26

Slide 1 [xx] GALAXY RESOURCES LIMITED US/Canada Ins6tu6onal Roadshow January 2016 ASX: GXY For personal use only

Slide 1 [xx]

GALAXY RESOURCES LIMITED US/Canada Ins6tu6onal Roadshow

January 2016 ASX: GXY

For

per

sona

l use

onl

y

Slide 2 [xx] Galaxy Resources Limited (ASX:GXY)

Company Highlights

§ One of the premier global lithium opportuni6es with market leading assets

§ Diversified porLolio with hard rock and brine based lithium assets across mulMple geographies

§ Spodumene and tantalum produc6on to commence at end Q1 2016 from Mt CaPlin, with near-‐term cash flow expected

§ Flagship Sal De Vida Project in Argen6na with market leading brine chemistry

§ New management has transformed balance sheet, reduced net debt from over A$200m historically to A$20m today

§ Highly credenMaled Management and Board with strong networks in the key Asian lithium markets

§ Robust lithium macro trends with surging demand from energy storage applica6ons and a lagged supply-‐side response

2

En route to Sal de Vida lithium project – Argen:na

Mt Ca=lin Opera:ons – Australia

For

per

sona

l use

onl

y

Slide 3 [xx] Galaxy Resources Limited (ASX:GXY)

Corporate Snapshot

Share price performance (1 year)

Financial Informa6on (2016.01.25) Share Price A$0.195

52 week high / low A$0.210 / A$0.023

Number of shares (m, undiluted)1,2 1,264

Market Capitaliza6on A$247m

Proforma Cash3 A$11m

Proforma Debt A$31m

Proforma Net debt A$20m

Enterprise value A$267m

Source: IRESS Notes: 1 Excludes 43.9m unlisted opMons on issue at various vesMng and expiry dates with

exercise prices between A$0.03 and A$1.16 2 Excludes 34.1m share appreciaMon rights 3 Includes cash reserve from debt facility

An emerging global lithium business with leading ins6tu6onal shareholders and an increasing share price

3

Shares %

Acorn Capital 82.5m 6.5%

Paradice Investment Management 72.3m 5.7%

Private Individual 43.8m 3.5%

OCP Asia 42.5m 3.4%

Creat Group 37.6m 3.0%

Private Individual 35.9m 2.8%

Deutsche SecuriMes 28.4m 2.2%

Nero Resource Fund 28.3m 2.2%

Eternal Faith Holdings 19.6m 1.6%

UBS 18.3m 1.4%

Management 61.1m 4.8%

Top 10 409.2m 32.3%

Top Shareholders

Share Price Performance (1 Year)

-‐

10

20

30

40

50

-‐

0.04

0.08

0.12

0.16

0.20

Jan-‐15 Apr-‐15 Jul-‐15 Oct-‐15 Jan-‐16

Volume (m) Share price (A$)

Volume GXY S&P/ASX Small Resources Index

For

per

sona

l use

onl

y

Slide 4 [xx] Galaxy Resources Limited (ASX:GXY)

Board & Management

Anthony Tse – Managing Director § 20+ years corporate experience in high growth industries, including

technology, media and resources

§ Extensive senior management experience in corporate strategy and development, M&A, capital markets

§ Former Director Corporate Development at Hutchison Whampoa’s TOM Group (HKSE:2383), Deputy General Manager of TOM Online (NASDAQ:TOMO), President of CETV and CEO of CSN Corp.

Charles Whi^ield – Execu1ve Director § Principal Investment Officer of Drumrock Capital

§ Formerly Managing Director at CiMgroup, Corporate Equity SoluMons, and Deutsche Bank, Strategic Equity TransacMons

Mar6n Rowley – Independent Non-‐Execu1ve Chairman § Co-‐founder and ExecuMve Director of First Quantum

§ First Quantum is among the largest copper producMon companies in the world with a market cap of C$4bn

§ Non-‐ExecuMve Chairman of Forsys Metal Corp (TSX: FSY)

§ Previously Non-‐ExecuMve Chairman of Lithium One Inc. (acquired by Galaxy in July 2012)

Jian-‐Nan Zhang – Non-‐Execu1ve Director § Deputy General Manager of Fengli Group, a subsidiary of a

leading private Chinese industrial group

§ Galaxy’s Chairman is a respected leader in the global mining industry and a co-‐founder of First Quantum (TSX: FM)

§ New Managing Director appointed in 2013 successfully led Galaxy turnaround and restructuring

§ Team brings strong financial acumen to Galaxy, with over an aggregate A$300m of debt restructuring, M&A and financing completed without external advisors

§ Importantly, the current management and key employees have successfully developed lithium projects into produc6on and have established customer relaMonships in key Asian markets

The new Board and Management Team has successfully transformed the balance sheet, reducing net debt from over A$200m to A$20m

4

Execu:ve Board members Non-‐Execu:ve Board members

For

per

sona

l use

onl

y

Slide 5 [xx] Galaxy Resources Limited (ASX:GXY)

