137 Gadjah Mada International Journal of Business –May-August, Vol. 20, No. 2, 2018 Gadjah Mada International Journal of Business Vol. 20, No. 2 (May-August 2018): 137-164 * Corresponding author’s e-mail: [email protected]ISSN: 1141-1128 http://journal.ugm.ac.id/gamaijb Financial Flexibility as an Investment Efficiency Factor in Asian Companies Victoria Cherkasova, * and Evgeny Kuzmin National Research University Higher School of Economics (NRU HSE), Faculty of Economic Sciences, Department of Finance, Russian Federation Abstract: This study explores the impact of a company’s financial flexibility on the effectiveness of its investments.The number of companies that have financial flexibility was calculated with the application of thespare debt capacity method. The research identifies the impact of financial flexibility on investment activity and on the level of suboptimal investments. The data from 1,736 companies in theAsian region, during the 2005-2015time period, are presented. The Asian region has unique institutional, economic and commercial environments that present a great basis for this paper. The results of the research reveal that financially flexible companies spend more on their investment expenditure and conduct more effective investment policiesby reducing the level of over- and underinvestment. Financial flexibility helps compa- nies to make effective investments during a crisis period, but the difference in the flexibility between developed and developing countries and between large and small companies was not observed. Keywords: financial flexibility; financial leverage; investment expenditure; spare debt capacity; suboptimal investment JEL classification: D92, G01, G31, G32

Transcript

137

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

Gadjah Mada International Journal of BusinessVol. 20, No. 2 (May-August 2018): 137-164

Financial Flexibility as an Investment Efficiency Factorin Asian Companies

Victoria Cherkasova,* and Evgeny KuzminNational Research University Higher School of Economics (NRU HSE), Faculty of Economic Sciences,

Department of Finance, Russian Federation

Abstract: This study explores the impact of a company’s financial flexibility on the effectiveness of itsinvestments.The number of companies that have financial flexibility was calculated with the applicationof thespare debt capacity method. The research identifies the impact of financial flexibility on investmentactivity and on the level of suboptimal investments. The data from 1,736 companies in theAsian region,during the 2005-2015time period, are presented. The Asian region has unique institutional, economic andcommercial environments that present a great basis for this paper. The results of the research reveal thatfinancially flexible companies spend more on their investment expenditure and conduct more effectiveinvestment policiesby reducing the level of over- and underinvestment. Financial flexibility helps compa-nies to make effective investments during a crisis period, but the difference in the flexibility betweendeveloped and developing countries and between large and small companies was not observed.

IntroductionFinancial flexibility is a company’s ca-

pability to obtain financial resources in orderto have a timely reaction to any future unex-pected events and to maximize the company’svalue. Flexibility is closely connected to theavailability of external financing, since thismethod of obtaining funds has gained an in-creasing importance in capital structure de-cisions. The importance of financial flexibil-ity for a company is a relevant subject, as inrecent years receiving capital from third-partycredit organizations has become crucial forcompanies that want to achieve a sustainablepace of development, expand their businessand have a financial advantage over theircompetitors.

Authors focus on Asian countries be-cause of their diversity and varied economicpotential. The region is represented by bothwell-established countries and quickly grow-ing economies with growing numbers of edu-cated people and increased domestic con-sumption. The question of financial flexibil-ity’s presence is essential for Asian compa-nies because the developing economiesstimulate new investment opportunities andcause managers to find tools for increasingthe flexibility, in order to attract additionalresources for their businesses’ development.

The goal of this research is to identifythe existence of a relationship between finan-cial flexibility and the investment decisions’effectiveness. The execution of efficient in-vestment decisions is a vital objective for mostcompanies, as it facilitates sustainable growthand contributes to the maximization of share-holders’ wealth. This work combines meth-ods for determining a company’s financialflexibility and assessing its investment effi-ciency, which was not done in previous workson the subject of flexibility. The paper also

examines the effects of flexibility in the broad,fast-growing and diverse Asian region. Thedataset consists of 1,736 Asian public com-panies from 8 countries – India, Indonesia,China, Japan, South Korea, Taiwan, HongKong and Singapore.

Theoretical frame works, along with theempirical research, imply that financial flex-ibility plays a significant role in mitigating theissues of suboptimal investments. Most stud-ies on financial flexibility and its various ef-fects on company performance were under-taken in the late 2000s by such authors asByoun (2007), DeAngelo and DeAngelo(2007), Marchica and Mura (2010). Works byByoun (2007) and DeAngelo and DeAngelo(2007) have primarily focused their attentionon determining the sources of financial flex-ibility, while later research focuses more onthe implications of flexibility and have a moreholistic approach to its calculation. The con-nection between financial flexibility and in-vestment activity relates to the pecking or-der theory of Myers and Majluf (1984) andwas also covered by Yung et al. (2015),Ferrando et al. (2016) and others. Brief con-siderations of flexibility’s effects on invest-ment efficiency were described by Ma and Jin(2016), Nouri and Jafari (2016).

The problem of firms’ investment effi-ciency is of great interest to scholars and re-searchers, due to its relevance and practical-ity. While most of the current research pro-vides insights into how flexibility affects in-vestment levels, the volume of equitypayouts and firm value, authors contributeto the financial literature by examining theimpact of financial flexibility, in the form ofthe spare debt capacity, on the reduction ofsuboptimal investment decisions. Authorsinvestigate whether financially flexible com-panies make more optimal investment deci-sions (by reducing the levels of over- and

139

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

underinvestment)compared to the inflexibleones and whether the level of suboptimalinvestment expenditure is consequentlyless.In terms of the practical application ofthe research, the presence of financial flex-ibility can be considered by the managerialboard while making its investment policypreparations, which in turn will increase thecompany’s value - that is why the analysisprovided here can be used in business devel-opment decision making.

In contrast to previous research, authorshave combined two types of decisions bycompanies - financial and investment. Theoutcome of the research revealed that finan-cial decisions directly affect investment de-cisions and that a correctly selected capitalstructure leads to more optimal decisions forthe investment policy, by reducing the levelof suboptimal investments and increasing thecompany’s value.

Authors investigate three other topicsin addition to the main purpose of the ar-ticle. The 2008-2009 financial crisis raisedmany questions concerning the efficiency ofthe investment strategies by companies ofvarious sizes and in firms operating in coun-tries with various levels of economic devel-opment. To investigate these effects, firstly,authors have taken data from the Asian re-gion, which is a vast and rapidly growing eco-nomic zone that consists of many emergingand developed economies. Authors assumethat during a crisis it is easier for financiallyflexible companies to implement an optimalinvestment strategy, since these companieshave more resources at hand. Secondly, au-thors focus theirs research on the implicationsof countries’ economic development onfirms’ investment decisions. Authors supposethat this factor can significantly increase theimpact of flexibility’s presence, as with lessdeveloped financial institutions it represents

the stability and trust-worthiness of the com-pany. And finally, authors explore companiesof various sizes, suggesting that larger com-panies have more financial freedom and areless risky, so they consequently implementmore effective investment decisions.

The rest of this paper is structured asfollows. Section 1 provides the summary ofprevious research in to the concepts of fi-nancial flexibility, investment efficiency andtheir relation. Section 2 develops the hypoth-eses. Section 3 describes the methods that willbe used in this paper. Section 4 describes thesample of data used in the research. Section 5presents the analysis and discusses the resultsof the paper.

Literature Review

Financial FlexibilityEven though active studies on the topic

of financial flexibility have only been broughtout in recent decades, the roots of the ques-tion can be traced back to the classic worksin the field of finance. Modigliani and Miller(1963) were one of the first scientists to in-troduce the overall definition of flexibility,which they defined as a company’s ability tomaintain “a substantial reserve of untappedborrowing power.” These authors have statedthat even though higher levels of debt presenta tax shield advantage, firms with significantamounts of liabilities more commonly facefinancial constraints. Such an ambiguitymakes firms lower the reserve of their bor-rowing power, but not eliminate it completely.Myers (1984) confirms that firms plan tofund some of their investment through bor-rowing; however they try to restrain them-selves to avoid the cost of financial distress.Companies also maintain the level of theirborrowing power through their financial slack,

Cherkasova and Kuzmin

140

which is represented in the form of cash, realassets or marketable securities.

Despite the recognition of flexibility asa significant factor in the determination ofcapital structure in those works, it has notbeen discussed at length until recently. Byoun(2007), and DeAngelo and DeAngelo (2007),as well as many other researchers, haveshifted their focus towards this topic becausethe role of corporate finance strategy hasgreatly increased and the efficient manage-ment of capital no longer results in just mini-mizing the cost of capital and cash manage-ment. The detailed research by Graham andHarvey (2001) proved that the managementof companies do value financial flexibility,because it allows them to make future expan-

sions and acquisitions more easily. Thismeans that companies follow the Modiglianiand Miller (1963) trade-off theory and targettheir debt ratios.

