1/33 Joh. Berenberg, Gossler & Co. KG Sector Special European Telecoms – Vol. I European Telecoms Vol. I: Better together! - Initiation on Altice “The telecoms sector hasn’t had its Lehman moment yet. But with declining revenues, rising debt, dated business models, I worry about that happening.” Former Digital Agenda Commissioner Neelie Kroes certainly made a point at the European Internet Foundation Breakfast Debate two years ago. The telecommunications sector has been hit hard in recent years, mainly by the impact of EC regulations, fierce competition and flagging economic growth. However, the sector narrative started to change in 2014, on the back of the EC’s newfound openness to consolidation, the brightening economic outlook as well as on the general excitement about data growth and the related future-proof technologies such as 4G and fibre. Despite a still challenging competitive environment, we expect the telecoms sector to have reached its trough and recover from 2015 on. While convergence and in-market consolidation should have more of a stabilising impact on ARPU, we expect a clearly positive impact on opex and capex, both benefitting from synergies (labour and maintenance costs, network and IT infrastructure). Due to superior network assets, we expect operators with cable based fixed-line networks to keep their competitive and obtain a substantial financial advantage over traditional telecoms, which need to intensify the expensive fibre deployment in order to become competitive again. We therefore like the Altice Group, which through its subsidiaries Altice France (Numericable-SFR) and Altice International operates a multinational cable and telecommunications business with leading positions in its respective markets. By following a very distinct pattern – mainly debt-financed acquisitions of underperforming telecom assets in order to boost their profitability by generating synergies – Altice has emerged out of relative obscurity. When comparing its subsidiaries, we prefer Altice International over Altice France given the proven track record of high EBITDA growth, lower leverage and less potential to experience another near-term leverage-intense acquisition. Moreover, Altice International’s bonds ALTICE 6 ½ 01/22 and ALTICE 8 12/19 offer considerable spread tightening potential towards their CDS curve, which is more in line with the ALTICE 5 ¼ 05/23. A comparison with the closest peers draws a similar picture, with lower rated UPC bonds trading at tighter spreads within the same time-to-worst bucket. We therefore initiate with an overweight on the ALTICE 6 ½ 01/22 and the ALTICE 8 12/19. Please find further recommendations in the report. Companies covered in this study: (Screening coverage) Company Bond ratings/Outlook Altice S.A. (Altice Group) B1/neg. (Moody’s) B+/neg. (S&P) Altice Financing (Altice International) B1/neg. (Moody’s) Bonds only: BB- (S&P) Altice Finco S.A. (Altice International) B3/neg. (Moody’s) Bonds only: B- (S&P) Numericable-SFR SAS (Altice France) Ba3/neg.* (Moody’s) B+/neg. (S&P) * ratings under review for possible downgrade Berenberg’s top picks: Bond/recom. Price / YTW / Z-spread ALTICE 8 12/19 Overweight 107.9 / 2.4% / 232bps Next call: 12/[email protected]ALTICE 6 ½ 01/22 Overweight 108.4 / 4.1% / 405bps Next call: 12/[email protected]ATCNA 7 ¼ 05/22 Overweight 104.1 / 6.3% / 604bps Next call: 05/[email protected](Pricing: 24/03/2015 BGN Close) 25 March 2015 Alexandre Daniel Analyst +49 69 91 30 90-593 [email protected]Patrick Voßkamp Research Support +49 69 91 30 90-596 [email protected]Type BERF <Go> at Bloomberg for further Berenberg FI Research EUR denominated bonds of the Altice Group Source: Bloomberg, Berenberg Research (Pricing: 24/03/15 BGN Close) ALTICE 8 12/15/19 ALTICE 6 1/2 01/15/22 ALTICE 9 06/15/23 ATCNA 7 1/4 05/15/22 NUMFP 5 3/8 05/15/22 ALTICE 5 1/4 05/15/23 NUMFP 5 5/8 05/15/24 ATCNA 6 1/4 02/15/25 0 100 200 300 400 500 600 700 0 1 2 3 4 5 6 7 8 9 10 11 Z-/CDS-spread (bps) time to worst Altice SA CDS Finco/Financing CDS Numericable CDS FIXED INCOME RESEARCH | CORPORATES

Transcript

1/33 Joh. Berenberg, Gossler & Co. KG Sector Special European Telecoms – Vol. I

European Telecoms Vol. I: Better together! - Initiation on Altice

“The telecoms sector hasn’t had its Lehman moment yet. But with declining revenues, rising debt, dated

business models, I worry about that happening.”

Former Digital Agenda Commissioner Neelie Kroes certainly made a point at the

European Internet Foundation Breakfast Debate two years ago. The telecommunications

sector has been hit hard in recent years, mainly by the impact of EC regulations, fierce

competition and flagging economic growth. However, the sector narrative started to

change in 2014, on the back of the EC’s newfound openness to consolidation, the

brightening economic outlook as well as on the general excitement about data growth

and the related future-proof technologies such as 4G and fibre.

Despite a still challenging competitive environment, we expect the telecoms sector to

have reached its trough and recover from 2015 on. While convergence and in-market

consolidation should have more of a stabilising impact on ARPU, we expect a clearly

positive impact on opex and capex, both benefitting from synergies (labour and

maintenance costs, network and IT infrastructure). Due to superior network assets, we

expect operators with cable based fixed-line networks to keep their competitive and

obtain a substantial financial advantage over traditional telecoms, which need to intensify

the expensive fibre deployment in order to become competitive again.