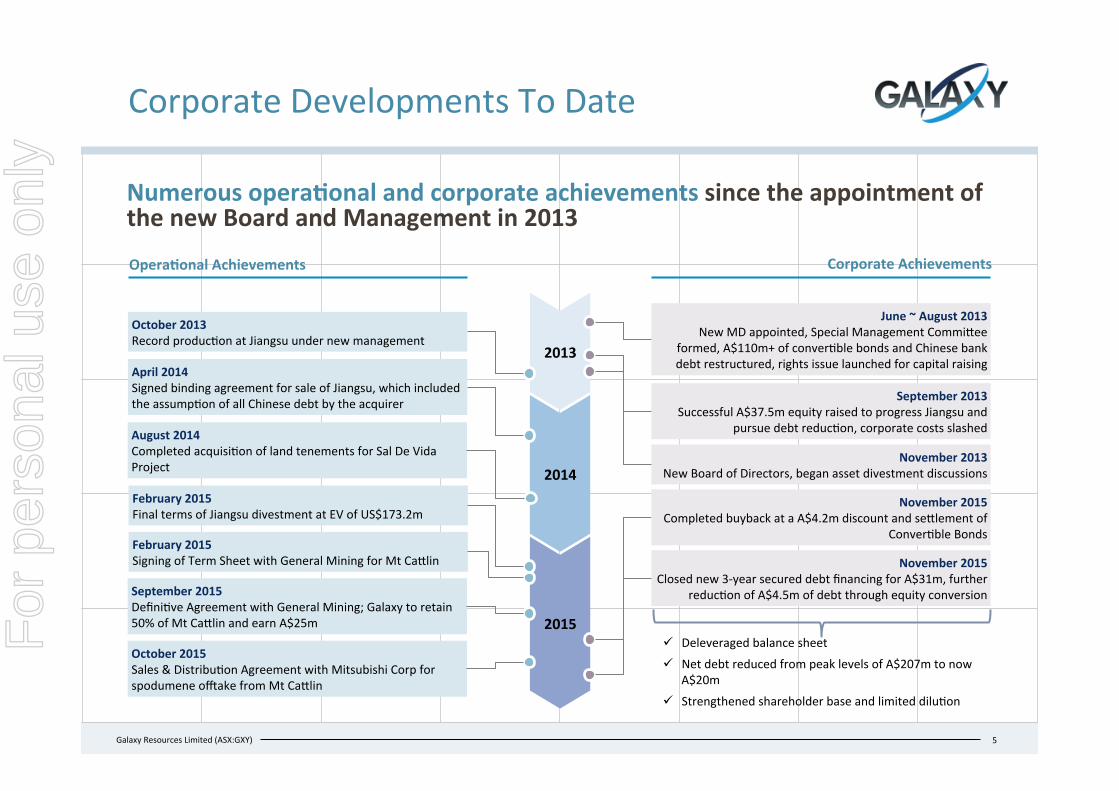

Corporate Developments To Date

October 2013 Record producMon at Jiangsu under new management

September 2015 DefiniMve Agreement with General Mining; Galaxy to retain 50% of Mt CaPlin and earn A$25m

February 2015 Final terms of Jiangsu divestment at EV of US$173.2m

April 2014 Signed binding agreement for sale of Jiangsu, which included the assumpMon of all Chinese debt by the acquirer

June ~ August 2013 New MD appointed, Special Management CommiPee

formed, A$110m+ of converMble bonds and Chinese bank debt restructured, rights issue launched for capital raising

Numerous opera6onal and corporate achievements since the appointment of the new Board and Management in 2013

October 2015 Sales & DistribuMon Agreement with Mitsubishi Corp for spodumene ooake from Mt CaPlin

5

Corporate Achievements Opera6onal Achievements

September 2013 Successful A$37.5m equity raised to progress Jiangsu and

pursue debt reducMon, corporate costs slashed

February 2015 Signing of Term Sheet with General Mining for Mt CaPlin

November 2013 New Board of Directors, began asset divestment discussions

2013

2014

2015

November 2015 Closed new 3-‐year secured debt financing for A$31m, further

reducMon of A$4.5m of debt through equity conversion

ü Deleveraged balance sheet ü Net debt reduced from peak levels of A$207m to now

A$20m

ü Strengthened shareholder base and limited diluMon

August 2014 Completed acquisiMon of land tenements for Sal De Vida Project

November 2015 Completed buyback at a A$4.2m discount and sePlement of

ConverMble Bonds

For

per

sona

l use

onl

y

Slide 6 [xx] Galaxy Resources Limited (ASX:GXY)

31.0

(20.0)

Financial Restructuring Complete

Galaxy has successfully completed its balance sheet restructuring ini6a6ves and is in its strongest financial posi6on in over 2 years

6

Jun-‐13: § Secured total of A

$10m bridge financing

§ Used for working capital and interest payments

Jul-‐13: § Restructure of

A$61.5m 8% converMble bonds, removed put-‐opMon

§ RenegoMated US$51m Chinese debt falling due

§ Launched rights issue

Sep-‐13: § A$37.5m raised in

rights issue, applied to debt reducMon and working capital

§ Corporate costs reduced by over 50%

Apr-‐14: § Announced

divestment of Jiangsu OperaMons

§ TransacMon subject to China regulatory approvals

Apr-‐15: § Jiangsu sale

completed at an enterprise value of US$173.2m

§ As a result of the sale, US$101.5m of debt deconsolidated from balance sheet

Nov-‐15: § Discounted buyback

and sePlement of CBs (saving A$4.2m)

