18

FINANCIAL EDUCATION TO INCREASE FINANCIAL ACCESS Mr. Y. Santoso Wibowo Directorate of Credit, Rural Bank and MSME Bank Indonesia Bali, July 2011

| Date post: | 18-Dec-2015 |

| Category: |

Documents |

| Upload: | henry-mckinney |

| View: | 215 times |

| Download: | 0 times |

FINANCIAL EDUCATION TO INCREASE FINANCIAL ACCESS

Mr. Y. Santoso WibowoDirectorate of Credit, Rural Bank and MSMEBank IndonesiaBali, July 2011

ACCESS TO FINANCE IN INDONESIA

Below Poverty

Line

Living in Rural

Area

13.33% 64.25%

Without access to

bank

60%

MSME Entrepreneur

99.91%

MSMEs that have not

been linked to bank

60-70%

2

MSME’S PROBLEMS TO ACCESS TO FINANCE

3

Community who have access to financial services Population who don’t have access

Sumber: World Bank (2009)

Access to formal financial services still become constraints to majority people in Indonesia, including MSME.

World Bank’s Survey shows that community who have access to formal financial services is 52%.

Communities who lived outside java have smaller access to financial services.

Access to Financial Services

Sumber: World Bank (2009)

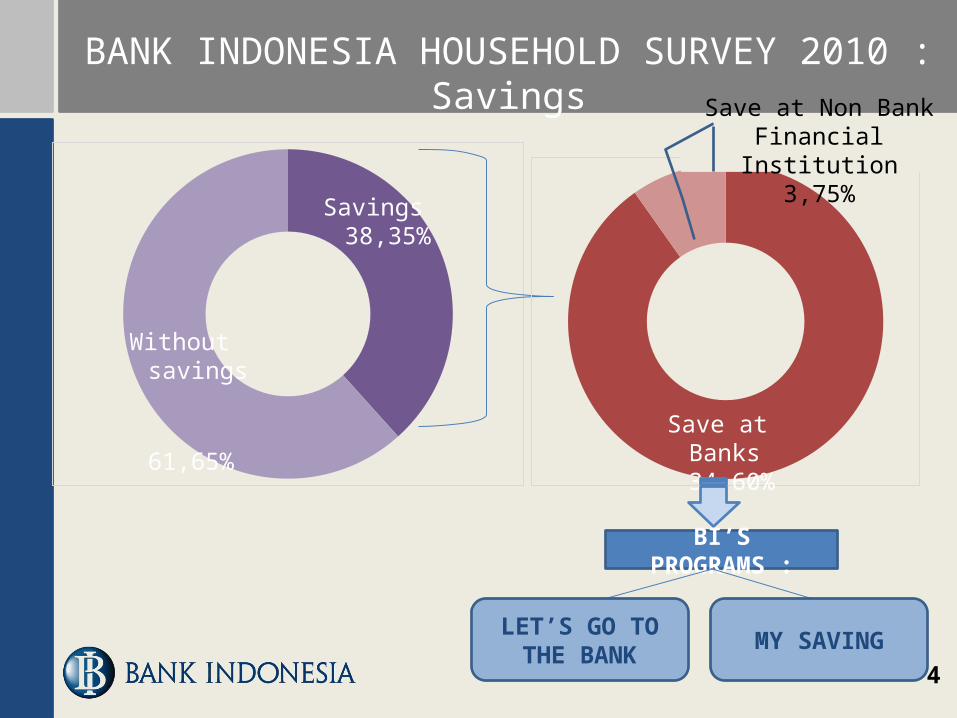

BANK INDONESIA HOUSEHOLD SURVEY 2010 : Savings

Savings 38,35%

Without savings

61,65% Save at Banks

34,60%

Save at Non Bank Financial Institution

3,75%

BI’S PROGRAMS :

4

LET’S GO TO THE BANK MY SAVING

Source of loan

BI HOUSEHOLD SURVEY 2010 : Credit

With loans 40,92%

Without loans 59,08%

Non Banks & Non MFIs 66,28%

Rural Banks 3,14%

Banks 18,25%

MFIs 12,33%

5

FINANCIAL INSTITUTION FOR MSME

MSMEs (52,8 millions business

units)

