38

Financial Options: Introduction

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | marsha-austin |

| View: | 216 times |

| Download: | 0 times |

Financial Options: Introduction

2

Option Basics

• A stock option is a derivative security, because the value of the option is “derived” from the value of the underlying common stock.

• Derivatives are contingent claims because their payoffs depend on the value of other securities.

• An option is a contract which gives its holder the right, but not the obligation, to buy (or sell) an asset at some predetermined price within a specified period of time.

• There are two basic financial option types. – Call options are options to buy the underlying asset. When

exercising a call option, you “call in” the asset.– Put options are options to sell the underlying asset. When

exercising a put, you “put” the asset to someone.

3

The Option Contract

• A call option gives its holder the right to buy an asset:– At the exercise or strike price– On or before the expiration date– Exercise the option to buy the underlying asset if market

value > strike.

• A put option gives its holder the right to sell an asset:– At the exercise or strike price– On or before the expiration date– Exercise the option to sell the underlying asset if market

value < strike.

4

Option Basics• Option contracts are legal agreements between two parties—the

buyer of the option, and the seller of the option.

• The minimum terms stipulated by stock option contracts are:– The identity of the underlying stock.– The strike price, or exercise price.– The option contract size.– The option expiration date, or option maturity.– The option exercise style (American or European).– The delivery, or settlement, procedure.

• Stock options trade at organized options exchanges, such as the CBOE, as well as over-the-counter (OTC) options markets. Listed option contracts are standardized to facilitate trading and price reporting.– Listed stock options give the option holder the right to buy or sell

100 shares of stock.

5

Option Vocabulary

• Exercise (or strike) price: The price stated in the option contract at which the security can be bought or sold.

• Option price (premium): The market price of the option contract.

• Expiration date: The date the option matures.• Exercise value (option payoff): The value of a

call or put option if it were exercised today – EV of Call = Max (ST ─ X, 0)

– EV of Put = Max (X ─ ST, 0)

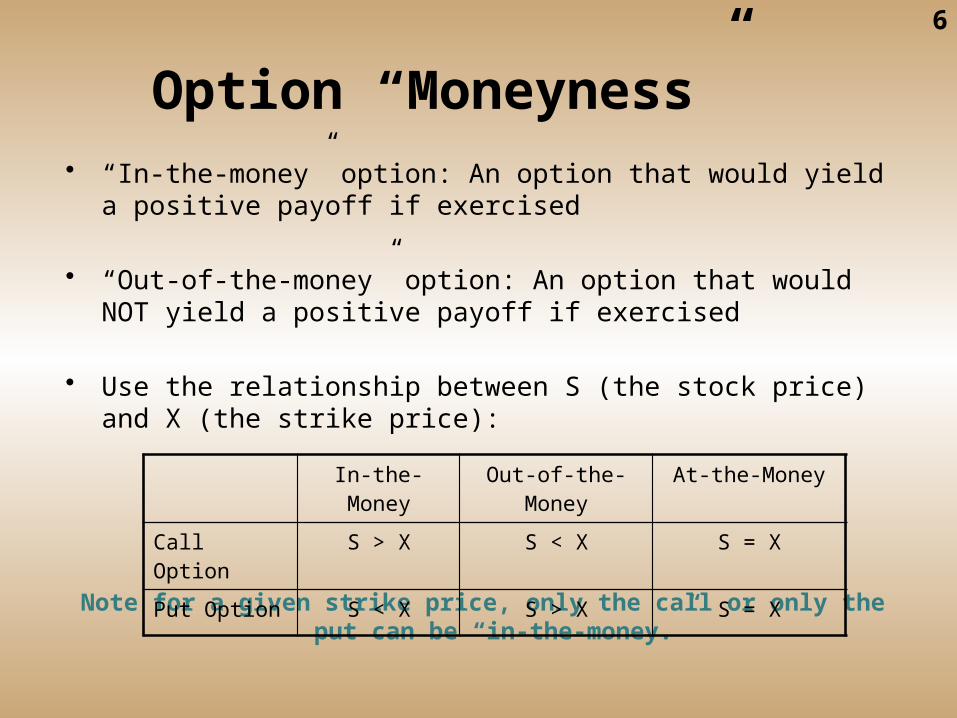

Option “Moneyness”• “In-the-money” option: An option that would yield a positive payoff if

exercised

• “Out-of-the-money” option: An option that would NOT yield a positive payoff if exercised

• Use the relationship between S (the stock price) and X (the strike price):

Note for a given strike price, only the call or only the put can be “in-the-money.”

