25

FOUNDATIONS OF CORPORATE FINANCE edition FOUNDATIONS OF CORPORATE FINANCE 2 Kent A. Hickman Gonzaga University Hugh O. Hunter San Diego State University John W. Byrd Fort Lewis College

FOUNDATIONS OFCORPORATE FINANCE

ed i t i o n

FOUNDATIONS OFCORPORATE FINANCE

2

Kent A. HickmanGonzaga University

Hugh O. HunterSan Diego State University

John W. ByrdFort Lewis College

1

A Financial Modelof the Corporation

c h ap t e r 1

“No, you have the wrong number. This is not the Skyler Corporation.

We are the Skylers, but ours is a limited partnership.”

A Financial Modelof the Corporation

Chapter 1 is an overview of corporate finance and provides you with im-portant building blocks for the rest of the course. The first section of thechapter describes why finance is an important part of your business edu-

cation and why the corporation was chosen as the vehicle for studying finance.Next, some important features of corporate products, bonds, and stocks arediscussed, along with characteristics of the people whose actions affect corpo-rations. A model of the corporation, called the financial balance sheet, is pre-sented in the third section of the chapter. This model is the centerpiece of Chap-ter 1 and is designed to assist you in visualizing the financial concepts anddecisions that you study throughout this course. The fourth section covers thefinancial goal of the corporation—shareholder wealth maximization. Some ofthe problems encountered by corporations in attaining this goal and the effec-tiveness of corporations as a means of creating wealth are also covered in thissection of the chapter. The influence of society, markets, and governments in-fluences on corporations’ activities are introduced in the concluding section ofthe chapter.

Why Corporate Finance?Soon you will be leaving school. You will be deciding whether to rent or buy ahome and whether to invest your savings in the stock market or certificates ofdeposit. You will be choosing what type and amount of life insurance coverageyou should purchase to protect your family. At work you may find that makinga sale depends on your ability to show that your product is a cost-effective in-vestment for your customer. You may be asked to structure a contract that en-sures that all parties to the agreement are properly compensated and motivated.Key elements of all these decisions are financial in nature.

The skills and intuition you will be developing in this course are critical formaking decisions throughout your life. Our aim in this textbook is to enhanceyour financial reasoning ability. If you are successful in this course, you willfind that the cost of tuition will be returned to you manyfold in the future. Inshort, the time, money, and effort you invest here should reward you with ex-cellent returns.

Chapter 1 • A Financial Model of the Corporation2

Investments made by the firm Capital supplied to the firm

Chapter 1 develops the financial perspective of business by introducing the financial balance sheet.

CHAPTER 1 IN FOCUS

Customers Products Cash Investors

Cash

THE FINANCIAL BALANCE SHEET

Much of finance may already be familiar to you. The theories, tools, andconcepts covered in this text will simply add a coherent structure to the intuitionyou have developed through experience. From your day-to-day activities as aconsumer, employee, and student forced to deal with a bureaucracy, you possessa large part of the intuition upon which financial theory is based.

Developing financial intuition by understanding the underlying theory givesyou a foundation for dealing with many problems. The alternative is learninggeneral rules that may not prepare you for a rapidly changing financial environ-ment. Twenty years ago, for example, adjustable rate mortgages, money marketaccounts, and universal life insurance did not exist—all are now pervasive finan-cial products to which you will certainly be exposed. The intuition and underly-ing theory of finance gives you the flexibility to deal with new, unusual problemsas they emerge.

As a vehicle for learning the principles of finance, this course focuses on thecorporation. Other choices were available. Examples are public finance, whichstudies how governments raise and disburse funds, and personal finance, whichconcentrates on individual financial decisions like shopping for life insurance andpersonal investing. Corporate finance was chosen for several reasons. First, manyof you will be working for corporations. Understanding key financial considera-tions in corporate decision making will aid in advancing your career regardlessof your major. Second, as an individual you will be making personal investmentdecisions. Corporate securities, such as stocks and bonds, make up a large pro-portion of the investment opportunities you will have. And last, the same finan-cial approach to problems used in corporate finance is also properly used tomake personal, partnership, or public financial decisions. In effect, you are get-ting the most “bang for your buck” by studying corporate finance.

Corporations: Products,Bonds, Stocks, and PeopleThis course is about corporations. Corporations are associated with the productsthey produce and the securities they issue. For example, we know that AT&Tprovides long-distance service and Boeing manufactures airplanes. The stocksand bonds of these firms are discussed on a daily basis in the media and areclosely followed by a large segment of the population.

The goods and services produced by corporations are almost endless in theirdiversity. Each corporation attempts to match its expertise with consumers’needs in order to produce successful products. Thus, Ralston-Purina processesand sells a variety of agricultural products. General Electric makes and sells re-frigerators, radios, and aircraft engines. Yamaha sells motorcycles as well as pi-anos. Sometimes a corporation’s primary products are not what they may firstappear to be. McDonald’s sells hamburgers, but they also sell uniform qualityand service. Why has McDonald’s been successful? Is it because their hamburg-ers are superior or because consumers know what to expect when they enter anyMcDonald’s? McDonald’s, we could argue, is successful not because they per-ceived a need for more hamburgers, but because they satisfy a need for a fast, af-fordable, uniform hamburger, consistently delivered in a clean environment.

