24

Financial Controls Task Force Report Joint Financial-HRMS Unit Liaison Meeting March 17, 2004 Mike Kalasinski Norel Tullier Cheryl Soper

| Date post: | 20-Dec-2015 |

| Category: |

Documents |

| View: | 215 times |

| Download: | 1 times |

Financial Controls Task Force Report

Joint Financial-HRMS Unit Liaison MeetingMarch 17, 2004

Mike KalasinskiNorel TullierCheryl Soper

Today we are going to cover:

•Brief background of Financial Controls Task Force

•Update on work completed to date and in process

•Review the Fiscal Responsibilities SPG

•Review the Payroll SPG

•Management Reporting and Control Tools

•Questions

1

Financial Controls Task Force Members

Medical School Financial Operations

William R. Elger, Chair Cheryl Soper

Carmen Jones, Staff Fred Caryl

Internal Audit School of Public Health

Robert Moenart Mike Kalasinski

Jim Ollar

MAIS LS&A

Debbie Mero Peggy Norgren

Purchasing

Phil Abruzzi 2

Background of the Task Force

The Financial Controls Task Force was established by the University Executive Vice President and CFO in 1999, as a result of comments made by the independent financial auditors.

3

Charge to the Task Force

• Review general policy and financial sections of the University SPG’s (500 and 600 series)

• Understand current financial processes

• Develop recommendations to have a consistent framework for making improvements in:

–Internal accounting controls –Business practices and efficiencies 4

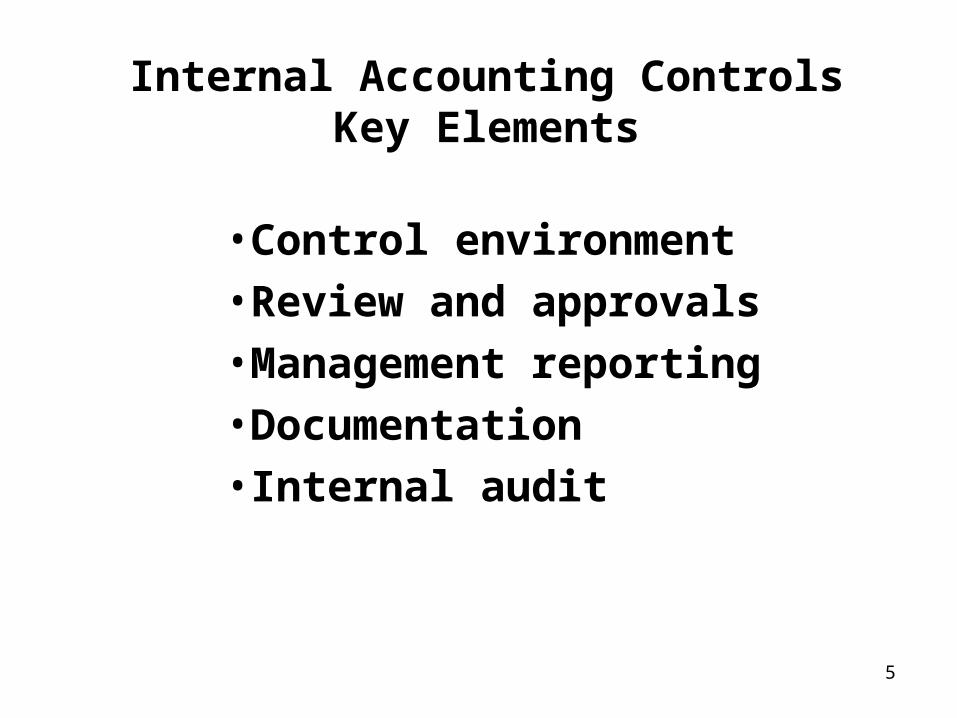

Internal Accounting ControlsKey Elements

•Control environment

•Review and approvals

•Management reporting

•Documentation

•Internal audit

5

6

An optimal control environment calls forclearly defined roles and responsibilities,policies based on principles rather thanprocedures, and a minimal number ofexceptions to those policies.

7

Review and approvals provide controls byutilizing clear definitions of what theapprovals mean, and also by establishingmateriality levels for consistent andmeaningful approvals.

8

The use of management reporting as a controlmethod reduces emphasis on individualtransactions and allows management tomonitor trends.

9

Appropriate documentation standards willassure compliance with various internal andoutside oversight agencies’ requirements andalso eliminate nonessential documentation.

10

The role of Internal Audit will be to focus on high risk or high exposure areas, and throughthe use of internal control self-assessment programs and horizontal audits, help units toimplement best practices in establishing unitcontrol policies and procedures.

Status Report

Total SPG’s identified for review – 56

Have completed and sent forward – 35

In process of completing review – 21

11

Fiscal Responsibilities

12

Fiscal Responsibilities SPG

• The old SPG was titled “Fiscal Responsibilities of a Project Director” and was highly procedural.

e.g., the projector director initiates a purchasing requisition; purchasing determines the vendor and places the order…

• The old SPG stated “…the responsibility for many of the fiscal controls rests principally with the account project directors.”

13

Fiscal Responsibilities SPG

• The new SPG is titled “Fiscal Responsibilities” and the major changes are:

–Scope is broadened so the policy clearly applies to all faculty and staff

–Emphasize that people in executive management positions are responsible for the fiscal integrity of

their units and must provide leadership

–Guidance is provided within the policy to help units think through and implement financial controls

–Tools are provided to help units assess internal controls 14

Fiscal Responsibilities SPG

• Essential Department Level Requirements

–Preparation of a Budget Plan• e.g., including anticipated revenues & expenses

–Processing of Financial Transactions• e.g., management & compliance review

–Financial Review• e.g., budget variance reporting

–Internal Controls and Management Responsibilities

• e.g., preventive & detective internal controls

15

Fiscal Responsibilities SPG

• Oversight Responsibilities and Individual Roles

– Executive Management• role must provide leadership, oversight and management philosophy

– Financial Management• role must include oversight on how funds are spent and managed, internal controls are in place, etc.

– Faculty and Staff with Delegated Financial Authority

• role for individuals (including faculty who are a PI) must include oversight, assuring adequate separation of duties exists, etc. 16

Payroll

Payroll SPGMajor Points of Change

•The old SPG dealt soley with the payment of temporary employees.

•The revised SPG was expanded to cover all payments to faculty, staff, and independent consultants.

Payroll SPGMajor Points of Change

•Section added summarizing payroll approval procedures for non-exempt and exempt staff.

•Section added emphasizing department responsibility for implementing and maintaining effective internal controls.

•Section added providing guidelines for departments that utilize electronic time data interface and specific department time documents that are not retained centrally.

Management Reporting and Control Tools

17

Tools to Strengthen Fiscal Controls

- Management Reports Matrix

- List of available reports

- Who should be using them

- Frequency the reports should be used

The staff of MAIS is meeting with the Schools and Colleges Budget Administrators to provide support in the use of the reports using their data and sharing best practices.

18

Tools to Strengthen Fiscal Controls (continued)

• Internal Control Guide and Questionnaire - Provides a framework for developing department/unit control systems, consistent with the mission of the University and the department/unit operations

- Aids with the department/unit identifying common internal control weaknesses

• Other Tools and Guidance

19

Questions…

20