49

FOREIGN ACCOUNT TAX COMPLIANCE ACT CONFERENCE MAY 2013 The Latest Updates BDO TAX & ACCOUNTING 2013

FOREIGN ACCOUNT TAX COMPLIANCE ACT CONFERENCE MAY 2013

The Latest Updates

BDO TAX & ACCOUNTING

2013

WELCOME TO BDO FATCA CONFERENCE

BDO SPEAKERS GERDY ROOSE – BDO Lead Tax Partner

SYLVIE MAESTRI – BDO FATCA Tax Lead

GUEST SPEAKER FREDERIC BATARDY – KBL European Private Bankers S.A.

Chairman of ABBL US Tax issues Working Group

Chairman of EBF US Tax issues Working Group

FATCA

BDO FATCA Conference - 28 May 2013 Page 3

AGENDA

BDO FATCA Conference - 28 May 2013 Page 4

TOPICS

INTRODUCTION

RECENT DEVELOPMENTS

OPERATIONAL ASPECTS

REGISTRATION PROCESS

Q&A SESSION

INTRODUCTION Gerdy Roose

INTRODUCTION Why FATCA?

• New reporting enacted by the US to combat tax evasion by US tax payers

• Improve tax compliance of non-US entities with substantial US ownership and specified US persons by strengthening due diligence and reporting obligations

• Additional US compliance obligations on top of existing QI obligations

• 30% punitive tax applicable in case of non-compliance on US source payments made to NPFFIs and other non compliant passive NFFEs (Final Regs)

• Generally speaking, FFIs must enter into an agreement / register with the IRS

BDO FATCA Conference - 28 May 2013 Page 6

INTRODUCTION Key Objectives and Features of FATCA • Projected to raise $7.6 billion in tax revenue over a 10 year period

• Requires FFIs to enter into compliance agreements with US Treasury and to identify and report on US financial accounts annually

• Requires Passive NFFEs to disclose substantial US owners or to certify that they have no US ownership, have an active business or are publicly traded

• Requires FFIs (<> IGA I FFI) to withhold on passthru payments to recalcitrant account holders

BDO FATCA Conference - 28 May 2013 Page 7

INTRODUCTION Political Environment • FATCA has moved from a pure US initiated reporting law to a global initiative on tax reporting.

• 4 IGAs have been signed (i.e. officially disclosed)

• The US is now engaged in discussion and negotiation with more than 75 countries (e.g. Russia, India, Cayman Islands, Singapore, BVI)

• Intergovernmental Agreements (“IGA”) are negotiated into order to facilitate the implementation of the FATCA. They contain the same broad principles, especially in the area of income tax withholding. However, there are significant differences with respect to the tax information reporting, registration requirements with the IRS, account due diligence and information exchange

• There are two versions of the model agreement, IGA 1 (which includes a reciprocal version and a nonreciprocal version) and IGA 2

• Model I FFIs must be compliant with local laws and not with Final Regs. Model II FFIs have to comply with Final Regs except otherwise provided by the IGA. Co-existence of 3 different versions of IGAs & Annexes models (old, hybrid and new models)

BDO FATCA Conference - 28 May 2013 Page 8

INTRODUCTION Political Environment (Cont’d) • US Treasury and OECD are working together in order to elaborate a unique exchange of information

tool i.e. TRACE

• IGA framework is a stepping stone to global automatic information exchange!

• UK FATCA: Tax reporting to the UK (e.g. Guernsey, Jersey, Isle of Man, Bermuda)

• Pilot project between UK, France, Germany, Italy, Spain, Netherlands, Belgium, Poland, Romania

BDO FATCA Conference - 28 May 2013 Page 9

INTRODUCTION Next Steps

“In the context of its FATCA negotiations with the United States of America, Luxembourg has chosen the Model I which will provide automatic exchange of information between the Luxembourg and American fiscal authorities on bank accounts held in Luxembourg by citizens and residents of the United States.

This decision will put Luxembourg’s relations with the US in line with the declaration of 10 April 2013 by which Luxembourg announced that it will introduce, on 1 January 2015 and within the scope of the 2003 EU Savings Directive, the automatic exchange of information within the European Union.

