25

For Producer Use Only 1 Updates and Opportunities for 2009 January 2009 Webinar

| Date post: | 21-Dec-2015 |

| Category: |

Documents |

| View: | 214 times |

| Download: | 0 times |

For Producer Use Only1

Updates and Opportunitiesfor 2009

January 2009 Webinar

For Producer Use Only2

The Advanced Underwriting Team

Lawrence J. Owens, JD, CLU, ChFC, MBA, FLMILarry has worked as an Estate Tax Attorney for the IRS, counsel for a pension consulting firm and as an advanced sales attorney for an Indianapolis-based life insurance company. Larry is also a writer, and speaker, and has taught college classes and published numerous articles on business insurance, pensions and estate planning.

Michael Sharry, JDMike is an estate planning attorney in Dallas, Texas. He has been in the estate planning and life insurance advanced sales business since 1979.

Linas Sudzius, JD, CLU, ChFCLinas worked for a Chicago-based insurance company as their Director of Advanced Sales and most recently as their Chief Marketing Officer. He now manages an active estate planning law practice in Franklin, Tennessee. Linas also co-authors the publication Think About It with Steve Leimberg.

For Producer Use Only3

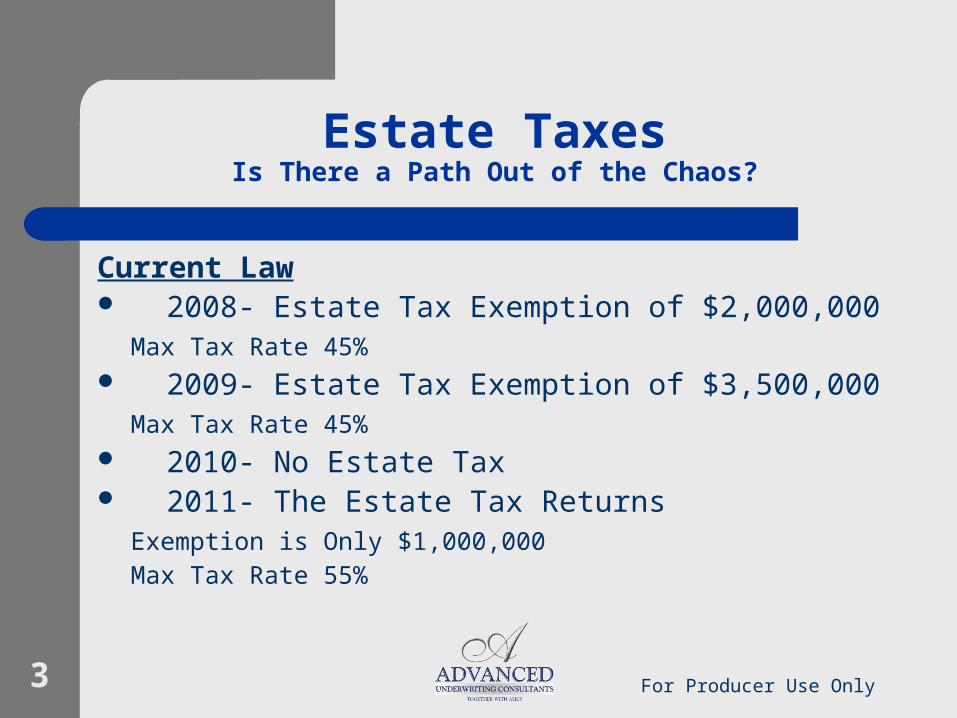

Estate TaxesIs There a Path Out of the Chaos?

Current Law 2008- Estate Tax Exemption of $2,000,000

Max Tax Rate 45% 2009- Estate Tax Exemption of $3,500,000

Max Tax Rate 45% 2010- No Estate Tax 2011- The Estate Tax Returns

Exemption is Only $1,000,000Max Tax Rate 55%

For Producer Use Only4

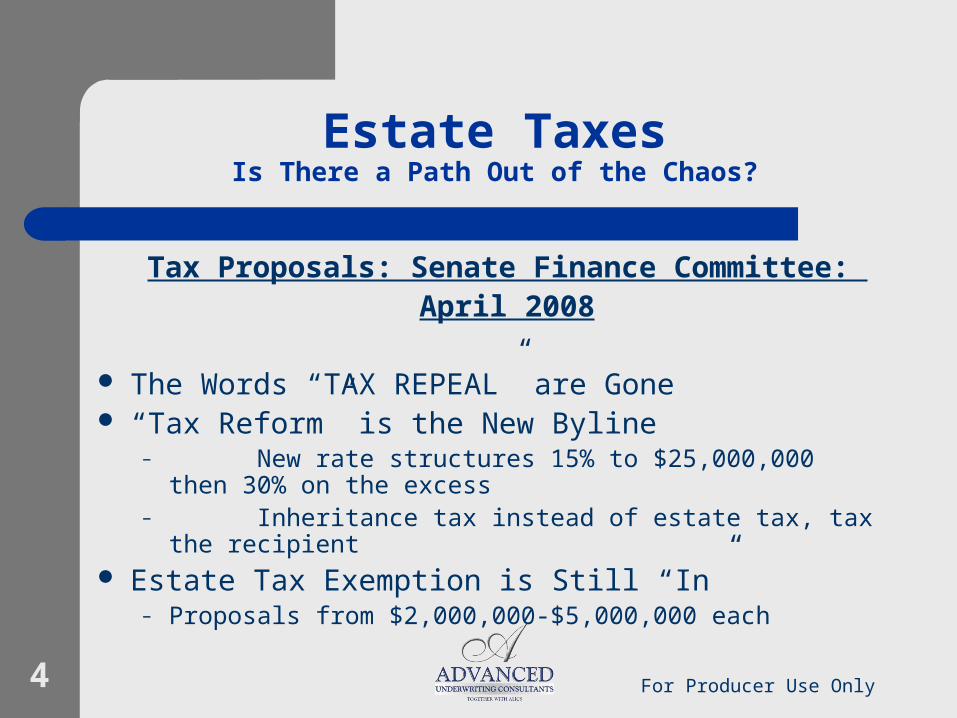

Estate TaxesIs There a Path Out of the Chaos?

