Foreign Investment Strategies Presentation to Bouygues Management Institute Chris Barrilleaux Angela Etherton Todd Gallati Keith Gibbons Kathryn Herrold Greg Lawrence Troy LeMaire Pete Persson Nat Phillips Brent Vidrine A.B. Freeman School of Business Tulane University June 11, 2003

• Developing a Winning Foreign Direct Investment Strategy

• Case Studies in Foreign Direct Investment

3

Foreign Investment Overview and Trends

4

Defining foreign investment

There are two types of foreign investment:• Portfolio: foreign investors purchase a local firm’s securities or bonds without

exerting control

• Direct: foreign investor starts a greenfield operation or acquires control of a local firm

If an investor holds at least 10% of a firm’s equity, it is classified as a Foreign Direct Investment (FDI) by the IMF, UNCTAD, and the US Department of Commerce• Other nations have differing definitions on level of control. Examples: UK

20%, Germany 25%

Portfolio investments typically follow FDI

Source: Laura Alfaro, Harvard Business School

5

1.99

1.89

1.51

1.5

1.29

1.23

1.22

1.2

1.19

1.16

1.15

1.12

1.09

1.07

1.05

1.02

0.99

0.95

0.95

0.93

0.91

0.89

0.86

0.85

0.85

ChinaUnited States

United KingdomGermany

FranceItaly

SpainCanadaMexico

AustraliaPolandJapanBrazil

Czech RepublicIndia

HungaryRussia

Hong KongNetherlands

ThailandSouth Korea

SingaporeBelgiumTaiwanAustria

Low confidence High confidence

China and the US are the preferred nations for FDI today

Source: A.T. Kearney

FDI Confidence Index September 2002

10%

20%

30%

40%

5%

15%

25%

35%

0%

Russia

Poland

China

Japan

Canada

Mexico

United States Turkey

Brazil

Rest of Europe

Rest ofAsia Pacific

Rest of Latin America

Rest of the region

Europe Asia Pacific North America Africa, Near and Middle East

Latin America

Reg

iona

l sha

re o

f tot

al p

lann

ed fi

rst-

time

inve

stm

ents

10%

20%

30%

40%

5%

15%

25%

35%

0%

Russia

Poland

China

Japan

Canada

Mexico

United States Turkey

Brazil

Rest of Europe

Rest ofAsia Pacific

Rest of Latin America

Rest of the region

Europe Asia Pacific North America Africa, Near and Middle East

Latin America

Reg

iona

l sha

re o

f tot

al p

lann

ed fi

rst-

time

inve

stm

ents

Planned New Market Entry by Region

6

Global competition is driving FDI decisions

Shifting Input Costs / Availability of Inputs

36%

47%

48%

54%

56%

60%

75%

78%

0% 20% 40% 60% 80%

Emergence of New Industry Segments

Privatization

New Technologies

Deregulation

Changes in Government Regulation

New/Shifting Consumer Needs

Matching Competitors' Actions

Responding to competitor’s actions is a more powerful driver of FDI than the appeal of opening markets

