u . s . DEPARTMENT OF ENERGY DIVISION OF ENERGY STORAGE SYSTEMS

Grant No. EC-77-G-05-5570

By

C. J. HUANG

NOllC~ I I

j spemoccd 5y .h; Oldt~ Szaln C.~miwnt ~|ther she | United Ststn nor t~e United ~.atcs Dcl~ub-t~n¢ of | | EqeillY . nnc any Or ~ cmpb)~-es, a~ ~ or tSeLr |

I l?gldlltl' °s ~nlzY f~r me ~s~Y. ~mPl~'~n~s I I car Inel'ulllCU or llly lllloflmSllOll, IF'#IIIIlI~I~ FIQIIUCl Ol | | i~ocr~ dbclo~'~, m ~pr~enu ~ Is we woukl not |

WORKSHOP DIRECTOR

UNIVERSITY OF HOUSTON ENERGY INSTITUTE and

DEPARTMENT OF CHEMICAL ENGINEERING

p P

CONTENTS

Workshop Objectives

Workshop Overview

Workshop Summary and Recommendations

Future Supply and Demand of Energy and Hydrogen

Demand and Supply of Hydrogen for Oil Refining, Ammonia and Methanol Synthesis

Demand and Supply of Hydrogen for Small Consumers and Future Technology

Production of Hydrogen from Sources Other Than Oil and Natural Gas

Scenarios and Other Comments for Supplying Hydrogen as a Chemical Feed Stock

Appendix

I

I I

I I I

Steering Committee Membership

List of Workshop Participants

Paper by Dr. ]%hn J. McKetta: What is the Energy Picture . . Tomorrow?

• Today,

IV Paper by Dr. lames H. Swisher: Current At~dtudes Toward Hydrogen Energy Systems and Highlights of Recent Work in the United States and Abroad

V

VI

Paper by Dr. Calvin B. Cobb: Energy and Hydrogen in the United States Refinin9 industry

Tables and Figures by Mr. Hampton G. Corneil: Production Economics for Hydrogen Ammonia and Methanol During the 1980- 2000 Period

1

2

9

13

18

29

41

48

52

54

57

75

86

95

0 [3

VII

VIH

IX

X

XI

XII

XIII

XIV

XV

XVI

XVII

XVIII

Paper by Dr. Paul A. C. Cook: Comments on Methanol

Viewgraph Used by Mr. David Netzer: Production of Ammonia from Coal

Presentation of Mr. R. S. Watson: Use of Hydrogenation in the Edible Oil Industry

Viewgraphs Presented by Mr. David Owens: Hydrogen for Isocyanate Processes

Viewgraphs and Narrative Comments Presented by Mr. A. H. Levy: Hydrogen for Fuel Cells

Table Presented by Mr. R. Pa.rthasarathy: Hydrogen for Coal Liquefaction

Paper by Jim Michaels: Hydrogen Production via Kopper-Totzek Process

Paper by M. C. Goodman: Hydrogen and Carbon Monoxide from Coal by Winkler Press

Viewgraphs Used by Mr. L. J. Nuttalh Hydrogen by Water Electrolysis

Paper by Drs. K. E. Cox and M. G. Bowman: Thermochemical Production of Hydrogen from Water

Graphs Prepared by Mr. W. H. Stanton: Alternate Scenarios of Supplying Hydrogen

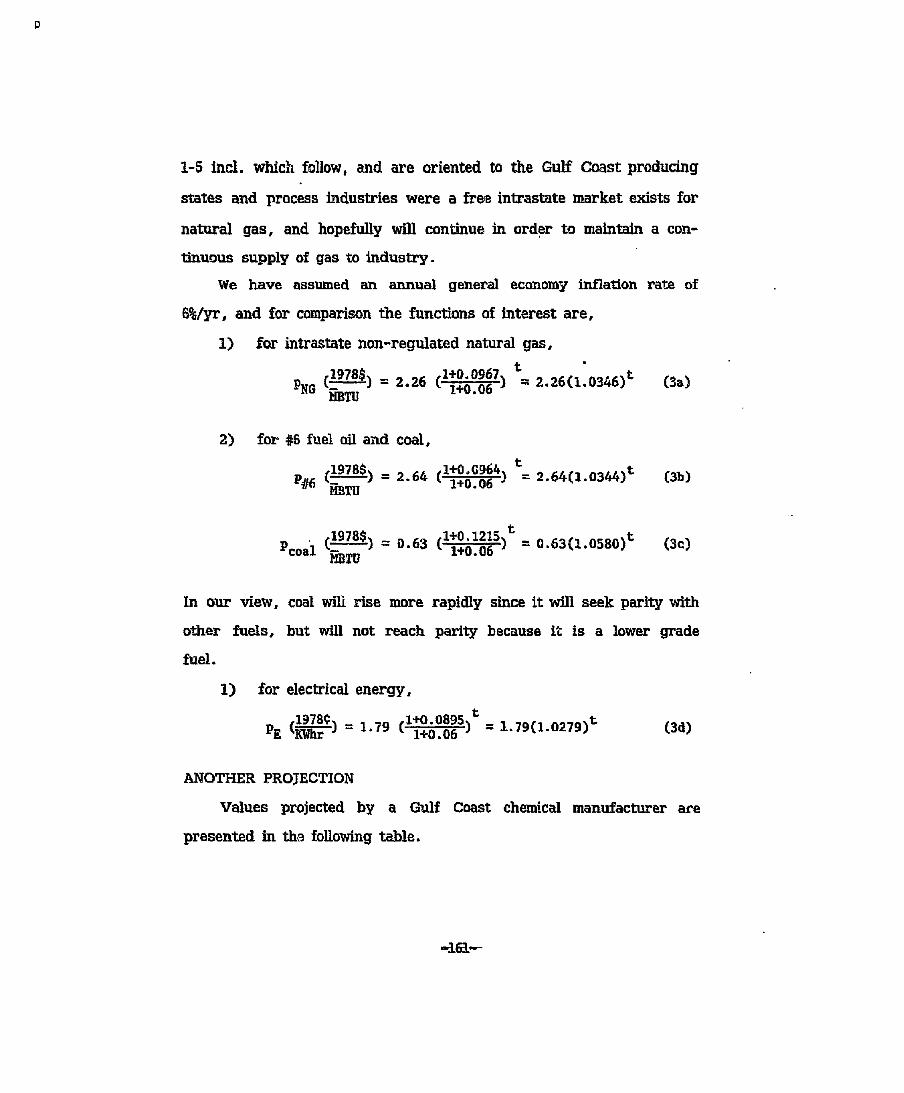

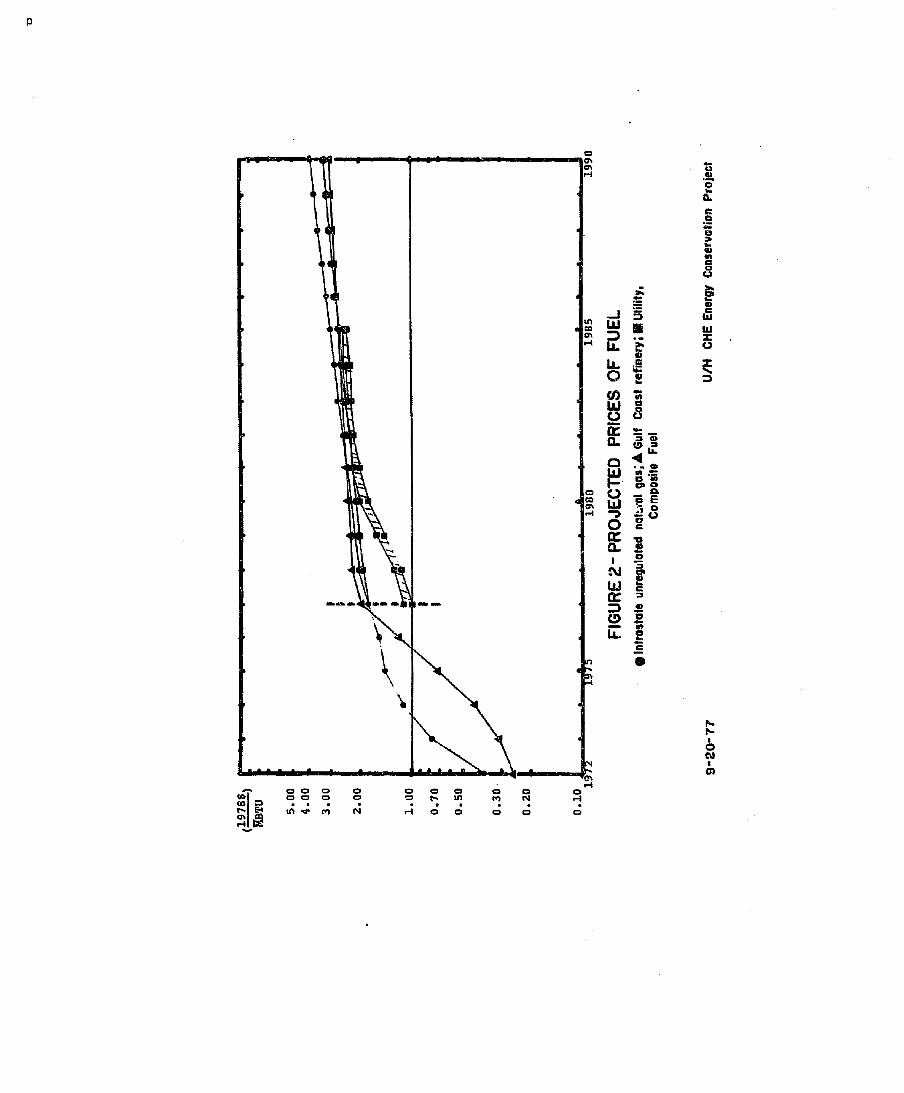

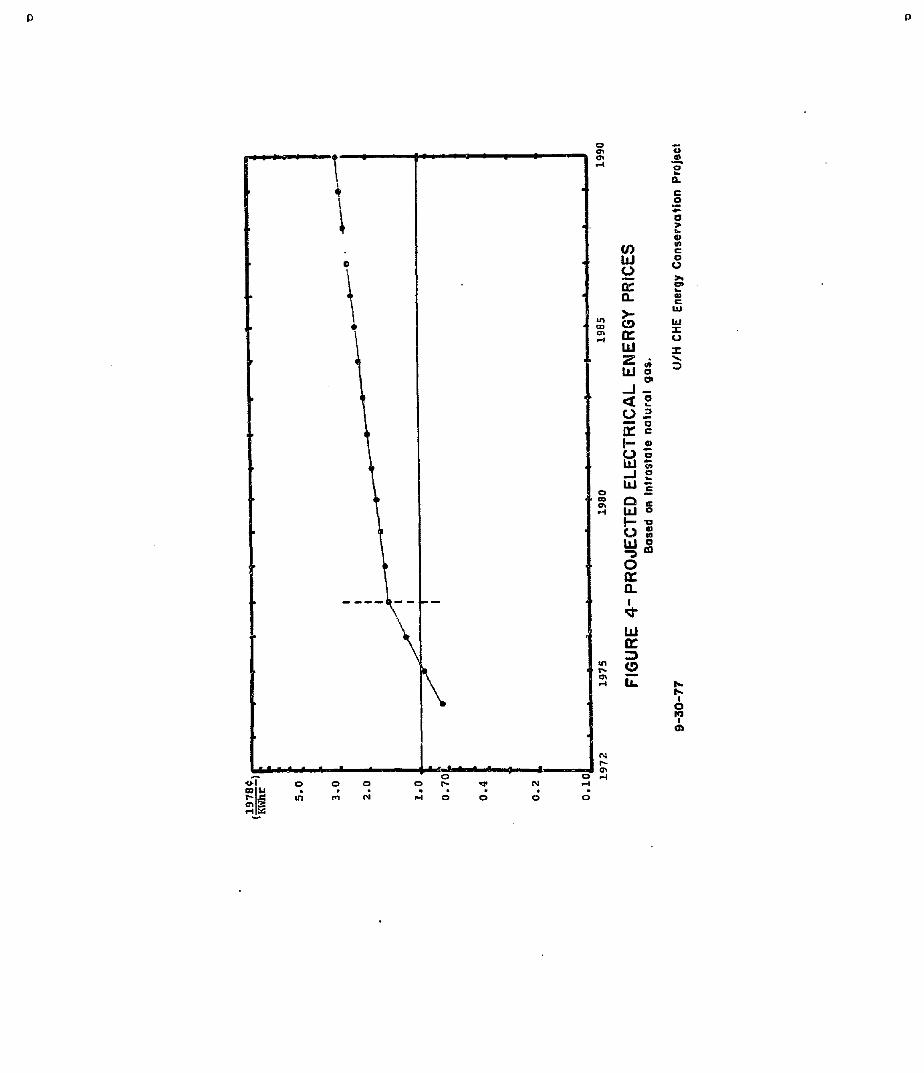

Memorandum by Dr. H. W. Prengle, Jr., Mr. W. H. Stanton, and Mr. J. E. Stevens: Projected Prices of Energy/Hydrogen Feedstocks

96

100

I01

107

I08

114

116

125

131

132

153

154

P P

ACKNOWLEDGMENT

With funding from ~he U.S. Department of Energy, Division of

Energy Storage System, and technical management by the NASA ~et

Propulsion Laboratory, the Workshop was conducted by the Energy

Institute and the Department of Chemical Engineering, both of the

University of Houston.

We wish to thank the following individuals who monitored and

assisted the director in conducting this workshop.

Dr. J. H. Swisher, DOE

Dr. Beverly Berger0 DOE

Mr. J. H. Kelley, JPL

Mr. Kenneth Tang, [[PL

The advice and suggestions from the Workshop Steering Commit-

tee and the Participants are gratefully acknowledged. The names of

the Steering Committee members and the participants listed in Appen-

dices I and If.

Workshop Director

0 P

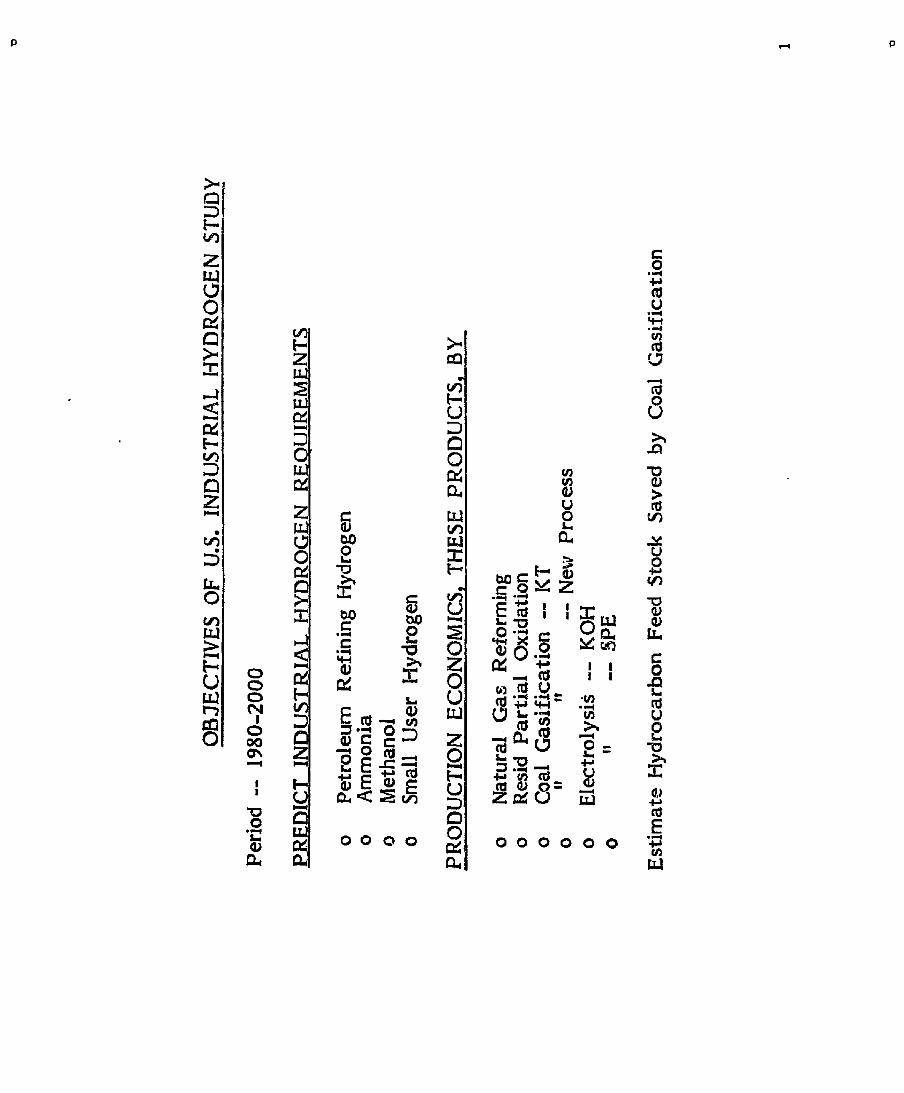

WORKSHOP OBJECTIVES

As a chemical raw material, hydrogen is important to many

manufacturing processes in oil refining, petrochemical, agricultural

and other industries. In the past, the hydrogen needed for these

processes has been supplied mainly by cracking petroleum fractions or

natural gas. However, if the hydrogen for these processes could be

supplied from sources other than petroleum or natural gas, that much

of the latter could be "conserved".

With this objective in mind, a workshop was organized, assem-

bling those who are competent and interested in this subject, in order

to:

(i) Assess and predict the present and future demand and supply of hydrogen used as a chemical feed stock,

(2) Discuss and evaluate the available technology and economic feasibility of manufacturing hydrogen from sources other than oil or natural gas,

(3) Develop implementation scenarios and to formulate policy recommendations for obtaining chemical raw material hydro- gen from sources other than oil or natural gas.

-i-

p P

WORKSHOP OVER~,qEW

With a grant (Grant No. EC-77-G-05-5570) from the Department

of Energy, Division of Energy Storage Systems, the Workshop ori

"Supply and Demand of Hydrogen as Chemical Feed Stock" was con-

ducted by Energy Institute and College of Engineering of the Univer-

sity of Houston. It was held on the University's Central Campus,

December 12-14, 1977.

Mr. Ken Tang of NASA's yet Propulsion Laboratory, operated by

the California Institute of Technology, was the technical monitor of

the program.

The Steering Committee and other interested persons were in-

vited to the preliminary meetings of ~uly 7 and September 21-22,

1977, at which important topics for the workshop were screened and

the final technical program adopted. Names of persons who attended

these two preliminary meetings ae given in Appendix I. They also

acted as advisors to the workshop Director, recommending speakers

and participants for the Workshop.

