49

TRANSPORTATION RESEARCH BOARD @NASEMTRB #TRBwebinar Forecasting Zero Emission Vehicles: Fleet Scenarios & Emissions Implications June 30, 2020 1:00-3:00 PM Eastern

TRANSPORTATION RESEARCH BOARD

@NASEMTRB#TRBwebinar

Forecasting Zero Emission Vehicles: Fleet Scenarios &

Emissions ImplicationsJune 30, 2020

1:00-3:00 PM Eastern

The Transportation Research Board

has met the standards and

requirements of the Registered

Continuing Education Providers

Program. Credit earned on completion

of this program will be reported to

RCEP. A certificate of completion will

be issued to participants that have

registered and attended the entire

session. As such, it does not include

content that may be deemed or

construed to be an approval or

endorsement by RCEP.

PDH Certification Information:

•2 Professional Development Hours (PDH) – see follow-up email for instructions•You must attend the entire webinar to be eligible to receive PDH credits•Questions? Contact Reggie Gillum at [email protected]

#TRBwebinar

Learning Objectives

#TRBwebinar

1. Identify different ZEV adoption models in the U.S.

2. Discuss how different fleet scenarios will effect emissions

Forecasting Zero Emission Vehicles

(ZEVs): Future Fleet Scenarios and

Emissions Implications

A Transportation Research Board (TRB) Webinar

June 30, 2020

STI-7401

Work completed under

NCHRP 25-25/Task 115 (Panel D2525115)

Research Organizations: Louis Berger U.S. Inc. and Sonoma Technology, Inc. (STI)

2

Garnet Erdakos, PhD (Principal Investigator, STI)

Shih Ying Chang, PhD (STI)

Douglas Eisinger, PhD (Senior Advisor, STI)

Adrienne Heller, AICP, ENV SP (formerly Louis Berger/WSP)

Heather Unger, LEED AP, ENV SP (Louis Berger/WSP)

NCHRP Senior Program OfficerAnn M. Hartell, PhD

Author Acknowledgments

3

• Rick Baker, Eastern Research Group, Inc.

• John Davies, Federal Highway Administration (Liaison)

• Jeffrey R. Lidicker, California Air Resources Board

• Jane Jie Lin, University of Illinois – Chicago

• Natalie Ries, Minnesota Department of Transportation

• Melissa Savage, American Association of State Highway and Transportation Officials (Liaison)

• Lubna Shoaib, East West Gateway Council of Government

• Colleen M. Turner, Maryland Department of Transportation

• Benjamin P. VanGessel, U.S. Environmental Protection Agency

The research team also thanks Dr. Song Bai of the Bay Area Air Quality Management District for his input on the research

approach used in this study. In addition, appreciation goes to John Davies of the U.S. Federal Highway Administration, Dr.

Zhenhong Lin of the Oak Ridge National Laboratory, and Andrew Breck of the Volpe National Transportation Systems Center,

for their assistance regarding use of the MA3T model.

Key Acronyms in Today’s Talk

4

• AEO: Annual Energy Outlook (by Energy Information Admin., U.S. Dept. of Energy)

• ATV: advanced technology vehicle (as used here: BEV, FCEV, PHEV, HEV)

• BEV: battery electric vehicle

• CARB: Calif. Air Resources Board

• DOT: state department of transportation

• EVSE: electric vehicle supply equipment (think: charging station)

• FCEV: fuel cell electric vehicle

• HEV: hybrid electric vehicle (not a plug-in)

• IPCC: Intergovernmental Panel on Climate Change

• HOV: high occupancy vehicle

• LDV: light-duty vehicle

• MA3T: Market Acceptance of Advanced Automotive Technologies; Oak Ridge Nat’l Lab. model

• MOVES: EPA emissions model used here to estimate on-road vehicle emissions

• MPO: metropolitan planning organization (regional transportation planning agency)

• OEM: original equipment manufacturer (as used here, refers to auto makers)

• PHEV: plug-in hybrid electric vehicle

• VMT: vehicle miles traveled

• ZEV: zero emission vehicle, as used here, battery electric vehicle (BEV) and fuel cell electric (FCEV)

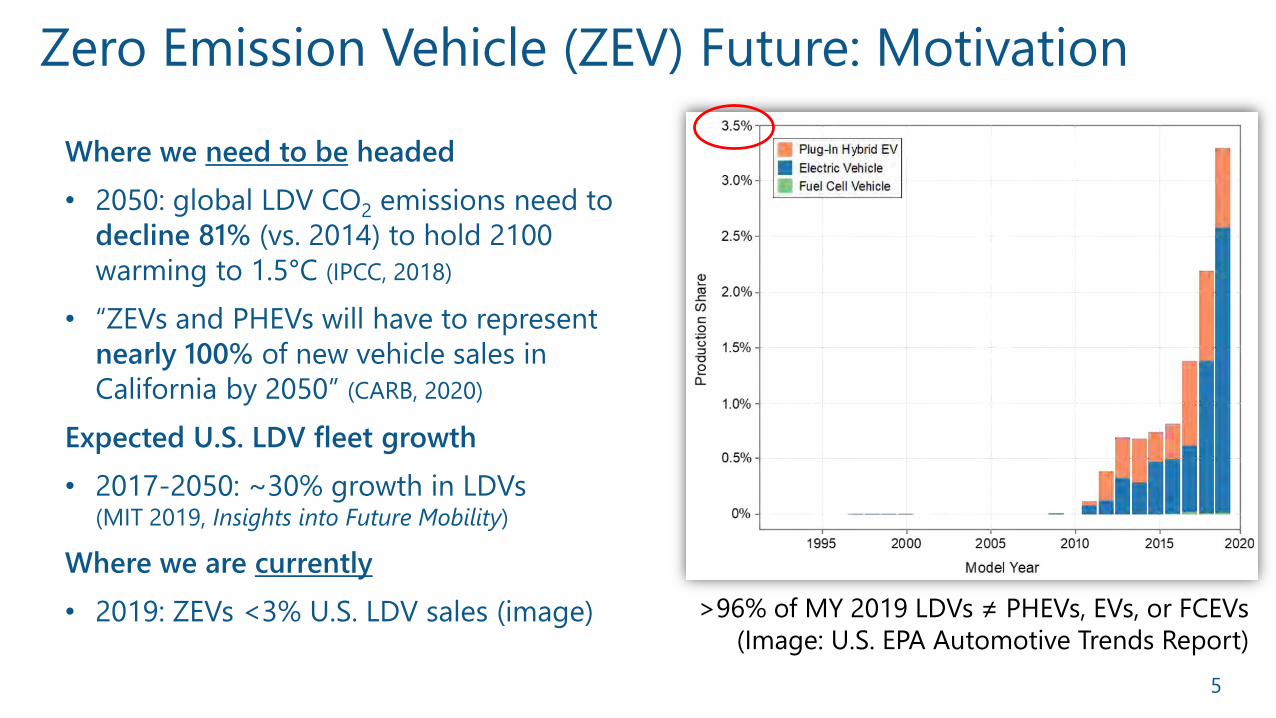

Zero Emission Vehicle (ZEV) Future: Motivation

Where we need to be headed

• 2050: global LDV CO2 emissions need to

decline 81% (vs. 2014) to hold 2100

warming to 1.5°C (IPCC, 2018)

• “ZEVs and PHEVs will have to represent

nearly 100% of new vehicle sales in

California by 2050” (CARB, 2020)

Expected U.S. LDV fleet growth

• 2017-2050: ~30% growth in LDVs (MIT 2019, Insights into Future Mobility)

Where we are currently

• 2019: ZEVs <3% U.S. LDV sales (image) >96% of MY 2019 LDVs ≠ PHEVs, EVs, or FCEVs

(Image: U.S. EPA Automotive Trends Report)

5

Learning Objective

6

• Describe how to support efforts to promote adoption of

ZEVs in the U.S.

Project Tasks

• Brief literature review

• Develop ZEV adoption analysis scenarios

• Assess emissions reductions

Outline

7

• Key findings from the literature review

• Rationale for using the MA3T model

• Guiding principles for development and selection of scenarios

• ZEV adoption scenarios

• Modeled ZEV population increases

• Modeled emissions reductions

• Implications and future research suggestions

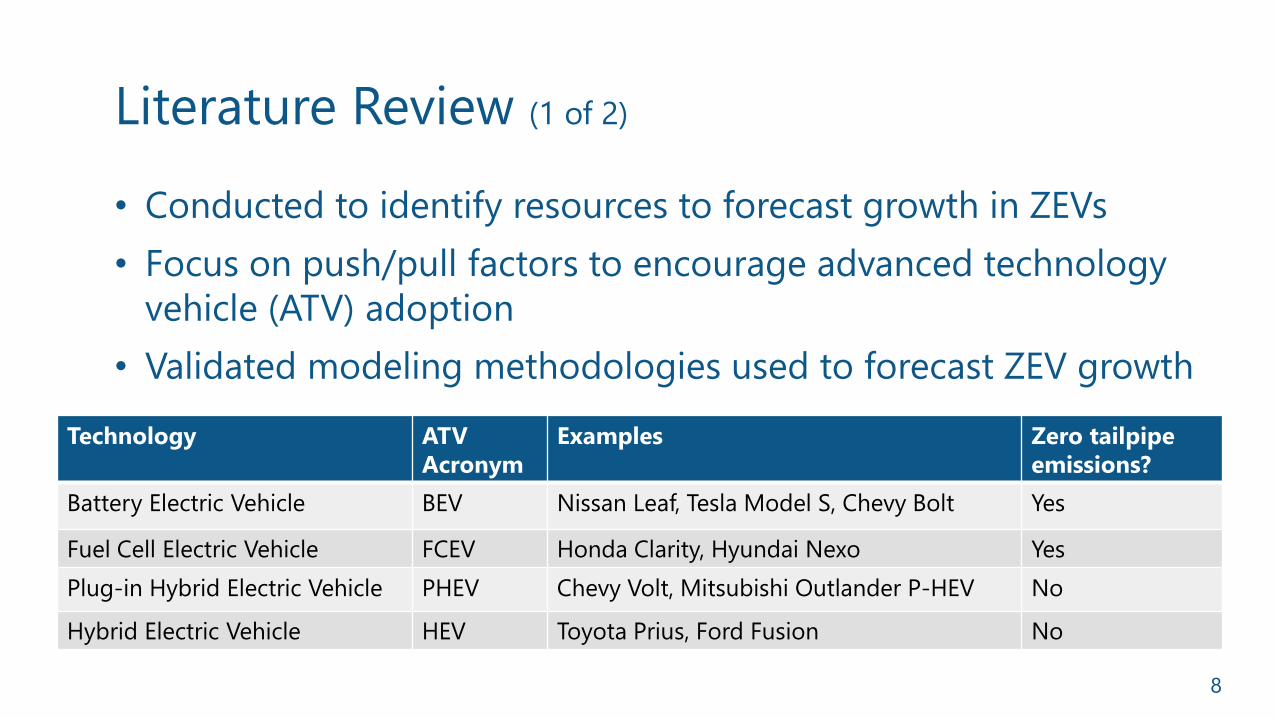

Literature Review (1 of 2)

8

Technology ATV

Acronym

Examples Zero tailpipe

emissions?

