October 2010 For Your Benefit: Retirees DISCLAIMER: This communication describes benefits that become effective Jan. 1, 2011. This communication has been prepared for benefits-eligible retired career agents and General Agents of the Massachusetts Mutual Life Insurance Company (MassMutual) and benefits-eligible retired employees of MassMutual; The MassMutual Trust Company FSB; MML Investors Services, Inc.; MassMutual International LLC; Babson Capital Management LLC; Invicta Advisors LLC; and Cornerstone Real Estate Advisors LLC. It is not for active employees, agents or field staff. This represents a Summary of Material Modifications (SMM) for the MassMutual Employee Welfare Benefits Plan and the MassMutual Agents’ Welfare Benefits Plan. All information contained in this newsletter is for general information purposes only and is not tax or financial advice. Benefits are determined by the terms of the plans in effect. MassMutual reserves the right to modify, revoke, change, suspend or terminate any one or all plans, programs, policies, benefits or services described in this newsletter or the underlying plan documents at any time and from time to time, with or without notice. In the event of a discrepancy between descriptions in this newsletter and information in relevant benefit plan documents, the plan documents will govern. Provisions are based on current law and regulations, which are subject to change. Receipt of this material does not imply your eligibility for any one or all of the plans and programs described. All information described in this newsletter is current as of the October 2010 publication date and all references to time are Eastern Time (ET) unless specified otherwise. What’s Inside 2 | Your 2011 Annual Benefits Enrollment 3 | Medicare Primary Coverage 3 | How the Medical Options Work 5 | Prescription Drug Benefits 6 | Non-Medicare Primary Coverage 6 | How the Medical Options Work 9 | Prescription Drug Benefits 10 | New in 2011: Integrated Personal Health Team 10 | Health Savings Account 12 | Filling Your Prescriptions in 2011 14 | Retiree Assistance Program 14 | Life Insurance 14 | Dental 15 | Did You Know? 16 | Benefits Enrollment 17 | Contacts 18 | Appendices 18 | Preventive Care Chart – Appendix A 19 | Medicare Primary Participants: Medical Coverage Chart – Appendix B 23 | Non-Medicare Primary Participants: Medical Coverage Chart – Appendix C 27 | Notice of Creditable Coverage – Appendix D 29 | Medicaid & CHIP Notice – Appendix E 31 | Enrollment Instructions – Appendix F

Transcript

October 2010

For Your Benefit: Retirees

DISCLAIMER: This communication describes benefits that become effective Jan. 1, 2011. This communication has been prepared for benefits-eligible retired career agents and General Agents of the Massachusetts Mutual Life Insurance Company (MassMutual) and benefits-eligible retired employees of MassMutual; The MassMutual Trust Company fsb; MML Investors Services, Inc.; MassMutual International LLC; Babson Capital Management LLC; Invicta Advisors LLC; and Cornerstone Real Estate Advisors LLC. It is not for active employees, agents or field staff. This represents a Summary of Material Modifications (SMM) for the MassMutual Employee Welfare Benefits Plan and the MassMutual Agents’ Welfare Benefits Plan. All information contained in this newsletter is for general information purposes only and is not tax or financial advice. Benefits are determined by the terms of the plans in effect.

MassMutual reserves the right to modify, revoke, change, suspend or terminate any one or all plans, programs, policies, benefits or services described in this newsletter or the underlying plan documents at any time and from time to time, with or without notice. In the event of a discrepancy between descriptions in this newsletter and information in relevant benefit plan documents, the plan documents will govern. Provisions are based on current law and regulations, which are subject to change. Receipt of this material does not imply your eligibility for any one or all of the plans and programs described. All information described in this newsletter is current as of the October 2010 publication date and all references to time are Eastern Time (ET) unless specified otherwise.

3 | How the Medical Options Work 5 | Prescription Drug Benefits

6 | Non-Medicare Primary Coverage 6 | How the Medical Options Work 9 | Prescription Drug Benefits 10 | New in 2011: Integrated Personal Health Team 10 | Health Savings Account

12 | Filling Your Prescriptions in 2011 14 | Retiree Assistance Program 14 | Life Insurance 14 | Dental 15 | Did You Know? 16 | Benefits Enrollment 17 | Contacts 18 | Appendices

18 | Preventive Care Chart – Appendix A 19 | Medicare Primary Participants: Medical

Coverage Chart – Appendix B 23 | Non-Medicare Primary Participants: Medical

Coverage Chart – Appendix C 27 | Notice of Creditable Coverage – Appendix D 29 | Medicaid & CHIP Notice – Appendix E 31 | Enrollment Instructions – Appendix F

2

If you and any of your covered dependents do not have the same Medicare primary status, special rules apply. If you choose to cover your depen-dents, your medical election as the MassMutual retiree will dictate your spouse/eligible depen-dent’s option as follows:

• If Medicare is your primary coverage, but your covered spouse/domestic partner or dependent is not enrolled in Medicare, based on the medical option you select, your dependent(s) will automatically be enrolled in the corresponding non-Medicare primary option. For example, if you enroll in the Med 1300 (Option 1) Indemnity option, your spouse/domestic partner will be enrolled in the Med 1300 (Option 1) high deductible health plan.

• If Medicare is not your primary coverage, but your covered spouse/domestic partner or dependent has Medicare as primary coverage, based on the medical option you select, your dependent(s) will automatically be enrolled in the corresponding option that coordinates with Medicare as the primary payor. For example, if you enroll in the Med 1300 (Option 1) high deductible health plan, your Medicare spouse/domestic partner or dependent will be enrolled in the Med 1300 (Option 1) Indemnity option.

The 2011 annual benefits enrollment for retirees begins on Mon., Nov. 1 and ends on Tues., Nov. 30, 2010. This special issue of For Your Benefit describes what’s changing in 2011 and explains how to complete the enrollment process. Benefit changes vary depending on whether or not you are enrolled in Medicare:

Participants who are age 65 or older and/or disabled and enrolled in Medicare have Medicare as their primary coverage. Note: If you are not enrolled in Medicare, but are eligible for it, the MassMutual plan will calculate the benefit it pays assuming Medicare is in place and is your primary coverage. The information on the green pages explains your 2011 health care coverage options (see pages 3-5 and 19-22). There is also information on page 12 about filling your prescriptions in 2011. (You can disregard the information on the orange pages, which describes non-Medicare primary coverage.)

Participants who are not eligible for Medicare (generally, those under age 65) have MassMutual medical coverage as their primary coverage. The information on the orange pages explains your 2011 coverage options (see pages 6-11 and 23-26). There is also information on page 12 about filling your prescriptions in 2011. (You can disregard information on the green pages, which describes Medicare primary coverage.)

Whether you’re enrolled in Medicare or not, read the information on the maroon pages throughout this booklet (see pages 12-18 and 27-31).

Your 2011 Annual Benefits Enrollment

3

You have three medical options to choose from for your 2011 MassMutual medical coverage:

• Med 500 Indemnity

• Med 1300 Indemnity (previously Med 1500) – shown as “Option 1” on your enrollment worksheet

• Med 2500 Indemnity – shown as “Option 2” on your enrollment worksheet

All three medical options cover a broad range of medical services including preventive and sick care, emergency services, inpatient and outpatient care and mental health services, administered by CIGNA. Prescription drug coverage is adminis-tered by Express Scripts.

How the Medical Options Work All three medical options work the same way. The key differences between the medical options are:

1 | the amounts of your monthly “premiums” (as shown on your enrollment worksheet),

2 | the annual deductibles (the amount you pay before paying just a percentage of the cost of eligible medical and prescription expenses) and

3 | the annual out-of-pocket maximums (the cap on how much you pay out-of-pocket each year: annual deductibles plus coinsurance).

The deductibles and out-of-pocket maximums are included in the tables on pages 4 and 5. You’ll want to consider these factors as you decide which option is best for you.

With Medicare Primary coverage, regardless of the medical option you select, you can receive care from any licensed medical provider. When you receive care, you and the MassMutual plan share in the cost of eligible medical expenses. Here’s how:

• Eligible preventive care is covered at 100% with no medical annual deductible or coinsurance. The plan covers the services in full. You pay $0 for eligible preventive care services.1 For certain prescription medications classified as preventive, the annual prescription drug deductible does not apply; you’ll pay only coinsurance. See Appendix A on page 18 for a list of eligible preventive care and page 22 for a list of preventive drugs.

• You must meet the annual medical deductible.2

• Once you meet the annual medical deductible, you pay 20% of the cost of eligible medical care (coinsurance).

• To limit your financial risk, there is an annual medical out-of-pocket maximum.3

1 Any amount that is over the Reasonable and Customary (R&C) allowance (as determined by CIGNA) is not covered by the plan and does not go toward the deductible or out-of-pocket maximum; it is your financial responsibility. R&C is the normal charge made by a provider for a similar service or supply that does not exceed the charge by most providers in a given geographic region. R&C applies to services covered under the MassMutual medical options for any services not covered by Medicare. Any services covered by Medicare are subject to the Medicare allowable charge.

2 If you cover yourself and any one or more dependents (under Med 500 Indemnity, Med 1300 Indemnity or Med 2500 Indemnity), you pay the individual deductible for each participant’s eligible expenses, and then the plan begins paying a percentage of charges for that individual. (For example, if you’ve met your individual annual deductible, but your spouse hasn’t met his, you’d pay coinsurance for your eligible expenses. You’d continue to pay the full cost of your spouse’s eligible expenses until he reaches his annual individual deductible.) Once the family deductible dollar amount is reached, no further deductible applies. This is called a non-collective calendar year deductible.

3 The out-of-pocket maximum includes what you pay to meet the annual deductible and the amount you pay in coinsurance. It does not include amounts over the Reasonable and Customary (R&C) allowance.

Medicare Primary Coverage

4

Medicare Primary Coverage

• A separate deductible, coinsurance and out-of-pocket maximum applies to prescription drugs (see page 5). Once you meet the deductible, you’ll pay a percentage of eligible prescription drug costs up to per-prescription maximums until you reach the separate out-of-pocket maxi-mum that applies to prescription drugs. (Certain preventive prescription drugs are not subject to the deductible, see the list of preventive medica-tions on page 22 for more information.)

• For information about how the MassMutual plan coordinates with Medicare, refer to the Medicare Primary Participants: Medical Coverage Chart – Appendix B on page 19.