§ New A$31m 3-‐year debt financing

§ A$4.45m of debt converted to equity

Gross Debt (A$m)

Net Debt (A$m)

Cash (A$m)

Dec-‐12 Jun-‐13 Dec-‐13 Jun-‐14 Dec-‐14 Jun-‐15 Current

7.7 1.4 2.8 2.4 13.4 42.9

12.0

(168.1)

(160.4) (193.2)

(191.8)

(183.7)

(180.9)

(192.4)

(190.0)

(220.3)*

(206.9)

(64.5)

(21.6)

Balance sheet overleveraged, debt in China amounted to over US$100m, leverage issues exacerbated by the ongoing weakening of the A$ * Excludes Tianqi advances

For

per

sona

l use

onl

y

Slide 7 [xx] Galaxy Resources Limited (ASX:GXY)

-‐

40

80

120

160

2015 2020

Consumer electronics Auto Grid

-‐

100

200

300

400

2014 2020 2025

Frits and glass LubricaMng greases Other BaPeries

Growth In Lithium Demand AcceleraMng

Macro drivers are set to propel demand for lithium as energy storage demand rises and end-‐usage applica6ons grow § Strong growth in lithium bahery demand is expected to be driven by three major factors:

↑ ConMnued increase in demand for lithium bahery powered devices (consumer and portable electronics con1nuing to grow)

↑ Increase in demand for more advanced lithium baheries (higher energy storage capacity demanded with new devices)

↑ Growth in hybrid and electric vehicles, mass energy storage systems (lithium baReries a preferred technology)

§ Currently, almost 95% of baPeries used in electronic devices have adopted lithium-‐ion as the technology of choice

§ Growth in demand for lithium in China, as much of global baPery and materials producMon capacity is concentrated there

Lithium market driven by growth in baPery demand +285% (2014-‐2025)

Forecast Lithium Demand By Applica6on (Mt)

Source: signumBOX esMmates, CEMAC 2015

Lithium Bahery Demand By Applica6on (GWh)

7

Future demand driven by stable growth in consumer electronics and step funcMon growth in auto

For

per

sona

l use

onl

y

Slide 8 [xx] Galaxy Resources Limited (ASX:GXY)

Diverse Asset PorLolio

With a por^olio of both hard rock and brine based lithium assets, Galaxy is also well networked with key customers in the Asian lithium market

Mt Ca=lin, WA, Australia – hard rock

Sal de Vida, Salta & Catamarca, Argen:na – brine

James Bay, Quebec, Canada – hard rock

§ 100% owned § Lithium hard rock

development

§ 23Mt at 1.2% Li2O

§ Targe6ng to commence work on DFS in 2016

§ 100% owned § Lithium and potash brine

project

§ 1.1Mt LCE, 4.2Mt KCl

§ Completed DFS in 2013 § Lithium and tantalum hard

rock mining operaMons being recommissioned

§ 16Mt at 1.08% Li2O and 5.7Mlbs Ta2O5

§ Targe6ng produc6on at end Q1 2016

8

Lithium produc6on heavily concentrated in Asia

§ 88% of global capacity based in Asia

§ China produces >50% of global lithium cathodes

§ Galaxy is uniquely posi6oned to supply this market given management’s history with and network of customer contacts in the region

LiB Manufacturing Capacity (2015, MWh)

Source: CEMAC 2015

39,010

16,059

11,978

4,970

2,440

1,798

China

Korea

Japan

U.S.

Rest of World

EU For

per

sona

l use

onl

y

Slide 9 [xx] Galaxy Resources Limited (ASX:GXY)

Mt CaPlin – Overview

A significant lithium and tantalum ore reserve with near-‐term spodumene produc6on expected at a 6me of increasingly robust global demand

§ Mt CaPlin is a spodumene (lithium concentrate) and tantalum mining operaMon, located in Ravensthorpe, Western Australia

§ Placed on care and maintenance from 2012, with 118kt spodumene concentrate produced historically

§ Lithium concentrate is a preferred feedstock for lithium chemical producers in China

§ Finalized deal with General Mining (ASX: GMM) in September 2015 enMtling them to a 50% earn-‐in for A$25m

ü Deal allows Galaxy to restart producMon into a lithium market with strong demand

ü Restart capital mainly borne by GMM

ü Will generate near-‐term cash flow upon producMon restart awer Q1 2016

§ Earn-‐in structured as A$7m in upfront CAPEX contribuMons and annual cash payments to Galaxy of A$6m over 3 years

Key Project Informa6on1 Resource category Tonnes Li2O % Ta2O5 ppm

Measured 2,540,000 1.20 152

Probable 9,534,000 1.06 170

Inferred 4,343,000 1.07 132

Total 16,416,000 1.08 157

Mine life 17 years at 800kt p.a.