In-the-Money Out-of-the-Money At-the-Money

Call Option S > X S < X S = X

Put Option S < X S > X S = X

6

7

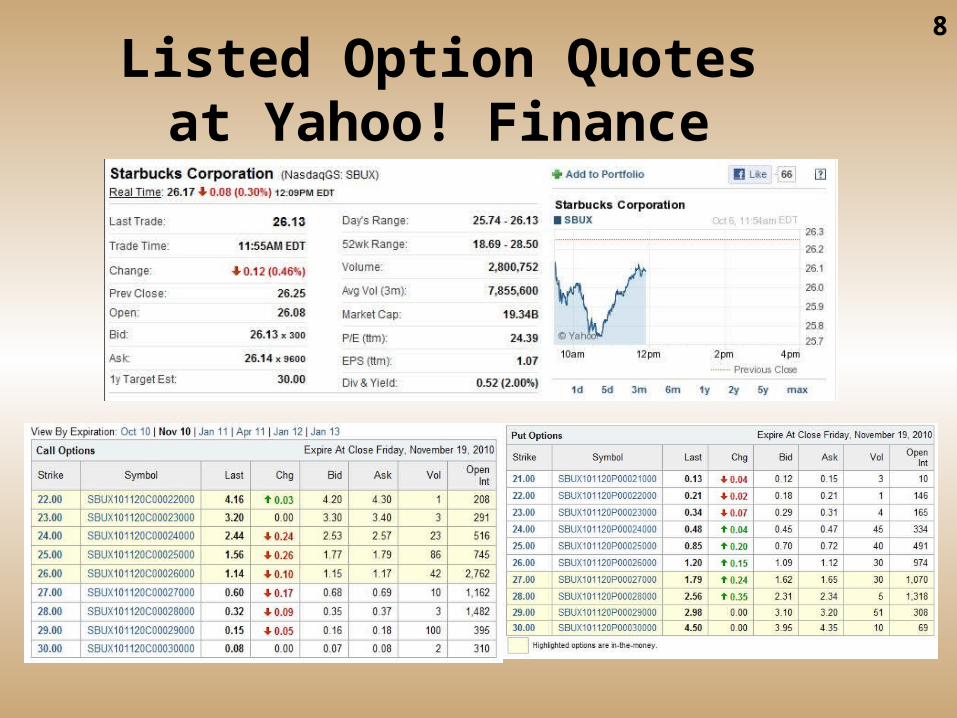

Option Price Quotes

• A list of available option contracts and their prices for a particular security is known as an option chain.

• Option chains are available online through many sources, including the CBOE (http://quote.cboe.com) and Yahoo! Finance (http://finance.yahoo.com).

• Stock option ticker symbols include:– Letters to identify the underlying stock.– A letter to identify the expiration month as well as whether the option is

a call or a put. (A through L for calls; M through X for puts).– A letter to identify the strike price (a bit more complicated—see Yahoo

for tables to explain this letter.)

8

Listed Option Quotesat Yahoo! Finance

9

The Options Clearing Corporation

• The Options Clearing Corporation (OCC) is a private agency that guarantees that the terms of an option contract will be fulfilled if the option is exercised.

• The OCC issues and clears all option contracts trading on U.S. exchanges.

• Note that the exchanges and the OCC are all subject to regulation by the Securities and Exchange Commission (SEC).

Visit the OCC at: www.optionsclearing.com.

10

• Stock Options• Index Options• Futures Options• Foreign Currency Options• Interest Rate Options

Different Types of Options

20-11

EXAMPLES

12

Example: Call Option

• You buy the call option contract that will allow you to buy from an option seller 100 shares of IBM for $50 per share at any time during the next three months. The call option is traded at $1 for each share of underlying stock.

• Exercise (or strike) price = $50• Option Price = $1• Expiration: Three months• Suppose the price of IBM share rises to $55. You

can exercise your option to buy IBM share at an exercise price ($50). Thus, the exercise value is $5 ($55 - $50).

13

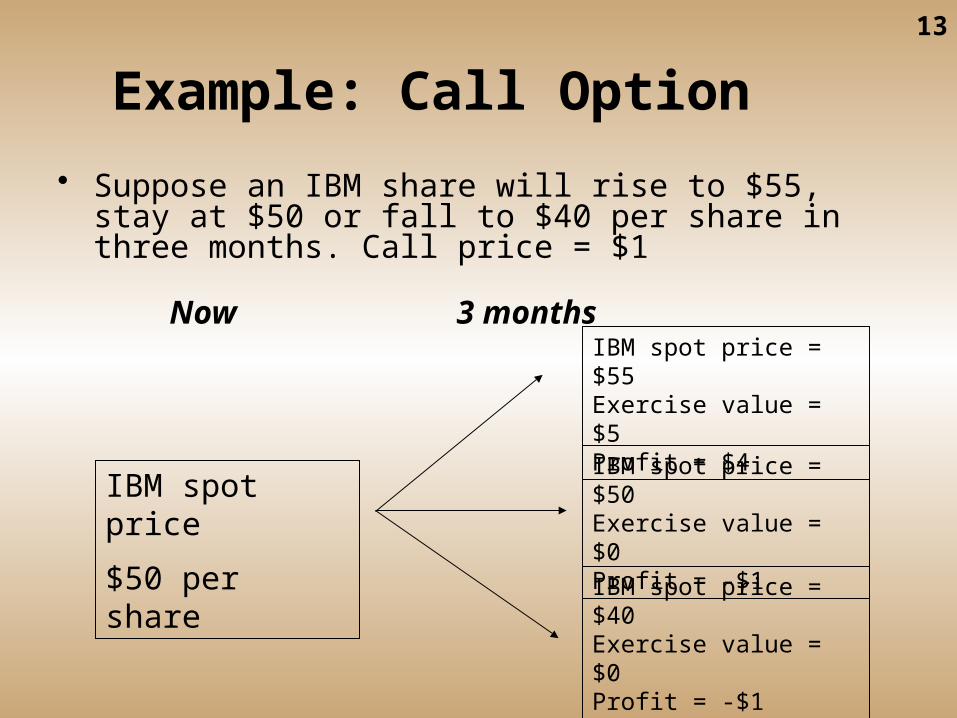

Example: Call Option

• Suppose an IBM share will rise to $55, stay at $50 or fall to $40 per share in three months. Call price = $1