Your Share of Covered Medical Expenses(medical coverage administered by CIGNA)

Med 500 Indemnity

Med 1300 (Option 1)Indemnity

Med 2500 (Option 2)Indemnity

Preventive care Eligible preventive care is covered at 100%; annual deductible and coinsurance do not apply4

Annual medical deductible(how much you pay each year in medical costs before the plan begins paying a percentage)

$500 Individual$1,000 Family5

$1,300 Individual $2,600 Family5

$2,500 Individual $5,000 Family5

Coinsurance(the percentage of costs you pay after you pay your annual deductible)

20% after the deductible, and all amounts over the R&C allowance4

Annual medical out-of-pocket maximum6 (the most you could pay in a year for medical deductible and coinsurance amounts)

$3,000 Individual $5,000 Family

$3,000 Individual $5,000 Family

$4,500 Individual $9,000 Family

For more information, refer to Medicare Primary Participants: Medical Coverage Chart - Appendix B on page 19.4 Any amount that is over the Reasonable and Customary (R&C) allowance (as determined by CIGNA) is not covered by the plan and does not go toward the

deductible or out-of-pocket maximum; it is your financial responsibility. R&C is the normal charge made by a provider for a similar service or supply that does not exceed the charge by most providers in a given geographic region. R&C applies to services covered under the MassMutual medical options for any services not covered by Medicare. Any services covered by Medicare are subject to the Medicare allowable charge.

5 If you cover yourself and any one or more dependents (under Med 500 Indemnity, Med 1300 Indemnity or Med 2500 Indemnity), you pay the individual deductible for each participant’s eligible expenses, and then the plan begins paying a percentage of charges for that individual. (For example, if you’ve met your individual annual deductible, but your spouse hasn’t met his, you’d pay coinsurance for your eligible expenses. You’d continue to pay the full cost of your spouse’s eligible expenses until he reaches his annual individual deductible.) Once the family deductible dollar amount is reached, no further deductible applies. This is called a non-collective calendar year deductible.

6 The out-of-pocket maximum includes what you pay to meet the annual deductible and the amount you pay in coinsurance. It does not include amounts over the Reasonable and Customary (R&C) allowance.

5

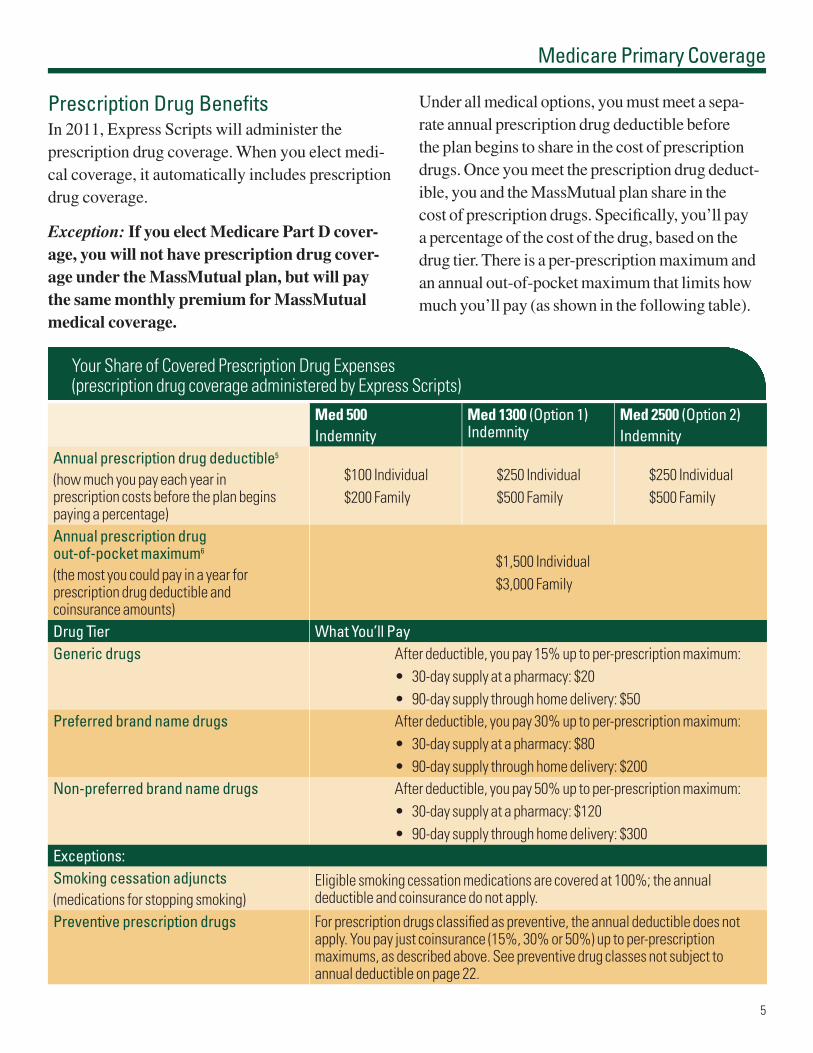

Prescription Drug BenefitsIn 2011, Express Scripts will administer the prescription drug coverage. When you elect medi-cal coverage, it automatically includes prescription drug coverage.

Exception: If you elect Medicare Part D cover-age, you will not have prescription drug cover-age under the MassMutual plan, but will pay the same monthly premium for MassMutual medical coverage.

Under all medical options, you must meet a sepa-rate annual prescription drug deductible before the plan begins to share in the cost of prescription drugs. Once you meet the prescription drug deduct-ible, you and the MassMutual plan share in the cost of prescription drugs. Specifically, you’ll pay a percentage of the cost of the drug, based on the drug tier. There is a per-prescription maximum and an annual out-of-pocket maximum that limits how much you’ll pay (as shown in the following table).

Your Share of Covered Prescription Drug Expenses (prescription drug coverage administered by Express Scripts)

Med 500Indemnity

Med 1300 (Option 1) Indemnity

Med 2500 (Option 2)Indemnity

Annual prescription drug deductible5

(how much you pay each year in prescription costs before the plan begins paying a percentage)

$100 Individual $200 Family

$250 Individual $500 Family

$250 Individual $500 Family

Annual prescription drug out-of-pocket maximum6

(the most you could pay in a year for prescription drug deductible and coinsurance amounts)

$1,500 Individual $3,000 Family

Drug Tier What You’ll PayGeneric drugs After deductible, you pay 15% up to per-prescription maximum:

• 30-day supply at a pharmacy: $20• 90-day supply through home delivery: $50

Preferred brand name drugs After deductible, you pay 30% up to per-prescription maximum: • 30-day supply at a pharmacy: $80• 90-day supply through home delivery: $200

Non-preferred brand name drugs After deductible, you pay 50% up to per-prescription maximum: • 30-day supply at a pharmacy: $120• 90-day supply through home delivery: $300

Exceptions:Smoking cessation adjuncts(medications for stopping smoking)

Eligible smoking cessation medications are covered at 100%; the annual deductible and coinsurance do not apply.

Preventive prescription drugs For prescription drugs classified as preventive, the annual deductible does not apply. You pay just coinsurance (15%, 30% or 50%) up to per-prescription maximums, as described above. See preventive drug classes not subject to annual deductible on page 22.

Medicare Primary Coverage

6

You have three medical options to choose from for your 2011 MassMutual medical coverage:

• Med 500 Preferred Provider Organization (PPO)

• Med 1300 High Deductible Health Plan (HDHP) – shown as “Option 1” on your enrollment worksheet

• Med 2500 HDHP – shown as “Option 2” on your enrollment worksheet

All three options cover a broad range of medical services including preventive and sick care, emer-gency services, inpatient and outpatient care and mental health services, administered by CIGNA. Prescription drug coverage is administered by Express Scripts.

How the Medical Options Work The key differences between the medical options are:

1 | the amounts of your monthly “premiums” (as shown on your enrollment worksheet),

2 | the annual deductible (the amount you pay before paying just a percentage of the cost of eligible medical and prescription expenses) and

3 | the annual out-of-pocket maximum (the cap on how much you pay out-of-pocket each year: annual deductible plus coinsurance).

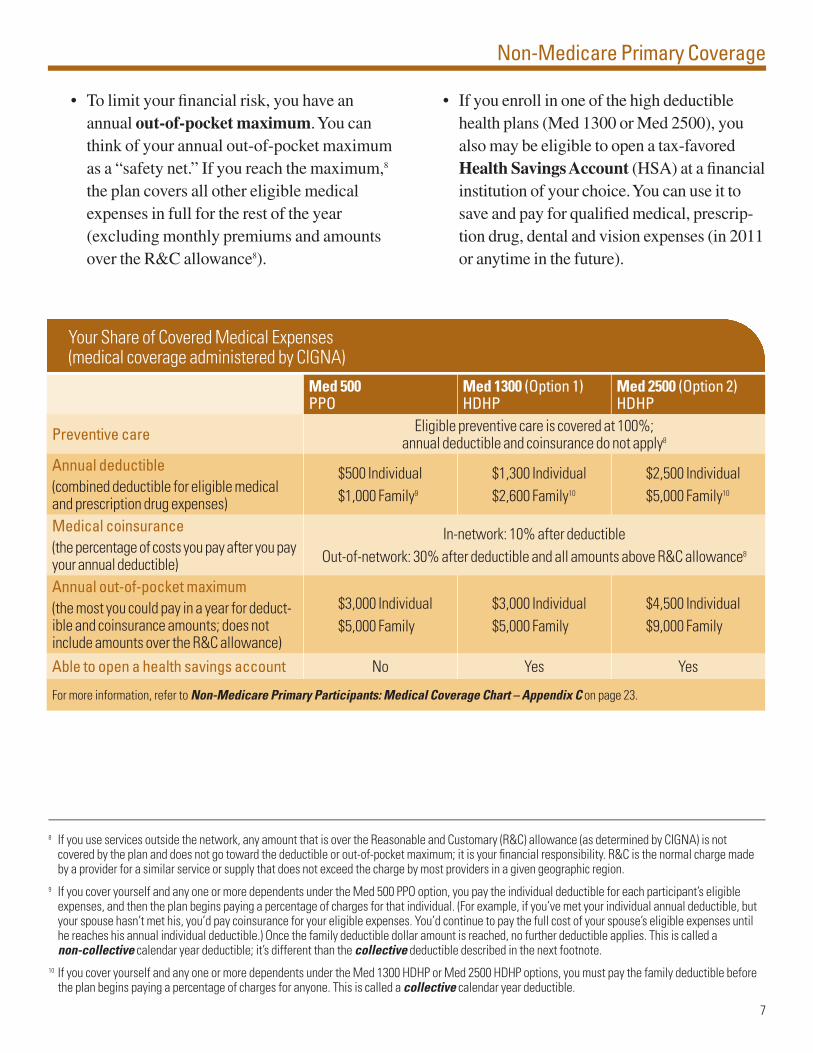

These amounts are included in the table on page 7 and on the Non-Medicare Primary Participants: Medical Coverage Chart – Appendix C on page 23. You’ll want to consider these factors as you decide which option is best for you.

Regardless of the medical option you select, you can receive care from any licensed medical provider. You’ll receive a higher level of benefits when you receive care from providers who are part of the CIGNA network. When you receive care, you and the MassMutual plan share in the cost of eligible medical expenses. Here’s how:

• Eligible preventive care is covered at 100% with no annual deductible or coinsurance. The plan covers the services in full. You pay $0 for eligible preventive care services.7 For certain prescription medications classified as preven-tive, the annual deductible does not apply; you’ll pay only coinsurance. See Appendix A on page 18 for a list of eligible preventive care and page 26 for a list of preventive drugs.

