21

First Quarter Report TSX EQB EQB.PR.C For the three months ended March 31, 2018

1

First QuarterReport

T S X E Q BE Q B . P R . C

For the three months ended March 31, 2018

2

Forward-Looking Statements

Certain forward-looking statements may be made in this presentation, including statements regarding possible future business, financing and growth objectives. Forward-looking statements include, but are not limited to, statements relating to our financial performance objectives, vision and strategic goals, the economic and market review and outlook, the regulatory environment in which we operate, the outlook and priorities for each of our business lines, the risk environment including our liquidity and funding risk, and statements by our Chief Executive Officer and Chief Financial Officer. The forward-looking information contained herein is presented for the purpose of assisting the holders of our securities and financial analysts in understanding our financial position and results of operations as at and for the periods ended on the dates presented, as well as our financial performance objectives, vision and strategic goals, and may not be appropriate for other purposes. Forward-looking statements are typically identified by words such as “believe”, “expect”, “foresee”, “forecast”, “anticipate”, “intend”, “estimate”, “goal”, “plan” and “project” and similar expressions of future or conditional verbs such as “will”, “may”, “should”, “could” or “would”. Investors are cautioned that such forward-looking statements involve risks and uncertainties detailed from time to time in the Company’s periodic reports filed with Canadian regulatory authorities. Many factors could cause actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements. Equitable Group Inc. does not undertake to update any forward-looking statements, oral or written, made by itself or on its behalf except in accordance with applicable securities laws.