Luxembourg wishes to see the same conditions apply to all competing financial centers and to see the automatic exchange of information accepted as the international standard. It has therefore agreed on 14 may 2013 to grant the European Commission a mandate to negotiate with Switzerland, Liechtenstein, Andorra, Monaco and San Marino”

http://www.mf.public.lu/actualites/2013/05/facta_210513/index.html

BDO FATCA Conference - 28 May 2013 Page 10

INTRODUCTION Poll question

Who is in favor of Model I?

Who is in favor of Model II?

BDO FATCA Conference - 28 May 2013 Page 11

INTRODUCTION Why an IGA I is a good thing for a Luxembourg FI?

ADVANTAGES

• Legal certainty

- Reporting towards Luxembourg Tax Authorities

- Domestic legislation

- Not bound by an extra-territorial agreement/obligations

• No withholding tax obligations

• No account closure obligations

• Soften “Responsible Officer” responsibilities

BDO FATCA Conference - 28 May 2013 Page 12

More safety More simplicity Less expensive er

RECENT DEVELOPMENTS Frederic Batardy

RECENT DEVELOPMENTS FATCA Final Regulations • The FATCA Final Regulations (~500 pages) have been released on 17/01/2013

• Final Regulations have clarified a number of topics

- Certain account identification and due diligence rules have been relaxed

- Rules on withholding on grandfathered obligations have been expanded

- Transition rule pertaining to Limited affiliates and branches has been maintained

- Definitions of certain Deemed Compliant stati for FFIs and Investment Entities have been

changed

- FFI Agreement has been included in the core text of the Regulations

BDO FATCA Conference - 28 May 2013 Page 14

RECENT DEVELOPMENTS FATCA Final Regulations • Technical corrections are still needed and expected to be published in corrective notices

• Certain topics have been reserved and will be published in separate Proc. Regs

• Generally speaking Treasury has taken into accounts comments made by the Financial Sector

BDO FATCA Conference - 28 May 2013 Page 15

INTERGOVERNMENTAL AGREEMENTS (IGA) IGAs vs. Treasury Regulations

BDO FATCA Conference - 28 May 2013 Page 16

• FATCA essentially becomes

domestic legislation administered by local tax authority

• No FFI Agreement but IRS registration only

• Final Regs only applicable to the extent expressly mentioned in IGA

• Interpretative authority of local legislator

• Country-specific Deemed Compliant stati in Annex II

• No withholding • No closing of accounts • No Responsible Officer • Reporting to local tax authority

Model 1 IGA

•Contractual Agreements between FFI and IRS •Full application of Regulations (500 pages) •No Annex II Deemed Compliant stati or exempt accounts •Withholding •Closing of accounts •Responsible Officer Certifications •Direct reporting to IRS

Treasury Regulations

• Contractual Agreements between FFI and IRS

• Full application of Final Regs (500 pages) unless IGA (30 pages) provides otherwise

• No withholding • No closing of accounts • Responsible Officer Certifications • Direct reporting to IRS under new

OECD “Group Request Model”

Model 2 IGA

LUXEMBOURG POSITION Where do we stand? • Minister of Finance has confirmed on May 21, 2013 that Luxembourg will enter into an IGA ModeI I

Agreement

– Decision in line with announcement made at ECOFIN on April 10, 2013 to apply automatic Exchange of Information under EU Savings Directive (EC 2003/48) starting January 1, 2015

– Both decisions have to be seen in conjunction with most favored nation clause in Art. 19 of the Council Directive 2011/16/EU of 15 February 2011 on administrative cooperation in the field of taxation and repealing Directive 77/799/EEC

• Negotiations between Luxembourg and US Treasury are in progress and cover i.a.

– Country-specific contents to be included in Annex II

• Negotiators aim to conclude negotiations by the summer in order to

– Bring the draft law before parliament in the Fall, and

– Ensure its enactment before the end of the year

BDO FATCA Conference - 28 May 2013 Page 17

TEMPLATES MODEL 1 IGA Annexes I & II - General Comments

As negotiations are under way and the contents of both Annexes are not publicly available yet, this presentation will reflect

the contents of the Templates as they have been posted by the US Treasury on its website on May 9, 2013

• Annex I

– Deals in more general terms with the due diligence requirements that have to be performed by FFIs under their respective IGAs

– Has been aligned to the requirements published in final Regs

– Does not as a matter of principle provide for the possibility of material changes under IGAs

• Annex II

– Is country-specific and allows for inclusions of entities and products that are not covered by Regs

– New Annex II aims at reducing the necessity to include country-specific entities and products

BDO FATCA Conference - 28 May 2013 Page 18

TEMPLATE MODEL 1 IGA Annex I APPLICABLE TO REPORTING FI

• Details due diligence requirements that have to be fulfilled for the identification of reportable vs. non-reportable accounts

- Type of documentation that can be used (i.a.)

