By Jacqueline Irving Opinions are divided over whether the intro- duction of the single European currency (euro) on 1 January 1999 will prove to be a boon or a bane for African economies. Two certainties for the foreseeable future are that the CFA franc used by 14 African countries will be pegged to the euro instead of the French franc — to which it has been tied since 1948 — and that 65 per cent of these countries’ external reserves will continue to be kept in an account held by the French Treasury. Many economists and financial analysts agree that the euro — which will be the only legal tender in 11 countries known as “euroland” after 30 June 2002 (see box, page 25) — will alter trade and financial flows between Europe and Africa. The CFA countries — together with Central Europe and the Southern Mediterranean — comprise the three groups of countries outside euroland that will be “affected most” by the euro’s introduction, according to a December 1998 World Bank report. But the direction of change is not yet clear, (see box, below). Some analysts point out that actual outcomes for Africa could vary considerably by region and over time. Trade links between euro- land and African countries, particularly in the CFA zone, are already tight. Trade with euroland accounts for 40-50 per cent of total African trade, according to IMF figures. The figures are generally at the higher end of this range for CFA countries (although CFA trade with the European Union countries has declined quite steeply in recent years — see graph, page 28). If the euro regime leads to an economic upswing in euroland, it could boost that region’s output and demand for imports. In turn, this could benefit the econo- mies of euroland’s African trading partners. For companies in CFA countries trading with companies in the European countries sharing the euro with France, the shift in the currency peg from the French franc to the euro would also mean lower com- mercial and currency transaction costs. Central bankers of the mainly francophone West African Economic and Monetary Union (WAEMU) are opti- mistic. The CFA franc-euro link “will give a new impulse to trade and financial flows” between WAEMU and European countries, offering “new opportunities to the economies of WAEMU and new mar- kets to European countries,” said an offi- cial of WAEMU’s Central Bank of West African States (BCEAO). The link should also offer to WAEMU’s eight members the distinct advantages of “more commercial outlets, [the ability to] attract more European investors and access to the European financial market.” But WAEMU officials also note that among the chal- lenges posed by the euro link is the continuing obligation that WAEMU members “implement sound and convergent economic and financial policies.” Optimism not universal Some economists are more dubious about the extent to which the euro’s introduction will have positive trade effects for any countries, including those in the CFA zone. “I don’t believe that there is going to be much benefit For better or for worse: the euro and the CFA franc Comoros West African Economic and Monetary Union (WAEMU) members Central African Economic and Monetary Community (CEMAC) members The euro symbol The Comoros, also a franc zone member, issues the Comorian franc. Burkina Faso Côte d’Ivoire Central African Republic Guinea- Bissau Togo Equatorial Guinea Benin Mali Niger Chad Senegal Cameroon Gabon Congo United Nations Department of Public Information Vol. 12 No. 4 April 1999 Varied impact on Africa expected from new European currency Focus on Namibia pages 18-24 Africa needs scientists page 30-31 The introduction of the euro is expected to tighten economic links between euroland on the one hand, and the CFA franc zone countries and the Comoros, on the other. turn to page 25 Possible gains for Africa from the euro include: But the euro would be bad for African economies if it causes: Impact of the euro on Africa • Increased export sales • Faster growth • Transaction cost savings • Improved macroeconomic stability • More inbound foreign investment • Cheaper foreign borrowing rates • A spur to regional integration • A loss of export markets • Slower growth • Macroeconomic instability • Diversion of international investment from Africa • Less favourable foreign borrowing conditions • Setbacks in local capital market development • Impediments to regional integration Map does not imply official UN endorsement of names and boundaries

Transcript

By Jacqueline Irving

Opinions are divided over whether the intro-duction of the single European currency (euro)on 1 January 1999 will prove to be a boon or abane for African economies.

Two certainties for the foreseeable future arethat the CFA franc used by 14 African countrieswill be pegged to the euro instead of the Frenchfranc — to which it has been tied since 1948 —and that 65 per cent of these countries’ externalreserves will continue to be kept in an accountheld by the French Treasury.

Many economists and financial analystsagree that the euro — which will be the onlylegal tender in 11 countries known as“euroland” after 30 June 2002 (see box, page 25) — will alter trade and financial flowsbetween Europe and Africa. The CFA countries— together with Central Europe and theSouthern Mediterranean — comprise the threegroups of countries outside euroland that will be“affected most” by the euro’s introduction,according to a December 1998 World Bankreport. But the direction of change is not yet clear, (see box, below). Some analysts point

out that actual outcomes forAfrica could vary considerablyby region and over time.

Trade links between euro-land and African countries,particularly in the CFA zone,are already tight. Trade witheuroland accounts for 40-50per cent of total African trade,according to IMF figures. Thefigures are generally at the higher end of this range for CFA countries (although CFA trade with the EuropeanUnion countries has declinedquite steeply in recent years —see graph, page 28). If the euroregime leads to an economicupswing in euroland, it couldboost that region’s output anddemand for imports. In turn,this could benefit the econo-mies of euroland’s African trading partners. For companies in CFA countries trading withcompanies in the European countries sharing

the euro with France, the shift in the currencypeg from the Frenchfranc to the euro wouldalso mean lower com-mercial and currencytransaction costs.

