Financial ManagementManagement text book for learning, reference book for MBA students.Text book or course book for management students. Annamalai university, India.

393

LESSON - 1 NATURE OF FINANCIAL MANAGEMENT Learning Objectives After reading this lesson you should be able to: • Know the meaning of financial management. • Identify the changes in the concept of finance. • Understand the goals of financial management. • Detail the scope of finance function. • Explain the functions of Finance Manager. Lesson Outline A. Financial Management as a branch of management B. Evolutionary changes in the concept of finance C. Definitions of Financial Management D. Goals of Financial Management E. Scope of finance function F. Functions of Treasurer and Controller G. Routine Duties of Financial Manager H. Social Responsibility of Financial Manager Finance is to business what blood is to the human body. Thus it is the lifeblood of business. Fortunately for the human body there is an automatic regulation of the quantity and quality of blood required. No such auto control is available in the case of a business firm. Hence the necessity to manage finances of that the firm may have at its disposal adequate funds of various types but at the same time avoiding idleness of funds. There was a time when it was thought that financial management consisted merely of providing funds required by the various departments or divisions of the firm. This has now changed completely and it is accepted that proper financial management consists of a dynamic approach towards the achievement of firm's objectives. A. Financial Management as a Branch of Management Of all the branches of management, financial management is of the highest importance. The primary purpose of a business firm is to produce and distribute goods and services to the society in which it exists. We need finance for the production of the goods and services as well as their distribution. The efficiency of production, personnel and marketing operations is directly influenced by the manner in which the finance function of the enterprise is performed by the finance personnel. Thus it may be stated that all

Transcript

LESSON - 1

NATURE OF FINANCIAL MANAGEMENT

Learning ObjectivesAfter reading this lesson you should be able to:

• Know the meaning of financial management.• Identify the changes in the concept of finance.• Understand the goals of financial management.• Detail the scope of finance function.• Explain the functions of Finance Manager.

Lesson Outline

A. Financial Management as a branch of managementB. Evolutionary changes in the concept of financeC. Definitions of Financial ManagementD. Goals of Financial ManagementE. Scope of finance functionF. Functions of Treasurer and ControllerG. Routine Duties of Financial ManagerH. Social Responsibility of Financial Manager

Finance is to business what blood is to the human body. Thus it is the lifeblood ofbusiness. Fortunately for the human body there is an automatic regulation of thequantity and quality of blood required. No such auto control is available in the case of abusiness firm. Hence the necessity to manage finances of that the firm may have at itsdisposal adequate funds of various types but at the same time avoiding idleness offunds. There was a time when it was thought that financial management consistedmerely of providing funds required by the various departments or divisions of the firm.This has now changed completely and it is accepted that proper financial managementconsists of a dynamic approach towards the achievement of firm's objectives.

A. Financial Management as a Branch of Management

Of all the branches of management, financial management is of the highest importance.The primary purpose of a business firm is to produce and distribute goods and servicesto the society in which it exists. We need finance for the production of the goods andservices as well as their distribution. The efficiency of production, personnel andmarketing operations is directly influenced by the manner in which the finance functionof the enterprise is performed by the finance personnel. Thus it may be stated that all

the functions or activities of the business are ultimately related to finance function. Thesuccess of the business depends on how best all these functions can be coordinated. Atree keeps itself green and growing as long as its roots sap the life juice from the soil anddistribute the same among the branches and leaves. The activities of an organisationalso keep going smoothly as long as finance flows through its veins. Any and everybusiness activity will ultimately be reflected through its finance the mirror and also thebarometer of the enterprise functions.Finance and Other Functional Areas of Management

Financial Management and Research & Development:

The R&D manager has to justify the money spent on research by coming up with newproducts and process which would help to reduce costs and increase revenue. If theR&D department is like a bottomless pit only swallowing more and more money but notgiving any positive results in return, then the management would have no choice but toclose it. No commercial entity runs an R&D department for conducting infructuousbasic research.For instance, until 5 years ago, 80% of the R&D efforts of Bush India, the 45-year oldconsumer electronics company, well known for its audio systems, was in TVs and only20% was in audio. But the fact that a 15-year stint in the TV market starting from 1981when the company shifted its interest from the audio line to TV manufacturing, led thecompany’s decline to near oblivion, pushing the once famous Bush brand name to nearanonymity, called for a change in production and re-orientation of R&D, strategy. Thecompany has also identified and shut down some of its non-productive divisions andtrimmed its workforce. At the beginning of 1992, Bush had 872 employees. By the endthis was cut down to 550. The company had to further cut it down to 450 by the end of1993.

Financial Management and Materials Management:

Likewise the materials manager should be aware that inventory of different items instores is nothing but money in the shape of inventory. He should make efforts to reduceinventory so that the funds released could be put to more productive use. At the sametime, he should also ensure that inventory of materials does not reach such a low level asto interrupt the production process. He has to achieve the right balance between toomuch inventory and too little inventory. This is called the 'liquidity-profitability trade-off' about which you will read more in the lessons on Working Capital Management.

The same is true with regard to every activity in an organisation. The results of allactivities in an organisation are reflected in the financial statements in rupees.

Financial Management and Production Management:

In any manufacturing firm, the Production Manager controls a major part of theinvestment in the form of equipment, materials and men. He should so organize hisdepartment that the equipment under his control are used most productively, theinventory of work-in-process or unfinished goods, and stores and spares is optimised

and the idle time and work stoppages are minimised. If the Production Manager canachieve this, he would be holding the cost of the output under control and thereby helpin maximizing profits. He has to appreciate the fact that whereas the price at which theoutput can be sold is largely determined by factors external to the firm like competition,government regulations etc., the cost of production is more amenable to his control.Similarly, he would have to make decisions regarding make or buy, buy or lease etc., forwhich he has to evaluate the financial implications before arriving at a decision.

Financial Management and Marketing Management:

Marketing is one of the most important areas on which the success or failure of the firmdepends to a very great extent. The philosophy and approach to the pricing policy arecritical elements in the company's marketing effort, image and sales level.Determination of the appropriate price for the firm's products is important both to themarketing and the financial managers and, therefore, should be a joint decision of both.The marketing manager provides information as to how different prices will affect thedemand for the company's products in the market and the firm’s competitive positionwhile the finance manager can supply information about costs, change in costs atdifferent levels of production, and the profit margins required to carry on the business.Thus, the finance manager contributes substantially towards formulation of the pricingpolicies of the firm.

Financial Management and Personnel Management:

The recruitment, training and placement of staff is the responsibility of the PersonnelDepartment. However, all this requires finances and, therefore, the decisions regardingthese aspects cannot be taken by the Personnel Department in an isolation of theFinance Department. Thus, it will be seen that the financial management is closelylinked with all other areas of management. As a matter of fact, the financial managerhas a grasp over all areas of the firm because of his key position. Moreover, the attitudeof the firm towards other management areas is largely governed by its financial position.A firm facing a critical financial position will devise its recruitment, production andmarketing strategies keeping the overall financial position in view. A firm having acomfortable financial position may give flexibility to the other management functions,such as, personnel, materials, purchase, production, marketing and other policies.

B. Evolutionary Change in the Concept of Finance

The word "finance" has been interpreted differently by different authorities. Moresignificantly, the concept of finance has changed markedly from time to time. For theconvenience of analysis different viewpoints on finance have been categorized into threemajor groups.

1. Finance means Cash only: Starting from the early part of the present century,finance was described to mean cash only. The emphasis under this approach is only onliquidity and financing of the firm. Since nearly every business transaction involves

cash, directly or indirectly, finance is concerned with everything that takes place in theconduct of the business. However, it must be noted that this meaning of finance is toobroad to be meaningful.

2. Finance is raising of funds: The second grouping, also called the 'traditionalapproach', is concerned with raising funds used in an enterprise. It covers, (a)instruments, institutions, practices through which funds are raised and (b) the legal andaccounting relationships between a company and its sources of funds, including theredistribution of income and assets among these sources. This concept of finance is, ofcourse, broader than the first, as it is concerned with raising of funds.

Finance, during the forties through the early fifties, was dominated by this traditionalapproach. However, it could not last for long because of some shortcomings. First, thisapproach emphasised the perspective of an outsider lender.It only analysed the firm and did not emphasis decision-making within the firm. Second,this approach laid heavy emphasis on areas of external sources of long-term finance.However, short-term finance, i.e. working capital is equally important. Third, thefunction of efficient employment of resources was totally ignored.

