Page 1

Sector Thematic

Food & Grocery

From a disruptor’s lens

The view from a disruptor’s lens is a salivating one as short of a few well-

capitalised operators, the organised Food & Grocery ecosystem remains (1)

profitless, (2) cash-strapped and (3) supported by increasing crutches (high gross

margins, inefficient cost structures and increasing vendor support). Our read-

through across the ecosystem suggests (1) the phase of capital dumping by

global/domestic biggies may soon be upon us, (2) selection/pricing arbitrage vis-

a-vis industry bellwether DMART continues to shrink, (3) margin cracks are

imminent and (4) Reliance Retail-FRL combination could change the complexion

of competition in top Indian districts.

Jay Gandhi Retail, Paints

[email protected]

+91-22-6171-7320

Page 2

09 February 2021 Sector Thematic

Food & Grocery

HSIE Research is also available on Bloomberg ERH HDF <GO> & Thomson Reuters

From a disruptor’s lens The view from a disruptor’s lens is a salivating one as short of a few well-

capitalised operators, the organised Food & Grocery ecosystem remains (1)

profitless, (2) cash-strapped and (3) supported by increasing crutches (high

gross margins, inefficient cost structures and increasing vendor support). Our

read-through across the ecosystem suggests (1) the phase of capital dumping

by global/domestic biggies may soon be upon us, (2) selection/pricing

arbitrage vis-a-vis industry bellwether DMART continues to shrink, (3)

margin cracks are imminent and (4) Reliance Retail-FRL combination could

change the complexion of competition in top Indian districts.

Capital dumping is likely to take center-stage: Global/domestic retailers

Amazon, Walmart-backed Flipkart and Reliance Retail (refer link) have

significantly strengthened their war chests for investments in supply chain,

fulfillment capabilities and pricing/selection. An inkling of this can already

be seen in the reducing selection/pricing arbitrage of DMART over these

biggies. Fulfillment/supply chain investments of Amazon’s F&G unit (adj.

for scale) is already >6x that of DMART’s (Comparison: DMART Ready vs

Amazon). Former remains aggressive on footprint expansion.

Margin crack for ecosystem is imminent: Over FY15-20, despite low

competitive intensity, most organised grocers’ sales velocity (1-4% CAGR)

has undershot inflation, signaling a gradual but structural footfall reduction.

Most (1) continue to hide behind high gross margins as cost of retailing

remains inefficient and (2) have bare-bone investments in online fulfilment

capabilities. Moreover, as subsidised home delivery becomes table stakes,

even the best (D-MART) may get arm-twisted into bringing a part of online

fulfillment costs on their books (not factored in, remains a risk to estimates).

Thus, the imperative to remain competitive (reducing GMs) + rising cost of

retailing is likely to crack operational margins for the ecosystem over FY21-

25. This has played out globally too (Walmart’s CY15-20 margin crack).

Reliance + Future Retail > DMART in store density: Post integration and, if

executed well, the Reliance Retail + FRL store network is likely to get nearly

as dense as DMART’s (Refer table) in the latter’s key markets (HSIE: 48% of

DMART’s stores, 65-70% of revenue). These markets are the most

populated/over-retailed districts in India with high PCI. Hence, the rise in

competitive intensity/price action and near-zero sourcing margin arbitrage

seems to be a foregone conclusion. The high population density in these

districts could help fulfill JioMART orders within controlled costs too.

Meanwhile, well-funded e-grocers are scaling up nicely: Even pre-

COVID19, e-grocers had been scaling up nicely. The concoction of (1) higher

AoVs and GMs (3) lower CACs and (4) better national brands representation

has changed the complexion of online grocers’ P&L during the pandemic.

Survivors don’t offer any margin of safety: While consolidation in F&G is

imminent, survivors (DMART) do not offer any margin of safety at 75x+

FY23 P/E. DMART’s growth is likely to be healthy (21/23/23%

revenue/EBITDA/PAT CAGR), largely underpinned by network expansion.

Alas, pressure on sales velocity and margins remains probabilistically high

as deep-pocketed operators enter DMART’s key catchments. We maintain

our SELL recommendation on DMART with a DCF-based TP: 2,160/sh –

implying 34x FY23 EV/EBITDA + 2x FY23 sales for e-comm. Note: we

currently have an SOTP-based fair value of Rs. 3,743bn for RRVL, implying

20x FY23 EV/EBITDA + 3x FY23 sales for its e-comm business.

Jay Gandhi

[email protected]

+91-22-6171-7320

Page 3

Page | 2

F&G: Sector Thematic

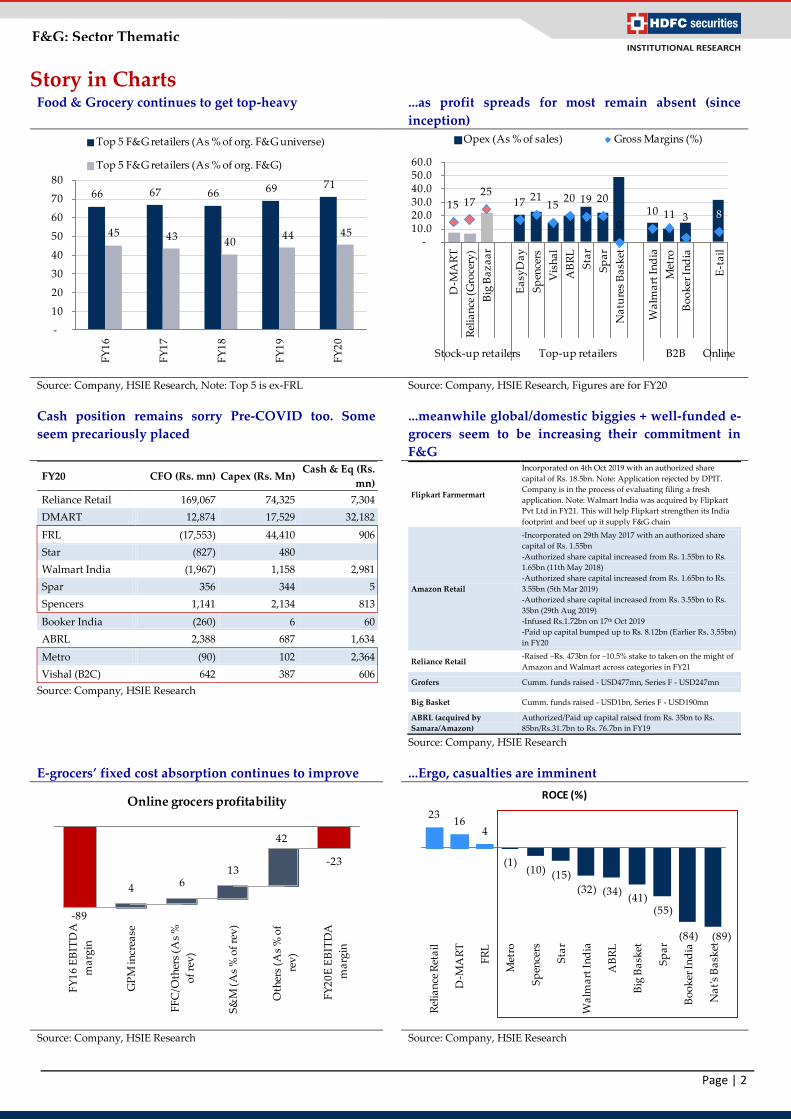

Story in Charts Food & Grocery continues to get top-heavy ...as profit spreads for most remain absent (since

inception)

Source: Company, HSIE Research, Note: Top 5 is ex-FRL Source: Company, HSIE Research, Figures are for FY20

Cash position remains sorry Pre-COVID too. Some

seem precariously placed

...meanwhile global/domestic biggies + well-funded e-

grocers seem to be increasing their commitment in

F&G

FY20 CFO (Rs. mn) Capex (Rs. Mn) Cash & Eq (Rs.

mn)

Reliance Retail 169,067 74,325 7,304

DMART 12,874 17,529 32,182

FRL (17,553) 44,410 906

Star (827) 480

Walmart India (1,967) 1,158 2,981

Spar 356 344 5

Spencers 1,141 2,134 813

Booker India (260) 6 60

ABRL 2,388 687 1,634

Metro (90) 102 2,364

Vishal (B2C) 642 387 606

Source: Company, HSIE Research

Flipkart Farmermart

Incorporated on 4th Oct 2019 with an authorized share

capital of Rs. 18.5bn. Note: Application rejected by DPIT.

Company is in the process of evaluating filing a fresh

application. Note: Walmart India was acquired by Flipkart

Pvt Ltd in FY21. This will help Flipkart strengthen its India

footprint and beef up it supply F&G chain

Amazon Retail

-Incorporated on 29th May 2017 with an authorized share

capital of Rs. 1.55bn

-Authorized share capital increased from Rs. 1.55bn to Rs.

1.65bn (11th May 2018)

-Authorized share capital increased from Rs. 1.65bn to Rs.

3.55bn (5th Mar 2019)

-Authorized share capital increased from Rs. 3.55bn to Rs.

35bn (29th Aug 2019)

-Infused Rs.1.72bn on 17th Oct 2019

-Paid up capital bumped up to Rs. 8.12bn (Earlier Rs. 3.55bn)

in FY20

Reliance Retail -Raised ~Rs. 473bn for ~10.5% stake to taken on the might of

Amazon and Walmart across categories in FY21

Grofers Cumm. funds raised - USD477mn, Series F - USD247mn

Big Basket Cumm. funds raised - USD1bn, Series F - USD190mn

ABRL (acquired by

Samara/Amazon)

Authorized/Paid up capital raised from Rs. 35bn to Rs.

85bn/Rs.31.7bn to Rs. 76.7bn in FY19

Source: Company, HSIE Research

E-grocers’ fixed cost absorption continues to improve

...Ergo, casualties are imminent

Source: Company, HSIE Research Source: Company, HSIE Research

66 67 66 69 71

45 43 40 44 45

-

10

20

30

40

50

60

70

80

FY

16

FY

17

FY

18

FY

19

FY

20

Top 5 F&G retailers (As % of org. F&G universe)

Top 5 F&G retailers (As % of org. F&G)

15 1725

17 2115

20 19 20

010 11 3 8

-10.0 20.0 30.0 40.0 50.0 60.0

D-M

AR

T

Rel

ian

ce (

Gro

cery

)

Big

Ba

za

ar

Ea

syD

ay

Sp

ence

rs

Vis

ha

l

AB

RL

Sta

r

Sp

ar

Na

ture

s B

ask

et

Wa

lma

rt I

nd

ia

Met

ro

Bo

ok

er I

nd

ia

E-t

ail

Stock-up retailers Top-up retailers B2B Online

Opex (As % of sales) Gross Margins (%)

-89

-23

4 6

13

42

FY

16

EB

ITD

A

ma

rgin

GP

M in

crea

se

FF

C/O

ther

s (A

s %

of

rev

)

S&

M (

As

% o

f re

v)

Oth

ers

(As

% o

f

rev

)

FY

20

E E

BIT

DA

ma

rgin

Online grocers profitability23

16 4

(1)(10) (15)

(32) (34)(41)

(55)

(84) (89)

Rel

ian

ce R

eta

il

D-M

AR

T

FR

L

Met

ro

Sp

ence

rs

Sta

r

Wa

lma

rt I

nd

ia

AB

RL

Big

Ba

sket

Sp

ar

Bo

ok

er I

nd

ia

Na

t's

Ba

sket

ROCE (%)

Page 4

Page | 3

F&G: Sector Thematic

Contents

Capital dumping to take centerstage .................................................................................4

Margin crack for the ecosystem is imminent ..............................................................4

Increasing cost of retailing and margin crack is a global trend ................................5

Case Study: Globally, even the best got bruised! .......................................................7

Could this happen to DMART? ....................................................................................8

DMART Ready vs Amazon India’s F&G performance .............................................8

Reliance Retail + Future Group > DMART in store density: ........................................9

District-wise store map across per capita income and population density ..........10

Market share gain in top districts unlikely for DMART ......................................... 10

D-MART’s pricing/assortment arbitrage over peers continues to shrink ............... 11

Well funded e-grocers scaling up nicely ........................................................................ 14

Case Study: Grofers ...................................................................................................... 15

The heat is being felt by offline grocers already ...................................................... 16

Comparative Analysis ........................................................................................................17

Page 5

Page | 4

F&G: Sector Thematic

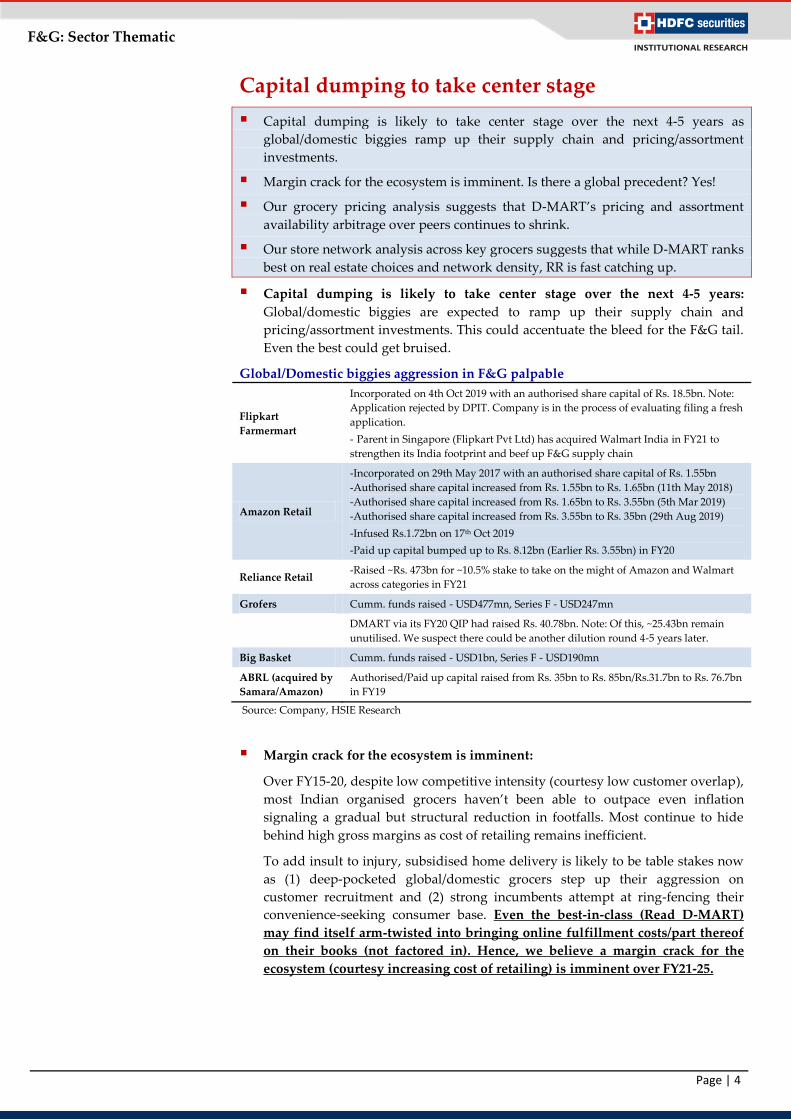

Capital dumping to take center stage

Capital dumping is likely to take center stage over the next 4-5 years as

global/domestic biggies ramp up their supply chain and pricing/assortment

investments.

Margin crack for the ecosystem is imminent. Is there a global precedent? Yes!

Our grocery pricing analysis suggests that D-MART’s pricing and assortment

availability arbitrage over peers continues to shrink.