Source: Corporate Strategy Board

Percentage of companies identifying driver as being of high importance

7

Developing a winning FDI strategy

8

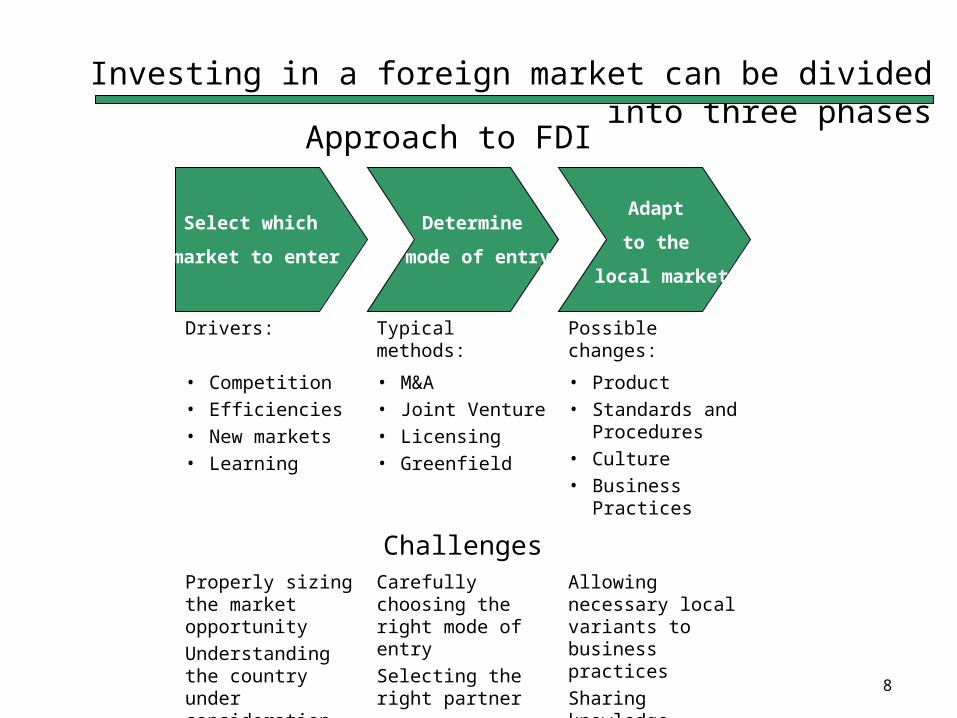

Investing in a foreign market can be divided into three phases

Select which

market to enter

Determine

mode of entry

Adapt

to the

local market

Drivers: Typical methods: Possible changes:

• Competition• Efficiencies• New markets• Learning

• M&A• Joint Venture• Licensing• Greenfield

• Product• Standards and

Procedures• Culture• Business

Practices

ChallengesProperly sizing the market opportunity

Understanding the country under consideration

Carefully choosing the right mode of entry

Selecting the right partner

Allowing necessary local variants to business practices

Sharing knowledge

Maintain efficiencies

Approach to FDI

9

Two frameworks for market selection could be used

CAGE Framework

Culture Administrative

Geography Economics

“The problem [with market selection] is rooted in the very analytical tools that managers rely on in making judgments about international investments, tools that consistently underestimate the costs of doing business internationally.

Measures a country’s ability to attract, absorb, and retain FDI. Although developed for national FDI policy makers, it could be used to ascertain a country’s attractiveness for FDI.

Sources: Pankaj Ghemawat , Harvard Business School; EAGER Project

10

Selecting markets using the CAGE Distance Framework

Attributes Creating Distance

Culture Administrative

Language Shared monetary or

political association

Ethnicity Colonial ties

Connective social networks

Political culture

Religion Regulatory policies

Social norms Institutional weakness

Geography Economics

Physical distance Consumer incomes

Common border Costs and quality of:• Natural resources• Financial resources• Human resources• Infrastructure• Intermediate inputs• Information or

knowledge

Sea or river access

Country size

Transportation or

communication links

Climate

Source: Pankaj Ghemawat , Harvard Business School; Jeffrey Frankel and Andrew Rose

Managers are accused of using outdated analytic tools that underestimate the cost of doing business internationally.

Example: Country Portfolio Analysis (CPA), which focuses on potential sales and ignores the costs and risks of doing business in a new market.

Analysis should incorporate distance as an analytic factor.

Distance AttributeIncome level: GDP per capita (1% increase)Economic size: GDP (1% increase)Physical distance (1% increase)Physical size (1% increase) Access to oceanCommon borderCommon languageCommon regional trading blocColony-colonizer relationshipCommon colonizerCommon polityCommon currency

+0.7+0.8-1.1-0.2+50+80+200+330+900+190+300+340

Change in international trade (%)Distance Attribute

Income level: GDP per capita (1% increase)Economic size: GDP (1% increase)Physical distance (1% increase)Physical size (1% increase) Access to oceanCommon borderCommon languageCommon regional trading blocColony-colonizer relationshipCommon colonizerCommon polityCommon currency