3. Finance is raising and utilisation of funds: The third grouping is called theIntegrated Approach or 'Modern Approach'. According to this approach, the concept offinance is concerned not only with the optimum way of raising of funds but also theirproper utilisation in time and low cost in a manner that each rupee is made to work atits optimum without endangering the financial solvency of the firm. This approach tofinance is concerned with (a) determining the total amount of funds required in thefirm, (b) allocating these funds efficiently to the various assets, (c) obtaining the bestmix of financing-type and amount of corporate securities, (d) use of financial tools toensure proper and efficient use of funds.

C. Definitions of Financial ManagementIn general, finance may be defined as the provision of money at the time it iswanted. However, as a management function it has a special meaning. Finance functionmay be defined as the procurement of funds and their effective utilisation. Some of theauthoritative definitions are as follows:

According to Ezra Solomon, "Financial management is concerned with the efficientuse of an important economic resource, namely Capital Funds".

In the words of Howard and Upton, "Finance may be defined as that administrativearea or set of administrative functions in an organisation which relate with thearrangement of cash and credit so that the organisation may have the means to carry outits objectives as satisfactorily as possible".

Phillippatus has given a more elaborate definition of the term 'financial management'.According to him "Financial management is concerned with the managerial decisionsthat result in the acquisition and financing of long-term and short-term credits for thefirm. As such it deals with the situations that require selection of specific assets (or

combination of assets), the selection of specific liability (or combination of liabilities) aswell as the problem of size and growth of an enterprise. The analysis of these decisions isbased on the expected inflow and outflow of funds and their effects upon managerialobjectives".

Financial Management may also be defined as "planning, organising, direction andcontrol of financial resources with the objectives of ensuring optimum utilisation of suchresources and providing insurance against losses through financial deadlock". Thisdefinition clearly explains four broad elements viz., planning, organising, direction andcontrol. The details under these elements are as follows:

a) Ascertainment of need Planningb) Determination of sources Planningc) Collection of funds Organizingd) Allocation of funds Organizinge) Communication of planned objective Direction

f) Monitoring of funds (though 'financial discipline' inrespect of funds utilization) Control

g) Knowing performance actuals Control

h) Judging performance against norms, standards, targetsetc. Control

i) Taking corrective action which in turn involvesremoval of snags as well as revision of targets. Control

While the functions under planning and organising are mostly of 'discrete' nature(undertaken from time to time and very often independently) those under control areaare 'continuous' in nature. All the principles, steps and weapons of managerial controlare applicable in proper control of financial resources and their utilisation. Hence, it isrightly said by Howard and Upton that financial management is an application ofgeneral managerial principles to the area of financial decision making viz., fundsrequirement decision, investment decision, financing decision and dividend decision.Hunt, William and Donaldson have rightly called it as 'Resource Management'.

Financial management is intimately interwoven into the fabric of management itself.Not only is this because the results of management's actions are expressed in financialterms, but also principally because the central role of financial management isconcerned with the same objectives as those of management itself and with the way inwhich the resources of the business are employed and how it is financed. Because it isabout making profits and profits will be determined by the way in which the resources ofthe business in terms of people, physical resources, capital, and any other specifictalents are organized.

Financial management is concerned with identifying sources of profit and the factorswhich affect profit. That is to say with operating activities in the way in which the assetsare used, and from a longer term point of view, the process of allocating funds to usewithin the business. In these activities, financial managers form part of a managementteam applying their specialist advice and processing and marshalling the data uponwhich decisions are based.

D. Goals of Financial Management

The goal of the financial management should be to achieve the objective of the businessowners, who are the suppliers of capital. In the case of company, the owners areshareholders. The financial manager’s function is not to fulfill his own objectives, whichmay include higher salaries, earning reputation, or maintaining and advancing hispersonal power and prestige. If the manager is successful in company's endeavour, hewill also achieve his personal objectives. It is generally agreed that the financialobjective of the firm should be the maximization of owner’s wealth. However, there isdisagreement as to how the economic welfare of owners can be maximized. Two wellknown and widely discussed criteria which are put forth for this purpose are: (a) profitmaximization, and (b) wealth maximization.

(a) Profit Maximization:

Traditionally, the business has been considered as an economic institution and profithas come to be accepted as a rationally valid criterion of measuring efficiency. As a goal,however, profit maximization suffers from certain basic weaknesses:

- it is vague,

- it is a short-run point of view,

- it ignores risks, and

- it ignores the timing of returns.

Please use headphones

An unambiguous meaning of the profit maximization objective is neither available norpossible. It is rather very difficult to know about these: Does it mean short-term profitsor long-term profits? Does it refer to profit before or after tax? Does it refer to totalprofits or profit per share?

Besides it being ambiguous, the profit maximization objective takes a short-run point ofview. Professor Drucker and Professor Galbraith contradict the theory of profitmaximization and observe that exclusive attention on profit maximization misdirectsmanagers to the point where they may endanger the survival of the business. Prof.Galbraith gives the following points to argue his line of reasoning: (1) it undermines thefuture for today’s profit; (2) it shortchanges research promotion and other investments;(3) it may shy away from any capital expenditure that may increase the invested capitalbase against which profits are based, and the result is dangerous obsolescence ofequipment. In other words, the managers are directed into the worst practices ofmanagement. Risk and timing factors are also ignored by this objective. The streams ofbenefits may possess different degrees of certainty and uncertainty. Two firms may havesame total expected earnings, but if the earnings of one firm fluctuate considerably ascompared to the other, it will be more risky. Also, it does not make a difference betweenreturns received in different time periods i.e., it gives no consideration to the time valueof money and value benefits received today and benefits after six months or oneyear. For these reasons, the profit maximization objective cannot be taken as theobjective of financial management.

(b) Wealth Maximization:

The maximization of wealth is a more viable objective of financial management. Thesame objective, if expressed in other terms, would convey the idea of net present worthmaximization. Any financial action which creates wealth or which has a net presentworth is a desirable one and should be undertaken. Wealth of the firm is reflected in themaximization of the present value of the firm i.e., the present worth of the firm. Thisvalue may be readily measured if the company has shares that are held by the public,because the market price of the share is indicative of the value of the company. And to ashareholder, the term ‘wealth’ is reflected in the amount of his current dividends and themarket price of share. Ezra Solomon has defined wealth maximization objective in thefollowing manner:

"The gross present worth of a course of action is equal to the capitalized value of the flowof future expected benefits, discounted (or capitalized) at a rate which reflects thecertainty or uncertainty. Wealth or net present worth is the difference between grosspresent worth and the amount of capital investment required to achieve the benefits."

From the above clarification, one thing is certain that the wealth maximization is a long-term strategy that emphasises raising the present value of the owner's investment in acompany and the implementation of projects that will increase the market value of thefirm's securities. This criterion, if applied, meets the objections raised against earliercriterion of profit maximization. The financial manager also deals with the problem of

uncertainty by taking into account the trade-off between the various returns andassociated levels of risks. It also takes into account the payment of dividends toshareholders. All these ingredients of the wealth maximization objective are the result ofthe investment, financing and dividend decisions of the firm.

Please use headphones

E. Scope of finance functionThe question of 'scope of finance function' determines the decisions or functions to becarried out by the financial manager in pursuit of achieving the objective of wealthmaximization. The various functions of the financial manager relate to the estimation offinancial requirements, investment of funds in long-term and short-term assets,determining the appropriate capital structure, identification of the various sources offinance, decision regarding retention of earnings and distribution of dividend, andadministering proper financial controls. These decisions have been categorized into twobroad groupings:

(1) Long-term financial decisions:

The long term financial decisions pursued by the financial manager have significant longterm effects on the value of the firm. The results of these decisions are not confined to afew months but extend over several years and these decisions are mostly irreversible. Itis, therefore, necessary that before committing the scarce resources of the firm a carefulexercise is done with regard to the likely costs and benefits of various decisions like...

i. Investment Decision (capital allocation for fixed and currentassets): Investment decision (also known as capital-budgeting decision) is concernedwith the allocation of given amount of capital to fixed assets of the business. Theimportant characteristic of fixed assets is that their benefits are realized in the future(generally after one year). Thus, capital-budgeting decision adds to the total fixed assetsof the concern by selecting and investing in new investments. lt must be properlyunderstood at this stage that because the future benefits are not known with certainty,investment proposals necessarily involve risk. Consequently, they must be evaluated inrelation to their expected income and risk they add to the function as a whole.Obviously, the management will select investments adding something to the value of thefirm. The criteria of judging the profitability of projects is the difference between thecost of the investment proposals and its expected earnings. The important methodsemployed to judge the profitability of the investment proposals are:

(a) Payback method, (b) Average rate of return method, (c) Internal rate of returnmethod, and (d) Net present value method.

