37

FINANCIAL STATEMENTS Walton Edgemont Development Corporation For the years ended December 31, 2013 and December 31, 2012 (Expressed in Canadian dollars)

FINANCIAL STATEMENTS

Walton Edgemont Development Corporation For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

PricewaterhouseCoopers LLP111-5th Avenue SW, Suite 3100, Calgary, Alberta, Canada T2P 5L3T: +1 403 509 7500, F: +1 403 781 1825“PwC” refers to PricewaterhouseCoopers LLP, an Ontario limited liability partnership.

April 29, 2014

Independent Auditor's Report

To the Shareholders of Walton Edgemont Development Corporation

We have audited the accompanying financial statements of Walton Edgemont Development Corporation, which

comprise the statements of financial position as at December 31, 2013 and December 31, 2012 and the

statements of comprehensive loss, changes in shareholders' equity and cash flows for the years then ended and

the related notes, which comprise a summary of significant accounting policies and other explanatory

information.

Management's responsibility for the financial statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance

with International Financial Reporting Standards, and for such internal control as management determines is

necessary to enable the preparation of financial statements that are free from material misstatement, whether

due to fraud or error.

Auditor's responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our

audits in accordance with Canadian generally accepted auditing standards. Those standards require that we

comply with ethical requirements and plan and perform the audits to obtain reasonable assurance about

whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the

financial statements. The procedures selected depend on the auditor's judgment, including the assessment of

the risks of material misstatement of the financial statements, whether due to fraud or error. In making those

risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation

of the financial statements in order to design audit procedures that are appropriate in the circumstances, but

not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also

includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting

estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained in our audits is sufficient and appropriate to provide a basis

for our audit opinion.

Opinion

In our opinion, the financial statements present fairly, in all material respects, the financial position of Walton

Edgemont Development Corporation as at December 31, 2013 and December 31, 2012 and its financial

performance and its cash flows for the years then ended in accordance with International Financial Reporting

Standards.

Chartered Accountants

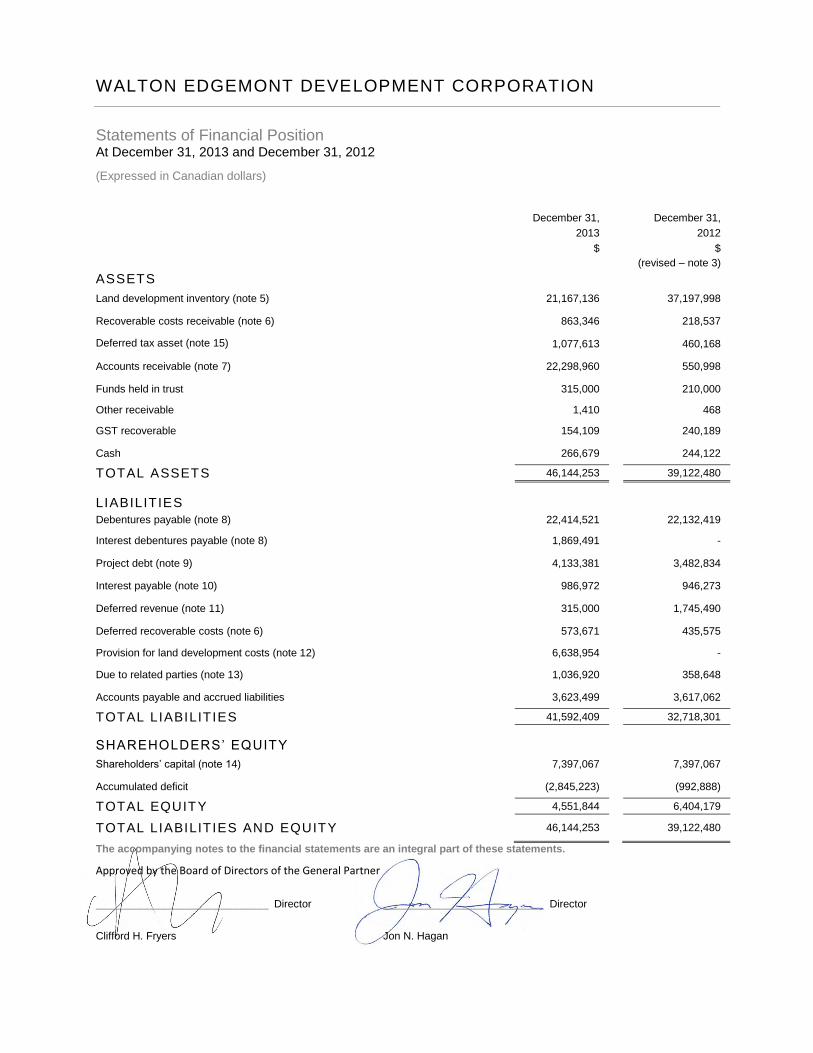

WALTON EDGEMONT DEVELOPMENT CORPORATION

Statements of Financial Position At December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

December 31,

2013

$

December 31,

2012

$

(revised – note 3)

ASSETS

Land development inventory (note 5) 21,167,136 37,197,998

Recoverable costs receivable (note 6) 863,346 218,537

Deferred tax asset (note 15) 1,077,613 460,168

Accounts receivable (note 7) 22,298,960 550,998

Funds held in trust 315,000 210,000

Other receivable 1,410 468

GST recoverable 154,109 240,189

Cash 266,679 244,122

TOTAL ASSETS 46,144,253 39,122,480

LIABILITIES

Debentures payable (note 8) 22,414,521 22,132,419

Interest debentures payable (note 8) 1,869,491 -

Project debt (note 9) 4,133,381 3,482,834

Interest payable (note 10) 986,972 946,273

Deferred revenue (note 11) 315,000 1,745,490

Deferred recoverable costs (note 6) 573,671 435,575

Provision for land development costs (note 12) 6,638,954 -

Due to related parties (note 13) 1,036,920 358,648

Accounts payable and accrued liabilities 3,623,499 3,617,062

TOTAL LIABILITIES 41,592,409 32,718,301

SHAREHOLDERS’ EQUITY

Shareholders’ capital (note 14) 7,397,067 7,397,067

Accumulated deficit (2,845,223) (992,888)

TOTAL EQUITY 4,551,844 6,404,179

TOTAL LIABILITIES AND EQUITY 46,144,253 39,122,480

The accompanying notes to the financial statements are an integral part of these statements.

Approved by the Board of Directors of the General Partner

_____________________________ Director ___________________________ Director

Clifford H. Fryers Jon N. Hagan

WALTON EDGEMONT DEVELOPMENT CORPORATION

Statements of Comprehensive Loss

For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

December 31,

2013

$

December 31,

2012

$

(revised – note 3)

REVENUE

Land development sales 32,642,900

-

COST OF SALES

Land development 33,982,997

-

GROSS LOSS (1,340,097)

-

OTHER INCOME/(EXPENSES)

Interest income 14,478

42,732

Management fees (note 13) (581,060) (581,060)

Servicing fees (note 13) (139,664)

(139,664)

Marketing expenses (282,679)

(217,462)

Directors’ fees (note 13) (52,129)

(52,129)

Office and other expenses (57,573)

(18,598)

Professional fees (31,056) (40,554)

(1,129,683)

(1,006,735)

NET LOSS BEFORE TAXES (2,469,780)

(1,006,735)

Deferred income tax recovery (note 15) 617,445

251,684

NET AND COMPREHENSIVE LOSS (1,852,335)

(755,051)

Basic and diluted net loss per share attributable to class B shares (note 14) (0.59)