One of the first modern works that isfocused primarily on the topic was the articleby DeAngelo and DeAngelo (2007). Accord-ing to authors, flexibility represents the criti-cal missing link in the previous theories ofcapital structure. The research introduces itsown approach to the capital structure theory,which links the agency costs, dividend poli-cies and the need for financial flexibility. Com-panies maintain low leverage to store theirunused debt capacity, in case of future unex-pected events. Stockpiling cash reserves isexpensive because of the potential tax dis-

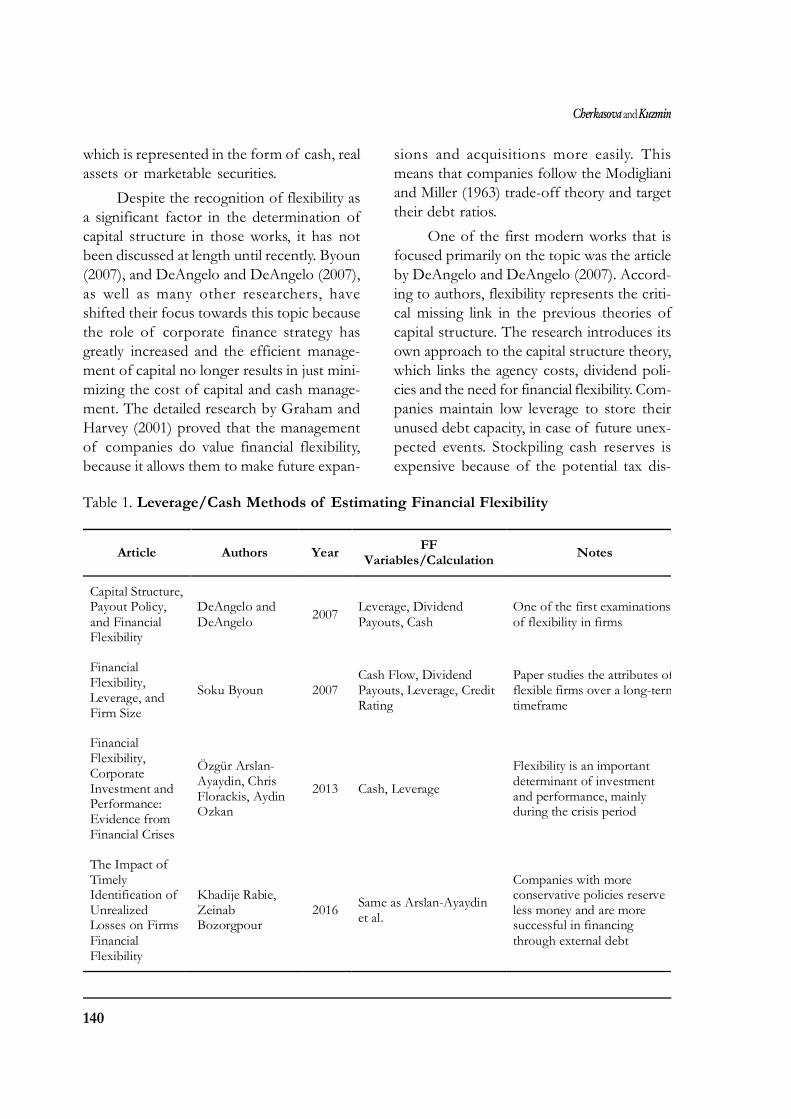

Table 1. Leverage/Cash Methods of Estimating Financial Flexibility

Article Authors Year FF Variables/Calculation Notes

Capital Structure, Payout Policy, and Financial Flexibility

DeAngelo and DeAngelo 2007 Leverage, Dividend

Payouts, Cash One of the first examinations of flexibility in firms

Paper studies the attributes of flexible firms over a long-term timeframe

Financial Flexibility, Corporate Investment and Performance: Evidence from Financial Crises

Özgür Arslan-Ayaydin, Chris Florackis, Aydin Ozkan

2013 Cash, Leverage

Flexibility is an important determinant of investment and performance, mainly during the crisis period

The Impact of Timely Identification of Unrealized Losses on Firms Financial Flexibility

Khadije Rabie, Zeinab Bozorgpour

2016 Same as Arslan-Ayaydin et al.

Companies with more conservative policies reserve less money and are more successful in financing through external debt

141

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

advantages, high opportunity costs and po-tential agency problems. DeAngelo refers toLa Porta et al. (2000)and Shleifer and Vishny(1997), stating that mature firms limit theoverall level of their internal funds by issu-ing substantial dividend payouts.

Byoun (2008) continued the analysis ofthe importance of financial flexibility andcreated one of the first independent defini-tions of the term, which is “the degree ofcapacity and speed at which the firm canmobilize its financial resources in order to

Article Authors Year FF Variables/Calculation Notes

Growth Opportunities and the Choice of Leverage, Debt Maturity, and Covenants

Matthew T. Billett, Tao-Hsien Dolly King, David C. Mauer

2007 Covenant Index - financial flexibility is higher with the decreasing number of covenants

Stable and mature firms are more flexible because they can dictate the number of covenants and their essence

Financial Flexibility, Investment Ability and Firm Value: Evidence from Firms with Spare Debt Capacity

Maria-Teresa Marchica, Roberto Mura

2010

Spare Debt Capacity model that combines leverage, market-to-book ratio, tangibility, size, profitability and industry leverage

One of the first articles to implement the mathematical approach to the flexibility model

Financial Inflexibility and the Value Premium

Michael Poulsen, Robert Faff and Stephen Gray

2013

Inflexibility Index - multiplication of normalized fixed assets ratio, leverage and financial constraints

Financial inflexibility is significantly related to the book-to-market ratio

Financial Flexibility and Capital Structure

Chris Harris 2015 Financial Flexibility is the ratio of share repurchases to the total payout

Higher levels of financial flexibility obtained through share repurchases are positively related to higher levels of firm debt

What Drives the Relationship Between Financial Flexibility and Firm Performance: Investment Scale or Investment Efficiency? Evidence from China

Chun-Ai Ma, Yanbo Jin

2016

Financial Flexibility Index (FFI), which accounts for the basic cash holdings, potential cash inflows and financing costs (i.e. external debt ability)

Proved that there is a link between the flexibility and investment efficiency/scale

Table 2. Mathematical and Other Financial Methods of Estimating Financial Flexibility

Cherkasova and Kuzmin

142

take reactive, preventive and exploitive ac-tions to maximize firm value.” The authorsupported the idea that businesses primarilymaintain their flexibility through the preser-vation of debt and equity payouts. The au-thor also suggested the existence of a nega-tive relation between cash holdings and le-verage, contrary to the framework ofDeAngelo.

The scope of the papers on the topichas greatly improved and now studies offer abigger variety of definitions for flexibility.Tables 1 and 2provideanoverall view of thevarious approaches to financial flexibility thatscientists have shown in the recent years.

Two main approaches can be definedfrom the analysis. The first one accounts fortwo factors, debt and cash reserves and isnarrower and more consistent with the clas-sical theories. The second approach is broader,as it also includes other variables, such as liq-uid assets sales, dividend reductions etc. Thelatter method is more up-to-date – research-ers are attempting to give flexibility a stricterdefinition and find ways to calculate the val-ues or dummies for the flexibility.

The use of leverage, as the proxy forfinancial flexibility, is currently the most ro-bust method that produces results which areconsistent with the economic theory and pre-vious research. According to the hierarchytheory, the information asymmetry that ex-ists in the imperfect financial world gives debtfinancing a clear advantage, compared to ad-ditional equity financing. The main challengein the use of leverage relates to the idea ofestimating the debt’s target level. The researchthat is developing the financial flexibilityproxies, based on the leverage approach, usethe works about the adjustments of capitalstructures to find out the factors that definecompanies’ capital policies. The basis of that

method lies both in the classical empiricalstudies and in the current studies.

Flannery and Rangan (2006) confirmedthat firms identify and pursue targeted capi-tal ratios. The targeting behavior was observedin various definitions of leverage and authorsestimated that with the occurrence of finan-cial shocks, the firms adapt their strategiesand quickly return to their target levels. Frankand Goyal (2009) studied the factors that af-fect the capital structure decisions of publiccompanies. Authors have gathered data fromvarious research papers and created a list offactors, such as size, growth, profitability andmany others, that can influence corporate le-verage.

Many authors have adopted and ex-panded the use of the leverage model.Marchica and Mura (2010) provided evidencethat companies with higher levels of flexibil-ity demonstrate improved levels of invest-ments. Their work has defined flexibility asthe presence of deviation between the pre-dicted and real value of leverage, now calledthe spare debt capacity. A similar techniquewas used by Yung et al. (2015) – that researchshowed that the conservative policy of lowleverage is beneficial for businesses in devel-oping countries and confirmed the value offlexibility during the global crises.

Investment Activity andEfficiency

The importance of financial flexibilityis closely related with a company’s investmentability. According to the managers’ surveys,flexibility in the form of a conservative le-verage policy allows managers to make deci-sions in imperfect markets (those that fea-ture contracting issues and asymmetric infor-mation). Companies are eager to maintain acertain level of flexibility, so that they can

143

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

escape the potential financial distress whennegative shocks appear and put money intolucrative projects when such possibilitiesarise.

The efficiency of the investments is re-lated to the deviations from the optimal levelof investments – the level in which the com-pany chooses to pursue all the profitableprojects and reject all the cases that will gen-erate losses. In the imperfect capital marketsthat suffer from agency problems and infor-mation asymmetry, firms may choose projectsthat have a negative Net Present Value(NPV), or not carry out ones with a positiveNPV – those situations are defined asoverinvestment and underinvestment respec-tively. La Rocca et al. (2008) explains whycompanies choose to keep their debt ratio low,even when there are lucrative options fromlenders to attract additional funds. The choiceof a specific leverage ratio for a certain pe-riod is a strategic tool for the company thatinfluences the financial behaviournot only ofthe firm itself, but of its competition as well.

