FOR OFFICIAL USE ONLY FINANCIAL SECTOR ASSESSMENT PARAGUAY MAY 2006 LATIN AMERICA & THE CARIBBEAN REGION VICE PRESIDENCY FINANCIAL SECTOR VICE PRESIDENCY BASED ON THE JOINT IMF-WORLD BANK FSAP 1. Monetary Fund/World Bank Financial Sector Assessment Program (FSAP), a joint IMFW team conducted an assessment o f the financial sector in Paraguay during two missions that visited Asuncion from April 18 to 29 and from July 5 to 15,2005.' The principal objectives of the mission were to assist the authorities in assessing the development needs o f the financial sector and identifying potential vulnerabilities of financial institutions and markets to macroeconomic shocks, as well as the risks to macroeconomic stability from weaknesses and shortcomings in the financial sector? The members of the FSAP team wish to express their appreciation to the Paraguayan authorities, and to the staff of all the institutions that they visited and worked with, for their hospitality and exemplary c~operation.~ At the request o f the Paraguayan government, in the context o f the International The FSAP team included Giovanni Majnoni (mission chief, World Bank), Armando Morales (deputy mission chief, IMF), Ernesto Aguirre, Mario Guadamillas; Olivier Hassler, Mariano Lanfianconi, Martin Naranjo, Lisa Taber, Flavio Rabelo (consultant) and Florencia Liporaci (staff assistant) (all World Bank); Felix Fischer, Giancarlo Gasha, Claudia Jadrisevic, Tobias Roy, Ernesto Livacic (consultant), Camilla Ferenius (consultant), Jose Benjamin Escobar (consultant) (all IMF). In parallel with the first FSAP mission, Adolfo Rouillon (consultant) conducted the assessment o f The Principles and Guideline for Effective Insolvency and Creditor Rights Systems. The missions were assisted by Luis Duran-Downing and Peter Hansen, respectively, the IMF and the World Bank Resident Representative. Assessments were conducted of compliance with the Basel Core Principles for Efective Banking Supervision (BCP), the IMF Code of Good Practices on Transparency in Monetary and Financial Policies, and the Core Principles for Systemically Important Payment Systems (CPSIPSS). A parallel assessment of observance o f the World Bank Principles and Guidelinefor Effective Insolvency and Creditor Rights Systems was conducted by a World Bank team, and the conclusions have been incorporated into the assessment. Findings fiom an assessment of compliance with the Principles for Anti-Money Laundering and Combating the Finance of Terrorism (AMLKFT), to be conducted by the Financial Action Task Force o f South America (GAFISUD), will take place in the second half o f the year, and the results will be incorporated into the FSAP assessment once they become available. The team held meetings with the Minister and Vice Minister o f Finance, the Minister Adviser to the President, the Central Bank President and Central Bank Board members and officials, the Superintendent o f Banks and Insurance, the Superintendent o f the Securities Market, and other senior officials o f the Ministry of Finance, Tax Authority, and national regulatory authorities for banks, insurance and market regulation. The team also met (continued) 1 2 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

FOR OFFICIAL USE ONLY

FINANCIAL SECTOR ASSESSMENT PARAGUAY MAY 2006

LATIN AMERICA & THE CARIBBEAN REGION VICE PRESIDENCY FINANCIAL SECTOR VICE PRESIDENCY

BASED ON THE JOINT IMF-WORLD BANK FSAP

1. Monetary Fund/World Bank Financial Sector Assessment Program (FSAP), a jo int I M F W team conducted an assessment o f the financial sector in Paraguay during two missions that visited Asuncion from April 18 to 29 and from July 5 to 15,2005.' The principal objectives o f the mission were to assist the authorities in assessing the development needs o f the financial sector and identifying potential vulnerabilities o f financial institutions and markets to macroeconomic shocks, as wel l as the risks to macroeconomic stability from weaknesses and shortcomings in the financial sector? The members o f the FSAP team wish to express their appreciation to the Paraguayan authorities, and to the staff o f all the institutions that they visited and worked with, for their hospitality and exemplary c~operat ion.~

At the request o f the Paraguayan government, in the context o f the International

The FSAP team included Giovanni Majnoni (mission chief, Wor ld Bank), Armando Morales (deputy mission chief, IMF), Ernesto Aguirre, Mario Guadamillas; Olivier Hassler, Mariano Lanfianconi, Mart in Naranjo, Lisa Taber, Flavio Rabelo (consultant) and Florencia Liporaci (staff assistant) (all Wor ld Bank); Felix Fischer, Giancarlo Gasha, Claudia Jadrisevic, Tobias Roy, Ernesto Livacic (consultant), Camilla Ferenius (consultant), Jose Benjamin Escobar (consultant) (all IMF). In parallel with the f i rs t FSAP mission, Adolfo Rouil lon (consultant) conducted the assessment o f The Principles and Guideline for Effective Insolvency and Creditor Rights Systems. The missions were assisted by Luis Duran-Downing and Peter Hansen, respectively, the IMF and the Wor ld Bank Resident Representative.

Assessments were conducted o f compliance with the Basel Core Principles for Efective Banking Supervision (BCP), the IMF Code of Good Practices on Transparency in Monetary and Financial Policies, and the Core Principles for Systemically Important Payment Systems (CPSIPSS). A parallel assessment o f observance o f the Wor ld Bank Principles and Guideline for Effective Insolvency and Creditor Rights Systems was conducted by a Wor ld Bank team, and the conclusions have been incorporated into the assessment. Findings f i o m an assessment o f compliance with the Principles for Anti-Money Laundering and Combating the Finance of Terrorism (AMLKFT), to be conducted by the Financial Action Task Force o f South America (GAFISUD), will take place in the second ha l f o f the year, and the results will be incorporated into the FSAP assessment once they become available.

The team held meetings with the Minister and Vice Minister o f Finance, the Minister Adviser to the President, the Central Bank President and Central Bank Board members and officials, the Superintendent o f Banks and Insurance, the Superintendent o f the Securities Market, and other senior officials o f the Ministry o f Finance, Tax Authority, and national regulatory authorities for banks, insurance and market regulation. The team also met

(continued)

1

2

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

- 2 -

I. OVERALL ASSESSMENT AND KEY RECOMMENDATIONS

2. opportunity to address key financial vulnerabilities that would otherwise be an obstacle to future growth. After a decade o f financial instability that has dramatically reduced the size o f the banking system and curtailed the number o f active institutions by two thirds and the level o f credit to 13 percent o f GDP, macroeconomic policy has succeeded in reducing inflation while restoring economic growth. Lingering lack o f trust in financial institutions, weak corporate governance and contract enforcement, and lack o f confidence in the government’s capacity to fulfill i t s obligations constitute an obstacle to a wider supply o f financial services (Figure 1). This hinders the development o f long-term financing alternatives and saving instruments, and conspires against adequate social security protection and a lower cost o f financial transactions. By modernizing the legal and regulatory frameworks, the authorities would start developing the sound financial infrastructure required for adequate financial intermediation.