(0.24)

The accompanying notes to the financial statements are an integral part of these statements.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Statements of Changes in Shareholders’ Equity For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

Class A Voting Common Shares

(note 14)

Class B Non-voting Common Shares

(Revised – note 3)

Accumulated Deficit

(Revised – note 3)

Total

# of Shares $ # of Shares $ $ $

DECEMBER 31, 2011 100 100 3,120,140 7,396,967 (237,837) 7,159,230

Net and Comprehensive loss - - - - (755,051) (755,051)

DECEMBER 31, 2012 100 100 3,120,140 7, 396,967 (992,888) 6,404,179

Net and Comprehensive loss - - - - (1,852,335) (1,852,335)

DECEMBER 31, 2013 100 100 3,120,140 7, 396,967 (2,845,223) 4,551,844

The accompanying notes to the financial statements are an integral part of these statements.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Statements of Cash Flows For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

December 31,

2013

$

December 31,

2012

$

(Revised - note 3)

CASH PROVIDED BY (USED IN)

OPERATING ACTIVITIES

Net and Comprehensive loss for the year (1,852,335) (755,051)

Adjustments for:

Interest income (14,478) (42,732)

Items not affecting cash:

Deferred tax recovery (617,445) (251,684)

Changes in non-cash operating items:

Decrease/(increase) in land development inventory 18,223,154 (8,671,443)

Increase in recoverable costs receivable (644,809) (218,537)

Increase in accounts receivable (21,747,962) (550,998)

Increase in funds held in trust (105,000) (210,000)

Decrease/(increase) in GST recoverable 86,080 (240,189)

(Decrease)/increase in deferred revenue (1,430,490) 1,745,490

Increase in deferred recoverable costs 138,096 435,575

Increase in provision for land development costs 6,638,954 -

Increase in due to related parties 678,272 19,293

Increase in accounts payable and accrued liabilities 6,437 3,414,660

Decrease in GST payable - (31,667)

Interest received 13,536 44,200

(627,990) (5,313,083)

FINANCING ACTIVITIES

Advances from project debt 8,908,874 3,482,834

Project debt repayments (8,258,327) -

650,547 3,482,834

Decrease in cash 22,557 (1,830,249)

Cash – Beginning of year 244,122 2,074,371

Cash – End of year 266,679 244,122

SUPPLEMENTAL INFORMATION Excluded from the statement of cash flows is $282,102 (December 31, 2012 - $259,115) of accretion relating to the Debentures

payable and $1,910,190 (December 31, 2012 - $149,630) of non-cash interest relating to the Debentures payable capitalized to

land development inventory. Interest paid on project debt of $223,008 (December 31, 2012 - $107,834) is capitalized to Land

development inventory.

The accompanying notes to the financial statements are an integral part of these statements.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

1

1. NATURE OF BUSINESS

Walton Edgemont Development Corporation (the “Corporation”) was incorporated under the laws of the province of

Alberta on May 5, 2011.

The Corporation was formed to provide investors with the opportunity to participate in the development of the

approximately 201.5 acre “Edgemont” properties located in Edmonton, Alberta (the “Properties”) through the

purchase of units in the Corporation. Each unit issued by the Corporation (“Unit”) through its initial public offering

(“IPO”) and private placement offering (“Private Placement”) was comprised of a $7.50 principal amount of offering

debenture (“Debenture”) and one class B non-voting common share (“Class B share”) at a price of $2.50 per share.

The Corporation intends to preserve the capital investment of the investors of Units in the Corporation and provide

cash distributions on the Units by executing the following four step strategy:

i) acquire the Properties;

ii) obtain contractual commitments from homebuilders to purchase lots to be serviced in each of the four

planned phases of the development of the Properties before construction commences on that phase;

iii) construct municipal services infrastructure on the Properties in phases to provide a controlled supply of

serviced lots to the marketplace; and

iv) use the revenue from the sale of the serviced lots to repay construction loans and other obligations of the

Corporation and then pay the remainder to the holders of the offering debentures (“Debentures”) and Class

B shares by paying the interest and principal on Debentures and by declaring a dividend or dividends on the

Class B shares and/or winding up the Corporation and distributing its assets to the holders of the Class B

shares.

Distributions by the Corporation are neither guaranteed nor will they be paid in a steady or stable stream. The amount

and timing of any distributions will be at the sole discretion of the Corporation and only after the Corporation has paid

or reserved funds for its expenses, liabilities and commitments (other than with respect to the Debentures), including

(i) the fees payable to Walton Asset Management L.P. (“WAM”) and Walton Development and Management (Alberta)

LP (“WDM”) (including the performance fee – note 13), and (ii) any amounts outstanding, on a phase by phase basis,

under the construction loans required to develop the Properties. The performance fee is only payable if the investors

of Units in the Corporation have received cash payments or distributions equal to $10.00 per Unit, plus a cumulative

compounded priority return thereon, equal to 8% per annum.

The registered office and principal place of business is 23rd

floor, 605 – 5th

Avenue SW, Calgary, Alberta, T2P 3H5.

These financial statements were authorized by the Board of Directors on April 29, 2014.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

2

2. BASIS OF PREPARATION

Statement of Compliance

These financial statements, including comparatives, have been prepared in full compliance with International

Financial Reporting Standards (“IFRS”) and using accounting policies that are consistent with IFRS as issued by the

International Accounting Standards Board (“IASB”).

Basis of Presentation

The Corporation’s financial statements have been prepared on the historical cost basis, except for certain financial

instruments which are initially measured at fair value as explained in the accounting policies set out in note 4.

The statements of financial position have been prepared using a liquidity based presentation because the operating

cycle of the Corporation revolves around the sale of land, the timing of which is uncertain. As a result, presentation

based on liquidity is considered by management to provide information that is more reliable and relevant to the users

of the financial statements. With the exception of land development inventory (note 5), recoverable costs receivable

(note 6), deferred tax asset (note 15), debentures payable (note 8) and interest debentures payable (note 8), all

assets and liabilities are current in nature and are expected to be settled in less than twelve months.

Change in Presentation

During the year ended December 31, 2013, the Corporation recognized revenue from lot sales. This revenue differs

significantly from the type of revenues previously generated by the Corporation, which consisted of interest income

and other incidental income. For the year ended December 31, 2013, the Corporation has reported all interest income

and other incidental income as part of other income/ (expenses). Interest income and other incidental income

recognized by the Corporation during the comparative prior period has also been reclassified to other

income/(expenses) for consistency with the presentation for the current year.

The Statement of Financial Position for December 31, 2012 was changed to combine land held for development and

land developments costs as a single item referred to as land development inventory to be consistent with the current

year presentation.

In the Statements of Cash Flows, the treatment of interest income/receivable and interest paid/payable has been changed to be consistent with the current year presentation.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

3

3. CHANGE IN ACCOUNTING POLICY AND REVISION OF PRIOR PERIOD BALANCES

For the year ended December 31, 2013 the Corporation has changed its accounting policy for the development

agreement with the City of Edmonton, revised the presentation of offering costs and adjusted the timing of receipt of

recovery. Prior period has been amended for the changes which are described in further detail below.

Change in accounting policy for development agreement

Previously, land development costs and recoverable costs from the City of Edmonton (note 5 and note 6) and a

corresponding provision for land development costs were recognized upon approval of a development servicing

agreement with the municipality. These costs and the associated provision were recognized within the statement of

financial position at the amount estimated to be incurred to develop their land inventory under the development

agreement with the City of Edmonton and costs that would be recoverable from the City of Edmonton. Management

re-evaluated its accounting policy after determining that a reclassification on the balance sheet for recoverable costs

would be required.