Our store network analysis across key grocers suggests that while D-MART ranks

best on real estate choices and network density, RR is fast catching up.

Capital dumping is likely to take center stage over the next 4-5 years:

Global/domestic biggies are expected to ramp up their supply chain and

pricing/assortment investments. This could accentuate the bleed for the F&G tail.

Even the best could get bruised.

Global/Domestic biggies aggression in F&G palpable

Flipkart

Farmermart

Incorporated on 4th Oct 2019 with an authorised share capital of Rs. 18.5bn. Note:

Application rejected by DPIT. Company is in the process of evaluating filing a fresh

application.

- Parent in Singapore (Flipkart Pvt Ltd) has acquired Walmart India in FY21 to

strengthen its India footprint and beef up F&G supply chain

Amazon Retail

-Incorporated on 29th May 2017 with an authorised share capital of Rs. 1.55bn

-Authorised share capital increased from Rs. 1.55bn to Rs. 1.65bn (11th May 2018)

-Authorised share capital increased from Rs. 1.65bn to Rs. 3.55bn (5th Mar 2019)

-Authorised share capital increased from Rs. 3.55bn to Rs. 35bn (29th Aug 2019)

-Infused Rs.1.72bn on 17th Oct 2019

-Paid up capital bumped up to Rs. 8.12bn (Earlier Rs. 3.55bn) in FY20

Reliance Retail -Raised ~Rs. 473bn for ~10.5% stake to take on the might of Amazon and Walmart

across categories in FY21

Grofers Cumm. funds raised - USD477mn, Series F - USD247mn

DMART via its FY20 QIP had raised Rs. 40.78bn. Note: Of this, ~25.43bn remain

unutilised. We suspect there could be another dilution round 4-5 years later.

Big Basket Cumm. funds raised - USD1bn, Series F - USD190mn

ABRL (acquired by

Samara/Amazon)

Authorised/Paid up capital raised from Rs. 35bn to Rs. 85bn/Rs.31.7bn to Rs. 76.7bn

in FY19

Source: Company, HSIE Research

Margin crack for the ecosystem is imminent:

Over FY15-20, despite low competitive intensity (courtesy low customer overlap),

most Indian organised grocers haven’t been able to outpace even inflation

signaling a gradual but structural reduction in footfalls. Most continue to hide

behind high gross margins as cost of retailing remains inefficient.

To add insult to injury, subsidised home delivery is likely to be table stakes now

as (1) deep-pocketed global/domestic grocers step up their aggression on

customer recruitment and (2) strong incumbents attempt at ring-fencing their

convenience-seeking consumer base. Even the best-in-class (Read D-MART)

may find itself arm-twisted into bringing online fulfillment costs/part thereof

on their books (not factored in). Hence, we believe a margin crack for the

ecosystem (courtesy increasing cost of retailing) is imminent over FY21-25.

Page 6

Page | 5

F&G: Sector Thematic

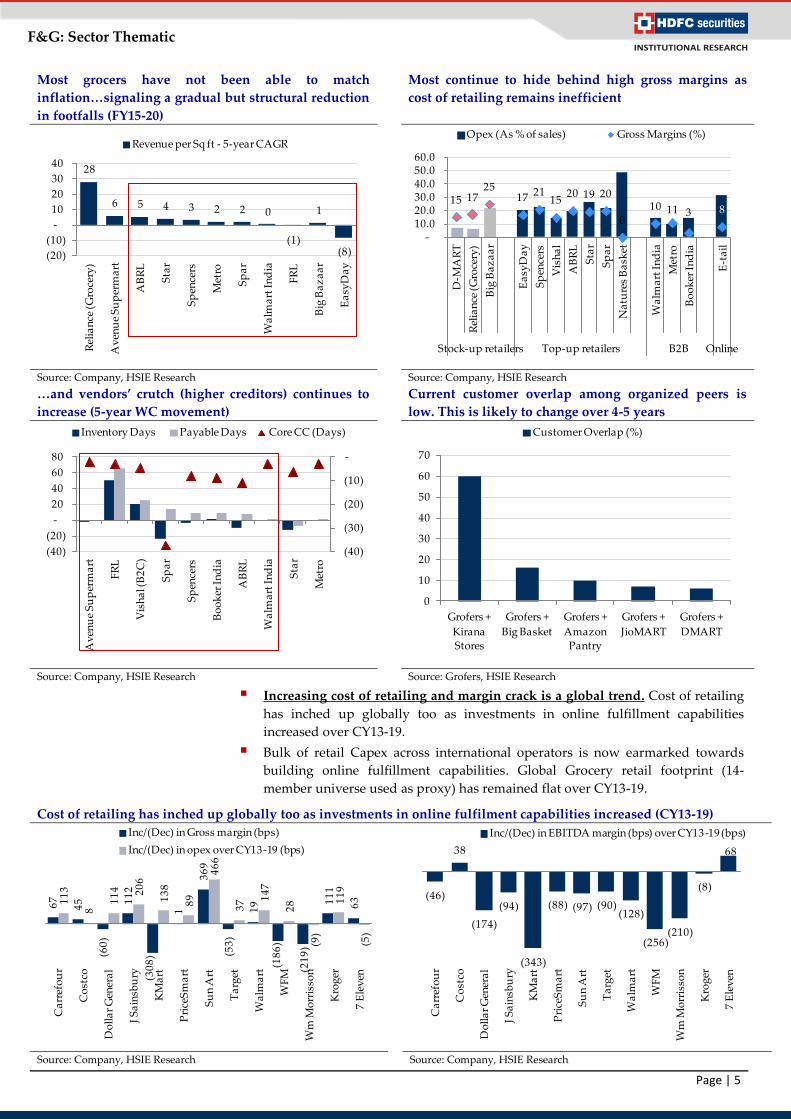

Most grocers have not been able to match

inflation…signaling a gradual but structural reduction

in footfalls (FY15-20)

Most continue to hide behind high gross margins as

cost of retailing remains inefficient

Source: Company, HSIE Research Source: Company, HSIE Research

…and vendors’ crutch (higher creditors) continues to

increase (5-year WC movement)

Current customer overlap among organized peers is

low. This is likely to change over 4-5 years

Source: Company, HSIE Research Source: Grofers, HSIE Research

Increasing cost of retailing and margin crack is a global trend. Cost of retailing

has inched up globally too as investments in online fulfillment capabilities

increased over CY13-19.

Bulk of retail Capex across international operators is now earmarked towards

building online fulfillment capabilities. Global Grocery retail footprint (14-

member universe used as proxy) has remained flat over CY13-19.

Cost of retailing has inched up globally too as investments in online fulfilment capabilities increased (CY13-19)

Source: Company, HSIE Research Source: Company, HSIE Research

28

6 5 4 3 2 2 0

(1)

1

(8)(20)

(10)

-

10

20

30

40

Rel

ian

ce (

Gro

cery

)

Av

enu

e S

up

erm

art

AB

RL

Sta

r

Sp

ence

rs

Met

ro

Sp

ar

Wa

lma

rt I

nd

ia

FR

L

Big

Ba

za

ar

Ea

syD

ay

Revenue per Sq ft - 5-year CAGR

15 1725

17 2115

20 19 20

010 11 3 8

-10.0 20.0 30.0 40.0 50.0 60.0

D-M

AR

T

Rel

ian

ce (

Gro

cery

)

Big

Ba

za

ar

Ea

syD

ay

Sp

ence

rs

Vis

ha

l

AB

RL

Sta

r

Sp

ar

Na

ture

s B

ask

et

Wa

lma

rt I

nd

ia

Met

ro

Bo

ok

er I

nd

ia

E-t

ail

Stock-up retailers Top-up retailers B2B Online

Opex (As % of sales) Gross Margins (%)

(40)

(30)

(20)

(10)

-

(40)

(20)

-

20

40

60

80

Av

enu

e S

up

erm

art

FR

L

Vis

ha

l (B

2C

)

Sp

ar

Sp

ence

rs

Bo

ok

er I

nd

ia

AB

RL

Wa

lma

rt I

nd

ia

Sta

r

Met

ro

Inventory Days Payable Days Core CC (Days)

0

10

20

30

40

50

60

70

Grofers +

Kirana

Stores

Grofers +

Big Basket

Grofers +

Amazon

Pantry

Grofers +

JioMART

Grofers +

DMART

Customer Overlap (%)

67

45

(60

)

11

2

(30

8)

1

36

9

(53

)

19

(18

6)

(21

9)

11

1

63

11

3

8 1

14

20

6

13

8

89

46

6

37

14

7

28

(9)

11

9

(5)

Ca

rref

ou

r

Co

stco

Do

lla

r G

ener

al

J S

ain

sbu

ry

KM

art

Pri

ceS

ma

rt

Su

n A

rt

Ta

rget

Wa

lma

rt

WF

M

Wm

Mo

rris

son

Kro

ger

7 E

lev

en

Inc/(Dec) in Gross margin (bps)

Inc/(Dec) in opex over CY13-19 (bps)

(46)

38

(174)

(94)

(343)

(88) (97) (90)(128)

(256)(210)

(8)

68

Ca

rref

ou

r

Co

stco

Do

lla

r G

ener

al

J S

ain

sbu

ry

KM

art

Pri

ceS

ma

rt

Su

n A

rt

Ta

rget

Wa

lma

rt

WF

M

Wm

Mo

rris

son

Kro

ger

7 E

lev

en

Inc/(Dec) in EBITDA margin (bps) over CY13-19 (bps)

Page 7

Page | 6

F&G: Sector Thematic

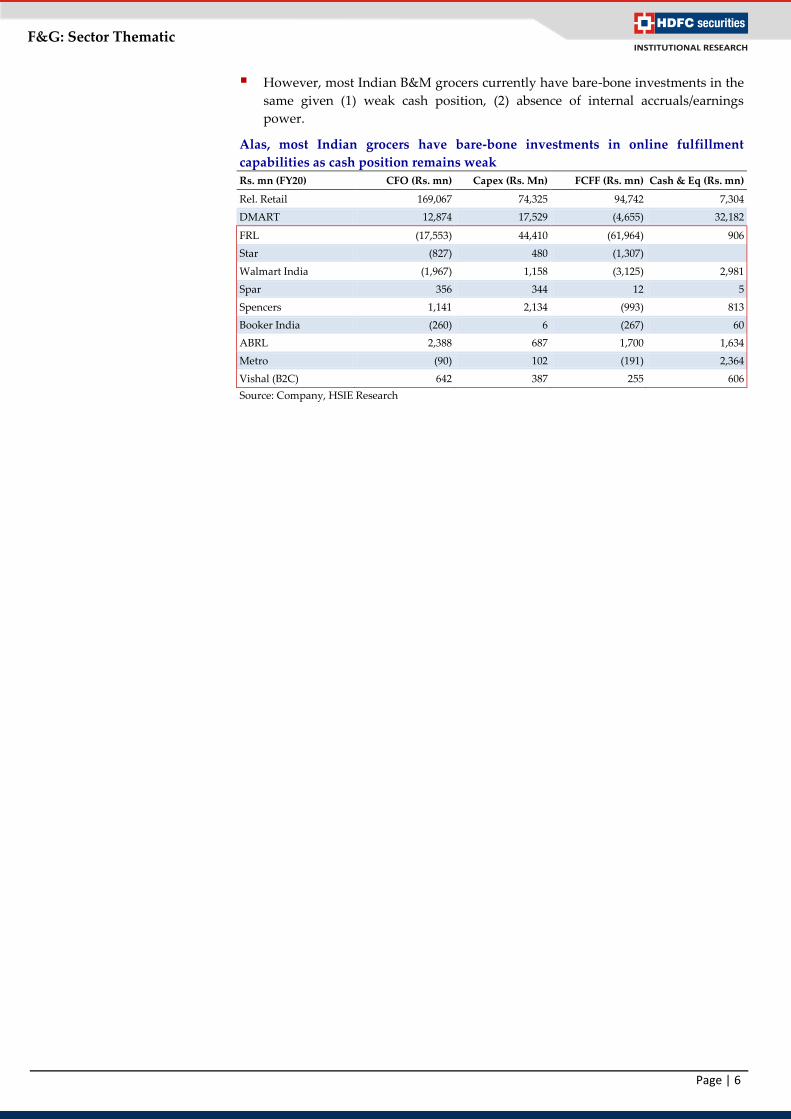

However, most Indian B&M grocers currently have bare-bone investments in the

same given (1) weak cash position, (2) absence of internal accruals/earnings

power.

Alas, most Indian grocers have bare-bone investments in online fulfillment

capabilities as cash position remains weak

Rs. mn (FY20) CFO (Rs. mn) Capex (Rs. Mn) FCFF (Rs. mn) Cash & Eq (Rs. mn)

Rel. Retail 169,067 74,325 94,742 7,304

DMART 12,874 17,529 (4,655) 32,182

FRL (17,553) 44,410 (61,964) 906

Star (827) 480 (1,307)

Walmart India (1,967) 1,158 (3,125) 2,981

Spar 356 344 12 5

Spencers 1,141 2,134 (993) 813

Booker India (260) 6 (267) 60

ABRL 2,388 687 1,700 1,634

Metro (90) 102 (191) 2,364

Vishal (B2C) 642 387 255 606

Source: Company, HSIE Research

Page 8

Page | 7

F&G: Sector Thematic

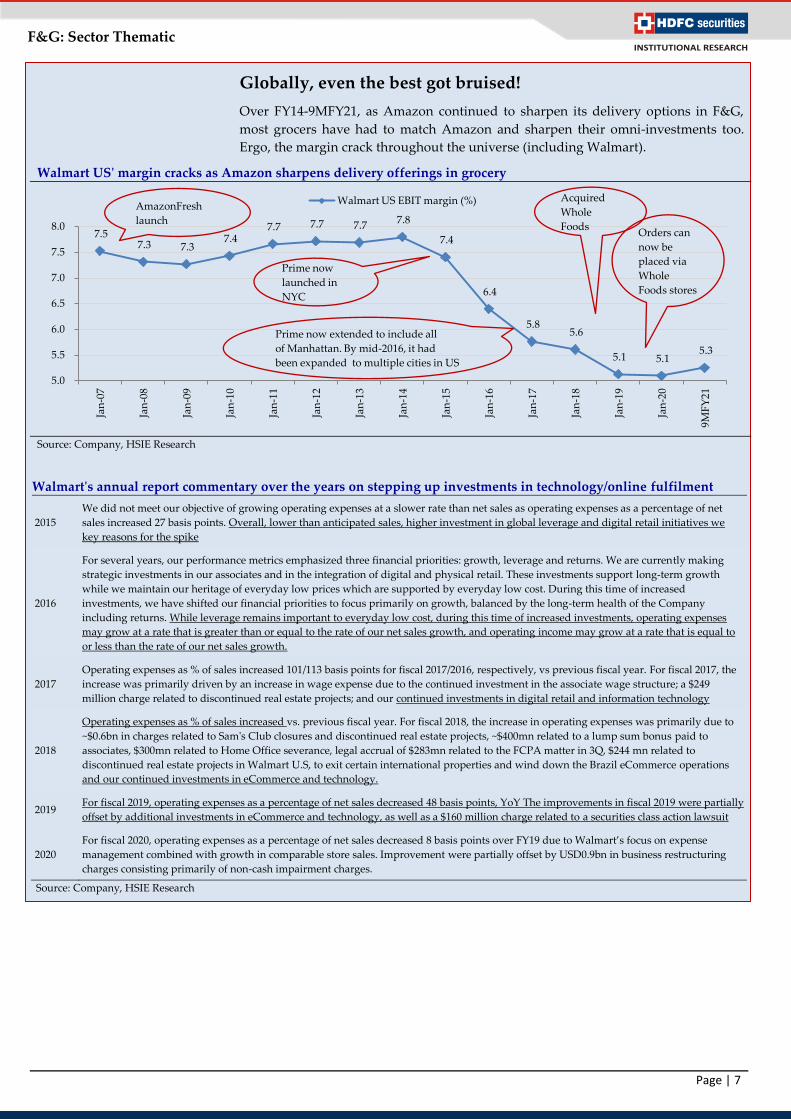

Globally, even the best got bruised!