The recovery o f economic activity after a decade of stress provides a window of

3. problems that were made evident by the prolonged financial turmoil, including upgrading current norms towards sound practices and international standards. However, continuing a piece-meal approach would not only impair the effectiveness o f measures that have been undertaken, but would also make the overall reform process less credible, exposing the authorities to pressure from different interest groups to backtrack on government decisions or delay the introduction o f prudential measures, as i s occurring with the implementation o f upgraded prudential regulations envisaged for 2007 (Resolucibn 8/03). The concerted effort o f revising the banking legislation and regulations was initiated in 2003 with the approval o f a new banking resolution framework, the introduction o f limits to the operations o f the state-owned National Development Bank (BNF), and the approval o f Resolucibn 8/03.The main objective o f the government measures has been to introduce safeguards to prevent inappropriate lending practices, including by the BNF, and increase the supervisors’ oversight capacity.

The government has adopted partial measures to solve some of the structural

4. building trust in the financial system and reversing disintermediation, reducing the large banks’ reluctance to lend, and lengthening the maturity o f loans and deposits. In this regard, the envisaged upgrade o f the banking legal framework would spur the effectiveness o f prudential regulation and oversight. To complement th is effort, upgraded prudential regulations (Resolucibn 8/03) should be introduced in l ine with the approved schedule; the central bank should adopt an action plan to strengthen banking supervision within a strict timetable; supervision o f other financial agents (cooperatives, pensions) must

A more comprehensive effort towards financial reform would contribute to

with officials o f many o f the domestic and foreign-owned banks, with numerous nonbank financial institutions including cooperatives, finance companies and insurance companies, with the Asunci6n Stock Exchange, managers o f the Instituto de Previsidn Social (IPS), members o f the legal and auditing professions, and some o f the listed public companies.

- 3 -

be promptly introduced; the BNF must be -at the minimum- drastically restructured; and a strategy to facilitate long-term financing must be designed.

5. Reported capital adequacy ratios (CAR) for the private banking system appear sufficient to support the current levels of fmancial intermediation, but capitalization i s overstated and shows high variance across banks. High liquidity explains the average CAR o f 2 1.8 percent for private foreign banks at the end o f 2004, while compliance o f private domestic banks with capital requirements (CAR o f 12.5 percent) is helped by softer prudential requirements compared with international prudential standards (Figure 2). Segmentation in the Paraguayan financial system has deepened in recent years following a decade o f economic and financial instability, with foreign banks withdrawing from the retail market to cater to the tradable sector’s needs (mainly soy bean producers), and surviving domestic banks (and credit cooperatives, see below) absorbing part o f the retail clientele.

6. The rapid growth of financial intermediation by credit cooperatives merits prompt implementation of new prudential regulations in coordination with the Superintendency o f Banks. Credit cooperatives, until recently largely unregulated, are gaining higher systemic relevance and they have achieved participation unequaled in the rest o f Latin America, with a share o f 11 o f total deposits and 18 percent o f credits to the productive sector. Improving the quality and the quantity o f information provided by the cooperative sector has become a priority not only for supervisory purposes but also for the adequate measurement and control o f monetary aggregates. Progress has been made on the regulatory front with the formalization o f the new role o f INCOOP through the law 2 157/03 and with the regulations issued by INCOOP in December 2004 and in January 2005. However, a basic implementation framework and coordination arrangements with the Superintendency o f Banks are sti l l absent, raising uncertainty about timely further progress to consolidate effective supervision o f this sector. A clear prioritization o f objectives should include focusing efforts on the largest financial cooperatives (about 25-30 institutions) at the initial stage.

7. resolute eradication of moral hazard in the financial sector. This bank had a long history o f mismanagement, politically-motivated lending and lack o f accountability, until i t s operations were drastically restricted by law in 2003. Since then, BNF operations have declined and the bank i s not anymore o f systemic importance. Therefore, the only justification to restructure the bank rather than closing it would be to concentrate on sectors not served by the market and to eliminate all potential risk to use the bank again as a vehicle for political favors. A decisive restructuring would entail transferring the bad-loan portfolio to a trust fund in charge o f maximizing loan recovery, focusing its activities in areas not covered by private institutions, and strengthening governance rules. Prompt action would constitute a strong signal to the market o f the authorities’ intention to modernize the financial system.

A drastic restructuring of the BNF would constitute a decisive step towards a

8. introduction of a prudential framework for pension funds; basic conditions for debt management; and the rationalization of existing institutional arrangements, would help increase the availability of long-term financing. Strengthening creditor rights and

A wide-ranging strategy comprising an overhaul o f insolvency procedures; the

- 4 -

streamlining insolvency procedures require the overhaul o f procedures for the execution o f collateral and foreclosure. Allowing a better use o f pension funds to finance long-term investment alternatives requires the designation o f an authority in charge o f regulating governance, solvency, transparency, and investment policies. Introducing appropriate debt management, which would help recover credibility in the capacity o f the government to fulfill its obligations, would not be possible without an orderly legal framework and a systematic effort to identify al l existing government obligations. Finally, recent efforts to consolidate second-tier institutional arrangements to channel long-tern financing would not be productive if new distortions are introduced, such as using pensions to finance productive activities directly.

9. Socia2 (IPS), the mandatory pension fund. In this regard, the prohibition against IPS investing in government securities should be removed, and arrangements to repay long overdue government obligations to the IPS should be put in place. More generally, the current surplus o f the IPS plus the expected positive cash flow over the next two decades should not be used to compensate for the deficit in other bankrupt pension funds (Caja Bancaria), which should be dealt with separately through appropriate resolution procedures, currently absent in the pension legislation.

Clear risk management guidelines need to be defined for the Instituto de Prevision

10. An overhaul of the Paraguayan payments system i s a necessary precondition for the development of a capital market. Major aspects to be improved in the legal framework are: settlement finality protection o f the systems against bankruptcy procedures, legal basis for dematerialization and/or immobilization o f securities, legal basis for custody arrangements, legal basis for netting arrangements, legal definition o f rep0 operations, legal underpinning o f the pledge and legal basis for electronic documents and signatures. The approval o f a comprehensive payments system law should be considered as a priority by the central bank.

