69

Document of The World Bank FOR OFFICIAL USE ONLY Report No.: 19973-UNI Financing Nigeria’s Rural Micro and Small-Scale Enterprises May 11, 2000 MAIN REPORT Rural Development 2 Africa Region

Document of The World Bank

FOR OFFICIAL USE ONLY

Report No.: 19973-UNI

Financing Nigeria’s Rural Micro and Small-Scale Enterprises

May 11, 2000

MAIN REPORT

Rural Development 2 Africa Region

CURRENCY EQUIVALENTS

Currency Unit = Naira (N) US$1.00 = N105.0 (as of May 11, 2000) N1 = 100 Kobo

ABBREVIATIONS AND ACRONYMS

ACGSF Agricultural Credit Guarantee Scheme Fund AfDB African Development Bank ADPs Agricultural Development Projects CBN Central Bank of Nigeria CDAs Community Development Associations CGAP Consultative Group to Assist the Poorest DFI Development Finance Institution EBRD European Bank for Reconstruction and Development ECOWAS Economic Community of West Africa EDF European Development Fund EIB European Investment Bank ESW Economic and Sector Work ESSD Environmentally and Socially Sustainable Development FACU Federal Agricultural Coordinating Unit FEAP Family Economic Advancement Program FGN Federal Government of Nigeria FMBN Federal Mortgage Bank of Nigeria GAAP Generally Accepted Accounting Principles GDP Gross Domestic Product IBRD International Bank for Reconstruction and Development IFAD International Fund for Agricultural Development MIS Management Information System NACB Nigeria Agricultural and Cooperative Bank NAIC Nigeria Agricultural Insurance Corporation NBCI Nigeria Bank for Commerce and Industry NBCB National Board for Community Banks NBFI Non-Bank Financial Institution NEB Nigeria Education Bank NEXIM Nigeria Export-Import Bank NGO Non-Governmental Organization NIDB Nigeria Industrial Development Bank PBN People’s Bank of Nigeria RBP Rural Banking Program RFI Rural Financial Institution RFM Rural Financial Market ROSCAs Rotating Saving and Credit Associations SAP Structural Adjustment Program SDI Subsidy Dependence Index UBN Union Bank of Nigeria UDB Urban Development Bank

This Economic and Sector Work (ESW) is prepared by a study team comprising Sidi Jammeh (Team Leader, AFTR2); Stephanie Charitonenko (Lead Consultant); Ayo Adeniyi of the Federal Agricultural Coordinating Unit (FACU), Nigeria; James Akinwumi, Professor of Agricultural Economics at the University of Ibadan, Nigeria. Contributions were also made by Sam Eremie, Dele Ilebani, Esther Walabai, and Foluso Okunmadewa (AFMNG), and our ESW partners in Nigeria. The peer reviewers for this paper are Carlos Cuevas and William F. Steel (AFTP1); and Jacob Yaron (RDV). Joseph Baah-Dwomoh (Sector Manager, AFTR2) is providing quality assurance support. As this is a work in progress, please do not cite or quote. However, comments are welcome and can be sent to Sidi Jammeh at [email protected].

Financing Nigeria’s Rural Micro And Small-Scale Enterprises

TABLE OF CONTENTS

Page No.

EXECUTIVE SUMMARY ............................................................................................ i-x Chapter 1. INTRODUCTION ........................................................................................1

A. Background ......................................................................................................................1 B. Objectives and Methodology............................................................................................1 C. Data Sources.....................................................................................................................2 D. Organization of this Report..............................................................................................3

Chapter 2. COUNTRY CONTEXT ...............................................................................4

A. Macroeconomic Indicators and Performance...................................................................4 B. Banking System Structure ................................................................................................5 C. Rural Financial Markets ...................................................................................................6

Chapter 3. POLICY, LEGAL, AND REGULATORY ENVIRONMENT ................9

A. Summary of Banking System Policies, Programs, and Reforms .....................................9 B. Macro and Sectoral Policy Environment........................................................................10

(a) Maximum Interest Rate Ceilings and Spreads ....................................................10 (b) Effective Taxation of Agriculture ........................................................................11 (c) Investments in Infrastructure and Human Services ............................................12

C. Legal and Regulatory Framework..................................................................................12 (a) Regulation and Supervision of NBFIs.................................................................13 (b) Creation, Perfection, and Enforcement of Security Interests .............................14

Chapter 4. MAJOR RURAL FINANCE INSTITUTIONS .......................................15

A. Nigeria Agricultural and Cooperative Bank...................................................................15 (a) Ownership and Governance ...............................................................................15 (b) Mission and Services...........................................................................................16 (c) Performance........................................................................................................18 (d) Constraints..........................................................................................................20 (e) Recommendations ...............................................................................................22

B. People’s Bank of Nigeria ...............................................................................................23 (a) Ownership and Governance ...............................................................................23 (b) Mission and Services...........................................................................................24 (c) Performance........................................................................................................25 (d) Constraints..........................................................................................................26 (e) Recommendations ...............................................................................................28

C. Rural Support Programs .................................................................................................29 (a) Family Economic Advancement Program ..........................................................29 (b) Agricultural Credit Guarantee Scheme Fund .....................................................30 (c) Nigeria Agricultural Insurance Corporation ......................................................33

Page No. D. Informal Rural Finance Providers ...................................................................................35

(a) Trade and Input Supply Financing .....................................................................35 (b) Cooperative Societies..........................................................................................36 (c) Non-Governmental Organizations ......................................................................38 (d) Esusus, Family and Friends, and Moneylenders ................................................39

Chapter 5. RECOMMENDATIONS ...........................................................................41

A. Creating an Enabling Macro and Sectoral Policy Environment.....................................41 B. Improving the Legal and Regulatory Framework ..........................................................42 C. Building the Institutional Capacity of Rural Finance Providers.....................................42 D. Encouraging Banking System Linkages ........................................................................43 E. Next Steps.......................................................................................................................44

REFERENCES.................................................................................................................47 BOXES Box 1.1: Eight Pillars of Urban-Biased Policies ...........................................................................2 Box 1.2: Key Performance Indicators for Rural Finance Institutions ...........................................2 Box 2.1: Interest Rate Structure ....................................................................................................5 Box 2.2: Banking Service Outlets in Rural Areas.........................................................................6 Box 2.3: Banking System Institutions...........................................................................................6 Box 3.1: Important Policy Reforms Affecting the Banking System, 1996 - 1998......................10 Box 3.2: FGN Rationale for Cheap Credit and Empirical Evidence...........................................11 Box 3.3: Institutional Development in Nigeria’s Financial Sector .............................................13 Box 4.1: NACB’s Foreign Funding Sources...............................................................................16 Box 4.2: NACB’s Loan Products................................................................................................17 Box 4.3: NACB’s Investments....................................................................................................17 Box 4.4: NACB’s Lending Terms...............................................................................................18 Box 4.5: NACB’s Loans and Advances......................................................................................18 Box 4.6: NACB’s Financial Highlights ......................................................................................19 Box 4.7: NACB’s Foreign Exchange Rate Problems..................................................................21 Box 4.8: PBN’s Mission Statement.............................................................................................24 Box 4.9: PBN’s Financial Highlights..........................................................................................26 Box 4.10: PBN’s Loan Approval Process .....................................................................................27 Box 4.11: PBN’s Average Loan Processing Period ......................................................................27 Box 4.12: ACGSF Loan Repayment by Number and Volume .....................................................31 Box 4.13: Deposit Mobilization through the ACGSF’s Self-Help Group Program......................32 Box 4.14: Commercial Bank Branches in Rural Areas.................................................................32 Box 4.15: The National Agricultural Insurance Committee .........................................................34 Box 4.16: The Bauchi State Cooperative Financing Agency Limited ..........................................38 Box 4.17: Distribution of Occupational Groups by Sources of Informal Credit...........................40

ANNEXES Annex 1. Executive Summary of “Nigeria: Rural Finance Issues Paper” ...................................49 Annex 2. Description of NACB’s Specialized Project Lending Products ...................................50 Annex 3. Description of PBN’s Proposed Loan and Savings Products .......................................51

