Financial Ratios, Formulas, and Calculations – 2017 1 Financial Ratios, Formulas, and Calculations During this course, we will review key financial ratios, formulas, and calculations, including but not limited to: time value of money concepts, mortgage payments, amortization schedules, college planning calculations, retirement planning calculations, Monte Carlo Simulation, bond valuation, return analysis, insurance/annuity calculations, net present value (NPV), and internal rate of return (IRR). With a mastery of this material, you can help your clients enhance project or portfolio returns, maximize cash flow, minimize interest payments, and avoid excessive fees.

Transcript

Financial Ratios, Formulas, and Calculations – 2017 1

Financial Ratios,

Formulas, and Calculations

During this course, we will review key financial ratios, formulas, and calculations, including but not limited to: time value of money concepts,

mortgage payments, amortization schedules, college planning calculations, retirement planning calculations, Monte Carlo Simulation, bond valuation,

return analysis, insurance/annuity calculations, net present value (NPV), and internal rate of return (IRR). With a mastery of this material, you can help

your clients enhance project or portfolio returns, maximize cash flow, minimize interest payments, and avoid excessive fees.

Financial Ratios, Formulas, and Calculations – 2017 2

Table of Contents

I. Future Value ............................................................................................................................... 4 1) FV Concepts 1 ...................................................................................................................................... 4 2) FV Concepts 2 ...................................................................................................................................... 4 3) FV Concepts 3 ...................................................................................................................................... 4 4) Future Value – Compounded Annually 1 ..................................................................................... 4 5) Future Value – Compounded Annually 2 ..................................................................................... 5 6) Future Value – Compounded Annually 3 ..................................................................................... 5 7) Future Value – Compounded Monthly 1 ...................................................................................... 5 8) Future Value – Compounded Monthly 2 ...................................................................................... 6 9) Future Value – Compounded Monthly 3 ...................................................................................... 6

II. Present Value ............................................................................................................................ 7 10) Present Value – Compounded Annually 1 ................................................................................ 7 11) Present Value – Compounded Annually 2 ................................................................................ 7 12) Present Value – Compounded Annually 3 ................................................................................ 7 13) Present Value – Compounded Semiannually 1 ....................................................................... 8 14) Present Value – Compounded Semiannually 2 ....................................................................... 8 15) Present Value – Compounded Semiannually 3 ....................................................................... 8 16) Present Value – Compounded Monthly 1 .................................................................................. 9 17) Present Value – Compounded Monthly 2 .................................................................................. 9

III. Payment .................................................................................................................................. 10 18) Payment Example 1 ...................................................................................................................... 10 19) Payment Example 2 ...................................................................................................................... 10

IV. Term Calculations ................................................................................................................ 10 20) Term Calculation – Compounded Annually 1 ........................................................................ 10 21) Term Calculation – Compounded Annually 2 ........................................................................ 11 22) Term Calculation – Compounded Annually 3 ........................................................................ 11 23) Term Calculation – Compounded Monthly 1 ......................................................................... 11 24) Term Calculation – Compounded Monthly 2 ......................................................................... 12

V. Solving for Interest Rates .................................................................................................... 12 25) Interest Rates Example 1 ............................................................................................................ 12 26) Interest Rates Example 2 ............................................................................................................ 12

VI. Annuities ................................................................................................................................. 13 27) Future Value of an Ordinary Annuity – Compounded Annually ....................................... 13 28) Future Value of an Annuity Due – Compounded Annually................................................. 13 29) Present Value of an Ordinary Annuity – Compounded Annually ..................................... 13 30) Present Value of an Ordinary Annuity – Compounded Semiannually ............................ 14 31) Present Value of an Annuity Due – Compounded Annually ............................................... 14 32) Present Value of an Annuity Due – Compounded Monthly ................................................ 14

