57

Flexible Benefits Plans Flexible Benefits Plans • Group #10 Group #10 Cecilia Martinez Cecilia Martinez Melissa Martin Melissa Martin Ravi Arman Ravi Arman Jas Sangha Jas Sangha

| Date post: | 23-Dec-2015 |

| Category: |

Documents |

| Upload: | edgar-wiggins |

| View: | 214 times |

| Download: | 0 times |

Flexible Benefits PlansFlexible Benefits Plans

• Group #10Group #10

Cecilia MartinezCecilia Martinez

Melissa MartinMelissa Martin

Ravi ArmanRavi Arman

Jas SanghaJas Sangha

Flexible BenefitsFlexible Benefits

• Central idea is to let employees Central idea is to let employees choose among cash or nontaxable choose among cash or nontaxable benefits provided by their employers benefits provided by their employers

• To maximize the cost-effectiveness of To maximize the cost-effectiveness of the plan sponsor’s expenditures for all the plan sponsor’s expenditures for all employee benefits it is important to employee benefits it is important to incorporate work and family issues. incorporate work and family issues.

Why offer Benefits plans?Why offer Benefits plans?

• Many employers have Many employers have implemented flexible implemented flexible benefit plans to benefit plans to respond to their respond to their workers’ deferring workers’ deferring needsneeds

• Competitive advantageCompetitive advantage

• Retain existing staff Retain existing staff

Flexible Benefits Effects on Flexible Benefits Effects on EmployeesEmployees

• Employee OwnershipEmployee Ownership

• Employee AppreciationEmployee Appreciation

• BudgetsBudgets

• ParticipationParticipation

Employee OwnershipEmployee Ownership

• Basic prerequisite for success.Basic prerequisite for success.

• Important for employees to feel Important for employees to feel sense of ownership.sense of ownership.

• Acceptance, understanding, and Acceptance, understanding, and usage will be enhanced.usage will be enhanced.

Employee AppreciationEmployee Appreciation

• Plan sponsors feel employees will be Plan sponsors feel employees will be more appreciative if given a choice.more appreciative if given a choice.

• Employees’ reactions are favorable Employees’ reactions are favorable to flex benefits programs.to flex benefits programs.

BudgetsBudgets

• Flex benefits help solve budget Flex benefits help solve budget problems.problems.

• The plan sponsor can set specific The plan sponsor can set specific dollar amounts as the plan credits for dollar amounts as the plan credits for a given year.a given year.

ParticipationParticipation

• All participants must be employees.All participants must be employees.

• Spouses and beneficiaries may Spouses and beneficiaries may receive benefits due to employees’ receive benefits due to employees’ participation.participation.

Cost and SavingsCost and Savings

• Flex programs will involve Flex programs will involve employees in benefit costs.employees in benefit costs.

• Optional benefits can create Optional benefits can create costly adverse selection.costly adverse selection.

• Flexible spending accounts if Flexible spending accounts if not designed properly can not designed properly can increase costs.increase costs.

• Redesigning certain Redesigning certain programs can create programs can create significant administrative significant administrative savings.savings.

Overall Purpose of Flex Benefit Overall Purpose of Flex Benefit ProgramsPrograms

• Improve compensation effectiveness.Improve compensation effectiveness.

• Increase perceived value.Increase perceived value.

• Contain costs.Contain costs.

• Manage compensation more effectively.Manage compensation more effectively.

The Process of Developing a The Process of Developing a Flexible Benefits ProgramFlexible Benefits Program

• Examination of all benefits and Examination of all benefits and compensation issues.compensation issues.

• Maximizing savings.Maximizing savings.

• Communicating the program.Communicating the program.

• Compliance with regulatory issues.Compliance with regulatory issues.

• Plan implementation must be Plan implementation must be accompanied by administrative accompanied by administrative system.system.