IBM spot price

$50 per share

IBM spot price = $55 Exercise value = $5Profit = $4

Now 3 months

IBM spot price = $50 Exercise value = $0Profit = -$1

IBM spot price = $40 Exercise value = $0Profit = -$1

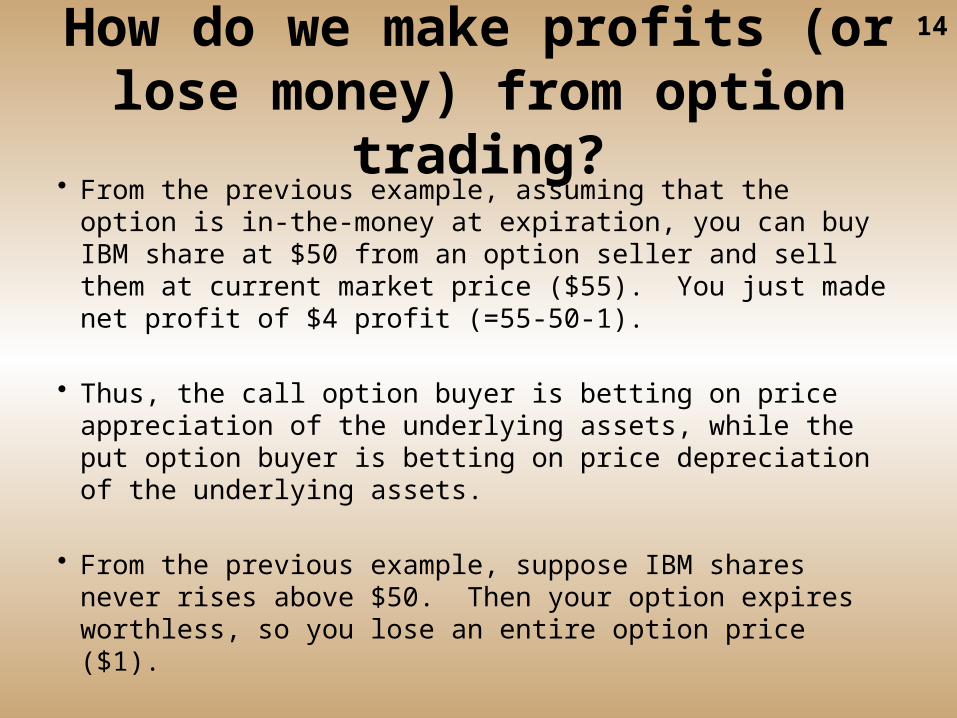

14How do we make profits (or lose money) from option

trading?• From the previous example, assuming that the option is in-

the-money at expiration, you can buy IBM share at $50 from an option seller and sell them at current market price ($55). You just made net profit of $4 profit (=55-50-1).

• Thus, the call option buyer is betting on price appreciation of the underlying assets, while the put option buyer is betting on price depreciation of the underlying assets.

• From the previous example, suppose IBM shares never rises above $50. Then your option expires worthless, so you lose an entire option price ($1).

15

Call Option Profits

-20

100908070600 10 20 30 40 50

-40

20

0

-60

40

60

Stock price ($)

Op

tio

n p

rofi

t (

$)

Buy a call

Exercise price = $50

16

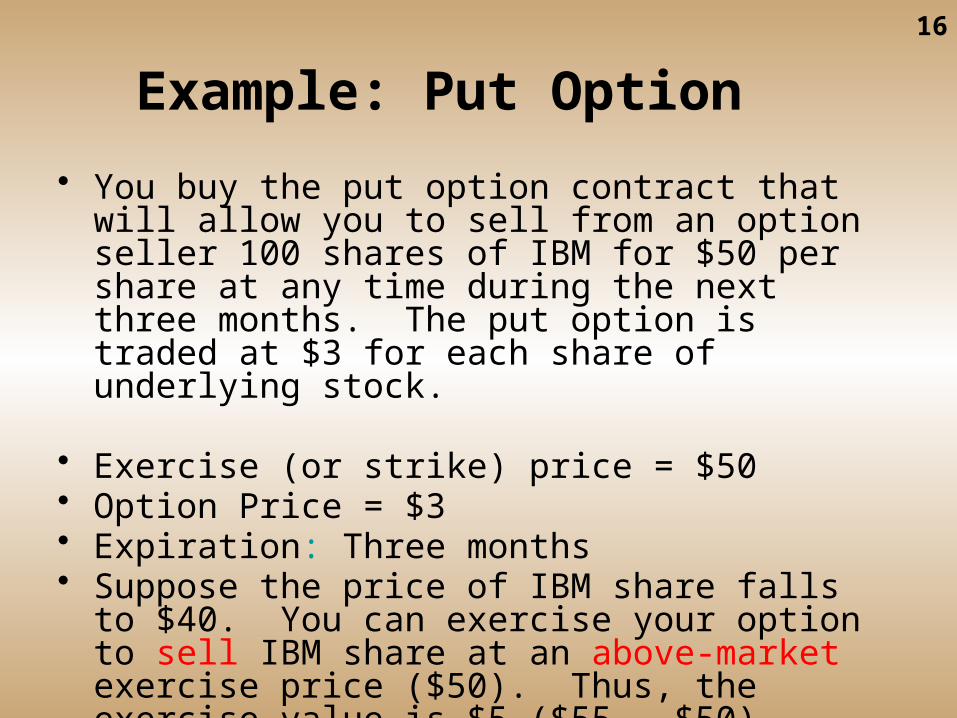

Example: Put Option

• You buy the put option contract that will allow you to sell from an option seller 100 shares of IBM for $50 per share at any time during the next three months. The put option is traded at $3 for each share of underlying stock.