Central bankers of the mainlyfrancophone West African Economic andMonetary Union (WAEMU) are opti-mistic. The CFA franc-euro link “willgive a new impulse to trade and financialflows” between WAEMU and Europeancountries, offering “new opportunities tothe economies of WAEMU and new mar-kets to European countries,” said an offi-cial of WAEMU’s Central Bank of West

African States (BCEAO). The link should alsooffer to WAEMU’s eight members the distinctadvantages of “more commercial outlets, [the

ability to] attract moreEuropean investors andaccess to the Europeanfinancial market.” ButWAEMU officials alsonote that among the chal-lenges posed by the euro

link is the continuing obligation that WAEMUmembers “implement sound and convergenteconomic and financial policies.”

Optimism not universalSome economists are more dubious about theextent to which the euro’s introduction willhave positive trade effects for any countries,including those in the CFA zone. “I don’tbelieve that there is going to be much benefit

For better or for worse: the euroand the CFA franc

Comoros

West African Economic andMonetary Union (WAEMU) members

Central African Economic andMonetary Community (CEMAC) members

The euro symbol

The Comoros, also afranc zone member, issues

the Comorian franc.

BurkinaFaso

Côted’Ivoire Central African

Republic

Guinea-Bissau

Togo

Equatorial Guinea

Benin

MaliNiger

ChadSenegal

Camero

on

Gabon

Congo

United Nations Department of Public Information Vol. 12 No. 4 April 1999

Varied impact on Africa expected from new European currency

Focus on Namibiapages 18-24

Africa needs scientistspage 30-31

The introduction of the euro is expected to tighten economiclinks between euroland on the one hand, and the CFA franc zonecountries and the Comoros, on the other.

turn to page 25

Possible gains for Africa from the euro include:

But the euro would be bad forAfrican economies if it causes:

Impact of the euro on Africa

• Increased export sales

• Faster growth

• Transaction cost savings

• Improved macroeconomicstability

• More inbound foreign investment

• Cheaper foreign borrowing rates

• A spur to regional integration

• A loss of export markets

• Slower growth

• Macroeconomic instability

• Diversion of international investment from Africa

• Less favourable foreign borrowing conditions

• Setbacks in local capital marketdevelopment

• Impediments to regional integration

Map does not im

ply official UN

endorsement of nam

es and boundaries

in terms of trade to any partner of the eurozone, including the CFA,” says Mr. YilmazAkyuz, Chief, Macroeconomic and Develop-ment Policies of the UN Conference on Tradeand Development (UNCTAD). He acknowl-edges that reduced transaction costs and theelimination of exchange rate uncertainty withinEurope following the euro’s introduction couldboost euroland’s income levels and demand forimports. But citing recent economic forecasts,Mr. Akyuz points out that, in the period to2010, total income for all euroland could risejust 3 per cent and increased trade witheuroland would lead to a rise in developingcountries’ GDP of just 0.3 per cent over thesame period.

Moreover, Mr. Akyuz speculates thateuroland’s growth may not even reach 3 per centas a result of costs associated with member

countries’ obligation to meet tight fiscal andmonetary policy targets. And even if the overalleffects on African trade are positive, the euroregime could have a negative impact on certainbusinesses, sectors and/or economies inEurope. In turn, this could slow export growthin certain sectors of African economies.

Freer, greater financial flowsIn the positive scenario for financial flows,exchange rate stability promoted by the CFA-euro link could lead to benefits such as greaterinflows of direct investment from eurolandcountries, says a recent International MonetaryFund (IMF) report1. Other investment flowsfrom Europe into the CFA zone could increaseif European institutional investors — such as

pension fund and insurance companies —decide to diversify their portfolios by movingsome of their funds to CFA countries, anotherrecent IMF report notes2. And these benefitscould be enhanced and reinforced by theimproved access of CFA countries toeuroland’s financial markets. Borrowers inCFA countries would find that they could raisefunds more easily and at cheaper rates in thedeeper, more competitive financial marketsexpected to emerge in euroland.

Addressing the European Parliament in lateOctober, Mr. Tommaso Padoa-Schioppa, mem-ber of the Executive Board of the EuropeanCentral Bank, drew a promising picture.“Capital movements between the CFA franczone and the entire euro area, and not onlyFrance, are expected to be liberalized after thepegging of the CFA franc to the euro,” Mr.Padoa-Schioppa remarked. “This, together withthe ongoing trade liberalization within the CFAfranc zone, should help the zone to reap the

benefits from globalization. However, this willtake time and will also depend on the pursuit ofsound macroeconomic policies and thestrengthening of domestic financial systems.”

BCEAO officials recently said that theyexpect the CFA-euro peg to attract moreEuropean investors to CFA financial markets,who will be notably more interested in theoperations of the regional stock market inAbidjan, Côte d’Ivoire.

But there is a possible downside associatedwith the freer, greater financial flows expectedbetween the two regions. For example, freeraccess to euroland financial markets couldmean that many CFA borrowers would leaveCFA financial markets altogether, hinderingtheir development. In a different scenario, if the

euro boosts productivity and growth in eurolandand increases the relative attractiveness of euroassets, borrowing costs for CFA countries couldactually increase.

And in the event of acrisis of confidence — ifthe euro gains so muchstrength that a devaluationof the CFA franc becomesnecessary — capital flightfrom the CFA to eurolandcould be destabilizing. Thisrisk is not new, however: the possi-bility of capital flight following aspeculative attack also existed underthe French franc-CFA franc link.