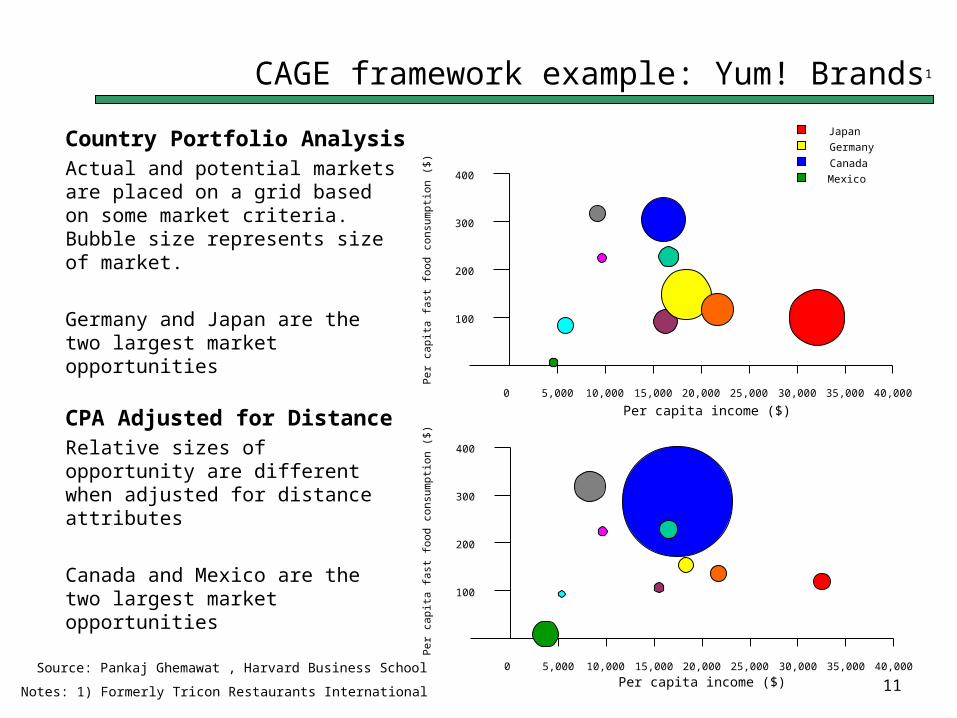

Country Portfolio AnalysisActual and potential markets are placed on a grid based on some market criteria. Bubble size represents size of market.

Germany and Japan are the two largest market opportunities

CPA Adjusted for DistanceRelative sizes of opportunity are different when adjusted for distance attributes

Canada and Mexico are the two largest market opportunities

Source: Pankaj Ghemawat , Harvard Business School

Notes: 1) Formerly Tricon Restaurants International

12

Case Studies in FDI

13

Case Studies

The world’s largest dedicated agribusiness. The decision-making process associated with the sourcing of products in the global supply chain

To increase its European X-ray machine market share, GE sold RCA to Thomson Electronics in exchange for Companie Generale de Radiologie.

The world’s largest environmental services provider seeks growth in water distribution business. Decides if the acquisition of US Filter meets that goal.

14

Case Study: Syngenta

Product sourcing process

New Product Supply Chains• Make (in-house) or Buy (external) studies• Siting studies

— Checklists used to standardize process

Existing Product Supply Chains• Continuous optimization of supply chains throughout product lifecycle• 2000 merger and impact on supply chain

15

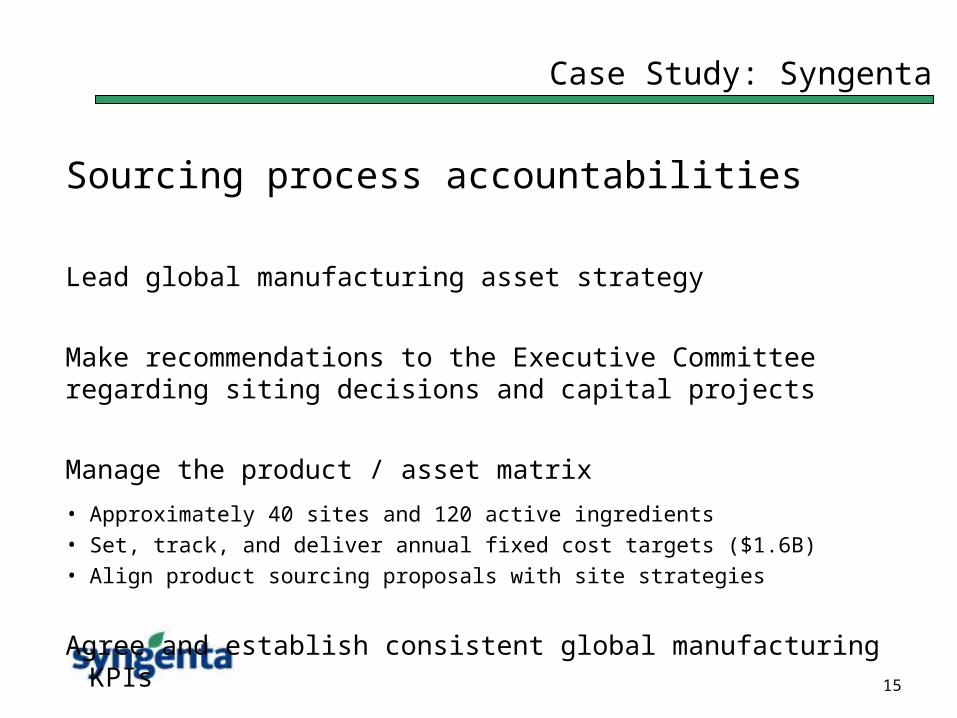

Case Study: Syngenta

Sourcing process accountabilities

Lead global manufacturing asset strategy

Make recommendations to the Executive Committee regarding siting decisions and capital projects

