31

FINISHING TOUCHES Pub 4012 – Pages K-16 to K-22 Pub 4491 – Lesson 31

| Date post: | 09-Sep-2018 |

| Category: |

Documents |

| Upload: | truongminh |

| View: | 215 times |

| Download: | 0 times |

FINISHING TOUCHES

Pub 4012 – Pages K-16 to K-22

Pub 4491 – Lesson 31

FINISHING UP

2

YOU ARE NOT DONE YET

NTTC Training – TY2016 3

●Review intake-Interview

●View return

● [continue] to e-file

●Select Federal Return type

●Select State return type

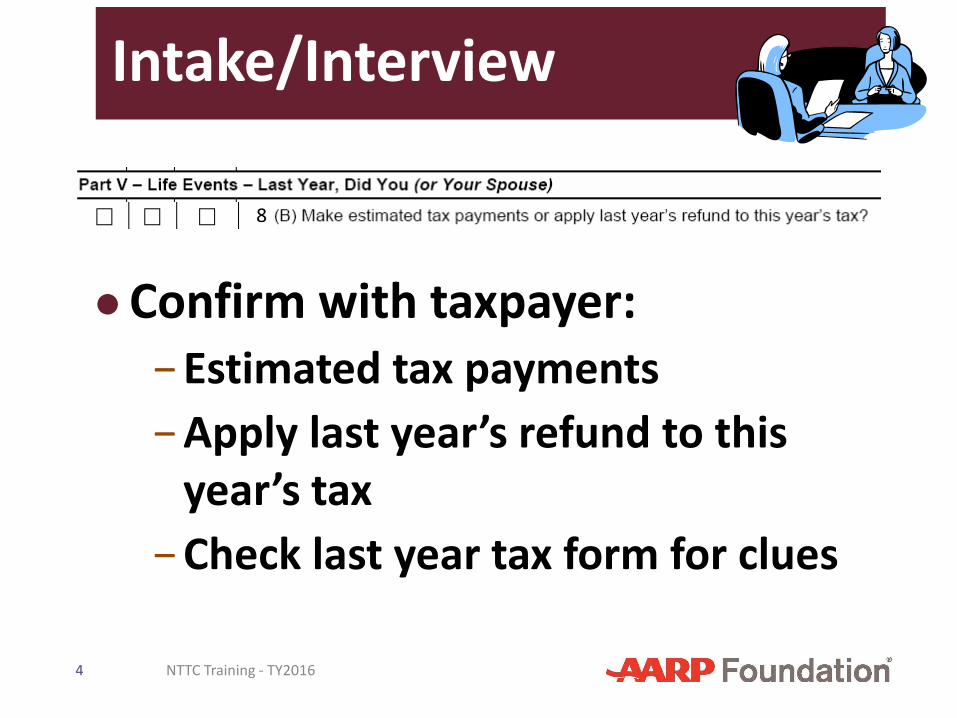

Intake/Interview

●Confirm with taxpayer: −Estimated tax payments

−Apply last year’s refund to this year’s tax

−Check last year tax form for clues

8

NTTC Training - TY2016 4

Estimated Payments

● Typically made if: − Self-employed − Investment income − Projected balance due >$1,000 (to avoid

penalty)

● Payments made periodically by taxpayer

● No form – ask taxpayer if payments made − “When” and “How Much” for each − Check last year’s Form 1040-ES

NTTC Training - TY2016 5

Reporting

NTTC Training - TY2016 6

Refund or Payment?