Strong or volatile euro poses risksExploring possible negative aspects of the CFA-euro link, some analysts warn that either astrong or a volatile euro could harm CFAeconomies. Among the main risks associatedwith the euro peg “could be the potential appre-ciation of the real effective exchange rate of theCFA franc zone countries” which could under-mine the competitiveness of CFA countries’exports, says Mr. Cornelius Mwalwanda, SeniorEconomic Affairs Officer with the UN Eco-nomic Commission for Africa. Heightenedvolatility of the euro in terms of other majorcurrencies, “both in the transition and earlyyears as well as over the long run” would alsohurt CFA countries’ trade performance, he adds.

Such risks, said Mr. Mwalwanda, wereamong the many issues raised at a November1998 symposium on the future of the CFA franczone, held by the Council for the Developmentof Social Science Research in Africa (Codesria)in Dakar, Senegal.

For example, one symposium participant,Mr. Karamoko Kane of the Cheikh Anta DiopUniversity in Dakar, Senegal, was willing tobet that “the euro will be in future one of thestrongest currencies of the international mone-tary system.” In this scenario, the CFA francwould “follow the euro in its appreciationagainst the US dollar or yen and also, in thesame movement, against the currencies ofdeveloping countries, notably those of Asia andLatin America which are fixed to the dollar,

25APRIL 1999

The euro and Africafrom page 1

The euro — the single European currency — will replace the national currencies of 11 membercountries* of the European Union (euroland) during a three-and-a-half year period that beganon 1 January 1999. On this date, the exchange rates of the euroland countries were “irrevoca-bly fixed” to the euro. The 11 national currencies and the euro will coexist until mid-2002, thedate by which the national currencies must be completely withdrawn from circulation.

While marking a milestone in the European Union’s economic integration process, thelaunch of the euro has significance beyond Europe. Some economists and financial expertsbelieve the euro could become a major international currency to rival the US dollar.

The euro does not yet circulate in the form of notes and coins, but many banks, busi-nesses and other institutions — within and outside euroland — already have begun denomi-nating transactions in euro.

* Austrian schilling, Belgian franc, Finnish markka, French franc, German deutschemark, Irish pound, Italianlira, Luxembourg franc, Dutch guilder, Portuguese escudo, Spanish peseta.

What is the euro?

1 Michael T. Hadjimichael and Michel Galy, The CFAFranc Zone and the EMU, IMF Working Paper, No. WP/97/156 (Washington, DC, November 1997).

2 John Green and Phillip L. Swagel, “The Euro Areaand the World Economy,” Finance & Development,Volume 35, No. 4 (December 1998).

yen and even to the [IMF’s] special drawingright (SDR).” Mr. Kane concluded: “A devel-oping region with an overvalued currencywould be excluded from global competition.”

In other words, a strongeuro could hit CFA econo-mies hard by making theirexports more expensiveand by making importprices cheaper than thoseof competing domestical-

ly-produced goods. Thiscould be especially devas-

tating in the light of stiffercompetition already posed by

exports from countries withdevalued currencies in Asia and in other emerg-ing market countries.

And because the euro is forecast to be astronger currency than the French franc, somebelieve this could put pressure on the CFA francto devalue against the euro. “If the euro isstrong, I expect that the CFA countries willcome under pressure in terms of loss of com-petitiveness and this could effectively necessi-tate more frequent [exchange rate] adjustmentsthan we’ve seen under the system of pegging tothe French franc,” Mr. Akyuz of UNCTAD toldAfrica Recovery.

In fact, the CFA franc has only undergoneone devaluation in its 50-year history — inJanuary 1994, it went from CFA 50 to CFA 100= FF1 — a measure virtually imposed byFrance, the IMF and the World Bank to jumpstart franc zone economies after nearly a decadeof recession. The memories of the 1994 devalu-ation and its immediate effects linger.Described at the time as “brutal and painful” byBenin’s then-President Nicéphore Soglo, thedevaluation was followed by a series of harsheconomic policy changes. But many econo-mists now give credit to the 1994 devaluation,together with the associated policy changes, forthe region’s stronger economic performance ofrecent years.

Devaluation fears recede — for nowIn the months preceding the euro’s launch,off icials within the CFA franc zone andFrance sought to dispel periodic rumours thatthe shift in the CFA franc’s peg to the eurowould lead to a devaluation of the CFA franc.On numerous occasions in the last year,French government officials publicly reaf-firmed the French treasury’s commitment todefending the f ixed parity following the

euro’s introduction (see box, page 27).BCEAO governor Charles Konan Banny

also has been giving repeated and emphaticreassurances that the euro’s launch would notimply a CFA franc devaluation. In a lateNovember 1998 speech, Mr. Banny stressedthat the CFA franc “is currently supported by asound and efficient macroeconomic framework

which will permit it to maintain its value beforeand after its pegging to the euro.” Citing singledigit inflation in WAEMU economies since1995, along with robust economic growth rates,reduced public deficits, improvements in thetrade account and increased foreign reserves,Mr. Banny declared that the “major difficultiesaffecting [WAEMU] have been surmountedand the future is rather promising.” All marketeconomies are open to speculative attacks,Mr. Banny said, noting that speculators areoften wrong, most notably in the recent past, inanticipating a CFA devaluation following theMay 1998 meeting of the European Council todetermine European countries eligible to partic-ipate in the euro. “That’s why we should remainserene, be self-confident and have faith in ourcommon currency,” he urged.

