18

KNGX NOTES FINS1613 1 1 [FINS1613] Comprehensive Notes

KNGXNOTESFINS1613

1

1

[FINS1613]ComprehensiveNotes

KNGXNOTESFINS1613

2

2

TABLEOFCONTENTSTableofContents.........................................................................................................................................2

1.Introduction&TimeValueofMoney.......................................................................................................3

2.NetPresentValue&InterestRates..........................................................................................................8

3.ValuationofSecuritiesI..........................................................................................................................19

4.ValuationofSecuritiesII........................................................................................................................29

5.InvestmentDecisionRules......................................................................................................................44

6.CapitalBudgetingI.................................................................................................................................50

7.CapitalBudgetingII................................................................................................................................56

9.CapitalAssetPricingModel....................................................................................................................60

10.TheCostofCapital...............................................................................................................................66

11.CapitalStructure..................................................................................................................................70

12.PayoutPolicy/FreeCashFlowValuationModels..................................................................................78

KNGXNOTESFINS1613

3

3

1.INTRODUCTION&TIMEVALUEOFMONEY

1.1INTRODUCTION

PROJECTS

Keycharacteristics:

1. ProfitsandCosts–cashflows:determinedbya. Expectedamountand;b. Expectedtiming

2. Uncertainty–risk:describedbypossibleoutcomesfromtheproject

TERMINOLOGY

- Ownership:therighttoashareinafirm’sprofits- Control:therighttodirectlymanageorelectmanagementofafirm- Personalliability:theresponsibilitytopayafirm’sfinancialobligationsusingpersonalassetswhen

thefirmcannot- LimitedLiability:alimitthattheownercanonlylosethevalueoftheirinvestmentwhenthefirm

cannotpayitsfinancialobligations

1.2TYPESOFCOMPANIES

SOLETRADER

Asoletraderisabusinessownedandrunbyoneperson.

- Straightforwardtosetup- Noseparationbetweenthefirmandtheowner- Ownerhasunlimitedpersonalliabilityforthefirm’sdebts- Thelifeofasoletraderislimitedtothelifeoftheowner

PARTNERSHIP

Apartnershipisabusinessownedandrunbymorethanoneowner

- Hastwotypesofpartnerso Generalpartners:ownership,controlandpersonalliabilityo Limitedpartners:ownership,nocontrolandlimitedliability

- Thepartnershipendsintheeventofthedeathorwithdrawalofasinglegeneralpartnerunlessotherprovisionsaremade

KNGXNOTESFINS1613

4

4

- Profittaxedatpersonallevel

CORPORATIONS

Acorporationisalegallydefined,artificialbeing,separatefromitsowners.Itactsasitsownentity,abletoentercontracts,acquireassetsinitsownname,sueandbesuedandincurobligationsdirectlywithoutrecoursetoitsowners.

Ownershipofacorporation

- Shares:thedividedownershiporequityofacorporation- Equity:thecollectionofalloutstandingsharesofacorporation- Shareholder:anownerofashareoftheequityinacorporation- DividendPayment:paymentsmadeatthediscretionofthecorporationtoitsshareholders- Sharescanbeownedbyanyone,andcanbetradedfreelyonthestockexchange

Taximplicationsforcorporateentities

- Thecorporationpaystaxonitsownpersonalincomeasitisitsownlegalentity- Whentheremainingprofitsaredistributedtotheshareholders,theshareholderspaytheirown

personalincometaxonthisincome- Thisresultsinwhatisknownas‘doubletaxationwhereyouaretaxedtwiceontheincomereceived- Note:inAustralia,theimputationsystemoftaxationisusedwhereataxcredit(frankingcredit)is

transferredtoshareholdersfortheamountoftaxthecompanyhaspaid

FirmStructure:

Person(s) Role

BoardofDirectors

- Eachdirectoriselectedbythefirm’sowners- HirestheChiefExecutiveOfficer- Monitorsfirmandsetshighlevelstrategy- Hastheultimatedecision-makingauthority- Objectivesistomaximizefirmvalue

ChiefExecutiveOfficer(CEO)

- Everydaymanagerofthefirm- Implementsrulesandpoliciessetbyboardofdirector- Advisedbyhigh(C-)levelexecutives- Objectivesistomaximizefirmvalue

