59

Forensic Accounting and Fraud Prepared and presented by CPA Peter Mwambuja Managing Partner UPTAKE Business Resources

Forensic Accounting and Fraud

Prepared and presented byCPA Peter MwambujaManaging Partner UPTAKE Business Resources

INTRODUCTION“You know, with all the massive and almost completelyunpunished fraud perpetrated on the American publicand Globally by such companies as Enron, GlobalCrossing, Tyco, WorldCom and Adelphia, we finally gotthe ringleader. Maybe now we can lower the nationsterror alert to periwinkle.”

INTRODUCTIONThe paper defines forensic accountant and accounting,• Defines and describe fraud,• Defines investigation and investigative Accounting,• Explains the roles of forensic accountants,• Identify’s knowledge and skills forensic accountants

are expected to possess,• Explains who retains the forensic accountant,• Explains the use of the forensic accountant report.

Forensic AccountantForensic accountants are viewed as a combination of anauditor and private investigator. Knowledge and skillsof a forensic accountant include the following:investigation skills, research, law, quantitative methods,finance, auditing, accounting and law enforcementofficer insights, organizational behavior and appliedpsychology knowledge and skills are essential.“Forensic accountants inhabit a cloak and dagger

corner of the accounting world. Their job: respond at amoment’s notice when a client spots trouble – anything

Forensic AccountantForensic Accountants are trained to look beyond thenumbers and deal with the business reality of thesituation.Forensic accountants are often expert witnesses.Forensic is more interesting because you have to thinklike a thief.

Forensic accountant

Forensic accountingIs defined as the use of accounting skills to investigatefraud or embezzlement and to analyze financialinformation for use in legal proceedings.Forensic Accounting is the specialty practice area ofaccounting that describes engagements that result fromactual or anticipated disputes or litigation. “Forensic”means suitable for use in Court, and it is to that standardand potential outcome that forensic accountantsgenerally have to work. The goal of which would be todetect fraud and provide evidence which can be used in

Forensic accounting"Forensic", according to the Webster's Dictionarymeans, "Belonging to, used in or suitable to courts ofjudicature or to public discussion and debate.""Forensic Accounting", provides an accounting analysisthat is suitable to the court which will form the basis fordiscussion, debate and ultimately dispute resolution.Forensic Accounting encompasses both LitigationSupport and Investigative AccountingAs Forensic Accountants, we utilize accounting,auditing and investigative skills when conducting aninvestigation. Equally critical is our ability to respondimmediately and to communicate financial informationclearly and concisely in a courtroom setting

Forensic accountingForensic accounting includes fraud investigations, butalso includes lots of other accounting work designed tosupport legal action such as:• Disputes with ex-employees who were sacked because

of allegations of incompetence.• Summarising the effects of complicated financial

transactions.• Business valuations needed for messy divorce/

family/... disputes.

Forensic Audit and litigation supportForensic audit is an examination of evidence regardingan assertion to determine its correspondence toestablished criteria carried out in a manner suitable tothe court. An example would be a Forensic Audit ofsales records to determine the quantum of rent owingunder a lease agreement, which is the subject oflitigation."Litigation Support", provides assistance of anaccounting nature in a matter involving existing orpending litigation. It deals primarily with issues related

FraudFraud is an activity that takes place in a social settingand has severe consequences for the economy,corporations, and individuals. It is an opportunisticinfection that bursts forth when greed meets thepossibility of deception. The fraud investigator is likethe attending physician looking and listening for thesigns and symptoms that reveal an outbreak

Fraud

FraudFBI definition of fraudThe Federal Bureau of Investigation (FBI) offers abroad but useful definition of fraud that incorporates theelements recognized over the centuries:White-collar crimes are characterized by deceit,concealment, or violation of trust and are not dependentupon the application or threat of physical force orviolence. Such acts are committed by individuals andorganizations to obtain money, property, or services; toavoid the payment or loss of money or services; or to

