21

Foro Internacional NIIF-XBRL 2009 La adopción XBRL-IFRS a nivel global y los avances del IASB en el desarrollo del reporte financiero 21/05/09 Fundación NIC-NIIF www.nicniif.org

| Date post: | 30-Jul-2018 |

| Category: |

Documents |

| Upload: | duonghuong |

| View: | 213 times |

| Download: | 0 times |

Foro Internacional NIIF-XBRL 2009

La adopción XBRL-IFRS a nivel global y los avances del IASB en el desarrollo del

reporte financiero

21/05/09 Fundación NIC-NIIF www.nicniif.org

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter, not necessarily those of the IASC Foundation or the IASB

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

IFRS and XBRL An ideal combination?

Friday, 15th May 2009

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

3Agenda

• XBRL @ the IASB and IASC Foundation

• The IFRS Taxonomy

• The SEC mandate

• Q & A

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

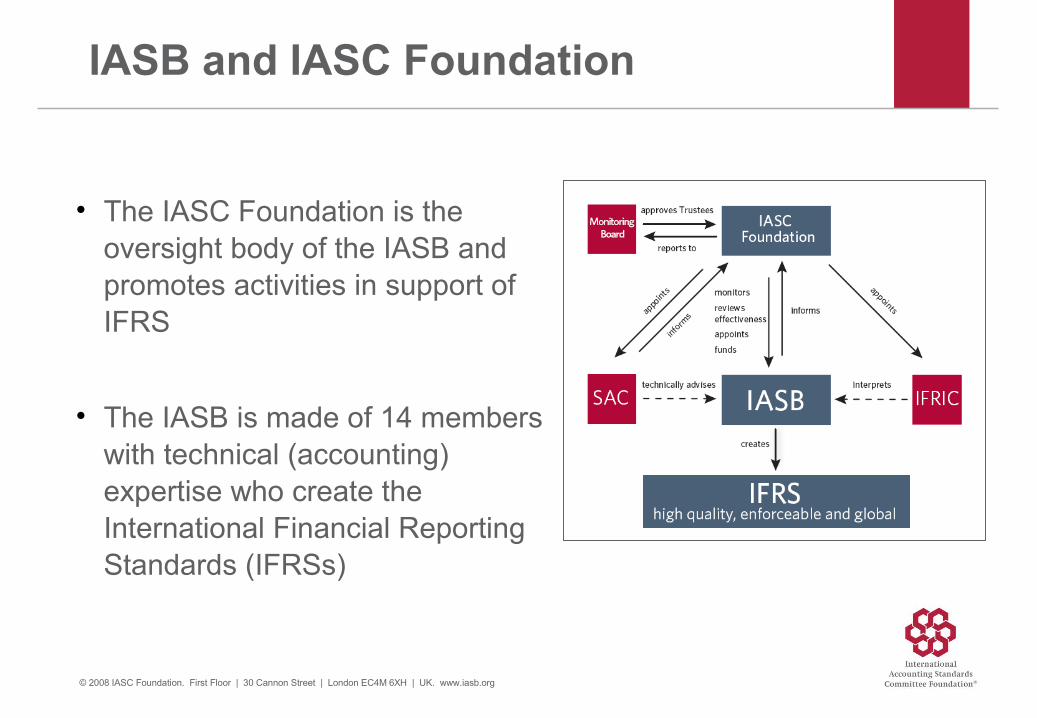

IASB and IASC Foundation

• The IASC Foundation is the oversight body of the IASB and promotes activities in support of IFRS

• The IASB is made of 14 members with technical (accounting) expertise who create the International Financial Reporting Standards (IFRSs)