A careful employment of these methods helps in determining the contribution ofinvestment projects to owners' wealth.

ii. Financing Decision (capital sourcing): Financing decision (also known ascapital structure decision) is intimately tied with the investment decision. To undertakeinvestment decision the firm needs proper finance. The solution to the question ofraising finance is solved by financing decision. There are number of sources from whichfunds can be raised. The most important sources of financing are equity capital and debtcapital. The central tasks before the financial manager is to determine the proportion ofequity capital and debt capital. He must endeavour to obtain a financing mix or optimalcapital structure for the firm where overall cost of capital is the minimum or the value ofthe firm is maximum. In taking this decision, the financial manager must bear in mindthe likely effects on shareholders and the firm. The use of debt capital, for instance,affects the return and risk of the shareholders. Not only the return on equity willincrease, but also the risk. A proper balance will have to be struck between return andrisk. When the shareholder's return is maximized with minimum risk, the market valueper share will be maximized and firm's capital structure would be optimum. Once thefinancial manager is able to determine the best combination of debt and equity, he mustraise this appropriate amount through best available sources.

Fig. 1.1 Decisions, Return, Risk, and Market Value

iii. Dividend Decision: The next crucial financial decision is the dividend decision.This decision is the basis of dividends payment policy, reserves policy, etc. Thedividends are generally paid as some percentage of earnings on the paid-up capital.However, the policy pursued by management concerning dividends payment isgenerally stable in character. Stable dividends policy implies the payment of sameearnings percentage with only small variations depending upon the pattern of earnings.The stable dividends policy among other things, increases the market value of the share.The amount of undistributed profits is called 'retained earnings'. In other words,dividends payout ratio determines the amount of earnings retained in the firm. Theamount of earnings or profit to be kept undistributed with the firm must be evaluated inthe light of the objective of maximizing shareholders' wealth.

(2) Short-Term Financial Decisions (Working capital management):

i. cash,

ii. investments (marketable securities),

iii. receivables, and

iv. inventory

The job of the financial manager is not just limited to the long-term financial decisions,but also extends to the short-term financial decisions aiming at safeguarding the firmagainst illiquidity or insolvency. Surveys indicate that the largest portion of a financial

manager's time is devoted to the day-to-day internal operations of the firm; this may beappropriately subsumed under the heading Working Capital Management. Workingcapital management requires the understanding and proper appreciation of its twoconcepts - gross and net working capital. Gross working capital refers to the firm'sinvestment in current assets such as cash, short-term securities, debtors, bills receivableand inventories. Current assets have the distinctive characteristics of being convertibleinto cash within an accounting year. Net working capital refers to the difference betweencurrent assets and current liabilities. Current liabilities are those claims of outsiderswhich are expected to mature for payment within an accounting year and include tradecreditors, bills payable, bank overdraft and outstanding expenses. For the financialmanager both these concepts of gross and net working capital are relevant.

Investment in current assets affects firm's profitability, liquidity and solvency. In orderto ensure that neither insufficient nor unnecessary funds are invested in current assets,the financial manager should develop sound techniques of managing current assets. Heshould estimate firm's working capital needs and make sure that funds would be madeavailable when needed.

The cost of capital acts as the core in the framework for financial management decisionmaking. In has a two-way effect on the investment, financing and dividend decisions. Itinfluences and is in turn influenced by them. The cost of capital leads to the acceptanceor rejection of projects, as it is the cut-off criterion in investment decisions. In turn, the

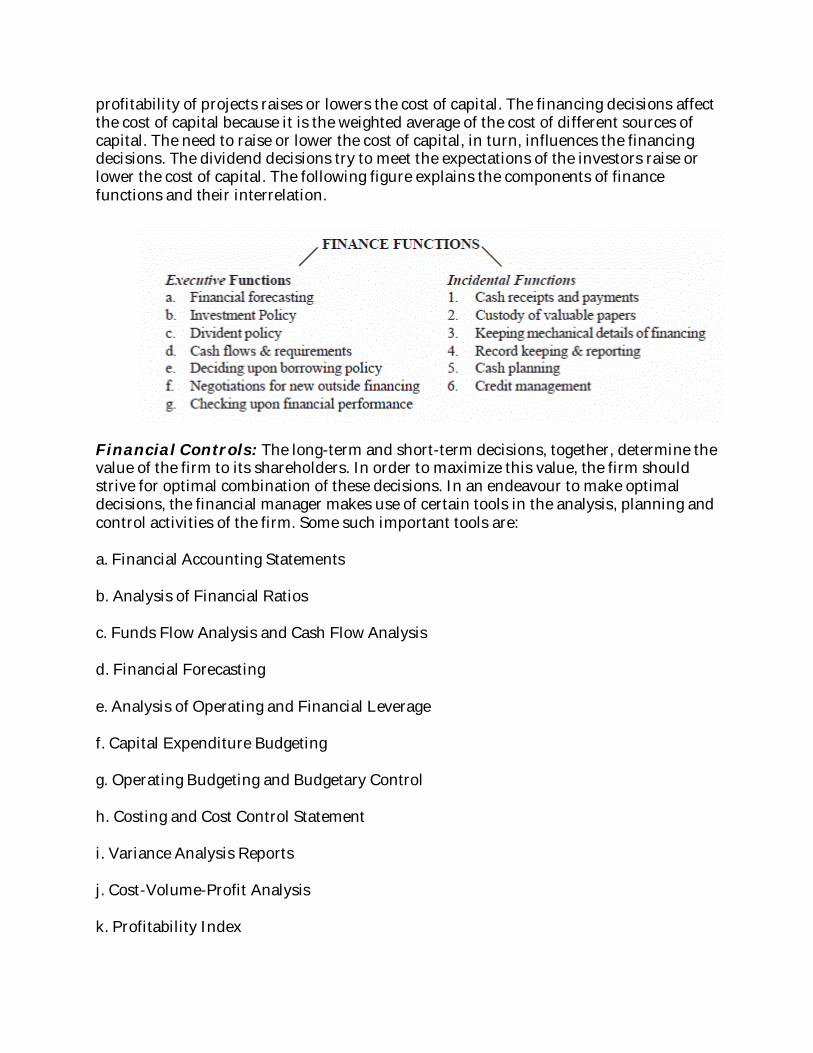

profitability of projects raises or lowers the cost of capital. The financing decisions affectthe cost of capital because it is the weighted average of the cost of different sources ofcapital. The need to raise or lower the cost of capital, in turn, influences the financingdecisions. The dividend decisions try to meet the expectations of the investors raise orlower the cost of capital. The following figure explains the components of financefunctions and their interrelation.

Financial Controls: The long-term and short-term decisions, together, determine thevalue of the firm to its shareholders. In order to maximize this value, the firm shouldstrive for optimal combination of these decisions. In an endeavour to make optimaldecisions, the financial manager makes use of certain tools in the analysis, planning andcontrol activities of the firm. Some such important tools are:

a. Financial Accounting Statements

b. Analysis of Financial Ratios

c. Funds Flow Analysis and Cash Flow Analysis

d. Financial Forecasting

e. Analysis of Operating and Financial Leverage

f. Capital Expenditure Budgeting

g. Operating Budgeting and Budgetary Control

h. Costing and Cost Control Statement

i. Variance Analysis Reports

j. Cost-Volume-Profit Analysis

k. Profitability Index

l. Financial Reports

Organisation for Finance Function: Almost anything in the financial realm fallswithin such a committees realm, including questions of financing, budgets,expenditures, dividend policy, and future planning. Such is the power of financialcommittee that in most cases their recommendations are approved as a matter of courseby the full board of directors.

On the operational level, the financial management team may be headed up by afinancial Vice President. This is a recent development; the financial Vice Presidentanswers directly to the President. Serving under him are Treasurer and Controller. Anillustrative organisation chart of finance function of management in a large organisationis given below:

VP Mktg VP Purchase VP Production VP Finance VPPersonnel

|

-------------------------

| |

Treasurer Controller

Fig. 1.3 Organization Chart of Finance Functions of Management

The chart below shows that the Vice President Finance exercises his function throughhis two deputies known as 'Controller' concerned with internal matters, and 'Treasurer'who basically handles external financial matters.