There exist various approaches to cal-culate the efficiency of investments - Titmanet al. (2009); Cherkasova and Zakharova(2016)all used the historic average level ofinvestments for a 5- or 3-year period to esti-mate the optimal level of investment. If theaverage value of investments in the last threeperiods was the same as the current period’sinvestment volume, the company was under-taking its optimal level of investment. Au-thors have found a negative relation betweenan abnormal level of investments and stockreturns. Richardson (2006) decomposed to-tal investments in to the sum of capital ex-penditure, acquisitions and the expenses forresearch and development. The total amountof investment can be divided into three cat-egories: maintenance investments, investmentexpenditures into efficient projects and ab-

normal investments. A company’s growthpotential, financial leverage, cash flow, age,company size, stock returns, sector specific-ity and investments from the previous periodare the main determinants of its optimal in-vestments.

Richardson’s technique proves to beversatile; it is used in various papers that ex-amine the problems of investment efficiency.Han and Zhang (2016) modified the approachof Richardson and have implemented mon-etary policy factors, such as the growth ratesof the money supply and policy changes, toanalysethe impact of those factors on the ef-ficiency of the investment. Chen et al. (2011)and Biddle et al. (2009) proved the existenceof the link between the quality of financialreports and the subsequent efficiency of theinvestments. Ma and Jin (2016) have used thisparticular approach to determine the relationbetween investment efficiency and the Finan-cial Flexibility Index (FFI) that they have cal-culated.

Both the importance of the flexibilityobtained through leverage and cash holdingsfrom the company’s investment activity andthe connection of these factors with invest-ment efficiency have created a new field ofstudy that is being developed currently bysome financial researchers. Modern studiesexpand on the idea of financial flexibility asthe missing link between capital structuredecisions and firm performance. Research-ers have discovered that this flexibility canserve as a mediator between the external bor-rowing power and the implementation ofprofitable projects on-time and in-line withthe competition. There exist several possibleexplanations about how and why flexibility

Cherkasova and Kuzmin

144

serves as an intermediary between invest-ments and their efficiency.

The effect of this flexibility can be de-scribed with behavioral terms. The flexibilityallows corporate managers to undertakeriskier projects, despite the market’s frictionthat would otherwise prevent the firm fromundertaking some profitable deals. Flexibil-ity also affects the reduction of the princi-pal-agent conflict. The high amount of debtdoes not provide investors with confidence,because it means that the company is beingexposed to the risk of default or bankruptcy.The prudent behavior of managers reducesthe suspicions of the investors and eliminatesinefficient investments, to a certain extent.(Myers 1974)

De Jong et al. (2012) proved that finan-cial flexibility is one of the integral parts incapital policy decisions, which have a posi-tive impact on companies’ future invest-ments. The ability to issue additional debtresults in thereduction of investment distor-tions, especially in the periods when accessto capital is constrained. The findings sup-port the fact that flexibility can be one of thereasons why firms have lower leverage, eventhough additional debt may provide a lucra-tive option for tax-shielding.

Bancel and Mittoo (2011) state thatflexible firms experience a lower effect froma crisis on their business operations. The re-sults of their research into the2008 financialcrisis on the flexibility and performance ofthe European firms also confirm that flex-ibility is one of the more important determi-nants of the capital structure policy of a firmduring an economic downfall.

Ma and Jin (2016) developed a mecha-nism that defines the investment scale andefficiency as a mediator between flexibilityand firm performance. According to their

analysis, flexibility has a positive and signifi-cant effect on the two main parts of an in-vestment strategy – scale and efficiency. Theresearch stated that flexibility’s effect isgreater on the investment scale compared toits effect on efficiency. This outcome may beexplained by the nature of the rapidly grow-ing Chinese economy that authors are study-ing – in the developing countries companiesare more willing to pay more attention towardsexpansion rather than focusing on efficiencyfactors.

Yung et al. (2015) examined the effectsof flexibility in emerging countries andshowed that flexibility can enhance afirm’sinvestment ability and contribute to the re-duction of its investment sensitivity fromcash flows. Authors state that flexibility hasa more significant effect during a global eco-nomic crisis. Flexible companies cut lessfunding from their investment levels in com-parison with inflexible firms and have a bet-ter overall operating performance.

Some of the research, however, op-poses the results stated above. Gdala (2009)argues that for the companies present on theWarsaw Stock Exchange, there is no signifi-cant relationship between their debt policiesand changes in their capital expenditure.Moreover, the value of cash holdings isproven to be more significant for their growthprospects. Nouri and Jafari (2016) examinedthe importance of flexibility on investmentefficiency with respect to managerial owner-ship and discovered a correlation that con-tradicts the other studies. According to au-thors, the increase in flexibility levels leadsto an increase in both over- and under-invest-ment. Although the article does not commenton the obtained results and does not providea possible explanation for thisbehaviour,which is inconsistent with other research, itshows that certain approaches may expose the

145

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

negative relation between financial flexibil-ity and the efficiency of investments.

Unlike other authors, authors want tocombine the methods for determining acompany’s financial flexibility and investmentefficiency, so authors can examine the rela-tion between the two in this paper. The pro-vided theoretical background gives the op-portunity to prove that firms can use this flex-ibility factor in their future investment poli-cies, to make their decisions more effective.

Hypotheses DevelopmentModigliani and Miller (1963) state that

firms tend not to use an abnormal amountof debt in their capital structure, despite thetax advantages from doing so - the reason forthat is “the need for preserving flexibility.”Marchica and Mura (2010) provide evidencethat a conservative policy of low leveragehelps companies to maintain their financialflexibility, which in turn allows firms to ex-hibit enhanced levels for their investmentabilities. Flexibility gives the corporate man-agers the opportunity to anticipate certaingrowth possibilities in the future and increasethe level of their capital expenditure. Thetheoretical framework provided gives the ideathat a period of flexibility prevents the com-pany from borrowing and presents bettergrowth opportunities in the future. The ma-jor subject of this research is to define therelationship between financial flexibility andinvestment efficacy and this task is reflectedin the first hypothesis.Hypothesis 1: Financial flexibility has a positive

impact on the investment expenditureof a firm.

Our second hypothesis is connectedwith the idea of the increased efficiency of

investments in flexible companies – the ideathat has been discussed by some of the pre-vious researchers. Ma and Jin (2016) andDenis and McKeon (2012) state that compa-nies use flexibility to respond to positiveshocks and adapt their investment policiesaccordingly. Flexibility has a positive effecton firm performance, serving as a mediatorbetween investment and performance levels.

Following the provided theoretical re-search, authors can assume that flexibilitygives more opportunities for the managers notonly to increase the levels of investment, butalso to invest funds in profitable projects andavoid the projects with higher amounts of riskand lower returns. This consequently meansthat financial flexibility can improve the in-vestment strategy of the firm and thecompany’s overall performance as a result.Hypothesis 2: Flexibility has a positive effect on re-

ducing the level of suboptimal invest-ments.

To make the study more complex andcoherent, authors also pose several additionalhypotheses that are concerned with the addi-tional factors that affect flexibility and invest-ment efficiency. These factors are thecompany’s size, the economic developmentof the country where the firm operates andthe presence or absence of an economic cri-sis.

Financial flexibility has a significant ef-fect during a period of crisis, especially onthe levels of investment and performance.Arslan-Ayaydin et al. (2014) have found outthat firms in the East Asian region, duringthe period from1994 to2009 maintained theirflexibility through a conservative leveragepolicy and by their cash holdings, which cre-ated a buffer during times of uncertainty.More importantly, financial flexibility turned

Cherkasova and Kuzmin

146

out to be a major determinant of investmentand performance levels during the Asian cri-sis of 1997-1998.Hypothesis 3: An economic crisis significantly in-

creases the impact of financial flex-ibility on the efficiency of investments.

Ma and Jin (2016) examined the effectof financial flexibility on both investment’sefficiency and scale in the rapidly developingChinese economy and conclude that whileflexibility has a much greater impact on thescale of the investments, rather than on theirefficiency, both effects are significant for theemerging country. Yung et al. (2015) statesthat in the data sample of 33 emerging coun-tries, flexibility improves firms’ investmentabilities and values. Authors claim that theimportance of flexibility in those economiesis greater compared to the developed ones,since volatile capital flows, which are typicalin the developing markets, confine the avail-ability of bank credit. This turns financial flex-ibility into an important instrument for thefirms in the rapidly growing countries, thevalue of which is more significant than in theestablished economies.Hypothesis 4: Flexibility has a more significant

impact on investment efficiency indeveloping countries.

Byoun (2011) states that flexibility’spresence assures credit organisations aboutthe stability of a company and allows themto supply it with credit at little risk. Financialflexibility’s status gives a signal about thecompetitive advantage for large and smallcompanies that either struggle with obtain-ing money for projects that require significantcapital expenditure, or have a very narrowaccess to the capital market.

Ferrando et al. (2016) shows that whilethe presence of flexibility is more commonin larger firms, it also plays an important part

in the policies of smaller sized companies.Being a larger size allows a company to havea more efficient investment policy; while fora smaller firm flexibility gives it the opportu-nity to have a broader variety of credit op-tions, which improves its investments.Hypothesis 5: Flexibility has an identical impact

on the investment efficiency of smalland large companies.

Research Design

Determining Financially FlexibleCompanies

The methods in our research stay in-linewith those from prior studies while expand-ing them further with the help of additionalvariables and model specifications. The firststep is connected with finding financiallyflexible firms using the Marchica and Mura(2010)space debt capacity model. The sec-ond and third steps involve modelling theinvestment efficiency and finding the linkbetween financial flexibility and investmentability, while later research is dedicated to-wards the influence of the additional factorsof flexibility and investment efficiency.

