54

Chapter 7 - Chapter 7 - V aluation and V aluation and Characteristics of Bonds Characteristics of Bonds 2005, Pearson Prentice Hall

| Date post: | 26-Feb-2018 |

| Category: |

Documents |

| Upload: | jawadzaheer |

| View: | 224 times |

| Download: | 0 times |

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 1/54

Chapter 7 -Chapter 7 - Valuation andValuation andCharacteristics of BondsCharacteristics of Bonds

2005, Pearson Prentice Hall

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 2/54

Characteristics of Bonds

•Bonds pay fixed coupon (interest)payments at fixed intervals (usually

every six months) and pay the parvalue at maturity.

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 3/54

Characteristics of Bonds

•Bonds pay fixed coupon (interest)payments at fixed intervals (usually

every six months) and pay the parvalue at maturity.

00 1 1 2 . . .2 . . . nn

$I $I $I $I $I $I+$$I $I $I $I $I $I+$

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 4/54

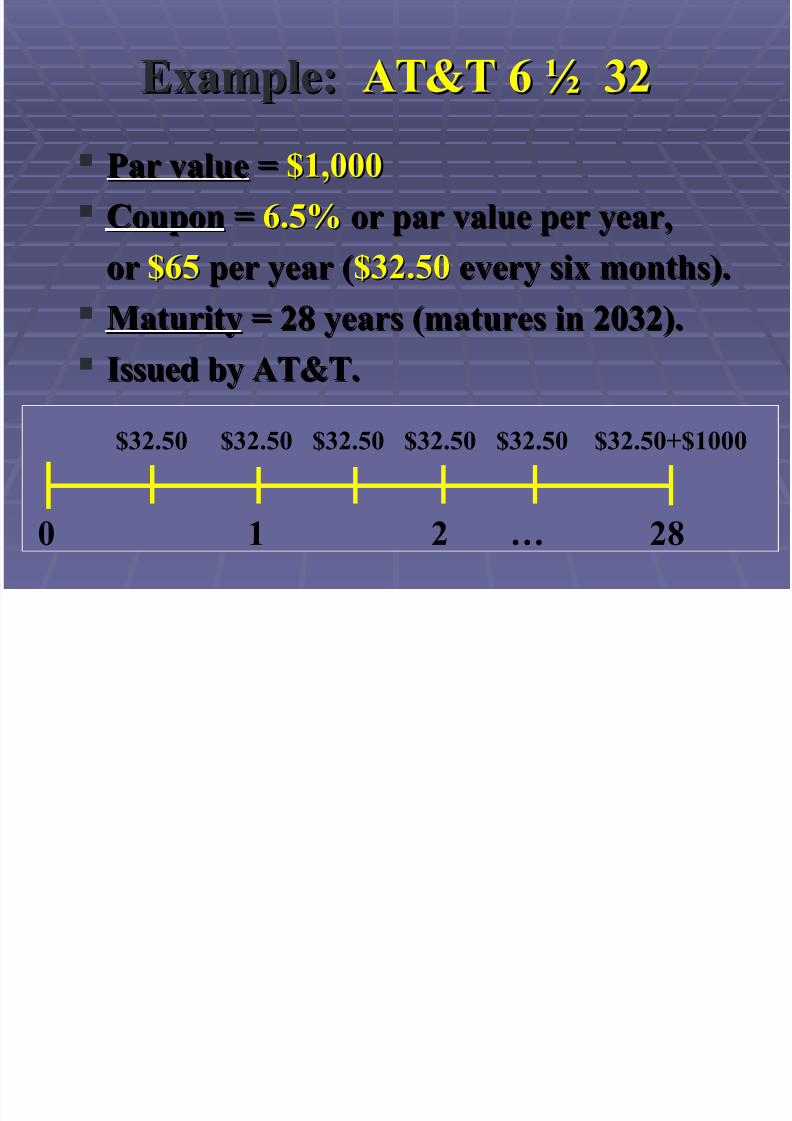

!xample"!xample" #% & ' 2#% & ' 2

ar valuear value ** $1000$1000

CouponCou

pon ** &.,-&.,- or par value per yearor par value per year

oror $&,$&, per year (per year ($2.,0$2.,0 every six months).every six months). aturityatur

ity * 2 years (matures in 202).* 2 years (matures in 202).