Over FY14-9MFY21, as Amazon continued to sharpen its delivery options in F&G,

most grocers have had to match Amazon and sharpen their omni-investments too.

Ergo, the margin crack throughout the universe (including Walmart).

Walmart US' margin cracks as Amazon sharpens delivery offerings in grocery

Source: Company, HSIE Research

Walmart's annual report commentary over the years on stepping up investments in technology/online fulfilment

2015

We did not meet our objective of growing operating expenses at a slower rate than net sales as operating expenses as a percentage of net

sales increased 27 basis points. Overall, lower than anticipated sales, higher investment in global leverage and digital retail initiatives we

key reasons for the spike

2016

For several years, our performance metrics emphasized three financial priorities: growth, leverage and returns. We are currently making

strategic investments in our associates and in the integration of digital and physical retail. These investments support long-term growth

while we maintain our heritage of everyday low prices which are supported by everyday low cost. During this time of increased

investments, we have shifted our financial priorities to focus primarily on growth, balanced by the long-term health of the Company

including returns. While leverage remains important to everyday low cost, during this time of increased investments, operating expenses

may grow at a rate that is greater than or equal to the rate of our net sales growth, and operating income may grow at a rate that is equal to

or less than the rate of our net sales growth.

2017

Operating expenses as % of sales increased 101/113 basis points for fiscal 2017/2016, respectively, vs previous fiscal year. For fiscal 2017, the

increase was primarily driven by an increase in wage expense due to the continued investment in the associate wage structure; a $249

million charge related to discontinued real estate projects; and our continued investments in digital retail and information technology

2018

Operating expenses as % of sales increased vs. previous fiscal year. For fiscal 2018, the increase in operating expenses was primarily due to

~$0.6bn in charges related to Sam's Club closures and discontinued real estate projects, ~$400mn related to a lump sum bonus paid to

associates, $300mn related to Home Office severance, legal accrual of $283mn related to the FCPA matter in 3Q, $244 mn related to

discontinued real estate projects in Walmart U.S, to exit certain international properties and wind down the Brazil eCommerce operations

and our continued investments in eCommerce and technology.

2019 For fiscal 2019, operating expenses as a percentage of net sales decreased 48 basis points, YoY The improvements in fiscal 2019 were partially

offset by additional investments in eCommerce and technology, as well as a $160 million charge related to a securities class action lawsuit

2020

For fiscal 2020, operating expenses as a percentage of net sales decreased 8 basis points over FY19 due to Walmart’s focus on expense

management combined with growth in comparable store sales. Improvement were partially offset by USD0.9bn in business restructuring

charges consisting primarily of non-cash impairment charges.

Source: Company, HSIE Research

7.5 7.3 7.3

7.4 7.7 7.7 7.7

7.8

7.4

6.4

5.8 5.6

5.1 5.1 5.3

5.0

5.5

6.0

6.5

7.0

7.5

8.0

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

Jan

-18

Jan

-19

Jan

-20

9MF

Y21

Walmart US EBIT margin (%)

Prime now

launched in

NYC

Prime now extended to include all

of Manhattan. By mid-2016, it had

been expanded to multiple cities in US

Acquired

Whole

Foods Orders can

now be

placed via

Whole

Foods stores

AmazonFresh

launch

Page 9

Page | 8

F&G: Sector Thematic

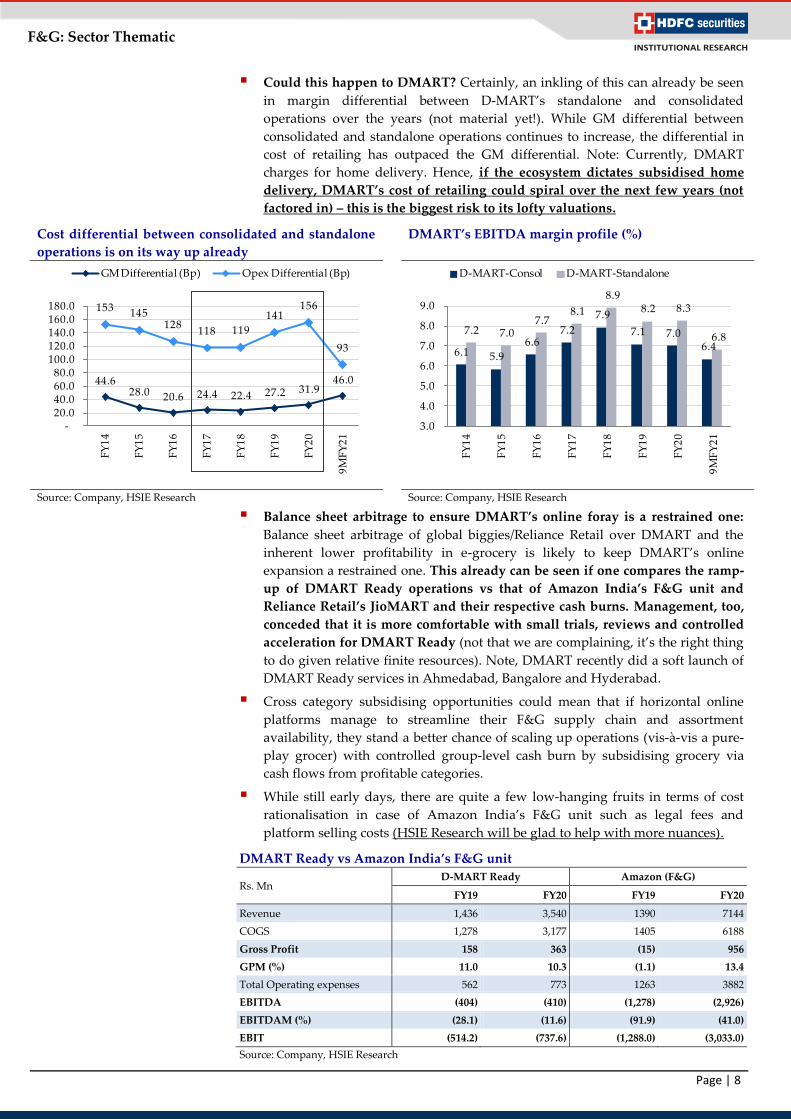

Could this happen to DMART? Certainly, an inkling of this can already be seen

in margin differential between D-MART’s standalone and consolidated

operations over the years (not material yet!). While GM differential between

consolidated and standalone operations continues to increase, the differential in

cost of retailing has outpaced the GM differential. Note: Currently, DMART

charges for home delivery. Hence, if the ecosystem dictates subsidised home

delivery, DMART’s cost of retailing could spiral over the next few years (not

factored in) – this is the biggest risk to its lofty valuations.

Cost differential between consolidated and standalone

operations is on its way up already

DMART’s EBITDA margin profile (%)

Source: Company, HSIE Research Source: Company, HSIE Research

Balance sheet arbitrage to ensure DMART’s online foray is a restrained one:

Balance sheet arbitrage of global biggies/Reliance Retail over DMART and the

inherent lower profitability in e-grocery is likely to keep DMART’s online

expansion a restrained one. This already can be seen if one compares the ramp-

up of DMART Ready operations vs that of Amazon India’s F&G unit and

Reliance Retail’s JioMART and their respective cash burns. Management, too,

conceded that it is more comfortable with small trials, reviews and controlled

acceleration for DMART Ready (not that we are complaining, it’s the right thing

to do given relative finite resources). Note, DMART recently did a soft launch of

DMART Ready services in Ahmedabad, Bangalore and Hyderabad.

Cross category subsidising opportunities could mean that if horizontal online

platforms manage to streamline their F&G supply chain and assortment

availability, they stand a better chance of scaling up operations (vis-à-vis a pure-

play grocer) with controlled group-level cash burn by subsidising grocery via

cash flows from profitable categories.

While still early days, there are quite a few low-hanging fruits in terms of cost

rationalisation in case of Amazon India’s F&G unit such as legal fees and

platform selling costs (HSIE Research will be glad to help with more nuances).

DMART Ready vs Amazon India’s F&G unit

Rs. Mn D-MART Ready Amazon (F&G)

FY19 FY20 FY19 FY20

Revenue 1,436 3,540 1390 7144

COGS 1,278 3,177 1405 6188

Gross Profit 158 363 (15) 956

GPM (%) 11.0 10.3 (1.1) 13.4

Total Operating expenses 562 773 1263 3882

EBITDA (404) (410) (1,278) (2,926)

EBITDAM (%) (28.1) (11.6) (91.9) (41.0)

EBIT (514.2) (737.6) (1,288.0) (3,033.0)

Source: Company, HSIE Research

44.6 28.0 20.6 24.4 22.4 27.2 31.9

46.0

153 145 128

118 119

141 156

93

-20.0 40.0 60.0 80.0

100.0 120.0 140.0 160.0 180.0

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

9M

FY

21

GM Differential (Bp) Opex Differential (Bp)

6.1 5.9

6.6 7.2

7.9

7.1 7.0 6.4

7.2 7.0 7.7

8.1

8.9 8.2 8.3

6.8

3.0

4.0

5.0

6.0

7.0

8.0

9.0

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

9M

FY

21

D-MART-Consol D-MART-Standalone

Page 10

Page | 9

F&G: Sector Thematic

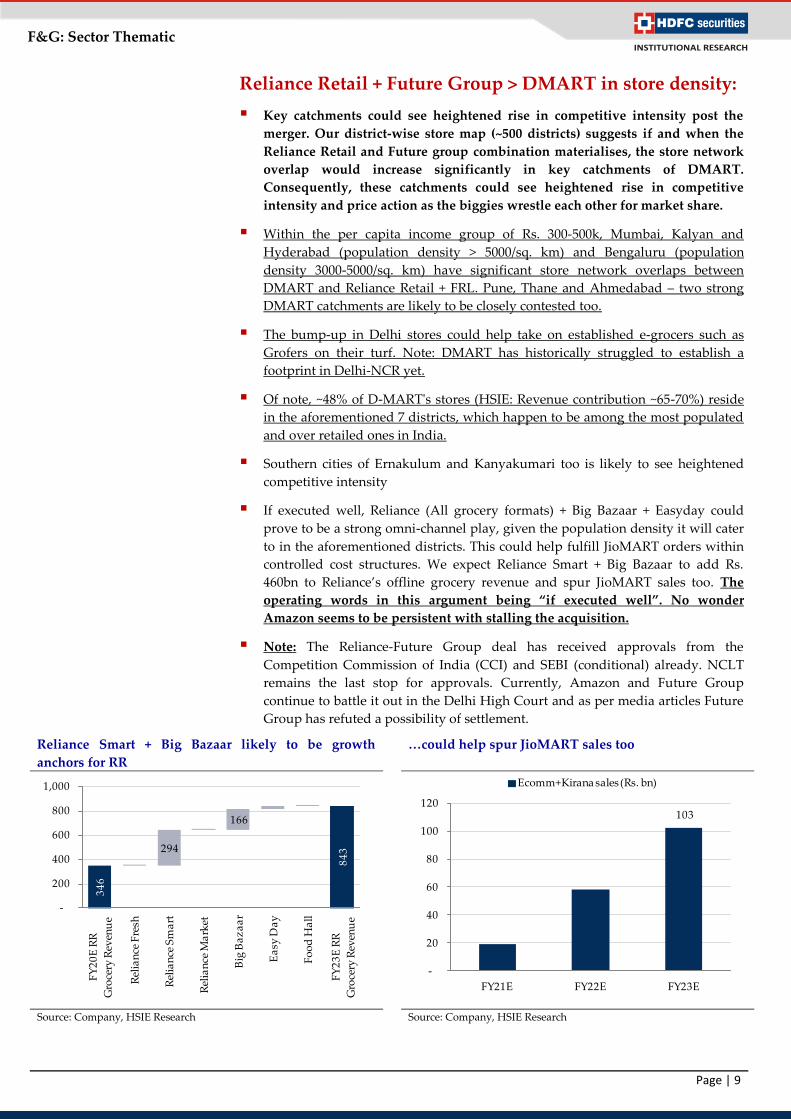

Reliance Retail + Future Group > DMART in store density:

Key catchments could see heightened rise in competitive intensity post the

merger. Our district-wise store map (~500 districts) suggests if and when the

Reliance Retail and Future group combination materialises, the store network

overlap would increase significantly in key catchments of DMART.

Consequently, these catchments could see heightened rise in competitive

intensity and price action as the biggies wrestle each other for market share.

Within the per capita income group of Rs. 300-500k, Mumbai, Kalyan and

Hyderabad (population density > 5000/sq. km) and Bengaluru (population

density 3000-5000/sq. km) have significant store network overlaps between

DMART and Reliance Retail + FRL. Pune, Thane and Ahmedabad – two strong

DMART catchments are likely to be closely contested too.

The bump-up in Delhi stores could help take on established e-grocers such as

Grofers on their turf. Note: DMART has historically struggled to establish a

footprint in Delhi-NCR yet.

Of note, ~48% of D-MART's stores (HSIE: Revenue contribution ~65-70%) reside

in the aforementioned 7 districts, which happen to be among the most populated

and over retailed ones in India.

Southern cities of Ernakulum and Kanyakumari too is likely to see heightened

competitive intensity

If executed well, Reliance (All grocery formats) + Big Bazaar + Easyday could

prove to be a strong omni-channel play, given the population density it will cater

to in the aforementioned districts. This could help fulfill JioMART orders within

controlled cost structures. We expect Reliance Smart + Big Bazaar to add Rs.

460bn to Reliance’s offline grocery revenue and spur JioMART sales too. The

operating words in this argument being “if executed well”. No wonder

Amazon seems to be persistent with stalling the acquisition.

Note: The Reliance-Future Group deal has received approvals from the

Competition Commission of India (CCI) and SEBI (conditional) already. NCLT

remains the last stop for approvals. Currently, Amazon and Future Group

continue to battle it out in the Delhi High Court and as per media articles Future

Group has refuted a possibility of settlement.