The Technical Program consisting of the six following sessions,

was presented at the Workshop:

1. Future Supply and Demand of Energy and Hydrogen.

2. Demand and Supply of Hydrogen for Oil Refining, Ammonia and Methanol Synthesis.

3. Demand and Supply of Hydrogen for Small Consumers and Future Technology.

-2 -

P

4. Production of Hydrogen from Sou~'ces Other than Oil and Natural Gas.

5. Scenarios of Supplying Hydrogen Chemical Feed Stock.

6. Recommendation on Future Supply of Hydrogen as Chemical Peed Stock.

The presentations and discussions within each session are sum-

marized later in this report. The program brochure showing t/ties of

the presentations and speakers, and session chairpersons, is repro-

duced on pages 4-8 of this report.

Approximately 150 executives, energy policy and economic plan-

ners, feed stock manager, process and project engineers, and tech-

nical journal editors were invited to attend the Workshop. Fifty-six

specialists who attended the Workshop are representatives of the

following "Hydrogen-related" organizations:

Petroleum Refining 9

Chemical & Petrochemical 9

Small Hydrogen Consumers and Future Hydrogen Consumers 6

Hydrogen Technology 14

Government & Non-Profit Research Laboratories 7

Universities 9

Technical Journal Editors 2

Appendix II is a list of names and affiliations of the Workshop

participants.

-3-

p P

WORKSHOP OVERVIEW

With a grant (Grant No. EC-77-G-05-5570) from the Depar~nent

of Energy, Division of Energy Storage Systems, the Workshop off

"Supply and Demand of Hydrogen as Chemical Feed Stock" was con-

ducted by Energy Institute and College of Engineering of the Univer-

sity of Houston. It was held on the University's Central Campus,

December 12-14, 1977.

Mr. Ken Tang of NASA's Jet Propulsion Laboratory, operated by

the California Instit~tte of Tech~aology, was the technic~l monitor of

the program.

The Steering Committee and other interested persons were in-

vited to the preliminary meetings of Iuly 7 and September 21-22,

1977, at which important topics for the workshop were screened and

the final technical program adopted. Names of persons who attended

these two preliminary meetings ae given in Appendix I. They also

acted as advisors to the World, hop Director, recommending speakers

and participents for the ~orkshop.

The Technical Program consisting of the six following sessions,

was presented at the Workshop:

1. Future Supply and Demand of Energy and Hydrogen.

2. Demand and Supply of Hydrogen for Oil Refinhlg, Ammonia and Methanol Synthesis.

3. Demand and Supply of Hydrogen for Small Consumers and Future Technology.

- 2 -

D P

4. Production of Hydrogen from Sources Other than Oil and Natural Gas.

5. Scenarios of Supplying Hydrogen Chemical Feed Stock.

6. Recommendation on Future Supply of Hydrogen as Chemical Feed Stock.

The presentations and discussions within each session are sum-

marized later in this report. The program brochure showing titles of

the presentations and speakers, and session chairpersons, is repro-

duced on pages 4-8 of this report.

Approximately 150 executives, energy policy and economic plan-

ners, feed stock manager, process and project engineers, and tech-

nical journal editors were invited to attend the Workshop. Fifty-six

specialists who attended the Workshop are representatives of the

following "Hydrogen-related" organizations:

P~troleum Refining 9

Chemical & Petrochemical 9

Small Hydrogen Consumers and Future Hydrogen Consumers 6

Hydrogen Technology 14

Government & Non-Proflt Research Laboratories 7

Universities 9

Technical Journal F~ditors 2

Appendix II is a list of names and affiliations of the Workshop

participants.

-3-

p P

f.,,,i it,,,. I I L ; , i I ~ . 1 I f- , , | I~;., I I

H2H2H2H2H2H2 2H2H2H2H2H2H H i " l l I,f't_a !~'~a !,o'La

2H21 SUPPLY AND [JEHAND i!H2 H 2 H:I HYD::GEN il2 H 2H211 ,, l:H2 2 H H2 H~,,-.-.. ,,,.. 12 H

~IH2H2H2 H2H2H 2H H2 H2 2,ii..ol. , o , , o , SPOhtSORED BY:

H 2 L}. S. DEPARTPtE~I1 OF E::ERC'f

H 2H; I ooo ,: IIhlIVEI~SITY OF HDUqT~I~ ~:OLLEGE OF ENGII'~EERING

2H H2

F21H 2 2 . ~ `') a:~,~_H2H2H2H2H H2H2H2H2H2H2

OP.,ENING SESS,ION MONDAY MORNING

9:00 am Registration

9:30 Welcoming Remarks

C. J. Huang Workshop Director University of Houston

9=45 General Announcements

s~ssIo. 1 .~emz~Y MO~Z~,G

"~me ~pZy~Da,.cz~of E.er~ a.~Sydroge."

Session Chairman: John R. Howell Director, Energy Institute University of Houston

I0:00 Keynote Speaker:

10:45

John J. Mc/~etta E. P. Schoch Professor of Chemical Engineering University of Texas

General Discussion on Objectives and Key Issues of the Workshop

ii:30 Luncheon Speaker:

Calvin Cobb Pace Company Consultant & Engineers

,s~sszoa,,Z S0.~AY~TS~OON

"Dern~ ~ ~p~y of gg~,,ogen for GZ Refini~, Ammonia a~ Me#~a~noZ ~nt~Lesi8"

Session Chairman= J. H. Kelley Jet Prolsulsion Laboratory

1:30 pm Informal Presentation

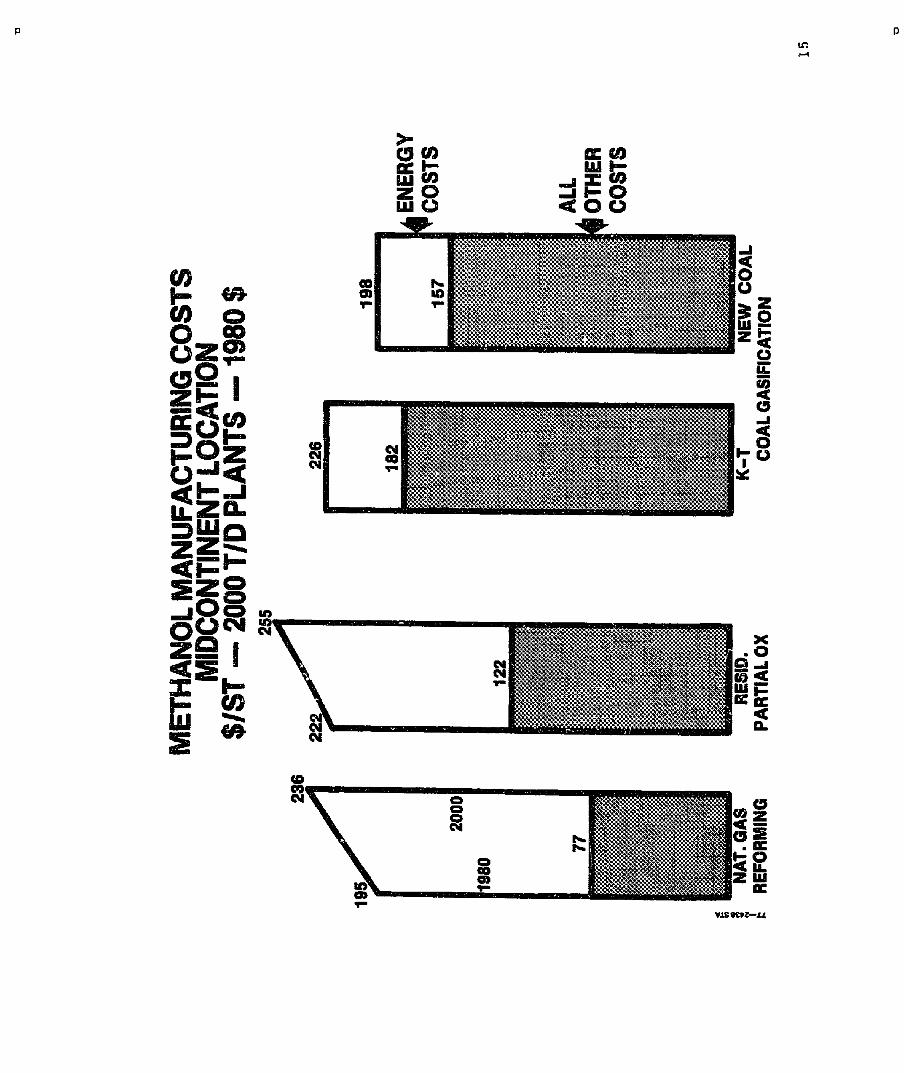

~oduo~ionEaonomlos foP.B~dmoge.j Avvnonia~Me#bo~nol D ~ the 2980-2000Pe~od

Hampton G. Corneil Exxon Research and Engineering Co.

De,.a~ and ~VpZy of ~y~oge. for ~tha.o ~ 6~jnthesis

Paul A. Cook Celanese Chemical Company

p P

~'amonia~om Coal David Netzer Fluor Engineers and constructors

2:15

3:30

3:50

Group Discussion

Discussion of the past, present and future demands of Hydrogen in refining, a~noniaand methanol syntheses. Analysis of processes, the quantities of hydrogen demand and supply, and economic values of hydrogen for major processes.

Coffee Break

Group Disuussion (continued)

6 : 3 0

DINNER

Dinner Speaker

James H. Swisher U . S . Department of Energy

SESSION 3 TUESDAY MORNING

"De~e',~d and ~ p ~ y o f Syd_.-.oge. f o r ~ la l l Conatenea~s and Fu%uz, e TechnoZ.og'g"

Session Chaiman- James Graybill Air Produ¢ts, inc.

9 : O0 am informal Presentation

HHdrog~n for Edible Oil l~oeBsinH

R. S. Watson Anderson Clayton, Inc.

Bydz,ogen ~or Isoeyanate Pz, ooeesee

David Owens Mobay Chemical Corp°

C ~ z , en~; l~ethods o:f sydz, ogen Z~od~m~n for 5'raaZZ Coneun~re L° C. Bassett HoWe-Baker, Inc°

S~cL,,og~ 8oz' Zauel Ce~ls

A. H. Levy United Technology, Inc.

SHd~ogen for Coal r.iquefao~ion

R. Parthasarathy Hydrocarbon Reseazoh, Inc°

-6-

p P

1o=15

10=3o

Coffee Break

Group Disc~.ssion Discussion on supply and demand of hydrogen in food processitlg, steel, coal liquefaction, fuel cell, and future technologies.

12:00

=uN oa Luncheon

sEsszc~ 4 TU~SDAY~ERNOON

'~a~ocZ~tion o~ayd.t, o g ~ f z , om So.sees O~wThc.~ 0~ ur~ZNa-~.raZ Gas"

Session Chain~nan= H. William Prengle, Jr. University of Houston

1=30 9m

2:20 pm

Informal Presentation | w , ,

H~drogen by ~eotrolysi8 of Water

L. J. Nuttall General Electric Company

Httd.~gen Fz, om CoaZ C-asi f i ~ f ~ . o n

Jim Miohaels Koppers Co., I~.

~oehe.~ea~ i~oduntlo~ of Hydrogen Fz, om Water

Kenneth E. Cox LOS Alamos Scientific Laboratory

Hyc~ogen a ~ Carbon l~o~oxlde F~om Coal. 1~ Win~i~ez, Pz~ocess Mike Gooclman Da~n~ Power Gas Co.

Grou~ Discussion

Process analysis, economical evaluation of the processes. Primary energy sources for hy- drogen production include nuclear power, solar energy, coal, and hio-mass° Major processes to be discussed are coal gasification, and electrolysis, thermochemical decomposition of water.

0 P

3:30 p~ Coffee Break

3:50 Group Discussion (Continued)

6:30

DINNER

Dinner

SESSION 5 WEDNESDAY MORNING

"8oena~ios of SuppZyi.qBydrogen Ch~oaZ Feed Stoek"

Session Chairman: James E. Funk University of Kentucky

9:00 am Informal Presentation

9:30

10:45

llz00

Gene~u~ Basis for Est~ieh~ng a Beenario

Wally Stanton

Monsanto Chemical

Group Discussion

Establishment of alternative scenarios and their respective assumptions and limitations. Technical and economic feasibility of the proposed scenarios.

Coffee Break

Group Discussion (Continued)

12:15

LUNCHEON

Luncheon

SESSION 6 WEDNESDAY AFTEP/~00N

"Reeovvverala%ion on ~tu~e ~PPEH of //y~og~ as Chem~eaZ Feed Stock"

Session Chairman: James E. Funk University of Kentucky

2:00 pm General Discussion

Comparison and evaluation of alternative scenarios. Imple- mentation mechanism and time schedule. Legal and social bene- fit considerations. Recommendations.

-8 -

o P

SUMMARY AND RECOMMENDATION

The discussions during the three-day workshop culminated in the

adoption of the following summary statements during the last session:

.

.

T h e r e a r e no compeJling economic r e a s o n s fo r chemica l i n d u s t r y u s e r s o f h y d r o g e n t o u s e o t h e r t h a n n a t u r a l g a s and oil as s o u r c e s o f hydroflfen a t t h e p r e s e n t t ime.

Financial incentives would have to be provided by the Government for industry to consider installing plants which produce hydrogen from coal or water electrolysis in the next several years.

. Natural gas curtailments are worrisome, but the impact to dat___ee has been of critical importance only in certain regiona-I areas. The prospect of future curtailment is of great concern to the industry.

. At t h e p r e s e n t , t h e r e is more i n t e r e s t in ob t a in ing h y d r o - gen b y coal g a s i f i c a t i o n when n e w s o u r c e s o f h y d r o g e n m u s t be f o u n d t h a n b y e l e c t r o l y s i s o f w a t e r , e x c e p t f o r small u s e r a p p l i c a t i o n s .

. It is likely that the development of high-pressure (~450 psi) coal gasification processes for hydrogen will be technically successful. Development requires continued Governmental support.

. The chemical industry feels that the Government should continue to fund research and development of new tech- nology for electrolytic and thermochemical hydrogen produc- tion from water to meet long-term needs, short of prototype demonstration plants.

. Production and distribution of syngas (CO+H2) by coal gasification is an option worth being considered for indus- trial users of hydrogen and gaseous fuel.

. New pipelines may be needed to distribute coal gasification products (H2 or syngas). Technology is available to dis- tribute these products at moderate pressures. It is recom- mended that the distribution at high pressures (greater than 2000 psi) should be studied to determine the extent of problems and their respective solutions. (It is expected

-9-

0 0

that American Petroleum Institute will publish design proce- dures for hydrogen pipelines in the Spring of 1978.)

The discusson during Sessions 5 and 6 was directed to determine

the industry's views, as represented by the workshop participants,

on what research and development should be supported by the Gov-

ernment and where and what kind of financial incentives would be

required for commercial demonstration.

The responses may be surnnmrized in Table I. Neither R&D nor

financial incentives are required for reforming refinery gases or

methane since these are well-known technologies. Heavy petroleum

(residuum) partial oxidation is also well-known, although it is prac-

ticed more extensively outside than ~thin the U.S.

Both R&D and financial incentives for commercialization are

required for processes to produce hydrogen from coal or bio-mass.

The next step in coal gasification is the development of high-pressure

(300-500 psi) gasifiers. A few companies are involved in such a

development and Exxon projects that high-pressure gasifiers will be

available by 1982. The most strongly and emphatically preferred

financial incentive for commercialization of new energy conversion

processes was decontrol of prices by the Government. This was a

general position, not limited to hydrogen production processes. The

next best financial incentive involved either investment credits or

accelerated write-off. The other techniques were generally held not

to be very attractive.

-10-

Research and development on water electrolysis and thermocheml-

cal processes should continue to be funded by the Government, but

the time has not yet come to consider the commercialization of ~ermo-

chemical processes.

A strong feeling was expressed that the results of this workshop

s h o u l d b e made avaiLable to t h e p r o p e r pa r t i e s so t h a t t h e chemical

i n d u s t r y will h a v e a s t r o n g i n p u t to f u t u r e dec i s ions on t h e s e mat-

t e r s .

-_I.1.=

P p

T a b l e 1

Chemical Industry view of R&D and Financial Incentives Required to Bring Various Hydrogen

Production Processes into the Marketplace

Refinery Gases

Methane Reforming

Heavy Petroleum Liquids

Coal Gasification

Bio-~lass (Including Water)

Water Electrolysis

Thermochemical Processes

0

(I) Choices are in the following order:

R & D Funding Financial Incentives from the Government from the Government

Required Required

No No

No No

No No

Yes (Slmgas) Yes (1)

Yes Yes

Yes Yes(l) (3)

y C2.)

1. Decontrol (by far the most preferable and strongly recom- mended).

2. Investment Tax Credit or Accelerated Write-Off.

3. Loan Guarantees.

4. Government-Owned and Contractor-Operated.

5. Take-or-Pay Contract.

6. Cost Sharing.

(2) Not yet ready for. commercial demonstration.

(3) For small-.user applications.

-12-

p 0

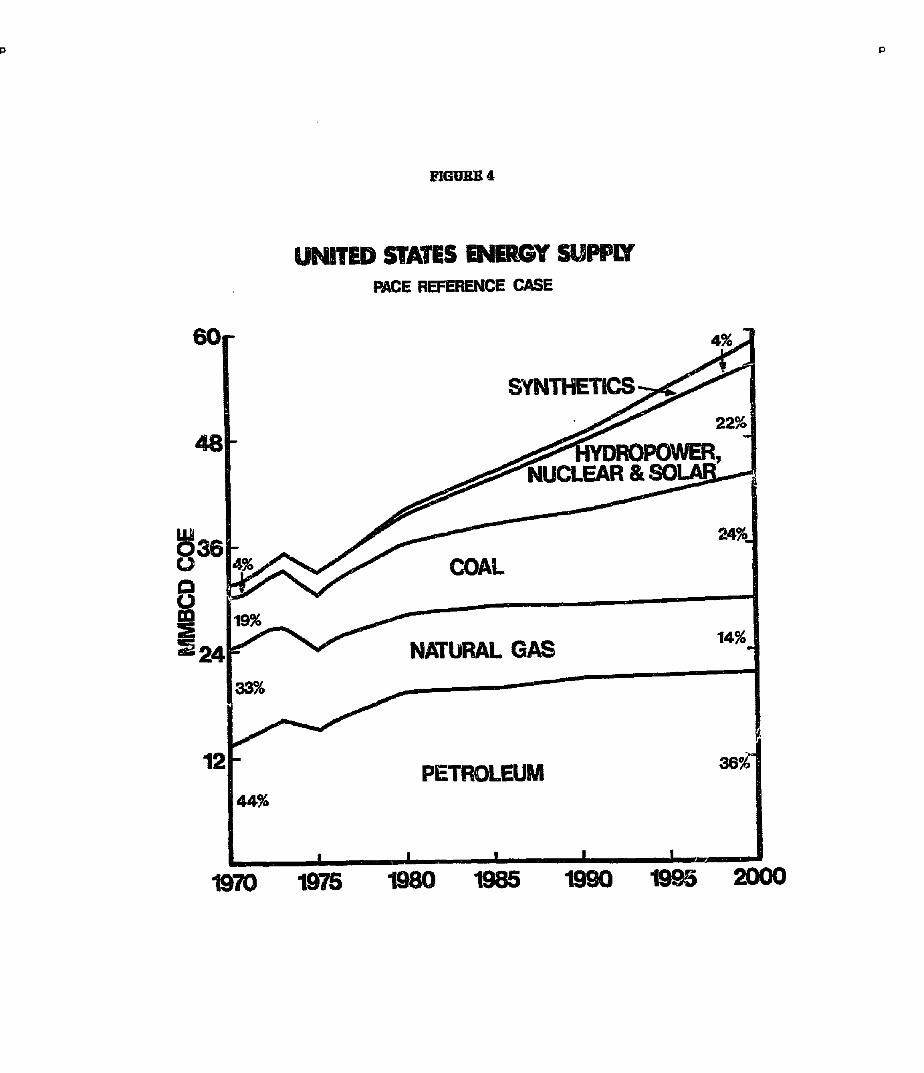

FUTURE SUPPLY AND DEMAND OF

ENERGY AND HYDROGEN

- Session i and Banquet~,

The product ion and s u p p l y of h y d r o g e n is d i r e c t l y re la ted to the

s u p p l y and demand of e n e r g y . In p rac t i ce , all t h e c u r r e n t h y d r o g e n

demand is met b y e x t r a c t i n g It from nat~ra l gas o r pet roleum f r a c -

t ions . Furthermore, a hydrogen manufacturing process requires a

significant amount of energy. Therefore, it is only natural that the

discussion of hydrogen supply and demand be undertaken with the

full knowledge of its interrelationship with the total energy picture.