ChiefFinancialOfficer(CFO)

- Evaluatesinvestmentdecisionsforthefirm- Evaluatesfinancingdecisionsforthefirm- Objectivesistomaximizefirmvalue

KNGXNOTESFINS1613

5

5

Advantages Disadvantages

- Limitedliabilityfortheowners- Businesscontinuesoperationwhen

ownershipchanges

- AgencyCostsbetweenownersand

management- Taxation(injurisdictionswith“classical”

taxsystems)

AgencyCosts

- Weassumethatemployeeshavetheirownpersonalobjectives- Thesepersonalobjectivesmaynotalwaysagreewiththevaluemaximizingobjectiveofthefirm’s

owners- Anagencycostariseswhenanemployeetakesanactionthatservestheirowninterestsinsteadof

maximizingfirmvalue.

Owners Liability Owner’sControl

Ownershipchange

dissolvesfirm

Taxation

SoleTrader One Personal Yes Yes Personal

GeneralPartnership

Twoto20(somemayhavemore)

Personal Yes Yes Personal

LimitedPartnership

GeneralPartners(GP)–Atleastone

Personal Yes Yes Personal

LimitedPartners(LP)-Unlimited

Limited No No Personal

Corporations Unlimited Limited No No Companyandpersonal

KNGXNOTESFINS1613

6

6

THEFINANCIALMANAGER

Wewillfocusontwoprimaryresponsibilitiesofthefinancialmanager:

- Investmentdecisionso Whichprojectsshouldthefirmpursue?

- Financingdecisionso Howshouldthefirmraisecapitaltofinancetheseprojects?o Howshouldthefirmdistributeprofitstoinvestors?

1.4THESTOCKMARKET

PRIMARYVSSECONDARYMARKETS:

- Primarymarket:whenacorporationissuesnewsharesandsellsthemtoinvestors- Secondarymarket:marketssuchastheASXorNYSE,wheresharesofacorporationaretraded

betweeninvestorswithouttheinvolvementofthecorporation

BIDVSASKPRICE

- Bidprice:thepriceatwhichabuyeriswillingtobuyasecurity- Askprice:thepriceatwhichaselleriswilingtosellasecurity- Bid-askspread:theamountbywhichtheaskpriceexceedsthebidprice- Transactioncost:inmostmarkets,anexpensesuchasabroker’scommissionandthebid-askspread

investorsmustpayinordertotradesecurities

1.5FINANCIALINSTITUTIONS

Thefinancialcycle:

1. Peopleinvestandsavetheirmoney2. Thatmoneygrowsthroughloansandshares,flowstocompanieswhouseittofundgrowththrough

newproducts,generatingprofitsandwages3. Themoneythenflowsbacktothesaversandinvestors

Allfinancialinstitutionsplayaroleatsomepointinthiscycle.

Thestockmarketorstockexchangeisanorganizedmarketonwhichthesharesofmanycorporationsaretraded

Financialinstitutions:areentitiesthatprovidefinancialservices,suchastakingdeposits,managinginvestments,brokeringfinancialtransactionsormakingloans