Manage the product / asset matrix• Approximately 40 sites and 120 active ingredients• Set, track, and deliver annual fixed cost targets ($1.6B)• Align product sourcing proposals with site strategies

Agree and establish consistent global manufacturing KPIs

16

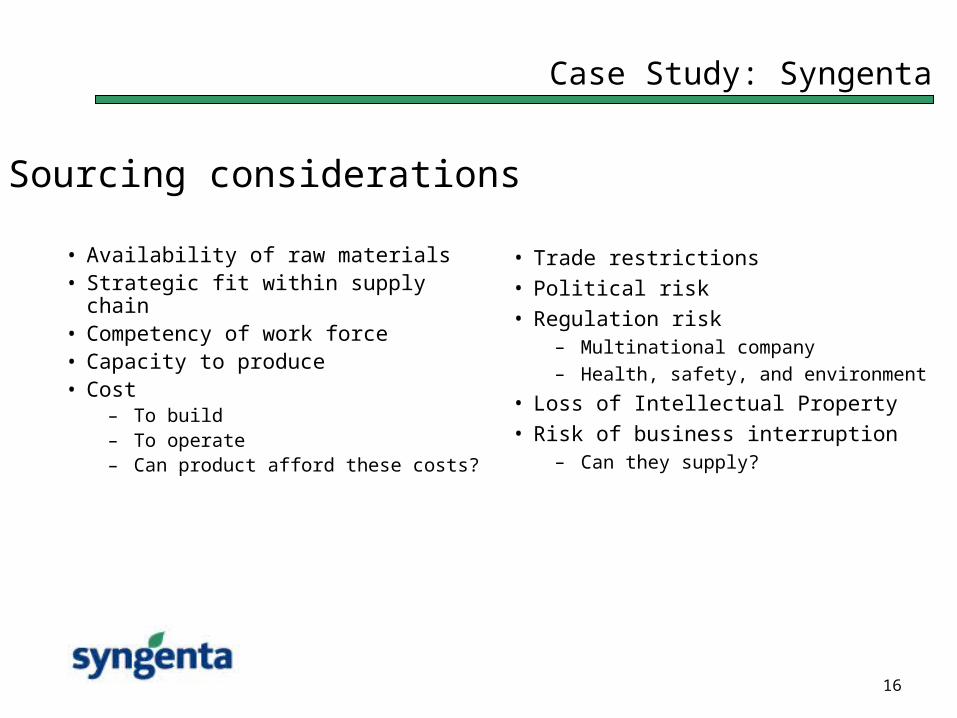

Case Study: Syngenta

• Availability of raw materials• Strategic fit within supply chain• Competency of work force• Capacity to produce• Cost

– To build– To operate– Can product afford these costs?

• Trade restrictions

• Political risk

• Regulation risk– Multinational company– Health, safety, and environment

• Loss of Intellectual Property

• Risk of business interruption– Can they supply?