• For all other covered services, you’ll pay the full cost of eligible medical expenses until you reach your annual deductible. Both medical and non-preventive prescrip-tion drug expenses count toward your annual deductible.

• Once you meet your annual deductible, you and the plan share in the cost of eligible medical and prescription drug expenses. You’ll pay a percentage of the cost (called coinsurance) for covered medical services and prescription drugs, up to per-prescription maximums.

7 If you use services outside the network, any amount that is over the Reasonable and Customary (R&C) allowance (as determined by CIGNA) is not covered by the plan and does not go toward the deductible or out-of-pocket maximum; it is your financial responsibility. R&C is the normal charge made by a provider for a similar service or supply that does not exceed the charge by most providers in a given geographic region.

Non-Medicare Primary Coverage

7

Non-Medicare Primary Coverage

Your Share of Covered Medical Expenses(medical coverage administered by CIGNA)

Med 500 PPO

Med 1300 (Option 1)HDHP

Med 2500 (Option 2)HDHP

Preventive care Eligible preventive care is covered at 100%; annual deductible and coinsurance do not apply8

Annual deductible(combined deductible for eligible medical and prescription drug expenses)

$500 Individual $1,000 Family9

$1,300 Individual $2,600 Family10

$2,500 Individual $5,000 Family10

Medical coinsurance(the percentage of costs you pay after you pay your annual deductible)

In-network: 10% after deductibleOut-of-network: 30% after deductible and all amounts above R&C allowance8

Annual out-of-pocket maximum(the most you could pay in a year for deduct-ible and coinsurance amounts; does not include amounts over the R&C allowance)

$3,000 Individual $5,000 Family

$3,000 Individual $5,000 Family

$4,500 Individual $9,000 Family

Able to open a health savings account No Yes Yes

For more information, refer to Non-Medicare Primary Participants: Medical Coverage Chart – Appendix C on page 23.

• To limit your financial risk, you have an annual out-of-pocket maximum. You can think of your annual out-of-pocket maximum as a “safety net.” If you reach the maximum,8 the plan covers all other eligible medical expenses in full for the rest of the year (excluding monthly premiums and amounts over the R&C allowance8).

8 If you use services outside the network, any amount that is over the Reasonable and Customary (R&C) allowance (as determined by CIGNA) is not covered by the plan and does not go toward the deductible or out-of-pocket maximum; it is your financial responsibility. R&C is the normal charge made by a provider for a similar service or supply that does not exceed the charge by most providers in a given geographic region.

9 If you cover yourself and any one or more dependents under the Med 500 PPO option, you pay the individual deductible for each participant’s eligible expenses, and then the plan begins paying a percentage of charges for that individual. (For example, if you’ve met your individual annual deductible, but your spouse hasn’t met his, you’d pay coinsurance for your eligible expenses. You’d continue to pay the full cost of your spouse’s eligible expenses until he reaches his annual individual deductible.) Once the family deductible dollar amount is reached, no further deductible applies. This is called a non-collective calendar year deductible; it’s different than the collective deductible described in the next footnote.

10 If you cover yourself and any one or more dependents under the Med 1300 HDHP or Med 2500 HDHP options, you must pay the family deductible before the plan begins paying a percentage of charges for anyone. This is called a collective calendar year deductible.

• If you enroll in one of the high deductible health plans (Med 1300 or Med 2500), you also may be eligible to open a tax-favored Health Savings Account (HSA) at a financial institution of your choice. You can use it to save and pay for qualified medical, prescrip-tion drug, dental and vision expenses (in 2011 or anytime in the future).

8

Prescription Drug BenefitsWhen you elect medical coverage, it automatically includes prescription drug coverage. In 2011, Express Scripts will administer prescription drug coverage. Express Scripts’ pharmacy network is nationwide and includes both major chains and independent pharmacies. To see if your pharmacy is in the Express Scripts network, talk to your pharmacist or call Express Scripts at 866-219-1933.

Whether you enroll in Med 500, Med 1300 or Med 2500, you pay the full cost of prescription drugs until you meet the annual combined medical/prescription drug deductible (other than preventive medications). Once you meet the deductible (which includes both medical and prescription drug costs), you and the plan share in the cost of prescription drugs. You’ll pay a percentage of the cost of the drug, based on the drug tier. There is also a per-prescription maximum and an annual out-of-pocket maximum that limits how much you’ll pay (as shown in the table on the following page).

Important Notes about Med 500For 2011, the Med 500 option for non-Medicare primary retirees will work differently than in past years.

• In place of fixed copayments, most medical and prescription drug expenses will be subject to an annual deductible and coinsurance.

• There will no longer be a separate $50/$100 prescription drug deductible. The annual deductible includes both medical and prescription drug expenses.

• The individual annual out-of-pocket maxi-mum will increase from $2,500 to $3,000 in 2011. This is a combined medical and prescription drug out-of-pocket maximum (in 2010, prescription drug expenses had a separate out-of-pocket maximum of $1,500/$3,000). The family annual out-of-pocket maximum remains the same for eligi-ble expenses both in- and out-of-network.

Non-Medicare Primary Coverage

To see if your doctor is in the CIGNA network…

Talk to your doctor’s office, call CIGNA at 800-548-3980 or visit www.cigna.com (see “access to network providers” on page 23 for instructions on how to find a provider online). A vast majority of current providers are part of CIGNA’s nationwide Open Access Plus network, but if your providers aren’t part of the network, you can contact them directly to request that they contact CIGNA to discuss joining the network for the 2011 plan year.

9

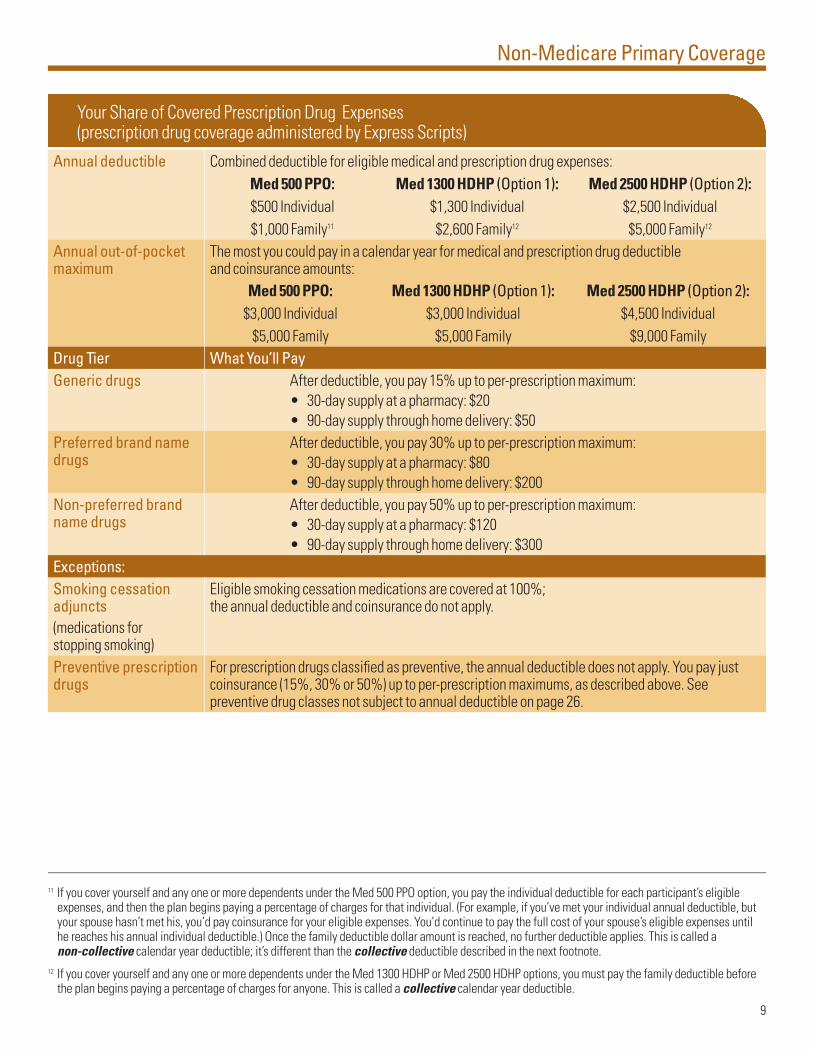

Your Share of Covered Prescription Drug Expenses (prescription drug coverage administered by Express Scripts)

Annual deductible Combined deductible for eligible medical and prescription drug expenses:Med 500 PPO: $500 Individual $1,000 Family11

Med 1300 HDHP (Option 1): $1,300 Individual$2,600 Family12

Med 2500 HDHP (Option 2): $2,500 Individual$5,000 Family12

Annual out-of-pocket maximum

The most you could pay in a calendar year for medical and prescription drug deductible and coinsurance amounts:

Med 500 PPO: $3,000 Individual

$5,000 Family

Med 1300 HDHP (Option 1): $3,000 Individual

$5,000 Family

Med 2500 HDHP (Option 2): $4,500 Individual

$9,000 FamilyDrug Tier What You’ll PayGeneric drugs After deductible, you pay 15% up to per-prescription maximum:

• 30-day supply at a pharmacy: $20• 90-day supply through home delivery: $50

Preferred brand name drugs

After deductible, you pay 30% up to per-prescription maximum: • 30-day supply at a pharmacy: $80• 90-day supply through home delivery: $200

Non-preferred brand name drugs

After deductible, you pay 50% up to per-prescription maximum: • 30-day supply at a pharmacy: $120• 90-day supply through home delivery: $300

Exceptions:Smoking cessation adjuncts(medications for stopping smoking)

Eligible smoking cessation medications are covered at 100%; the annual deductible and coinsurance do not apply.

Preventive prescription drugs

For prescription drugs classified as preventive, the annual deductible does not apply. You pay just coinsurance (15%, 30% or 50%) up to per-prescription maximums, as described above. See preventive drug classes not subject to annual deductible on page 26.

Non-Medicare Primary Coverage

11 If you cover yourself and any one or more dependents under the Med 500 PPO option, you pay the individual deductible for each participant’s eligible expenses, and then the plan begins paying a percentage of charges for that individual. (For example, if you’ve met your individual annual deductible, but your spouse hasn’t met his, you’d pay coinsurance for your eligible expenses. You’d continue to pay the full cost of your spouse’s eligible expenses until he reaches his annual individual deductible.) Once the family deductible dollar amount is reached, no further deductible applies. This is called a non-collective calendar year deductible; it’s different than the collective deductible described in the next footnote.