11. OVERVIEW OF THE FINANCIAL SYSTEM

A. Macro Financial Background

1 1. low growth and financial instability. Paraguay’s record o f real GDP and per-capita GDP growth compares unfavorably with that o f most Lat in American countries. Following financial liberalization in the late 80s and early 9Os, the emergence o f widespread inappropriate lending practices -led by the state-owned National Development Bank (BNF) - translated into financial instability. Excessive risk exposure by financial institutions remained undetected in the context o f a weak supervisory framework and fragile institutions. Prior to the crisis, the number o f banks had increased from 26 to 35. Between 1988 and 1995, the number o f finance companies increased from 28 to 63 and the ratio o f credit over GDP doubled. Following the failure o f many institutions throughout the crisis period, the ratio o f credit over GDP declined to pre-liberalization levels. Deposits generally remained within the system, until intermediation started to decline in 2002 presumably as a response to the failure o f a systemically important institution (Banco Alemhn), the severe deterioration o f the loan portfolio o f the BNF (Table 1) and the confluence o f the crises in Brazil and Argentina.

Paraguay’s economic performance during the past 10 years has been marred by

- 5 - .

12. The quality of the business environment remains a serious obstacle to sustained credit growth and the lack of diversification heightens the vulnerability of the financial system to fiscal and external shocks. Institutional quality, as measured by indicators o f governance, corruption, judicial efficiency, creditor r ights and informality o f the economy compares unfavorably with the Latin American region average (Figure 1). At the same time, tax revenues, at 12 per cent o f GDP, do not adequately reflect all obligations with the private sector and other public institutions (Central Bank, IPS) and contingent liabilities could seriously compromise the fiscal balance. External shocks constitute an additional source o f vulnerability. In particular, economic l i n k s with Brazil make Paraguayan economic activity and balance o f payments highly dependent on the evolution o f economic activity and exposed to the risk o f sudden depreciation o f the exchange rate o f i t s large neighbor.

13. spreads in domestic currency remain high at about 20 percentage points as the fall o f deposit interest rates (induced by banks trying to discourage deposits in the face o f the lack o f credit opportunities) exceeds any decline in lending interest rates. After the shock represented by the liquidation in June 2002 o f the third largest bank in Paraguay (Banco Alerncin), bank credit has started to grow again. Domestic banks lend more aggressively to increase market share by taking advantage o f some economic recovery and the reported retrenchment by foreign banks. Small-scale deposits and loans appear to have migrated to local banks and, increasingly, to financial cooperatives. Large foreign currency deposits have somewhat concentrated in foreign banks leaving domestic institutions to face systemic risk associated with retail deposits and lending to borrowers who operate in the domestic market that i s more exposed to shocks arising from fluctuations in economic activity.

Credit growth has resumed in 2003-4 with new lending patterns. Interest rate

14. financial system which i s now dominated by banks with foreign ownership. Between 1995 and 2005, the number o f banks fell from 34 to 13 and the number o f finance companies from 65 to 14. As a result o f the consolidation in the financial system and a flight-to-quality shift o f deposits, the participation o f foreign institutions in the Paraguayan banking system, as measured by the share o f banking assets, increased from 54 percent in 1995 to 74 percent in March 2005. However, banks have lost market share to credit cooperatives, because o f a migration o f depositors as a response to negative interest rates offered by banks in combination with higher yields (and credit access) offered by cooperatives, helped by lower regulatory costs. In the period 2000-04, banks’ assets have fallen from 73 to 67 percent o f the Paraguayan financial system, compared with an increase from 8 to 12 percent for the credit cooperatives’ assets. Other financial institutions such as finance companies, mainly providers o f consumer loans, have remained at a 7 percent share o f total market (Table 1).

A decade of severe banking crises has modified drastically the structure of the

111. COMMERCIAL BANKS SOUNDNESS

15. Apparent high capitalization of the private banking system i s explained by less stringent prudential standards, a low level of credit and a high share of risk-free liquid assets. At the end o f 2004, the average CAR for private foreign banks was 2 1.8 percent and that o f private domestic banks 12.5 percent. Some foreign banks are willing to hold more capital to be allowed to lend to large customers and at the same time comply with domestic regulations. The divergence o f solvency ratios between domestic and foreign banks may also

- 6 -

be the result o f foreign banks following prudential practices more in l ine with international standards relative to domestic banks (therefore, although they may be holding capital in l ine with international standards, i t would appear that they are keeping capital adequacy ratios wel l in excess o f domestic standards). Moreover, if credit to the private sector starts to increase capital requirements would increase accordingly, and capital adequacy would deteriorate.

16. The share of nonperforming loans plus restructured and refinanced loans remains above 20 percent but profitability i s recovering. This evolution i s consistent with the increasing reluctance o f banks to lend. The reduction in financial intermediation up to 2003 resulted in declining profitability, with signs o f a turnaround observed once bank lending growth resumed. Although efficiency indicators are superior for foreign banks, domestic banks’ higher profitability can be explained by increased credit growth and higher operating margins in domestic currency lending.