Issues Addressed in Issues Addressed in Effective Flex ProgramsEffective Flex Programs• Issues for both activities and retireesIssues for both activities and retirees

• Eligibility Eligibility

• Communication/EducationCommunication/Education

• Paid time off ( Sick Leave, Holidays, Paid time off ( Sick Leave, Holidays, Vacation)Vacation)

• Define benefitsDefine benefits

• Define contributionDefine contribution

• Salary compensationSalary compensation

Reasons for PopularityReasons for Popularity

• Historically, plans have been more Historically, plans have been more uniform, and had few choices.uniform, and had few choices.

• Radical changes in the work Radical changes in the work environment have led to:environment have led to:– More individualized plans.More individualized plans.– Greater degree of choices.Greater degree of choices.

The Changing WorkforceThe Changing Workforce

• The major reason plan sponsors The major reason plan sponsors implement flex programs is to meet the implement flex programs is to meet the need of the changing workforce.need of the changing workforce.

• The need to address the diversity in the The need to address the diversity in the workforce. workforce.

• Family compensation has also dramatically Family compensation has also dramatically changed. changed.

• Rising levels of education also affect the Rising levels of education also affect the motivation for flex programs.motivation for flex programs.

• Plan sponsors face competition for their Plan sponsors face competition for their customers and their staff.customers and their staff.

Present Demographic of Present Demographic of Family Composition in the Family Composition in the U.S. IsU.S. Is• Married-both Married-both

spouses spouses work, 45%.work, 45%.

• Single-head Single-head of household-of household-no no dependent, dependent, 25%.25%.

• Married-Married-husband husband works, wife works, wife does not, does not, 20%.20%.

• Single-head Single-head of household-of household-with with dependents, dependents, 10%.10%.

US Age Composition of Adult Population

0

5

10

15

20

25

30

1950 1970 1990 2000

Year

Pe

rce

nt

of

Ad

ult

P

op

ula

tio

n16-2425-3435-4445-5455-6465 & Over

Other Types of Flexible Other Types of Flexible Benefit Plans Include:Benefit Plans Include:

• Flexible Spending AccountsFlexible Spending Accounts

• Job SharingJob Sharing

• Section 125Section 125

• Cafeteria AccountsCafeteria Accounts

Flexible Spending Accounts Flexible Spending Accounts (FSA) (FSA) • Generic term for reimbursement accounts.Generic term for reimbursement accounts.

• Allows employees to be reimbursed on a pretax Allows employees to be reimbursed on a pretax basis for out-of-pocket health care and dependant basis for out-of-pocket health care and dependant care expenditures.care expenditures.

• Two types of spending accounts:Two types of spending accounts:– Health care spending account; for your family Health care spending account; for your family

health care costs which are not covered by health care costs which are not covered by insurance.insurance.

– Dependant day care spending account; for Dependant day care spending account; for eligible expenses incurred for dependant daycare eligible expenses incurred for dependant daycare while you are at work.while you are at work.

Health FSAHealth FSA

• Allows employees to be reimbursed Allows employees to be reimbursed for eligible health care expenses.for eligible health care expenses.– Ex: insurance deductibles, co-Ex: insurance deductibles, co-

payments, dental work, eye payments, dental work, eye glasses etc.glasses etc.

• Employees elect at the beginning of Employees elect at the beginning of the plan year how much they wish to the plan year how much they wish to have withheld on a pre-tax basis have withheld on a pre-tax basis each pay period.each pay period.

Health FSA ContinuedHealth FSA Continued

•Amounts set aside which are not Amounts set aside which are not used can NOT be rolled over.used can NOT be rolled over.

•City may establish a maximum City may establish a maximum contribution amount to limit risk, contribution amount to limit risk, since IRS does not provide it.since IRS does not provide it.

•Health FSA’s may be subject to Health FSA’s may be subject to federal requirements such as federal requirements such as COBRA.COBRA.

Dependant Care Assistance Dependant Care Assistance Plan (DCAP)Plan (DCAP)• EE reimbursed up to max of EE reimbursed up to max of

$5000 per year.$5000 per year.