Battery Electric Vehicle BEV Nissan Leaf, Tesla Model S, Chevy Bolt Yes

Fuel Cell Electric Vehicle FCEV Honda Clarity, Hyundai Nexo Yes

Plug-in Hybrid Electric Vehicle PHEV Chevy Volt, Mitsubishi Outlander P-HEV No

Hybrid Electric Vehicle HEV Toyota Prius, Ford Fusion No

• Conducted to identify resources to forecast growth in ZEVs

• Focus on push/pull factors to encourage advanced technology

vehicle (ATV) adoption

• Validated modeling methodologies used to forecast ZEV growth

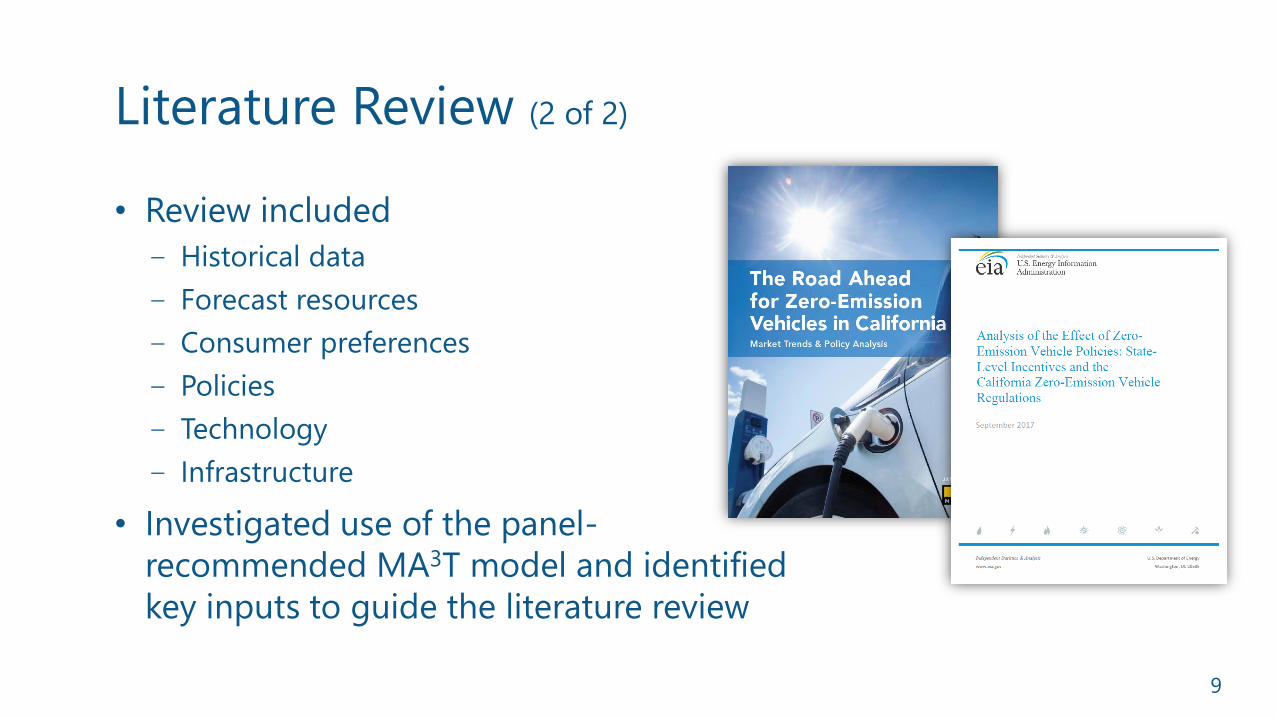

Literature Review (2 of 2)

9

• Review included

‒ Historical data

‒ Forecast resources

‒ Consumer preferences

‒ Policies

‒ Technology

‒ Infrastructure

• Investigated use of the panel-

recommended MA3T model and identified

key inputs to guide the literature review

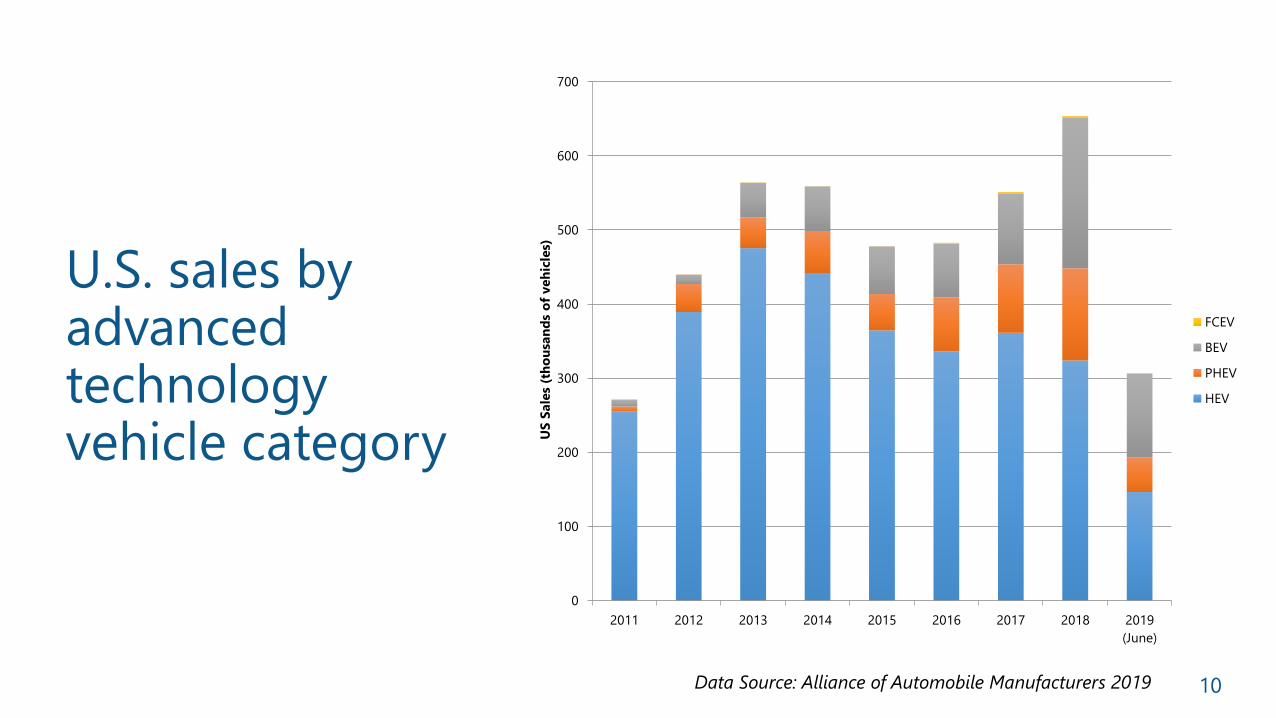

0

100

200

300

400

500

600

700

2011 2012 2013 2014 2015 2016 2017 2018 2019

(June)

US

Sale

s (t

ho

usa

nd

s o

f veh

icle

s)