Reliance Smart + Big Bazaar likely to be growth

anchors for RR

…could help spur JioMART sales too

Source: Company, HSIE Research Source: Company, HSIE Research

34

6

84

3 294

166

-

200

400

600

800

1,000

FY

20

E R

R

Gro

cery

Rev

enu

e

Rel

ian

ce F

resh

Rel

ian

ce S

ma

rt

Rel

ian

ce M

ark

et

Big

Ba

za

ar

Ea

sy D

ay

Fo

od

Ha

ll

FY

23

E R

R

Gro

cery

Rev

enu

e

103

-

20

40

60

80

100

120

FY21E FY22E FY23E

Ecomm+Kirana sales (Rs. bn)

Page 11

Page | 10

F&G: Sector Thematic

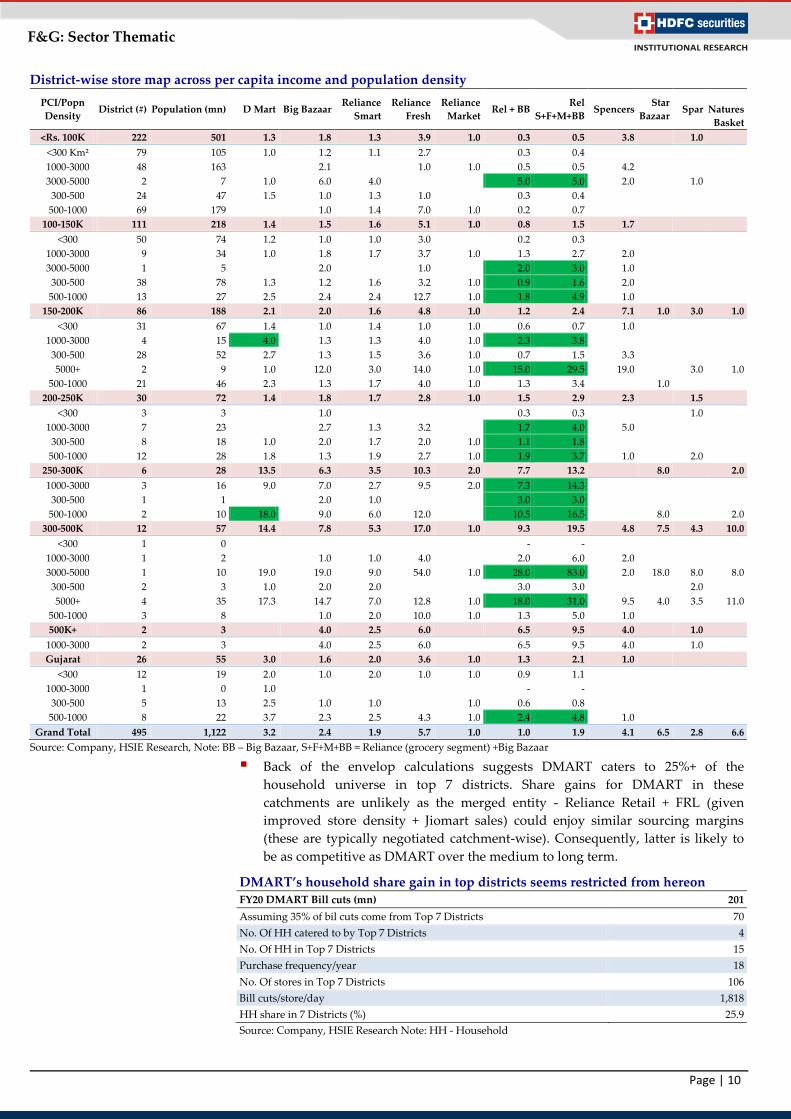

District-wise store map across per capita income and population density

PCI/Popn

Density District (#) Population (mn) D Mart Big Bazaar

Reliance

Smart

Reliance

Fresh

Reliance

Market Rel + BB

Rel

S+F+M+BB Spencers

Star

Bazaar Spar

Natures

Basket

<Rs. 100K 222 501 1.3 1.8 1.3 3.9 1.0 0.3 0.5 3.8

1.0

<300 Km² 79 105 1.0 1.2 1.1 2.7 #DIV/0! 0.3 0.4 #DIV/0! ###### ###### #DIV/0!

1000-3000 48 163 #DIV/0! 2.1 #DIV/0! 1.0 1.0 0.5 0.5 4.2 ###### ###### #DIV/0!

3000-5000 2 7 1.0 6.0 4.0 #DIV/0! #DIV/0! 5.0 5.0 2.0 ###### 1.0 #DIV/0!

300-500 24 47 1.5 1.0 1.3 1.0 #DIV/0! 0.3 0.4 #DIV/0! ###### ###### #DIV/0!

500-1000 69 179 #DIV/0! 1.0 1.4 7.0 1.0 0.2 0.7 #DIV/0! ###### ###### #DIV/0!

100-150K 111 218 1.4 1.5 1.6 5.1 1.0 0.8 1.5 1.7

<300 50 74 1.2 1.0 1.0 3.0 #DIV/0! 0.2 0.3 #DIV/0! ###### ###### #DIV/0!

1000-3000 9 34 1.0 1.8 1.7 3.7 1.0 1.3 2.7 2.0 ###### ###### #DIV/0!

3000-5000 1 5 #DIV/0! 2.0 #DIV/0! 1.0 #DIV/0! 2.0 3.0 1.0 ###### ###### #DIV/0!

300-500 38 78 1.3 1.2 1.6 3.2 1.0 0.9 1.6 2.0 ###### ###### #DIV/0!

500-1000 13 27 2.5 2.4 2.4 12.7 1.0 1.8 4.9 1.0 ###### ###### #DIV/0!

150-200K 86 188 2.1 2.0 1.6 4.8 1.0 1.2 2.4 7.1 1.0 3.0 1.0

<300 31 67 1.4 1.0 1.4 1.0 1.0 0.6 0.7 1.0 ###### ###### #DIV/0!

1000-3000 4 15 4.0 1.3 1.3 4.0 1.0 2.3 3.8 #DIV/0! ###### ###### #DIV/0!

300-500 28 52 2.7 1.3 1.5 3.6 1.0 0.7 1.5 3.3 ###### ###### #DIV/0!

5000+ 2 9 1.0 12.0 3.0 14.0 1.0 15.0 29.5 19.0 ###### 3.0 1.0

500-1000 21 46 2.3 1.3 1.7 4.0 1.0 1.3 3.4 #DIV/0! 1.0 ###### #DIV/0!

200-250K 30 72 1.4 1.8 1.7 2.8 1.0 1.5 2.9 2.3

1.5

<300 3 3 #DIV/0! 1.0 #DIV/0! #DIV/0! #DIV/0! 0.3 0.3 #DIV/0! ###### 1.0 #DIV/0!

1000-3000 7 23 #DIV/0! 2.7 1.3 3.2 #DIV/0! 1.7 4.0 5.0 ###### ###### #DIV/0!

300-500 8 18 1.0 2.0 1.7 2.0 1.0 1.1 1.8 #DIV/0! ###### ###### #DIV/0!

500-1000 12 28 1.8 1.3 1.9 2.7 1.0 1.9 3.7 1.0 ###### 2.0 #DIV/0!

250-300K 6 28 13.5 6.3 3.5 10.3 2.0 7.7 13.2

8.0

2.0

1000-3000 3 16 9.0 7.0 2.7 9.5 2.0 7.3 14.3 #DIV/0! ###### ###### #DIV/0!

300-500 1 1 #DIV/0! 2.0 1.0 #DIV/0! #DIV/0! 3.0 3.0 #DIV/0! ###### ###### #DIV/0!

500-1000 2 10 18.0 9.0 6.0 12.0 #DIV/0! 10.5 16.5 #DIV/0! 8.0 ###### 2.0

300-500K 12 57 14.4 7.8 5.3 17.0 1.0 9.3 19.5 4.8 7.5 4.3 10.0

<300 1 0 #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0! - - #DIV/0! ###### ###### #DIV/0!

1000-3000 1 2 #DIV/0! 1.0 1.0 4.0 #DIV/0! 2.0 6.0 2.0 ###### ###### #DIV/0!

3000-5000 1 10 19.0 19.0 9.0 54.0 1.0 28.0 83.0 2.0 18.0 8.0 8.0

300-500 2 3 1.0 2.0 2.0 #DIV/0! #DIV/0! 3.0 3.0 #DIV/0! ###### 2.0 #DIV/0!

5000+ 4 35 17.3 14.7 7.0 12.8 1.0 18.0 31.0 9.5 4.0 3.5 11.0

500-1000 3 8 #DIV/0! 1.0 2.0 10.0 1.0 1.3 5.0 1.0 ###### ###### #DIV/0!

500K+ 2 3

4.0 2.5 6.0 6.5 9.5 4.0

1.0

1000-3000 2 3 #DIV/0! 4.0 2.5 6.0 #DIV/0! 6.5 9.5 4.0 ###### 1.0 #DIV/0!

Gujarat 26 55 3.0 1.6 2.0 3.6 1.0 1.3 2.1 1.0

<300 12 19 2.0 1.0 2.0 1.0 1.0 0.9 1.1 #DIV/0! ###### ###### #DIV/0!

1000-3000 1 0 1.0 #DIV/0! #DIV/0! #DIV/0! #DIV/0! - - #DIV/0! ###### ###### #DIV/0!

300-500 5 13 2.5 1.0 1.0 #DIV/0! 1.0 0.6 0.8 #DIV/0! ###### ###### #DIV/0!

500-1000 8 22 3.7 2.3 2.5 4.3 1.0 2.4 4.8 1.0 ###### ###### #DIV/0!

Grand Total 495 1,122 3.2 2.4 1.9 5.7 1.0 1.0 1.9 4.1 6.5 2.8 6.6

Source: Company, HSIE Research, Note: BB – Big Bazaar, S+F+M+BB = Reliance (grocery segment) +Big Bazaar

Back of the envelop calculations suggests DMART caters to 25%+ of the

household universe in top 7 districts. Share gains for DMART in these

catchments are unlikely as the merged entity - Reliance Retail + FRL (given

improved store density + Jiomart sales) could enjoy similar sourcing margins

(these are typically negotiated catchment-wise). Consequently, latter is likely to

be as competitive as DMART over the medium to long term.

DMART’s household share gain in top districts seems restricted from hereon FY20 DMART Bill cuts (mn) 201

Assuming 35% of bil cuts come from Top 7 Districts 70

No. Of HH catered to by Top 7 Districts 4

No. Of HH in Top 7 Districts 15

Purchase frequency/year 18

No. Of stores in Top 7 Districts 106

Bill cuts/store/day 1,818

HH share in 7 Districts (%) 25.9

Source: Company, HSIE Research Note: HH - Household

Page 12

Page | 11

F&G: Sector Thematic

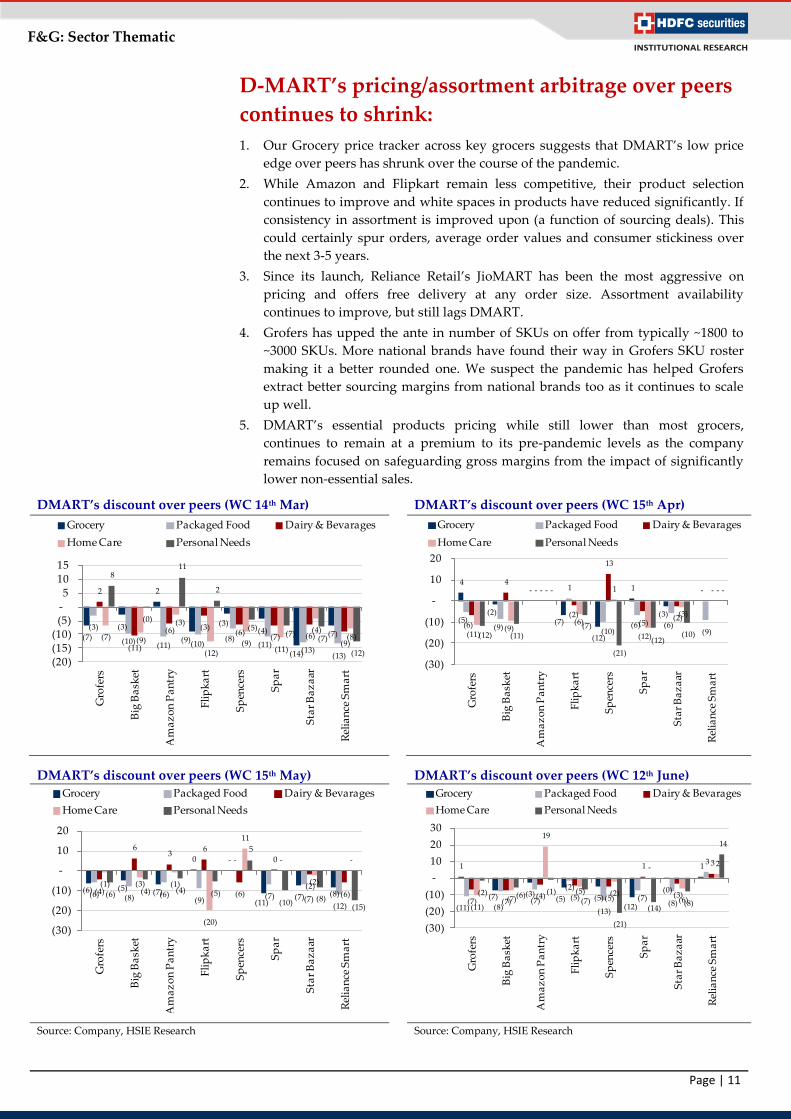

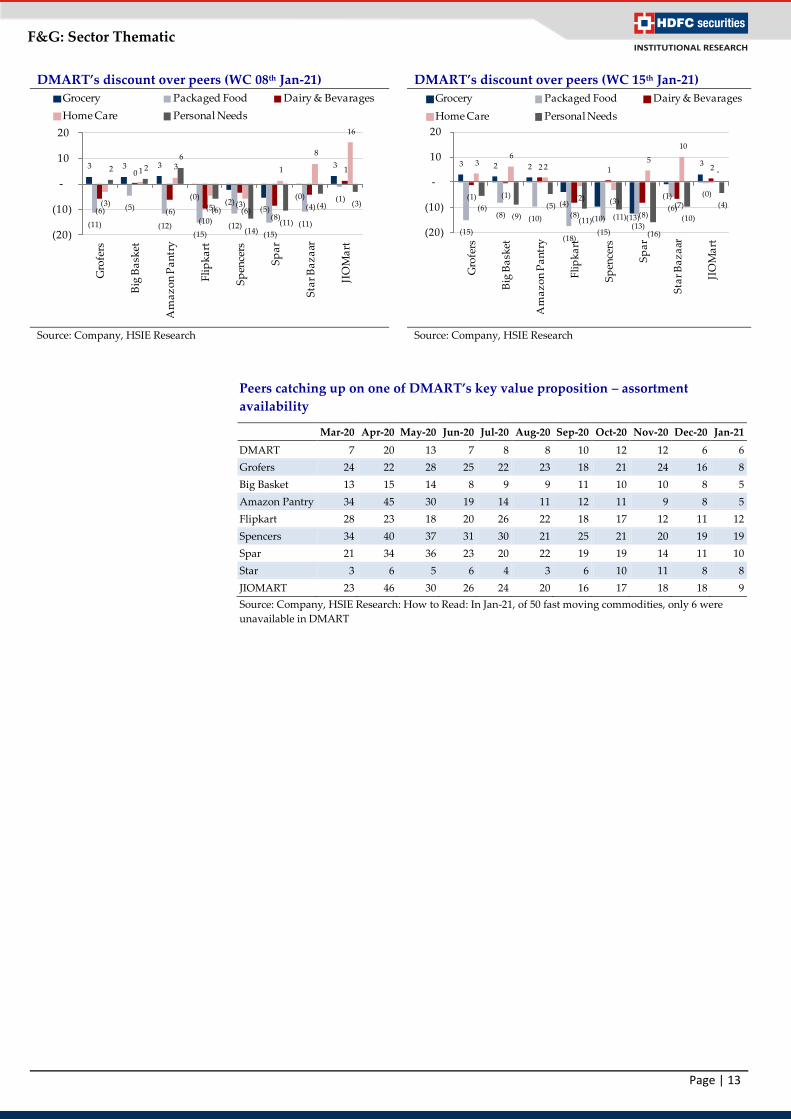

D-MART’s pricing/assortment arbitrage over peers

continues to shrink:

1. Our Grocery price tracker across key grocers suggests that DMART’s low price

edge over peers has shrunk over the course of the pandemic.