Fears of a devaluation in the near-term now

seem to have been put to rest. The BCEAO cutin the discount rate by 0.5 percentage point atthe time of the euro’s launch “is not behaviourthat smacks of a fear of devaluation,” Mr. Jean-Louis Sarbib, World Bank Vice President forAfrica, told Africa Recovery.

But in the medium- to long-term, othersfeel less certain that the euro and the CFA francwill be kept at the current parity. Some analystsadvise companies dealing in CFA francs tokeep contracts short to protect against a possi-ble devaluation.

Mr. Pierre Messmer, a former French primeminister who forecast the 1994 CFA franc deval-uation several months in advance, predicts thatthe currency will come under increasing pres-sure to devalue in the next few years. BecauseFrance is committed to fiscal restraint underEuropean Economic and Monetary Union(EMU) rules, Mr. Messmer argues that Francewill not be able indefinitely to cover CFA franczone deficits and defend the CFA franc’s value.

Mr. Messmer and others even doubt that thecurrency peg will last. This reflects uncertaintysurrounding both the future of the euro as thesystem’s anchor and the future of the euroitself. “In the long term we don’t know whetherthe euro will survive or not… It’s speculative atthis stage to say what’s going to happen in 10or 20 years’ time to the euro as an anchor cur-rency, as a reserve currency and as a main com-petitor in the denomination of internationaltrade, assets and liabilities,” notes Mr. Akyuz.

Symposium debates CFA franc’s futureThe uncertainty associated with the CFAfranc-euro peg has intensif ied the debatewithin CFA countries on whether or not afixed exchange rate system anchored to a non-CFA currency should remain in place. Indeed,this question tended to dominate the presenta-tions and discussions at the symposium on thefuture of the CFA franc zone held in Dakar inNovember 1998.

Among those at the symposium discussingideas for alternative exchange rate systems wasMr. Wilfrid René M’Voula of the GaboneseMinistry of Economy and Finance. The possiblescenarios envisaged by Mr. M’Voula and otherparticipants included a fixed exchange rate sys-tem managed by the CFA countries themselves,and complete abandonment of fixed exchangerates in favour of 14 freely floating rates. Mr.M’Voula noted that monetary policy sovereigntyassociated with floating exchange rates “wouldpermit these countries to make the adjustments

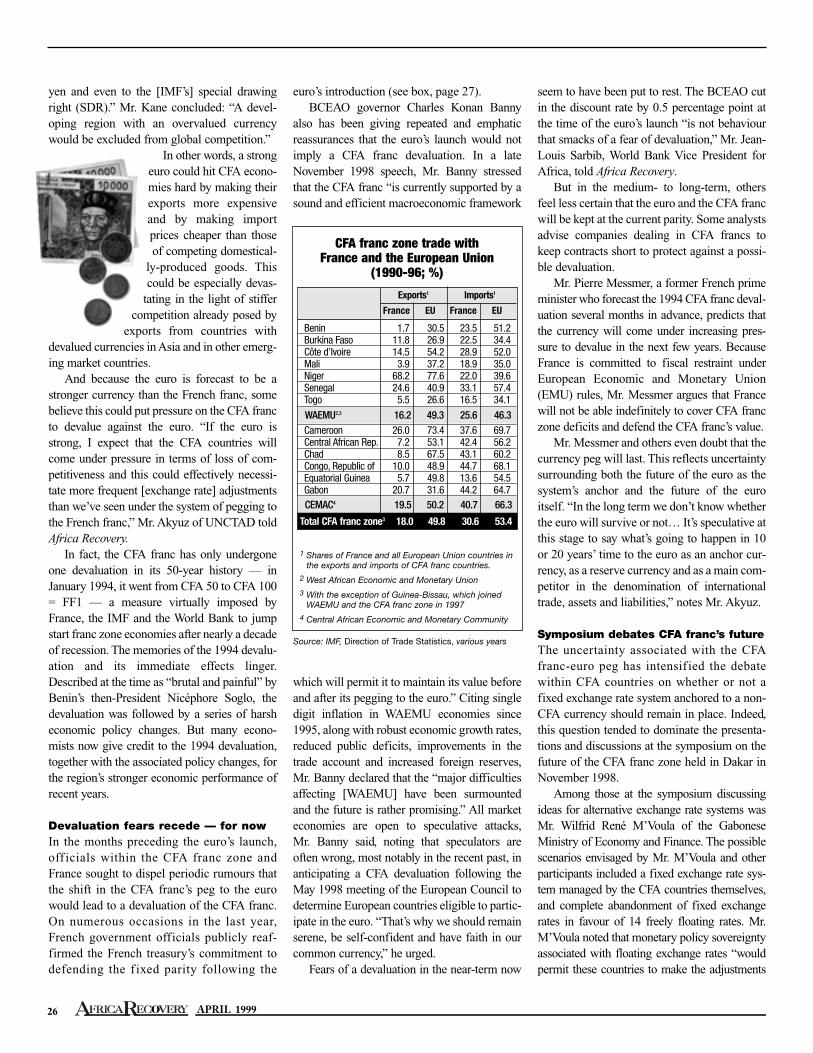

Source: IMF, Direction of Trade Statistics, various years

1 Shares of France and all European Union countries inthe exports and imports of CFA franc countries.

2 West African Economic and Monetary Union3 With the exception of Guinea-Bissau, which joined

WAEMU and the CFA franc zone in 19974 Central African Economic and Monetary Community