Financing Nigeria’s Rural Micro and Small-Scale Enterprises

EXECUTIVE SUMMARY

Background 1. The rural sector is central to Nigeria’s development strategy and agriculture continues to play a key role in rural growth. Empirical evidence suggests that financial markets in Nigeria are fragmented and inadequate to meet the rural demand for financial services. The absence of efficiently operating rural financial markets has become a serious constraint on sustainable rural development. Efficient and cost-effective financial services are essential elements of an environment that supports entrepreneurship, innovation, and production to develop and flourish. Households need access to safe savings facilities. In addition, farm and off-farm entrepreneurs need timely access to appropriately designed financial services to take advantage of market and investment opportunities. 2. To date, the Government of Nigeria has taken the “traditional” supply-led approach to the provision of agricultural credit. The underlying premise has been that there is market failure.1 Under such a premise, the “free” market cannot be relied upon to supply adequate credit to “weaker” economic agents in the rural economy. As a result, the solution has been the establishment of government policies and programs to ensure the adequate transfer of “cheap” credit to smallholder farmers. With little or no regard to the nature of the demand for financial services and with exclusive emphasis on agricultural credit over rural financial intermediation2, the government-sponsored programs have not achieved their objectives of sustained poverty reduction and rural development. Indeed, most of the government-sponsored agricultural credit programs have become huge liabilities to the government, with large loan losses and limited outreach.

Introduction to the Study and Report

3. The micro and rural finance institutions (RFIs) operating in the rural areas of Nigeria are complex, given the wide variety of state, collective, and private decision-making groups that influence their operations and use their services. Description and analysis of the rural financial markets is also complicated by the rapid and substantial changes in economic policies in Nigeria over the last two years and the necessity of key RFIs to change as a result. This study examines the environment for the development of rural financial markets in Nigeria, including an analysis of: (a) the main policies, laws, and regulations affecting the public and private delivery of financial services to rural micro and small-scale, farm and off-farm enterprises; and (b) the operation and performance of major formal and informal RFIs in terms of their outreach and

1 World Bank (1994). 2 Two government-sponsored institutions, which have been operating since 1990, are exceptions to this.

The People’s Bank of Nigeria (PBN) and the Community Banks (CBs) provide rural financial intermediation (by offering both deposit and loan products) to on-farm and off-farm enterprises. Indeed, although over 70 percent of the client base of both PBN and the CBs is rural, both intermediaries operate in urban areas as well.

- ii -

sustainability. It also highlights critical issues and recommends key policy and institutional changes to enhance the efficiency of rural financial market operations. 4. This report presents the findings of Phase II of a two-part study, which has focused on the issues raised in the paragraph above (Annex 1). It has been prepared in coordination with a Financial Sector Review, which has assumed responsibility for analyzing the Community Bank system. Although the Community Banks were introduced in Phase I of this study, only basic data on the system has been updated in this report and readers interested in learning more about the Community Banks are encouraged to refer to the (March 2000) Financial Sector Review. The information contained in this report is expected to inform the development of a vision for a privately-oriented financial system to serve rural micro and small-scale entrepreneurs in the context of a possible rural financial market development program, based on private enterprise and competition in all possible markets. The Macro and Sectoral Policy Environment 5. Economic development plans in many developing countries have historically been characterized by policies that were implemented in pursuit of accelerated industrial development. Nigeria is no exception. While the Government has made impressive policy improvements toward creating an enabling environment for rural financial market development, several ill-designed policies and programs remain, and as a result of these, the vast majority of rural micro and small-scale entrepreneurs still do not have access to adequate credit, savings, and insurance services. The most important of these policies are: (a) the continued funding of a plethora of public micro and rural finance institutions and support programs, with overlapping mandates and unsustainable designs, such as the mandatory charging of concessional lending interest rates by several state-sponsored credit providers; and (b) the inadequate investment in physical and institutional infrastructure, as well as in basic social services in rural areas. Each of these is described in further detail below. 6. The several and identical programs that the Federal Government of Nigeria (FGN) has promoted over the last twenty years, notably the development finance institutions, agriculture development and poverty reduction programs (especially the ACGSF and FEAP), and specialized financial institutions (in particular, the PBN and the Community Banks), need to be rationalized and consolidated. Perhaps the most damaging of these programs is the directed, subsidized credit disbursement through FEAP, which effectively “crowds out” any privately-based micro or rural financial service provision. 7. Although as of June 1999, interest rates are deregulated for licensed commercial and merchant banks, several of the DFIs are still subject to interest rate ceilings. Such interest rate restrictions are inconsistent with general financial sector policies of interest rate deregulation and in particular they constrain the flow of financial resources to the less privileged rural sector. In fact, the Central Bank of Nigeria (CBN) itself has previously agreed that, “The under-pricing of credit…creates excess demand for cheap funds, which have to be administratively managed via a rationing system, which is itself, costly and ineffective…” (World Bank, 1994). 8. There are clearly good intentions behind setting lending interest rates so low, but it ignores the really difficult decision that policy makers considering similar programs all over the world have had to cope with. The “Cruel Dilemma” describes whether, subject to unavoidable budget constraints, to allow more people to solve what may be their binding constraint to income production/poverty alleviation, that is, obtaining access to formal credit or, rather to use the scarce public resources to subsidize relatively few, rationed producers in the real good sector through artificially low lending interest rates. Once it is agreed that the objective is to expand

- iii -

access to credit, the choice becomes clear. Any subsidization of lending interest rates would have to come at the expense of poor people, who have often been found eager to pay higher interest rates for timely and reliable financial services, but who would be deprived from having access to such services, as the funds allocated for such an objective would be wasted instead on subsidized lending interest rates that could benefit only fewer clients. With respect to the “Cruel Dilemma”, it appears that FGN policies still pay tribute to the old paradigm, as if relatively few agricultural producers deserve to benefit from cheap credit, and as if the rural financial market is not considered to become an integral part of the overall financial system. 9. Rural infrastructure and human development remains weak compared to the relatively more developed urban areas. Deficiencies in rural infrastructure, including roads, electricity, and water supply increase per unit transaction costs of providing rural financial services and reduce returns on private rural investments in the real goods sector, and therefore, pose a serious constraint on rural financial market development. In addition, human development services in rural areas remain weak, especially in the areas of education and health. For instance, as of 1995, 63 percent of the urban population versus 26 percent of the rural population had access to safe water (expressed as a percentage of the population with access). Access to roads and electricity follows a similar pattern.3 Also as of 1995, 33 percent of males and 53 percent of females were pre-literate, with literacy rates dramatically decreased in predominantly rural States of Sokoto (84 percent), Jigawa (88 percent), Yobe and Taraba (89 percent).4 Inadequate physical and institutional infrastructure have inhibited the establishment and growth of rural enterprises and the development of rural financial markets. For example, infrastructure deficiencies have contributed to preventing the timely sale of marketable agricultural surpluses and, hence have kept farmgate prices low and lessened incentives to increase production. The availability of appropriate infrastructure and human services need to be increased if financing of the rural sector is ever to be provided on a cost-effective and sustainable basis. The Legal and Regulatory Framework 10. The legal and regulatory framework of the Nigerian RFIs remains weak due to political and technical reasons. For instance, although both the People’s Bank and the Community Banks have undergone organizational restructuring over the last five years, they still continue to be plagued by political influence and limited institutional capacity. In addition, the regulation and supervision standards to which most RFIs are subject have changed over the last two years, and are still in the process of being clarified for the CBN and the institutions that have recently come under its regulation and supervision. These issues continue to translate into poor management practices and weak accountability at the financial institution level. Both the technical capacity of RFIs and the CBN’s regulatory and supervisory framework need to be strengthened before the flow of financial services to the rural areas can be sustainably increased. The most pressing legal and regulatory issues, namely the needed strengthening of the CBN’s capacity to supervise and enforce prudential regulations on the RFIs that have recently come under its supervision and the required enhancement of property rights and framework for secured transactions, are described below.