• Exercise (or strike) price = $50• Option Price = $3• Expiration: Three months• Suppose the price of IBM share falls to $40. You

can exercise your option to sell IBM share at an above-market exercise price ($50). Thus, the exercise value is $5 ($55 - $50).

17

Example: Put Option

• Suppose an IBM share will rise to $55, stay at $50 or fall to $40 per share in three months. Put price = $3

Now 3 months

IBM spot price

$50 per share

IBM spot price = $55 Exercise value = $0Profit = -$3

IBM spot price = $50 Exercise value = $0Profit = -$3

IBM spot price = $40 Exercise value = $10Profit = $7

18

Put Option Profits

-20

100908070600 10 20 30 40 50

-40

20

0

-60

40

60

Stock price ($)

Op

tio

n p

rofi

t ($

)

Buy a put

19

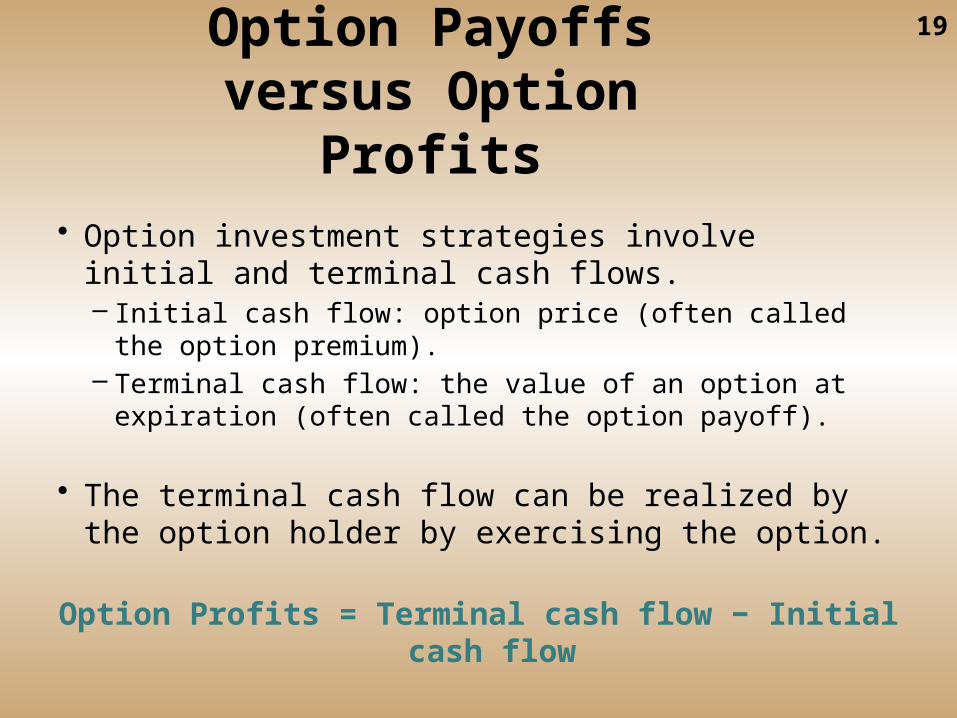

Option Payoffs versus Option Profits

• Option investment strategies involve initial and terminal cash flows.– Initial cash flow: option price (often called the option

premium).– Terminal cash flow: the value of an option at expiration

(often called the option payoff).

• The terminal cash flow can be realized by the option holder by exercising the option.