Good product decisions are rewarding. Consumers benefit as their needsand wants are met. Employees are rewarded with continued employment and jobsecurity. Communities in which the corporation is located benefit from a strongeconomic base. Investors who hold corporate securities are also rewarded. Stocks

Chapter 1 • A Financial Model of the Corporation 3

Microsoft Corporation is an excellentexample of the interplay between prod-ucts, securities, and people. Microsoft’sWindows program is pervasive, andmillions of investors own shares of thecorporation’s stock. Bill Gates providedthe entrepreneurial vision for the com-pany and is now a face as recognizableas the president’s.

Wonder what careers in finance are all about? Visit http://www.cob.ohio-state.edu/~fin/overview

See which companies are on theForbes Super 100 list at http://www.forbes.com/tool/toolbox/forbes500s/1998/Super100.htm

and bonds represent the overwhelming majority of these securities. The moneymade by corporations is distributed to owners of these securities, the stockhold-ers and bondholders, providing them with returns on their holdings.

Bonds represent loans made by investors to the corporation. Thus, bondsare a form of corporate debt. The firm is obligated to pay its bondholders a fixedseries of payments until the bonds mature. These payments, generally made semi-annually, are called coupon payments. At maturity, the corporation must repaythe bondholder the face amount, or par value, of the bond, usually $1,000. Forexample, a bond may have a $1,000 face value and a 6% annual coupon rate,make payments semiannually, and mature in 20 years. This bond represents thecorporation’s promise to pay the bondholder 40 coupon payments (one every 6months) of $30 each. At the end of the 20-year period, the bond matures and isreturned to the issuing corporation. The corporation then repays the $1,000 facevalue along with the last $30 coupon. The ability of the corporation to meetthese obligations hinges on its success in making and selling products or services.

Corporate common stock represents an equity or ownership interest in thefirm. If a corporation has 100 shares of common stock outstanding, then anowner of 1 share owns 1% of that corporation, and one holding 10 shares of thisstock owns 10% of the corporation. Stockholders receive payments from thecorporation in the form of dividends, usually paid quarterly. Dividends, unlikecoupon interest payments on bonds, are not fixed. Dividends may be raised, low-ered or not paid at all at the discretion of the corporation. Microsoft is a largeand well-known corporation that has never paid a dividend. Morrison Knudsonpaid dividends for years but suspended its dividend payment in 1995.

As owners, common stockholders elect a board of directors. Each share ofcommon stock entitles its holder to vote for directors at the corporation’s annualshareholders’ meeting. Because most shareholders of large corporations do notattend these annual meetings, most vote through the proxy process, similar to theabsentee-ballot system used in governmental elections. The board of directorsgoverns the corporation on behalf of the shareholders, determining the dividendsto be paid that year, hiring and firing top management, approving corporatestrategic decisions, and making compensation decisions.

Corporate finance is, in large part, the study of the interaction betweenproducts, stocks, bonds, and the people who make decisions affecting them. Fi-nance, therefore, includes the study of investors, managers, corporate directors,consumers, and corporate employees. One assumption underlying finance is thatpeople act in their own self-interest. This is considered to be economically ratio-nal behavior. It does not pretend to explain the complexity of human behavior,but it does allow us to explain how people are likely to behave when making fi-nancial decisions and market transactions. They buy stocks and bonds to in-crease their wealth. People work to make a living; some people desire power andprestige. People make product purchases to fulfill needs and desires. Some mayboycott, strike, vote, or petition because they perceive injustice. In corporate fi-nance, it is important to recognize that the self-interest of individuals motivatestheir actions.

People also are assumed to act rationally. Rationality means that peoplewill, by and large, make the correct decisions that lead toward fulfilling their self-interest. Departures from rationality are eventually corrected by competition.Competition exists when many individuals are seeking to achieve the same per-sonal goals. We seldom see money lying on the sidewalk, although it is oftendropped. The reason is that many individuals are interested in increasing theirwealth, and the rational thing to do is to pick up the money!

Chapter 1 • A Financial Model of the Corporation4

Common stock represents an ownershipinterest in the corporation.

Stockholders elect the board of direc-tors to oversee the business for them.

Bonds are securities that representloans made by investors to businesses.

The Financial Balance SheetThe authors of this text have attempted to make this course interesting and use-ful to you. We have also tried to make your job easier. Whenever possible we il-lustrate key concepts and theories with easily understood examples. Further,these concepts and theories are put into context throughout the text so you bet-ter understand why the topic is important and where it fits into the discipline ofcorporate finance. To achieve a coherent structure, we have incorporated a vi-sual financial model of the firm, which we call The financial balance sheet. Thistool will be used to introduce and link topics as we study corporate finance.

You are already familiar with the balance sheet that accountants use to re-port the status of a firm in its annual report. The financial balance sheet (FBS) isa conceptual counterpart to the accounting balance sheet. The FBS is a model ofthe corporation that serves several purposes. It is useful for visualizing the finan-cial functions of the firm and their objectives. Theories and concepts can be in-troduced using the FBS—thereby maintaining a coherent structure throughoutthe course. Its use helps answer questions such as, Why are we studying this?Also, because it is similar to an accounting balance sheet, accounting and finan-cial decision making can be contrasted and clarified.