12 If you cover yourself and any one or more dependents under the Med 1300 HDHP or Med 2500 HDHP options, you must pay the family deductible before the plan begins paying a percentage of charges for anyone. This is called a collective calendar year deductible.

10

Non-Medicare Primary Coverage

New in 2011: Integrated Personal Health TeamAs a non-Medicare-primary participant, you’ll have access – at no additional cost – to a CIGNA Integrated Personal Health Team that provides total health management with easy access to a team of health professionals/advocates including individuals trained as nurses, coaches, dieticians, clinicians, counselors, and more – who listen, understand your needs and help you find solutions.

You can partner with a health advocate one-on-one to find local counselors, doctors or other health profes-sionals; get support for mental health, substance abuse and crises; know what to expect if time in the hospital is required; get advice on options to help you make an informed decision with your health professional; and understand the importance of preventive screen-ings. Starting Jan. 1, 2011, you’ll be able to connect with a health advocate via phone by calling CIGNA at 800-548-3980.

Health Savings AccountIf you enroll in Med 1300 or Med 2500 and you are not simultaneously enrolled in other non-high deductible health plan medical coverage (e.g., Medicare), the IRS allows you to open a special account called a Health Savings Account (HSA). You can open an HSA at a financial institution of your choice.

You can use your HSA to pay your out-of-pocket health care expenses (e.g., deductible and coinsur-ance) and qualified long-term care premiums. Once you are age 65 or older, you can also use your HSA to pay your retiree medical premiums (but not MediGap premiums). HSAs offer a triple tax advan-tage13: tax-deductible contributions, tax-free earn-ings and tax-free withdrawals when used toward qualified medical expenses, including prescription drug expenses. In addition, the money in your HSA carries forward from year to year – money you don’t use in any particular year will be available to help pay for eligible health care expenses in future years.

For complete information on HSAs, call the IRS at 800-829-1040, visit the IRS website at www.irs.gov and search for IRS Publication 969 or consult with your tax advisor or financial planner to see if an HSA is right for you.

Opening an HSAIf you are eligible for an HSA,14 you can open one at the financial institution of your choice; consult with your preferred bank to learn about the options that might be available to you. A bank specialist should be able to assist you in initiating the bank application process, provide information on HSA terms, fees and conditions and process deposits to and withdrawals from your account. For example, you can inquire about JPMorgan Chase’s HSA program by calling Chase HSA member services at 877-807-0206 or visiting www.chase.com (click “Savings,” then “Health Savings Account”).

13 The following states currently do not offer favorable tax treatment to HSAs: Alabama, California, New Hampshire, New Jersey, Tennessee and Wisconsin. 14 Since HSAs have special tax advantages, the IRS defines specific participation rules. To be eligible to contribute to an HSA, you must be enrolled in a

“high deductible health plan” as defined by the IRS. Both the Med 1300 and Med 2500 medical options for non-Medicare primary participants are high deductible health plans. Also, you cannot be claimed as a dependent on another person’s tax return, and you cannot have any other health coverage (except under another high deductible health plan). You must not be covered: • by your spouse’s medical or pharmacy plan • through Medicare Part A or B • through a general-purpose Flexible Spending Account (FSA) plan (e.g., your spouse’s FSA)

11

and your family might incur in 2011. Remember that your HSA allows you to set aside money for health care expenses and at the same time allows you to save on taxes by deducting the amount you contribute to your HSA from your taxable income each year. In addition, you can earn interest on the money in your HSA tax-free and withdraw funds to pay for qualified medical expenses, including prescription drug expenses, tax-free.

You contribute to your HSA with after-tax dollars. Most banks allow you to deposit dollars anytime by writing a personal check. You’ll be eligible for a federal tax deduction when you file your taxes for that year. Consult with your tax advisor for more details.

Contributing to Your HSAThe IRS sets annual limits on how much you can contribute to an HSA. In 2011, the annual maxi-mums are:

• $3,050 if you elect individual medical coverage

• $6,150 if you elect family coverage (any level other than individual)

• Plus an additional $1,000 in catch-up contri-butions if you will be age 55 or older in 2011

To determine how much you’ll want to contribute, you might find it helpful to review your health care costs for 2010 and think about the costs you

HSA and RHRA

Retirees who are eligible for the Retiree Health Reimbursement Account (RHRA) will no longer have a “full-use” RHRA. Beginning Jan. 1, 2011, the RHRAs will be changed to “limited-use” reimbursement accounts. This means the RHRA may be used only for retiree medical premiums, dental and vision expenses and qualified long term care premiums. In other words, retirees can use the RHRA to pay for the annual medical premiums but they can’t use it towards their medical deductibles or coinsurance. Federal requirements prohibit participants from contributing to an HSA if they have access to a “full-use” RHRA.

Reimbursement for OTC Drugs Eliminated

According to federal law, in 2011 only over-the-counter (OTC) medications that are prescribed by your doctor will be considered qualified medical expenses under the HSA and RHRA. Which means: Beginning Jan. 1, 2011, you may not use funds from your HSA or RHRA to purchase or be reimbursed for an over-the-counter medication, unless that medication is prescribed by your doctor. Keep prescriptions for OTC medications with your health care paperwork, in case you ever need to validate your HSA or RHRA withdrawals.

Non-Medicare Primary Coverage

12

If you have a current prescription with CIGNA, here’s how the transition to Express Scripts will be handled:

• At a pharmacy: If you have refills remaining on a current prescription, you can go to any participating Express Scripts pharmacy (call Express Scripts at 866-219-1933 for a list of participating pharmacies). Just present your new Express Scripts ID card and your phar-macist will be able to fill your prescription. You’ll receive a new ID card in December. You can use it beginning Jan. 1, 2011.

• Through home delivery: If you have mail-order refills remaining with CIGNA Tel-Drug, those refills should automatically be transferred to Express Scripts’ Home Delivery Pharmacy effective Jan. 1, 2011. In most cases, you do not need to get a new prescription (exceptions include prescriptions for controlled substances or compound medi-cations and prescriptions that are expired). After Jan. 1, 2011, contact Express Scripts by phone to set up your profile so your refills can be delivered to your home through Express Scripts Home Delivery Pharmacy.

• For step therapy: Step therapy is a method of treating a medical condition with the most cost-effective and safest drug therapy first, and then progressing to other more costly or risky therapies only if necessary, with the goal of minimizing risks and controlling costs. If you’ve already completed step therapy with CIGNA for blood pressure, cholesterol or stomach acid medicines, you won’t need to go through the step therapy process again with Express Scripts, unless your prescription changes. New prescriptions for blood pressure, cholesterol or stomach acid medicines filled on or after Jan. 1, 2011 must go through the Express Scripts step therapy process. For more information about step therapy, contact Express Scripts.

• If prior authorization is required: If you currently have a prescription that requires prior authorization, you’ll only need to get prior authorization for new prescrip-tions filled on or after Jan.1, 2011. Current prescriptions with active prior authorization will transfer to Express Scripts. For more information on which prescriptions require prior authorization, contact Express Scripts.

Prescriptions with no refills remaining, controlled substances, compound medications and expired prescriptions cannot be transferred to Express Scripts. If you do not have refills remaining as of Jan. 1, 2011, or are currently receiving a controlled substance or compound medication, you’ll need to ask your doctor for a new prescription and fill it either at the pharmacy or through the Home Delivery Pharmacy.

Filling Your Prescriptions in 2011

13

Watch for more information from Express Scripts

All prescription drug plans have a “formulary.” A formulary is a listing of generic and brand-name drugs that are considered “preferred” by the Pharmacy and Therapeutics Committee at Express Scripts. MassMutual’s plan utilizes the Express Scripts National Preferred Formulary. Formulary drugs are safe and effective and are generally less expensive than other brand-name drugs. If you are currently using a medication that will change drug tiers when we transition to Express Scripts (e.g., from preferred brand name to non-preferred brand name), you will receive a letter from Express Scripts in mid-November. You will also be contacted by Express Scripts if you use a specialty medication. Bottom line? If you see a letter in your mailbox from Express Scripts, open it immediately and take action.

Tip: In the future, the formulary will change from time to time. If you have questions about the formulary, contact Express Scripts 24/7 at 866-219-1933. Starting Jan.1, 2011, you can also go to Express Scripts’ website for the latest information on the formulary.

Filling Your Prescriptions in 2011

Want to save on your prescription drug costs? Here are some points to consider:

• Buy generics or preferred-brand drugs. When your doctor prescribes a brand-name drug, ask if there is a generic equivalent/alternative or a less expensive brand-name drug that meets your needs. You can contact Express Scripts at 866-219-1933 for more information.

• Buy home delivery prescriptions. If you have a chronic condition that requires ongoing medication, order a three-month supply through Express Scripts’ Home Delivery Pharmacy and have it delivered to your home. You’ll save time and – in most cases – money.

• Consider over-the-counter medications. Over-the-counter medications are usually less expensive than prescription drugs and are often very effective. Many brand-name drugs are available over the counter, includ-ing Prilosec, Zyrtec and Allegra.

14

Retiree Assistance Program Effective Jan. 1, 2011, the Retiree Assistance Program will transition from Aetna to CIGNA. MassMutual will continue to make the Retiree Assistance Program available to you and anyone living in your household. You and your household members can get help with a range of personal, financial and legal issues including parent-ing, senior care, child care, identity fraud and will preparation.

Starting in January, there will be a new Retiree Assistance Program website with CIGNA. You’ll also be able to call a single CIGNA phone number – 800-548-3980, 24 hours a day, 7 days a week – for both medical services and Retiree Assistance Program counseling. And, the six free visits per incident (no deductible, no coinsurance)

that are part of today’s Retiree Assistance Program and behavioral health program will continue to be available in 2011. Other than the six free visits per incident, all behavioral health services are part of your medical option and will be subject to the deductible, coinsurance and out-of-pocket maximum.

Life InsuranceIf you have group term life (GTL) insurance, it will only display on your benefit confirmation state-ment, which will be mailed to you in December. Since you cannot elect additional coverage, your group term life (GTL) insurance does not appear on your enrollment worksheet. Remember: You can reduce or drop GTL coverage during the year by notifying MassMutual Benefits in writing. Your coverage will end the first of the month following the date you notify MassMutual Benefits. However, once you reduce or drop coverage, you cannot increase or re-elect it at a later date.

Note: Group variable universal life (GVUL) insurance will not be listed on benefit confir-mation statements. GVUL participants may contact Executive Group Life Client Services at 800-548-0073 with any GVUL questions.

DentalIf you are eligible for dental coverage, it will be included on your enrollment worksheet. In 2011, the CIGNA dental network will be enhanced to include the expanded CIGNA Radius network of preferred providers. To confirm if your dentist is in the CIGNA Radius network, ask your dentist or call CIGNA at 800-548-3980. Note: You can use in-network or out-of-network dentists, as long as they’re licensed.