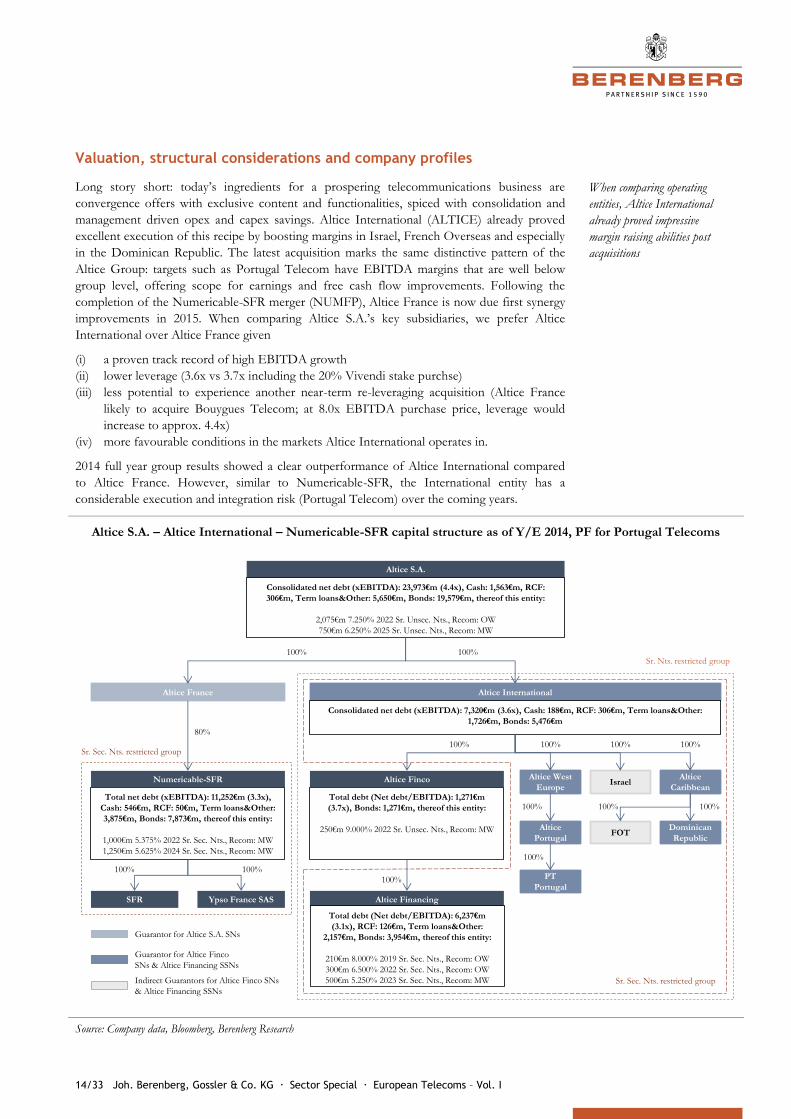

We therefore like the Altice Group, which through its subsidiaries Altice France

(Numericable-SFR) and Altice International operates a multinational cable and

telecommunications business with leading positions in its respective markets. By

following a very distinct pattern – mainly debt-financed acquisitions of underperforming

telecom assets in order to boost their profitability by generating synergies – Altice has

emerged out of relative obscurity. When comparing its subsidiaries, we prefer Altice

International over Altice France given the proven track record of high EBITDA growth,

lower leverage and less potential to experience another near-term leverage-intense

acquisition. Moreover, Altice International’s bonds ALTICE 6 ½ 01/22 and ALTICE 8

12/19 offer considerable spread tightening potential towards their CDS curve, which is

more in line with the ALTICE 5 ¼ 05/23. A comparison with the closest peers draws a

similar picture, with lower rated UPC bonds trading at tighter spreads within the same

time-to-worst bucket. We therefore initiate with an overweight on the ALTICE 6 ½

01/22 and the ALTICE 8 12/19. Please find further recommendations in the report.

4/33 Joh. Berenberg, Gossler & Co. KG Sector Special European Telecoms – Vol. I

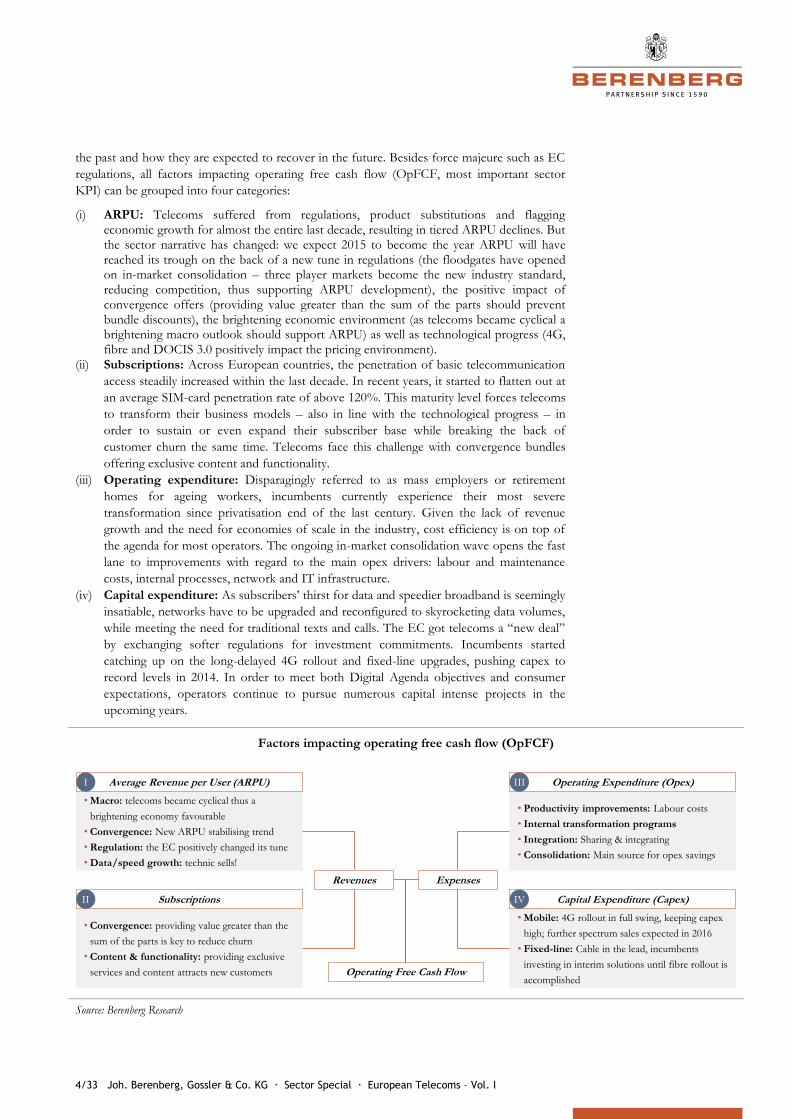

the past and how they are expected to recover in the future. Besides force majeure such as EC

regulations, all factors impacting operating free cash flow (OpFCF, most important sector

