23

FMCGs in Vietnam All images within this document are examples for illustrative purposes.

FMCGs in Vietnam

All images within this document are examples for illustrative purposes.

2Source: GSO Vietnam

FAST-MOVING CONSUMER GOODS (FMCGS)

OR CONSUMER PACKAGED GOODS (CPGS) ARE

PRODUCTS THAT ARE SOLD QUICKLY AND (GENERALLY)

AT A RELATIVELY LOW COST.

3

KEY ECONOMIC INDICATORS : VIETNAM LOOKING GOOD

FOR GROWTH

Q1 2017 vs. YA

Source: GSO Vietnam

CPI

4.09

0.63

2.663.53 3.54

GDP

5.98

6.68

6.21

6.817.08

Retail Sales of Consumer Goods

11.39.5 10.2 10.9

12.4

4

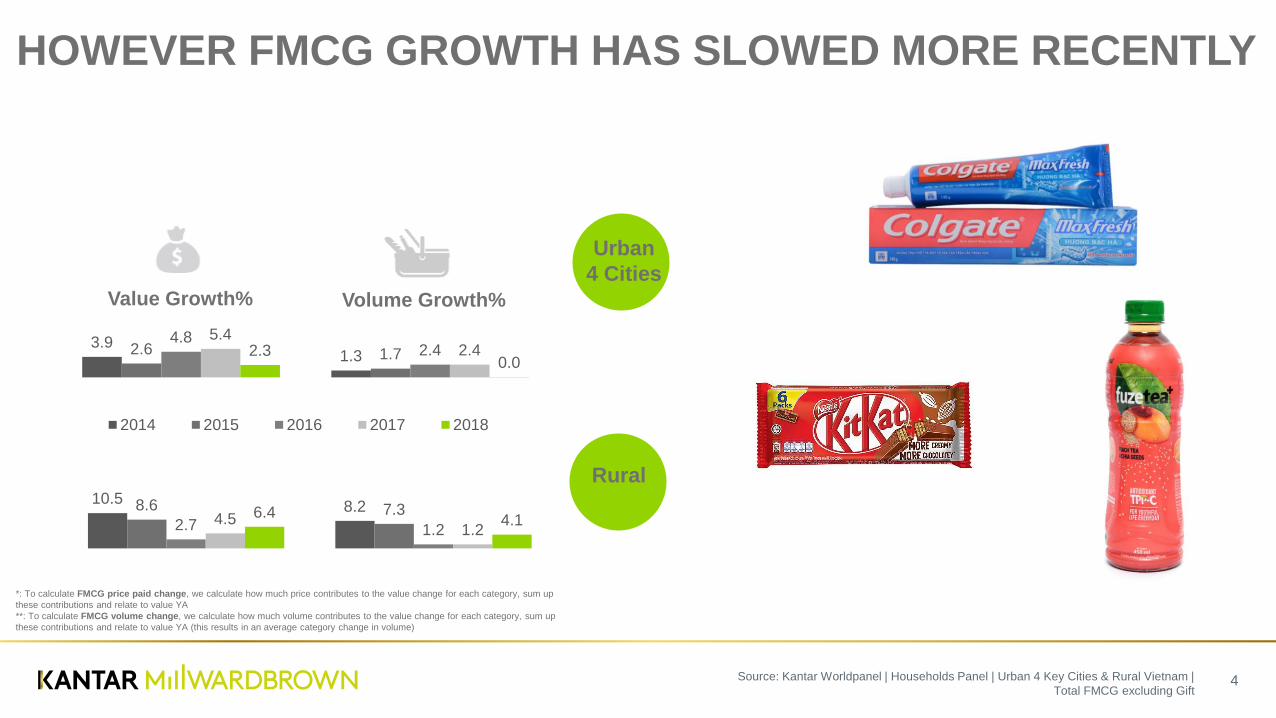

HOWEVER FMCG GROWTH HAS SLOWED MORE RECENTLY

Urban

4 Cities

Rural

Value Growth% Volume Growth%

*: To calculate FMCG price paid change, we calculate how much price contributes to the value change for each category, sum up

these contributions and relate to value YA

**: To calculate FMCG volume change, we calculate how much volume contributes to the value change for each category, sum up

these contributions and relate to value YA (this results in an average category change in volume)

Source: Kantar Worldpanel | Households Panel | Urban 4 Key Cities & Rural Vietnam |