Retiree Assistance Program • Life Insurance • Dental

15

Expanded Dependent Eligibility Based on recently passed health care reform legislation, dependent eligibility for MassMutual benefit plans will be expanded. You will now be able to cover eligible children through the end of the month in which they turn age 26 without regard to student, marital or financial status or tax dependency. You may elect medical coverage during annual benefits enrollment, and coverage will take effect Jan. 1, 2011. You and your eligible child(ren) will be enrolled in the same medical option. Exception: If you are Medicare primary and your child(ren) are not, your dependent(s) will automatically be enrolled in the corresponding non-Medicare primary option.

Mastectomy-related ServicesMassMutual’s medical plans, as required by the Women’s Health and Cancer Rights Act of 1998, provide benefits for mastectomy-related services including reconstruction and surgery to achieve symmetry between the breasts, prostheses, and complications resulting from a mastectomy, includ-ing lymphedema. For details, contact CIGNA at 800-548-3980.

MassMutual’s Prescription Drug Coverage is Considered Creditable CoverageAn independent actuarial consulting firm has deter-mined that the prescription drug coverage offered by the MassMutual Employee Welfare Benefits Plan or the MassMutual Agents’ Welfare Benefits Plan is, on average for all plan participants,

expected to pay out as much as standard Medicare prescription drug coverage pays and is therefore considered Creditable Coverage for purposes of Medicare Part D. Refer to the Notice of Creditable Coverage – Appendix D on page 27 for details.

Health Coverage Assistance for Children & FamiliesIf you’re eligible for company-sponsored health coverage, but unable to afford the premiums, some states have premium assistance programs that can help pay for coverage. These states use funds from their Medicaid or CHIP programs to help people who are eligible for company-sponsored health coverage, but need assistance in paying their health premiums.

If your eligible dependents become ineligible for a Medicaid Plan or a state children’s health insur-ance program (CHIP), you may enroll them in MassMutual health care coverage at a later date if you meet any of the following conditions:

• You or your dependent were covered under a Medicaid Plan or state CHIP and that cover-age terminated due to a loss of eligibility; or

• You or your dependent became eligible for assistance from a Medicaid Plan or state CHIP, with respect to coverage under the plan.

You must request special enrollment within 60 days for the loss of Medicaid/CHIP or of the eligibility determination. Refer to the Medicare/CHIP Notice – Appendix E on page 29 for more information.

Did You Know?

16

Annual Benefits Enrollment begins Mon., Nov. 1 and ends Tues., Nov. 30, 2010. We encourage you to take the following steps to be sure you’re electing the coverage you need:

o Review this information for details about your 2011 benefits, and share information with anyone else who participates in making benefit decisions.

o Think about your health history and your health care needs, including how much you typically spend on health care each year and how this might change over the next year.

o Call the CIGNA pre-enrollment hotline at 800-548-3980 and Express Scripts at 866-219-1933 if you have additional ques-tions. Both phone lines are open 24 hours a day, 7 days a week.

o Decide which medical option is right for you.

o Enroll in your 2011 benefits. You can either log on to Retiree Center and make your elections online, or complete the enclosed paper form and return it to MassMutual using the enclosed business reply enve-lope or by faxing it to 413-226-4382. Refer to Enrollment Instructions – Appendix F on page 31 for details.

Benefits Enrollment

Some of the medical options are different and will not automatically continue in 2011. If your current medical option is no longer available in 2011 and you do not make an election, you and your covered dependents will automatically be enrolled in a “default” medical option, as shown in the following chart.

Your other benefits (dental and life insurance, if applicable) will roll over into 2011, based on your 2010 elections. Unless you have a qualify-ing change in status (such as marriage, the birth or adoption of a child), the next time you’ll be able to make changes to your benefits (other than drop-ping or reducing your coverage) will be during the annual benefits enrollment in the fall of 2011. If you experience a qualifying change in status during the year, contact MassMutual Benefits within 30 days of the event by calling 866-662-6448 or e-mailing [email protected]

If you do not make an election

If your 2010 medical option is …

In 2011, you’ll be enrolled in …

Aetna Select (Open Access)Blue Cross/Blue Shield Advantage Blue EPOCIGNA Open Access Plus In-NetworkConnectiCare EPOHealth New England HMO

Med 500

Med 500 Med 500High Deductible Health Plan Med 1500

Med 1300 (Option 1)

Watch for New ID Cards

If you’ll be a MassMutual medical participant in 2011, you’ll receive the following ID cards in December. You can use them beginning Jan. 1, 2011. · a new Medical ID card from CIGNA · a new prescription drug card from Express Scripts

If you haven’t received your new ID cards by Jan. 1, 2011, call CIGNA and/or Express Scripts.

17

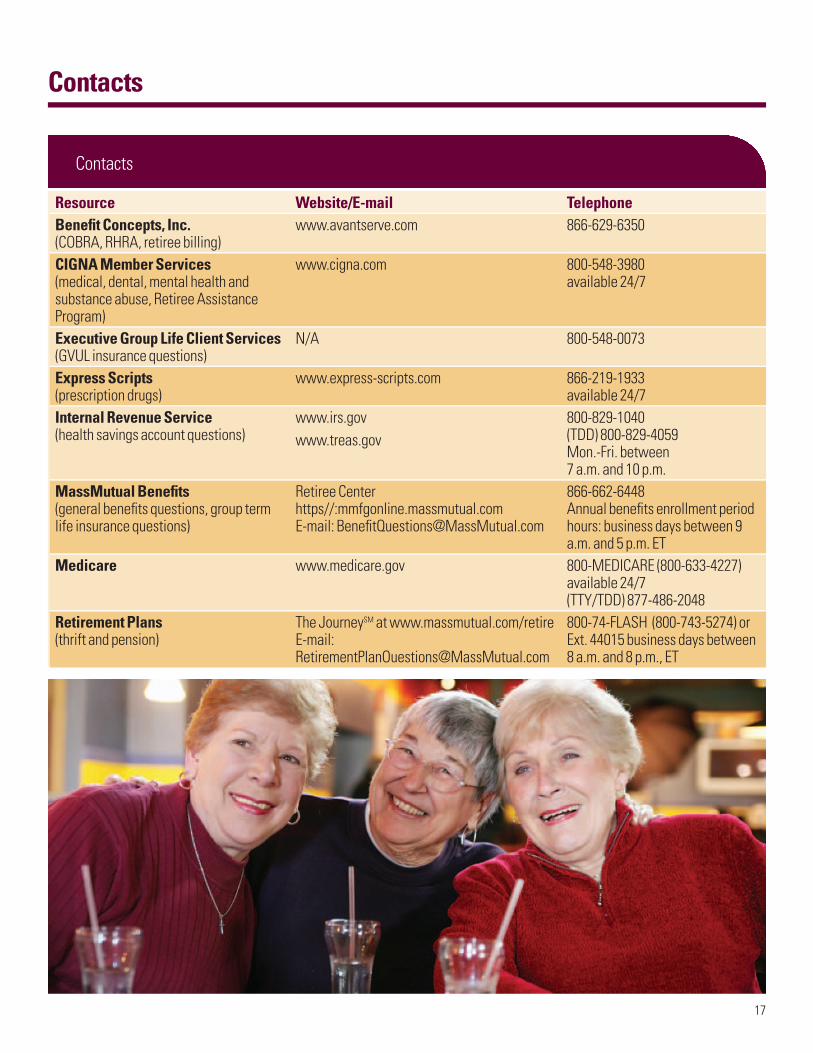

Contacts

Contacts

Resource Website/E-mail TelephoneBenefit Concepts, Inc. (COBRA, RHRA, retiree billing)

www.avantserve.com 866-629-6350

CIGNA Member Services (medical, dental, mental health and substance abuse, Retiree Assistance Program)

www.cigna.com 800-548-3980 available 24/7

Executive Group Life Client Services (GVUL insurance questions)

N/A 800-548-0073

Express Scripts(prescription drugs)

www.express-scripts.com 866-219-1933 available 24/7

800-829-1040 (TDD) 800-829-4059 Mon.-Fri. between 7 a.m. and 10 p.m.

MassMutual Benefits (general benefits questions, group term life insurance questions)

Retiree Center https//:mmfgonline.massmutual.com E-mail: [email protected]

866-662-6448 Annual benefits enrollment period hours: business days between 9 a.m. and 5 p.m. ET

Medicare www.medicare.gov 800-MEDICARE (800-633-4227) available 24/7 (TTY/TDD) 877-486-2048

Retirement Plans (thrift and pension)

The JourneySM at www.massmutual.com/retire E-mail: [email protected]

800-74-FLASH (800-743-5274) or Ext. 44015 business days between 8 a.m. and 8 p.m., ET

Generally, preventive medical care is covered at 100% with no annual deductible or coinsurance; you’ll pay $0 for eligible preventive care services.15 Regardless of the medical option you choose, using preventive services and following recommended health guidelines may help keep you healthy as well as detect health problems early, which may allow you to avoid a more complicated (and more costly) medi-cal condition later on.

Eligible preventive care services include routine physical exams, screenings and immunizations that your doctor determines are appropriate based on your age, gender and family history. It’s important to note that doctor’s visits to monitor existing conditions are not considered preventive care. Here’s a list of services typically considered preventive care:

Preventive Care Chart – Appendix A

Appendices

Well-Child Care (through age 18) Well-Adult Care (after age 18)Well-baby and Well-child visits• Periodic visits, depending on age

Well-man and Well-woman visits• Periodic visits, depending on age

Immunizations (as appropriate by age and sex)• Diphtheria, tetanus toxoids and acellular pertussis (DTaP)• Haemophilus influenzae type b conjugate (Hib)• Hepatitis A (Hep A) and B (Hep B)• Human papillomavirus HPV in girls and women ages 9 - 26• Influenza: annually 6 months through 18 years• Measles, mumps, and rubella (MMR)• Meningococcal (MCV): ages 11 - 18• Pneumococcal (pneumonia)• Poliovirus (IPV)• Rotavirus• Varicella (chickenpox)

Immunizations• Hepatitis A (Hep A) and B (Hep B): for those at risk• Human papillomavirus (HPV) in girls and women ages 9 - 26• Influenza: ages 19 - 49, as your doctor advises; ages 50+, annually• Pneumococcal (pneumonia): ages 65+ once (or younger for those with

risk factors)• Rubella (German Measles) for women of childbearing age if not immune• Tetanus and diphtheria toxoids booster (Td) every 10 years

(or Tdap, as indicated)• Varicella (chickenpox): second dose catch-up, or if no evidence of prior

immunization or chickenpox• Zoster: ages 60+

Preventive care

Screenings (as appropriate by age)• Cholesterol: for those at risk after age 2 but by age 10• Hearing and vision performed during the wellness visit• Hemoglobin or hematocrit: once a year for females

after menarche• Pap test within 3 years of sexual activity (or by age 21) at least

every 3 years

Screenings• Cholesterol ages 20+, every 5 years• Diabetes screening ages 45+, or at any age if asymptomatic with

sustained blood pressure greater than 135/80, every 3 years• Mammogram once a year for women ages 40+• Osteoporosis screening for women ages 65+; 60 for women at high risk• Pap test within 3 years of sexual activity, or ages 21-64 at least every 3 years• Prostate screening (PSA) for men ages 50+, once per year• Ultrasound for abdominal aortic aneurysm (AAA): men ages 65-75 who

have ever smoked• Chlamydia screening, sexually active women ages 24 and under• Colon cancer screenings ages 50+ (or at any age if risk factors):

– Flexible sigmoidoscopy every 5 years– Fecal occult blood test (FOBT) or fecal immunochemical test– (FIT) annually– Colonoscopy every 10 years– Double contrast barium enema every 5 years– Computed tomographic colonoscopy (CTC)/virtual colonoscopy every

15 The R&C allowance is the normal charge made by a provider for a similar service or supply that does not exceed the charge made by most providers in a given geographic region for the same service or supply. R&C applies to services covered under the MassMutual medical option for any services not covered by Medicare. Any services covered by Medicare are subject to the Medicare allowable charge.