KNGXNOTESFINS1613

7

7

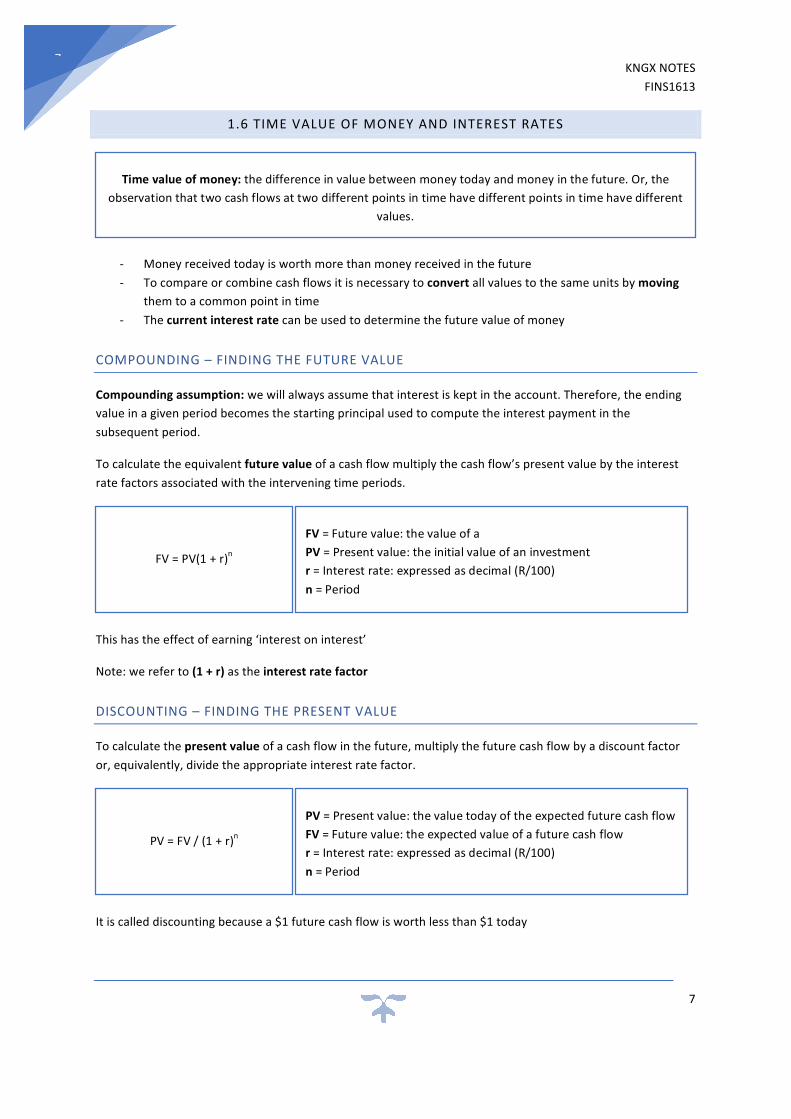

1.6TIMEVALUEOFMONEYANDINTERESTRATES

- Moneyreceivedtodayisworthmorethanmoneyreceivedinthefuture- Tocompareorcombinecashflowsitisnecessarytoconvertallvaluestothesameunitsbymoving

themtoacommonpointintime- Thecurrentinterestratecanbeusedtodeterminethefuturevalueofmoney

COMPOUNDING–FINDINGTHEFUTUREVALUE

Compoundingassumption:wewillalwaysassumethatinterestiskeptintheaccount.Therefore,theendingvalueinagivenperiodbecomesthestartingprincipalusedtocomputetheinterestpaymentinthesubsequentperiod.

Tocalculatetheequivalentfuturevalueofacashflowmultiplythecashflow’spresentvaluebytheinterestratefactorsassociatedwiththeinterveningtimeperiods.

Thishastheeffectofearning‘interestoninterest’

Note:wereferto(1+r)astheinterestratefactor

DISCOUNTING–FINDINGTHEPRESENTVALUE

Tocalculatethepresentvalueofacashflowinthefuture,multiplythefuturecashflowbyadiscountfactoror,equivalently,dividetheappropriateinterestratefactor.

Itiscalleddiscountingbecausea$1futurecashflowisworthlessthan$1today

Timevalueofmoney:thedifferenceinvaluebetweenmoneytodayandmoneyinthefuture.Or,theobservationthattwocashflowsattwodifferentpointsintimehavedifferentpointsintimehavedifferent

values.

FV=PV(1+r)n

FV=Futurevalue:thevalueofaPV=Presentvalue:theinitialvalueofaninvestmentr=Interestrate:expressedasdecimal(R/100)n=Period

PV=FV/(1+r)n

PV=Presentvalue:thevaluetodayoftheexpectedfuturecashflowFV=Futurevalue:theexpectedvalueofafuturecashflowr=Interestrate:expressedasdecimal(R/100)n=Period

KNGXNOTESFINS1613

8

8

2.NETPRESENTVALUE&INTERESTRATES

2.1INTERESTRATES

ANNUALPERCENTAGERATE(APR)

- Financialmathematicsequationsarealwaysstatedintermsofperiodsandinterestratesperperiod- InterestratesareoftenquotedintermsofanAnnualPercentageRate(APR)- APRsmustbeconvertedintonumberofperiodsandinterestratesperperiodforcalculations