NTTC Training – TY2016 7

● In TaxSlayer, amounts are shown at top of screen, −Green is a refund

−Red is owed

●Also on 1040 view, Lines 63 – 78

●Client has choices

Refund Options

NTTC Training – TY2016 8

● Receive refund by check

● Receive refund by Direct Deposit − One account -OR- − Split refund

▪ Up to three different accounts ▪ Can deposit to MyRa account ▪ Can purchase US Series I Savings Bond ▪ Can receive a portion in a check

● Apply some or all to next year’s tax

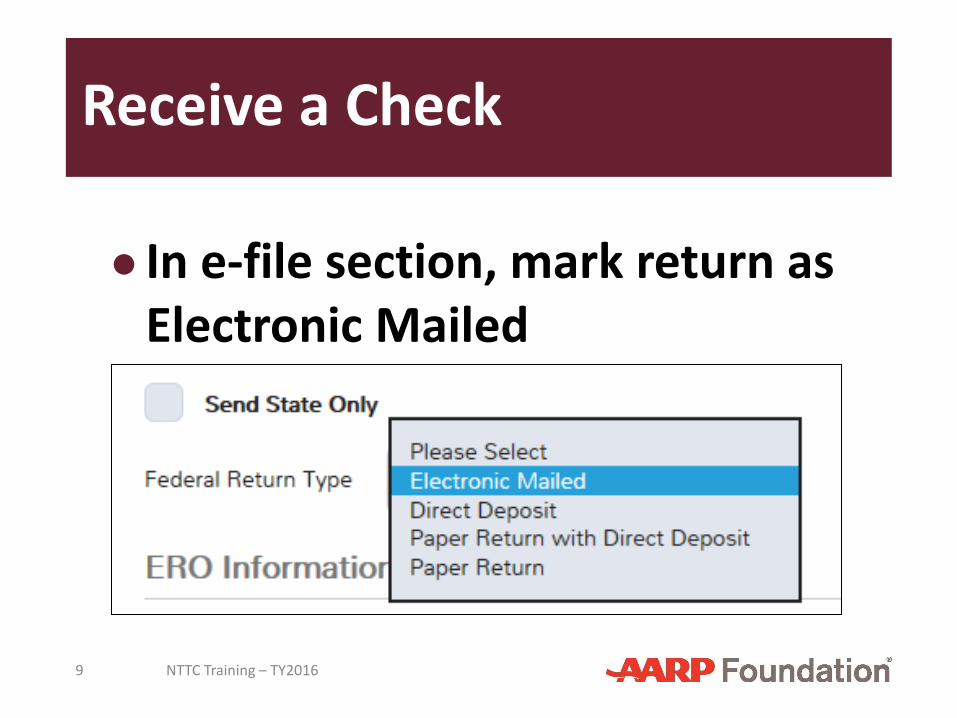

Receive a Check

NTTC Training – TY2016 9

● In e-file section, mark return as Electronic Mailed

Direct Deposits

NTTC Training – TY2016 10

● Encourage Direct Deposit – Pub 4012, Pg K-16 − Faster (1-2 weeks versus 3+ weeks by

mail) − Safer

● Best to take numbers from current check with nine-digit routing transit number and account number