Option Profits = Terminal cash flow − Initial cash flow

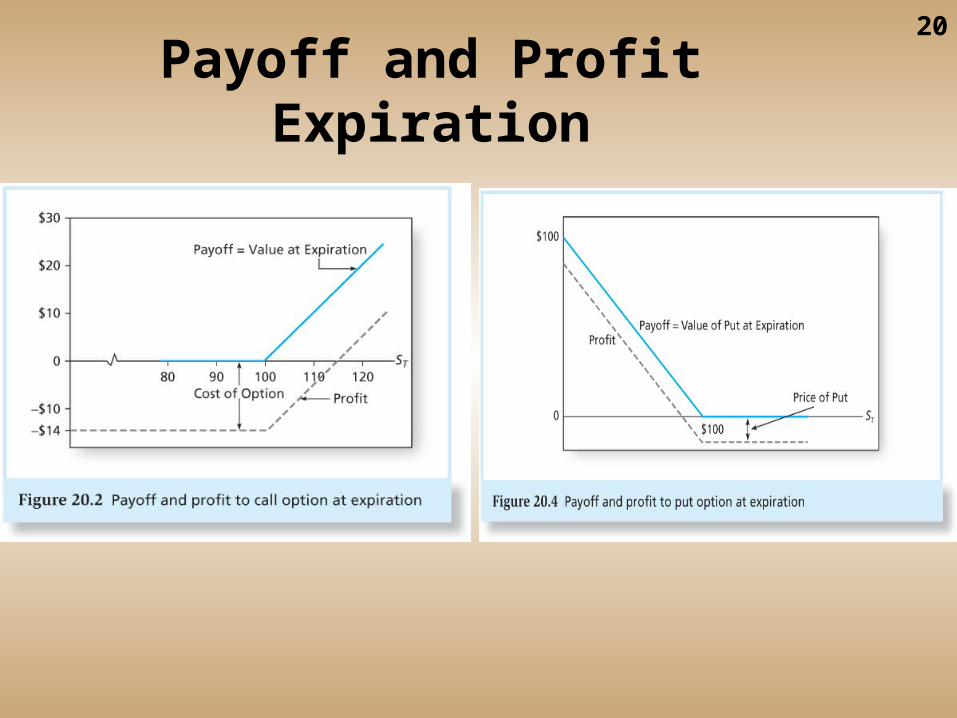

20

Payoff and Profit Expiration

21

Option Payoffs

22

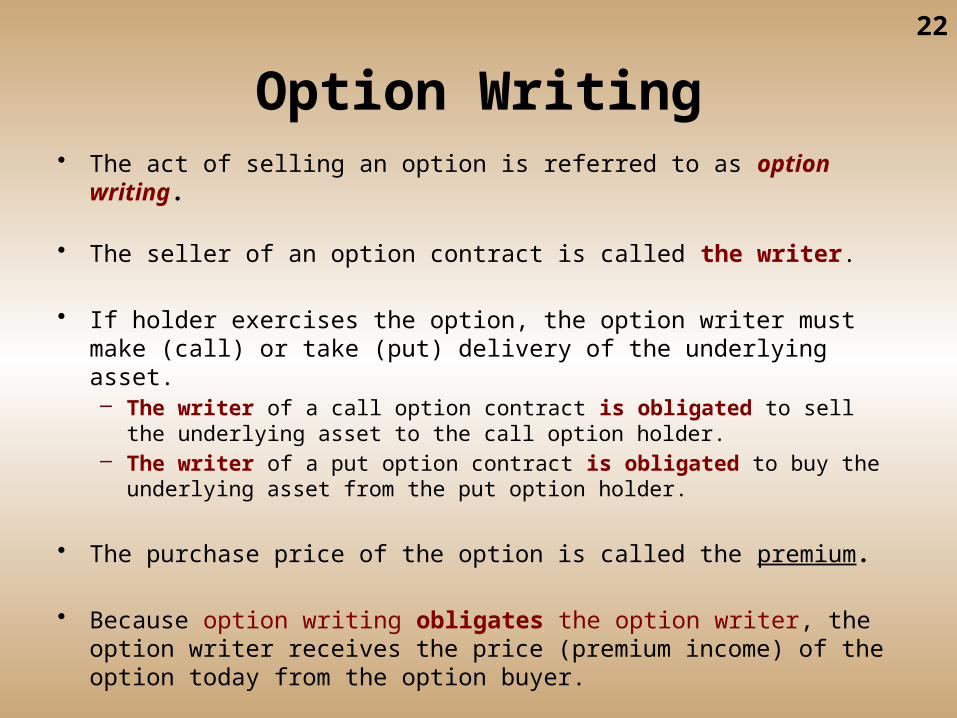

Option Writing• The act of selling an option is referred to as option writing.

• The seller of an option contract is called the writer.

• If holder exercises the option, the option writer must make (call) or take (put) delivery of the underlying asset.– The writer of a call option contract is obligated to sell the underlying

asset to the call option holder.– The writer of a put option contract is obligated to buy the underlying

asset from the put option holder.

• The purchase price of the option is called the premium.

• Because option writing obligates the option writer, the option writer receives the price (premium income) of the option today from the option buyer.

23

Example: Profit and Loss on a Call

• A January 2010 call on IBM with an exercise price of $130 was selling on December 2, 2009, for $2.18.

• The option expires on the third Friday of the month, or January 15, 2010.

• If IBM remains below $130, the call will expire worthless.