The Corporation has changed its policy to only recognize those costs associated with activities that have been

incurred to date with respect to the development of its land development inventory. A provision for land development

costs is recognized in conjunction with land sales as part of the cost to complete.

The Corporation believes that this change in accounting policy provides reliable and more relevant information as it

aligns the carrying value underlying the land development inventory with the progress the Corporation has made with

respect to the underlying development of the land and promotes comparability across the industry.

Those costs that are recoverable from the City of Edmonton are recognized to recoverable costs receivable as they

have been incurred. For those recoverable costs received in advance of incurring costs, these amounts will be

deferred and offset against associated costs as incurred. There was no impact on net loss, net loss per share, cash

flows and equity of the Corporation as a result of this change.

Revision of presentation of offering costs

For the year ended December 31, 2013, the Corporation has revised the prior period balance for offering costs which

were previously charged to profit and loss. The Corporation has determined that these costs are directly related to the

issuance of share capital and debentures and therefore should be included as offering costs. As at January 1, 2012,

$450,000 of the accumulated deficit has been reclassified with $112,500 being recorded as a reduction to share

capital and $337,500 recorded as a reduction to debentures payable. This resulted in an increase in accretion on

the debentures at January 1, 2012 of $26,225 which was capitalized to land development inventory.

The deferred tax impact relating to the offering costs results in the deferred tax asset increasing by $3,357, share

capital by $129,205 with accumulated deficit being increased by $125,848.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

4

As at December 31, 2012, the revision has resulted in an adjustment to the accretion on the debentures and land

development inventory of $88,480. The deferred tax impact resulted in deferred tax asset and recovery decreasing by

$87,732.

Revision of prior period receivable for timing of receipt of recovery

During the period it was noted that a deposit was made for a recovery in the current year that should have been

recorded in the year ended December 31, 2012. As a result, $550,998 was recorded as accounts receivable as

amounts in transit at December 31, 2012 increasing the deferred recoverable cost by $435,575 and land

development inventory by $115,422.

The change in presentation (note 2) and these revisions have resulted in the following changes to the financial

statements as at December 31, 2012 and January 1, 2012:

Impact as at January 1, 2012: Previously Reported

Offering Costs

Adjustment

Change in Accounting

Policy

Adjusted Amount

$ $ $ $

Land development costs 1,365,598 26,225 - 1,391,823

Land held for development 26,725,987 - - 26,725,987

Land development inventory 28,091,585 26,225 - 28,117,810

Deferred tax asset 205,127 3,357 - 208,484

Debentures payable 22,184,579 (311,275) - 21,873,304

Shareholder’s capital 7,380,362 16,705 - 7,397,067

Accumulated deficit (561,989) 324,152 - (237,837)

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

5

Impact at December

31, 2012

Previously

Reported

Offering Costs Adjustment

Change in Accounting

Policy

Prior Period Receipt of Recovery

Adjusted

Amount

$ $ $ $ $

Land development

costs

49,964,946 88,480 (39,465,992) (115,423) 10,472,011

Land held for sale 26,725,987 - - - 26,725,987

Land development

inventory

76,690,933 88,480 (39,465,992) (115,423) 37,197,998

Accounts receivable - - - 550,998 550 998

Recoverable costs

receivable

- - 218 537 - 218 537

Deferred tax asset 544,543 (84,375) - - 460,168

Debentures payable 22,381,439 (249,020) - - 22,132,419

Deferred recoverable

costs

- - - 435,575 435,575

Provision for land

development costs

39,247,455 - (39,247,455) - -

Shareholder’s capital 7,380,362 16,705 - - 7,397,067

Accumulated deficit (1,229,308) 236,420 - - (992,888)

Deferred income tax

recovery

339,416 (87,732) - - 251,684

4. ACCOUNTING POLICIES

Use of Estimates and Judgements

The preparation of financial statements in conformity with IFRS requires management to make estimates and

assumptions that affect the reported amounts of assets, liabilities and equity at the date of the financial statements,

and the reported amounts of revenue and expenses during the year. The estimates and assumptions that have the

most significant effect on the amounts recognized in the Corporation’s financial statements are as follows:

Recoverability of land development inventory - In assessing the recoverability of the land development

inventory, management is required to make estimates and assumptions regarding the sale price for serviced

lots, the costs to service the lots, the timing of lot sales, the completion date for the serviced lots and the

Corporation’s cost of capital. Changes in these estimates and assumptions could cause the net recoverable

value of land development inventory to differ materially from the carrying amount.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

6

Deferred tax asset - In assessing the amount of the deferred tax asset to recognize, significant judgment is

required in determining the likelihood, timing and level of future taxable profits. Changes in the timing and

level of future taxable profits could cause the amount of the deferred tax asset recovered to differ materially

from the carrying amount.

Capitalization of Borrowing Costs – The Corporation capitalizes borrowing costs to qualifying assets by

determining if borrowings are general or specific to the Properties, the Edgemont development project

(“Project”) will be active throughout the period of capitalisation and will take a substantial period of time to

prepare the Properties for its intended use or sale. The Corporation considers a substantial period of time to

be a period that is greater than one year.

Provision for land development costs - In estimating the amount of the provision to be recognized for land

development costs, significant judgment is required in estimating the the costs required to complete the

development of lots for which revenue has been recognized. These estimates are based on internal cost

budgets prepared for each phase of development, which are reviewed regularly to determine what

adjustments are needed to the provision for land development costs. The provision for land development

costs includes, but is not limited to, construction costs, consulting costs, project management fees and

financing costs. Changes in these estimates and assumptions could cause the total costs required to satisfy

the obligations to differ materially from the amount of this provision.

Cost of sales - In determining the amount of cost of sales to recognize in respect of completed lot sales,

significant judgement is required in estimating each lot’s proportionate share of land development

inventory, as well any remaining costs to complete the development of the lots sold. Changes in these

estimates and assumptions could cause the actual cost of each lot sold to differ from the cost of sales

recognized at the time that revenue was recognized.

Revenue Recognition – In assessing when to recognize revenue, significant judgment is required in

estimating when the purchaser can commence construction and when collection of sales proceeds are

reasonably assured. Changes in the market and the economy or the credit worthiness of the purchaser

may impact the amount of the deposit required prior to recognizing revenues, which would impact the

timing of revenue recognition.

Land Development Inventory

Land development inventory consists of land held for development and land development costs. Land development

inventory is acquired or constructed for sale in the ordinary course of business and is held as inventory and

measured at the lower of cost and net realizable value. The land is recorded at the acquisition cost, which is based

on the price paid by the Corporation for the Property. All direct costs related to land development are capitalized to

land development inventory. These costs include, but are not limited to, construction costs, consultant costs, project

management fees, property taxes and borrowing (financing) costs such as interest on debt specifically related to

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

7

the land development inventory, but exclude general and administrative overhead expenses. Land development

inventory are then relieved through cost of sales proportionately, based on the discounted sale price of each lot.

Where the carrying amount exceeds the net realizable value, the difference is recognized as an impairment loss. If

in a future period, the net realizable value of the land development inventory increases the impairment is reversed

up to the original cost of the inventory.

Recoverable costs receivable and deferred recoverable costs

Recoverable costs receivable are costs incurred in excess of recoveries received associated with the development agreement with the City of Edmonton. Deferred recoverable costs represent recoveries received in advance of funds being incurred. Deferred recoverable costs are reduced as associated costs are incurred.