The Controller is concerned with the management and control of the firm's assets. Hisduties include providing information for formulating the accounting and financialpolicies, preparation of financial reports, direction of internal auditing, budgeting,inventory control, taxes, etc. The Treasurer is mainly concerned with management ofthe firm's funds. His duties include forecasting the financial needs, administering theflow of cash, managing credit, floating securities, maintaining relations with financialinstitutions, and protecting funds and securities. A brief description of the functions ofthe Controller and the Treasurer, as given by the Controllers Institute of America, isgiven below and in Fig. 1.4.

F. Functions of Controller and Treasurer

Functions of Controller:

1. Planning and Control: To establish, coordinate and administer, as part ofmanagement, a plan for the control of operations. This plan would provide to theextent required in the business, profit planning, programmes for capital investingand for financing, sales forecasts and expense budgets.

2. Reporting and Interpreting: To compare actual performance withoperating plans and standards, and to report and interpret the results ofoperations to all levels of management and to the owners of business. To consultwith the management about the financial implications of its actions.

3. Tax Administration: To establish and administer tax policies andprocedures.

4. Government Reporting: To supervise or coordinate the preparation ofreports to government agencies.

5. Protection of Assets: To ensure protection of business assets throughinternal control, internal auditing and assuring proper insurance coverage.

6. Economic Appraisal: To appraise economic and social forces andgovernment influences and interpret their effect upon business.

Functions of Treasurer:

1. Provision of Finance: To establish and execute programmes for theprovision of the finance required by the business, including negotiating itsprocurement and maintaining the required financial arrangements.

2. Investor Relations: To establish and maintain adequate market for thecompany's securities and to maintain adequate contact with the investmentcommunity.

3. Short-term Financing: To maintain adequate sources for the company'scurrent borrowings from the money market.

4. Banking and Custody: To maintain banking arrangements, to receive, havecustody of and disburse the company's moneys and securities and to beresponsible for the financial assets of real estate transactions.

5. Credit and Collections: To direct the granting of credit and the collection ofaccounts receivables of the company.

6. Investments: To invest the company's funds as required, and to establish andcoordinate policies for investment in pension and other similar trusts.

7. Insurance: To provide insurance coverage as may be required.

Another way of looking at these functions is...

The Controller function generally concentrates on the asset side of the balance sheet,while the Treasurer function concentrates on the claims side i.e., identifying the bestsources of finance to utilize in the business and timing the acquisition of funds.Controller's and Treasurer's Functions in the Indian Context:

The terms 'controller' and 'treasurer' are essentially used in U.S.A. However, this patternis not popular in India. Some companies do use the term 'Controller' for the official whoperforms the functions of the chief accountant or the management accountant.However, in most cases, in case of Indian companies, the term General Manager(Finance) or Chief Finance Manager is more popular. Some of the functions of theController and the Treasurer such as government reporting, insurance coverage, etc.,are taken care of by the Secretary of the company. The Treasurer's function ofmaintaining relations with its investors is also not much relevant in the Indian contextsince by and large Indian investors/shareholders are indifferent towards attending the

general meetings. The finance manager in Indian companies is mainly concerned withthe management of the firm's financial resources. His duties are not compounded withother duties generally in large companies. It is a healthy sign since the management offinances is an important business activity requiring extraordinary skill and attention. Hehas to ensure that the scarce financial resources are put to the optimum use keeping inview various constraints. It is, therefore, necessary that the finance manager devotes hisfull time attention and energies only in raising and utilising the financial resources ofthe firm.

G. Routine Duties of Financial ManagerApart from the three broad functions of financial management mentioned above, thefinancial manager has to perform certain routine or recurring functions as these:

(i) Keeping track of actual and projected cash outflows and making adequate provisionin time for any shortfall that may arise.

(ii) Managing of cash centrally and supplying the needs of various divisions anddepartments without keeping idle cash at many points.

(iii) Negotiations and relations with banks and other financial institutions.

(iv) Investment of funds available and free for a short period.

(v) Keeping track of stock exchange prices in general and prices of the company's sharesin particular.

(vi) Maintenance of liaison with production and sales departments for seeing thatworking capital position is not upset because of inventories, book debts, etc.

(vii) Keeping management informed of the financial implication of variousdevelopments in and around the company.Non-Routine Duties:

The non-recurring duties of the financial executive may involve preparation of financialplan at the time of company promotion, expansion, diversification, readjustments intimes of liquidity crisis, valuation of the enterprise at the time of acquisition and mergerthereof, etc. Today's financial manager has to deal with a variety of developments thataffect the firm's liquidity and profitability, including...

(i) High financial cost identified with risk-bearing investments in a capital-intensiveenvironment.

(ii) Diversification by firms into differing businesses, markets, and product lines.

(iii) High rates of inflation that significantly affect planning and forecasting the firmsoperations.

(iv) Emphasis on growth, with its requirements for new sources of funds and improveduses of existing funds.

(v) High rates of change in technology, with an accompanying need for expenditures onresearch and development.

(vi) Speedy dissemination of information, employing high speed computers andnationwide and worldwide networks for transmitting financial and operating data.

H. Social Responsibility of Financial Manager

Another point that deserves consideration is social responsibility: should businessesoperate strictly in the stockholder's best interest, or are firms also partly responsible forthe welfare of society at large? In tackling this question, consider first the firms whoserates of return on investment are close to normal, that is, close to the average for allfirms. If such companies attempt to be socially responsible, thereby increasing theircosts over what they otherwise would have been, and if the other business in theindustry do not follow suit, then the socially oriented firms will probably be forced toabandon their efforts. Thus , any socially responsible acts that raise costs will bedifficult, if not impossible, in industries subject to keen competition.

What about firms with profits above normal levels - can they not devote resources tosocial projects? Undoubtedly they can many large, successful firms do engage incommunity projects, employee benefit programmes, and the likes to a greater degreethan would appear to be called for by pure profit or wealth maximization. Still, publiclyowned firms are constrained in such actions by capital market factors. Suppose a saverwho has funds to invest is considering two alternative firms. One firm devotes asubstantial part of its resources to social actions, while the other concentrates on profitsand stock prices. Most investors are likely to shun the socially oriented firm, which willput it to a disadvantage in the capital market. After all, why should the stockholders ofone corporation subsidise society to a greater extent than stockholders of otherbusinesses? Thus, even highly profitable firms (unless they are closely held rather thanpublicly owned) are generally constrained against taking unilateral cost increasing socialaction.Does all this mean that firms should not exercise social responsibility? Not at all - itsimply means that most cost-increasing actions may have to be put on a mandatoryrather than a voluntary basis, at least initially, to insure that the burden of such actionfalls uniformly across all businesses. Thus, fair hiring practices, minority trainingprogrammes, product safety, pollution abatement, antitrust actions, and are more likelyto be effective if realistic rules are established initially and enforced by governmentagencies. It is critical that industry and government cooperate in establishing the rulesof corporate behavior and that firms follow the spirit as well as the letter of the law intheir actions. Thus, the rules of the game become constraints, and firms should strive tomaximize stock prices subject to these constraints.

REVIEW QUESTIONS

1. "Finance is the oil of wheel, marrow of bones and spirit of trade, commerce andindustry"- Elucidate.2. Discuss the role and significance of financial management in the functional areas ofmodern management.

3. Some of the early concerns of financial management are related to preservation ofcapital, maintenance of liquidity and reorganisation. Do you think these topics are stillimportant in our current unpredictable economic environment?

4. Who discharges the finance function and what are his specific responsibilities?

5. Contrast profit maximization and value maximization as criteria for financialmanagement decisions in practice.

6. Why is it inappropriate to seek profit maximization as the goals of financial decisionmaking? How do you justify the adoption of present value maximization as an aptsubstitute for it?

7. "The operative objective of financial management is to maximize wealth or netpresent worth'- Ezra Solomon. Explain the statement and explain the finance functionperformed by a Finance Manager to achieve this goal.

8. Explain the scope of finance function and suggest an organisational structure that youconsider suitable for an effective financial control of a large manufacturing concern.

9. Discuss the respective roles of 'Treasurer' and 'Controller' in the financial set-up of alarge corporation. Out of these two finance officers who is more important in themodern contest and why?10. As a Financial Manager of a company, how would you reconcile between financialgoals and social objectives of the concern?

SUGGESTED READINGS

1. Chandra, Prasanna: Fundamentals of Financial Management, New Delhi, TataMcGraw Hill Co.2. Hampton, J.J.: Financial Decision Making, New Delhi, Prentice Hall of India.