2. While Amazon and Flipkart remain less competitive, their product selection

continues to improve and white spaces in products have reduced significantly. If

consistency in assortment is improved upon (a function of sourcing deals). This

could certainly spur orders, average order values and consumer stickiness over

the next 3-5 years.

3. Since its launch, Reliance Retail’s JioMART has been the most aggressive on

pricing and offers free delivery at any order size. Assortment availability

continues to improve, but still lags DMART.

4. Grofers has upped the ante in number of SKUs on offer from typically ~1800 to

~3000 SKUs. More national brands have found their way in Grofers SKU roster

making it a better rounded one. We suspect the pandemic has helped Grofers

extract better sourcing margins from national brands too as it continues to scale

up well.

5. DMART’s essential products pricing while still lower than most grocers,

continues to remain at a premium to its pre-pandemic levels as the company

remains focused on safeguarding gross margins from the impact of significantly

lower non-essential sales.

DMART’s discount over peers (WC 14th Mar)

DMART’s discount over peers (WC 15th Apr)

DMART’s discount over peers (WC 15th May) DMART’s discount over peers (WC 12th June)

Source: Company, HSIE Research Source: Company, HSIE Research

(7)

(3)

2

(9)

(3)(4)

(14)

(7)(3)

(10) (11) (10)(8)

(11)(13)

(13)

2

(11)

(6) (3)(6)

(7) (6)(9)

(7) (9)

(3)

(12)(9)

(11)

(4)(8)

8

(0)

11

2

(5)(7)

(7)

(12)(20)(15)(10)

(5)-5

10 15

Gro

fers

Big

Ba

sket

Am

az

on

Pa

ntr

y

Fli

pk

art

Sp

ence

rs

Sp

ar

Sta

r B

az

aar

Rel

ian

ce S

ma

rt

Grocery Packaged Food Dairy & Bevarages

Home Care Personal Needs

4

(2)

-

(7)

(12)

1

(3)

-

(5)(9)

- 1

(10)(6) (6)

(9)(6)

4 -

(2)

13

(5)(2)

-

(11)(9)

-

(6)

1

(12)

(3)

-

(12) (11)

-

(7)

(21)

(12)(10)

-

(30)

(20)

(10)

-

10

20

Gro

fers

Big

Ba

sket

Am

az

on

Pa

ntr

y

Fli

pk

art

Sp

ence

rs

Sp

ar

Sta

r B

az

aar

Rel

ian

ce S

ma

rt

Grocery Packaged Food Dairy & Bevarages

Home Care Personal Needs

(6) (5) (7)

0 -

(11)(7) (8)(6) (8) (6)

(9)

-

(7) (7)(12)

(4)

6 3

6

(6)

0

(2)(6)

(1) (3) (1)

(20)

11

-

(2)

-

(6) (4) (4) (5)

5

(10) (8)(15)

(30)

(20)

(10)

-

10

20

Gro

fers

Big

Ba

sket

Am

az

on

Pa

ntr

y

Fli

pk

art

Sp

ence

rs

Sp

ar

Sta

r B

az

aar

Rel

ian

ce S

ma

rt

Grocery Packaged Food Dairy & Bevarages

Home Care Personal Needs

1

(7) (3)(5) (5)

(12)

(0)

1

(11) (8)(7)

(2)

(13)

(7)(8)

3

(7) (7)(4) (5) (5)

1

(3)

3

(11)(7)

19

(5) (2)

-

(6)

2

(2) (6) (1)(7)

(21)

(14)(8)

14

(30)

(20)

(10)

-

10

20

30

Gro

fers

Big

Ba

sket

Am

az

on

Pa

ntr

y

Fli

pk

art

Sp

ence

rs

Sp

ar

Sta

r B

az

aar

Rel

ian

ce S

ma

rt

Grocery Packaged Food Dairy & Bevarages

Home Care Personal Needs

Page 13

Page | 12

F&G: Sector Thematic

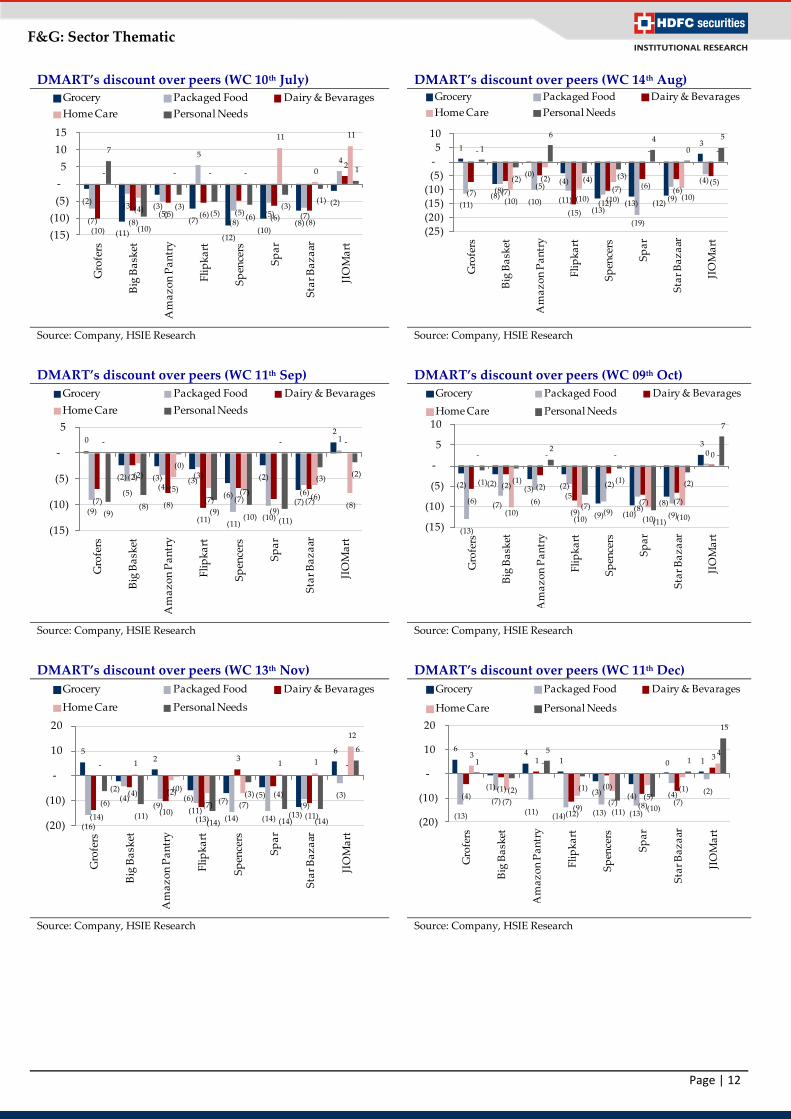

DMART’s discount over peers (WC 10th July) DMART’s discount over peers (WC 14th Aug)

Source: Company, HSIE Research Source: Company, HSIE Research

DMART’s discount over peers (WC 11th Sep) DMART’s discount over peers (WC 09th Oct)

Source: Company, HSIE Research Source: Company, HSIE Research

DMART’s discount over peers (WC 13th Nov) DMART’s discount over peers (WC 11th Dec)

Source: Company, HSIE Research Source: Company, HSIE Research

(2)

(11)

(3)

(7)

(12)(10)

(8)

(2)

(7)

(3)(5)

5

(8)(5) (7)

4

(10)(8)

(5) (6) (5)(6)

(8)

2 -

(4)

- - -

11

0

11

7

(10)

(3)(5) (6)

(3)(1)

1

(15)

(10)

(5)

-

5

10

15

Gro

fers

Big

Ba

sket

Am

az

on

Pa

ntr

y

Fli

pk

art

Sp

ence

rs

Sp

ar

Sta

r B

az

aar

JIO

Ma

rt

Grocery Packaged Food Dairy & Bevarages

Home Care Personal Needs

1

(8)

(0)(4)

(13)(13) (12)

3

(11)

(8)

(10) (11) (12)

(19)

(9)

(4)

(7) (7)(5)

(15)

(10)

(6)(6)

(5)

-

(10)

(2)

(10)(7)

-

(10)

-1

(2)

6

(4) (3)

4

0

5

(25)

(20)

(15)

(10)

(5)

-

5

10

Gro

fers

Big

Ba

sket

Am

az

on

Pa

ntr

y

Fli

pk

art

Sp

ence

rs

Sp

ar

Sta

r B

az

aar

JIO

Ma

rt

Grocery Packaged Food Dairy & Bevarages

Home Care Personal Needs

(2) (2)(3) (2)

(9) (10)

(8)

3

(13)

(7) (6)(5)

(9) (8)(9)

0

(6)

(2) (2)

(9)

(2)

(7) (7)

0 -

(10)

-

(10)

-

(10) (10)

-

(1) (1)

2

(7)

(1)

(11)

(2)

7

(15)

(10)

(5)

-

5

10

Gro

fers

Big

Ba

sket

Am

az

on

Pa

ntr

y

Fli

pk

art

Sp

ence

rs

Sp

ar

Sta

r B

az

aar

JIO

Ma

rt

Grocery Packaged Food Dairy & Bevarages

Home Care Personal Needs

6

(1)

4 1

(3) (4)

0 1

(13)

(7)

(11)(14) (13) (13)

(4) (2)(4)

(1)

1

(12)

(0)

(8) (7)

3 3

(7)

-

(9)(7)

(5)(1)

4 1

(2)

5

(1)

(11) (10)

1

15

(20)

(10)

-

10

20

Gro

fers

Big

Ba

sket

Am

az

on

Pa

ntr

y

Fli

pk

art

Sp

ence

rs

Sp

ar

Sta

r B

az

aar

JIO

Ma

rt

Grocery Packaged Food Dairy & Bevarages

Home Care Personal Needs

0

(2) (3) (3)

(6)

(2)

(7)

2

(9)

(5)(4)

(3)

(11)(10)

(6)

1

(7)

(2)

(8)

(11)

(7)

(9)(7)

--

(2)

(5)

(7)(7)

-

(6)(8)

(9)(8)

(0)

(9)(10) (11)

(3)(2)

(15)

(10)

(5)

-

5

Gro

fers

Big

Ba

sket

Am

az

on

Pa

ntr

y

Fli

pk

art

Sp

ence

rs

Sp

ar

Sta

r B

az

aar

JIO

Ma

rt

Grocery Packaged Food Dairy & Bevarages

Home Care Personal Needs

5

(2)

2

(6) (7)(5)

(13)

6

(16)

(4)(9)

(11)(14) (14)

(9)

(3)

(14)

(4)

(10)(13)

3

(4)

(11)

-- 1

(2)

(7) (7)

1 1

12

(6)

(11)

(0)

(14)

(3)

(14) (14)

6

(20)

(10)

-

10

20

Gro

fers

Big

Ba

sket

Am

az

on

Pa

ntr

y

Fli

pk

art

Sp

ence

rs

Sp

ar

Sta

r B

az

aar

JIO

Ma

rt

Grocery Packaged Food Dairy & Bevarages

Home Care Personal Needs

Page 14

Page | 13

F&G: Sector Thematic

DMART’s discount over peers (WC 08th Jan-21) DMART’s discount over peers (WC 15th Jan-21)

Source: Company, HSIE Research Source: Company, HSIE Research

Peers catching up on one of DMART’s key value proposition – assortment

availability

Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21

DMART 7 20 13 7 8 8 10 12 12 6 6

Grofers 24 22 28 25 22 23 18 21 24 16 8

Big Basket 13 15 14 8 9 9 11 10 10 8 5

Amazon Pantry 34 45 30 19 14 11 12 11 9 8 5

Flipkart 28 23 18 20 26 22 18 17 12 11 12

Spencers 34 40 37 31 30 21 25 21 20 19 19

Spar 21 34 36 23 20 22 19 19 14 11 10

Star 3 6 5 6 4 3 6 10 11 8 8

JIOMART 23 46 30 26 24 20 16 17 18 18 9

Source: Company, HSIE Research: How to Read: In Jan-21, of 50 fast moving commodities, only 6 were

unavailable in DMART

3 3 3

(0)(2)

(5)

(0)

3

(11)

(5)

(12)(15)

(12)(15)

(11)

(1)

(6)

0

(6)(10)

(3)

(8)

(4)

1

(3)

1 3

(5) (6)

1

8

16

2 2

6

(6)

(14)(11)

(4) (3)

(20)

(10)

-

10

20

Gro

fers

Big

Ba

sket

Am

az

on

Pa

ntr

y

Fli

pk

art

Sp

ence

rs

Sp

ar

Sta

r B

az

aar

JIO

Ma

rt

Grocery Packaged Food Dairy & Bevarages

Home Care Personal Needs

3 2 2

(4)

(10) (13)

(1)

3

(15)

(8) (10)

(18)(15)

(13)

(6)

(0)(1) (1)

2

(8)

1

(8)(7)

2 3

6

2

(2) (3)

5

10

-

(6)(9)

(5)

(11) (11)

(16)

(10)

(4)

(20)

(10)

-

10

20

Gro

fers

Big

Ba

sket

Am

az

on

Pa

ntr

y

Fli

pk

art

Sp

ence

rs

Sp

ar

Sta

r B

az

aar

JIO

Ma

rt

Grocery Packaged Food Dairy & Bevarages

Home Care Personal Needs

Page 15

Page | 14

F&G: Sector Thematic

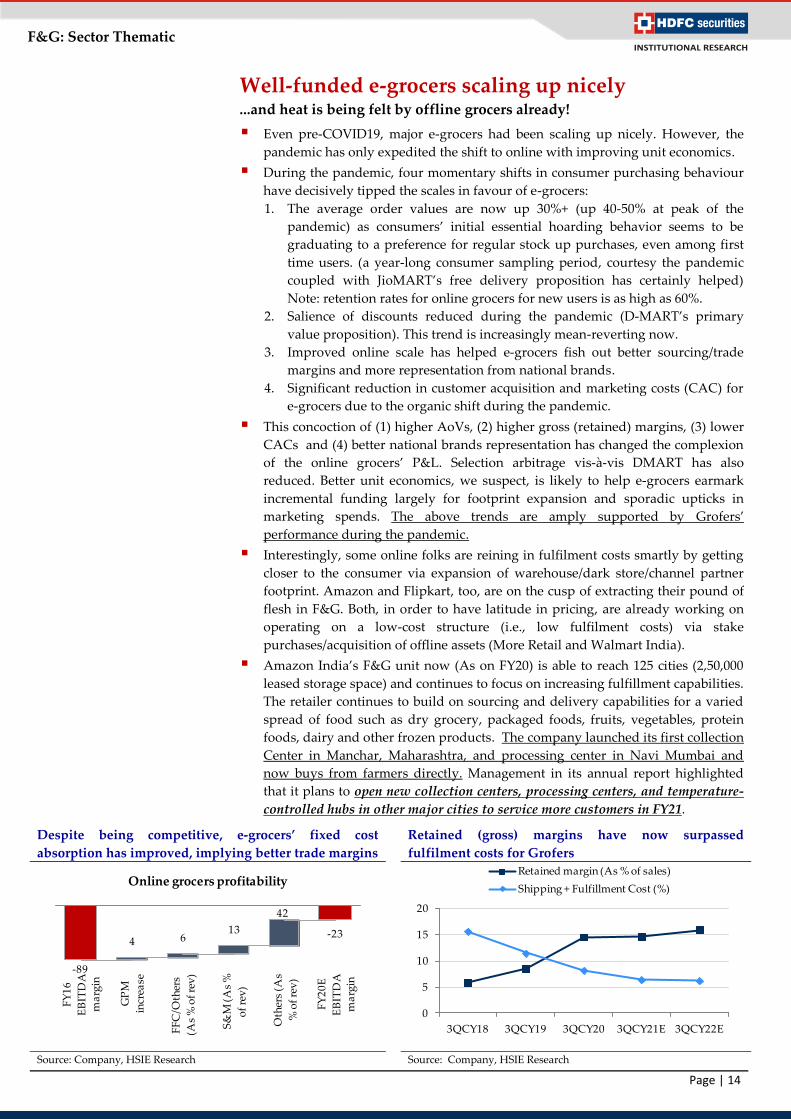

Well-funded e-grocers scaling up nicely ...and heat is being felt by offline grocers already!

