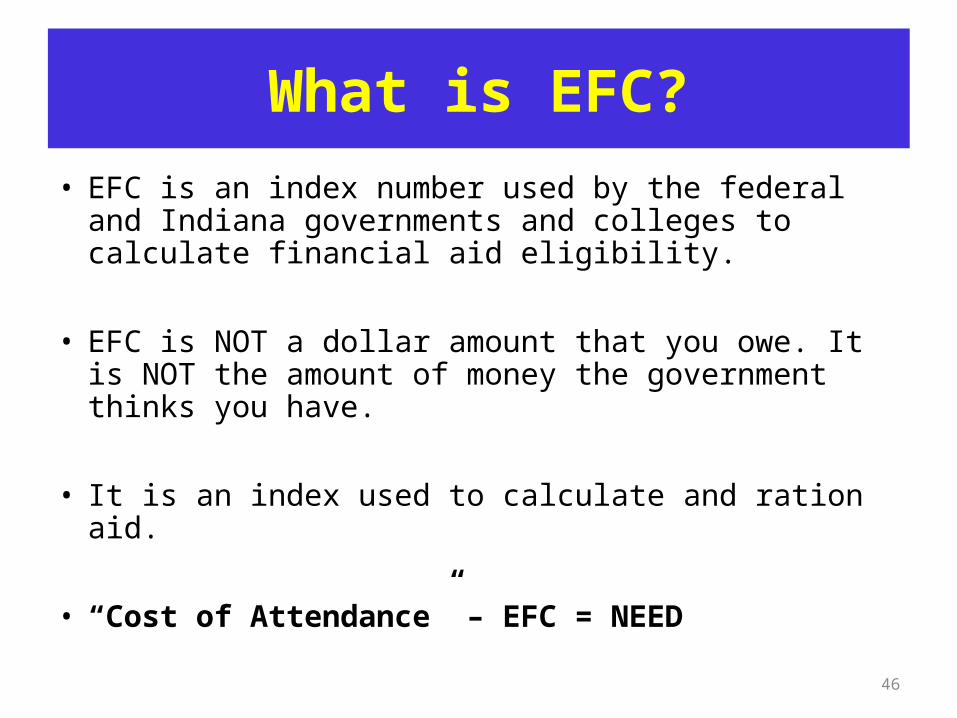

What is EFC?

• EFC is an index number used by the federal and Indiana governments and colleges to calculate financial aid eligibility.

• EFC is NOT a dollar amount that you owe. It is NOT the amount of money the government thinks you have.

• It is an index used to calculate and ration aid.

• “Cost of Attendance” – EFC = NEED

46

Cost ($) - EFC = “Need”

47

Federal Pell Grant

• Needy students may be offered a Federal Pell Grant – gift aid which is not repaid.

• Amount is often same at different colleges, and prorated for part-time enrollment.

• Eligibility is directly connected with EFC index.

48

State of Indiana Grants• FAFSA will load into State’s system – Division of Student

Financial Aid for the Indiana Commission on Higher Education.

• FAFSA must be received by March 10 ! No exceptions!

• 21st Century Scholars is one of the state’s aid programs; also Frank O’Bannon Higher Education (public colleges) and Freedom of Choice Award (private colleges).

• Amounts vary by college and diploma type. Amounts are related to EFC.

49

• http://www.in.gov/sfa

• Create an eStudent Account to view your state aid record

• FAFSA errors (“edits”) must be corrected by May 15 or eligibility is forfeited

State of Indiana Grants, cont.

50

51

Create an “eStudent” account to view your

status for state grants

Federal Direct Stafford Loan

• Annual eligibility, up to maximum of $5,500 will be listed on colleges’ aid offers

• All FAFSA filers are eligible for this loan

• Loan in student’s name

• Student repays loan after college

52

Subsidized vs. Unsubsidized Loan Amounts

• Subsidized portions do not accrue interest during college. Maximum subsidized is $3,500 for first-year college student.

• Unsubsidized portions accrue interest during college. Current fixed rate is 4.66%.

• Sub vs. Unsub amounts may vary by college

53

Other Aid You May be Offered

• Some colleges may offer a “grant” which does not have to be repaid.

• Federal Work-study – a job on campus where students earn wages. Understand how many hours per week are expected and how the student secures the job.