Fraud‘ Fraud’ refers to an intentional act by one or moreindividuals among Management, Board of directors,employees, or third parties, involving the use ofdeception to obtain unjust or illegal advantage.Fraud involving one or more members of managementor those charged with governance is referred to as“management fraud” whereas fraud involving onlyemployees of the entity is referred to as “employeefraud”. There may be collusion within the entity orwith third parties outside of the entity with either of the

Fraudulent Financial Reporting (FFR)Fraudulent financial reporting involves intentionalmisstatements including omissions of amounts ordisclosures in financial statements to deceive financialstatement users. FFR may be accomplished by:i. Manipulation, falsification (including forgery), or

alteration of accounting records.ii.Misrepresentation in or intentional omission of the

significant information.

Fraudulent Financial Reporting (FFR)FFR often involves management override of controlsthat otherwise may appear to be operating effectively.FFR techniques include:i. Recording fictitious journal entries or to manipulate

operating results.ii.Inappropriately assumptions and judgments used to

estimate account balances.iii.Omitting, advancing or delaying recognition of

Misappropriation of Assets (MoA)MoA involves the theft of an entity’s assets and is oftenperpetrated by employees.In some cases MoA can also involve management whoare usually more able to disguise or concealmisappropriations in ways that are difficult to detect.MoA can be accomplished in a variety of waysincluding:i. Embezzling receipts e,g misappropriatingcollections or diverting receipts.

Misappropriation of Assets (MoA)