In view of the above, at the outset of the workshop, Dr. John 3.

McKet~ca, E.P. Schoch Professor of Chemical Engineering at the

University of Texas, was asked to discuss the overall energy picture.

Provessor McKetta is a world-renowned authority on the subject and

was chairman of the National Energy Policy Committee. In his key-

note speech, Professor McKetta covered a wide range of the following

important subjects and brought the partlclpanm up to date on the

major vectors of the energy supply and demand.

Imported Energy

Increased Use of Coal

Nuclear Energy

Environmental Requirements

Present and Future Energy Pictures

* Sess ion Chairman: John R. Howell Un ive r s i t y of Rouston

i -_13-

p P

Problems and Means to Achieve Energy Self-Sufficiency

Professor McKettats original paper is included as Appendix Ill in this

report. A few significant points are summarized here. Professor

McKetta stressed the fact that while the domestic production of crude

oil and natural-gas-liquid (NGL) has declined in recent years, its

consumption has increased substantially. In order to show this

trend, he cited the data on the same day for two different years.

On February 1, 1973 the domestic production of crude oil and NGL

was about 11 million barrels a day, but 4 years later, on February 1,

1977, its production was decreased by 7.94 to about 9.6 million bar-

rels. ~'his is not an average. It is a comparison between the same

day, four years apart. On an average, it was about 14~ less in 1977

than in 1973. On that same day, the import of crude and products in

1973 was about 5.9 million barrels a day but in 1977 it jtu~ped by

75.6~ to the tune of 10.3 million barrels a day. On February I, 1977

cur import was equivalent to 514 of the total liquid hydrocarbon con-

sumed, but the average over the years was about 46-474. The cost

of import for 1973 was approximately 6.0 billion dollars, at an average

price of $2.80/barrel, but it was increased in 1977 to approximately

50.7 billion dollars at an average price of $13.0/barrel.

In the future, this average price of $13.01barrel will be in-

creased substantially because the product percentage of the total

import will undoubtedly be raised. Everyone can appreciate the great

-I~I-

P 0

strain on our economy to pay 50 or more billion dollars every year for

the imported crude and products. Obviously, we cannot continue

producing-less -but-consuming-more.

Another point emphasized by Professor McKetta is that energy

conservation along will not solve our energy problem. More produc-

tion of all the important vectors of energy should be encouraged by

government policy, legislations, and public support. Of course,

appropriate safeguards should be provided to protect the public

safety and welfare and to maintain the environmental qualYcy. The

audience was reminded that i t usually takes several years to develop

and construct an energy production facility, whether it be a nuclear

power plant or a new coal mine. Therefore, a lack of a national

energy policy prolongs the difficult period of unsolved energy prob-

lems.

On the evening of December 12, 1977, the workshop banquet was

held and the speaker, Dr. lames H. Swisher, discussed the status of

the current work related to hydrogen energy. Dr. Swisher is Assis-

tant Director of the Division of Energy Storage Systems, Department

of Energy, and also Chairman of the DOE Hydrogen Energy Coordinat-

ing Committee which coordinates the hydrogen-related programs within

the Department of Energy. Dr. Swisher gave an excellent and con-

cise presentation of changing attitudes and research efforts on hydro-

gen energy systems in the United States and in other countries. His

paper is included in this report as Appendix IV. In his talk, Dr.

-15-

0 P

Swisher traced the recent history of hydrogen-related programs back

to early 1970 when hydrogen was proposed as a lmiversal fuel. He

observed that there are currently two types of research and develop-

ment activities. In one, hardware is being developed for near term

applications of rather specific nature. In the other, bench-scale

research and exploratory work are undertaken to find significantly

better processes, devices, and materials for hydrogen energy sys-

tems. I t makes good sense to have these two types of research and

development work progress concurrently.

Dr. Swisher cited different approaches and emphases which have

been taken by the United States and other countries, depending on

the availability of energy resources. There is an International Ener-

gy Agency agreement on exchange of R & D results of hydrogen

production from water. In the Unit~. States, thirteen divisions of

the Department of Energy sponsor R & D related to hydro~.n energy

systems. The total fund of 24.3 million dollars in Fiscal year i977

was spent by the Energy Research and Development Ad~n'nistration

for sponsoring R & D in hydrogen production, storage, materials and

basic research, and others. The strategy is to place emphasis on

projects which may lead to commercialization in the 1980's, even if the

~otal impact in reducing oil and natural gas consumption is modest.

From now until the year 2000, the use of hydrogen, produced

from water or coal, as chemical feed stock has the greatest and most

attractive potential for reducing oil and natural gas consumption.

-16-

P P

Therefore, Dr. Swisher urged the participants to include the follow-

Ing subjects for discussion during the workshop:

(I) For what specific apptications, use rates, and geographical locations does it make more sense to produce hydrogen from water r a the r than from coal?

(2) What are the research and development needs for hydrogen storage, compression0 and distribution technology?

(3) How do these research and development needs change with outlet pressure of the hydrogen production process?

Dr. Swisher concluded that with recognition of the potential

hydrogen has as a clean-burning fuel and w i ~ financial incentives to

accelerate development and commercialization, the hydrogen program

in the Department of Energy could take a quanL~un jump in priority

and emphasis.

--17-

n P

0 P

DEMAND AND SUPPLY OF HYDROGEN FOR

OIL REFINING, AMMONIA AND METI~_ ,NOL SYNTHES!,S

- Session 2 and Luncheon*

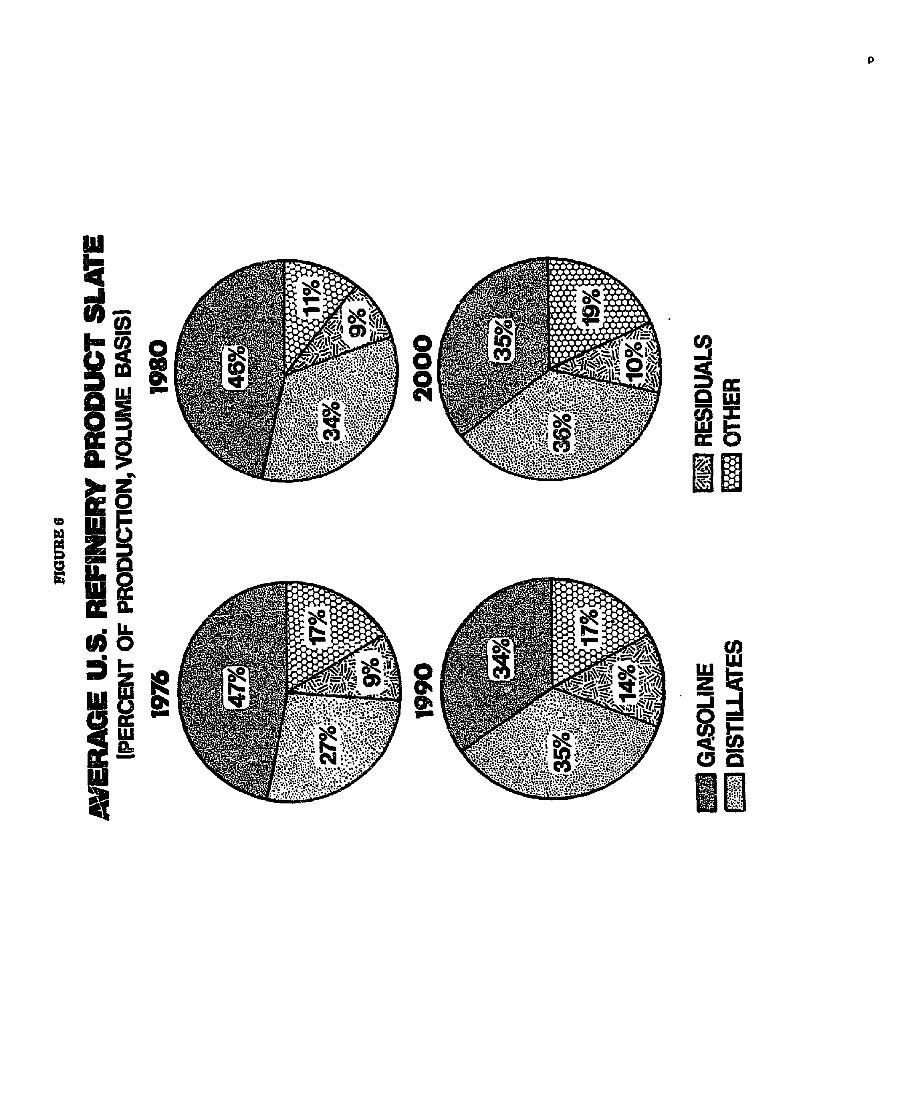

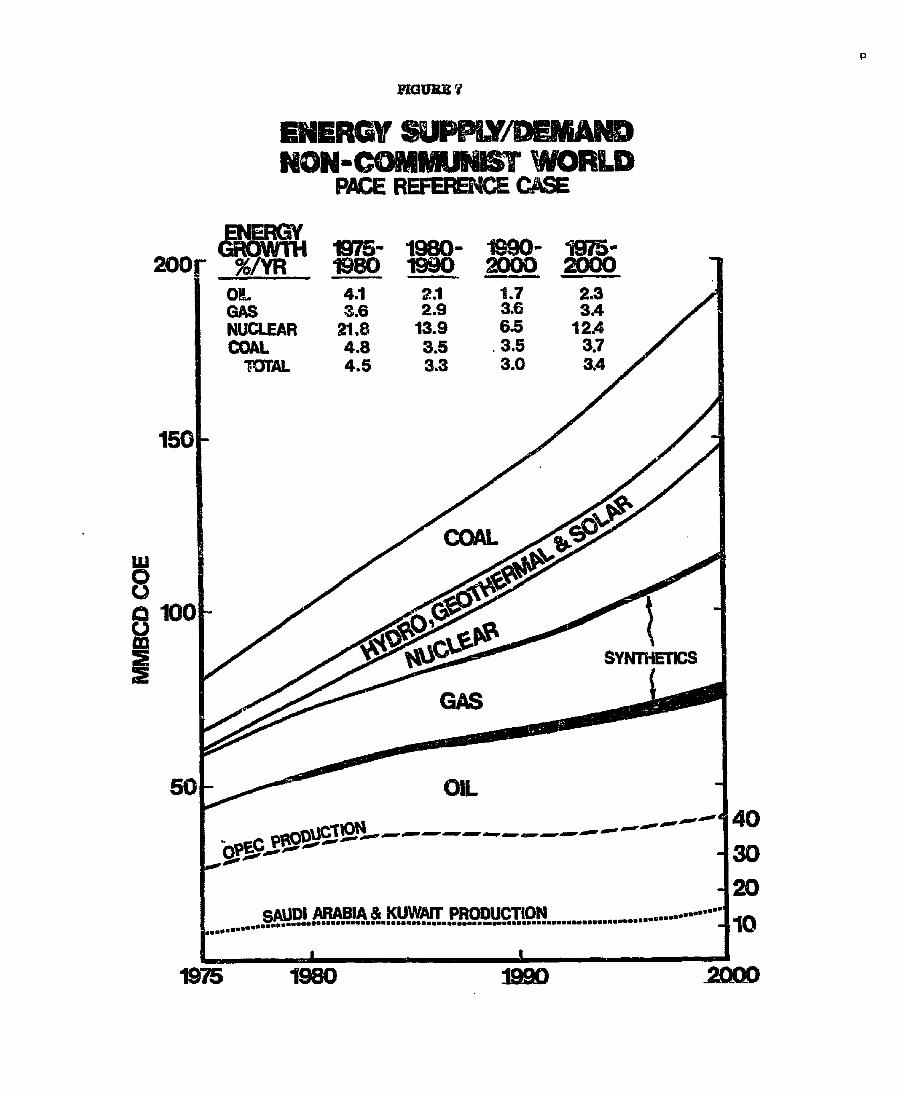

As the luncheon speaker, Dr. Calvin B. Cobb, Vice-President,

Engineering Serv/ces of The Pace Company Consultants & Engineers,

Inc. , discussed "Energy and Hydrogen in the U.S. Refining Indus-

t ry. , ' His presentation covered the following subjects and the paper

is included in this report as Al~pendix V.

Energy to 2000:

The Pace Forecasting System

Outlook for the Economy

Energy Demand/Supply

World Crude Oil Supply

The "Energy Crisis"

Hydrogen in the United States Refining Industry:

Industry Supply/Demand

Effects on Individual Refineries

The Pace Forecasting System is a computer system consisting of seven

oils, and certain animal-derived oils are hydrogenated for preserva-

tion and to provide desirable attributes of stability, consistency, and

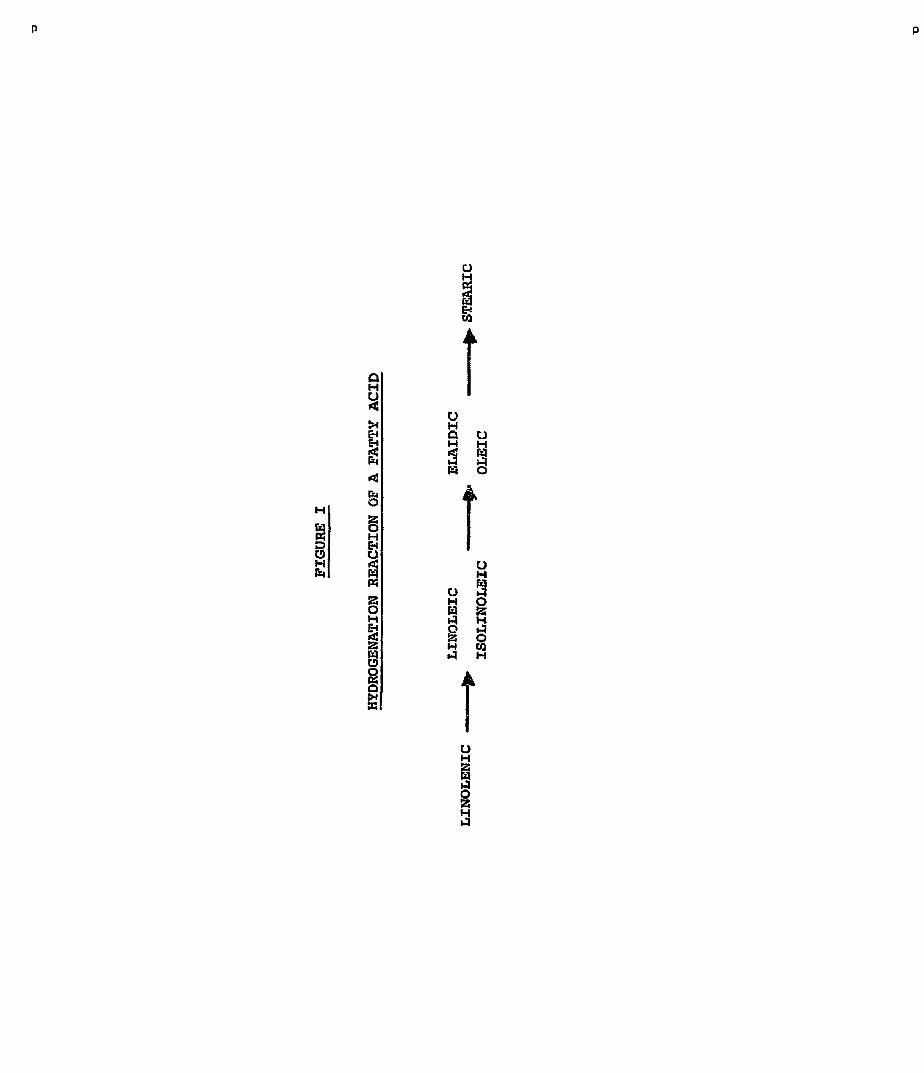

uniformity. Hydrogenation is the largest single chemical reaction in

the edible oil industry. The reaction is extremely complex but for

our purpose here, may be considered as a very simple addition of

hydrogen to the ethylenic linkage. It is accomplished in the presence

of a catalyst, normally nickel, at minimal pressure and a temperature

of 325 to 400°F.

For the approximately 9 billion lb /yr of oils that are hydroge-

nated, the estimated hydrogen requirement is 5.85 billion CF/yr.

Practically all this demand is met by on-site natural gas reformers

(propane backup). A typical hydrogen generating plant produces

10,000 to 40,000 CF/hr and as a replacement value of $1.2 million.

Most were installed between 1940 and 1970.

* Session Chairman: Jame.~ Orayb£11 A i r P r o d u c ~ s . I n c .

-~.q-

P P

Hydrogen production accounts for about 15% of the typical

plant 's energy requirements. No carbon oxides or sulfur can be left

in the processing hydrogen, as this would poison the hydrogenation

catalysts. I t requires a pur i ty of 99.9% plus. The newer molecular

sieve systems are favored over the MEA process for removal of the

contaminant gases.

Interestingly, even in view of the high purity requirement and a

relatively low sensitivity to hydrogen cost of the hydrogenation pro-

cess, to Mr. Watson~s knowledge, no U.S. manufacturers employ

electrolyzers. He noted thr" _~lectrolysis is used in Brazil and other

South American countries and, in the long run, may be a replacement

to the hydrocarbon reforming processes.

Mr. Watson stated that hydrogen demand will be rather stable in

the oil hydrogenation industry, despite normal production growth.

The difference is accounted for by a reduced specific usage (CF/Ib)

because of the increasing stress on less-saturated products, the

polyunsaturates.