The Left-Hand Side of the Financial Balance SheetLet’s begin by describing a simple financial balance sheet and contrasting it withits accounting counterpart. On the left-hand side (LHS) of the financial balancesheet appear the investments made by the firm (as opposed to assets listed in anaccounting balance sheet). It is important to note that LHS accounts are invest-ments—that is, they reflect carefully considered decisions, which, as the term in-vestments implies, should produce some payoff for the corporation. As a simpleexample, consider the cash account. The level of cash does not happen by acci-dent—the cash is there to help produce more cash. A fast-food restaurant thatbegins each day with only $10 in the cash register has not made an optimal in-vestment in cash. It will surely lose some customers because the restaurant can-not make proper change. At the other extreme, if each day is begun with $10,000in the cash register, the restaurant has over-invested in cash. The excess fundscould be better utilized by paying off a loan, thus saving interest expense (orworse, the restaurant could be robbed). For the fast-food restaurant, the samelogic applies to other investment accounts. Too high an inventory of hamburgerbuns would result in unused and stale bread; too low an inventory would resultin lost sales. Too large an investment in furniture and fixtures is wasted money(i.e., too much seating capacity), whereas too low an investment might lead tolost sales (insufficient seating capacity).

The left-hand side of the financial balance sheet includes all the accounts ap-pearing on the accounting statement (cash, inventory, furniture and fixtures,property, plant, etc.), because these are all investments. It is useful, however, tocategorize investments into two types: tangible and intangible assets. Tangibleassets include those things you can touch—bricks and mortar as the saying goes.Most of the assets associated with the accounting balance sheet are of this type.Intangible assets include patents and copyrights but go well beyond that. Thiscategory includes investments that are often just as important to the firm as themore obvious investments in factories and inventory. See Figure 1.1.

Chapter 1 • A Financial Model of the Corporation 5

The financial balance sheet is a toolfor helping you understand the wayfinancial managers view business.

The left-hand side of the financialbalance sheet is labeled investmentsmade by the firm.

One of the most important intangible assets is human resources. Investmentin this asset can produce excellent returns. Recruiting and training programs arecostly, but the payoffs, in the form of employee productivity, loyalty, and thequality service provided to customers, may make such investments worthwhile.Other intangibles that create value for the corporation may include establishingthe firm’s reputation for product quality, ethical behavior, research and develop-ment, and establishing brand recognition.

Both tangible and intangible investments require an outlay of cash that is ex-pected to produce future cash inflows. If the cash outlay is a good financial deci-sion, the cash flows received should have value greater than the initial cost of theinvestment.

The Right-Hand Side of the Financial Balance SheetThe right-hand side (RHS) of the financial balance sheet reflects the firm’s sourcesof financing. It records the sources of cash that finance the investments reflectedon the LHS. The title “Sources of Financing” contrasts with the “Liabilities andOwner’s Equity” title commonly used on the traditional accounting balance sheet.A second difference between the two statements is that the financial balance sheetaccounts are divided into two types of claims: residual claims and fixed claims.Each of these types of accounts has a claim on the cash flows generated by thecorporation’s investments. These cash flows may be generated via the normal cy-

Chapter 1 • A Financial Model of the Corporation6

The Financial Balance Sheet

Investments made by the corporation

• Tangible investments (for example, cash, inventory, factory)

• Intangible investments (for example, R&D, product development, reputation for quality and service, quality control, human resources)

FINANCIAL BALANCE SHEETThe left-hand side of the financial balance sheet includes tangible and intangibleassets.

FIGURE 1.1

The corporation strives to invest intangible assets, like factories, andintangible assets, like employeetraining, whose value to the businessis greater than their cost.

The right-hand side of the financialbalance sheet is labeled sources offinancing.

cle of producing and selling products and services. Cash may also be generatedthrough the sale of the entire firm (as might occur in the case of a liquidation or atakeover) or through the sale of a division of the corporation. When these cashflows are generated, by whatever means, their distribution is dependent on thetype of claim held by the supplier of financial resources. See Figure 1.2.

Fixed claims receive a contracted or fixed amount of cash. If fixed claimants(e.g. bondholders or employees) receive less than this amount, they have legal re-course to force the firm to meet these fixed obligations. Bank loans and bondsare two examples of fixed claims. Both require contractually specified paymentsof interest and principal. If these payments are not made in a timely manner, thebank or bondholder may seek full payment through the legal system. In this case,the corporation that has not met its obligations is in default on its payments andmay be forced into bankruptcy.

Suppliers of inventory to the corporation may also help finance the firm bynot demanding immediate payment for the goods they have delivered. The firm,therefore, has made an investment in inventory which, for a period of time, isbeing financed by the supplier. The claim that reflects this financing is an ac-count payable. If the account is not fully paid on time, then the supplier canlegally seek repayment. Similarly, workers supply financing to the firm in theform of wages payable. It’s no accident, for instance, that some organizationspay their employees on a weekly basis, while other firms pay biweekly ormonthly. The employees’ labor may be invested in finished goods inventory,while financing for that labor is being supplied by the workers themselves for aperiod of a week, two weeks, or a month, depending on the firm’s payroll pol-icy. In order not to help finance the firm, employees would need to be paid atthe end of each day. Again, if employees are not paid on a timely basis, they maysue the firm for their wages.

Chapter 1 • A Financial Model of the Corporation 7

The Financial Balance Sheet

Sources of Financing

• Fixed claims (for example, accounts payable, short-term loans, bonds)

• Residual claims (for example, common stock)

FINANCIAL BALANCE SHEETSources of financing, including fixed and residual claims, are recorded on the right-hand side of the financial balance sheet.

FIGURE 1.2

Fixed claims, like bonds, bank loans,and wages payable, are entitled to afixed payment and receive their pay-ments prior to any payments to theowners of the business.