Tax Proposals: Senate Finance Committee: April 2008

The Words “TAX REPEAL” are Gone “Tax Reform” is the New Byline

– New rate structures 15% to $25,000,000 then 30% on the excess

– Inheritance tax instead of estate tax, tax the recipient Estate Tax Exemption is Still “In”

– Proposals from $2,000,000-$5,000,000 each

For Producer Use Only5

Estate TaxesIs There a Path Out of the Chaos?

Portability of Exemption is “In”– If you don’t use it you don’t lose it– Hurts Charitable giving

Unification of the Estate Tax and Gift Tax Exemption is “In”

– Would permit the earlier transfer of property– And greater tax on subsequent sale

No Federal Estate Tax Deduction for State Death Taxes Paid is “In”

– Boost to Revenues

For Producer Use Only6

Estate TaxesIs There a Path Out of the Chaos?

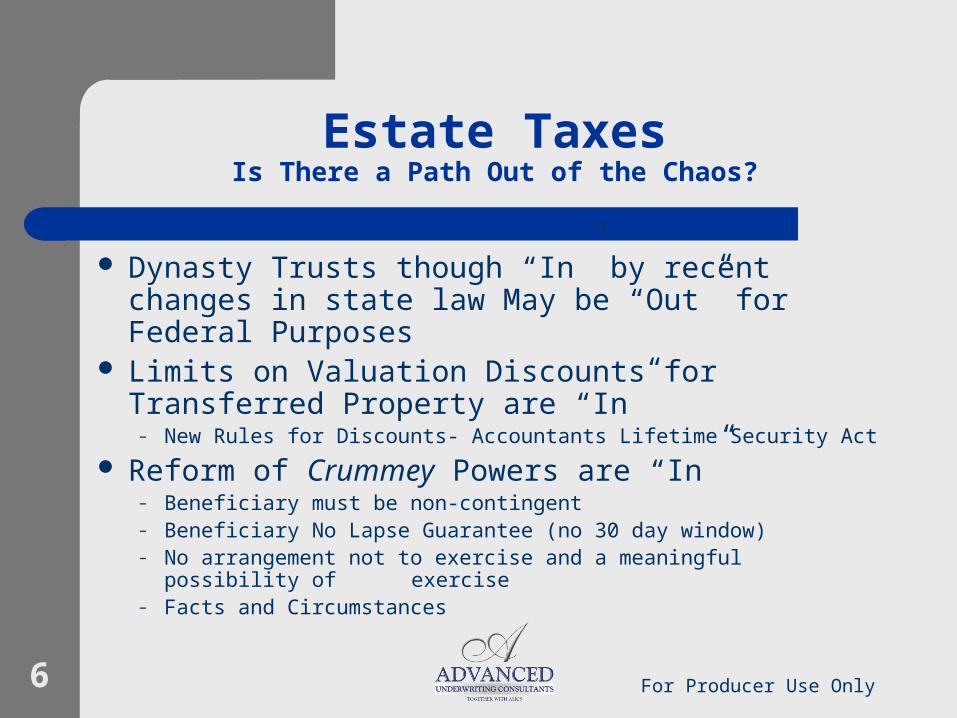

Dynasty Trusts though “In” by recent changes in state law May be “Out” for Federal Purposes

Limits on Valuation Discounts for Transferred Property are “In”

– New Rules for Discounts- Accountants Lifetime Security Act

Reform of Crummey Powers are “In”– Beneficiary must be non-contingent– Beneficiary No Lapse Guarantee (no 30 day window)– No arrangement not to exercise and a meaningful possibility of

exercise– Facts and Circumstances

For Producer Use Only7

Estate TaxesIs There a Path Out of the Chaos?

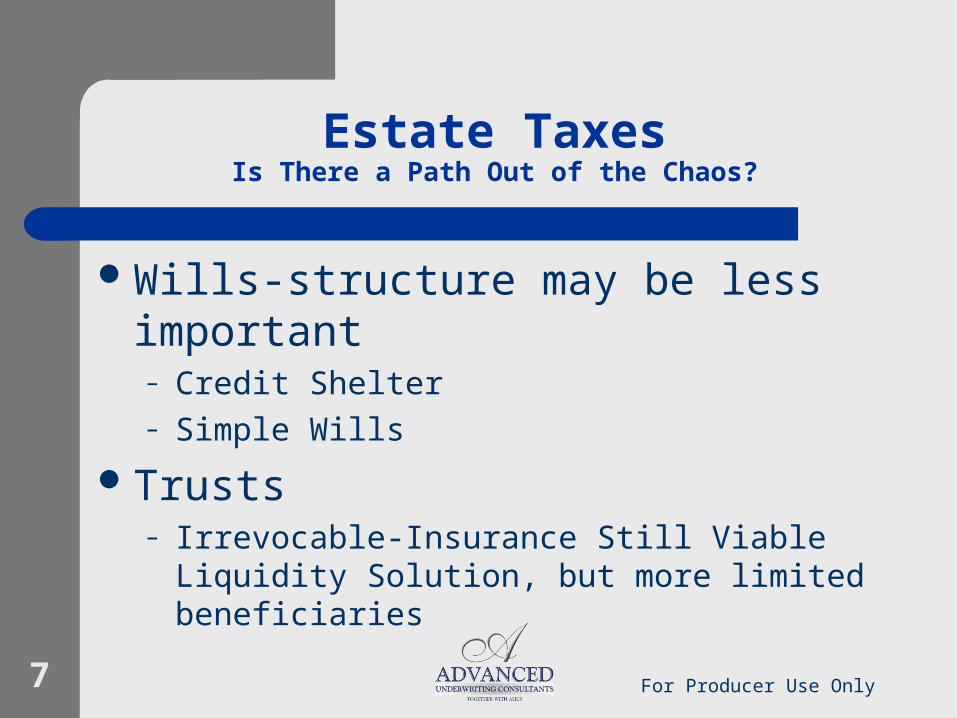

Wills-structure may be less important – Credit Shelter – Simple Wills

Trusts– Irrevocable-Insurance Still Viable Liquidity

Solution, but more limited beneficiaries

For Producer Use Only8

Estate TaxesIs There a Path Out of the Chaos?

