Financial Derivatives Section 3 Introduction to Option Pricing Michail Anthropelos [email protected]http://web.xrh.unipi.gr/faculty/anthropelos/ University of Piraeus Spring 2018 M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 1 / 49

http://web.xrh.unipi.gr/faculty/anthropelos/University of Piraeus

Spring 2018

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 1 / 49

Outline

1 Factors that Affect Option Prices

2 Arbitrage BoundsNo dividend caseThe effect of dividend

3 More Strategies with Options and further Arbitrage Bounds

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 2 / 49

Outline

1 Factors that Affect Option Prices

2 Arbitrage BoundsNo dividend caseThe effect of dividend

3 More Strategies with Options and further Arbitrage Bounds

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 3 / 49

Pricing and Assumptions

The option pricing

The question is simple:

How should the price of an option be determined?

The pricing of options is a very important and challenging problem in finance.

Assumptions

Throughout the following sections, we are going to impose the following standardassumptions:

1 There is no arbitrage opportunity in the market.

2 There are no transaction costs.

3 Borrowing and lending at the same risk-free interest rate is possible.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 4 / 49

Main Factors that Affect Option Pricing

Option pricing... first steps

We should first ask: Which are the main factors that affect the option prices?

Main factorsB Price of the underlying asset.

B Strike price.

B Risk-free interest rate.

B Volatility of the underlying asset price.

B Dividend paid by the underlying asset until maturity.

B Time to maturity.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 5 / 49

Notation

S(t): Spot price at time t.K : Strike price.

T − t: Time to maturity.r : Risk-free interest rate (continuously compounded).

D(t): Present value (at time t) of dividend given bythe underlying asset until maturity T .

q: Dividend yield given by the underlying asset until maturity.c(t): Price of the European call option at time t.p(t): Price of the European put option at time t.C (t): Price of the American call option at time t.P(t): Price of the American put option at time t.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 6 / 49

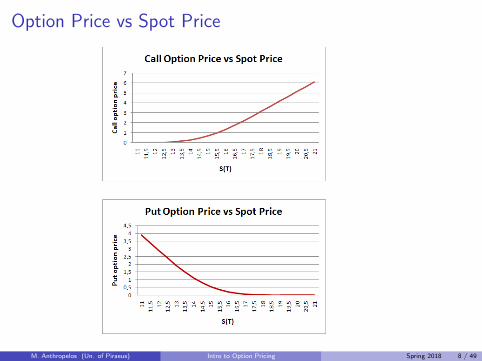

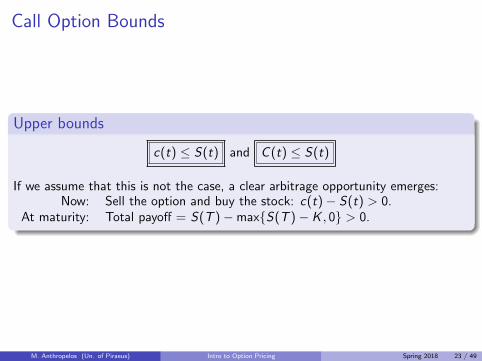

Option Price vs Spot Price

Intrinsic value of a call option = max{S(t)− K , 0}.Call options become more valuable as the spot price increases.

Call options become less valuable as the strike price increases.

Intrinsic value of a put option = max{K − S(t), 0}.Put options become less valuable as the spot price increases.

Put options become more valuable as the strike price increases.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 7 / 49

Option Price vs Spot Price

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 8 / 49

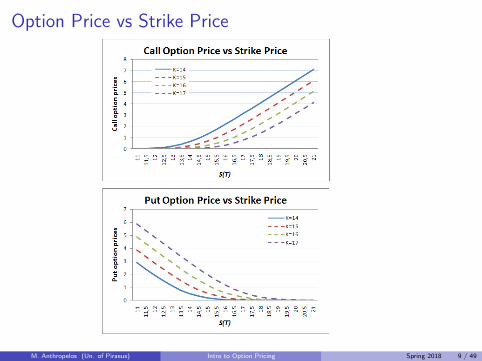

Option Price vs Strike Price

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 9 / 49

Option Price vs Risk-free Interest Rate

As the risk-free interest rate increases, the present value of the strike pricedecreases. Normally,

I The buyer of the call option is going to pay this amount.I The buyer of the put option is going to receive this amount.