Issued /y #%.Issued /y #%.

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 5/54

!xample"!xample" #% & ' 2#% & ' 2

ar valuear value ** $1000$1000

CouponCou

pon ** &.,-&.,- or par value per yearor par value per year

oror $&,$&, per year (per year ($2.,0$2.,0 every six months).every six months). aturityatur

ity * 2 years (matures in 202).* 2 years (matures in 202).

Issued /y #%.Issued /y #%.

0 1 2 2

$2.,0 $2.,0 $2.,0 $2.,0 $2.,0 $2.,0+$1000

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 6/54

ypes of Bondsypes of Bonds

e/enturese/entures unsecured /onds. unsecured /onds.

3u/ordinated de/entures3u/ordinated de/entures unsecured unsecured

45unior6 de/t.45unior6 de/t.

ort7a7e /ondsor

t7a7e /onds secured /onds. secured /onds.

8eros8eros /onds that pay only par value at /onds that pay only par value at

maturity9 no coupons.maturity9 no coupons.

:un; /onds:un; /onds speculative or /elo< speculative or /elo<

investment 7rade /onds9 rated BB andinvestment 7rade /onds9 rated BB and

/elo<. =i7hyield /onds./elo<. =i7hyield /onds.

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 7/54

ypes of Bondsypes of Bonds

!uro/onds!uro/onds /onds denominated in /onds denominated inone currency and sold in anotherone currency and sold in another

country. (Borro<in7 overseas.)country. (Borro<in7 overseas.)

exampleexample suppose isney decides to sellsuppose isney decides to sell

$1000 /onds in >rance. hese are ?.3.$1000 /onds in >rance. hese are ?.3.

denominated /onds tradin7 in a forei7ndenominated /onds tradin7 in a forei7n

country. @hy do thisAcountry. @hy do thisA

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 8/54

ypes of Bondsypes of Bonds

!uro/onds!uro/onds /onds denominated in /onds denominated inone currency and sold in anotherone currency and sold in another

country. (Borro<in7 overseas.)country. (Borro<in7 overseas.)

exampleexample suppose isney decides to sellsuppose isney decides to sell

$1000 /onds in >rance. hese are ?.3.$1000 /onds in >rance. hese are ?.3.

denominated /onds tradin7 in a forei7ndenominated /onds tradin7 in a forei7n

country. @hy do thisAcountry. @hy do thisA

If /orro<in7 rates are lo<er in >rance.If /orro<in7 rates are lo<er in >rance.

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 9/54

ypes of Bondsypes of Bonds

!uro/onds!uro/onds /onds denominated in /onds denominated inone currency and sold in anotherone currency and sold in another

country. (Borro<in7 overseas).country. (Borro<in7 overseas).

exampleexample suppose isney decides to sellsuppose isney decides to sell$1000 /onds in >rance. hese are ?.3.$1000 /onds in >rance. hese are ?.3.

denominated /onds tradin7 in a forei7ndenominated /onds tradin7 in a forei7n

country. @hy do thisAcountry. @hy do thisA

If /orro<in7 rates are lo<er in >rance.If /orro<in7 rates are lo<er in >rance.

o avoid 3!C re7ulations.o avoid 3!C re7ulations.

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 10/54

he Bond Indenturehe Bond Indenture

hehe /ond contract/ond contract /et<een the firm/et<een the firm

and the trustee representin7 theand the trustee representin7 the

/ondholders./ondholders. ists all of the /onds features"ists all of the /onds features"

coupon par value maturitycoupon par value maturity etc.etc.

istsists restrictive provisionsrestrictive provisions <hich are<hich are

desi7ned to protect /ondholders.desi7ned to protect /ondholders.

escri/es repayment provisions.escri/es repayment provisions.