Processing design capacity 137,000tpa of ~6% lithium concentrate

9

Mt Ca=lin Opera:ons

1. Source: General Mining Announcement (2015.08.04) – Galaxy understands that all material assumpMons underpinning the producMon target and financial informaMon set out in the General Mining announcement released conMnue to apply and have not materially changed

For

per

sona

l use

onl

y

Slide 10 [xx] Galaxy Resources Limited (ASX:GXY)

Mt CaPlin – Project Economics

Progressing towards first produc6on at the end of Q1 2016, project will be coming on line in a strong pricing environment

10

§ Lithium economics have significantly improved since Mt CaPlin was last producing in 2012

― In 2012: spodumene pricing was circa US$300/t and US$/A$ exchange rate was US$1.00+/A$

― In 2015: spodumene pricing is US$445/t and US$/A$ exchange rate is c. US$0.70/A$

§ Spodumene prices now 50% higher and the Australian dollar is 30% lower, resulMng in viable and strong economics suppor6ng the restart of produc6on at Mt Cahlin

― Low exchange rate makes spodumene pricing especially favourable in A$ terms

― Overall cost of mining operaMons also reduced now as part of industry trend in recent years

― Combined with rising demand for lithium, all resulMng in aPracMve economics for Mt CaPlin

Entech Independent Review Economic Parameters1 Item Outcome

Life of mine and throughput rate 17 years at 800ktpa

LOM revenue A$1,164m

Total operaMng costs A$576m

Total operaMng costs (per tonne) A$47.8/t

LOM net cash flow A$526m

Net cash flow 2017-‐2019 (first 3 years full producMon) A$120m

Internal rate of return 230%

NPV at 8% discount rate, AUD/USD at 0.75 A$247.5m

1. Source: General Mining Announcement (2015.10.12) – Galaxy understands that all material assumpMons underpinning the producMon target and financial informaMon set out in the General Mining announcement released conMnue to apply and have not materially changed

Change In Economics vs Care & Maintenance Period

For

per

sona

l use

onl

y

Slide 11 [xx] Galaxy Resources Limited (ASX:GXY)

Mt CaPlin – Restart Of ProducMon

11

Spodumene ooake confirmed with Mitsubishi, produc6on targeted for restart at the end of Q1 2016

October 2015: Signed sales and distribuMon agreement for lithium concentrate with Mitsubishi Corp

Lithium Ooake

CAPEX For Restart

Tantalum Ooake

Restart Of Produc6on

Accelerated Ramp-‐Up

By December 2015: General Mining contribuMon of A$7m for capital expenditure

Being Finalized: Signing of sales and distribuMon agreement for tantalum concentrate

End Of Q1 2016: Restart of producMon expected, post compleMon of plant refurbishment

Post Q1 2016: Accelerated ramp-‐up period post restart of producMon

Mt Ca=lin Mining Opera:ons

§ Mt CaPlin is expected to restart producMon with an accelerated ramp-‐up period

§ Significant volume material in tailings dam and ROM pads ― Processing will be able to commence before

mining is restarted

For

per

sona

l use

onl

y

Slide 12 [xx] Galaxy Resources Limited (ASX:GXY)

Sal De Vida – Overview

One of the world’s largest and highest quality undeveloped brine deposits with significant expansion poten6al

§ A premier lithium and potash brine development project ― 100% owned by Galaxy ― Located between Salta and Catamarca Province in ArgenMna,

in an area known as the ‘Lithium Triangle’ § The Lithium Triangle is home to more than 60% of the world’s

annual produc6on of lithium ― Sal de Vida is located on the same salar as FMC Lithium’s

Fenix operaMons

§ Brine projects have the advantages of lower operaMonal costs and greater ability to expand producMon faciliMes

§ DefiniMve Feasibility Study completed in 2013, assumed lithium carbonate price of US$5,500/t ― Current lithium carbonate prices up to $12,800/t

§ Discussions underway for poten6al strategic JV partners at the project level

Key Project Informa6on

Reserve category

Time period

Tonnes Li total mass

Tonnes equivalent Li2CO3

Tonnes K total mass

Tonnes equivalent

KCl

Proven 1 – 6 34,000 181,000 332,000 633,000

Probable 7 – 40 180,000 958,000 1,869,000 3,564,000

Total 40 years 214,000 1,139,000 2,201,000 4,197,000

Source: Proven & Probable Reserve Statement – April 2013. Assumes 500mg/L Li cut off

12

Sal De Vida Brine

For

per

sona

l use

onl

y

Slide 13 [xx] Galaxy Resources Limited (ASX:GXY)

§ Calculated NPV based on an assumed lithium carbonate price of US$5,500/t

― Most recent volume contract pricing for lithium carbonate in China now up to $12,800/t net

Sal De Vida – Project Economics

The DFS provided compelling ra6onale for Sal de Vida which has further strengthened with higher lithium prices