Hence, an increase in interest rates (ceteris paribus) means:

Increase of the call option prices.

Decrease of the put option prices.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 10 / 49

Option Price vs Risk-free Interest Rate

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 11 / 49

Option Price vs Volatility

What is volatility?

The volatility, usually denoted by σ, is defined so that σ√

∆t is the standarddeviation of the return of the underlying asset price in a short length of time

√∆t.

Facts about volatility

Volatility is a measure of the uncertainty (riskness) on the future prices of theunderlying asset.

As volatility increases, the chances that the stock price will movesubstantially (upwards or downwards) increases.

The volatility of the price of the underlying asset is its most... interestingfeature.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 12 / 49

Option Price vs Volatility, cont’d

Volatility and option prices

As the volatility increases:

the owner of the call benefits when price of the underlying increases, but haslimited downside risk when the price of the underlying decreases,

similarly, the owner of the put benefits when price of the underlying decreases,but has limited downside risk when the price of the underlying increases.

⇓

As volatility increases both call and put price increase.

This effect is more intense for ATM options. (why?)

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 13 / 49

Option Price vs Volatility

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 14 / 49

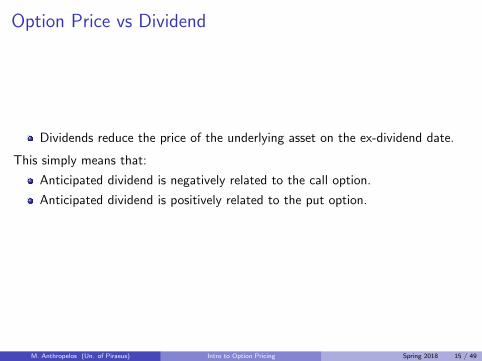

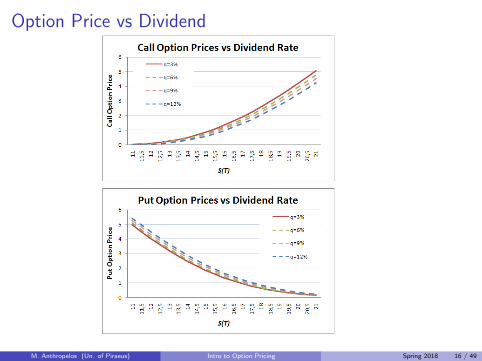

Option Price vs Dividend

Dividends reduce the price of the underlying asset on the ex-dividend date.

This simply means that:

Anticipated dividend is negatively related to the call option.

Anticipated dividend is positively related to the put option.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 15 / 49

Option Price vs Dividend

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 16 / 49

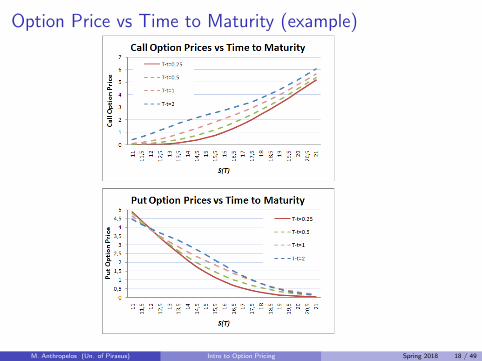

Option Price vs Time to Maturity

Three simultaneous effectsAn increase on the time-to-maturity affects the option prices in three ways:

1 More time to maturity means more (aggregated) volatility. This increasesc(t) and p(t).

2 More time to maturity means more interest rate involved. This increases c(t)and decreases p(t).

3 More time to maturity means more dividend paid. This decreases c(t) andincreases p(t).

The net result of the above influences is not known a priori.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 17 / 49

Option Price vs Time to Maturity (example)

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 18 / 49

American Call Options and Time to Maturity

The dividend factorThere are two cases:

When no dividend is paid, an increase in time to maturity increases theAmerican call option price.In fact, as we will see, there is an equality between the price of the Europeanand the American call, in the case of no dividend.