KPI) can be grouped into four categories:

(i) ARPU: Telecoms suffered from regulations, product substitutions and flagging economic growth for almost the entire last decade, resulting in tiered ARPU declines. But the sector narrative has changed: we expect 2015 to become the year ARPU will have reached its trough on the back of a new tune in regulations (the floodgates have opened on in-market consolidation – three player markets become the new industry standard, reducing competition, thus supporting ARPU development), the positive impact of convergence offers (providing value greater than the sum of the parts should prevent bundle discounts), the brightening economic environment (as telecoms became cyclical a brightening macro outlook should support ARPU) as well as technological progress (4G, fibre and DOCIS 3.0 positively impact the pricing environment).

(ii) Subscriptions: Across European countries, the penetration of basic telecommunication

access steadily increased within the last decade. In recent years, it started to flatten out at

an average SIM-card penetration rate of above 120%. This maturity level forces telecoms

to transform their business models – also in line with the technological progress – in

order to sustain or even expand their subscriber base while breaking the back of

customer churn the same time. Telecoms face this challenge with convergence bundles

offering exclusive content and functionality.

(iii) Operating expenditure: Disparagingly referred to as mass employers or retirement

homes for ageing workers, incumbents currently experience their most severe

transformation since privatisation end of the last century. Given the lack of revenue

growth and the need for economies of scale in the industry, cost efficiency is on top of

the agenda for most operators. The ongoing in-market consolidation wave opens the fast

lane to improvements with regard to the main opex drivers: labour and maintenance

costs, internal processes, network and IT infrastructure.

(iv) Capital expenditure: As subscribers’ thirst for data and speedier broadband is seemingly

insatiable, networks have to be upgraded and reconfigured to skyrocketing data volumes,

while meeting the need for traditional texts and calls. The EC got telecoms a “new deal”

by exchanging softer regulations for investment commitments. Incumbents started

catching up on the long-delayed 4G rollout and fixed-line upgrades, pushing capex to

record levels in 2014. In order to meet both Digital Agenda objectives and consumer

expectations, operators continue to pursue numerous capital intense projects in the

investing in interim solutions until fibre rollout is

accomplished

Capital Expenditure (Capex)IV

Expenses

Operating Free Cash Flow

5/33 Joh. Berenberg, Gossler & Co. KG Sector Special European Telecoms – Vol. I

ARPU – tough times behind, turnaround ahead

Telecoms suffered from regulations, product substitutions and flagging economic growth for almost the entire last

decade, resulting in tiered ARPU declines. But the sector narrative has changed: we expect 2015 to become the

year ARPU has reached its trough on the back of

(i) a new tune in regulations: the floodgates have opened on in-market consolidation. Three player markets

become the new industry standard, reducing competition, thus supporting ARPU development.

(ii) convergence offers: providing value greater than the sum of the parts should prevent bundle discounts

(iii) macro improvements: as telecoms became cyclical a brightening macro outlook should support ARPU

(iv) data/speed growth: 4G, fibre and DOCIS 3.0 positively impact the pricing environment

Overall trend

Almost the entire last decade has seen the European telecom industry ride out by far its

toughest times, with revenues that have undergone a fairly precipitous decline and margins

losing more and more ground. The persistent downward pressure mainly arose from:

(i) challenging regulations: By far the greatest obstacle telecoms had to overcome. Almost the entire last two decades telecom regulators on the national and the European level have created rules intended to keep communication prices low by stimulating increased competition or by directly imposing price ceilings. Thus, authorities gradually curbed lucrative revenue streams (i.a. roaming or termination charges) and imposed wholesale access (to wireless and wireline networks) at specified rates, the breeding ground for MVNO’s (mobile virtual network operator).

(ii) flagging economic growth: The telecom sector is billed as being defensive, however, Berenberg Equity Research (BER) questioned this former text book wisdom and established good versus bad mobile markets on the basis of mobile service revenue growth ex-MTRs (mobile termination rate) over the last six years. In testing numerous factors, and running over 30 separate regressions, only one factor truly stood out – GDP growth. In a second step, Equity Research regressed the three largest GDP constituents (government spending, investment and consumption) against mobile service revenue growth and identified consumption growth as the real underlying driver. In particular for the last two years an R² of 67% indicates a meaningful result. The sector has gone from no cyclicality to being cyclical, in particular since the financial crisis.

(iii) substitution: Telecoms by nature are closely related to technologies and their increasingly shortening life-cycles, thus are constantly faced with substitution threats. However, whereas substitution processes used to take place within the industry, telecoms recently have been increasingly challenged by other sectors such as the software industry, providing services “over the top” of the operators’ networks (OTT). Taking Voice as an example, on top of the progressing fixed-mobile substitution. Voice is now translated into Data (Voice over IP), opening the door for OTT providers such as Skype or Viper. All mobile services are transformable into simple data. Thus, given increased bandwidth for fixed and mobile users, they can be offered by OTT providers. Lucrative revenue streams as traditional Voice and Text services are step by step cannibalized by low-margin data and benefitting OTT’s.