Besides legal recourse for payment, a distinguishing characteristic of fixedclaims is that, if the firm is extraordinarily profitable in any period, the fixedclaimants receive no more than the amount they are owed. For example, when abusiness has a good year, no bank expects the firm to repay more than the amountof the loan and accrued interest. Fixed claims, therefore, have legal protectionagainst losses but do not share in profits. The amount of a fixed claim is limitedto the amount of the loan or the value of the resources provided to the firm.

Even with legal protection, fixed claimants still are exposed to the risk of loss.There is no guarantee that normal business or even a forced liquidation of a firmwill generate enough cash to satisfy all of the fixed claims. Fixed claim investorsassess the likelihood of loss when arranging the terms of loans to the corporation.

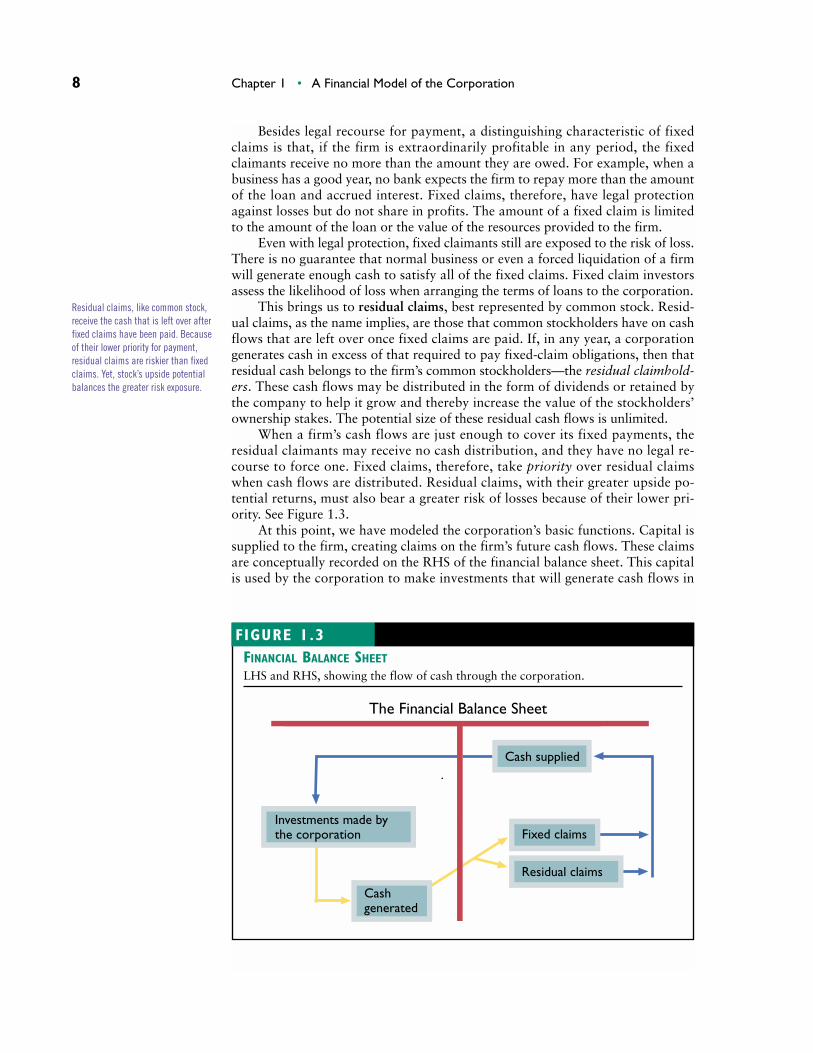

This brings us to residual claims, best represented by common stock. Resid-ual claims, as the name implies, are those that common stockholders have on cashflows that are left over once fixed claims are paid. If, in any year, a corporationgenerates cash in excess of that required to pay fixed-claim obligations, then thatresidual cash belongs to the firm’s common stockholders—the residual claimhold-ers. These cash flows may be distributed in the form of dividends or retained bythe company to help it grow and thereby increase the value of the stockholders’ownership stakes. The potential size of these residual cash flows is unlimited.

When a firm’s cash flows are just enough to cover its fixed payments, theresidual claimants may receive no cash distribution, and they have no legal re-course to force one. Fixed claims, therefore, take priority over residual claimswhen cash flows are distributed. Residual claims, with their greater upside po-tential returns, must also bear a greater risk of losses because of their lower pri-ority. See Figure 1.3.

At this point, we have modeled the corporation’s basic functions. Capital issupplied to the firm, creating claims on the firm’s future cash flows. These claimsare conceptually recorded on the RHS of the financial balance sheet. This capitalis used by the corporation to make investments that will generate cash flows in

Chapter 1 • A Financial Model of the Corporation8

Investments made bythe corporation Fixed claims

Residual claims

Cash supplied

Cashgenerated

The Financial Balance Sheet

FINANCIAL BALANCE SHEETLHS and RHS, showing the flow of cash through the corporation.

FIGURE 1.3

Residual claims, like common stock,receive the cash that is left over afterfixed claims have been paid. Becauseof their lower priority for payment,residual claims are riskier than fixedclaims. Yet, stock’s upside potentialbalances the greater risk exposure.

the future. These investments are shown on the LHS of the financial balancesheet, and the cash flows they generate will be distributed to claimants who havesupplied capital to the corporation or reinvested in the company.