When dividend is paid, an increase in time to maturity increases theAmerican call option price up to ex-dividend day.Theoretically, as we will see, this is the only case to consider the earlyexercise of an American call.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 19 / 49

American Put Options and Time to Maturity

The dividend factorAgain we have two cases:

When no dividend is paidI and the effect of interest rate is greater than the oppositely directed effect of

volatility, P decreases which means that an early exercise is preferable.I Otherwise, P increases, which means that the early exercise is not profitable.

When dividend is paid, the early exercise is preferable after the ex-dividenddate.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 20 / 49

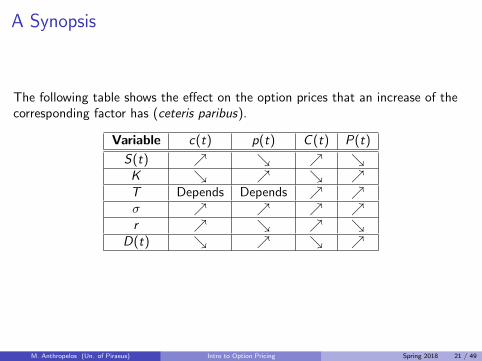

A Synopsis

The following table shows the effect on the option prices that an increase of thecorresponding factor has (ceteris paribus).

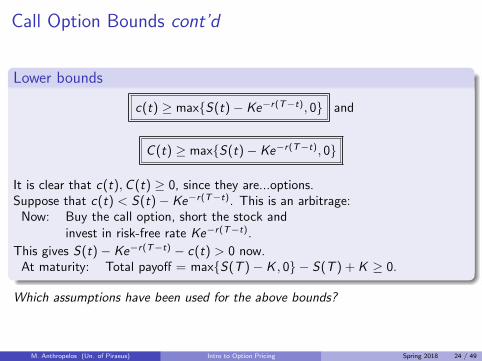

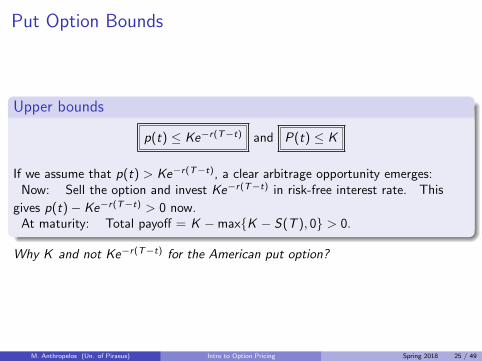

It is clear that p(t),P(t) ≥ 0, since they are...options.Suppose that p(t) < Ke−r(T−t) − S(t). This is an arbitrage:

Now: Buy the put option, buy the stock andborrow in risk-free rate Ke−r(T−t).

This gives Ke−r(T−t) − p(t)− S(t) > 0 now.At maturity: Total payoff = max{K − S(T ), 0}+ S(T )− K ≥ 0.

A slight change in the case of American put option price:If P(t) < K − S(t), the clear arbitrage opportunity is to buy the option, buy thestock, borrow K and instantly exercise the option and return the money to thebank.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 26 / 49

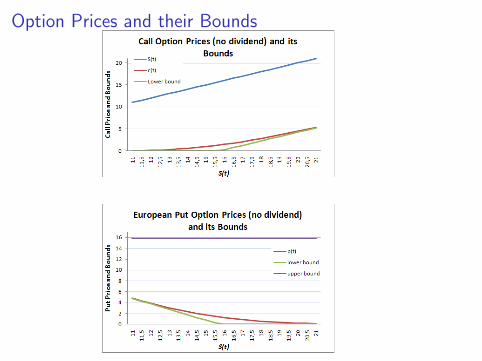

Option Prices and their Bounds

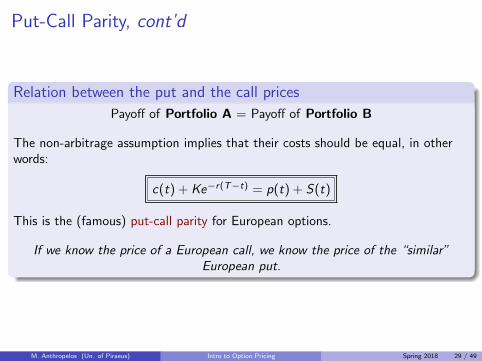

Put-Call Parity

Two interesting portfolios

We can use non-arbitrage arguments to find an exact relation between the pricesof European call and European put option written on the same asset, strike priceand maturity.Consider the following two portfolios:

Portfolio A: Long one European call option written on the stockand invest Ke−r(T−t) in the free-risk interest until T .