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

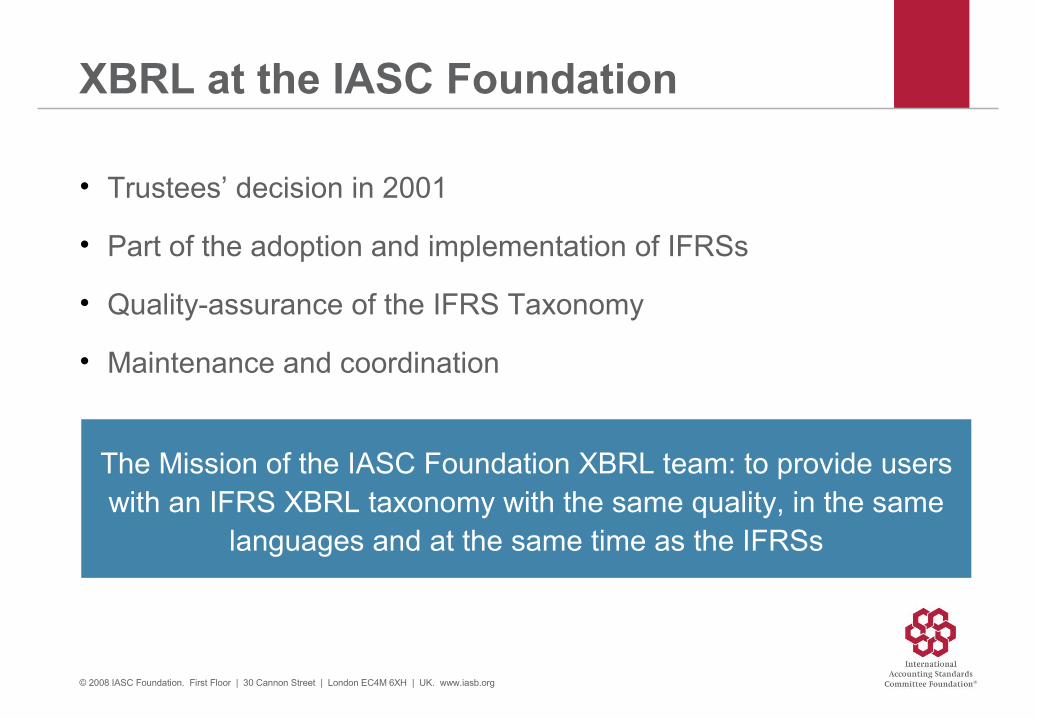

XBRL at the IASC Foundation

• Trustees’ decision in 2001

• Part of the adoption and implementation of IFRSs

• Quality-assurance of the IFRS Taxonomy

• Maintenance and coordination

The Mission of the IASC Foundation XBRL team: to provide users with an IFRS XBRL taxonomy with the same quality, in the same

languages and at the same time as the IFRSs

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

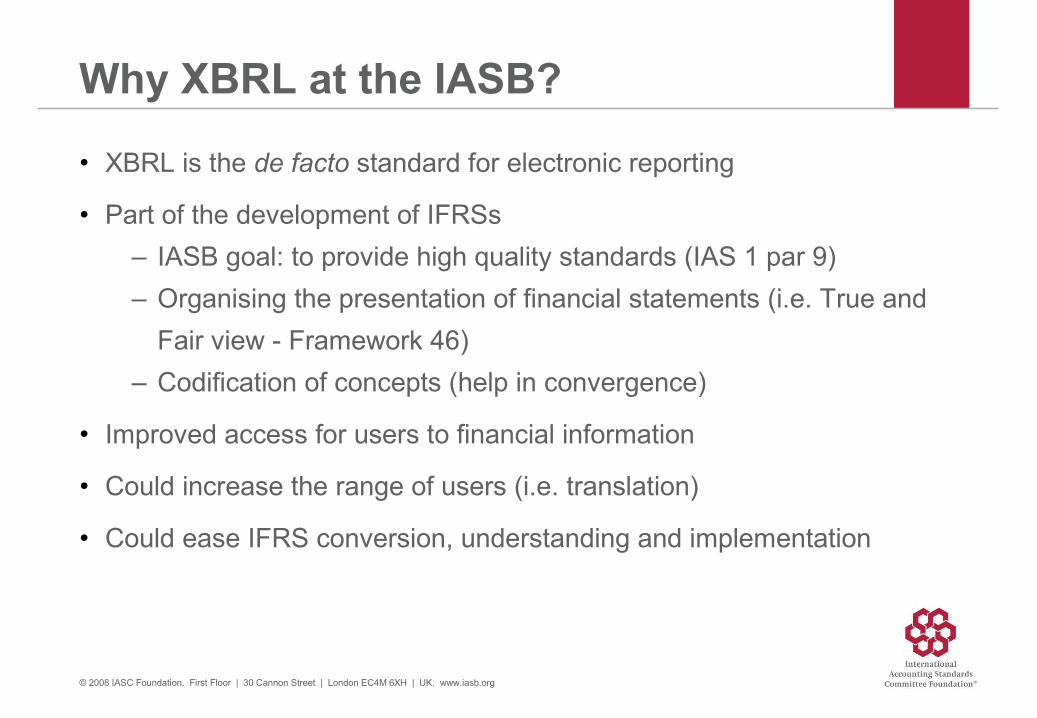

Why XBRL at the IASB?

• XBRL is the de facto standard for electronic reporting

• Part of the development of IFRSs

– IASB goal: to provide high quality standards (IAS 1 par 9)

– Organising the presentation of financial statements (i.e. True and

Fair view - Framework 46)

– Codification of concepts (help in convergence)

• Improved access for users to financial information

• Could increase the range of users (i.e. translation)