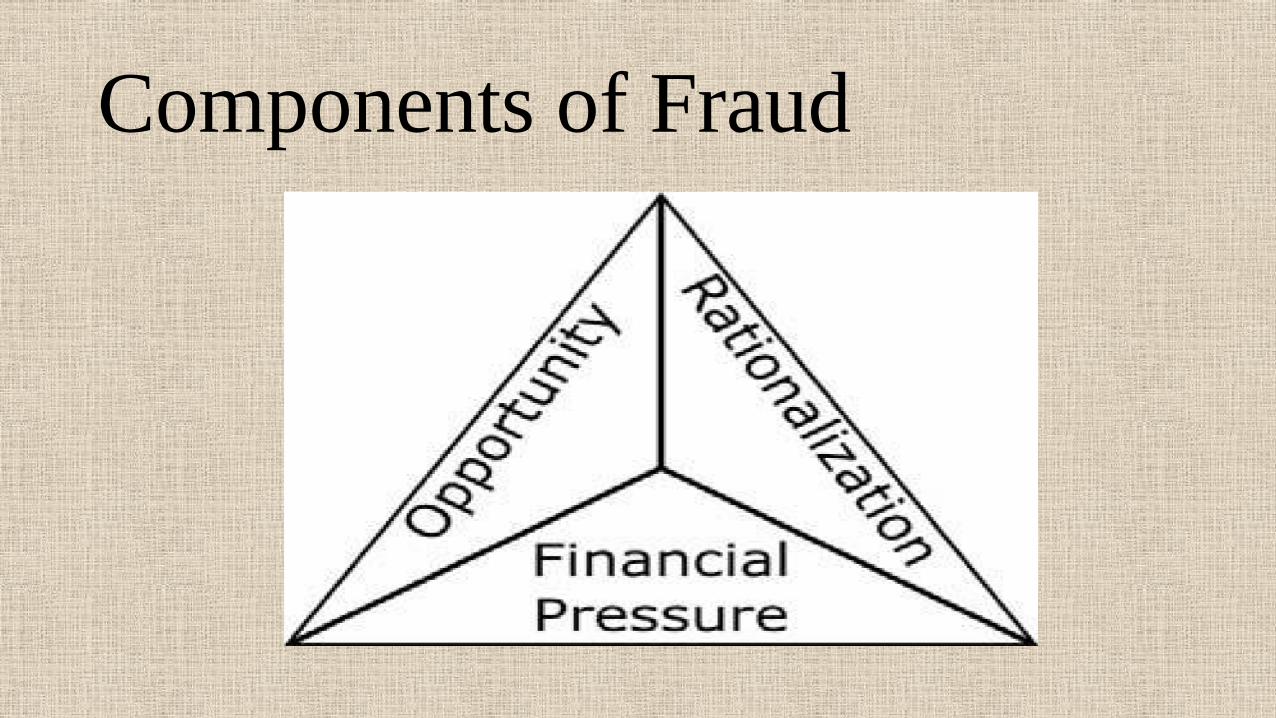

Components of FraudFraud involves:• Incentive or pressure to commit fraud,• A perceived opportunity to do so and• Some rationalization of the act.

Components of Fraud

Society’s Perception of FraudFraud was perceived as a victimless crime. Fraud wasalso viewed as an easy way to get money withoutrunning the risk of severe punishment. Dismissal iscertainly a possibility, but many employers will, in fact,try to hush up news that they have been defrauded forfear of adverse publicity with their customers, vendors,bankers, and insurers.PricewaterhouseCoopers (PwC) survey showed that, thenumber of companies reporting fraud globally hasincreased from 37 percent to 45 percent.“Deterrents aren’t sufficiently strong because too manywhite collar crimes seldom result in conviction.”Despite the public outrage caused by Enron and others

Society’s Perception of FraudIt is noted, $660 billion in revenues is diverted annuallyby fraudsters, then $660 billion will never work its waythrough to shareholders’ equity and increase the wealthof the national industrial base. Since most fraud occursat small, and thus more vulnerable, businesses, the riskis greater that it can cause bankruptcy with itsconsequent costs to vendors and lenders andunemployment for company staff.A lifetime of building respect in business, in thecommunity, and with the family can be destroyed when

Who Commits Fraud?Profile of the Typical FraudsterDespite enormous scandals such as Watergate, the Iran-Contra Affair, the Savings and Loan debacle, the WallStreet insider trading exposé, the collapse of the Bankof Credit and Commerce International (BCCI), andBarings Bank, white-collar crime has not beensubjected to as much research as other types of crime.In general terms we typically describe the perpetrator assomeone who has experience, is placed in a position oftrust, and who will have to be in a position of having the

Who Commits Fraud?The study shows that 67.8 percent of the perpetratorswere employees, 34 percent were managers, and 12.4owner/executives.The largest amounts, however, were stolen byuniversity-educated older men with no criminal recordswho were in positions of financial responsibility andperpetrating the frauds in collusion.Women commit just about as many frauds as men!Most executive and managerial positions are still heldby men, and their opportunities to steal large sums aregreater. Fraudulent acts by women seem to increase asone descends the occupational hierarchy.

Fraud detection and presentationThe primary responsibility for the presentation anddetection of fraud rests with those charged withgovernance and with management.Management, with the oversight of the Board shouldplace a strong emphasis on fraud presentation, whichmay reduce opportunities for fraud to take place, andfraud deterrence, which could persuade individuals notto commit fraud because of the like hood of detectionand punishment. This involves a culture of honesty andethical behavior. Such culture, based on a strong set ofcore values should be communicated and demonstrated

Fraud detection and presentationCreating a culture of honesty and ethical behaviorinclude:i. Setting the proper toneii. Creating a positive workplace environmentiii. Hiring, training and promoting appropriateemployeesiv. Requiring periodic confirmation by employees oftheir responsibilities , andv. Taking appropriate action in response to actual,

Investigation• Investigation is the act of determining whethercriminal matters such as employee theft, securitiesfraud, identity theft, or insurance fraud have occurred.Investigation may also occur in civil matters. Aforensic accountant may be hired to search for hiddenassets in a divorce case.

• Forensic accountants are suspicious. They must beable to apply their accounting knowledge to legalissues.