The methods in our research stay in-linewith the ones from prior studies, while beingexpanded further with the help of additionalvariables and model specifications. Modernstudies provide evidence that financial flex-ibility is being maintained primarily throughleverage decisions (Graham and Harvey 2001;Bancel and Mittoo 2011). Because flexibilityis being defined by corporate decisions aboutthe possibilities for future growth, in the math-ematical framework it is being defined as afactor that will generate the difference be-tween the predicted and observed levels ofleverage. To calculate the estimation for the

147

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

leverage, authors are going to use the modi-fied version of the Marchica and Mura (2010)approach, which captures the effect of finan-cial flexibility in the leverage model.

For the first step of the analysis, authorsuse the model to divide companies into twogroups of flexible and inflexible firms. Theequation for calculating the baseline level ofthe leverage for each company is representedbelow:

Leverageit= Leveragei,t-1 + 1Industry Leveragei,t

+ 2MTBi,t + 3Sizei,t

4Tangibilityi,t + 5Profitabilityi,t

+ ui,t ....................................(1)

where is the ratio of the bookvalue of total debt to total assets,

is the median indus-try level of leverage, is the market-to-book value, which is a ratio calculated asthe book value of the assets plus the marketvalue of equity minus the book value of eq-uity divided by the book value of the assets,

is the natural logarithm of total assets(measured in thousands of U.S dollars),

is the ratio of fixed assets tototal assets and is the returnon assets’ ratio.

The leverage prediction is estimatedwith the use of the dynamic generalizedmethod of moments methodology, proposedby Arellano and Bond (1991). This approachallows us to control for heteroscedasticity andcollinearity problems that arise when themodel includes the lagged value of the de-pendant variable. Table 2 provides a detaileddescription of the variables used.

The data are used to calculate the lin-ear prediction of the estimated leverage from

the fitted model - firms that will have a nega-tive difference between their actual and pre-dicted leverage are assumed to have SpareDebt Capacity (SDC). This means that thecompanies had an ability to use their addi-tional debt funding, but they chose not to useit. The difference should be more than 5 per-cent to exclude all the insignificant resultsthat might impact the outcome of the fur-ther calculations.

Works using the SDC model usuallystate that a firm is financially flexible when ithas demonstrated at least three consecutiveyears of SDC. While authors said that thistime-span does not follow any previous ra-tionale, this technique can reduce the pres-ence of noise in the model. Financial flex-ibility is then defined as a dummy variable(0, 1) which is given a value of 1 when thefirms show three consecutive years of sparedebt capacity and is given a value of 0 other-wise.

Finding the Link betweenFinancial Flexibility andInvestment Ability

In line with the capital structure theory,authors assume that when a firm reaches fi-nancial flexibility, it will increase its invest-ment. The equation that tests this notion isas follows:

Investmentit=nvestmenti,t-1 + 1CFi,t-1

+ 2TobinQi,t + 3FFi,t

4(FFi,t x CFi,t-1)+ ui,t ..........(2)

where is the ratio of the netchanges in property, plant and equipmentwith the addition of the maintenance coststo the total assets, is the ratio of earn-ings before interest, taxes, depreciation and

Cherkasova and Kuzmin

148

amortisation divided by total assets, is the ratio of the value of the

company to the total assets and is theavailability of spare debt capacity, as definedin Step 1 of the methodology. The model in-corporates the FF dummy as well as its inter-action with the cash flow of the firm. Thisinteraction will show how flexibility definesthe presence of the cash flow in the overallinvestment and explains whether the flexiblefirms have a lower sensitivity of investmentto the cash flow compared to the inflexibleones.

Following Richardson, authors will cal-culate the total investment as the sum of newinvestments and the maintenance cost. Au-thors are going to sum these parts to find eachcompany’s real investment level. This modelwill test Hypothesis 1 – the financial flexibil-ity dummy should have a positive and sig-nificant effect on the capital expenditure ofthe companies. In line with Marchica andMura (2010) the negative interaction betweenthe cash flow and financial flexibility shouldalso be observed; that will mean that flexiblefirms are more willing to fund external invest-ments thought debt rather than through theirinternal funds.

Measurement of InvestmentEfficiency and Regression Models

The third step of the research is dedi-cated to the calculation of the investment’sefficiency, which was previously defined asthe level of abnormal investments (over-in-vestment and under-investment).

To calculate the optimal level of invest-ment, authors are going to use Richardson’s(2006) model. The regression predicts thepossible investment level, along with thenumber of main determinants for the invest-ment. Authors are going to modify the model

in accordance to our goals and include addi-tional factors that can affect the level of in-vestment:

Invit= + 1Leveragei,t-1 + 2Cashi,t-1

+ 3MTBi,t-1 4Sizeit-1 + 5Returnit-1

6Invit-1 + eit ................................(3)

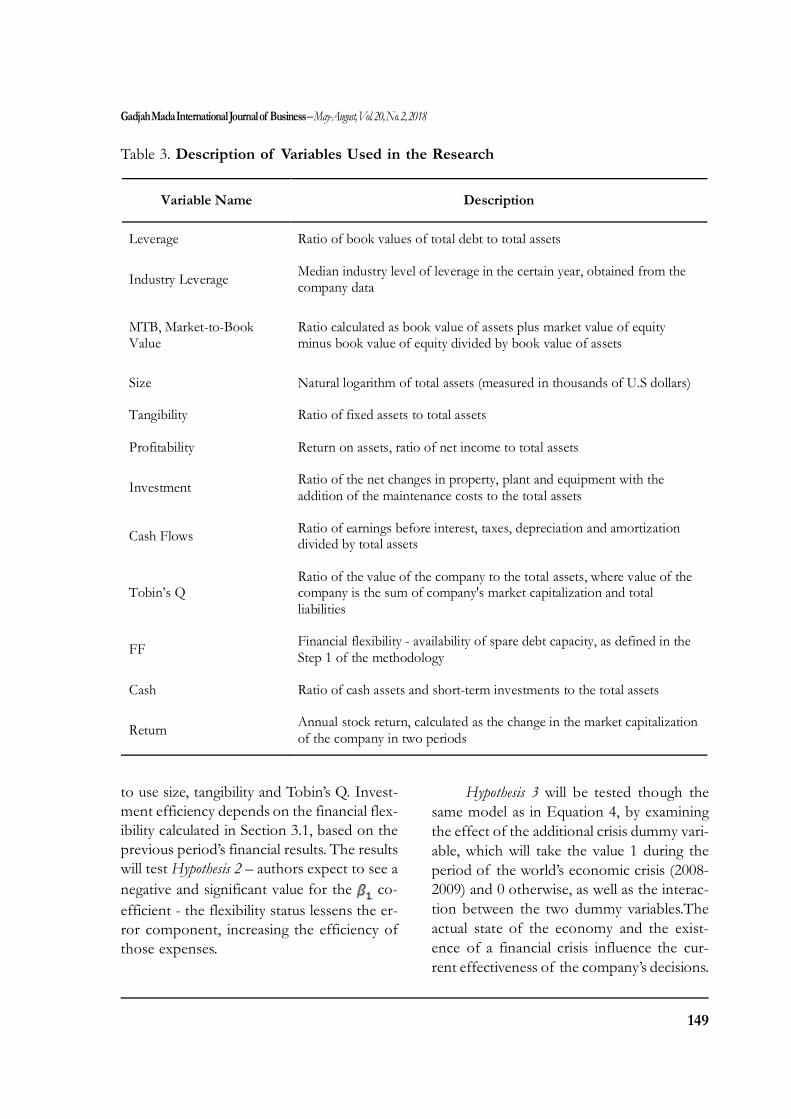

where is a ratio of the cash assetsand short-term investments to the total as-sets and is the annual stock re-turn, calculated as the change in the marketcapitalization of the company in two peri-ods. Other variables have been defined in theprevious equations – the full list of variablesused, along with their definitions, is presentedin Table 3.

Authors will then calculate the residu-als that were observed in the model fromEquation 3 - positive residuals will mean acase of over-investment by the company,while the reverse situation will be valid forthe under-investment scenario. The absolutevalue of from Equation 3 will become theproxy for the efficiency of the investments,which will be named as in further esti-mations.

In the next part of the research authorsare going to estimate the effect of financialflexibility along with the supporting factors:

IEit= + 1FFit + nControlVari,t-1

+ uit ..............................................(4)

where is the absolute value of error that authors obtained from the previousmodel and stands for the value of subopti-mal investments; standsfor the variables that can also define the effi-ciency of the investment – authors are going

149

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

to use size, tangibility and Tobin’s Q. Invest-ment efficiency depends on the financial flex-ibility calculated in Section 3.1, based on theprevious period’s financial results. The resultswill test Hypothesis 2 – authors expect to see anegative and significant value for the co-efficient - the flexibility status lessens the er-ror component, increasing the efficiency ofthose expenses.

Table 3. Description of Variables Used in the Research

Hypothesis 3 will be tested though thesame model as in Equation 4, by examiningthe effect of the additional crisis dummy vari-able, which will take the value 1 during theperiod of the world’s economic crisis (2008-2009) and 0 otherwise, as well as the interac-tion between the two dummy variables.Theactual state of the economy and the exist-ence of a financial crisis influence the cur-rent effectiveness of the company’s decisions.

