34

DR.V.N.BEDEKAR INSTITUTE MANAGEMENT STUDIES MMS I DIV B SUBJECT : FINANCIAL ACCOUNTING TOPIC : RATIO ANALYSIS OF ASIAN PAINTS SUBMITTED TO : PROF. SMITA JAPE MA’AM

| Date post: | 13-Jul-2015 |

| Category: |

Education |

| Upload: | tushar-sadhye |

| View: | 818 times |

| Download: | 8 times |

DR.V.N.BEDEKAR INSTITUTE MANAGEMENT

STUDIES

MMS I DIV B

SUBJECT : FINANCIAL ACCOUNTING

TOPIC : RATIO ANALYSIS OF ASIAN PAINTS

SUBMITTED TO : PROF. SMITA JAPE MA’AM

Group Members

Sonali Sakpal 48

Sayali Phatak 44

Tanvi Pawar 43

Nikita Rathod 46

Nikita Watve 55

Tushar Sadhye 47

Vikrant Pokharkar 45

RATIO ANALYSIS

Ratio analysis is the process of determining and

interpreting numerical relationship based on

financial statements. It is the technique of

interpretation of financial statements with the

help of accounting ratios derived from the

balance sheet and profit and loss account.

Basis Of Comparision

Trend Analysis involves comparison of a firm over a period of time, that is, present ratios are compared with past ratios for the same firm. It indicates the direction of change in the performance –improvement, deterioration or constancy – over the years.

Interfirm Comparison involves comparing the ratios of a firm with those of others in the same lines of business or for the industry as a whole. It reflects the firm’s performance in relation to its competitors.

Comparison with standards or industry average

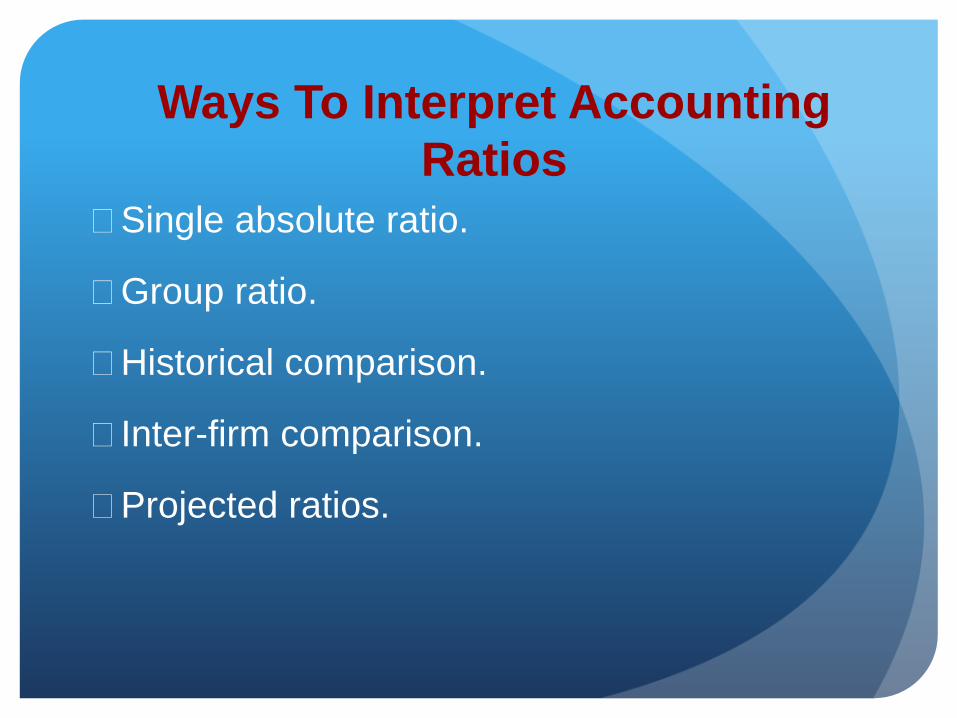

Ways To Interpret Accounting

Ratios

Single absolute ratio.