- Self-certification (foreign status or US status), documentary evidence, GIINs, etc

- Non-US passport and a copy of US loss of nationality or reason why the account holder did not obtain

US citizenship at birth (in case of US place of birth)

- Special rules for QIs

- QIs will be able to rely on documentation obtained for the purpose of QI Agreement

- Due Diligence of QIs will thus be limited to Relationship Manager Enquiry

BDO FATCA Conference - 28 May 2013 Page 19

TEMPLATE MODEL 1 IGA Annex II ONLY APPLICABLE TO NON REPORTING FI (I.E. EXEMPT BO & CERTIFIED DEEMED COMPLIANT FFI)

• Exempt Beneficial Owners other than Funds

– Government Entity, International Organization, Central Bank

– Funds that qualify as Exempt Beneficial Owners

- Treaty-Qualified Retirement Fund, Broad Participation Retirement Fund, Narrow Participation

Retirement Fund, Pension Fund of an Exempt Beneficial Owner, Investment Entity wholly owned by

Exempt Beneficial Owners

• Deemed Compliant FFIs

– Small or Limited Scope FI that qualify as DCFFI

– FI with a Local Client Base, Local Bank, FI with Low Value Account, Qualified Credit Card Issuer

– Investment Entity that Qualify as DCFFI and other Special Rules

• The Annex II is different for Model I IGA and Model II IGA

BDO FATCA Conference - 28 May 2013 Page 20

?

TEMPLATE MODEL 1 IGA Annex II - CDCFFI

BDO FATCA Conference - 28 May 2013 Page 21

REQUIREMENTS FOR FI WITH A LOCAL CLIENT BASE

Licensed and regulated in Luxembourg as Financial Institution

No fixed place of business outside country of incorporation

Does not solicit account holders outside of country of incorporation (Website restrictions)

Required by local laws

To perform certain information reporting / withholding obligations with respect to resident accounts or

To apply due diligence requirements to resident accounts

98% of accounts (individual or entity accounts) by value must be held by residents in Luxembourg or other EU countries

?

TEMPLATE MODEL 1 IGA Annex II - CDCFFI

BDO FATCA Conference - 28 May 2013 Page 22

REQUIREMENTS FOR FI WITH A LOCAL CLIENT BASE (CONT’D)

Implement policies and procedures to ensure that it does not open or maintain accounts for NPFFI and monitor whether Financial Account are only held for non-resident Specified US Person or Passive NFFE with Controlling US residents / non-resident US citizens

Review and monitor Specified US Person and Controlling Persons resident status

Review and monitor FFI status

Close or Report any identified non resident US and NPFFI accounts (as if Reporting FI)

Follow registration requirements

If part of Expanded Affiliated Group, each entity must be

Incorporated or organised in the same country

A local FI itself

No discriminating policies or procedures against opening or maintaining accounts for individuals who are specified US persons and who are local residents

?

TEMPLATE MODEL 1 IGA Annex II

BDO FATCA Conference - 28 May 2013 Page 23

REQUIREMENTS FOR INVESTMENT ADVISORS & MANAGERS

Investment Entity

Sole activity is

To render investment advice to and act on behalf of a customer, or

To manage portfolios for a customer based on a power of attorney or similar instrument issued by the holder of a financial account, or based on investment powers in a directorship capacity for the purpose of investing, managing, or administering funds deposited in the name of the person or Entity granting the power or issuing the similar instrument with a FI other than a NPFFI

?

TEMPLATE MODEL 1 IGA Annex II - CDCFFI

BDO FATCA Conference - 28 May 2013 Page 24

REQUIREMENTS FOR COLLECTIVE INVESTMENT VEHICLES

Investment Entity

Regulated as a Collective Investment Vehicle in the country where it is established

All of the interests in the CIV (incl. debt interest in excess of $ 50.000) are held by or through

Exempt Beneficial Owners

Active NFFEs

US person other than Specified US person

Financial Institutions other than NPFFI

Issuance of Bearer Certificates forbidden as of 01/01/2013 and forced redemption/immobilization of all outstanding certificates before 01/01/2017 by applying Annex I requirements

?

