Page 1

An Authorised Financial Services Provider

First National First National BankBank

UBS Conference October 2005

In the business world, the rear view mirror is always clearer than the windshield.

Warren Buffett

Page 2

Page 2 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

OutlineOutline

Historical turning points

Regulatory

Competitive

Macro-environment

Creating the future

Page 3

Page 3 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

FNBFNB’’s historic turning pointss historic turning points

1998 2002 2004

Cultural revolutionCultural revolution

• Management replaced by investment bankers

• Businesses chunked

• CEO’s empowered

Outward focusOutward focus

Good to greatGood to great

•Unified FNB•Segment structure

Page 4

Page 4 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

The ability to respondThe ability to respond

Wealth

Public SectorCommercial Corporate

PersonalSmart Solutions

Page 5

Page 5 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

RegulatoryRegulatory

Page 6

Page 6 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Customers feel they overpay Customers feel they overpay

Page 7

Page 7 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

……but there is another side but there is another side to the story to the story

SA perceived to be most expensive

Structural reasons

Pressure from consumerism with possible regulatory response

Fees margins

Page 8

Page 8 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

2.00%

3.00%

4.00%

Advances

A cigarette box illustrationA cigarette box illustration

Up 17bps

Required adjustment for

10% decrease in NIR

Page 9

Page 9 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Deliberate positioning as low cost provider

Innovative pricing options

Customer education campaign

Already taking actionAlready taking action

Page 10

Page 10 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Charter spells opportunitiesCharter spells opportunities

Voluntary signing – 17 October 2003

Integral part of transformation

Requires innovative response

Page 11

Page 11 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Mass Mass –– playing to our strengthplaying to our strength

0

100

200

300

Payo

ut

(P

ayo

ut

( RR’’ mm

))

+182%

MicroloansMicroloans Smart HousingSmart HousingPlanPlan

+75%

2004 20042005 2005

1 313 mini-ATMs

22 Community banks

Page 12

Page 12 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Commercial Commercial –– playing to our playing to our strengthstrength

0

50

100

2004 2005

FES P

ayout

(FE

S P

ayout

( RR’’ mm

))And growing…

FNB Enterprise Solutions (FES)

Enterprises experiencing difficulty with raising capital due to:

o Early stage of development

o Lack of equity or adequate security

o Complexity of financing requirements

Page 13

Page 13 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

National Credit BillNational Credit Bill

PositivesPositives

Opens microloan market for ethical players

Disclosure will favour the trusted brand

No R10 000 exemption

NegativeNegative

More cross-subsidisation across risk profiles

Regulations will determine financial impact

Page 14

Page 14 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

CompetitiveCompetitive

Page 15

Page 15 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Retailers getting more aggressiveRetailers getting more aggressive

• Large credit books

• Extensive infrastructure

• Dominate point of sale

• Better operating hours

• Partnering with large banks

•Deals need proper structuring

•Branch operating hours

•Preference for intra-FirstRand deals

Retailer advantagesRetailer advantages

Page 16

Page 16 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

0

100

200

March April May June July August

So are the cellphone operatorsSo are the cellphone operators

SMS and USSD (not WIG and WAP)

Any network, any cellphone

2.1m SMS customers

Botswana and Namibia next

Transactions processed Transactions processed per month since launchper month since launch

Tra

nsa

ctio

ns

per

month

(‘

000)

Page 17

Page 17 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Even Branson canEven Branson can’’t resist!t resist!