3

First Quarter Highlights

Solid Quarterly Earnings of $40.2MM

Record Mortgages Under Management of $23.8Bn

2nd Common Share Dividend Increase of 2018

Continued to Enhance and Diverse Our Business

Successfully Expanding Our Role as Canada’s Challenger Bank™

4

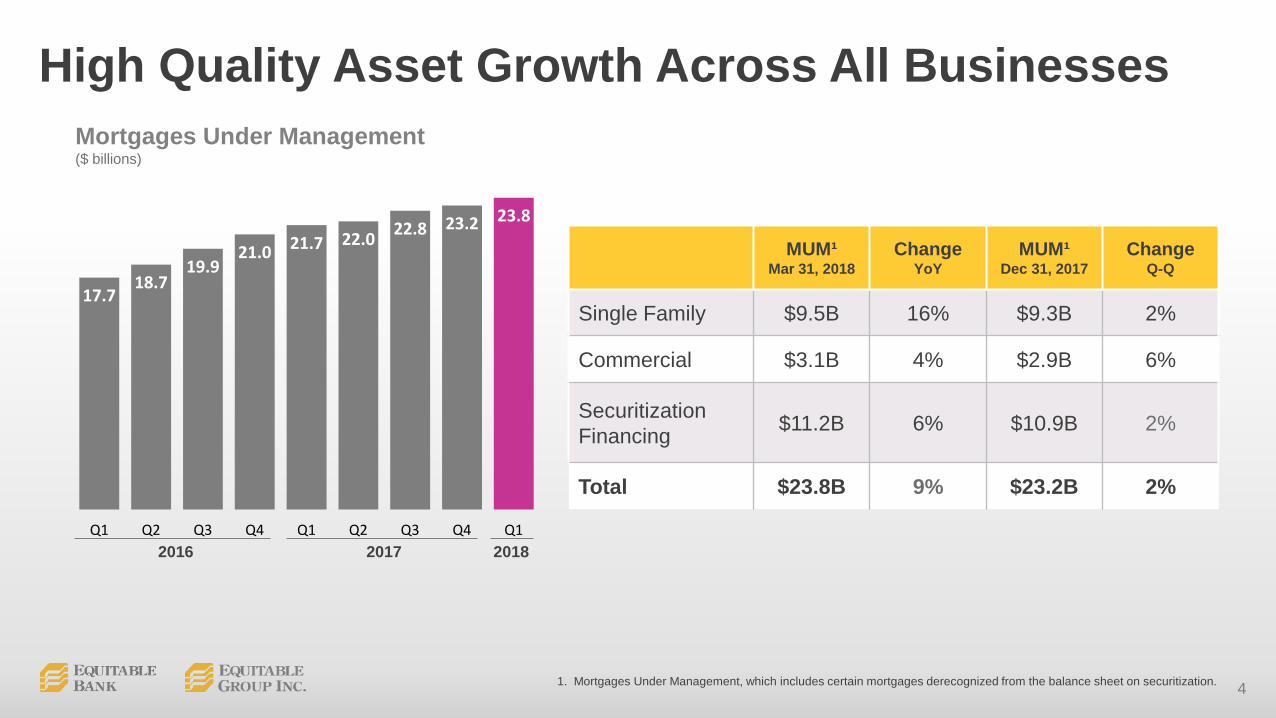

High Quality Asset Growth Across All BusinessesMortgages Under Management($ billions)

17.718.7

19.921.0 21.7 22.0 22.8 23.2 23.8

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q12016 2017 2018

MUM¹Mar 31, 2018

ChangeYoY

MUM¹Dec 31, 2017

ChangeQ-Q

Single Family $9.5B 16% $9.3B 2%

Commercial $3.1B 4% $2.9B 6%

Securitization Financing $11.2B 6% $10.9B 2%

Total $23.8B 9% $23.2B 2%

1. Mortgages Under Management, which includes certain mortgages derecognized from the balance sheet on securitization.

5

Alternative Single Family Lending

4.3 4.6 4.95.4 5.7 5.9 6.2 6.4

6.87.2 7.5

7.9 8.2 8.59.1 9.3 9.5

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q12014 2015 2016 2017 2018

Mortgage Principal($ billions)

Assets Grow Despite Challenging Market Conditions

6

Commercial Lending

4.3 2.3 2.3 2.3 2.3 2.3 2.2 2.2 2.3 2.42.7 2.8

3.02.8 2.9 2.9

3.1

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Mortgage Principal($ billions)