Borrowing Costs

General and specific borrowing costs directly attributable to the acquisition, construction or production of qualifying

assets, which are assets that necessarily take a substantial period of time to get ready for their intended use or sale,

are added to the cost of those assets, until such time as the assets are substantially ready for their intended use or

sale. The Corporation considers land development inventory to be a qualifying asset.

Investment income earned on the temporary investment of specific borrowings pending their expenditure on qualifying

assets is deducted from the borrowing costs eligible for capitalization.

Borrowing costs on debt not directly attributable to the acquisition, construction or production of qualifying assets are

expensed.

Transaction Costs

Issuance costs of project debt obligations are capitalized against the associated debt and amortized using the effective interest rate method.

Financial Instruments

Financial instruments are any contract that gives rise to a financial asset of one party and a financial liability or equity

instrument of another party. Financial assets and liabilities are recognized when the Corporation becomes a party to

the contractual provisions of the instrument. Financial assets are derecognized when the rights to receive cash flows

from the assets have been transferred and the Corporation has transferred substantially all risks and rewards of

ownership. Financial liabilities are derecognized when the obligation specified in the contract is discharged.

Financial instruments are recognized initially at fair value, which is the price that would be received to sell an asset or

paid to transfer a liability in an orderly transaction between market participants at the measurement date.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

8

At each reporting period, the Corporation will assess whether there is any objective evidence that a financial asset,

other than those classified as fair value through profit or loss, is impaired. Impairment, if any, is recorded in net

income.

The following table lists the Corporation’s financial instruments and the method of measurement subsequent to initial recognition: Financial Instrument Category Measurement Method

Accounts receivable Loans and receivables Amortized cost

Recoverable costs receivable Loans and receivables Amortized cost

Funds held in trust Loans and receivables Amortized cost

Other receivable Loans and receivables Amortized cost

Cash Loans and receivables Amortized cost

Debentures payable Other financial liabilities Amortized cost

Interest debentures payable Other financial liabilities Amortized cost

Project debt Other financial liabilities Amortized cost

Interest payable Other financial liabilities Amortized cost

Due to related parties Other financial liabilities Amortized cost

Accounts payable and accrued liabilities Other financial liabilities Amortized cost

Debentures Payable

Debentures payable consist of the Corporation’s convertible debentures. As the debentures are convertible at the

sole discretion of the Corporation by dividing the principal amount of the Debentures and/or the amount of the

accrued and unpaid interest by the current fair value per Class B shares at the time of conversion, the full amount of

the debentures are recorded as a financial liability and are initially recorded at fair value and subsequently carried at

amortized cost using the effective interest rate method.

The debentures payable issued by the Corporation are extendable at the option of the Corporation for a period of two

years. This extension feature is considered a loan commitment under International Accounting Standard 39:

Recognition and Measurement (“IAS 39”), and as a result, no embedded derivative has been recognized is respect

of this extension feature.

Cash

Cash consists of amounts in demand deposits at financial institutions.

Provision for Land Development Costs The provision for land development costs is comprised of the estimated costs to complete the development of lots for which revenue has been recognized. These amounts have not been discounted as the majority of the costs are expected to be utilized within one year.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

9

Share Capital

Class A voting common shares (“Class A shares”) have been classified as equity because they represent residual

assets of the Corporation after the deduction of all its liabilities, and do not provide the holder of the shares with the

right to put the shares back to the Corporation.

Class B non-voting common shares (”Class B shares”) issued by the Corporation have been classified as equity

because the shares represent a residual interest in the Corporation after the payment of all its liabilities, and do not

provide the holder of the shares with the right to put the shares back to the Corporation. Costs directly attributable

to the issuance of such shares are recognized as a deduction from equity, net of tax.

Accumulated Deficit

Accumulated deficit comprises the accumulated balance of income less losses arising from the operation of the

Corporation, after taking into account dividends declared by the Corporation.

Revenue Recognition

Land is sold by way of an agreement of purchase and sale. Revenue is recognized on these sales once the

agreement is duly executed and delivered, the collection of sales proceeds is reasonably assured, the purchaser can

commence construction, and all other material conditions are met, including a deposit of not less than 20%.

Customer deposits received for purchases of lots on which revenue recognition criteria have not been met are

recorded as deferred revenue.

The Corporation recognizes interest income on an accrual basis in the period when it is earned.

Cost of Sales

At the time that revenue recognition criteria are met, the Corporation recognizes cost of sales for the lots sold by

allocating to each lot its proportionate share of land development inventory using the net yield method. Under the net

yield method, land development inventory is allocated to each lot sold based on the discounted sales price of the lot

over the estimated total discounted lot sales that will benefit from the land development inventory. This results in

phase specific costs being allocated proportionately based on the net yield of each lot in that phase, general costs

being allocated proportionately based on the net yield of each lot that will benefit from the general costs, and land

held for development being allocated proportionately based on the aggregate net yield of each lot of the Project.

Included in the cost of sales recognized is a provision for land development costs for costs to complete the

development of lots for which revenue is recognized.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

10

Current and Deferred Income Tax

Income tax expense for the period comprises current and deferred tax. Income tax is recognized in the statement of

comprehensive income except to the extent that it relates to items recognized directly in other comprehensive income

or directly in equity, in which case the income tax is recognized directly in other comprehensive income or equity,

respectively.

Current tax is the expected tax payable on the taxable income for the year, using tax rates enacted or substantively

enacted, at the end of the reporting period, and any adjustment to tax payable in respect of previous years.

The deferred income tax method is used to account for income taxes. Under this method, deferred income taxes are

recognized for the deferred income tax consequences attributable to differences between the financial statement

carrying values and their respective income tax basis. Deferred income tax assets and liabilities are measured using

tax rates that have been enacted, or substantively enacted, by the date of the financial statements and are expected

to apply when the related deferred income tax asset is realized or the deferred income tax liability is settled. The

effect on deferred income tax assets and liabilities of a change in tax rates is included in income in the period that

includes the enactment date. Deferred income tax assets are recognized to the extent they are more likely than not of

being realized.

Current Changes in Accounting Policies

The accounting policies used in the preparation of these financial statements are consistent with those which were

disclosed in the Corporation’s audited financial statements for the year ended December 31, 2012, except as

explained below and as disclosed in note 3.

Fair value measurement

The Corporation adopted IFRS 13: Fair Value Measurement (“IFRS 13”) for the annual year beginning on January 1,

2013. IFRS 13 is a comprehensive standard for fair value measurement and disclosure for use across all IFRS

standards. The new standard clarifies that fair value is the price that would be received upon the sale of an asset, or

paid to transfer a liability in an orderly transaction between market participants, at the measurement date. The

standard also requires an increase in the disclosure around valuation methods and inputs used in measuring fair

value in the notes to the financial statements. The Corporation does not carry any assets, liabilities or equity at fair

value. The adoption of IFRS 13 has resulted in increased disclosure around fair value contained in note 16 of these

financial statements.

Offsetting Financial Assets and Liabilities

International Accounting Standard (“IAS”) 32 Financial Instruments - Presentation (“IAS 32”) was issued with

amendments in December 2011. The amendments clarify certain aspects of the existing guidance on offsetting

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

11

financial assets and financial liabilities. The IASB also amended IFRS 7 Financial Instruments - Disclosure (“IFRS 7”)

to require information about all recognized financial instruments that are set off in accordance with IAS 32. The

amendments also require disclosure of information about recognized financial instruments subject to enforceable

master netting arrangements and similar agreements even if they are not set off under IAS 32.