• Could ease IFRS conversion, understanding and implementation

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

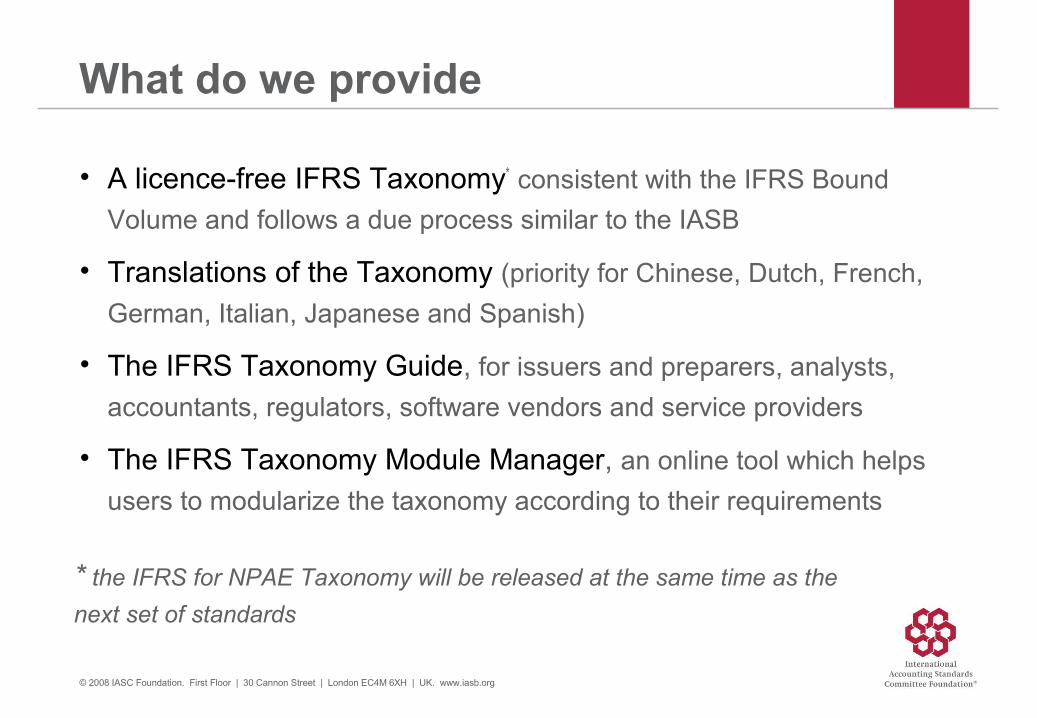

What do we provide

• A licence-free IFRS Taxonomy* consistent with the IFRS Bound

Volume and follows a due process similar to the IASB

• Translations of the Taxonomy (priority for Chinese, Dutch, French,

German, Italian, Japanese and Spanish)

• The IFRS Taxonomy Guide, for issuers and preparers, analysts,

accountants, regulators, software vendors and service providers

• The IFRS Taxonomy Module Manager, an online tool which helps

users to modularize the taxonomy according to their requirements

* the IFRS for NPAE Taxonomy will be released at the same time as the

next set of standards

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

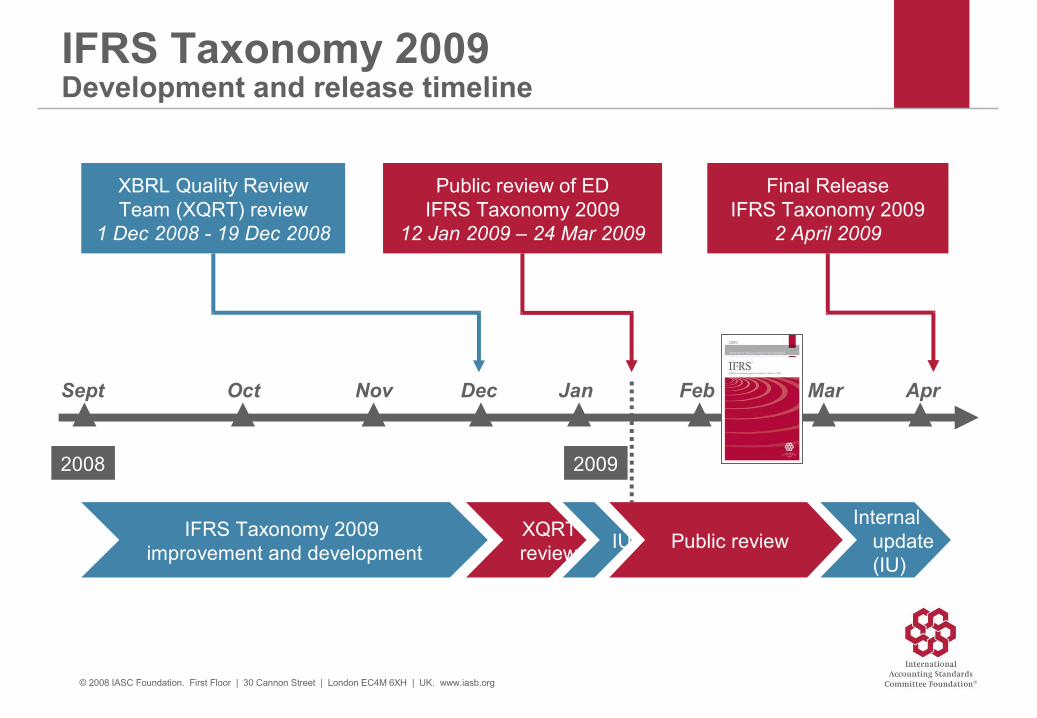

IFRS Taxonomy 2009 Development and release timeline

IFRS Taxonomy 2009 improvement and development

2008 2009

Sept Nov Dec Apr

XQRT review

Internal update

(IU)