Sourcing considerations

17

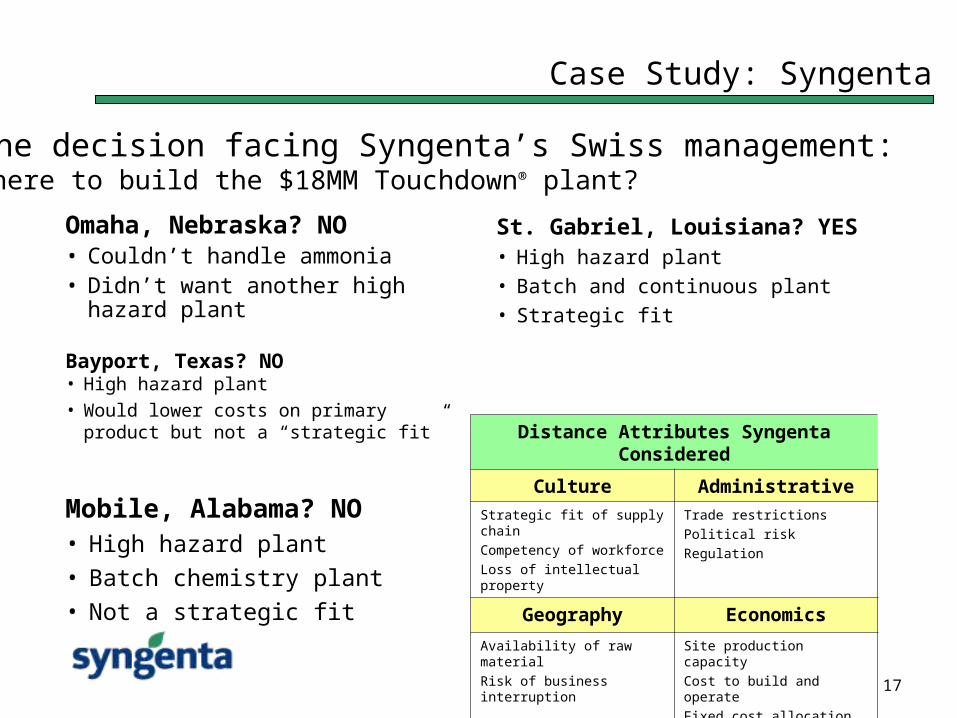

Case Study: Syngenta

Omaha, Nebraska? NO• Couldn’t handle ammonia• Didn’t want another high hazard

plant

Mobile, Alabama? NO• High hazard plant

• Batch chemistry plant

• Not a strategic fit

The decision facing Syngenta’s Swiss management:Where to build the $18MM Touchdown® plant?

Bayport, Texas? NO• High hazard plant

• Would lower costs on primary product but not a “strategic fit”

St. Gabriel, Louisiana? YES• High hazard plant

• Batch and continuous plant

• Strategic fit

Distance Attributes Syngenta Considered

Culture Administrative

Strategic fit of supply chain

Competency of workforce

Loss of intellectual property

Trade restrictions

Political risk

Regulation

Geography Economics

Availability of raw material

Risk of business interruption

Site production capacity

Cost to build and operate

Fixed cost allocation

18

Case Study: GE

GE• Consumer Electronics (sales $3B) faced

stiff competition from Lucky Goldstar and Samsung

• Medical Systems business wanted to increase European market share from 6%

• Jack Welch once ran Medical Systems, did not see Consumer Electronics as strategic

Thomson Electronics• French government forced it to acquire Cie

Generale de Radiologie (CGR), one of Europe’s largest manufacturers of X-ray machines (sales $800MM).

• Could not get the government to take it back

The Deal

Jack Welch and Alain Gomez, Thomson chairman, met over dinner during the French Open. They agreed to swap businesses: GE got CGR, Thomson got Consumer Electronics.

The decision was made in 30 minutes.

“We didn’t need to go back to headquarters for a strategic analysis and a bunch of reports. ….it took us 30 minutes to decide the deal made sense, and then a meeting of maybe two hours with the Thomson people to work out the basic terms.”

Jack Welch

19

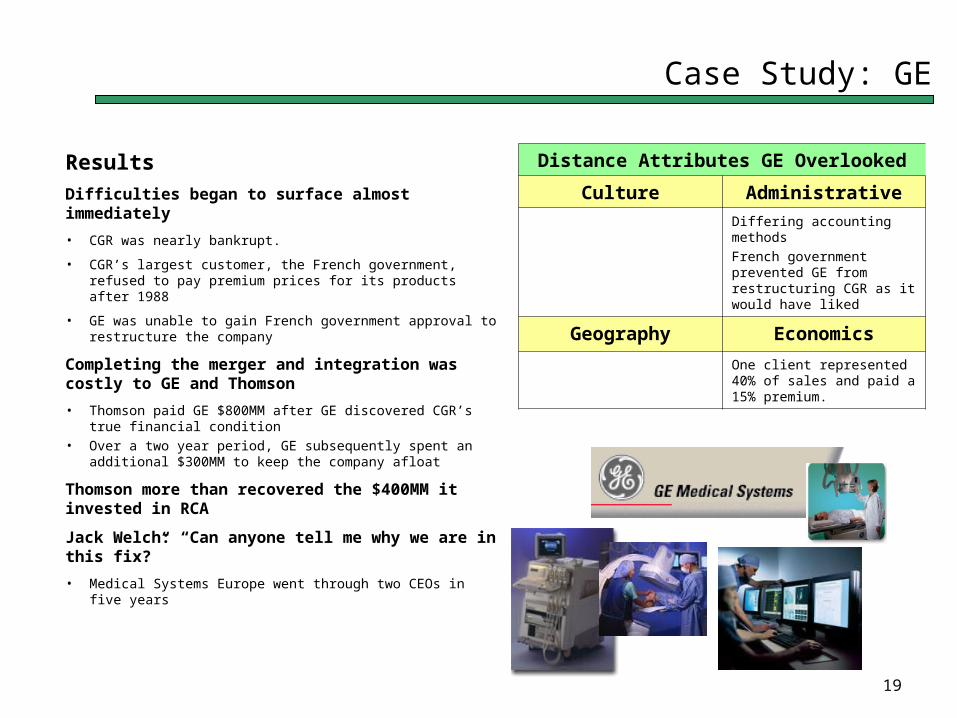

Case Study: GE

Distance Attributes GE Overlooked

Culture Administrative

Differing accounting methods

French government prevented GE from restructuring CGR as it would have liked

Geography Economics

One client represented 40% of sales and paid a 15% premium.

