Page 1

Executive Summary

The report provides a brief analysis of the financial performance of the company Titas Gas

Transmission and Distribution Company Limited of the years 2007 to 2011. From the balance

sheets and income statements from Titas gas, a vertical balance sheet and income statement is

created. In the vertical balance sheet, all figures are divided by total assets and expressed as a

percentage. In the vertical income statements, all figures are divided by sales and expressed as a

percentage, including averages and standard deviations. The horizontal balance sheets and

income statements are produced using a different approach. The figures are based on the year

2007, and all base year figures are taken as 100%. All the other items are expressed as a

percentage of its base year figures. The report further forecasts income statements and balance

sheets for 2012 and 2013.

This report also provides ratio analysis of year 2007 to 2011 and these ratios are calculated and

interpreted so that a trend of the performance in particular areas may be observed. The derived

data is also used to compare against past performances of the company and current performances

of existing competitors. Graphical representation is also provided for better understanding of the

numerical content. The method of analysis used is trend analysis for the mentioned years. The

types of ratios discussed are liquidity, asset management, debt management, and profitability and

stock-market ratios. The calculations are shown in details in the appendix and the formulas are

given within the ratio tables.

Required market return is determined using a risk free rate of 9.05 which is set by Bangladesh

Bank. Beta is calculated using market returns from July 2008 to July 2011. A weighted average

cost of capital is calculated using cost of equity, cost of debt and cost of retained earnings. This

helped us formulate an optimum capital structure for Titas. Finally, the report determined

intrinsic price using the dividend discount model. The calculations are shown in details in the

appendix and the formulas are given within the ratio tables.

In fact, the report has established a comprehensive view to understand company’s financial

position and the market performance of the company through important indicators and authentic

interpretations.

Page 2

Introduction

The report has represented an overall financial and market position of the company ‘Titas Gas

Transmission Co. Ltd. Preparing this report, the company has been compared with the companies

which are enlisted in DSE in the same industry sector named ‘Fuel and Energy Sector’.

The report has tried to understand the company’s current financial position and compared it with

previous performance. Moreover, monthly market return has been realized to understand the

company’s volatility with market and the required rate of return that a shareholder can assume as

a perfect rate of return.

Moreover, report has tried to understand industry condition and tried to find the Titas Gas

Transmission Co Ltd. Loop holes in different performance indicator while giving suggestion to

improve the situation.

Company Background

Titas Gas T & D Co. Ltd. (TGTDCL) was formed in November 1964 as a joint Stock Company

(Under the Company’s Act 1913) of the central Government of Pakistan on the one hand and

Pakistan Shell Oil Company on the other, with a view to transmitting and distributing natural gas

to the Dhaka city the then provincial capital of Pakistan from the discovered gas field called

“Titas” located on the bank of the River Titas, within the close vicinity of the present

Brahmanbaria district of Bangladesh. The authorized capital was Taka 17.8 million only, divided

into 17800 shares of Taka 10.00 each. Ninety percent of the shares were subscribed by the then

central Government of Pakistan and remaining ten percent by the Shell Oil Company.

In December 1971, after nine months of liberation war, Bangladesh emerged in the world map as

a new independent state with the same geographical boundary of the then East Pakistan. In

March 26, 1972 Govt. has formed “ Bangladesh Oil, Gas & Mineral Corporation (BOGMC)

under the Presidential Executive Order and Titas Gas T&D Co. Ltd. has become an enterprise of

BOGMC. Titas Gas T&D Co. Ltd. which was earlier established as a joint stock company with

90% share capital of the Govt. of Pakistan naturally vested to the Govt. of the People’s Republic

Page 3

of Bangladesh and the rest 10% share capital of Pakistan Shell Oil Company was transferred to

the newly formed Bangladesh Shell Oil Company. During 1975, under the nationalization

program, Govt. has brought back 10% share of Shell Oil Co. and Titas Gas T&D Co. Ltd. has

become a 100% Government owned Company. Meanwhile, during August1974, Bangladesh Oil

& Gas Corporation/Petrobangla and during October 1975, Ministry of Energy & Mineral

Resources had been formed. TGTDCL has been placed under the administrative control of the

newly formed ministry along with Petrobangla and its subsidiary Companys.

The basic objective of the Company was to construct, own and operate natural gas transmission

& distribution facilities in the mid-eastern region of Bangladesh i.e. Comilla, Mymensingh and

Dhaka district with the right of purchasing, transmission, distribution, sales and disposal of

natural gas within the jurisdiction of greater districts before creation of new districts.

Common Size Statements

Titas Gas Transmission and Distribution Company Limited

Vertical balance sheet

2007 2008 2009 2010 2011 AVERA

GE

STANDA

RD

DEVIATI

ON

1. CAPITAL

AND

RESERVES

28.9215

%

37.3510

%

38.7550

%

41.5726

%

47.2751

%

38.7750

%

6.6932%

a) Share

capital

7.1077% 23.3623

%

19.9490

%

16.9568

%

15.7679

%

16.6288

%

6.0800%

b) Deposits

for Share

0.0020% 0.0029% 0.0039% 0.0136% 0.0490% 0.0143% 0.0200%

Page 4

c) Capital

reserves

2.2455% 2.0586% 1.7578% 1.4942% 1.2631% 1.7639% 0.4007%

d) Revenue

reserves

19.5663

%

11.9272

%

17.0443

%

23.1080

%

30.1951

%

20.3682

%

6.8377%

2. LONG-

TERM

BORROWIN

GS

13.6503

%

7.3386% 5.9360% 4.2541% 3.4960% 6.9350% 4.0395%

a) Unsecured

loans - local

sources

4.6579% 0.0000% 0.0000% 0.0001% 0.0053% 0.9327% 2.0825%

b) Unsecured

loans -

foreign

sources

8.9925% 7.3386% 5.9360% 4.2540% 3.4907% 6.0024% 2.2414%

3. OTHER

LONG-

TERM

LIABILITIES

15.5279

%

17.3713

%

17.3848

%

15.7697

%

13.5497

%

15.9207

%

1.5848%

a) Pension

fund

1.4845% 1.4146% 1.1988% 0.9892% 0.7723% 1.1719% 0.2960%

b) Gratuity 0.0276% 0.0287% 0.0223% 0.0293% 0.0263% 0.0268% 0.0028%

Page 5

c) Leave pay 0.3934% 0.3874% 0.3446% 0.3208% 0.2888% 0.3470% 0.0443%

d) General

provident

fund

0.5817% 0.9121% 0.8861% 0.8276% 0.7522% 0.7919% 0.1326%

e) Customers'

security

deposits

13.0407

%

14.6285

%

14.9331

%

13.6028

%

11.7100

%

13.5830

%

1.2960%

4. TOTAL

CAPITAL

EMPLOYED

58.0997

%

62.0609

%

62.0759

%

61.5964

%

64.3208

%

61.6307

%

2.2410%

APPLICATI

ON OF

FUNDS :

0.0000% 0.0000% 0.0000% 0.0000% 0.0000% 0.0000% 0.0000%

5. FIXED

ASSETS

35.3803

%

31.9513

%

27.3558

%

22.5859

%

19.3961

%

27.3339

%

6.5502%

a) Fixed

assets (at

cost- less

accum.

depreciation)

35.3716

%

31.9404

%

27.3375

%

22.3235

%

18.8006

%

27.1547

%

6.7747%

b) Capital

work-in-

progress

0.0088% 0.0109% 0.0182% 0.2624% 0.5955% 0.1792% 0.2567%

Page 6

6.

INVESTME

NTS AND

OTHER

ASSETS

14.5783

%

16.7379

%

23.8109

%

31.3809

%

36.1923

%

24.5401

%

9.2630%

a) Long-term

bank deposits

12.0701

%

14.5220

%

21.9376

%

29.9952

%

34.5558

%

22.6161

%

9.6721%

b) Loan to

employees

2.5082% 2.2159% 1.8734% 1.3857% 1.6366% 1.9239% 0.4476%

7. CURRENT

ASSETS

50.0414

%

51.3108

%

48.8333

%

46.0332

%

44.4116

%

48.1261

%

2.8499%

a) Inventories

of stores and

other

materials

3.9339% 3.9198% 4.2662% 3.6019% 3.0377% 3.7519% 0.4633%

b) Advances,

deposits and

prepayments

0.7680% 2.9310% 0.6486% 0.6848% 0.4050% 1.0875% 1.0394%

c) Trade

debtors (Net)

41.1249

%

38.6690

%

30.3638

%

27.9368

%

25.5293

%

32.7248

%

6.8222%

d) Cash and

bank balances

3.5031% 5.4864% 12.0233

%

12.2200

%

13.3685

%

9.3203% 4.4900%

Page 7

e) Other

current assets

0.7115% 0.3045% 1.5313% 1.5897% 2.0711% 1.2416% 0.7163%

TOTAL

ASSET

100.0000

%

100.0000

%

100.0000

%

100.0000

%

100.0000

%

100.0000

%

0.0000%

8.