Homeloan direct

Page 18

Page 18 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

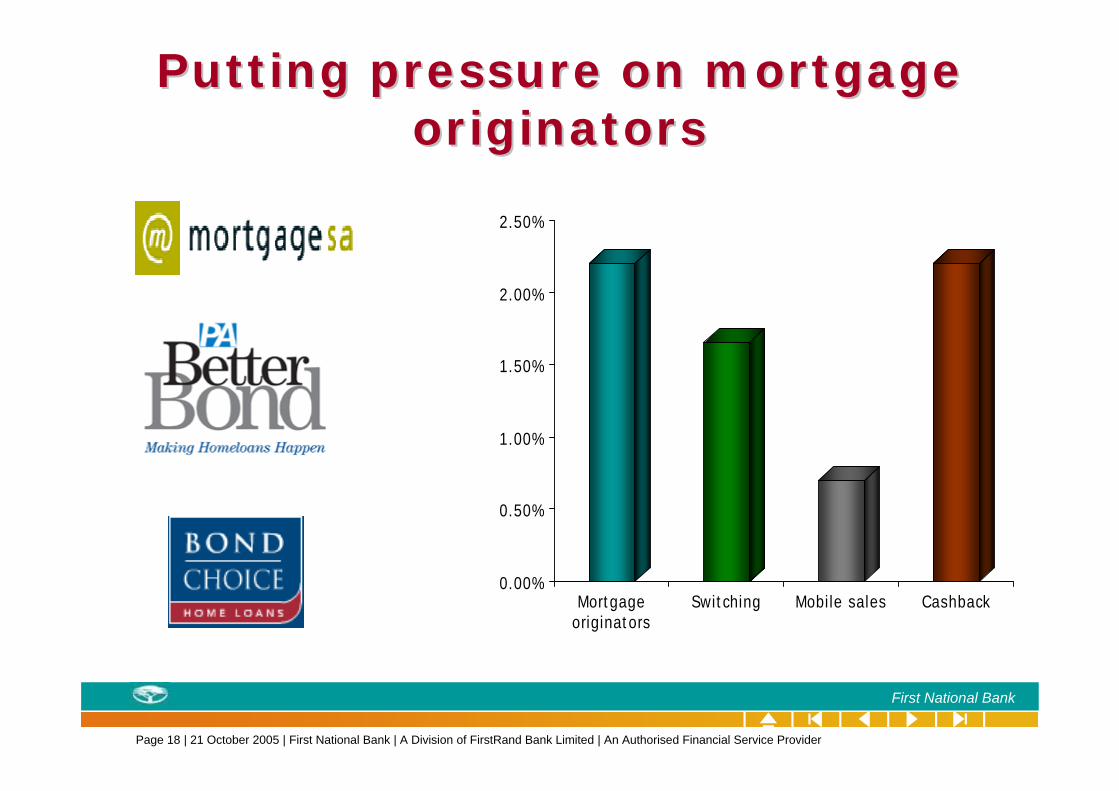

First National Bank

Putting pressure on mortgage Putting pressure on mortgage originatorsoriginators

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

Mortgageoriginators

Switching Mobile sales Cashback

Page 19

Page 19 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Barriers to entry are highBarriers to entry are high

Page 20

Page 20 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Large corporate lending is Large corporate lending is toughtough

0.00%

1.00%

2.00%

Overnight lending - money market

2003 2004 2005

-10

0

10

20

30

40

50

Dec-93 Dec-94 Dec-95 Dec-96 Dec-97 Dec-98 Dec-99 Dec-00 Dec-01 Dec-02 Dec-03 Dec-04

% c

hang

e Y

-o-Y

Page 21

Page 21 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

MacroMacro--environmentenvironment

Page 22

Page 22 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Higher economic growth

World Cup catalyst for growth

Emerging market

Balancing act: Top line growth vs. cost containment

A structural shiftA structural shift

Page 23

Page 23 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Emerging marketEmerging market

10

20

30

40

50

60

70

80

90

100

10 20 30 40 50 60 70 80 90 100

TOP 10%

NEXT 10%

BO

TTO

M5

0%

%

%

MID

DLE

White

Black

Coloured&

Indian

1980

Source: FinMark Trust 2002Source: FinMark Trust 2002

Page 24

Page 24 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

White

Black

10

20

30

40

50

60

70

80

90

100

10 20 30 40 50 60 70 80 90 100

TOP 10%

NEXT 10%

Coloured&

Indian

%

%

BO

TTO

M5

0%

MID

DLE

30%

1991

Source: FinMark Trust 2002Source: FinMark Trust 2002

Emerging marketEmerging market

Page 25

Page 25 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

10

20

30

40

50

60

70

80

90

100

10 20 30 40 50 60 70 80 90 100

TOP 10%

NEXT 10%

%

%

White

Black

Coloured&

Indian

BO

TTO

M5

0%

MID

DLE

30

%

2001

Source: FinMark Trust 2002Source: FinMark Trust 2002

Emerging marketEmerging market

Page 26

Page 26 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Other banks = STD, ABSA,and NedcorSource: Consumer and Business Tracker Research November 2004 and AMPS 2004

MassR0-60K

84%76%

37%46%

39%

22%

16%24%

52%62% 63%

54%61%

78%

38%48%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FNB OtherBanks

FNB OtherBanks

FNB OtherBanks

FNB OtherBanks

White

Black

WealthR750K+

ConsumerR60 – R750K

BusinessR60k – R400m

WellWell--positioned in growing black positioned in growing black marketmarket

Page 27

Page 27 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Branch repositioning

Mobile sales force

FNB Private Clients

FNB Housing Finance

Cellphone Banking

Commercial Property Finance

Capitalising on growthCapitalising on growth

Page 28

Page 28 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Creating the futureCreating the future

Page 29

Page 29 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Single product to integrated Single product to integrated solutionsolution

Page 30

Page 30 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Encouraging savings despite low Encouraging savings despite low interest ratesinterest rates

Page 31

Page 31 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Entrepreneurs need single entryEntrepreneurs need single entry

Page 32

Page 32 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

FirstRand building blocksFirstRand building blocks

Page 33

Page 33 | 21 October 2005 | First National Bank | A Division of FirstRand Bank Limited | An Authorised Financial Service Provider

First National Bank

Thank you.Thank you.