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 11/54

DalueDalue

Boo; value"Boo; value" value of an asset as sho<n onvalue of an asset as sho<n on

a firms /alance sheet9 historical cost.a firms /alance sheet9 historical cost.

iEuidation value"iEuidation value" amount that could /eamount that could /e

received if an asset <ere sold individually.received if an asset <ere sold individually.

ar;et value"ar;et value" o/served value of an asseto/served value of an asset

in the mar;etplace9 determined /y supplyin the mar;etplace9 determined /y supply

and demand.and demand.

Intrinsic value"Intrinsic value" economic or fair value ofeconomic or fair value of

an asset9 the present value of the assetsan asset9 the present value of the assets

expected future cash flo<s.expected future cash flo<s.

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 12/54

3ecurity Daluation3ecurity Daluation

In 7eneral theIn 7eneral the intrinsic valueintrinsic value of anof an

asset * theasset * the present valuepresent value of the streamof the stream

of expected cash flo<s discounted atof expected cash flo<s discounted at

an appropriatean appropriate reEuired rate ofreEuired rate of

returnreturn..

Can theCan the intrinsic valueintrinsic value of an assetof an asset

differ from itsdiffer from its mar;et valuemar;et valueAA

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 13/54

DaluationDaluation

CCtt * cash flo< to /e received at time* cash flo< to /e received at time t t ..

; ; * the investors reEuired rate of return.* the investors reEuired rate of return.

DD * the intrinsic value of the asset.* the intrinsic value of the asset.

D *D * t * 1t * 1

nn

$Ct

(1 + ;)t

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 14/54

Bond DaluationBond Daluation

iscount the /onds cash flo<s atiscount the /onds cash flo<s at

the investors reEuired rate ofthe investors reEuired rate of

return.return.

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 15/54

Bond DaluationBond Daluation

iscount the /onds cash flo<s atiscount the /onds cash flo<s at

the investors reEuired rate ofthe investors reEuired rate of

return.return. hehe coupon payment streamcoupon payment stream (an(an

annuity).annuity).

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 16/54

Bond DaluationBond Daluation

iscount the /onds cash flo<s atiscount the /onds cash flo<s at

the investors reEuired rate ofthe investors reEuired rate of

return.return. hehe coupon payment streamcoupon payment stream (an(an

annuity).annuity).

hehe par value paymentpar value payment (a sin7le(a sin7le

sum).sum).

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 17/54

Bond DaluationBond Daluation

D/ * $It (DI># ; / n) + $ (DI> ; / n)

$It $

(1 + ; /)t (1 + ; /)n

DD// * +* +

nn

t * 1t * 1

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 18/54

Bond !xampleBond !xample

3uppose our firm decides to issue3uppose our firm decides to issue 20year20year

/onds <ith a par value of/onds <ith a par value of $1000$1000 andand

annual coupon payments. he return onannual coupon payments. he return onother corporate /onds of similar ris; isother corporate /onds of similar ris; is

currently 12- so <e decide to offer acurrently 12- so <e decide to offer a 12-12-

couponcoupon interest rate.interest rate.

@hat <ould /e a fair price for these@hat <ould /e a fair price for these

/ondsA/ondsA

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 19/54

0 1 2 . . . 20

1000

120 120 120 . . . 120

FGH * 1

* 20

I-GH * 12>D * 1000

* 120

3olve D * $1000

Note Note:: If theIf the coupon ratecoupon rate ** discountdiscount

raterate the /ond <ill sell for the /ond <ill sell for par valuepar value..

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 20/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

D * 120 (DI>#D * 120 (DI># .12+ 20.12+ 20 ) + 1000 (DI>) + 1000 (DI> .12+ 20.12+ 20 ))

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 21/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

D * 120 (DI>#D * 120 (DI># .12+ 20.12+ 20 ) + 1000 (DI>) + 1000 (DI> .12+ 20.12+ 20 ))

11

D * 1 (1 + i)D * 1 (1 + i)nn + >D F (1 + i) + >D F (1 + i)nn

ii

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 22/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

D * 120 (DI>#D * 120 (DI># .12+ 20.12+ 20 ) + 1000 (DI>) + 1000 (DI> .12+ 20.12+ 20 ))

11

D * 1 (1 + i)D * 1 (1 + i)nn + >D F (1 + i) + >D F (1 + i)nn

ii

11

D * 120 1 (1.12 )D * 120 1 (1.12 )2020 + + 1000F (1.12)1000F (1.12) 2020 ** $1000$1000

.12.12

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 23/54

3uppose3uppose interest rates fallinterest rates fall

immediately after <e issue theimmediately after <e issue the/onds. he reEuired return on/onds. he reEuired return on

/onds of similar ris; drops to/onds of similar ris; drops to 10-10-..