CURRENT

LIABILITIES

( 8i + 8ii )

41.9003

%

37.9391

%

37.9241

%

38.4036

%

35.6792

%

38.3693

%

2.2410%

i) GROUP

COMPANY

ACCOUNTS

34.7699

%

25.6940

%

24.9805

%

24.0934

%

23.4682

%

26.6012

%

4.6444%

a) Payable for

gas purchase

&

transmission

31.8303

%

23.8113

%

22.7944

%

20.2214

%

1.8943% 20.1103

%

11.0690%

b) Payable for

PDF&

BAPEX

margin

3.2323% 2.1774% 1.6848% 1.6378% 2.3397% 2.2144% 0.6454%

c) Payable for

defi cit

wellhead

margin fund

for BAPEX

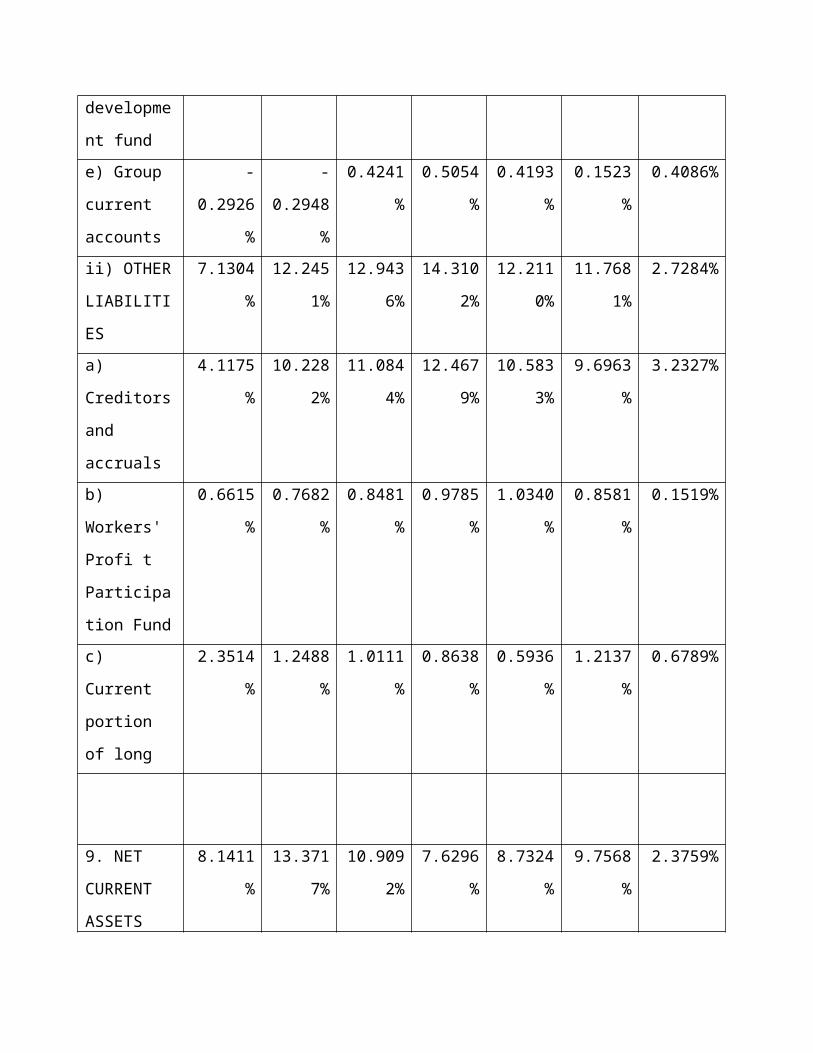

0.0000% 0.0000% 0.0771% 0.0911% 0.1331% 0.0603% 0.0588%

d) Payable for

gas

development

0.0000% 0.0000% 0.0000% 1.6377% 1.6332% 0.6542% 0.8958%

Page 8

fund

e) Group

current

accounts

-0.2926% -

0.2948%

0.4241% 0.5054% 0.4193% 0.1523% 0.4086%

ii) OTHER

LIABILITIES

7.1304% 12.2451

%

12.9436

%

14.3102

%

12.2110

%

11.7681

%

2.7284%

a) Creditors

and accruals

4.1175% 10.2282

%

11.0844

%

12.4679

%

10.5833

%

9.6963% 3.2327%

b) Workers'

Profi t

Participation

Fund

0.6615% 0.7682% 0.8481% 0.9785% 1.0340% 0.8581% 0.1519%

c) Current

portion of

long

2.3514% 1.2488% 1.0111% 0.8638% 0.5936% 1.2137% 0.6789%

9. NET

CURRENT

ASSETS ( 7

8.1411% 13.3717

%

10.9092

%

7.6296% 8.7324% 9.7568% 2.3759%

10. NET

ASSETS

( 5+6+9 )

58.0997

%

61.9627

%

62.0759

%

61.5964

%

64.3208

%

61.6111

%

2.2367%

Page 9

Here all the figures were divided by Total assets of that particular year and they were expressed

as a percentage of that year’s total asset.

Titas Gas Transmission and Distribution Company Limited

Vertical Income statement

2007 2008 2009 2010 2011 AVERAG

E

STANDAR

D

DEVIATIO

N

1. SALES 100.0000% 100.0000

%

100.0000% 100.0000% 100.0000% 100.0000% 0.0000%

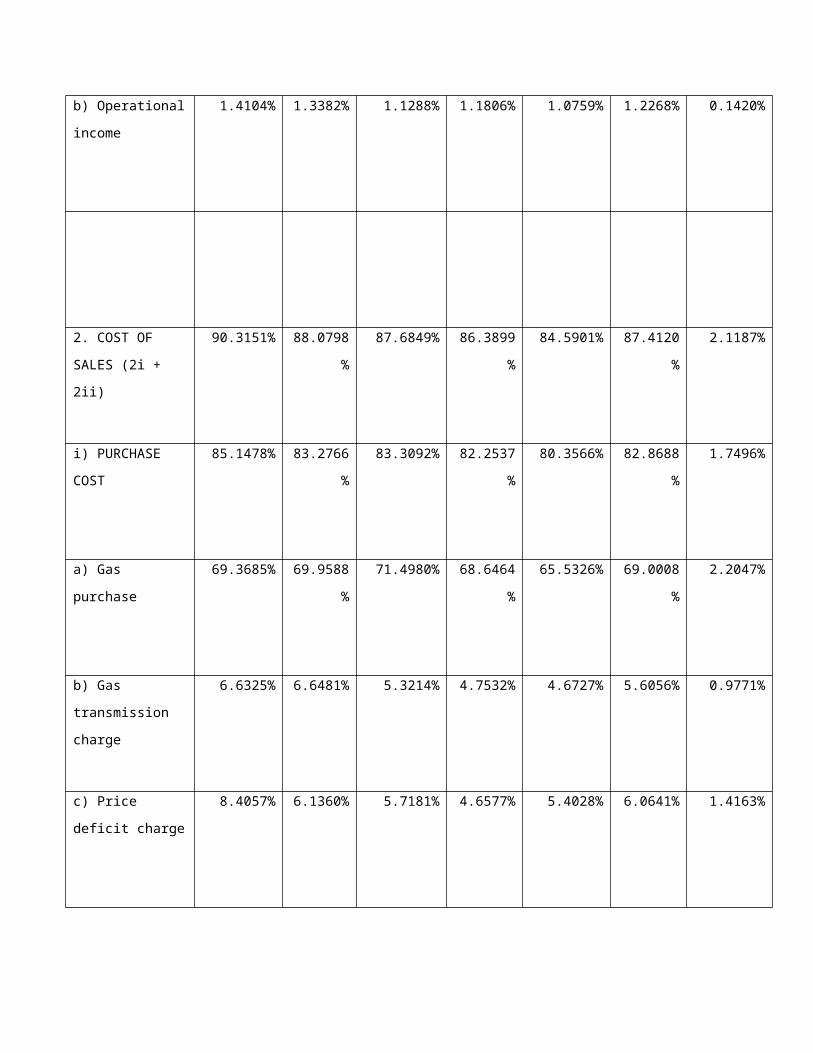

a) Gas sales revenue 98.5896% 98.6618% 98.8712% 98.8194% 98.9241% 98.7732% 0.1420%

b) Operational

income

1.4104% 1.3382% 1.1288% 1.1806% 1.0759% 1.2268% 0.1420%

2. COST OF SALES

(2i + 2ii)