CFA franc zone trade with France and the European Union

(1990-96; %)

WAEMU2,3 16.2 49.3 25.6 46.3

CEMAC4 19.5 50.2 40.7 66.3

Total CFA franc zone3 18.0 49.8 30.6 53.4

Exports1 Imports1

France EU France EU

needed to render their economies competitive.” While the CFA-euro peg is the “most proba-

ble” scenario in the short- to medium-term, Mr.M’Voula believes that “the break up, recompo-sition or independence of the two African mon-

etary unions [comprising the CFA zone] is pos-sible,” in the longer term.

Arguing in favour of flexible exchange rates,Mr. Célestin Monga, a World Bank consultant,urged CFA countries to “abandon both their

fixed exchange rate regime and their determina-tion to build an artificial integration, in order foreach country to develop, at the national level, atrue development policy that maximizes theadvantages of an indepen-dent monetary policy.”

But the “question ofthe future of the CFA francshould not be posed interms of issues of sover-eignty or dependence butin terms of efficiency,”argued Mr. Fidèle Magouangou ofthe University of the MéditerranéeAix-Marseille II. While the decisionto peg the CFA franc to the euro“appears acceptable,” he stressed that the CFAeconomies would not benefit from the pegunless there were “some reforms of the func-tioning of the CFA franc zone.”

He pointed to the need to neutralize the neg-ative effects of a strong euro on the competi-

tiveness of the countries concernedand to “limit the transmission ofshocks from the center to theperiphery.” For Mr. Magouangou,therefore, the principal reformwould be “the adoption of a regu-larly adjustable peg [to the euro] in place of a fixed peg.” But in the long term, as CFA monetaryinstitutions get stronger, he envis-ages “an African ‘monetary des-tiny’ that is independent of that ofthe Europeans.”

French neo-colonialism?One of the hottest issues at theDakar symposium was the ques-tion of whether maintaining a cur-rency link defended by the FrenchTreasury perpetuates French neo-colonialism. While CFA countrieshave made some gains in thefranc zone system, Mr. TchetcheN’Guessan, Director of the Côted’Ivoire Centre for Economic andSocial Research, was among

those arguing that France has reaped muchgreater benefits.

Reviewing the history of economic relationsand monetary systems between France and itsformer African colonies, Mr. N’Guessan saidthese systems took various forms but werealways designed to enhance France’s develop-ment as a colonial power. Many CFA franc zone

27APRIL 1999

The CFA franc is the common currency of 14 countries in West and Central Africa, 12 ofwhich are former French colonies. These 14 countries comprise the African FinancialCommunity, which in turn is comprised of two regional economic and monetary groupings.Eight countries — Benin, Burkina Faso, Côte d’Ivoire, Guinea-Bissau, Mali, Niger, Senegaland Togo — form the West African Economic and Monetary Union (WAEMU) while six coun-tries — Cameroon, Central African Republic, Chad, Republic of Congo, Equatorial Guineaand Gabon — are linked as members of the Central African Economic and Monetary Com-munity (CEMAC).

Each regional grouping issues its own CFA franc. The common currency of WAEMU is thefranc de la Communauté financière de l’Afrique (CFA franc), issued by the Banque centrale desEtats de l’Afrique de l’Ouest (BCEAO). CEMAC’s common currency is the franc de la Coopéra-tion financière africaine (also known as CFA franc), issued by the Banque des Etats de l’Afriquecentrale (BEAC). Although the two CFA francs are legal tender only in their respective regions,each region’s central bank maintains the same parity of its CFA franc against the French francand capital can move freely between the two regions.

The CFA franc has been pegged to the French franc since1948*. Only one devaluation has occurred during the historyof the currency peg — from CFA50 to CFA100 = FF1 inJanuary 1994.

With the introduction of the euro on January 1, 1999, theFrench franc is fixed against the currencies of the 10 otherEuropean countries participating in the euro. Nevertheless, themember countries of the CFA franc zone and France agreedto maintain the currency peg following the euro’s introductionthrough an arrangement with the French Treasury.

The French Treasury has retained sole responsibility forguaranteeing convertibility of CFA francs into euros, withoutany monetary policy implication for the Bank of France(French central bank) or the European Central Bank. While thetwo CFA central banks maintain an overdraft facility with theFrench Treasury, the amount that can be withdrawn is limitedby operating rules that have applied since 1973. Each CFAcentral bank must keep at least 65 per cent of its foreignassets in its operations account with the French Treasury; pro-vide for foreign exchange cover of at least 20 per cent forsight liabilities; and impose a cap on credit extended to eachmember country equivalent to 20 per cent of that country’spublic revenue in the preceding year.

The fixed parity between the euro and the CFA franc isbased on the official, fixed conversion rate for the Frenchfranc and the euro set on January 1, 1999 (FF6.55957 =EURO1). As a result, the value of the CFA franc is now fixedagainst all 11 euro-zone country currencies. Since the CFA100= FF1 exchange rate has remained unchanged, the CFA franc-euro exchange rate is simplyCFA665.957 = EURO1.