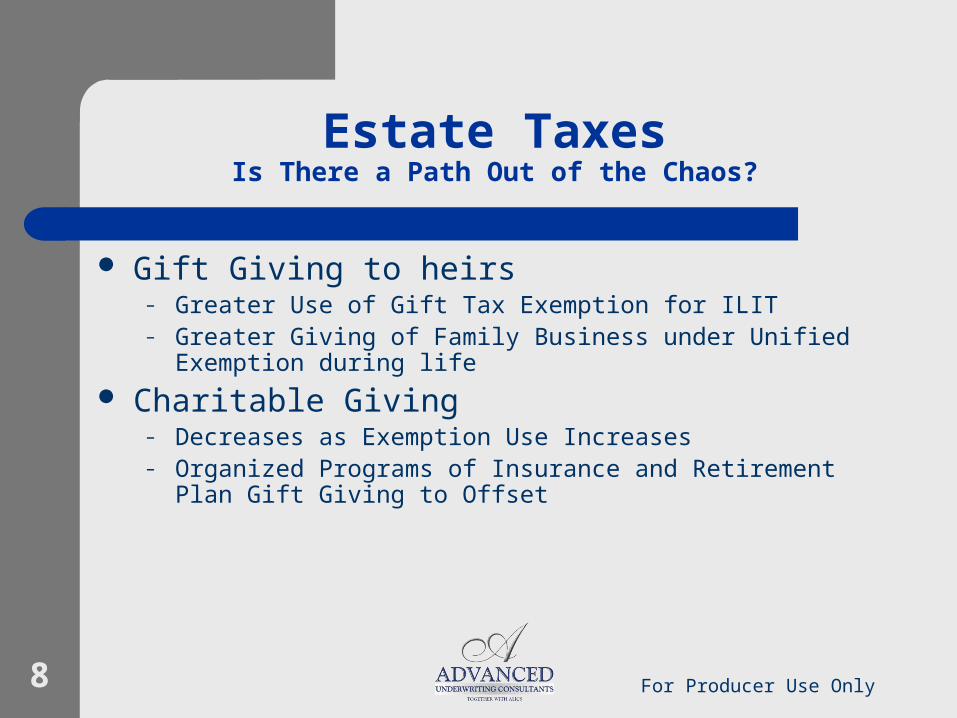

Gift Giving to heirs– Greater Use of Gift Tax Exemption for ILIT– Greater Giving of Family Business under Unified Exemption during

life

Charitable Giving– Decreases as Exemption Use Increases– Organized Programs of Insurance and Retirement Plan Gift Giving

to Offset

For Producer Use Only9

Estate TaxesIs There a Path Out of the Chaos?

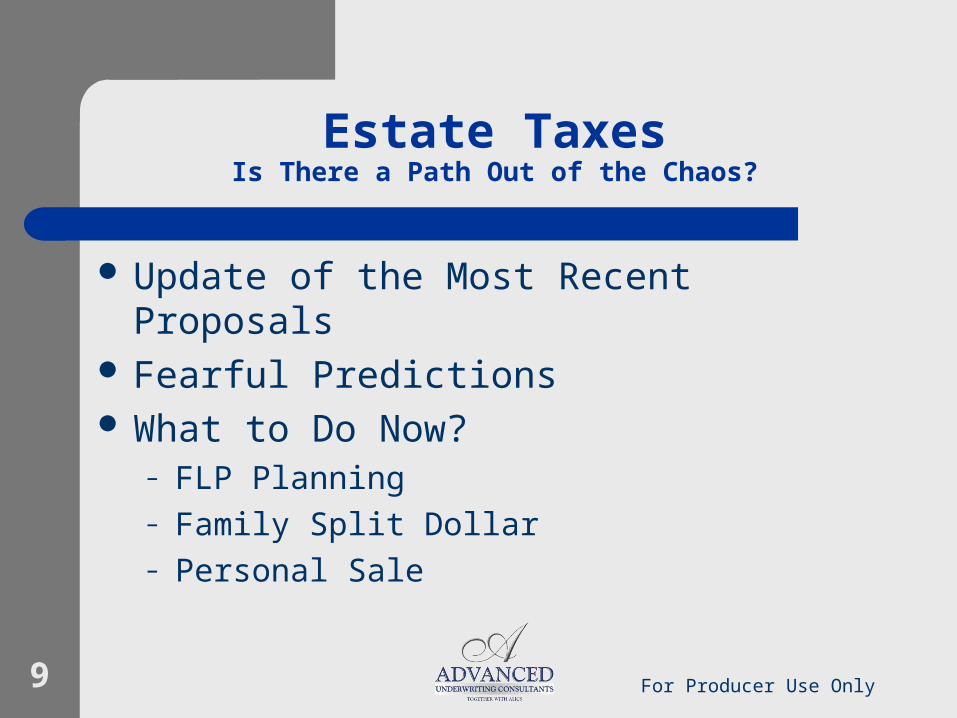

Update of the Most Recent Proposals Fearful Predictions What to Do Now?

– FLP Planning– Family Split Dollar– Personal Sale

For Producer Use Only10

Key Ideas for 2009

Business Owners– Offer a 409 A Review

Provisions are Still Little Understood Potentially Apply to Deferred Compensation Plans Penalties for Failure to Comply Are Severe We Can Help

For Producer Use Only11

Key Ideas for 2009

Business Owners– Offer a COLI Review

Section 101(j) Creates New Compliance Issues Failure to Comply Creates Unexpected Income Taxation

of Life Insurance Bring Form 8925 for the CPA Review All Life Policies for Compliance While You’re At It…

For Producer Use Only12

SEC Proposed Rule 151A

Dated June 25, 2008 According to the SEC

“We are proposing a new rule that would define the terms “annuity contract” and “optional annuity contract” under the Securities Act of 1933. The proposed rule is intended to clarify the status under the federal securities laws of indexed annuities, under which payments to the purchaser are

dependent on the performance of a securities index.”