Group ratio.

Historical comparison.

Inter-firm comparison.

Projected ratios.

Classification Of Ratios

Category Also Called Measures

Liquidity Ratios Solvency Ratios Company’s ability in the

near future to pay its debts

as they become due

Profitability Ratios Margin Ratios Company’s success-or

failure-at earning a

profit(i.e., generating more

revenues than expenses

Asset Management

Ratios

Turnover Ratios

Efficiency Ratios

Activity Ratios

Company’s effectiveness at

using various assets

Leverage Ratios Coverage ratios

Capital

Structure Ratio

Company’s long-term ability

to pay debt as it becomes

due

Topic for observation

Asian Paint 70 years of innovation in paint

Since its foundation in 1942,

India’s largest and Asia’s third largest paint company, with a turnover of Rs.127.15 billion.

Asian Paints operates in 17 countries and has 23 paint manufacturing facilities in the world servicing consumers in over 65 countries.

Category - Paints/ Varnishes

Competitors- Jenson & Nicolson India, Kansai Nerolac, Akzonobel, Sherwin-Williams, Nippon Paints, PPG Industries Inc.

BALANCE SHEET RATIOS

CURRENT RATIO

QUICK RATIO

DEBT EQUITY RATIO

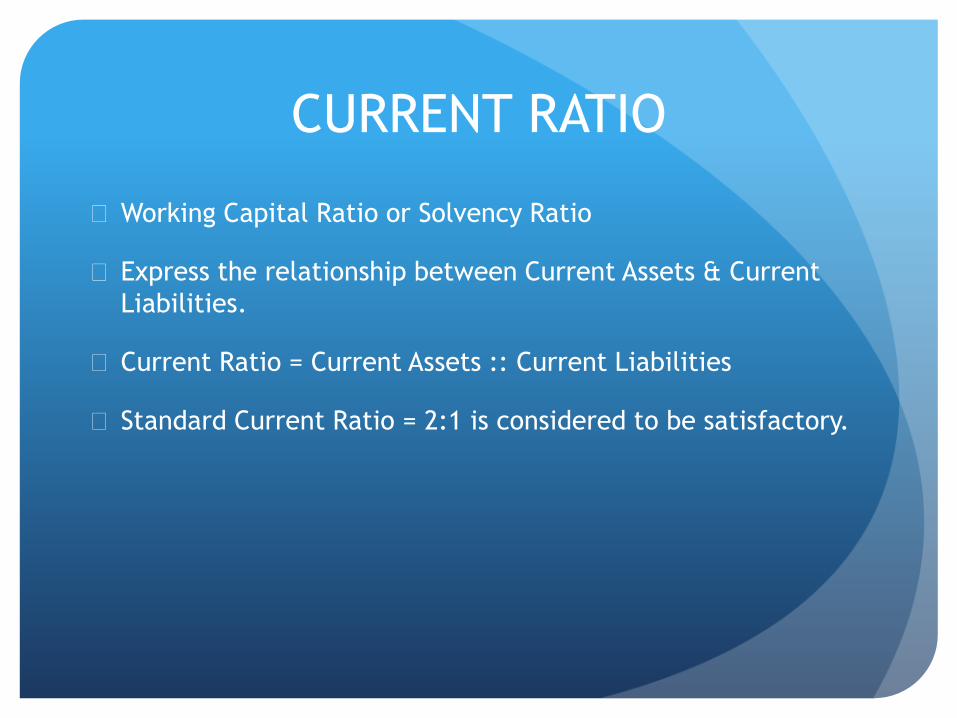

CURRENT RATIO

Working Capital Ratio or Solvency Ratio

Express the relationship between Current Assets & Current

Liabilities.

Current Ratio = Current Assets :: Current Liabilities

Standard Current Ratio = 2:1 is considered to be satisfactory.

SIGNIFICANCE & PURPOSE

Significance

Test of Credit strength & solvency of an organization.

Indicates the strength of the working capital (CA-CL).

Company’s ability to meet its day-to-day financial obligation.