Oct Feb Mar

IU

Jan

XBRL Quality ReviewTeam (XQRT) review

1 Dec 2008 - 19 Dec 2008

Public review of EDIFRS Taxonomy 2009

12 Jan 2009 – 24 Mar 2009

Final ReleaseIFRS Taxonomy 2009

2 April 2009

Public review

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

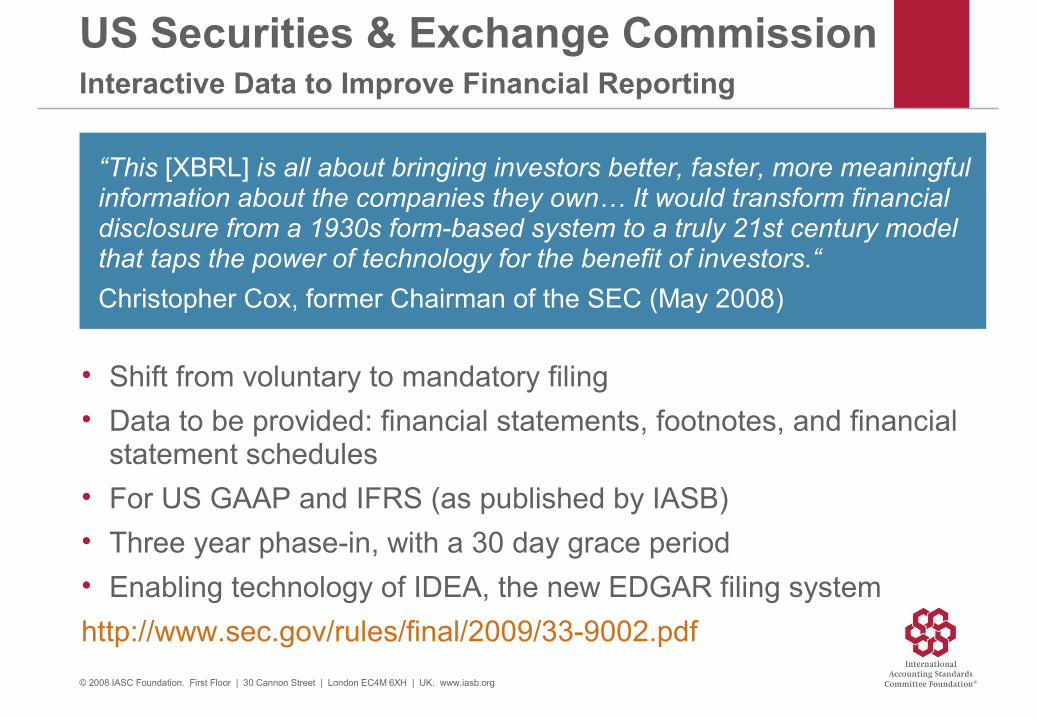

US Securities & Exchange CommissionInteractive Data to Improve Financial Reporting

“This [XBRL] is all about bringing investors better, faster, more meaningful information about the companies they own… It would transform financial disclosure from a 1930s form-based system to a truly 21st century model that taps the power of technology for the benefit of investors.“

Christopher Cox, former Chairman of the SEC (May 2008)

• Shift from voluntary to mandatory filing

• Data to be provided: financial statements, footnotes, and financial statement schedules

• For US GAAP and IFRS (as published by IASB)

• Three year phase-in, with a 30 day grace period

• Enabling technology of IDEA, the new EDGAR filing system

http://www.sec.gov/rules/final/2009/33-9002.pdf

10

DisclaimerDisclaimer

As a matter of policy, the Securities and Exchange Commission disclaims responsibility for the private statements of SEC employees. The views I am expressing today are solely my own, and do not reflect the views of the Commission, the Commissioners, or of any employees other than myself.

Participation in this meeting does not constitute any endorsement by me or the SEC of the sponsor of this meeting, nor are any comments expressed here exclusive to this meeting.

11

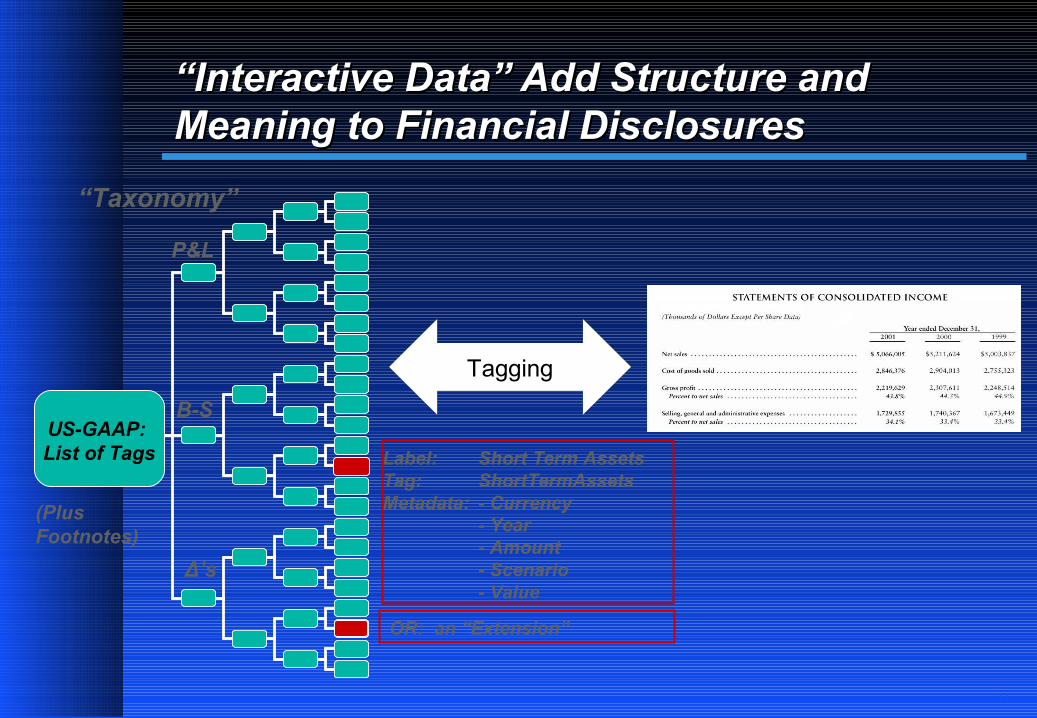

““Interactive Data” Add Structure and Interactive Data” Add Structure and Meaning to Financial DisclosuresMeaning to Financial Disclosures