3 World Bank (1992) estimated that about 70 percent of Nigeria rural road network was in “poor” or “very

poor” condition, with only 5 percent in “good” condition. With 1.1 kilometer of road per 1,000 population, Nigeria’s rural road density is one of the lowest in Sub-Saharan Africa, compared to Cameroon (6.5), Cote d’Ivoire (4.8), and Ghana (2.3). Due in part to Nigeria’s low rural road density, post-harvest losses have been estimated as quite high, ranging between 20 percent in the semi-arid/arid north and 30 percent in the humid forest zones in the south (World Bank, 1994).

4 World Bank (1998) and Federal Office of Statistics (1997).

- iv -

11. Given the wide geographic and functional dispersion of the financial institutions now under the regulatory and supervisory responsibility of the CBN and the central bank’s limited physical and human resources, the regulatory and supervisory framework needs to be reviewed and strengthened during the transition period to appropriately account for the various activities of non-bank financial institutions (NBFIs).5 The activities of the NBFIs, especially the DFIs need to be streamlined, with most of the functions being housed in two to three institutions. Although this report focuses on one of the main DFIs, the NACB, and the PBN, as a major specialized financial institution, the Financial Sector Review being prepared in close coordination with this report is addressing recommended enhancements in the regulation and supervision of the other NBFIs. 12. The FGN is the only institution with the ability to create an environment in which a wider range of assets (tangible or intangible) can be used as collateral for financial transactions. In particular, Nigeria’s current system for creating, perfecting, and enforcing security interests has serious weaknesses, which need to be addressed. This inadequate system negatively affects the costs of credit transactions, the characteristics of credit contracts, and the degree of access by rural micro and small-scale entrepreneurs to financial services. Suitable reforms would include: (a) introducing a new law of secured transactions, which would allow effective use of movable assets, including equipment, inventory, receivables, and consumer goods as collateral; (b) improving the efficiency of public registries, permitting lenders to record pledges of land and housing, and provide quick access to information about existing liens; and (c) introducing a mechanism for expeditious recovery of collateral, including foreclosure of mortgage loans. Restructuring public registries and an improved legal framework are necessary conditions for well-functioning rural financial markets. Major Rural Finance Institutions 13. The main formal and informal financial institutions serving Nigeria’s rural sector are reviewed in Chapter 4. The types of RFIs discussed include one of the DFIs, NACB; one of the specialized banks, PBN (with the Community Banks [CBs] being covered in the parallel Financial Sector Review); three of the rural support programs, FEAP, ACGSF, and NAIC; and three categories of informal rural finance providers, cooperative societies; NGOs; esusus, family and friends, and moneylenders. In addition, this report reviews the scale and scope of trade and input supply financing being carried out by the formal and informal sectors. 14. These semi-formal rural finance providers and support programs have generally had only limited outreach to date and most of the formal and semi-formal institutions are unsustainable as currently designed. A few have recently made great strides toward increasing their outreach, namely PBN, the CBs, and NAIC; nevertheless, all RFIs continue to be severely hampered by existing policies, inadequate funding in relation to their mandates, and lack of technical expertise in banking. To date, the main three RFIs – NACB, PBN, and the CBs have only managed to reach less than ten percent of the rural households. Each of these RFIs is further analyzed in Chapter 4 in terms of their ownership and management, mission and services, performance, and constraints. However, specific options and recommendations for each institution to consider so that they may better contribute to rural financial market development in the future are shared below.

5 The NBFIs referred to in this report include: (a) the seven development finance institutions (NACB,

NIDB, FMBN, NBCI, NEXIM, NEB, and UDB); (b) the two major specialized financial institutions (PBN and the Community Banks); (c) licensed finance companies; (d) primary mortgage institutions; and (e) discount houses.

- v -

15. Based on the findings of a 1994 World Bank study, a 1994 FAO report, and additional survey data gathered as part of the preparation of this report, it has been found that the informal sector continued to provide the bulk of rural dweller’s credit needs (mainly working capital). The three most important sources of rural credit are ROSCAs (40 percent), family (30 percent), and friends; commercial banks come a distant fourth, with only 11 percent of the sample sourcing credit from them. Trade and input supply financing has been found to be widely practiced by these and other informal groups, but despite the well-adapted operations of informal rural finance providers, the total amount of financial services provided by these institutions has not been sufficient to satisfy the rural demand for credit, which is both seasonal and short term in nature. Moreover, by extending loans with an average maturity of three months, the informal sector has not been involved in the provision of medium to long-term credit for term investment in long-gestation crops, livestock, agro-processing, or small-scale irrigation development activities. In addition, informal rural finance providers have not had the technical capacity for assessing the financial viability of projects. Hence, informal rural sector lending, even for short-term loans, has been restricted to traditional activities, whose financial viability has been established over the years. Thus, informal rural lenders have generally tended to rule out financing of new activities, about which they have had little or no knowledge – a typical risk-averse behavior – thereby limiting the provision of rural loans. Recommendations and Next Steps 16. The main recommendations of the study are related to the need to improve the macroeconomic and sectoral policy environment to promote rural financial markets, enhancing the legal and regulatory framework governing the operation of RFIs, building the institutional capacity of the main formal and informal rural finance providers, and the development of the supporting linkage between the formal and informal sectors of the banking system. General recommendations and suggested next steps to forming a holistic rural financial market development strategy and action plan are also included below.

Creating an Enabling Policy Environment

17. While improvements have been made in the policies and laws of Nigeria, especially since 1996, there are still many challenges which need to be met in order to create an environment that is supportive of the development of rural financial markets. Key to building an enabling environment are maintenance of a stable and growing economy as well as improvements in the legal and regulatory framework to improve property rights and enhance the capacity of CBN to effectively supervise and enforce prudential guidelines on several of the RFIs which have recently come under its jurisdiction. In addition, a rationalization and restructuring of several government-sponsored development finance institutions is necessary for the development of rural financial markets. 18. Sound Macroeconomic Policies. Above all, the development of rural financial markets requires sound monetary and fiscal policies which result in macroeconomic stability with low and stable inflation. Extra-budgetary expenditures must also be minimized to ensure price stability. Consistent and rational economic policies foster investor and consumer confidence and encourage the development of rural financial markets. 19. Investment in Rural Infrastructure and Human Services. More resources from FGN budget allocations need to be directed to the rural sector, consistent with the need to invest adequately in rural infrastructure and human services, especially in the areas of providing safe drinking water, roads, electricity, telephone service, health, and education. Structural adjustment policies and deregulation programs, in the late 1980s and early 1990s, have left Nigeria’s agricultural sector

- vi -

largely deregulated; however, the years of austere fiscal policies accompanying adjustment and deregulation diminished the pool of funds available to be invested in rural services. Nevertheless, the creation of off-farm jobs hinges on the existence of essential supporting infrastructure and a pool of well-educated workers. In addition, improvements in on-farm productivity and profitability depend on the quality and density of rural infrastructure and investments in agricultural crop research and post harvest handling technologies. Both are necessary for rural financial market development and depend on adequate rural investment in infrastructure and human services. 20. Rationalization/Consolidation of FGN Rural Development Programs. The numerous microfinance programs that the FGN has promoted over the last twenty years need to be rationalized and consolidated. At present, the missions of many programs overlap. Perhaps the most damaging of these programs is the directed, subsidized credit disbursement through FEAP, which effectively “crowds out” any privately-based micro or rural financial service provision. 21. Promoting Private Risk Management. As the FGN lessens its emphasis on state-supported, supply-led interventions in rural financial markets, private risk management mechanisms must accommodate the risks formerly assumed by the government. The FGN should build off the successes achieved in the last several years through NAIC in this regard. NAIC’s operations have become widely recognized throughout West Africa as being innovative and developing best practices and the organization deserves a more in-depth study to discern where further efficiencies in the system might be found. Depending on the results of a more in-depth analysis and institutional development plan, the NAIC might be a good candidate to receive a one time injection of further funds to increase its share capital and make it a good candidate for privatization, provided it would keep the majority of its business oriented toward its core operations – meeting the insurance needs of Nigeria’s rural farm and off-farm enterprises.