The CFA franc is actually pegged to the euro in de facto terms from January 1999. The pegwill become official in 2002 — when France and the other euro-zone countries must com-pletely withdraw their national currencies from circulation.

*The Comoros also pegs its currency, the Comorian franc, to the French franc and, since January 1999, to theeuro. The Comorian franc was also devalued against the French franc in January 1994, by 33 per cent.

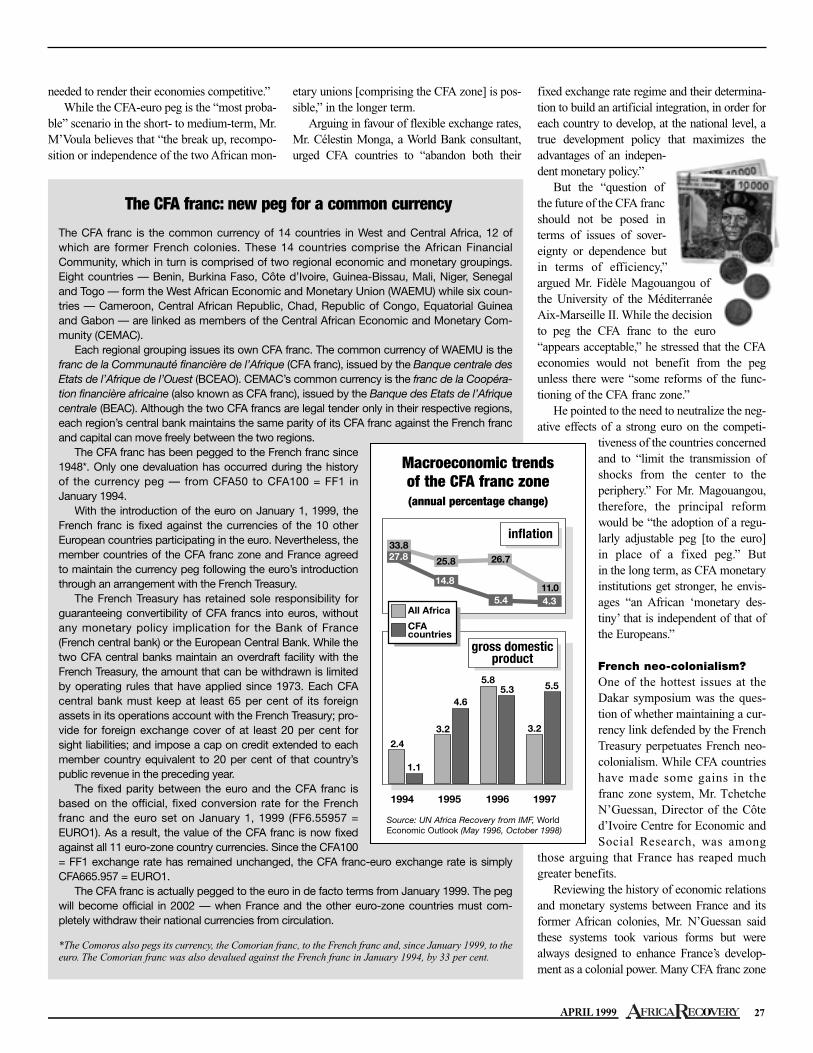

The CFA franc: new peg for a common currency

1994

2.4

3.2

1.1

4.6

5.8

3.2

5.3 5.5

1995 1996 1997

27.8

14.8

5.4 4.3

33.8

25.8 26.7

11.0

All Africa

CFAcountries

inflation

gross domesticproduct

Macroeconomic trendsof the CFA franc zone(annual percentage change)

Source: UN Africa Recovery from IMF, WorldEconomic Outlook (May 1996, October 1998)

mechanisms were simply the “monetary dimen-sion of the colonial agreement,” he said, notingthat “exchange rate policies played a major rolein [France’s] domination of its colonies.” And

today, the fixed exchange rateregime “remains an essen-tial factor in determiningthe economic performanceof the CFA franc zone,”Mr. N’Guessan argued.

When the terms oftrade were favourable, Mr. N’Guessan continued,

CFA countries had goodtrack records in containing

inflation and achieving superiorgrowth relative to non-CFA countries. But heblamed the “financial repression” associatedwith the exchange rate regime for poor perfor-mance in terms of savings and debt levels.

The balance sheet according to Mr. Jean-Louis Sarbib of the World Bank, is very differ-ent. “It’s really quite extraordinary that theseAfrican countries in the CFA zone have had foryears what euroland has only had for severalweeks. If you look at the performance over aperiod of time, I think the advantages of the cur-rent fixed exchange rate arrangement outweighthe disadvantages… the only real shock, so tospeak, was the 1994 devaluation from which Ithink countries have benefited,” he told AfricaRecovery. This good performance is largely dueto the peg to a stable currency, Mr. Sarbib con-tinued, adding: “I don’t know of many otherplaces in Africa where management of the cur-rency has been as good as it has been in thefranc zone.”

Some analysts think that the shift in the cur-rency peg from French franc to euro mightweaken French influence in the CFA region. “Tothe extent that the French influence over the[euro-zone] exchange rates is less than theFrench influence over the French franc… thepolitical link between France and the CFA coun-tries may be expected to weaken a bit,” says Mr.Akyuz. “But on the other hand, France becomesthe main country [within the euro zone] thattakes care of the interests of the CFA countries.”