• Option payoff= 0,• Profit = -$2.18 per share

24

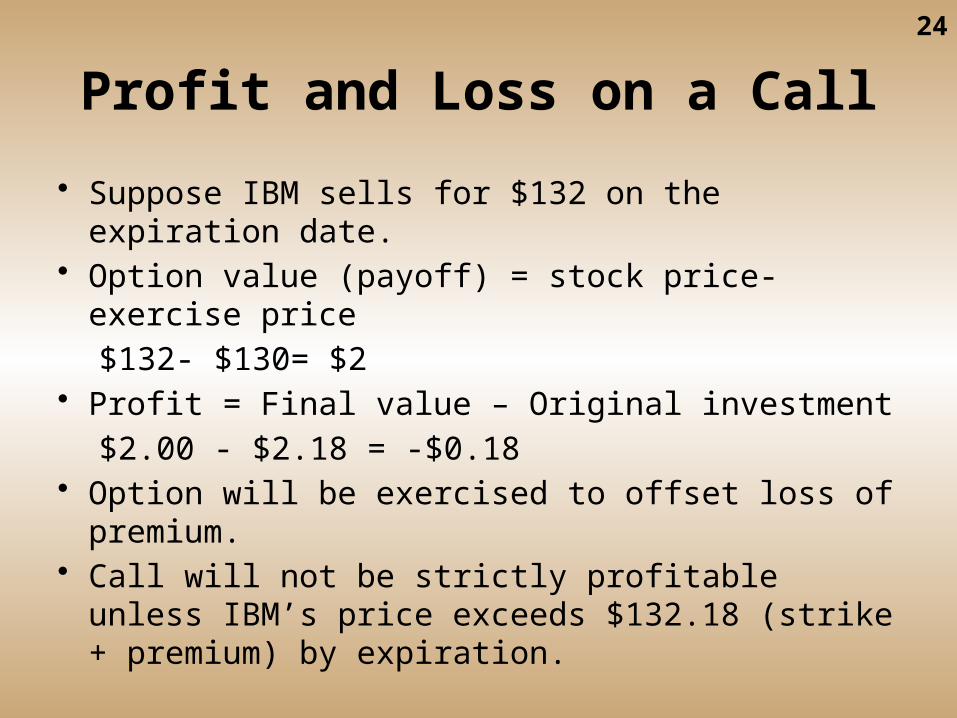

Profit and Loss on a Call

• Suppose IBM sells for $132 on the expiration date.• Option value (payoff) = stock price-exercise price

$132- $130= $2• Profit = Final value – Original investment

$2.00 - $2.18 = -$0.18• Option will be exercised to offset loss of premium.• Call will not be strictly profitable unless IBM’s price

exceeds $132.18 (strike + premium) by expiration.

25

Example: Profit and Loss on a Put

• Consider a January 2010 put on IBM with an exercise price of $130, selling on December 2, 2009, for $4.79.

• Option holder can sell a share of IBM for $130 at any time until January 15.

• If IBM goes above $130, the put is worthless.

• Option payoff= 0,• Profit = -$4.79 per share

26

Profit and Loss on a Put

• Suppose IBM’s price at expiration is $123.• Value at expiration = exercise price –

stock price:$130 - $123 = $7

• Investor’s profit:$7.00 - $4.79 = $2.21

• Holding period return = 46.1% over 44 days!