90.3151% 88.0798% 87.6849% 86.3899% 84.5901% 87.4120% 2.1187%

Page 10

i) PURCHASE

COST

85.1478% 83.2766% 83.3092% 82.2537% 80.3566% 82.8688% 1.7496%

a) Gas purchase 69.3685% 69.9588% 71.4980% 68.6464% 65.5326% 69.0008% 2.2047%

b) Gas transmission

charge

6.6325% 6.6481% 5.3214% 4.7532% 4.6727% 5.6056% 0.9771%

c) Price deficit

charge

8.4057% 6.1360% 5.7181% 4.6577% 5.4028% 6.0641% 1.4163%

d) Gas development

charge

0.0000% 0.0000% 0.0000% 3.5695% 4.0319% 1.5203% 2.0881%

e) BAPEX margin 0.7412% 0.5337% 0.4062% 0.3345% 0.3784% 0.4788% 0.1643%

f) Deficit wellhead

margin for BAPEX

0.0000% 0.0000% 0.3656% 0.2924% 0.3382% 0.1992% 0.1838%

Page 11

ii)

ADMINISTRATIVE

& OTHER COST

5.1673% 4.8032% 4.3757% 4.1363% 4.2336% 4.5432% 0.4320%

a) Personnel costs 1.7536% 1.5391% 1.4251% 1.5457% 1.6623% 1.5852% 0.1261%

b) Professional

services

0.0396% 0.0355% 0.0336% 0.0200% 0.0210% 0.0300% 0.0089%

c) Promotional costs 0.0212% 0.0155% 0.0136% 0.0156% 0.0110% 0.0154% 0.0038%

d) Power costs 0.0592% 0.0438% 0.0339% 0.0339% 0.0331% 0.0408% 0.0112%

e) Communication

costs

0.0134% 0.0116% 0.0087% 0.0074% 0.0064% 0.0095% 0.0029%

f) Transport costs 0.1677% 0.1388% 0.1262% 0.1218% 0.1121% 0.1333% 0.0215%

Page 12

g) Occupancy costs 0.1049% 0.0915% 0.0766% 0.0793% 0.0964% 0.0898% 0.0118%

h) Administrative

costs

0.0765% 0.1144% 0.0833% 0.0856% 0.0964% 0.0913% 0.0148%

i) Miscellaneous

costs

0.0584% 0.0432% 0.0310% 0.0225% 0.0288% 0.0368% 0.0142%

j) Transmission &

distribution costs

0.1040% 0.0592% 0.0937% 0.0533% 0.0616% 0.0744% 0.0229%

k) Financial charges 0.0164% 0.0038% 0.0019% 0.0025% 0.0043% 0.0058% 0.0060%

l) Bad & doubtful

debts provision

0.8146% 0.8489% 0.7637% 0.6757% 0.6957% 0.7597% 0.0744%

m) Depreciation

charges

1.7658% 1.7460% 1.5360% 1.2993% 1.2295% 1.5153% 0.2474%

Page 13

n) Petrobangla

Service Charge

0.1464% 0.1119% 0.1484% 0.1737% 0.1751% 0.1511% 0.0258%

3. OPERATING

PROFIT (1-2)

9.6849% 11.9202% 12.3151% 13.6101% 15.4099% 12.5880% 2.1187%

4. NON-

OPERATIONAL

INCOME

0.6291% 0.7547% 0.6795% 0.5637% 0.8363% 0.6927% 0.1064%

5. TOTAL INCOME

(3+4)

10.3140% 12.6750% 12.9945% 14.1738% 16.2461% 13.2807% 2.1703%

6. FINANCIAL

INCOME

-0.3141% -0.6247% 1.5502% 1.8634% 2.6419% 1.0233% 1.4237%

Page 14

Interest income 0.4633% 0.3636% 1.7571% 2.0069% 2.7604% 1.4703% 1.0336%

Less: Interest cost 0.7774% 0.9882% 0.2070% 0.1435% 0.1185% 0.4469% 0.4061%

7. NET PROFIT

BEFORE

CONTRIBUTION

TO ‘WPPF’ (5+6)

10.6281% 13.2996% 14.5447% 16.0372% 18.8880% 14.6795% 3.0778%

8. WORKERS’

PARTICIPATION

IN PROFITS

0.5061% 0.6333% 0.6926% 0.7637% 0.8994% 0.6990% 0.1466%

9. NET PROFIT

BEFORE

TAXATION (7-8)

10.1220% 12.6663% 13.8521% 15.2735% 17.9886% 13.9805% 2.9312%

Page 15

10. PROVISION

FOR TAXATION

3.5115% 3.2296% 3.5437% 3.9145% 4.6008% 3.7600% 0.5293%

a) Current Tax 0.0000% 3.1349% 3.4284% 3.7802% 4.4522% 2.9591% 1.7256%

b) Deferred Tax 0.0000% 0.0947% 0.1153% 0.1343% 0.1486% 0.0986% 0.0587%

11. NET PROFIT

FOR THE YEAR

AFTER TAXATION

(9-10)

6.6104% 9.4367% 10.3084% 11.3590% 13.3878% 10.2205% 2.4991%

Here all the figures were divided by Total sales of that particular year and they were expressed as

a percentage of that year’s total sales.

Titas Gas Transmission and Distribution Company Limited

Horizontal Balance sheet

2007 2008 2009 2010 2011

1. CAPITAL

AND RESERVES

100.0000% 140.8718% 171.1765% 216.0233% 290.5956%

Page 16

a) Share capital 100.0000% 358.5342% 358.5342% 358.5342% 394.3876%

b) Deposits for

Share

100.0000% 160.9869% 252.4671% 1046.2096% 4463.0694%

c) Capital

reserves

100.0000% 100.0000% 100.0000% 100.0000% 100.0000%

d) Revenue

reserves

100.0000% 66.4922% 111.2773% 177.4872% 274.3495%

2. LONG-TERM

BORROWINGS

100.0000% 58.6429% 55.5506% 46.8364% 45.5304%

a) Unsecured

loans - local

sources

100.0000% 0.0000% 0.0000% 0.0038% 0.2017%

b) Unsecured

loans - foreign

sources

100.0000% 89.0184% 84.3244% 71.0945% 69.0095%

3. OTHER

LONG-TERM

LIABILITIES

100.0000% 122.0290% 143.0195% 152.6248% 155.1297%

a) Pension fund 100.0000% 103.9452% 103.1654% 100.1457% 92.4894%

b) Gratuity 100.0000% 113.4480% 103.0497% 159.8528% 169.7612%

c) Leave pay 100.0000% 107.4262% 111.9082% 122.5379% 130.5295%

d) General

provident fund

100.0000% 171.0220% 194.5680% 213.8010% 229.8694%

e) Customers'