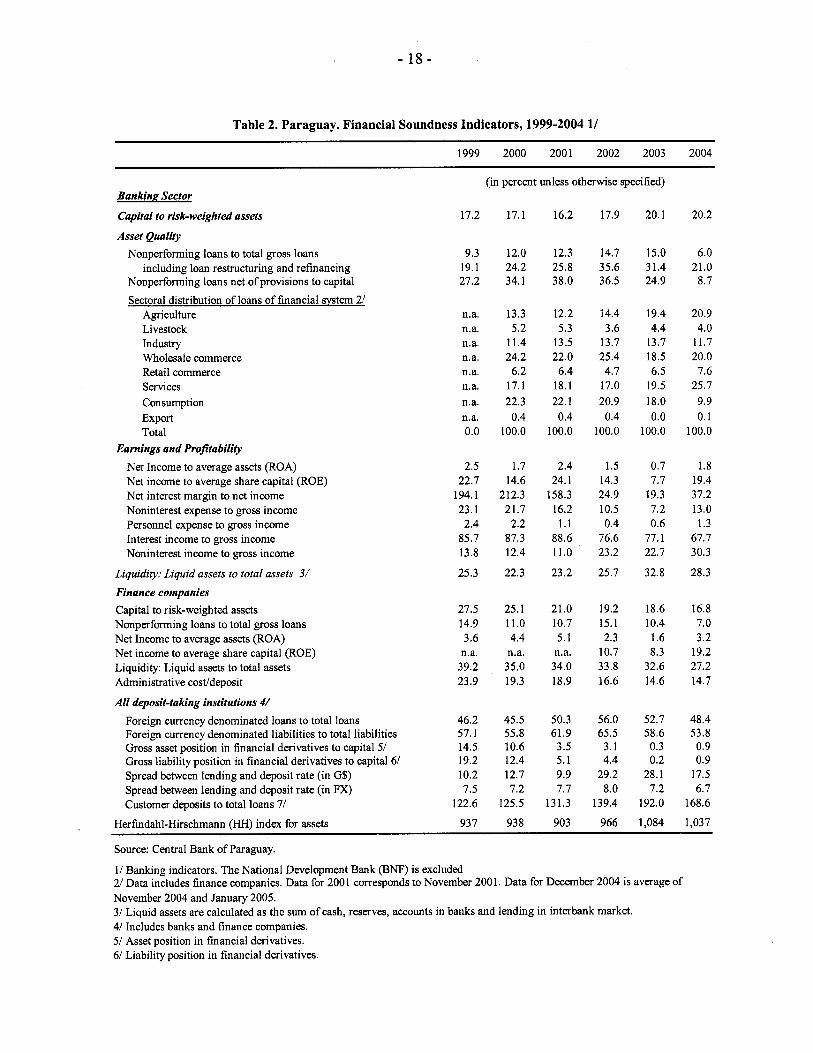

17. Banks are in a position to adjust to the impact of the implementation of Resolucidn 8/03 (upgrade of prudential regulations) on capitalization. As o f December 2004, the CAR o f the Paraguayan banking system equaled 20.3 percent (Table 2), with three domestic banks close to the 10 percent regulatory threshold On average, the application o f the Resolucibn 8/03 would lead to a decline o f the CAR to 16.3 percent, but two domestic banks and two out o f the four largest finance companies would see their CARS declining below the regulatory threshold. However, the required magnitude o f additional capital is relatively moderate, and i t seems reasonable to expect that sufficient capital could be raised.

18. The state-owned BNF shows a serious capital shortfall and i s technically insolvent. I f international provisioning standards were applied to BNF, the bank would be insolvent. In these circumstances, closing down the institution or implementing a significant restructuring are the only viable options. If the bank resumes lending operations, capital requirements would quickly increase. The government has opted to restructure the bank, based on the view it provides the only access to a bank for some areas in the country. If not fully closed and liquidated, the BNF should be substantially restructured, made to comply with all prudential regulations applied to private banks and focus i t s operations on segments o f the market that are not served by private banks.

19. Continuous delays in resolving the BNF transmit confusing signals to the financial sector as to the government’s intentions to carry out financial reform. The government decided to restructure the BNF in the framework o f a new law currently discussed by congress. However, the process has been marked by lack o f clarity in the conception o f the h t u r e activities of the BNF. An effective restructuring strategy should: (i) reestablish the solvency o f the bank and subject to the same prudential regulations as other commercial banks; (ii) redefine the features o f the main business activity o f the BNF, allowing the bank to operate where market failures are an impediment to the presence o f commercial banks, and liquidating assets that do not fit with this objective; (iii) provide for a governance structure o f the bank so that the lending processes remain based on sound and prudent lending policies; (iv) establish limits to BNF credits in a way consistent with the projection o f i t s future business; and (v) stipulate rules regarding regularization plans to deal with solvency problems confionted by the bank. If the law approved by congress fails to

- 7 -

address these issues properly, the government should promptly design an alternative strategy to embark on an ambitious rationalization plan to make the bank viable. Otherwise, continuing to operate the bank would not be justified.

IV. LEGAL AND REGULATORY FRAMEWORK FOR BANKING SUPERVISION AND FINANCIAL INTERMEDIATION

A. Legal Framework

20. The legal framework for banking supervision and financial intermediation needs to be upgraded to conform to accepted practices and international standards. A comprehensive approach i s necessary to align many elements o f the existing law that need to be modified in order to facilitate a more effective banking prudential fiarnework. Changes to the General Law on Banks, Financial and Credit Entities (banking law) should be a key element o f financial reform, complemented by reforms to the Central Bank law to clarify the role o f the Central Bank and grant more autonomy to supervisory functions.

21. government upgraded the banking resolution; however, this i s only one component o f a comprehensive banking law. The government has submitted to congress a draft comprehensive banking law addressing problems related to the banks’ governance, risk identification, and monitoring and enforcement capacity o f the Superintendency. The draft has not been discussed since the authorities are reassessing the adequate balance between autonomy and accountability o f the supervisory unit in the central bank, and are preparing an action plan to that effect. The draft banking law includes among i t s provisions: (i) strengthening fit and proper rules applicable to shareholders, managers and directors o f banks; (ii) stipulating clear responsibilities for bank managers and board members regarding risk management and control; (iii) requiring authorization for significant transactions o f banking shares, as wel l as significant transfers o f loan portfolio; (iv) improving risk identification and monitoring; (v) strengthening the enforcement capacity o f the Superintendency o f Banks.

The authorities recognize the weaknesses of the banking law. In 2003, the

22. accountability than the draft law would provide. Measures to strengthen the autonomy o f the SB should include among others: (i) granting powers to the SB to issue rules for the classification o f assets, currently approved by the central bank board; (ii) establishing that the SB would have the authority to license banks and withdraw banking licenses, and grant authorizations o f other property transfers; (iii) stipulating legal protection to SB employees regarding the discharge o f their official duties in good faith; (iv) establishing that appeals and judicial review procedures shall not suspend the effect o f supervisory decisions, including sanctions and that SB’s decisions would not be subject to appeals before the BCP Board, but to judicial review only. The broader autonomy o f the SB needs to be accompanied by new accountability provisions, specified by the law.

The enhancement of the effectiveness of the SB requires more autonomy and

23, The reform of the banking law needs to be accompanied by a revision of the central bank law. The increased autonomy o f the SB and i t s reduced degree o f subordination to the central bank board require a modification o f the central bank law. Also, the central bank

- 8 -

law would need to be modified to empower the SB to impose sanctions to banks and to instruct summary proceedings. Moreover, legal protection to BCP and SB employees regarding the discharge o f their official duties in good faith should be stipulated.

24. A reform of the central bank law i s also needed to clarify the role of the central bank. The law grants the BCP autonomy to pursue the objectives o f monetary and financial stability. However, constitutional provisions constrain the degree o f autonomy to be granted to the central bank, since they establish a subordination o f central bank policy to the government’s policy objectives. In addition government financing on the primary market should be forbidden and government obligations with the BCP should be regularized.

25. ante rules for the restitution of deposits but deposit insurance coverage i s exceedingly generous for an economy such as Paraguay’s. The deposit insurance scheme guarantees deposits in private banks and finance companies up to 75 minimum salaries (about US$12,000), equivalent to 10 times GDP per-capita, which compares with an international average o f about 3 times GDP per-capita. The premiums are set at an annual 0.48 percent o f total deposits. The high cost and the policy o f large banks to discourage retail depositors has resulted in depositors being charged by large banks to compensate for premium fees. Therefore, the expensive deposit insurance scheme in place i s indirectly causing a reduction on deposit returns for retail depositors, the ones that are supposed to be primarily protected b y such a scheme.