• A forensic CPA will be asked to write expert reports

Forensic investigationThe utilization of specialized investigative skills incarrying out an inquiry conducted in such a manner thatthe outcome will have application to a court of law. AForensic Investigation may be grounded in accounting,medicine, engineering or some other discipline.The process of forensic accounting includes the‘forensic investigation’ itself, which refers to thepractical steps that the forensic accountant takes inorder to gather evidence relevant to the allegedfraudulent activity. The investigation will include aplanning stage, evidence gathering, a review process,and a report to the client.

Investigative Accounting"Investigative Accounting", is often associated withinvestigations of criminal matters. A typicalinvestigative accounting assignment would be aninvestigation of employee theft. Other examplesinclude securities fraud, insurance fraud, kickbacks andproceeds of crime investigationsThe purpose of the investigation, in the case of analleged fraud, would be to discover if a fraud hadactually taken place, to identify those involved, toquantify the monetary amount of the fraud and to

Investigative Accounting

Types of investigationThe forensic accountant could be asked to investigate many different types of fraud. Three groups to provide an overview of the wide range of investigations that could be carried out. The three categories of frauds are;• corruption,• asset misappropriation and • financial statement fraud.

Corruption

Corruption• There are three types of corruption fraud:conflicts of interest,bribery, andextortion.Research shows that corruption is involved in aroundone third of all frauds.

Corruption• In a conflict of interest fraud, the fraudster exerts their

influence to achieve a personal gain whichdetrimentally affects the company. The fraudster maynot benefit financially, but rather receives anundisclosed personal benefit as a result of thesituation. For example, a manager may approve theexpenses of an employee who is also a personal friendin order to maintain that friendship, even if theexpenses are inaccurate.

• Bribery is when money is offered in order to influence

Asset misappropriation

Asset misappropriationThe most common frauds are those involving assetmisappropriation, example:Cash theft – the stealing of physical cash, e.g petty

cash, from the premises of a company.Fraudulent disbursements – making fraudulent

payments. Examples include where payments aremade to a fictitious supplier, where payments are madeto fictitious employees (often known as ‘ghostemployees’).Inventory frauds – the theft of inventory from the

company.Misuse of assets – employees using company assets

Financial statement fraud

This is also known as fraudulent financial reporting, andis a type of fraud that causes a material misstatement inthe financial statements.It can include deliberate falsification of accountingrecords; omission of transactions, balances ordisclosures from the financial statements; or themisapplication of financial reporting standards.This is often carried out with the intention of presentingthe financial statements with a particular bias, forexample concealing liabilities in order to improve any

What does a Forensic Accountant do?

What does a Forensic Accountant do?A Forensic Accountant is often retained to analyze,interpret, summarize and present complex financial andbusiness related issues in a manner which is bothunderstandable and properly supported. ForensicAccountants can be engaged in public practice oremployed by insurance companies, banks, police forces,government agencies and other organizations. AForensic Accountant is often involved in the following:• Investigating and analyzing financial evidence;• Developing computerized applications to assist in the

analysis and presentation of financial evidence;• Communicating their findings in the form of reports;and

How can a Forensic Accountant be of assistance?A Forensic Accountant can be of assistance in variousways, including:• Investigative AccountingReview of the factual situation and provision ofsuggestions regarding possible courses of action.Assistance with the protection and recovery of assets.Co-ordination of other experts, including:Private investigators;Forensic document examiners;

How can a Forensic Accountant be of assistance?• Litigation SupportAssistance in obtaining documentation necessary tosupport or refute a claim.Review of the relevant documentation to form an

initial assessment of the case and identify areas of loss.Assistance with Examination for Discovery including

the formulation of questions to be asked regarding thefinancial evidence.Review of the opposing expert's damages report and

reporting on both the strengths and weaknesses of thepositions taken.Assistance with settlement discussions and

Assignments does a Forensic Accountant perform?• Forensic Accountants become involved in a wide

range of investigations, spanning many differentindustries. Areas in which a Forensic Accountant isinvolved. Criminal InvestigationShareholders' and Partnership DisputesPersonal Injury Claims / Motor Vehicle AccidentsBusiness Interruption / Other Types of InsuranceClaims

Assignments does a Forensic Accountant perform?Matrimonial DisputesBusiness Economic Losses e.g contract disputes,

construction claimsProfessional Negligence especially technicalnegligent and loss quantificationMediation and ArbitrationBecause of their familiarity and comfort with legalissues and procedures some Forensic Accountants havesought out special training and become involved in

Who retains a Forensic Accountant?