INTRODUCTION Open Questions • Final Regulations

– Interaction between QI and FATCA rules

– Registration

• IGA

– Refers to the existence of a DTT / TIEA. What impact for Luxembourg as amended US–LUX DTA not ratified by USA?

• Annex II

– Entities and products that will be covered still unknown

– What happened to “Restricted Funds” and other “Deemed Compliant” stati that are available under Final Regulations but have not been included in Template ?

• Scope and content of implementing local legislation

BDO FATCA Conference - 28 May 2013 Page 25

OPERATIONAL ASPECTS Sylvie Maestri

GENERAL UPDATE ‘‘The IRS will still evaluate the information it gets from a jurisdiction’s

FFI. It will also receive information from US taxpayers about the taxpayers’ foreign accounts. So the IRS will have different sources of

information it can use to match up and see if there are any issues with an FFI’s reporting.”

Michael Plowgian

Senior Advisor OECD

BDO FATCA Conference - 28 May 2013 Page 27

OPERATIONAL ASPECTS Process

Communication Plan

Due Diligence & Remediation

Process

Withholding?

Monitoring & Verification

Reporting

Identification Classification

Entity Status

Determination

Registration

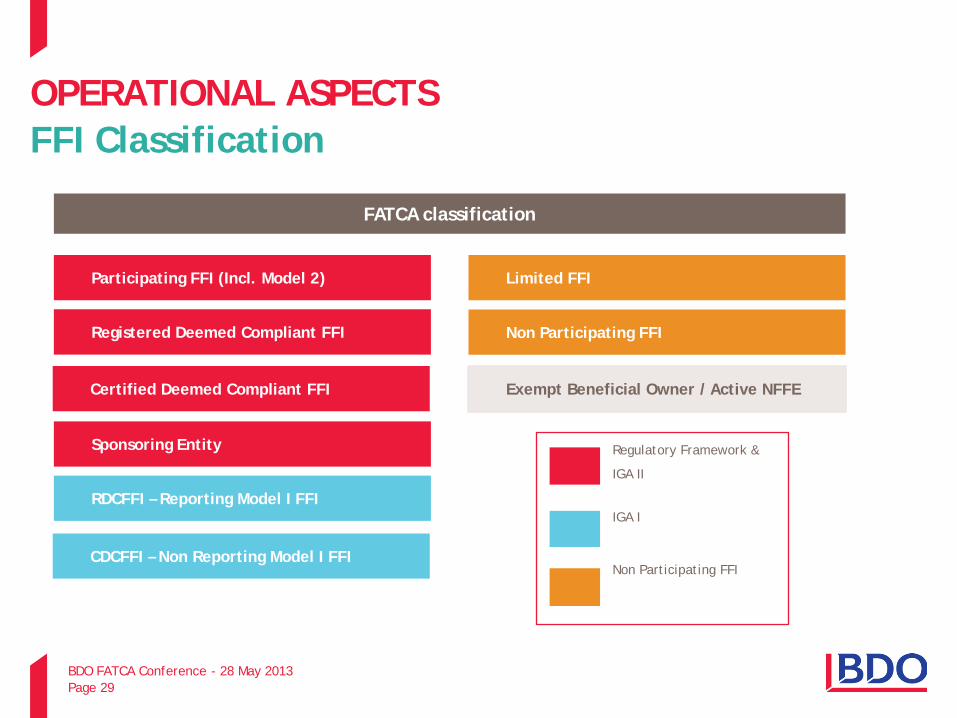

OPERATIONAL ASPECTS FFI Classification

Regulatory Framework &

IGA II

IGA I

Non Participating FFI

BDO FATCA Conference - 28 May 2013 Page 29

Participating FFI (Incl. Model 2)

Registered Deemed Compliant FFI

Sponsoring Entity

RDCFFI – Reporting Model I FFI

FATCA classification

Limited FFI

Certified Deemed Compliant FFI

Non Participating FFI

CDCFFI – Non Reporting Model I FFI

Exempt Beneficial Owner / Active NFFE

OPERATIONAL ASPECTS FFI FATCA Process

GENERAL FFI OBLIGATIONS

• Register with the IRS if necessary

• QI agreement renewal for QIs

• Apply new due diligence policies and procedures as of 01/01/2014 and review all preexisting accounts

• Report annually to its domestic tax authorities (IGA I) US Reportable Accounts (inc. “Recalcitrant Account Holders”) and Financial Accounts held by NPFFI

• Withhold 30% on FDAP income paid to NPFFIs in non IGA countries

BDO FATCA Conference - 28 May 2013 Page 30

Luxembourg FFI

US Owned Foreign Entity US Specified Person

Counterparties

?