Appendices

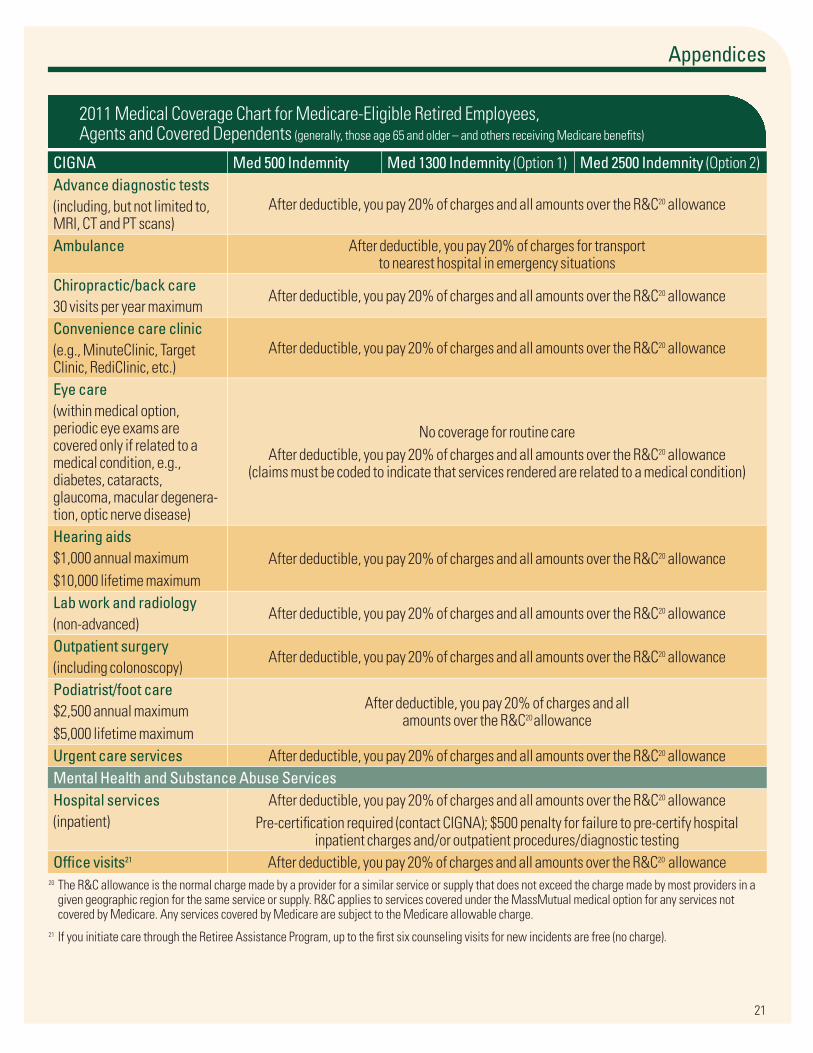

Medicare Primary Participants: Medical Coverage Chart – Appendix B

19

The current “Medicare & You” guide or “Your Medicare Benefit” booklet, both available by call-ing 800-MEDICARE, can provide you with details on what Medicare covers.

The MassMutual medical options for retired employees, agents and their covered dependents generally covers the services Medicare covers,16 in addition to some expenses that Medicare does not cover, as shown in the pages that follow (this list is not all-inclusive).

16 If you elect Medicare Part D, there is no prescription benefit through your MassMutual coverage but you pay the same monthly premium.

Disclaimer: The details contained in this chart reflect information available at the time of printing. For more detailed and up-to-date information, please contact CIGNA and Express Scripts directly. The chart contains an overview of the various MassMutual medical options for retired employees, agents and their covered dependents (refer to your enrollment worksheet for eligibility). It does not contain all plan information and is neither a plan document nor a summary plan description. It is for informational purposes only. In the event of any differences between this chart and the plan document, the plan document shall prevail. Some provisions may vary by state. MassMutual reserves the right to modify, revoke, change, suspend or terminate any and all of the plans, programs, policies, benefits or services described in the chart at any time or from time to time, with or without notice. Except for preventive care, coverage is limited to medically necessary services. Physician must follow American Medical Association (AMA) standard medical guidelines for services to be covered.

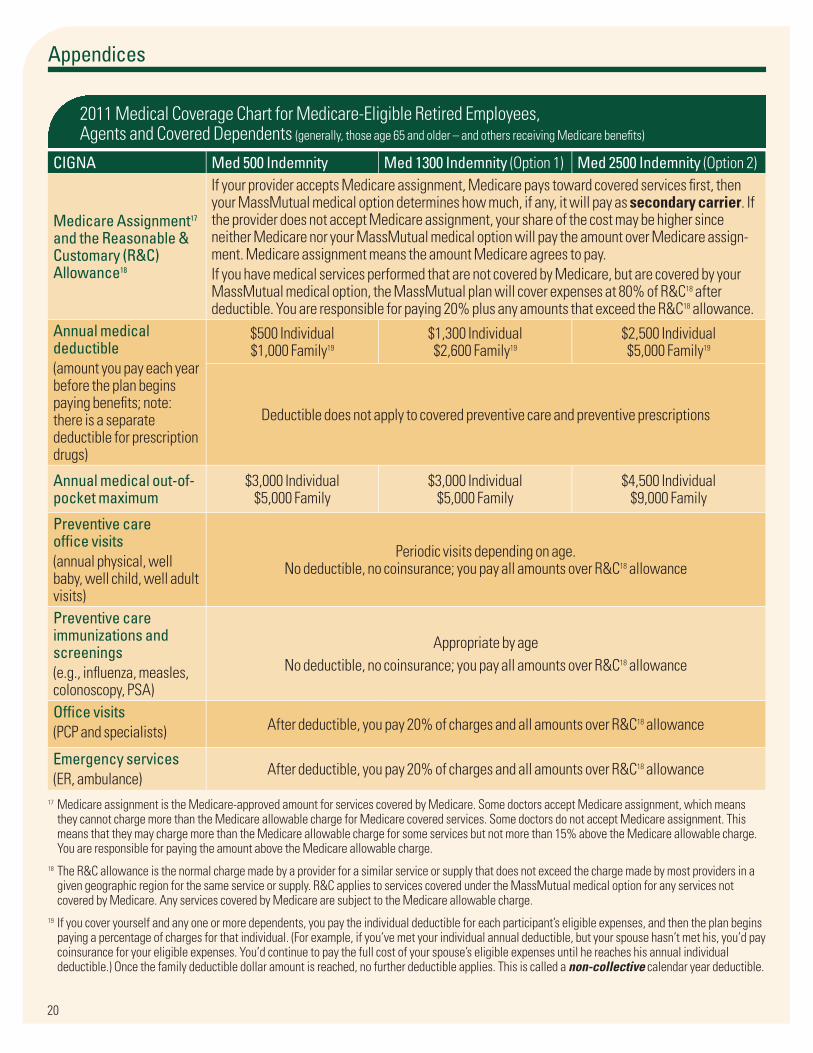

2011 Medical Coverage Chart for Medicare-Eligible Retired Employees, Agents and Covered Dependents (generally, those age 65 and older – and others receiving Medicare benefits)

CIGNA Med 500 Indemnity Med 1300 Indemnity (Option 1) Med 2500 Indemnity (Option 2)Geographic location and providers

National – you may use any licensed provider in the country. However, if the provider does not accept Medicare, your MassMutual medical option (administered by CIGNA) will not cover the part of the expense that Medicare would have covered, had the provider accepted Medicare. Providers must tell you if they have opted out of, or been excluded from, the Medicare program.

MassMutual plan is secondary coverage to Medicare

Medicare is the primary payer for medical expenses, so it pays your claims first; your MassMutual retiree medical option pays a portion, or none of, the remaining balance as secondary payer. In other words, Medicare processes your claim first. Then CIGNA processes your claim. Once you’ve met your annual deductible, the MassMutual plan (through CIGNA) pays the difference between what Medicare paid and the allowable charge under Medicare. If an eligible expense covered by the MassMutual plan is not covered by Medicare, the MassMutual plan will pay 80% of the expense, after you’ve met your annual deductible. If you are not enrolled in Medicare, but are eligible for it, your MassMutual retiree medical option processes your claim as if Medicare was the primary payer. The portion of the expense that would have been paid by Medicare (had you been enrolled) will not be covered by your MassMutual retiree medical option. You are responsible for paying that amount.

Appendices

20

17 Medicare assignment is the Medicare-approved amount for services covered by Medicare. Some doctors accept Medicare assignment, which means they cannot charge more than the Medicare allowable charge for Medicare covered services. Some doctors do not accept Medicare assignment. This means that they may charge more than the Medicare allowable charge for some services but not more than 15% above the Medicare allowable charge. You are responsible for paying the amount above the Medicare allowable charge.

18 The R&C allowance is the normal charge made by a provider for a similar service or supply that does not exceed the charge made by most providers in a given geographic region for the same service or supply. R&C applies to services covered under the MassMutual medical option for any services not covered by Medicare. Any services covered by Medicare are subject to the Medicare allowable charge.

19 If you cover yourself and any one or more dependents, you pay the individual deductible for each participant’s eligible expenses, and then the plan begins paying a percentage of charges for that individual. (For example, if you’ve met your individual annual deductible, but your spouse hasn’t met his, you’d pay coinsurance for your eligible expenses. You’d continue to pay the full cost of your spouse’s eligible expenses until he reaches his annual individual deductible.) Once the family deductible dollar amount is reached, no further deductible applies. This is called a non-collective calendar year deductible.