security deposits

100.0000% 122.3607% 146.2797% 156.7619% 159.6373%

4. TOTAL

CAPITAL

EMPLOYED

100.0000% 116.5164% 136.4853% 159.3294% 196.8134%

Page 17

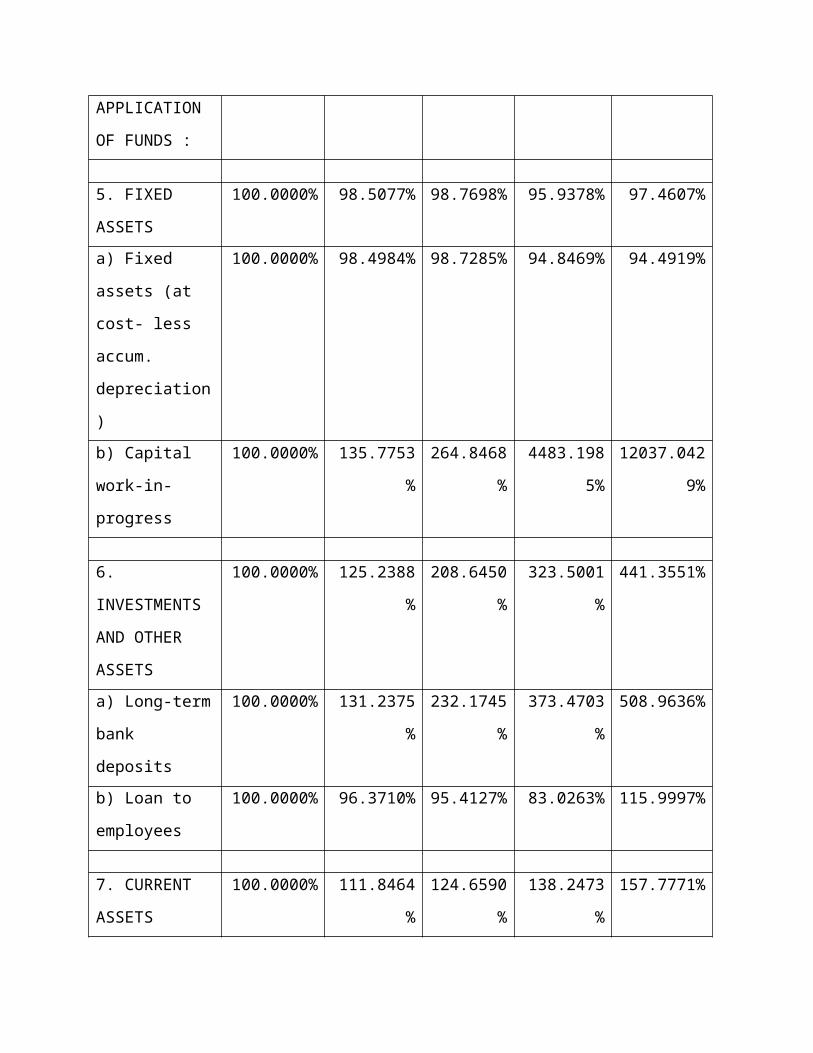

APPLICATION

OF FUNDS :

5. FIXED

ASSETS

100.0000% 98.5077% 98.7698% 95.9378% 97.4607%

a) Fixed assets (at

cost- less accum.

depreciation)

100.0000% 98.4984% 98.7285% 94.8469% 94.4919%

b) Capital work-

in-progress

100.0000% 135.7753% 264.8468% 4483.1985% 12037.0429

%

6.

INVESTMENTS

AND OTHER

ASSETS

100.0000% 125.2388% 208.6450% 323.5001% 441.3551%

a) Long-term

bank deposits

100.0000% 131.2375% 232.1745% 373.4703% 508.9636%

b) Loan to

employees

100.0000% 96.3710% 95.4127% 83.0263% 115.9997%

7. CURRENT

ASSETS

100.0000% 111.8464% 124.6590% 138.2473% 157.7771%

a) Inventories of

stores and other

materials

100.0000% 108.6893% 138.5357% 137.6009% 137.2788%

b) Advances,

deposits and

prepayments

100.0000% 416.2701% 107.8791% 133.9937% 93.7354%

c) Trade debtors

(Net)

100.0000% 102.5656% 94.3168% 102.0909% 110.3601%

Page 18

d) Cash and bank

balances

100.0000% 170.8351% 438.4349% 524.2433% 678.4314%

e) Other current

assets

100.0000% 46.6838% 274.9443% 335.7970% 517.5022%

8. CURRENT

LIABILITIES ( 8i

+ 8ii )

100.0000% 98.7673% 115.6207% 137.7432% 151.3824%

i) GROUP

COMPANY

ACCOUNTS

100.0000% 80.6066% 91.7770% 104.1381% 119.9924%

a) Payable for gas

purchase &

transmission

100.0000% 81.5994% 91.4798% 95.4742% 10.5799%

b) Payable for

PDF& BAPEX

margin

100.0000% 73.4817% 66.5868% 76.1497% 128.6854%

c) Payable for defi cit wellhead

margin fund for BAPEX

d) Payable for gas

development fund

e) Group current

accounts

100.0000% 109.9033% -

185.1467%

-259.5647% -254.7592%

ii) OTHER

LIABILITIES

100.0000% 187.3249% 231.8899% 301.6124% 304.4504%

a) Creditors and

accruals

100.0000% 270.9619% 343.8881% 455.0664% 456.9470%

b) Workers' Profi

t Participation

Fund

100.0000% 126.6744% 163.7896% 222.3195% 277.9012%

c) Current portion 100.0000% 57.9304% 54.9279% 55.2056% 44.8826%

Page 19

of long

9. NET

CURRENT

ASSETS ( 7

100.0000% 179.1613% 171.1767% 140.8421% 190.6893%

10. NET ASSETS

( 5+6+9 )

100.0000% 116.3321% 136.4853% 159.3294% 196.8134%

AVERAGE 100.0000% 127.8041% 145.5692% 299.8819% 615.5089%

STANDARD

DEVIATION

0.0000% 77.2441% 106.4167% 724.1199% 2032.1331%

Here, the figures of 2007 balance sheet were taken as the base year data and all the other figures

for other 4 years were expressed as percentage of the figures of 2007.

Titas Gas Transmission and Distribution Company Limited

Horizontal Income statement

2007 2008 2009 2010 2011

1. SALES 100.0000% 114.7410

%

135.7982% 165.7129% 175.9656%

a) Gas sales

revenue

100.0000% 114.8250

%

136.1861% 166.0991% 176.5626%

b) Operational

income

100.0000% 108.8707

%

108.6813% 138.7169% 134.2335%

2. COST OF

SALES (2i + 2ii)

100.0000% 111.9011

%

131.8434% 158.5109% 164.8113%

i) PURCHASE

COST

100.0000% 112.2195

%

132.8660% 160.0804% 166.0641%

a) Gas purchase 100.0000% 115.7175 139.9670% 163.9880% 166.2353%

Page 20

%

b) Gas transmission

charge

100.0000% 115.0113

%

108.9531% 118.7575% 123.9709%

c) Price deficit

charge

100.0000% 83.7587% 92.3794% 91.8237% 113.1020%

d) Gas development

charge

e) BAPEX margin 100.0000% 82.6221% 74.4214% 74.7865% 89.8300%

f) Deficit wellhead

margin for BAPEX

ii)

ADMINISTRATIV

E & OTHER COST

100.0000% 106.6548

%

114.9941% 132.6475% 144.1684%

a) Personnel costs 100.0000% 100.7075

%

110.3648% 146.0739% 166.8052%

b) Professional

services

100.0000% 102.7088

%

115.0358% 83.7747% 93.2909%

c) Promotional

costs

100.0000% 83.8129% 86.8999% 121.7389% 90.8989%

d) Power costs 100.0000% 84.8104% 77.8006% 94.6853% 98.2623%

e) Communication

costs

100.0000% 99.1870% 87.6410% 91.3799% 83.6163%

f) Transport costs 100.0000% 94.9911% 102.1950% 120.3268% 117.6912%

g) Occupancy costs 100.0000% 100.0746

%

99.1929% 125.2357% 161.7564%

h) Administrative

costs

100.0000% 171.6710

%

147.9413% 185.5579% 221.8503%

i) Miscellaneous

costs

100.0000% 84.9515% 72.1055% 63.9472% 86.6814%

j) Transmission &

distribution costs

100.0000% 65.2907% 122.3062% 84.8456% 104.1918%

Page 21

k) Financial charges 100.0000% 26.4307% 15.6336% 25.4553% 46.2341%

l) Bad & doubtful

debts provision

100.0000% 119.5733

%

127.3174% 137.4543% 150.2809%

m) Depreciation

charges

100.0000% 113.4586

%

118.1299% 121.9327% 122.5228%

n) Petrobangla

Service Charge

100.0000% 87.6839% 137.6357% 196.6873% 210.4414%

3. OPERATING

PROFIT (1-2)

100.0000% 141.2245

%

172.6778% 232.8751% 279.9837%

4. NON-

OPERATIONAL

INCOME

100.0000% 137.6471

%

146.6616% 148.4899% 233.9034%

5. TOTAL

INCOME (3+4)

100.0000% 141.0062

%

171.0909% 227.7278% 277.1729%

6. FINANCIAL

INCOME

100.0000% 228.2081

%

-670.2454% -983.1501% -

1480.1405

%

Interest income 100.0000% 90.0297% 514.9773% 717.7448% 1048.3014

%

Less: Interest cost 100.0000% 145.8530

%

36.1533% 30.5919% 26.8237%

7. NET PROFIT

BEFORE

CONTRIBUTION

TO ‘WPPF’ (5+6)

100.0000% 143.5832

%

185.8417% 250.0517% 312.7225%

8. WORKERS’

PARTICIPATION

IN PROFITS

100.0000% 143.5832

%

185.8417% 250.0517% 312.7225%

9. NET PROFIT 100.0000% 143.5832 185.8417% 250.0517% 312.7225%

Page 22

BEFORE

TAXATION (7-8)

%

10. PROVISION

FOR TAXATION

100.0000% 105.5275

%

137.0408% 184.7282% 230.5495%

a) Current Tax

b) Deferred Tax

11. NET PROFIT

FOR THE YEAR

AFTER

TAXATION (9-10)

100.0000% 163.7987

%

211.7652% 284.7523% 356.3735%

AVERAGE 100.0000% 113.8777

%

110.6839% 130.4038% 146.3029%

STANDARD

DEVIATION

0.0000% 34.9823% 156.7841% 225.2809% 329.7675%

Here, the figures of 2007 income statement were taken as the base year data and all the other

figures for other 4 years were expressed as percentage of the figures of 2007.