The changing face of communication

Source: Berenberg Research

1995 2005 2010 2015 2020

The future is all about data - on the wireline and

wireless. Voice, msgs and content are all measured on

data. Network speed/quality comes

as the last possible differentiation

Same revenue streams as 5 years before, different

significance. 3G made mobile data consumable,

driving strong

growth

Whereas communication used to be almost entirely

voice driven in the early 90s, data started to play an

increasingly important role for

revenues from the mid 90s on

Telecoms are fighting declining revenues in fix and

mobile with content offers and network investments

Mobile services increasingly offset precipitous revenue

declines in fixed line services. Mobile data about to

Text Msgs Voice-MobileVoice-Fix Data-Fix Data-Mobile

SMS

Text Msgs Add Ons-Services

Data-Fix Data-Mobile

ARPU knew but one direction

in recent years: downwards

Regulatory hurdles by far

curbed revenue streams the most

Telecoms became cyclical, thus

suffered from flagging economic

growth

OTT services offer free or

inexpensive alternatives to

traditional telecom services such

as voice and text

6/33 Joh. Berenberg, Gossler & Co. KG Sector Special European Telecoms – Vol. I

We saw a first light at the end of tunnel in 2014, with softening declines on the top-line and

margins somewhat stabilising. The industry is currently turning former hurdles into stepping

stones and benefits from a brightening market environment in general. We thus expect 2015 to

become the year ARPU will have seen its trough and going forward noticeably stabilise on the

back of:

(i) favourable regulations: As much as most telecom executives saw regulation as root of all evil in the past, the newfound favourable stance of the EC towards consolidation now appears as a path to salvation for them. Authorities kept discussing the chicken or the egg causality dilemma for years, with a digital single market across the 28 EU member states representing the chicken and a fully consolidated market with only a few pan-European operator giants representing the egg. Applying a more benign regulatory regime seemed to be within a more easy reach compared to a consolidation of the heavily national regulation microcosms, thus the EC obviously opted for the egg as the clearance of several 4-to-3 merger suggests. Remedies imposed by the EC have been proven toothless so far. In Austria and Germany, prices for subscribers have uniformly risen following M&A deals. Going forward, consolidation is likely to remain a near to medium term ARPU support. The M&A train is picking up pace, with recent deals in the UK, France, Denmark and Norway leading the way. The window of opportunity for more deals is wide open, pushed trough the lenient credit environment, structural challenges of mobile operators, the favourable stance of EC regulators towards consolidation, some operators opting to sell non-core assets to regain financial flexibility and the ongoing fixed-mobile integration (in order to leverage fixed-line networks’s ability to carry fast rising data traffic generated by mobile users while offering customers convergence bundles that are highly successful in many European markets).

Four player markets likely to see in-market consolidation Prices for bundles already reached the trough in Europe

Source: Berenberg Research Source: European Commission, Berenberg Research

(ii) convergence offers: Besides fuelling the consolidation pipeline, the convergence trend in theory also offers the opportunity to improve market share, reduce churn rates and at least stabilise revenues. Convergence offers – packages bundling multiple services such as fixed and mobile telephony, broadband and television services – help to steer away customers from other providers, in particular if convergence provides value that is greater than the sum of its parts. Following the idea that discount isn’t the differentiator but rather unique, compelling services that can’t be easily replicated, convergence offers are expected to have a stabilising impact on ARPU. As an example, by applying the approach of “if you can’t beat them, join them”, thus partnering up and striking exclusive deals with OTT providers, telecoms can differentiate their service bundles.

(iii) supportive economic environment: BER questioned the defensive nature of the sector and found that telecoms became cyclical since the financial crisis. The sensitivity to the economy results from the exposure to cyclical factors such as travel (especially business travel is clearly cyclical and roaming for outside and coming into the EU is highly profitable) and B2B (businesses become savvier in optimising spend and less sensitive to who they buy services from). A regression based analysis of the relationship between real GDP growth and mobile service revenue growth ex-MTRs had an R² range between 30-60% as a result, depending on the time horizon chosen. Within the last two years, 1ppt of GDP growth implied 2ppt of service revenue growth. Although developments diverge

Consolidation pending

regulatory approvals

Not covered

3 MNOs

4 MNOs

40

50

60

70

80

90

100

2009 2011 2012 2013 2014

Mo

nth

ly p

rice o

f in

tern

et+

fix

ed

te

lep

ho

ny+

TV

by s

peed

(€)

8 - 12 Mbps 12 - 30 Mbps 30 - 100 Mbps

2015 is about to become the

year ARPU has seen its trough

The EC’s newfound openness to

consolidation has opened the

floodgates on in-market M&A

deals, reducing competition and

thus at least stabilising ARPU

Convergence offers providing

value that is greater than the

sum of its parts should

contribute to ARPU

stabilisation

As telecoms became cyclical, a

brightening economic outlook

should further support the

ARPU development

7/33 Joh. Berenberg, Gossler & Co. KG Sector Special European Telecoms – Vol. I

across markets, our economists forecasts notable macro improvements for the Eurozone in general, which should exert upward pressure on the ARPU development in 2015 and 2016.

Economic outlook brightens over almost entire Europe 2-year regression implies mobile has become cyclical

2012 2013 2014 2015e 2016e

Eurozone GDP -0.4 -0.4 0.9 1.3 1.9

Private consumption -1.4 -0.6 0.9 1.4 1.2

UK GDP 0.3 1.7 2.6 3.1 3.0

Private consumption 1.5 1.7 2.0 3.0 3.0

Germany GDP 0.9 0.2 1.6 1.8 2.3

Private consumption 0.7 0.9 1.3 1.9 1.7

France GDP 0.0 0.4 0.4 0.8 1.4

Private consumption -0.3 0.3 0.6 1.0 1.2

Italy GDP -2.6 -1.9 -0.4 0.3 1.1

Private consumption -4.1 -2.7 0.3 0.5 0.7

Source: Berenberg Economists, Berenberg Research Source: Berenberg Equity Research

(iv) data/speed growth: wireless voice and text revenues remain under heavy pressure as subscribers switch to data-and-voice bundles or use cheaper, unmetered, IP related voice and texting alternatives. This trend to data-centric business models and tiered pricing (by data buckets and/or speed) should translate into some further rises in data revenues, given increasing 4G coverage as well as widespread usage of smartphones and content-rich applications. BER found that on average, a 4G user chose larger data plans than a 3G users, and on average consumed 57% of the bundle vs 46% for the 3G user. With 4G penetration still relatively low in Europe, it should be a good near to medium term support for upselling data packages. We are confident that 4G is driving a genuine increase in data usage, however, not translating into respective ARPU improvements. Regressions conducted by BER for the last two years showed a positive, albeit weak, relationship between 4G and service revenue growth ex-MTR – with each incremental 10ppt take up of 4G implying only a 1ppt benefit to revenue growth. The sector promotes higher data bundles at almost no premium as a retention tool to stabilise prices and fight competitors. We thus expect at least a stabilising effect on ARPU, similar to the upward gearing trend on the fixed-line/cable side. The rollout of fibre and DOCSIS3.0 technology enables users to a broadband speed experience for which 60% would pay a premium for (Accenture survey 04/14).