Variable Name Description

Leverage Ratio of book values of total debt to total assets

Industry Leverage Median industry level of leverage in the certain year, obtained from the company data

MTB, Market-to-Book Value

Ratio calculated as book value of assets plus market value of equity minus book value of equity divided by book value of assets

Size Natural logarithm of total assets (measured in thousands of U.S dollars)

Tangibility Ratio of fixed assets to total assets

Profitability Return on assets, ratio of net income to total assets

Investment Ratio of the net changes in property, plant and equipment with the addition of the maintenance costs to the total assets

Cash Flows Ratio of earnings before interest, taxes, depreciation and amortization divided by total assets

Tobin’s Q Ratio of the value of the company to the total assets, where value of the company is the sum of company's market capitalization and total liabilities

FF Financial flexibility - availability of spare debt capacity, as defined in the Step 1 of the methodology

Cash Ratio of cash assets and short-term investments to the total assets

Return Annual stock return, calculated as the change in the market capitalization of the company in two periods

The impact of a crisis should be nega-tive since more companies are constrainedand are more likely to make suboptimal in-vestment decisions. The presence of finan-cial flexibility should reduce the distortionduring the period of the crisis (Arslan-Ayaydin et al. 2014).

Hypothesis 4 will incorporate a similardesigned dummy for the economic develop-ment of the country, entitled - it equals 0 if the economy is considered asdeveloped by the World Bank List of HighIncome Economies, and will take the value1 if the country is classified as a developingone.

IEi,t= 0 + 1FFit + 2Developingi,t

+ 3(FFi,t x Developingi,t )+ nnControlVari,t-1 + uit

Developing countries are more exposedto inefficiency risks due to their restrainedaccess to capital, so authors expect a posi-tive value for the coefficient. The betacoefficient of the interaction between devel-oping countries and financial flexibility is ex-pected to be negative – this will mean thatflexibility plays a more substantial role in theemerging and rapidly growing economies.

For Hypothesis 5 the data will be split intotwo groups: firms that are smaller or largerthan the mean level. Equation 4 will be cal-culated from two datasets, to provide the pre-liminary results about the differences in flex-ibility – then dummy will be in-

troduced– it will take the value of 1 for thosecompanies whose total assets are smaller thanthe mean, while the value 0 will be given toall the other firms. The dummy variable willreplace the control variable of size to avoidany collinearity issues. Furthermore, size (andconsequently the categorization)along with the other financial results from pre-vious periods that determine a company’s flex-ibility, or affect the future investment effi-ciency of a firm will also be replaced, unlikethe external factors of development and cri-sis that the business is exposed to in the cur-rent period and that affect the current per-formance of investments.

The value of the coefficient shouldbe positive, since smaller companies are morerestrained in their financing choices andchoose projects not based on their efficiency,but on the external financing sources avail-able to them and the amount of debt thatthey can obtain. To prove Hypothesis 5 thecoefficient should be insignificant – for allthe presented companies’ flexibility presentssimilar levels of importance that do not fluc-tuate with an increase in the total assets.

Sample DescriptionThe sample in our research consists of

eight countries over the period from 2005 to2015. The data were taken from ThomsonReuters DataStream database. Authors elimi-nated the outliers’ effect by winsorising thefinancial variables at the 1 percent level. Thefinal sample consists of 1,736 firms over 11periods that comprise 19,096 firm-year ob-servations.

151

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

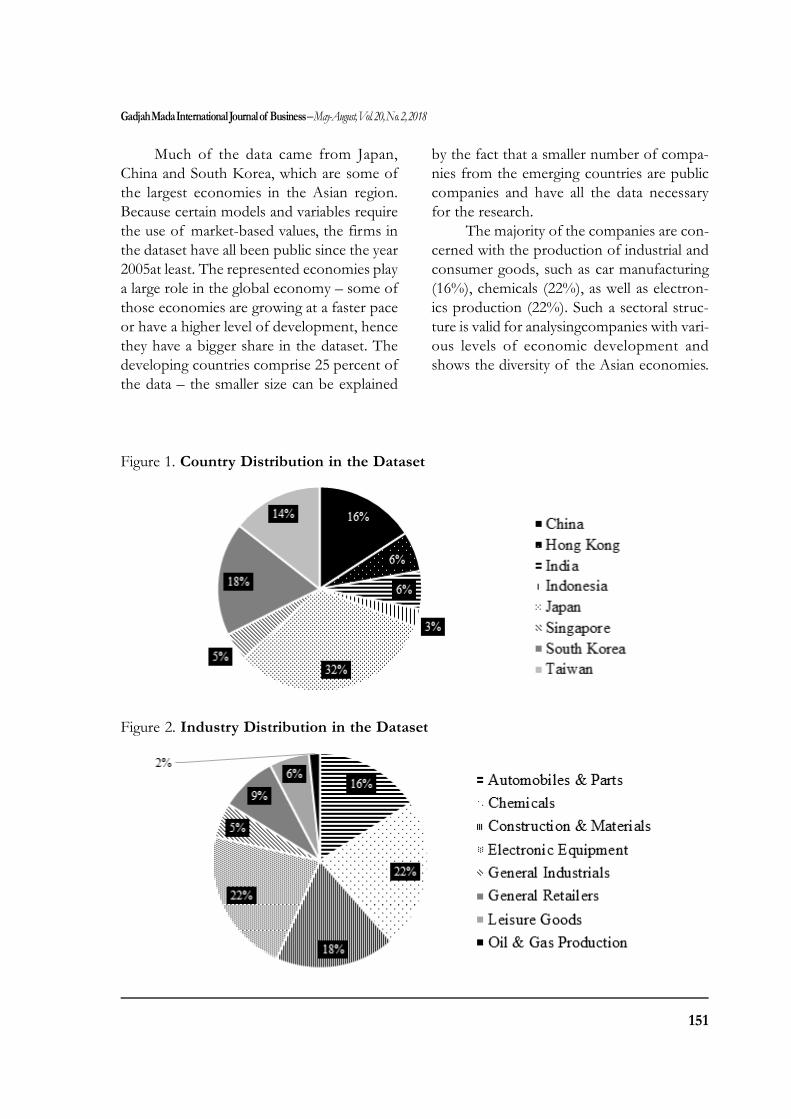

Much of the data came from Japan,China and South Korea, which are some ofthe largest economies in the Asian region.Because certain models and variables requirethe use of market-based values, the firms inthe dataset have all been public since the year2005at least. The represented economies playa large role in the global economy – some ofthose economies are growing at a faster paceor have a higher level of development, hencethey have a bigger share in the dataset. Thedeveloping countries comprise 25 percent ofthe data – the smaller size can be explained

by the fact that a smaller number of compa-nies from the emerging countries are publiccompanies and have all the data necessaryfor the research.

The majority of the companies are con-cerned with the production of industrial andconsumer goods, such as car manufacturing(16%), chemicals (22%), as well as electron-ics production (22%). Such a sectoral struc-ture is valid for analysingcompanies with vari-ous levels of economic development andshows the diversity of the Asian economies.

Figure 1. Country Distribution in the Dataset

Figure 2. Industry Distribution in the Dataset

Cherkasova and Kuzmin

152

Results and Discussion

Identification of FinanciallyFlexible Behavior in Companies

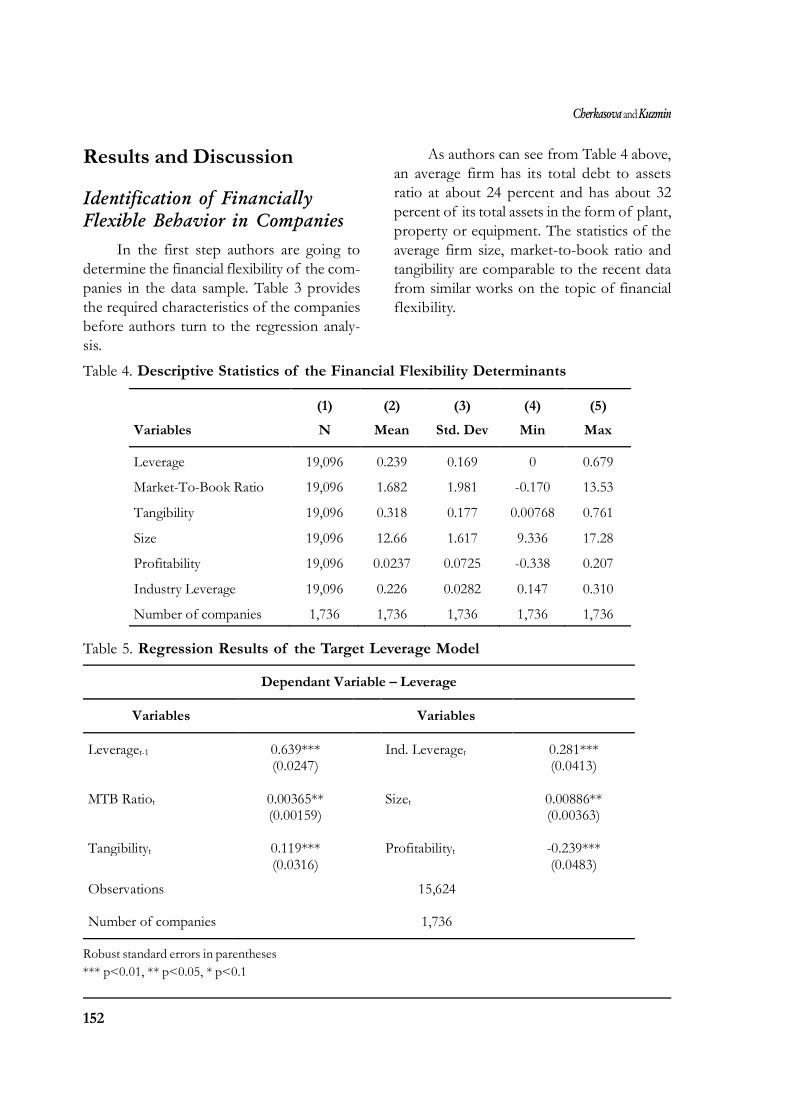

In the first step authors are going todetermine the financial flexibility of the com-panies in the data sample. Table 3 providesthe required characteristics of the companiesbefore authors turn to the regression analy-sis.

