60

BLUECHIIP LIMITED ABN 79 104 795 922 Annual Report 2015 For personal use only

BLUECHIIP LIMITED ABN 79 104 795 922

Annual Report 2015

For

per

sona

l use

onl

y

Corporate Information

ContentsChairman’s Report 1

Managing Director’s Report 2

Directors’ Report 6

Auditor Independence Declaration 11

Remuneration Report (audited) 12

Corporate Governance 23

Consolidated Statement of Financial Position 24

Consolidated Statement of Comprehensive Income 25

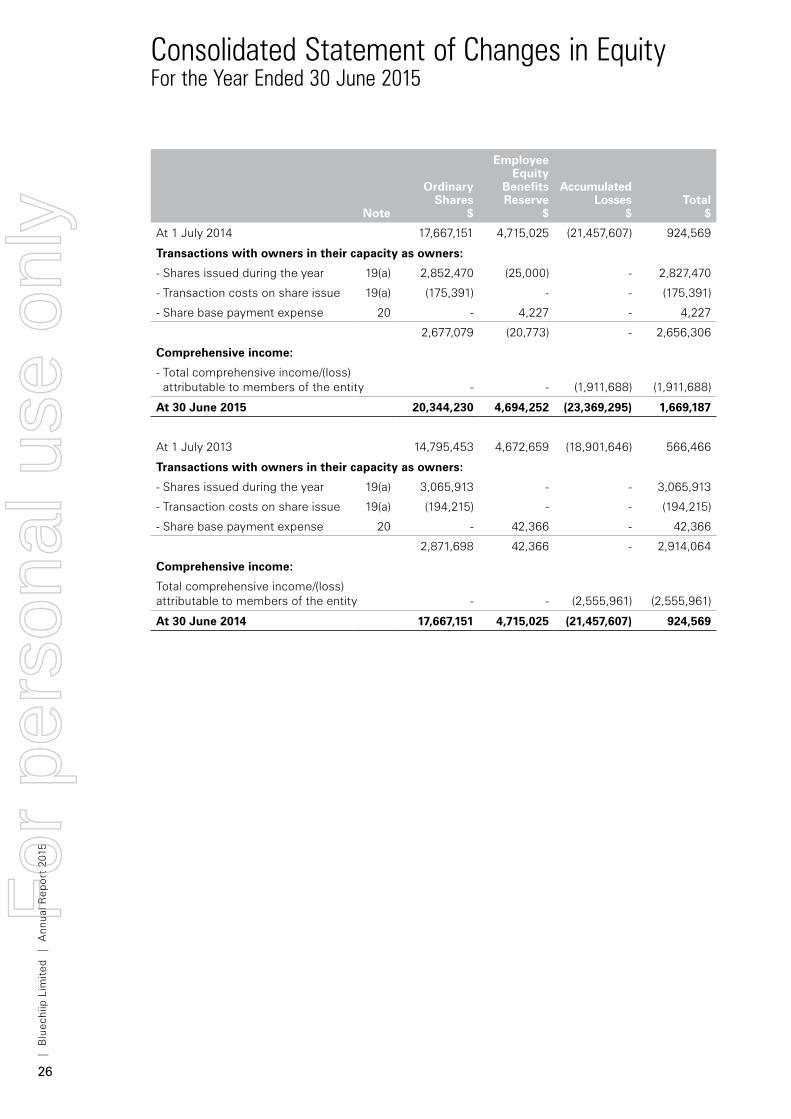

Consolidated Statement of Changes in Equity 26

Consolidated Statement of Cash Flows 27

Notes to the Consolidated Financial Statements 28

Directors’ Declaration 51

Independent Auditors Report 52

ASX Additional Information 54

DirectorsMr Iain Kirkwood Non-Executive Chairman

Mr Andrew McLellan CEO/Managing Director – appointed 27 January 2015

Mr Matthew Morgan Non-Executive Director

Mr Michael Ohanessian Non-Executive Director – appointed 15 December 2014

Company SecretaryMr Lee Mitchell

Registered office1 Dalmore Drive Caribbean Business Park Scoresby Victoria 3179

Phone: +613 9763 9763 Fax: +613 9763 9764

Principal place of business1 Dalmore Drive Caribbean Business Park Scoresby Victoria 3179

Phone: +613 9763 9763 Fax: +613 9763 9764

Share registryBoardroom Pty Limited GPO Box 3993 Sydney NSW 2001

Phone: +612 9290 9600 Fax: +612 9279 0664

Bluechiip Limited shares are listed on the Australian Stock Exchange (ASX: BCT).

BankersNational Australia Bank Limited Melbourne, Victoria 3000

AuditorsErnst & Young 8 Exhibition Street Melbourne Victoria 3000

Websitewww.bluechiip.com

Cover: An artist’s impression and does not represent the final product design of Bluechiip.

For

per

sona

l use

onl

y

1

Chairman’s Report

Dear Shareholder,

On behalf of the Board of directors of Bluechiip Limited, I am pleased to present to you our 2015 Annual Report.

The 2015 financial year (FY15) presented us with another series of challenges as the Company continues to commercialise its unique technology. Not least of these was finding a CEO to replace Dr Jason Chaffey who unexpectedly resigned. However, the Board was delighted to have secured Andrew McLellan who, as you can read in his short biography in the Directors’ Report, has extensive experience and a long background in commercialization of technology. He joined us in January and, in the short time since, has already made an impressive contribution.

At the beginning of the financial year, we bade farewell to two directors, Joe Baini and Ron Finkel, to whom we extend our gratitude for their contribution and, in December, we welcomed Michael Ohanessian to the Board. Michael brings a wealth of industry experience into our boardroom which will be invaluable as we focus on delivering our strategy to commercialise Bluechiip’s technology.

Andrew’s arrival provided the opportunity to have a set of ‘fresh eyes’ on Bluechiip’s technology, its commercialisation strategy and execution. As he explains in considerable detail in his Managing Director’s report that follows, our commercialisation strategy was adjusted, inter alia, to simplify access to the technology. This modification was in response to crucial feedback gathered by Andrew as he systematically assessed and tested the status quo whilst visiting a number of key stakeholders. I commend Andrew’s excellent report to you.

I need to make a comment regarding Bluechiip’s share price and resultant market capitalisation which, needless to say, your Board believes is a poor reflection of the underlying value of the Company. Bluechiip’s unique tracking technology is a world leader and, to date, unleashing its value has been a challenge. However, we expect a number of events in FY16 will demonstrate that the commercialisation strategy is gaining traction and attracting demand for our technology in the significant biobanking market.

As always we are grateful for the tireless efforts of a very small team of dedicated and committed staff. Thank you all.

Finally, on behalf of the Board, I thank you for your support as a shareholder as we continue on the journey ahead and look forward to meeting you at the AGM on 23 October 2015.

Iain Kirkwood Chairman

For

per

sona

l use

onl

y

2

| B

luec

hiip

Lim

ited

|

Ann

ual R

epor

t 20

15

Managing Director’s Report

Since joining Bluechiip in January I have been continually encouraged by the fundamental characteristics of Bluechiip and its core technology, this positive outlook has been reinforced and reiterated by partners, customers, distributors, suppliers and shareholders across the globe.

Bluechiip serves a clear unmet market need in severe environment tracking, especially in the large target market of cryogenic biosample storage which is forecast to be in excess of 300 million samples a year. Bluechiip’s solution is, unlike other electronic tags, impervious to extreme high and low temperatures, gamma radiation, moisture, and other harsh conditions that would compromise traditional identification.

In addition, Bluechiip’s core technology is able to rapidly expand beyond the initial targeted applications in the healthcare and biomedical industries. The technology’s extreme robustness, ability to track temperature, and resistance to tampering is ideally suited for high-value applications in food, vaccines, security, defence, aerospace and aviation.

In summary, Bluechiip:

• Has developed world leading technology in the field of sample tracking technology for extreme environments;

• Owns a highly differentiated and well protected technology platform, including 20 patents and patent applications across 7 core patent families in Australia, US and Europe;

• Has an existing product suit with a unique chip, reader and associated software;

• Benefits from a world-class supply chain, including market leaders such as ST Micro-electronics, Plexus, Europlaz and RC Precision;

• Has an expanding distribution network with partners in North America, Europe, Asia, South America and Australia;

• Is increasing the number of opportunities with OEM partners looking to incorporate Bluechiip technology into their own products;

• Maintains a highly motivated team focused on fully commercialising the technology; and

• Continues to be dedicated to research and development and expansion of its suit of products to meet the unmet market needs through its partner networks.

Given these fundamental characteristics, our aim and corporate goal is to;

• Continue to penetrate and expand our market for existing products;

• Embed Bluechiip technology in OEM partner’s products; and

• Expand applications across multiple sectors.

The company’s initial commercial strategy was to manufacture and sell products to end users in a commodity product target market. This strategy not only competed directly with large multinational competitors with significant resources and market share but committed Bluechiip’s resources on manufacturing and sales and marketing to end users. This strategy has been amended in response to feedback from distributors, OEM partners and thought leaders and Bluechiip now seeks to simplify how partners access Bluechiip technology.