A new comprehensive banking resolution law, approved in 2003, introduced ex-

26. implemented strictly, to help recover credibility in the financial system while the banking resolution framework i s streamlined. In the past, liquidity support mechanisms have been adapted to specific circumstances, including the approval o f specific laws by congress to deal with specific cases during the period o f financial turmoil. The law envisages a discount window and a liquidity advance for temporary liquidity shortfalls. In practice, the only mechanism to provide liquidity i s the reverse rep0 window for central bank securities, recently modified in M a y 2005, incorporating recommendations by IMF technical assistance missions. Modifications include the introduction o f an automatic facility for instruments with very short maturity.

The authorities should design comprehensive safety net regulations that could be

B. Banking Regulation and Supervision

27. The Superintendency of Banks lacks autonomy and resources to adequately perform its duties and does not have sanctioning capacity. Lack o f independence i s a major shortcoming, as well as availability o f human and financial resources. Furthermore the effectiveness o f the supervisory function is weakened by a summary process that in practice i s unduly long, and that i s many times followed by a judicial review. Once an appeal i s presented, the implementation o f all supervisory decisions i s suspended for periods that frequently exceed one year. Only SB decisions on accounting issues are not suspended (additional provisioning and valuation adjustments).

28. The planned improvement of loans classification and provisioning (Resolucidn 8/03) will

Capital requirements are more lax than international standards and practices.

- 9 -

upgrade prudential regulations in this area. Although capital requirements at 10 percent o f risk weighted assets are higher than the Base1 minimum o f 8 percent, they do not distinguish between tier 1 and tier 2, and there are no requirements for market risk. Risk weights for loans backed by mortgage, warrants and other collaterals are not higher than 50 percent, even for commercial loans. The risk weight for government bond holdings i s zero. While th is i s customary in other jurisdictions in the region, i t seems less appropriate in Paraguay where most obligations are in foreign currency and banks have been subject to compulsory refinancing o f government obligations in the recent past. Moreover, there i s no limit for the reserve built for the revaluation o f assets. The introduction o f Resolucidn 8/03 will improve the regulatory framework. The FSAP found that most financial institutions individually feel prepared to adjust to this regulatory framework, and that pressures for delaying i t s implementation are not warranted.

29. There are no provisions in laws and regulations for the supervisory oversight of bank policies, procedures and credit risk management. Regulation o f credit risk i s based on the review o f individual loan exposure rather than on credit policies and lending processes. The SB took some steps in 2003 to conduct such oversight, and to require financial institutions to submit credit manuals and to adopt credit policies. However, the lack o f legal basis impinges on the efficacy o f these actions, since many banks tend to comply strictly with formal regulations. Moreover, SB staff require additional training to be more effective in the performance o f these duties.

V. ACCESS TO FINANCIAL SERVICES

A. Cooperatives

30. The volume of financial intermediation of credit cooperatives relative to total credit in Paraguay i s among the highest in the region. The extraordinarily large share o f financial system loans held by Paraguayan cooperatives - about 18.7 percent o f domestic credit to the private sector - compares to 6 percent in Honduras, the next highest in Latin America. The number o f members o f credit and savings cooperatives (CACs) as a percentage o f the economically active population i s similarly very high (23 percent) with respect to other L A C countries. The growth o f the cooperative sector has generally been favored by lower confidence in domestic banks and regulatory and fiscal advantages. In 2004, the growth rates in assets, loan portfolio, and deposits remained high for the cohort o f regularly reporting institutions. However, lack o f reliable data precludes a precise estimation o f the volume o f financial intermediation conducted through cooperatives in Paraguay. Only 287 o f the estimated active 600 cooperatives submitted basic financial data to INCOOP in 2004. Cooperatives are divided into three types according to their self-determined “main activity”: Cooperativas de Ahorro y Crkdito (CAC), Cooperativas de Produccidn, and a small group o f “other” types o f cooperative organizations.

3 1. extent. Differential treatment o f cooperatives comprises: (i) no obligation to pay income or sales taxes; (ii) no reserve requirements; (iii) no deposit insurance contributions; (iv) lower capital requirements. This certainly helps cooperatives to offer more attractive deposits and lending interest rates than banks. However, banks have been discouraging retail depositors

Regulatory arbitrage explains the development of cooperatives to a certain

- 1 0 -

and do not provide access to credit to customer base o f credit cooperatives. Therefore, financial instability and commercial banks’ policy may be more important to explain the shift o f retail depositors away from banks and into cooperatives. Finance companies are probably the sector that i s more affected by regulatory arbitrage favoring cooperatives. However, the increasing systemic importance o f cooperatives justifies putting in place prudential regulations, which in turn would reduce over time the scope for regulatory arbitrage.

32. The approval of Law 2157 and the definition o f prudential regulation in December 2004 represent a positive step towards establishing appropriate oversight for the sector but the lack of effective second-tier entities constrains the development of the sector. An effective enforcement o f the new regulatory framework would require strengthening the human and technological resources within INCOOP, as well as o f their network organizations. Second tier institutions have not effectively helped to improve the economies o f scale o f the sector.

B. Housing Finance

33. financing schemes secured by mortgages. Following financial reforms in the late 90s, a wide range o f instruments exists: Letras or Cbdulas Hipotecarias, Bonos Hipotecarios, Mutuos Hipotecarios Endosables, mortgage-backed securities. Regarding the latter, it i s noteworthy that two legal frameworks are available for securitization, through a trust mechanism and through securitization companies. However, none o f these instruments has been used so far due to (i) the lack o f interest by institutional investors in buying long term instruments subject to the price volatility o f the underlying collateral; (ii) the flaws affecting the registration o f properties and mortgages; and (iii) some technical flaws in the legal frameworks for mortgage related securities.

Paraguay already has in place a regulatory framework to support long term

34. A new second-tier structure (Agenciu Finuncieru de Desurrollo, AFD) i s being designed to provide long-term capital to the financial sector. In the housing finance sector, the AFD may assume the role inefficiently played by BANAVI. The AFD i s planned to be funded through international assistance, and therefore it could play a useful role while the domestic bond market develops. However, the AFD should operate without distortions, open to any potential lender, with loans priced at market conditions and any eventual government subsidies should be explicitly disclosed.