Three Major Distinctions: The Financial BalanceSheet versus the Accounting Balance SheetWe must pause to highlight three features of finance that differ from accounting,as shown in Exhibit 1.1. First, finance focuses on cash flows, while accountingfocuses on profit or net income. You should remember that accounting net in-come includes deductions that involve no outlay of cash—depreciation being theclassic example. A corporation, therefore, may have an accounting loss in a year(negative net income), yet the firm may have generated enough cash flow to meetits fixed claims and, perhaps, even make cash distributions to its residualclaimants. Thus, we focus on cash in finance because ultimately only cash canpay the bills or be invested.

A second distinguishing feature is that accountants record the historical costof assets on the LHS and the historical amount of capital contributed in the RHSaccounts. In finance, we are more concerned with the current value of these ac-counts. An example illustrates why. Consider a firm that invested in undevelopedreal estate in downtown Houston in 1950. If the property cost $10,000 in 1950, itwould appear on the LHS of 2000’s accounting balance sheet at its original cost of$10,000. What is its true value? The current value might be $1,000,000. Whichfigure is relevant for decision-making purposes? The opposite sometimes holdstrue as well: A manufacturer may have an inventory of stereos with cassette play-ers in which it historically invested $1,000,000, but today stereos with CD playersdominate the market. What is the current value of these cassette stereos—morethan the original $1,000,000 investment or less? Again, which number is relevant?

The third point we want to make is that an accounting balance sheet is read-ily available for all to see, whereas the financial balance sheet is a conceptualconstruct—you won’t find it printed in an annual report. Sharp managers andfinancial analysts, however, have a clear mental picture of the FBS and under-stand how decisions will affect its accounts. The development of that same men-tal picture and intuition is one of the objectives of this course.

Chapter 1 • A Financial Model of the Corporation 9

Understanding the differences be-tween the financial balance sheet andthe accounting balance sheet is agood first step toward understandingthe way financial managers and ana-lysts view the business world.

KEY DIFFERENCES BETWEEN ACCOUNTING STATEMENTS AND THE FINANCIALBALANCE SHEET

ACCOUNTING FOCUS FINANCIAL FOCUS

1.Net income, profits, earnings. 1.Cash flows.2.Records assets at their historical 2.Records the current values of LHS

cost and claims at the historical investments made by the firm andamount contributed. the current value of RHS claims.

3.Reported in audited financial 3.Not observable; its condition is statements. determined by analysis. Accounting

statements act as clues, or evidence, of the true financial condition of the corporation.

EXHIBIT 1.1

Acquisition of CapitalLet us return to the financial balance sheet. The cash invested by the corporation,reflected on the LHS of the financial balance sheet, is raised by the firm via threemethods. (See Figure 1.4.) The first method is spontaneously generated loans ortrade credit such as payables to suppliers or employees, and taxes payable. Thefirm has LHS investments, such as inventory, a portion of whose costs are bornefor a period by suppliers who do not demand immediate payment. These typesof fixed claims held by suppliers are usually short term in nature. They are spon-taneous because the firm does not have to seek approval for such loans formallyeach time the credit is granted.

The second method of raising cash is issuing and selling securities to individ-uals and institutions. Firms are able to attract this capital because LHS invest-ments are expected to yield returns that are as attractive or more attractive thanalternative investment opportunities available to these suppliers of capital. Suchsecurities may represent fixed claims on cash flows, such as bonds and bankloans, or common stock that represents a residual claim. Notes payable are short-term fixed claims, term loans are usually intermediate-term, and bonds generallyare long term. Common stock is a perpetual claim, because it might never be re-paid by the corporation.

Once issued and sold, the corporation’s outstanding securities, particularlyits stock and long-term bonds, are actively traded among individual and institu-tional investors. Such trading produces changes in the prices of the firm’s out-standing securities, reflecting either changes in the attractiveness of competinginvestments or changes in investors’ expectations of the returns the firm’s invest-ments will generate, or a combination of both factors. This secondary trading ofsecurities produces no additional capital for the firm, but it reflects the traders’refined opinions of the firm’s value and so acts as a measure of how investors re-gard the corporation’s future prospects.

The final method for acquiring capital is through the retention of residualcash flows. These cash flows belong to the stockholders, but the firm may choosenot to pay out all of this cash as dividends, deciding instead to retain the cashand reinvest it in promising LHS projects.

It is convenient to view the corporation as a conduit that acquires capitalfrom individual and institutional investors and invests this capital in promisingprojects on behalf of these claimants. Subsequent buying and selling of the cor-poration’s securities produces changes in the prices of these claims.

Chapter 1 • A Financial Model of the Corporation10

ACCOUNTING

Finance in the Firm

The trend in accounting has been toward nar-rowing the differences between financial and ac-counting perspectives. For example, several yearsago the Statement of Changes in Working Capi-tal was replaced by the Statement of Cash Flows.Within financial reports, some investments andsecurities must now be valued at their fair valuerather than their historical cost, according to gen-

erally accepted accounting principles. Interest-ingly, when market prices are available, thesesatisfy the definition of fair value. The FinancialAccounting Standards Board (FASB) requires dis-closure of the fair value of certain financial in-struments in Statement 107. To learn more aboutthe current initiatives and trends in financial ac-counting, visit http://www.fasb.org.

The three most important methodsused by firms to finance their needsare trade credit, selling securities (in-cluding loans), and retained residualcash flows.

The United States’ national and OTCexchanges support extensive Websites where they describe themselves,the stocks they trade, how to becomelisted on their exchanges, and so on.Visit http://www.nyse.com,http://www.amex.com, orhttp://www.nasdaq.com.