As a result of these changes we have seen a dramatic increase in the pipeline of OEM opportunities in the initial biosample storage market in the last 12 months. Some of these opportunities are from companies which previously viewed Bluechiip as a direct competitor. This change in strategy will enable the company to convert these OEM opportunities to license, royalty and sales revenue of chips and embedded readers in the near term and enable Bluechiip to focus its resources on its core capabilities of MEMs technology development for permanent and severe environment tracking.

For

per

sona

l use

onl

y

3

1 Key Strategic ImperativesThe core strategies the company is implementing are:

1.1 Expansion and Reinforcement of Bluechiip’s global distribution and supply chain network

Global distributionIn FY15 Bluechiip continued to expand its distribution network in biobanking and other life science-related markets.

Distribution channels were established in Asia with:

• NPO Bio Bank Support Organisation in Japan

• Glory Biotech Corp in South Korea

• Axon Scientific Sdn Bhd in Malaysia

• Integrated Bio Limited in Taiwan

And in South America with:

• Micronic North America LLC

This adds to the existing distribution partnerships already introduced in FY14 in:

• North America: Micronic North America LLC and MiTeGen

• China: Bluechiip China

• Australia: OnQ Software Pty Ltd

These distribution networks are actively marketing and selling Bluechiip products, and while the expected pull through of sales has been slower than expected, the distribution networks have created significant OEM opportunities.

Key highlights in the last 12 months included:

• In Australia, direct validation sales of the Bluechiip system to Florey Institute of Neuroscience and Mental Health, Flinders University, Taylor Wharton Australia, Wesley-St Andrews Research Institute and Cell Care Australia;

• Sale and installation through our distributor of Bluechiip chain of custody solutions at BluBioBank (China), a greenfield high value biobanking facility focused on regenerative health, which commenced operations in May utilising Bluechiip technology;

• Micronic America LLC achieving the first Canadian installation of bluechiip® technology products in February 2015; and

• In Japan, brand awareness following the establishment of a distribution channel leading to an evolving range of OEM partnering opportunities in the regenerative medicine space.

Supply chain networkIn August 2014 Bluechiip and STMicroelectronics expanded production of Bluechiip Delta Tags. This critical milestone meant that Bluechiip could meet demand in excess of 1 million tags a year. The continued support of our supply chain partners is allowing Bluechiip to have a mature product available for growing demand in the market.

1.2 Progressing and expanding our co-development OEM partnerships

OEM partnerships are critical to gaining a step change in market penetration and end customer pull through. As such, expansion of our OEM activities has been a key focus, especially in the second half of the year. As a result the pipeline of OEM opportunities has increased dramatically.

• The relationship with Micronic Holdings BV, a manufacturer of cryosample vials and storage solutions, continued with a co-development agreement. The outputs of the agreement were highlighted in February at The Society of Laboratory Automation Systems (SLAS) exhibition in Washington, where Bluechiip and its North American distributor Micronic America co-demonstrated key technologies in Bluechiip’s development pipeline, including:

o Dual-identity cryovials incorporating bluechiip® tags moulded into Micronic 2D barcoded cryovials; and

o The multi-vial reader, enabling increased productivity with the ability to read a full tray of bluechiip® tagged cryovials.

Both technologies received positive feedback.

• In November 2014 Bluechiip announced that it had signed a Test and Evaluation Agreement with SIAD Group in Italy to integrate the bluechiip® cryotag into SIAD’s cryobags, which are used to store cord blood and other biological products. Subsequent to the trial, SIAD highlighted additional requirements to be incorporated into the bluechiip® technology. These requirements have been fed back into the development program and are progressing through working with research partners in programs such as the Australian Governments Research Connections.

• In line with Bluechiip’s OEM strategy and in response to requests from multiple OEMs, Bluechiip recently launched a Developer Kit which includes a Matchbox Reader, tray(s) of delta tags, StreamTM Software and engineering support. Strategically important, the Developer Kit allows potential OEM

For

per

sona

l use

onl

y

4

| B

luec

hiip

Lim

ited

|

Ann

ual R

epor

t 20

15

partners to incorporate and evaluate the Bluechiip technology in their products to assess the competitive advantage it provides. On successful evaluation Bluechiip will be in a position to support custom integration and to establish ongoing license agreements with these parties.

Bluechiip has also recently engaged a Business Development representative in North America to support distribution of its products and OEM partners in our largest geographic market.

1.3 Executing on market based feedback through continued refinement and development of Bluechiip’s core technologies

Global Market feedbackBluechiip’s expanding distribution networks provide critical market feedback and exposure to OEM partnering opportunities. Feedback from exhibitions, our distribution networks and OEM engagement indicates that:

• Leading biobank technology vendors are increasingly aware of bluechiip® technology;

• There is a clear unmet need for products like Bluechiip’s multi-vial reader, dual ID cryovial and handheld reader, especially within the cryogenic biobank market where:

o Innovation is a key differentiator for vendors;

o Automation is key in this high-volume industry;

o Cryogenic storage of samples is increasing dramatically;

o Guidelines on sample storage including ISBER and CAP are emerging.

Translation into new Productsa. Portable Handheld Reader DevelopmentIn response to market feedback from biobanks, Bluechiip is continuing to develop new reading technologies and has partnered with Planet Innovation, Australia’s Most Innovative company in BRW’s 2015 rankings, to further develop the portable hand held reader.

The project involves incorporating the internal electronics of the Bluechiip Matchbox reading system into a portable reader package to open up mobile applications of the technology.

A handheld reader will enable operators in the large biobanking sample market to move about a facility freely and complete identification at the sample site rather than relocating the sample prior to identification. This development will also open opportunities in adjacent markets requiring portability.

b. Bluechiip button development initiated for biobanking retrofit market

To date Bluechiip has focused on the new biosample storage market. Feedback received from multiple biobanks, however, has identified a need to retrofit existing bio samples and identify multiple cryovial types before committing to changes in identification for new biobank samples.

In response to these requests and to open Bluechiip’s technology to the large existing market of stored samples, the Company is developing “Bluechiip buttons” capable of being easily retrofitted into existing biobank cryovials and samples to aid in the identification and temperature tracking. The buttons include a Bluechiip Delta tag in a plastic housing which can be retrofitted into a range of different vials.

Bluechiip’s initial target market for this initiative, biobank cryosample storage, is forecast to be in excess of 300 million new cryosamples per annum being placed into storage by 2017. This (annual) volume is adding to the existing store of samples with reports of well in excess of 2 billion samples currently in storage globally.

c. Multivial Reader DevelopmentTo date Bluechiip has been limited in its ability to meet the needs of the high volume biobanking sector as it was not able to manage a high volume of samples. Market feedback indicates that a multivial reader is essential to being able to scan trays of up to 100 cryovials at a time; therefore, Bluechiip has developed and demonstrated a prototype multivial reader at the SLAS tradeshow in Washington DC in February FY15 with positive results. Development has continued through FY15.

The portable handheld reader complemented with Bluechiip buttons and the multivial reader, also in development with OEM partners, will position Bluechiip to address the high volume biobanking facilities requirement across the globe and is in direct response to feedback from key opinion leaders and OEM partners on the Bluechiip technology and application.

Trials and testing with OEMs and biobanks are expected in the fourth quarter 2015.

1.4 Medium to long term development of core technology

Bluechiip has continued to progress in its R&D development pipeline and will continue pursuing developments on its core chip and reading technology in the medium to long term. During the year the company pursued discussions with research partners and sought associated grant opportunities. In August 2015 Bluechiip was successful in its application for the Research

Managing Director’s ReportF

or p

erso

nal u

se o

nly

5

Connections Grant through the Australian Federal Governments AusIndustry Entrepreneurs Programme.

This research collaboration is focused on expanding Bluechiips core chip technology in areas such as increased and expanded sensing capability, the ability to sense temperature excursion events, increasing read range and reduction in size.

Expanding and reinforcing Bluechiips core technology is critical to providing a basis for a robust platform technology which will cascade into increased growth and opportunities or the Company in serving the BioBanking market and offer a range of products along a continuum of markets in the future.

PatentsDuring the year The Bluechiip Patent “RFID Memory Devices” Patent Number 8,884,743 was granted.

2 OutlookIn FY16 Bluechiip is positioned to increase the value for shareholders in the underlying core technology and associated channels to market.

Bluechiip will execute on its commercialisation strategy by adapting to the market with a modified range of product offerings that allow OEM partners easy access to the Bluechiip tracking technology. Trials of the new products in development with OEMs and biobanks are expected in the fourth quarter of 2015 and subsequent integration of Bluechiip’s readers and software into products through FY16. Bluechiip will maintain tight control on costs and continue to seek assistance through available refunds and grant funding to support its ongoing R&D and commercialisation activities.