Item Outcome

Lithium Carbonate ProducMon 25,000tpa

Potash ProducMon 95,000tpa

Mine Life > 40 years

Capital Costs US$369m

OperaMng Costs (Net Of Potash Credits) US$2,200/t LC

Average Annual Revenues US$160m

Average Annual Net Cash Flows (Pre Interest & Tax)2 US$118m

Net Present Value (Post-‐Tax) @ 10% Discount Rate US$380m

Internal Rate Of Return (Post-‐Tax) 19%

Net present value (post tax) at AUD/USD of 1.03, as at April 2013 A$369m

Net present value (post tax) at AUD/USD of 0.70, as at November 2015 A$543m

Notes: 1. Released 2013.04.12 2. Based on lithium carbonate pricing of US$5,500/t

13

Defini6ve Feasibility Study (April 2013)1

For

per

sona

l use

onl

y

Slide 14 [xx] Galaxy Resources Limited (ASX:GXY)

Sal De Vida – CompeMMve Advantages

14

Development at Sal de Vida will be assisted by its substan6al natural advantages of its strategic loca6on § Sal de Vida has several natural advantages arising from its loca6on in the

‘Lithium Triangle’ of Argen6na

ü ‘Lithium Triangle’ accounts for more than 60% of the world’s annual producMon of lithium

ü Sal de Vida comprises an area of 385km2 on the eastern half of the Salar De Hombre Muerto – the western half owned by global producer FMC

ü Property is readily accessible from the city of Salta via an all-‐seasons road

ü Galaxy benefits from FMC’s development in the region

― Close proximity to infrastructure, access to deep sea port and trained labour, as well as supporMve local government

§ Significant development progress already achieved

ü Environmental approvals granted and new Fenix gas pipeline now operaMonal

ü Fully permiPed through to construcMon

§ Track record of successful lithium project development and produc6on

ü Contributes valuable customer relaMonships from an established base of 40+ clients and product markeMng experience

ü Experience and know-‐how of making high quality product that meets stringent industry specificaMons for baPery grade

For

per

sona

l use

onl

y

Slide 15 [xx] Galaxy Resources Limited (ASX:GXY)

Sal De Vida – World Class Chemistry

One of the highest quality lithium brine developments globally, as demonstrated by its leading brine chemistry

15

Sal De Vida Project A Project B

Resource 7.2Mt LCE (lithium carbonate) 28.8Mt KCl (potassium chloride)

6.4Mt LCE 19.9Mt KCl

11.8Mt LCE 35.3Mt KCl

Reserve 1.1Mt LCE 4.2Mt KCl

Reserve not disclosed 2.7Mt LCE 8.0Mt KCl

Grade/Chemistry 810mg/l Li 9,100mg/l K 11.2 K/Li ra6o 12.1 SO4/Li ra6o 2.4 Mg/Li ra6o

774mg/l Li 6,227mg/l K 8.0 K/Li ra6o 24.4 SO4/Li ra6o 2.6 Mg/Li ra6o

666mg/l Li 5,401mg/l K 8.1 K/Li ra6o 28.5 SO4/Li ra6o 2.4 Mg/Li ra6o

Capacity 25ktpa LC 95ktpa KCl

16.4ktpa LC 10-‐20ktpa KCl

20ktpa LC 40ktpa KCl

Capex US$369.0m US$206.7m US$313.8m

Capital intensity US$14,760/t US$12,603/t US$15,688/t

Well fields 20 wells – southwest field 30 wells – eastern well field

Not stated 21 wells – iniMal phase 23 wells – phase 2

Tenements Owned No other operaMons

Owned Mixed with Project B properMes

Owned Mixed with lease from Project A

Jurisdic6on Catamarca/Salta Jujuy Jujuy

§ High lithium (Li) content to facilitate large scale producMon

§ High potassium (K) yields significant potash credits, reducing operaMng costs

§ Low magnesium (Mg), a low Mg/Li raMo reduces costs and yields higher quality, impuriMes are detrimental to being able to achieve grade spec

For

per

sona

l use

onl

y

Slide 16 [xx] Galaxy Resources Limited (ASX:GXY)

James Bay – Overview

The project provides a valuable op6on for capitalising on long term lithium demand growth, poten6al future supply to North American markets

§ Lithium pegmaMte project located in James Bay, Quebec Province, Canada

― Strategically located in a mining friendly jurisdicMon with a low cost of energy and good infrastructure

§ Galaxy owns 100% of James Bay, recently entered into an agreement with GMM, who have an opMon to earn 50% interest for US$5m in development funding over a 3 years

§ Agreement requires 50% of funds to be deployed in first 2 years

§ The project is currently at pre-‐DFS stage ― Will take advantage of Mt CaPlin experience to fast track

DFS process

§ Total indicated and inferred resources are 22.2Mt at 1.28% Li2O

§ Valuable opMon to be a future supplier into the rapidly growing North American market

16

James Bay earth-‐moving equipment

Field work at James Bay

For

per

sona

l use

onl

y

Slide 17 [xx] Galaxy Resources Limited (ASX:GXY)

Sal de Vida § Discussions are underway for potenMal strategic partners at the project level

§ Established relaMonships with 40+ clients, including leading baPery material producers in China, Japan and Korea

§ Opportunity to take advantage of those relaMonships for Sal de Vida ooake discussions