3. Pandey, I.M.: Financial Management, New Delhi, Vikas Publishing House.

4. Van Home, James C : Financial Management and Policy, New Delhi, Prentice Hall ofIndia.

- End of Chapter -

LESSON - 2

WORKING CAPITAL MANAGEMENT

Learning Objectives

After reading this lesson you should be able to:

• Understand the concept of working capital• Classify the different types of working capital• Recognize the element of working capital• Assess the requirements of working capital• Identify the strength and weakness of inadequate or excess working capital.

Lesson Outline

A. Concept of Working CapitalB. Classification of Working CapitalC. Elements of Working CapitalD. Assessment of Working Capital RequirementsE. Problems of inadequacy of Working CapitalF. Reasons for inadequacy of Working CapitalG. Excessive Working CapitalH. Principles of Working Capital

Proper management of working capital is very important for the success of anenterprise. It aims at protecting the purchasing power of assets and maximising thereturn on investment. Constant management is required to maintain appropriate levelsin the various working capital components. Sales expansion, dividend declaration, plantexpansion, new product line, increased salaries and wages, rising price levels etc. putadded strain on working capital maintenance. Failure of business is undoubtedly due topoor management and absence of a management skill. Shortage of working capital, sooften advanced as the main cause for failure of concerns, is nothing but the clearestevidence of mismanagement which is so common.

Please use headphones

It has been found that the major portion of a financial manager's time is utilized in themanagement of working capital. Current assets account for a very large portion of thetotal investment of a firm. In some of the industrial current assets on an averagerepresent over three-fifth of the total assets. In the case of trading concerns they accountfor about 80 percent. A firm may, sometimes, be able to reduce the investment in fixedassets by renting or leasing plant and machinery. But it cannot avoid investment in cash,accounts receivable and inventory. The management of working capital also helps themanagement in evaluating various existing or proposed financial constraints andfinancial offerings. All these factors clearly indicate the importance of working capitalmanagement in a firm.

A. Concepts of Working Capital

There are two concepts regarding the meaning of Working Capital - Net working Capitaland Gross Working Capital. According to one school of thought (supported bydistinguished authorities like Lincoln, Doris, Stevens and Saliers), Working Capital isthe excess of Current Assets over Current Liabilities, as designated in the followingequation:

Working Capital = Current Assets — Current Liabilities

According to another school of thought (supported by authorities like Mead Baker,Mallot and Field), Working Capital represents only the current (capital) assets.

There is basis for both these contentions. To understand them, correct conception ofcurrent assets and liabilities is essential.

Current Assets are those assets that in the ordinary course of business can be or willbe turned into cash within a brief period (not exceeding one year, normally) withoutundergoing diminution of value and without disrupting the organisation. Examples ofcurrent assets are:

(i) Cash in hand and in bank;

(ii) Accounts receivable from customers (less reserves);

(iii) Promissory Notes and Bills receivable from customers (less reserves);

(iv) Inventories comprising of raw material, work-in-progress, finished goods (ofmanufactures)

(v) Marketable securities held as temporary investment;

(vi) Prepaid expenses;

(vii) Maintenance materials;

(viii) Accrued income.

Current Liabilities are those liabilities intended at their inception to be paid inordinary course of business within a reasonable short time (normally within a year) outof the current assets or by creating another current liability or the income of thebusiness. Its examples are:

(i) Accounts payable to creditors;

(ii) Notes or Bills payable;

(iii) Accrued expenses, such as accrued taxes, salaries and interest;

(iv) Bank over-draft, cash credit;

(v) Bonds to be paid within one year;

(vi) Dividends declared and payable.

The arguments of the first school of thought in regarding working capital as the excessof current assets over current liabilities are that:

1. It is an established definition of working capital which is in use since long;

2. This concept of working capital enables the shareholders to judge the financialsoundness of the concern and the extent of protection afforded to them. It is particularlybecause with an increase in short-term borrowings the working capital does notincrease; it will increase only by following the policy of ploughing back of profits orconversion of fixed assets into liquid assets or by procuring fresh capital fromshareholders;

3. Any concern with an excess of current liabilities can successfully tide over periods ofemergency, e.g., depression;

4. Further, there is no obligation on the part of the company to return the amountinvested by the shareholders;

5. Such a definition is of great use in ascertaining the true financial position ofcompanies having current assets of similar amount.

Those who regard working capital and current assets as synonymous advance thefollowing arguments in support of their contention:

1. Earnings in each enterprise are the outcome of both fixed as well as current assets.Individually these assets have no significance. The points of similarity in these assets arethat both are borrowed and they yield profit much more than the interest cost. But thedistinction in the two lies in the fact that fixed assets constitute the fixed capital of acompany, whereas current assets are of a circulating nature. Hence, logic demands thatcurrent assets should be considered as the working capital of the company;

2. This definition takes into consideration the fact that there would be an automaticincrease in the working capital with every increase in the funds of the company; but it isnot so according to the net concept of working capital;

3. Every management is interested in the total current assets out of which the operationof an enterprise is made possible, rather than in the sources from where the capital isprocured;

4. The former concept of working capital may hold good only in the case of sole trader orpartnership organisation; but under the modern age of company organisation, wherethere is divorce between ownership, management and control, the ownership of currentor fixed assets is of little significance.

B. Classification of Working Capital

Generally speaking, the amount of funds required for operating needs varies from timeto time in every business. But a certain amount of assets in the form of working capitalare always required, if a business has to carry out its functions efficiently and without abreak. These two types of requirements, permanent and variable, are the basis for aconvenient classification of working capital:

1. Permanent or Fixed Working Capital:

As is apparent from the adjective 'permanent' it is that part of the capital which ispermanently locked up in the circulation of current assets and in keeping it moving. Forexample, every manufacturing concern has to maintain stock of raw materials, works-in-progress (work-in-process), finished products, loose tools, and spare parts. It alsorequires money for the payment of wages and salaries throughout the year. Thepermanent or fixed working capital can again be subdivided into

(i) Regular Working Capital

It is the minimum amount of liquid capital needed to keep up the circulation of thecapital from cash to inventories to receivables and back again to cash. This wouldinclude a sufficient cash balance in the bank to discount all bills, maintain an adequatesupply of raw materials for processing, carry a sufficient stock of finished goods to giveprompt delivery and effect the lowest manufacturing costs, and enough cash to carry thenecessary accounts receivables for the type of business engaged in.

(ii) Reserve Margin or Cushion Working Capital

It is the excess over the need for regular working capital that should be provided forcontingencies that arise at unstated periods. The contingencies included

(a) raising prices, which may make it necessary to have more money to carryinventories and receivables, or may make it advisable to increase inventories;

(b) business depressions, which may raise the amount of cash required to ride outof usually stagnant periods;

(c) strikes, fires and unexpectedly severe competition, which use up extra suppliesof cash; and

(d) special operations, such as experiments with new products, or with newmethod of distribution, war contracts, contractors to supply new businesses, andthe like, which can be undertaken only if sufficient funds are available, and whichin many cases mean the survival of a business.

2. Temporary or Variable Working Capital: The variable working capital changeswith the volume of business. It may be subdivided into

(i) Seasonal Working Capital: In many lines of business (e.g. jaggery or sugar and furindustry operations are highly seasonal and, as a result, working capital requirementsvary greatly during the year. The capital required to meet the seasonal needs of industryis termed as Seasonal Working Capital.

(ii) Special Working Capital: Special Working Capital is that part of the variable workingcapital which is required for financing special operations, such as the inauguration ofextensive marketing campaigns, experiments with new products or with new methods of

distribution, carrying out of special jobs and similar to the operations that are outsidethe usual business of buying, fabricating and selling.