Financial Ratios, Formulas, and Calculations – 2017 3

33) Annuity Due with Lump Sum Deposit – Compounded Monthly ....................................... 15 34) PV of Inflation-Adjusted Retirement Needs of an Annuity Due ........................................ 15 35) PV of Inflation-Adjusted Annuity Due – Compounded Annually ...................................... 15

VII. Bond Valuation .................................................................................................................... 16 36) Bond Concept 1 .............................................................................................................................. 16 37) Bond Concept 2 .............................................................................................................................. 16 38) Bond Valuation 1 ........................................................................................................................... 16 39) Bond Valuation 2 ........................................................................................................................... 16

XI. Cost of Capital ........................................................................................................................ 21 52) Cost of Capital – Cost of Equity ........................................................................................................ 21 53) Cost of Capital – Weighted Average Cost of Capital .............................................................. 21

XII. Net Present Value ................................................................................................................ 21 54) NPV Concept 1 ................................................................................................................................ 21 55) NPV Concept 2 ................................................................................................................................ 22 56) NPV Example 1 ............................................................................................................................... 22 57) NPV Example 2 ............................................................................................................................... 22

XIII. Internal Rate of Return .................................................................................................... 23 58) IRR Concept 1 ................................................................................................................................. 23 59) IRR Concept 2 ................................................................................................................................. 23 60) IRR Example 1 ................................................................................................................................ 23

XIV. Statistics ............................................................................................................................... 24 61) Statistics – Normal Distribution ................................................................................................ 24 62) Statistics - Sharpe Ratio .................................................................................................................................... 24

Financial Ratios, Formulas, and Calculations – 2017 4

I. Future Value

1) FV Concepts 1 The process of discounting or finding the present value of a cash flow to be received in the future is really the reverse of compounding. True or False?

2) FV Concepts 2 One of the potential benefits of investing early for retirement is that an investor can receive greater benefits from the compounding of interest. True or False?

3) FV Concepts 3 Disregarding risk, if money has time value, the future value of some amount of money always

will be more than the amount originally invested, and the present value of some amount to be

received in the future is always less than that future amount to be received. True or False?

4) Future Value – Compounded Annually 1 John purchased a rare gold coin for $100,000. He expects it to increase in value at a rate of 8.5%

compounded annually for the next 7 years. How much will the coin be worth at the end of the

seventh year if his expectations are correct?

Financial Ratios, Formulas, and Calculations – 2017 5

5) Future Value – Compounded Annually 2 What is the future value of $11,000 invested for 30 years assuming an annual interest rate of

12.5%?

6) Future Value – Compounded Annually 3 What is the future value of $13,500 invested for 15 years assuming an annual interest rate of

6.5%?

7) Future Value – Compounded Monthly 1 Fred invested $25,000 in an interest-bearing promissory note earning a 9% annual rate of

interest compounded monthly. How much will the note be worth at the end of 8 years assuming

all interest is reinvested at the 9% rate?

Financial Ratios, Formulas, and Calculations – 2017 6

8) Future Value – Compounded Monthly 2 What is the future value of $15,000 invested for 18 years assuming an annual interest rate of

12%, compounded monthly?

9) Future Value – Compounded Monthly 3 Calculate the future value of $1,000 invested for 100 years assuming an annual interest rate of

8%, compounded monthly.

Financial Ratios, Formulas, and Calculations – 2017 7

II. Present Value

10) Present Value – Compounded Annually 1 Sandy wants to give her daughter $50,000 to start her own business in 10 years. How much

should she invest today at an annual interest rate of 9% (compounded annually) to have

$50,000 in 10 years?

11) Present Value – Compounded Annually 2 Calculate the present value of $10 million to be received in 50 years assuming an annual interest

rate of 10%.

12) Present Value – Compounded Annually 3 What is the present value of $75,000 to be received in 20 years if the estimated annual interest

rate is going to be 6%?