Enhancing the Legal and Regulatory Framework

22. General areas of action regarding the legal and regulatory framework include: (a) adapting regulation and supervision to the growth of NBFIs; (b) promoting self-regulation of NBFIs; (c) provision of deposit insurance to specialized financial institutions; and (d) enhancing property rights in terms of recognizing non-traditional forms of collateral and promoting credit bureaus and rating agencies. In this section, we raise these issues as recommended areas of further research over a longer-term. No specific recommendations are provided here. The Next Steps matrix at the end of this section appropriately notes each of the issues raised below for further review and analysis over the longer term. 23. Adapting to the Growth of NBFIs – Appropriate Regulation and Supervision. The regulatory and supervisory framework needs to be reviewed and need to be strengthened to embrace the recently expanded activities of NBFIs. The legislation that governs the entry, capital adequacy, legal lending limits, risk classification standards should be adapted to the specialized operations of informal NBFIs that mobilize deposits. Furthermore, there is a need to harmonize and coordinate the efforts of apex organizations to maintain sustainable growth patterns in the informal system. 24. Adapting to the Growth of NBFIs – Effective Deposit Insurance. Another dimension to the issue of providing adequate protection to the investing public, particularly individuals, collective investment institutions, and contractual savings institutions, from mismanagement, is to instill confidence in the system, and ensure capital market stability by providing effective deposit insurance. The regulatory framework should clearly delineate the rights and obligation of parties engaging in financial transactions, and assure adequate disclosure, transparency, and protection

- vii -

for small and relatively unsophisticated depositors and investors. This is especially an issue with the large numbers of depositors in NBFIs such as the PBN and the Community Banks. Determining what form effective deposit insurance should take (for example, traditional deposit insurance or other, more indirect mechanisms such as an apex stabilization fund to instill depositor confidence and effectively safeguard funds), however, merits further review. 25. Clearly Defining Property Rights. Property rights need to be more clearly defined. Small agricultural producers in Nigeria tend not to hold secure title to land they own and farm. The absence of clear and legally-recognized ownership or access contributes to under-investment and unsustainable exploitation of the natural resource base. Farmers without title to land are unlikely to invest in productivity-enhancing technologies and to adopt soil and water conservation practices. These issues particularly affect women’s access to adequate micro and rural financial services. Ill-defined property rights also inhibit lending for long gestation crops without real collateral.

Building the Institutional Capacity of the Main RFIs

26. Several common issues affect each of the rural finance providers examined in this report. The scarcity of skilled banking professionals, which is a generic problem of the banking industry affects the main rural finance providers as well. Poor managerial and technical skills of both the formal and informal financial institutions are major bottlenecks to efficient rural financial intermediation. In addition, the maintenance of concessional interest rates by many of the RFIs continues to generate inadequate returns to cover costs and has generally led to severe liquidity constraints for the rural financial system. A rationalization of the plethora of state-sponsored RFIs and support programs is badly needed, and the restructuring of most of the institutions will be a necessary condition for the development of Nigeria’s rural financial markets. The Financial Sector Review being prepared in coordination with this report contains recommendations to combine the seven DFIs into two or three institutions. Recommendations regarding the Community Bank system have also been reserved for the Financial Sector Report. The one DFI analyzed here, NACB, is recommended to undergo substantial restructuring and revitalization, so that it may restructure its balance sheet and adjust its operating policies and procedures to be on a path to financial self-sustainability. The PBN, as in the case of NACB, should also undergo dramatic restructuring. Specific recommendations which address these concerns follow. 27. NACB: This institution has the largest branch network of any commercial bank or DFI, and is second only to the Community Banks in terms of the total number of rural outlets. Regarding overall country coverage, NACB has the greatest geographic representation and the best coverage of major agricultural centers in the rural areas. In addition to the extensive physical network, NACB also has substantial investment in human capital. The total number of its staff as at April 14, 1999 was 1,660. This number comprised 33 management staff, 508 senior staff, and 1,119 junior staff. The number of staff at headquarters was 432, while 1,228 were in the field. The organization benefits from over 25 years of accumulated wealth of experience in smallholder finance. Although many staff have left and low morale is a lingering problem, most of the remaining staff are dedicated professionals and are hopeful that the organization will change for the better, with adjustments in NACB’s operating policies and procedures. The staff who have been there the longest appear to be technically competent, well-experienced professionals in rural lending. 28. Perhaps most importantly, NACB’s senior management are aware of international best practices in rural finance, including the provision of micro and small-scale financial services, and are eager to adapt these to the context of Nigeria. There is widespread support in the organization

- viii -

for dramatically changing the operating policies and procedures to overcome the constraints identified above. 29. Provided NACB successfully undergoes a significant and widespread restructuring and revitalization process, this DFI would merit further recapitalization and restructuring of its debt burden. Critical elements of such a restructuring program would include: (a) balance sheet restructuring and adjusting the products and services offered; (b) changing the mission to emphasize financial self-sustainability; (c) appointing a new Board of Directors and instituting appropriate staff incentive systems to ensure appropriate governance; (d) introducing incentive systems for clients; (e) training in micro and rural finance institution management, operations, and lending technologies; and (f) improving the quality of its management information systems and reporting. Each of these areas is discussed in more detail in Chapter 4. 30. PBN. As recommended for NACB, PBN should also embark upon a substantial restructuring program so that it can be positioned to the a path towards financial self-sustainability in the near term. PBN’s on-lending of funds from FEAP should cease immediately, as it competes with PBN’s own loan products and creates the image of PBN as a cheap, short-term government credit disbursement center instead of a long-term financial service provider. Essential elements of PBN’s restructuring program would include areas similar to those described for the NACB above and are described further in Chapter 4.

Encouraging Banking System Linkages

31. In order to develop deeper, more efficient and complete markets, competitive forces have to be allowed to be in play. In Nigeria, competition in rural financial markets is largely absent. The predominant actors are state-owned, specialized financial institutions, credit granting NGOs, and informal financial suppliers. The clientele of each is segmented. The terms and conditions for each typical provider varies significantly. Financial costs are lowest for the state-owned institutions but the transaction costs are the highest. The reverse is true for the informal lenders. Part of the solution entails expansion of financial service provision along a sustainable path by NACB and the PBN. By virtue of being close to their clients, each of these institutions intermediates between community-based, informal groups and the formal financial sector with less processing time and expense than commercial banks. Strengthening these RFIs would facilitate banking system linkages. Another part of the solution requires building and strengthening trade and input supplier financiers and other informal providers of rural financial services. These intermediaries have a potentially significant role to play in the development of supplier finance and other inter-linked contracts. Specifically, improving the regulation and supervision of cooperatives that provide financial services, coupled with expansion of a properly established cooperative financial structure, along the lines of the Bauchi State Cooperative Financing Agency Limited as discussed in Chapter 4, could provide an excellent linkage between the formal and informal financial sectors.

Next Steps

32. The options and recommendations provided in the last section have been summarized below in matrix form. The recommendations fall under short, medium, and long-term priorities. The findings of this report, along with the prioritized recommendations, will enrich the Bank’s dialogue on financial sector issues with the FGN, as well as lead to the development of a vision for a privately-oriented financial system to serve rural micro and small-scale entrepreneurs in the context of a possible rural financial market development program, based on private enterprise and competition in all possible markets.