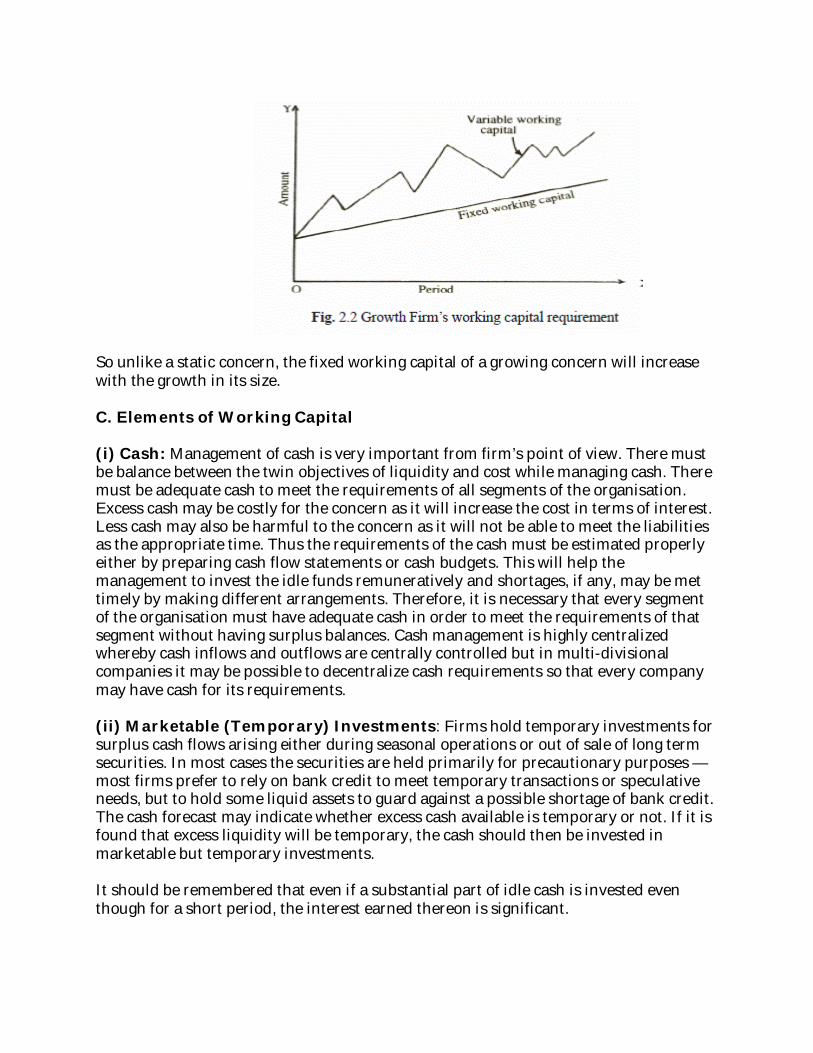

This distinction between permanent/fixed and temporary/variable working capital is ofgreat significance particularly in arranging the finance for an enterprise. Regular orfixed working capital should be raised in the same way as fixed capital is procured -through a permanent investment of the owner or through long-term borrowing. Asbusiness expands, this regular capital will necessarily expand. If the cash returning fromsales includes a large enough profit to take care of expanding operations and growinginventories, the necessary additional working capital may be provided by the earnedsurplus of the business. Variable needs can, however, be financed out of short-termborrowings from banks or from public in the form of deposits. The position with regardto the 'fixed working capital' and 'variable working capital' can be shown with the help ofthe following figures:

From the above figure it should not be presumed that permanent working capital shallremain fixed throughout the life of the concern. As the size of the business grows,permanent working capital too is bound to grow. The position can be depicted with thehelp of the following figure:

So unlike a static concern, the fixed working capital of a growing concern will increasewith the growth in its size.

C. Elements of Working Capital

(i) Cash: Management of cash is very important from firm’s point of view. There mustbe balance between the twin objectives of liquidity and cost while managing cash. Theremust be adequate cash to meet the requirements of all segments of the organisation.Excess cash may be costly for the concern as it will increase the cost in terms of interest.Less cash may also be harmful to the concern as it will not be able to meet the liabilitiesas the appropriate time. Thus the requirements of the cash must be estimated properlyeither by preparing cash flow statements or cash budgets. This will help themanagement to invest the idle funds remuneratively and shortages, if any, may be mettimely by making different arrangements. Therefore, it is necessary that every segmentof the organisation must have adequate cash in order to meet the requirements of thatsegment without having surplus balances. Cash management is highly centralizedwhereby cash inflows and outflows are centrally controlled but in multi-divisionalcompanies it may be possible to decentralize cash requirements so that every companymay have cash for its requirements.

(ii) Marketable (Temporary) Investments: Firms hold temporary investments forsurplus cash flows arising either during seasonal operations or out of sale of long termsecurities. In most cases the securities are held primarily for precautionary purposes —most firms prefer to rely on bank credit to meet temporary transactions or speculativeneeds, but to hold some liquid assets to guard against a possible shortage of bank credit.The cash forecast may indicate whether excess cash available is temporary or not. If it isfound that excess liquidity will be temporary, the cash should then be invested inmarketable but temporary investments.

It should be remembered that even if a substantial part of idle cash is invested eventhough for a short period, the interest earned thereon is significant.

(iii) Receivables: Management of receivables involves a trade-off between the gainsdue to additional sales on account of liberal credit facilities and additional cost ofrecovering those debts. If liberal credit facilities are given to the customers, sales willdefinitely increase. But on the other hand bad debts, collection expenses and interestcharge will increase. Similarly if the credit policy is strict, the sales will be less andcustomers may go to the competitors where liberal credit facilities are available. Thiswill result in loss of profit because of less sales but there will be saving because of lessbad debts, collection and interest charges. Management of debtors also covers analysisof the risks associated with advancing credit to a particular customer. Follow up ofdebtors and credit collection are the remaining aspects of receivables management.

(iv) Inventories: Inventories include all investments in raw materials, work-in-progress, stores, spare parts and finished goods; they constitute an important part of thecurrent assets. The purchase of inventory involves investment which must be properlycontrolled. There are many issues of inventory management which must be taken intoconsideration as fixation of minimum and maximum level, deciding the issue of pricingpolicy, setting up the procedures for receipts and inspection, determining the economicordering quantity, providing proper storage facilities, keeping control on obsolescenceand setting up an effective information system with reference to inventories. Inventorymanagement requires the attention of stores manager, production manager andfinancial manager. There must be adequate inventories in order to avoid thedisadvantages of both inadequate and excessive inventories.

(v) Creditors: Management of creditors is very important aspect of working capital. Ifthe payment of creditors is delayed there is a possibility of saving of some interest but itcan be very costly because it will spoil the goodwill of the concern in the market. As faras possible, the credit manager should try to get the liberal credit terms so that paymentmay be made at the stipulated time.

D. Assessment of Working Capital Requirements

The following factors are considered for a proper assessment of the quantum of workingcapital requirements:

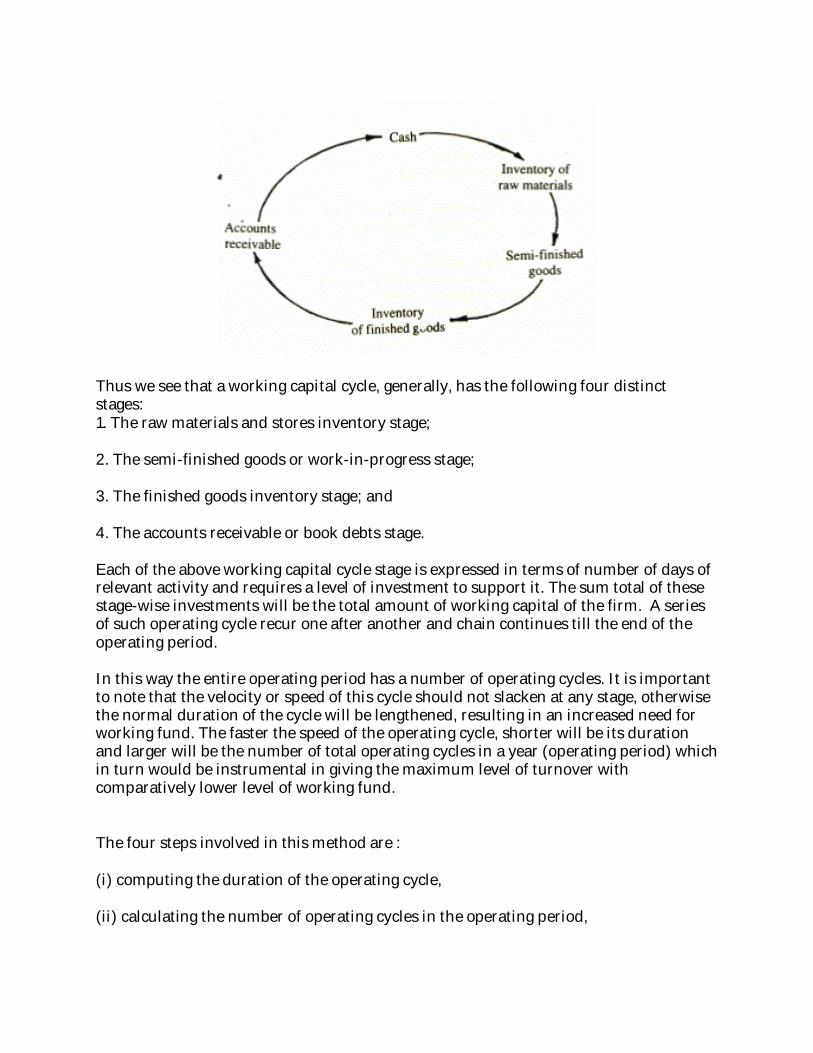

(i) The Production Cycle: There is bound to be time span in raw materials input inmanufacturing process and the resultant output as finished product. To sustain suchproduction activities the requirement of investment in the form of working capital isobvious. The lesser the production cycle (or the operating cycle) the lesser will be therequirements of working capital. There are enterprises due to their nature of businesswill have shorter cycle than others. Further, even within the same group of industries,the more the application of technological advances in, will result in shortening theoperating cycle. In this context the choice of product requiring shorter or greateroperating cycle will have a direct impact on the working capital requirements. This is afactor of paramount importance irrespective of whether a new industry is venturingproduction of the first time or an ongoing business. Hence it can be said that the timespan for each stage of the process of manufacture if geared to improve upon will lead tobetter efficiency and utilisation of working capital.