Financial Ratios, Formulas, and Calculations – 2017 8

13) Present Value – Compounded Semiannually 1 John expects to receive $105,000 in 7 years. What is the current value of this sum if it is discounted at 9% compounded semiannually?

14) Present Value – Compounded Semiannually 2 Penelope expects to receive $10,000,000 from a rich uncle in 7 years. What is the current value of this sum if it is discounted at 6% compounded semiannually?

15) Present Value – Compounded Semiannually 3 Robert expects to receive $400,000 from a trust fund in 12 years. What is the current value of this fund if it is discounted at 8% compounded semiannually?

Financial Ratios, Formulas, and Calculations – 2017 9

16) Present Value – Compounded Monthly 1 Billy Mack expects to receive $105,000 in 9 years. His opportunity cost is 10% compounded monthly. What is this sum worth to Billy today?

17) Present Value – Compounded Monthly 2 Calculate the present value of $30,000 to be received in 5 years assuming an annual interest

rate of 12%, compounded monthly.

Financial Ratios, Formulas, and Calculations – 2017 10

III. Payment

18) Payment Example 1 If a 5-year regular annuity has a present value of $1,000, and if the interest rate is 10 percent, what is the amount of each annuity payment?

19) Payment Example 2 Suppose the present value of a 2-year ordinary annuity is $100. If the discount rate is 10 percent, what must be the annual cash flow?

IV. Term Calculations

20) Term Calculation – Compounded Annually 1 Terry purchased a painting for $28,000. Today, he sold the painting for $50,000. Terry estimated his average annual opportunity cost on the painting was 11%. Approximately how many periods did Terry own the painting?

Financial Ratios, Formulas, and Calculations – 2017 11

21) Term Calculation – Compounded Annually 2 Paul purchased an antique for $15,000. Today, he sold the antique for $71,000. Paul estimated the average annual compound rate of return on the antique was 9%. Approximately how many periods did Kerry own the antique?

22) Term Calculation – Compounded Annually 3 Barry purchased several gold coins for $3,000. Today, he sold the coins for $5,500. Barry estimated the average annual rate of return (compounded monthly) on the coins was 15%. Approximately how many periods did Barry own the coins?

23) Term Calculation – Compounded Monthly 1 Today, Stewart put all of his cash into an account earning an annual interest rate of 10% compounded monthly. Assuming he makes no withdrawals from or additions to this account. Approximately how many periods must Stewart wait to double his money? (Suggestion: Use $1 as the amount to be invested.)

Financial Ratios, Formulas, and Calculations – 2017 12

24) Term Calculation – Compounded Monthly 2 Today, Robert put all of his cash into an account earning an annual interest rate of 15% compounded monthly. Assuming he makes no withdrawals from or additions to this account. Approximately how many periods must Robert wait to double his money? (Suggestion: Use $1 as the amount to be invested.)

V. Solving for Interest Rates

25) Interest Rates Example 1 In the 60’s, the average tuition for one year at a state university was $1,800. Thirty years later, in 1988, the average cost was $13,700. What was the growth rate in tuition over the 30-year period?

26) Interest Rates Example 2 Assuming you need $50,000 five years from now to buy a new Lexus and you currently have $25,000, what annual rate of return would you need to achieve your goal?

Financial Ratios, Formulas, and Calculations – 2017 13

VI. Annuities

27) Future Value of an Ordinary Annuity – Compounded Annually Rudy has been investing $1,000 at the end of each year for the past 20 years in an equity mutual fund. How much is the fund worth now assuming he has earned 12.5% compounded annually on his investment?

28) Future Value of an Annuity Due – Compounded Annually Hector has been investing $2,000 at the beginning of each year for the past 27 years. How much has he accumulated assuming he has earned 8% compounded annually on his investment?

29) Present Value of an Ordinary Annuity – Compounded Annually Phillip expects to receive $8,000 at the end of each of the next 5 years from a trust fund. His opportunity cost is 11.5% compounded annually. What are these payments worth today?