Even pre-COVID19, major e-grocers had been scaling up nicely. However, the

pandemic has only expedited the shift to online with improving unit economics.

During the pandemic, four momentary shifts in consumer purchasing behaviour

have decisively tipped the scales in favour of e-grocers:

1. The average order values are now up 30%+ (up 40-50% at peak of the

pandemic) as consumers’ initial essential hoarding behavior seems to be

graduating to a preference for regular stock up purchases, even among first

time users. (a year-long consumer sampling period, courtesy the pandemic

coupled with JioMART’s free delivery proposition has certainly helped)

Note: retention rates for online grocers for new users is as high as 60%.

2. Salience of discounts reduced during the pandemic (D-MART’s primary

value proposition). This trend is increasingly mean-reverting now.

3. Improved online scale has helped e-grocers fish out better sourcing/trade

margins and more representation from national brands.

4. Significant reduction in customer acquisition and marketing costs (CAC) for

e-grocers due to the organic shift during the pandemic.

This concoction of (1) higher AoVs, (2) higher gross (retained) margins, (3) lower

CACs and (4) better national brands representation has changed the complexion

of the online grocers’ P&L. Selection arbitrage vis-à-vis DMART has also

reduced. Better unit economics, we suspect, is likely to help e-grocers earmark

incremental funding largely for footprint expansion and sporadic upticks in

marketing spends. The above trends are amply supported by Grofers’

performance during the pandemic.

Interestingly, some online folks are reining in fulfilment costs smartly by getting

closer to the consumer via expansion of warehouse/dark store/channel partner

footprint. Amazon and Flipkart, too, are on the cusp of extracting their pound of

flesh in F&G. Both, in order to have latitude in pricing, are already working on

operating on a low-cost structure (i.e., low fulfilment costs) via stake

purchases/acquisition of offline assets (More Retail and Walmart India).

Amazon India’s F&G unit now (As on FY20) is able to reach 125 cities (2,50,000

leased storage space) and continues to focus on increasing fulfillment capabilities.

The retailer continues to build on sourcing and delivery capabilities for a varied

spread of food such as dry grocery, packaged foods, fruits, vegetables, protein

foods, dairy and other frozen products. The company launched its first collection

Center in Manchar, Maharashtra, and processing center in Navi Mumbai and

now buys from farmers directly. Management in its annual report highlighted

that it plans to open new collection centers, processing centers, and temperature-

controlled hubs in other major cities to service more customers in FY21.

Despite being competitive, e-grocers’ fixed cost

absorption has improved, implying better trade margins

Retained (gross) margins have now surpassed

fulfilment costs for Grofers

Source: Company, HSIE Research Source: Company, HSIE Research

-89

-23 4 6

13

42

FY

16

EB

ITD

A

ma

rgin

GP

M

incr

ease

FF

C/O

ther

s

(As

% o

f re

v)

S&

M (

As

%

of

rev

)

Oth

ers

(As

% o

f re

v)

FY

20

E

EB

ITD

A

ma

rgin

Online grocers profitability

0

5

10

15

20

3QCY18 3QCY19 3QCY20 3QCY21E 3QCY22E

Retained margin (As % of sales)

Shipping + Fulfillment Cost (%)

Page 16

Page | 15

F&G: Sector Thematic

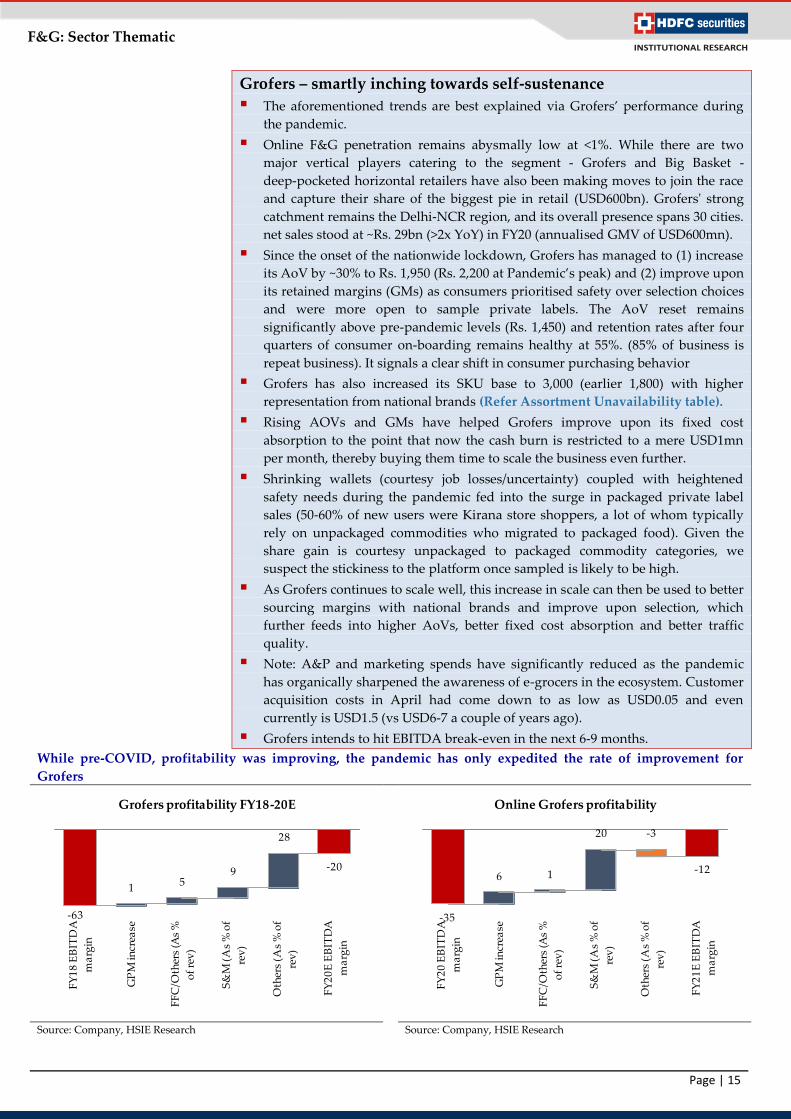

Grofers – smartly inching towards self-sustenance

The aforementioned trends are best explained via Grofers’ performance during

the pandemic.

Online F&G penetration remains abysmally low at <1%. While there are two

major vertical players catering to the segment ‐ Grofers and Big Basket -

deep‐pocketed horizontal retailers have also been making moves to join the race

and capture their share of the biggest pie in retail (USD600bn). Grofers' strong

catchment remains the Delhi‐NCR region, and its overall presence spans 30 cities.

net sales stood at ~Rs. 29bn (>2x YoY) in FY20 (annualised GMV of USD600mn).

Since the onset of the nationwide lockdown, Grofers has managed to (1) increase

its AoV by ~30% to Rs. 1,950 (Rs. 2,200 at Pandemic’s peak) and (2) improve upon

its retained margins (GMs) as consumers prioritised safety over selection choices

and were more open to sample private labels. The AoV reset remains

significantly above pre-pandemic levels (Rs. 1,450) and retention rates after four

quarters of consumer on-boarding remains healthy at 55%. (85% of business is

repeat business). It signals a clear shift in consumer purchasing behavior

Grofers has also increased its SKU base to 3,000 (earlier 1,800) with higher

representation from national brands (Refer Assortment Unavailability table).

Rising AOVs and GMs have helped Grofers improve upon its fixed cost

absorption to the point that now the cash burn is restricted to a mere USD1mn

per month, thereby buying them time to scale the business even further.

Shrinking wallets (courtesy job losses/uncertainty) coupled with heightened

safety needs during the pandemic fed into the surge in packaged private label

sales (50-60% of new users were Kirana store shoppers, a lot of whom typically

rely on unpackaged commodities who migrated to packaged food). Given the

share gain is courtesy unpackaged to packaged commodity categories, we

suspect the stickiness to the platform once sampled is likely to be high.

As Grofers continues to scale well, this increase in scale can then be used to better

sourcing margins with national brands and improve upon selection, which

further feeds into higher AoVs, better fixed cost absorption and better traffic

quality.

Note: A&P and marketing spends have significantly reduced as the pandemic

has organically sharpened the awareness of e-grocers in the ecosystem. Customer

acquisition costs in April had come down to as low as USD0.05 and even

currently is USD1.5 (vs USD6-7 a couple of years ago).

Grofers intends to hit EBITDA break-even in the next 6-9 months.

While pre-COVID, profitability was improving, the pandemic has only expedited the rate of improvement for

Grofers

Source: Company, HSIE Research

Source: Company, HSIE Research

-63

-20

1 5

9

28

FY

18

EB

ITD

A

ma

rgin

GP

M in

crea

se

FF

C/O

ther

s (A

s %

of

rev

)

S&

M (

As

% o

f

rev

)

Oth

ers

(As

% o

f

rev

)

FY

20

E E

BIT

DA

ma

rgin

Grofers profitability FY18-20E

-35

-12 6 1

20 -3

FY

20

EB

ITD

A

ma

rgin

GP

M in

crea

se

FF

C/O

ther

s (A

s %

of

rev

)

S&

M (

As

% o

f

rev

)

Oth

ers

(As

% o

f

rev

)

FY

21

E E

BIT

DA

ma

rgin

Online Grofers profitability

Page 17

Page | 16

F&G: Sector Thematic

The heat is being felt by offline grocers already

The heat is being felt by offline grocers already and their actions continue to corroborate the increasing preference

for online and omni investments!

“Price discounting has gone up in the last 1-1.5 years. This is a new variable playing out as earlier competition was not

discounting as much as they have begun in the last 12 to 18 months. Hence, it is very tough to predict what will happen

next year” - FY19 Avenue Supermarts’ Annual Analyst Meet

“There continues to be a distinct behaviour of shopping more efficiently by shoppers. Lesser trips and higher basket

values continue to be the norm. While there is a general reduction in basket values compared to peak pandemic levels,

they still continue to be relatively higher than pre-COVID levels”. This coupled with DMART’s 3QFY21 growth rate

(10%) suggests that footfall recovery hasn’t yet reached the pre-COVID level.

“Post COVID-19, environment is creating opportunities to launch DMart Ready in more cities. However, we will

continue with our approach of small trials, reviews and controlled acceleration for DMart Ready” – Commentary in

3QFY21 results

- CEO Neville Noronha -

“We witnessed deep and consistent investment in pricing by brick-and-mortar retailers, primarily to match and/or

ward off e-commerce players who were aggressively focused on customer acquisition and, hence, are passing on huge

benefits to recruit customers. This aggressive push by e-commerce has started impacting offline monthly shopping

missions, forcing brick-and-mortar retailers to follow suit in order to stay competitive and relevant for the customer.

As seen in other markets, we expect India to go through this phase of intensive price-based competition before

reaching a mature environment”

-ABRL (now More Retail) in its FY19 Annual Report

“Company expects the pandemic-led challenges to continue. The customer is changing the way he/she shops. There is a

significant share of orders moving to online platforms, and the company is making sure to fulfill all the customer’s

requirement”

– More Retail (earlier ABRL) FY20 Annual Report.

“We revamped our pricing policy making great deals always available to more customers, provided greater choice

through a wide assortment and made it easier for our customers to shop with us with easy credit, payment and

delivery options. This resulted in a healthy double-digit growth in these core customer segments”.

“We further expanded our foot print with 5 new store openings in the cities of Vijaywada, Indore, Nizamabad,

Warangal and Kurnool, taking the total tally to eight new openings in the last 18 months. In line with our strategy to

build strong tech capability supporting superior omni-channel customer experience, we completed roll out of new

front-end system across all stores and introduced a digital solution for member on-boarding. We also launched a new

e-Commerce website & application to make it easier for our members to shop with us in ways that are most convenient

to them”

“Finally, our endeavor towards building capabilities for the future is continuing via investments to expand our Omni

channel reach. The increased capex during the year reflects the investments that we are making to build for long term

growth”.

“The management believes that it is in growth phase and had expected to incur losses for carrying wholesale cash and

carry business in India. The Company has got a commitment of continued financial support from the Ultimate Holding

Company (Walmart Inc.) to contribute to the shortfall of the capital requirements, if any”.

- Walmart India in its FY20 Annual Report

Page 18

Page | 17

F&G: Sector Thematic

Comparative Analysis

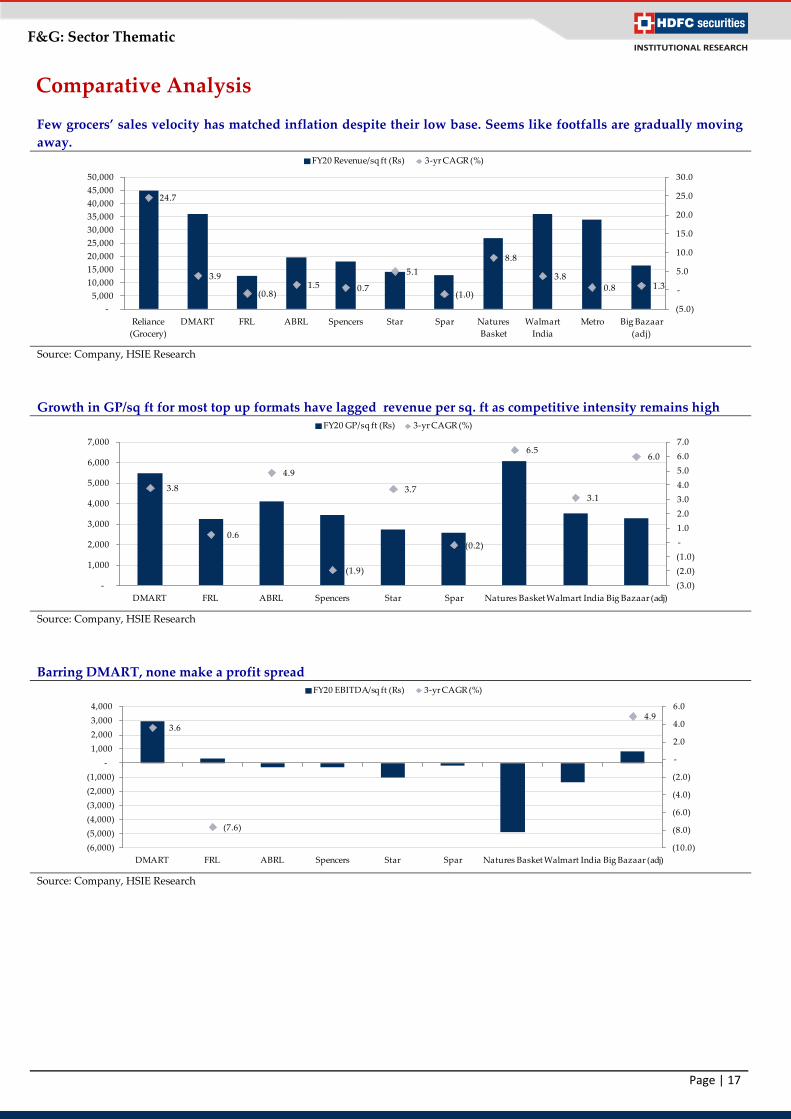

Few grocers’ sales velocity has matched inflation despite their low base. Seems like footfalls are gradually moving

away.