Total FMCG excluding Gift

10.58.28.6 7.3

2.7 1.24.5

1.26.4

4.1

3.91.32.6 1.7

4.82.4

5.42.42.3

0.0

2014 2015 2016 2017 2018

5

FAST GROWTHSLOW GROWTH GROWTH H1’18 vs YA

Agriculture

3.9% GDP 7.1%Industry

9.1%

Services

6.9%

HRC

9.6%

Retail

10.7%

FMCG

+0.0%Phones*

9.4%

Big Appliances*

17.1%

Pharmaceuticals*

10.0%

Motorbikes*

4.8%

Consumer

Electronics*

14.7%

Small

Appliances*

8.2%

Tourism

19.5%

Telecom

7.1%

DESPITE THE POSITIVE ECONOMIC ENVIRONMENT, CONSUMERS ARE SPENDING

LESS FOR FMCGS, AND MORE FOR A FOR LIFESTYLE UPGRADATION

Source: Vietnam GSO Social and Economic Situation in H1’18, Vietnam Association of Motorbike Manufacturers FY 2017 (http://vietnamnews.vn/economy/421098/sale-

of-motorcycles-up-in-2017-vamm.html#bwI7WEpraq4DLhJC.97), GfK TEMAX results for Vietnam, FY 2017; http://english.vietnamnet.vn/fms/business/192807/vietnam-

s-pharmaceutical-sector-expected-higher-growth.html; Nielsen RA ending Jun’18;

• FMCG brands need to invest in the right innovations to spur

growth by addressing better the new changing lifestyles

RAPID URBANIZATION AND RISING MIDDLE CLASS

6

(*) Urbanization: increasing the densities of people and production in cities and towns

Source: Vietnam 2035 report – World Bank, Vietnam Ministry of planning Investment

Vietnam’s urbanization(*) was

faster than the global rate.

50% of population will belong to

Global middle class by 2035

• Premiumization trends

• Rising demand for Health & Wellness products and services

FURTHER IMPACTING FMCG CONSUMPTION IS INCREASED AWARENESS OF

FOOD SAFETY AND HEALTH AND WELLNESS

7

The Vietnamese government imposition of a special consumption tax (SCT) for sugary drinks

will be placed on carbonated and non-carbonated soft drinks, energy drinks, sports drinks and

bottled instant coffee and tea. Vietnam's Ministry of Finance (MoF) announced its plans at a

press conference in mid-August 2017 to apply a 10% or 20% tax that will take effect from

2019.

Source: Asia Pacific Journal of Clinical Nutrition – Non-communicable diseases, food and

nutrition in Vietnam from 1975 to 2015: the burden and national response

• Opportunity to develop better-for-me products • Promote good related health functions (i.e. anti pollution)

-0.7%

3.9%0.7%

6.3% 5.8%

-2.6%

1.2%

-1.0%

2.1%4.9%

8

DAIRY AND PACKAGED FOODS STAGNANT

DAIRY BEVERAGES PACKAGED FOODS PERSONAL CARE HOME CARE

7.9% 8.1%

3.9%

9.0%

2.8%6.6%

3.6% 3.7% 4.4%0.8%

URBAN 4 CITIES

RURAL

Value change%

Volume* change%

2018 versus year ago

*: To calculate FMCG volume change, we calculate how much volume contributes to the value change for each category, sum up these contributions and relate to value YA (this results in an average category change in volume)

Source: Kantar Worldpanel | Households Panel | Urban 4 Key Cities & Rural Vietnam | Total FMCG excluding Gift

Source: Vietnam Retailer Sentiment Q2’16

FOOD SAFETY HAS IMPACT BEVERAGES IN PARTICULAR

Extensive marketing campaigns employed

and to regain consumers' trust.

10

CONSUMERS NOW INCREASINGLY LOOKING TO

NATURAL INGREDIENTS

11

AGEING POPULATION WILL IMPACT FMCGS INCREASINGLY TARGETING AN

OLDER AGE BAND

32% 27% 24% 23% 23% 22%

10%11%

10% 7% 7% 7%

26%27%

27%27% 25% 21%

18% 20%21%

21%22%

23%

7% 9% 12% 14% 16% 17%

6% 7% 7% 7% 8% 10%

2000 2005 2010 2015 2020 2025

0-14 15-19 20-34 35-49 50-64 65+

❑ Vietnam – Total population and % by age group

2000 - 2025 CAGR

Total 1.0

0-14 -0.4

15-19 -0.6

20-34 0.2

35-49 1.9

50-64 4.3

65+ 2.8

80,286 84,309 88,473 93,572 98,360 102,764

Vietnam population (‘000 people)