In over 30 regressions BER carried out, by far the most meaningful driver of mobile service

revenue growth was GDP growth. Based on a brightening economic forecast of our

economists, we expect at least stabilising ARPU in 2015. Despite showing a weaker

relationship to revenue growth, we also expect data growth, consolidation and convergence

offers to contribute to this trend in mobile ARPU as well as support fixed-line/cable ARPU.

ARPU shifts in France as an example Convergence about to reach 50% penetration in Europe

Source: ARCEP, Berenberg Research Source: European Commission, Berenberg Research

i) NLR is net of uncapped cash/equivalents, meaning it can be

manipulated by injection of cash

ii) Relevant Credit Facilities baskets excluded from debt

numerators (whether initial RCF or any subsequent RCF or

term bank/bond debt)

iii) Pro Forma EBITDA denominator is last two quarters

multiplied by two, not on last four quarter basis.It includes add-

back for management fees etc. to Permitted Holders and

addback for any uncapped, anticipated cost savings/synergies

(including from general business optimisation programmes)

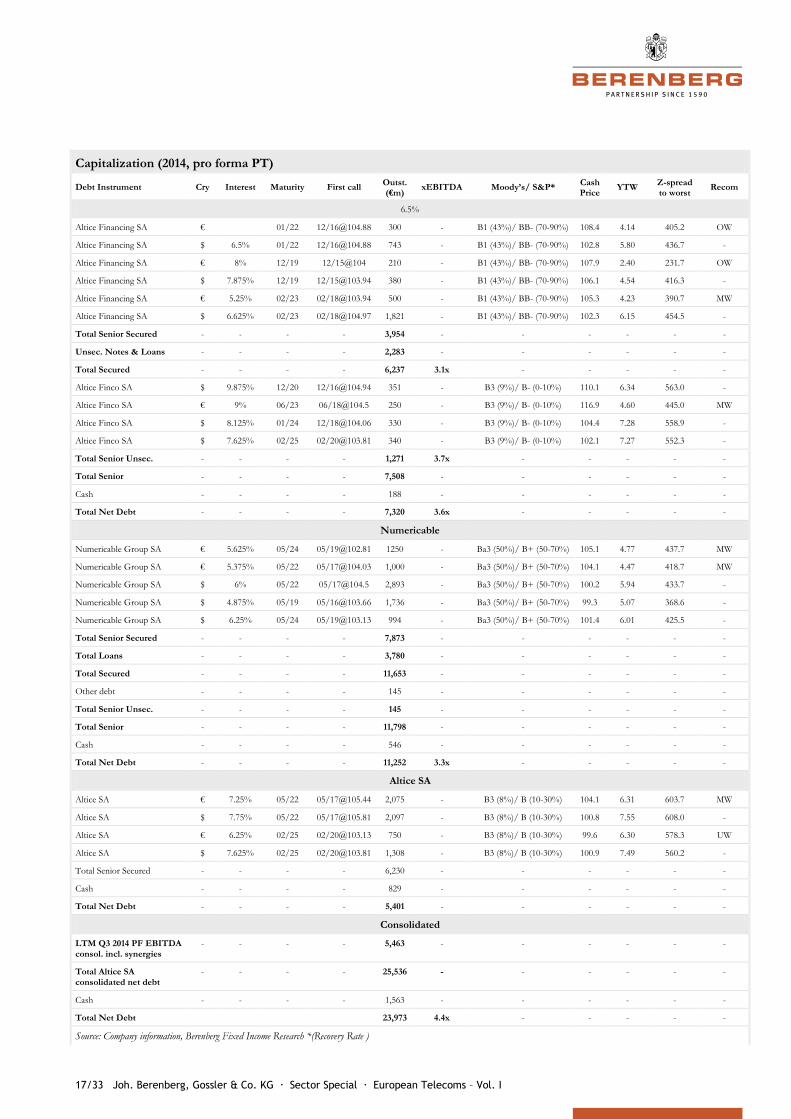

Altice SA 7 ¼ 05/22

Altice Financing 5 ¼ 02/23

Collateral enforcement/distressed disposals proceeds applied first to Super Priority debt

Unrestricted Subs (not regulated by any of the covenants) will be Altice Finco SA Green Datacenter and Auberimmo SAS. Investment in Altice Finco SA (can include loan or guarantee of its liabilities) can be made under JV/Unrestricted Subs basket up to greater of 3% Total Assets and €325mm. Such upstreaming could also occur under general €350mm/3% Total Assets basket, in addition Competition-law driven disposals will not trigger put (even if Rating Decline) and proceeds of such disposals may repay other (including pari debt) without pro rata offer to Noteholders.

Leverage Ratio and Senior Secured Leverage Ratio used in various contexts are net of uncapped cash/eq and numerator subject to some exclusions (including €1.5B/80% EBITDA Credit Facilities baskets in some places) and denominator subject to aggressive add-backs. Note ability for issuer/Guarantors to guarantee on subordinated basis Holdco [ie Altice Finco SA] debt subject to 4x CNLR (3.7x in OM - so immediate headroom). Guarantees of Holdco debt may also be given under contribution debt basket and €500mm/4% Total Assets general basket without CNLR test and without requirement that such guarantees be subordinated. As drafted such guaranteed Holdco debt may be but does not have to be downstreamed to Restricted Group (thus these could enable dividend recap/incurrence of debt by Altice Finco for other purposes than Restricted Group's business, but guaranteed by Restricted Group)

Altice Financing 8 12/19

The most important piece of Collateral appears to be the HOT Refinancing Note. This is how noteholders have a direct interest in the assets at HOT. However, some of the assets require regulatory approval before they are pledged and if regulatory approval is not obtained within 180 days, the interest rate will increase by 100 bps.