(ii) Work-in-Process: A close attention is to be given to the accumulation of work-in-progress or work-in-process. Unless the sequences of production process leading toconversion into finished product is kept under close observation to achieve betterproduction and productivity, more and more working capital funds will be tied up. Inthis context, proper production planning and control is vital.

(iii) Terms of Credit from Suppliers of Materials & Services: The more theterms of credit is favourable i.e. the more the time allowed by the creditors to pay them,the lesser will be the requirement of working capital. Hence, the negotiation with thesuppliers in respect of price and the credit period is an important aspect in workingcapital management. In this process the impact of the requirement of finance is sharedby the creditors for goods and services.

(iv) Realisation from Sundry Debtors: The lesser the time span between sellingthe product and the realisation, the quicker will be the inflow of cash. This, in turn, willreduce the finance required for working capital purposes. A realistic credit control willreduce locking up of finance in the form of sundry debtors. The impact of betterrealisation will not only help in reducing the working capital fund requirement but alsocan boost up the finance needed for other operational needs. The important factors incredit control will be: (a) volume of credit sales desired; (b) terms of sales and (c)collection policy.

(v) Control on Inventories: The decision to maintain appropriate minimuminventories either in the form of raw material, stores materials, work-in-process orfinished products is an important factor in controlling finance locked up. The better thecontrol on inventories the lesser will be the requirements of working capital. Thefollowing vital factors involved in inventory management are to be considered for aneffective inventory control: (a) volume of sales, (b) seasonal variation in sales, (c) sellingoff the shelf, (d) stocking to gain from higher price under inflationary conditions, (e) theoperating cycle, i.e., the time interval between manufacturing, selling and realisation,and (f) safety or buffer stock. A minimum policy level of stock may have to bemaintained to seize the opportunity of selling when there is spark in demand for theproduct.

(vi) Liquidity versus Profitability: The management dilemma as to the optimalbalancing between liquidity (or solvency) and the profitability is another factor of greatimportance on the determination of the level of working capital requirement. In otherwords, the level of liquidity and the profitability is to be maintained according to thegoals of financial management.

(vii) Competitive Conditions: The whole question of cash inflow depends as to thequickness in selling the products and the realisation thereof. In this context, the natureof business and the product will be the two important contributory factors as to thepolicy on the quantum of working capital requirements.

(viii) Inflation and the Price Level Changes: In an inflationary trend, the impacton working capital is that more finance is needed for the same volume of activity i.e.,

one has to pay more price for the purchase of same quantity of materials or services tobe obtained. Such raising impact of prices can be fully or partly compensated byincreasing the selling price of the product. All business may not be in a position to do sodue to their nature of product, competitive market, or Government’s regulatory prices.

(ix) Seasonal Fluctuation and Market Share of Product: There are productswhich are mostly in demand in certain periods of the year. In other words, there maynot be any sale or only a fraction of the total sale in off-season due to seasonal nature ofdemand for the product. There may be shifting of demand due to better substitute of theproduct available. This means the company affected by this economics, attempts to plandiversification to sustain profit, expansion and growth of the business. In certainbusinesses, demands for products are of seasonal in nature and for certain businesses,the raw materials buying have to be done during certain seasonal timings. Naturally theworking capital requirement will be more in certain periods than in others.

Please use headphones

(x) Management Policy on Profits, Retained Profit, Tax Planning andDividend Policy: The adequacy of profit will lead to strengthening the financialposition of the business through cash generation which will be ploughed back as internalsource of financing. Tax planning is an integral part of working capital planning. It isnot only the question of quantum of cash availability for tax payment at the appropriatetime but also through tax planning the impact of tax payable can be reduced. DividendPolicy considers the percentage of dividend to be paid to the shareholders as interimand/or final dividend. There must be cash available at the appropriate time after thedividend is declared. This way the dividend payment is connected with working capitalmanagement.

(xi) Terms of Agreement: It refers to the terms and conditions of agreement to repayloans taken from bankers and financial institutions and acceptance of ‘fixed deposits’from public. The question of fund arrangement whether for working capital needs or tolong term loans is to be decided after taking into account the repayment ability. Thecash flow projection will have to be made accordingly.

(xii) Cash (Flow) Budget: In order to meet certain cash contingencies it may benecessary to have liquidity in form of marketable securities as cash reservoir. This extracash reserve may remain as an idle fund. This type of cash reserve is necessary to meetemergency disbursements.

(xiii) Overall Financial and Operational Efficiency: A professionally managedcompany always applies appropriate tools and techniques to achieve efficiency andutilisation of working capital fund. Adequacy of assessment and control of business willlead to improve the 'working capital turnover'. Management also will have to keep itselfabreast of the environmental, technological and other changes affecting the business sothat an effective and efficient financial management can play a vital role in reducing theproblems of working capital management.

(xiv) Urgency of Cash: In order to avoid product becoming obsolete or to undercutthe competitors to hold the market share or in case of emergency for cash funds, it maybe necessary to sell out products at a cheaper rate or at a discount or allowing cashrebate for early realisation from sundry debtors (customers). This situation may boostup the cash availability. However, this sort of critical situation should be avoided as thisresults in reducing profit.

(xv) Importance of Labour Mechanisation: Capital intensive industries, i.e.mechanized and automated industries, will require lower working capital, while labourintensive industries such as small scale and cottage industries will require largerworking capital.

(xvi) Proportion of Raw Material to Total Costs : If the raw materials are costly,the firm may require larger working capital, while if raw materials are cheaper andconstitute a small part of the total cost of production, lower working capital is required.

(xvii) Seasonal variation: During the busy season, a business requires largerworking capital while during the slack season a company requires ‘lower workingcapital. In sugar industry the season is November to June, while in the woolen industrythe season is during the winter. Usually the seasonal or variable needs of working capitalare financed by temporary borrowing.

(xviii) Banking Connections: If the corporation has good banking connections andbank credit facilities, it may have minimum margin of regular working capital overcurrent liabilities. But in the absence of the availability of bank finance, it should haverelatively larger among of net working capital.

(xix) Growth and Expansion: For normal rate of expansion in the volume ofbusiness, one may have greater proportion of retained profits to provide for moreworking capital; but fast growing concerns require larger amount of working capital. Aplan of working capital should be formulated with an eye to the future as well as presentneeds of a corporation.

E. Problem of Inadequacy of Working Capital

In case of inadequacy of working capital, a business may have to face the followingproblems:

(i) Production Facilities: It may not be possible to have the full utilisation of theproduction facilities to the optimum level due to the inability of buying sufficient rawmaterial and/or major renovation of the plant and machinery.

(ii) Raw Material Purchases: Advantage of buying at cash discount or on favourableterms may not be possible due to paucity of funds.

(iii) Credit Rating: When financial crisis continues, the credit worthiness of thecompany may be lost, resulting in poor credit rating.

(iv) Seizing Business Opportunities: In case of boom for the products and for thebusiness, the company may not be in a position to produce more to earn 'opportunityprofit' as there may be inadequacy of finished products availability.

(v) Proper Maintenance of Plant and Machinery: If the business is on financialcrisis, adequate sums may not be available for regular repair and maintenance,renovation or modernisation of plant to boost up production and to reduce per unit cost.