Gen Y

and Z

❑ Vietnam – Population CAGR 2000 - 2025

Source: United Nations, WUP, 2014

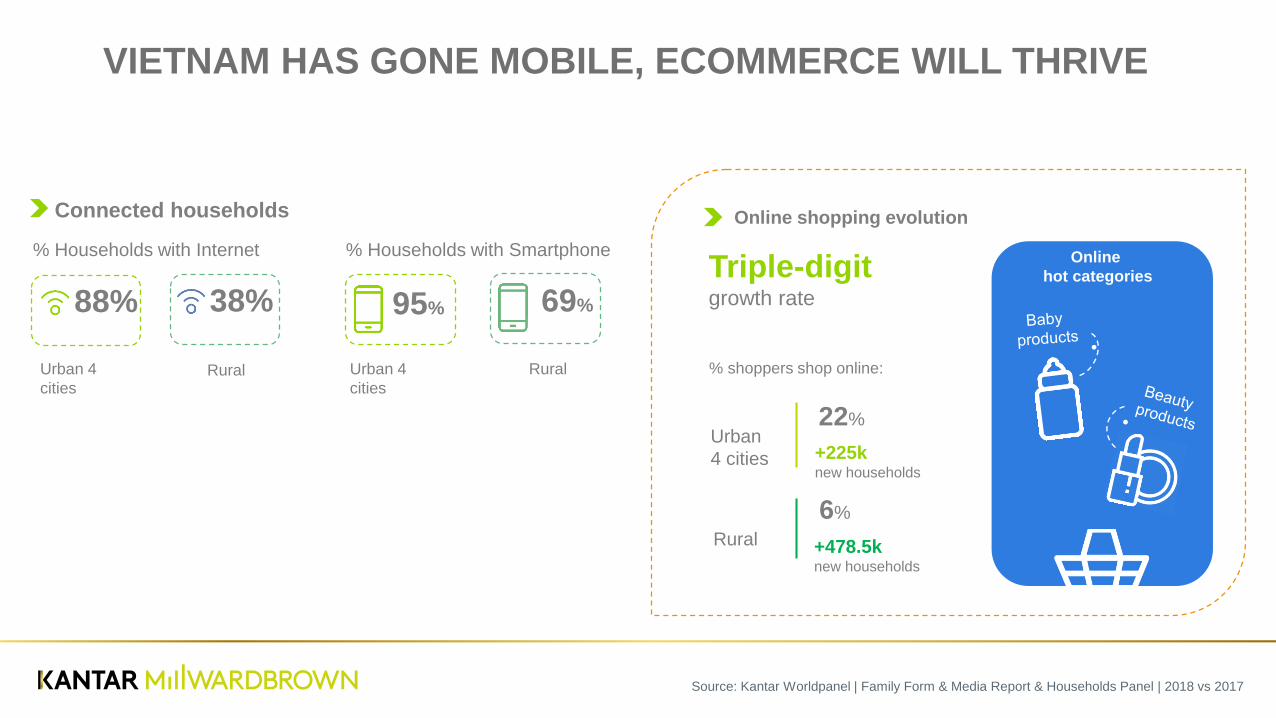

Connected households

% Households with Internet % Households with Smartphone

69%95%88% 38%

Urban 4

cities

Urban 4

citiesRural Rural

Online shopping evolution

Triple-digitgrowth rate

% shoppers shop online:

Online

hot categories

Urban

4 cities

Rural

22%

+225k new households

6%

+478.5k new households

Source: Kantar Worldpanel | Family Form & Media Report & Households Panel | 2018 vs 2017

VIETNAM HAS GONE MOBILE, ECOMMERCE WILL THRIVE1

33 33

39

13

7

17

Traditional advertising Digital advertising

Gen

Z

Gen X Gen Y

People are less accepting of digital

advertising

People use technology to avoid ads (e.g. ad blockers) as

well as skipping and engaging in other activity

72% skip or pay

to avoid ads

47% use tech

to block ads

40% don’t watch/

do something else

Net Positive attitude to advertising format

EVEN THOUGH CONSUMERS NOW SPEND AN AVERAGE OF OVER 4 HOURS/DAY

ON DEVICES IN VIETNAM, THEY ARE GENERALLY LESS RECEPTIVE TO DIGITAL

ADVERTISING, WITH MANY TAKING ACTION TO AVOID IT

14

UPTRADING

LESS THAN 1 IN 10 BRANDS GREW SIGNIFICANTLY OVER A 3 YEAR TIME

FRAME

15

▪ In many categories no brands grew

▪ Growth tends to come in the form of a step

change, something that disrupts the status

quo

▪ Incremental gains are easily countered by

the competition and the status quo remains

▪ Budgets, protocols and processes create a

“comfort zone” which encourages business

as usual

Source: BrandZ™, analysis of 2,052 brands between 2014 and 2017

6%

Source: BrandZ™, profile scores comparing absolute to expected values for

each brand, brands that grew or declined measured across 3 years16

THE NEW WISDOM SUGGESTS THAT SALIENCE IS ALL A BRAND NEEDS TO

GROW

So which of our three topline measures of brand equity best anticipates whether brands grow or decline?