In response to a question on the impact of natural gas cur',nil-

ments on the industry during the last winter, Mr. Watson said that

the Midwest locations had been significantly affected, with Illinois

sites experiencing as much as a 40~ cutback. Although the industry

has not been seriously affected, the scarcity of natural gas in the

years ahead is of considerable concern.

-30-

D P

• °

As an example of hydrogen ' s role in ,.he general area of the

chemicals and plastics industr ies , 1~. David Owens of Mobay Chemical

C~rporation addressed the workshop on the subject of isocyanate

manufacture. The viewgraphs used in the presentation are repro-

duced as Appendix X in this report.

Isocyanates, in combination with polyethers, are the primary raw

materials for the manufacture of polyurethane products. The isocya-

nate field is dominated by two compounds:

A. Toluene Diisocyanate (TDI) is the first isocyanate to be commercialized and is still the leader in volume. Its pri- mary application is in the manufacture of flexible foams for end uses such as furniture, bedding and carpet underlay.

B. Diphenylmethane Diisocyanate (MDI) is the other major isocyanate compound and is used to produce rigid foams. With the current emphasis on energy conservation, the demand, for rigid foam insulation in buildings, process plants, and appllances is contributing to a high gro~th rate in demand.

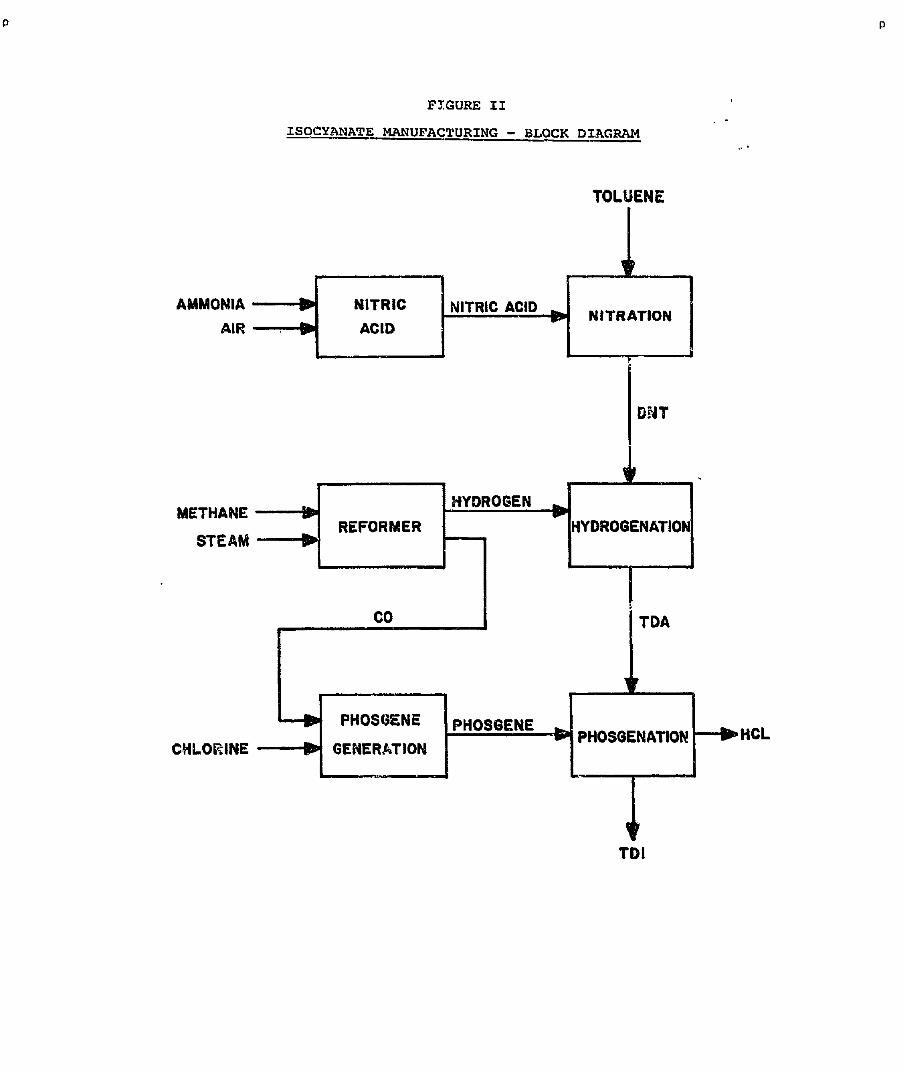

The basic chemical reactions for production of TDI (Figure I of

Appendix X) illustrate the role of H2 and CO in this field. Toluene

is nl~crated to DNT, which in turn is reacted with H~ to form toluene

diamine (TDA). TDA is then reacted with phosgene, produced from

CO and chlor/ne, to form TDI. The basic chemistry for MDI, which

uses benzene as a starting material, is similar. In both cases, the

molar ratio of Hs to CO required to produce the end product is 3 to

l--the same H21CO ratio obtained by steam reforming of natural gas.

Figure II (in Appendix X) is a block diagram which illustrates a

typical integrated plant complex for the production of TDI. It can be

k ̧ - 3 ! -

0 P

seen from inspection of the diagram that a reliable, continuous supply

of CO and Hs, therefore natural gas is critical to the success of the

operation.

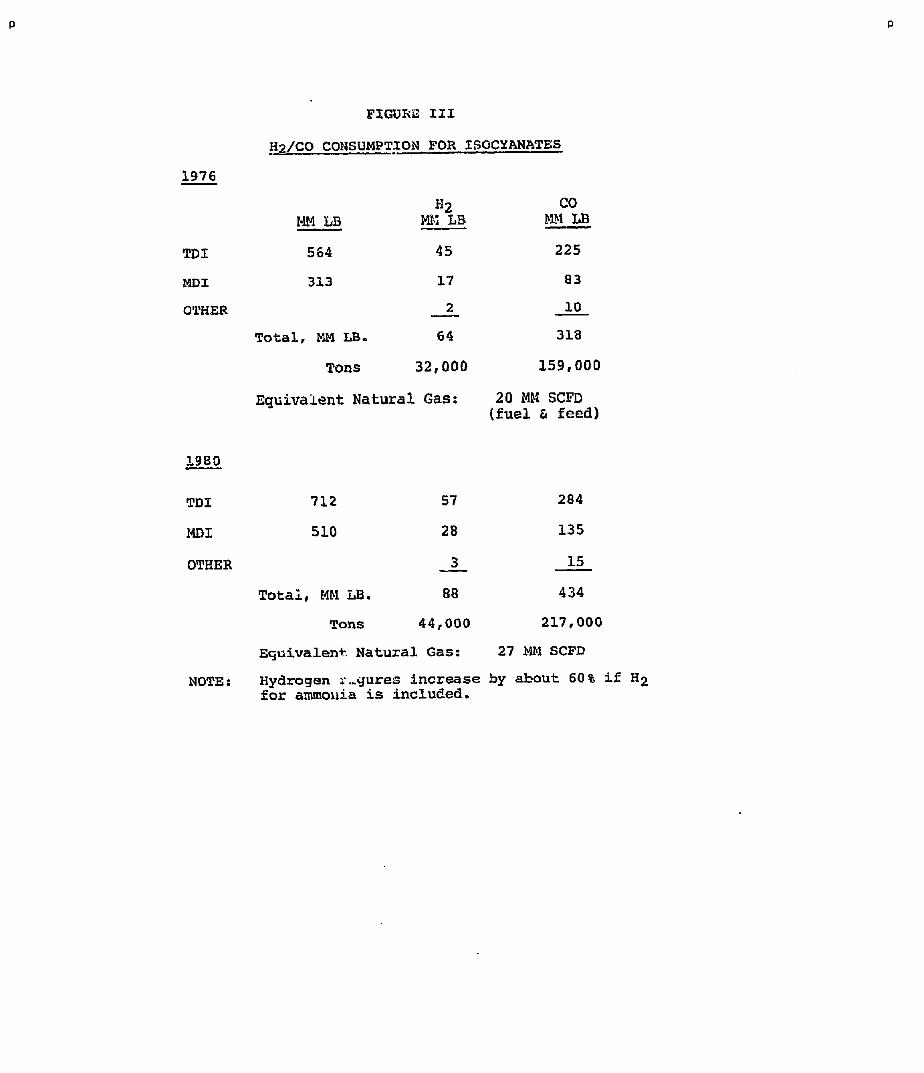

An estimate of the H2 and CO required to produce the total

isocyanate quantity manufactured in the U.S. in 1976 is shown in

Figure III. A rough projection for 1980 is indicated below the 1976

figures. If all CO and H2 is produced from natural gas, the 1980

requirements equate to about 27 MM SCFD of natural gas. This does

not include the hydrogen needed to produce ammonia feedstock, which

would add another 60% to the overall hydrogen requirement. Because

of their central position in the production scheme, reliability of CO

and H2 supply have largely overshadowed cost implication until recent

years. As a major products approac.h maturity with the attendant

pressure on profit margins, the cost of H 2 and CO is becoming an

equally important factor. Rapidly increasing natural gas prices,

coupled with declining availability, make the situation more serious.

Combined Ms and CO costs now fall in the range of 7-11°6 of TDI

manufacturing cost and 5-8% of MDI manufacturing cost, making CO

and H2 one of the major cost contributors.

Some of the possibilities for reducing or eliminating the depen-

dence on natural gas for H2 and CO supply are listed below:

A. Alternate reformer feed stock/fuels

B. Producton of synthesis gas by coal gasification

C. CO generation from coke

D. H~ recovery from electrolysis of by-product HCI

New processes for both TDI and ~.~I, which eliminate the hy-

drogenation step (but not the need for CO), have been announced

but could be several years away from possible commercialization.

Therefore, the effect of H~ requirements cannot be accurately gauged

at this time. In any case, the large existing capacity based on

hydrogenationlphosgenation technology will mandate a steadily in-

creasing requirement for H2 and CO for the foreseeable future.

Regarding the impact of gas curtailments, Owens said plants in

certain areas were severely affected last 3anuary and February. In

West Virginia, for example, steam generators were converted from gas

to oil. Some companies began drilling, with limited success, for their

own gas. Also, coal-gasification-produced synthesis gas is now being

given serious "attention.

Mr.' L.. Carl Bassett of Howe-Baker, Inc., discussed current

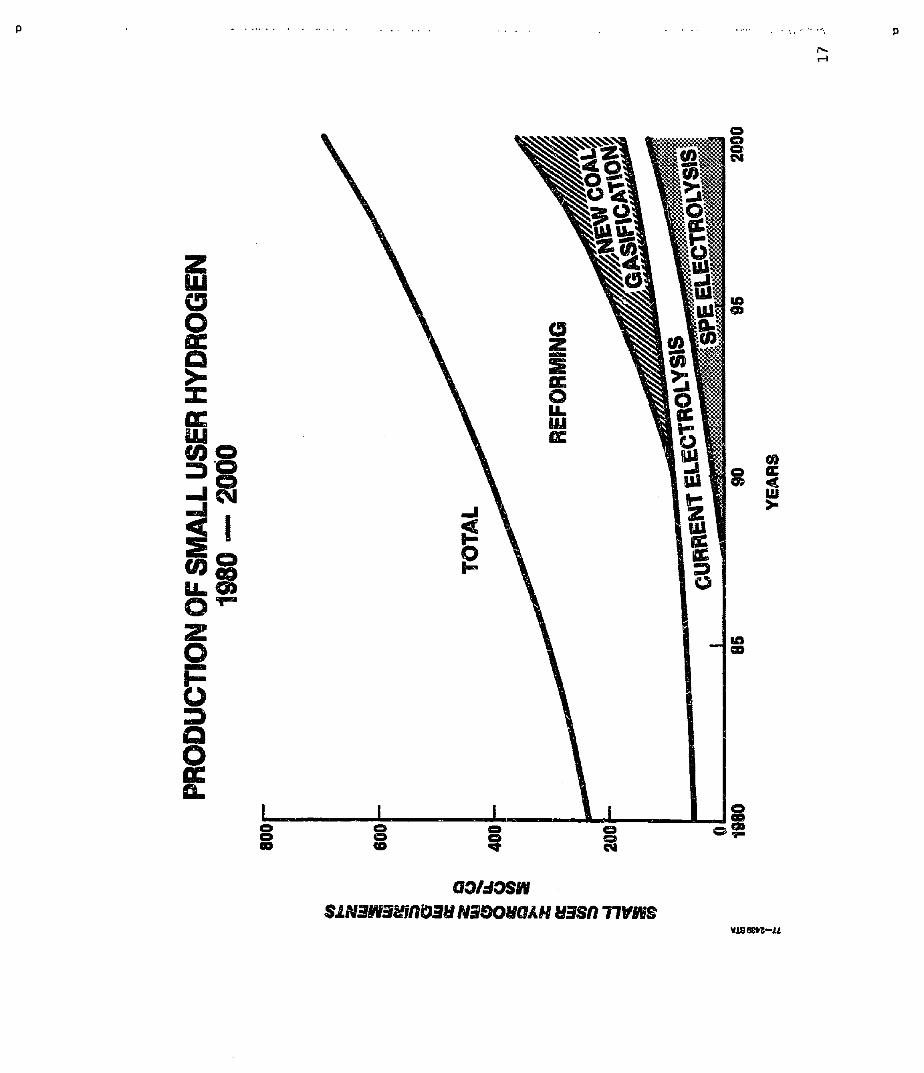

technology of producing hydrogen for small consumers of about

1,000,000 SCFD. The most common method is steam-hydrocarbon

reforming follow~d by shift conversion and hydrogen purification.

Technology in reforming and hydrogen purification has advanced to

the state that hydrogen purity of 99.999+4 is possible with fixed bed

adsorption. I t can meet the requi~rements of liquid hydrogen users .

The minimum size reforming plant from a capital investment standpoint

is approximately 120,000 SCFD.

-33-

P P

Other processes available for hydrogen production are electro-

lytic and partial oxidation. Liquid hydrogen production is an exten-

sion of the above processes.

Hydrogen is also available to small consumers as an off gases

from several chemical and refinery sources either to be taken as pure

hydrogen or recovered from high hydrogen content streams.

Mr. Bassett presented the following comparison of the energy

requirements of the various methods of hydrogen production:

Method for Energy Req't H2 Production BTU/SCF H 2 Basis

Steam-Hydrocarbon Reforming

Electrolytic

500 Feed & Fuel (NG, LPG, Naphtha)

1,593 140 KWHII000 SCF-30% efficiency

636 Feed - Fuel (#6 oil)

788 Reforming plus power req't.

274 Compression co 200 psig

274 Compression to 200 psig

Partial Oxidation

Liquid Hydrogen

Chlorine Cell Off Gas

Ethylene Plant Off Gas

The technological advance in the future may affect in a dramat~.c

way the picture of hydrogen supply demand. For example, using a

and producing 100,000 BPSD of all distillate synthet ic crude will re-

quire up to 635 MM scfd of hydrogen feedstock. An additional 100

MM scfd is estimated to be required in re f inery type processing to

produce marketable No. 2 fuel oil and high octane materials.

A two-year observation program has been scheduled for the

H-CoalO Pilot Plant, beginning the last quarter of 1978. Extensive

economic studies for commercial plants are under way. Design of

commercial coal liquefaction facilities can be commenced now and the

analyses of the prototype plant operation and the economic studies are

expected to confirm the optimization of these designs. The first

commercial plant could be expected to go on stream around 1985.

-38-

p o

• : : . . . . . . . . . . :.,.....

Given the current activity in development of coal liquefaction pro-

cesses, a number of processes will reach commercialization potential in

the eighties. Assuming current predictions of world energy pres-

sures and in the right socio-political atmosphere, a number of coal

liquefaction plants will probably be operating on a commercial scale by

the turn of the century.

A number of energy forecasts have been made (see: R . E .

Balshizer, "Energy Options to the Year 2000", Chem. Engineering,

~anuary 3, 1977), projecting energy consumption by the year 2000,

ranging from 100 Quads (1 Quad=10 is BTU) annually for zero energy

growth to 170 Quads annually for a growth rate of about 3%. (Over

the last 30 years energy consumption in the U.S. has been increasing

at 2.9% annually and at 4.1% for the years 1960-1973).

Assuming an ordered growth and allowing for conservation and

environmental needs, the demand in 2000 will probably he around 150

quads. Assuming domestic oil and gas reserves will provide 50

Quads, 100 Quads will have to be provided by imported energy and

coal and nuclear fuels. Allowing for 11 Quads of imported oil (5 I~4

B/D) and all the power generation recp~irements of 75 Q to be pro-

vided by nuclear sources and direct coal firing, leaves a deficit of

14 Q. If 7 Quads are provided by direct coal firing in the industrial

section, synthetic fuels will have to provide 7 Quads. Assuming

equal markets for gases and liquids derived from coal, coal liquids

will provide 3.5 Quads representing 1.6 MM barrels of oil daily. This

w{ll translate to a hydrogen demand of 11.8 x 10 9 SCFD, to provide

gasoline and home heating oil by coal liquefaction.

These projections were predicated on no special measures being

taken for the development of synthet}c fuels. Alternate scenarios are

possible. A government poUcy decision to actively encourage syn-

thetic fuels and eliminate oil imports could ra~ult in a crash program

of building synthet ic oil plants. I t is anticipated that up to 1 MM

B/D coal liquefaction capacity can be added annually start ing in 1985,

the base assumed above for the f i rs t plant to be in operation. This

would mean an incremental hydrogen demand of 7.35 x 109 SCFD

annually, commencing in 1985.

- 4 0 -

P 0

PRODUCTION OF HYDROGEN FROM SOURCES

OTHER THAN OIL AND NATURAL GA~

- Session 4"-

Among the several industrially deployed "first generation" sys-

tems that gasify coal to produce hydrogen and H2/CO synthesis gas

are the Koppers-Totzek and Winkler processes. These two processes

were reviewed and discussed by Mr. yim Michaels of Koppers Com-

pany, Inc. and Mr. M. C. Goodman of Davy Powergas, Inc., respec-

tively.

As pointed out by Mr. Michaels, the production of hydrogen

from indigenous coal supplies via coal gasification technology offers

many advantages, particularly regarding the reliability of supply and

the predictability of cost. He described the Koppers-Totzek process

as a mature technology and has been used commercially since 1952.

Thirteen plants containing a total of 39 gasifiers have been con-

structed primarily in areas of the world that are deficient in oil and

gas supplies but have ample coal supplies.