- ix -

33. This study has attempted to provide a holistic treatment of the major issues affecting the constitution and performance of rural financial markets serving micro and small-scale enterprises in Nigeria. As such, it exposes several important complex areas that require further, more focused analysis to appropriately address them. Specifically, more detailed qualitative and quantitative analyses of NACB, PBN, NAIC, and ACGSF need to be carried out in the context of working papers geared toward redefining their mandates and developing institutional development plans for each, where warranted. Two additional working papers would further sharpen the analysis and refine the recommendations of this report. The first would be focused on: 1) macro issues specifically related to the “Eight Pillars of Urban-Biased Policies” traditionally found to hamper the development of rural financial markets in many developing countries; and 2) the comparative advantages, if any, Nigerian farmers have in their production in import substitution or export crops. The second would more concretely address the issue of trade financing as a potentially important mechanism through which to substantially improve the performance of rural financial markets. Finally, a demand and supply analysis of the number and types of “constrained borrowers”, similar to previous studies carried out in El Salvador, Mexico, and Romania would complement the findings of this report and facilitate the production of any warranted institutional development plans for NACB, PBN, NAIC, or ACGSF. 34. As part of this ESW, the Bank is co-sponsoring a three-day sub-regional conference on micro and rural finance to be held in September, 2000 in Abuja, Nigeria. This conference is being closely coordinated and co-sponsored with the Central Bank of Nigeria, the Ford Foundation, USAID, DFID, IFAD, UNDP, and several other major stakeholders, including microfinance institutions operating in Nigeria and the West Africa Region. The objectives of the conference are to: validate the findings of this study, exchange views on “best practices” in rural microfinace and building consensus on the way forward. The outcome of this stakeholder meeting is expected to prepare the way for preparing an operation to support the implementation of the recommendations of this study.

Recommendations Priority Matrix

Issue(s) Problem(s) and Empirical

Evidence Recommendation(s)

Immediate Recommendations Rationalizing the plethora of similar government programs.

Several of the DFIs, the PBN, and FEAP have overlapping mandates and program designs with varying degrees of unsustainability, requiring large amounts of continued state support.

Consolidate the seven DFIs into two to three institutions, streamlining their mandates, restructure NACB and the PBN as part of this rationalization process, and phase out FEAP. Restructure the ACGSF to increase its outreach and operating efficiency.

Recommendations for the Short-Term

Promoting better rural risk management.

As the FGN decreases its emphasis on state-supported, supply-led interventions in rural financial markets, private risk management mechanisms must accommodate the risks formerly assumed by the government.

Develop an institutional development plan for NAIC to become a privatized insurance provider while keeping its focus on insuring rural farm and off-farm enterprises on a commercial basis.

Recommendations for the Medium-Term Developing formal - informal financial sector linkages.

The predominant actors are state-owned, specialized financial institutions, credit- granting NGOs, and informal financial suppliers, with the clientele of each being segmented and relatively unconnected to the formal financial system.

Restructure NACB and PBN so that they can operate along a sustainable growth path, and build on their existing strength in intermediating between community-based, informal groups and the formal financial sector with less processing time and expense than commercial banks. Strengthen linkages between the formal financial sector and trade and input supplier financiers and other informal providers of rural financial services, as they have a potentially significant role to play in the development of inter-linked contracts.

Recommendations for the Long-Term Ensuring macroeconomic stability.

Large fiscal deficits and extra-budgetary expenditures can lead to rising inflation, undermining the ability of financial institutions to set appropriate interest rate policies and extend loan maturates.

Adopt a combination of sound fiscal and monetary policies to keep inflation low and controlled, minimize policy reversals and avoid contradictory policies across Ministries and between the Federal and State levels of government.

- - x

Issue(s) Problem(s) and Empirical

Evidence

Recommendation(s)

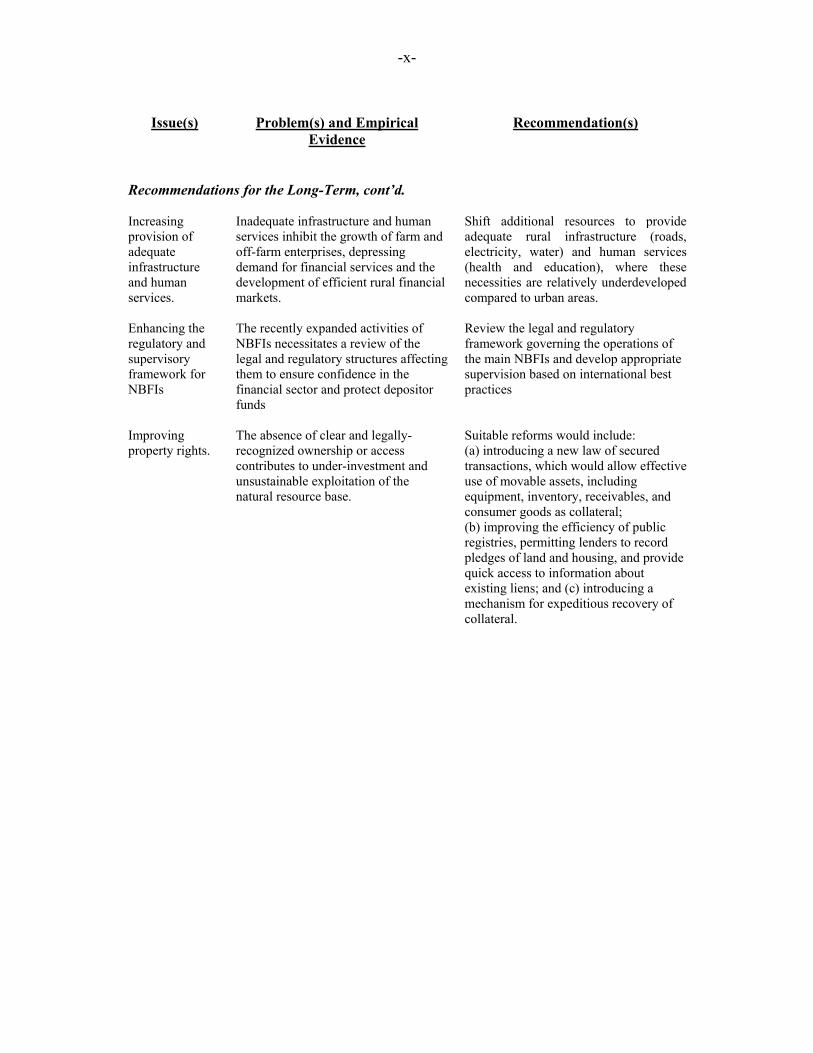

Recommendations for the Long-Term, cont’d.

Increasing provision of adequate infrastructure and human services.

Inadequate infrastructure and human services inhibit the growth of farm and off-farm enterprises, depressing demand for financial services and the development of efficient rural financial markets.

Shift additional resources to provide adequate rural infrastructure (roads, electricity, water) and human services (health and education), where these necessities are relatively underdeveloped compared to urban areas.

Enhancing the regulatory and supervisory framework for NBFIs

The recently expanded activities of NBFIs necessitates a review of the legal and regulatory structures affecting them to ensure confidence in the financial sector and protect depositor funds

Review the legal and regulatory framework governing the operations of the main NBFIs and develop appropriate supervision based on international best practices

Improving property rights.

The absence of clear and legally-recognized ownership or access contributes to under-investment and unsustainable exploitation of the natural resource base.

Suitable reforms would include: (a) introducing a new law of secured transactions, which would allow effective use of movable assets, including equipment, inventory, receivables, and consumer goods as collateral; (b) improving the efficiency of public registries, permitting lenders to record pledges of land and housing, and provide quick access to information about existing liens; and (c) introducing a mechanism for expeditious recovery of collateral.

Chapter 1. INTRODUCTION

A. Background

1.1 Rural financial institutions (RFIs) in Nigeria are complex, given the wide variety of state, collective, and private decision-making groups which influence their operations and use their services. Description and analysis of the rural financial markets is also complicated by the rapid and substantial changes in economic policies in Nigeria over the last two years and, as a result, the need for some of the key RFIs to change. This study examines the environment for the development of rural financial markets in Nigeria, including an analysis of: (a) the main policies, laws, and regulations affecting the public and private delivery of financial services to rural micro and small-scale, farm and off-farm enterprises; and (b) the operation and performance of major formal and informal RFIs in terms of their outreach and sustainability. It also highlights critical issues and recommends key policy and institutional changes to enhance the efficiency of rural financial market operations. 1.2 This report presents the findings of Phase II of a two-part study, which has focused on the issues raised in the paragraph above (also, see Annex 1). It has been prepared in coordination with a Financial Sector Review, which has assumed, as part of its coverage, responsibility for analyzing the Community Bank system. The contents of this report would contribute to the development of a vision for a privately-oriented financial system to serve rural micro and small-scale entrepreneurs in the context of a possible rural financial market development program, based on private enterprise and competition in all possible markets.