Forecasted Statements for 2010 and 2011:

Forecasted balance sheets and Income statements for 2012 and 2013 have been created through

percentage of sales method. Discretionary financing and common equity excluding retained earnings

assumed to be fixed for both two years.

Forecasted Balance Sheet:

Titas Gas Transmission Distribution Ltd

Page 23

Pro forma balance sheet (% of Sales Method)

As at 2012 & 2013

Notes:

2012 2013

Current asset 30582950474.29 35246850421.61

Fixed Asset 13356272254.46 15397164573.22

Investments 24926171208.05 28727412317.28

Total asset 68865393936.79 79371427312.11

Equity and

Liabilities

Current liabilities 24570647371.49 28317671095.63

Long term

Borrowings

2,088,802,253 2,088,802,253

Others Long term

liabilities

8,095,811,119 8,095,811,119

Total Liabilities 34755260743.49 38502284467.64

Equity

Share capital 9,421,160,300 9,421,160,300

Deposits for Share 29,272,335 29,272,335

Capital reserves 754,693,866 754,693,866

Revenue

reserve/retained

earnings

3293498371.21 3798623967.99

Total Equity 13498624872.21 14003750468.99

Total Equity and

Liabilities

48253885615.70 52506034936.63

Discretionary

Financing Needed

20611508321.09 26865392375.49

Page 24

While calculating retained earnings dividend was calculated as the percentage of the

income of the 2011 dividend paid.

Forecasted Income Statements:

Sales Growth Calculation:

Year Growth (g) Average growth

2008 14.74% 15.33%

2009 18.35%

2010 22.02%

2011 6.19%

Growth calculation from Future value formula

FV=PV*(1+g)4

Or, (1+g)4 =6855123385238957171618

Or, g= 0.1517 or 15.17%

Average sales growth:

g= 15.33+15.17

2

Or, g= 15.25%

Page 25

Titas Gas Transmission Distribution Ltd

Pro forma Income Statements (% of Sales Method)

For the year ended June 30, 2012 & 2013

Page 26

Notes:

2012 2013

Revenue 79005297014.43 91053604809.13

Cost of turnover 63485936927.77 73167542309.26

Gross Profit 15519360086.65 17886062499.86

Operating Expenses:

Operating Expenses 3341924063.71 3851567483.42

Operating profit 12177436022.94 14034495016.44

Non Operational

Income

663644494.92 764850280.39

Total Income 12841080517.86 14799345296.83

Financial Income 2099307225.6 2431840520.73

Net profit Before

Contribution to

WPPF

14940387743.46 17231185817.56

Workers Participation

In Profit

711047673.12 819482443.28

Net Profit Before

Tax(EBT)

14229340070.33345 16411703374.28531

Tax 3638442255.98 4196472552.80

Net Profit for the

Year After Tax

10590897814.34 12215230821.4

2012 2013

Revenue 79005297014.43 91053604809.13

Cost of turnover 63485936927.77 73167542309.26

Gross Profit 15519360086.65 17886062499.86

Operating Expenses:

Operating Expenses 3341924063.71 3851567483.42

Operating profit 12177436022.94 14034495016.44

Non Operational

Income

663644494.92 764850280.39

Total Income 12841080517.86 14799345296.83

Financial Income 2099307225.6 2431840520.73

Net profit Before

Contribution to

WPPF

14940387743.46 17231185817.56

Workers Participation

In Profit

711047673.12 819482443.28

Net Profit Before 14229340070.33345 16411703374.28531

Page 27

Depreciation expenses changes with changes in sales overtime

Ratio Analysis

Liquidity Ratio

Current Ratio:

Current Ratio=Current Asset

Current Liabilities

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 1.19 times 1.35 times 1.29 times 1.20 times 1.24 times 1.97 times

2007 2008 2009 2010 20111.1

1.15

1.2

1.25

1.3

1.35

1.4

1.19

1.35

1.29

1.2

1.24

Current Ratio

Current Ratio

TIMES

YEAR

Page 28

Tita

s Gas

Desco

Meg

hna

Jam

una

Padm

a

Barak

atulla

h

Power

Grid

Indust

ry A

vera

ge0

0.5

1

1.5

2

2.5

3

3.5

4

1.24

3.49

1.12 1.19 1.05

3.64

2.09 1.97

Current Ratio(2011)

Current Ratio

TIMES

Company & Industry Avg.

Analysis:

In 2011, Titas Gas Transmission & Distribution Co. Ltd’s current assets were only 1.24 times of

their current liabilities. The ratios are fluctuating through 2007 to 2011. In 2011 current ratio

slightly increased by changing the trend from downward to upward but it is less than 2008

&2009. So performance is not satisfactory. It caused due to more relative change in current asset

than current liabilities. Some of the Company like Barakatullah & Desco are doing much better

than Titas. They are above industry average whereas Titas is operating below industry Average.

So performance is really bad.

Quick/Acid Test Ratio:

Acid Test Ratio=Current Asset−Inventory

Current Liabilities

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 1.10 times 1.24 times 1.18 times 1.10 times 1.16 times 1.69 times

Page 29

2007 2008 2009 2010 20111

1.05

1.1

1.15

1.2

1.25

1.3

1.1

1.24

1.18

1.1

1.16

Acid Test Ratio

Acid Test Ratio

TIMES

YEAR

Tita

s Gas

Des

co

Meg

hna

Jam

una

Padm

a

Barak

atulla

h

Power

Grid

Indust

ry A

vera

ge0

0.5

1

1.5

2

2.5

3

3.5

4

1.16

2.78

0.8700000000000010.72000000000000

10.9

3.51

1.91.69

Acid Test Ratio(2011)

Acid Test Ratio

Company & In-dustry Avg.

TIMES

Analysis:

In 2011, Titas gas transmission and co. ltd’s Current asset excluding inventory was only 1.16

times of its current liabilities. It declined compared to 2008 and 2009. The trend is fluctuating

from year to year. It also is operating below industry average. So Performance is not favorable.

But it increased from 2010 due to more relative change in current asset excluding inventory that

current liabilities.

Net Working Capital:

Net Working Capital=Current Asset-Current Liabilities

Year 2007 2008 2009 2010 2011 Industry

Page 30

Average

Ratio 2736131661

TK

4902089610

TK

4683621210

TK

3853625688

TK

5217510630

Tk

5,072,665,231tk

2007 2008 2009 2010 2011BDT 0.00

BDT 1,000,000,000.00

BDT 2,000,000,000.00

BDT 3,000,000,000.00

BDT 4,000,000,000.00

BDT 5,000,000,000.00

BDT 6,000,000,000.00

2736131661

49020896104683621210

3853625688

5217510630

Net Working Capital

Net Working Capital

YEAR

Amount

Titas

Gas

Desco

Meg

hna

Jamuna

Padma

Barak

atulla

h

PowerGrid

Industry A

vera

geBDT 0.00

BDT 2,000,000,000.00

BDT 4,000,000,000.00

BDT 6,000,000,000.00

BDT 8,000,000,000.00

BDT 10,000,000,000.00

BDT 12,000,000,000.00

BDT 14,000,000,000.00

BDT 16,000,000,000.00

BDT

5,21

7,51

0,63

0.00

BDT

14,0

16,1

89,5

92.0

0

BDT

2,28

8,12

2,38

1.00

BDT

2,31

2,89

1,94

0.00

BDT

2,77

7,51

6,00

0.00

BDT

921,

625,

711.