The outline and process flow diagram of the Koppers-Tot.zek

process were presented by Mr. M/chaels and included in Appendix

XIII of this report. Only the important production economic data are

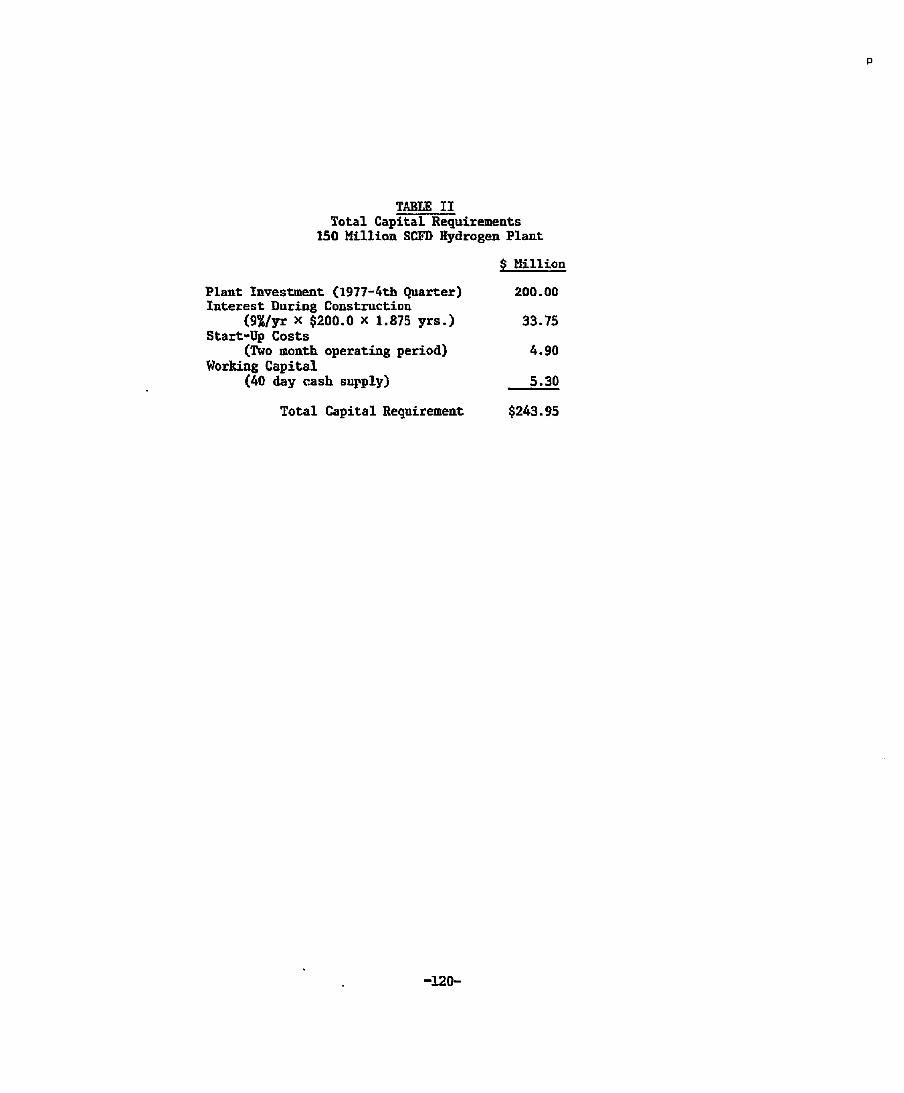

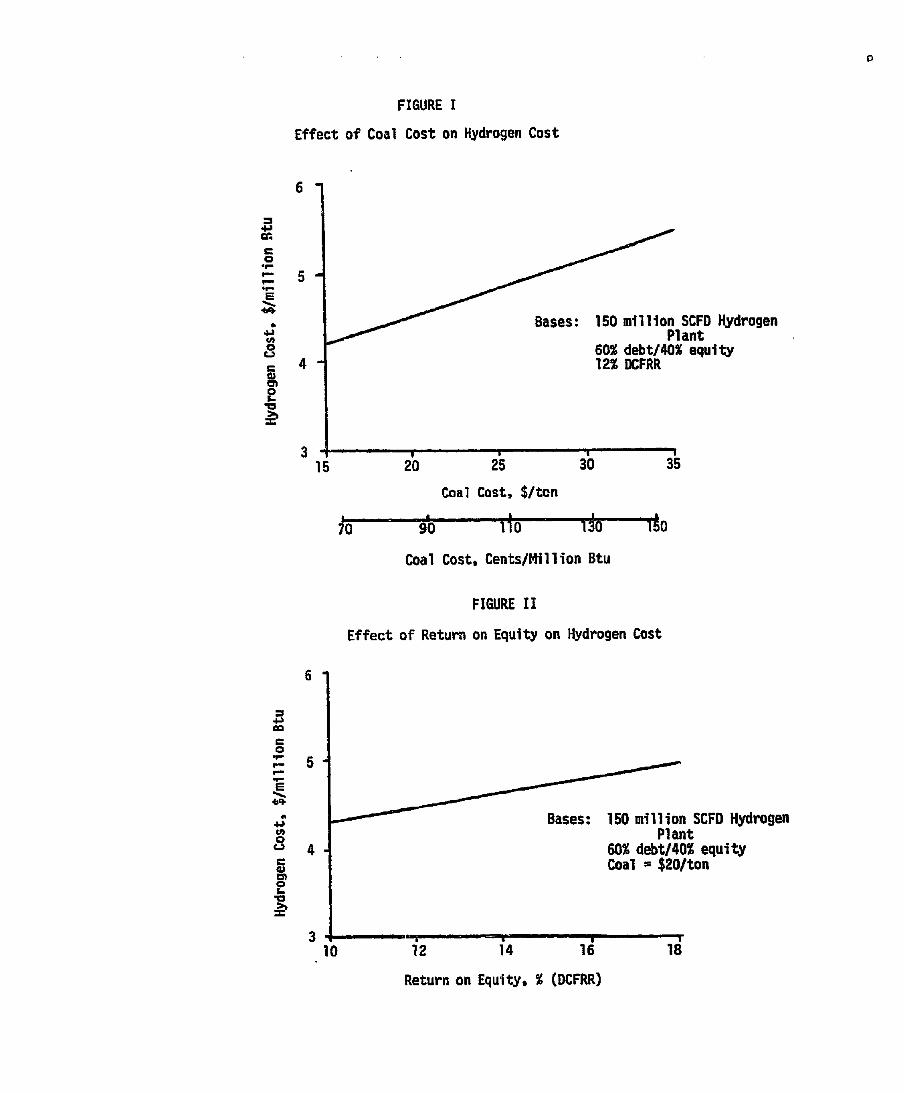

summarized here. Mr. Michaels' study showed flint the estimated

capital cost for a Koppers-Totzek based hydrogen plant producing 150

million standard cubic feet per day (SFD) of 96~ puri ty hydrogen at a

* Session Chair.-mn: H. Nilllam Prengle, J r . U n i v e r s i t y o£ Houston

0 P

pressure of 500 psig is $200 million (fourth q u a r t e r - 1977). The

plant is comprised of four four-headed K-T gasifiers which produce a

synthesis gas rich in carbon monoxide and hydrogen which is then

further processed to yield a gas containing 96% (volume) hydrogen.

The feedstock of the plant (mid-continent location) is an Illinois

bituminous coal containing 3.44 sulfur at the feed rate of 3000 tons

per day. The plant is not completely self-sus~ining in the present

design since electrical power must be brought to the battery limits.

The plant consumes approximately 2400 gallons/minute of raw water,

but no operating costs are charged for water since power facilities

are included for supplying and treating raw water.

When coal is available at $201ton ($0.901milUon Btu), the annual

operating costs are estimated to be $2.751million Btu, or $0.901thou-

sand cubic feet (MSCF) of hydrogen produced. A discounted cash

flow rate of return method was used to compute constant (level)

product costs over the twenty-year life of the project such that

sufficient revenues were generated to cover operating costs, debt

service (interest plus principal), income taxes, and the return of

equity capital to satisfy a given discounted cash flow rate of return.

Assum'mg that financing consisting of 604 debt and 404 equity

can be arranged, the cost of hydrogen is $4.50/million Btu or $1.45/

MSCF. These costs assume a 124 discounted cash flow rate of return

(DCFRR) on equity. Of the $4.50 about $3.50 is allocated to synthe-

sis gas production, and the remaining $1.00 to CO shift, purification

and compression.

-42 -

O P

P D

blichaels said that although this cost is not currently competitive

with hydrogen manufactured by the stream reforming of regulated

natural gas, it may become competiti~a in the near future due to a

variety of possible political and economic circumstances.

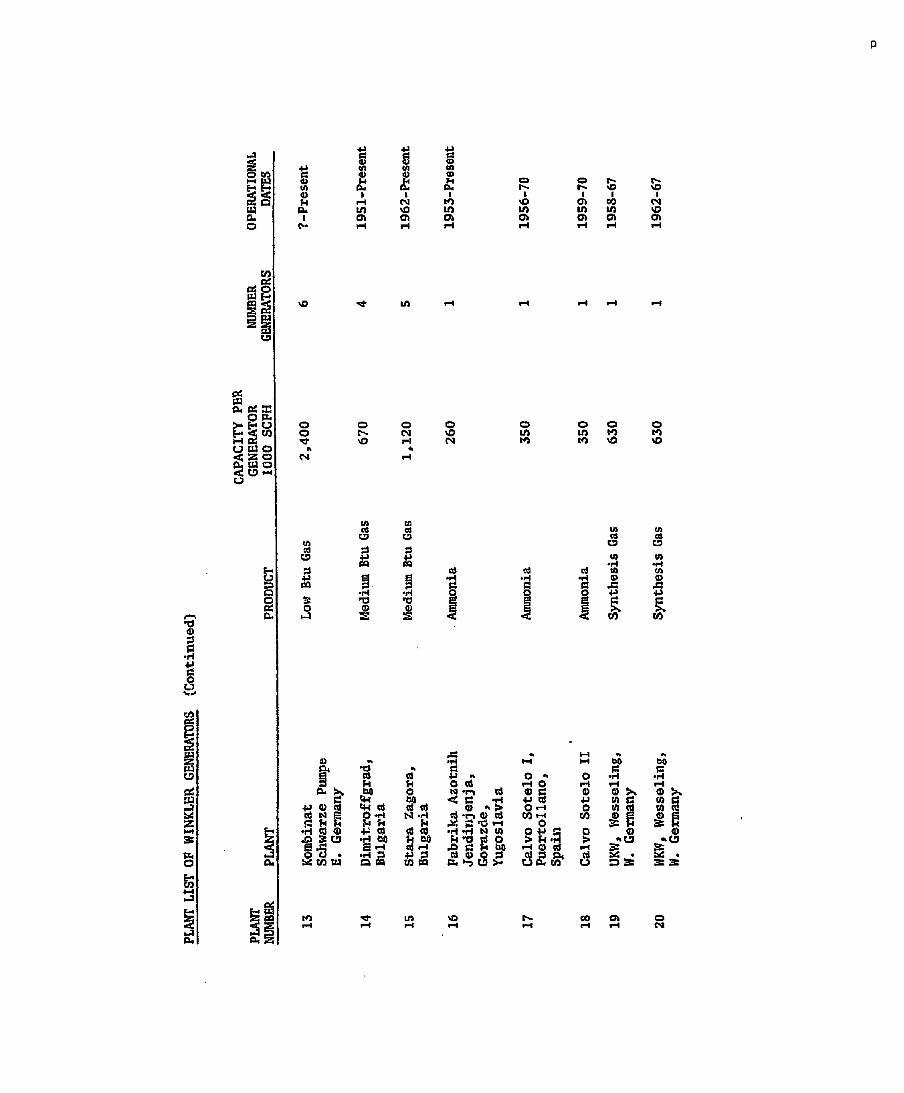

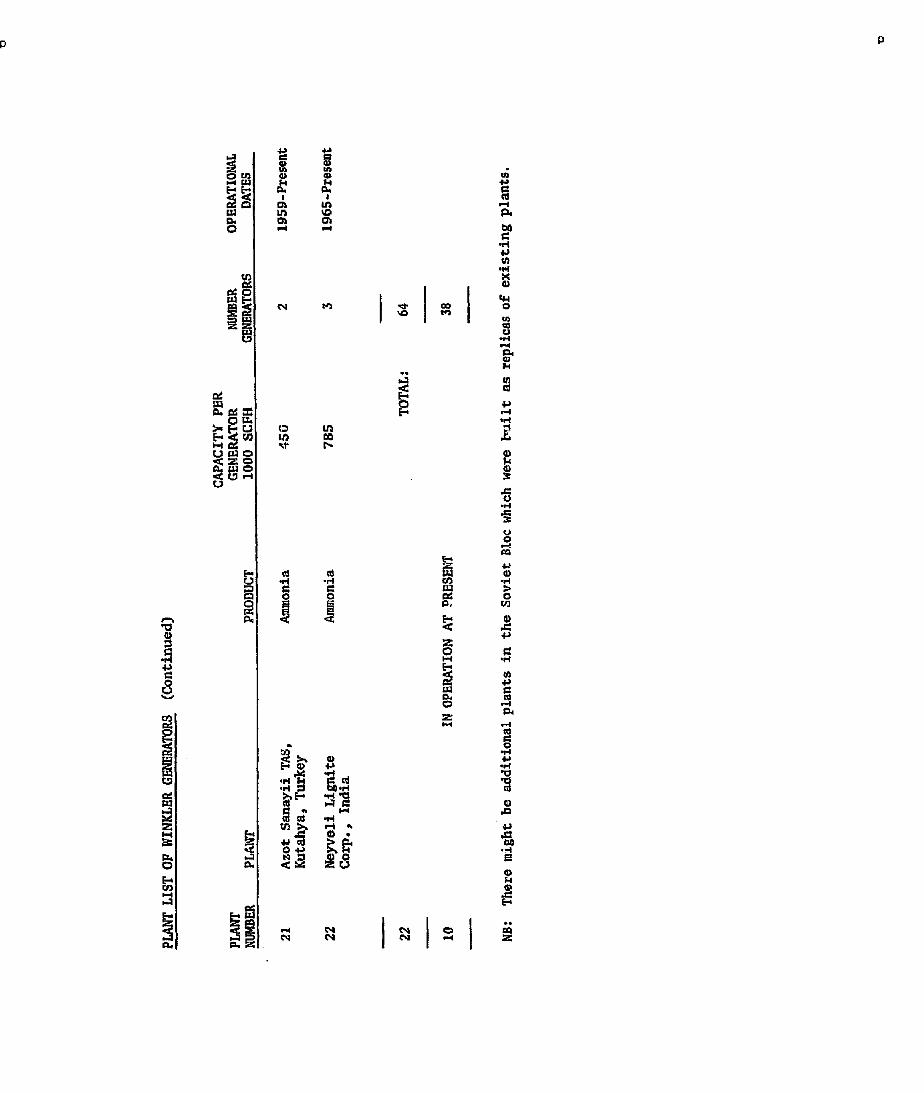

According to Mr. M. C. Goodman, the earliest commercial-scale

plant adopting the Winkler process was built in 1928 in Germany. It

operated successfully until 1970 at the rate of 3.730 million SCFH for

each of 5 generators. Since then, 21 more plants were built and

have been in operation in Germany, Japan, U.S.S.R., India, Turkey

and other European countries. Lignite, sub-bituminous, or other

coking coals may also be used as a feed. Basically, it is a fluidized

bed gasification process operating at low pressure with oxygen or air

to produce a medium Btu or low Btu ir~dustrial gas. The typical raw

gas from the Winkler process contains 35.2~46.0 volume percent of Hs

and 30.8- 48.1 percent CO. A process including CO shift, CO2

removal and methanation will yield a gas mixture containing 94.8~ of

hydrogen. It is possible to get an even higher purity. Mr. Goodman

stated that the cost of medium Btu gas via the Winkler process is

within the range of $2.76 to $3.351million Btu. In terms of CO + H2

this represents $1.00 to $1.22/MSCF (CO + H2). Mr. Goodman

stressed that for chemical feed stock purposes, CO + Hs synthesis

gas should be directly produced from coal rather than going through

the route of CH4 (SNG). He advocated the embracing of the devel-

oped processes to create an industry and expertise which world act

-43-

p 0

0 0

as a springboard for research and development based upon the knowl-

edge gained by the successful operation of these processes, rather

than expanding funds for new research and development in completely

novel coal gasification processes which, by their very nature, will

have a poor record of operability. The presentation of Mr. Goodman

is included in this report as Appendix XIV.

Water electrolysis is an alternate process of manufacturing hy-

drogen from non=hydrocarbon sources. Mr. L. N. Nuttall of General

Electric Company reported on its program to develop an efficient,

economic, large-scale water electrolysis system using the solid polymer

electrolyte cell technology. His process description consists of the

following subjects:

Historical Background

Development Program

Current Status

Cost Reduction Program

Improved Efficiency

Cell Scale-Up

Developmental Schedule

Mr. Nu~all also showed how water electrolysis would compare

with stream reforming of natural gas as a source of hydrogen for

chemical and industrial applications. Three d~erent size plants were

considered, which covers a range of possible applications. A large

plant of 100 million SCF/day capacity (387 MW) which might be appro-

priate for ammonia or methanol production, an intermediate size plant

-44-

P P

of 480 KSCF/day (1.9 MW) which might represent a food processing

or metal processing application and a small plant of 96 KSCF/day (370

KW) which might be suitable for some of the glass or lamp manufac-

turing operations.

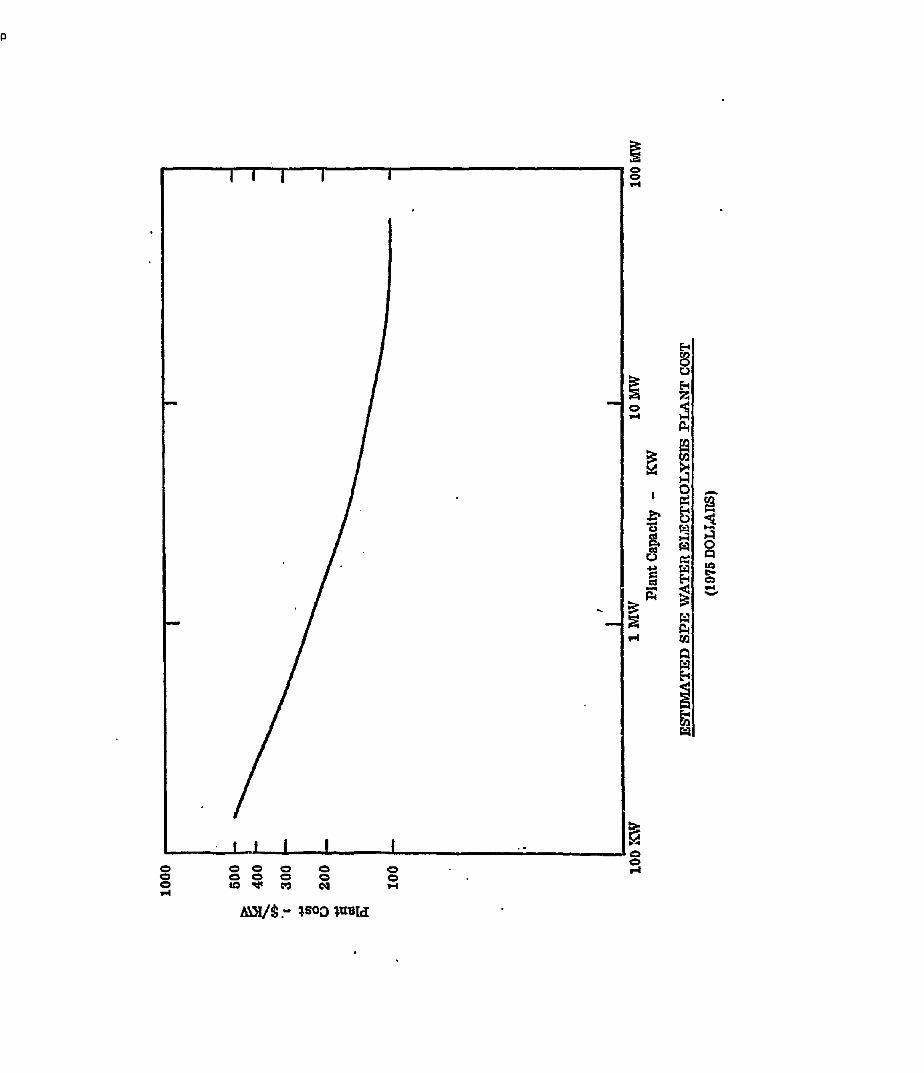

The capital cost used for the electrolysis plants was based on an

estimated curve shown in Figure 1. The figures used in Mr. NuttaIPs

presentation were reproduced as Appendix XV. The capital costs

used for the steam reformer were taken from the table on page 59 of

the Exxon Research and Engineering Co. Report No. BNL-50663

(Reference: Mr. CornsiPs presentation in Session 2). Two different

projections for the future cost of electrical power and natural gas

were considered, as ~ in Figure 2. The solid lines represent a

projection made by some components of the General Electric Company

and the dashed llne the projection reported in the above Exxon re-

port.