Financial Ratios, Formulas, and Calculations – 2017 14

30) Present Value of an Ordinary Annuity – Compounded Semiannually Jim, who was injured in an automobile accident, won a judgment that provides him $3,500 at the end of each 6-month period for the next 6 years. If the escrow account that holds Jim’s settlement award earns an average annual rate of 11 % compounded semiannually, how much was the defendant initially required to deposit so that Jim would be compensated for his injuries?

31) Present Value of an Annuity Due – Compounded Annually Julie wants to withdraw $10,000 at the beginning of each year for the next 9 years. She wants to have $50,000 left at the end of the 9 years. She expects to earn 11.5% compounded annually on her investment. What lump sum should Julie deposit today?

32) Present Value of an Annuity Due – Compounded Monthly Carla wants to withdraw $5,000 at the beginning of each month for the next 10 years. She expects to earn 10% compounded monthly on her investments. What lump sum should she deposit today?

Financial Ratios, Formulas, and Calculations – 2017 15

33) Annuity Due with Lump Sum Deposit – Compounded Monthly Alex received an inheritance of $500,000. He wants to withdraw equal periodic payments at the beginning of each month for the next 15 years. He expects to earn 12% compounded monthly on his investments. How much can he receive each month?

34) PV of Inflation-Adjusted Retirement Needs of an Annuity Due Billy and Marlene are ready to retire. They want to receive the equivalent of $25,000 in today’s dollars at the beginning of each year for the next 20 years. They assume inflation will average 4% over the long run, and they can earn 10% compounded annually on investments. What lump sum do they need to invest today to attain their goal?

35) PV of Inflation-Adjusted Annuity Due – Compounded Annually Barbara needs an income stream equivalent to $50,000 in today’s dollars at the beginning of each year for the next 12 years to maintain her standard of living. Assume inflation will average 4.5% and she can earn 12% compounded annually on investments. What lump sum does she need to invest today to fund her needs?

Financial Ratios, Formulas, and Calculations – 2017 16

VII. Bond Valuation

36) Bond Concept 1 As interests rates increase, the value of a bond increases. True or False?

37) Bond Concept 2 When the coupon rate of a bond exceeds the going market rate of interest for a comparable bond with similar characteristics, does the bond trade at a discount, a premium, or at par?

38) Bond Valuation 1 You intend to purchase a 10-year, $1,000 face value bond that pays interest of $60 every 6 months. If your single annual required rate of return is 10 percent with semiannual compounding, how much should you be willing to pay for this bond?

39) Bond Valuation 2 Assume that you wish to purchase a 20-year bond that has a maturity value of $1,000 and makes semiannual interest payments of $40. If you require a 10 percent simple yield to maturity on this investment, what is the maximum price you should be willing to pay for the bond?