§ Management have extensive experience in the sector having produced and marketed lithium carbonate previously

Mt Cahlin

§ Previous relaMonship with Mitsubishi through Jiangsu OperaMons

§ Sales & DistribuMon Agreement signed by GMM in October 2015 with Mitsubishi for 100% of lithium concentrate

§ Galaxy has produced and sold lithium carbonate previously which passed qualificaMon to meet the high quality specificaMon of baPery material producers

Key Customer RelaMonships

Galaxy has a proven history in the lithium market with strong customer rela6onships in the leading bahery manufacturing regions (China, Korea, Japan)

17

§ Customers are looking to Galaxy for future supply given our history of being able to produce at high quality to meet specifica6on and the excellent brine chemistry at Sal de Vida

For

per

sona

l use

onl

y

Slide 18 [xx] Galaxy Resources Limited (ASX:GXY)

The China Market For Lithium

Significant 6ghtening of available supply of lithium carbonate – con6nued rapid growth in demand from bahery and energy storage segments § China conMnues policy push in renewable energy – expansion of generaMon capacity, electrificaMon of transportaMon etc.

— Record breaking year of new energy (xEV) vehicle sales, over 379k units sold ~ projected at 500k+ units for 2016 § Over 70% of LCE producMon in China is reliant on spodumene supply from Talison, limited availability of feedstock from domesMc

producMon and imports from South America

— Market guidance in early Q4 of 2015 that spodumene pricing will be liwed at least 20% from previous ~US$450/t

— Tianqi and Albemarle (co-‐owners of Talison) have expressed that no spodumene will be made available for third parMes, essenMally creaMng a supply monopoly in China

— Lithium converters in China eagerly seeking alternate supply of spodumene from Mt CaPlin, strong potenMal to command premium pricing in light of recent price increases in lithium carbonate

20,000

30,000

40,000

50,000

60,000

70,000

Jan.08 Jan.09 Jan.10 Jan.11 Jan.12 Jan.13 Jan.14 Jan.15

Lithium Carbonate Price Comparison (RMB/t) Lithium Carbonate China (RMB/t)

Source: Asian Metals, IRESS, CJ SecuriMes, Company EsMmates (* Based on recent market aucMon of 4kt of LiOH – 2016.01.12)

18

100,000 …

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2015 Start Pricing Big 3 Contract Pricing

China Volume Contract Pricing *

China Off Contract Pricing

Gross Pricing/t

Net Pricing/t

US$6.5K US$6.1K

US$12.8K

US$18.2K

For

per

sona

l use

onl

y

Slide 19 [xx] Galaxy Resources Limited (ASX:GXY)

Share Price Catalysts

Mul6ple catalysts should support a sustained market re-‐ra6ng

MT CATTLIN Restar1ng produc1on

§ New capital refurbishments to be completed by end of 2015, with producMon expected to restart at end Q1 2016

§ Concentrate pricing adjustments taking into account China market

CORPORATE Financial strength

§ Financial restructuring that has taken over 2 years is now complete, with the balance sheet strengthened, sePlement of its outstanding converMble bonds and compleMon of a new 3-‐year debt financing

19

§ Favourable economics and acceleraMng demand growth for lithium § Significant Mghtening of supply side, both in lithium carbonate and

concentrate feedstock, entering into period of significant price increase

MACRO Robust lithium demand

SAL DE VIDA Con1nued progress

§ Development conMnues to progress, new Fenix gas pipeline now operaMonal and the Environmental Impact DeclaraMon approved

§ Recent elecMons in ArgenMna pave way for posiMve change § Review of DFS economics in light of market and macro policy changes

For

per

sona

l use

onl

y

Slide 20 [xx] Galaxy Resources Limited (ASX:GXY)

APPENDIX

20

Lithium Market Background

For

per

sona

l use

onl

y

Slide 21 [xx] Galaxy Resources Limited (ASX:GXY)

Lithium 101

Lithium is the world’s lightest metal element with the highest electrochemical poten6al – lithium bahery now a technology of choice

§ Lithium is a small, sou silver-‐grey metal, the 3rd element in the periodic table

— Highest specific heat capacity among solids

— Highest electrochemical potenMal of all metals

— Low atomic mass and low density

§ Lithium can be mined as a hark rock mineral (pegma6te) or extracted from brine (salar)

§ Preferred material for use in energy storage baheries compared to tradiMonal lead acid or nickel based baPeries

ü Superior energy density ü Lighter, more compact and portable

ü More efficient

ü Longer life cycle ü More environmentally friendly

§ Lithium is an emerging “green mineral”

— ProducMon from brine is based on solar evaporaMon

— High recyclability of lithium baPery products

— Key material for the booming energy storage industry

Hard rock lithium mineral

BaPeries Frits and glass LubricaMng greases Metallurgy Air condiMoning Polimers Medicine Others

Lithium Demand By Applica6on (2014)

Source: signumBOX esMmates

21

For

per

sona

l use

onl

y

Slide 22 [xx] Galaxy Resources Limited (ASX:GXY)