As authors can see from Table 4 above,an average firm has its total debt to assetsratio at about 24 percent and has about 32percent of its total assets in the form of plant,property or equipment. The statistics of theaverage firm size, market-to-book ratio andtangibility are comparable to the recent datafrom similar works on the topic of financialflexibility.

Table 4. Descriptive Statistics of the Financial Flexibility Determinants

Table 5. Regression Results of the Target Leverage Model

(1) (2) (3) (4) (5)

Variables N Mean Std. Dev Min Max

Leverage 19,096 0.239 0.169 0 0.679

Market-To-Book Ratio 19,096 1.682 1.981 -0.170 13.53

Tangibility 19,096 0.318 0.177 0.00768 0.761

Size 19,096 12.66 1.617 9.336 17.28

Profitability 19,096 0.0237 0.0725 -0.338 0.207

Industry Leverage 19,096 0.226 0.0282 0.147 0.310

Number of companies 1,736 1,736 1,736 1,736 1,736

Robust standard errors in parentheses*** p<0.01, ** p<0.05, * p<0.1

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

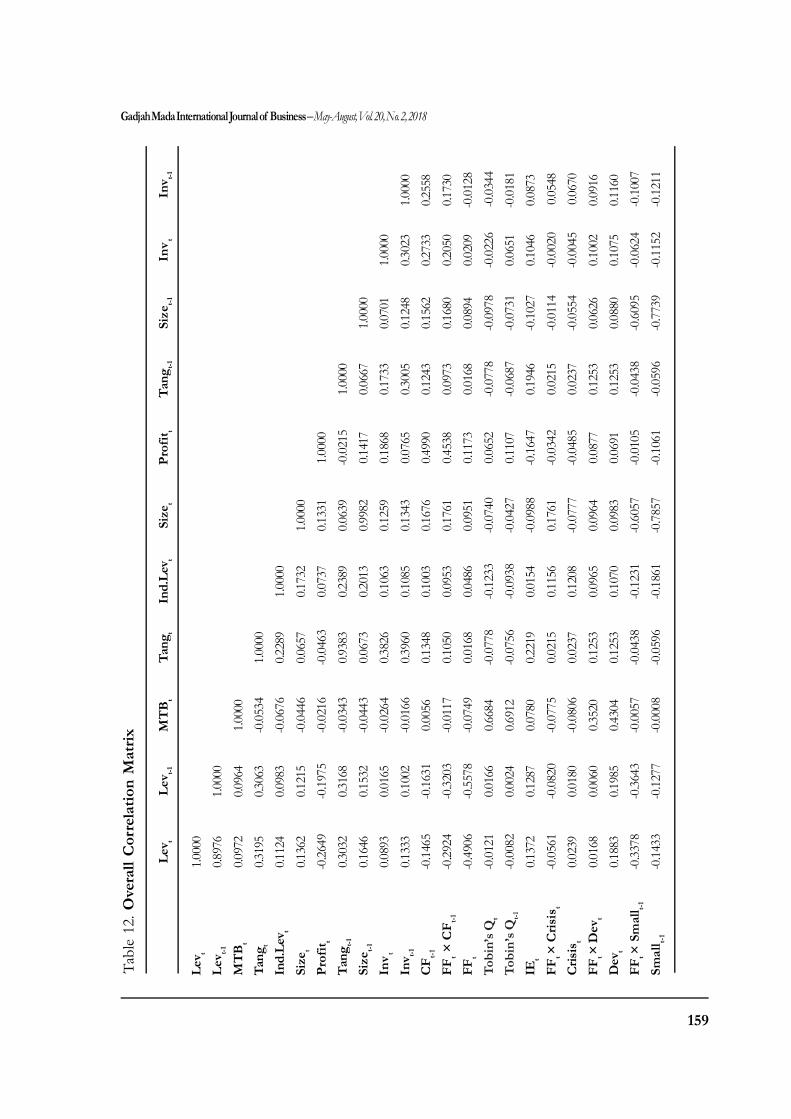

Authors will move on to the regressionanalysis and the prediction of the target le-verage level for the companies – this estima-tion will then be used to identify the level ofspare debt capacity and the presence of fi-nancial flexibility in the companies. Table 12presents the correlation matrix of all the usedvariables in this and the later steps of the re-search. Authors can observe the expectedcorrelation between the current and laggedlevels of leverage – this confirms the idea ofthe firms’ intention to follow the target le-verage approach. The model that authors willuse to determine the results accounts for sucha correlation effect.

Table 5 shows the results of the regres-sion that determines the impact of financialfactors on the debt issuing behaviourof thefirm and estimates the possible target levelof its leverage. Authors divide the firm/yearobservations into two groups: when the com-

pany showed flexible behavior and when itdid not. Authors assigned the firm a finan-cially flexible badge only when it demon-strated three years of consecutive spare debtcapacity. The use of the previous periods al-lows us to find flexibility’s status during the2008 to 2015 period only. In our dataset, au-thors see that 70 percent of the firm/yearobservations can be classified as represent-ing the financial flexibility status of the com-pany for a certain period. The results showthat most of the companies in the non-finan-cial sector are pursuing the policy of havingspare debt capacity.

Determining the Connectionbetween Financial Flexibility andInvestment Ability

The second step determines whetherflexibility has any impact on the company’sinvestment policy. Flexible companies are less

Robust standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

Table 6. Regression Results of the Investment Activity Model

constrained financially and should thereforeshow higher levels of investment activity.Authors are going to prove the existence ofthe link between flexibility and investmentactivity. Table 6 presents the outcome of thecalculation.

The results show that financial flexibili-ty’s effect is positive and statistically signifi-cant, which proves the descriptive resultsobtained earlier. Their conservative leveragepolicy allows firms to borrow additional fundswithout high levels of risk– this provides theopportunity for them to spend more on theirinvestment projects - something the inflex-ible firms cannot afford to do. This evidenceand the big share of the flexible firms in thesample may suggest that after achieving a flex-ible status, companies tend to increase theirinvestments to finance more projects. The

increase is not large, so that the companiescan maintain their levels of stability, avoidinflexibility and use the excess debt capacityto respond to possible market shocks.

We can also see that while the availabil-ity of the cash flow increases capital expen-diture, flexible firms are less dependent on it- flexible companies may shift their focusfrom equity sources to debt sources whenfunding new projects. These results allow usto claim that Hypothesis 1 is not rejected.

Examining the Link betweenFinancial Flexibility andInvestment Efficiency

In this stage authors consider the im-pact of flexibility’s presence on investment’sefficiency. Firms with spare debt capacity

Robust standard errors in parentheses*** p<0.01, ** p<0.05, * p<0.1

Table 7. Regression Results of the Expected Investments Model

155

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

increase their overall investment and, becauseof the easy access to external financing andless pressure from the debt holders and share-holders, they should also make better invest-ment decisions. Financial flexibility, whileincreasing the investment amount, should alsoserve as a mediator between the investmentsand their efficiency.

Authors will begin the analysis by con-structing the investment predictions for allthe available time periods. The results willthen be used to find the residuals of thismodel, which will be used as proxies for theover- and underinvestment amounts in eachfirm/year observation. Following the ap-proach of Richardson, authors are going to

Industry Effects Yes Yes Robust standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

Table 8. Impact of Financial Flexibility on Investment Efficiency

Cherkasova and Kuzmin

156

use the fixed effects regression model, ac-counting for the year-specific effects.

The results show that the level of in-vestments is growing with the higher levelsof returns, investments from the previousperiod and the bigger stock of cash and thehigh level of debt reduces the amount of in-vestment, which is consistent with the resultsof previous studies. A possible explanationfor the negative relation of the company’s sizeand investment level may lie in the notionthat large and mature companies find it diffi-cult to manage their increasing number ofassets and hence implement large-scaleprojects less often. Market-to-book valueshows itself as insignificant, which may becaused by the unobserved factors that causea small impact in this dataset. Expected in-

vestment is in accordance with previous re-search and is reliable to measure the size ofnon optimal investments.

Authors will begin with the testing ofhypotheses 2 and 3. The first regression will in-clude the effect of flexibility only, while thesecond one will also add the crisis dummyvariable, as well as the interaction betweenthe two dummy variables. The results can beseen in Table 8.

Authors can observe that the presenceof financial flexibility negatively affects theabsolute value of the investment model’s er-rors. The control variables also show the ex-pected behavior - increasing levels of fixedassets and Tobin’s Q results in the undertak-ing of more suboptimal projects. Firmsclassed as being flexible face less financial

Table 9. Impact of Financial Flexibility on Investment Efficiency in the Developing Coun-tries

157

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

constraints and undertake their projects withfewer distortions, which the inflexible com-panies face. Flexibility serves as the interac-tion variable that creates a connection be-tween the investments and their efficiency,which allows us to state that Hypothesis 2 isnot rejected.

The effect of a crisis is proven to besignificant, and the impact of flexibility dur-ing the crisis turned out to be significant aswell. This notion leads to the idea that flex-ible companies could undertake some projectsthat were efficient for their business, evenduring a period of economic recession. Whilea crisis influences investment performance,financially flexible companies could imple-ment projects that other firms are not able topick up, due to the recession’s effects. In this

situation flexibility worked as a tool that al-lowed companies to take advantage of theunexpected market shock. In general, suchresults lead to the conclusion that Hypothesis3 is not rejected.