Record Q1 Originations Reflect Increased Strategic Focus on Commercial

2014 2015 2016 2017 2018

7

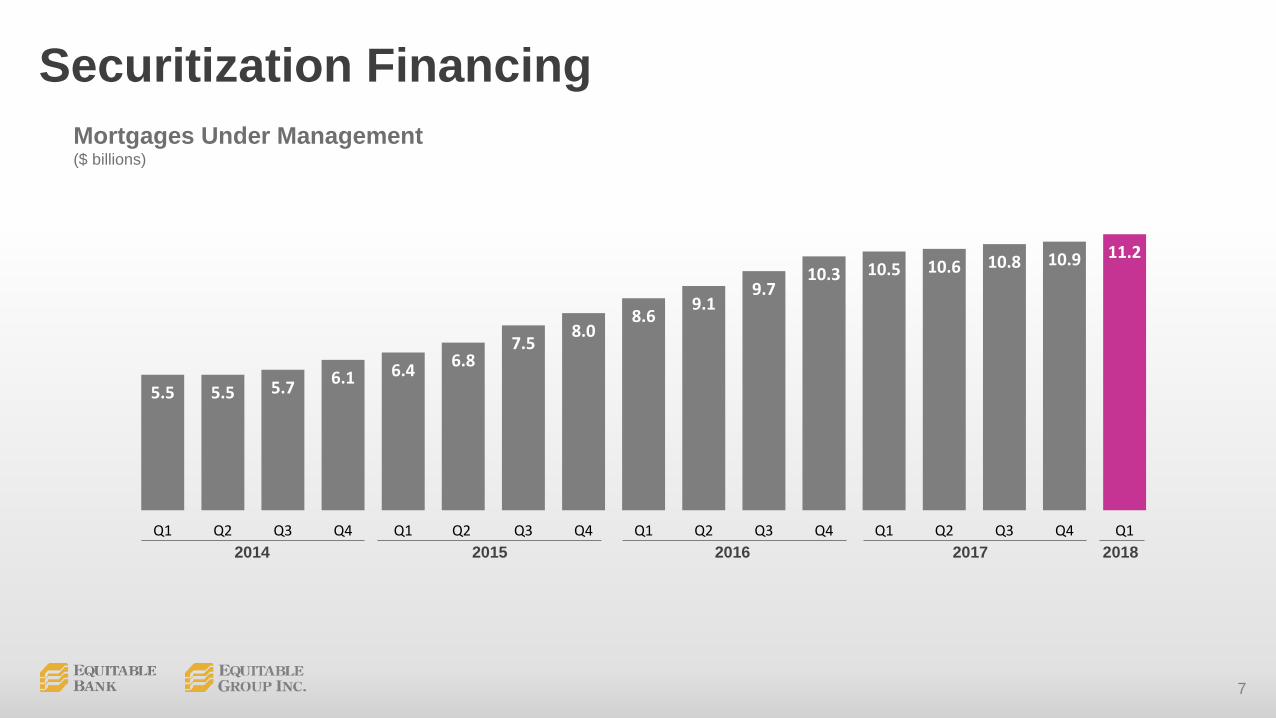

Securitization Financing

5.5 5.5 5.7 6.1 6.4 6.87.5

8.08.6

9.19.7

10.3 10.5 10.6 10.8 10.9 11.2

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Mortgages Under Management($ billions)

2014 2015 2016 2017 2018

8

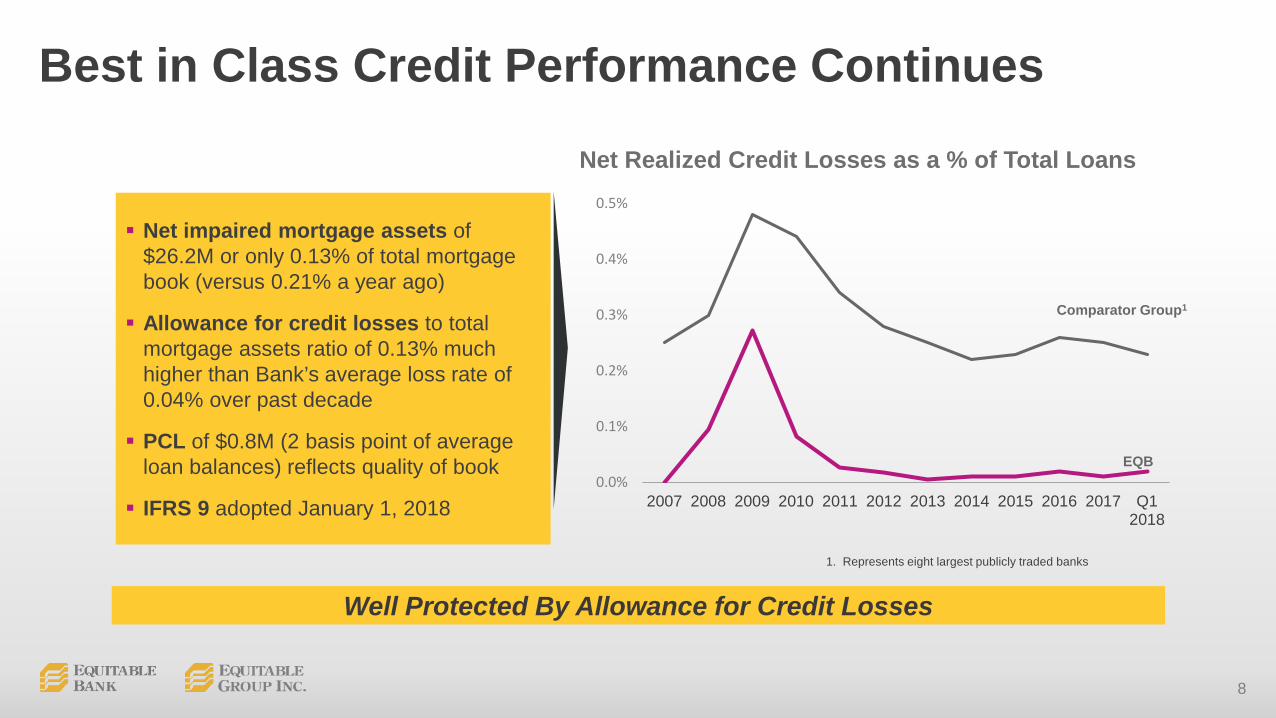

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Q12018

Best in Class Credit Performance Continues

Well Protected By Allowance for Credit Losses

EQB

Comparator Group1

1. Represents eight largest publicly traded banks

Net Realized Credit Losses as a % of Total Loans

Net impaired mortgage assets of$26.2M or only 0.13% of total mortgage book (versus 0.21% a year ago)