The amendments to IAS 32 are effective for annual periods beginning on or after January 1, 2014. However, the new

offsetting disclosure requirements are effective for annual periods beginning on or after January 1, 2013, and interim

periods within those annual periods. The Corporation has adopted the offsetting disclosure requirements for the

period beginning January 1, 2013. The Corporation has assessed that there is no impact of the adoption on the

financial statements currently or retrospectively.

Future Changes in Accounting Policies

Financial instruments

In November 2009, as part of the IASB project to replace International Accounting Standard (“IAS”) 39 Financial

Instruments: Recognition and Measurement, the IASB issued the first phase of IFRS 9 Financial Instruments. It

contained requirements for the classification and measurement of financial assets, and was updated in October

2010 to incorporate financial liabilities. In November 2013, the IASB issued amendments to include the new general

hedge accounting model and to postpone the mandatory effective date of this standard indefinitely. The full impact

of this standard will not be known until the amendments addressing impairments, classification and measurement

have been completed. When these projects are completed, an effective date will be added by the IASB.

Offsetting financial assets and liabilities

IAS 32 Financial Instruments - Presentation (“IAS 32”) was issued with amendments in December 2011. The

amendments clarify certain aspects of the existing guidance on offsetting financial assets and financial liabilities. The

amendments to IAS 32 are effective for annual periods beginning on or after January 1, 2014. The Corporation has

assessed that there will be no impact of the adoption on the financial statements currently or retrospectively.

Levies

International Financial Reporting Interpretation Committee (“IFRIC”) 21 – Levies (“IFRIC 21”)is an interpretation of

IAS 37 - Provisions, Contingent Liabilities and Contingent Assets (“IAS 37”). IAS 37 sets out criteria for the

recognition of a liability to pay a levy imposed by government, other than an income tax. The interpretation requires

the recognition of a liability when the event, identified by the legislation as triggering the obligation to pay the levy,

occurs. This standard is required to be applied for accounting periods beginning on or after January 1, 2014. The

Corporation has not yet determined the impact of IFRIC 21 on its financial statements.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

12

5. LAND DEVELOPMENT INVENTORY

December 31,

2013

December 31,

2012

$ $

(Revised –

note 3)

BALANCE – BEGINNING OF YEAR 37,197,998 28,117,810

Development costs 17,952,135 9,080,188

Cost of sales (33,982,997) -

BALANCE – END OF YEAR 21,167,136 37,197,998

Land development inventory is relieved through cost of sales at the time that revenue from lot sales is recognized.

The timing of future lot sales is estimated by management, however, is subject to uncertainty because lot sales are

influenced by factors that are beyond the control of management, such as market demand for residential lots and the

timing of cash flows of the homebuilders. As a result, while a portion of land development inventory could be current

in nature, it is not possible for management to reasonably estimate the portion that will be realized within the next

twelve months. During the year, $2,133,198 (December 31, 2012 - $ 2,099,890) of interest was capitalized to

development costs.

6. RECOVERABLE COSTS RECEIVABLE AND DEFERRED RECOVERABLE COSTS

The table below reconciles the change in recoverable costs receivable:

December 31,

2013

December 31,

2012

$ $

(Revised – note

3)

BALANCE – BEGINNING OF YEAR 218,537 -

Cost incurred to be recovered 1,072,993 333,959

Recoveries received (428,184) (115,422)

BALANCE – END OF YEAR 863,346 218,537

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

13

The table below reconciles the change in deferred recoverable costs:

December 31,

2013

December 31,

2012

$ $

(Revised – note

3)

BALANCE – BEGINNING OF YEAR 435,575 -

Recoverable costs received in advance of costs incurred 138,096 435,575

BALANCE – END OF YEAR 573,671 435,575

Recoverable costs receivable are received from the City of Edmonton. These are in relation to the construction of

infrastructure required as part of the development agreement with the City of Edmonton. The City of Edmonton will

reimburse the Corporation for the proportionate share related to future developers. Future reimbursement will only be

made as other developers sign their respective development agreements with the City of Edmonton. There is no

guarantee as to the expected timing of when other developers may enter into their respective development

agreements. Upon completion and acceptance by the City of Edmonton of the infrastructure, the recoverable costs

are subject to receive interest at the lower of a rate equal to the prime rate +1% or the Construction Price Index

Variation, which is defined as the percentage change in the Edmonton Non-Residential Construction Price Index

published by Statistics Canada. As these rates are representative of a risk-free interest rate, the recoverable costs

are not discounted as the carrying value approximates the fair value at initial recognition.

7. ACCOUNTS RECEIVABLE

At December 31, 2013, the accounts receivable is comprised of amounts owing from builders for the sale of Phase 1

lots. At December 31, 2013 there were no amounts past due. For all lot sales, the ownership of the lot is not

transferred to the purchaser until the full purchase price has been received.

At December 31, 2012, the accounts receivable represents a recovery received but not deposited by year-end.

8. DEBENTURES PAYABLE AND INTEREST DEBENTURES PAYABLE

Debentures payable are comprised of the Debentures which were issued by the Corporation as part of its IPO,

Private Placement and in exchange for Walton International Group Inc.’s (“WIGI”) ownership interest in the

Properties. The total number of Debentures outstanding as at December 31, 2013 was 3,120,140 (December 31,

2012 – 3,120,140).

Interest debentures are comprised of the debentures that were issued by the Corporation on September 30, 2013 to

settle the 2013 interest payment on the Debentures. The interest debentures have a face value of $1,869,491.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

14

The Debentures and Interest Debentures are unsecured and bear interest at a rate of 8% per annum. Interest on the

Debentures and Interest Debentures is calculated annually based on the face value of the Debentures and Interest

Debentures on June 30, and is payable annually on September 30. The Debentures mature on December 31, 2016 at

a face value of $7.50, however, the maturity date can be extended by the Corporation at its sole discretion until

December 31, 2018. The Interest Debentures mature on December 31, 2016 at their principal amount.

The Corporation may also, in its sole discretion, (i) repay all or any portion of the principal amount of, or interest under, the Debentures or Interest Debentures through the issuance of Class B shares, (ii) evidence its obligation to pay all or any portion of the interest under the Debentures or interest under the Interest Debentures through the issuance of interest debentures, and/or (iii) convert all or any principal amount of the Debentures or Interest Debentures into Class B Shares. The Debentures and Interest Debentures may be converted into the number of shares obtained by dividing the principal amount of the Debentures and Interest Debentures by the current fair value of Class B shares.

The following table reconciles the change in debentures payable:

December 31,

2013

$

December 31,

2012

$

(revised – note

3)

BALANCE – BEGINNING OF YEAR 22,132,419 21,873,304

Accretion on debentures 282,102 259,115

BALANCE – END OF YEAR 22,414,521 22,132,419

The following table reconciles the change in interest debentures payable:

December 31,

2013

$

December 31,

2012

$

BALANCE – BEGINNING OF YEAR - -

Interest debentures issued 1,869,491 -

BALANCE – END OF YEAR 1,869,491

-

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

15

As at December 31, 2013 and December 31, 2012, WIGI owned approximately 5.1% of the outstanding Units of the

Corporation. As a result, approximately 5.1% of the balance of debentures payable and interest debentures payable

was payable to WIGI.

9. PROJECT DEBT

The Corporation has a construction loan with a Canadian-based financial services company to help finance Phase

1 of the Project (“Phase 1 Construction Loan”). The Phase 1 Construction Loan consists of a $26.9 million non-

revolving loan facility and an $8.9 million letter of credit facility. Included in the non-revolving loan facility is an

interest reserve of $1.75 million. The total advances under the construction loan, including the authorized letters of

credit, are not to exceed $31.5 million at any given time.