Lithium Pricing

Lithium has been one of the strongest performing commodi6es over the last 12 months – due to surging global demand for the lithium-‐ion bahery § Lithium carbonate is not exchange traded, pricing determined bilaterally between producer and purchaser

— Contract price can be either on a RMB/t or US$/t basis

— Most contracts are over fixed annual volumes which provide certainty of demand for producers

§ Market conMnuing to guide significant annual price increases

— August 2015: YTD increase for China spot price of 20% — September 2015: FMC announces price increase of 15% across almost all of lithium products, effecMve October 2015

— … 41%

(3%)

(22%) (25%) (33%) (36%)

Lithium Carbonate (99% China)

Gold Copper Zinc Nickel Iron ore (62% fines China) 20,000

30,000

40,000

50,000

60,000

70,000

Jan.08 Jan.09 Jan.10 Jan.11 Jan.12 Jan.13 Jan.14 Jan.15

US$ Commodity Price Performance (LTM) Lithium Carbonate 99% China (RMB/t)

Source: Asian Metals, IRESS

22

For

per

sona

l use

onl

y

Slide 23 [xx] Galaxy Resources Limited (ASX:GXY)

Potash & Tantalum Overview

Galaxy’s projects will also produce potash and tantalum – two commodi6es with posi6ve demand mechanics and limited supply op6ons POTASH § Sal de Vida is expected to produce 95ktpa potash for 40+ years

§ Potash refers to a variety of potassium bearing minerals that are primarily used to produce ferMliser

— EssenMal to the world’s food supply with no subsMtutes — South America is a growing ferMliser demand centre

§ Demand for potash is driven by global populaMon growth and the reducMon in arable land

ü Increasing food demand requires higher yielding crops

ü Higher yielding crops require more ferMliser

23

TANTALUM § Mt CaPlin will produce tantalum alongside spodumene from

its reserves which have grades of 149ppm Ta2O5

§ Tantalum is a rare, hard, dark grey metal

— Very high natural corrosion resistance — Significant tantalum supply from Africa

§ Tantalum is primarily used in the manufacture of capacitors for electronic equipment

ü High capacitance for a small amount of metal

ü Superior alloying qualiMes

2014 Tantalum Ore Produc6on (t)1 Arable Land (ha/capita)

600

200

98

85

60

60

40

14

Rwanda

Congo

Brazil

Mozambique

Nigeria

China

Ethiopia

Burundi

Source: US Geological Survey Note: 1 Excludes producMon of tantalum contained in Mn slags

-‐

0.2

0.4

0.6

0.8

1960 1980 2000 2020 2040

Popula6on Growth (bn)

-‐

3

6

9

12

1960 1980 2000 2020 2040

Source: United NaMons, FAO

For

per

sona

l use

onl

y

Slide 24 [xx] Galaxy Resources Limited (ASX:GXY)

Gigafactories Need New Supply

Growing demand is crea6ng new opportuni6es for emerging lithium producers, with Galaxy at the forefront of the next wave of suppliers

24

§ Tesla set to generate 35GWh of lithium-‐ion baPery producMon per year § Other major manufacturing faciliMes also coming online

2016-‐2017: Tesla’s Gigafactory expected to be operaMonal

§ Albermarle (NYSE:ALB) awer acquiring Rockwood, as yet to announce start of producMon at La Negra, already delayed for 2 years from when first announced under Rockwood Lithium

§ FMC (NYSE:FMC) currently experiencing constrained producMon, reported revenue decline due to lowered third party supply

§ Orocobre (ASX:ORE) encountering further delays in the ramp-‐up of producMon at the Olaroz Project

2015: Increasing demand creates new opportuniMes for growing lithium companies as current producers lack expansion capacity

§ Taiwan’s Aleees, Sony and Siemens partner to develop a pure electric bus in September

§ BMW launch second home charging staMon for electric and plug-‐in hybrid vehicles

2014: Large companies invest heavily in lithium-‐ion baPeries

§ LG Chem (7GWh), Foxconn (15GWh), BYD (20GWh) and Boston Power (10GWh) have all announced lithium-‐ion baPery factories

§ Combined with Tesla, the factories are expected to triple current lithium-‐ion baPery producMon capacity by 20201

2020: MulMple lithium-‐ion baPery megafactories expected to be online

Source: 1. Benchmark Mineral Intelligence

For

per

sona

l use

onl

y

Slide 25 [xx] Galaxy Resources Limited (ASX:GXY)