(vi) Dividend Policy: In the absence of fund availability it may not be possible tomaintain a steady dividend policy. Under such financial constraint, whatever surplus isavailable will be kept in general reserve account to strengthen the financial soundness ofthe business.

(vii) Reduced Selling: Due to the constraint in working capital, the company may notbe in a position to increase credit sales to boost up the sales revenue.

(viii) Loan Arrangement: Due to the emergency for working capital the companymay have to pay higher rate of interest for arranging either short-term or long-termloans.

(ix) Liquidity versus Profitability: The lower liquidity position may also result inlower profitability.

(x) Liquidation of the Business: If the liquidity position continues to remain weakthe business may run into liquidation. To remedy the situation of working capital crisis,the following steps are required:

(a) An appraisal and review is to be conducted to minimize the operating cycle.(b) Adequate credit control measures are to be adopted for early and promptrealisation from the debtors.(c) Proper planning and control of cash management through cash flowforecasting.(d) Whether more credit periods can be obtained for buying is to be explored.

F. Reasons for Inadequacy of Working Capital

Inadequacy or shortage of working capital may arise for various reasons, of which, themain reasons are:

(i) Operating Losses: This may arise when the cost of production and other relatedcosts are more than the sales revenue, reduction in sales, falling prices, increaseddepreciation, etc. It is obvious that a company facing losses will not have any cashgeneration to sustain its ongoing business.

(ii) Extraordinary Losses: There may be exceptional losses due to fall in price offinished product stocks, government action, obsolescence or otherwise. The effect ofsuch a loss will be a reduction in current assets or increase in current liabilities withoutany corresponding favourable change in the working capital composition.

(iii) Expansion of Business: The company during the profitable years might haveinvested substantially in fixed capital assets, increased production and increased creditsales to make the sales volume grow rapidly. Against those activities, the pitfalls of over-trading may show its ugly face subsequently. That is why a balancing judgment betweeninvestment, liquidity and profitability is to be drawn and projected to save the businessfalling into financial crisis. Thus the continuity and growth of the business may bejeopardized. Along with the increased sales there may be increase in inventories andhigher sundry debtors. Such excessive build-up of inventories and receivables mayamount to alarming figures.

(iv) Payment of Dividend and Interest: The payment of interest from borrowingswill have to be made as per terms of agreement. Similarly, the payment of dividend mayhave to be arranged to keep up the business prestige to the public and to theshareholders. There may be profit to declare dividend but there may not be adequatecash to disburse dividend. In case of insufficient funds to meet the aforesaid liabilities,the mobilising of funds will be necessary.

G. Excessive Working Capital

The following are the major disadvantages of having or holding excessive workingcapital:

(i) Overtrading: A time may come when overtrading will engulf the financialsoundness of the business.

(ii) Excessive Inventories: The inventories holding may become excessive under theinfluence of excessive funds availability.

(iii) Liquidity versus Profitability: The situation of liquidity and the profitabilitymay be imbalanced.

(iv) Inefficient Operation: Availability of excessive production facilities may resultin higher production but sales may not be anticipated to match goods produced.

(v) Lower Return on Capital Employed: There may be reduced profit in relation tototal capital employed, resulting in lower rate of return on capital employed.

(vi) Increased Fixed Capital Expenditure: As enough fund is available, there maybe boost-up in acquiring plant and machinery to enhance production facilities. In casethere is not enough sales potentiality with adequate margin of profit such fixedinvestment may not be worthwhile for fund employment.

H. Principles of Working Capital Management

1. Principle of Risk Variation: If working capital is varied relative to sales, theamount of risk that a firm assumes is also varied and the opportunity for gain or loss isincreased. This principle implies that a definite relation exists between the degree of riskthat management assumes and the rate of return. That is, the more risk that a firmassumes, the greater is the opportunity for gain or loss. It should be noted that while thegain resulting from each decrease in working capital is measurable, the losses that mayoccur cannot be measured.

It is believed that while the potential loss, the exactly opposite, occurs if managementcontinues to decrease working capital, that is to say, potential losses are small at first foreach decrease in working capital but increase sharply if it continues to be reduced. Itshould be the goal of management to find that point of level of Working Capital at whichthe incremental loss associated with a decrease in Working Capital investment becomesgreater than the incremental gain associated with that investment. Since most of themanagers do not know what the future holds, they tend to maintain an investment inworking capital that exceeds the ideal level. It is this excess that concerns since the sizeof the investment determines firm’s rate of return on investment. The obviousconclusion is that managers should determine whether they operate in business thatreacts favourably to changes in working capital levels, if not, the gains realized may notbe adequate in comparison to the risk that must be assumed when working capitalinvestment is decreased.

2. Principle of Equity Position: Capital should be invested in each components ofworking capital as long as the equity position of the firm increases. It follows from theabove that the management is faced with the problem of determining the ideal 'level' ofworking capital. The concept that each rupee invested in fixed or variable workingcapital should contribute to the net worth of the firm should serve as a basis for such aprinciple.

3. Principle of Cost of Capital: The type of capital used to finance working capitaldirectly affects the amount of risk that a firm assumes, as well as the opportunity forgain or loss and cost of capital.

Whereas the first principle dealt with the risk associated with the amount of workingcapital employed in relation to sales, the third principle is concerned with the riskresulting from the type of capital used to finance current assets. It has been observedthat return to equity capital increases directly with the amount of risk assumed by themanagement. This is true but only to a certain point. When excessive risk is assumed, afirms opportunity for loss will eventually overshadow its opportunity for gain, and atthis point return to equity is threatened. When this occurs, the firm stands to sufferlosses. Unlike rate of return, cost of capital moves inversely with risk; that is, asadditional risk capital is employed by management, cost of capital declines. Thisrelationship prevails until the firm’s optimum capital structure is achieved; thereafter,the cost of capital increases.

4. Principle of Maturity of Payment: A company should make every effort to relatematurities of payment to its flow of internally generated funds. There should be the leastdisparity between the maturities of the firm’s short term debt instrument and its flow ofinternally generated funds because a greater risk is generated with greater disparity. Amargin of safety should, however, be provided for short term debt payments.

5. Principle of Negotiation:

The risk is not only associated with the amount of debt used relative to equity, it is alsorelated to the nature of the contracts negotiated by the borrower.

Some of the clauses of the contracts such as restrictive clauses and dates of maturitydirectly affect a firms operation. Lenders of short term funds are particularly consciousof this problem and they ask for cash flow statements. Lenders realize that a firm'sability to repay short term loan directly related to cash flow and not to earnings and,therefore, a firm should make every effort to tie maturities to its flow of internallygenerated funds. This concept serves as the basis for the final hypothesis of thispresentation. Specifically, it may be stated as follows:

"The greater the disparity between the maturities of firms short term debt instrumentand its flow of internally generated funds, the greater the risk and vice-versa".

One can see that it is possible for a firm to face insolvency or embarrassment eventhough it might be making a profit. It is extremely difficult to predict accurately a firm’scash flow in an economy such as ours. Therefore, a margin of safety should be includedin every short term debt contract; that is, adequate time should be allowed between thetime the funds are generated and the date of maturity.

Steps Involved in Efficient Management of Working Capital

1. Proper financial set up with appropriate authority and responsibility.

2. Coordination between the following functional areas in the organization:

Production planning and control

Sales credit control

Material management

Optimal utilisation of fixed plant and machinery together with other facilities

Sale of uneconomical fixed assets

Acquiring plant and machinery to augment production

Cost reduction programme

3. Financial planning and control for achieving increased profitability to have adequate'cash generation' and 'plough back' of profits so that there is adequate internal source offinance.

4. Proper cash management through projection of cash flow and source and applicationof funds flow statement.

5. Establishing appropriate Information and Reporting System.

REVIEW QUESTIONS

1. Discuss the importance of working capital for a manufacturing concern.

2. Explain the various determinants of working capital of a concern.

3. What are the advantages of having ample working capital funds?

4. Differentiate between fixed working capital and variable working capital.

5. What are the different principles of working capital management?

6. Summarise the causes for and changes in working capital of a firm.

SUGGESTED READINGS

1. Agarwal, N.K.: Working Capital Management, New Delhi, Sterling Publications (P)Ltd.

2. Khan, M.Y. and Jain, P.K.: Financial Management, New Delhi, Tata McGraw Hill Co.

3. Ramamoorthy, V.E.: Working Capital Management, Madras, Institute for FinancialManagement and Research.

- End of Chapter -

LESSON - 3

WORKING CAPITAL FORECASTING TECHNIQUES