Source: Company, HSIE Research

Growth in GP/sq ft for most top up formats have lagged revenue per sq. ft as competitive intensity remains high

Source: Company, HSIE Research

Barring DMART, none make a profit spread

Source: Company, HSIE Research

24.7

3.9

(0.8)1.5 0.7

5.1

(1.0)

8.8

3.8

0.8 1.3

(5.0)

-

5.0

10.0

15.0

20.0

25.0

30.0

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Reliance

(Grocery)

DMART FRL ABRL Spencers Star Spar Natures

Basket

Walmart

India

Metro Big Bazaar

(adj)

FY20 Revenue/sq ft (Rs) 3-yr CAGR (%)

3.8

0.6

4.9

(1.9)

3.7

(0.2)

6.5

3.1

6.0

(3.0)

(2.0)

(1.0)

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

DMART FRL ABRL Spencers Star Spar Natures BasketWalmart India Big Bazaar (adj)

FY20 GP/sq ft (Rs) 3-yr CAGR (%)

3.6

(7.6)

4.9

(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

-

2.0

4.0

6.0

(6,000)

(5,000)

(4,000)

(3,000)

(2,000)

(1,000)

-

1,000

2,000

3,000

4,000

DMART FRL ABRL Spencers Star Spar Natures Basket Walmart India Big Bazaar (adj)

FY20 EBITDA/sq ft (Rs) 3-yr CAGR (%)

Page 19

Page | 18

F&G: Sector Thematic

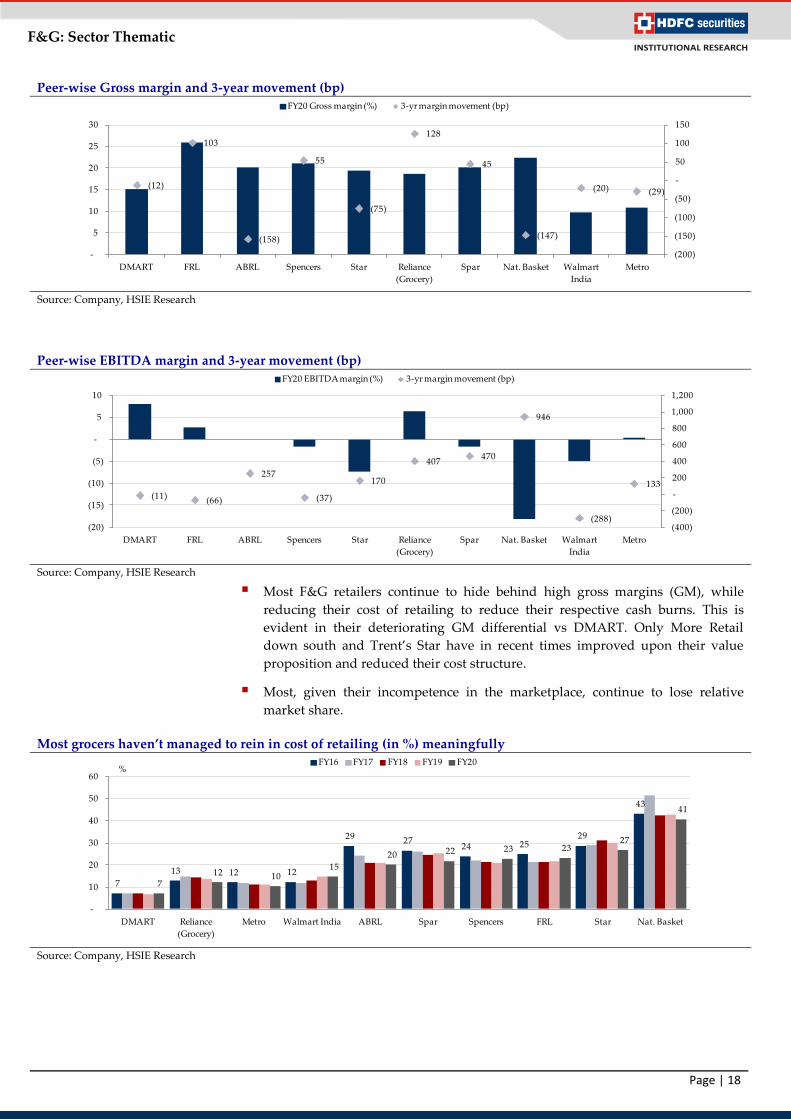

Peer-wise Gross margin and 3-year movement (bp)

Source: Company, HSIE Research

Peer-wise EBITDA margin and 3-year movement (bp)

Source: Company, HSIE Research

Most F&G retailers continue to hide behind high gross margins (GM), while

reducing their cost of retailing to reduce their respective cash burns. This is

evident in their deteriorating GM differential vs DMART. Only More Retail

down south and Trent’s Star have in recent times improved upon their value

proposition and reduced their cost structure.

Most, given their incompetence in the marketplace, continue to lose relative

market share.

Most grocers haven’t managed to rein in cost of retailing (in %) meaningfully

Source: Company, HSIE Research

(12)

103

(158)

55

(75)

128

45

(147)

(20) (29)

(200)

(150)

(100)

(50)

-

50

100

150

-

5

10

15

20

25

30

DMART FRL ABRL Spencers Star Reliance

(Grocery)

Spar Nat. Basket Walmart

India

Metro

FY20 Gross margin (%) 3-yr margin movement (bp)

(11) (66)

257

(37)

170

407 470

946

(288)

133

(400)

(200)

-

200

400

600

800

1,000

1,200

(20)

(15)

(10)

(5)

-

5

10

DMART FRL ABRL Spencers Star Reliance

(Grocery)

Spar Nat. Basket Walmart

India

Metro

FY20 EBITDA margin (%) 3-yr margin movement (bp)

7

13 12 12

29 27 24 25

29

43

7 12 10

15

20 22 23 23 27

41

-

10

20

30

40

50

60

DMART Reliance

(Grocery)

Metro Walmart India ABRL Spar Spencers FRL Star Nat. Basket

FY16 FY17 FY18 FY19 FY20%

Page 20

Page | 19

F&G: Sector Thematic

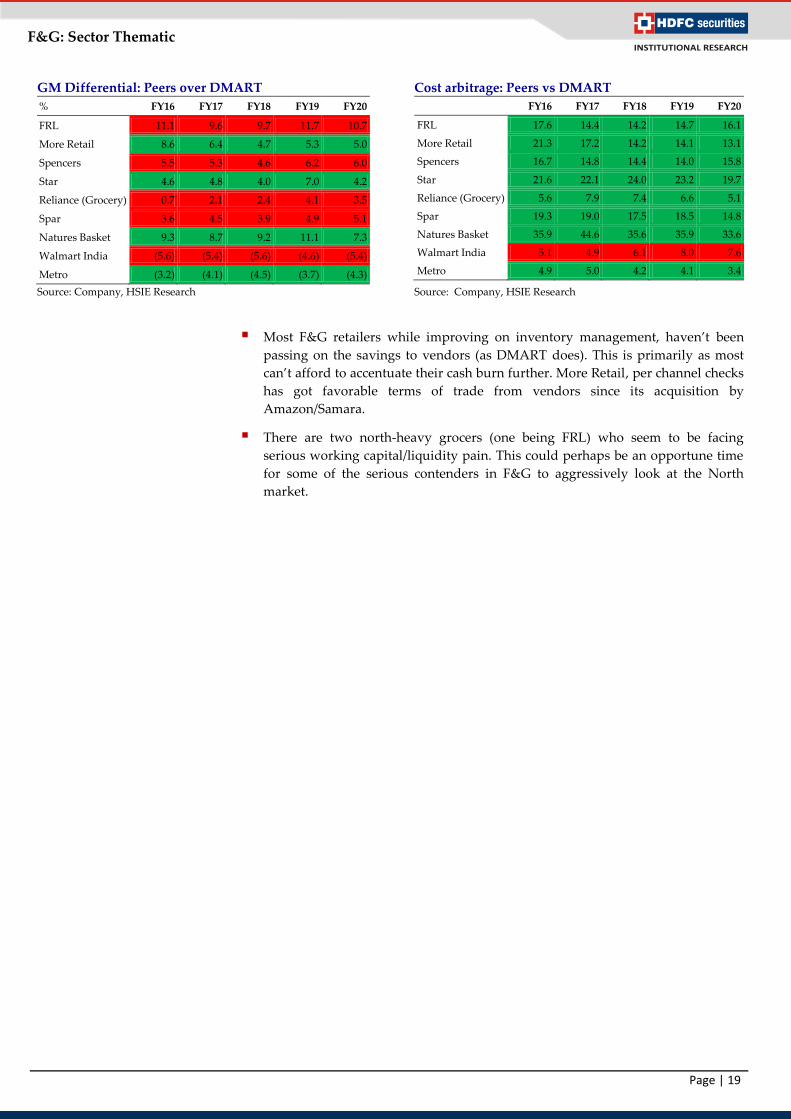

GM Differential: Peers over DMART Cost arbitrage: Peers vs DMART

% FY16 FY17 FY18 FY19 FY20

FRL 11.1 9.6 9.7 11.7 10.7

More Retail 8.6 6.4 4.7 5.3 5.0

Spencers 5.5 5.3 4.6 6.2 6.0

Star 4.6 4.8 4.0 7.0 4.2

Reliance (Grocery) 0.7 2.1 2.4 4.1 3.5

Spar 3.6 4.5 3.9 4.9 5.1

Natures Basket 9.3 8.7 9.2 11.1 7.3

Walmart India (5.6) (5.4) (5.6) (4.6) (5.4)

Metro (3.2) (4.1) (4.5) (3.7) (4.3)

FY16 FY17 FY18 FY19 FY20

FRL 17.6 14.4 14.2 14.7 16.1

More Retail 21.3 17.2 14.2 14.1 13.1

Spencers 16.7 14.8 14.4 14.0 15.8

Star 21.6 22.1 24.0 23.2 19.7

Reliance (Grocery) 5.6 7.9 7.4 6.6 5.1

Spar 19.3 19.0 17.5 18.5 14.8

Natures Basket 35.9 44.6 35.6 35.9 33.6

Walmart India 5.1 4.9 6.1 8.0 7.6

Metro 4.9 5.0 4.2 4.1 3.4

Source: Company, HSIE Research Source: Company, HSIE Research

Most F&G retailers while improving on inventory management, haven’t been

passing on the savings to vendors (as DMART does). This is primarily as most

can’t afford to accentuate their cash burn further. More Retail, per channel checks

has got favorable terms of trade from vendors since its acquisition by

Amazon/Samara.

There are two north-heavy grocers (one being FRL) who seem to be facing

serious working capital/liquidity pain. This could perhaps be an opportune time

for some of the serious contenders in F&G to aggressively look at the North

market.

Page 21

Page | 20

F&G: Sector Thematic

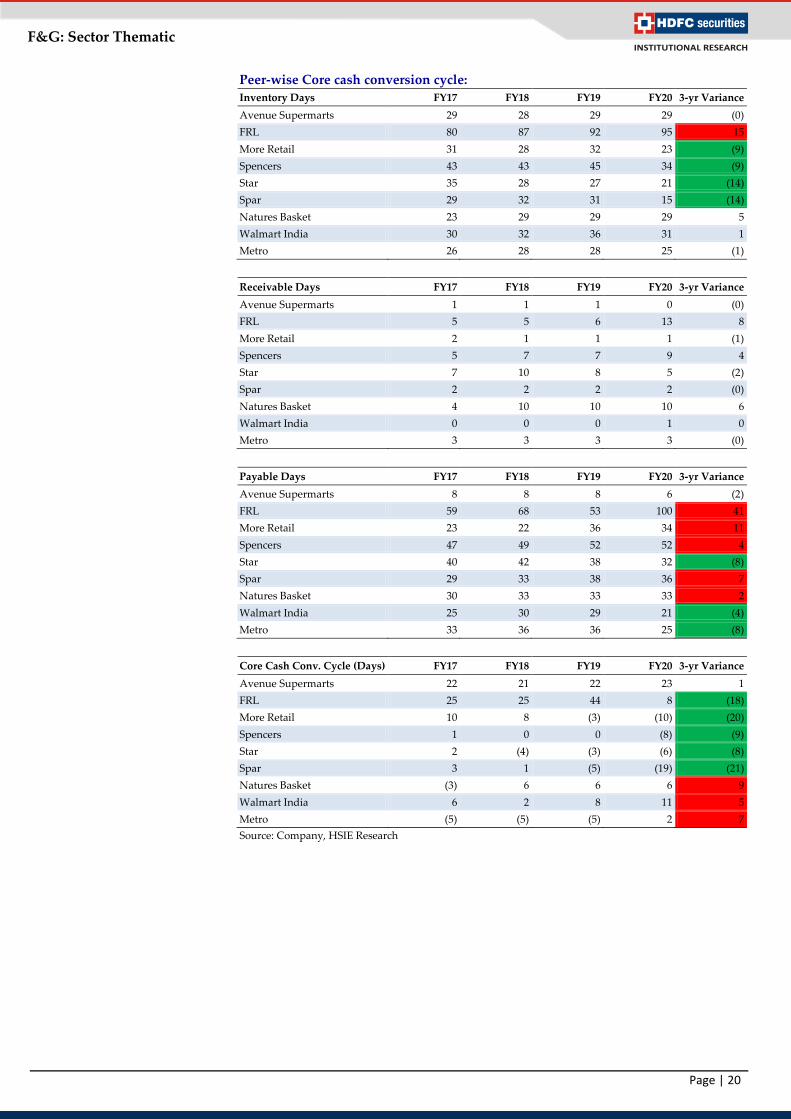

Peer-wise Core cash conversion cycle:

Inventory Days FY17 FY18 FY19 FY20 3-yr Variance

Avenue Supermarts 29 28 29 29 (0)

FRL 80 87 92 95 15

More Retail 31 28 32 23 (9)

Spencers 43 43 45 34 (9)

Star 35 28 27 21 (14)

Spar 29 32 31 15 (14)

Natures Basket 23 29 29 29 5

Walmart India 30 32 36 31 1

Metro 26 28 28 25 (1)

Receivable Days FY17 FY18 FY19 FY20 3-yr Variance

Avenue Supermarts 1 1 1 0 (0)

FRL 5 5 6 13 8

More Retail 2 1 1 1 (1)

Spencers 5 7 7 9 4

Star 7 10 8 5 (2)

Spar 2 2 2 2 (0)

Natures Basket 4 10 10 10 6

Walmart India 0 0 0 1 0

Metro 3 3 3 3 (0)

Payable Days FY17 FY18 FY19 FY20 3-yr Variance

Avenue Supermarts 8 8 8 6 (2)

FRL 59 68 53 100 41

More Retail 23 22 36 34 11

Spencers 47 49 52 52 4

Star 40 42 38 32 (8)

Spar 29 33 38 36 7

Natures Basket 30 33 33 33 2

Walmart India 25 30 29 21 (4)