In the next step authors are going to in-troduce the dummy variable of the develop-ing country, which takes a value of 1 whenthe country is emerging and 0 otherwise.

Table 9 provides the regression resultswhich include the dummy of the country’seconomic development. The importance offlexibility in the sample remained significant,however the effects that were added with theinclusion of the developing country effectshowed their insignificance in the model. Theoutcome suggests that while the underdevel-opment of the economy could present some

Table 10. Comparison of Financial Flexibility Effect in Companies of Various Size

Robust standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

Cherkasova and Kuzmin

158

challenges to the company, those challengesare not connected to the process of obtain-ing further debt. This result may be explainedby the fact that companies around the worldhave much wider access to capital from glo-bal banks and conglomerates. Firms are notrestricted to only borrowing money from creditorganizations inside their own country but canafford to seek funds from other countries,especially if these firms have financial flex-ibility. One of the other explanations mightlie in the idea that most of the developingAsian countries have established financialinstitutions that are similar to the ones in thedeveloped economies, in terms of their debtpolicies. The results allow us to conclude thatHypothesis 4 is rejected.

Authors are going to continue the re-search by exploring whether the flexibility

effects vary with changes to the total assets’volume. Authors begin with the preliminaryestimation of the FF coefficients in twogroups of observations. The smaller compa-nies are the ones that have total assets thatare less than the mean amount, large compa-nies have more assets compared to the aver-age level.

Table 10 shows that the effect remainedsimilar for both groups and did not show signsof a substantial difference. The results showthat generally small companies tend to makemore suboptimal decisions compared to theirlarger counterparts. This is consistent with thefinancial literature, where size is one of thereasons for asymmetry and agent issues.Larger firms can attract the money they needto borrow more easily, so they experiencefewer issues with large investment programs.

(0.00141) (0.00376) Small Companyt-1 0.00576*** Tobin’s Qt-1 0.00412*** (0.00191) (0.000761)

FFt × Small Companyt-1 0.00120 Intercept 0.0188***

(0.00205) (0.00255)

Observations 12,152

Number of companies 1,736

Year Effects Yes

Industry Effects Yes

Table 11. Impact of Financial Flexibility on Investment Efficiency in the Smaller-SizedCompanies

Robust standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

159

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

Lev t

Lev t-1

MT

Bt

Tang

tIn

d.Le

v tSi

zet

Prof

it tTa

ngt-1

Size

t-1

Inv t

Inv t-1

Lev t

1.000

0Le

v t-10.8

976

1.000

0M

TB

t0.0

972

0.096

41.0

000

Tang

t0.3

195

0.306

3-0

.0534

1.000

0In

d.Le

v t0.1

124

0.098

3-0

.0676

0.228

91.0

000

Size

t0.1

362

0.121

5-0

.0446

0.065

70.1

732

1.000

0Pr

ofit t

-0.26

49-0

.1975

-0.02

16-0

.0463

0.073

70.1

331

1.000

0Ta

ngt-1

0.303

20.3

168

-0.03

430.9

383

0.238

90.0

639

-0.02

151.0

000

Size

t-1

0.164

60.1

532

-0.04

430.0

673

0.201

30.9

982

0.141

70.0

667

1.000

0In

v t0.0

893

0.016

5-0

.0264

0.382

60.1

063

0.125

90.1

868

0.173

30.0

701

1.000

0In

v t-10.1

333

0.100

2-0

.0166

0.396

00.1

085

0.134

30.0

765

0.300

50.1

248

0.302

31.0

000

CF t-

1-0

.1465

-0.16

310.0

056

0.134

80.1

003

0.167

60.4

990

0.124

30.1

562

0.273

30.2

558

FFt ×

CF t-

1-0

.2924

-0.32

03-0

.0117

0.105

00.0

953

0.176

10.4

538

0.097

30.1

680

0.205

00.1

730

FFt

-0.49

06-0

.5578

-0.07

490.0

168

0.048

60.0

951

0.117

30.0

168

0.089

40.0

209

-0.01

28To

bin’

s Qt

-0.01

210.0

166

0.668

4-0

.0778

-0.12

33-0

.0740

0.065

2-0

.0778

-0.09

78-0

.0226

-0.03

44To

bin’

s Qt-1

-0.00

820.0

024

0.691

2-0

.0756

-0.09

38-0

.0427

0.110

7-0

.0687

-0.07

310.0

651

-0.01

81IE

t0.1

372

0.128

70.0

780

0.221

90.0

154

-0.09

88-0

.1647

0.194

6-0

.1027

0.104

60.0

873

FFt ×

Cris

ist

-0.05

61-0

.0820

-0.07

750.0

215

0.115

60.1

761

-0.03

420.0

215

-0.01

14-0

.0020

0.054

8C

risis

t0.0

239

0.018

0-0

.0806

0.023

70.1

208

-0.07

77-0

.0485

0.023

7-0

.0554

-0.00

450.0

670

FFt ×

Dev

t0.0

168

0.006

00.3

520

0.125

30.0

965

0.096

40.0

877

0.125

30.0

626

0.100

20.0

916

Dev

t0.1

883

0.198

50.4

304

0.125

30.1

070

0.098

30.0

691

0.125

30.0

880

0.107

50.1

160

FFt ×

Sm

all t-

1-0

.3378

-0.36

43-0

.0057

-0.04

38-0

.1231

-0.60

57-0

.0105

-0.04

38-0

.6095

-0.06

24-0

.1007

Smal

l t-1

-0.14

33-0

.1277

-0.00

08-0

.0596

-0.18

61-0

.7857

-0.10

61-0

.0596

-0.77

39-0

.1152

-0.12

11

Tabl

e 12

. Ove

rall

Cor

rela

tion

Mat

rix

Cherkasova and Kuzmin

160

CF t-

1FF

t × C

F t-1

FFt

Tobi

n’s

Tobi

n’s

IEt

FFt ×

Cris

ist

FFt ×

Dev

tD

evt

FFt

Smal

l t-1

Qt

Qt-

1C

risis

t

Lev t

Lev t-1

MT

Bt

Tang

t

Ind.

Lev t

Size

t

Prof

it t

Tang

t-1

Size

t-1

Inv t

Inv t-1

CF t-

11.0

000

FFt ×

CF t-

10.7

373

1.000

0

FFt

0.136

70.5

375

1.000

0

Tobi

n’s Q

t0.0

490

0.043

6-0

.0054

1.000

0

Tobi

n’s Q

t-10.1

075

0.095

4-0

.0455

0.818

11.0

000

IEt

-0.08

17-0

.0978

-0.10

060.0

711

0.077

71.0

000

FFt ×

Cris

ist

0.030

30.1

826

0.219

20.0

086

-0.07

91-0

.0062

1.000

0

Cris

ist

0.000

40.0

037

-0.00

41-0

.0466

-0.07

790.0

367

0.810

11.0

000

FFt ×

Dev

t0.1

104

0.239

50.2

784

0.366

90.3

470

0.039

00.0

409

-0.00

171.0

000

Dev

t0.1

012

-0.08

33-0

.1075

0.403

60.3

985

0.070

9-0

.0177

0.000

00.7

342

1.000

0

FFt ×

Sm

all t-

1-0

.0468

0.081

50.4

776

0.022

6-0

.0010

0.007

20.1

158

0.038

30.0

078

-0.11

561.0

000

Smal

l t-1

-0.13

50-0

.1001

-0.05

670.0

358

0.038

20.0

764

0.036

40.0

559

-0.11

63-0

.1572

0.705

31.0

000

Tabl

e 12

. Con

tinu

ed

161

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

To confirm the idea that the availabil-ity of the spare debt capacity does indeed playan equally important role for the companies,regardless of their size, authors will constructanother regression model where authors aregoing to include the dummy variable thatshows whether the company is small or not.The effects of flexibility in companies ofvarious sizes that were obtained during theresearch are presented in Table 11.

The interaction between size and flex-ibility showed no real significance – smallerflexible companies can attract additional debtissuing options, because banks can see theirstability and hence are less hesitant to fundthe projects. Bigger firms face less constrains,which provides an opportunity to respond toshocks in the market. The flexibility likeli-hood may increase with the companies’ size,because it is easier for larger companies tomaintain flexibility. The effect on investmentefficiency, on the other hand, will remain simi-lar whether the firm is large or small, becausein both cases it allows them to attract thefunds they need to respond to changes in themarket and will help to reduce the effect ofsuboptimal capital expenditure. Therefore,authors can conclude that Hypothesis 5 is notrejected.

To conclude, the overall results are inline with the previous research and with themajority of our expectations. Some of thefindings were not anticipated, but authorsfound explanations for the behaviour, takinginto the account Asia’s business and economicenvironment.

ConclussionThis study continues and expands the

research into the topic of financial flexibil-ity. The research pays closer attention to theconnection between flexibility and the effec-

tiveness of investments. Financial flexibilityis usually called the “missing link” in the capi-tal structure decisions that have a consider-able impact on firm performance. This re-search has investigated how flexibility affectsthe investment decisions and their perfor-mance in Asian countries. Authors took 1,736firms from 8 Asian countries and determinedtheir flexibility status using the spare debtcapacity model. The results showed that mostof the companies are showing the presenceof flexibility.