Financial Ratios, Formulas, and Calculations – 2017 17

VIII. Equity Valuation

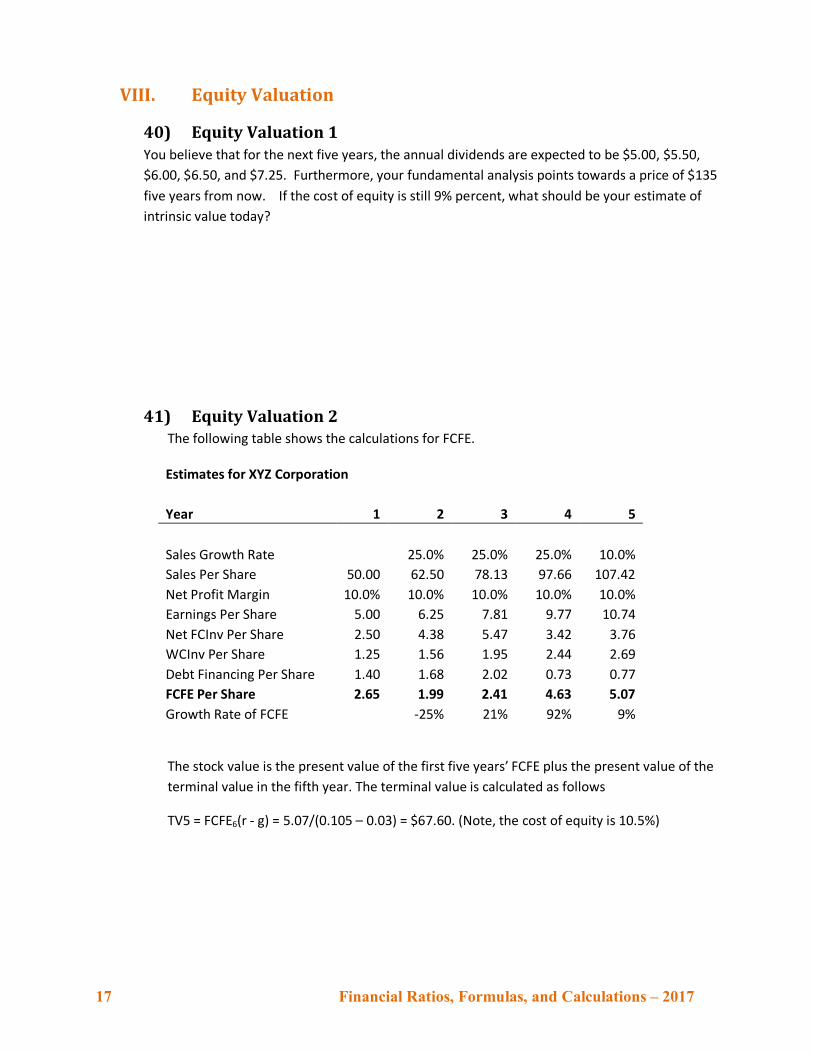

40) Equity Valuation 1 You believe that for the next five years, the annual dividends are expected to be $5.00, $5.50, $6.00, $6.50, and $7.25. Furthermore, your fundamental analysis points towards a price of $135 five years from now. If the cost of equity is still 9% percent, what should be your estimate of intrinsic value today?

41) Equity Valuation 2 The following table shows the calculations for FCFE.

Estimates for XYZ Corporation Year 1 2 3 4 5 Sales Growth Rate 25.0% 25.0% 25.0% 10.0% Sales Per Share 50.00 62.50 78.13 97.66 107.42 Net Profit Margin 10.0% 10.0% 10.0% 10.0% 10.0% Earnings Per Share 5.00 6.25 7.81 9.77 10.74 Net FCInv Per Share 2.50 4.38 5.47 3.42 3.76 WCInv Per Share 1.25 1.56 1.95 2.44 2.69 Debt Financing Per Share 1.40 1.68 2.02 0.73 0.77 FCFE Per Share 2.65 1.99 2.41 4.63 5.07 Growth Rate of FCFE -25% 21% 92% 9%

The stock value is the present value of the first five years’ FCFE plus the present value of the terminal value in the fifth year. The terminal value is calculated as follows

TV5 = FCFE6(r - g) = 5.07/(0.105 – 0.03) = $67.60. (Note, the cost of equity is 10.5%)

Financial Ratios, Formulas, and Calculations – 2017 18

IX. Return Calculations

42) Return Calculation 1 Stock A has annual returns of 10.7%, 12.9% and 23.2% for the fiscal years ended December 31,

of 2005, 2006, and 2007. What was the arithmetic average return over this three-year period?

43) Return Calculation 2 Stock A has annual returns of 20.7%, and -20.7% for the fiscal years ended December 31, 2006,

and 2007. What was the arithmetic average return over this two-year period?

44) Return Calculation 3 Stock B has annual returns of 10.7%, 12.9% and 23.2% for the fiscal years ended December 31,

of 2005, 2006, and 2007. What was the geometric average return over this three-year period?