These price changes produce no capital for the firm, but nonetheless play animportant role in corporate finances. Price changes reflect claimants’ ongoingjudgment regarding the attractiveness of the LHS investments, the value of whichunderlies the prices of the RHS claims. The prices of the firm’s securities act ason-going “report cards” on the effectiveness of the corporation’s decision mak-ing and management. Increases in the prices of traded claims provide claimantswith increases in wealth. Price appreciation, along with payments received di-rectly from the corporation (i.e. dividends and interest), provide investors with areturn on their investment in corporate securities.

The Financial Goal of the CorporationThe financial balance sheet models the corporation’s financial activities. In thefollowing section, these activities are linked to management’s goal. Because man-agers direct the corporation, they must have a clear understanding of the corpo-rate goal. They must understand for whom they work and what their job is ifthey are to be effective.

Chapter 1 • A Financial Model of the Corporation 11

The Financial Balance Sheet

1. Spontaneously generated financing (for example, payables)

2. Issue and sale of securities (for example, notes, loans, bonds, stock)

Investments made bythe corporation

3. Retained and reinvested residual cash flows

Cash flowsgeneratedby thecorporation’sinvestments

Cash toclaimants

THREE METHODS OF CAPITAL ACQUISITION

FIGURE 1.4

Management’s JobManagers make two types of important financial decisions (see Figure 1.5).First, managers choose which investments the firm makes (LHS decisions).Second, managers choose the sources of capital used to finance these invest-ments (RHS decisions). What should managers’ objectives be as they makethese decisions?

To help us answer this question, recall that a corporation’s managementteam operates the company on behalf of its owners, the stockholders. Stockhold-ers invest their money and accept the risk of being a residual claimant becausethey hope the value of their investment will grow; that is, shareholders invest toincrease their wealth. Therefore, as employees of the stockholders, managersmust make decisions that they expect will increase shareholder wealth. Figure 1.6illustrates the basic control mechanisms and rights that fixed and residualclaimants have in the corporate structure. This system of control is known ascorporate governance. Note that fixed claimants are protected by law. If they arenot paid as promised, these claimants can sue the corporation for the money thatthey are owed. Residual claimants have no such rights. The protection for resid-ual claimants is their ownership, which enables them to elect the board of direc-tors who may, for example, fire management if such action is judged to be in theshareholders’ best interest.

The job of managers, as employees of the stockholders, is to maximize thewealth of these residual claimants. If the cash generated by productive LHS in-vestments is to be large enough to flow to residual claims, there must also bemore than enough cash to satisfy the fixed claims. Therefore, maximizing share-holder wealth will generally be in the interest of fixed claimants as well.

Chapter 1 • A Financial Model of the Corporation12

Management

Left-hand side decisions:Which investment shouldbe made?

• Build a new factory?

• Increase expenditures on employee training?

• Develop a new product or service?

Right-hand side decisions:How should neededfinancing be acquired?

• A bank loan?

• Sell bonds?

• Retain cash flow?

• A mix of these?

Two types of managerial decisions correspond to the LHS and RHS of the financialbalance sheet.

FIGURE 1.5

The maximization of shareholderwealth is the goal of management.

Creating WealthManagers can meet their objective of maximizing shareholder wealth by makinginvestments (on the LHS) whose value is greater than the amount of capital uti-lized (from the RHS) to finance these investments. Therefore, managers musthave the ability to assess the value of potential LHS investments and to make thelowest cost RHS capital-acquisition decision.

Let’s illustrate wealth creation with a very simple example. Consider a firmthat has the opportunity to invest in a single project whose value is greater thanits cost. At the end of this project, the firm will be liquidated and all cash distrib-uted to the claimants. Management correctly identifies the attractive project andfinds sources of capital to finance the cost of the project. The investment is madeand almost instantly generates the expected cash flows. Because the value of theinvestment is greater than its cost, the cash flows more than cover the amountnecessary to repay all of both the fixed claims and residual claims used to financethe project. Because the project has more value than cost, there are funds leftover once all claims are repaid. These additional funds accrue to the residualclaimants. These leftover or residual cash flows, therefore, increase stockholders’wealth beyond that originally contributed to finance the project. Exhibit 1.2 il-lustrates this wealth-building process.

If this project’s payoff was certain, investors had full access to all informa-tion regarding the project, and the payoff was almost immediate, then shareholderwealth would increase as soon as the investment in the project was made—evenbefore the cash flows were distributed. Recall that stock, once issued and sold bythe corporation, is traded among individuals. These investors set the price of thestock based on their beliefs regarding the security’s attractiveness. If they knew,with certainty, the stock for which they paid $50 a share would soon distribute$54 a share, what would be the value of that stock to the investors? Clearly, theprice of the stock would immediately increase to very near $54 per share. Thus,when the company’s managers make decisions that maximize the wealth of resid-ual claimants, they also maximize the price of the company’s common stock.

Chapter 1 • A Financial Model of the Corporation 13

Legal remedies

Election of directorswho promote and

protect shareholders’interests

Residual claims

Fixed claims

The board hires,fires, compensates

and directsmanagement

ManagementBoard ofdirectors

CORPORATE GOVERNANCE

FIGURE 1.6

This example is greatly simplified, and we will take the rest of the book tofully develop your understanding of wealth creation through corporate decisionmaking. You must learn how the value of an investment project depends not onlyon the size of the cash flows that it is expected to generate (as in our precedingexample), but also on the degree of confidence claimants have that those cashflows will be achieved. In other words, value also depends on the risk associatedwith the investment. Another factor that must be considered when estimatingvalue is the timing of the cash flows that an investment generates. Claimants pre-fer to receive cash flows earlier rather than later. The longer claimants wait for agiven payoff, the less valuable that payoff is to them, all else the same. Last, thevalue of a particular investment also depends on how attractive that investmentis vis-a-vis alternative investments.