35. creation o f AFD, funded by external loans and grants, could provide the initial impulse to the development o f a mortgage market, with capital-market-based instruments to be used at a later stage. A development plan should include the following features: the design o f risk- based investment rules for institutional investors, with preferential treatment for mortgage related securities in accordance with their lower risk; the removal o f technical legal obstacles to rating o f structured assets; a prudent use o f indexation schemes; liquidity enhancing facilities; more efficient foreclosure procedures.

An integrated strategy i s required to reactivate a market for housing finance. The

- 11 -

C. Corporate Insolvency Procedures

36. In addition, almost all registries for property rights, secured transactions and other charges are unified under a single General Direction, which i s generally perceived as well managed. In spite o f this, a significant number o f shortcomings have been identified. Registration system for land titles and mortgages i s old-fashioned and ineffective as transactions over immovable assets are not computerized. They use a chronological “book system,” which i s an outdated and unsafe method for registration.

Legal provisions for the creation of security interests are generally satisfactory.

37. cumbersome. The length o f a disputed executing proceeding i s unpredictable; i t may take 3 to 4 years although there i s anecdotal evidence reporting cases whose duration has exceeded 5 years. The latter frequently occur when courts deal with major credits (measured by their amounts). The main reasons for observed delays are the following: (i) procedural laws requiring updates; (ii) abusive professional practices e.g. recurrent claims alleging the unconstitutionality o f different steps during the proceeding, even prior to getting a definitive court ruling, and simulation or enlargement o f labor credits -which are o f higher priority in ranking to mortgages or pledges- ; and (iii) the widespread inefficiency o f the judicial system.

Enforcement proceedings are unanimously perceived as lengthy and

38. Inefficiencies of insolvency proceedings can be attributed to an outdated insolvency law and a weak institutional framework. The insolvency law, enacted about 35 years ago, i s antiquated and requires an update. The insolvency administration agency (sindicatura) seems to be inadequate to the needs o f the country. Due to improprieties apparently perpetrated by insolvency administrators in several cases, the insolvency administration agency is currently subject to the Supreme Court intervention. The courts are not sufficiently staffed and trained to deal with insolvency cases. Though the insolvency law provides for the creation o f specialized insolvency courts, they have never been implemented.

39. both Iegal and institutional measures. These should include: (i) reform o f procedural legislation for efficient enforcement proceedings; (ii) improvement o f the legal framework for security interests over movable assets; (iii) implementation o f a comprehensive plan for modernization o f the registries, including computerized technology for recording and research; (iv) introduction o f a modern insolvency law providing for effective reorganization and liquidation proceedings; (v) implementation o f a comprehensive judicial reform; (vi) implementation o f an independent and effective body responsible for regulating and supervising insolvency administrators (sindicos), empowered to set standards o f conduct aimed at underscoring fairness, impartiality, transparency and accountability; and, (vii) creation o f a favorable environment for informal out-of-court processes for dealing with cases o f corporate financial difficulties or insolvency.

Measures to improve creditor rights and the insolvency system should include

- 1 2 -

VI. INSTITUTIONAL INVESTORS

A. The Insurance Industry

40. Latin America. Paraguay i s probably one o f the few countries in Latin America that has only one compulsory form o f insurance: passenger liabilities for public transport. Even th is compulsory insurance i s not fully enforced: i t i s estimated that out o f a fleet o f 7,000 public transport vehicles only between 60 to 70 percent are insured. A market-driven process o f mergers and acquisitions would reduce the excessive fragmentation o f the industry. This would discourage the destabilizing competition whereby some f i r m s charge prices below the level o f actuarial equilibrium (technical breakeven point). In 2004,36 insurance companies were registered in the country and 17 o f them reported premiums net o f cancellations less than U S $ l million. Given the size and growth potential o f Paraguay’s insurance market, the optimal number o f f i r m s would be around 7 to 10, a figure with which executives from the largest insurance companies and the Insurance Superintendency seem to agree.

Paraguay has one of the smallest and most fragmented insurance industries in

41. improvement since 2004, three critical issues require better regulation: investment requirements, governance principles and solvency requirements. In 2004, three important Resolutions (240,241 and 242) were issued by the Insurance Superintendency introducing a new accounting plan and a more rigorous criterion for the registration o f external auditors for insurance companies. Other areas need to be regulated more carefully. This i s the case for (i) investment requirements where limits, risk control and diversification procedures should be defined; (ii) governance o f insurance companies, an important issue for Paraguay where the Executive Boards o f most local companies are constituted by family members; and (iii) insurance companies solvency requirements. The Insurance Superintendency and representatives o f the insurance industry have agreed to constitute a jo int committee to review current solvency rules.

Although regulation of the insurance industry has shown significant signs of

B. Pensions

42. There are many pension arrangements in Paraguay but total coverage i s the smallest in Latin America. Providers o f pension services comprise the general scheme for private sector employees managed by the Instituto de Previsicin Social (IPS), the special compulsory schemes for certain categories o f the private sector workers and public employees (the Cajus) and voluntary private pension plans offered by non-profit organizations (the Cujus Mutuales). According to a recent World Bank (2004) study, based on census data, in 2000/2001 only 8 per cent o f the country’s economically active population made regular contributions to a pension plan. In addition, the pension coverage i s almost exclusive o f the medium and medium high earners, with a 24 percent coverage in the highest quintile and only 0.4 percent coverage in the lowest quintile.

43. profound negative social and economic consequences. Although the BCP has oversight responsibilities over the Cuju Buncuria, and the Contraloria General has general responsibility over the IPS and the Cuju Fiscal, Paraguay lacks a comprehensive regulatory

The absence of a comprehensive regulatory framework for the pension sector has

- 1 3 -

framework for pension schemes aimed at preventing excessive concentration o f risk, actuarial imbalances, absence o f transparency, and poor accountability. Reliable data on assets and liabilities are often missing due to the lack o f regular reporting obligations. Investment guidelines are needed to monitor the risk-return profiles o f pension schemes portfolios and discourage opportunistic behavior on the part o f pension managers that may affect negatively fbture payment capacity. Moreover, the inability to asses the current weaknesses o f existing schemes casts shadows over the feasibility o f a progressive broadening o f pension coverage beyond i t s present narrow limits.

44. The IPS requires clear investment guidelines. Given the high dependency ratio o f IPS’S covered population, the Institute has a positive cash flow o f about U S 2 4 mi l l ion per year. However, overly restrictive investment constraints prevent an efficient management o f IPS’S reserves which amount to US$180 mi l l ion in 2005. According to an actuarial evaluation conducted by the ILO, IPS, under the worst hypothesis, should continue experiencing a positive cash f low until 2025. However, lack o f investment alternatives, restriction to invest i t s reserves predominantly in projects that benefit the productive sector, and a prohibition to lend to the government (i.e. i t may not hold government bonds), led the IPS to invest in banks that offered higher returns but went eventually bankrupt (with total losses o f about U S 3 0 0 million). At the moment, all new IPS revenue is being invested in the BNF, since i t i s the only bank that benefits from a government guarantee.