FCEV

BEV

PHEV

HEV

U.S. sales by advanced technology vehicle category

Data Source: Alliance of Automobile Manufacturers 2019 10

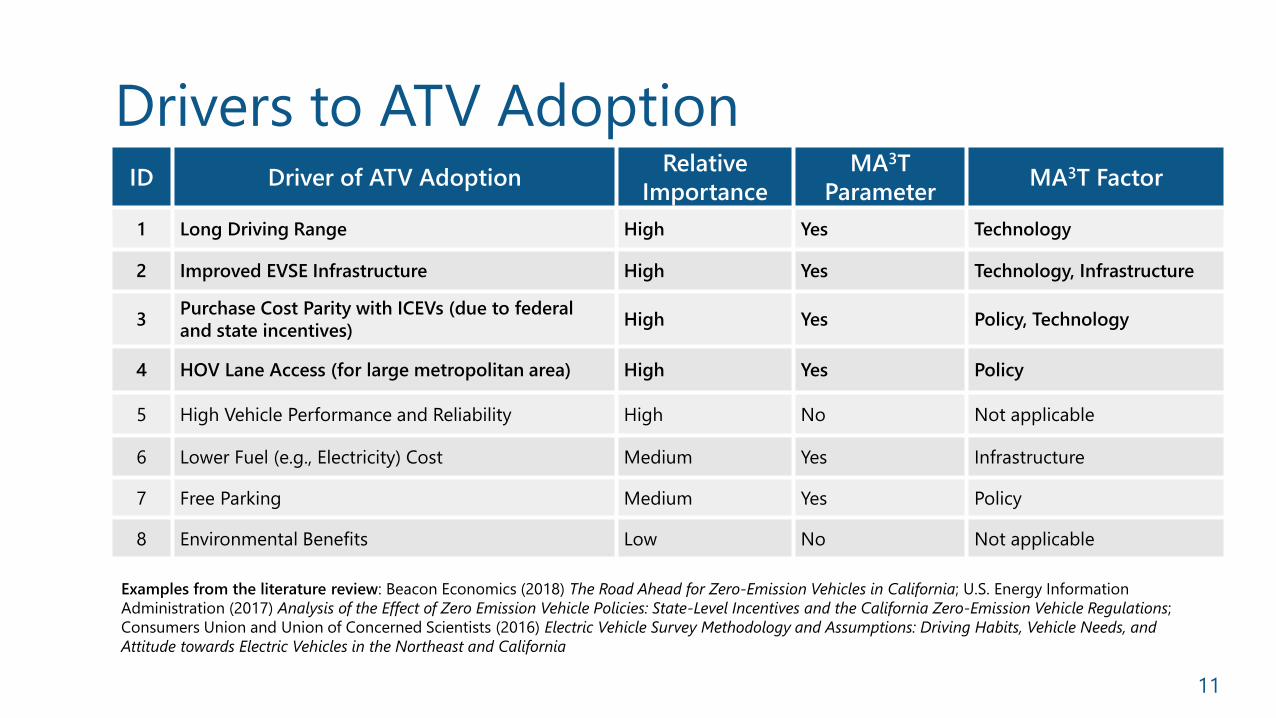

Drivers to ATV Adoption

11

ID Driver of ATV AdoptionRelative

Importance

MA3T

ParameterMA3T Factor

1 Long Driving Range High Yes Technology

2 Improved EVSE Infrastructure High Yes Technology, Infrastructure

3Purchase Cost Parity with ICEVs (due to federal

and state incentives)High Yes Policy, Technology

4 HOV Lane Access (for large metropolitan area) High Yes Policy

5 High Vehicle Performance and Reliability High No Not applicable

6 Lower Fuel (e.g., Electricity) Cost Medium Yes Infrastructure

7 Free Parking Medium Yes Policy

8 Environmental Benefits Low No Not applicable

Examples from the literature review: Beacon Economics (2018) The Road Ahead for Zero-Emission Vehicles in California; U.S. Energy Information

Administration (2017) Analysis of the Effect of Zero Emission Vehicle Policies: State-Level Incentives and the California Zero-Emission Vehicle Regulations;

Consumers Union and Union of Concerned Scientists (2016) Electric Vehicle Survey Methodology and Assumptions: Driving Habits, Vehicle Needs, and

Attitude towards Electric Vehicles in the Northeast and California

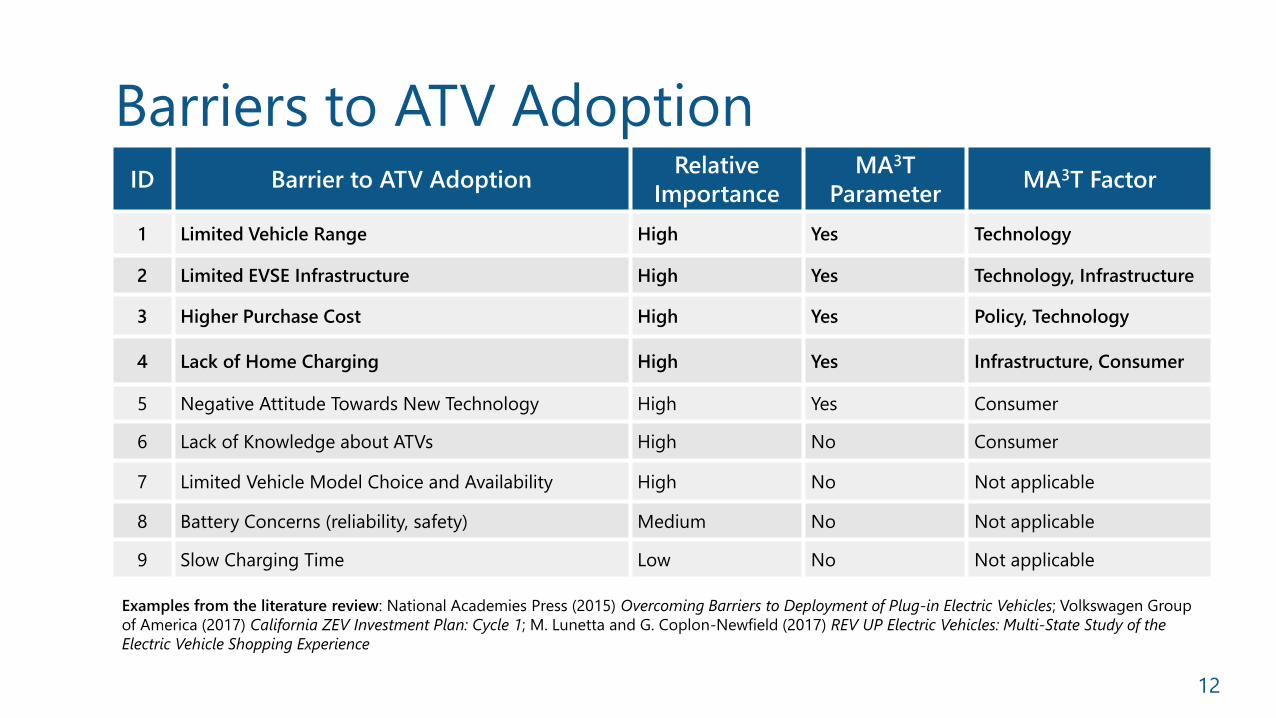

Barriers to ATV Adoption

12

ID Barrier to ATV AdoptionRelative

Importance

MA3T

ParameterMA3T Factor

1 Limited Vehicle Range High Yes Technology

2 Limited EVSE Infrastructure High Yes Technology, Infrastructure

3 Higher Purchase Cost High Yes Policy, Technology

4 Lack of Home Charging High Yes Infrastructure, Consumer

5 Negative Attitude Towards New Technology High Yes Consumer

6 Lack of Knowledge about ATVs High No Consumer

7 Limited Vehicle Model Choice and Availability High No Not applicable

8 Battery Concerns (reliability, safety) Medium No Not applicable

9 Slow Charging Time Low No Not applicable

Examples from the literature review: National Academies Press (2015) Overcoming Barriers to Deployment of Plug-in Electric Vehicles; Volkswagen Group

of America (2017) California ZEV Investment Plan: Cycle 1; M. Lunetta and G. Coplon-Newfield (2017) REV UP Electric Vehicles: Multi-State Study of the

Electric Vehicle Shopping Experience

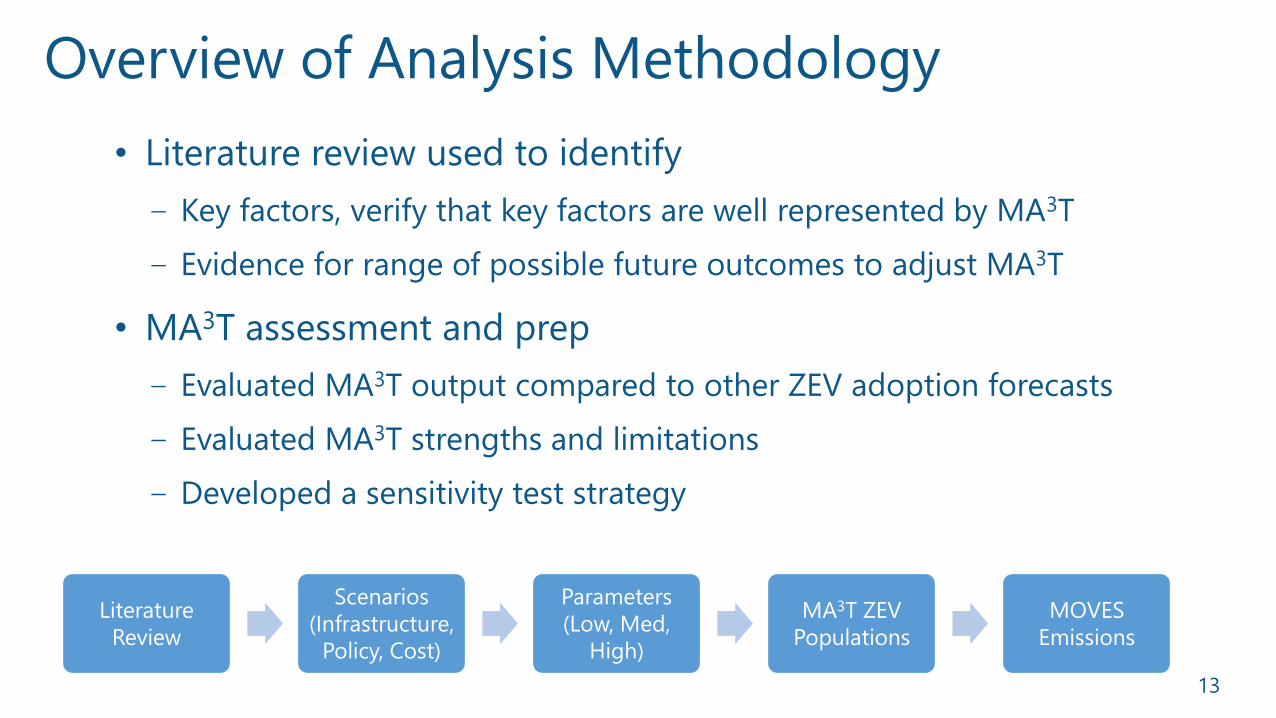

Overview of Analysis Methodology

13

• Literature review used to identify

‒ Key factors, verify that key factors are well represented by MA3T

‒ Evidence for range of possible future outcomes to adjust MA3T

• MA3T assessment and prep

‒ Evaluated MA3T output compared to other ZEV adoption forecasts

‒ Evaluated MA3T strengths and limitations

‒ Developed a sensitivity test strategy

Literature

Review

Scenarios

(Infrastructure,

Policy, Cost)

Parameters

(Low, Med,

High)

MA3T ZEV

Populations

MOVES

Emissions

MA3T Model Overview

14

• MA3T: Market Acceptance of

Advanced Automotive

Technologies model

• Consumer choice model; predicts

light-duty ATV sales, population,

and energy consumption

• Multiple input parameters on key factors affecting ATV adoption

• Calibrated to total light-duty vehicle sales data from the U.S. EIA’s

2019 Annual Energy Outlook (AEO) reference case

Transportation Energy Evolution Modeling (TEEM)

Program at ORNL (https://teem.ornl.gov/ma3t.shtml)

Charts developed with data from the 2019 Annual Energy Outlook (AEO) and MA3T 1515