Portfolio B: Long one European put optionand buy one stock at S(t).

The cost of Portfolio A is c(t) + Ke−r(T−t).The cost of Portfolio B is p(t) + S(t).

At time T

Payoff of Portfolio A is max{S(T )− K , 0}+ K .Payoff of Portfolio B is max{K − S(T ), 0}+ S(T ).

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 28 / 49

Put-Call Parity, cont’d

Relation between the put and the call prices

Payoff of Portfolio A = Payoff of Portfolio B

The non-arbitrage assumption implies that their costs should be equal, in otherwords:

c(t) + Ke−r(T−t) = p(t) + S(t)

This is the (famous) put-call parity for European options.

If we know the price of a European call, we know the price of the “similar”European put.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 29 / 49

Put-Call Parity, cont’d

What put-call parity gives:

A clear non-arbitrage relation between the call and the put price.

The way to exploit the arbitrage opportunity that emerges if this parity doesnot hold.

A way to extract the risk-free interest rate that is used.

And some more that are coming...

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 30 / 49

Put-Call Parity for American Options

As we have mentioned, the put-call parity holds only for the European options.It is also possible to derive the following relation between the American options(with no dividend involved):

S(t)− K ≤ C (t)− P(t) ≤ S(t)− Ke−r(T−t)

The proof is left as an exercise.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 31 / 49

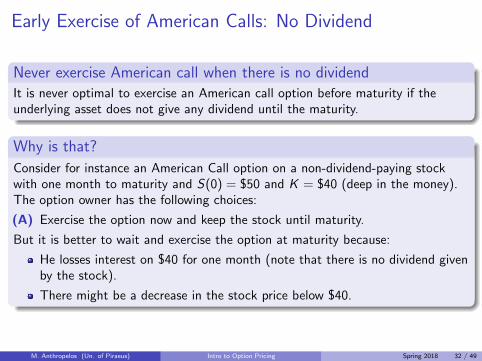

Early Exercise of American Calls: No Dividend

Never exercise American call when there is no dividendIt is never optimal to exercise an American call option before maturity if theunderlying asset does not give any dividend until the maturity.

Why is that?

Consider for instance an American Call option on a non-dividend-paying stockwith one month to maturity and S(0) = $50 and K = $40 (deep in the money).The option owner has the following choices:

(A) Exercise the option now and keep the stock until maturity.

But it is better to wait and exercise the option at maturity because:

He losses interest on $40 for one month (note that there is no dividend givenby the stock).

There might be a decrease in the stock price below $40.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 32 / 49

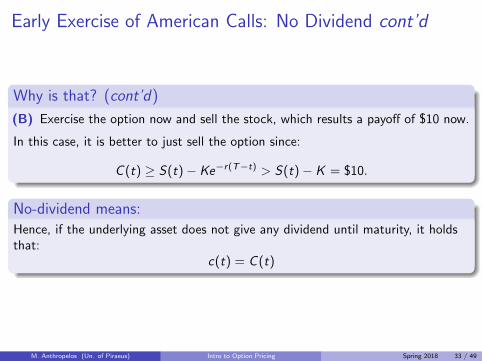

Early Exercise of American Calls: No Dividend cont’d

Why is that? (cont’d)

(B) Exercise the option now and sell the stock, which results a payoff of $10 now.

In this case, it is better to just sell the option since:

C (t) ≥ S(t)− Ke−r(T−t) > S(t)− K = $10.

No-dividend means:Hence, if the underlying asset does not give any dividend until maturity, it holdsthat:

c(t) = C (t)

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 33 / 49

Early Exercise of American Puts: No Dividend

It may be optimal to exercise American put even when there is nodividendConsider for instance an American put option on a non dividend paying stock withone month to maturity and S(t) = $30 and K = $40 (deep in the money). Theoption owner has the right to exercise the option and get $10 now and investthem until time T . By doing so the option owner:

exploits the difference K − S(t), which may be lower afterwards,

but losses any further increase of this difference.