B. Objectives and Methodology

1.3 This study seeks to enrich the dialogue between the Federal Government of Nigeria (FGN) and the World Bank on developing a strategy to increase the outreach and sustainability of RFIs. The main objective of this report is to deepen our understanding of the workings of rural financial markets in Nigeria and of those factors which are likely to influence their future performance. Specifically, the report highlights critical macro and sectoral policies as well as laws and regulations affecting rural financial market development and recommends critical policy changes to encourage efficiency in rural financial markets as part of an integrated approach to rural development. The analysis of policies and laws is guided by the “Eight Pillars of Urban-Biased Policies” (Yaron, 1992), which serve as a convenient checklist, on the grounds that international experience has identified a common set of urban-biased policies as commonly inhibiting the development of rural financial markets (Box 1.1).In addition, this report assesses the main providers of formal and informal financial services, using the key performance indicators of outreach and sustainability (Box 1.2).6 Based on these analyses, several recommendations are made in order to strengthen the capacity of RFIs to provide more appropriate and sustainable financial services to rural micro and small-scale rural enterprises.

6 One of the first publications to propose the use of outreach and sustainability as key performance

indicators was Yaron (1992). Since then, these two primary assessment criteria have become generally accepted and widely used in the field of microfinance.

- 2 -

Box 1.1: Eight Pillars of Urban-Biased Policies 1. Overvalued exchange rates. 2. Low, controlled, and seasonally invariant prices of agricultural products. 3. High effective rates of protection for domestic industry, the outputs of which are used as

agricultural inputs. 4. Disproportionately high budgetary allocations for urban, rather than rural infrastructure (roads,

electricity, and water supply.) 5. Disproportionately high investment in human resources in urban, rather than rural areas (health

and education.) 6. Usury laws that rule out the small, risky, and high-cost loans typical in rural areas. 7. Underdeveloped legal and regulatory provisions regarding land titling and collateral for typical

rural assets (land, crops, and farm implements) relative to urban assets (cars, homes, and other durables.)

8. Excessive taxes on agricultural exports. Source: Yaron, Benjamin, and Piprek (1997). Box 1.2: Key Performance Indicators for Rural Finance Institutions The key performance indicators for rural finance intermediaries are based on CGAP’s appraisal format, which is used to assess primarily microfinance intermediaries from four perspectives: (1) institutional factors (such as legal structure, ownership, management, and information systems); (2) the market and services provided; (3) strategic objectives; and (4) financial performance. The ten key outreach and financial performance indicators are listed below. Each represents a summary of more detailed areas of financial analysis. All the indicators should be based on audited balance sheets and income statements that conform to GAAP. • Number of voluntary consumer deposit accounts and outstanding loans. • Total volume of voluntary consumer deposits and outstanding loans. • Average voluntary consumer deposit amount and loan balance per client. • Loan loss rate. • Delinquency rate (loan portfolio at risk over 30 days). • Administrative efficiency. • Operational self-sufficiency. • Adjusted return on average assets. • Subsidy dependence index. • Total voluntary consumer deposits as a percentage of the total outstanding loan portfolio. • Total commercial liabilities as a percentage of the outstanding loan portfolio. Source: Adapted from Fruman and Goldberg (1997).

C. Data Sources

1.4. This report draws from a wide variety of published and unpublished data sources. These include policy and strategy papers prepared by several agencies of the FGN, apex and individual rural finance institutions in Nigeria, and Nigerian academicians. In addition, relevant data and analysis from the published and unpublished financial reports of several private and public rural finance institutions in Nigeria have been used.

- 3 -

D. Organization of the Report

1.5 Chapter 2 summarizes the country context, including macroeconomic indicators relevant to rural financial market operations, the financial sector structure, and the main institutions providing rural financial services. Chapter 3 reviews recent financial sector reforms and analyzes what elements of the policy and legal framework are likely to inhibit or promote the development of rural financial markets. Chapter 4 examines the structure and functions of the main RFIs and assesses their performance. Chapter 5 offers several recommendations on how to create an enabling environment for RFIs and build the institutional capacity of the main providers of rural financial services. The Annexes contain key background documents used in the production of this report, and financial and operational highlights of the RFIs studied.

- 4 -

Chapter 2. COUNTRY CONTEXT

A. Macroeconomic Indicators and Performance

2.1 The state of Nigerian economic development is dismal. Even the low 1997 GDP per capita of US$260 masks the depth of poverty in the country due to highly uneven income distribution. The economy remains dependent on the income generated by the capital intensive oil sector, which provides half of GDP, about 90% of foreign exchange earnings, and approximately 80% of budgetary revenues.7 Agriculture, on the other hand, only accounts for about one-third of GDP but it employs nearly two-thirds of the labor force, and about 90 percent of the rural population. In 1996, it was estimated that about 56 per cent of Nigeria’s total population of about 107 million (or about 60 million people) live below the poverty line and that about 24 percent (or 26 million) could be classified as “hard core” poor.8 It was also estimated that over 60 percent of rural dwellers live in poverty. Poverty in Nigeria is especially pronounced in the northern part of the country, with pockets of severe poverty in the riverine and remote Southern areas.9 2.2 Macroeconomic conditions, however, have markedly improved over the last three years, mainly due to restrictive fiscal and monetary policies pursued during the period 1994 - 1996. The most outstanding achievement is the sharp reduction in inflation from a peak of 72.5 percent in 1995 to 8.5 percent by 1997 and 9.8 percent in 1998. Real GDP growth was over 3 percent in 1996 and 1997, declining only slightly, to 2.4 percent growth in 1998. This has been accompanied by a transformation of the fiscal accounts from a deficit amounting to 15.4 percent of GDP in 1993 to modest surpluses for three consecutive years, 1995 – 1997. Monetary growth has also slowed considerably, from 54 percent in 1993 to 17 percent in 1997, due mainly to decreased claims on the FGN.10 2.3 The interest rate structure has also vastly improved in recent years and this has positive implications for the financial sector and the economy as a whole. While nominal Treasury bill and minimum rediscount rates were steady over the last five years, at about 12 percent and 14 percent, respectively, high inflation translated these into negative real interest rates until 1998 (Box 2.1). Although real saving deposit interest rates remain slightly negative (about negative two percent as of the end of September, 1998), the real Prime lending interest rate was positive for the first time in at least five years. This is due in part to the lifting of imposed maximum lending interest rates and spreads in 1996. This trend toward increasingly positive real interest rates provides incentives to mobilize savings and to increasingly lend funds.

7 The main source of these statistics is Central Bank of Nigeria (1998). 8 “Hard core” poor is a term used to refer to the bottom 50 percent of those living below the poverty line. 9 The statistics presented here are from the World Bank (1994) and Okunmadewa (1998). They are

consistent with the findings of earlier studies by the Nigerian Federal Office of Statistics in 1985 and 1992 as cited in Okunmadewa (1997).

10 Sources of these macroeconomic statistics include the International Monetary Fund (1998), and World Bank (1997 and 1999).

- 5 -

Box 2.1: Interest Rate Structure As at year end, unless otherwise specified Percentages Nominal Interest Rates 1994 1995 1996 1997 1998 Discount Rate 13.50 13.50 13.50 13.50 13.50 Prime Lending Rate 20.20 20.20 19.10 18.40 18.90 Savings Deposit Rate 12.30 12.60 10.10 6.10 6.10 Spread (Len 7.90 7.60 9.00 12.30 12.80

ding – Deposit)

Average Annual Inflation 57.05 72.80 29.29 8.53 10.30 Real Interest Rates 1994 1995 1996 1997 1998 Discount Rate -27.73 -34.32 -12.21 4.57 2.90 Prime Lending Rate -23.46 -30.44 -7.88 9.09 7.80 Savings Deposit Rate -28.49 -34.84 -14.84 -2.24 -3.81 Spread (Lending – Deposit) 5.03 4.40 6.96 11.33 11.61 Sources: International Monetary Fund (1998), World Bank (1999), and the authors’ calculations.