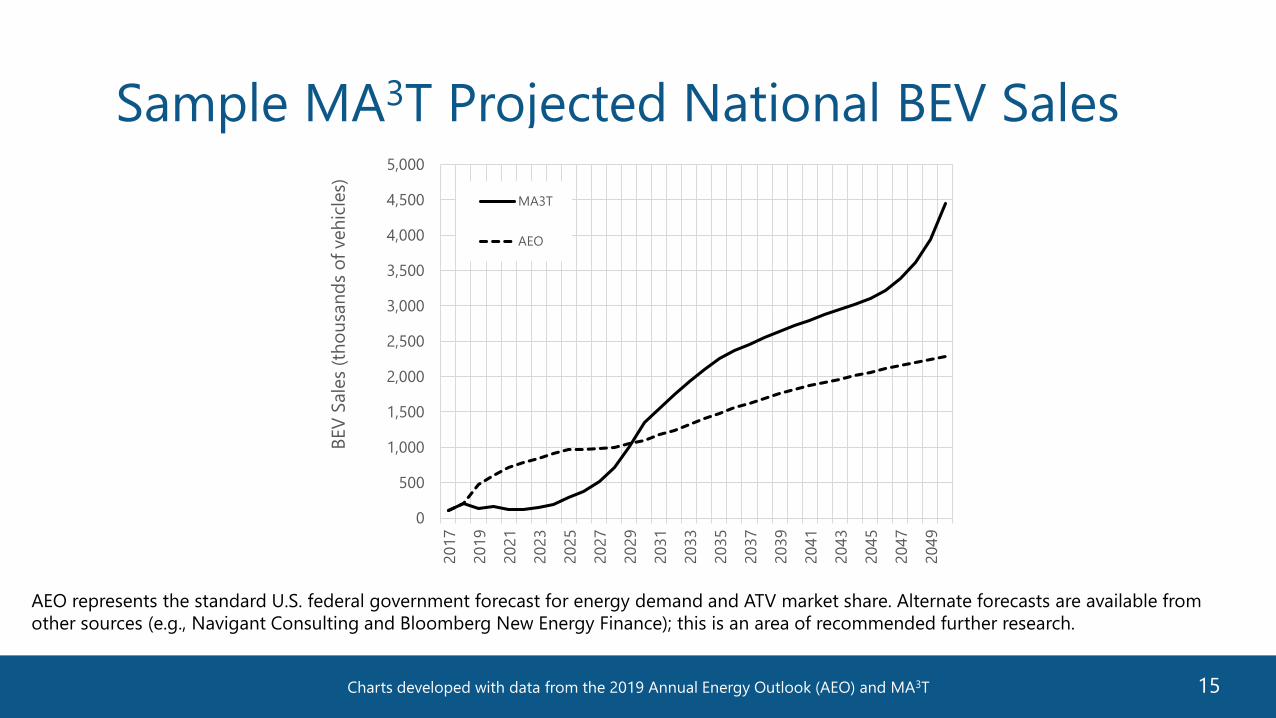

Sample MA3T Projected National BEV Sales

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

2037

2039

2041

2043

2045

2047

2049

BEV

Sale

s (t

ho

usa

nd

s o

f veh

icle

s)

MA3T

AEO

AEO represents the standard U.S. federal government forecast for energy demand and ATV market share. Alternate forecasts are available from

other sources (e.g., Navigant Consulting and Bloomberg New Energy Finance); this is an area of recommended further research.

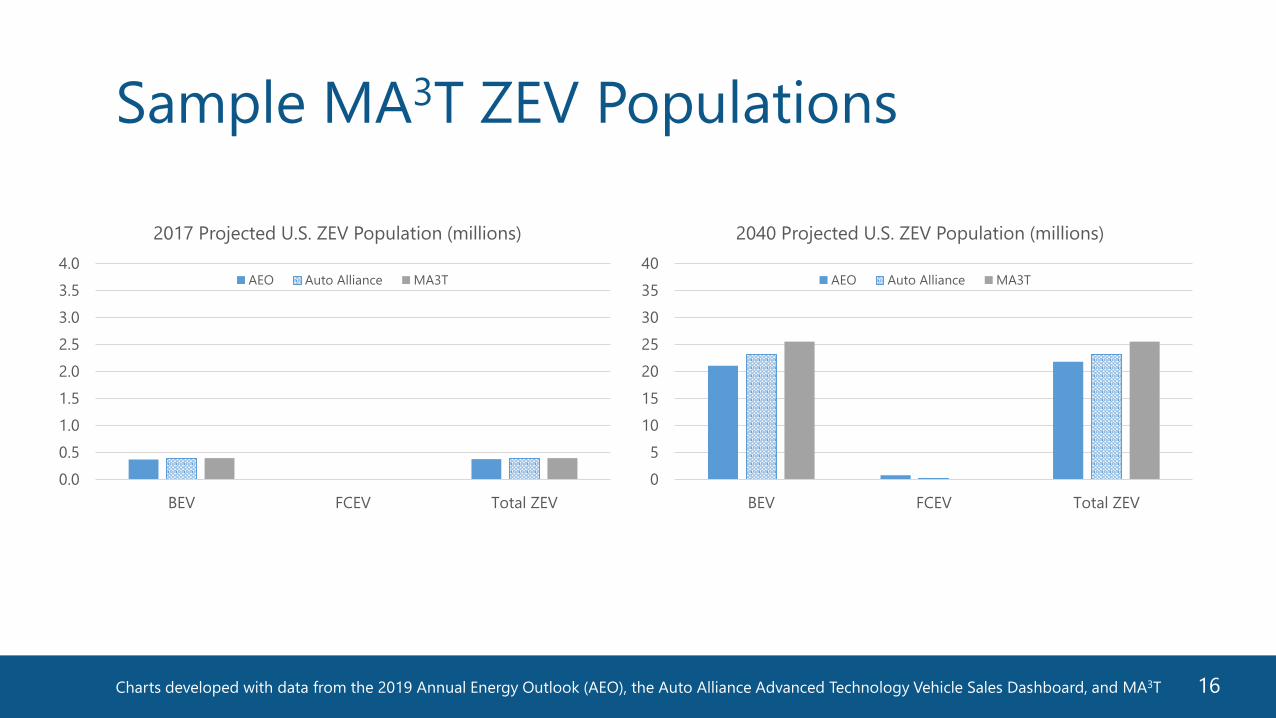

Charts developed with data from the 2019 Annual Energy Outlook (AEO), the Auto Alliance Advanced Technology Vehicle Sales Dashboard, and MA3T 1616

Sample MA3T ZEV Populations

0

5

10

15

20

25

30

35

40

BEV FCEV Total ZEV

2040 Projected U.S. ZEV Population (millions)

AEO Auto Alliance MA3T

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

BEV FCEV Total ZEV

2017 Projected U.S. ZEV Population (millions)

AEO Auto Alliance MA3T

Guiding Principles for Scenario Construction

17

• Include parameters that can be

adjusted using MA3T

• Reflect reviewed literature (drivers

and barriers)

• Represent areas that DOTs/MPOs

can practically influence

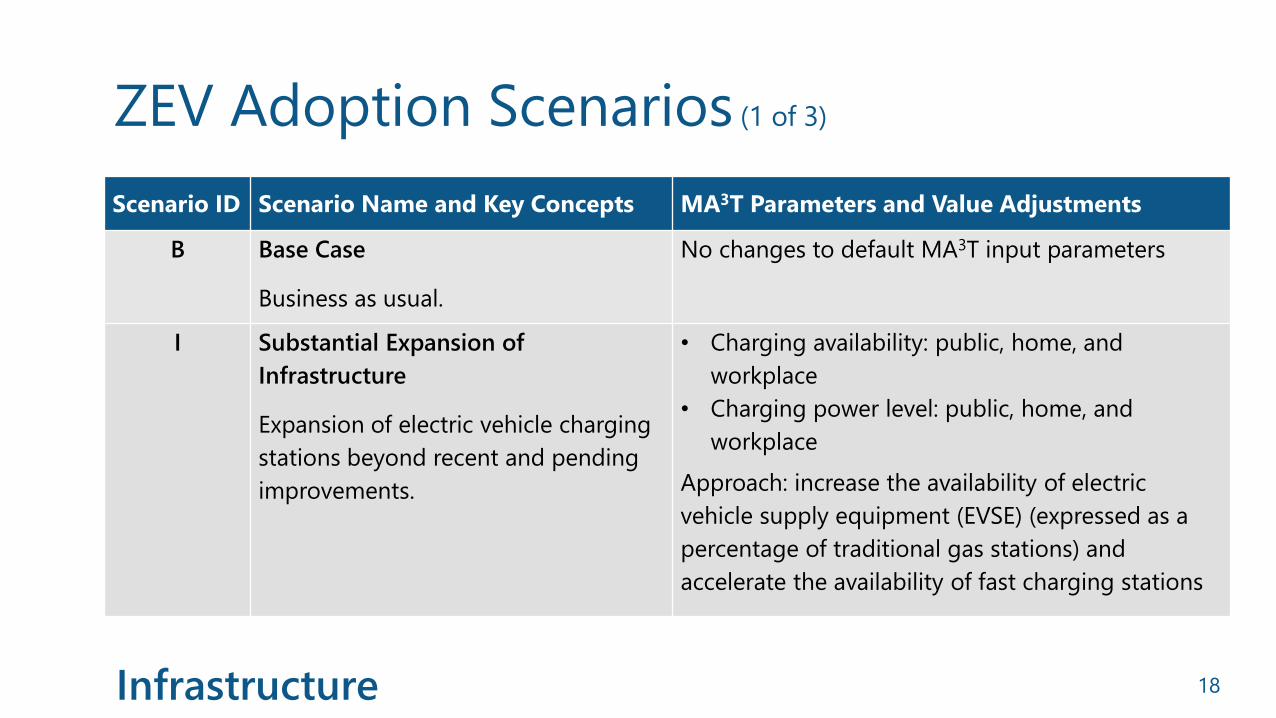

ZEV Adoption Scenarios (1 of 3)

18

Scenario ID Scenario Name and Key Concepts MA3T Parameters and Value Adjustments

B Base Case

Business as usual.

No changes to default MA3T input parameters

I Substantial Expansion of

Infrastructure

Expansion of electric vehicle charging

stations beyond recent and pending

improvements.