Commercial Bank

Rural Bank*

Saving and Loan Cooperatives Pawnshop

Other NBFI such as: leasing company,

multifinance, LPDB

Non Bank non Cooperatives MFI,

Such as BMT/LDKP/LPD/BK

K/LPK

BANK

Non

Bank

Finance both MSME and corporate

6

GAP BETWEEN BANKS AND MSMEs

7

SME

Scale GapGap between the loan size expected by banks

and the loan size needed by MSMEs, especially micro enterprises

Formalization gapGap between bank’s requirements for formal documents, such as formal business license,

property ownership, NPWP (tax number) versus the ability of MSME to fulfill the

requirements.

Information GapGap of information between bank products and procedures and the MSMEs knowledge

about them.

BANK

BI’S POLICY IN MSME DEVELOPMENT

The purpose of BI policy: • At the supply side is to increase bank’s

credit to MSME• At the demand side is to help increase

the eligibility and capability of MSME

8

BI’S POLICY IN MSME DEVELOPMENT

Training

Information Provision

Regulation

Infrastucture development

Dem

and

Side

Supp

ly S

ide

Cooperation with Government &

Other Institutions

SME’s access to finance

Growth of SME/Real

Sector

Research

9

DEMAND SIDE POLICY

ResearchTo support BI policy and strategy

•Lending model•provincial-based potential commodity •Other related topics

Training To increase bank’s expertise in MSME lending, BDSP’s skill in

assisting MSME and MSME access to finance

•Training to banking officers•Training to business development service providers (BDSP) in assisting MSME •Cluster development

Information provision

To disseminate research output to stakeholders

•Online information - DIBI (Indonesian Data and Business Information)•Workshop, seminar, road show

10

TRAINING

The purpose of training: – To enhance the knowledge, capability and to encourage

bank and Financial Institution for MSME to give loan to MSME

– To enhance the knowledge and capability of Business Development Service Provider (BDSP) in order to facilitate MSME access to finance and become Bank’s partner in developing MSME through loan monitoring and evaluation.

11

TRAINING cont’d…

Participants of training: – Commercial bank and Rural bank officers– Officers from other Financial Institution for MSME– Business Development Service Providers (BDSP) – Government officers involved in assisting and developing

MSME

12

TRAINING cont’d…

Training topic A. For Bank and Financial Institution :

- MSME business strategy- Survey of MSME Potential business with Rapid Rural

Appraisal (RRA) Method - Credit Analysis for MSME- How to handle non-performing loan- How to disburse loan to group of debtors with Self Help

Group scheme

B. For BDSP :Financial aspect including business feasibility (credit proposal)

13

TRAINING cont’d…

Number of Trainings : 41

Number of Participants : 1.221

14

Training performance (as of year 2010)

Number of Activ

e BDSP : 585

Number of

MSME :

7.935

Number of

Banks :

170

Total credit disbursed:

384.8 billion

IDR

TRAINING :

LINKAGE TO BANKS :

TRAINING cont’d…

Cooperation Bank Indonesia with other ministries:

Ministry of Cooperative and SME : BDSP for MSME Ministry of Agriculture : BDSP for Farmer Ministry of Marine Affairs and Fisheries : BDSP for fisher men

15

INFORMATION PROVISION

DIBI (Indonesian Data and Business Information)www.bi.go.id

16

A. Purpose of DIBI

Regional Government

Information on research, study and survey of Bank

Indonesia on various sector and industry

related with potential regional economy

development

Entrepreneur

Recognizing opportunity/expansion,

characteristic and business profile in

national and regional level and also directing

regional industry to grow and develop based on

potency and uniquenessBanking To support Bank Analysis

INFORMATION PROVISION cont’d…

17

A. Content of DIBI

1. Information for Entrepreneur :- priority commodity- funding scheme - MSME’s empowerment- bank’s service and MSME data)2. Information for Exporter :- export commodity profile- export regulation - export data3. Information for Banker :

- MSME credit report- MSME credit statistic - MSME data

4. Information for Public :- regional economy study- real sector study - publication- bank’s service and MSME data)5. Link to other Website

THANK YOU

18