For Producer Use Only13

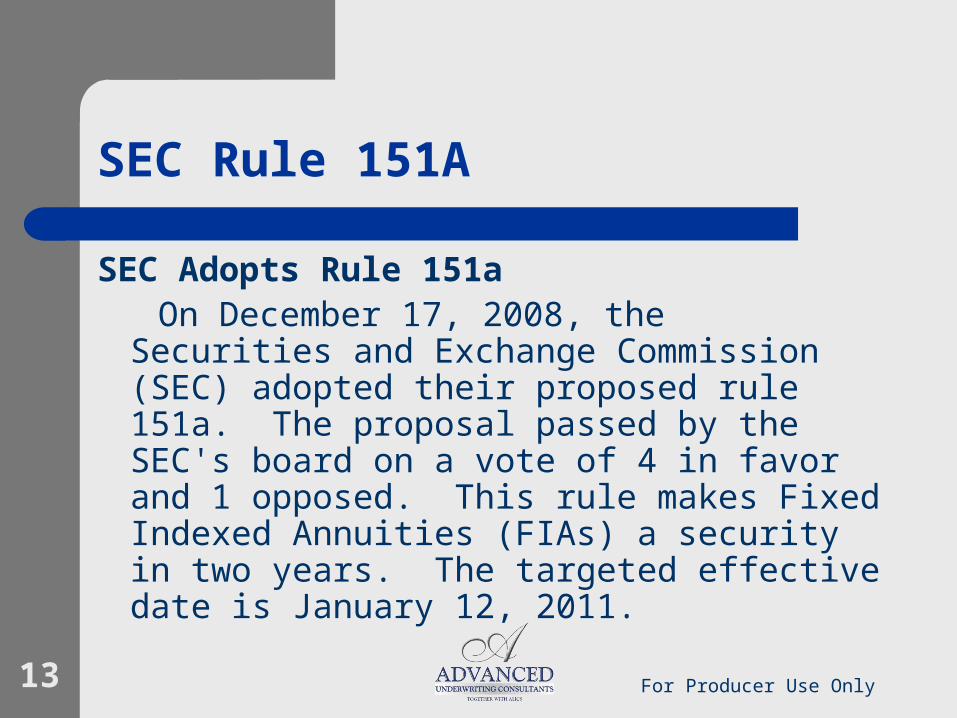

SEC Rule 151A

SEC Adopts Rule 151a On December 17, 2008, the Securities and

Exchange Commission (SEC) adopted their proposed rule 151a. The proposal passed by the SEC's board on a vote of 4 in favor and 1 opposed. This rule makes Fixed Indexed Annuities (FIAs) a security in two years. The targeted effective date is January 12, 2011.

For Producer Use Only14

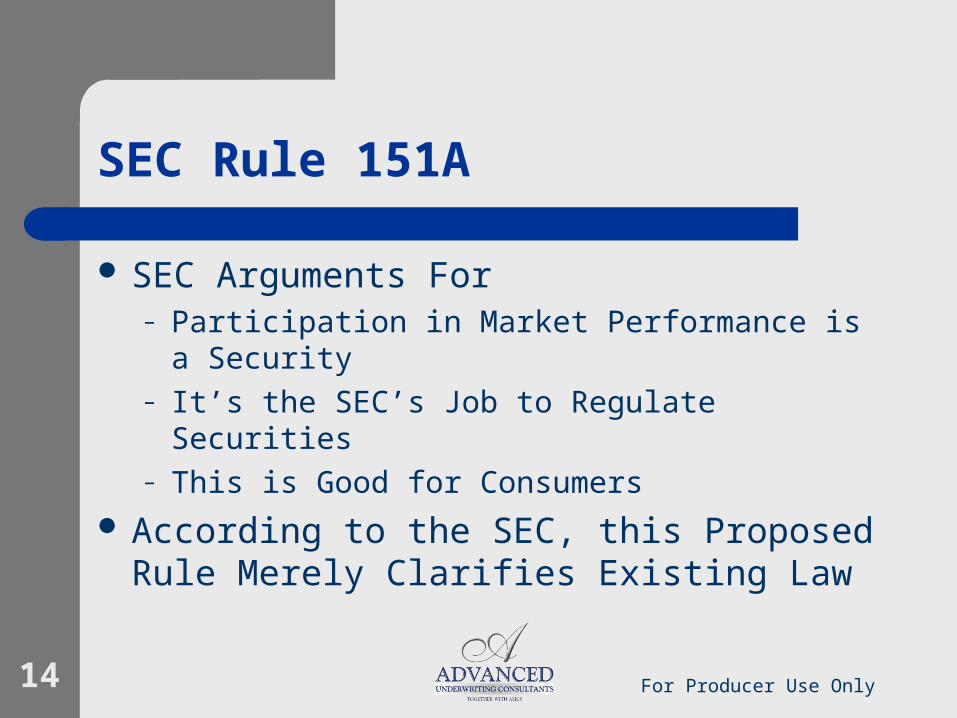

SEC Rule 151A

SEC Arguments For– Participation in Market Performance is a Security– It’s the SEC’s Job to Regulate Securities– This is Good for Consumers