The resulting hydrogen cost comparison for the large plant is

shown in Figure 3. It does not appear, from these data, that elec-

trolysis will be competitive with reforming of natural gas as a source

of hydrogen, at least before the year 2000, except in instances where

lower cost electrical power is available. However, if there is a real

concern about the future availability of natural gas, a study made by

T. D. Donakowski and W. 7. D. Escher of the Institute of Gas Tech-

nology showed that considerable economies could be made by using a

dedicated nuclear power plant to provide electric power for a large

145-

p D

P P

water electrolysis plant. This could make electrolytic hydrogen

competitive with steam reforming of natural gas, even for these larger

users of hydrogen.

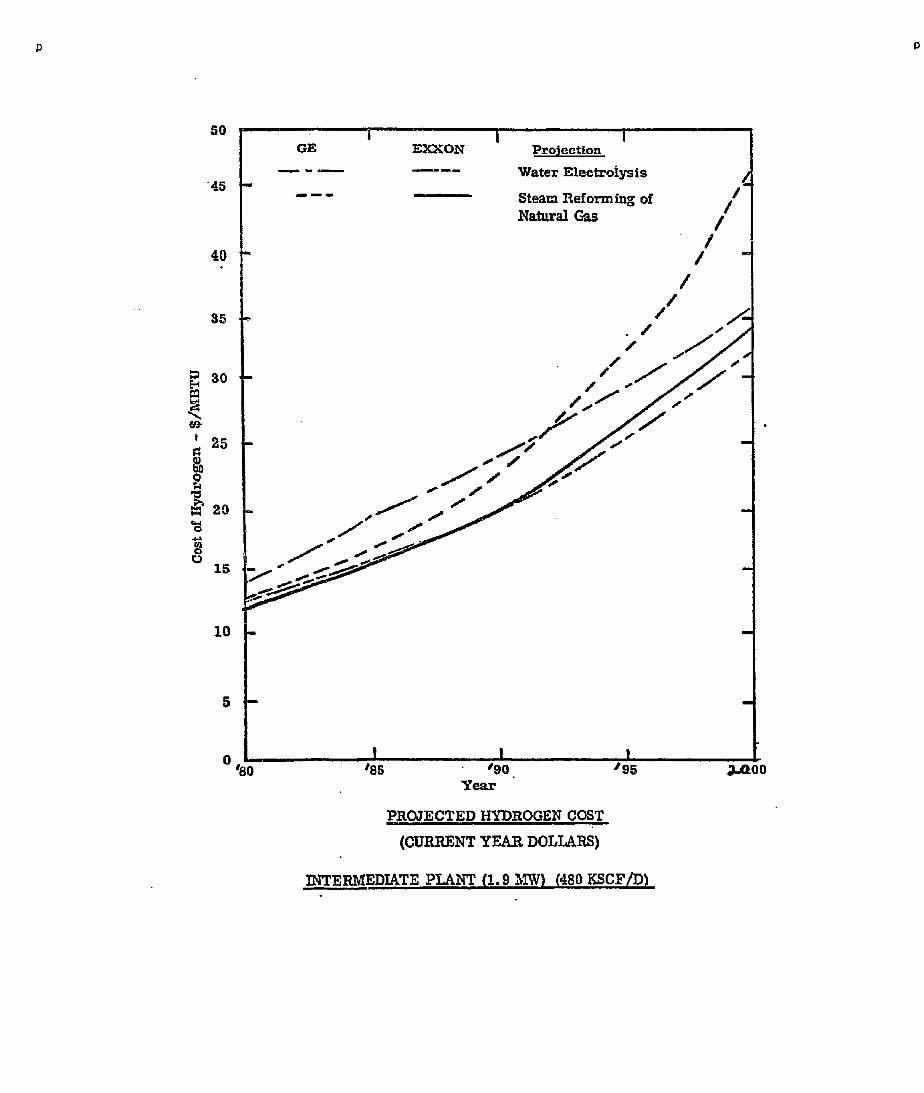

For the intermediate size p.~ant0 the cost of hydrogen from water

electrolysis would be almost competitive with the steam reforming, as

shown in Figure 4, and would become more economical starting around

1990. For the small plant, as shown in Figure 5, electrolytic hydro-

gen will be the most economical from the outset. It will also be more

economical than purchased liquid or high pressure gaseous hydrogen,

as shown in Figure 6.

Mr. NuttaU also presented the estimated data of annual hydrogen

usage within the component departments of General Electric Company.

These various GE departments my be typical of the smaller industrial

users of hydrogen.

As fossil energy becomes inadequate, large-scale hydrogen

production must utilize other energy sources such as nuclear fission,

fusion and/or solar energy for decomposition of water by electrolysis;

or by thermochemical cycles, and perhaps, by hybrid combinations of

these methods. Dr. K. E. Cox reviewed the research and develop-

ment status of therL~ochemical production of hydrogen from water. As

pointed out by Dr. Cox, it has been widely recognized that the

thermochemical methods are potentially more efficient and less expen-

sive than the overall electrolysis processes. Although a large number

-46-

D 0

P .,. . :..;.~.j ~.;:.

of thermochemical cycles have been conceived, many have published

without experimental verification of the reactions in the cycle. As a

result of this, most evaluations and/or comparisons of thermochemical

processes for process efficiency or cost have been based on assumed

data or on reaction conditions that have not actuolly been achieved.

Nevertheless, several cycles have now been published where all of the

reactions have been demonstrated experimentally. As a consequence,

the development of methods for engineering and cost analyses for this

new technology can be based on the actual chemisU'y involved in

demonstrated cycles.

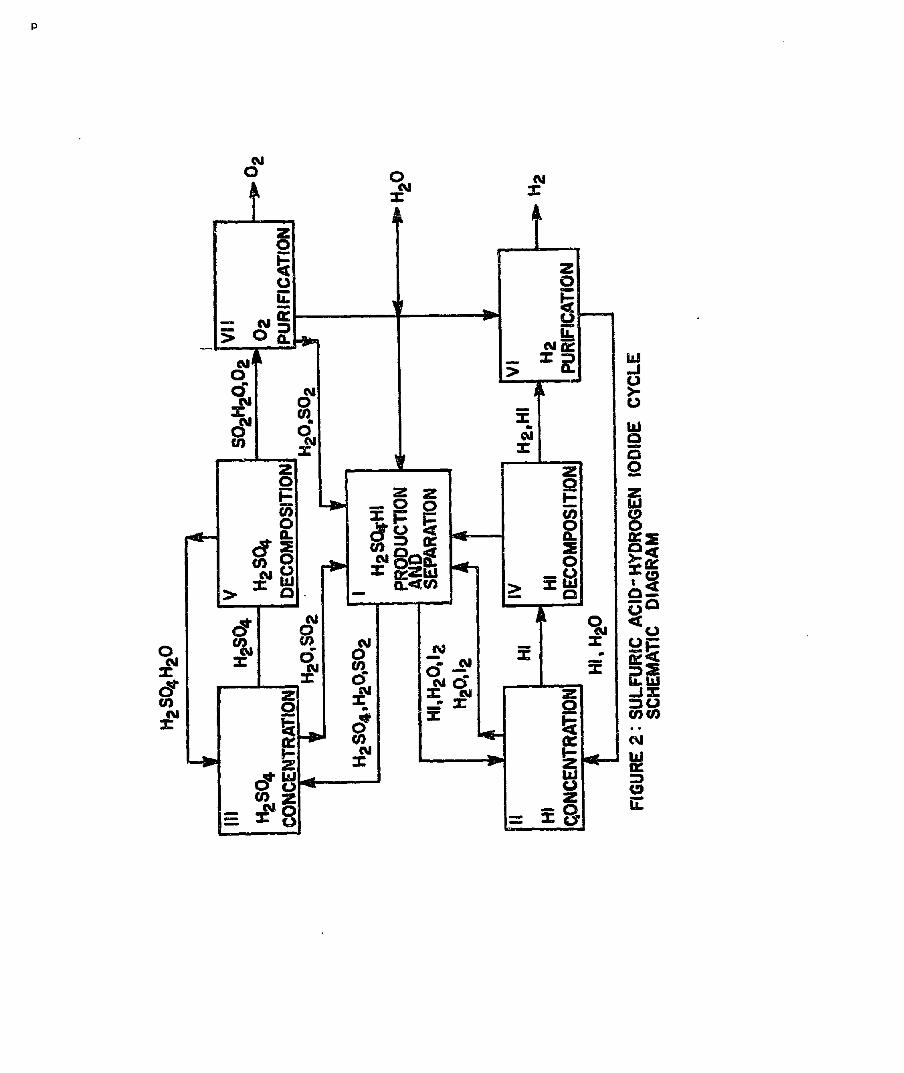

As examples, Dr. Cox described two thermochemical methods, the

sulfuric acid-hybrid cycle and the sulfuric acid-hydrogen iodide

cycle. Energy sources for thermochemical processes such as nuclear

energy and solar energy were also discussed.

The cost estimates for a thermochemical process is usually ob-

tained and often made on a set of assumptions and uncertain condi-

tions. Therefore, it is difficult to determine whether a particular

cost estimate is opl~is t ic or pessimistic. Dr. Cox summarized the

cost estimates made for the sulfurk: acid-hybrid and thermochemical

sulfuric acid-hydrogen iodide cycle. They are in the range of $5.27-

$7.18 per GJ in the 1975-76 dollars. The data are included in Ap-

pendix XVI of this report which is the paper prepared for this work-

shop by Drs. K. E. Cox and M. G. Bowman.

A4"y

o p

SCENARIOS AND OTHER COMMENTS

ON SUPPLYING HYDROGEN CHEMICAL FEED STOCK

- Session 5*-

At the present time, almost all hydrogen in Petroleum refining is

by-product from catalytic reforming and almost all hydrogen used in

chemical production is from reforming natural gas.

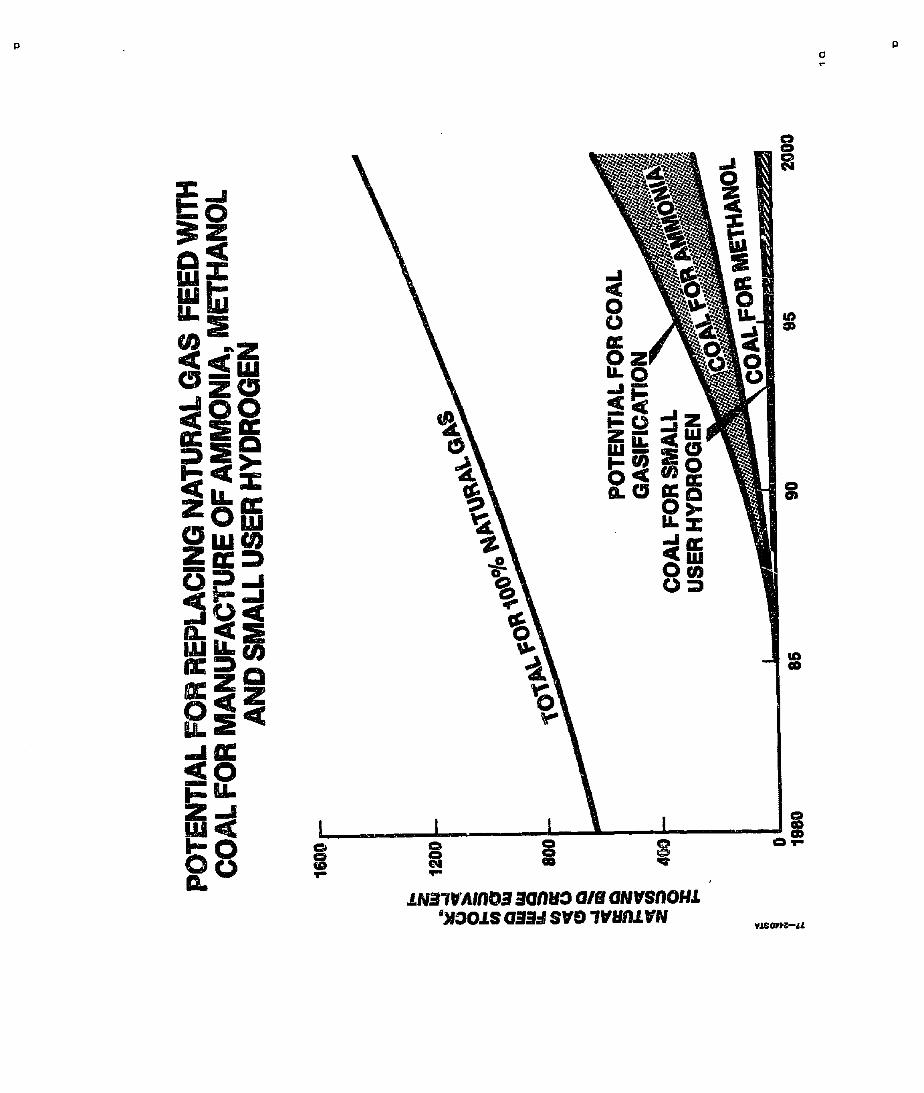

Between now and the year 2000, the uses of hydrogen will

increase in petroleum refining and as a chemical feedstock. A s tudy

has been made of what might happen during this period and the

results are presented in the Exxon-Brookhaven Report (Reference:

Mr. Corneil's presentation in Session 2). Mr. W. H. Stanton of the

Monsanto Co. summarized the results in the following four figures and

one table.