45. The special compulsory schemes face financial difficulties. They include the government administered plan for central government employees and members o f the judicial system (the Caja Fiscal) and six autonomous entities (Cajas) that manage pension plans for certain categories o f workers. The Caja Fiscal reported in 2002 a deficit o f US$130 mi l l ion but a parametric reform introduced in 2003 has brought partial relief to this situation, reforms that could s t i l l be reversed by Congress. Two out o f six autonomous Cajas show serious financial shortcomings with fiscal implications. Caja Bancaria covers workers from the banking industry. It experiences a structural deficit and its reserves have been depleted, falling into a virtual situation o f default (estimated present value of i t s actuarial deficit o f US$300 million).

VII. CAPITAL MARKET INFRASTRUCTURE

A. Securities Market

46. could improve the trading infrastructure significantly. The Bolsa de Valores y Productos de Asuncibn SA. (Asunc ih Stock Exchange, ASE) regulated by the Comisibn Nacional de Valores (National Commission o f Securities) channels primary and secondary market transactions. Securities activity i s limited in al l types o f instruments, in guaranies and dollars and in primary and secondary markets. The main types o f instrument that are traded are stocks, bonds, and promissory notes. Market capitalization at around US$200 million, represents only 3-3.5 percent o f GDP. Measures required to strengthen the market include: (i) preparing a law for securities depository; (ii) improving registration and listing systems; and (iii) enhancing the quality and transparency o f firms’ economic and financial information by allowing operations o f rating agencies. Important complementary actions include

The Paraguayan capital market i s thin and underdeveloped. A few measures

- 14-

improving liquidity management by the Central Bank, developing the government bond market and implementing an electronic trading system in the context o f a payments system reform.

47. management strategy would have several advantages. No secondary market for government bonds exists at present as existing bonds are not traded in the ASE, and very few isolated trading operations are conducted bilaterally. The development o f a secondary market for government bonds would help develop interbank markets, offering reliable collateral and benchmark yields, and would be instrumental to a more effective management o f monetary policy. Given current credibility problems, a plan to issue short-term treasury bil ls (for which credibility could be quickly gained) should be initiated. Government bonds would facilitate the allocation o f reserves o f institutional investors, including the IPS.

The development of a market for government bonds in the context o f a debt

48. A disagreement between the Treasury and the BCP regarding government debt obligations causes uncertainty about the prospects for monetary and fiscal policy. Government obligations amounted to US$825 mi l l ion in 1997. Given that more than hal f o f these obligations were not being repaid, a rescheduling agreement was reached and revised again in 1999. Compliance with this agreement has different interpretations at the Treasury and at the BCP for an amount o f about US$280 million, and the conflict has reached the courts. Other unrecorded obligations that may add up to more than $500 mi l l ion exist with the private sector and other public institutions (IPS).

B. Payment Systems

49. Two systems are considered systemically important in Paraguay: the check clearinghouse and the Interbank Funds Transfer System (BITF). In fact, there i s no separation between large value and retail payments as both are mostly settled through the check clearing system. The check clearing system operated by the BCP is systemically important due to the high volume and value settled through it. Thus, i t could potentially trigger or transmit systemic disruptions. The BITF involves exclusively some large value interbank transactions. The system does not have explicit tools for the management o f credit and liquidity risks.

50. The check clearinghouse fails to comply with most of the CPSS Core Principles for Systemically Important Payment Systems (CPSIPS). Therefore, there i s an urgent need for a more sound and eEcient payments system in the country. The BCP, recognizing these weaknesses, has initiated a reform in the payments system to launch an RTGS system and reduce the systemic importance o f checks, among other things. In this regard, the BCP should have a clear strategy to effectively migrate large value payments from the check clearinghouse into the RTGS. The introduction o f an RTGS system would allow the BCP to comply with the CPSIPS and reduce systemic risk

5 1. to be improved in the legal framework are: settlement finality protection o f the systems against bankruptcy procedures, legal basis for dematerialization and/or immobilization o f securities, legal basis for custody arrangements, legal basis for netting arrangements, legal

Pending legal issues should be addressed as a priority by the BCP. Major aspects

- 1 5 -

definition o f rep0 operations, legal underpinning o f the pledge and, legal basis for electronic documents and signatures. The possibility o f enacting a comprehensive payments system law should be assessed and pursued.

52. RTGS system in order to allow for Delivery versus Payment (DVP). This will help the development o f the interbank money market and the securities markets. In any case, the authorities (BCP, Ministry o f Finance, and Securities Regulator) should debate this issue to arrive at the best solution in terms o f financial markets development, taking into account safety and efficiency issues.

A securities depository should be developed as a matter o f urgency linked to the

53. Currently, the BCP’s legislative authority for the oversight o f clearance and settlement systems stems from article 45 o f the Central Bank Organic Law. The BCP should determine and disclose publicly the scope o f i t s action and i ts implementation strategies. With regard to the scope o f i t s oversight role, i t i s suggested that the BCP applies its oversight authority over al l payments and securities settlement systems in the country, both systemically important and retail systems.

The BCP needs to streamline its oversight function over the payments system.

- 16-

Box 1. Paraguay: FSAP Main Recommendations (MT: Medium Term. ST: Short term)

0

0

Grant the SB more autonomy, sanctioning capacity and regulatory powers. Improve quality and quantity o f human, material and technological resources in the SB. I ST

- 17-

Table 1. Paraguay: Financial System Structure by Asset Holding and Numbers of Intermediaries

U$ %oftotal % o f 2000 2004

U$ %oftotal % o f No. billion assets GDP billion assets GDP No.

Other public financial insitutions 41 6 0.2 5.5 3.1 6 0.1 4.4 2.1

Sources: Superintendency o f Banks, INCOOP, Superintendency o f Insurance, Caja Itaipu, Caja Mutual de Cooperativas, IPS. 11 BNF. 21 Cooperativas de Ahorro y Credito. For 2000, estimates based on data available for the 20 largest Cooperativas de Ahorro y Credito 31 Banks deposits. 41 Credito Agricola de Habilitacion, Fondo Ganadero, Banco Nacional de la Vivienda, Fondo de Desarrollo Campesino, UTEP, Fondo de Desarrollo Industrial.