According to the SEC, this Proposed Rule Merely Clarifies Existing Law

For Producer Use Only15

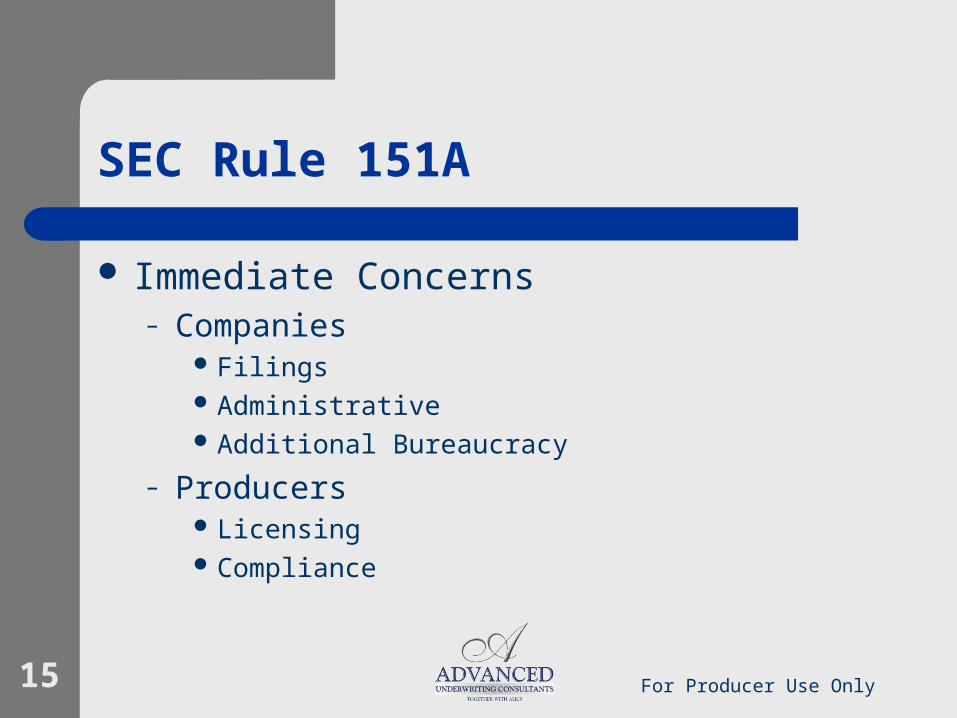

SEC Rule 151A

Immediate Concerns– Companies

Filings Administrative Additional Bureaucracy

– Producers Licensing Compliance

For Producer Use Only16

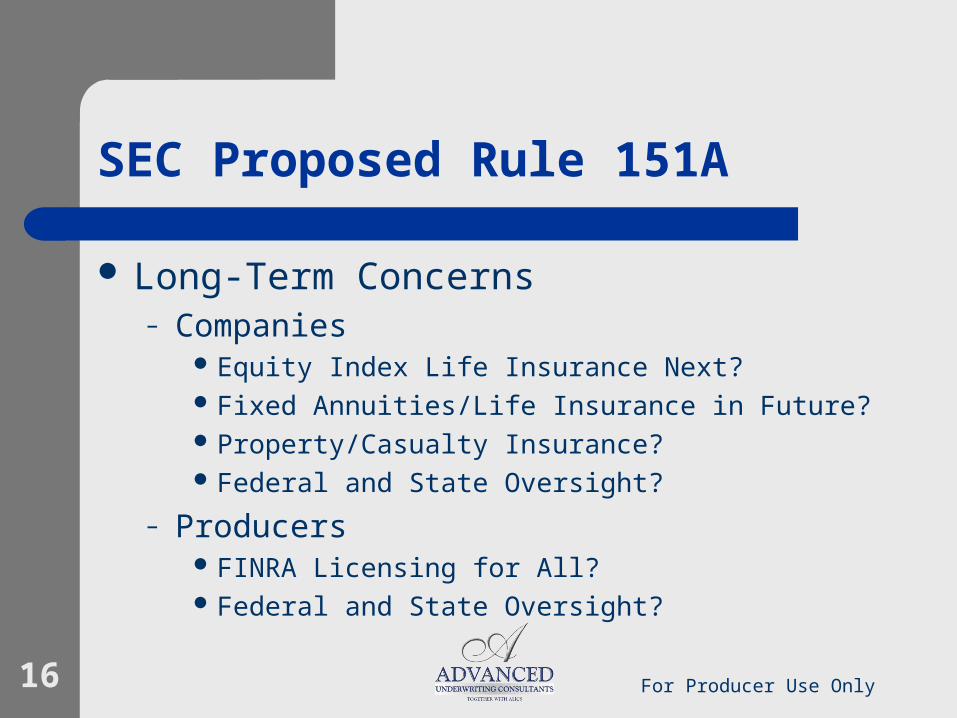

SEC Proposed Rule 151A

Long-Term Concerns– Companies

Equity Index Life Insurance Next? Fixed Annuities/Life Insurance in Future? Property/Casualty Insurance? Federal and State Oversight?

– Producers FINRA Licensing for All? Federal and State Oversight?

For Producer Use Only17

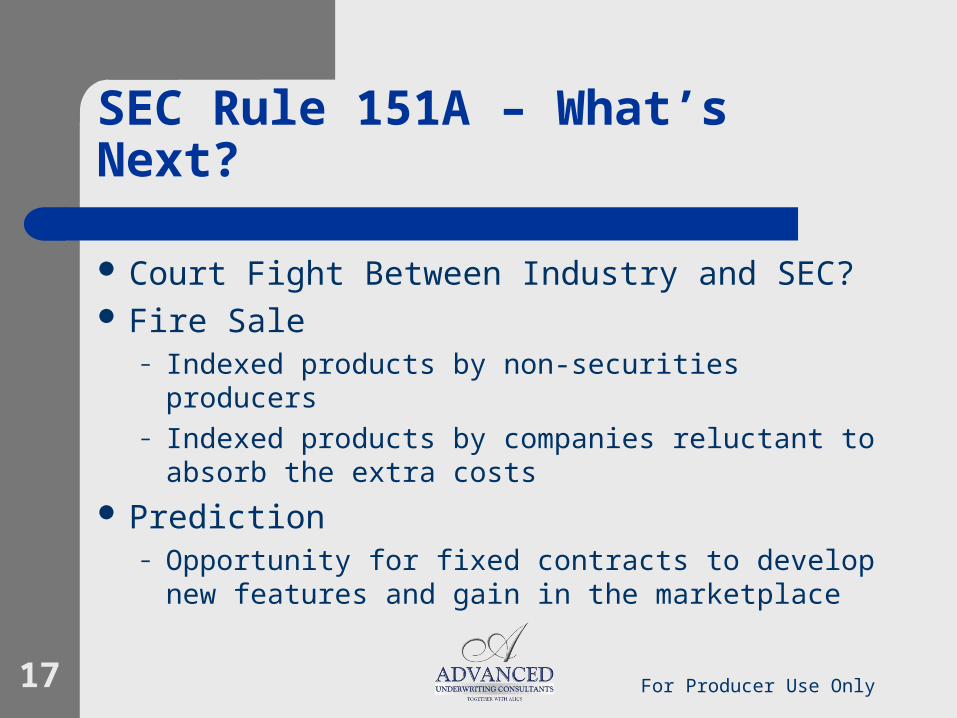

SEC Rule 151A – What’s Next?