Allowance for credit losses to total mortgage assets ratio of 0.13% much higher than Bank’s average loss rate of 0.04% over past decade

PCL of $0.8M (2 basis point of average loan balances) reflects quality of book

IFRS 9 adopted January 1, 2018

9

8.7 9.0 9.29.7 9.9 10.0

10.511.0

11.9

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018

Growing Our Deposit BaseDeposit Principal Balances($ billions)

19% YoY Growth With EQ Bank Ahead 42%

GIC

10

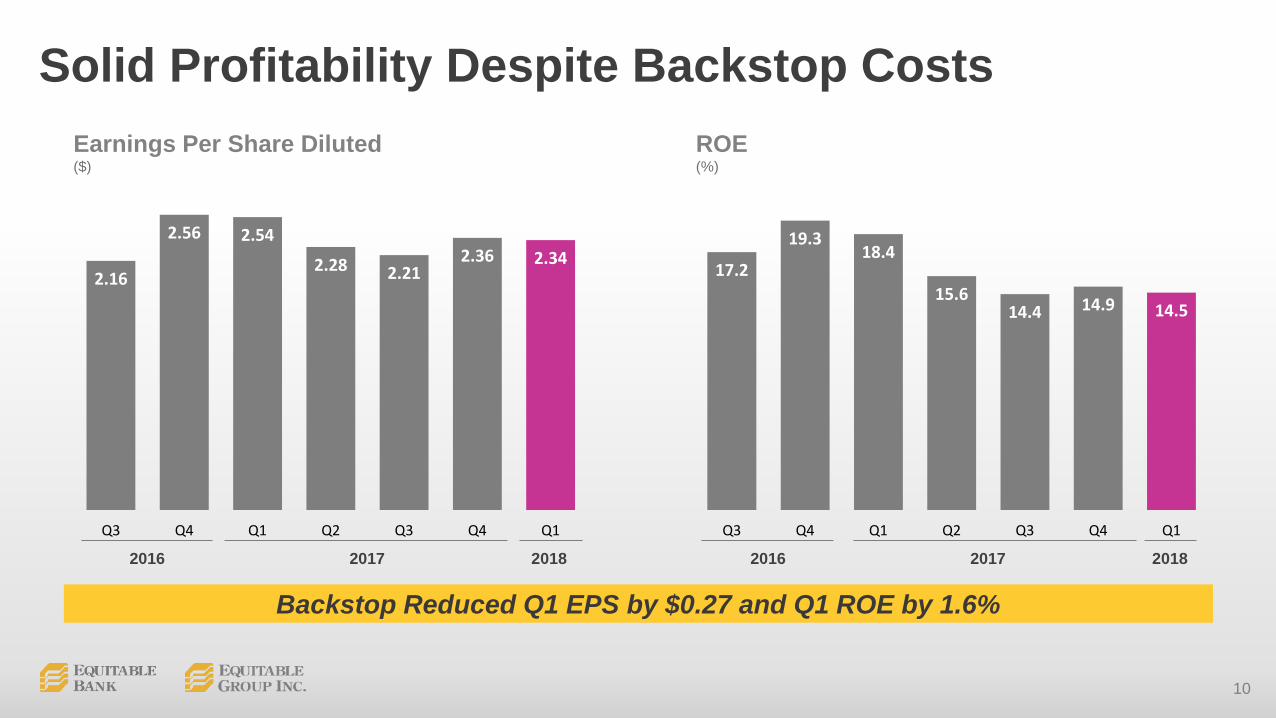

Backstop Reduced Q1 EPS by $0.27 and Q1 ROE by 1.6%

Solid Profitability Despite Backstop Costs

2.16

2.56 2.54

2.28 2.212.36 2.34

Q3 Q4 Q1 Q2 Q3 Q4 Q1

Earnings Per Share Diluted($)

2016 2017 2018

ROE(%)