• EE cannot be reimbursed through EE cannot be reimbursed through a flex plan and then claim child-a flex plan and then claim child-care credit on their tax return.care credit on their tax return.

• Health FSA’s and DCAP’s fall Health FSA’s and DCAP’s fall under different section of the IRS under different section of the IRS tax code.tax code.

How FSA’s WorkHow FSA’s Work

• Deduction from paycheck set asideDeduction from paycheck set aside

• When expense incurred file claim for When expense incurred file claim for reimbursement (tax free)reimbursement (tax free)

• Help reduce participants taxesHelp reduce participants taxes

• Risk incurred if funds not usedRisk incurred if funds not used

• Funds don’t rollover to next yearFunds don’t rollover to next year

• Account can ONLY be made within 31 Account can ONLY be made within 31 days of divorce, or the birth of the childdays of divorce, or the birth of the child

Which Expenses Are Which Expenses Are Reimbursed Under FSA?Reimbursed Under FSA?• Fee’s paid to doctors, dentists, surgeons, Fee’s paid to doctors, dentists, surgeons,

chiropractors, etc…chiropractors, etc…• Fee’s for hospital servicesFee’s for hospital services• Acupuncture treatmentsAcupuncture treatments• Inpatient treatmentInpatient treatment• Dentures, hearing aids, crutches, wheelchairsDentures, hearing aids, crutches, wheelchairs• DeductiblesDeductibles• BracesBraces• Prescription drugsPrescription drugs• NON-elective cosmetic surgeryNON-elective cosmetic surgery

What is the Advantage of Before-Tax What is the Advantage of Before-Tax Dollars?Dollars?

• Let’s assume you are the sole wage Let’s assume you are the sole wage earner in your family and will earn earner in your family and will earn $25,000 next year. You expect to $25,000 next year. You expect to spend $2000 for your child’s spend $2000 for your child’s orthodontic work. The following orthodontic work. The following illustrates how a health FSA actually illustrates how a health FSA actually increases your spendable income. The increases your spendable income. The table assumes a married filer with 3 table assumes a married filer with 3 dependants.dependants.

With a Health Care With a Health Care AccountAccount

Without a Health Without a Health Care AccountCare Account

Base SalaryBase Salary $25,000$25,000 $25,000$25,000

Health Care AccountHealth Care Account $2,000$2,000 $0$0

Gross IncomeGross Income $23,000$23,000 $25,000$25,000

Less Federal Income Less Federal Income TaxTax

$755$755 $955$955

Less Social Security Less Social Security TaxTax

$1,760$1,760 $1,913$1,913

Less State Income Less State Income TaxTax

$510$510 $570$570

After Tax IncomeAfter Tax Income $19,975$19,975 $21,562$21,562

Less Heath Care Less Heath Care Expenses Yet to be Expenses Yet to be

PaidPaid

$0$0 $2,000$2,000

Spendable IncomeSpendable Income $19,975$19,975 $19,562$19,562

Flex PricingFlex Pricing

• Now let’s look at an actual example Now let’s look at an actual example of pricing multiple health plans. We of pricing multiple health plans. We will start by using three distinct will start by using three distinct integrated steps in pricing flexible integrated steps in pricing flexible benefit programs.benefit programs.

• Step 1. Project the costs of the Step 1. Project the costs of the current benefit programs to the first current benefit programs to the first flex pricing year.flex pricing year.

• Step 2. Conduct an analysis of the Step 2. Conduct an analysis of the relative actuarial values of the options relative actuarial values of the options to be offered in the flex program.to be offered in the flex program.

• Step 3. Calculate the impact selection Step 3. Calculate the impact selection will have on overall costs, the will have on overall costs, the construction of the plan costs, and construction of the plan costs, and prices that reflect selection costs.prices that reflect selection costs.

Step 1. Projection of Current Step 1. Projection of Current Costs.Costs.

• The first step is the analysis of costs The first step is the analysis of costs to the flex pricing year.to the flex pricing year.