45) Return Calculation 4 Stock A has annual returns of 20.7%, and -20.7% for the fiscal years ended December 31, of

2006, and 2007. What was the geometric average return over this two-year period?

Financial Ratios, Formulas, and Calculations – 2017 19

46) Return Calculation 5 You invested $1,000,000 ten years ago. You now have $1,750,000. What was your average

annual geometric rate of return over the 10-year period?

X. Mortgage Payments

47) Mortgages – Monthly Payment Ed Johnson recently purchased a house for $250,000. He made a down payment of 20% and financed the balance over 30 years at 7%. How much will Ed’s monthly mortgage payment be?

48) Mortgages – Interest Ed Johnson recently purchased a house for $250,000. He made a down payment of 20% and financed the balance over 30 years at 7%. How much of the first payment will go towards interest?

Financial Ratios, Formulas, and Calculations – 2017 20

49) Mortgages – Principal Ed Johnson recently purchased a house for $250,000. He made a down payment of 20% and financed the balance over 30 years at 7%. How much of the first payment will go towards principal?

50) Mortgages – Interest Deduction Ed Johnson recently purchased a house for $250,000 on June 30th. He made a down payment of 20% and financed the balance over 30 years at 7%. How much interest will Ed be able to deduct on his tax return this year?

51) Mortgage – Total Interest Payment Ed Johnson recently purchased a house for $250,000 on June 30th. He made a down payment of 20% and financed the balance over 30 years at 7%. How much total interest will he pay over the life of the loan? So, how many times (total interest and principal) will he pay for his house over the life of the loan?

Financial Ratios, Formulas, and Calculations – 2017 21

XI. Cost of Capital

52) Cost of Capital – Cost of Equity Using the following information, estimate the cost of equity for XYZ Corporation. (Hint – Use the CAPM)

• XYZ’s beta is 1.2, the risk-free rate is 4 percent and the market risk premium is 5.5 percent.

• XYZ’s expected long-term growth rate is 3%.

53) Cost of Capital – Weighted Average Cost of Capital Kline Company (KC) has a cost of debt of 7.0 (pre-tax) percent and a cost of equity of 12.0 percent. The firm’s capital structure is 35% debt and 65% equity and expects this structure to remain in the future. The tax rate is 35 percent. Based on the information presented above, what is the weighted average cost of capital for KC?

XII. Net Present Value

54) NPV Concept 1 If the calculated NPV is negative, then which of the following must be true? The discount rate used is:

A. Equal to the internal rate of return.

B. Too high.

C. Greater than the internal rate of return.

D. Too low.

E. Less than the internal rate of return,

Financial Ratios, Formulas, and Calculations – 2017 22

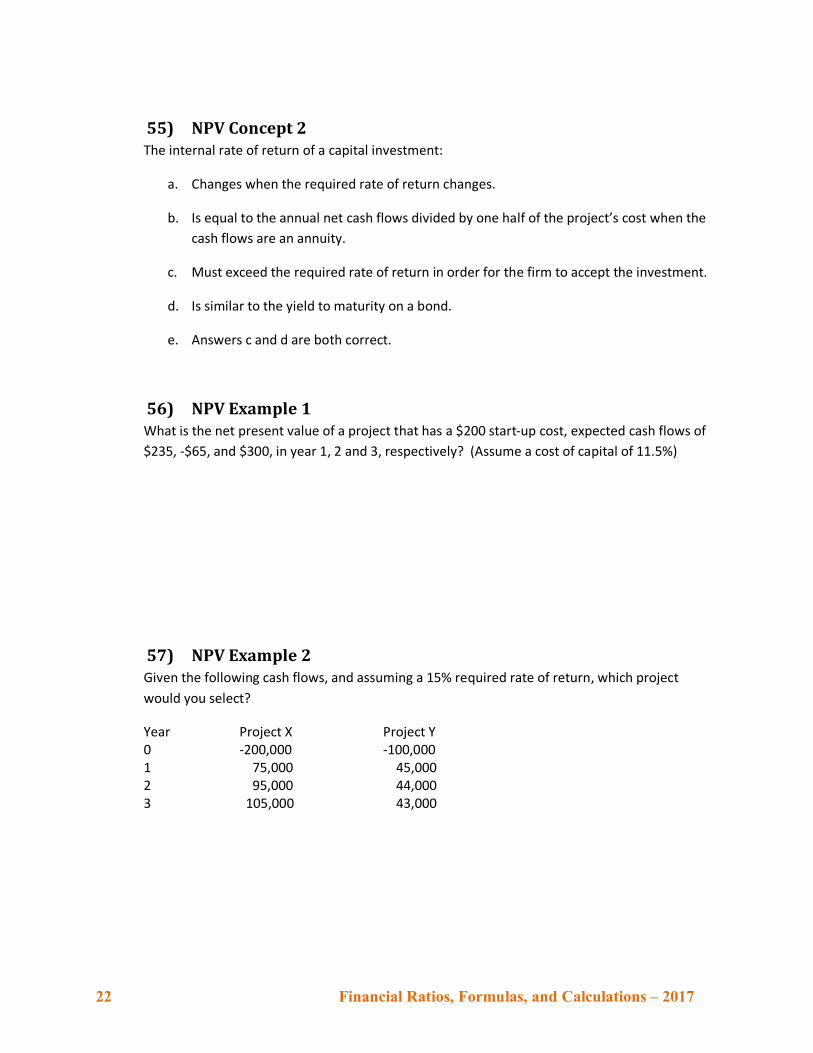

55) NPV Concept 2 The internal rate of return of a capital investment:

a. Changes when the required rate of return changes.

b. Is equal to the annual net cash flows divided by one half of the project’s cost when the cash flows are an annuity.

c. Must exceed the required rate of return in order for the firm to accept the investment.

d. Is similar to the yield to maturity on a bond.

e. Answers c and d are both correct.

56) NPV Example 1 What is the net present value of a project that has a $200 start-up cost, expected cash flows of $235, -$65, and $300, in year 1, 2 and 3, respectively? (Assume a cost of capital of 11.5%)

57) NPV Example 2 Given the following cash flows, and assuming a 15% required rate of return, which project would you select?

Year Project X Project Y 0 -200,000 -100,000 1 75,000 45,000 2 95,000 44,000 3 105,000 43,000

Financial Ratios, Formulas, and Calculations – 2017 23

XIII. Internal Rate of Return

58) IRR Concept 1 The internal rate of return is the discount rate which equates the present value of the cash outflows (or costs) with the present value of the cash inflows. True or False?

59) IRR Concept 2 The internal rate of return (IRR) method equates the present value of cash inflows with the present value of cash outflows by discounting all of the cash flows at the firm’s weighted average cost of capital. True or False?

60) IRR Example 1 An insurance firm agrees to pay you $3,310 at the end of 20 years if you pay premiums of $100 per year at the end of each year of the 20 years. Find the internal rate of return to the nearest whole percentage point.

Financial Ratios, Formulas, and Calculations – 2017 24

XIV. Statistics

61) Statistics – Normal Distribution ABC Company has a mean return of 11% for the past five years and a standard deviation of 8%.

Assuming a normal distribution, what is the chance that ABC Company will have a return less

than 3%?

62) Statistics - Sharpe Ratio You are trying to decide which mutual fund to invest in, YeeHaw MF or Castle in the Sky MF.

YeeHaw has an average annual return of 15% for the trailing 10 year period, and a standard

deviation of 7.5. Castle in the Sky has an average annual return of 17% for the trailing 10 year

period, and a standard deviation of 15. The risk free rate, on average, over the same period of

time was 4.65%. Which fund would you select, assuming that you are attempting to maximize