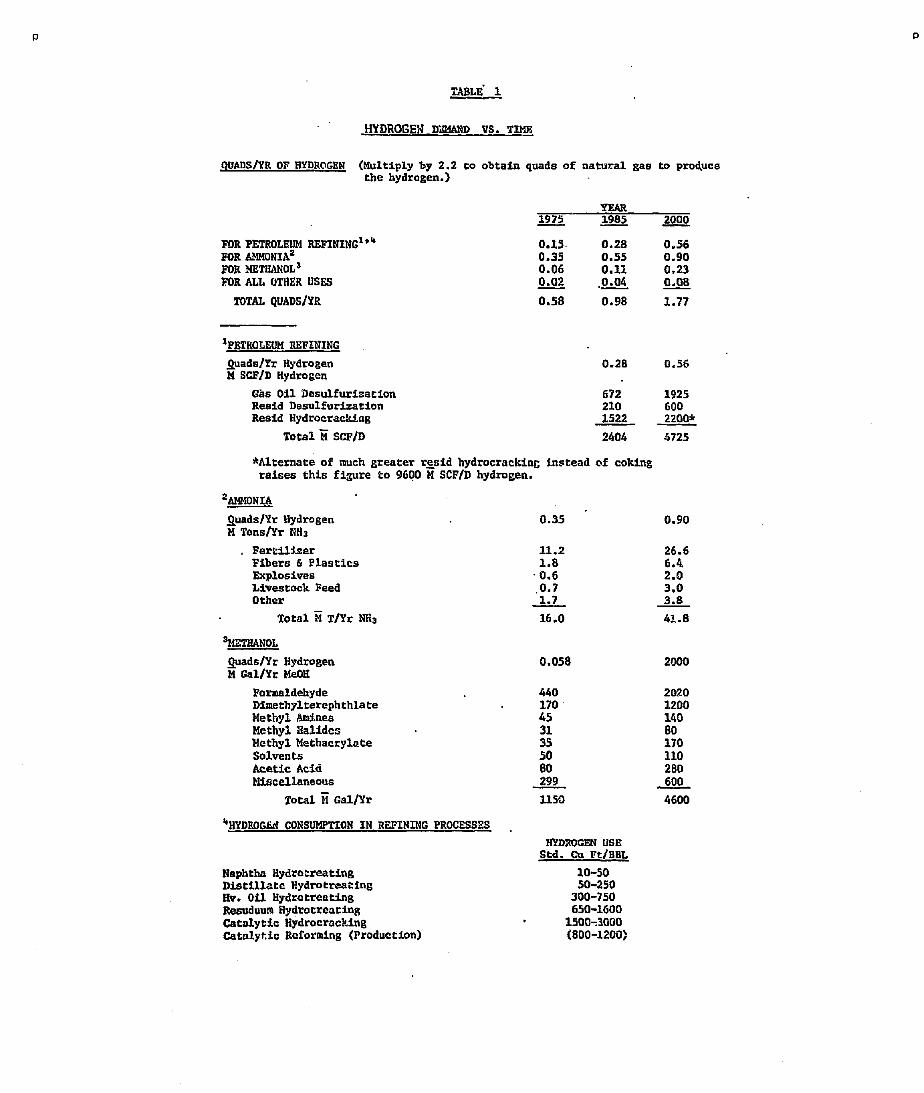

Figure 1 - - Raw lvlaterial Costs vs Time

Figure 2 m Total U.S. Energy Demand vs Time

Table 1 - - Hydrogen Demand vs Time

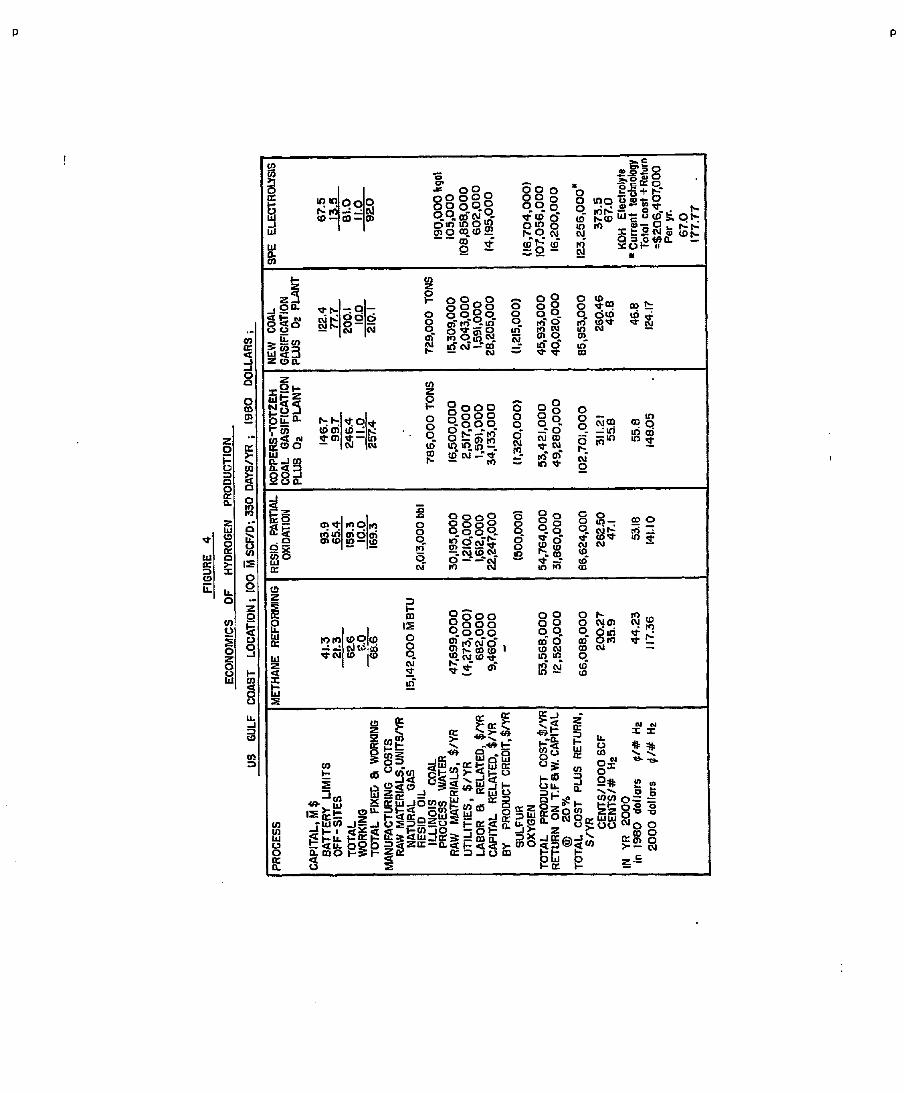

Figure 3 - - Processes for Hydrogen Production

Figure 4 - - Economics of Hydrogen Production

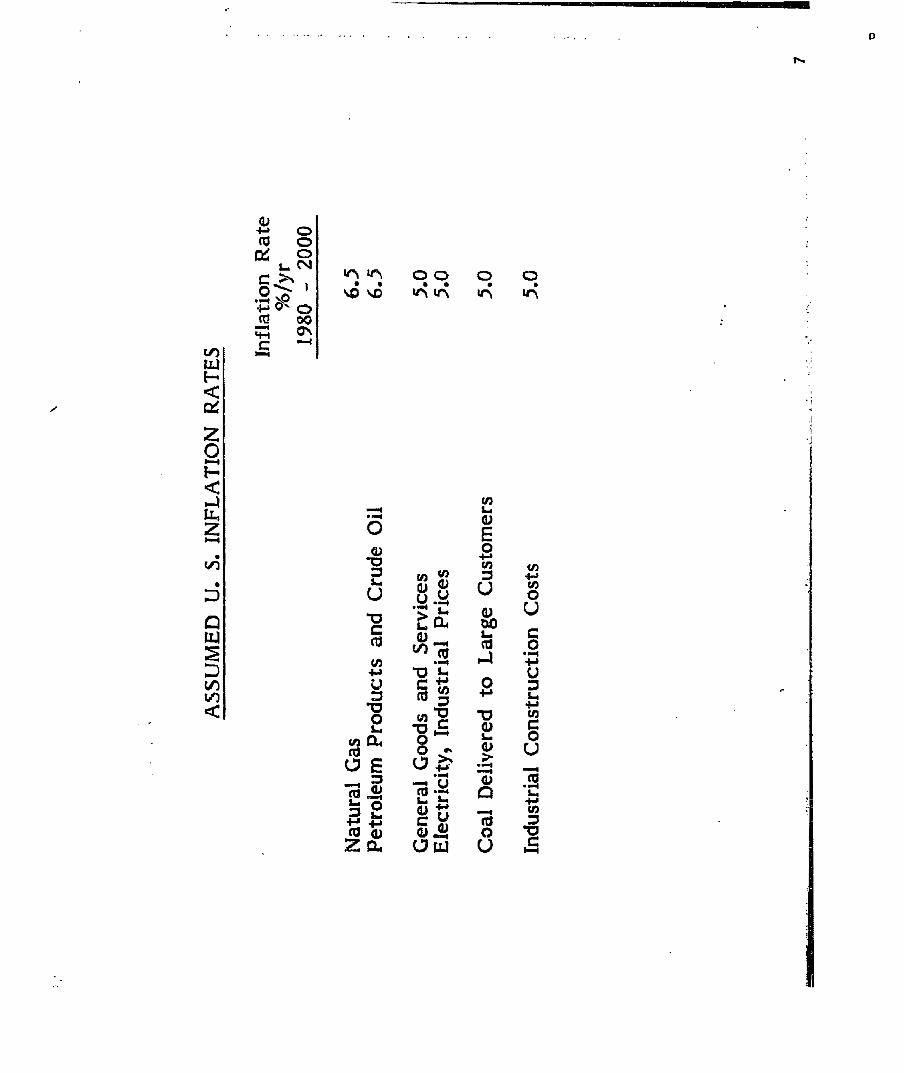

Raw materials are presented in 1980 and in the year 2000. For

the year 2000 the costs are reported in equivalent "1980" dollars and

also in "2000" dollars (based on a 5% annual il~*lation rate) .

Total U.S. energy demand is reported £u quads/yr . For 1974

actual demand was 76.8 quads-- i t is predicted that this will grow to

X* Session Chairman: James E. Funk Univers i ty o f Kentucky

- 4 R -

0 0

P 0

• . . . . . . . . ° . . - .

140.7 quads irt 2000. The expected growth is dependent on a large

increase in imported oil and in nuclear energy.

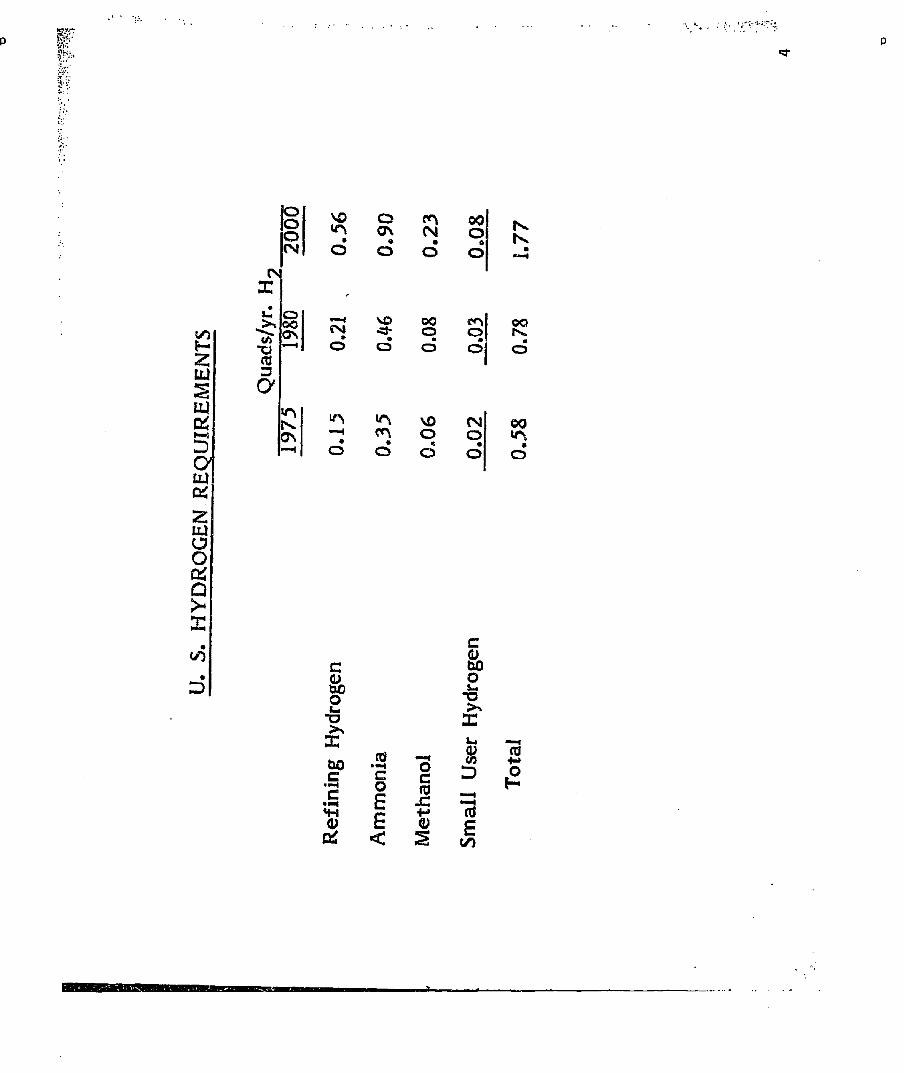

The energy required to produce hydrogen is 1.7~ of the total

U.S. demand in 1974 growing to 2.84 in 2000. The hydrogen pro-

duced as used in petroleum ref ining, ammonia production, methanol

production and others as summarized in Table 1.

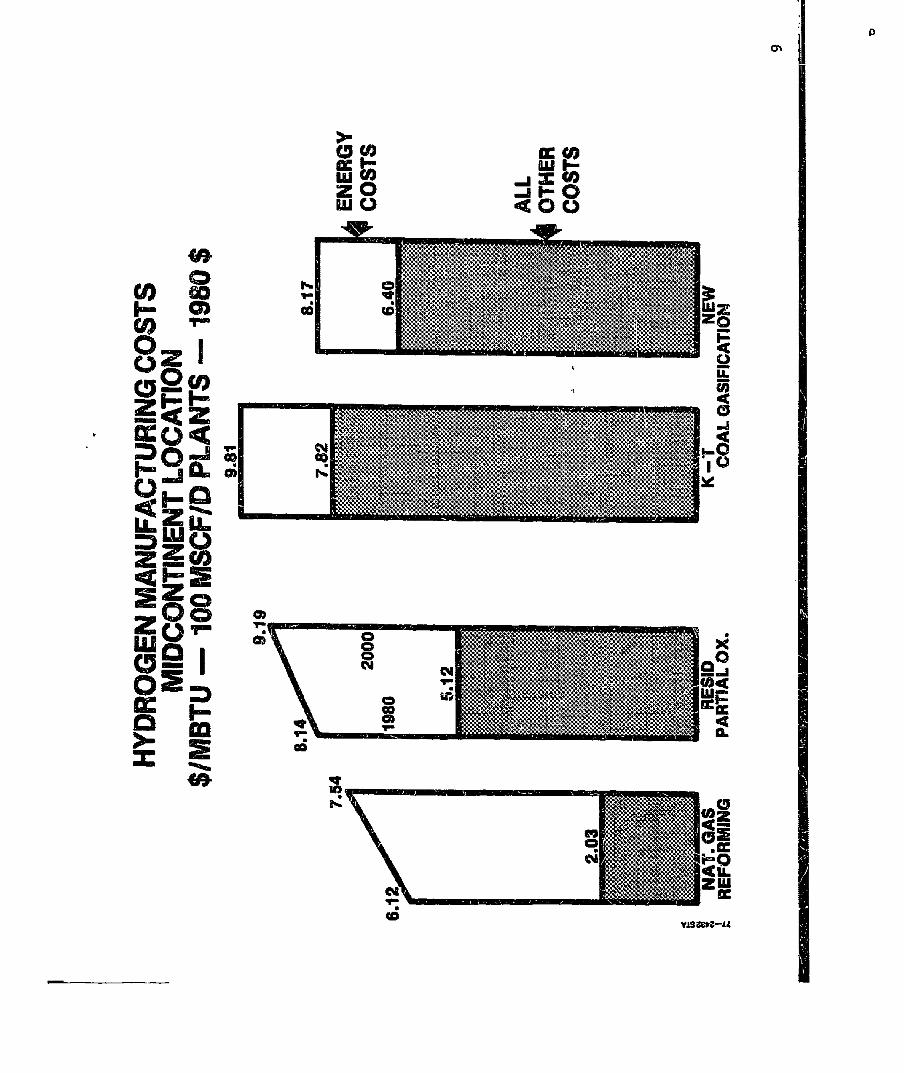

Processes for hydrogen production include: Steam reforming of

methane, partial oxidation of res id , KT coal gasification, new coal

gasification and SPE Electrolysis. The most economical process in

1980 is steam reforming of methane. The most economical process in

2000 is still steam reforming o~ methane. The new coal gasification

economics are a close second both years . New coal gasification is

being developed but still unproven. Perhaps it will be demonstrated

on a large-scale in the early 1980ts.

In order to calculate certain process economics, principally

operating costs on the various processe.~ for manufacturing hydrogen,

it was desirable for the part ic ipants to have some projections on

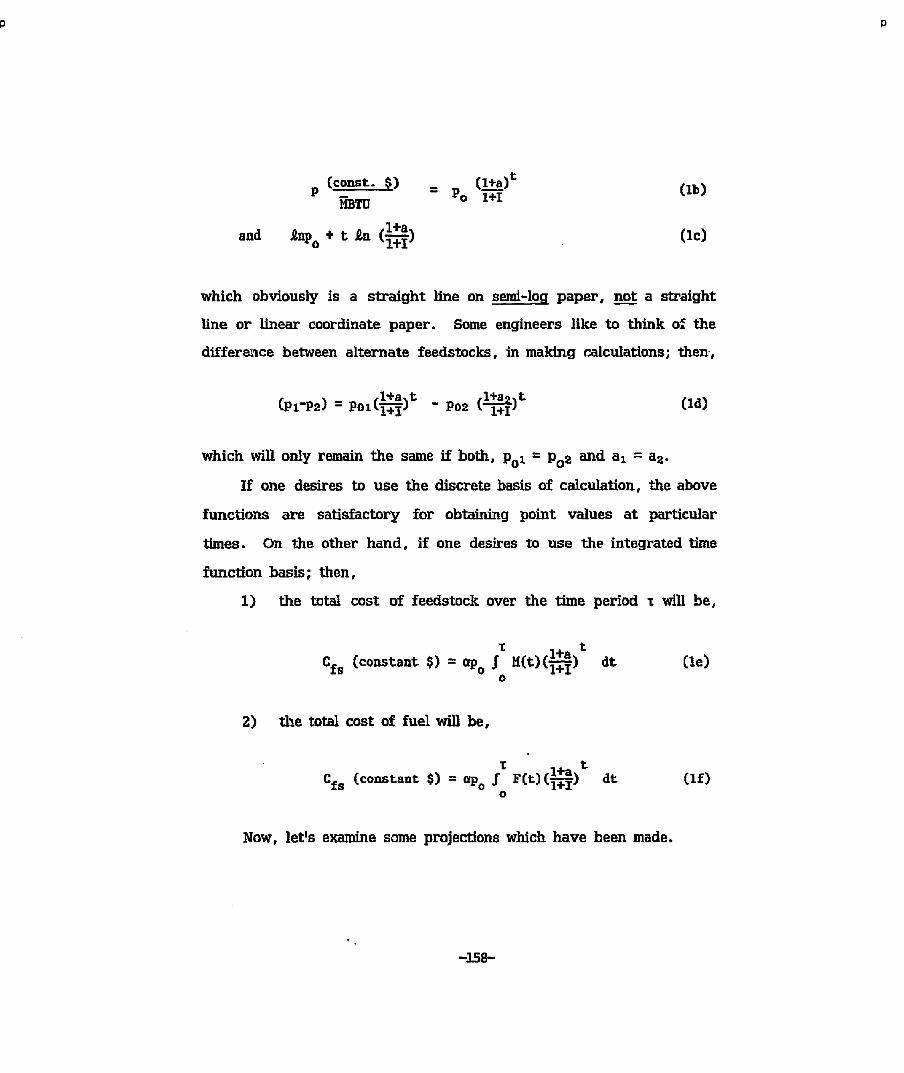

prices of energy/hydrogen feed stocks. Dr. H. W. Prengle, J r . of

the Univers i ty of Houston, ..~r. W. H. Stanton of Monsanto Company,

and Mr. 7. E. Stevens of Air Products prepared the information on

shor t notice, which was dis t r ibuted to the participants as guidelines

for the workshop discussion. The information is included in this

report as Appendix XVII.

p P

Many other scenarios can be imagined for the future energy/

hydrogen supply and demana. To provide the starting points for the

workshop discussion, the following three were suggested, but there

was no time available for the participants to discuss them in depth.

1. Gradual Decline

.

We continue as we have since 1974, each year we import more and more oil with prices rapidly rising as they have since the embargo. Our standard of living starts dropping--we cut back --the more we cut back the worse business becomes. We settle into a prolonged depression--after many years we get some leadership and start to rebuild with what we have--coal, nu- clear, solar, etc. By the year 2000 we work our way back to the standard of living of the 1960ts.

Gradual Rise to New Heights

We continue as we have since 1974; each year we import more and more oil. The oil is made available and at reasonable prices as there is a split in the OPEC groups and competition keeps prices down. Large world discoveries of oil and gas are found --we continue on our energy binge thru 2000--no problems. In the meantime, technical advances make fission the source of unlimited future energy.

. Sudden Abrupt Upheaval

We continue as we have since 1974, each year we import more and more oil with prices rapidly rising. It gets so only the very rich can afford heat, gasoline, air conditioning. The poor turn more and more to get t ing what they want by violent acts - -before it 's over we have civil uprising and a dictator form of government results. From then on, it 's close to the s tandard of l i~ng of Communist countries.

As par t of many inputs to the planning of future R & D pro-

grams, the workshop participants were asked to consider, among

others , the following questions:

D P

D p

1) What technological developments could have a significant impact in reducing hydrogen manufacturing costs?

2) What technological developments could have a significant impact in reducing hydrogen demand?

A lively discussion, to the extent it spilled over to Session 6,

yielded many interesting comments and useful recommendations:

Governmental work creased emphasis. SNG R & D).

on Hz production from coal needs in- (However, this was not the feeling for

Investment Tax Credits or accelerated depreciation are desirable incentives; loan guarantees often draw the gov- ernment into poor projects. Matching funds are similar to tax credits.