The RP covenant is flawed since it permits unlimited distributions if the 2.75x Leverage Ratio is met

Credit Facility debt will rank ahead of the notes. Since the Issuer is a financing vehicle, all debt it issues will be "secured" by a lien on the proceeds loan. Therefore, the ratio debt exception is tied to a 3x Secured Leverage Ratio. Covenant Parties and Restricted Subs can only incur debt under one of the Permitted Debt exceptions

Altice Financing 6 ½ 01/22

Super Priority Debt of €100mm/4% Total Assets plus certain hedging, which will be repaid from enforcement proceeds ahead of Notes. Super Priority hedging is extensive as it includes not just interest rate/fx hedging of financial debt but fx hedging of opex and capex. In addition to that Guarantees/ Collateral secure substantial amount of other existing debt as well as permitted future debt.

Altice Finco SA (the issuer of the $400mm senior notes to be issued contemporaneously) is

not a Restricted Subsidiary for the purpose of these (Senior Secured) Notes and is thus not bound by the covenants

Ratio Debt incurrence regulated by 3x Senior Secured Leverage Ratio - while leverage ratios typically used for telecoms issuers, note here it is senior secured leverage, not straight total leverage. In ratios, EBITDA is last 2 quarters x 2

Altice Finco 9 06/23

Guarantees will be given on a senior subordinated basis, being subordinated to a substantial amount of such Guarantors' senior debt. The negative pledge will permit a significant amount of debt to be secured either ahead of the Notes (via a first lien on the Collateral) or via pari passu lien on the Collateral. In each case, there could be a significant amount of collateral dilution

The RP covenant is permissive since it permits unlimited distributions if the 2.75x Leverage Ratio is met

Ratio debt incurrence is tied to a 3x Secured Leverage Ratio for the Senior Secured Notes Issuer and a 4x Leverage Ratio for the Issuer. Altice International and Restricted Subs can ONLY incur debt under one of the Permitted Debt exceptions

Numericable 5 3/8 05/22

Holders of the Notes will share in recovery from enforcement of the collateral on a pari passu basis with lenders of the Senior Credit Facility, Revolving Credit Facilities, counterparties to certain hedging obligations and the other series of Notes issued contemporaneously with these Notes.

Change of Control has portability as, to be triggered, put requires Rating Decline for so long as Vivendi owns at least 20% of Issuer. CNLR and CNSSLR tests (used in CoC, Liens, Indebtedness, Restricted Payments, Merger) are all on net basis, meaning they could be managed downwards by cash injection. In both, there are exclusions from debt numerator (large Credit Facilities basket, except for RP test) and CNSSLR numerator very narrowly drawn, making ratio easier to meet.

Summary of Intercreditor Agreement contemplates Super Priority Debt being incurred in future (comprising working capital facilities and hedging) repayable ahead of Notes from Collateral enforcement/disposalproceeds

Numericable 5 5/8 05/24

Sources: Xtract Research Reports, Berenberg Research. *Certain exemptions and further explanations may apply

19/33 Joh. Berenberg, Gossler & Co. KG Sector Special European Telecoms – Vol. I

marketing, network operations) and revenue synergies should

already come to effect from 2015 on. The SFR deal had a

clearly positive impact on Altice France’s business profile,

hence Moody’s placed its B1 rating on review for upgrade

following the announcement in April 2014. However, the new

number two operator in the French telecommunications

market has some clear obstacles to face in the current year: (i)

a still weakening operating performance of SFR with limited

growth prospects in a highly saturated market, (ii) ambitious

synergy targets are likely to absorb Numericable’s management

capacities for the coming years and (iii) additional investment

needs in the mobile network to remain competitive.

A combination with Bouygues Telecom might help ease the

competitive pressure and generate substantial synergies.

However, in spite of the ongoing damaging price war in the

French telecoms market and the resulting profit slide in 2014,

Bouygues Telecoms insists that it can survive alone.

We see a merger of both companies as a necessity for a market

repair in France. Even though convergence possibilities

emerging from the Numericable SFR consolidation should

further soften Altice France’s ARPU decline, further M&A

driven synergies on the opex and capex side would be

necessary to stabilise or even increase profit margins and

operating free cash flow.