17.2

19.318.4

15.614.4 14.9 14.5

Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018

11

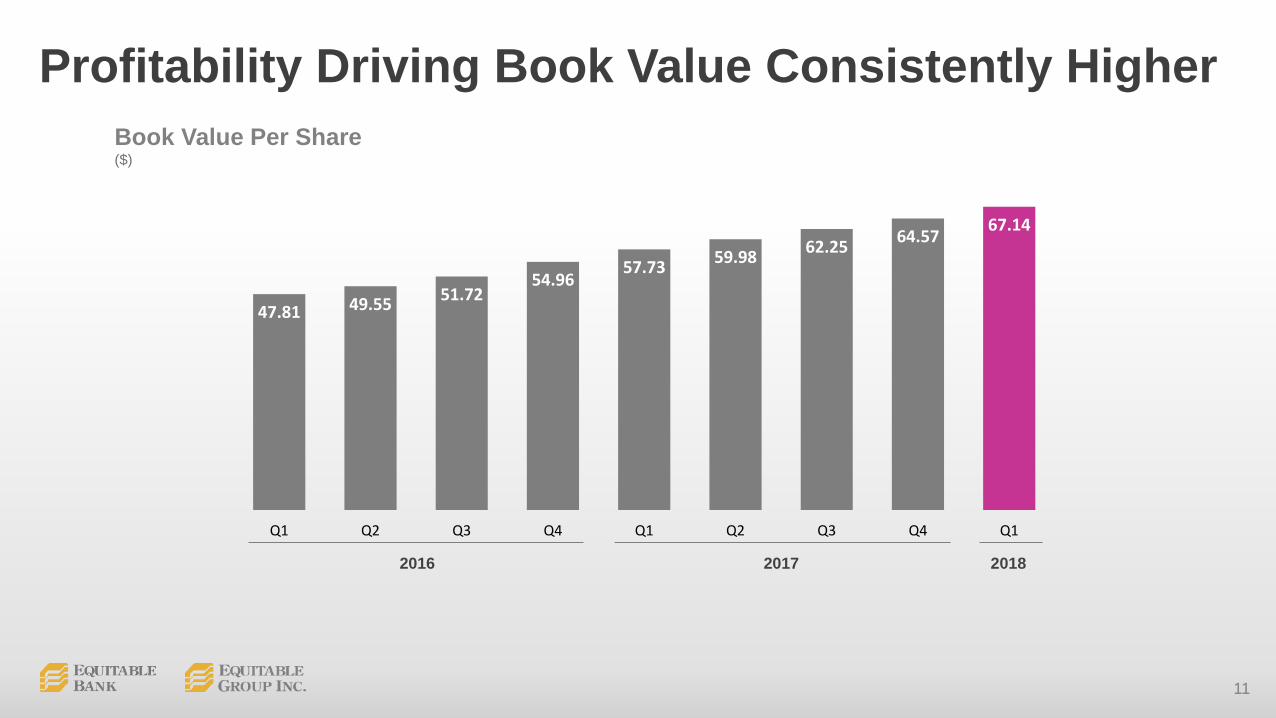

Book Value Per Share ($)

Profitability Driving Book Value Consistently Higher

47.81 49.55 51.7254.96

57.73 59.98 62.25 64.57 67.14

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018

12

0.270.26

0.250.24

0.230.22

0.210.20

0.190.18

0.170.16

0.150.14

0.12

Common Share Dividend Growth Continues

2011 2012 2013 2014 2015 2016 2017 2018

Dividend Per Common Share($)

Announced Second Increase of 2018

13

5.5

14.716.0

Capital Ratios Exceed Requirements

March 31, 2018 (%)