• Charging availability: public, home, and

workplace

• Charging power level: public, home, and

workplace

Approach: increase the availability of electric

vehicle supply equipment (EVSE) (expressed as a

percentage of traditional gas stations) and

accelerate the availability of fast charging stations

Infrastructure

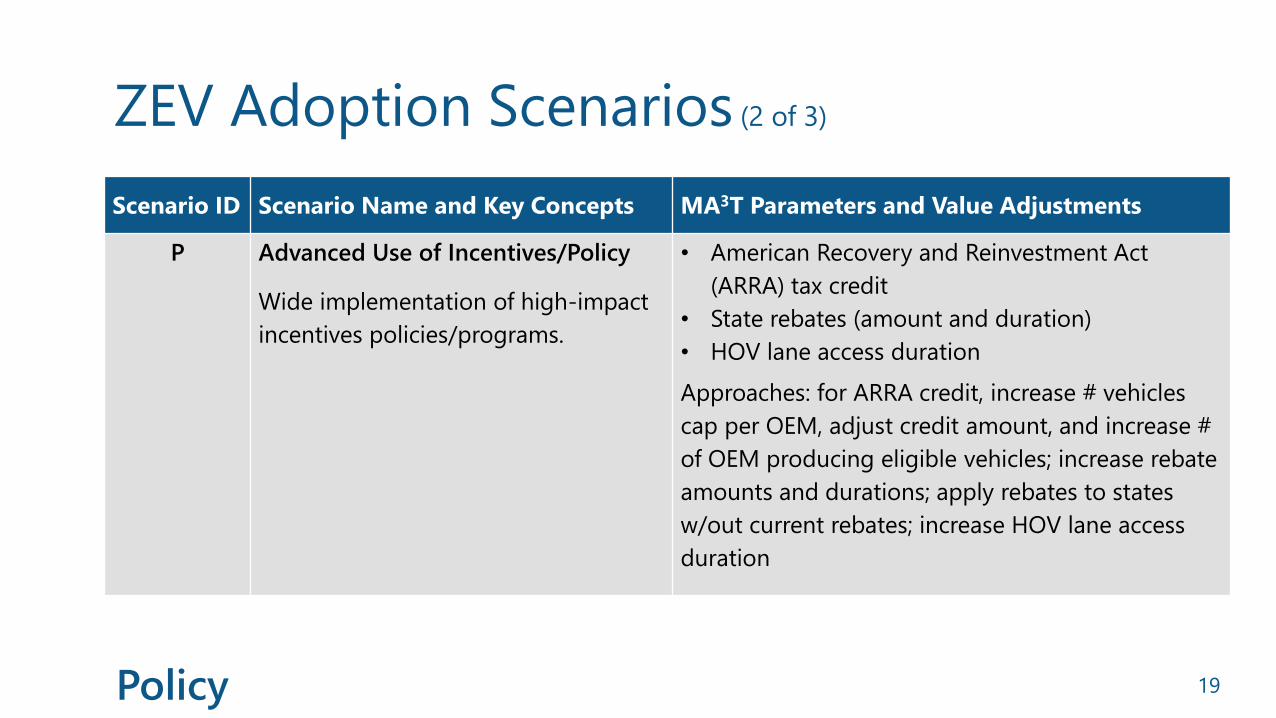

ZEV Adoption Scenarios (2 of 3)

19

Scenario ID Scenario Name and Key Concepts MA3T Parameters and Value Adjustments

P Advanced Use of Incentives/Policy

Wide implementation of high-impact

incentives policies/programs.

• American Recovery and Reinvestment Act

(ARRA) tax credit

• State rebates (amount and duration)

• HOV lane access duration

Approaches: for ARRA credit, increase # vehicles

cap per OEM, adjust credit amount, and increase #

of OEM producing eligible vehicles; increase rebate

amounts and durations; apply rebates to states

w/out current rebates; increase HOV lane access

duration

Policy

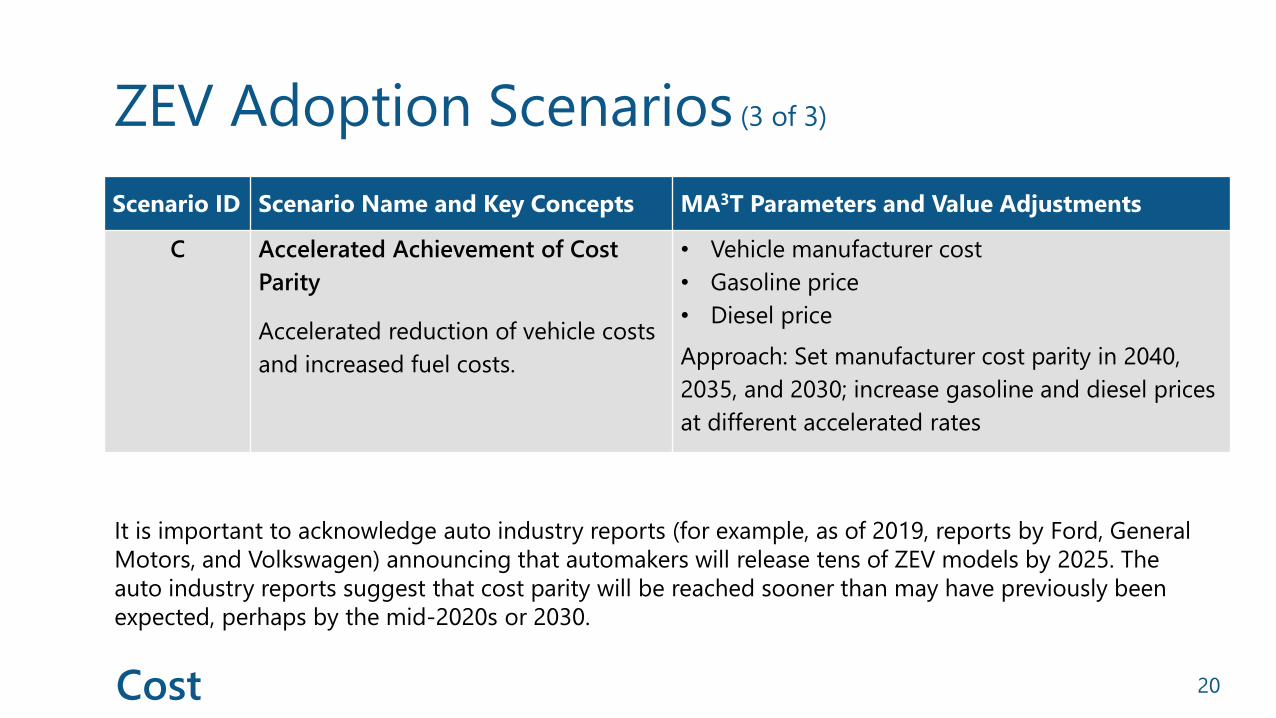

ZEV Adoption Scenarios (3 of 3)

20

Scenario ID Scenario Name and Key Concepts MA3T Parameters and Value Adjustments

C Accelerated Achievement of Cost

Parity

Accelerated reduction of vehicle costs

and increased fuel costs.

• Vehicle manufacturer cost

• Gasoline price

• Diesel price

Approach: Set manufacturer cost parity in 2040,

2035, and 2030; increase gasoline and diesel prices

at different accelerated rates

It is important to acknowledge auto industry reports (for example, as of 2019, reports by Ford, General

Motors, and Volkswagen) announcing that automakers will release tens of ZEV models by 2025. The

auto industry reports suggest that cost parity will be reached sooner than may have previously been

expected, perhaps by the mid-2020s or 2030.

Cost

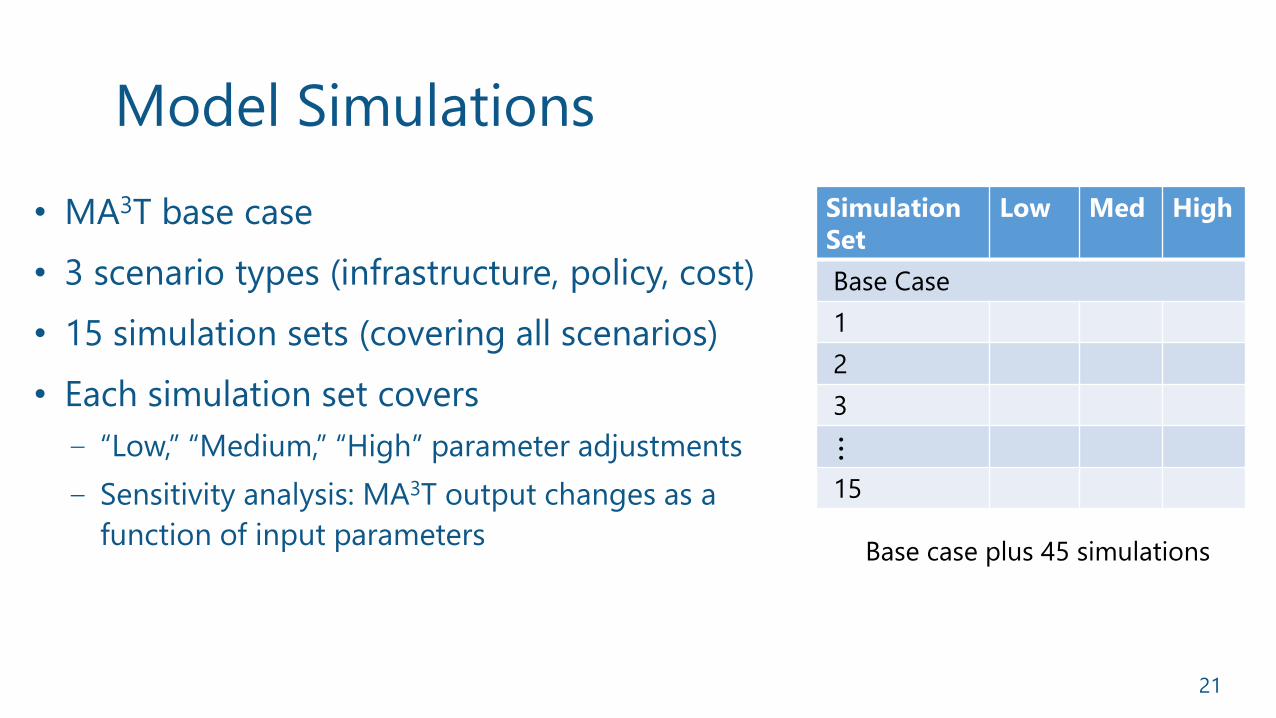

Model Simulations

21

• MA3T base case

• 3 scenario types (infrastructure, policy, cost)