@hat <ould happen to the /onds@hat <ould happen to the /onds

intrinsic valueAintrinsic valueA

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 24/54

FGH *FGH * 11

ode *ode * endend

* * 2020

I-GH *I-GH * 1010

* * 120120

>D *>D * 10001000

3olve D *3olve D * $11J0.2J$11J0.2J

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 25/54

FGH *FGH * 11

ode *ode * endend

* * 2020

I-GH *I-GH * 1010

* * 120120

>D *>D * 10001000

3olve D *3olve D * $11J0.2J$11J0.2J

Note: If the coupon rate K discount rate

the /ond <ill sell for a premium.

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 26/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

D * 120 (DI>#D * 120 (DI># .10+ 20.10+ 20 ) + 1000 (DI>) + 1000 (DI> .10+ 20.10+ 20 ))

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 27/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

D * 120 (DI>#D * 120 (DI># .10+ 20.10+ 20 ) + 1000 (DI>) + 1000 (DI> .10+ 20.10+ 20 ))

11

D * 1 (1 + i)D * 1 (1 + i)nn + >D F (1 + i) + >D F (1 + i)nn

ii

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 28/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

D * 120 (DI>#D * 120 (DI># .10+ 20.10+ 20 ) + 1000 (DI>) + 1000 (DI> .10+ 20.10+ 20 ))

11

D * 1 (1 + i)D * 1 (1 + i)nn + >D F (1 + i) + >D F (1 + i)nn

ii

11

D * 120 1 (1.10 )D * 120 1 (1.10 )2020 + 1000F (1.10)+ 1000F (1.10) 2020 ** $11J0.2J$11J0.2J

.10.10

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 29/54

3uppose3uppose interest rates riseinterest rates rise

immediately after <e issue theimmediately after <e issue the

/onds. he reEuired return on/onds. he reEuired return on

/onds of similar ris; rises to/onds of similar ris; rises to 1L-1L-..

@hat <ould happen to the /onds@hat <ould happen to the /onds

intrinsic valueAintrinsic valueA

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 30/54

FGH *FGH * 11

ode *ode * endend

* * 2020

I-GH *I-GH * 1L1L

* * 120120

>D *>D * 10001000

3olve D *3olve D * $&J.,L$&J.,L

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 31/54

FGH *FGH * 11

ode *ode * endend

* * 2020

I-GH *I-GH * 1L1L

* * 120120

>D *>D * 10001000

3olve D * 3olve D * $&J.,L$&J.,L

Note: If the coupon rate M discount ratethe /ond <ill sell for a discount.

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 32/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

D * 120 (DI>#D * 120 (DI># .1L+ 20.1L+ 20 ) + 1000 (DI>) + 1000 (DI> .1L+ 20.1L+ 20 ))

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 33/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

D * 120 (DI>#D * 120 (DI># .1L+ 20.1L+ 20 ) + 1000 (DI>) + 1000 (DI> .1L+ 20.1L+ 20 ))

11

D * 1 (1 + i)D * 1 (1 + i)nn + >D F (1 + i) + >D F (1 + i)nn

ii

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 34/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

D * 120 (DI>#D * 120 (DI># .1L+ 20.1L+ 20 ) + 1000 (DI>) + 1000 (DI> .1L+ 20.1L+ 20 ))

11

D * 1 (1 + i)D * 1 (1 + i)nn + >D F (1 + i) + >D F (1 + i)nn

ii

11

D * 120 1 (1.1L )D * 120 1 (1.1L )2020 + 1000F (1.1L)+ 1000F (1.1L) 2020 ** $&J.,L$&J.,L

.1L.1L

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 35/54

3uppose coupons are semiannual3uppose coupons are semiannual

FGH *FGH * 22

ode *ode * endend

* * L0L0

I-GH *I-GH * 1L1L

* * &0&0

>D *>D * 10001000

3olve D * 3olve D * $&&.&$&&.&

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 36/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