The products and the reference designs created will allow licence and OEM agreements to progress and partners to release their products incorporating Bluechiip technology.

In the next 12 months we expect to see revenue generated from sales, licence and royalty revenue through OEM partners’ co-development and collaboration agreements. This will provide a step change on incremental sales within the existing product suit and sale of development kits.

Finally, I wish to thank the Bluechiip team for their significant effort and dedication over the last 12 months. I would also like to specially thank the support of our shareholders, many of whom have remained committed to Bluechiip despite the challenging year.

Andrew McLellan Managing Director

For

per

sona

l use

onl

y

6

| B

luec

hiip

Lim

ited

|

Ann

ual R

epor

t 20

15

Directors’ Report30 June 2015

Your directors submit their report for the year ended 30 June 2015.

DirectorsThe names and details of the Company’s directors in office during the financial year and until the date of this report are as follows. Directors were in office for this entire year unless otherwise stated.

Names, qualifications, experience and special responsibilitiesIain M Kirkwood - Non-Executive Chairman Qualifications: MA (Hons) Oxon, FCPA, MAICD

Appointed to the Board in November 2007, Mr Kirkwood serves as Chairman. He was appointed as Executive Chairman on 28 January 2014 and reverted to the role of Non-Executive Chairman on 1 July 2014. He is an experienced private consultant, investor and non-executive director. He has considerable practical and operational experience gained from a successful financial career spanning 35 years in a range of industries including auditing, resources, manufacturing and latterly healthcare in Australia, Britain and the USA. He started his career at Arthur Andersen & Co in London. He held a range of senior financial and general management positions in Woodside Petroleum Limited, Santos Limited, Pilkington plc, F.H. Faulding & Co Limited and Clinuvel Pharmaceuticals Limited.

During the past three (3) years he has also served as a Director of the following other ASX listed companies:

• Avexa Limited (Appointed 9 August 2010)

• MHM Metals Limited (Appointed 13 February 2013, Resigned 23 March 2015)

• Vision Eye Institute Limited (Appointed 15 November 2004)

• Medical Developments International Limited (Appointed 27 October 2003, Resigned 26 February 2013)

Mr Andrew McLellan - Managing Director and CEO Qualifications: MBA, B Eng (Hons), GAICD

Appointed as Managing Director and CEO on 27 January 2015. Mr McLellan has vast experience in innovation and commercialisation combined with significant technical and operational experience. Prior to joining Bluechiip, he was the CEO of Advanced Manufacturing Co-operative Research Centre (AMCRC) which he now serves as a non-executive Director. Mr McLellan focused on bringing together industry and research to develop and commercialise ground breaking innovations. He has held a range of senior positions including Director at Leica Microsystems Pty Ltd (previously

Vision BioSystems Pty Ltd, a division of the former publicly listed Vision Systems Limited), Vice President of Marketing and Business Development North America and Director of Product Management at Vision BioSystems Pty Ltd. Mr McLellan holds a Bachelor of Engineering Degree (Hons) and an MBA (Strategy) from Monash University (Melbourne). In addition, he is also a graduate of the Australian Institute of Company Directors (GAICD).

During the past three (3) years he has also served as a Director of Advanced Manufacturing Co-operative Research Center (AMCRC).

Matthew Morgan - Non-Executive Director Qualifications: MBA, B Com, B App Sc, Kauffman Fellow

Appointed to the Board on 3 February 2014. Mr Morgan is an experienced advisor and non-executive director. He is currently the Principal of Millers Point Company, an advisory firm that works with management and shareholders of emerging companies advising on strategy, commercialisation and corporate transactions.

Prior to founding Millers Point Company he was a venture capitalist at QIC, a large institutional investor. He has spent the balance of his career working as an executive in the portfolio companies of various private equity investors. Throughout his career he has served on seed and venture capital stage investment committees and advised on a wide range of corporate transactions including licensing, debt and equity raisings and mergers and acquisitions.

During the past three (3) years he has also served as a Director of the following other ASX listed companies:

• Diversa Limited (Appointed 2 July 2008)

• Leaf Resources Limited (Appointed 21 July 2014)

• 3DM Limited (Appointed 18 June 2014, Resigned 28 May 2015)

Michael Ohanessian - Non-Executive Director Qualifications: B Eng, MBA

Appointed to the Board on 15 December 2014. Mr Ohanessian is currently the CEO and Managing Director of Praemium Limited. Mr Ohanessian has considerable executive experience gained from technology-related businesses with a mixture of operational, strategic and leadership capabilities. Following a ten year career at Mobil Oil before, Mr Ohanessian joined the Boston Consulting Group where he consulted to clients in a wide range of industries which include banking, airlines, mining, packaging, sports, oil and gas, retailing and biotechnology.

For

per

sona

l use

onl

y

7

Mr Ohanessian later moved on to be the CEO of Vision BioSystems, a division of the former publicly listed Vision Systems Limited, where he transformed the business over seven years from a small unprofitable contract manufacturer into a vertically integrated, profitable and growing medical diagnostics business with distribution to over 60 countries. More recently he has served as Chief Executive of Genetic Technologies Limited and has been involved in investment management and corporate advice with Lion Capital prior to joining Praemium Limited.

During the past three (3) years he has also served as a Director of Praemium Limited (Appointed March 2012).

Dr Jason Chaffey – former Managing Director and CEO (resigned on 14 November 2014) Qualifications: B. Sc (Adv.), PhD (RMIT), MAICD

Joe M Baini – former Non-Executive Director (resigned on 1 August 2014) Qualifications: BSc, Post Grad Diploma of Business Management

Ron Finkel – former Non-Executive Director (resigned on 1 August 2014) Qualifications: LLB, B Com (Melb)

Lee Mitchell Qualifications: BA, LLM (Melb)

Lee is a partner at Logie-Smith Lanyon, a mid-sized full service commercial law firm based in Melbourne, Victoria. He is a qualified solicitor practising principally in corporate and commercial law advising on corporate and securities regulation, equity capital raisings, formulation and implementation of mergers and acquisitions, corporate governance and company secretarial matters.

He joined Bluechiip Limited as Company Secretary in September 2010.

Interests in the shares and performance rights of the Company and related bodies corporateAs at the date of this report, the interests of the directors in the shares and performance rights of Bluechiip Limited were:

Number of ordinary

shares

Number of performance

rights over ordinary

shares

Iain Kirkwood 9,344,127 –

Andrew McLellan 348,000 1,500,000

Matthew Morgan 250,000 –

Michael Ohanessian – –

Other than 1,500,000 performance rights (zero exercise price options) issued to the CEO, Andrew McLellan on 27 April 2015, there was no options granted to directors. Further details of the performance rights and the terms are set out in the Variable Compensation – Long Term Incentive section.

DividendsNo dividends were paid or declared since the start of the financial year (2014:Nil). No recommendation for payment of dividends has been made.

Principal ActivitiesThe principal activity of the Group during the year was the development and commercialisation of a unique tracking system that offers enhanced technical capabilities over existing labels, barcode and Radio Frequency Identification (RFID) technologies.

There have been no significant changes in the nature of these activities during the year.

Operating and Financial Review

Operating ResultsThe consolidated loss of the Group for the financial year after providing for income tax amounted to $1,911,688 (2014: loss of $2,555,961).

Results of operationsThe Company recognised net revenue totalling $33,856 at 30 June 2015 (2014: $41,937) during the year contributed from sale of products which has increased to $33,856 (2014: $21,937).

Other income decreased from $742,043 to $700,935 mainly due to:

• Export Market Development Grant incentive for which no claim was made during the year (2014: $97,086)

Loss before income tax decrease from $2,555,961 to $1,911,688 resulted from lower operating expenses incurred of $2,525,189 (2014: $3,176,189) and the lower operating expenses is mainly attributed to:

• Lower employee benefit expenses - $864,120 (2014: $1,078,647) due to the resignation of R&D personnel in August 2014 and resignation of former Chief Executive Officer in November 2014;

• Lower business development expenditure - $97,859 (2014: $225,573).

Capital structureDuring the financial year ended 30 June 2015, the following material movements in share capital occurred:

For

per

sona

l use

onl

y

8

| B

luec

hiip

Lim

ited

|

Ann

ual R

epor

t 20

15

• In September 2014, the Company completed a capital raising of $1,095,000 to sophisticated and professional investors via a placement comprising 10,950,000 ordinary fully paid shares at $0.10 per ordinary share with one free attached unlisted share option per new share issued with an exercise price of $0.13 per option with an expiry of 31 March 2015. In addition, the Company also announced a Share Purchase Plan (SPP) which allowed participation from eligible existing Bluechiip’s shareholders to purchase further fully paid ordinary shares in the Company at $0.10 per share, which raised $763,000.

• In April 2015, the Company completed a capital raising of $1,000,000 at $0.045 per share via a placement to sophisticated and professional investors. The amount of $918,505 comprising 20,411,212 ordinary fully paid shares were issued and the remainder of $81,495 committed by Mr Iain Kirkwood and Mr Michael Ohanessian comprising 1,811,011 shares will be issued subject to the approval of the shareholders at the forthcoming Annual General Meeting.