CommonAPRcompoundingperiods:

Compounding #ofperiodsperyear

Monthly 12

Quarterly 4

Semi-Annually 2

Annually 1

EFFECTIVEANNUALRATE(EAR)

GivenanAPRandmcompoundingperiodsperyear,theEARcanbefoundasfollows:

AnnualPercentageRate(APR):asimplifiedwaytoquoteinterestrates.Itisequaltothetotalinterestthatwouldbeearnedinayearwithoutcompounding

APR=PerPeriodInterestRate(r)xNumberofCompoundingPeriodsperYear(m) APR=rm

EffectiveAnnualRate(EAR):thetotalamountofinterestthatwillbeearnedattheendofoneyearwithcompounding

EAR=(1+r)m-1 r=perperiodratem=periodsperannum

KNGXNOTESFINS1613

9

9

1. Computetheper-perioddiscountrate,r

2. Computethem-periodinterestratefactor

3. Computetheeffectiveannualrate

SUMARY:APRANDEPR

ConvertingAPRfromEAR ConvertingEARfromAPR

2.2VALUINGASTREAMOFCASHFLOWS

- Projectshavecashflowsoccurringatdifferentpointsintime- Evaluationofcashflowsrequires:

o Buildingatimelineofthestreamofcashflowsdescribingthetimingandamountofexpectedcashflows

o Computingthevalueofthestreamasofareferencepointintime,usuallytheinitialperiod

- Valuingastreamofcashflowscanbedonebytwoapproached:o SequentialApproach:movecashflowsoneperiodatatime,computingthetotalvalueofcash

flowsalreadyconsideredo ReferenceTimeApproach:computethevalueofeachindividualcashflowatthereference

time.Addthesetogetthetotalvalue- Bothapproacheswillgivethesamevalue

- Theterm“futurevalue”canbeconfusingandimprecisewhenappliedtoastreamofcashflows.- Insteadweusetheterms:

o Time-tvalue:avaluefoundbymovingallcashflowstoatimetandtakingthesumo Presentvalue:thevaluefoundattheimpliedreferencepointofaproblem,timet=0