Direct Deposits

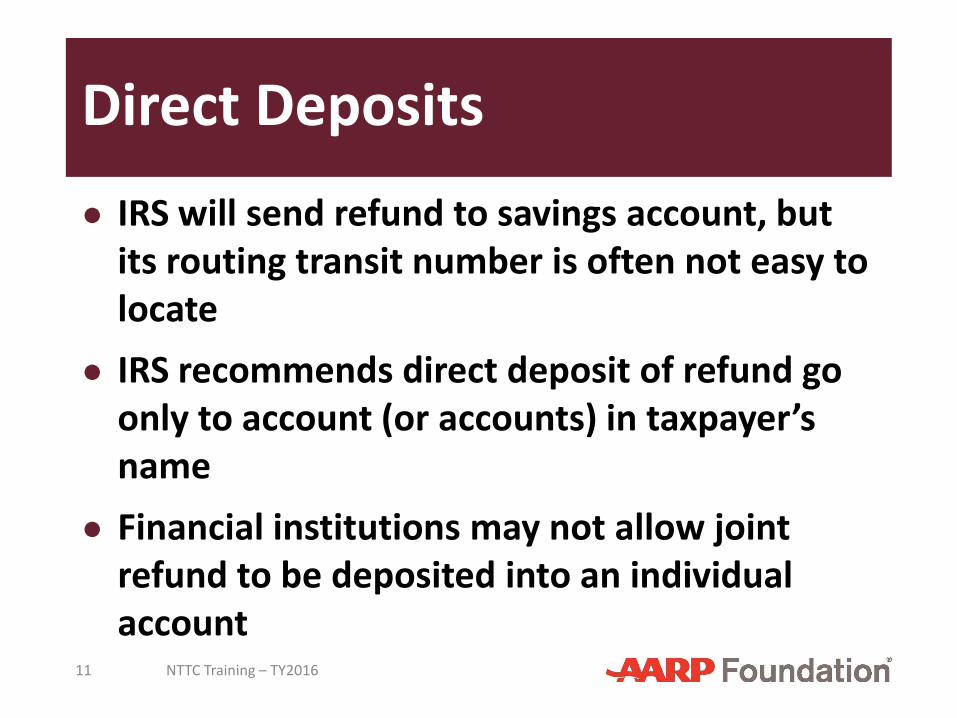

NTTC Training – TY2016 11

● IRS will send refund to savings account, but its routing transit number is often not easy to locate

● IRS recommends direct deposit of refund go only to account (or accounts) in taxpayer’s name

● Financial institutions may not allow joint refund to be deposited into an individual account