The shift to the CFA franc-euro peg willhave “no political implications [for the euromember countries] as such,” Mr. GeorgesPineau, Deputy Director-General for Interna-tional and European Relations at the EuropeanCentral Bank (ECB), told Africa Recovery.“Clearly, there is no implication whatsoever for the other [euroland] countries and certainly

not for the ECB,” says Mr. Pineau after point-ing out that the French Treasury has retainedsole responsibility for guaranteeing convert-ibility of CFA francs into euros. This means theFrench Treasury can defend the exchange rateby making credits to the CFA central banks tocover deficits on their operating accounts (seebox, page 27).

Mr. Pineau echoes theofficial French position onthis issue: the currency pegis an internal French bud-getary matter, not a mone-tary issue that wouldinvolve France’s euro part-ners. And French officialspoint to data showing thatthe CFA central banks’operating account deficitshave constituted only a tinyshare of the total Frenchbudget deficit.

But some are not so san-guine about the continuedability of France alone tocover CFA franc zone deficits. Mr. Messmer,one of the most vocal critics of the CFA francmechanism, argues that French fiscal commit-ments under European economic and monetaryunion will make it impossible for the mecha-nism to remain intact.

Spurring regional integrationOne potential benefit of the CFA-euro peg is if the maintenance and strengthening of acommon currency acts as a spur to broadereconomic integration in West and CentralAfrica. “Because maintenance of the commoncurrency requires harmonization of policies —including fiscal and trade policies — it’s astrong incentive to do the right thing to build a bigger base for regional integration,” Mr. Sarbib explained.

In West Africa, for example, CFA countriesform half of the 16-nation Economic Commu-nity of West African States (ECOWAS).Assuming the CFA countries continue to enjoylow inflation, strong growth and improvedeconomic stability through the macroeconom-ic policies associated with the euro peg, the“ECOWAS region as a whole will benefitfrom the spillover effects,” Mr. R.D. Asante,who heads the Money and Payments Divisionof the ECOWAS Secretariat, told AfricaRecovery. Mr. Asante refers to the euro as anincentive to non-CFA, ECOWAS countries to

work towards greater harmonization of mone-tary and financial policies with the CFA. “Andnow there is talk of having a dual monetaryzone in Africa because of what is happeningwith the euro,” he adds.

Other economists and public officialspredict renewed impetus for regional integra-

tion throughout Africa.The euro is likely to “rein-vigorate the current slowpace of economic integra-tion in Africa, particularlyin non-CFA Africa,” Mr.Maurice Kanga, ChiefEconomist at the CentralBank of Kenya, says. Hewent on to declare that “itwill be beneficial, from aneconomies of scale pointof view, to unify the many[African] currencies toface the euro.”

Echoing this view, Mr. J.E.O. Mwencha,Secretary-General of the

Common Market for Eastern and SouthernAfrica (COMESA), told Africa Recovery:“Strong regional trading blocs are taking shapeand we see this as a call for the countries inAfrica also to integrate their economies.”While he saw this call as one of the euro’s pos-itive effects on the 21 member states ofCOMESA, Mr. Mwencha also cautioned thatcompetition for export markets in euroland isgoing to intensify. “External suppliers will findit more difficult to penetrate the European mar-ket because the euro will make that marketeven more efficient,” he noted. While theEuropean Union is the destination of more than60 per cent of total COMESA exports, most ofthose exports are raw materials. Consequently,they may not be too greatly affected byincreased competition from other suppliers ineuroland, he explained. “But we see theEuropean Union becoming more prosperousand increasingly integrated [as a result of theeuro]. So we hope these countries will lookoutward to invest in Africa, where there is high-er return on capital,” Mr. Mwencha added.

Within weeks of the euro’s launch, the cen-tral bank of one COMESA member, Sudan,issued a circular to local banks urging them toconduct commercial transactions in euro. Sincethe bulk of Sudan’s trade is with Europe andbecause the euro could reduce transaction costsfor Sudanese traders, “we are encouraging our

28 APRIL 1999

94 95 96 97921991 93

55.653.6

51.8 52.754.6

49.2

56.4

52.0

46.648.3

49.8 48.7

40.6

59.5

Exports3

Imports2

CFA1 trade withEuropean Union (%)

1 with the exception of Guinea-Bissau, whichjoined the CFA franc zone in 1997

2 share of total CFA imports coming from theEU

3 share of total CFA exports going to the EU

Source: UN Africa Recovery from IMF,Direction of Trade Statistics Yearbook, 1998

banks to try to deal in euro and to encouragetheir customers — exporters and importers —also to deal in euro,” Mr. Sabir Muhammad al-Hassan, Governor of the Bank of Sudan, toldAfrica Recovery.

But Mr. al-Hassan alsopointed out that Sudan may be“a special case” because theeconomic embargo imposedon it by the US since 1997makes transfers in US dollarsby Sudanese businesses andbanks subject to confiscation.“There’s a lot of risk involvedand there are also additionaltransaction costs involved toavoid dollars in our transfers.So, by moving into euro, we will remove thatrisk, of course,” he explained.