Generally, there is a value S∗(t), and when S(t) is below S∗(t), the ownerexercises the put.It is more attractive to exercise an American put option when:

∗ Stock price decreases.

∗ Interest rate increases.

∗ Volatility decreases.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 34 / 49

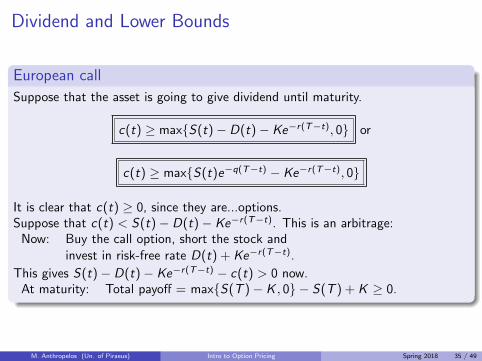

Dividend and Lower Bounds

European call

Suppose that the asset is going to give dividend until maturity.

c(t) ≥ max{S(t)− D(t)− Ke−r(T−t), 0} or

c(t) ≥ max{S(t)e−q(T−t) − Ke−r(T−t), 0}

It is clear that c(t) ≥ 0, since they are...options.Suppose that c(t) < S(t)− D(t)− Ke−r(T−t). This is an arbitrage:

Now: Buy the call option, short the stock andinvest in risk-free rate D(t) + Ke−r(T−t).

This gives S(t)− D(t)− Ke−r(T−t) − c(t) > 0 now.At maturity: Total payoff = max{S(T )− K , 0} − S(T ) + K ≥ 0.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 35 / 49

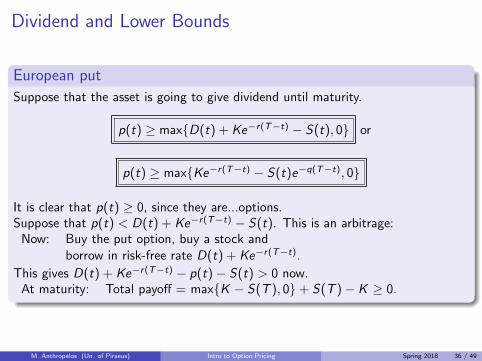

Dividend and Lower Bounds

European put

Suppose that the asset is going to give dividend until maturity.

p(t) ≥ max{D(t) + Ke−r(T−t) − S(t), 0} or

p(t) ≥ max{Ke−r(T−t) − S(t)e−q(T−t), 0}

It is clear that p(t) ≥ 0, since they are...options.Suppose that p(t) < D(t) + Ke−r(T−t) − S(t). This is an arbitrage:

Now: Buy the put option, buy a stock andborrow in risk-free rate D(t) + Ke−r(T−t).

This gives D(t) + Ke−r(T−t) − p(t)− S(t) > 0 now.At maturity: Total payoff = max{K − S(T ), 0}+ S(T )− K ≥ 0.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 36 / 49

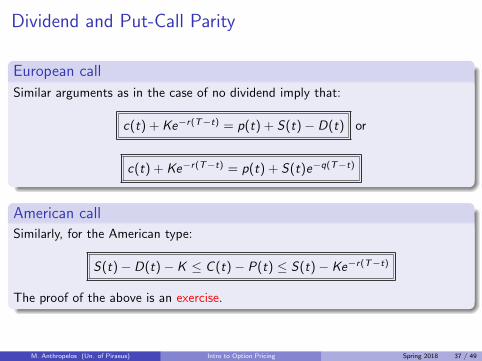

Dividend and Put-Call Parity

European call

Similar arguments as in the case of no dividend imply that:

c(t) + Ke−r(T−t) = p(t) + S(t)− D(t) or

c(t) + Ke−r(T−t) = p(t) + S(t)e−q(T−t)

American callSimilarly, for the American type:

S(t)− D(t)− K ≤ C (t)− P(t) ≤ S(t)− Ke−r(T−t)

The proof of the above is an exercise.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 37 / 49

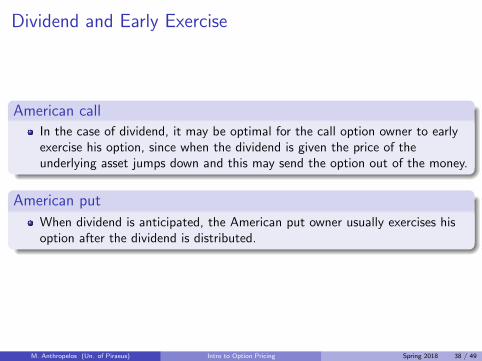

Dividend and Early Exercise

American callIn the case of dividend, it may be optimal for the call option owner to earlyexercise his option, since when the dividend is given the price of theunderlying asset jumps down and this may send the option out of the money.