• By looking at the number of claims By looking at the number of claims submitted per employee per month, submitted per employee per month, an analysis can be made.an analysis can be made.

Step 1. ContinuedStep 1. Continued

• Graph 4 shows the Graph 4 shows the change in utilization change in utilization over time. The graph over time. The graph shows the number of shows the number of claims per employee claims per employee over the last 30 over the last 30 months. months.

• Time series analysis is Time series analysis is applied to the 12 applied to the 12 month rolling average month rolling average to produce a projection to produce a projection of expected future use of expected future use of the medical program.of the medical program.

Step 1. ContinuedStep 1. Continued

• Graph 5 shows the Graph 5 shows the impact on price impact on price inflation on the inflation on the medical program over medical program over time. It represents time. It represents the average size claim the average size claim pad in a month.pad in a month.

• Graph 6 shows a Graph 6 shows a synthesis of these two synthesis of these two projections and the projections and the overall future costs.overall future costs.

Step 2. Relative ValuesStep 2. Relative Values

• The first step is The first step is developing a model developing a model of employee of employee distribution of distribution of claims by size. claims by size.

• Graph 7 shows the Graph 7 shows the distribution of distribution of percentage of percentage of employees with employees with various sizes of various sizes of claims.claims.

Step 2. ContinuedStep 2. Continued

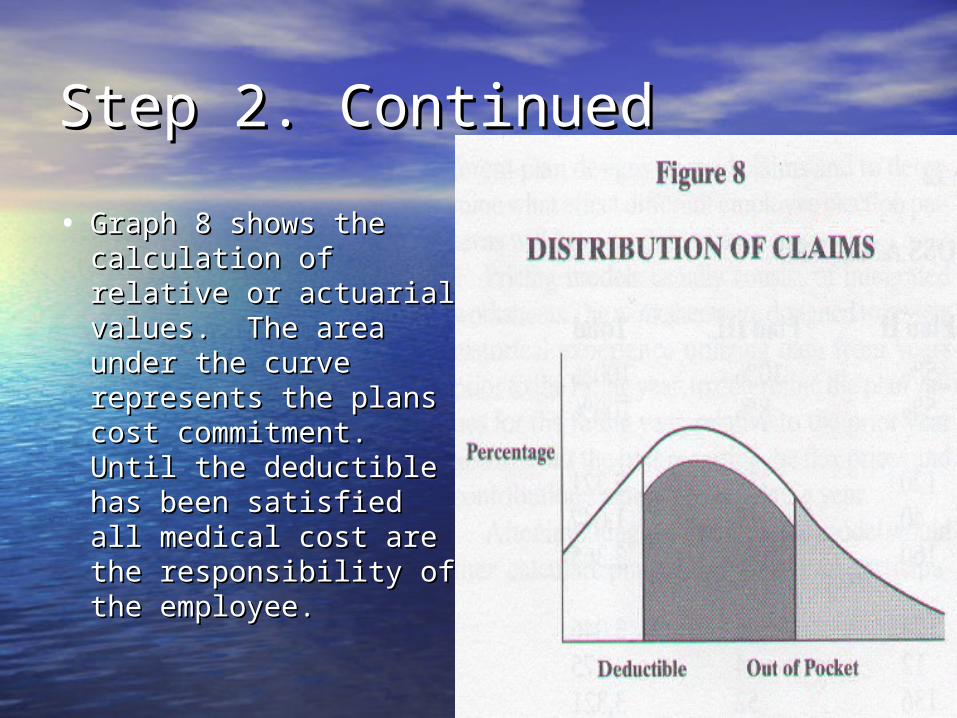

• Graph 8 shows the Graph 8 shows the calculation of relative or calculation of relative or actuarial values. The actuarial values. The area under the curve area under the curve represents the plans represents the plans cost commitment. Until cost commitment. Until the deductible has been the deductible has been satisfied all medical cost satisfied all medical cost are the responsibility of are the responsibility of the employee. the employee.