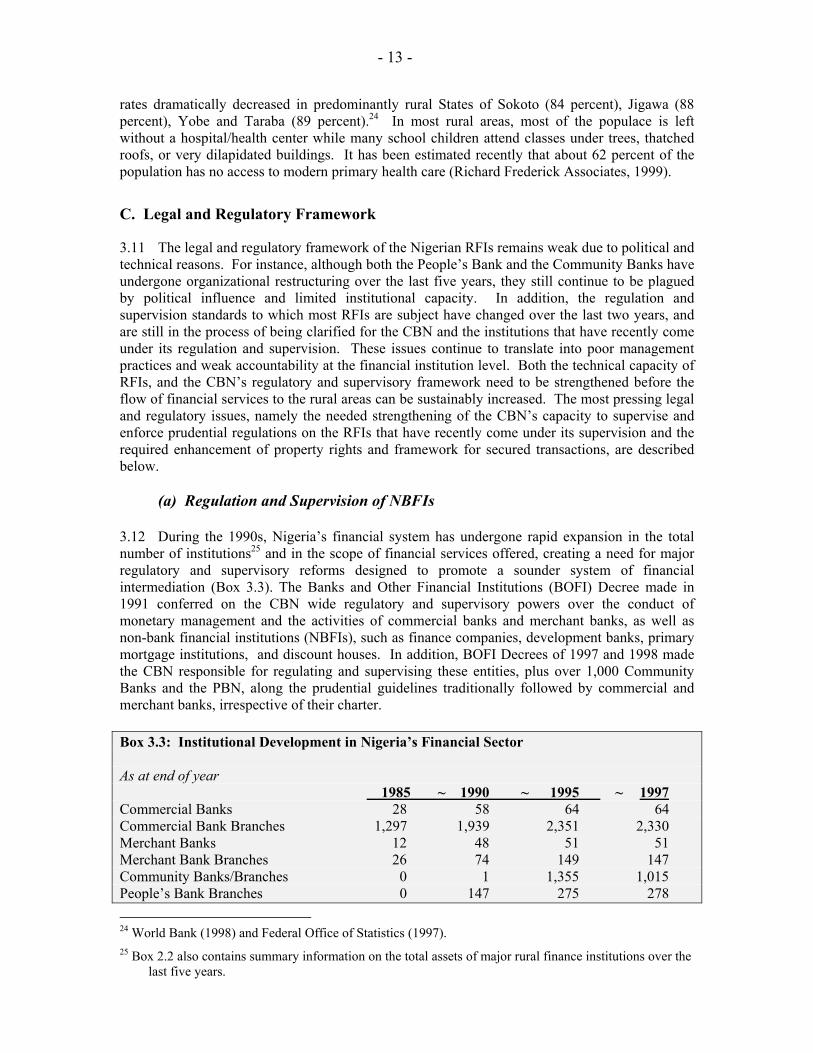

B. Banking System Structure11

2.4 The banking system at the end of 1998 comprised 89 licensed (predominantly private, for-profit) commercial and merchant banks; 1,014 Community Banks (privately owned by community shareholders); the People’s Bank (government owned), with about 278 branches; and seven development finance institutions (DFIs), also government owned-- the Nigeria Agricultural and Cooperative Bank (NACB), the Nigeria Industrial Development Bank (NIDB), the Federal Mortgage Bank of Nigeria (FMBN), the Nigeria Bank for Commerce and Industry (NBCI), the Nigeria Export-Import Bank (NEXIM), and the Nigerian Education Bank (NEB) and the Urban Development Bank (UDB). As a result of the ongoing restructuring and rationalization of commercial banks, the number of commercial bank branches fell from 2,402 in 1996 to 2,330 in 1997. Of these branches, 1,715 (74 percent) were located overseas or in urban areas and 615 (26 percent) were located in rural areas (Box 2.2).12 Merchant bank offices numbered 147 but all were located in urban areas. With the growing distress in the community banking system, 353 community banks had their licenses withdrawn by the National Board for Community Banks (NBCB) in 1997, thus reducing the number of community banks from 1,368 in 1996 to 1,015 in 1997. The total number of banking offices in Nigeria, comprising community, commercial, and merchant banks was 3,492 at the end of 1997, down from 3,917 a year earlier. This contributed to increasing the average number of people per banking office (of these types) from 25,342 in 1996 to 29,137 in 1997. 2.5 Commercial banks remain the dominant providers of financial intermediation, steadily accounting for over 80 percent of total banking assets (Box 2.3), as well as over

11 Box 3.3 depicts the banking system within the overall financial sector structure, as well as changes in

both 1985 – 1997. 12 The main source of these statistics is Central Bank of Nigeria (1998).

- 6 -

80 percent of total banking deposits and total loan and advances of the banking system.13 Merchant banks, which accept block deposits and provide mainly trade finance, account for virtually all of the remainder. Box 2.2: Banking Service Outlets in Rural Areas14 As at the end of 1998 (b) Total Outlets Rural Outlets b/a b/c Commercial Banks 2,330 615 26% 33% Merchant Banks 147 0 0% – NACB 379 379 100% 20% PBN 278 219 79% 12% Community Banks 1,014 710 70% 37% TOTAL 4,148 (a) 1,923 (c) 45% 100% Sources: Central Bank of Nigeria (1998), and published and unpublished financial reports of NACB, NBCB, and PBN (1999, 2000). Box 2.3: Banking System Institutions Total assets as at year end Figures rounded to nearest N billion

1994 1995 1996 1997 1998 Commercial Banks 295 385 459 579 NA Merchant Banks 62 80 90 119 NA NACB 6 6 6 5 5 Community Banks 4 5 5 5 5 PBN 0 0 1 1 2 TOTAL 367 476 561 709 NA Sources: Central Bank of Nigeria (1998), and published and unpublished financial reports of NACB, NBCB, and PBN (various years). 2.6 The Central Bank of Nigeria (CBN) is the primary regulatory and supervisory body for the banking system, and is responsible for protecting the integrity of the payment system. Its basic functions include the issuance of legal tender currency, maintenance and management of external reserves, promotion of monetary stability and sound financial structure, provision of banking services to banks and acts as banker and financial adviser to the government. In addition, there are three other supervisory agencies for the banking sector: the Nigeria Deposit Insurance Corporation (NDIC), which provides deposit insurance (mandatory for all licensed banks) and, in conjunction with the Central Bank, supervises the insured banks; the National Board for Community Banks (NBCB), which is responsible for overseeing the activities of the Community Banks; and the Federal Mortgage Bank of Nigeria (FMBN), which is responsible for the oversight of the primary mortgage institutions (World Bank, 1997).

13 Excluding the Central Bank of Nigeria. 14 “Outlets” include branches, representative offices, service units, etc. where financial transactions occur.

- 7 -

C. Rural Financial Markets

2.7 Rural financial services are provided by both formal and informal financial institutions. The main formal providers include commercial banks, government-sponsored DFIs and rural sector support programs. The most common informal-sector providers, in descending order of importance, are self-help groups, including the rotating savings and credit associations (ROSCAs) locally referred to as “Adashis” or “Esusus” by most Nigerians; family and friends; moneylenders; moneykeepers or savings collectors; and some cooperative societies which provide access to credit.15 This section reviews the major financial institutions operating in the rural areas and examines the structure and overall performance of rural financial markets.