D * &0 (DI>#D * &0 (DI># .1L+ 20.1L+ 20 ) + 1000 (DI>) + 1000 (DI> .1L+ 20.1L+ 20 ))

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 37/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

D * &0 (DI>#D * &0 (DI># .1L+ 20.1L+ 20 ) + 1000 (DI>) + 1000 (DI> .1L+ 20.1L+ 20 ))

11

D * 1 (1 + i)D * 1 (1 + i)nn + >D F (1 + i) + >D F (1 + i)nn

ii

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 38/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

D * &0 (DI>#D * &0 (DI># .1L+ 20.1L+ 20 ) + 1000 (DI>) + 1000 (DI> .1L+ 20.1L+ 20 ))

11

D * 1 (1 + i)D * 1 (1 + i)nn + >D F (1 + i) + >D F (1 + i)nn

ii

11

D * &0 1 (1.0J )D * &0 1 (1.0J )L0L0 + 1000 F (1.0J)+ 1000 F (1.0J) L0L0 ** $&&.&$&&.&

.0J.0J

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 39/54

Gield o aturityGield o aturity

hehe expected rate of returnexpected rate of return on aon a

/ond./ond.

he rate of return investors earn on ahe rate of return investors earn on a/ond if they hold it to maturity./ond if they hold it to maturity.

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 40/54

Gield o aturityGield o aturity

hehe expected rate of returnexpected rate of return on aon a

/ond./ond.

he rate of return investors earn on ahe rate of return investors earn on a/ond if they hold it to maturity./ond if they hold it to maturity.

$It $

(1 + ; /)t (1 + ; /)

n

00 * +* +nn

t * 1t * 1

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 41/54

G !xampleG !xample

3uppose <e paid3uppose <e paid $N.N0$N.N0 for afor a

$1000$1000 parpar 10-10- coupon /ondcoupon /ond

<ith years to maturity and<ith years to maturity andsemiannual coupon payments.semiannual coupon payments.

@hat is our@hat is our yield to maturityyield to maturityAA

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 42/54

FGH * 2FGH * 2

ode * endode * end

* 1& * 1&D * N.N0D * N.N0

* ,0 * ,0

>D * 1000>D * 1000

3olve I-GH *3olve I-GH * 12-12-

G !xample

B d ! l

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 43/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

N.N0 * ,0 (DI>#N.N0 * ,0 (DI># ;+ 1&;+ 1& ) + 1000 (DI>) + 1000 (DI> ;+ 1&;+ 1& ))

B d ! l

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 44/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

N.N0 * ,0 (DI>#N.N0 * ,0 (DI># ;+ 1&;+ 1& ) + 1000 (DI>) + 1000 (DI> ;+ 1&;+ 1& ))

11

D * 1 (1 + i)D * 1 (1 + i)nn + >D F (1 + i) + >D F (1 + i)nn

ii

B d ! lB d ! l

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 45/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ;+ n;+ n ) + >D (DI>) + >D (DI> ;+ n;+ n ))

N.N0 * ,0 (DI>#N.N0 * ,0 (DI># ;+ 1&;+ 1& ) + 1000 (DI>) + 1000 (DI> ;+ 1&;+ 1& ))

11

D * 1 (1 + i)D * 1 (1 + i)nn + >D F (1 + i) + >D F (1 + i)nn

ii

11

N.N0 * ,0 1 (1 +N.N0 * ,0 1 (1 + ii ))1&1& + + 1000 F (1 +1000 F (1 + ii)) 1&1&

ii

B d ! lB d ! l

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 46/54

Bond !xampleBond !xample

Mathematical Solution: Mathematical Solution:

D * (DI>#D * (DI># ; n; n ) + >D (DI>) + >D (DI> ; n; n ))

N.N0 * ,0 (DI>#N.N0 * ,0 (DI># ; 1&; 1& ) + 1000 (DI>) + 1000 (DI> ; 1&; 1& ))

11

D * 1 (1 + i)D * 1 (1 + i)nn + >D F (1 + i) + >D F (1 + i)nn

ii

11

N.N0 * ,0 1 (1 +N.N0 * ,0 1 (1 + ii ))1&1& + + 1000 F (1 +1000 F (1 + ii)) 1&1&

ii solve using trial and error solve using trial and error

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 47/54

8ero Coupon Bonds8ero Coupon Bonds

o coupon interest payments.o coupon interest payments.

he /ond holders return ishe /ond holders return is

determined entirely /y thedetermined entirely /y the

price discountprice discount..