Who retains a Forensic Accountant?

Forensic Accountants are often retained by thefollowing groups:Lawyers;Police Forces;Insurance Companies;Government Regulatory Bodies and Agencies;Banks;Courts; andBusiness Community.

Characteristics should a Forensic Accountant possess?

Characteristics should a Forensic Accountant possess?A Forensic Accountant must be open to consider allalternatives, scrutinize the fine details and at the sametime see the big picture. In addition, a ForensicAccountant must be able to listen effectively andcommunicate clearly and concisely in a timely manner.Key characters of forensic accountantcuriosity;persistence;detail-oriented;

Characteristics should a Forensic Accountant possess?discretion;skepticism;organization;Pro activeconfidence; andsound professional judgement.

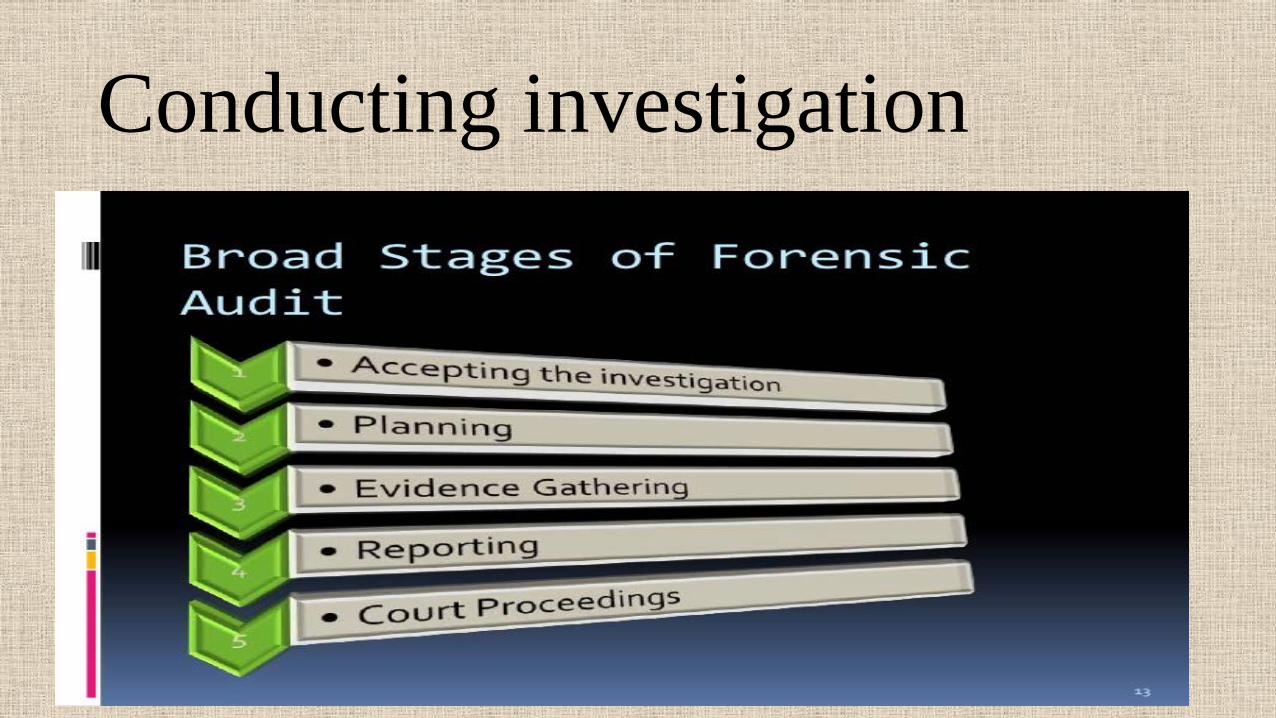

Conducting investigation

Conducting investigation

Conducting investigationAccepting the investigation• Must consider whether their firm has the necessary