(in percent unless otherwise specified) Bankinp Sector

Capital to risk-weighted assets

Asset Quality Nonperfonning loans to total gross loans

including loan restructuring and refinancing Nonperforrning loans net o f provisions to capital Sectoral distribution o f loans of financial system 2/

Agriculture Livestock Industry Wholesale commerce Retail commerce Services Consumption Export Total

Earnings and Profitability Net Income to average assets (ROA) Net income to average share capital (ROE) Net interest margin to net income Noninterest expense to gross income Personnel expense to gross income Interest income to gross income Noninterest income to gross income

Liquidity: Liquid assets to total assets 31 Finance companies Capital to risk-weighted assets Nonperforming loans to total gross loans Net Income to average assets (ROA) Net income to average share capital (ROE) Liquidity: Liquid assets to total assets Administrative costldeposit

AN deposit-taking institutions 41 Foreign currency denominated loans to total loans Foreign currency denominated liabilities to total liabilities Gross asset position in financial derivatives to capital 5/ Gross liability position in financial derivatives to capital 6/ Spread between lending and deposit rate (in G$) Spread between lending and deposit rate (in FX) Customer deposits to total loans 7/

17.2

9.3 19.1 27.2

n.a. n.a. n.a. n.a. n.a. n.a. ma. n.a. 0.0

2.5 22.7

194.1 23.1 2.4

85.7 13.8

25.3

27.5 14.9 3.6

n.a. 39.2 23.9

46.2 57.1 14.5 19.2 10.2 7.5

122.6

17.1

12.0 24.2 34.1

13.3 5.2

11.4 24.2

6.2 17.1 22.3 0.4

100.0

1.7 14.6

212.3 21.7 2.2

87.3 12.4

22.3

25.1 11.0 4.4 ma. 35.0 19.3

45.5 55.8 10.6 12.4 12.7 7.2

125.5

Herfindahl-Hirschmann (HH') index for assets 937 938

16.2

12.3 25.8 38.0

12.2 5.3

13.5 22.0

6.4 18.1 22.1 0.4

100.0

2.4 24.1

158.3 16.2 1.1

88.6 11.0

23.2

21.0 10.7 5.1 n.a. 34.0 18.9

50.3 61.9 3.5 5.1 9.9 7.7

131.3

17.9

14.7 35.6 36.5

14.4 3.6

13.7 25.4 4.7

17.0 20.9 0.4

100.0

1.5 14.3 24.9 10.5 0.4

76.6 23.2

25.7

19.2 15.1 2.3

10.7 33.8 16.6

56.0 65.5 3.1 4.4

29.2 8.0

139.4

20.1

15.0 31.4 24.9

19.4 4.4

13.7 18.5 6.5

19.5 18.0 0.0

100.0

0.7 7.7

19.3 7.2 0.6

77.1 22.7

32.8

18.6 10.4 1.6 8.3

32.6 14.6

52.7 58.6 0.3 0.2

28.1 7.2

192.0

20.2

6.0 21.0

8.7

20.9 4.0

11.7 20.0 7.6

25.7 9.9 0.1

100.0

1.8 19.4 37.2 13.0 1.3

67.7 30.3

28.3

16.8 7.0 3.2

19.2 27.2 14.7

48.4 53.8 0.9 0.9

17.5 6.7

168.6

903 966 1,084 1,037 I ,

Source: Central Bank o f Paraguay.

1/ Banking indicators. The National Development Bank (BNF) i s excluded 2/ Data includes finance companies. Data for 2001 corresponds to November 2001. Data for December 2004 i s average of November 2004 and January 2005. 3/ Liquid assets are calculated as the sum o f cash, reserves, accounts in banks and lending in interbank market. 41 Includes banks and finance companies. 5/ Asset position in financial derivatives. 6/ Liability position in financial derivatives.

- 19 -

5.0 -

0 3

E

2.5 -

0 0.0 - +

!i-2.5 - -5.0 -

Figure 1. Paraguay: Recent Macro and Financial Sector Developments

Governance standards are below average for Latin America

Voice and accountability

Political Stability

Government Effectiveness

-Paraguay """".Latin h e r c i a

Recurrent Jnancial crises impaired economic growth, Real GDP growth, 1990-2004

A Annual growth o f

Annual growth o f real GDP per capita

-7 .54 I , , , I $ , , , , , , , , I 1990 1992 1994 1996 1998 2000 2002 2004

... and have caused a reduction of the number of Bnancial intermedia ries...

Size o f the financial system 40

30 -

* . Finance companies B $ 2 5 -

2 0 -

15 -

cost to enforce contract

4

..and the costs for operating business are hrgher.

Number ofprocedura to open

l n f m l

NU* o f procedura to enforce contract

st to create collateral ParagUay-LAcavnage

.which remains among the lowest in Latin America,

-

60 7

6 50

40 4-

330 5, 8 LO 4 g

10

0 3

-10 2

... and a modification in the composition of lending

6,000 '1 8 4,000 -

3 E .r

2,000

1998 2000 2002 2004

Credit by banks, cooperatives, and finance companies

Sources: BCP, SIB, INCOOP, and staff estimates. I/ Doing Business, The World Bank; Heritage Foundation Index o f economic freedom.

- 20 -

45

Y 4o .z 35

," 30

8 20 3 25

8 15 a 10 5

Figure 2. Paraguay: Financial Sector Developments

-- 13

-- 11

- 9 3 - - 7 B - - 5 -- 3

1- 1

-1

Decreasing banking intermediation followed a

35

30

2 ; 25

2 g 20

2 15

10

financial crisis, Private sector credit and deposits

Annual average o f bank deposits by the private sector

/

bank credit to the private sector

1998 2000 2002 2004

... bank' preference for liquidity increased, Liquid assets to total asset ratio

45 r I 68 Foreign currency

n a 40 4 deposits + 64 {

60 4 58 1 56 L 54

62 .c & 'G;

3 1998 2000 2002 2004

Liquid assets to total asset ratio - Foreign currency deposits (right scale)

... and the lending-deposit spread widens.

Inf lat ion and interest rate spreads 50 I 15

- Domestic

- (rightscale) .. ,

... uncertainty and dollarization remain high,

Dollarization 150 0.8

100

50

0

-50

-loo Decrease in dollarization 0.0

Foreign uurency deposits -Enchange rate B D o m s t i c currency deposits - -I - -Shareofforeignnormcydsposh

..,financial intermediation is short-term,

Matur i ty o f bank assets and liabil i t ies ' 170

Average maturity o f commercial

bank assets

90 Average maturity o f

70 commercial bank liabilities

s 0 N m P 9 4 4 s

8 5 0 m

' ' ' ' ' ' ' ' ' ' T n ' a ' n 8 n ' a ' n

... allowing for higher capital. Capital Adequacy Ratio

25 , I

I/ Estimate: Long-term assetsfliabilities exceeding 3 years are weighted with 1081 days; long-term assets comprised 1.7 percent o f portfolio in March 2005.