Results

Difficulties began to surface almost immediately

• CGR was nearly bankrupt.

• CGR’s largest customer, the French government, refused to pay premium prices for its products after 1988

• GE was unable to gain French government approval to restructure the company

Completing the merger and integration was costly to GE and Thomson

• Thomson paid GE $800MM after GE discovered CGR’s true financial condition

• Over a two year period, GE subsequently spent an additional $300MM to keep the company afloat

Thomson more than recovered the $400MM it invested in RCA

Jack Welch: “Can anyone tell me why we are in this fix?”

• Medical Systems Europe went through two CEOs in five years

20

Case Study: Vivendi

• Founded in 1853 as Generale des Eaux• Vision: Becomes the world’s single

source service for water treatment.• Niche: Municipal privatization market• International Experience• Municipal service experience• 1998 Revenues of $7.3 billion• 40,000 employees• European Union Commission Approval

• Founded in 1990• Vision: Becoming the world’s largest

water treatment equipment manufacturer• Niche: Industrial market• International Experience• Strong management team• 1998 Revenues of $3.2 billion• 28,000 employees• U S anti-trust approval (Hart-Scott-Rodino

Act)

21

Case Study: Vivendi

becomes a wholly owned subsidiary of

• World's leading provider of outsourced and privatized water treatment services

• US Filter provides access to North American water treatment market and a strong management team.

• Generale des Eaux offers US Filter an enormous worldwide market for everything they manufacture

• 86,000 employees• Serve 110 million people in 94 countries• Sales of $15.2 billion, 44% of Veolia

Environment’s 2002 revenue • 43% market share of potable water

market in France• 47% market share of US outsourcing

market• Contract renewal >90% for 2002.

Shortening the Distance

Regulatory approval International Experience

Municipal Market Experience of Vivendi

Strong Management Team of US Filter

Offices and plants located in Europe and North America

EconomicsGeography

AdministrativeCulture

a division of

22

Conclusion

The FDI decision making process is not uniform when applied to the global market. Regional economic and political issues influence FDI decisions.

Investments are often made without fully investigating non-economic factors that can significantly affect the investment’s return.

The FDI fitness and CAGE FDI frameworks can be used to ensure often overlooked aspects of a potential market are considered.

23

Appendix

24

References

1. Laura Alfaro, “Foreign Direct Investment”, Harvard Business School, October 2002

2. US Department of Treasury, “Foreign Portfolio Investment Benchmark Surveys”, www.ustreas.gov/tic/fpis.html

3. US Department of Commerce, Bureau of Economic Analysis, www.bea.gov

4. “The 2002 State New Economy Index”, Progressive Policy Institute, www.neweconomyindex.org

5. “Growth Across Borders: Strategic Challenges of International Expansion”, Corporate Strategy Board, October 2001

6. “FDI Confidence Index: September 2002”, A.T. Kearney

7. “Foreign Direct Investment And Its Determinants In Emerging Economies”, African Economic Policy Paper, Saskia K.S. Wilhelms, July 1998

8. Pankaj Ghemawat, “Distance Still Matters: The Hard Reality of Global Expansion”, Harvard Business Review, September 2001

9. Jeffrey Frankel and Andrew Rose, “An Estimate Of The Effect Of Common Currencies On Trade And Income”, Draft paper, February 2002

25

The Tulane Team

Chris Barrilleaux Manager, Utility Operations Acctg Entergy Services, Inc. Work: 639 Loyola Ave. New Orleans, LA 70113 (504) 576-4309 (504) 576-4103 fax [email protected]

Angela Etherton Financial Analyst GE Plastics Work: 3531 Port and Harbor Bay St. Louis, MS 39520 (228) 466-6078 (228) 466-6000 fax [email protected]

Kathryn Herrold HSEQ Director Syngenta Work: P.O. Box 11 St. Gabriel, LA 70776 (225) 642-1255 (225) 642-1794 fax [email protected]

Peter Persson Retail – Customer Service Entergy Services, Inc. Work: 2901 Cypress St. L-WMO-400 West Monroe, LA 71291 [email protected]

Todd Gallati Research Analyst Marine Corps Division Work: 4400 Dauphine St. New Orleans, LA 70164 (504) 678-0753 [email protected]

Greg Lawrence Project Manager IBM Work: 16468 Monticello Dr. Prairieville, LA 70769 (225) 677-9762 (225) 677-9559 fax [email protected]

Nat Phillips Real Estate Manager La. Fruit Company Work: 826 Union St. New Orleans, LA 70112 (504) 525-2985 (504) 506-4798 [email protected]