The loan facility is available to finance the construction costs for Phase 1 of the Project, while the letters of credit act

as security for the completion of certain development obligations under the development servicing agreement for

Phase 1 of the Project (“Phase 1 Development Servicing Agreement”). The letters of credit typically decline as the

Corporation’s development obligations are completed, through a series of staged reductions over a period of time and

are ultimately extinguished when the municipality has issued final acceptance certificates. The construction loan is

due on demand, with a maturity date of February 26, 2016 and bears interest at a rate of prime + 1.25%, interest is

paid monthly through the use of an interest reserve. At December 31, 2013 the interest reserve utilized was

$600,000. The lender reserves the right to stop advancing from the interest reserve account if the loan is not in good

standing. The construction loan is partially guaranteed by WIGI and is also secured by a first priority security interest

in all present and after acquired personal property of the Corporation, a floating charge over all of the Corporation's

present and after acquired real and other property, and a first fixed and specific demand collateral land mortgage over

the Properties. The total guarantee by WIGI at December 31, 2013 is $7,475,255.

WIGI entered into a guarantee with the lender of the Phase 1 Construction Loan that guarantees the amount of

$7,475,255. WIGI also provided a guarantee that the Corporation will complete the development of the Project and

fund all cost overruns. During the year ended December 31, 2013 the total advance on project debt was $8,908,874

(December 31, 2012 - $3,482,834) offset by total project debt repayments of $8,258,327 (December 31, 2012 – nil).

As at December 31, 2013, an $8.9 million letter of credit had been issued but has not been drawn upon. The total

balance outstanding on the construction loan as at December 31, 2013 was $4,133,381 (December 31, 2012 -

$3,482,834). The Corporation is not subject to any externally imposed covenants as at December 31, 2013.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

16

10. INTEREST PAYABLE Interest payable is comprised of accrued interest on the debentures payable and interest debentures payable (note 8). The following table reconciles the change in interest payable:

December 31,

2013

$

December 31,

2012

$

BALANCE – BEGINNING OF YEAR 946,273 796,643

Accrued interest on the debentures 1,872,084 1,872,085

Accrued interest on the interest debentures 38,106 -

Settlement of interest through cash distribution - (1,722,455)

Settlement of interest through the issuance of interest debentures (note 8) (1,869,491) -

BALANCE – END OF YEAR 986,972 946,273

As at December 31, 2013 and December 31, 2012, WIGI owned approximately 5.1% of the outstanding Units of the

Corporation. As a result, approximately 5.1% of the balance of interest payable was payable to WIGI.

11. DEFERRED REVENUE

Deferred revenue is comprised of deposits received from homebuilders for lots, for which revenue recognition criteria

have not been met. The deposits are non-refundable and are paid in accordance with the terms of the purchase and

sale agreements between the Corporation and the homebuilders.

The table below reconciles the change in deferred revenue:

December 31,

2013

$

December 31,

2012

$

BALANCE – BEGINNING OF YEAR 1,745,490 -

Receipt of Phase 1 deposits from homebuilders 1,789,520 1,745,490

Recognition of revenue on Phase 1 deposits (3,220,010) -

BALANCE – END OF YEAR 315,000 1,745,490

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

17

12. PROVISION FOR LAND DEVELOPMENT COSTS

The following table provides a breakdown of the provision for land development costs:

December 31, 2013 December 31,

2012

$ $

(Revised –

note 3)

BALANCE - BEGINNING OF YEAR -

Additional provisions 7,652,994 -

Less actual costs incurred during the year (1,014,040) -

BALANCE – END OF YEAR 6,638,954 -

The provision for land development costs includes accrued costs based on the estimated costs to complete for the

land development projects for which revenue has been recognized. These amounts have not been discounted as the

majority are expected to be utilized within one year.

13. RELATED PARTY TRANSACTIONS

See notes 1, 8, 10, 14, 16, 17 and 18 for additional disclosures relating to certain related parties and other related

party transactions.

WAM, WDM and WIGI are considered to be related to the Corporation by virtue of the fact that they are all

controlled by Walton Global Investments Ltd. (“WGIL”). The balances due to these related parties as at December

31, 2013 and December 31, 2012 are outlined in the table below. With the exception of the development fee

payable to WDM and any amounts payable to WAM for the servicing fee and management fee, these amounts are

unsecured, due on demand, bear no interest and have no fixed terms of repayment. The development fees are

payable to WDM within 60 days of quarter-end and any amounts that are past due bear interest at a rate of prime +

3%. The servicing fee is payable to WAM semi-annually and the management fee is payable to WAM quarterly. Any

balances due to related parties may be secured by a debenture recorded against the titles of the properties. The

debenture would be discharged on settlement of amounts owing.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

18

December 31,

2013

$

December 31,

2012

$

Walton Asset Management L.P. (“WAM”) 971,722 250,997

Walton Development and Management (Alberta) LP (“WDM”) 65,198 106,604

Walton International Group Inc. (“WIGI”) - 1,047

1,036,920 358,648

Walton Asset Management L.P.

In accordance with the terms of the Management Services Agreement between the Corporation and WAM, WAM will

provide management and administrative services to the Corporation in return for an annual management fee equal to:

i) from July 15, 2011 until the earlier of the date of termination of the Management Services Agreement and

June 30, 2016, 2% of the aggregate of:

a) the net proceeds raised from the IPO of $24,032,390, calculated as the gross proceeds raise of

$25,772,000, net of selling commissions $1,353,030 and offering costs of $386,580;

b) the net proceeds raised from the Private Placement of $3,900,330, calculated as the gross proceeds

raised of $4,228,000, net of selling commissions $221,970, work fees of $42,280, and offering costs of

$63,420; and

c) the product of the number of Units issued by the Corporation to WIGI in exchange for its interest in

the Property multiplied by $9.325, which was equal to $1,120,306; and

ii) thereafter, from July 1, 2016 until the termination date of the Management Services Agreement, an amount

equal to 0.5% of the book value of the Properties.

Also in accordance with the Management Services Agreement, commencing on July 15, 2011 and continuing until the

earlier of the dissolution of the Corporation and June 30, 2016, the Corporation will pay to WAM a servicing fee equal

to 0.50% annually of the net proceeds for each Unit sold under the IPO and Private Placement. WAM is then

responsible for paying the servicing fee to the Corporation’s agents in accordance with the Agency Agreements

between WAM, WDM and the Corporation. The servicing fee is calculated from the date of the applicable closing,

calculated semi-annually and paid as soon as practicable after that date. During the year ended December 31, 2013,

the total servicing fees charged to the Corporation was $139,664 (December 31, 2012 - $139,664).

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

19

During the year ended December 31, 2013, the total management fees charged to the Corporation was $581,060

(December 31, 2012 - $581,060). There were no amounts paid to WAM during the year (December 31, 2012 -

$547,422).

The balance payable to WAM as at December 31, 2013 was in respect of the management fees and servicing fees.

Notwithstanding the payment terms for such fees, due to cash constraints of the Corporation, management has

communicated to WAM that it does not expect to make payments for the management fees and servicing fees until

such time that the Corporation has sufficient capital for the payment of such amounts. WAM has indicated that it will

continue to provide its services as manager of the Corporation and to fund the servicing fee on behalf of the

Corporation. All amounts that exceed the regular payment terms are due on demand and bear no interest.