Purpose

Serves index of short–term solvency.

Index of the strength of working capital of an organization.

ASIAN PAINTS RELATED CURRENT

RATIO ANALYSIS

Ratio less than 1.00 may

indicate liquidity issues.

Ratio between 1.00 and

2.00 is sufficient.

It can meet its short term

obligations with short

term assets.

CR in 2014 < CR in 2013

as CA > in 2014 but CL has

also > in 2014.

QUICK RATIO

Acid Test Ratio

Measures the ability of a company to

use its near cash or quick assets to

pay off its debts

An indicator of a company’s short-

term liquidity

Significance of Quick Ratio

Measure of a company's ability to settle its current

liabilities on a very short notice.

May provide a misleading indication of a company's

liquidity position

More reliable measure of liquidity for manufacturing

companies and construction firms that have relatively high

levels of inventory, work in progress and receivables

More conservative version of current ratio.

More rigorous assessment of a company's ability to pay

its current liabilities

Cash in hand + Cash at Bank +Receivables +

Marketable Securities Inventories

Current Liabilities – Provisions

Quick Ratio of 2014,

= 3122.77 + 478.6 – 1665.05

2423.55 – 617.72

Quick Ratio of 2013,

= 2681.53 + 362.61 – 1480.79

2078.94 – 500.32

Quick Ratio Will be calculated

as follows-

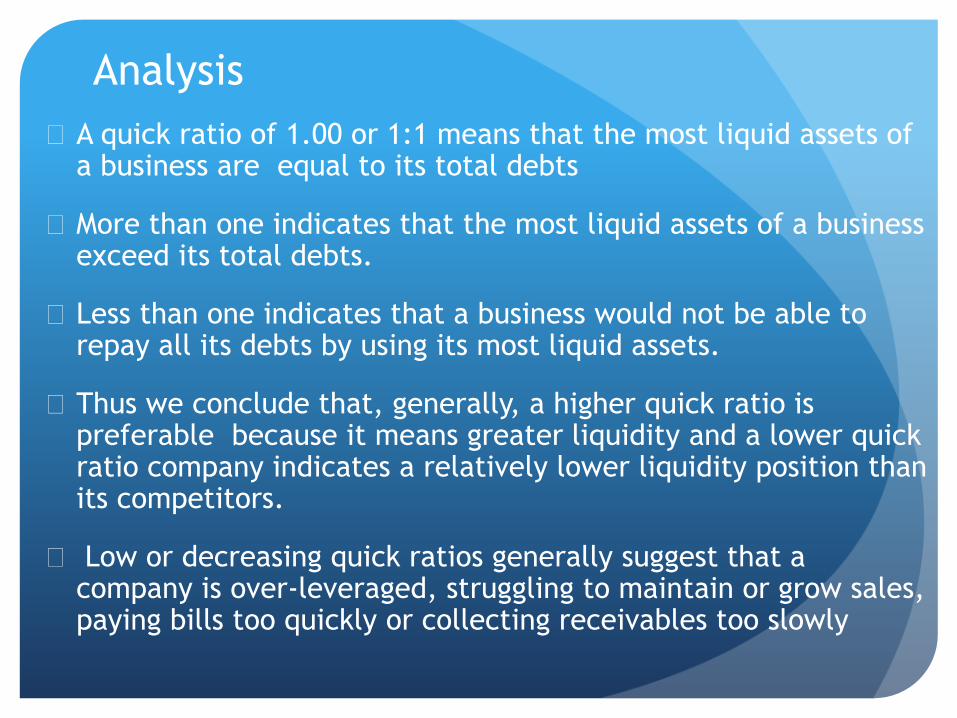

A quick ratio of 1.00 or 1:1 means that the most liquid assets of a business are equal to its total debts

More than one indicates that the most liquid assets of a business exceed its total debts.

Less than one indicates that a business would not be able to repay all its debts by using its most liquid assets.

Thus we conclude that, generally, a higher quick ratio is preferable because it means greater liquidity and a lower quick ratio company indicates a relatively lower liquidity position than its competitors.