Metro 33 36 36 25 (8)

Core Cash Conv. Cycle (Days) FY17 FY18 FY19 FY20 3-yr Variance

Avenue Supermarts 22 21 22 23 1

FRL 25 25 44 8 (18)

More Retail 10 8 (3) (10) (20)

Spencers 1 0 0 (8) (9)

Star 2 (4) (3) (6) (8)

Spar 3 1 (5) (19) (21)

Natures Basket (3) 6 6 6 9

Walmart India 6 2 8 11 5

Metro (5) (5) (5) 2 7

Source: Company, HSIE Research

Page 22

Page | 21

F&G: Sector Thematic

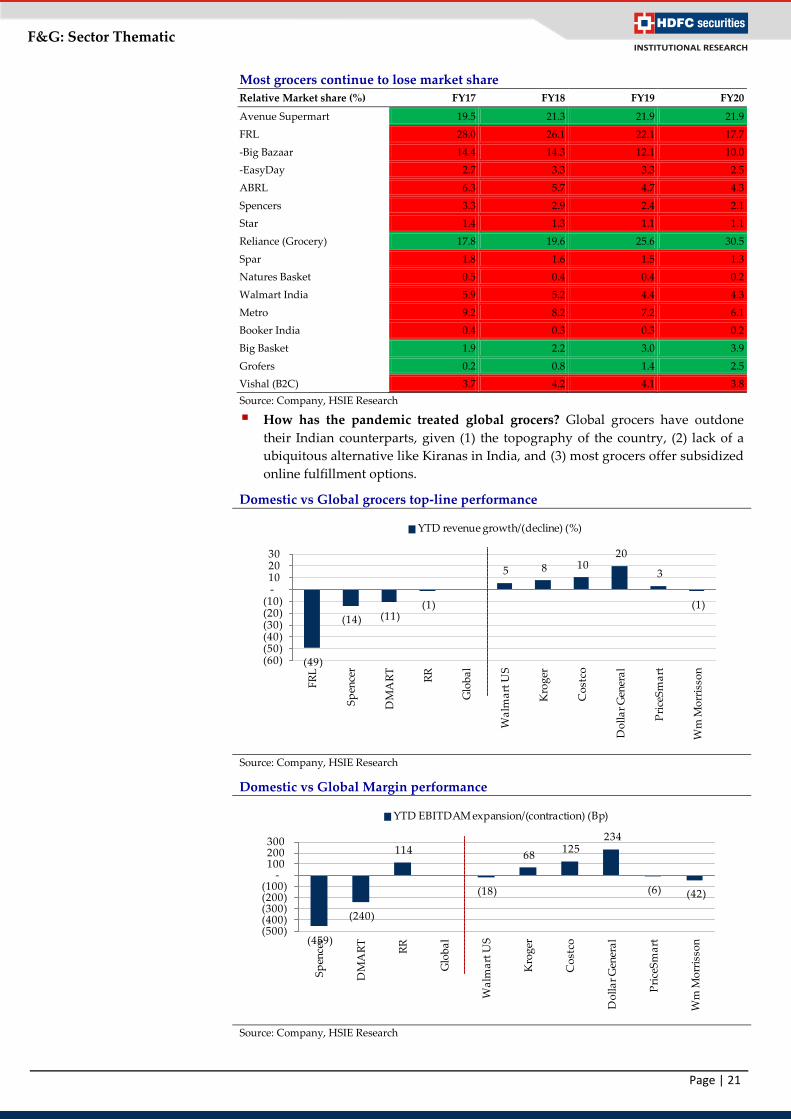

Most grocers continue to lose market share

Relative Market share (%) FY17 FY18 FY19 FY20

Avenue Supermart 19.5 21.3 21.9 21.9

FRL 28.0 26.1 22.1 17.7

-Big Bazaar 14.4 14.3 12.1 10.0

-EasyDay 2.7 3.3 3.3 2.5

ABRL 6.3 5.7 4.7 4.3

Spencers 3.3 2.9 2.4 2.1

Star 1.4 1.3 1.1 1.1

Reliance (Grocery) 17.8 19.6 25.6 30.5

Spar 1.8 1.6 1.5 1.3

Natures Basket 0.5 0.4 0.4 0.2

Walmart India 5.9 5.2 4.4 4.3

Metro 9.2 8.2 7.2 6.1

Booker India 0.4 0.3 0.3 0.2

Big Basket 1.9 2.2 3.0 3.9

Grofers 0.2 0.8 1.4 2.5

Vishal (B2C) 3.7 4.2 4.1 3.8

Source: Company, HSIE Research

How has the pandemic treated global grocers? Global grocers have outdone

their Indian counterparts, given (1) the topography of the country, (2) lack of a

ubiquitous alternative like Kiranas in India, and (3) most grocers offer subsidized

online fulfillment options.

Domestic vs Global grocers top-line performance

Source: Company, HSIE Research

Domestic vs Global Margin performance

Source: Company, HSIE Research

(49)

(14) (11)(1)

5 8 10 20

3

(1)

(60)(50)(40)(30)(20)(10)

-10 20 30

FR

L

Sp

ence

r

DM

AR

T

RR

Glo

ba

l

Wa

lma

rt U

S

Kro

ger

Co

stco

Do

lla

r G

ener

al

Pri

ceS

ma

rt

Wm

Mo

rris

son

YTD revenue growth/(decline) (%)

(459)

(240)

114

(18)

68 125

234

(6) (42)

(500)(400)(300)(200)(100)

-100 200 300

Sp

ence

r

DM

AR

T

RR

Glo

ba

l

Wa

lma

rt U

S

Kro

ger

Co

stco

Do

lla

r G

ener

al

Pri

ceS

ma

rt

Wm

Mo

rris

son

YTD EBITDAM expansion/(contraction) (Bp)

Page 23

Page | 22

F&G: Sector Thematic

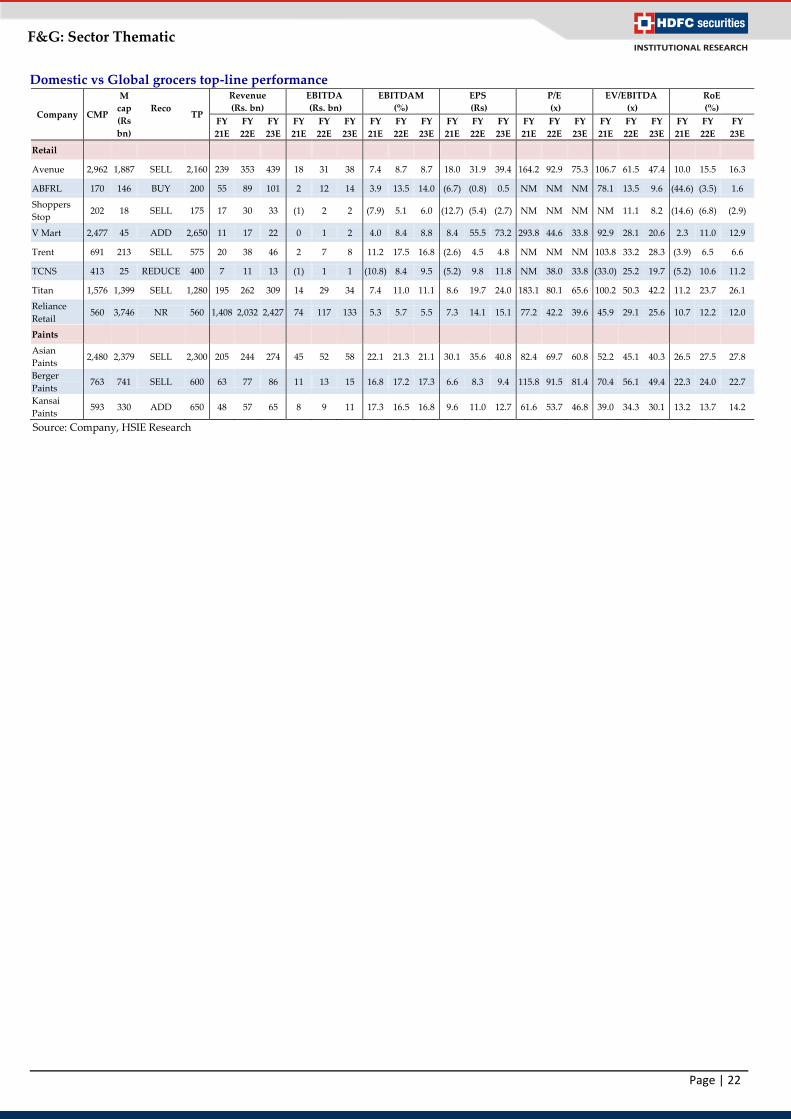

Domestic vs Global grocers top-line performance

Company CMP

M

cap

(Rs

bn)

Reco

TP

Revenue

(Rs. bn)

EBITDA

(Rs. bn)

EBITDAM

(%)

EPS

(Rs)

P/E

(x)

EV/EBITDA

(x)

RoE

(%)

FY

21E

FY

22E

FY

23E

FY

21E

FY

22E

FY

23E

FY

21E

FY

22E

FY

23E

FY

21E

FY

22E

FY

23E

FY

21E

FY

22E

FY

23E

FY

21E

FY

22E

FY

23E

FY

21E

FY

22E

FY

23E

Retail

Avenue 2,962 1,887 SELL 2,160 239 353 439 18 31 38 7.4 8.7 8.7 18.0 31.9 39.4 164.2 92.9 75.3 106.7 61.5 47.4 10.0 15.5 16.3

ABFRL 170 146 BUY 200 55 89 101 2 12 14 3.9 13.5 14.0 (6.7) (0.8) 0.5 NM NM NM 78.1 13.5 9.6 (44.6) (3.5) 1.6

Shoppers

Stop 202 18 SELL 175 17 30 33 (1) 2 2 (7.9) 5.1 6.0 (12.7) (5.4) (2.7) NM NM NM NM 11.1 8.2 (14.6) (6.8) (2.9)

V Mart 2,477 45 ADD 2,650 11 17 22 0 1 2 4.0 8.4 8.8 8.4 55.5 73.2 293.8 44.6 33.8 92.9 28.1 20.6 2.3 11.0 12.9

Trent 691 213 SELL 575 20 38 46 2 7 8 11.2 17.5 16.8 (2.6) 4.5 4.8 NM NM NM 103.8 33.2 28.3 (3.9) 6.5 6.6

TCNS 413 25 REDUCE 400 7 11 13 (1) 1 1 (10.8) 8.4 9.5 (5.2) 9.8 11.8 NM 38.0 33.8 (33.0) 25.2 19.7 (5.2) 10.6 11.2

Titan 1,576 1,399 SELL 1,280 195 262 309 14 29 34 7.4 11.0 11.1 8.6 19.7 24.0 183.1 80.1 65.6 100.2 50.3 42.2 11.2 23.7 26.1

Reliance

Retail 560 3,746 NR 560 1,408 2,032 2,427 74 117 133 5.3 5.7 5.5 7.3 14.1 15.1 77.2 42.2 39.6 45.9 29.1 25.6 10.7 12.2 12.0

Paints

Asian

Paints 2,480 2,379 SELL 2,300 205 244 274 45 52 58 22.1 21.3 21.1 30.1 35.6 40.8 82.4 69.7 60.8 52.2 45.1 40.3 26.5 27.5 27.8

Berger

Paints 763 741 SELL 600 63 77 86 11 13 15 16.8 17.2 17.3 6.6 8.3 9.4 115.8 91.5 81.4 70.4 56.1 49.4 22.3 24.0 22.7

Kansai

Paints 593 330 ADD 650 48 57 65 8 9 11 17.3 16.5 16.8 9.6 11.0 12.7 61.6 53.7 46.8 39.0 34.3 30.1 13.2 13.7 14.2

Source: Company, HSIE Research

Page 24

Page | 23

F&G: Sector Thematic

Thematic reports by HSIE

Cement: WHRS – A key cog in the

flywheel

Autos: Where are we on “S” curve? FMCG: Defensive businesses but

not valuations

Autos: A changed landscape Banks: Double whammy for some India Equity Strategy: Atma

Nirbhar Bharat

Indian IT: Demand recovery in

sight

Life Insurance: Recovery may be

swift with protection driving

margins

Retail: Whole flywheel is broken? Appliances: Looing beyond near-

term disruption

Pharma: Chronic therapy – A

portfolio prescription

Indian Gas: Looking beyond the

pandemic

India Equity Strategy: Quarterly

flipbook

Real Estate: Ripe for consumption Indian IT: expanding centre of

gravity

Indian Chemical: Evolution to

revolution!

Life Insurance: ULIP vs. MF Infrastructure: On the road to

rerating

Cement: Spotting the sweet spot Pharma: Cardiac: the heartbeat of

domestic market

Life Insurance: Comparative

annual report analysis

Indian microfinance: Should you

look micro as macros disappoint?

India Equity Strategy: Quarterly

flipbook

Autos: Divergent trends in PVs

and 2Ws

India Internet: the stage is set FMCG: Opportunity in adversity -

A comparative scorecard

Logistics: Indian Railways - getting

aggressive

Industrials: Triggering a new cycle Financial Services: Megatrends |

Re-bundling ahead

Indian IT: raising the bar

Page 25

Page | 24

F&G: Sector Thematic

Disclosure:

I, Jay Gandhi, MBA, author and the name subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our

views about the subject issuer(s) or securities. HSL has no material adverse disciplinary history as on the date of publication of this report. We also certify that

no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Research Analyst or his/her relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also Research Analyst or his relative

or HDFC Securities Ltd. or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding

the date of publication of the Research Report. Further Research Analyst or his relative or HDFC Securities Ltd. or its associate does not have any material

conflict of interest.

Any holding in stock –No

HDFC Securities Limited (HSL) is a SEBI Registered Research Analyst having registration no. INH000002475.

Disclaimer:

This report has been prepared by HDFC Securities Ltd and is solely for information of the recipient only. The report must not be used as a singular basis of any

investment decision. The views herein are of a general nature and do not consider the risk appetite or the particular circumstances of an individual investor;

readers are requested to take professional advice before investing. Nothing in this document should be construed as investment advice. Each recipient of this

document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in securities of the companies

referred to in this document (including merits and risks) and should consult their own advisors to determine merits and risks of such investment. The

information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be

reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy,

completeness or correctness. All such information and opinions are subject to change without notice. Descriptions of any company or companies or their

securities mentioned herein are not intended to be complete. HSL is not obliged to update this report for such changes. HSL has the right to make changes and

modifications at any time.

This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen

or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be

contrary to law or regulation or what would subject HSL or its affiliates to any registration or licensing requirement within such jurisdiction.

If this report is inadvertently sent or has reached any person in such country, especially, United States of America, the same should be ignored and brought to

the attention of the sender. This document may not be reproduced, distributed or published in whole or in part, directly or indirectly, for any purposes or in

any manner.

Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or

price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively

assume currency risk. It should not be considered to be taken as an offer to sell or a solicitation to buy any security.

This document is not, and should not, be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments. This report

should not be construed as an invitation or solicitation to do business with HSL. HSL may from time to time solicit from, or perform broking, or other services

for, any company mentioned in this mail and/or its attachments.

HSL and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of

the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a

market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any

other potential conflict of interests with respect to any recommendation and other related information and opinions.

HSL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments

made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates,

diminution in the NAVs, reduction in the dividend or income, etc.

HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt

in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations

described in this report.

HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject

company for any other assignment in the past twelve months.

HSL or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the