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 48/54

8ero !xample8ero !xample

3uppose you pay3uppose you pay $,0$,0 for a Oerofor a Oero

coupon /ond that hascoupon /ond that has 10 years10 years

left to maturity.left to maturity. @hat is your@hat is your yield to maturityyield to maturityAA

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 49/54

8ero !xample8ero !xample

3uppose you pay3uppose you pay $,0$,0 for a Oerofor a Oero

coupon /ond that hascoupon /ond that has 10 years10 years

left to maturity.left to maturity. @hat is your@hat is your yield to maturityyield to maturityAA

0 100 10

$,0 $1000$,0 $1000

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 50/54

8ero !xample8ero !xample

FGH * 1FGH * 1

ode * !ndode * !nd

* 10 * 10

D * ,0D * ,0

>D * 1000>D * 1000

3olve" I-GH *3olve" I-GH * J-J-

8ero !xample8ero !xample

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 51/54

Mathematical Solution: Mathematical Solution:

D * >D (DI>D * >D (DI> i ni n ))

,0 * 1000 (DI>,0 * 1000 (DI> i 10i 10 )).,0 * (DI>.,0 * (DI> i 10i 10 )) [use PVIF table][use PVIF table]

D * >D F(1 + i)D * >D F(1 + i) 1010

,0 * 1000 F(1 + i),0 * 1000 F(1 + i)1010

1.N&, *1.N&, * (1 + i)(1 + i)1010

i *i * J-J-

8ero !xample8ero !xample

0 10

D * ,0 >D * 1000

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 52/54

he >inancial a7es"he >inancial a7es" Corporate BondsCorporate Bonds

CurCur et etGld Dol Close Ch7Gld Dol Close Ch7

olaroid 11olaroid 11 11FF22 0& 1N. N, ,N0& 1N. N, ,N FFLL ... ...

@hat is the yield to maturity for this /ondA@hat is the yield to maturity for this /ondA

FGH *FGH * 22 * * 1010 >D * >D * 10001000

D *D * $,NJ.,0$,NJ.,0

* ,J.,0 * ,J.,0

3olve" IFGH * 2&.L-3olve" IFGH * 2&.L-

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 53/54

he >inancial a7es"he >inancial a7es" Corporate BondsCorporate Bonds

CurCur et etGld Dol Close Ch7Gld Dol Close Ch7

=e<l;d Or 1J ... 20 ,1=e<l;d Or 1J ... 20 ,1 11FF22 +1 +1

@hat is the yield to maturity for this /ondA@hat is the yield to maturity for this /ondA

FGH *FGH * 11 * 1& >D * * 1& >D * 10001000

D *D * $,1,$,1,

* * 00

3olve" IFGH * L.2L-3olve" IFGH * L.2L-

7/25/2019 FM10e_ch07

http://slidepdf.com/reader/full/fm10ech07 54/54

he >inancial a7es"he >inancial a7es" reasury Bondsreasury Bonds

aturityaturity #s; #s;

Hate oFGrHate oFGr Bid #s;edBid #s;ed Ch7Ch7 GldGld

NN ov 1 ov 1 1N"1L 1N"20 L1N"1L 1N"20 L ,.L& ,.L&

@hat is the yield to maturity for this@hat is the yield to maturity for this

reasury /ondA (assume , half years)reasury /ondA (assume , half years)

FGH *FGH * 22 * , >D * * , >D * 10001000

* * L,L,

D *D * 1N&.2, 1N&.2, (1N.&2,- of par) (1N.&2,- of par)