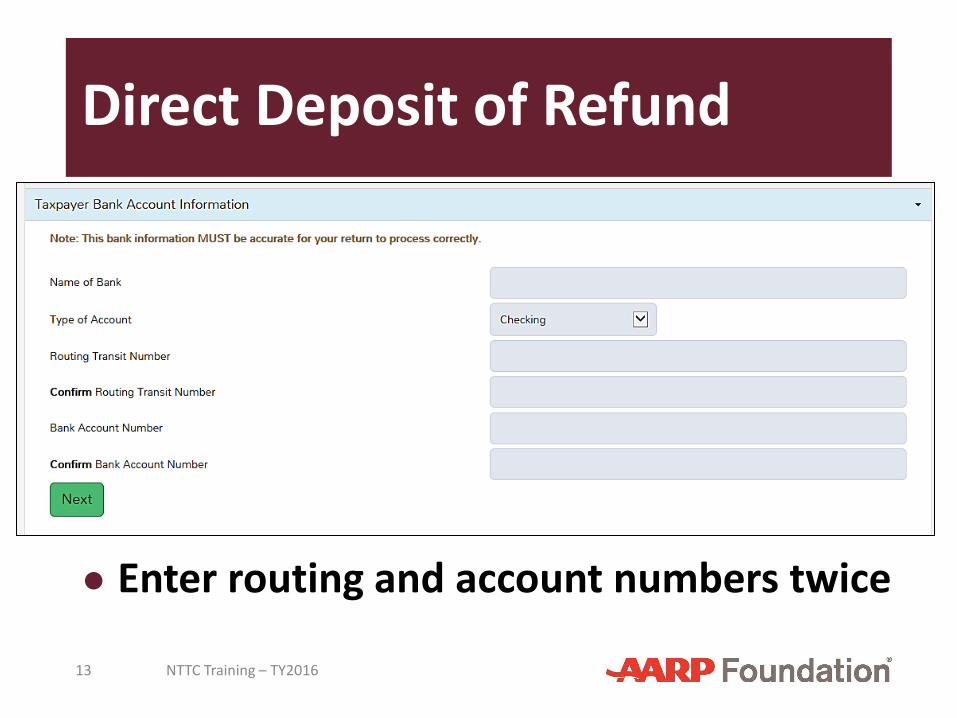

Direct Deposit of Refund

NTTC Training – TY2016 12

● In e-file section, select Direct Deposit

NTTC Training – TY2016 13

Direct Deposit of Refund

● Enter routing and account numbers twice

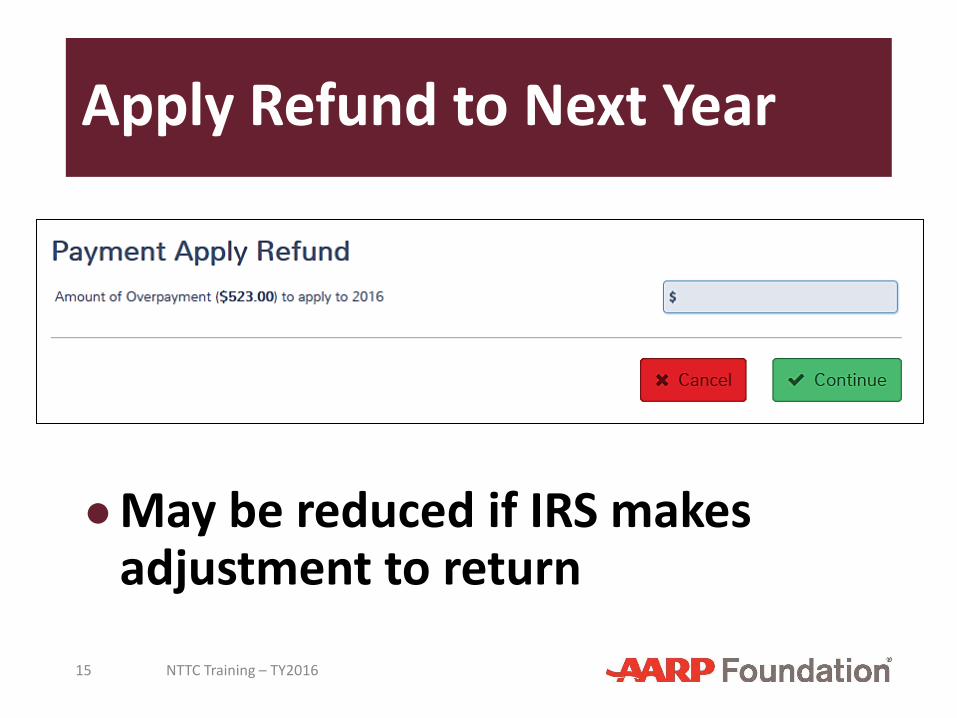

Apply Refund to Next Year

NTTC Training – TY2016 14

● In Payments & Estimates section, select Underpayment of Estimated Tax

Apply Refund to Next Year

NTTC Training – TY2016 15

●May be reduced if IRS makes adjustment to return

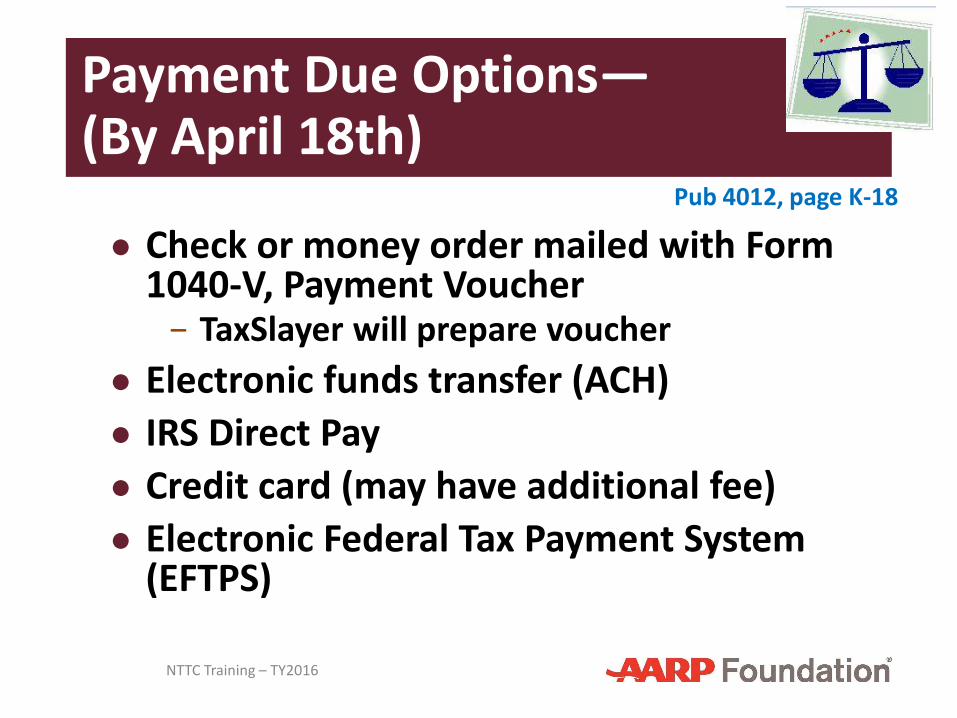

Payment Due Options— (By April 18th)