Δ’s

US-GAAP: List of Tags

B-S

P&L

(Plus Footnotes)

Mapping

Label: Short Term AssetsTag: ShortTermAssetsMetadata: - Currency

- Year- Amount- Scenario- Value

Tagging

OR: an “Extension”

“Taxonomy”

12

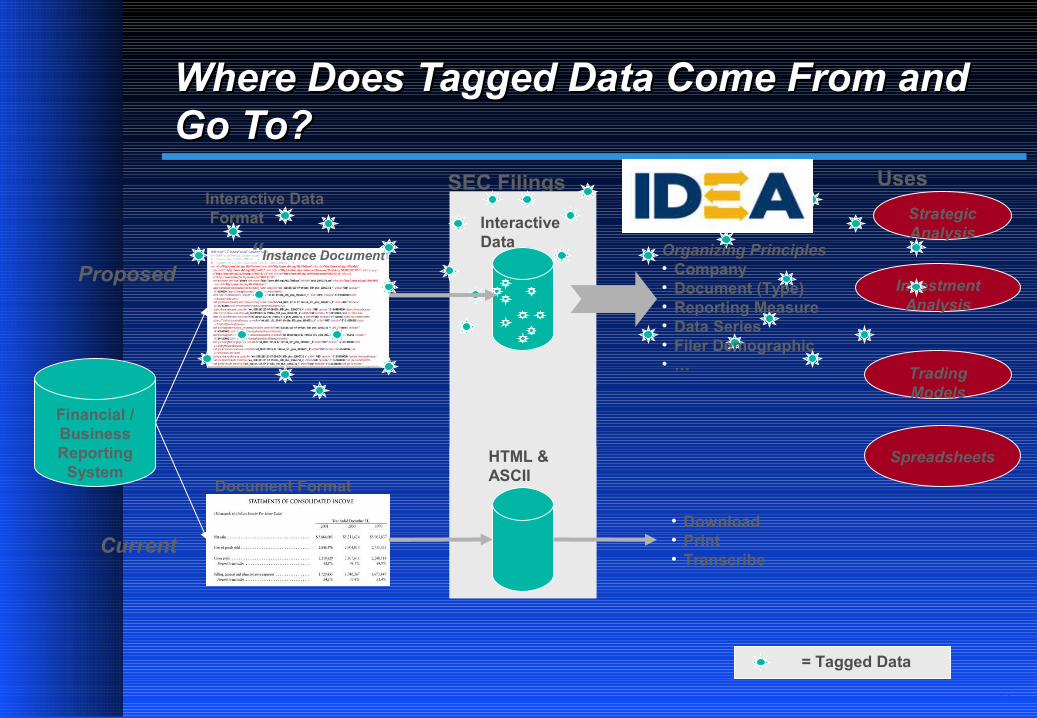

Where Does Tagged Data Come From and Where Does Tagged Data Come From and Go To?Go To?

Financial / Business Reporting

System

SEC Filings

InteractiveData

TradingModels

InvestmentAnalysis

StrategicAnalysis

Spreadsheets

Uses

SEC Filings

Document Format

• Download• Print• Transcribe

HTML &ASCII

Current

= Tagged Data

“Instance Document”

Interactive Data Format

ProposedOrganizing Principles• Company• Document (Type)• Reporting Measure• Data Series• Filer Demographic• …

13

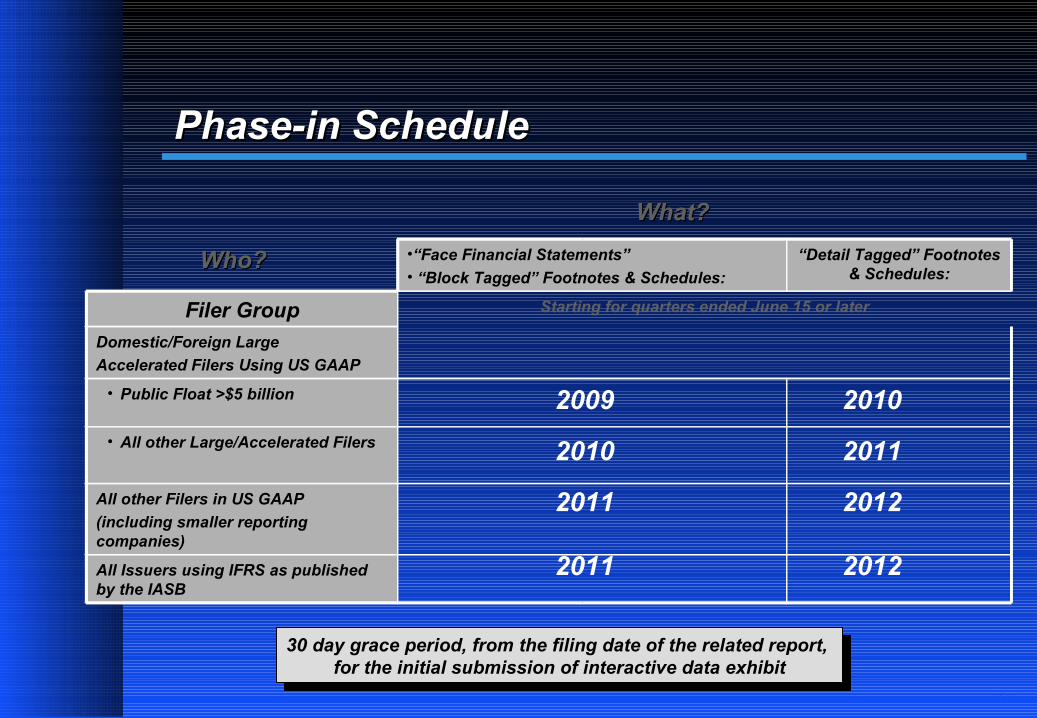

•“Face Financial Statements” • “Block Tagged” Footnotes & Schedules:

“Detail Tagged” Footnotes & Schedules:

Filer Group Starting for quarters ended June 15 or later

Domestic/Foreign Large

Accelerated Filers Using US GAAP

• Public Float >$5 billion

• All other Large/Accelerated Filers

All other Filers in US GAAP

(including smaller reporting companies)

All Issuers using IFRS as published by the IASB

Phase-in SchedulePhase-in Schedule

What?What?

Who?Who?

30 day grace period, from the filing date of the related report, for the initial submission of interactive data exhibit

2009 2010

2010 2011

2011 2012

2011 2012

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

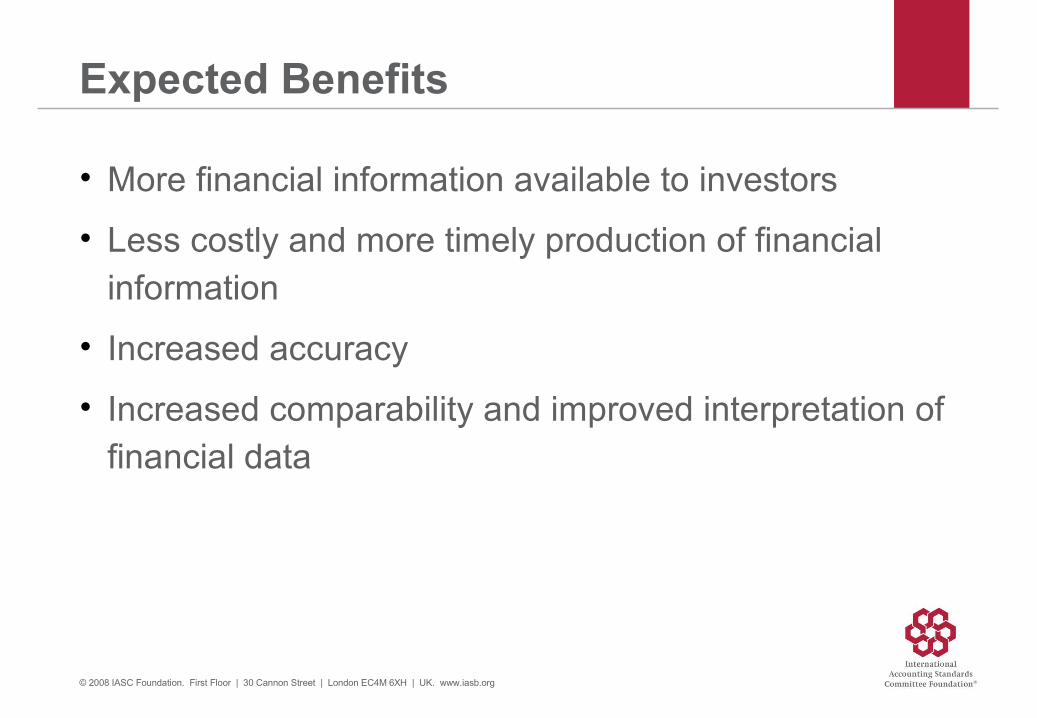

Expected Benefits

• More financial information available to investors

• Less costly and more timely production of financial information

• Increased accuracy

• Increased comparability and improved interpretation of financial data

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

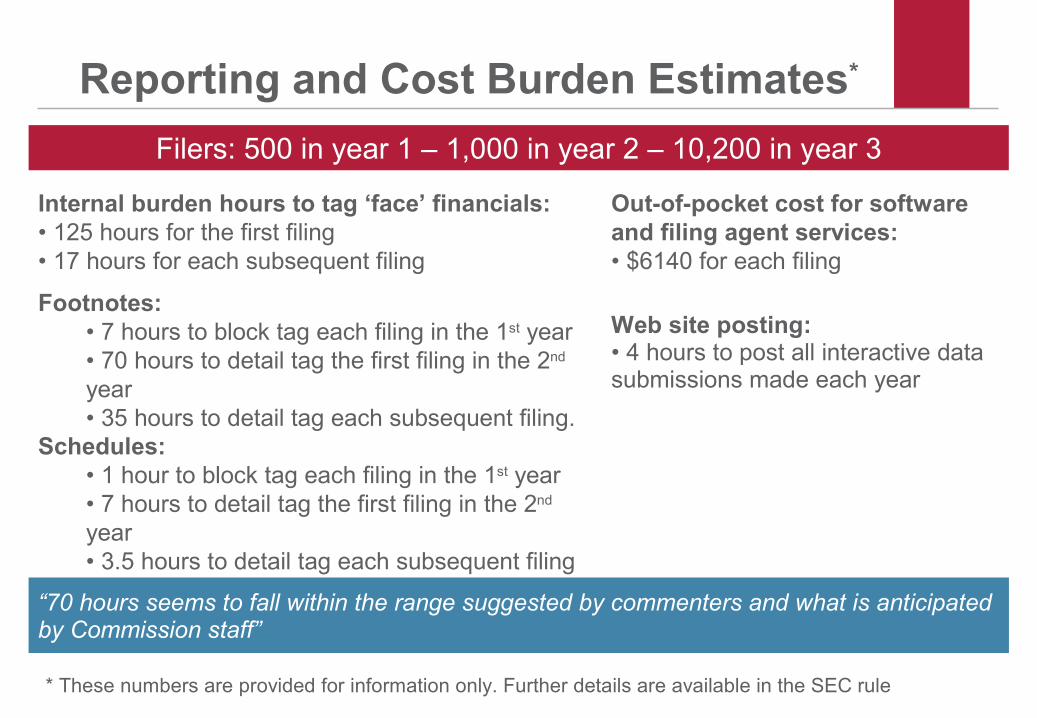

Reporting and Cost Burden Estimates*

Filers: 500 in year 1 – 1,000 in year 2 – 10,200 in year 3

Internal burden hours to tag ‘face’ financials:• 125 hours for the first filing• 17 hours for each subsequent filing