27

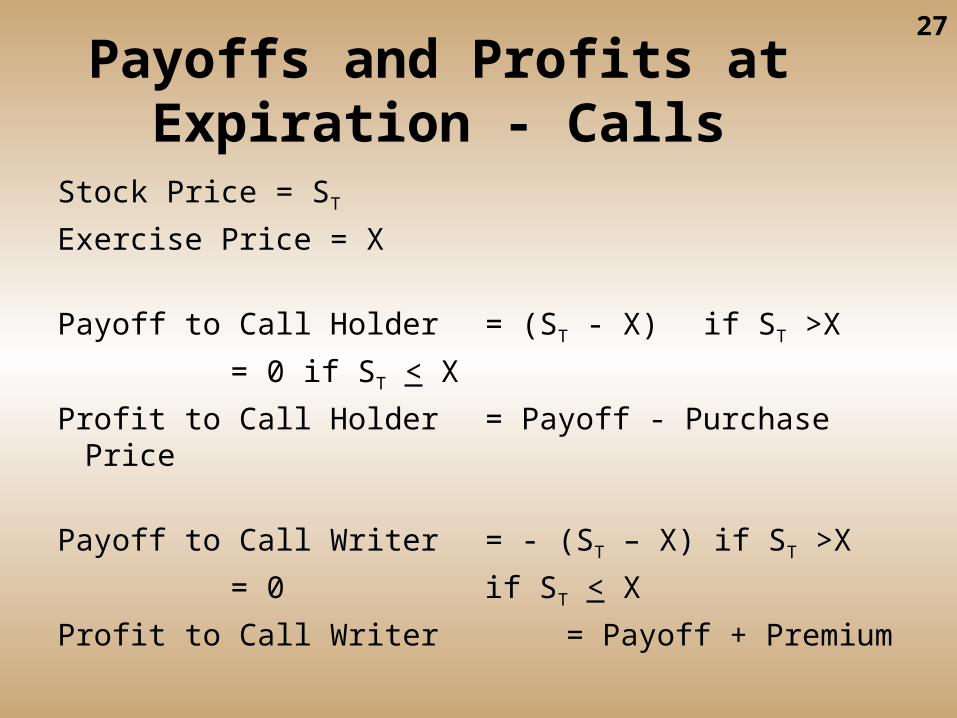

Payoffs and Profits at Expiration - Calls

Stock Price = ST

Exercise Price = X

Payoff to Call Holder = (ST - X) if ST >X

= 0 if ST < X

Profit to Call Holder = Payoff - Purchase Price

Payoff to Call Writer = - (ST – X) if ST >X

= 0 if ST < X

Profit to Call Writer = Payoff + Premium

28

Payoffs and Profits at Expiration - Puts

Payoffs to Put Holder

0 if ST > X

(X - ST) if ST < X

Profit to Put Holder

Payoff – Premium

Payoffs to Put Writer

0 if ST > X

-(X - ST) if ST < X

Profits to Put Writer

Payoff + Premium

29

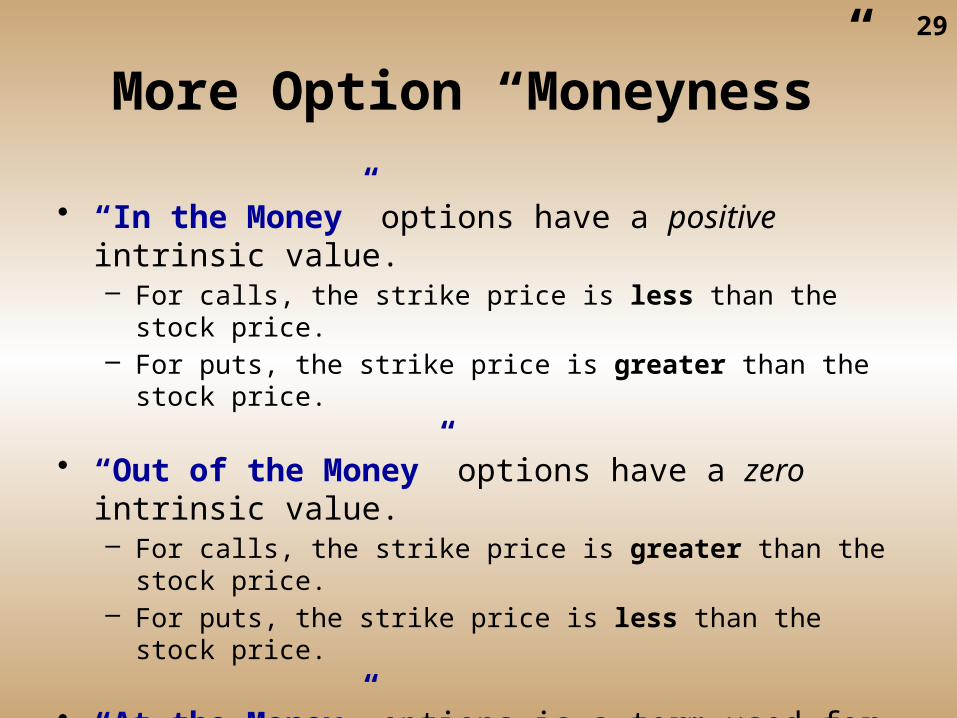

More Option “Moneyness”

• “In the Money” options have a positive intrinsic value.– For calls, the strike price is less than the stock price.– For puts, the strike price is greater than the stock price.

• “Out of the Money” options have a zero intrinsic value.– For calls, the strike price is greater than the stock price.– For puts, the strike price is less than the stock price.

• “At the Money” options is a term used for options when the stock price and the strike price are about the same.

20-30

WHY OPTIONS?

31

Why Options?

• A basic question asked by investors is: “Why buy stock options instead of shares in the underlying stock?”

• To answer this question, we compare the possible outcomes from these two investment strategies:– Buy the underlying stock.– Buy options on the underlying stock.

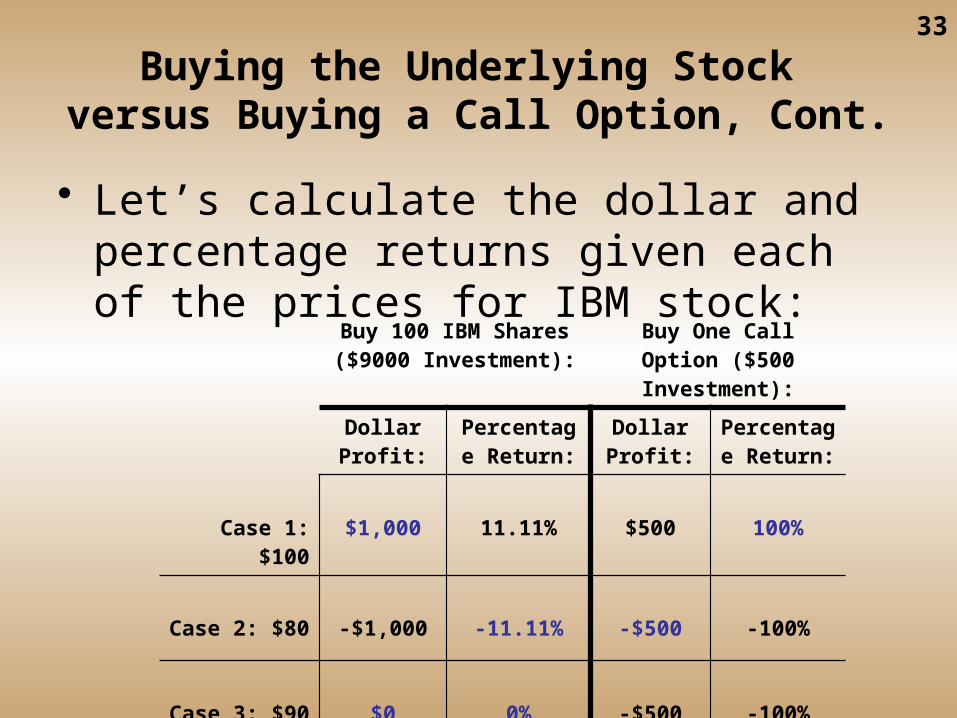

32Buying the Underlying Stock

versus Buying a Call Option• Suppose IBM is selling for $90 per share and call options

with a strike price of $90 are $5 per share.

• Investment for 100 shares:– IBM Shares: $9,000– One listed call option contract: $500

• Suppose further that the option expires in three months.

• Finally, let’s say that in three months, the price of IBM shares will either be: $100, $80, or $90.

33

Buying the Underlying Stock versus Buying a Call Option, Cont.