Brent Vidrine CEO Bank of Sunset and Trust Co. Work: 863 Napolean Ave. Sunset, LA 70584 (337) 662-5222 (337) 662-5707 fax [email protected]

26

Additional Slides

The following slides expand upon the preceding discussion

Pages 26-28: FDI Investment in the United States

Pages 29-31: FDI Fitness

Page 32: CAGE Framework Case Study: Star TV

27

Foreign portfolio investments in the US total $3,558B

Foreign holdings of US long-term securities in 20001

UK15.0%

Japan12.1%

Canada5.9%

Luxembourg3.0%

ROW30.8%

Bermuda3.1%

China2.6%

Unknown9.0%

Switzerland5.3%

Germany5.8%

Netherlands3.9%

Cayman Is.3.6%

Europe, Canada, and Japan account for 63% of foreign holdings

By Sector By Country

Source: US Department of Treasury

Finance, Insurance, and

Real Estate21.9%

Wholesale / Retail Trade

3.3%

Manufacturing24.8%

Transport and Public

Utilities7.0%

Other1.7%

Services8.0%

Government32.5%

Construction0.1%

Agriculture0.0%

Mining0.7%

Financial, insurance, and real estate holdings have grown from 8.96% in 1974 to 21.9% in 2000 while other have remained relatively constant

Services increased from 0% to 8% in the same timeframe

Note: 1) Latest complete data

28

Manufacturing and services led FDI in the US in 2001

Year 2001 FDI In the US by Industry

23.5%

11.8%

8.3%6.8%6.8%

42.8%

Mexico

Germany

Canada

United Kingdom

Netherlands

France

Switzerland

Other

Manufacturing

Wholesale trade

Finance2

Services

Petroleum

Insurance

Depository Institutions

Other

Source: Bureau of Economic Analysis

20011 Inward FDI (net)$124.4B

2001 Outbound FDI (net)$113.9B

Year 2001 FDI Abroad By Industry

30.7%

31.9%8.1%

11.1%

8.7%

9.4%

Year 2001 FDI Abroad by Country

11.6%

14.1%

12.7%

10.0%13.2%

38.4%

Year 2001 FDI In the US by Country

41.8%

22.5%

12.2%

11.8%11.4%

Other0.3%

Notes: 1) Latest complete data 2) Excludes depository institutions

To

p 5

Ind

ust

ries

To

p 5

Co

un

trie

s

29

On average, FDI accounts for 4.7% of US employment

The percentage of each state's workforce by foreign companies

8.3%

4.6%6.3%

3.3%

Source: Progressive Policy Institute

30

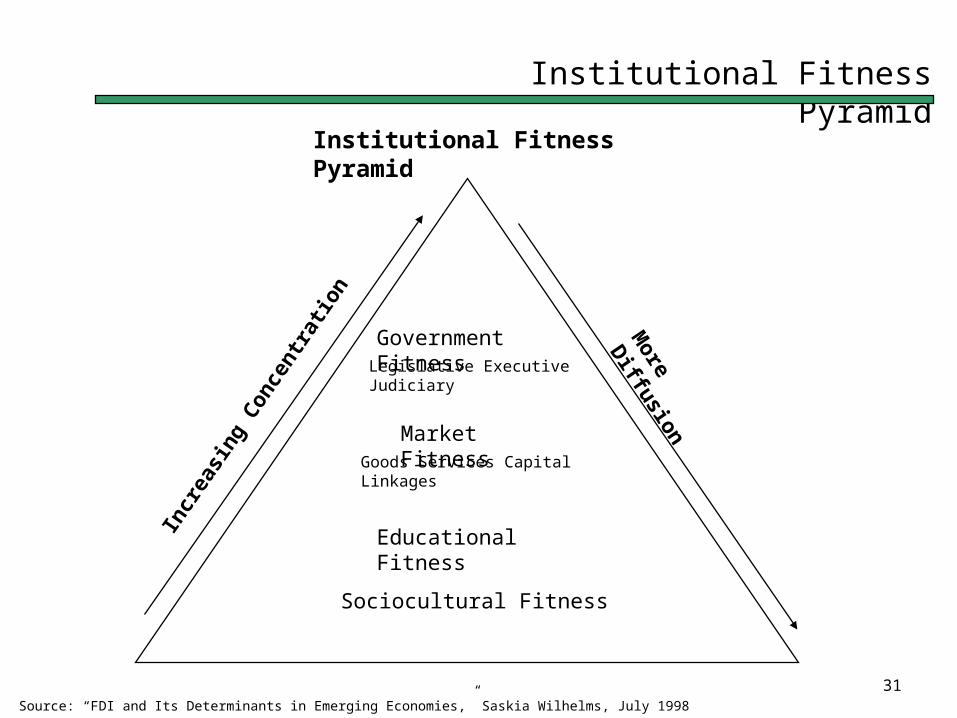

Concept of Institutional FDI Fitness

FDI Fitness indicates a country’s ability to attract, absorb, and retain FDI

• Supplemental framework for assessing FDI nation candidates• Demonstrates country’s adaptability to economic or market driven changes• Fitness theory suggests that abundant natural resources do not automatically mean a

country is a good FDI candidate• Foreign investor’s highly value flexibility rather than an intransigent environment• FDI fitness is grounded in a nation’s institutions