NTTC Training – TY2016 16

● Check or money order mailed with Form 1040-V, Payment Voucher − TaxSlayer will prepare voucher

● Electronic funds transfer (ACH)

● IRS Direct Pay

● Credit card (may have additional fee)

● Electronic Federal Tax Payment System (EFTPS)

Pub 4012, page K-18

Payment Due—Check

NTTC Training – TY2016 17

●From e-file section, select Mail Payment

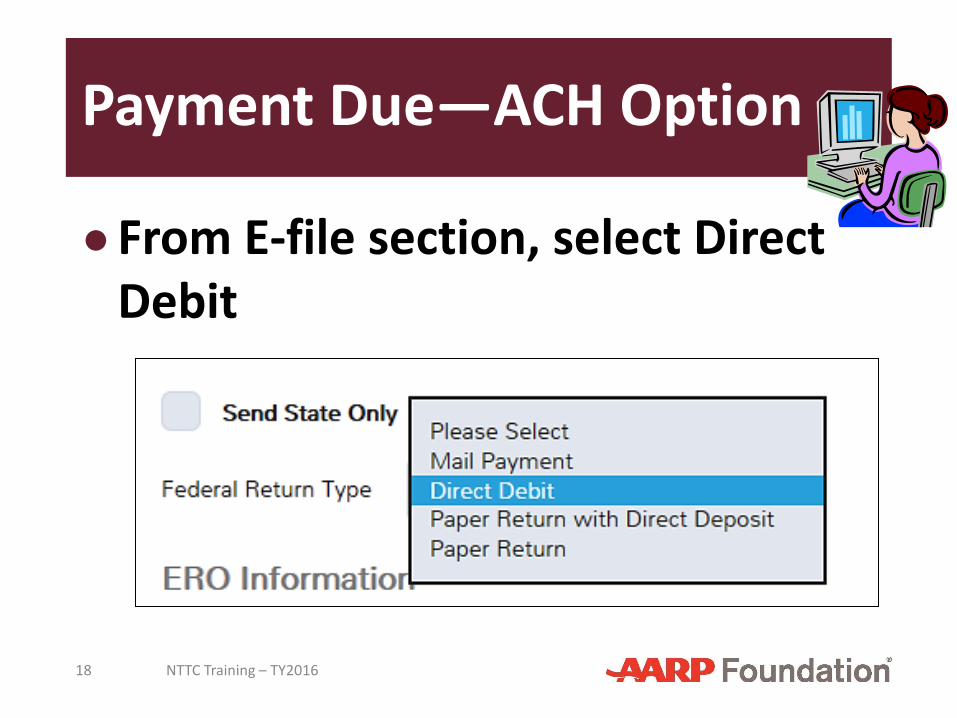

Payment Due—ACH Option

NTTC Training – TY2016 18

●From E-file section, select Direct Debit

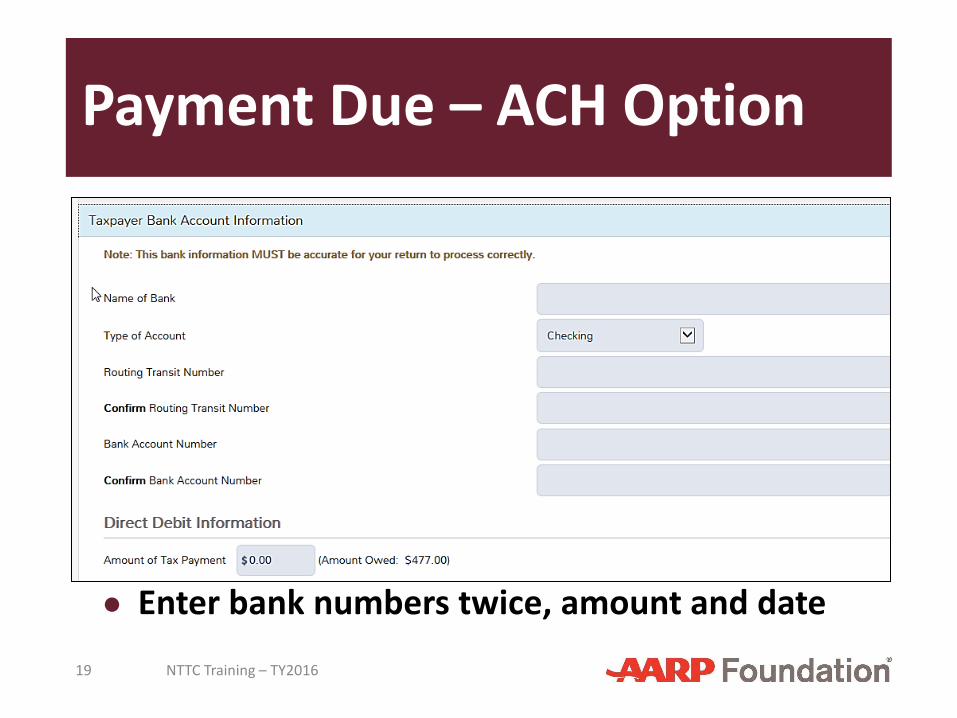

Payment Due – ACH Option

NTTC Training – TY2016 19

● Enter bank numbers twice, amount and date

Payment Due—Direct Pay, Credit Card or EFTPS

NTTC Training – TY2016 20

●Taxpayer does on own through irs.gov/Payments

Pub 4012, page K-18

Can’t Pay Now

NTTC Training – TY2016 21

●Full Pay in 60 or 120 Days

●Monthly Installment Payments

Full Pay in 60 or 120 Days

NTTC Training – TY2016 22

● No user fee

● Interest and penalties apply on amounts paid after April 15

● Apply online at irs.gov/Payments Online Payment Agreement Application

● File return on time or penalty is much higher!

Installment Payments

NTTC Training – TY2016 23

●Through www.irs.gov/payments OR

● In Miscellaneous Forms section, select Installment Agreement (Form 9465)—NEW HIGHER FEES

Online Payment Agreement at www.IRS.gov/payments

NTTC Training – TY2016 24

Line 77 Estimated Tax Penalty

NTTC Training – TY2016 25