• Capitalised share issue costs relating to the placements above totalled $175,391 and have been offset against the issued capital.

Significant Change in the State of AffairsOther than as detailed in this financial report, there has been no significant change in the state of affairs of the Company.

Events after Balance DateOn 25 August 2015, the Company entered into a Loan Agreement with Guerilla Nominees Pty Ltd for a loan facility of $600,000 (Loan Facility). The Loan Facility is to be drawn down in 2 tranches, first draw down of $300,000 on 26 August 2015 and second draw down of $300,000 in September 2015. The salient terms of the Loan Agreement are as follow:

(i) Interest rate of 10% per annum calculated daily is charged on the Loan; and

(ii) Establishment fee of $20,000 for the Loan Facility is to be paid;

The Loan, interest and establishment fee accrued are to be repaid in November 2015 from receipt of R&D Tax Incentive 2014/2015 to be received from AusIndustry.

Except for the above, there were no other matters or circumstances that have arisen since the end of the financial period which significantly affected or could significantly affect the operations of the Group, the results of these

operations or the state of affairs of the Group in future financial periods.

Basis of PreparationThe financial report has been prepared on a going concern basis which takes into account the Group’s assets and liabilities and assumes that funds will be obtained from several sources as outlined in Note 2 to the Notes to the Consolidated Financial Statements.

The audit opinion prepared by the independent auditor EY is not subject to any dispute or qualification, but is subject to an emphasis of matter paragraph regarding continuation of the Group as a going concern.

Likely Developments and Expected Results The year ahead will focus on consolidating the recent activities and pursuing further market and product opportunities which benefit from Bluechiip’s unique technology. Bluechiip will pursue its strategy to work and partner with original equipment manufacturers (OEM) to integrate Bluechiip technology with the OEM products. This is complemented by the launch of the Bluechiip Developer Kit released for OEM partner development. Bluechiip is also continuing to develop new reading technologies in the form of portable hand held reader and multi vial reader to meet the portable and high volume biobanking sector.

Funds generated and raised will be used for working capital requirements with a clear focus on sales, marketing and business development activities, including the operational capacity and resourcing within the Company.

The Company’s strategies above take into account the expected operating and market conditions. Bluechiip is exposed to a range of financial, market and operational risks and predicting future operating and market conditions is inherently uncertain. The material risks that could affect the Company’s financial prospects noted above may include the Company not being able to source sufficient funding for its commercialisation program, not being able to adequately protect its knowhow, expertise and trade secrets, difficulty in manufacturing its products at a commercially attractive price or competitors may develop products that are more effective or prove to be more readily acceptable by customers than those developed by the Company.

The Company has in place risk management and internal control systems to manage material risks.

Directors’ Report30 June 2015

For

per

sona

l use

onl

y

9

Environmental Regulation and PerformanceThe Group’s operations are not regulated by any significant environmental regulations under a law of the Commonwealth or of a state or territory.

Options

Unissued sharesAs at the date this report was signed, there were no unexercised options over ordinary shares. Refer to the Remuneration Report for details of the options outstanding issued to key management personnel.

Number of unlisted

options

Balance as at 30 June 2014 10,495,999

Options issued during the year 10,950,000

Options exercised during the year -

Options expired during the year (21,445,999)

Balance as at 30 June 2015 -

During the year, 1,500,000 performance rights (zero exercise price options) were issued to the CEO, Andrew McLellan on 27 April 2015. Further details of the performance rights and the terms are set out in the Variable Compensation - Long Term Incentive section. No other performance rights or options were issued to Directors or Key Management Personnel (KMP) in the financial

year ended 30 June 2015.

Indemnification of directors and officersThe Company has not granted any indemnity to any current or former directors or officers against any liability other than as provided in the Company’s constitution. However it is intended that the Company will indemnify the Directors and Company Secretary against any liability incurred while discharging their duties and obligations – subject to Part 20.2 of the Corporations Act.

During the financial year, the Company has paid premiums in respect of a contract insuring the directors of the Company (as named above) and all executive officers of the Company against a liability incurred as such a director, secretary or executive officer to the extent permitted by the Corporations Act 2001.

The total amount of Directors & Officers Liability insurance contract premiums paid was $19,412 (2014: $23,495).

Indemnification of auditorsTo the extent permitted by law, the Company has agreed to indemnify its auditors, Ernst & Young, as part of the terms of its audit engagement agreement against claims by third parties arising from the audit. No payment has been made to indemnify Ernst & Young during or since the financial year.

Directors’ meetingsThe number of meetings of directors (including meetings of committees of directors) held during the year and the number of meetings attended by each director was as follows:

Director’s meetings

Remuneration & Nomination committee

meetings (i)Audit committee

meetings

Eligible Attended Eligible Attended Eligible Attended

Number of meetings held 11 - - 2

I Kirkwood 11 11 - - 2 2

A McLellan 6 6 - - 1 1

J Chaffey 4 4 - - - -

M Morgan 11 11 - - 2 2

M Ohanessian 6 6 - - - -

J Baini 1 1 - - - -

R Finkel 1 1 - - - -

(i) During the year, Remuneration and Nomination committee matters were dealt with in meetings of Directors – but with executive personnel absent.

For

per

sona

l use

onl

y

10

| B

luec

hiip

Lim

ited

|

Ann

ual R

epor

t 20

15

Committee membershipAs at the date of this report, the Company had an Audit committee and a Remuneration and Nomination committee of the Board.

Members acting on the committees of the Board during the year were:

Audit Remuneration and Nomination

Matthew Morgan (Chairman) (Appointed as Chairman 1 August 2014)

Mr Michael Ohanessian (Chairman) (Appointed 20 February 2015)

Iain Kirkwood (former Chairman) (Chairman until 1 August 2014)

Iain Kirkwood (former Chairman) (Chairman 1 August 2014 - 20 February 2015)

Mr Andrew McLellan (20 February 2015 - 28 August 2015)

Matthew Morgan (Appointed 1 August 2014)

Mr Michael Ohanessian (Appointed 28 August 2015)

Joe Baini (former Chairman) (Resigned 1 August 2014)

Joe Baini (Resigned 1 August 2014)

Ron Finkel (Resigned 1 August 2014)

RoundingThe amounts contained in this report and in the financial report have been rounded to the nearest one dollar under the option available to the Company under ASIC CO 98/0100. The Company is an entity to which the Class Order applies.

Auditor independence declarationThe directors received the declaration set out on the following page from the auditor of Bluechiip Limited.

Non-audit servicesDuring the year, EY provided non-audit services relating to Bluechiip’s R&D tax off-set financing transaction. Fees for these services were $7,500 (2014: $9,000). The directors are satisfied that the provision of non-audit services is compatible with the general standard of independence for auditors imposed by the Corporations Act 2001. The nature, value and scope of the non-audit services are considered not to have compromised auditor independence.

Directors’ Report30 June 2015

For

per

sona

l use

onl

y

11

Auditor Independence Declaration

A member firm of Ernst & Young Global LimitedLiability limited by a scheme approved under Professional Standards Legislation

Ernst & Young8 Exhibition Street Melbourne VIC 3000 AustraliaGPO Box 67 Melbourne VIC 3001

Tel: +61 3 9288 8000Fax: +61 3 8650 7777ey.com/au

Auditor’s Independence Declaration to the Directors of Bluechiip Limited

In relation to our audit of the financial report of Bluechiip Limited for the financial year ended 30 June 2015, to the best of my knowledge and belief, there have been no contraventions of the auditor independence requirements of the Corporations Act 2001 or any applicable code of professional conduct.