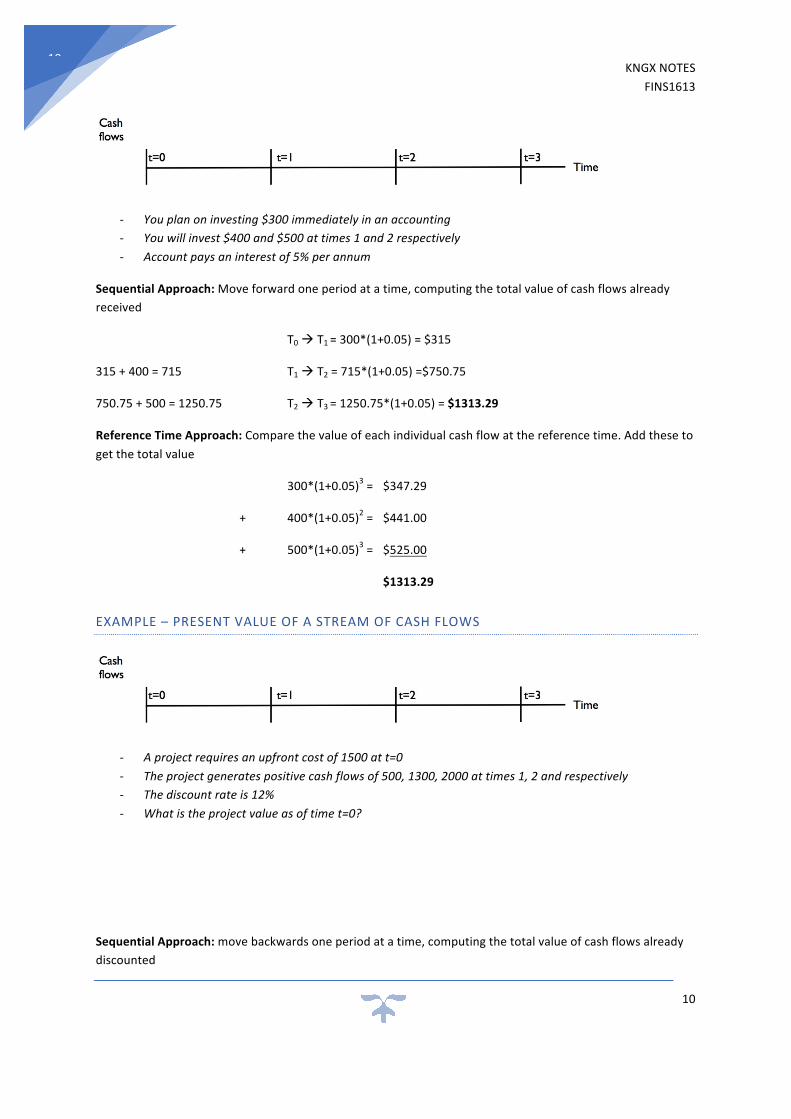

EXAMPLE–FUTUREVALUEOFASTREAMOFCASHFLOWS

KNGXNOTESFINS1613

10

10

- Youplanoninvesting$300immediatelyinanaccounting- Youwillinvest$400and$500attimes1and2respectively- Accountpaysaninterestof5%perannum

SequentialApproach:Moveforwardoneperiodatatime,computingthetotalvalueofcashflowsalreadyreceived

T0àT1=300*(1+0.05)=$315

315+400=715 T1àT2=715*(1+0.05)=$750.75

750.75+500=1250.75 T2àT3=1250.75*(1+0.05)=$1313.29

ReferenceTimeApproach:Comparethevalueofeachindividualcashflowatthereferencetime.Addthesetogetthetotalvalue

300*(1+0.05)3= $347.29

+ 400*(1+0.05)2= $441.00

+ 500*(1+0.05)3= $525.00

$1313.29

EXAMPLE–PRESENTVALUEOFASTREAMOFCASHFLOWS

- Aprojectrequiresanupfrontcostof1500att=0- Theprojectgeneratespositivecashflowsof500,1300,2000attimes1,2andrespectively- Thediscountrateis12%- Whatistheprojectvalueasoftimet=0?

SequentialApproach:movebackwardsoneperiodatatime,computingthetotalvalueofcashflowsalreadydiscounted

KNGXNOTESFINS1613

11

11

T3àT2=2000/(1+0.12)=$1785.71

1785.71+1300=3085.71 T2àT1=3085.71/(1+0.12)=$2755.10

2755.10+500=3255.10 T1àT0=3255.10/(1+0.12)=$2906.34

Deductupfrontcost 2906.34–1500=$1406.34

ReferenceTimeApproach:computethevalueofeachindividualcashflowatthereferencetime.Addthesetogetthetotalvalue

T3àT2=2000/(1+0.12)3=$1423.56

+ T2àT1=1300/(1+0.12)2=$1036.35

+ T1àT0=500/(1+0.12)1=$446.43

Deductupfrontcost - ($1500)

$1406.34

2.3ANNUITIES

CONSTANTANNUITY

ConstantAnnuity:astreamofspecifiednumberofequalcashflowsthatoccursatregularintervals

Theannuityvalueformulagivesthetotaltime-tvalueofallncashflowsbeginningatt+1

EXAMPLE–CONSTANTANNUITY

Annuity:astreamcashflowsarrivingataregularintervaloveraspecifiedtimeperiod

C=Periodiccashpaymentr=perperiodrate

KNGXNOTESFINS1613

12

12

Whatisthepresentvalueofa2-earannuitymakingsemi-annualpaymentsof$50atadiscountrateof4%APR?

AnnuityValuet=0=50x(1/0.02)*[1–(1/1.024)]

=$190.39

ANNUITYFACTORS

Theannuityformulacanbestatedintermsofanannuityfactor:

GROWINGANNUITY

GrowingAnnuity:astreamofspecifiednumberofgrowingcashflowsthatoccursatregularintervals.TheinitialcashflowisCandallsubsequentcashflowsgrowatarategperperiod

Thegrowingannuityvalueformulagivesthetotaltime-tvalueofallngrowingcashflowsbeginningatt+1