Step 3. Cost SelectionStep 3. Cost Selection

• The final step in the flex pricing process is The final step in the flex pricing process is determining the impact of selection of the determining the impact of selection of the program. The original distribution of claims program. The original distribution of claims model is used again rebuilding the distribution model is used again rebuilding the distribution for various segments of the employee for various segments of the employee population.population.

Step 3. ContinuedStep 3. Continued

• Figure 10 represents the Figure 10 represents the distribution of claims for distribution of claims for an overall population. an overall population. Rebuilding this graph for Rebuilding this graph for 10% of the population 10% of the population will cause a shift to the will cause a shift to the left, since this segment of left, since this segment of the typical employee the typical employee population has fewer and population has fewer and less severe claims then less severe claims then the overall population.the overall population.

Step 3. ContinuedStep 3. Continued

• Figure 10 shows the Figure 10 shows the claims for 10% of the claims for 10% of the employee population. employee population. Compared to figure 11 Compared to figure 11 which has shifted to which has shifted to the right because the the right because the least healthy 10% least healthy 10% tends to have both tends to have both more claims and more more claims and more severe claims than the severe claims than the overall population.overall population.

Step 3. ContinuedStep 3. Continued

• To analyze the impact of selection on To analyze the impact of selection on plan costs, build a distribution of claims plan costs, build a distribution of claims model for the healthiest to leas healthy model for the healthiest to leas healthy of the employee population.of the employee population.

• Then with initial enrollment assumptions Then with initial enrollment assumptions you can make the determination of over you can make the determination of over plan costs, including the impact f a plan costs, including the impact f a flexible benefits program.flexible benefits program.

Step 3. ContinuedStep 3. Continued

• Cost projections Cost projections and price tags can and price tags can be finalized based be finalized based on enrollment on enrollment results or feed results or feed back from focus back from focus groups and groups and survey’s show in survey’s show in figure 12.figure 12.

Job SharingJob Sharing

• Two people share the same position in Two people share the same position in a company, each working part of the a company, each working part of the week. week.

• They split the hours, pay, holidays and They split the hours, pay, holidays and benefits between them according to benefits between them according to hours they each work.hours they each work.

Job SharingJob Sharing

• Key necessities:Key necessities:– CompatibilityCompatibility– Co-operationCo-operation– CommunicationCommunication

Sharing Tasks and Sharing Tasks and ResponsibilitiesResponsibilities

• Differentiate between major and Differentiate between major and minor responsibilities.minor responsibilities.

• Identify the type of experience Identify the type of experience required for the position.required for the position.

• Divide responsibilities.Divide responsibilities.

• Learn from each other.Learn from each other.

Three Main Types of Job Three Main Types of Job Share:Share:

• Shared ResponsibilityShared Responsibility

• Divided ResponsibilityDivided Responsibility

• Unrelated ResponsibilityUnrelated Responsibility

Job Sharing Fact’sJob Sharing Fact’s

• In 1997, 89% out of 1,777,000 In 1997, 89% out of 1,777,000 employees sharing jobs were women.employees sharing jobs were women.

• 77% of Women returned to their jobs 77% of Women returned to their jobs after maternity leave. Up 7% from after maternity leave. Up 7% from 1988.1988.

Advantage/Disadvantage of Job Advantage/Disadvantage of Job ShareShare

• Lets you share the responsibilities Lets you share the responsibilities with a co-workerwith a co-worker

• Drawback is that since you will be Drawback is that since you will be working part-time your income will working part-time your income will be reduced and you may lose out on be reduced and you may lose out on promotions in the future.promotions in the future.

Cafeteria Plans??Cafeteria Plans??

• What is a Section 125 Cafeteria Plan?What is a Section 125 Cafeteria Plan?It is a plan designed and setup by the Internal Revenue It is a plan designed and setup by the Internal Revenue Service to allow participants to have money taken out of Service to allow participants to have money taken out of their paychecks pre-tax for group health insurance their paychecks pre-tax for group health insurance premiums, unreimbursed medical expenses, and child care premiums, unreimbursed medical expenses, and child care expenses.expenses.