00

BDT

7,97

4,80

0,36

2.00

BDT

5,07

2,66

5,23

1.00

Net Working Capital(2011)

Net Working Capital

Company & In-dustry Avg.

Amount

Analysis:

In 2011, net working capital increased but the trend is fluctuating significantly through 2007 to

2011. It is above industry average but significantly below some companies in the industry. So the

performance is not enough.

Page 31

Cash Conversion Cycle:

Cash Conversion Cycle = Days in Inventory + Days Sales Outstanding –Average Payment Period

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 27 days 45 Days 24 days 23 days 18 days 217.67days

2007 2008 2009 2010 20110

5

10

15

20

25

30

35

40

45

50

27

45

24 23

18

Cash Conversion Cycle

Cash Conversion Cycle

YEAR

DAYS

Tita

s Gas

Des

co

Meg

hna

Jam

una

Padm

a

Barak

atulla

h

Power

Grid

Indust

ry A

vera

ge

-1200

-1000

-800

-600

-400

-200

0

200

400

18

160

-1049

-0.44

82 75141

218

Cash Conversion Cycle(2011)

Cash Conversion Cycle

Company & Industry Avg

Days

Analysis:

On an average, In 2011 it takes 18 day to covert Titas gas distribution &transmission co. Ltd’s

invested Capital into cash.

Insight Gain:

Page 32

The company’s liquidity ratios are indicating that the company is not doing well in this section.

Their performance is not stable through the years. In some cases its performance is below

industry average whereas some company is doing above industry average. So management need

to find out the problem and should take necessary initiatives. Otherwise the company will not be

able to compete in the industry.

Asset Management Ratios

Inventory turnover:

Inventory turnover=Cost of Goods Sold

Inve ntory

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 25.08 times 25.90 times 24.06 times 29.19 times 31.95 times 10.01times

2007 2008 2008 2009 2010 20110

5

10

15

20

25

30

35

25.08 25.9

31.95

24.06

29.1931.95

Inventory turnover

Inventory turnover

Page 33

Tita

s

Jam

una

Padm

a

Meg

hna

Desco

Barka

tulla

h

Power

Grid

Indust

ry A

vera

ge0

5

10

15

20

25

30

35 31.95

13.4311.85

0.391000000000001

2.18

8.5

3.42

10.01

Inventory turnover

Inventory turnover

Analysis:

In 2011, the company has sold out and restored its inventory 31.95 times. Performance inclined

compared to 2009 and it’s far above industry average which shows a superior position in the

industry. However, inventory turnover ratio increased as relative change in COGS was higher

than the relative change in inventory.

Days in Inventory:

Days in Inventory=365

Inventory

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 15days 14.09days 15 days 13 days 11.42 days 188.54days

Page 34

2007 2008 2009 2010 20110

2

4

6

8

10

12

14

1615

14.0915

13

11.42

Days in invetory

Days in invetory

Titas

Jam

una

Padm

a

Meg

hna

Desco

Barka

tulla

h

Power G

rid

Industr

y Ave

rage

0100200300400500600700800900

1000

11.42 27.23 31

933.5

167.43

43106.72

188.54

Days Inventory

Days Inventory

Analysis:

It means the inventory of Titas Gas Transmission Co. Ltd on average stays in the inventory for

11.4 days before it sold out.

Total Asset turnover ratio:

TATO=Sales

Total Assets

Year 2007 2008 2009 2010 2011 Industry

Average

Page 35

Ratio 1.16 times 1.20 times 1.23 times 1.28 times 1.15 times 1.29 times

2007 2008 2009 2010 20111.05

1.1

1.15

1.2

1.25

1.3

1.16

1.2

1.23

1.28

1.15

TATO

TATO

Titas Jamuna Padma Meghna Desco Barkatullah Power Grid Industry Average

0

1

2

3

4

5

6

4.3

5.21

1.86

4.5

0.42 0.24 0.08

1.29

TATO

TATO

Analysis:

In 2011 every 1 TK worth of asset generated 1.15 TK worth of sales. Performance declined

compared to 2010 and the performance was unfavorable as it was below industry average.

However, the decline in the performance was caused by the higher relative change in total asset

than the relative change in sales.

Page 36

Fixed Asset turnover ratio:

FATO=Sales

¿ Assets

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 3.28 times 3.76 times 4.51 times 5.66 times 5.92times 39.33times

2007 2008 2009 20110

1

2

3

4

5

6

3.283.76

4.51

5.66

FATO

FATO

Titas

Jam

una

Padm

a

Meg

hna

Desco

Barka

tulla

h

Power G

rid

Industr

y Ave

rage

0

50

100

150

200

250

300

5.92 15.76

245.3

6.57 1.27 0.41 0.11

39.33

FATO

FATO

Analysis:

Page 37

In 2011 every 1 TK worth of fixed asset generated 1.15 TK worth of sales. Performance inclined

compared to 2010 but the performance was unfavorable as it was below industry average.

However, the incline in the performance was caused by the higher relative change in sales than

the relative change in fixed assets.

Days Sales Outstanding:

DSO =Account Receivables

Sales×365

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 130 day 117 days 90 day 80 days 81.22 days 219 days

2007 2008 2009 2010 20110

20

40

60

80

100

120

140130

117

9080 81.22

DSO

DSO

Page 38

Titas

Jam

una

Padm

a

Meg

hna

Desco

Barka

tulla

h

Power G

rid

Industr

y Ave

rage0

200

400

600

800

1000

1200

1400

81.222.01 55

1167

80.27 67 81219

DSO

DSO

Analysis:

In 2011, Titas took on an average 81.22 days to collect account receivables from the customers.

Days Payable Outstanding:

DSO =Account PayablesPurchase/COGS

×365

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 118 days 86 days 81 days 70 days 74.99 490 days

Page 39

2007 2008 2009 2010 20110

20

40

60

80

100

120

140

118

8681

7074.99

DPO

DPO

Titas

Jamuna

Padma

Meghna

Desco

Barkatu

llah

Power Grid

Industry A

verag

e0

500

1000

1500

2000

2500

3000

3500

74.99 29.68 4

3150

87.21 35 47

490

DPO

DPO

Analysis:

In 2011, Titas took on an average 74.99 days to make payment to its suppliers.

Comparing with DSO of 2011 Titas was in unfavorable position since it takes 81.22 days to

collect A/R from customers and 74.99 days to make payment to suppliers.

Insight Gained from Asset Management Ratio:

Page 40

Analyzing all the ratios it can be clear that the company has inefficiency in collecting A/R from

the customer which can create liquidity problem in future for the company. Moreover, it has

inefficiency in utilizing assets to generate higher sales revealing the company’s weakness in

asset management.

Debt Management Ratio:

Debt Ratio:

Debt Ratio =Total DebtTotal Asset

×100

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 29.18% 62.64% 61.24% 58.43% 52.72% 62.71%

2007 2008 2009 2010 20110.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

29.18%

62.64% 61.24%58.43%

52.72%

Debt Ratio

Debt Ratio

YEAR

Page 41

Tita

s Gas

Desco

Meg

hna

Jam

una

Padm

a

Barak

atulla

h

Power

Grid

Indust

ry A

vera

ge0.00%10.00%20.00%30.00%40.00%50.00%60.00%70.00%80.00%90.00%

100.00%

52.72%

9.40%

90.72%82.22%

94.00%

36.46%

73.45%62.71%

Debt Ratio(2011)

Debt Ratio

Company & Industry Avg

Analysis:

In 2011, the company’s 52.72% of the total assets were purchased by debt which means for

every 1 TK of total asset nearly .53 TK financed by debt. It is declining from 2008 which is very

favorable for the company because lower the debt ratio, the higher the cushion against creditor’s

losses in the event of bankruptcy.

From Capital Structure Point of View

Titas gas transmission & distribution company ltd’s capital structure consists of 52.72% debt and

rest is equity.

Times Interest Earned:

Times Interest Earned =EarningsBefore Interest∧Tax

Interest Expense

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 20.90 times 34.86 times 71.27 times 112.74 times 130.03 times 32.02times

Page 42

2007 2008 2009 2010 20110

20

40

60

80

100

120

140

20.9

34.86

71.27

112.74

130.03

Times Interest Earned

Times Interest Earned

TIMES

YEAR

Tita

s Gas

Des

co

Meg

hna

Jam

una

Padm

a

Barak

atulla

h

Power

Grid

Indust

ry A

vera

ge0

20

40

60

80

100

120

140 130.03

7.220

2.38 0.5293

32.02

Times Interest Earned(2011)

Times Interest Earned

Company & Industry Avg.