Numericable-SFR is the second largest mobile operator

Number three in the French fixed-line market

Maintenance offers great capex savings potential

Sources: Company data, Berenberg Research

0%

10%

20%

30%

40%

50%

2011 2012 2013 2014

Numericable SFR

Orange 35.8%

Numericable-SFR 28.1%

Iliad 13.1%

Bouygues 11.5%

MVNO's 11.5%

Orange 42.7%

Numericable-SFR 21.5%

Iliad 25.3%

Bouygues 10.5%

Maintenance 51%

Customer Acquisition

21%

Network Upgrade 28%

€1,781m15.6% of total revenue

27/33 Joh. Berenberg, Gossler & Co. KG Sector Special European Telecoms – Vol. I

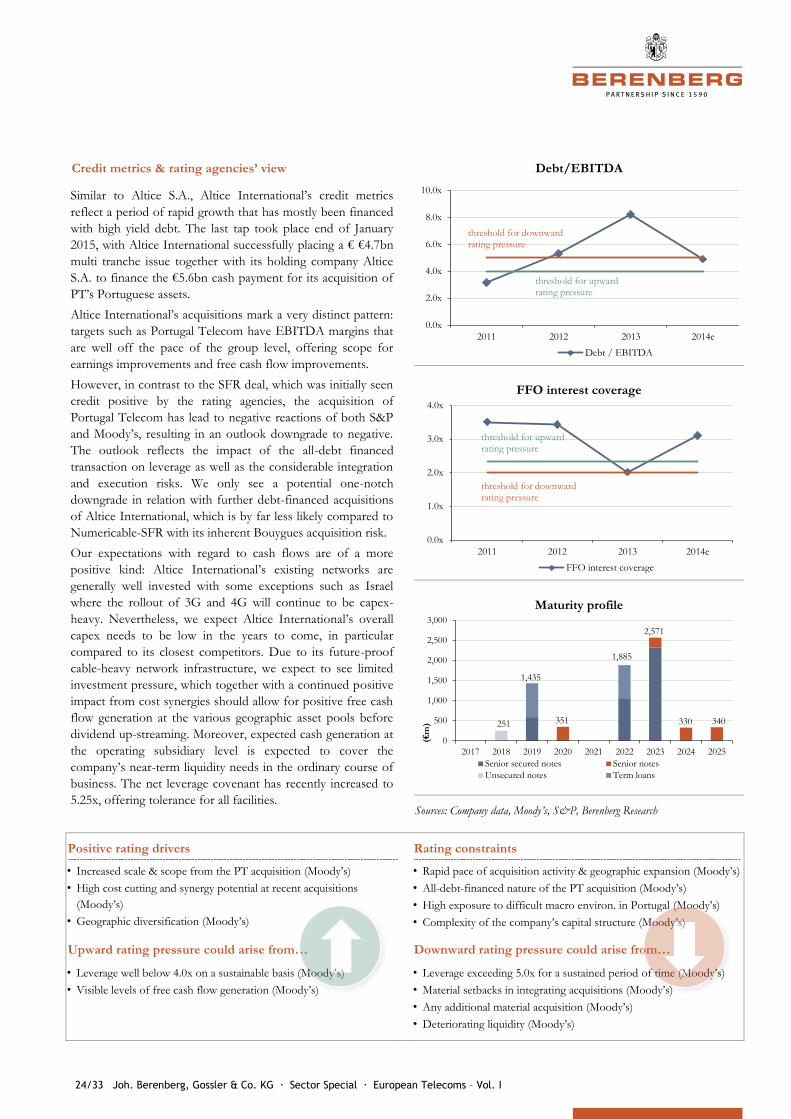

Credit metrics & rating agencies’ view

Debt/EBITDA

In April 2014, Numericable together with its TopCo Altice

S.A. issued the largest high yield bond on record, at $16.7bn,

to fund part of Numericable’s SFR acquisition. The SFR deal

left the new Numericable-SFR highly leveraged, which is

about to increase further as a consequence of the latest deal

approved in February 2015: Numericable-SFR together with

Altice S.A. acquires Vivendi’s remaining 20% stake in

Numericable-SFR. The €3.9bn purchase price will be split

equally. Nummericable-SFR’s intends to acquire its €1.95bn

stake through a share buyback programme, funded by

drawings on its RCFs and cash on its balance sheet. Altice

S.A.’s payment has to be made by April 2016 and is secured

through a bank guarantee.

Both rating agencies reacted by downgrading their outlook on

Numericable-SFR to negative. Moody’s even placed the

ratings under review for downgrade. The agency sees

significant uncertainties about the funding of the €1.95bn

share repurchase programme and its impact on Numericable-

SFR’s liquidity, leverage and operational flexibility. Both

agencies view the transaction as aggressive given the only

recently closed acquisition of SFR and the early stage of

integration. However, S&P overall expects the transaction to

have no significant impact on credit metrics as a planned

€750m earnout to Vivendi will be cancelled as part of the

transaction and most of excess cash was previously assumed

to be upstreamed as dividends to shareholders.

However, a large portion of the upcoming Numericable-SFR

free cash flow will be distributed to shareholders as the holdco

Altice S.A. needs to cover interest payments on €6.2bn of

holdco debt (including debt for the PT acquisition) at the

holdco level.

For 2015, S&P forecasts an adjusted debt/EBITDA slightly

above 4.0x for Numericable-SFR, still considerably lower than

the consolidated group average. However, the assumption

does not factor in any business combination with Bouygues

Telecom in the context of a consolidation of the French

mobile market, which Moody’s believes could occur over time.

FFO interest coverage

Maturity profile

Sources: Company data, Moody’s, S&P, Berenberg Research

Positive rating drivers Rating constraints

• SFR merger should lead to synergies from capex savings, opex

reductions and revenue synergies (Moody’s)

• Company’s significant leverage, also on the holdco level (Moody’s)

• Significant integration and execution risks (Moody’s)

• Exposure to a highly competitive and saturated market (Moody’s)

Upward rating pressure could arise from… Downward rating pressure could arise from…

• Leverage below 3.75x on an ongoing basis (Moody’s)

• Free cash flow/debt ratio greater than 10% (Moody’s)

• Success in broadly achieving synergy and cost savings targets

(Moody’s)

• Leverage exceeding 6.0x/5.5x (S&P/Moody’s)

• Missing turnaround of SFR’s EBITDA (S&P)

• No successful integration of newly acquired companies (S&P)

• Deteriorating liquidity (Moody’s)

0.0x

1.5x

3.0x

4.5x

6.0x

7.5x

2011 2012 2013 2014e

Debt / EBITDA

threshold for downwardrating pressure

threshold for upward rating pressure

0.0x

1.5x

3.0x

4.5x

6.0x

2011 2012 2013 2014e

FFO interest coverage

threshold for down-ward rating pressure

threshold for upward rating pressure

1,736

3,780 3,893

2,244

0

2,000

4,000

6,000

2018 2019 2020 2021 2022 2023 2024

(€m

)

Senior Secured Notes Loans

28/33 Joh. Berenberg, Gossler & Co. KG Sector Special European Telecoms – Vol. I

Please note that the use of this research report is subject to the conditions and restrictions set forth in the

“General investment-related disclosures” and the “Legal disclaimer” at the end of this document.