• What is the maximum that I can claim for the year What is the maximum that I can claim for the year for Section 125?for Section 125? For the Medical Reimbursement of the Section 125 plan it For the Medical Reimbursement of the Section 125 plan it depends on your company's plan document. You should depends on your company's plan document. You should have been given a copy of the Summary Plan Description have been given a copy of the Summary Plan Description when you became eligible for the plan. As for dependent when you became eligible for the plan. As for dependent Care Reimbursement the IRS annual maximum is $5,000.00 Care Reimbursement the IRS annual maximum is $5,000.00 per household.per household.

Cafeteria Plans cont.Cafeteria Plans cont.

• What happens when I terminate What happens when I terminate employment?employment? To claim any money in the Section 125 To claim any money in the Section 125 account after you terminate you can account after you terminate you can only submit receipts for services that only submit receipts for services that were done before your date of were done before your date of termination. All other expenses will not termination. All other expenses will not be allowed, unless you elect COBRA.be allowed, unless you elect COBRA.

Claims you may not be allowed Claims you may not be allowed to make?to make?• Can I claim getting my teeth bleached?Can I claim getting my teeth bleached?

No, teeth bleaching or whitening is classified as a cosmetic procedure.No, teeth bleaching or whitening is classified as a cosmetic procedure.

• When I get my varicose or spider veins stripped can I claim that When I get my varicose or spider veins stripped can I claim that procedure?procedure?No, stripping of the veins unless medically necessary, is considered to be a No, stripping of the veins unless medically necessary, is considered to be a cosmetic procedure.cosmetic procedure.

• I went to my Optometrist in 1999, but picked up and paid for my I went to my Optometrist in 1999, but picked up and paid for my glasses in January of 2000. Can I claim this expense in the 2000 glasses in January of 2000. Can I claim this expense in the 2000 plan year?plan year?No, the IRS regulations specify that expenses that are reimbursed must No, the IRS regulations specify that expenses that are reimbursed must have been incurred during the period for which the participant is actually have been incurred during the period for which the participant is actually covered under the plan for that specified plan year. covered under the plan for that specified plan year.

• I am taking treatments for infertility, such as prescription fertility I am taking treatments for infertility, such as prescription fertility drugs and artificial insemination. Are these claimable?drugs and artificial insemination. Are these claimable?Yes, But only when administered by a licensed physician.Yes, But only when administered by a licensed physician.

Claims cont.Claims cont.

• I am currently undergoing Birthing Classes, are I am currently undergoing Birthing Classes, are those expenses claimable under un-reimbursed those expenses claimable under un-reimbursed medical expenses? medical expenses? Yes, birthing classes are eligible, but only expenses for the Yes, birthing classes are eligible, but only expenses for the mother can be claimed. mother can be claimed.

• Are dietary supplements claimable?Are dietary supplements claimable?Not unless your doctor is willing to write a prescription for Not unless your doctor is willing to write a prescription for them or submit a letter stating that they are a medical them or submit a letter stating that they are a medical necessitynecessity

• I go to a message therapist can I claim these visits?I go to a message therapist can I claim these visits?Yes, recently message therapy has been added as an Yes, recently message therapy has been added as an eligible form of therapy to be reimbursed under Section 125 eligible form of therapy to be reimbursed under Section 125

Submitting the ReceiptsSubmitting the Receipts

• How do I get a claim form to How do I get a claim form to submit my receipts?submit my receipts?There are three ways that you can get There are three ways that you can get our claim forms:our claim forms:– you can get them from your Human you can get them from your Human

Resources Department Resources Department – you can get them off this website under you can get them off this website under

forms forms – you can contact our office either by you can contact our office either by

phone, email, or fax phone, email, or fax

Other Types of Flexible Other Types of Flexible PlansPlans• Medical Savings Account (MSA)Medical Savings Account (MSA)= =

is Tax-exempt trusts or accounts allowing is Tax-exempt trusts or accounts allowing individuals to pay certain medical expenses individuals to pay certain medical expenses that are not reimbursed under a health plan that are not reimbursed under a health plan with pr-tax contributions with pr-tax contributions