TIMES

Analysis:

In 2011, Titas gas distribution & company ltd’s Earnings before interest and tax is 130.03 times

higher than its interest expense and it is increasing through the year. The company is much

higher than industry average. So the company is in a good shape.

Insight Gain:

The company is doing well in the debt management in the company. The times interest earned is

increasing which is an indication that company using less amount of debt in its operation.

Profitability Ratio

Gross Profit Margin:

Page 43

Gross Profit Margin=Gross Profit

Sales×100 %

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 14.85% 16.95% 16.69% 17.75% 19.64% 22.33%

2007 2008 2009 2010 20110.00%

5.00%

10.00%

15.00%

20.00%

25.00%

14.85%

16.95% 16.69%17.75%

19.64%

Gross Profit Margin

Gross Profit Margin

Padma

Jamuna

Meg

hnaTit

as

Power G

rid

Desco

Barka

tulla

h

Industry A

vera

ge0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

1.46% 1.24%

35.19%

19.64%

26.86%22.75%

49.18%

22.33%

Gross Profit Margin

Gross Profit Margin

Analysis:

In 2011, for every 100 Tk sales Titas Gas Transmission Co. Ltd generated 19.64 Tk gross profit.

Performance inclined compared to 2009 and it’s certainly below industry average which shows

Page 44

an unfavorable position in the industry. However, gross profit margin increased as relative

change in gross profit was higher than the relative change in sales.

Operating Profit Margin:

Operating Profit Margin=OperatingProfit

Sales×100 %

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 9.68% 12.08% 12.32% 16.18% 15.41% 15.38%

2007 2008 2009 2010 20110.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

9.68%

12.08% 12.32%

16.18%15.41%

Operating Profit Margin

Operating Profit Margin

Page 45

Titas

Jamuna

Padma

Meghna

Desco

Barkatu

llah

Power Grid

Industry A

verag

e0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

15.41%

0.78% 1.19%

19.74%

16.28%

12.32%13.59%

15.41%

Operating Profit Margin

Operating Profit Margin

Analysis:

In 2011, for every 100 Tk sales Titas Gas Transmission Co. Ltd produced 14.41 Tk operating

profit. Performance declined compared to 2009 and it’s just above industry average which shows

a favorable performance in the industry. However, operating profit margin declined because

relative change in sales was higher than the relative change in operating profit.

Net Profit Margin:

Net Profit Margin=Net Profit after tax

Sales×100 %

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 6.61% 9.56% 10.31% 11.36% 13.39% 13.81%

Page 46

2007 2008 2009 2010 20110.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

6.61%

9.56%10.31%

11.36%

13.39%

Net Profit Margin

Net Profit Margin

Titas

Jamuna

Padma

Meg

hna

Desco

Barka

tulla

h

Power G

rid

Industry A

vera

ge0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

9.68%

1.30% 0.85%

30.93%

12.02%

21.40%

14.78% 13.81%

Net Profit Margin

Net Profit Margin

Analysis:

In 2011, Titas Gas Transmission Co. Ltd generated 13.39 Tk net profit for every 100 Tk of sales.

Performance inclined compared to 2010 whereas ratio was just below industry average showing

slightly unfavorable performance in the industry. However, the incline in the ratio compared to

2010 was caused due to higher relative change in net profit compared to relative change in sales

Return on Asset:

Return on Asset=Net Profit after tax

Total Asset×100 %

Year 2007 2008 2009 2010 2011 Industry

Page 47

Average

Ratio 7.66% 11.50% 12.70% 14.53% 15.36% 5.59%

2007 2008 2009 2010 20110.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

7.66%

11.50%12.70%

14.53%15.36%

Retrun on Asset

Retrun on Asset

Titas

Jamuna

Padma

Meg

hnaDes

co

Powergr

id

Barka

tulla

h

Industry A

vera

ge0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%15.36%

6.78%

1.58%

4.05%5.04%

14.78%

5.12% 5.59%

Return on Asset

Return on Asset

Analysis:

In 2011, Titas Gas Transmission Co. Ltd generated 15.36 Tk net profits from every 100 Tk

worth of total assets. The ratio inclined from 2010 and it was far above industry average

presenting its superior performance in the industry. However, the incline in the ratio in 2011 was

caused by a higher relative change in net profit than the relative change in total assets.

Page 48

Operating Return on Asset:

Operating Return on Asset=OperatingProfitTotal Asset

×100 %

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 11.23% 14.53% 12.32% 20.68% 17.68% 6.38%

2007 2008 2009 2010 20110.00%

5.00%

10.00%

15.00%

20.00%

25.00%

11.23%

14.53%

12.32%

20.68%

17.68%

Operating return on asset

Operating return on asset

Titas

Jamuna

Padma

Meghna

Desco

Powergrid

Barkatu

llah

Industry A

verag

e0.00%2.00%4.00%6.00%8.00%

10.00%12.00%14.00%16.00%18.00%20.00%

17.68%

4.05%2.22% 2.58%

6.82%

1.14%

10.23%

6.38%

Operating Return on Asset

Operating Return on Asset

Analysis:

Page 49

In 2011, Titas Gas Transmission Co. Ltd generated 17.68 Tk operating profit from every 100 Tk

worth of total assets. The ratio declined from 2010 but it was far above industry average

presenting its better performance in the industry. However, the decrease in the ratio in 2011 was

caused by a higher relative change in total assets than the relative change in operating profit.

Return on Equity

Return on Equity=Net Profit after taxTotalCommonEquity

×100 %

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio 26.49% 30.8% 32.78% 34.92.% 32.49% 26.11%

2007 2008 2009 2010 20110.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

26.49%

30.80%32.78%

34.92%32.49%

Return on Equity

Return on Equity

Page 50

Titas

Jam

una

Padm

a

Meg

hna

Desco

Powergr

id

Barka

tulla

h

Industr

y Ave

rage

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

32.49%

38.14%

26.65%

40.46%

14.90%

22.07%

8.06%

26.11%

Return on Equity

Return on Equity

Analysis:

In 2011, common share holders of the Titas Gas Transmission Co. Ltd earned 32.49 Tk for every

100 Tk invested in the company. The performance declined compared to 2010 but the

performance was far better than industry average showing a good position in the industry.

However, the decline in the performance in 2011 was caused by higher relative change in total

common equity than relative change in net income.

Insight Gained from the profitability ratio:

Analyzing the entire profitability ratio it is apparent that company is doing better in most of the

cases. However, it has not done well in the gross profit section reflecting its inefficiency in

controlling cost of goods sold which is reducing the gross profit in turn reducing the ratio.

Market Ratio:

Earnings per Share:

Earning per Share=

Net incomeav ailable ¿CommonShareholders ¿Total number of commonshare outstanding

Page 51

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio N/A TK 49.25/

share

Tk 63.67/

share

TK

85.62/share

TK 97.41/

share

TK 37.11/

share

2008 2009 2010 20110

20

40

60

80

100

120

49.25

65.67

85.62

97.41

EPS

EPS

Jam

una

Padm

a

Meg

hna

Desco

Power

grid

Tita

s

Barka

tulla

h

Indust

ry A

vera

ge0

20

40

60

80

100

120

4.3

29.8218.39

70.99

22.07

97.41

2.32

37.11

EPS

EPS

Analysis:

In 2011, the common share holder earns TK 97.41/ Share. EPS increased compared to 2010 and

it was far above industry average. However, the increase in EPS was caused by increase in net

income from 2010 to 2011.

Page 52

Market to Book Value Ratio (M/B):

M/B Ratio=Market Value

Book Value per share

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio N/A 3.12 times 3.53 Times 0.89times 0.23times 2.57 times

2008 2009 2010 20110

0.5

1

1.5

2

2.5

3

3.5

4

3.12

3.53

0.89

0.23

M/B Ratio

M/B Ratio

Titas Jamuna Meghna Padma Desco Power Grid

Barkatulla Industry average

0

1

2

3

4

5

6

7

8

0.23

3.644.13

7.4

0.2380.68

1.65

2.57

M/B ratio

M/B ratio

Analysis:

In 2011, the Market value of Titas share was .23 times higher than the book value per share. The

ratio declined compared to 2010 and it was far below industry average showing a serious

Page 53

unfavorable position in the industry. However, the ratio declined as relative change in book value

per share was higher than the relative change in market value.