skills and experience to accept the work. Forensicinvestigations are specialist in nature, and the workrequires detailed knowledge of fraud investigationtechniques and the legal framework. Investigatorsmust also have received training in interview andinterrogation techniques, and in how to maintain thesafe custody of evidence gathered.

• Also whether the investigation is being requested byan audit client. If it is, this poses extra ethicalquestions, as the investigating firm would bepotentially exposed to self review or advocacy threats

Planning the investigationThe investigating team must carefully consider whatthey have been asked to achieve and plan their workaccordingly. The objectives of the investigation willinclude:• identifying the type of fraud that has been operating,• how long it has been operating for, and how the fraudhas been concealed

• identifying the fraudster(s) involved• quantifying the financial loss suffered by the client• gathering evidence to be used in court proceedings• providing advice to prevent the reoccurrence of thef d

Gathering evidence• In order to gather detailed evidence, the investigator must

understand the specific type of fraud that has been carriedout, and how the fraud has been committed.

• The evidence should be sufficient to ultimately prove theidentity of the fraudster(s),

• the mechanics of the fraud scheme, and• the amount of financial loss suffered.It is important that the investigating team is skilled incollecting evidence that can be used in a court case, and inkeeping a clear chain of custody until the evidence ispresented in court. If any evidence is inconclusive or thereare gaps in the chain of custody, then the evidence may bechallenged in court, or even become inadmissible.

Gathering evidenceThe ultimate goal of the forensic investigation team isto obtain a confession by the fraudster, if a fraud didactually occur. For this reason, the investigators arelikely to avoid deliberately confronting the allegedfraudster(s) until they have gathered sufficient evidenceto extract a confession. The interview with the suspectis a crucial part of evidence gathered during theinvestigation.

ReportingThe client will expect a report containing the findings ofthe investigation, including a summary of evidence anda conclusion as to the amount of loss suffered as a resultof the fraud.The report will also discuss how the fraudster set up thefraud scheme, and which controls, if any, werecircumvented.It is also likely that the investigative team willrecommend improvements to controls within theorganisation to prevent any similar frauds occurring in

Court proceedingsThe investigation is likely to lead to legal proceedingsagainst the suspect, and members of the investigativeteam will be involved in any resultant court case. Theevidence gathered during the investigation will bepresented at court, and team members may be called tocourt to describe the evidence they have gathered and toexplain how the suspect was identified.It is imperative that the members of the investigativeteam called to court can present their evidence clearlyand professionally, as they may have to simplifycomplex accounting issues so that non-accountantsi l d i h d d h id

ConclusionA forensic accounting is a very specialist type ofengagement, which requires highly skilled teammembers who have experience not only of accountingand auditing techniques, but also of the relevant legalframework. Forensic accountants must therefore receivespecialist training in such matters to ensure that theircredibility and professionalism cannot be underminedduring the legal process.

ConclusionThere is no doubt the high-profile cases of WorldCom,Enron, Toshiba, Uchumi supermarkets, Richmond, Escrowsaga, and others brought an increased public scrutiny ofaccountants. The demise of the Arthur Andersen firm wasdirectly related to Enron and probably brought theaccounting profession to the fore more than any other singleincident. It is high time for we professionals in accounting toget involved in serving the public in this areaAlbert Estein once said “ The world will not be destroyedby those who do evil but by those who watch them withoutdoing anything while they have the skills to detect and

End Mwisho Cauda

Thankyou for your attention

Ahsanteni kwa usikivu

Gratias pro audire