• Health Reimbursement Health Reimbursement Arrangements (HRAs)=Arrangements (HRAs)= is a strictly is a strictly employer funded plan that reimburses employer funded plan that reimburses employees for certain medical expenses employees for certain medical expenses incurred by the employee and the employees incurred by the employee and the employees spouse or dependentspouse or dependent

FundingFunding

• Flexible benefit plans can be funded Flexible benefit plans can be funded by employer & employee by employer & employee contributions or bothcontributions or both

• The salary reduction that employees The salary reduction that employees agreed to pay before taxes is agreed to pay before taxes is frequently used to fund health care frequently used to fund health care and dependent care spending and dependent care spending accounts. accounts.

Benefits Of Implementing a Benefits Of Implementing a Flex PlanFlex Plan

• Help Manage Benefit costs.Help Manage Benefit costs.

• Pay less in taxes.Pay less in taxes.

• Offer employees new or expand benefits.Offer employees new or expand benefits.

• Respond to the need of a diverse work Respond to the need of a diverse work force.force.

Problems Facing the Health Problems Facing the Health Care SystemCare System• Few employees understand the cost their Few employees understand the cost their

companies spend for health care servicescompanies spend for health care services

• Plan sponsors and providers have not Plan sponsors and providers have not done a good job of educating employees done a good job of educating employees about various health care optionsabout various health care options

• Doctors and hospitals are geared to Doctors and hospitals are geared to respond to crises with all available respond to crises with all available resources.resources.

Disadvantages to Flexible Disadvantages to Flexible Benefit PlansBenefit Plans• Employees might not understand Employees might not understand

or have a difficulty in choosing or have a difficulty in choosing their needed benefitstheir needed benefits

• Flexible plans might result in Flexible plans might result in increased utilization and Adverse increased utilization and Adverse SelectionSelection

• Health care spending accounts Health care spending accounts that provide uniform coverage that provide uniform coverage throughout the plan year could throughout the plan year could expose an employer to additional expose an employer to additional liability liability

• Greater benefit flexibility can Greater benefit flexibility can result in a greater administrative result in a greater administrative complexity and costs to the complexity and costs to the company or firmcompany or firm

Solutions to Disadvantages:Solutions to Disadvantages:

• Careful PlanningCareful Planning

• Incorporate a program that will assure basic Incorporate a program that will assure basic protection and also an effective communication protection and also an effective communication programprogram

• Plan features can be added to minimize adverse Plan features can be added to minimize adverse selectionselection

• Define lower annual maximums or limiting midyear Define lower annual maximums or limiting midyear changes can minimize the exposure of the employer changes can minimize the exposure of the employer

liabilityliability • Restriction limit to the amount of flexibility benefits Restriction limit to the amount of flexibility benefits

can be controlledcan be controlled

Advantages to Flexible Advantages to Flexible Benefit:Benefit:• Employees can always change their benefits Employees can always change their benefits

as life fluctuates.as life fluctuates.• Employees can start to appreciate more their Employees can start to appreciate more their

benefits and therefore increases or improves benefits and therefore increases or improves their morale and productivity.their morale and productivity.

• Employees can be more involved in Employees can be more involved in controlling or balancing their benefit costs controlling or balancing their benefit costs

• Flexible compensation plans can be used to Flexible compensation plans can be used to convert workers income into Tax-Free convert workers income into Tax-Free Employee Benefits. Employee Benefits.

Impact on CostImpact on Cost

• Flexible benefit plans help reduce Flexible benefit plans help reduce their benefit costs and their overall their benefit costs and their overall expenditures for health coverage and expenditures for health coverage and other benefit programsother benefit programs

• Under flex plans employees have Under flex plans employees have more control over employer more control over employer contributionscontributions

Any Questions?Any Questions?