● If tax owed is $1,000 or more AND

● Withholding and estimated payments less than the smaller of: − 90% of tax shown on current tax return

OR − 100% of tax shown on 2015 tax return

● Advise the taxpayer of possible penalty

Line 77 Estimated Tax Penalty

NTTC Training – TY2016 26

●We do not calculate penalty

● IRS will automatically compute whether penalty is due based on current year or prior year’s facts

● IRS will send notice and bill if appropriate

Quality Review

NTTC Training – TY2016 27

●No estimated tax penalty shown

●Verify bank information if direct deposit or direct debit

●Verify ACH forms are correct

●State refund or balance due options?

Summary with Taxpayer

NTTC Training – TY2016 28

● Refund or balance due

● If paying balance due by check, ensure understands when/how to mail it

● If under or over withheld − Revise withholding – Forms W-4 − Estimated taxes (another lesson)

● If possible penalty, be sure taxpayer is aware may receive notice/bill from IRS

PAPER WORK

NTTC Training – TY2016 29

● Set the return tag

− Click on Return Tag in e-file area

● Log return on your Activity sheet

● If incomplete prepare “Pink sheet”

● Print return, Review return

● Have client sign the 8879 and state form

● Guide client to QC

RETURN TAGS

NTTC Training – TY2016 30

● 1 E-FILE FINISHED

● 2 E-FILE HOLD 8879

● 3 E-FILE INCOMPLETE

● 4 DO NOT FILE

● 5 PAPER FINISHED

● 6 PAPER INCOMPLETE

Refund/Tax Due

NTTC Training – TY2016 31

Questions?

Comments…