Basel III minimumTotal Capital level of 10.5%Basel III

minimum CET1 target of 7.0%

Full compliance with new standard

Leverage Ratio CET1 Total Capital

14

Liquidity Action Costs And Maple Continue To Influence Performance

Q1/18EPS Impact

Q4/17 EPS Impact

Q1/17 EPS Impact

Liquidity Events Costs ($0.27) ($0.32) Nil

Maple Asset EPS Benefit $0.06 $0.08 $0.11

Liquidity Event Costs Will Be ~$5M Per Quarter in 2018

15

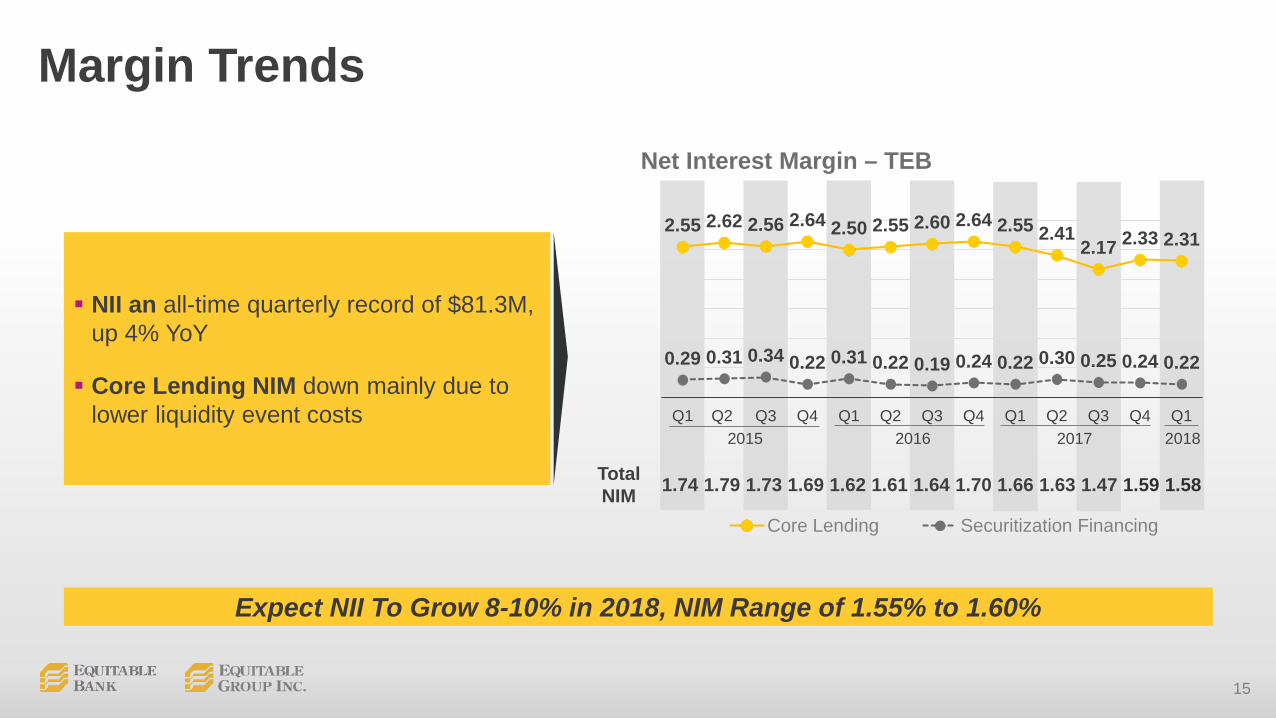

2.55 2.62 2.56 2.64 2.50 2.55 2.60 2.64 2.55 2.412.17 2.33 2.31

0.29 0.31 0.34 0.22 0.31 0.22 0.19 0.24 0.22 0.30 0.25 0.24 0.22

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Core Lending Securitization Financing