2011 Medical Coverage Chart for Medicare-Eligible Retired Employees, Agents and Covered Dependents (generally, those age 65 and older – and others receiving Medicare benefits)

CIGNA Med 500 Indemnity Med 1300 Indemnity (Option 1) Med 2500 Indemnity (Option 2)

Medicare Assignment17 and the Reasonable & Customary (R&C) Allowance18

If your provider accepts Medicare assignment, Medicare pays toward covered services first, then your MassMutual medical option determines how much, if any, it will pay as secondary carrier. If the provider does not accept Medicare assignment, your share of the cost may be higher since neither Medicare nor your MassMutual medical option will pay the amount over Medicare assign-ment. Medicare assignment means the amount Medicare agrees to pay. If you have medical services performed that are not covered by Medicare, but are covered by your MassMutual medical option, the MassMutual plan will cover expenses at 80% of R&C18 after deductible. You are responsible for paying 20% plus any amounts that exceed the R&C18 allowance.

Annual medical deductible(amount you pay each year before the plan begins paying benefits; note: there is a separate deductible for prescription drugs)

$500 Individual $1,000 Family19

$1,300 Individual $2,600 Family19

$2,500 Individual $5,000 Family19

Deductible does not apply to covered preventive care and preventive prescriptions

Annual medical out-of-pocket maximum

$3,000 Individual $5,000 Family

$3,000 Individual $5,000 Family

$4,500 Individual $9,000 Family

Preventive care office visits(annual physical, well baby, well child, well adult visits)

Periodic visits depending on age. No deductible, no coinsurance; you pay all amounts over R&C18 allowance

Preventive care immunizations and screenings(e.g., influenza, measles, colonoscopy, PSA)

Appropriate by ageNo deductible, no coinsurance; you pay all amounts over R&C18 allowance

Office visits(PCP and specialists) After deductible, you pay 20% of charges and all amounts over R&C18 allowance

Emergency services(ER, ambulance)

After deductible, you pay 20% of charges and all amounts over R&C18 allowance

Appendices

21

20 The R&C allowance is the normal charge made by a provider for a similar service or supply that does not exceed the charge made by most providers in a given geographic region for the same service or supply. R&C applies to services covered under the MassMutual medical option for any services not covered by Medicare. Any services covered by Medicare are subject to the Medicare allowable charge.

21 If you initiate care through the Retiree Assistance Program, up to the first six counseling visits for new incidents are free (no charge).

2011 Medical Coverage Chart for Medicare-Eligible Retired Employees, Agents and Covered Dependents (generally, those age 65 and older – and others receiving Medicare benefits)

CIGNA Med 500 Indemnity Med 1300 Indemnity (Option 1) Med 2500 Indemnity (Option 2)Advance diagnostic tests (including, but not limited to, MRI, CT and PT scans)

After deductible, you pay 20% of charges and all amounts over the R&C20 allowance

Ambulance After deductible, you pay 20% of charges for transport to nearest hospital in emergency situations

Chiropractic/back care30 visits per year maximum

After deductible, you pay 20% of charges and all amounts over the R&C20 allowance

Convenience care clinic(e.g., MinuteClinic, Target Clinic, RediClinic, etc.)

After deductible, you pay 20% of charges and all amounts over the R&C20 allowance

Eye care(within medical option, periodic eye exams are covered only if related to a medical condition, e.g., diabetes, cataracts, glaucoma, macular degenera-tion, optic nerve disease)

No coverage for routine careAfter deductible, you pay 20% of charges and all amounts over the R&C20 allowance

(claims must be coded to indicate that services rendered are related to a medical condition)

Hearing aids$1,000 annual maximum$10,000 lifetime maximum

After deductible, you pay 20% of charges and all amounts over the R&C20 allowance

Lab work and radiology (non-advanced)

After deductible, you pay 20% of charges and all amounts over the R&C20 allowance

Outpatient surgery (including colonoscopy)

After deductible, you pay 20% of charges and all amounts over the R&C20 allowance

Podiatrist/foot care$2,500 annual maximum$5,000 lifetime maximum

After deductible, you pay 20% of charges and all amounts over the R&C20 allowance

Urgent care services After deductible, you pay 20% of charges and all amounts over the R&C20 allowanceMental Health and Substance Abuse ServicesHospital services(inpatient)

After deductible, you pay 20% of charges and all amounts over the R&C20 allowancePre-certification required (contact CIGNA); $500 penalty for failure to pre-certify hospital

inpatient charges and/or outpatient procedures/diagnostic testingOffice visits21 After deductible, you pay 20% of charges and all amounts over the R&C20 allowance

Appendices

22

22 Net cost of drug means cost after applicable discounts, which may vary by pharmacy

2011 Medical Coverage Chart for Medicare-Eligible Retired Employees, Agents and Covered Dependents (generally, those age 65 and older – and others receiving Medicare benefits)

CIGNA Med 500 Indemnity Med 1300 Indemnity (Option 1) Med 2500 Indemnity (Option 2)Prescription Drug Coverage, Administered by Express ScriptsAnnual prescription drug deductible

$100 Individual $200 Family

$250 Individual $500 Family

$250 Individual $500 Family

Exceptions: Eligible smoking cessation medications are covered at 100%; the annual prescription drug deductible and coinsurance do not apply. For prescription drugs classified as preventive, the annual prescription drug deductible does not apply. You pay just coinsurance (15%, 30% or 50%) up to per-prescription maximums, as described below.

Annual prescription drug out-of-pocket maximum

$1,500 Individual$3,000 Family

Drug Tier – For drug tier info, call Express Scripts at 866-219-1933Generic (Tier 1)

After deductible, you pay 15% of the net22 cost of the drug up to per-prescription maximum:• 30-day supply at a pharmacy: $20• 90-day supply through home delivery: $50

Preferred brand name drugs (Tier 2)See Step Therapy, below

After deductible, you pay 30% of the net22 cost of the drug up to per-prescription maximum:• 30-day supply at a pharmacy: $80• 90-day supply through home delivery: $200

Non-preferred brand name drugs (Tier 3)See Step Therapy, below

After deductible, you pay 50% of the net22 cost of the drug up to per-prescription maximum:• 30-day supply at a pharmacy: $120• 90-day supply through home delivery: $300

Step TherapyThe step therapy program encourages use of lower cost alternatives in the following drug categories: blood pressure (ACE/ARB), cholesterol (statins) and stomach acid (proton pump inhibitors). If your prescription falls into one of these categories, it’ll be subject to step therapy. Your pharmacist will contact your provider to approve a lower-cost alternative. If approved, the lower-cost alternative will be dispensed. If your provider doesn’t agree with the substitute, the pharmacist will dispense as written. For more information, contact Express Scripts at 866-219-1933.Preventive Drug Classes Not Subject to Annual Deductible (you pay just coinsurance)U.S. Pharmacopia Drug Classes (more commonly known as)

• Antiasthmatics (asthma medications, including inhalers)

• Anticoagulants, platelet aggregation inhibitors (blood thinning medications taken for stroke prevention)

• Antidiabetic agents (diabetes medications and diabetes strips)

• Antineoplastic products (medications used to prevent breast cancer only)

• Appetite suppressants, lipase inhibitors (antiobesity/weight loss medication, only for those diagnosed with obesity)

• Bone resorption inhibitors, osteoporosis therapies, osteoporosis therapy adjuncts (osteoporosis medications, including medications that help prevent bone thinning)

• Prenatal vitamins, nutritional supplements and vitamin replenishers (vitamins for pregnancy and to prevent prenatal nutrient deficiency)

Note: For specific information on what constitutes a deductible-free preventive medication, call Express Scripts at 866-219-1933

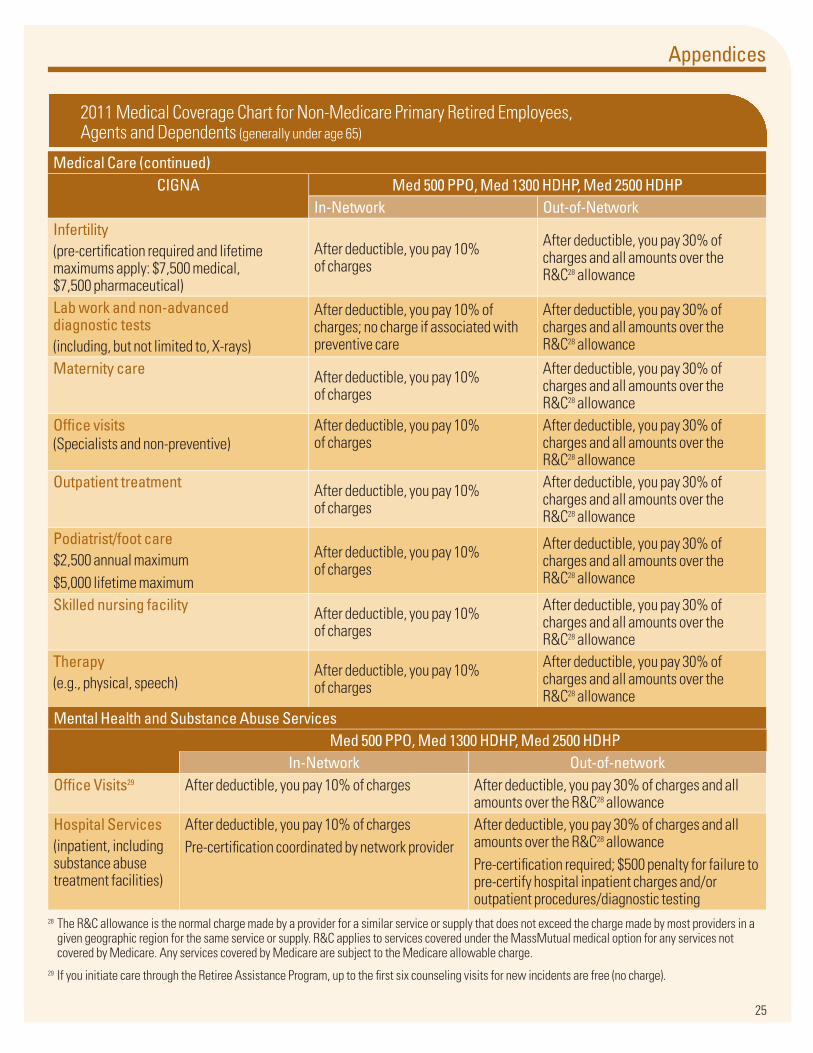

Non-Medicare Primary Participants: Medical Coverage Chart – Appendix C

Appendices

23

23 If you cover yourself and any one or more dependents under the Med 500 preferred provider organization (PPO) option, you pay the individual deductible for each participant’s eligible expenses, and then the plan begins paying a percentage of charges for that individual. (For example, if you’ve met your individual annual deductible, but your spouse hasn’t met his, you’d pay coinsurance for your eligible expenses. You’d continue to pay the full cost of your spouse’s eligible expenses until he reaches his annual individual deductible.) Once the family deductible dollar amount is reached, no further deductible applies. This is called a non-collective calendar year deductible; it’s different than the collective deductible described in the next footnote.