• 15 simulation sets (covering all scenarios)

• Each simulation set covers

‒ “Low,” “Medium,” “High” parameter adjustments

‒ Sensitivity analysis: MA3T output changes as a

function of input parameters

Simulation

Set

Low Med High

Base Case

1

2

3…

15

Base case plus 45 simulations

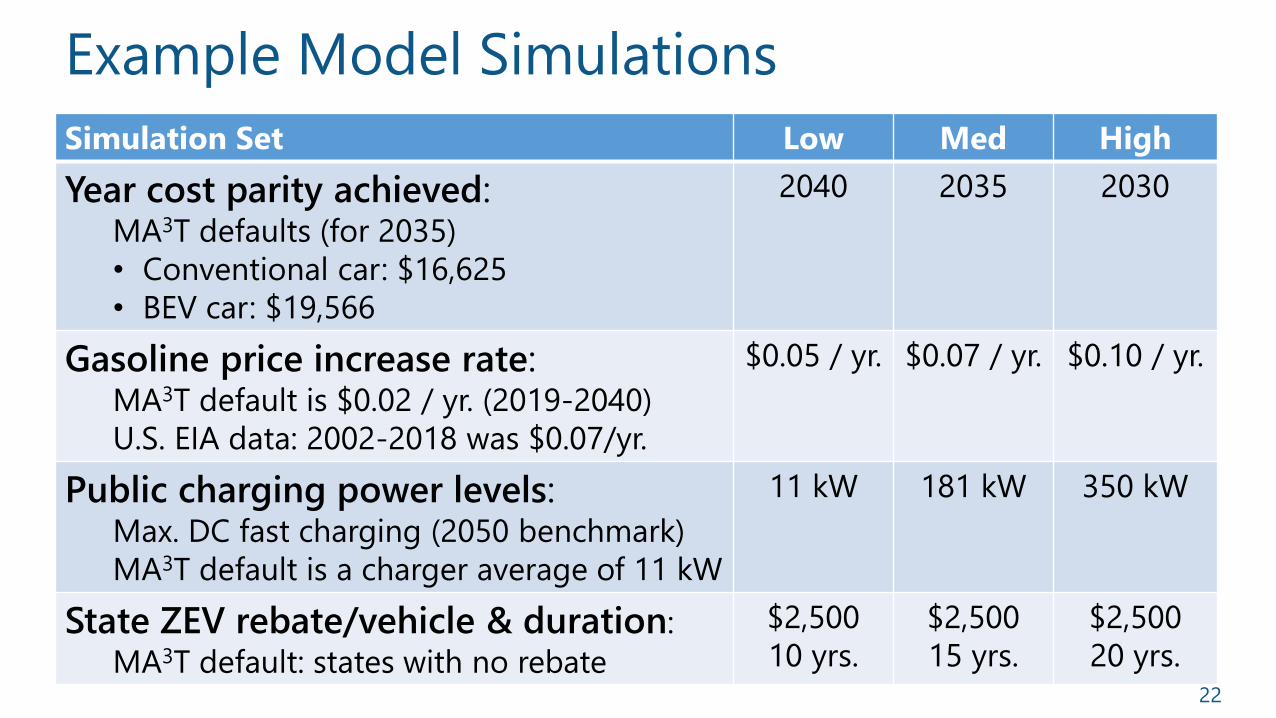

Example Model Simulations

22

Simulation Set Low Med High

Year cost parity achieved: MA3T defaults (for 2035)

• Conventional car: $16,625

• BEV car: $19,566

2040 2035 2030

Gasoline price increase rate:MA3T default is $0.02 / yr. (2019-2040)

U.S. EIA data: 2002-2018 was $0.07/yr.

$0.05 / yr. $0.07 / yr. $0.10 / yr.

Public charging power levels:Max. DC fast charging (2050 benchmark)

MA3T default is a charger average of 11 kW

11 kW 181 kW 350 kW

State ZEV rebate/vehicle & duration:

MA3T default: states with no rebate

$2,500

10 yrs.

$2,500

15 yrs.

$2,500

20 yrs.

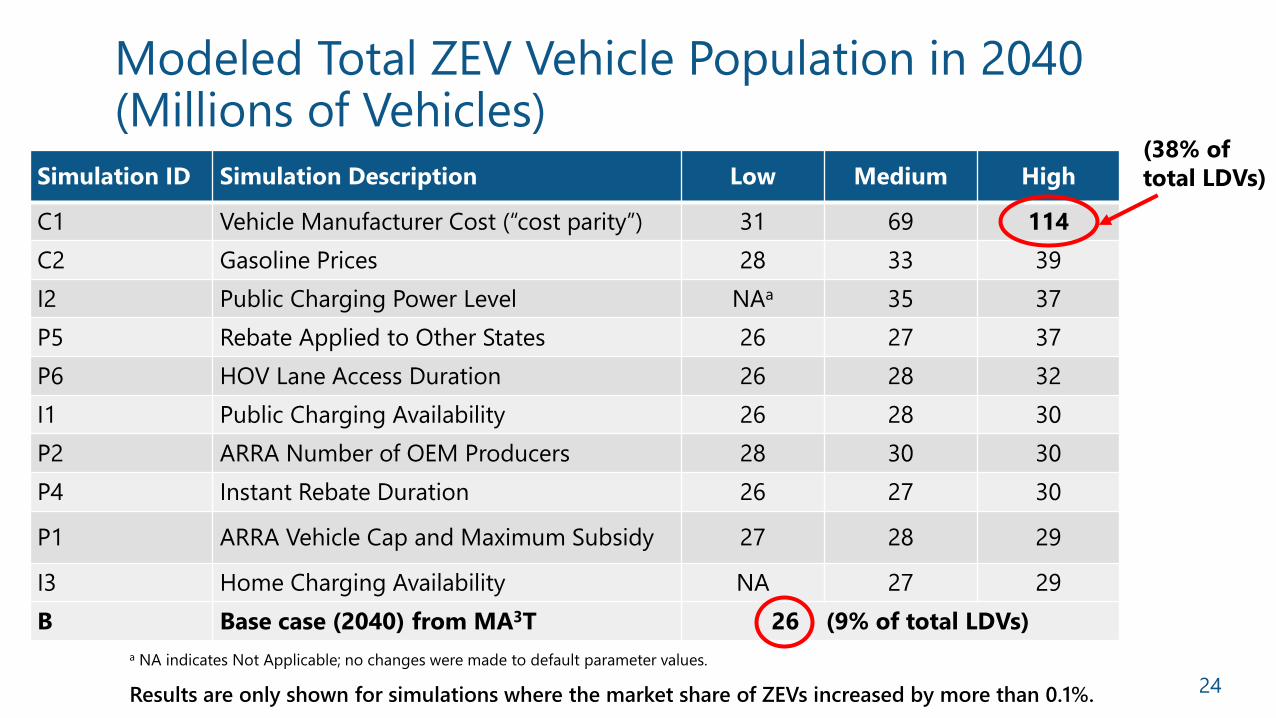

Results: Forecasted ZEV Populations

23

Modeled Total ZEV Vehicle Population in 2040 (Millions of Vehicles)

24

Simulation ID Simulation Description Low Medium High

C1 Vehicle Manufacturer Cost (“cost parity”) 31 69 114

C2 Gasoline Prices 28 33 39

I2 Public Charging Power Level NAa 35 37

P5 Rebate Applied to Other States 26 27 37

P6 HOV Lane Access Duration 26 28 32

I1 Public Charging Availability 26 28 30

P2 ARRA Number of OEM Producers 28 30 30

P4 Instant Rebate Duration 26 27 30

P1 ARRA Vehicle Cap and Maximum Subsidy 27 28 29

I3 Home Charging Availability NA 27 29

B Base case (2040) from MA3T 26 (9% of total LDVs)

a NA indicates Not Applicable; no changes were made to default parameter values.

Results are only shown for simulations where the market share of ZEVs increased by more than 0.1%.

(38% of

total LDVs)

Estimating Emissions for ZEV Scenarios

25

• Background and approach

‒ MA3T provides sales

(population), not emissions

‒ MOVES used to

• Estimate national default activity

• Derive g/mi (running exhaust),

g/start emission factors

‒ Emissions calculated for each

simulation (base + 45)

Image source: EPA, https://www.epa.gov/moves• Outcomes

‒ National level results

‒ Scalable to fleets similar to national average LDV composition

Assumptions for Calculating Emissions for Each ZEV Adoption Simulation

26

• Estimate emissions from on-road start and

running exhaust

‒ No tire or brake wear emissions

‒ No electric power generation emissions

• Focus: conventional vehicle populations

• Example

‒ Simulation 1: 9 conventional vehicles and 1 ZEV

‒ Simulation 2: 6 conventional vehicles and 4 ZEVs Analysis focus: exhaust emissions