• Let’s calculate the dollar and percentage returns given each of the prices for IBM stock:

Buy 100 IBM Shares ($9000 Investment):

Buy One Call Option ($500 Investment):

Dollar Profit:

Percentage Return:

Dollar Profit:

Percentage Return:

Case 1: $100 $1,000 11.11% $500 100%

Case 2: $80 -$1,000 -11.11% -$500 -100%

Case 3: $90 $0 0% -$500 -100%

34

Options vs. Stocks• Whether one strategy is preferred over another is a matter for each

individual investor to decide.

– That is, in some instances investing in the underlying stock will be better. In other instances, investing in the option will be better.

– Each investor must weight the risk and return trade-off offered by the strategies.

• It is important to see that call options offer an alternative means of formulating investment strategies.– For 100 shares, the dollar loss potential with call options is lower.– For 100 shares, the dollar gain potential with call options is lower.– The positive percentage return with call options is higher.– The negative percentage return with call options is lower.

35

Exercises

Option/Strike Exp. Vol. Last Vol. LastIBM 130 Oct 364 15¼ 107 5¼

Option 1 138¼ 130 Jan 112 19½ 420 9¼Option 2 138¼ 135 Jul 2365 4¾ 2431 13/16

Option 3 138¼ 135 Aug 1231 9¼ 94 5½Option 4 138¼ 140 Jul 1826 1¾ 427 2¾Option 5 138¼ 140 Aug 2193 6½ 58 7½

--Put----Call--

36

Exercises (cont’d)

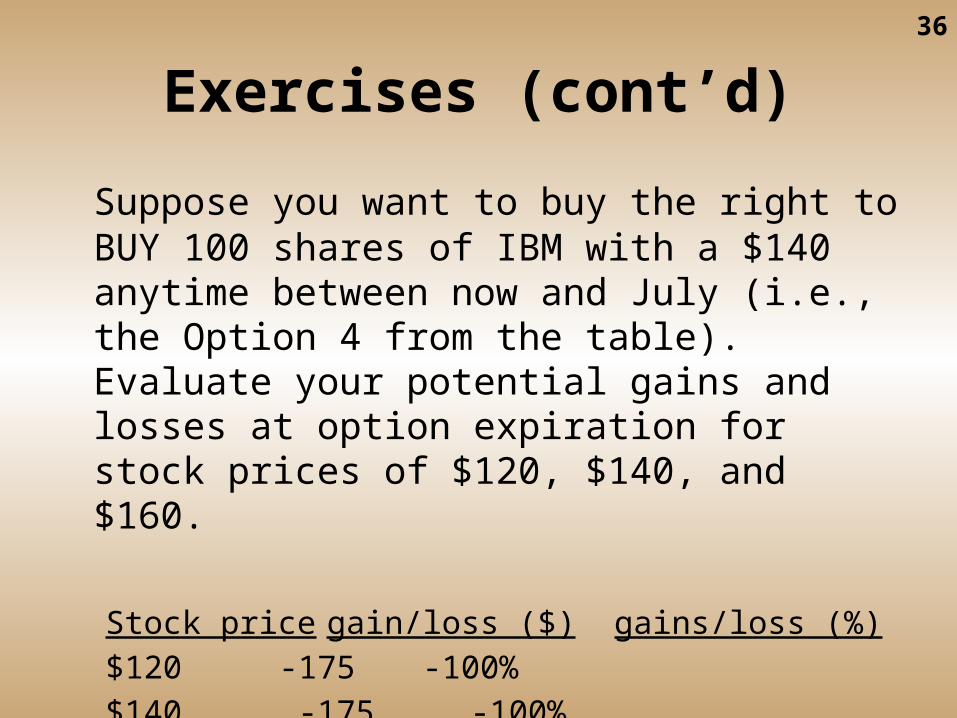

Suppose you want to buy the right to BUY 100 shares of IBM with a $140 anytime between now and July (i.e., the Option 4 from the table). Evaluate your potential gains and losses at option expiration for stock prices of $120, $140, and $160.

Stock price gain/loss ($) gains/loss (%)

$120 -175 -100%

$140 -175 -100%

$160 1825 1043%

37

Exercises (cont’d)

Given information in question 5, conduct the same analysis for IBM 140 July PUT options.

Stock Gain/Loss ($) Gain/Loss (%)

$120 1725 627%

$140 -275 -100%

$160 -275 -100%

38

Exercises (cont’d)

• Suppose you are Mark Cuban, Jr. who is currently holding 100,000 shares of IBM. Today, the market price of IBM shares is $$138.25, as shown in the table. You fear of growing volatility of IBM share prices and want to hedge against falling share prices for next several months ending August 2004 (i.e., the Option 5 from the table). What would you do using options on stocks available above? Be sure to identify the number of options contracts to be bought, the options premium, and expiration months. Suppose an IBM share price in August 2004 when the options expire is $100. Calculate net gain or loss from your strategy using options contracts. In your calculation, include gains or losses from the market value change in your holding of IBM shares.

![arXiv:1912.01618v1 [quant-ph] 3 Dec 2019 · B. European Option An option is a derivative contract for the trading of assets. In its call/put form, the option holder can buy/sell an](https://static.documents.pub/doc/80x56/5f02a6cf7e708231d40554ac/arxiv191201618v1-quant-ph-3-dec-2019-b-european-option-an-option-is-a-derivative.jpg)