-25 -5 15 35 55 -25 -5 15 35 55

SALIENCE DIFFERENCE

Disruptors

Brands that grew

Brands that declined

Dead and dying

-25 -5 15 35 55

MEANING

10

7

11

33

39

Beverages

Dairy

Home Care

Packaged Foods

Personal Care

33

32

35 New brand

New variant(flavor, benefit)

Changes to existing products(pack size/type, format)

Source: Kantar Worldpanel | Households Panel | New Launch Tracker

THERE ARE NOW 20 NEW LAUNCHES IN FMCG EACH DAY

Personal Care & Packaged Foods:

The most innovative environment

2018

More focus on brand’s variant portfolio

Successful launches remain hard to achieve

4.4%% Households a new launch

reached after 1 year

% Households repeat

purchase in the 1st year

Urban 4 cities

(< 5.4 in 2014)

23.9% (< 26.9% in 2014)

(2017 – 2018)

% of new launches

(2018 vs 2014)

2018

% of new launches

(2018 vs 2014)

18

INNOVATIONS THAT ARE DIFFERENT IN SOME WAY HAVE A GREATER CHANCE OF

SUCCESS

Vinamilk organic milk Sunlight Nature

Vinamilk introduced the first

organic RTD milk in Vietnam

Sunlight new added value variant

(with white tea, mineral salt,

lemon) claimed to be safe for kids,

gentle to skin and have mild

fragrance

[1] Natural products with clear evidence of nature

Clear’s new variant with 9 herbal

extracts such as Centella,

Asiatica, Cinnamomum, Ginseng

… to help get rid of dandruff

and helps to restore the

necessary nutrients for the scalp.

Clear Herbal Colgate Naturals

Colgate Natures -

reconnecting with nature to revive

our senses, rejuvenate our mind

and revitalise our body for a

healthy life with Lemon oil, Tea

Tree oil, Seaweed and Aloe Vera

extract, for a fresh and clean

mouth

19

Omo pioneered in UPGRADING THE

PACKAGE WITH A BALL helped to make

laundry easier – containing the liquid for

accurate dosage and supporting washing

machine from within.

Omomatic liquid washing ballAjinomoto with diverse

range of culinary products

Ajinomoto with WIDE RANGE OF

PRODUCTS facilitates the cooking process,

helping Vietnamese cook delicious food in

the convenient and less time-consuming

way.

[2] Make Life Easier

INNOVATIONS THAT ARE DIFFERENT IN SOME WAY HAVE A GREATER CHANCE OF

SUCCESS

20

[3] Mix of traditions and the modern

Number 1 Salted Lemon

Revive Salted Lemon

Number 1 Salted Lemon initiated the

salted lemon segment in isotonic drink

category, and Revive Salted Lemon

soon joined the band wagon.

Both could grasp significant growth,

hurting the long-established hard-core

isotonic segment, by delivering the great

traditional taste via a modern sporty &

youthful imagery

Push Max Passion fruit

Push Max was the first RTDJ brand

launching passion fruit flavor (a

popular fruit flavor in North), gaining

grounds quickly and hurting Twister

market share in this market

Cobote

Cobote - a new local brand offers wide

range of natural personal care

products made from natural

ingredients coconut, cucumber, ginger,

lemon grass,…

INNOVATIONS THAT ARE DIFFERENT IN SOME WAY HAVE A GREATER CHANCE OF

SUCCESS

21

[4] New mixes of ingredients

Coke Coffee

Coke Coffee offers a different experience

of Coke, which can also help them

refreshed and wake them up.

Fuzetea

The combination of Chia seed and

peach/ passion fruit flavour

ADM Chuối

Vinamilk launched ADM Banana – the

first-ever combination of milk and

banana in Vietnam

INNOVATIONS THAT ARE DIFFERENT IN SOME WAY HAVE A GREATER CHANCE OF

SUCCESS

22

[5] Packaging innovations that excite

Pepsi Next Generation

packaging collection

Pepsi is reintroducing its

iconic vintage design on

regular Pepsi products for

a limited time.

Coke and Pepsi launched

limited editions of packaging to

celebrate World Cup 2018

Milo launched can,

making it the first-ever

dairy drink in Can

format

Cocoxim excites

Vietnamese consumers

with packed coconut juice

Pepsi Coke and Pepsi

Milo

Milo Cocoxim

INNOVATIONS THAT ARE DIFFERENT IN SOME WAY HAVE A GREATER CHANCE OF

SUCCESS

FMCGs in Vietnam

All images within this document are examples for illustrative purposes.