Low or decreasing quick ratios generally suggest that a company is over-leveraged, struggling to maintain or grow sales, paying bills too quickly or collecting receivables too slowly

Analysis

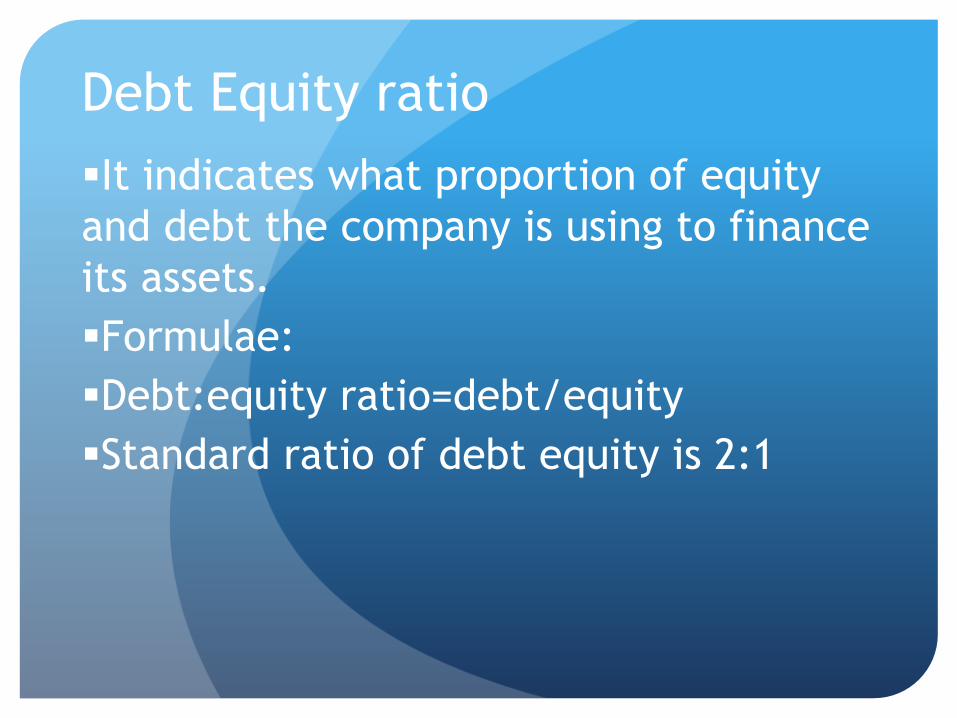

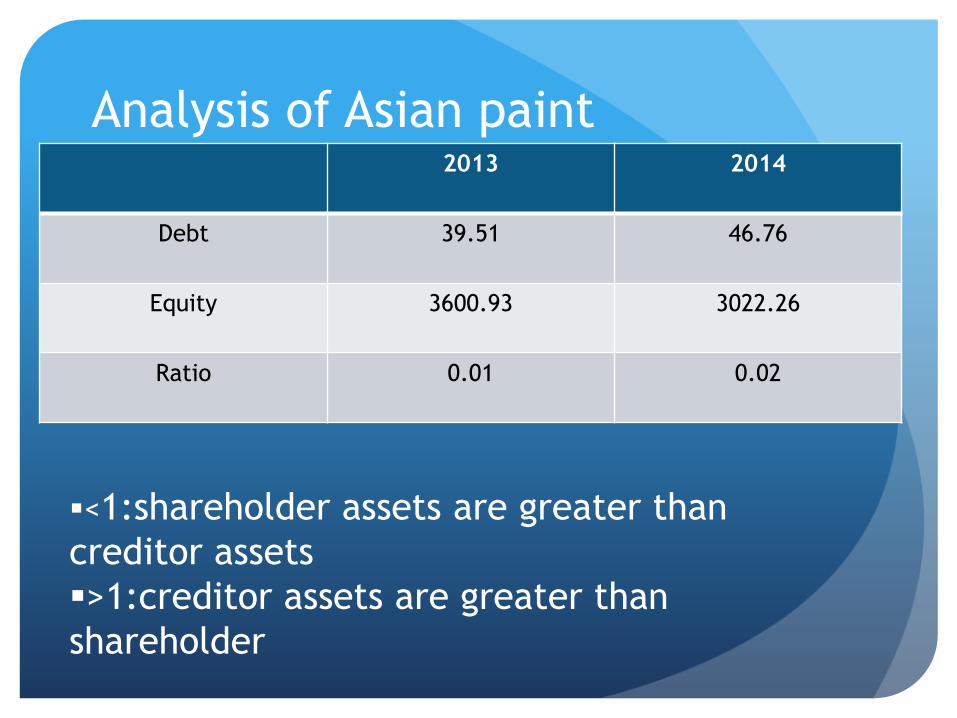

Debt Equity ratio

It indicates what proportion of equity

and debt the company is using to finance

its assets.

Formulae:

Debt:equity ratio=debt/equity

Standard ratio of debt equity is 2:1

Analysis of Asian paint2013 2014

Debt 39.51 46.76

Equity 3600.93 3022.26

Ratio 0.01 0.02

<1:shareholder assets are greater than

creditor assets

>1:creditor assets are greater than

shareholder

Profitability Ratio

A profitability ratio is a measure of profitability, which is a

way to measure a company's performance. Profitability is

simply the capacity to make a profit, and a profit is what is

left over from income earned after you have deducted all

costs and expenses related to earning the income.

DEFINITION OF ‘GROSS PROFIT’

A company's revenue minus its cost of goods sold. Gross

profit is a company's residual profit after selling a

product or service and deducting the cost associated

with its production and sales.

Significance:-

It is a profitability ratio measuring what proportion of

revenue is converted into gross profit .

Formula:

GP RATIO = 𝑔𝑟𝑜𝑠𝑠 𝑝𝑟𝑜𝑓𝑖𝑡

𝑛𝑒𝑡 𝑠𝑎𝑙𝑒𝑠*100

GROSS PROFIT = REVENUE - COST OF GOODS SOLD

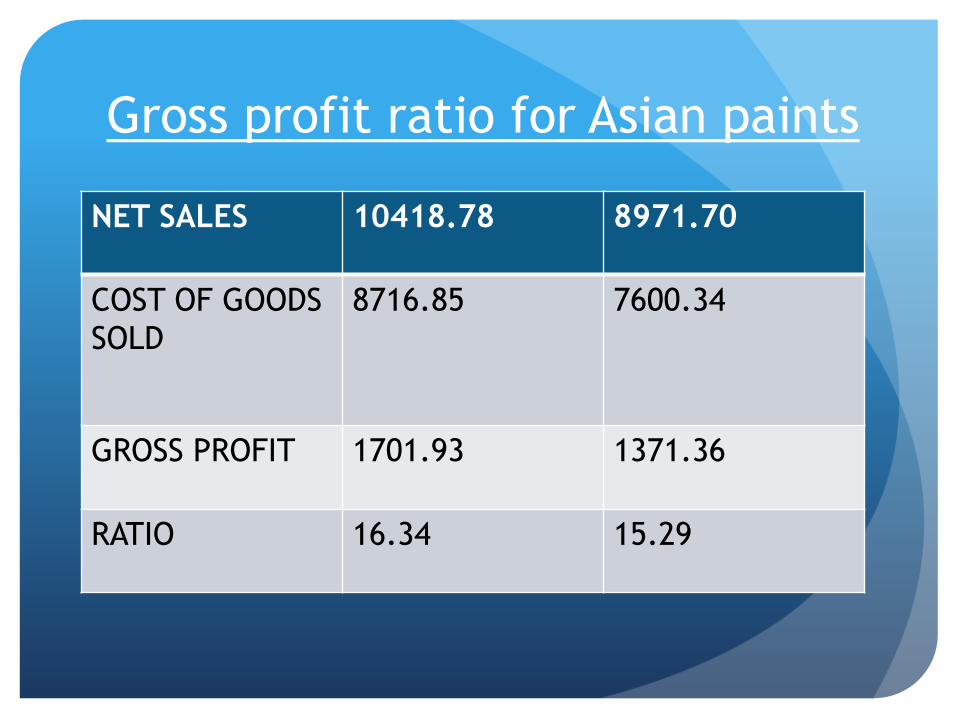

GROSS PROFIT RATIO

Gross profit ratio for Asian paints

NET SALES 10418.78 8971.70

COST OF GOODS

SOLD

8716.85 7600.34

GROSS PROFIT 1701.93 1371.36

RATIO 16.34 15.29

ANALYSIS:

The ideal level of gross profit margin depends on

the industries, how long the business has been

established and other factors.

High gross profit margin indicates that the

company can make a reasonable profit, as long as

it keeps the overhead cost in control.

Low gross profit margin indicates that the business

is unable to control its production cost.

Gross profit ratio is high in current year than that of

previous year which shows increase in profit which

indicates that even the small changes in gross profit can

affect profitability of the company significantly.

In current year it is shown that we have profit to cover

indirect expenses whichever are there for company.

It is showing that there is increase in gross profit ratio

from that of previous year which indicates company’s

growth.

Net Profit Ratio The net profit percentage is the ratio of after-tax profits to

net sales. It reveals the remaining profit after all costs of

production, administration, and financing have been deducted

from sales, and income taxes recognized.

Formula:-

Net Profit Ratio = 𝑁𝑒𝑡 𝑃𝑟𝑜𝑓𝑖𝑡 𝐴𝑓𝑡𝑒𝑟 𝑇𝑎𝑥

𝑁𝑒𝑡 𝑆𝑎𝑙𝑒𝑠x 100

Here,

NPAT = Gross Profit – Operating expenses –Tax

Net Sales = Gross Sales – Sales returns

Significance:-

Useful tool for profitability measurement.

Provides clues to company.

Acts as an indicator of risk/safety and efficiency of the

company.

Importance of net profit to different parties related to

business-

Owners