The main results of this study includeconclusions regarding the link between flex-ibility and investment efficiency, as well asthe impact of external and internal factorson this relationship. Authors calculated theimpact of the flexibility on the investmentlevels and the efficiency of those investments.Companies in the dataset showed that flex-ible firms tend to increase their investmentlevels, using flexibility as a mediator that al-lows them to undertake projects with a posi-tive NPV and reduce the level of suboptimalexpenditure. The flexibility helped to reducethe level of inefficient investments during theeconomic crisis, which was beneficial duringthe expansion of the Asian economy duringthat period. Amore detailed study of the im-pacts of the crisis in the region, along with amore detailed study of corporate governancemodels during that period are among the mostattractive areas for further research.

The difference inflexibility’s effects be-tween developing and developed countries inthe dataset was not observed. The processof globalization and the expansion of financ-ing services around the world make firm char-acteristics more important than changes in themacroeconomic factors, especially in suchcountries where fluctuations in the economyare not large. The results show that flexibility’simpact is similar for large and small firms.

Cherkasova and Kuzmin

162

While bigger companies are more likely todemonstrate flexible behaviour, the volumeof its impact does not change and remainssignificant.

This research confirms most of the out-comes that were obtained in other articlesthat are connected to examining the impactof financial flexibility. Apart from its aca-demic relevance, the research can also behelpful in the practical sphere, especiallywhen making decisions about the capital

structure of a firm.This paper provides fur-ther evidence that flexibility plays a big rolein company decisions and demonstrates thepositives of flexibility on investment perfor-mance. The research in this field is rather topi-cal, because more and more companies aregetting interested in gaining greater access tocapital markets around the world and thepresence of financial flexibility is a big ad-vantage that can improve these firms’ per-formance.

ReferencesArellano, M., and S. Bond. 1991. Some tests of specification for panel data: Monte Carlo evidence and an

application to employment equations. The Review of Economic Studies 58 (2): 277–97.Arslan-Ayaydin, Ö., C. Florackis, and A. Ozkan. 2014. Financial flexibility, corporate investment and

performance: Evidence from financial crises. Review of Quantitative Finance and Accounting 42 (2):211–50.

Bancel, F., and U. R. Mittoo. 2011. Financial flexibility and the impact of the global financial crisis. Interna-tional Journal of Managerial Finance 7 (2): 179–216.

Biddle, G. C., G. Hilary, and R. S. Verdi. 2009. How does financial reporting quality relate to investmentefficiency? Journal of Accounting and Economics 48 (2–3). Elsevier: 112–31.

Billett, M. T., T-H. D. King, and D. C. Mauer. 2007. Growth opportunities and the choice of leverage,debt maturity, and covenants. The Journal of Finance: The Journal of the American Finance Association 62(2): 697–730.

Brounen, D., A. de Jong, and K. Koedijk. 2004. Corporate finance in Europe: Confronting theory withpractice. Financial Management 33 (4): 71–101.

Brown, S., and E. Powers. 2015. Do Firms Value Financial Flexibility?. http://cicia.uprrp.edu/PII/scott_brown_informe_final.pdf

Byoun, S. 2007. Financial Flexibility, Firm Size and Capital. Hankamer School of Business.Byoun, S. 2008. How and when do firms adjust their capital structures toward targets? The Journal of

Finance LXIII (6) (Dec): 3069-3096.Byoun, S. 2011. Financial flexibility and capital structure decision. SSRN (http://dx.doi.org/10.2139/

ssrn.1108850 )Chen, F., O. K. Hope, Q. Li, and X. Wang. 2011. Financial reporting quality and investment efficiency of

private firms in emerging markets. Accounting Review 86 (4): 1255–88.Chen, N., and E-N. Hsiao. 2014. Insider ownership and financial flexibility. Applied Economics 6846 (June

2015): 1–21.Cherkasova, V., and E. Zakharova. 2016. Suboptimal investments and M&A: A deals in emerging capital

markets. Economic Annals 61 (208): 93–120.

163

Gadjah Mada International Journal of Business – May-August, Vol. 20, No. 2, 2018

DeAngelo, H., and L. DeAngelo. 2007. Capital structure, payout policy, and financial flexibility.” MarshallSchool of Business Working Paper (July): 1–24.

Denis, D. J., and S. B. McKeon. 2012. Debt financing and financial flexibility evidence from proactiveleverage increases. Review of Financial Studies 25 (6): 1897–1929.

Denis, D. J., and V. Sibilkov. 2010. Financial constraints, investment, and the value of cash holdings. Reviewof Financial Studies 23 (1): 247–69.

Dudley, E. 2012. Capital structure and large investment projects. Journal of Corporate Finance 18 (5): 1168–92. Elsevier B.V.

Eisdorfer, A., C. Giaccotto, and R. White. 2013. Capital structure, executive compensation, and invest-ment efficiency. Journal of Banking and Finance 37 (2): 549–62. Elsevier B.V.

Esfandiari, H., and B. Jamshidinavid. 2016. The investigation effect of value of financial flexibility ondividend policy, financial leverage and level of cash holdings. International Business Management 10 (7):1215–19.

Ferrando, A., M. T. Marchica, and R. Mura. 2016. Financial flexibility and investment ability across theEuro area and the UK. European Financial Management 23 (1): 87–126.

Flannery, M. J., and K. P. Rangan. 2006. Partial Adjustment toward Target Capital Structures.” Journal ofFinancial Economics 79 (3): 469–506.

Frank, M. Z., and V. K. Goyal. 2009. Capital structure decisions: Which factors are reliably important?Financial Management 38 (1): 1–37.

Gdala, I. 2009. Financial Flexibility and Investment: Evidence from the Warsaw Stock Exchange. http://pure.au.dk/portal/files/7768/220230.pdf[1 October 2013].

Graham, J. R., and C. R. Harvey. 2001. The theory and practice of corporate finance: Evidence from thefield. Journal of Financial Economics 60 (2–3): 187–243.

Han, D., and P. Zhang. 2016. Monetary policy, financing constraints and investment efficiency. NankaiBusiness Review International 7 (1): 80–98.

Harris, C. 2015. Financial flexibility and capital structure. Academy of Accounting and Financial Studies Journal19 (2): 119–28.

de Jong, A., M. Verbeek, and P. Verwijmeren. 2012. Does financial flexibility reduce investment distor-tions? Journal of Financial Research 35 (2): 243–59.

Jun, Z. 2003. Investment, investment efficiency, and economic growth in China. Journal of Asian Economics14 (5): 713–34.

Ma, C-A., and Y. Jin. 2016. What drives the relationship between financial flexibility and firm perfor-mance: Investment scale or investment efficiency? Evidence from China. Emerging Markets Financeand Trade 52 (9): 2043–55.

Marchica, M. T., and R. Mura. 2010. Financial flexibility, investment ability, and firm value: Evidence fromfirms with spare debt capacity. Financial Management 39 (4): 1339–65.

McNichols, M. F., and S. R. Stubben. 2008. Does earnings management affect firms’ investment deci-sions? Accounting Review 83 (6): 1571–1603.

Modigliani, F., and M. H. Miller. 1963. Corporate income taxes and the cost of Capital: A Correction. TheAmerican Economic Review 53 (3): 433–43.

Cherkasova and Kuzmin

164

Myers, S. 1974. Interactions of corporate financing and investment decisions - Implications for capitalbudgeting. The Journal of Finance 29 (1): 1–25.

Myers, S. C. 1984. The capital structure puzzle. Journal of Finance 39 (3): 576–92.Myers, S. C., and N. S. Majluf. 1984. Corporate financing and investment decisions when firms have

information that investors do not have. Journal of Financial Economics 13 (2) (June): 187-221Nouri, M., and S. M. Jafari. 2016. The impact of financial flexibility on investment efficiency (over-

investment and under-investment) with respect to managerial ownership in the firms listed inTehran Stock Exchange. ICP Business, Economics and Finance 3 (2): 18–22.

La Porta, R., F. Lopez-de-Silanes, A. Shleifer, and R. W. Visnhy. 2000. Agency problems and dividendpolices around the world. The Journal of Finance 55 (1) (Feb.): 1–33.

Poulsen, M., R. Faff, and S. Gray. 2013. Financial inflexibility and the value premium. International Review ofFinance 13 (3): 327–44.

Rabie, K., and Z. Bozorgpour. 2016. The impact of timely identification of unrealized losses on firmsfinancial flexibility. International Business Management 10 (8): 1455–60.

Rapp, M. S., T. Schmid, and D. Urban. 2014. The value of financial flexibility and corporate financialpolicy. Journal of Corporate Finance 29: 288-302. Elsevier B.V.

Richardson, S. 2006. Over-investment of free cash flow. Review of Accounting Studies 11:159–89.Rocca, M. La, T. La Rocca, and D. Gerace. 2008. A survey of the relation between capital structure and

corporate strategy. Australasian Accounting Business and Finance Journal 2 (2): 1–18.Shleifer, A., and R. Vishny. 1997. A survey of corporate governance. The Journal of Finance LII (2) (June):

737–83.Titman, S., K. C. J. Wei, and F. Xie. 2009. Capital Investments and Stock Returns. Journal of Financial and

Quantitative Analysis 39 (4): 677.Vogt, S. C. 1994. The role of internal financial sources in firm financing and investment decisions. Review

of Financial Economics 4 (1): 1–24.Walker, M. D. 2005. Industrial groups and investment efficiency. Journal of Business 78 (5): 1973–2001.Yung, K., D-Q. D. Li, and Y. Jian. 2015. The value of corporate financial flexibility in emerging countries.

Journal of Multinational Financial Management 32–33: 25–41. Elsevier B.V.