Court Fight Between Industry and SEC? Fire Sale

– Indexed products by non-securities producers– Indexed products by companies reluctant to

absorb the extra costs

Prediction– Opportunity for fixed contracts to develop new

features and gain in the marketplace

For Producer Use Only18

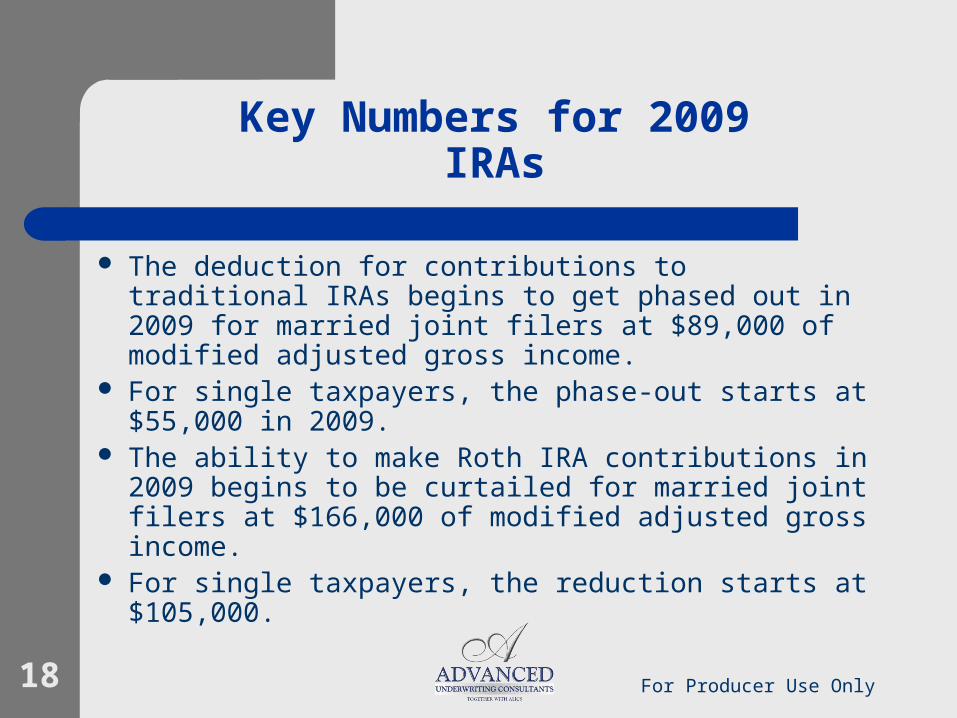

Key Numbers for 2009IRAs

The deduction for contributions to traditional IRAs begins to get phased out in 2009 for married joint filers at $89,000 of modified adjusted gross income.

For single taxpayers, the phase-out starts at $55,000 in 2009.

The ability to make Roth IRA contributions in 2009 begins to be curtailed for married joint filers at $166,000 of modified adjusted gross income.

For single taxpayers, the reduction starts at $105,000.

For Producer Use Only19

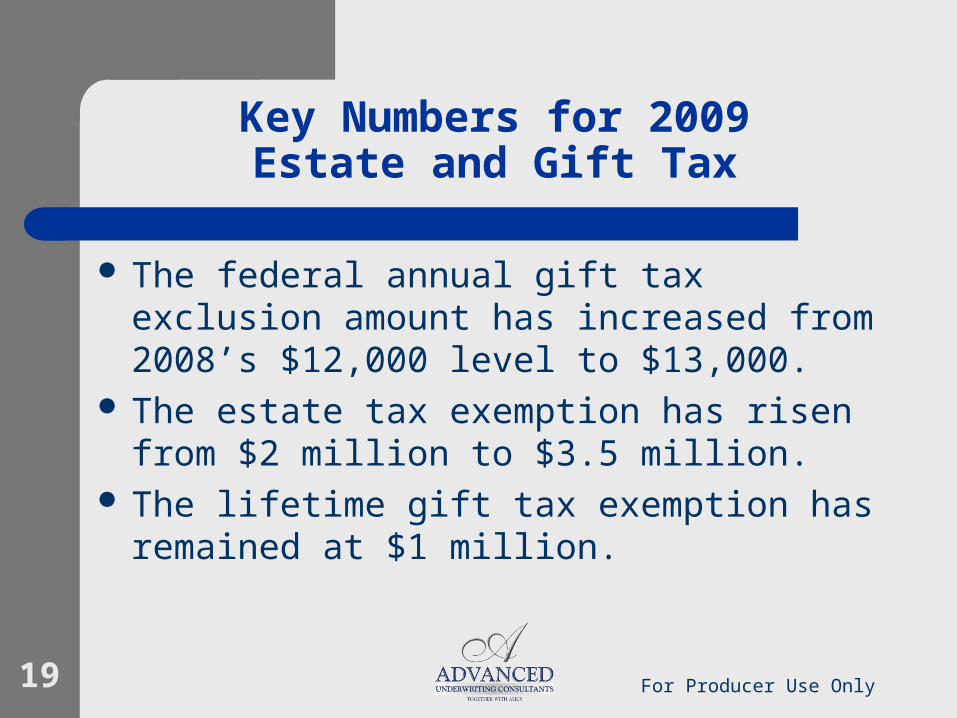

Key Numbers for 2009Estate and Gift Tax

The federal annual gift tax exclusion amount has increased from 2008’s $12,000 level to $13,000.

The estate tax exemption has risen from $2 million to $3.5 million.

The lifetime gift tax exemption has remained at $1 million.