Decontrol of energy prices would be the fastest incentive. This point was unanimously agreed to and expressed throughout the workshop. It was further recommended that it "should be a national objective to get the government out of the energy business" except for energy R & D.

It was suggested that a disincentive (tax) be placed on the use of natural gas for heat rather 1_han as a chemical feed- stock. And it was also noted that decontrol would accom- plish these objectives without a special program.

Uncertainty of government policies is a deterrent to indus- try actions toward developing new technologies.

It was generally indicated that the workshop was helpful to the part icipants for information flow. Some suggested tha t it be repeated next year and/or annually.

D 0

0 0

APPENDIX I

Lis t of Par t ic ipan ts in Steering Commttee and Preliminary Meetings

~uly 7, and September 21-22, 1977

J e f f r e y Anderson Koppers Company, Inc . P i t t s b u r g h , Pennsylvania

Bever ly Berger~ Department o f Energy Washington, D.C.

J. W. Bowles Howe and Baker T y l e r , Texas

A. E. Cover Pullman-Kellogg Company Houston, Texas

Jim Graybi l l Air Products and Chemicals , Inc . Allentown, Pennsulvania

Harold Hoffman Hydrocarbon Process ing Houston, Texas

John R. Howell U n i v e r s i t y o f Houston Houston, Texas

C. J . Huang ~ University of Houston Houston, Texas

James H. Kel ley ~ Jet Propu l s ion Laborato~3 Pasadena, Ca l i fo rn i a

Joe l Landis Anderson Clayton Houston, Texas

John J . McKetta~ Un ive r s i t y o f Texas Aust in , Texas

Jim Michaels Koppers Company, Inc . P i t t s b u r g h , Pennsylvania

Jim Newmann Armco S t e e l Company Middletown, Ohio

L. J . N u t t a l l General E l e c t r i c Wilmington, Massachuset t s

Mark Pascoo Fluor Engineers & Cons t ruc tors Los Angeles , C a l i f o r n i a

Richard Per ry ~, Union Ca r~ .~.~. Corpora t ion l~ew York, ~ . . York

H. W. Prengle Un ive r s i t y o f Houston Houston, Texas

Frank Salzano ~ Brookhaven Na t iona l Labora tor ies Upton~ New York

J. E. Stevens~ Air Products and Chemicals, Inc. Allentown, Pennsylvania

Ken Tang~ J e t Propulsion Laboratory Pasadena~ Cal i fornia

B i l l Turk Brown & Root H o u s t o n , T e x a s

Steering Comm4ttee

D P

p D

, . . ° . . . . . . . . . . . . . . .

APPENDIX II

WORKSHOP PARTICIPANTS

December 12-14, 1977

3effreyAnderson Koppers Company Pittsburgh, Pennsylvania

L. C. Bassett Howe-Baker, Inc. Tyler, Texas

Henry Bernstein IIl Cities Service Company Tulsa, Oklahoma

C. Bonifaz E. I. DuPont Company Wilmington, Delaware

Lloyd Busch Ashland Oil Co. Ashland, Ohio

Roger Chen Hudson Engineering Corp. Houston, Texas

George Clark Union Carbide Corporation New Yozk, New York

Calvin Cobb Pace Engineering Houston, Texas

Paul A. Cook Celanese Chemical Co. New York, New York

Hampton Cornei l Exxon En te rg r i s e , Inc . New York, New York

Kenneth E. Cox Los Alamos Scientific Lab. Los Alamos, New Mexico

Tom A. Czuppon Pullman-Kellogg Houston, Texas

George H. Daniel Union Carbide Co~poration S. Charleston, West Virginia

T. C. Dauphine Badger P l an t s , Inc. Cambridge, Maryland

F. J. Edeskuty Los Alamos Scientific Lab. Los Alamos, New Mexico

William J. D. Escher Institute of Gas Technology Chicago, Illinois

Ray Feldwick Teledyne Energy Systems Timonium, Maryland

Marshall Frank Chem Systems, Inc. New York, New York

James E. Funk Univer6ity of Kentucky Lexington, Kentucky

J. A. Gearhart Kerr-McGee Refining Corp. Oklahoma City, Oklahoma

P

p P

J . W. Gearinger E. I. DuPont & Co. Beaumont, Texas

Michael Goodman Davey Power Gas Houston, Texas

James Grayb i l l Air P roduc t s and Chemicals , Inc . Al lentown, Pennsylvania

Hiroshi Hara Murorau Institute of Tech. Japan

Harold Hoffman Gulf Publishing Co. Houston, Texas

John R. Howell University of Houston Houston, Texas

C. J . Huang U n i v e r s i t y of Houston Houston, Texas

J. T. Hul l F l u o r Engineers & Cons t ruc to r s Houston, Texas

John E. Johnson Union Carbide Corpora t ion New York, New York

J. H. Kelley Jet Propulsion Laboratory Pasadena, California

A. H. Levy Uni ted Technologies Corp. S . Windsor, Connect icut

Owen Livingston Tennessee Valley Authorit~ Muscle Shoals , Alabama

Bobby G. Loe Tenneco Oil Co. Houston, Texas

John J. McKetta University of Texas Austin, Texas

Warden Nayes American Petrofin~u Co. of Texas Big Spr ing , Texas

Jim Michaels Koppers Company Pittsburgh, Pennsy lvan ia

David Netzer Fluor EnEineers & Constructors Houston, Texas

Ken E. Notary Air Products and Chemicals, Inc. Allentown, Pennsylvania

I. J. Nuttall General Electric Company Wilmington, Delaware

David Owens MobayChemical Corporation Pittsburgh, Pennsylvania

R. Parthasarathy Hydrocarbon Research, Inc. Miami, Florida

H. W. Prensle , Jr. University of Houston Houston, Texas

J . H. Prescott McGraw-Hill Houston, Texas

J. T. Richardson University of Houston Houston, Texas

-55-

P 0

P P

Richard R. Roney V i s t ron Business Development Cleve land , Ohio

Richard C. Russell Exxon U.S.A. Houston, Texas

Frank J. Salzano Brookhaven National Lab. Upton, New York

C. C. S i l v e r s t e i n Westinghouse Advanced Energy

Systems Div i s ion P i t t s b u r g h , Pennsylvania

A. Max Souby University o f North Dakota Grand Forks, North Dakota

Wally S tan ton Monsanto Company Texas Ci ty , Texas

J . H. Swisher U.S. Department of Energy Washington, D. C.

Ken Tang J e t P ropu l s ion Labora tory Pasadena, C a l i f o r n i a

Frank Tsai K ine t i c s Technology I n t e r n a t i o n a l Pasadena, C a l i f o r n i a

William J . Turk Brown & Root Houston, Texas

Charles Vadovic Exxon Research and EnEineer ing Baytown, Texas

R. S. Watson Anderson Clayton Dal las , Texas

-56-

P D

p P

APPENDIX III

SUBJECT:

What is the Energy Picture . . . Today, Tomorrow?

AUTHOR(S):

~ohn ~. McKetm University of Texas

Austin, Texas

CONTENT:

Technical Paper

-57-

p 0

p

What is the Energy Picture . . Today, Tomorrow?

Dr. yohn y. McKetta E. P. Schoch Professor of Chemical Engineering

The University of Texas at Austin Austin, Texas

The biggest joke traveling around the U.S.A. this year is that "The U.S. Congress will solve the energy problems of the country."

The energy problem is not a joke! The energy story is a very complex one and cannot be told in its entirety in one lecture. It is well known that we are in a terrible energy mess but only a few people realize that there is no solution during our lifetime. By this I mean that we will not have the luxurious use of energy during the next 35-40 years that we will have today. Contrary to the accusa- tions coming from Washington there is no conspiracy unless there is a secret conspiracy between Congress and the Middle East. This coun- try is in trouble. In the vernacular of a boxer we have been hit hard on the chin, we are fiat on our back, the count is up to 9, and the referee has both feet in our chest. We are just not going to make it.

I am disappointed, confused, and appalled with the mysteriously seemingly anti-U.S, voting record of the U.S. Congress in energy ~olicies. Current policies of energy pricing and over-regulation of industry will spell disaster for the United States in less than ten years.

Many of you wishful thinkers have been led to believe we will have energy self-sufficiency by 1985. I predict that at the current rate of energy demand growth, the U.S. will have a severe recession brought about by the lack of domestic energy by 1985. In fact, there will be an energy shortage in the United States by 1985 that will make your hair curl. Most of this is because of the shortsighted- ness and lethargy of our Congress in energy matters.

Our energy supply is in trouble. We just cannot meet the fan- tastic energy demands through the year 2000 without yearly increas- ihg the energy imported from outside our border. Today over 45 percent of oil used in the USA is imported.

Almost everyone in this count ry , with the exception of one group, finally became aware of the energy crisis in October 1973 when the oil embargo was imposed by the OPEC countries. That one group was your U.S. Congress. Do you know that your Congress

-58-

D

has not put an extra drop of energy into your supply tanks since that data? By this I mean that none of the legislation that they have passed helped to improve our domestic energy situation. In fact many of the new governmental regulations have decreased the supply of domestic energy.

Sometimes it seems tha t th is country 's politicians and environmen- talists are linked together in a plot to br ing America to eventual disas ter by making domestic energy expansion impossible. I believe that the problems of h igher taxes, price controls, t h rea t of excess profit penalties, embargoes on leasing or operating in favorable coas- tai areas , and rigid excessive environmental requirements serve only as roadblocks in efforts to explore for new reserves or to build new facilities.

At a recent meed:ing in Washington, Senator Muskie told us, "We live in a mixed economy.where private enterprise and market forces are supposed to do the ]oh, but if they fumble the ball the Federal govexnment will intervene." He reminded us that the auto exhaust catalyst technology was greatly accelerated by the Federal law. Gosh, wouldn't it be wonderful if there were some reciprocal arrange- merit that if the Federal government fumbled the ball, private indus- try could intervene.

IMPORTED ENERGY

In 1976 we paid other countries about 37 billion dollars for oil and natural gas. So far this year we are importing oil and gas at a 20% higher rate. You might think that at least that's progress. We haven't doubled the amount of imports. But in the larger sense, these figures don't spell progress at all--they spell failure---failure and potential disaster for a nation which simply should not spend that much money for imported energies.

Although we continue to he less dependent on imported oil thm~ are Western Europe or :/apan, that dependence is growing. Within a few years the amount of imports of Middle -Eastern oil will take a huge jump. As you have been reading, our largest oil and gas supplier, Canada, wisely plans to eliminate all exporm of petroleum to the U.S. in order to conserve supplies for her own domestic use.

This sickening increasing dependence on imported oil will mean only grea ter r isks of another embargo,and nure i n ~ . i m i d a ~ n in the conduct of foreign policy, which jeopardizes our entire nation.

..qq.

0 P

Many wishful thinkers believe that the OPEC price of oil will decrease by 1980. My own prediction is that the OPEC price will go as high as $25/bbi oil by 1980 if we do not develop an effective energy program here in the USA.

How in the world could the wealthiest and most powerful nation in earth allow itself to be boxed into a corner like this? The reasons include the senseless inflexible governmental regulations and the extreme demands of the environmentalism. We now have so many roadblcks to expanded production that the energy industry is prac- tically inert because of goverr~-nental laws and red tape. Despite the continued warning from experts, the Federal Power Commission has been required for more than 20 years to keep the wellhead price of natural gas at extremely low levels in order to hold down the prices of consumers. These controls decrease the incentives for the devel- opment of new domestic supplies so that, just as we predicted in the early fifties, there is much less natural gas than we need today. Instead of repeating our mistakes in the oil industry where we again have imposed price controls. Again, we can predict the results: By keeping the prices of natural gas and domestic oil at ridiculously low levels, we are forcing consumers to buy more expensive foreign products from foreign oil and gas sources because we are producing so much less of our own oil and gas.

No wonder many o2 my senior students think ~.hey can run the country better than the Congress!

INCREASED USE OF COAL

The companies trying to use more coal are having troubles. While one branch of government is starting to order more plants to use coal, other branches take action that will eliminate a million tons from the market. Expanded production is being held up by rules limiting strip mining and a moratorium on leasing Federal coal !.~nds. While the domestic use of coal is limited by too strict clean air rules, at the same time the export of coal to Germany and Japan is being promoted by our government with the result that the eastern U.S. reserves are being used for foreign consumers who bid up the price making the fuel more expensive to AJnericans. In the midst of this tremendous energy crisis it's difficult to believe that the coal produc- tion in the United States today is lower than it was 30 years ago. Most of this is because of FPC, EPA and MESA. Since EPA and MESA have come into existence in the early 70's, over 20~ of our coal mines have been shut down.

It's necessary for us to triple the amount of coal that we use by 1990. We must find a way to produce this much coal and we must be allowed to consume this much coal if we wish to free ourselves of the increasing import. The recent attempt by Congress to pass strip mining legislation that would create dis-incentive to production, tulnecessarily, add to costs, and adversely affect jobs illustrates again the wrong directlon Congress takes for the energy policy. Even my own congressman voted this way. Thank God the President's veto prevailed.

Here is just one of the many senseless predicaments in which we find ourselves:

Thirty-six coal burning electrical plants were instructed by EPA to use certain scrubbers to remove sulfur dioxide form the stack gas. The EPA claims these scrubbers have been proven to be effective by the Japanese. If the electrical power companies put these scrubbers on these 36 coal burning electrical plants, they will produce a toothpaste-like sludge from the scrubbers that will cover 13 square miles of surface, one foot deep, each ~ ej~ea~. You see, many times the EPA controls are worse than the or~nal problems. None of us can forget the tail gas catalytic converters fau.._._xx pas on the '75 and later cars.

NUCLEAR ENERGY

In the field of nuclear energy, the story is again a sad one. This country was the pioneer in the development of nuclear power. Yet today we require up to 11 years to build a nuclear power plant in the United States while it takes only 4½ years in Europe or Japan. Why? Again, because of excessive governmental regulations!

Many of you will recall the story that way back in 1889 some- thing was bothering Thomas Edison. He wrote an article for the Scientific American warning the public about what he perceived as a major public danger.

"My personal desire would be to prohibit entirely the use of alternating currents," Edison wrote. "They are unnecessary as they are dangerous. I can therefore see no justificatlo1~ for the introduc- tion of a system which has no element of permanency and every element of danger to life and property."

Now from the vantage point of our alternating current world 88 years later, it is apparent that this great person either was unex- plainably wrong in principle, or he failed to anticipate the technology

0 P

tha t put alternating current electricity into nearly universsd use across the United States.

We solved the alternating current hazard--we can solve the new hazards.

Nowadays people are worried about nuclear radiation risks and hazards just as Mr. Edison was worried 86 years ago about AC elec- tricity. Everyone admits that radiation can be dangerous just as gasoline can be dangerous, automobile driving can be dangerous, and electricity can be dangerous. But reasonable people will take moder- ate risks for great benefits, small risks for moderate benefits, and no risks if there are no benefits. Our policy makers must learn that the world is risky, and that the problem isn't whether something is safe, but what the risks are, and whethez the benefits are worth those risks. If we could get governmental regulation founded on such a rational basis, we really would be a step ahead on the road to further progress through the benefits of modern science and technology.

Our nation and its laws should aim at devising the best possible means to manage the risks involved--rather than deceiving ourselves and the public into believing that all risks can be banned by human force.

Rather than simply banning the material that m y be dangerous, we need to answer more basic questions. What is the nature of the hazard? How serious is it? Can it be managed properly? In short , we must weigh the r isks and our ability to manage them with the benefits. If the human need is great, such as radioactive materials use for medical t reatment, then a safe way for manufacture and use must be found. Risks are to be found everywhere in life.

CAN~EHAVE ZERO RISK?

EPA uses statistics to prove that "even negative experiments do not guarantee absolute safety."

Since when has it been a government function to "guarantee safety" to a 100% level? There is no activity of man, including the normal basic psychological functions, without r isk. As some witty Irishman once said, "The path from the cradle to the grave is so beset with perils, 'tis a wonder that any of us live to reach the la t ter ." All that any of us have the r ight to expect, and all that the vast majority of us ask, is that government regulations help keep the r isks within the reasonable bounds, not that they "guarantee absolute safety" --there is no such animal!

P

P p

During the past 20 years we again have dire warnings from many highly educated people. They tell us of the imminent doom from hazards (which are, by any reasonable assessment, re~lly quite small). They have helped convince the average U.S. citizen that all chemicals are dangerous and should be avoided..They proclaim L~ terrible danger that a few people m_~-----~ fall victim to "~m~er originated by me chlorination of public water ~upplies and they cause wide- spread concern abut the safety of the water the public drinks. But they totally ignore ~he millions of people who died of typhoid, and other waterborne diseases, before the general adoption of chlorina- tion. They shudder over the possibility that a few people may be adversely affected by food preservatives. They neglect to point out that there would be a greater incidence of disease, and loss of food- staffs (in a world already concerned about adequate food supply) if the preservatives are not used. Here are other examples of their misguided crusading:

You know the plain fact is that there is no substance, including water and oxygen, which is not harmful to, or which will not produce toxic reaction in, laboratory animals or in human beings when admin- istered in massive overdose. Similarly, there is no substance which, even in small amounts, will not cause problems t~-a few unfortunate individuals who happen to b-e--sensitive or allergic to--~at particular material. We simply cannot guarantee complete safetzv by government fiat or any other means. Of course, we need to curb pollution, but we need to do it rationally, balancing general benefits against general risks.

Shouldn't we rataer get a better perspective on relative hazards and devote more of our energies to stopping some of the more genuine menaces to the average citizen, such as our annual highway death toll, the rise of violent crime, increasing rates of rape, murder, etc. If I should be injured in a collision with a drunken or reckless driv- er, or while helpless people should be robbed and perhaps murdered, it would be a small consolation to know that EPA has "protected" us from the very slight chance that we might develop cancer from an additive which has been in general and beneficial use for many years wlth no discernible Ill effect on the general public health! Let's get off cloud nine and down to earth about th~ real risks and chances involved in living in this imperfect ~rZd.

When we consider zero risks let's remember that in the 18-year history of commercial nuclear plant operations (1958-1976), no acci- dents have occurred involving public injury nor over-radiation. Yet, in the sar~_e period in the United States alone 848,544 people have been killed ~-y motor vehicles and more than 75 million have been injured by this highly popular invention. To my knowl^dge there is no popular, movement to "ban the auto."

D 0

In 1976 alone there were over 31,000 truck accidents which included 3,000 deaths and over 20 million dollars worth of damage. Should we eliminate trucks from our highways?

In 1976 over 154 miners were killed in the United States and over 1,000 people were electrocuted from electric power Rues and appliances. Should we cut out electricity and shut down the coal mines?

In 1976 .over 70,000 teachers were assaulted in the classroom by their students, ranging from slaps by the student to killings with knives or ice picks. Should we eliminate classrooms? Over 24,000 people were mtu-dered in the U.S. in 1976.