Footnotes:• 7 hours to block tag each filing in the 1st year• 70 hours to detail tag the first filing in the 2nd year • 35 hours to detail tag each subsequent filing.

Schedules: • 1 hour to block tag each filing in the 1st year • 7 hours to detail tag the first filing in the 2nd year • 3.5 hours to detail tag each subsequent filing

* These numbers are provided for information only. Further details are available in the SEC rule

Out-of-pocket cost for software and filing agent services:• $6140 for each filing

Web site posting:• 4 hours to post all interactive data submissions made each year

“70 hours seems to fall within the range suggested by commenters and what is anticipated by Commission staff”

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

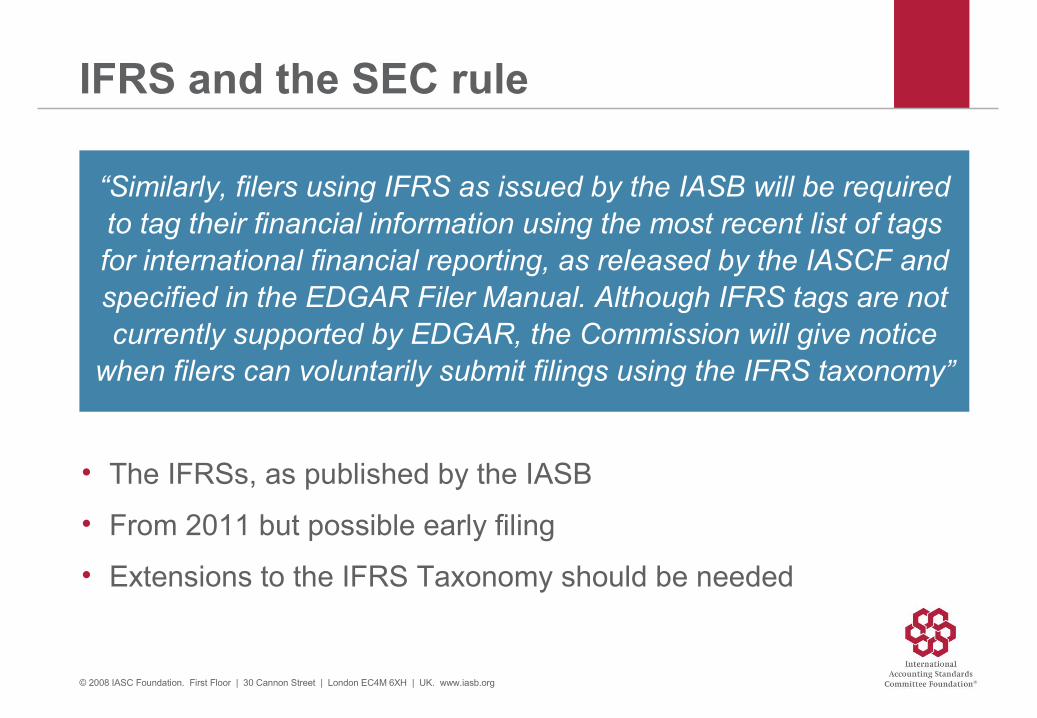

IFRS and the SEC rule

“Similarly, filers using IFRS as issued by the IASB will be required to tag their financial information using the most recent list of tags for international financial reporting, as released by the IASCF and specified in the EDGAR Filer Manual. Although IFRS tags are not currently supported by EDGAR, the Commission will give notice

when filers can voluntarily submit filings using the IFRS taxonomy”