• Federal Perkins Loan – a loan in student’s name with repayment after college. Funds are limited and college determines who is offered the funds.

54

How will you pay your balance?

• Understand how much you will owe the college after all financial aid has been subtracted

• Understand the ways you may elect to pay that balance: by the semester, monthly installments, Federal Parent PLUS Loan, additional private loan for student?

55

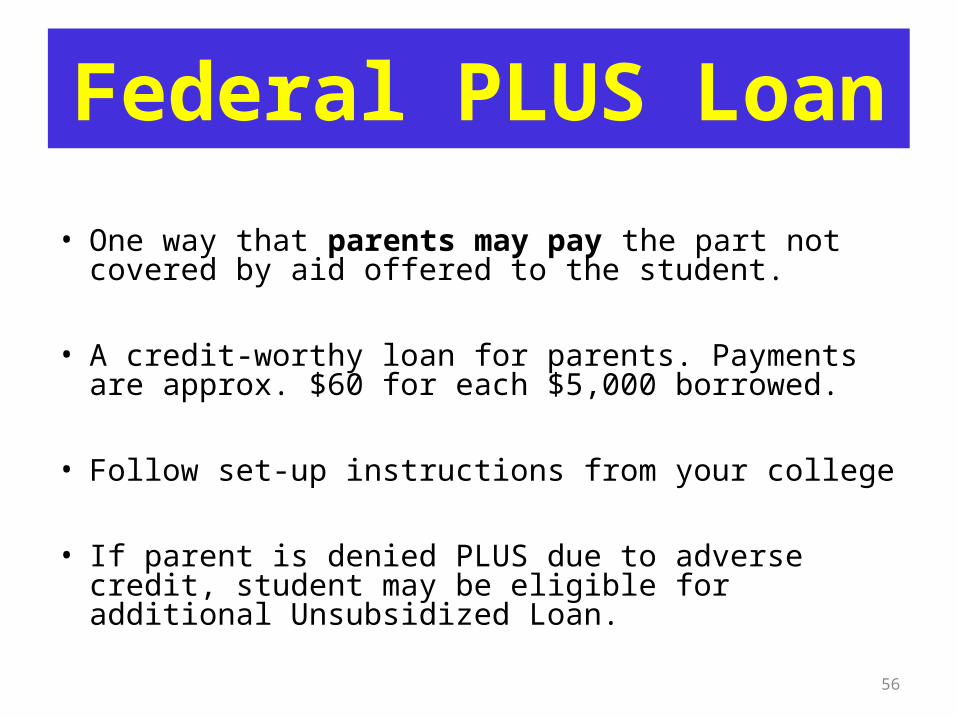

Federal PLUS Loan

• One way that parents may pay the part not covered by aid offered to the student.

• A credit-worthy loan for parents. Payments are approx. $60 for each $5,000 borrowed.

• Follow set-up instructions from your college

• If parent is denied PLUS due to adverse credit, student may be eligible for additional Unsubsidized Loan.

56

www.studentloans.gov

• Go to studentloans.gov for more information about both federal student/parent loans.

57

Private Educational Loans

• There are dozens of private educational lenders.

• Most offer loan in the student’s name with repayment after college. Interest will accrue during college.

• Most require an adult, credit-worthy co-signer, although it usually does NOT have to be a parent.

58

Senior Year Checklist

Apply for admission and merit-based scholarships for all colleges you likeFile the 2015-16 FAFSA before March 10Apply for private, outside scholarships Financial Aid Notification Letters come from colleges,

likely between March 15-April 15Compare your aid offers Make final college decision by May 1 Return all required forms to your chosen college

59

College Goal Sunday

• Financial Aid Counselors will be available to assist with questions while you file the FAFSA.

• Sunday, February 22 at IVY Tech at 2:00 p.m.

• www.collegegoalsunday.org

60

Education is Important!• “An investment in knowledge pays the best interest.” ~~ Benjamin Franklin

• “Energy and persistence conquer all things.” ~~ Benjamin Franklin

• “By failing to prepare, you are preparing to fail.” ~~ Benjamin Franklin

• “Education is the most powerful weapon you can use to change the world.” ~~ Nelson Mandela

• “Education is the golden key to unlock the door of freedom.” – George Washington Carver

• “Live as if you were to die tomorrow. Learn as if you were to live forever.” ~~ Mahatma Gandhi

61