For analyst certification and remarks regarding foreign investors and country-specific disclosures, please

refer to the respective paragraph at the end of this document.

Disclosures in respect of section 34b of the German Securities Trading Act (Wertpapierhandelsgesetz – WpHG)

Company Disclosures

Altice S.A. no disclosures

Altice International S.a.r.l no disclosures

Numericable-SFR SAS no disclosures

(1) Joh. Berenberg, Gossler & Co. KG (hereinafter referred to as “the Bank”) or its affiliate(s) was Lead Manager or Co-Lead Manager over the previous 12 months of a public offering of this company.

(2) The Bank acts as Designated Sponsor for this company.

(3) Over the previous 12 months, the Bank and/or its affiliate(s) has effected an agreement with this company for

investment banking services or received compensation or a promise to pay from this company for investment

banking services.

(4) The Bank and/or its affiliate(s) holds 5 % or more of the share capital of this company.

(5) The Bank holds a trading position in shares of this company.

Initiation of coverage: 25 March 2015

Historical recommendation changes for ATCNA 7 1/4 05/22 in the last 12 months

Date Recommendation

25 March 2015 Overweight

Historical recommendation changes for ATCNA 6 1/4 02/25 in the last 12 months

Date Recommendation

25 March 2015 Marketweight

Historical recommendation changes for ALTICE 8 12/19 in the last 12 months

Date Recommendation

25 March 2015 Overweight

Historical recommendation changes for ALTICE 6 1/2 01/22 in the last 12 months

Date Recommendation

25 March 2015 Overweight

29/33 Joh. Berenberg, Gossler & Co. KG Sector Special European Telecoms – Vol. I

Historical recommendation changes for ALTICE 5 1/4 02/23 in the last 12 months

Date Recommendation

25 March 2015 Marketweight

Historical recommendation changes for ALTICE 9 06/23 in the last 12 months

Date Recommendation

25 March 2015 Marketweight

Historical recommendation changes for NUMFP 5 3/8 05/22 in the last 12 months

Date Recommendation

25 March 2015 Marketweight

Historical recommendation changes for NUMFP 5 5/8 05/24 in the last 12 months

Date Recommendation

25 March 2015 Marketweight

Berenberg distribution of recommendations and in proportion to investment banking services

Overweight 25.64 % 9.09 %

Underweight 26.50 % 18.18 %

Marketweight 47.86 % 72.73 %

Valuation basis / recommendation key

Overweight: Sustainable spread tightening potential higher 10% within 3-6 months.

Underweight: Sustainable spread widening potential lower 10% within 3-6 months.

Marketweight: Limited spread movement potential. No immediate catalyst visible.

NB The Bank’s Fixed Income Research Department does not make recommendations on the basis of

absolute performance, but on performance expected relative to the market or peer group as spreads move

with markets and sectors as well as with the issuer itself.

Competent supervisory authority

Bundesanstalt für Finanzdienstleistungsaufsicht -BaFin- (Federal Financial Supervisory Authority),

Graurheindorfer Straße 108, 53117 Bonn and Lurgiallee 12, 60439 Frankfurt am Main

General investment-related disclosures

Joh. Berenberg, Gossler & Co. KG (hereinafter referred to as „the Bank“) has made every effort to carefully research

all information contained in this financial analysis. The information on which the financial analysis is based has been

obtained from sources which we believe to be reliable such as, for example, Thomson Reuters, Bloomberg and the

relevant specialised press as well as the company which is the subject of this financial analysis.

30/33 Joh. Berenberg, Gossler & Co. KG Sector Special European Telecoms – Vol. I

Only that part of the research note is made available to the issuer (who is the subject of this analysis) which is

necessary to properly reconcile with the facts. Should this result in considerable changes a reference is made in the

research note.

Opinions expressed in this financial analysis are our current opinions as of the issuing date indicated on this

document. We do not commit ourselves in advance to whether and in which intervals an update is made. The

companies analysed by the Bank are divided into two groups: “full coverage“ - continued updates - and “screening

coverage“ - updates as and when required in irregular intervals.

The functional job title of the person/s responsible for the recommendations contained in this report is “Fixed-

Income Research Analyst” unless otherwise stated on the cover.

The following internet link provides further remarks on our financial analyses:

https://www.berenberg.de/en/fir_en.html

Legal disclaimer

This document has been prepared by Joh. Berenberg, Gossler & Co. KG (hereinafter referred to as „the Bank“). This

document does not claim completeness regarding all the information on the stocks, stock markets or developments

referred to in it.

On no account should the document be regarded as a substitute for the recipient procuring information for

himself/herself or exercising his/her own judgements.

The document has been produced for information purposes for institutional clients or market professionals.

Private customers, into whose possession this document comes, should discuss possible investment decisions with

their customer service officer as differing views and opinions may exist with regard to the stocks referred to in this

document.

This document is not a solicitation or an offer to buy or sell the mentioned stock.

The document may include certain descriptions, statements, estimates, and conclusions underlining potential market

and company development. These reflect assumptions, which may turn out to be incorrect. The Bank and/or its

employees accept no liability whatsoever for any direct or consequential loss or damages of any kind arising out of the

use of this document or any part of its content.

The Bank and/or its employees may hold, buy or sell positions in any securities mentioned in this document,

derivatives thereon or related financial products. The Bank and/or its employees may underwrite issues for any

securities mentioned in this document, derivatives thereon or related financial products or seek to perform capital

market or underwriting services.

Analyst certification

I, Alexandre Daniel, hereby certify that all of the views expressed in this report accurately reflect my personal views

about any and all of the subject securities or issuers discussed herein.

In addition, I hereby certify that no part of my compensation was, is, or will be, directly or indirectly related to the

specific recommendations or views expressed in this research report, nor is it tied to any specific investment banking

transaction performed by the Bank or its affiliates.

Remarks regarding foreign investors

The preparation of this document is subject to regulation by German law. The distribution of this document in other

jurisdictions may be restricted by law, and persons into whose possession this document comes should inform

themselves about, and observe, any such restrictions.