24 If you cover yourself and any one or more dependents under the Med 1300 or Med 2500 high deductible health plan (HDHP) options, you must pay the family deductible before the plan begins paying a percentage of charges for anyone. This is called a collective calendar year deductible.

25 The R&C allowance is the normal charge made by a provider for a similar service or supply that does not exceed the charge made by most providers in a given geographic region for the same service or supply. R&C applies to services covered under the MassMutual medical option for any services not covered by Medicare. Any services covered by Medicare are subject to the Medicare allowable charge.

26 Non-network charges are subject to the reasonable and customary (R&C) allowance – this is the normal charge made by a provider for a similar service or supply that does not exceed the charge by most providers in a given geographic region. You are responsible for paying any charges over R&C. Amounts in excess of R&C will not count toward the accumulation of your annual deductible or annual out-of-pocket maximum.

Disclaimer: The details contained in this chart reflect information available at the time of printing. For more detailed and up-to-date information, please contact the medical carriers directly. The chart contains an overview of the various MassMutual medical options (refer to online or printed enrollment worksheet for eligibility). It does not contain all plan information and is neither a plan document nor a summary plan description. It is for informational purposes only. In the event of any differences between this chart and the plan document, the plan document shall prevail. Some provisions may vary by state. MassMutual reserves the right to modify, revoke, change, suspend or terminate any and all of the plans, programs, policies, benefits or services described in the chart at any time or from time to time, with or without notice. Except for preventive care, coverage is limited to medically necessary services. Physician must follow American Medical Association (AMA) standard medical guidelines for services to be covered.

2011 Medical Coverage Chart for Non-Medicare Primary Retired Employees, Agents and Dependents (generally under age 65)

CIGNA Med 500Preferred Provider

Organization

High Deductible Health PlanMed 1300(Option 1)

Med 2500(Option 2)

Access to network providers These CIGNA options use a national network with coverage in most geographic areas. Please check the online directory at www.cigna.com and select “Provider Directory,” enter your ZIP code, the distance you’re willing to travel to a network provider, and under “What type of plan do you have?” Select “Open Access Plus, OA Plus, Choice Fund OA Plus.” Or call CIGNA at 800-548-3980 for help.

Annual deductible(amount you pay each year for eligible medical and prescription drug expenses before the plan begins paying benefits; deductible does not apply to preventive care and preventive medications)

$500 Individual $1,000 Family23

$1,300 Individual$2,600 Family24

$2,500 Individual $5,000 Family24

Coinsurance (that YOU pay)

In-Network: After deductible, you pay 10% on all services other than preventive care and prescription drugsOut-of-Network: After deductible, you pay 30% of charges other than preventive care and prescription drugs, and all amounts over the R&C25 allowance

Annual out-of-pocket maximum26 $3,000 Individual $5,000 Family

$3,000 Individual $5,000 Family

$4,500 Individual$9,000 Family

Choice of physician or hospital In-Network: Any network physician or hospital Out-of-Network: Any licensed physician or hospital

Appendices

24

2011 Medical Coverage Chart for Non-Medicare Primary Retired Employees, Agents and Dependents (generally under age 65)

Medical CareCIGNA Med 500 PPO, Med 1300 HDHP, Med 2500 HDHP

In-Network Out-of-NetworkAdvanced diagnostic tests (including, but not limited to, MRI, CT and PT scans)

After deductible, you pay 10% of charges

After deductible, you pay 30% of charges and all amounts over the R&C27 allowance

Chiropractic/back services office visits(30 visits per calendar year)

After deductible, you pay 10% of charges

After deductible, you pay 30% of charges and all amounts over the R&C27 allowance

Convenience care clinics(e.g., Minute Clinic, Target Clinic, RediClinic, etc.)

After deductible, you pay 10% of charges

After deductible, you pay 30% of charges and all amounts over the R&C27 allowance

Dental coverage for injury to sound, natural teeth (within medical option; treatment must be initiated within six months of injury)

After deductible, you pay 10% of charges

After deductible, you pay 30% of charges and all amounts over the R&C27 allowance

Emergency services(ER, ambulance) After deductible, you pay 10% of charges

Eye care (within medical option, periodic eye exams are covered only if related to a medical condition, e.g., diabetes, cataracts, glaucoma, macular degeneration, optic nerve disease)

After deductible, you pay 10% of charges

After deductible, you pay 30% of charges and all amounts over the R&C27 allowance

Hearing aids $1,000 annual maximum$10,000 lifetime maximum

After deductible, you pay 10% of charges

After deductible, you pay 30% of charges and all amounts over the R&C27 allowance

Home health care(incl. outpatient private duty nurse)

After deductible, you pay 10% of charges

After deductible, you pay 30% of charges and all amounts over the R&C27 allowance

CIGNA Med 500Preferred Provider

Organization

High Deductible Health PlanMed 1300(Option 1)

Med 2500(Option 2)

Preventive care office visits(annual physical, well baby, well child, well adult visits)

Periodic visits depending on ageDeductible and coinsurance do not apply; you pay all amounts over the R&C27 allowance

Preventive care immunizations and screenings(e.g., influenza, measles, colonoscopy, PSA)

Appropriate by ageDeductible and coinsurance do not apply; you pay all amounts over the R&C27 allowance

27 The R&C allowance is the normal charge made by a provider for a similar service or supply that does not exceed the charge made by most providers in a given geographic region for the same service or supply. R&C applies to services covered under the MassMutual medical option for any services not covered by Medicare. Any services covered by Medicare are subject to the Medicare allowable charge.

25

Appendices

2011 Medical Coverage Chart for Non-Medicare Primary Retired Employees, Agents and Dependents (generally under age 65)

Mental Health and Substance Abuse Services Med 500 PPO, Med 1300 HDHP, Med 2500 HDHP

In-Network Out-of-networkOffice Visits29 After deductible, you pay 10% of charges After deductible, you pay 30% of charges and all

amounts over the R&C28 allowanceHospital Services (inpatient, including substance abuse treatment facilities)

After deductible, you pay 10% of chargesPre-certification coordinated by network provider

After deductible, you pay 30% of charges and all amounts over the R&C28 allowancePre-certification required; $500 penalty for failure to pre-certify hospital inpatient charges and/or outpatient procedures/diagnostic testing

28 The R&C allowance is the normal charge made by a provider for a similar service or supply that does not exceed the charge made by most providers in a given geographic region for the same service or supply. R&C applies to services covered under the MassMutual medical option for any services not covered by Medicare. Any services covered by Medicare are subject to the Medicare allowable charge.

29 If you initiate care through the Retiree Assistance Program, up to the first six counseling visits for new incidents are free (no charge).

Medical Care (continued)CIGNA Med 500 PPO, Med 1300 HDHP, Med 2500 HDHP

After deductible, you pay 30% of charges and all amounts over the R&C28 allowance

Lab work and non-advanced diagnostic tests(including, but not limited to, X-rays)

After deductible, you pay 10% of charges; no charge if associated with preventive care

After deductible, you pay 30% of charges and all amounts over the R&C28 allowance

Maternity care After deductible, you pay 10% of charges

After deductible, you pay 30% of charges and all amounts over the R&C28 allowance

Office visits(Specialists and non-preventive)

After deductible, you pay 10% of charges

After deductible, you pay 30% of charges and all amounts over the R&C28 allowance

Outpatient treatment After deductible, you pay 10% of charges

After deductible, you pay 30% of charges and all amounts over the R&C28 allowance

Podiatrist/foot care $2,500 annual maximum$5,000 lifetime maximum

After deductible, you pay 10% of charges

After deductible, you pay 30% of charges and all amounts over the R&C28 allowance

Skilled nursing facility After deductible, you pay 10% of charges

After deductible, you pay 30% of charges and all amounts over the R&C28 allowance

Therapy(e.g., physical, speech)

After deductible, you pay 10% of charges

After deductible, you pay 30% of charges and all amounts over the R&C28 allowance

Appendices

26

Prescription Drug Coverage – Administered by Express ScriptsAnnual deductible Medical and prescription drug deductibles are combined; see “annual deductible” on page 23.

For certain preventive drug classes (see the “Preventive Drug Classes Not Subject to Annual Deductible” chart below), the deductible does not apply and you pay just the coinsurance subject to per-prescription maximums. Eligible smoking cessation medications are covered at 100%; the annual deductible and coinsur-ance do not apply.

Annual out-of-pocket maximum

Combined medical and prescription out-of-pocket maximum applies; see “annual out-of-pocket maximum” on page 23.

Drug Tier – For drug tier info, call Express Scripts at 866-219-1933 Generic (Tier 1)

After deductible, you pay 15% of the net30 cost of the drug up to per-prescription maximum:• 30-day supply at a pharmacy: $20• 90-day supply through home delivery: $50

Preferred brand name drugs (Tier 2)See Step Therapy, below

After deductible, you pay 30% of the net30 cost of the drug up to per-prescription maximum:• 30-day supply at a pharmacy: $80• 90-day supply through home delivery: $200

Non-preferred brand name drugs (Tier 3)See Step Therapy, below

After deductible, you pay 50% of the net30 cost of the drug up to per-prescription maximum:• 30-day supply at a pharmacy: $120• 90-day supply through home delivery: $300

Step TherapyThe step therapy program encourages use of lower cost alternatives in the following drug categories: blood pressure (ACE/ARB), cholesterol (statins) and stomach acid (proton pump inhibitors). If your prescription falls into one of these categories, it’ll be subject to step therapy. Your pharmacist will contact your provider to approve a lower-cost alternative. If approved, the lower-cost alternative will be dispensed. If your provider doesn’t agree with the substitute, the pharmacist will dispense as written. For more information, contact Express Scripts at 866-219-1933.Preventive Drug Classes Not Subject to Annual DeductibleU.S. Pharmacopia Drug Classes (more commonly known as)

thinning medications taken for stroke prevention)• Antidiabetic agents (diabetes medications and

diabetes strips)• Antineoplastic products (medications used to prevent

breast cancer only)• Antihyperlipidemics (high cholesterol medications)• Antihypertensives (high blood pressure medications)

• Appetite suppressants, lipase inhibitors (antiobesity/weight loss medication, only for those diagnosed with obesity)

• Bone resorption inhibitors, osteoporosis therapies, osteopo-rosis therapy adjuncts (osteoporosis medications, including medications that help prevent bone thinning)

• Prenatal vitamins, nutritional supplements and vitamin replenishers (vitamins for pregnancy and to prevent prenatal nutrient deficiency)

Note: For specific information on what constitutes a deductible-free preventive medication, call Express Scripts at 866-219-1933.

2011 Medical Coverage Chart for Non-Medicare Primary Retired Employees, Agents and Dependents (generally under age 65)

30 Net cost of drug means cost after applicable discounts, which may vary by pharmacy

Appendices

27