For Producer Use Only20

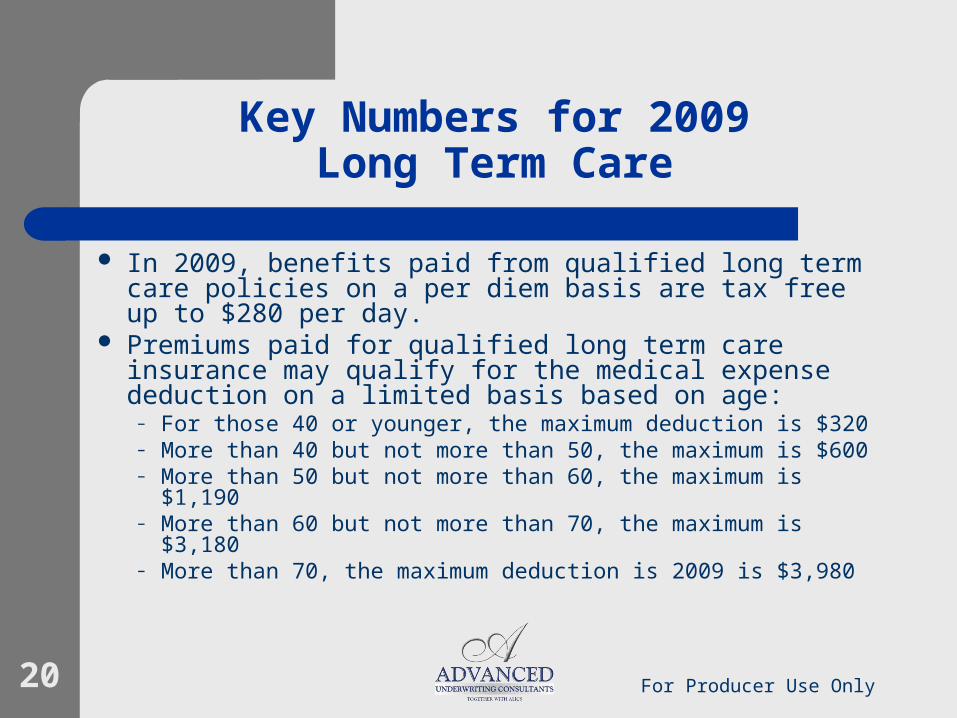

Key Numbers for 2009Long Term Care

In 2009, benefits paid from qualified long term care policies on a per diem basis are tax free up to $280 per day.

Premiums paid for qualified long term care insurance may qualify for the medical expense deduction on a limited basis based on age:

– For those 40 or younger, the maximum deduction is $320– More than 40 but not more than 50, the maximum is $600– More than 50 but not more than 60, the maximum is $1,190– More than 60 but not more than 70, the maximum is $3,180– More than 70, the maximum deduction is 2009 is $3,980

For Producer Use Only21

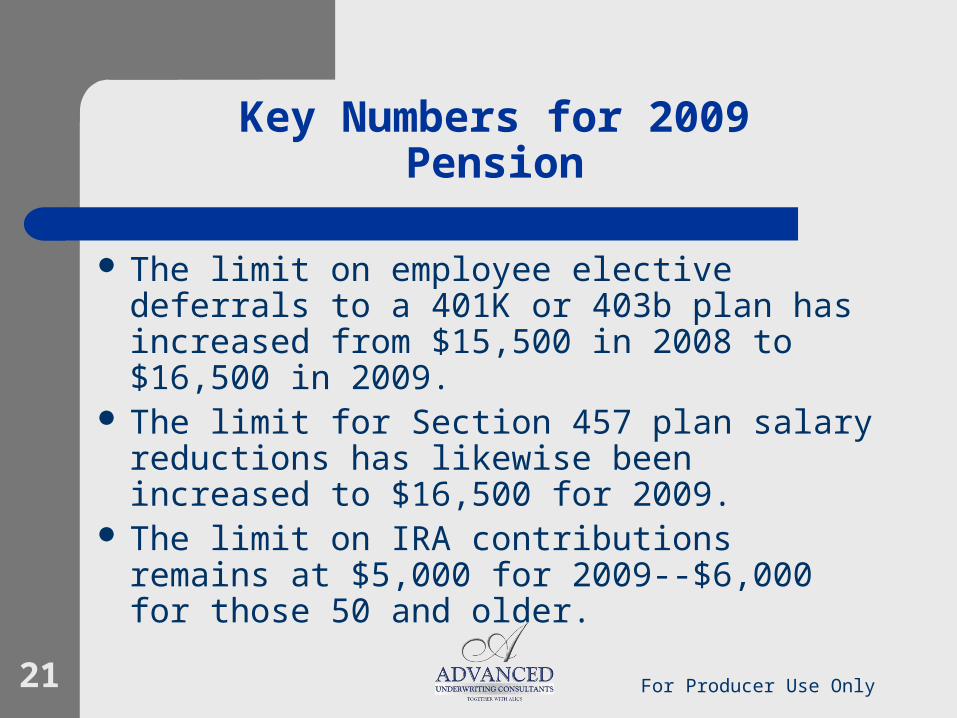

Key Numbers for 2009Pension

The limit on employee elective deferrals to a 401K or 403b plan has increased from $15,500 in 2008 to $16,500 in 2009.

The limit for Section 457 plan salary reductions has likewise been increased to $16,500 for 2009.

The limit on IRA contributions remains at $5,000 for 2009--$6,000 for those 50 and older.

For Producer Use Only22

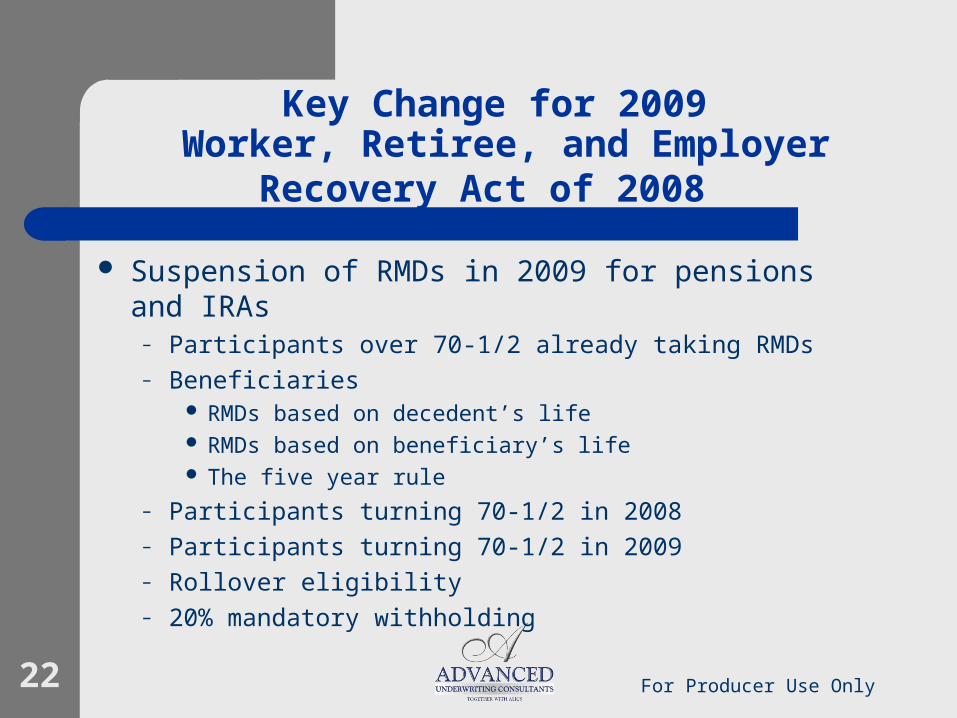

Key Change for 2009 Worker, Retiree, and Employer Recovery

Act of 2008

Suspension of RMDs in 2009 for pensions and IRAs– Participants over 70-1/2 already taking RMDs– Beneficiaries