Ernst & Young

David Petersen Partner 18 September 2015

For

per

sona

l use

onl

y

12

| B

luec

hiip

Lim

ited

|

Ann

ual R

epor

t 20

15

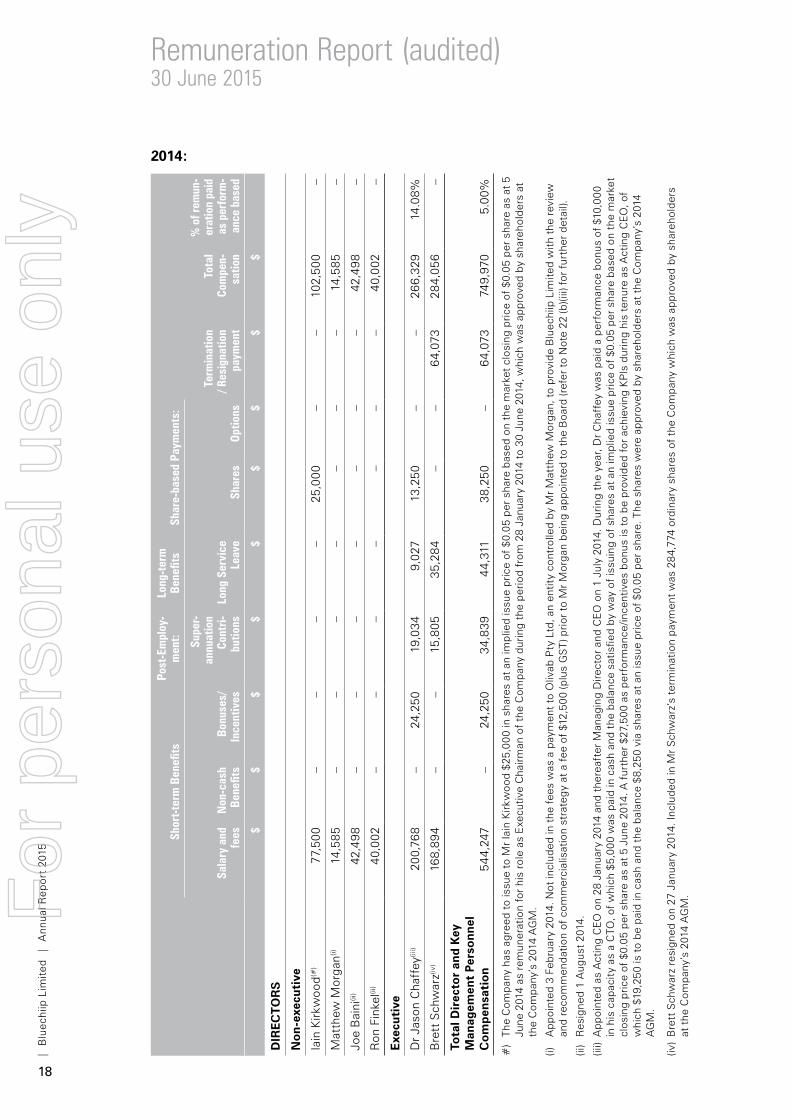

Remuneration Report (audited)30 June 2015

Compensation of ExecutivesThis report outlines the compensation arrangements in place for directors and senior executives of the Company being the KMP of the Company – being those persons having authority and responsibility for planning, directing and controlling the major activities of the Company, directly or indirectly, including any director and includes all the executives in the Company. For the purposes of this report, the term “executive” includes the interim CEO/CSO and senior executives but does not include the non-executive directors or the secretary of the Company.

All sections contained herein have been subject to audit as required by section 308(3C) of the Corporations Act. Remuneration is referred to as compensation in this report.

Individual KMP disclosuresDetails of KMP of the Company are set out below:

Directors

Mr Iain Kirkwood Non-Executive Chairman

Mr Andrew McLellan CEO/Managing Director – appointed 27 January 2015

Mr Matthew Morgan Non-Executive Director

Mr Michael Ohanessian Non-Executive Director – appointed 15 December 2014

Dr Jason Chaffey Former Managing Director and CEO – appointed 1 July 2014 and resigned 14 November 2014

Mr Joe Baini Non-Executive Director – resigned 1 August 2014

Mr Ron Finkel Non-Executive Director – resigned 1 August 2014

There have been no changes to KMP after the reporting date and before the date of this report.

Remuneration and Nomination CommitteeThe Remuneration and Nomination Committee of the Board is responsible for making recommendations to the Board on the remuneration arrangements for non-executive directors (NEDs) and executives. The Board approves the remuneration arrangements for executives having regard to the recommendations made by the Remuneration and Nomination Committee including any Short

Term Incentive (STI) or Long Term Incentive (LTI) arrangements. The Board also sets the aggregate fee pool for NEDs (which is subject to shareholder approval) and NED fee levels.

The Remuneration and Nomination Committee comprises all three NEDs, each of which is considered independent.

The Remuneration and Nomination Committee meets periodically during the year. Executives are not present at meetings of the Committee except by invitation.

The Remuneration and Nomination Committee has not engaged any external remuneration advisers during the financial year.

Further information on the Remuneration and Nomination Committee’s role, responsibilities and membership is located at http://www.bluechiip.com/corporate-governance/

Principles of Compensation and strategyThe Remuneration & Nomination Committee of the Board assesses the appropriateness of the nature and amount of remuneration of NEDs and executives on a periodic basis by reference to relevant employment market conditions, with the overall objective of ensuring maximum stakeholder benefit from the retention of a high performing director and executive team and aligning the interests of the executives with those of the shareholders. During the year, some Remuneration and Nomination Committee matters were dealt with in meetings of Directors, but with executive personnel absent.

Bluechiip’s remuneration strategy is designed to attract, motivate and retain employees and NEDs by identifying and rewarding high performers and recognising the contribution of each employee to the continued growth and success of the Company. To this end, key objectives of the Company’s reward framework are to ensure that remuneration practices are aligned to the Company’s business strategy, offer competitive remuneration benchmarked against the external market, provide strong linkage between individual and Group performance and rewards and align the interests of executives with shareholders. Where relevant, the remuneration framework incorporates at risk components through STI and LTI arrangements tailored to the particular executive by reference to both financial and other metrics which generate value for shareholders.

In accordance with best practice corporate governance, the structure of NED and executive remuneration is separate and distinct.

The Board assumes full responsibility for compensation policies and packages applicable to directors and senior executives of the

For

per

sona

l use

onl

y

13

Company. The broad compensation policy is to ensure the compensation package appropriately reflects the person’s duties and responsibilities, and that compensation levels are competitive in attracting, retaining and motivating people who possess the requisite level of skill and experience. Employees may receive at-risk incentive payments remunerated as cash or share options based on the achievement of specific goals related to the performance of the individual and the Company (as determined by the directors). Incentives are provided to senior executives and employees for the achievement of individual and strategic objectives with the broader view of creating value for shareholders.

Components of total compensation are ‘at risk’ (variable compensation) and dependent on meeting pre-determined performance benchmarks including Key Performance Indicators (KPIs). The inclusion of appropriate challenging performance hurdles in relation to variable compensation is designed to align employee performance with the creation of shareholder value and wealth. KPIs are agreed and set each year for KMP with the specific objective of influencing both short and long term performance and the generation of shareholder wealth.

Variable or performance-linked compensation comprises cash bonus and/or share based payments.

Fixed CompensationFixed compensation consists of a base salary and employer superannuation contributions. Fixed compensation levels are set so as to provide a base level of compensation which is both appropriate to the position and is competitive in the market.

Fixed compensation is reviewed at least annually by the Remuneration and Nomination Committee and the process consists of a review of the Company’s performance, relevant comparative compensation in the market and, where appropriate, external advice on policies and practices. Employees receive their fixed compensation in cash. The Board’s policy is to ensure that fixed remuneration is market competitive having regard to industry peers and companies of similar financial size. Given the Company’s size the Company generally undertakes its own review of these matters, which it does on an ongoing basis, but does from time to time engage remuneration consultants where considered necessary.

Key Performance Indicators (KPIs) are individually tailored by the Board, based on recommendations and input from the Remuneration & Nomination Committee in advance for each employee each year, and reflect an assessment of how that employee can fulfil his or her particular responsibilities in a way

that best contributes to Company performance and shareholder wealth in that year with close alignment to the role and responsibility within the organisation and in conjunction with the strategic objectives of the Company.

Performance linked CompensationAll employees are potentially eligible to receive at-risk incentive payments and/or securities (shares or options) based on the achievement of specific goals related to (i) performance against individual KPI’s and/or (ii) the performance of the Company as a whole as determined by the Board based on a range of factors, both financial and non-financial. These factors include traditional financial considerations such as operating performance, cash consumption and deals concluded and also industry-specific factors. The purpose of these payments is to reward employees for their contribution to the Company.

Employment contracts for staff other than the CEO provide for variable compensation of up to 10 per cent of their total fixed compensation package (although higher variable compensation payments may be made at the Board’s discretion).

The Remuneration & Nomination Committee makes a recommendation annually to the Board in respect of incentive compensation for employees and executives. The Board at its sole discretion determines the total amount of variable compensation payable as a percentage of the total annualised salaries for all employees employed as at the end of the financial year (with pro rata reductions to the annualised salary made for any employee not employed for the entire financial year).

The CEO has the discretion to recommend the offer of rights or options to acquire ordinary shares or the direct issue of shares to any member of staff in recognition of exemplary performance. Such securities may be fully vested upon issue given that they are issued as a reward for past performance rather than as a long term incentive. Any issue of rights or options proposed as incentive compensation requires approval by the Board and is subject to any limitations imposed by the Corporations Act and the ASX Listing Rules. The Board considers that the performance linked compensation structure is operating effectively.

At, or as soon as practicable after, the beginning of the financial year, individual and team performance for the previous year is assessed for every employee by their manager and new objectives set for the forthcoming year. These objectives include department and project specific objectives together with individual stretch objectives, challenging, realistic and personal development objectives tailored to the employee’s role within the organisation. Measurement, management support, target

For

per

sona

l use

onl

y

14

| B

luec

hiip

Lim

ited

|

Ann

ual R

epor

t 20

15

dates and training course requirements are all set. Progress against the objectives is reviewed during the year and percentage achievement concluded at the end of the year, whereupon the cycle recommences. The outputs of this process form the basis of the assessment of the individual’s personal incentive compensation.