American put

When dividend is anticipated, the American put owner usually exercises hisoption after the dividend is distributed.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 38 / 49

Outline

1 Factors that Affect Option Prices

2 Arbitrage BoundsNo dividend caseThe effect of dividend

3 More Strategies with Options and further Arbitrage Bounds

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 39 / 49

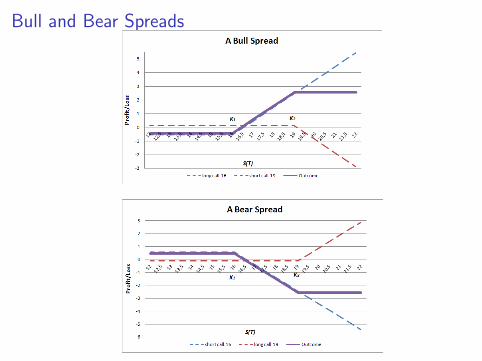

Bull and Bear Spreads

The spread

A spread trading strategy involves taking a position in two or more options of thesame type. Depending on which stock prices the spread gives profit, the spreadsare bull spreads and bear spreads.

The bull spread

The bull spread is created by buying a call option on a stock with certain strikeprice and selling a call option on the same stock with a higher strick price. Thisstrategy has small cost and anticipates (limited) profit if stock price increases.

The bear spread

The bear spread is created by buying a call option on a stock with certain strikeprice and selling a call option on the same stock with a lower strick price. Thisstrategy has small cost and anticipates (limited) profit if stock price decreases.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 40 / 49

Bull and Bear Spreads

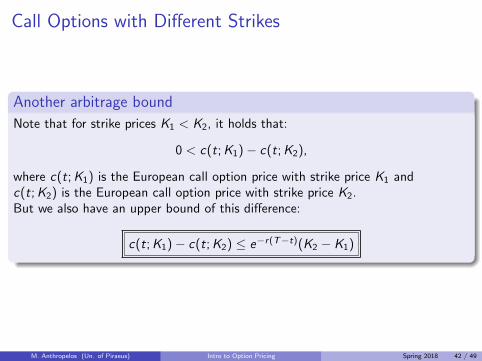

Call Options with Different Strikes

Another arbitrage bound

Note that for strike prices K1 < K2, it holds that:

0 < c(t; K1)− c(t; K2),

where c(t; K1) is the European call option price with strike price K1 andc(t; K2) is the European call option price with strike price K2.But we also have an upper bound of this difference:

c(t; K1)− c(t; K2) ≤ e−r(T−t)(K2 − K1)

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 42 / 49

Two Call Options with Different Strikes cont’d

Non-arbitrage proof

Suppose that c(t; K1)− c(t; K2) > e−r(T−t)(K2 − K1). Here is the emergedarbitrage:

Now: Buy call with strike price K2,short the call with strike price K1 andinvest e−r(T−t)(K2 − K1) in the bank.

This gives now c(t; K1)− c(t; K2)− e−r(T−t)(K2 − K1) > 0.At maturity there are three possible cases:

1 If S(T ) < K1, Payoff = (K2 − K1) > 0.

2 If K1 ≤ S(T ) < K2, Payoff = K2 − S(T ) > 0.

3 If S(T ) ≥ K2, Payoff = 0.

In any case, we start with something positive and end up in somethingnon-negative, which means that we have an arbitrage.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 43 / 49