• The IFRSs, as published by the IASB

• From 2011 but possible early filing

• Extensions to the IFRS Taxonomy should be needed

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

Japan

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

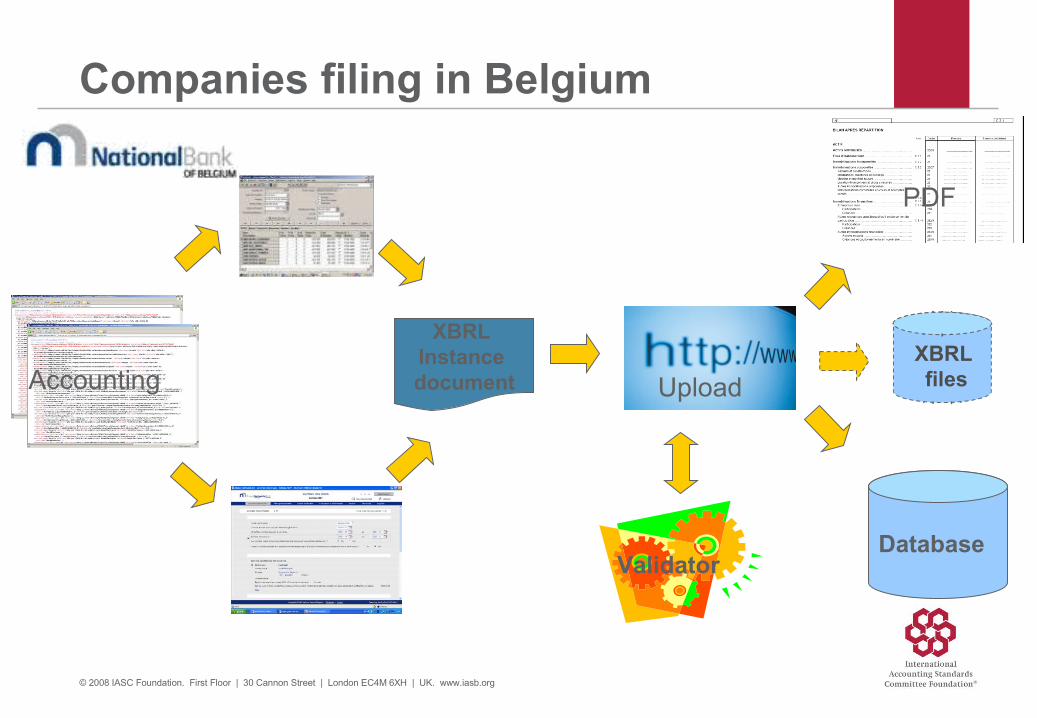

Companies filing in Belgium

Accounting

Validator

Upload

XBRL Instance document

Database

XBRL files

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

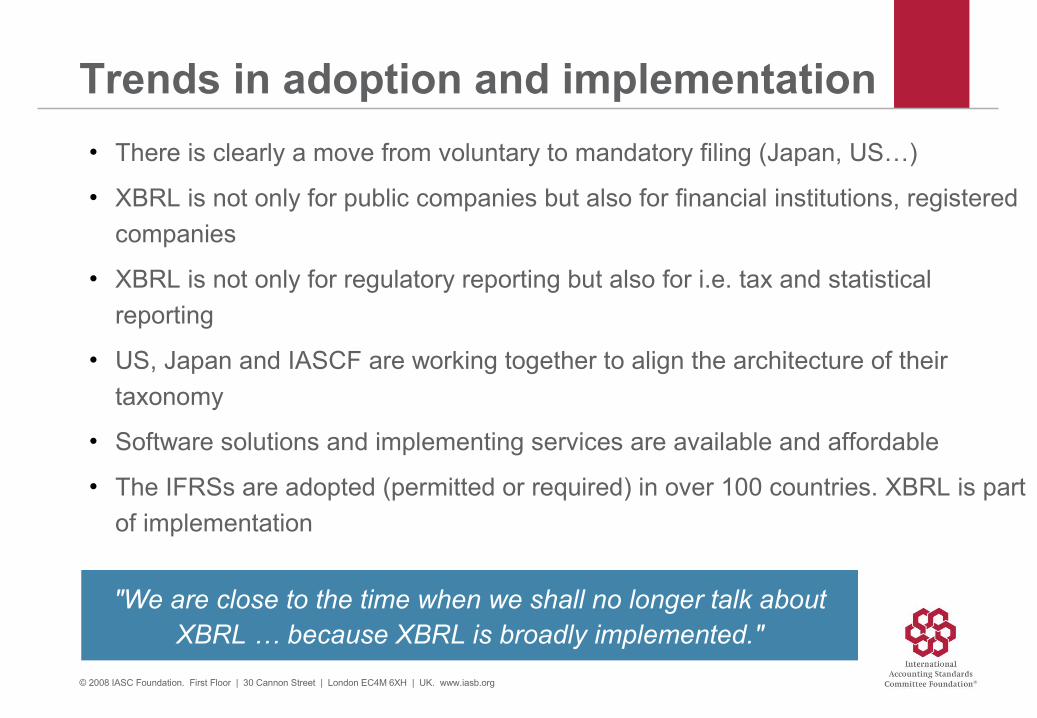

Trends in adoption and implementation

• There is clearly a move from voluntary to mandatory filing (Japan, US…)

• XBRL is not only for public companies but also for financial institutions, registered

companies

• XBRL is not only for regulatory reporting but also for i.e. tax and statistical

reporting

• US, Japan and IASCF are working together to align the architecture of their

taxonomy

• Software solutions and implementing services are available and affordable

• The IFRSs are adopted (permitted or required) in over 100 countries. XBRL is part

of implementation

"We are close to the time when we shall no longer talk about XBRL … because XBRL is broadly implemented."

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

Contact us

+44 (0)207 246 6410

www.iasb.org/xbrl

© 2008 IASC Foundation. First Floor | 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

Questions or comments?

Thank you for listening

Expressions of individual views by members of the IASB and its staff are encouraged. The views expressed in this presentation are those

of the presenter. Official positions of the IASB on accounting matters are determined only after extensive due process and deliberation.