GENERAL UPDATE FATCA - IRS information • Available

- FATCA email news updates via subscription on

FATCA page

- FFI list schema and test file on IRS.gov

- Draft form 8957 on IRS.gov (FATCA registration

process)

- Draft US Certification Forms (W-8BEN, W-8BEN-

E, W-8IMY, W-8EXP, W-9)

- Draft Reporting Forms (1042, 1042-S)

• Upcoming

- FFI Agreement / QI renewal instrument

- GIIN composition summary

- Form 8957 instructions

- FFI registration overview document

- FI online tutorial with registration summary and

steps

- FI registration user guide

- FI Frequently Asked Questions

- FFI List to search or download

- Forms & Instructions

BDO FATCA Conference - 28 May 2013 Page 31

OPERATIONAL ASPECTS QI update • IRS has expressed concerns again about the quality of the QI reporting received

• Some documentation submitted to the IRS has been qualified as “lousy” by Stuart Mann (Manager, IRS Large Business and International Division). Basic mistakes are still detected like confusion between the Boxes 7, 8 and 9

• Prompt remediation actions should be taken by QIs as the IRS has improved its control tools. Check of consistency, based on historical data will be made. Repeated errors will result in penalties

• Repeated Audit Waiver request showing no income and no customers will lead - after the 3rd year - to the termination of the QI agreement

• Audit Waiver acceptance for Reportable Amounts under $ 50.000 (if there is no other issue) will not automatically be confirmed by letter

BDO FATCA Conference - 28 May 2013 Page 32

OPERATIONAL ASPECTS QI update - Latest updates • QI documentation requirements could be align on FATCA obligations

• Duplicative reporting is expected (e.g. NPFFI, US person)

• QI External Audit program will be subject to an complete overhaul

BDO FATCA Conference - 28 May 2013 Page 33

REGISTRATION PROCESS Sylvie Maestri

REGISTRATION PROCESS Latest updates

- IGA I Reporting FIs do not need to register before 2015 -

When and how should start the registration of

FFIs members of EAG where the Lead FFI is located

in an IGA I country?

When should an IGA I Reporting FI register if it has also

to renew its QI Withholding Agreement?

BDO FATCA Conference - 28 May 2013 Page 35

!

!

REGISTRATION PROCESS Latest updates • EAG needs to determine which entity will take the role of Lead FFI. Not necessarily the Head Office

• The “Lead” status of a Lead FI cannot be changed on the FATCA Portal

• Lead FFI should list all members of their EAG as Members should not register themselves as single FFI

• EAG within an EAG will not be possible

• Identify the Responsible Officers as well as the different POCs

• The term RO has three different meanings in the registration process i.e. the person ensuring the FATCA compliance, the person allowed to add points of contacts and the person that electronically signs the registration form. The term does not refer necessarily to the same person. Additional information will be included in the Registration Process

BDO FATCA Conference - 28 May 2013 Page 36

ONLINE REGISTRATION PORTAL Latest updates • Each FFI will have a customized home page with its account information, recommended next steps,

communication from the IRS and the account options

• Registration process limited to 15 questions and certain amenities have been included (e.g. drop-down lists, links to help pages) where possible

• Any change made on the EAG information or notice will be automatically notified by email to the designated Responsible Officer

• Highly recommended to set up a generic email address (e.g. [email protected])

• First FFI list will be published December 2nd , 2013

• Subsequent changes to the status (e.g. change of classification of a branch) can be made through the website

BDO FATCA Conference - 28 May 2013 Page 37

ONLINE REGISTRATION PORTAL Latest updates • A GIIN will have 19 characters and three periods which will contain the Lead FFI’s FATCA ID, the FFI

status, its country code

• The EIN of a QI will be associated with the GIIN and still be used for 1042 reporting purposes