C=periodiccashpaymentr=perperiodrateg=paymentgrowthrate

KNGXNOTESFINS1613

13

13

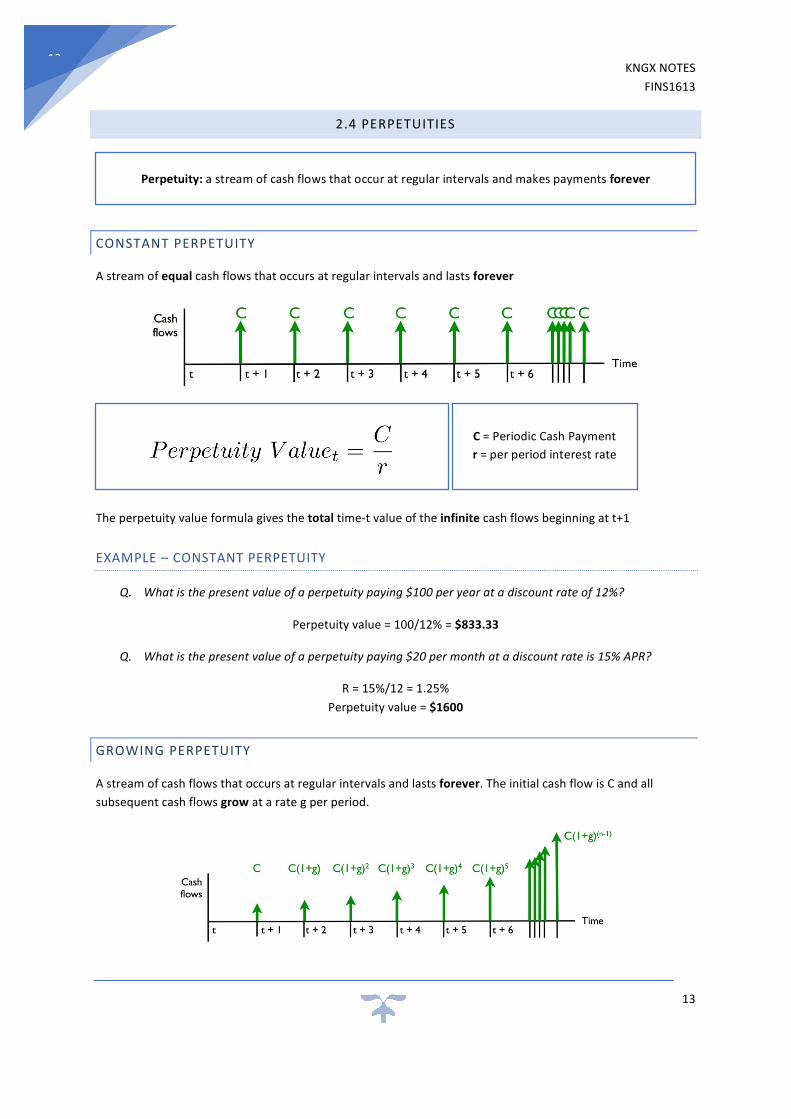

2.4PERPETUITIES

CONSTANTPERPETUITY

Astreamofequalcashflowsthatoccursatregularintervalsandlastsforever

Theperpetuityvalueformulagivesthetotaltime-tvalueoftheinfinitecashflowsbeginningatt+1

EXAMPLE–CONSTANTPERPETUITY

Q. Whatisthepresentvalueofaperpetuitypaying$100peryearatadiscountrateof12%?

Perpetuityvalue=100/12%=$833.33

Q. Whatisthepresentvalueofaperpetuitypaying$20permonthatadiscountrateis15%APR?

R=15%/12=1.25%Perpetuityvalue=$1600

GROWINGPERPETUITY

Astreamofcashflowsthatoccursatregularintervalsandlastsforever.TheinitialcashflowisCandallsubsequentcashflowsgrowatarategperperiod.