27

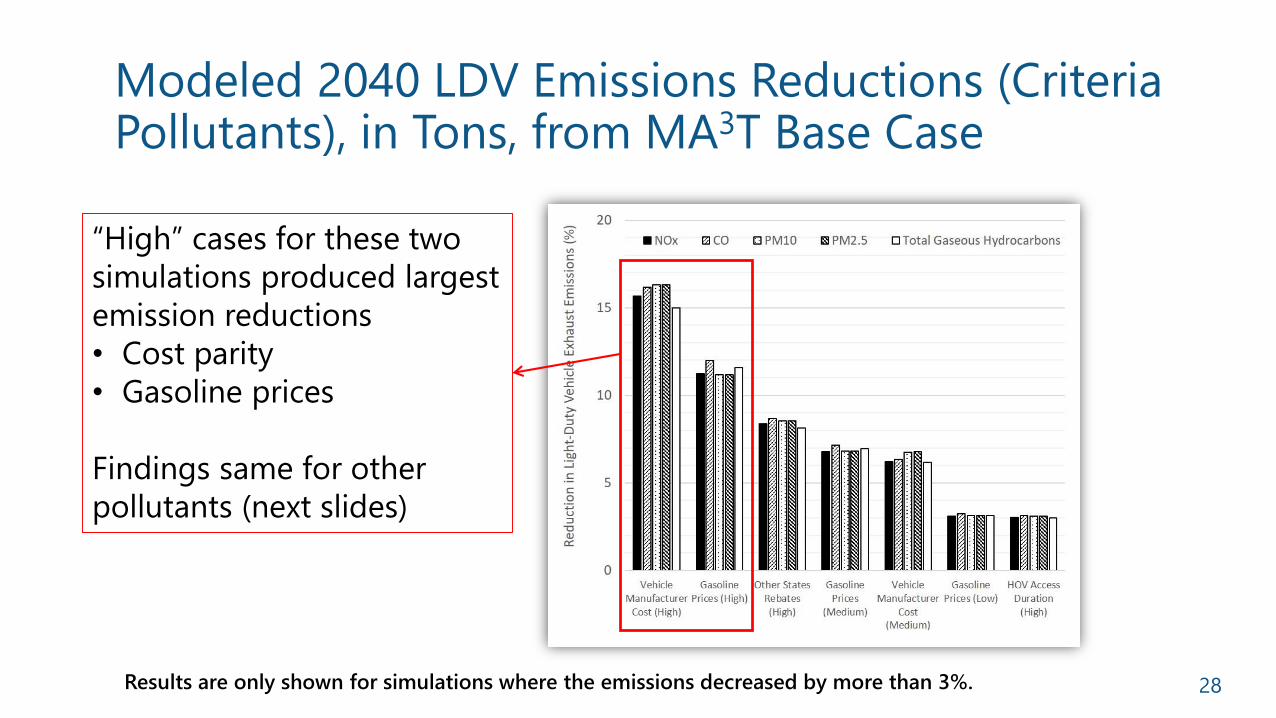

Results: Forecasted Emissions Reductions

Modeled 2040 LDV Emissions Reductions (Criteria Pollutants), in Tons, from MA3T Base Case

28Results are only shown for simulations where the emissions decreased by more than 3%.

“High” cases for these two

simulations produced largest

emission reductions

• Cost parity

• Gasoline prices

Findings same for other

pollutants (next slides)

/

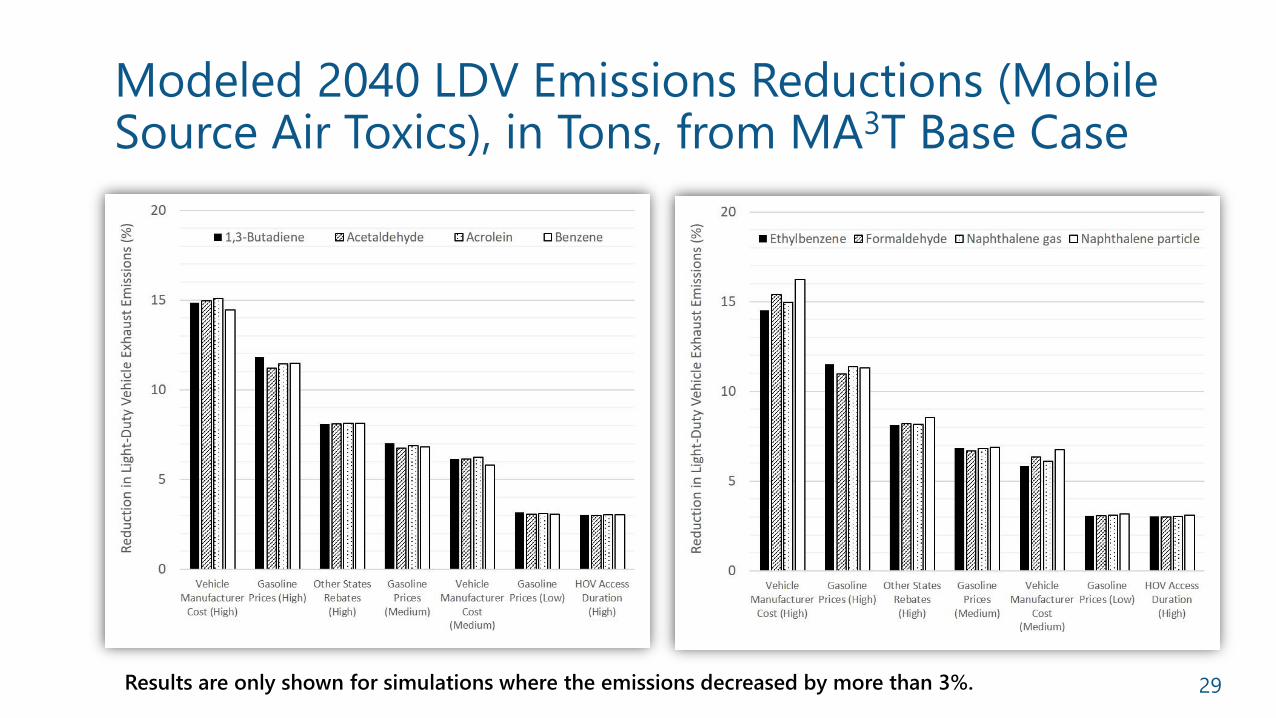

Modeled 2040 LDV Emissions Reductions (Mobile Source Air Toxics), in Tons, from MA3T Base Case

29Results are only shown for simulations where the emissions decreased by more than 3%.

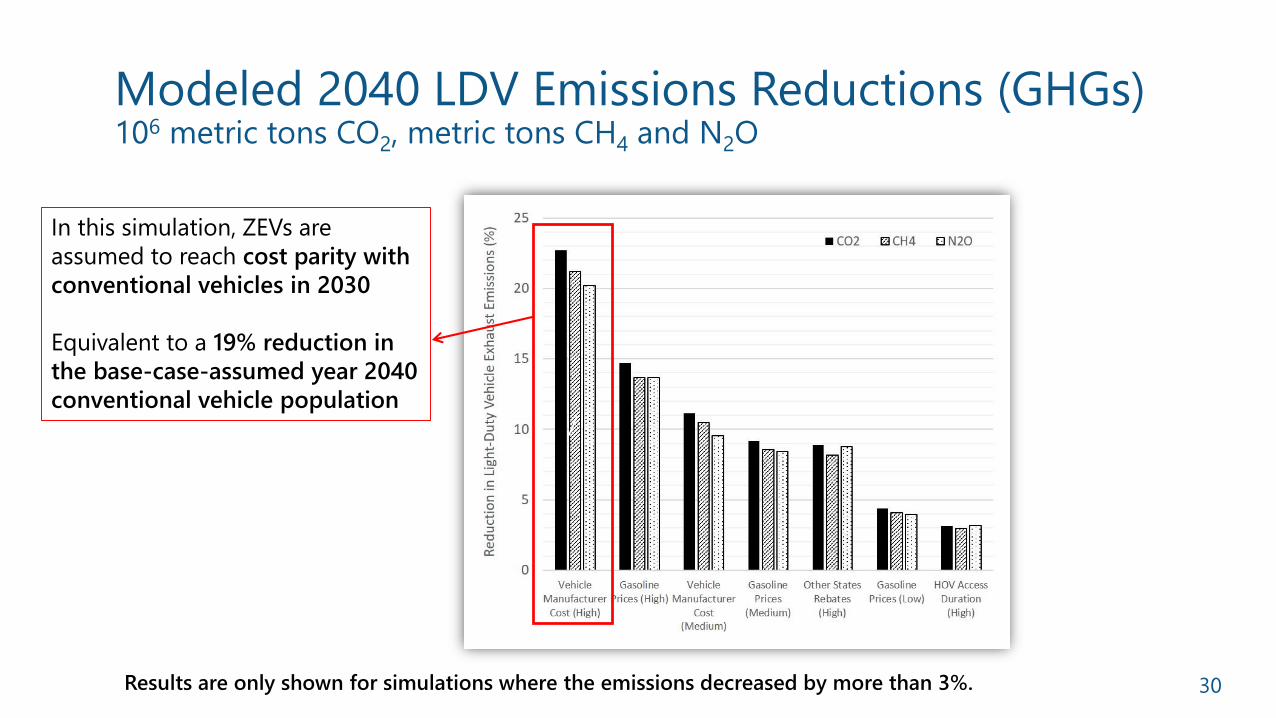

Modeled 2040 LDV Emissions Reductions (GHGs) 106 metric tons CO2, metric tons CH4 and N2O

30Results are only shown for simulations where the emissions decreased by more than 3%.

/

In this simulation, ZEVs are

assumed to reach cost parity with

conventional vehicles in 2030

Equivalent to a 19% reduction in

the base-case-assumed year 2040

conventional vehicle population

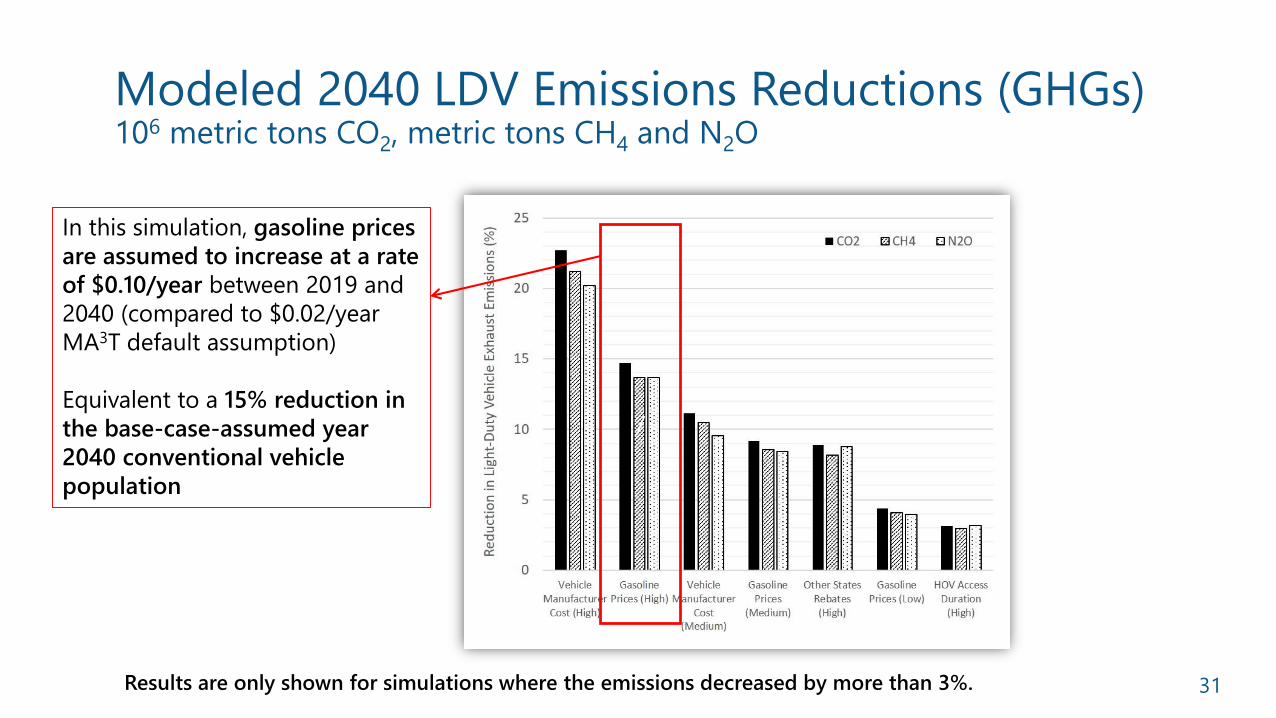

Modeled 2040 LDV Emissions Reductions (GHGs) 106 metric tons CO2, metric tons CH4 and N2O

31Results are only shown for simulations where the emissions decreased by more than 3%.