2.8 The operations of the commercial banks continue to be urban-biased and oligopolistic. Less than a third of the total commercial bank branches are located in rural areas and only four banks account for over half of the total rural branch network, receiving only limited competition for rural clients. As of the end of 1997, First Bank of Nigeria had 105 rural branches; Union Bank of Nigeria (UBN) had 91 rural branches, the United Bank for Africa had 86 rural branches; and Afribank had 43 rural branches.16 Micro and small-scale, farm and off-farm entrepreneurs have historically been underserved by the commercial banking system and no new evidence contradicts this pattern. Sectoral allocations of credit extension imposed on commercial banks by the FGN were lifted in 1998 and since then, although commercial banks are prohibited from outright closure of rural branches by the CBN, the trend appears to be de facto closure of rural branches with little new small-scale lending taking place despite presumed continuance of deposit services. The main reasons for this seem to be the perceived high risks associated with operating in the rural environment, coupled with low anticipated returns of providing financial services to rural micro and small-scale entrepreneurs, especially smallholder farmers; lack of adequate rural infrastructure, including roads, telephone service, water, and electricity; and the dearth of knowledge about new financial service provision technologies which commercial banks could use to overcome the relatively high costs of doing business in the rural sector. 2.9 The relative share of total financial intermediation by the government-sponsored DFIs and rural support programs providing credit has been extremely low.17 However, these account for almost the total rural financial services provided. A few RFIs have recently made great strides toward sustainably increasing financial service outreach, namely NACB, PBN, the CBs, and NAIC. Nevertheless, all RFIs continue to be severely hampered by existing policies, inadequate funding in relation to their mandates, and lack of technical expertise in banking. For example, when one compares Nigeria’s total rural population estimated to be about 70 million with even the most liberal outreach estimates for the main rural finance providers – NACB, PBN, and the CBs – at most a combined total of five million clients over the respective lives of the programs, it is clear that the rural sector remains extremely under-served.

15 These claims are based on survey results presented in World Bank (1994). 16 Data on the branches presence of commercial banks was gathered from the 1997 Annual Report of the

Central Bank of Nigeria (1998). 17 The combined financial assets of development banks, insurance companies, and other non-bank RFIs

were estimated at less than four percent of total financial assets in 1997 in a 1999 draft Financial Sector Note prepared by the World Bank.

- 8 -

2.10 Based on the findings of a 1994 World Bank study, a 1994 FAO report, and additional survey data gathered as part of the preparation of this report, it has been found that the informal sector continued to provide the bulk of rural dweller’s credit needs (mainly working capital). The three most important sources of rural credit are ROSCAs (40 percent), family (30 percent), and friends; commercial banks come a distant fourth, with only 11 percent of the sample sourcing credit from them. Trade and input supply financing has been found to be widely practiced by informal groups, but despite the well-adapted operations of informal rural finance providers, the total amount of financial services provided by these institutions has not been sufficient to satisfy the rural demand for credit, which is both seasonal and short term in nature. Moreover, with an average maturity of three months, the informal sector does not appear to be interested in the provision of medium to long-term credit for term investment in long-gestation crops, livestock, agro-processing, or small-scale irrigation. In addition, informal rural finance providers have not had the technical capacity for assessing the financial viability of projects. Hence, even for short-term loans, informal rural sector lending has normally been restricted to traditional activities, whose financial viability has been established over the years. This both ruled out the financing of new activities, about which informal rural lenders had little or no knowledge and decreased the provision of rural loans.

- 9 -

Chapter 3. POLICY, LEGAL, AND REGULATORY ENVIRONMENT

A. Summary of Banking System Policies, Programs, and Reforms

3.1 After experimentation with various development-oriented financial institutions in the former regions of the country during the period prior to independence in 1960, the modern form of DFIs started to emerge with the establishment of the Nigerian Industrial Development Bank (NIDB) in 1964 to promote investment and rapid industrialization. In the 1970s, three other major DFIs were established at the national level, apart from several state development agencies. These three DFIs comprise the Nigerian Agricultural and Cooperative Bank (NACB), established in 1973 to raise output and encourage adoption of new agricultural technologies; the Nigerian Bank for Commerce and Industry (NBCI), created in 1978 to promote small and medium-scale enterprises; and the Federal Mortgage Bank of Nigeria (FMBN), also begun in the late 1970s to fund housing development and promote mortgage institutions.18 3.2 In addition to the creation of these DFIs, several state-supported programs were introduced in the 1970s to promote rural banking. Perhaps most important among these was the Rural Banking Program (RBP) which began in 1977 and which was designed to extend banking services to the rural areas. The RBP was implemented in three phases under which commercial banks were mandated to open and operate specific numbers of rural branches. The first phase terminated in 1980, while the second and third phases ended in 1984 and 1989, respectively. The specific objectives of the program were to: (a) mobilize rural savings and financing productive activities in rural areas; (b) finance small-scale industries; (b) establish a banking culture in Nigeria’s rural population; and (d) facilitate agricultural and allied industries to attain self-sufficiency in food production.19 In 1977, when the program became operational, commercial banks had only 13 branches in rural areas.20 As at December 31, 1989, the total number of rural branches opened by commercial banks stood at 756. Since then, the commercial bank presence in rural areas has declined to about 615 branches at the end of 1997, with the remaining branches generally acting as deposit collection centers and most operating at a loss. The RBP was replaced by the community banking system, which was introduced in December, 1990.

3.3 Many other programs were introduced by the government in the 1970s to promote rural banking. Two of these deserve attention because of the large amount of resources allocated to them and the fact that they are still operating today. These are the Agricultural Credit Guarantee Scheme Fund (ACGSF), established in 1977 to guarantee 75 percent of the lending by banks to the rural areas; and the Nigerian Agricultural Insurance Company (NAIC), established in 1988 to provide insurance coverage to farmers and mandated insurance coverage on loans granted by banks to the agricultural sector. To complement the RBP which had been suspended in the wake of financial deregulation, the government established the People’s Bank of Nigeria and the Community Bank system in 1990. Initiated in late 1997, the most recent government sponsored program, designed in large part to supply credit to the rural areas, is the Family Economic Advancement Program (FEAP) of the Family Support Program.

18 Data on these early DFIs was gathered from the Central Bank of Nigeria (1997) and from Odu (1996). 19 Yahaya (1998), page 4. 20 Yahaya (1998), page 5.

- 10 -

3.4 In addition to program promotion, several policies have been introduced over the years specifically to promote rural banking. In an effort to ensure unhindered expansion of banking services to rural areas and the transformation of the rural economy, the CBN waived the feasibility study requirement to support a bank’s application to establish a rural branch in 1977. In the 1980s, as part of Nigeria’s Structural Adjustment Program, the licensing of banks was liberalized to promote a more competitive banking environment and thereby encourage efficient service delivery by the banking system.21 The most notable recent policies are included in Box 3.1.

Box 3.1: Important Policy Reforms Affecting the Banking System, 1996 - 1998 • Sectoral credit allocations were abolished. • Interest rate ceilings and margins were abolished. • Minimum paid-up capital for all banks was raised to N500 million ($5.6 million). • Official announcement that all insolvent banks would have to be recapitalized by March 31,

1997 or be liquidated (although Presidential approval for this still not received as of May 25, 1999).

• The CBN Decree was amended to provide for a part-time chairman and board, and placement of the CBN under the (direct) authority of the Federal Ministry of Finance.

• The NDIC Decree was amended to give it clear authority for administration of distressed bank (having capital adequacy of three percent or less), once taken over by the CBN.

• Elimination of fertilizer subsidy. • Liberalization of exchange rates as of January 1, 1999. Sources: Central Bank of Nigeria (1997 and 1998).

B. Macro and Sectoral Policy Environment

3.5 Economic development plans have historically been characterized by policies that were implemented in pursuit of accelerated industrial development. Nigeria is no exception. Several of the “Eight Pillars of Urban-Biased Policies” introduced in Chapter 1 continue to hamper the development of the rural sector and the promotion of rural financial markets. Pillars related to macro and sectoral policies are discussed below while those related to the legal and regulatory framework are discussed in the following section. The FGN has made impressive policy improvements toward creating an enabling environment for rural financial market development. However, several crucial policy weaknesses remain and as a result of these, the vast majority of rural micro and small-scale entrepreneurs still have inadequate access to credit, savings, and insurance services.

(a) Maximum Interest Rate Ceilings and Spreads 3.6 Although as of June 1999, interest rates are deregulated for licensed commercial and merchant banks, several of the DFIs and specialized financial institutions like PBN are still subject to interest rate ceilings. Such interest rate restrictions are inconsistent with general financial sector policies of interest rate deregulation and constrain the flow of financial resources to the less privileged rural sector. In fact, the CBN itself has previously agreed that, “The under-pricing of credit…creates excess demand for cheap funds, which have to be administratively managed via a rationing system, which is itself,

21 Central Bank of Nigeria (1998).

- 11 -