Perpetuity:astreamofcashflowsthatoccuratregularintervalsandmakespaymentsforever

C=PeriodicCashPaymentr=perperiodinterestrate

KNGXNOTESFINS1613

14

14

Thegrowingperpetuityvalueformulagivesthetotaltime-tvalueoftheinfinitegrowingcashflowsbeginningatt+1

SUMMARY:ANNUITIESANDPERPETUITIES

Whenusingtheformulasbesurethat:

- Thediscountrate,r,ispositive- Forperpetuities,thegrowthrate,g,mustbelessthanthediscountrate g<r

Checkthetimingofcashflowscarefully

- Formulasgivevalueattimetwhenthefirstcashflowisreceivedatt+1(thenextperiod)

Allannuityandperpetuityequationscanbederivedfromthegrowingannuityequation

2.5THELAWOFONEPRICE

- Pricesrespondtosupplyanddemando Themorepeoplewanttobuysomething,thehigherthepriceo Themorepeoplewanttosellsomething,thelowertheprice

- Arbitragerepresentsanopportunitytomakewithouttakinganyrisksàrisklessprofit- TheLawofOnePricemustholdbecausearbitrageopportunitiescannotexistinfinancialmarketsfor

longperiodsoftime

C=PeriodicCashPaymentr=perperiodinterestrateg=paymentgrowthrate

TheLawofOnePrice:ifequivalentinvestmentopportunities’tradesimultaneouslyindifferentcompetitivemarkets,thentheymusttradeforthesamepriceinbothmarkets.

KNGXNOTESFINS1613

15

15

KeyimplicationsoftheLawofOnePricewhenvaluingcashflowsrelateto:

- Scalingcashflows- Addingandsubtractingcashflows- Delayingandacceleratingcashflows

EXAMPLE–SCALINGOFCASHFLOW

Given:

Whatisthepresentvalueofthecashflowsata10%discountrate?

Thepresentvalueofthecashflowsaboveata10%discountrateis

M*X=2*599.2=$1199.84

Ifthetimetvalueofthecashflowis:

ThenthetimetvalueofMtimesthecashflowis:

EXAMPLE–ADDINGANDSUBTRACTINGCASHFLOWS

Given:

Whatisthepresentvalueofthecashflowsbelowat10%discountrate?

KNGXNOTESFINS1613

16

16

ThepresentvalueofthecashflowsAandBaboveata10%discountrateisX+Y=599.92+49.59=$649.51

IfthetimetvalueofthecashflowsAandBare:

Thenthetimetvalueofthecombinedcashflowsis

Note:thevaluesXandYmustbeatthesamereferencetimeandusethesamediscountrate

EXAMPLE–“DELAYED”CASHFLOWS

Given

Whatisthetimet=0valueofthecashflowsbelowata10%discountrate?

Justdiscountoncemoreatarateof10%=$545.38

EXAMPLE–“ACCELERATED”CASHFLOWS

Given:

Whatisthetimet=0valueofthecashflowsbelowata10%discountrate?

Justcompoundoneperiodatarateof10%=$659.91

KNGXNOTESFINS1613

17

17

SUMMARY:“DELAYED/ACCELERATED”CASHFLOWS

Ifthetimetvalueofcashflowsis:

Delayedby‘s’periods Acceleratedby‘u’periods

Delayedcashflowsarereceivedlater,theyareworth Acceleratedcashflowsarereceivedearlier.“less”,sodivide(discount). Theyare“more”valuable,somultiply (compound).

SAMPLEPROBLEM1

Q.Anannuitydueisanannuitywherethefirstcashflowisreceivedimmediately.Whatistheformulaforthepresentvalueofa7-periodannuitydue?

Solution1:

PresentValue =CashFlowToday+6-periodStandardAnnuityValue =c+c*(1/r)*[1-1/(1+r)6]

Solution2:

Presentvalue =A7-periodannuityacceleratedby1period =c+c*(1/r)*[1-1/(1+r)7]*(1+r)

KNGXNOTESFINS1613

18

18

SAMPLEPROBLEM2

Q.Whatistheformulaforthepresentvalueofaperpetuitywherethefirstcashflowisreceivedatt=5?

Solution:

Presentvalue =PerpetuityValuedelayed4years=(c/r)/(1+r)4

SAMPLEPROBLEM3

Q.Atwo-stagegrowthmodelcombinesanannuityandperpetuity.

Assumeaprojectisexpectedtopay$100in1period.Cashflowswillgrowby15%untilperiod5.Afterthis,cashflowsgrowby3%inperpetuity.Whatisthepresentvalueifthediscountrateis12%perperiod?

Presentvalue =Valueof5-periodrowingannuity+Valueofgrowingperpetuitydelayedby5periods =470.99+1135.78 =$1606.77