Margin Trends

Net Interest Margin – TEB

2015 2016 2017 2018

Expect NII To Grow 8-10% in 2018, NIM Range of 1.55% to 1.60%

TotalNIM 1.74 1.79 1.73 1.69 1.62 1.61 1.64 1.70 1.66 1.63 1.47 1.59 1.58

NII an all-time quarterly record of $81.3M, up 4% YoY

Core Lending NIM down mainly due to lower liquidity event costs

16

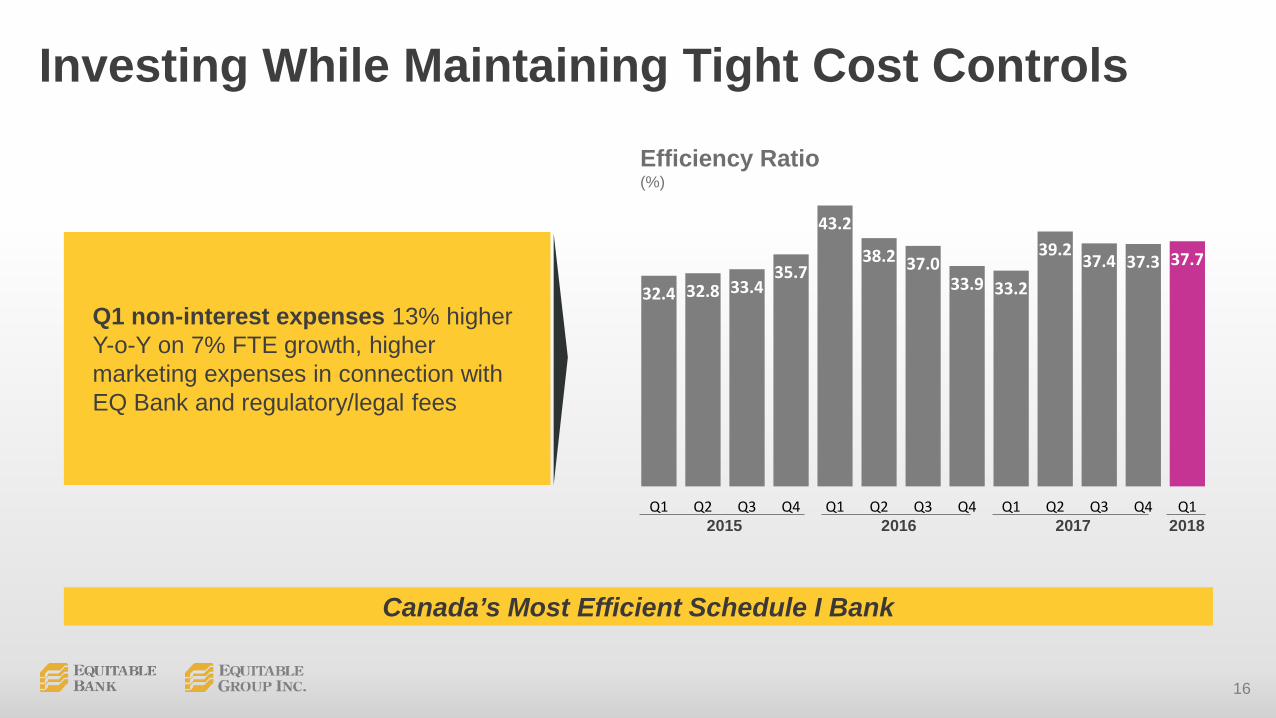

32.4 32.8 33.435.7

43.2

38.2 37.033.9 33.2

39.2 37.4 37.3 37.7

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q12015 2016 2017 2018

Investing While Maintaining Tight Cost Controls

Canada’s Most Efficient Schedule I Bank

Efficiency Ratio(%)

Q1 non-interest expenses 13% higher Y-o-Y on 7% FTE growth, higher marketing expenses in connection with EQ Bank and regulatory/legal fees

17

Strong Operating and Financial Metrics

18

PATH Home Plan Socialization Begins

Target Market

Distribution

Brand

Loan Parameters

• Homeowners 55 years and older• Residents of larger urban centers, such as Toronto or Calgary

• Through Canada’s vibrant mortgage broker community

• Maximum LTV at origination of 40%• Term of up to 5 years• Floating interest rate (based off prime)

• PATH Home Plan branding• Delivers message of reverse mortgages being a natural part of an overall financial plan

19

Deploy capital to grow existing business, with more emphasis on Commercial

Evaluate capital needs relative to opportunities

Consider funding strategies including need, cost of backstop facility post June 2019

2018 Capital And Liquidity Areas Of Focus

Asset Growth Return to Shareholders

P o t e n t i a l C a p i t a l S t r a t e g i e s

20

Our Newest FinTech Partnership

New deposit account offering for Wealthsimple clients

Equitable chosen because of our strong technology foundation and customer-focused approach

Partnership further diversifies funding sources, underscores our focus on digital banking opportunities

21

Summary

Solid quarter of asset growth and profitability

Dividend increased for 2nd time in 2018

Launched EQ Bank GICs, Reverse Mortgages

Expect continued asset growth