Managers must, therefore, consider the size of a project’s expected cashflows, their timing, the riskiness of these cash flows, and the returns available toshareholders on alternative investments as they assess value in pursuit of stock-holder wealth maximization. See Exhibit 1.3.

Information AsymmetryOne of the difficulties claimants have in assessing how well management is doingin achieving its goal of shareholder wealth maximization is a lack of information.In large corporations, neither the board of directors nor the stockholders can re-view all of management’s decisions. Thus, managers have much more informa-tion than those individuals who are not involved in the day-to-day operations ofthe firm. This relationship is characterized as information asymmetry betweencorporate insiders and outsiders because the two groups do not have equal (orsymmetric) information. Managers, as insiders, have a pretty clear view of boththe RHS and the LHS of the financial balance sheet. Claimants who are not alsoemployees of the corporation can observe the RHS sources of capital, becausemost of these claims are represented by actively traded securities (bonds andstocks), but LHS investments may only be viewed obscurely. Thus, outsidershave less information to use in drawing conclusions about the value of the activ-ities of the corporation than do insiders. See Figure 1.7.

Chapter 1 • A Financial Model of the Corporation14

A THREE-MINUTE CORPORATION ILLUSTRATING THE WEALTH-BUILDING PROCESS

Minute 0A project is identified requiring a $100 investment by the firm.The project will produce $105 in cash flows 1 minute after the firm makes itsinvestment.

Minute 1Sources of capital are identified:

A 1-minute loan of $50 bearing an interest rate of $1 per minute.Stock can be sold for $50.

Minute 2$100 of capital is raised from the two sources.The $100 investment in the project is made by the firm.

Minute 3The project generates the $105 cash flow.The fixed claim of $51 is paid in full: $50 principal repayment and $1 interest.The residual cash flow of $54 is paid to stockholders, increasing their wealth by $4.

EXHIBIT 1.2

Value depends on the size of aninvestment’s expected cash flows, theriskiness of those cash flows, theirtiming, and the attractiveness of al-ternative investments.

Information asymmetry occurs whencorporate managers (insiders) knowmore about the firm than do outsideinvestors.

The degree of information asymmetry is largely dependent on the size, com-plexity, and organizational structure of the corporation. Large, widely-held cor-porations with stock held by millions of investors are characterized by a sepa-ration of ownership (held by the common stockholders) and control (held bymanagers). Stockholders of such giant companies individually own a very smallproportion of the corporation; thus they have little incentive to closely scrutinizemanagerial action. Additionally, with such a small stake, individual shareholdershave little voting power with which to affect a change if they are dissatisfied withthe management and the board. These shareholders tend to simply sell their

Chapter 1 • A Financial Model of the Corporation 15

FACTORS DETERMINING AN INVESTMENT’S VALUE

FACTORS AFFECTING VALUE THEIR EFFECT ON VALUE

1.The expected level of cash flows 1.The higher the expected cash flows, the higher the value of the invest-ment, all else being the same.

2.The riskiness of cash flows 2.The more uncertain are the expected cash flows, the lower the value of theinvestment, all else being the same.

3.The timing of cash flows 3.The longer it takes to receive the cashflows, the lower the value of the investment, all else being the same.

4.The returns available on alternative, 4. If other similar investments offer similar investments higher returns, the less valuable is the

investment, all else being the same.

EXHIBIT 1.3

Investments made by the firm

Fixed claims

Residual claims

Insiders

Outsiders

ASYMMETRY OF INFORMATION BETWEEN CORPORATE INSIDERS AND OUTSIDERS

FIGURE 1.7

shares in the corporation if they are unhappy. Such large organizations tend tohave a relatively large degree of information asymmetry.

Small, closely-held corporations often have fewer shareholders, each havinga large financial stake in the firm. These claimants have a greater incentive tomonitor decision making. The closer scrutiny of outsiders reduces the degree ofinformation asymmetry. In the extreme case, insiders may own a very large stakein the corporation and information asymmetry is minimized. Many small busi-nesses are organized as corporations. Often there is only one residual claimant,who holds all of the common stock and also manages the business. In such acase, there is no information asymmetry between management and the residualclaimant because they are one and the same. Even here, some asymmetry existsbecause fixed claimants remain corporate outsiders (e.g., suppliers and bankers)and so have less information about the company than does the owner/manager.

There are costs associated with information asymmetry. Corporate insiders,for example, may trade the firm’s outstanding securities and reap huge profitsbased on their superior knowledge of the firm’s prospects. The cost associated withinsider trading would eventually be borne by society. Outsiders would soon losefaith in the fairness of trading the company’s securities because of their informa-tion disadvantage. The ability of the firm to raise capital would be hampered as po-tential capital suppliers became reluctant to commit their funds for fear they werepaying too much. Lack of financing would leave promising investment projects un-touched, leading to a stagnant economy or one in decline. To protect the integrityand fairness of the security markets, society has legislated strict regulations on thetrading of corporate securities by insiders. Ivan Boesky, a celebrated securitiestrader, was sent to prison as a result of his violations of insider trading laws.