The Board has discretion to reduce, cancel or clawback any unvested performance-based remuneration in the event of serious misconduct or a material misstatement in the Group’s financial statements.

Variable Compensation – Short Term Incentive (STI)The Company does not operate a formal STI program other than in respect of the CEO. The CEO is eligible to receive a cash bonus subject to the attainment of defined KPIs. The actual STI payment awarded to the CEO will depend on the extent to which specific targets set at the beginning of the year are met but potentially could be an amount equal to 25% of the CEO’s base remuneration package.

A summary of the measures and weightings are set out below.No payment has been approved for the financial year ended 30 June 2015 (2014 $10,000), by way of an employee benefit provision in respect of performance incentives for the 2015 financial year.

An amount of $4,227 (2014: 93,331) has been recognised in the 2015 financial year by way

of share based payment expense in respect of performance rights issues (unvested) issued to performance incentives achieved in respect of key performance indicators set for the 2015 financial year.

Service contractsRemuneration arrangements for executives are formalised in employment agreements. The following outlines the details of contracts with executives.

Chief Executive OfficerThe CEO, Mr McLellan, is employed under an ongoing employment contract which can be terminated with notice by either party.

The key terms of the contract are as follows:

• Annual base Salary of $275,000 including superannuation;

• Short Term Incentive of a cash being up to 25% of annual base salary payable on the achievement of agreed performance targets;

• Long Term Incentive being the grant (subject to shareholder approval) of 1,500,000 performance rights each entitling Mr McLellan to acquire one fully paid share in the Company for a nil exercise price (Performance Rights). Vesting of the Performance Rights are subject to achievement of performance conditions relating to TSR and agreed financial targets over the measurement period (1 July 2015 to 30 June 2018)

Remuneration Report (audited)30 June 2015

Notice period

Payment in lieu of notice

Treatment of short term incentives

Treatment of Long Term incentives

Termination by Company (death, disablement, redundancy etc)

3 months 3 months Any STI payments are at Board discretion

At the discretion of the Board

Termination for Cause None None Any STI payments are at Board discretion

Unvested awards forfeited. Vested and unexercised awards forfeited.

Resignation by Employee 3 months None Any STI payments are at Board discretion

Unvested awards forfeited.

• All other KMP are or were employed under contracts with the following common terms and conditions:

- combination of twelve (12) months fixed terms and/or no fixed term and no termination payment prescribed;

- terminable by either party on the giving of one (1) month notice in writing; and

- the Company may terminate any contract for cause as defined.

For

per

sona

l use

onl

y

15

Variable Compensation – Long Term Incentive (LTI)The Remuneration and Nomination Committee also reviews and approves the issue of share based payments to staff and KMP as a means of providing a LTI for performance and loyalty.

LTI awards to executives are made under the executive Performance Rights Plan and are delivered in the form of performance rights or zero exercise price options. The performance rights will vest over a period of up to three years subject to meeting performance measures,

The Company uses a combination of absolute total shareholder return (TSR) and commercial targets (CS Targets) as the performance measure for the LTI plan. The details of the performance measures are as follow:

Performance Measure Rules

TSR performance targets

The TSR hurdle in relation to the TSR Rights is based on the TSR of Bluechiip securities measured over the Performance periods. Performance has regard to the starting share price of $0.08 per share as at 27 January 2015 and the 30 day Volume Weighted Average Price (VWAP) as at 30 June 2017 for TSR-1 and 30 June 2018 for TSR-2.

CS performance targets

The CS hurdle is based on Bluechiip achieving commercial sales and royalty income targets over the Performance periods.

During the year, a total of 1,500,000 Performance Rights were granted (subject to shareholders approval) to Mr McLellan. The Performance Rights have been issued in two tranches of 750,000 (i.e. a total of 1,500,000 Performance Rights).

Tranche 1 Performance Rights

Vesting Date: 27 January 2017 (subject to achievement of Performance Targets)

Performance Period:

27 January 2015 to 27 January 2017

Expiry Date: 27 April 2020

Performance Targets:

50% of the Tranche 1 Performance Rights will vest based on achievement of CS Targets.

The balance of the Tranche 1 Performance Rights will vest based on the TSR of Bluechiip shares over the Performance Period having regard to a starting value of $0.08 per share as at 27 January 2015 (TSR-1). The vesting schedule is as follows:

Bluechiip TSR-1 Percentage of Performance Rights Vesting

Less than 150% 0%

150% or more but less than or equal to 250%

Vest progressively on a pro rata basis from 50% to 100%

Greater than 250% 100%

Tranche 2 Performance Rights

Vesting Date: 27 January 2018 (subject to achievement of Performance Targets)

Performance Period:

27 January 2015 to 27 January 2018

Expiry Date: 27 April 2020

Performance Targets:

50% of the Tranche 2 Performance Rights will vest based on achievement of CS Targets.

The balance of the Tranche 2 Performance Rights will vest based on the TSR of Bluechiip shares over the Performance Period having regard to a starting value of $0.08 per share as at 27 January 2018 (TSR-2). The vesting schedule is as follows:

For

per

sona

l use

onl

y

16

| B

luec

hiip

Lim

ited

|

Ann

ual R

epor

t 20

15

Bluechiip TSR-2 Percentage of Performance Rights Vesting

Less than 250% 0%

250% or more but less than or equal to 375%

Vest progressively on a pro rata basis from 50% to 100%

Greater than 375% 100%

2015:1,500,000 performance rights (zero exercise price options) were issued to the CEO on 27 April 2015 on the terms specified above. No other performance rights or options were issued to Directors or KMP in the financial year ended 30 June 2015.

2014:No options were issued to Directors or KMP in the financial year ended 30 June 2014.

Non-Executive Director CompensationThe Constitution and the ASX Listing Rules specify that the aggregate compensation of Non-Executive Directors shall be determined from time to time by a general meeting. An amount not exceeding the amount approved by shareholders is then divided between the Directors as agreed by the Board. An amount of $500,000 was approved at the Company’s Annual General Meeting held on 10 November 2011.

Non-Executive Directors do not receive performance related compensation and the structure of Non-Executive Director and senior management compensation is separate and distinct. Non-Executive Directors do not have contracts of employment but are required to evidence their understanding and compliance with the Board policies of Bluechiip Limited. These Board policies do not prescribe how compensation levels for Non-Executive Directors are modified from year to year.

Compensation levels are to be reviewed by the Board each year taking into account cost of living changes, changes to the scope of the roles of the Directors, and any changes required to meet the principles of the overall Board policies.

The remuneration of Non-Executive Directors’ for the years ended 30 June 2015 and 30 June 2014 is detailed in the table below under ‘Remuneration of Key Management Personnel’.

Directors’ and Executive Officers’ Compensation TablesDetails of the nature and amount of each major element of the compensation of each KMP including Directors of the Company are disclosed in accordance with Accounting Standard AASB 124 Related Party Disclosures and with the Corporations Act 2001 in the following tables.

No options or performance rights held by persons in the following compensation tables were exercised during the 2014 and 2015 financial years.

In the following tables, the fair value of the performance rights granted to executive officers has been calculated based on the value at the date of grant using a valuation model that takes into account the performance hurdles and vesting period related to those performance rights. The value as disclosed is the portion of the fair value of the performance rights allocated to this reporting year. Refer to the next sections of this report for full details of the performance rights valuations.

LoanThere were no loans to any Directors or KMPs during the financial year.

Other transactions and balances with KMPDuring the year, Mr Kirkwood and Mr Ohanessian in connection with the Company’s placement to sophisticated and professional investors in April 2015 agreed to subscribe for 1,811,011 ordinary shares of the Company in aggregate at an issue price of $0.045 per share subject to the approval of the shareholders at the forthcoming Annual General Meeting (refer to Note 22(b)(iii) for further details).

Remuneration Report (audited)30 June 2015

For

per

sona

l use

onl

y

17

2015:

Shor

t-ter

m B

enefi

tsPo

st-

Empl

oym

ent:

Long

-ter

m

Bene

fits

Shar

e-ba

sed

Paym

ents

:

Term

inat

ion

/ Res

igna

tion

paym

ent

Tota

l Co

mpe

n-sa

tion

% o

f rem

un-

erat

ion

paid

as

per

form

-an

ce b

ased

Sala

ry a

nd

fees

Non

-cas

h Be

nefit

sBo

nuse

s/

Ince

ntiv

es

Supe

r-an

nuat

ion

Cont

ri-

butio

ns

Long

Se

rvic

e Le

ave

Shar

es

Optio

ns/

Perf

orm

ance

Ri

ghts

$$

$$

$$

$$

$

DIR

EC

TOR

S

No

n-e

xecu

tive

Iain

Kirk

woo

d70

,000

--

--

--

-70

,000

0.0%

Mat

thew

Mor

gan

35,0

04-

--

--

--

35,0

040.