RMDs based on decedent’s life RMDs based on beneficiary’s life The five year rule

– Participants turning 70-1/2 in 2008– Participants turning 70-1/2 in 2009– Rollover eligibility– 20% mandatory withholding

For Producer Use Only23

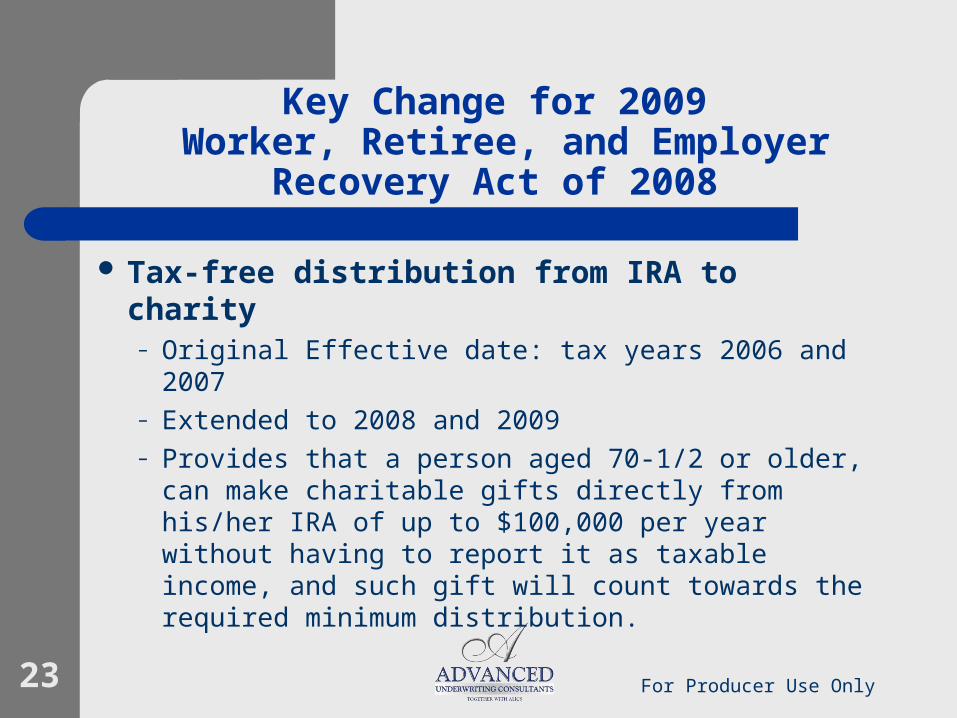

Key Change for 2009 Worker, Retiree, and Employer Recovery

Act of 2008

Tax-free distribution from IRA to charity– Original Effective date: tax years 2006 and 2007– Extended to 2008 and 2009– Provides that a person aged 70-1/2 or older, can

make charitable gifts directly from his/her IRA of up to $100,000 per year without having to report it as taxable income, and such gift will count towards the required minimum distribution.

For Producer Use Only24

Key Change for 2009 Worker, Retiree, and Employer Recovery

Act of 2008

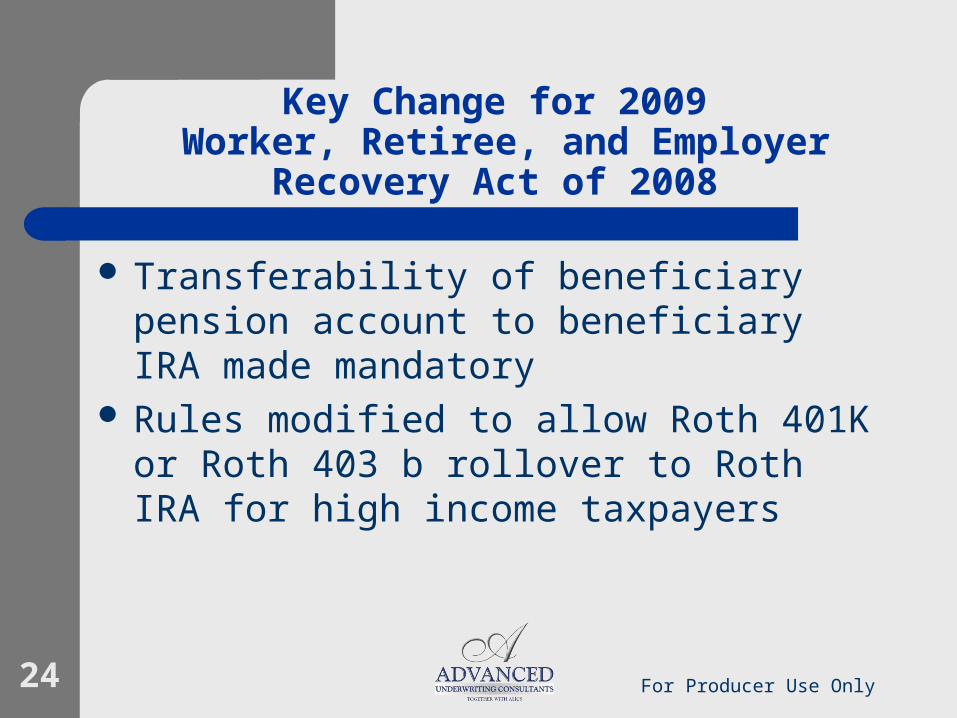

Transferability of beneficiary pension account to beneficiary IRA made mandatory

Rules modified to allow Roth 401K or Roth 403 b rollover to Roth IRA for high income taxpayers

For Producer Use Only25

About …

About ALICS

Advanced Life Insurance Consulting Services LLC (ALICS) provides customized advanced sales support to life insurance professionals. ALICS delivers the following services to customers:

• Telephone/email consultation• Proposal support• Sample documents• Point-of-sale assistance• Seminars• Monthly newsletter

ALICS delivers its services through a sophisticated nationwide network of life insurance-oriented attorneys, technology experts and accountants.

ALICS can be reached at 1-615-224-1291.