Still, the euro could help promote regionalintegration, says Mr. al-Hassan. “In theCOMESA area, the trade settlement arrange-ment is [transacted] in dollars. Because of theUS embargo, we were having difficulty bene-fiting from this arrangement. Now with theeuro’s introduction we have proposed [to ourCOMESA partners] that the settlement also bedone in euro, not just in dollars.” According toMr. al-Hassan, this would likely increase trad-ing activity throughout the COMESA area.

Ten COMESA member states are alsomembers of the 14-nation Southern AfricanDevelopment Community (SADC). Whileanticipating that the euro will lead to greaterdemand for SADC exports by eurolandcountries, Mr. F.C. Kani, Chief Economist forSADC, also stresses the role of the euro as “a corridor to the low inflation experiencedin the euroland region.” To the extent that the low inflation rates and low interest rates in euroland result in lower import prices forSADC countries, “this will transmit into lower inflation in the SADC region itselfbecause the pass-through effects of importprices in most SADC economies will be quitehigh,” he explained.

Emphasizing that it is “early days yet,”Mr. Kani did not completely rule out an alter-native scenario, where macroeconomic perfor-mance in euroland deteriorates. “If, forinstance, inflation [in euroland] starts going upor there’s a recessionary trend in the Europeaneconomy… that can indirectly have a negativeimpact on the growth and inflation statisticswithin the SADC region itself.”

Nevertheless, Mr. Kani feels that the euro is

more likely to bring benefits than costs toSADC economies. The emergence of a highlyliquid capital market from euroland’s stableexchange rate regime and low-interest rate envi-ronment would be a “very attractive source of

capital and short-term financ-ing for African countries, andespecially the SADC region,”he noted.

“The successful introduc-tion of the euro will stimulatethe ambitious and long-termobjective of financial integra-tion in SADC,” declared Mr.Chris Stahls, Governor of theSouth African Reserve Bank(the central bank), speaking at a

January meeting with ambassadors of eurocountries to South Africa.

Mr. Stahls shares Mr. Kani’s view thatAfrican countries could benefit from the euro’s stimulating effect on European capitalmarkets. “As the euro establishes itself as a sta-ble currency, and as liquidity in the financialmarkets of the participating [euro] countries isintegrated, South Africa will most probably lookmore to Europe, not only for short-term trade financing, but also forraising longer-term loan and equi-ty funds,” declared Mr. Stahls.

End-1997 figures show theEuropean Union already account-ing for 58 per cent of total foreigninvestment in South Africa, whichhas the largest economy in Africa.Moreover, Mr. Stahls forecast anincrease in the flow of investmentfrom South Africa to eurolandcountries.

More euro transactions likelyMr. Stahls also pointed out theconsiderable merchandise tradebenefits expected to accrue toSouth Africa following the euro’slaunch, in view of the fact thateuroland accounts for 28 per centof South Africa’s foreign trade.Predicting that the euro will gainin stature as a major internationalcurrency, he said a greater share of SouthAfrican trade with Europe would likely betransacted in euro in future.

“We’ve really gone the ‘big bang’ route atStandard Bank Johannesburg — we can nowentertain clients’ requests for any of the

[euroland national] currencies or for the euro,”says Mr. Willie Potgieter, Director of ForeignExchange and responsible for setting up theeuro systems for Standard Corporate andMerchant Bank, a topSouth African bank. Heexpects many of thebank’s corporate clients toconvert to using the euroover the next year as theirtrading partners in euro-land also switch over. Ascompanies convert into euros, theycan enjoy the benefits of handlingcash and risk management for for-eign exchange transactions witheuroland in just one currency, he says.

“In response to the challenge posed by theeuro, we are expecting to see greater pressure formonetary and economic integration [in WestAfrica] and this can only serve to boost businessvolumes,” says Ms. Karen Tanoh, financial con-troller of Ecobank (Ghana). The bank’s cus-tomers still continue to prefer the national cur-rencies to the euro, reports Ms. Tanoh, thoughshe notes that Ecobank’s European counterparts

are happier dealing in euro and itis likely the volume of euro trans-actions will increase in future.

Not all observers expect theeuro to have far-reaching effectson their countries’businesses andeconomies. “In talking to ourcustomers, my impression is thatthe impact of the euro’s introduc-tion has been negligible,” saysMr. Atedo Peterside, ChiefExecutive Officer of InvestmentBanking & Trust Company(IBTC), a top merchant bank inNigeria. Mr. Peterside attributesthis largely to the fact that themain destination of Nigeria’scrude oil, which accounts forsome 95 per cent of export rev-enues, is the US, and the bulk ofthese exports is priced in dollars.“Even where European countriesbuy crude oil, they tend to pay adollar price,” he notes.

“But our bank offers accounts in euros since1 January, the date of the euro’s launch. I expectthat deutschemark and French franc businesswill decrease while euro business will increase,though this hasn’t really begun to happen yet,”he adds. ■

29APRIL 1999

39.8

48.1

Euroarea

otheradvanced

economies

34.4

23.7

Africa*

CFA franc zone*

Africa’s totaltrade with

euroland (1996)

* Imports plus exports ofgoods from and to partnercountries in 1996 as a percentage of total importsplus exports

Source: UN Africa Recoveryfrom IMF, World EconomicOutlook, October 1998

CFA economies will notbenefit from the euro pegunless there are “somereforms of the functioningof the CFA franc zone.”