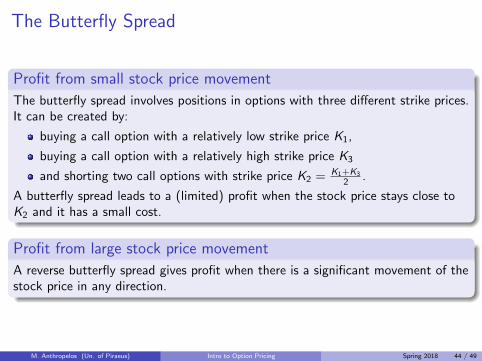

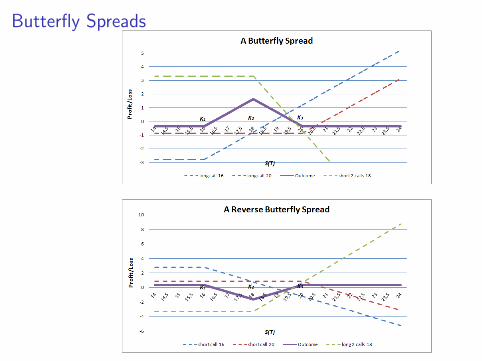

The Butterfly Spread

Profit from small stock price movement

The butterfly spread involves positions in options with three different strike prices.It can be created by:

buying a call option with a relatively low strike price K1,

buying a call option with a relatively high strike price K3

and shorting two call options with strike price K2 = K1+K3

2 .

A butterfly spread leads to a (limited) profit when the stock price stays close toK2 and it has a small cost.

Profit from large stock price movement

A reverse butterfly spread gives profit when there is a significant movement of thestock price in any direction.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 44 / 49

Butterfly Spreads

Three Call Options with Different Strike Prices

An non-arbitrage inequality

For strike prices K1 < K3 and K2 = K1+K3

2 , it holds that:

c(t; K2) ≤ 12 (c(t; K1) + c(t; K3))

where c(t; Ki ) is the European call option price with strike price Ki .

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 46 / 49

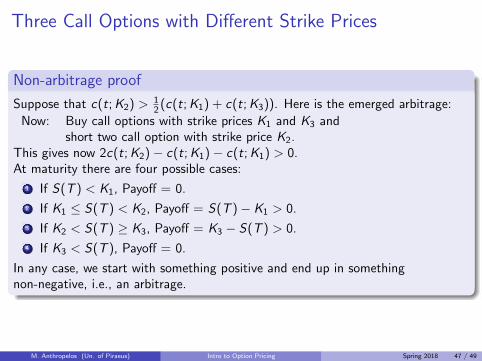

Three Call Options with Different Strike Prices

Non-arbitrage proof

Suppose that c(t; K2) > 12 (c(t; K1) + c(t; K3)). Here is the emerged arbitrage:

Now: Buy call options with strike prices K1 and K3 andshort two call option with strike price K2.

This gives now 2c(t; K2)− c(t; K1)− c(t; K1) > 0.At maturity there are four possible cases:

1 If S(T ) < K1, Payoff = 0.

2 If K1 ≤ S(T ) < K2, Payoff = S(T )− K1 > 0.

3 If K2 < S(T ) ≥ K3, Payoff = K3 − S(T ) > 0.

4 If K3 < S(T ), Payoff = 0.

In any case, we start with something positive and end up in somethingnon-negative, i.e., an arbitrage.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 47 / 49

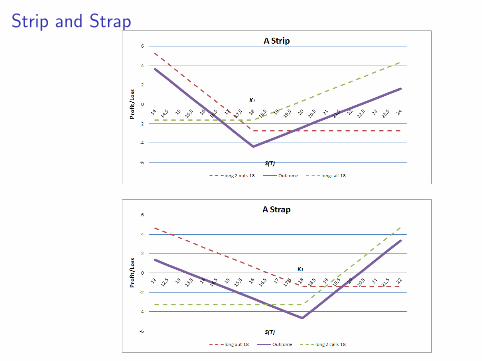

Strip and Strap

A strip

A strip consists of:

a long position in a call option.

a long position in two put options with the same strike price and the samematurity.

It anticipates profit with a large movement of the stock price, especially when ithas negative direction.

A strap

A strap consists of:

a long position in two call options.

a long position in a put option with the same strike price and the samematurity.

It anticipates profit with a large movement of the stock price, especially when ithas positive direction.

M. Anthropelos (Un. of Piraeus) Intro to Option Pricing Spring 2018 48 / 49