Walton Development and Management (Alberta) LP

In accordance with the terms of the Project Management Agreement between the Corporation and WDM, the fees and

costs for services provided by WDM are divided into the following two categories:

i) WDM will receive a development fee, plus applicable taxes, equal to 2% of certain development costs

incurred in the calendar quarter, payable within 60-days of the end of such quarter; and

ii) WDM will receive a performance fee, plus applicable taxes, equal to 25% of cash distributions after all

investors of Units in the Corporation have received cash payments or distributions equal to $10.00 per

Unit, plus a cumulative compounded priority return of 8% per annum. The priority return is calculated on

that $10 amount per Unit, reduced by any cash payments or distributions by the Corporation.

During the year ended December 31, 2013, the total development fee charged to the Corporation was

$213,442(December 31, 2012 - $129,251), total development fees paid by the Corporation was $259,827 (December

31, 2012 - $25,503). The developments fees are capitalized to land development inventory as incurred.

No performance fee was incurred by the Corporation during the year ended December 31, 2013 or the comparative

prior periods because the $10 per Unit amount and the cumulative priority return have not been received by the

investors of Units in the Corporation.

The balance due to WDM as at December 31, 2013 was comprised of unpaid development fees.

During the year ended December 31, 2013, the Corporation incurred a total amount payable to WDM of $20,545(December 31, 2012 - $15,076) for day to day expenses that were initially funded by WDM on the Corporation’s behalf. The total amount paid to WDM for amounts that were incurred on behalf of the Corporation’s during the year ended December 31, 2013 was $15,566 (December 31, 2012 - 14,403).

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

20

Walton International Group Inc.

As at December 31, 2013, the Corporation owed to WIGI $nil (December 31, 2012 - $1,047). The balance

outstanding as at December 31, 2012 was comprised of costs that were initially funded by WIGI on behalf of the

Corporation but were reimbursable by the Corporation. During the year ended December 31, 2013, the Corporation

incurred a total amount payable to WIGI of $8,603 (December 31, 2012 - $9,137) in costs initially funded by WIGI on

the Corporation’s behalf. The total amount paid to WIGI for amounts funded on the Corporation’s behalf was $9,650

(December 31, 2012 – 275,547).

Key Management Compensation

Key management personnel are comprised of the Corporation’s directors and executive officers. The total

compensation expense incurred by the Corporation relating to its independent directors was as follows:

December 31,

2013

$

December 31,

2012

$

Directors’ fees 52,129 52,129

All services performed for the Corporation by its executive officers and non-independent director are governed by the

Management Services Agreement. The annual management fee that WAM receives under the Management Services

Agreement has been disclosed above.

The compensation of Key Management does not include the remuneration paid to individuals who are paid directly by

WGIL and WAM. The Officers of the Corporation are also Officers and Directors of numerous entities controlled or

managed by WGIL and it is not practicable to make a reasonable apportionment of their compensation in respect of

each of those entities.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

21

14. SHARE CAPITAL

Authorized

Unlimited Class A shares

Unlimited Class B shares

Outstanding

December 31, 2013 December 31, 2012

(Revised – note 3)

Number of

shares

Amount

$

Number of

shares

Amount

$

Class A Shares 100 100 100 100

Class B Shares issued through the initial public

offering and private placement 3,000,000 7,500,000 3,000,000 7,500,000

Class B Shares issued to WIGI in exchange for

land held for development

120,140

284,582

120,140

284,582

Share issuance costs - (387,615) - (387,615)

3,120,240 7,397,067 3,120,240 7,397,067

All Class A shares of the Corporation are held by 1389211 Alberta Ltd., a wholly owned subsidiary of WIGI. WIGI is a

wholly owned subsidiary of WGIL. All or substantially all of the shares of WIGI are owned indirectly by members of the

Doherty family, including William K. Doherty, the Chief Executive Officer and director of WGIL.

Per Share Amount

Basic net loss per share is calculated by dividing the Corporation’s net loss by the weighted average number of

shares outstanding. The Class A shares outstanding have not been included in the weighted average shares

outstanding because the Class A shares do not participate in the profits or losses of the Corporation. The weighted

average number of shares outstanding for the year ended December 31, 2013 and the year ended December 31,

2012 was 3,120,140.

As the Corporation has the right to convert any portion of the debentures payable into Class B shares, this conversion

feature could result in potentially dilutive shares in the determination of the weighted average diluted shares

outstanding. For the year ended December 31, 2013 and the year ended December 31, 2012, the potentially dilutive

shares were nil because the Corporation generated net losses during those years.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

22

Share Issuance Price

The Class A shares issued and outstanding of the Corporation were issued at a price of $1.00/share.

The Class B shares issued and outstanding of the Corporation were issued at a price of $2.50/share.

15. INCOME TAXES

The following table reconciles the tax recovery calculated on the Corporation’s net loss before tax using the Corporation’s statutory tax rate to the income tax recovery recognized.

December 31,

2013

$

December 31,

2012

$

(revised – note

3)

Net loss before tax (2,469,780) (1,006,735)

Statutory tax rate 25% 25%

EXPECTED AND ACTUAL DEFERRED TAX RECOVERY (617,445) (251,684)

Deferred income tax assets are a result of temporary differences between the carrying amount of assets and liabilities

in the financial statements and their carrying amount for income tax purposes, as well as the recognition of tax losses.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

23

The following table reconciles the change in the deferred tax asset:

December 31,

2013

$

December 31,

2012

$

(revised – note

3)

DEFERRED TAX ASSET - BEGINNING OF YEAR 460,168 208,484

Change due to origination and reversal of temporary differences (4,985) (103,410)

Recognition of tax losses from current year 622,430 355,094

DEFERRED TAX ASSET - END OF YEAR 1,077,613 460,168

The components of the deferred tax assets are as follows:

December 31,

2013

December 31,

2012

$ $

Debenture issuance costs (51,743) (88,711)

Loan Fees (16,112) -

Non-capital loss carry forward 1,085,008 462,577

Share issuance costs 60,460 86,302

1,077,613 460,168

As outlined in the Corporation’s accounting policies, deferred income tax assets are recognized only to the extent that

it is probable that future taxable profit will be available against which temporary differences and prior year tax losses

can be utilized. The nature of the Corporation’s business is such that until the sale of lots commences, any revenue

generated by the Corporation is not significant. Management believes that based on the level of commitments

received for the purchase of serviced lots and the anticipated costs required to complete the development of those

serviced lots, the Corporation will be able to recover all previously incurred tax losses prior to the expiry date of those

tax losses. Management cannot however, reasonably estimate the portion of the deferred tax asset that will be settled

in the next twelve months because this will be impacted by the amount of net income generated by the Corporation

during that time.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

24

16. FINANCIAL INSTRUMENTS

The Corporation’s financial instruments consist of recoverable costs receivable, accounts receivable, funds held in

trust, other receivable, cash, debentures payable, interest debentures payable, project debt, interest payable,

accounts payable and accrued liabilities, and due to related parties.

With the exception of recoverable costs receivable, project debt, debentures payable and interest debentures

payable, the fair value of these financial instruments approximate their carrying value due to the short-term nature of

these items. The fair value of the recoverable costs receivable approximates its carrying value as the interest

accruing with the City of Edmonton for amounts owing and inflation offset the impact of discounting. The fair value of

project debt approximates its carrying value because the debt is due on demand and the interest rate on the debt is

variable based on the prime lending rate.