Disclaimer

This document contains forward looking statements concerning the projects owned by Galaxy. Statements concerning mining reserves and resources may also be deemed to be forward looking statements in that they involve esMmates based on specific assumpMons. Forward-‐looking statements are not statements of historical fact and actual events and results may differ materially from those described in the forward looking statements as a result of a variety of risks, uncertainMes and other factors. Forward-‐looking statements are inherently subject to business, economic, compeMMve, poliMcal and social uncertainMes and conMngencies. Many factors could cause the Company’s actual results to differ materially from those expressed or implied in any forward-‐looking informaMon provided by the Company, or on behalf of, the Company. Such factors include, among other things, risks relaMng to addiMonal funding requirements, metal prices, exploraMon, development and operaMng risks, compeMMon, producMon risks, regulatory restricMons, including environmental regulaMon and liability and potenMal Mtle disputes. Forward looking statements in this document are based on Galaxy’s beliefs, opinions and esMmates of Galaxy as of the dates the forward looking statements are made, and no obligaMon is assumed to update forward looking statements if these beliefs, opinions and esMmates should change or to reflect other future developments. There can be no assurance that Galaxy’s plans for development of its mineral properMes will proceed as currently expected. There can also be no assurance that Galaxy will be able to confirm the presence of addiMonal mineral deposits, that any mineralizaMon will prove to be economic or that a mine will successfully be developed on any of Galaxy’s mineral properMes. Circumstances or management’s esMmates or opinions could change. The reader is cauMoned not to place undue reliance on forward-‐looking statements. Data and amounts shown in this document relaMng to capital costs, operaMng costs, potenMal or esMmated cashflow and project Mmelines are internally generated best esMmates only. All such informaMon and data is currently under review as part of Galaxy’s ongoing operaMonal, development and feasibility studies. Accordingly, Galaxy makes no representaMon as to the accuracy and/or completeness of the figures or data included in the document. Not For Release in US This presentaMon does not consMtute an offer of securiMes for sale in any jurisdicMon, including the United States. Any securiMes described in this presentaMon may not be offered or sold in the United States absent registraMon or an exempMon from registraMon under the United States SecuriMes Act of 1933, as amended, following the preparaMon of required documents and compleMon of required processes to permit such offer or sale.

CONTACT INFORMATION Level 1/16 Ord Street West Perth, Western Australia 6005 PO Box 1136, West Perth WA 6872 T: +61 8 9215 1700 F: +61 8 9215 1799 E: [email protected]

25

For

per

sona

l use

onl

y

Slide 26 [xx] Galaxy Resources Limited (ASX:GXY)

Competent & Qualified Persons’ Statement

Sal de Vida Competent Persons The informaMon in this report that relates to Mineral Resources for the Sal de Vida lithium project is based on work completed by Mr. Michael Rosko, who is a Member of the Society of Mining, Metallurgy and ExploraMon Inc a Recognised Overseas Professional OrganisaMon. Mr. Rosko is a full Mme employee of E. L. Montgomery and Associates and has sufficient experience which is relevant to the style of mineralisaMon and type of deposit under consideraMon and to the acMvity which he is undertaking to qualify as a Competent Person as defined in the 2004 EdiMon of the ‘Australasian Code for ReporMng of ExploraMon Results, Mineral Resources and Ore Reserves’. Mr. Rosko consents to the inclusion in this report of the maPers based on his informaMon in the form and context in which it appears. This informaMon was prepared and first disclosed under the JORC Code 2004 it has not been updated since to comply with JORC code 2012 on the basis that the informaMon has not materially changed since it was last reported. Na6onal Instrument 43-‐101 -‐ Qualified Person The mineral resources for the Sal de Vida lithium project are reported in accordance with NaMonal Instrument 43-‐101 and have been esMmated in conformity with generally accepted CIM “EsMmaMon of Mineral Resource and Mineral Reserves Best PracMces” guidelines. Resource evaluaMon work was completed by Mr. Michael Rosko, P.Geo (Arizona 25065, Texas 6359, California 5236) an independent Qualified Person as defined by NI 43-‐101. Mr. Rosko has read and approved the content of this news release. A Technical Report compliant with NI 43-‐101 standards describing the resource esMmaMon was filed on SEDAR within 45 days of its release. James Bay Competent Person The informaMon in this report that relates to Mineral Resources for the James Bay project is based on work completed by Mr. SébasMen Bernier, who is a Member of a Recognised Overseas Professional OrganisaMon. Mr Bernier is a full Mme employee of SRK ConsulMng (Canada) Inc. and has sufficient experience which is relevant to the style of mineralisaMon and type of deposit under consideraMon and to the acMvity which he is undertaking to qualify as a Competent Person as defined in the 2004 EdiMon of the ‘Australasian Code for ReporMng of ExploraMon Results, Mineral Resources and Ore Reserves’. Mr Bernier consents to the inclusion in this report of the maPers based on his informaMon in the form and context in which it appears. This informaMon was prepared and first disclosed under the JORC Code 2004 it has not been updated since to comply with JORC code 2012 on the basis that the informaMon has not materially changed since it was last reported. Na6onal Instrument 43-‐101 -‐ Qualified Person The mineral resources for the James Bay project are reported in accordance with NaMonal Instrument 43-‐101 and have been esMmated in conformity with generally accepted CIM “EsMmaMon of Mineral Resource and Mineral Reserves Best PracMces” guidelines. Resource evaluaMon work was completed by Mr. SébasMen Bernier, P.Geo (OGQ#1034, APGO#1847) an independent Qualified Person as defined by NI 43-‐101. Mr. Bernier has read and approved the content of this news release. A Technical Report compliant with NI 43-‐101 standards describing the resource esMmaMon was filed on SEDAR within 45 days of its release.

26

For

per

sona

l use

onl

y