/

In this simulation, gasoline prices

are assumed to increase at a rate

of $0.10/year between 2019 and

2040 (compared to $0.02/year

MA3T default assumption)

Equivalent to a 15% reduction in

the base-case-assumed year

2040 conventional vehicle

population

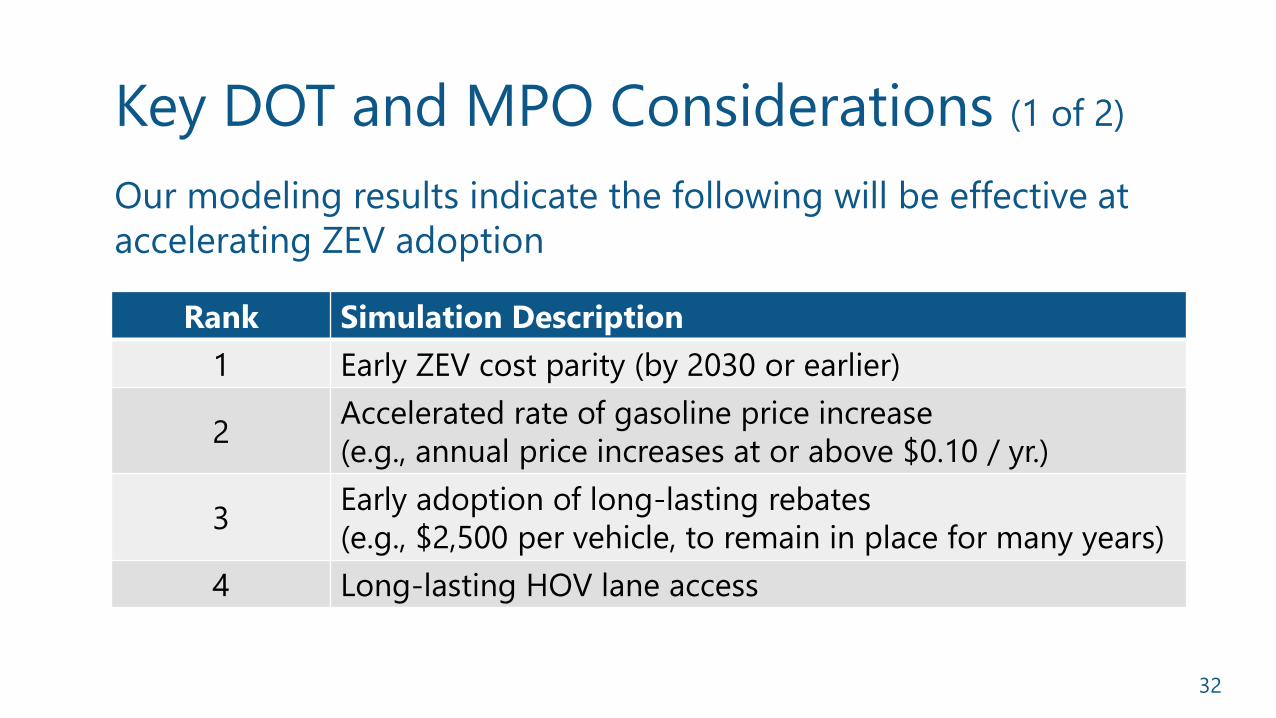

Key DOT and MPO Considerations (1 of 2)

32

Our modeling results indicate the following will be effective at

accelerating ZEV adoption

Rank Simulation Description

1 Early ZEV cost parity (by 2030 or earlier)

2Accelerated rate of gasoline price increase

(e.g., annual price increases at or above $0.10 / yr.)

3Early adoption of long-lasting rebates

(e.g., $2,500 per vehicle, to remain in place for many years)

4 Long-lasting HOV lane access

33

Potential actions might be taken independently

or require collaboration with other agencies

• Reduce ZEV cost (e.g., manufacturer incentives)

• Increase gasoline prices (gas taxes) and non-ZEV

registration fees

• Implement rebate programs

• Provide long-duration HOV lane access

• Expand locations and power of ZEV charging

infrastructure

• Increase consumer awareness and educationImage source: cleanvehiclerebate.org

Key DOT and MPO Considerations (2 of 2)

34

MA3T-focused General ZEV research

Suggestions for Future Research (1 of 7)

35

MA3T-focused R&D needs:

• Need: Assess, modify (if needed) MA3T

calibration; calibration is now to U.S. EIA AEO.

Others, e.g., Navigant Consulting, Bloomberg,

project greater ZEV adoption

• Benefit: Enhances MA3T by reflecting multiple

(“weight of evidence”) data sources

• Need: Manufacturer cost differences by ZEV

size classes

• Benefit: Improves MA3T as more large-class

ZEVs enter market

Suggestions for Future Research (2 of 7)

Suggestions for Future Research (3 of 7)

36

MA3T-focused R&D needs:

• Need: Enable users to more easily

forecast FCEV market penetration by

specifying FCEV entry year on the

market and availability of H2

refueling infrastructure (framework

exists, but input values are null by

default); AEO forecast is also

conservative

• Benefit: FCEV technology and

infrastructure are likely to change

over next 20+ years; MA3T updates

will facilitate FCEV analysis

Image source: U.S. DOE, Fuel Cell

Technologies Market Report 2016

Suggestions for Future Research (4 of 7)

37

MA3T-focused R&D needs:

• Need: Enable inflation-adjusted valuations

• Benefit: Will enable users to adjust inflation rates and sensitivity test outcomes;

Currently, MA3T uses 2018 dollars for costs, prices, tax credits and rebates

38

General ZEV research needs

• Need: Continuously assess public

education’s influence; response may

change with “normalization” of ZEVs

Research:

‒ HOV access

‒ Home charging availability

‒ Range anxiety

• Benefit: Education may become

increasingly cost-effective if, as ZEVs

become commonplace, consumer

demand increases

Image source: Electrify America National ZEV

Investment Plan: Cycle 2, Public Version, 2019

Suggestions for Future Research (5 of 7)

39

General ZEV research needs

• Need: ZEV-friendly revenue generating

mechanisms to replace lost gasoline tax revenue

• Benefit: Avoids increasing the effective cost of

ZEVs and potentially slowing the growth of ZEVs

• Need: Options to accelerate truck fleet

electrification

• Benefit: Medium- and heavy-duty vehicles

contribute nearly one quarter of GHG emissions

from the U.S. transportation sector

Suggestions for Future Research (6 of 7)

40

General ZEV research needs

• Need: Integrated research to promote

simultaneous de-carbonization of

electric power production and

electrification of on-road fleet

• Benefit: As ZEVs become increasingly

commonplace, the change in emissions

associated with electric vehicles will

increasingly be driven at the grid levelImage source: US EIA, Alternative Fuels Data Center,

https://afdc.energy.gov/vehicles/electric_emissions.html

Suggestions for Future Research (7 of 7)

Summary Implications and Suggestions

41

Research Implications

• Cost parity is most important factor to encourage ZEVs and reduce emissions

• Other factors that lead to adoption: increased gasoline prices, increased availability and power of charging facilities, long-duration ZEV purchase rebates

• Education programs also have promise as low-cost actions

Research Needs

• MA3T: Consider alternative ZEV penetration forecasts and electrification of larger vehicle types

• General: Ongoing research to assess changes in consumer preferences with “normalization” of ZEVs

• General: Policies that support ZEVs while easing financial loss of gas tax revenues

For More Information

42

Task 115: Estimates of Emissions Reductions from Future Fleet Changes for

Use in Air Quality Models:

https://apps.trb.org/cmsfeed/TRBNetProjectDisplay.asp?ProjectID=4485

Garnet Erdakos [email protected]

Changsy Chang [email protected]

Adrienne Heller [email protected]

Doug Eisinger [email protected]

Zhenhong Lin [email protected]

#TRBwebinar

Adrienne [email protected]

Doug Eisinger [email protected]

Garnet [email protected]

Shih Ying Chang (Changsy)[email protected]

Zhenhong [email protected] Ridge National Laboratory

Get Involved with TRB

#TRBwebinar

Receive emails about upcoming TRB webinarshttps://bit.ly/TRBemails

Find upcoming conferenceshttp://www.trb.org/Calendar

Get Involved with TRB

Be a Friend of a Committee bit.ly/TRBcommittees– Networking opportunities

– May provide a path to Standing Committee membership

Join a Standing Committee bit.ly/TRBstandingcommittee

Work with CRP https://bit.ly/TRB-crp

Update your information www.mytrb.org

#TRBwebinar

Getting involved is free!

#TRB100

![[XLS] - Mar15/District Reasi new proforma... · Web view2035 2300 2036 2300 2037 2300 2038 2300 2039 2300 2040 2300 2041 2300 2042 2300 2043 2300 2044 2300 2045 2300 2046 2300 2047](https://static.documents.pub/doc/80x56/5aa68dbc7f8b9a517d8ea409/xls-mar15district-reasi-new-proformaweb-view2035-2300-2036-2300-2037-2300.jpg)