The fair value of debentures payable and interest debentures payable is determined using the income approach, primarily making use of level 3 (unobservable) inputs. Using the income approach, the expected future cash commitments arising from these financial liabilities are discounted by the Corporation’s market rate. As at December 31, 2013, the fair value of debentures payable and interest debentures payable approximated the carrying amount because there have not been significant changes in the Corporation’s risk premium or to market interest rates, since the issuance of these financial liabilities.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

25

The following tables set out the Corporation’s classification and carrying amount of the financial instruments along with the fair value as at December 31, 2013 and December 31, 2012: DECEMBER 31, 2013 Fair Value Amortized Cost Totals

Through profit

and loss

Loans and

receivables

Other financial

liabilities

Carrying

amount

Fair Value

$ $ $ $ $

Asset (liability):

Accounts receivable - 22,298,960 - 22,298,960 22,298,960

Recoverable costs receivable - 863,346 - 863,346 863,346

Funds held in trust - 315,000 - 315,000 315,000

Other receivable - 1,410 - 1,410 1,410

Cash - 266,679 - 266,679 266,679

Debentures payable - - (22,414,521) (22,414,521) (22,414,521) 1

Interest debentures payable - (1,869,491) (1,869,491) (1,869,491) 1

Project debt - - (4,133,381) (4,133,381) (4,133,381)

Interest payable - - (986,972) (986,972) (986,972)

Due to related parties - - (1,036,920) (1,036,920) (1,036,920)

Accounts payable and accrued

liabilities - - (3,623,499) (3,623,499) (3,623,499)

- 23,745,395 (34,064,784) (10,319,389) (10,319,389)

1 – Note that sensitivity table below shows that the carrying value approximates fair

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

26

DECEMBER 31, 2012 Fair

Value

Amortized Cost Totals

Through

profit

and loss

Loans and

receivables

Other

financial

liabilities

Carrying

amount

Fair Value

$ $ $ $ $

Asset (liability):

Accounts receivable - 550,998 - 550,998 550,998

Recoverable costs receivable - 218,537 - 218,537 218,537

Funds held in trust - 210,000 - 210,000 210,000

Other receivable - 468 - 468 468

Cash - 244,122 - 244,122 244,122

Debentures payable - - (22,132,419) (22,132,419) (22,132,419) 1

Project debt - - (3,482,834) (3,482,834) (3,482,834)

Interest payable - - (946,273) (946,273) (946,273)

Due to related parties - - (358,648) (358,648) (358,648)

Accounts payable and accrued

liabilities - - (3,617,062) (3,617,062) (3,617,062)

- 1,224,162 (30,537,236) (29,313,074) (29,313,074)

1 – Note that sensitivity table below shows that the carrying value approximates fair

The following table shows the impact on the fair value to debentures payable and interest debentures payable if the

market interest rate were to change.

Sensitivity Analysis

Change in market interest rate +/- 1% +/- 3% +/- 5%

Debentures Payable (8% interest per annum) 53,966 161,454 268,353

Interest Debentures Payable (8% interest per annum) 3,973 11,890 19,770

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

27

Risk – overview

The Corporation’s financial instruments and the nature of the risks to which they may be subject are as set

out in the following table.

Risk

Credit Liquidity Interest rate Currency

Accounts receivable X

Recoverable costs receivable X X

Funds held in trust X

Other receivable X

Cash X X

Debentures payable X X

Interest debentures payables X X

Project debt X X

Interest payable X

Due to related parties X

Accounts payable and accrued

Liabilities

X

i) Credit risk

Credit risk is the risk that one party to a financial instrument will cause a financial loss for the other party by

failing to discharge an obligation. Credit risk arises from accounts receivables, funds held in trust, other

receivables and cash held with banks. The maximum exposure to credit risk is equal to the carrying value of

these financial instruments.

Accounts receivable – The balance of accounts receivable are due from large, reputable homebuilders who

have demonstrated to management their ability to meet the payment terms included in the purchase and sale

agreements. In addition, the balance of the receivable is secured by a 20% deposit on the sale price of each

lot sold, and the Corporation retains title on the lots until such time that 100% of the sale proceeds has been

received. The Corporation is exposed to concentration risk as all revenue is attributable to four homebuilders

all having a concentration of greater than 10% of revenue. At December 31, 2013, the concentration of

revenue from the four homebuilders was 23%, 25%, 27% and 25%, respectively. The concentration of

accounts receivable was 10%, 25%, 27% and 27%, respectively. There were no additional customers.

Recoverable costs receivable– The recoverable costs receivable are received from future developers

via the City of Edmonton. Future developers are required to pay their proportionate share of off-site

costs at the time that they sign their development agreement with the City of Edmonton. The

Corporation has a contractual right with the City of Edmonton whereby the City will not permit other

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

28

developers to develop within the adjacent lands, without the collection of these amounts. Therefore,

management believes the exposure to credit risk is minimal.

Funds held in trust – Funds held in trust are held by trustees in the name of the Corporation and

homebuilders. The trustees are considered by management to be credible, which minimizes the

Corporation’s exposure to credit risk. These funds will be released to the Corporation once the

Corporation completes its responsibilities for the release of such funds under the terms of the purchase

and sale agreements.

Other receivable - The Corporation’s exposure to credit risk associated with other receivable is not

material because the balance of other receivable is typically not material and is settled monthly.

Cash - Cash is on deposit with a major financial institution, which substantially minimizes its exposure to

credit risk.

ii) Liquidity risk

Liquidity risk arises from the possibility that the Corporation will encounter difficulties in meeting its financial

obligations as they become due. The Corporation manages its liquidity risk by continuously monitoring the

progress of the development, ensuring timely collection of lot sales, and managing cash receipts and

payments. The liabilities which expose the Corporation to liquidity risk are as follows:

Debentures payable, interest debentures payable and interest payable –Management has the ability to

settle the interest on the Debentures payable or Interest Debentures payable through the issuance of

interest debentures. The Debentures have a maturity date of December 31, 2016 however; the maturity

date can be extended to December 31, 2018 at the sole discretion of the Corporation. The Corporation

intends to repay the Debentures payable and Interest Debentures payable through future lot sale

revenues generated by the Corporation.

Project debt – Project debt is comprised of a construction loan with a Canadian financial institution for

Phase 1 of the Project. The construction loan consists of a $26.9 million non-revolving loan facility and

an $8.9 million letter of credit facility. Under the terms of the loan agreement, the total advances under

the construction loan, including the authorized letters of credit, are not to exceed $31.5 million at any

given time. The loan is secured by all assets of the Corporation, and is also partially guaranteed by

WIGI. There is no assurance that WIGI will provide future guarantees to secure the Corporation’s future

financing requirements or be able to maintain loan covenants, if applicable. In order to minimize the

Corporation’s exposure to liquidity risk as a result of the project debt, management ensures that all

conditions and requirements under the loan agreement are adhered to, and that the collateral secured by

the bank exceeds the balance of project debt outstanding. The Corporation intends to repay the project

debt through future lot sale revenues generated by the Corporation. It is anticipated that further

construction loans will be required to fund the costs of development for Phase 2, 3, and 4 of the Project.

WALTON EDGEMONT DEVELOPMENT CORPORATION

Notes to the Financial Statements For the years ended December 31, 2013 and December 31, 2012

(Expressed in Canadian dollars)

29

As at December 31, 2013, the outstanding balance of the loan facility was $4,133,381 (December 31,

2012 - $3,482,834), and an $8.9 million (December 31, 2012 - $8.9 million) letter of credit had been

issued to the City of Edmonton, but had not been drawn upon.

Accounts payable and accrued liabilities – These liabilities are a result of the normal operations of the

Corporation and are current in nature. Management considers exposure to liquidity risk from these financial