Investors

Creditors

Competitors

Government

Net Profit ratio =

𝑁𝑃𝐴𝑇

𝑁𝑒𝑡 𝑆𝑎𝑙𝑒𝑠x 100

For The Year

Ended March

2013

In Rs.(Cr)

For The Year

Ended March

2014

In Rs.(Cr)

NPAT 1050.00 1169.06

Net Sales 8971.70 10418.78

Net Profit Ratio 11.70 % 11.22 %

Net Profit Ratio calculated for Asian Paints for the year ended

2013 & 2014

Analysis:- A high ratio indicates the efficient management of the affairs of

business.

Net Profit Ratio can vary significantly from business to business and

can be affected by internal and external factors, Examples of factors

that can affect the net profit ratio are as follows –

Industries & Segments

Selling Price

Cost of Factors

Efficiency

Taxation

Here, In this case of Asian Paints, the Net Profit Ratio has decreased from

11.70% in 2013 to 11.22% in 2014, which means company has failed to convert

its revenue into actual profit.

FIXED ASSET TURNOVER RATIO

Fixed-asset turnover is the ratio of sales (on the profit and loss account) to the value of fixed assets (on the balance sheet). It indicates how well the business is using its fixed assets to generate sales.

Formula:

FIXED ASSET TURNOVER RATIO :-

Net Sales/Fixed Assets

Where, NET SALES = GROSS SALES - SALES RETURN

Purpose of FATR

Ratio establishes a relationship between fixed assets and sales.

Higher ratio is better

Standard ratio:5 times

Comparison for year to year

Not useful for short term

Asian paints fixed assets turnover ratio

TRENDS OBSERVED

TRENDS OBSERVED

TRENDS OBSERVED

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

2013-2014 2012-2013 2011-2012

Trend in Debt Equity Ratio

Series1

10.9

11

11.1

11.2

11.3

11.4

11.5

11.6

11.7

11.8

2013-2014 2012-2013 2011-2012

Trend in Net Profit Ratio

Series1

THANK YOU