• The FFI List will be downloadable from the IRS site and searchable by GIIN, FI name and country of tax residence

• More information and tutorials to be realized in the coming weeks

BDO FATCA Conference - 28 May 2013 Page 38

ONLINE REGISTRATION PORTAL Account creation / confirmation / registration

BDO FATCA Conference - 28 May 2013 Page 39

ONLINE REGISTRATION PORTAL Registration

BDO FATCA Conference - 28 May 2013 Page 40

ONLINE REGISTRATION PORTAL Registration, Home Page

BDO FATCA Conference - 28 May 2013 Page 41

ONLINE REGISTRATION PORTAL FATCA Search IRS FFI List

BDO FATCA Conference - 28 May 2013 Page 42

CONCLUSIONS

CONCLUSIONS • Do not wait anymore, the worst thing you can do is nothing at all! 7 to 18 months required to build

and test FATCA in-house systems and procedures

• Conduct an impact assessment to evaluate the effects of FATCA on the global organization and develop a pragmatic and proportionate response to it

• Identify impacted operational processes and key stakeholders: get FATCA out of tax

• Communication towards your Customers will be determinant

• Health Checks are highly recommended

• Training is essential

BDO FATCA Conference - 28 May 2013 Page 44

TIMELINE

BDO FATCA Conference - 28 May 2013 Page 45

QUESTIONS?

BDO CONTACTS

BDO CONTACTS FATCA Subject Matter Experts

BDO FATCA Conference - 28 May 2013 Page 48

Current role at BDO Luxembourg

BDO Tax Partner

Relevant experience

Gerdy joined BDO in 2010 after more than 20 years in the financial sector. He has been head of the tax department of two major Luxembourg banks.

He is recognized in Luxembourg as an expert on tax matters relating to securities (e.g. Savings Directive, QI, FATCA).

He has been chairman of the tax committee of the ABBL for more than 5 years and is still an active member. He is also a member of the tax committee of ALFI and of the ABBL/ALFI QI and other US tax issues working group.

Gerdy Roose Partner Tax (+352) 451 23 371 (+352) 451 23 203 [email protected]

Current role at BDO Luxembourg

BDO Operational Tax Senior Manager

Relevant experience

Sylvie joined BDO in October 2011. She is a specialist in advising financial institutions.

Before joining BDO, she built up experience in a Big 4 firm (7 years) as well as in the banking sector (12 years).

Sylvie actively participates in operational tax projects, specifically on the US Qualified Intermediary regime (QI), the Foreign Account Tax Compliance Act (FATCA), the European Savings Directive (EUSD) and other operational tax related legislations.

At present, she is the FATCA Country Tax Leader for Luxembourg / France / Monaco, has a specific experience in QI & FATCA tax advisory services, and is heavily involved in QI audit reviews. She is a member of different ABBL/ALFI QI and other US tax issues working groups.

Sylvie Maestri Senior Manager Tax (+352) 451 23 589 (+352) 451 23 203 [email protected]

BDO DISCLAIMER THIS PRESENTATION CONTAINS GENERAL INFORMATION ONLY AND BDO TAX & ACCOUNTING, S.A. IS NOT, BY MEANS OF THIS PRESENTATION RENDERING ACCOUNTING, BUSINESS, FINANCIAL, INVESTMENT, LEGAL, TAX OR OTHER PROFESSIONAL ADVICE OR SERVICES. THIS PRESENTATION IS NOT SUITABLE FOR SUCH PROFESSIONAL ADVICE OR SERVICES, NOR SHOULD IT BE USED AS A BASIS FOR ANY DECISION OR ACTION THAT MAY AFFECT YOUR BUSINESS. BEFORE MAKING ANY DECISION OR TAKING ANY ACTION THAT MAY AFFECT YOUR BUSINESS, YOU SHOULD CONSULT A QUALIFIED ADVISER. BDO TAX & ACCOUNTING, S.A. OR ITS AFFILIATES AND RELATED ENTITIES SHALL NOT BE RESPONSIBLE FOR ANY LOSS SUFFERED BY ANY PERSON WHO RELIES UPON THIS PRESENTATION

BDO FATCA Conference - 28 May 2013 Page 49