Price Earnings ratio:

Price Earnings ratio=Market Price

EPS

Year 2007 2008 2009 2010 2011 Industry

Average

Ratio N/A 10.13 10.78 11.67 0.69 10.49

2008 2009 2010 20110

2

4

6

8

10

12

14

10.1310.78

11.67

0.690000000000001

P/E Ratio

P/E Ratio

Tita

s

Barka

tulla

h

Jam

una

Padm

a

Meg

hna

Desco

Power

Grid

Indust

ry a

vera

ge0

5

10

15

20

25

30

0.690000000000001

20.52

9.54

27.77

10.21

1.593.12

10.49

P/E ratio

P/E ratio

Page 54

Analysis:

In 2011, the common share holders of Titas were willing to pay .69 TK for every dollar of

reported earnings. The ratio is very low compared to industry average showing the share price is

highly undervalued. It also implies that it will create lack of confidence among the common

share holder on the company.

Insight gained from Market ratios:

Analyzing entire market ratios, it is apparent that in 2011 in DSE the price of share was

undervalued which is actually reflected by the P/E ratio. Although earning per share was

significantly high, investors were having lack of confidence to invest on it. It may be caused due

to the severe market fall in 2011 which caused the market price to fall significantly.

Risk and Return Analysis

Here,

Standard Deviation = √∑ (ki−k )2

n−1 * 100

Coefficient of variation=Standard DeviationRateof return

Average Return Standard

Deviation

Coefficient of

Variation

Titas Gas Co Ltd 2.37% 12.84% 5.42

DSE General

Index

0.89% 10.21% 11.47

Page 55

Analysis:

From the table, it is clear that Titas has a high rate of return and risk compared to market (DSE

general index). As we know, coefficient of variation measures the risk involved in per unit of

return, from the table it is apparent that Titas has low risk per unit of return compared to DSE

general index.

Market Return Analysis

Beta calculation:

-40.00% -20.00% 0.00% 20.00% 40.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

f(x) = 0.849430795667443 x + 0.0161013677374449

Chart Title

TitasLinear (Titas)Linear (Titas)

Titas monthly Return

DSE General Index

Average Return Standard

Deviation

Coefficient of

Variation

Titas Gas Co Ltd 2.37% 12.84% 5.42

DSE General

Index

0.89% 10.21% 11.47

Page 56

Notes: Beta has been calculated by the monthly return from July, 2008 to July, 2012 as the

company was enlisted in DSE since July, 2012.

Analysis:

So the beta for the company is 0.8494 found by the scattered diagram and the regression analysis

which shows that the company’s volatility to the market returns. It means 1% change in the

market return will lead to .85% change in the company’s return.

Risk Free Rate (RF:

Reason to choose the rate of monthly T-Bill as the Risk Free Rate (RF):

From Bangladesh Bank website risk free rate of 9.05% has been chosen, which is the rate of

monthly T-bill is. It is chosen monthly as all the data used to calculate beta are in monthly basis.

Moreover, to calculate the average market return (RM) rate of return, DSE general index are used

which are also monthly. So, to match the period while calculating required rate of return (RK)

through CAPM, monthly risk free rate has been chosen.

Monthly Required Rate of Return (RE) Using CAPM:

Here,

Monthly Average Market Return= 0.89%

Risk Free return= 9.05%

β = 0.85

CAPM:

β=.85

RF= 9.05%

RE = RF+ β×(RM-RF)

RE=9.05%+.85(.89%-9.05%)

RE=2.11%

Annual Required Rate of Return (RE)= 25.37%

Page 57

Interest and other Cost of financing of debt:

Cost of debt is the calculated from the 2011 interest expense divided by long term loan of

2011and tax rate is calculated is divided by the tax paid in 2011 by the corresponding EBT.

Moreover, cost of equity/ retained earnings is the company’s annual required rate of return.

WD (weight of

debt)

KD (Cost of

debt)

Tax rate WE( Weight of

Common

equity)

WRE( Weight

of Retained

Earnings)

KE /KR ( Cost

of Common

equity/retained

earnings)

26.50% 3.89 % 25.57 % 26.55 % 46.95 % 25.37%

Weighted Average Cost of Capital:

WD*KD

(1-T)

WE*KE WRE*KRE WACC

7.67% 6.74% 11.91% 26.32%

Analysis:

WACC is a calculation of a firm's cost of capital in which each category of capital is

proportionately weighted. All capital sources - common stock, preferred stock, bonds and any

other long-term debt - are included in a WACC calculation. So, it is apparent from the table that

Titas has to spend proportionately 7.67% as the cost of debt, 6.74% as the cost of equity and

11.91% as the cost of retained earnings generating a total cost of capital of 26.32%.

Page 58

Optimal Capital Structure

Note: Weight combination of different categories of capital is arbitrary assumed

Analysis:

As we can see from the table, the optimal structure of the firm is the combination-5 which

consist of 66.95% retained earnings, 26.55% common equity and 6.50% generating highest value

of 30712975867.19 for the firm.

Dividend Policy

There are three views of dividend policy that a company can follow.

1st View: “Dividend Policy is absolutely irrelevant”

combinat

ion

Capital Debt WACC Value of the firm

Retained

Earnings

Common

Equity

1 46.95% 26.55% 26.50% 26.32% 29872803275.08

2 36.95% 16.55% 36.50% 26.68% 29469721971.51

3 26.95% 6.55% 46.50% 26.75% 29392604942.06

4 56.95% 36.55% 16.50% 26.96% 30287064029.28

5 66.95% 26.55% 6.50% 26.60% 30712975867.19

Page 59

This view says that there is no relationship between dividend policy and stock value. The logic

behind this is (total return=Capital gain yield + Dividend yield) that investor do not care whether

return come from capital gain yield or dividend yield. What they care is the total rate of return.

This view assumes perfect capital market exist.

2nd View: “Dividend is absolutely relevant”

This view says high dividend increases the share price because t believes that dividend income

has a higher value to the investor than do capital gains income. Logic for this is that dividends

are more certain than capital gains. There is no assumption in this view.

3rd View: “Low Dividend increases the Share Price”

This view says people always try to maximize after tax income. Investors always try to defer

taxes whenever possible. In case of dividend income taxes are paid when the dividend is

received, whereas capital gains are deferred until the stock is actually sold. So investors want

low dividend and high retention of firm’s earnings to increase the share price.

Titas Gas Transmission & Distribution Company ltd follows the 2nd view that is High

Dividend Increases the share price.

Justification:

As we see the historical dividend payment of Titas gas transmission and distribution company ltd

from 2008 to 2011, we see that it is increasing. So we can say that they are actually following 2nd

view. The reason behind this is that people are always concern about their certain income. In the

view of people dividend is a certain income whereas they are uncertain about the income from

the capital gain. The reason behind their belief is dividends can be predictable compared to

capital gain as management can control dividend but it cannot dictate the price of stock.

Keeping all this in mind the company decided to follow the view of Dividend is totally relevant.

Payment plans regarding dividend:

Page 60

Titas gas limited has been paying cash dividend to its shareholders since it started giving

dividends. The dividend per share paid to the shareholders in 2008, 2009, 2010, 2011 has been

9.38, 15.52, 26.98, and 24.80 taka respectively.

They have maintained a stable trend of increase in dividends in small amounts from 2008 to

2010. Only in 2011 there has been a slight decrease in dividend. Apart from this year, our

forecasted dividend for 2012, 2013 and 2014 has been 33.29, 44.94 and 47.19 taka respectively

which show small but upward increments in dividends.

So, we can conclude that Titas gas limited follows ‘stable dollar dividend payment’ plan in

paying dividends to its shareholders.

Conclusion

The financial position and performance of the company was overall good. The company should

try to improve the performance in certain areas especially in the asset management area to use of

the company’s full capability. Moreover, the company should use debt properly as a source of

fund rather than mostly depend on high cost sources like common holders equity and retained

earnings.

However, the market position of the firm was volatile as the price at the December end 2011 was

very low. P/E ratio indicates the undervaluation of the share price as well as the intrinsic price

determined in the report also proves the same. To improve the situation company should come

forward with new techniques and better understanding of the market.

![GAS SUPPLY AGREEMENT - bpdb.gov.bd · [insert month and year], in Dhaka, Bangladesh BY AND BETWEEN Titas Gas Transmission and Distribution Company Ltd . , with its registered office](https://static.documents.pub/doc/80x56/5dd11e2ad6be591ccb644e9d/gas-supply-agreement-bpdbgovbd-insert-month-and-year-in-dhaka-bangladesh.jpg)