0%

Mic

hael

Oha

ness

ian (i

) 20

,000

--

--

--

-20

,000

0.0%

Joe

Bai

ni (i

i)2,

917

--

--

--

-2,

917

0.0%

Ron

Fin

kel (i

i)2,

917

--

--

--

-2,

917

0.0%

Exe

cuti

ve

And

rew

McL

ella

n (iii)

#*

99,1

948,

889

-10

,268

1,92

1-

4,22

7-

124,

499

3.4%

Dr

Jaso

n C

haff

ey (i

v)**

79,5

82-

-10

,173

--

-54

,239

143,

994

0.0%

Tota

l Dir

ecto

r an

d K

ey

Man

agem

ent

Pers

onn

el

Co

mp

ensa

tio

n30

9,61

48,

889

-20

,441

1,92

1-

4,22

754

,239

399,

331

1.1%

(i)

App

oint

ed 1

5 D

ecem

ber

2014

.

(ii)

Res

igne

d 1

Aug

ust

2014

.

(iii)

App

oint

ed 2

7 Ja

nuar

y 20

15

(iv) J

ason

Cha

ffey

res

igne

d fr

om B

luec

hiip

as

CEO

and

Man

agin

g D

irect

or o

n 14

Nov

embe

r 20

14.

# T

his

rela

tes

to m

onth

ly n

ovat

ed le

ase

paym

ent

mad

e on

beh

alf

of A

ndre

w M

cLel

lan.

* D

urin

g th

e ye

ar, 1

,500

,000

per

form

ance

rig

hts

wer

e gr

ante

d to

And

rew

McL

ella

n as

par

t of

the

Lon

g Te

rm In

cent

ive.

An

amou

nt o

f $4

,227

has

bee

n re

cogn

ised

in t

he 2

015

by w

ay o

f sh

are

base

d pa

ymen

t ex

pens

e in

res

pect

of

the

Perf

orm

ance

Rig

hts.

Fur

ther

det

ails

of

the

Perf

orm

ance

Rig

hts

and

the

term

s ar

e se

t ou

t in

the

Var

iabl

e C

ompe

nsat

ion

- LTI

sec

tion.

** N

ot in

clud

ed in

the

rem

uner

atio

n of

Jas

on C

haff

ey is

a f

ee p

aid

to L

umic

yn P

ty L

td, a

com

pany

ow

ned

by J

ason

Cha

ffey

for

pro

visi

on o

f ad

viso

ry s

ervi

ce t

o B

luec

hiip

for

a p

erio

d fr

om 1

9 N

ovem

ber

2014

to

17 D

ecem

ber

2014

aft

er h

is r

esig

natio

n.

For

per

sona

l use

onl

y

18

| B

luec

hiip

Lim

ited

|

Ann

ual R

epor

t 20

15

Shor

t-ter

m B

enefi

tsPo

st-E

mpl

oy-

men

t:Lo

ng-t

erm

Be

nefit

sSh

are-

base

d Pa

ymen

ts:

Term

inat

ion

/ Res

igna

tion

paym

ent

Tota

l Co

mpe

n-sa

tion

% o

f rem

un-

erat

ion

paid

as

per

form

-an

ce b

ased

Sala

ry a

nd

fees

Non

-cas

h Be

nefit

sBo

nuse

s/

Ince

ntiv

es

Supe

r-an

nuat

ion

Cont

ri-

butio

nsLo

ng S

ervi

ce

Leav

eSh

ares

Optio

ns

$$

$$

$$

$$

$

DIR

EC

TOR

S

No

n-e

xecu

tive

Iain

Kirk

woo

d(#

)77

,500

––

––

25,0

00–

–10

2,50

0–

Mat

thew

Mor

gan(i)

14,5

85–

––

––

––

14,5

85–

Joe

Bai

ni(ii

)42

,498

––

––

––

–42

,498

–

Ron

Fin

kel(ii

)40

,002

––

––

––

–40

,002

–

Exe

cuti

ve

Dr

Jaso

n C

haff

ey(ii

i)20

0,76

8–

24,2

5019

,034

9,02

713

,250

––

266,

329

14.0

8%

Bre

tt S

chw

arz(iv

)16

8,89

4–

–15

,805

35,2

84–

–64

,073

284,

056

–

Tota

l Dir

ecto

r an

d K

ey

Man

agem

ent

Pers

onn

el

Co

mp

ensa

tio

n54

4,24

7–

24,2

5034

,839

44,3

1138

,250

–64

,073

749,

970

5.00

%

#)

The

Com

pany

has

agr

eed

to is

sue

to M

r Ia

in K

irkw

ood

$25,

000

in s

hare

s at

an

impl

ied

issu

e pr

ice

of $

0.05

per

sha

re b

ased

on

the

mar

ket

clos

ing

pric

e of

$0.

05 p

er s

hare

as

at 5

Ju

ne 2

014

as r

emun

erat

ion

for

his

role

as

Exe

cutiv

e C

hairm

an o

f th

e C

ompa

ny d

urin

g th

e pe

riod

from

28

Janu

ary

2014

to

30 J

une

2014

, whi

ch w

as a

ppro

ved

by s

hare

hold

ers

at

the

Com

pany

’s 2

014

AG

M.

(i)

App

oint

ed 3

Feb

ruar

y 20

14. N

ot in

clud

ed in

the

fee

s w

as a

pay

men

t to

Oliv

ab P

ty L

td, a

n en

tity

cont

rolle

d by

Mr

Mat

thew

Mor

gan,

to

prov

ide

Blu

echi

ip L

imite

d w

ith t

he r

evie

w

and

reco

mm

enda

tion

of c

omm

erci

alis

atio

n st

rate

gy

at a

fee

of

$12,

500

(plu

s G

ST)

prio

r to

Mr

Mor

gan

bein

g ap

poin

ted

to t

he B

oard

(ref

er t

o N

ote

22 (b

)(iii)

for

fur

ther

det

ail).

(ii)

Res

igne

d 1

Aug

ust

2014

.

(iii)

App

oint

ed a

s A

ctin

g C

EO

on

28 J

anua

ry 2

014

and

ther

eaft

er M

anag

ing

Dire

ctor

and

CE

O o

n 1

July

201

4. D

urin

g th

e ye

ar, D

r C

haff

ey w

as p

aid

a pe

rfor

man

ce b

onus

of

$10,

000

in h

is c

apac

ity

as a

CTO

, of

whi

ch $

5,00

0 w

as p

aid

in c

ash

and

the

bala

nce

satis

fied

by w

ay o

f is

suin

g of

sha

res

at a

n im

plie

d is

sue

pric

e of

$0.

05 p

er s

hare

bas

ed o

n th

e m

arke

t cl

osin

g pr

ice

of $

0.05

per

sha

re a

s at

5 J

une

2014

. A f

urth

er $

27,5

00 a

s pe

rfor

man

ce/in

cent

ives

bon

us is

to

be p

rovi

ded

for

achi

evin

g K

PIs

dur

ing

his

tenu

re a

s A

ctin

g C

EO

, of

whi

ch $

19,2

50 is

to

be p

aid

in c

ash

and

the

bala

nce

$8,2

50 v

ia s

hare

s at

an

issu

e pr

ice

of $

0.05

per

sha

re. T

he s

hare

s w

ere

appr

oved

by

shar

ehol

ders

at

the

Com

pany

’s 2

014

AG

M.

(iv)

Bre

tt S

chw

arz

resi

gned

on

27 J

anua

ry 2

014.

Incl

uded

in M

r S

chw

arz’

s te

rmin

atio

n pa

ymen

t w

as 2

84,7

74 o

rdin

ary

shar

es o

f th

e C

ompa

ny w

hich

was

app

rove

d by

sha

reho

lder

s at

the

Com

pany

’s 2

014

AG

M.

2014:

Remuneration Report (audited)30 June 2015

For

per

sona

l use

onl

y

19

Grants, Modifications and Exercise of Options and Rights Over Equity Instruments Granted as Compensation

2015:Other than 1,500,000 performance rights granted to Andrew McLellan, there were no options granted as compensation during the financial year to any other person in the Directors’ and KMP’s compensation table. During the financial year no Performance Rights held by this person lapsed. There were no alterations or modifications to existing terms and conditions during the year ended 30 June 2015.

2014:There were no options granted as compensation during the financial year 2014 to any other person in the Directors’ and KMP’s compensation table and all options held by these persons lapsed. There were no alterations or modifications to existing terms and conditions during the year ended 30 June 2014.

Fair Value of Performance RightsThe fair value of the performance rights granted to the CEO and officers in the table below has been calculated at grant date using a Black-Scholes-Merton model to value the performance rights over the shares, the Binomial Option Pricing Model to estimate the value of the performance rights and Monte Carlo simulation based models to test the likelihood of attaining the performance hurdle. The following factors and assumptions have been used in determining the fair value on grant date. A zero dividend yield assumption has been adopted in every valuation.