FDI Fitness Institutions:

• Government• Markets• Education• Socioculture

31

Institutional Fitness Pyramid

Government FitnessLegislative Executive Judiciary

Market FitnessGoods Services Capital Linkages

Educational Fitness

Sociocultural Fitness

More D

iffusion

Incr

easi

ng C

once

ntra

tion

Institutional Fitness Pyramid

Source: “FDI and Its Determinants in Emerging Economies,” Saskia Wilhelms, July 1998

32

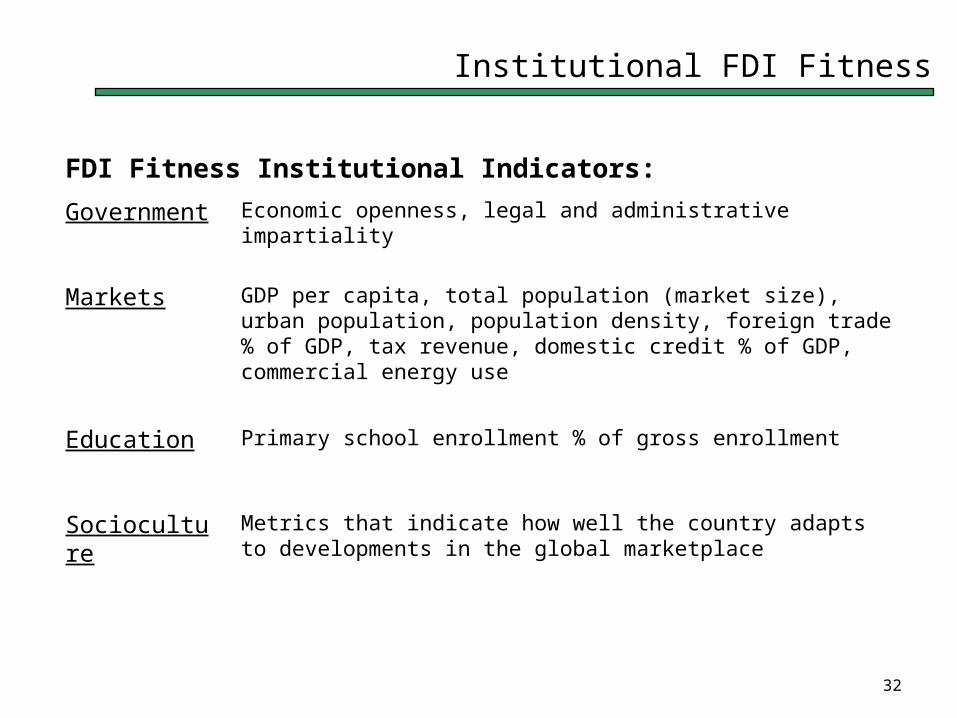

Institutional FDI Fitness

FDI Fitness Institutional Indicators:

Government Economic openness, legal and administrative impartiality

Markets GDP per capita, total population (market size), urban population, population density, foreign trade % of GDP, tax revenue, domestic credit % of GDP, commercial energy use

Education Primary school enrollment % of gross enrollment

Socioculture Metrics that indicate how well the country adapts to developments in the global marketplace

33

Overlooking distance can undermine FDI efforts

Source: Pankaj Ghemawat , Harvard Business School

Not considering distance factors when deciding which markets to enter can be costly

Star TV• Launched in 1991, it targeted the

wealthiest 5% in Asia• It broadcast English language TV

programming via satellite• Used readily available and cheap

programming without requiring investment in new programming development

• Purchased by Rupert Murdoch for $825MM between 1993-95

• Lost at least $500MM in 1996-99• Lost $141MM pretax in 1999

Distance Attributes Star TV Ignored

Culture Administrative

People prefer TV programming in their native language

Murdoch said that TV was “an unambiguous threat to totalitarian regimes.” Chinese government banned reception of foreign satellite TV services.

Geography Economics

China represents 60% of Star TV’s target market

Economics and Geography are understood better than Administrative and Culture