2015

Number and recipient Performance Rights

Grant date

Expiry date

Fair value per Performance

RightExercise

price

Price of shares

on value date

Risk free interest

rateEstimated

volatility

1,500,000 to Andrew McLellan comprising:

27 April 2015

27 April 2020

• Tranche 1 TSR: 375,000 $0.012 Nil $0.057 1.926% 80%

• Tranche 2 TSR: 375,000 $0.014 Nil $0.057 1.882% 80%

• CS Target 750,000 $0.057 Nil $0.057

Not applicable 80%

2014No options were issued to Directors or other KMP in the financial year ended 30 June 2014.

Other than the Performance Rights granted to the CEO, Andrew McLellan as above, no options were issued to Directors or other KMP in the financial year ended 30 June 2015.

For

per

sona

l use

onl

y

20

| B

luec

hiip

Lim

ited

|

Ann

ual R

epor

t 20

15

Shares Issued on Exercise of OptionsSince the end of the financial year up to the date of this report no options have been exercised.

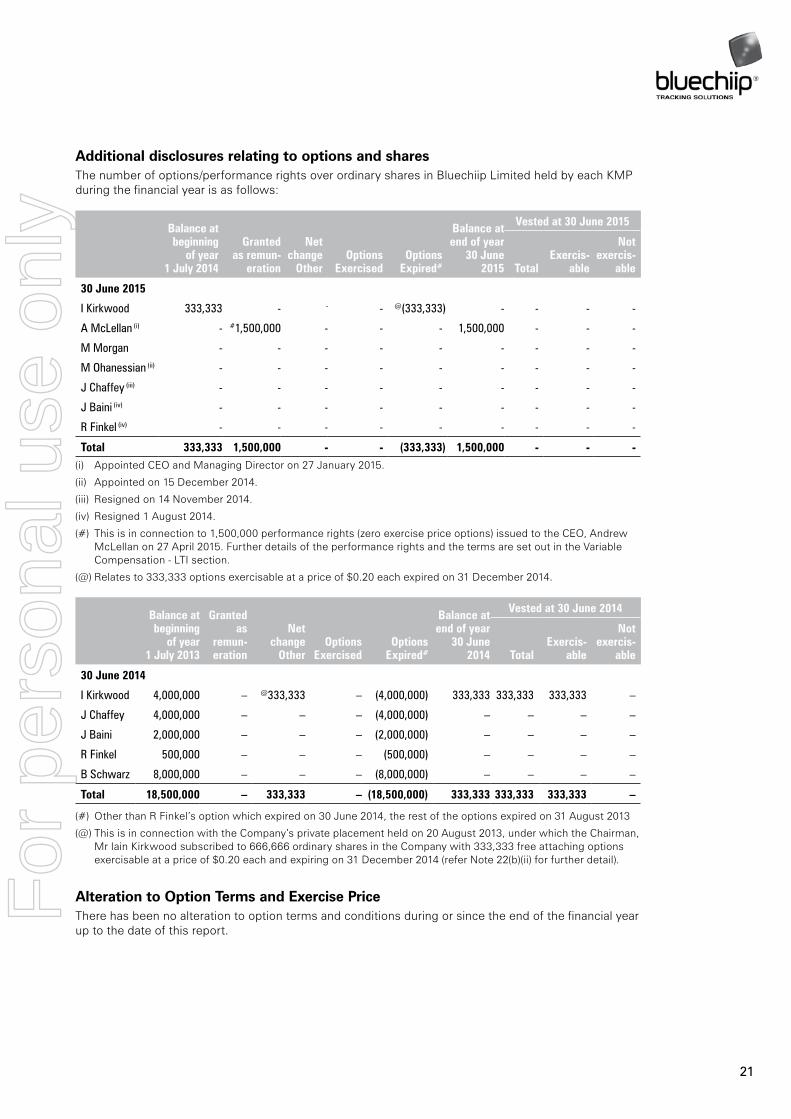

Additional disclosures relating to options and sharesThe number of ordinary shares in Bluechiip Limited held by or controlled by each KMP of the Group during the financial year is as follows:

2015:

Balance at 1 July

2014

Granted as remuner-

ationPurchased

during year

On exercise of options/

performance rights

Net change other

Balance at 30 June

2015

30 June 2015

I Kirkwood (i) 8,844,127 500,000 - - - 9,344,127

A McLellan (ii) - - 348,000 - - 348,000

M Morgan 100,000 - 150,000 - - 250,000

M Ohanessian (iii) - - - - - -

J Chaffey (iv) 458,458 206,250 - - (664,708) -

J Baini (v) 104,000 - - - (104,000) -

R Finkel (v) 158,958 - - - (158,958) -

Total 9,665,543 706,250 498,000 - (927,666) 9,942,127

(i) During the year the Company issued to Mr Iain Kirkwood $25,000 in shares at an implied issue price of $0.05 per share based on the market closing price of $0.05 per share as at 5 June 2014 as remuneration for his role as Executive Chairman of the Company during the period from 28 January 2014 to 30 June 2014, The share issue was approved by the shareholders at the Company’s 2014 AGM.

(ii) Appointed CEO and Managing Director on 27 January 2015.

(iii) Appointed on 15 December 2014.

(iv) Resigned on 14 November 2014. During the year the Company issued to Dr Jason Chaffey $8,250 in shares at an issue price of $0.05 per share as part of performance/incentives bonus of $19,250 for achieving KPIs during his tenure as Acting CEO, via shares at an issue price of $0.05 per share. The shares were approved by shareholders’ at the Company’s 2014 AGM. The number of shares held on 14 November 2014 at the time of resignation was 664,708.

(v) Resigned 1 August 2014.

2014:

Balance at 1 July 2013

Granted as remuner-

ationPurchased

during yearOn exercise

of optionsNet change

other

Balance at 30 June

2014

30 June 2014

I Kirkwood(i) 7,602,460 – 1,241,667 – – 8,844,127

J Chaffey(ii) 353,458 100,000 5,000 – – 458,458

M Morgan(iii) – – 100,000 – – 100,000

J Baini(iv) 104,000 – – – – 104,000

R Finkel(iv) – – 158,958 – – 158,958

B Schwarz(v) 7,602,000 – 5,000 – (7,607,000) –

Total 15,661,918 100,000 1,510,625 – (7,607,000) 9,665,543

(i) Mr Iain Kirkwood subscribed in connection with the Company’s private placement held on 20 August 2013, to 666,666 ordinary shares and 333,333 free attaching options at an issue price of $0.15 per share exercisable at a price of $0.20 each and with expiry on 31 December 2014. The issue of these shares was approved by shareholders at the 2013 AGM.

(ii) Appointed Acting CEO (former CTO) on 28 January 2014 and subsequently as CEO and Managing Director of the Company on 1 July 2014. The opening balance represents the shareholding as at the date appointment as Acting CEO.

(iii) Appointed on 3 February 2014.

(iv) Resigned 1 August 2014.

(v) Resigned on 27 January 2014. The number of shares held on 27 January 2014 at the time of resignation was 7,607,000.

Remuneration Report (audited)30 June 2015

For

per

sona

l use

onl

y

21

Additional disclosures relating to options and sharesThe number of options/performance rights over ordinary shares in Bluechiip Limited held by each KMP during the financial year is as follows:

Balance at beginning

of year 1 July 2014

Granted as remun-

eration

Net change

OtherOptions

ExercisedOptions

Expired#

Balance at end of year

30 June 2015

Vested at 30 June 2015

TotalExercis-

able

Not exercis-

able

30 June 2015

I Kirkwood 333,333 - - - @(333,333) - - - -

A McLellan (i) - #1,500,000 - - - 1,500,000 - - -

M Morgan - - - - - - - - -

M Ohanessian (ii) - - - - - - - - -

J Chaffey (iii) - - - - - - - - -

J Baini (iv) - - - - - - - - -

R Finkel (iv) - - - - - - - - -

Total 333,333 1,500,000 - - (333,333) 1,500,000 - - -(i) Appointed CEO and Managing Director on 27 January 2015.

(ii) Appointed on 15 December 2014.

(iii) Resigned on 14 November 2014.

(iv) Resigned 1 August 2014.

(#) This is in connection to 1,500,000 performance rights (zero exercise price options) issued to the CEO, Andrew McLellan on 27 April 2015. Further details of the performance rights and the terms are set out in the Variable Compensation - LTI section.

(@) Relates to 333,333 options exercisable at a price of $0.20 each expired on 31 December 2014.

Balance at beginning

of year 1 July 2013

Granted as

remun-eration

Net change

OtherOptions

ExercisedOptions

Expired#

Balance at end of year

30 June 2014

Vested at 30 June 2014

TotalExercis-

able

Not exercis-

able

30 June 2014

I Kirkwood 4,000,000 – @333,333 – (4,000,000) 333,333 333,333 333,333 –