Other information asymmetry costs are borne by the corporation. A goodexample is audited financial statements. Corporations hire reputable accountingfirms to examine and, following well-defined standards, attest to the accuracy ofinformation reported by insiders (the firm’s management). Banks supplying fi-nancing to the corporation generally require that certain conditions be met bythe firm throughout the life of the loan. For example, to ensure that these protec-tive covenants are being met, banks may require that the firm regularly provideaudited financial statements. Such statements reduce information asymmetry be-tween the firm and these fixed claimants. Restrictive covenants are also includedin bond agreements, while audited financial statements are a reporting require-ment for virtually all actively traded corporate securities.

In the 1980s an interesting phenomenon took place with a frequency neverbefore seen. Many large, complex, and widely held corporations’ stocks were pur-chased in their entirety by relatively small groups of individuals or institutions ina process known as a leveraged buy-out. In essence, widely held firms were trans-formed into closely held firms. One important rationale for these billion-dollartransactions was the reduction of information asymmetry. How can a reductionof this information gap translate into the wealth creation that apparently moti-vated these megadeals?

Agency CostsTo answer that question, we must more fully understand the costs that accompanyinformation asymmetry and the separation of ownership and control. As we notedearlier, managers control the firm, whereas shareholders own the firm. Managersare acting as the agents of the firm’s principals or owners. Managers are hired toact on the owners’ behalf, maximizing shareholders’ wealth and—in the process—

Chapter 1 • A Financial Model of the Corporation16

satisfying the corporation’s fixed obligations. However, managers are also con-cerned with their own welfare and act in their own self-interest. At times managers,acting to satisfy their own desires, may take actions that are costly to claimants yetproduce no wealth for these suppliers of capital. Such actions may be character-ized as investments whose value is less than their cost and are, therefore, in directconflict with the goal of maximizing shareholder wealth. Some corporate expendi-tures on perquisites may contradict shareholder wealth maximization.

Perquisites (or perks) are benefits to employees beyond their compensationpackages and are often cost-effective investments. Many executives, for example,are supplied a company-owned car. Shareholders may benefit from such invest-ment—it may be less costly to supply the corporate president with a vehicle thanto reimburse her for mileage. The company-owned car also assures stockholdersthat the corporate reputation for being a quality institution is enhanced by hav-ing clients met in a clean, comfortable mode of transportation. On the otherhand, what if the president of the firm is supplied with a $200,000 Rolls-Roycerather than a $40,000 Lincoln? Will the decision to supply her with the Rollsproduce additional value greater than the cost differential of $160,000? TheRolls seems to be a questionable investment. This is an example of an excessiveperquisite, an expense that benefits an executive while producing no increase inshareholder wealth. On whose judgment does the authorization of such expensesfall? Ordinarily management makes these decisions. This is an example of anagency cost, a cost that arises because of the separation of principals and agentsin large corporations (see Figure 1.8).

Another source of agency costs is shirking by top management. A corpora-tion’s top managers are selected and highly compensated because the board feelsthey have the talent and will expend the effort to seek out value-creating invest-ment projects. But only the managers know precisely how much effort they aredirecting to their job. Since managerial effort is difficult to monitor, managerscan reduce their efforts (i.e., shirk) and thereby generate costs for shareholders

Chapter 1 • A Financial Model of the Corporation 17

Agency costs, such as excessive perks,shirking, and empire building, lowerfirm value as they waste cash.

Agencycosts

Waste

Management

Retainedcash

Factory Cash flowgenerated To claimants

$

$

$

$

Investments madeby the corporation

Sources of financing

AGENCY COSTSThe agency problem creates costs for the business, wasting corporate resources.

FIGURE 1.8

with no offsetting benefits. Such managers may choose to take a three-hourlunch, for which they are richly compensated, but which produces no increase inshareholder wealth. Shirking by top management sets a costly example becausethe behavior may percolate down through the corporation.

Studies have shown that top executives’ pay is positively correlated with thesize of the corporation. Some incentive, therefore, exists for chief executive offi-cers (CEOs) to engage in empire building. A firm may expand in size (add LHSinvestments) with less regard to the value of these investments than to the impactthat a larger firm has on the CEO’s pay, power, and prestige. Empire-building hasbeen documented as one of the most damaging agency costs in its impact onshareholder wealth.

An important characteristic of these examples of the agency problem is thatthey would not exist if information asymmetry did not also exist. The megamerg-ers of the 1980s often were economically linked to the reduction of agency costs.By replacing wasteful management, by increasing the accountability of manage-ment to a smaller group of claimants whose stake was high enough to motivateclose monitoring of the firm, and through dismantling ill-conceived and ineffi-cient empires, wealth gains were achieved as many corporations became closelyheld through buy-outs in the 1980s.

Competing Organizational FormsEven with the problems inherent in the widely held corporation—problems suchas information asymmetry and agency costs—the modern corporation dominatesthe economic landscape in several key respects. The bulk of domestic sales (90%)and profits (80%)1 are generated by the corporate form of business organization.

To be sure, sole proprietorships and partnerships are also important—theyperhaps best embody the entrepreneurial spirit and often are the spawningground for major corporate entities. Proprietorships and partnerships also haveless significant agency problems than do widely held corporations. These organi-zational forms are also attractive because of their relatively low organizationalcosts, and their owners may benefit from lower taxes. (See Exhibit 1.4.) Corpo-rate cash flows to residual claimants (dividends) are subject to double taxation—once at the corporate level and again at the individual level—while proprietor-ship and partnership income is taxed only once as part of the owner’s personaltax return.

But the corporation has attributes that offset the advantages of proprietor-ships and partnerships. These attributes are particularly important for largefirms, requiring large amounts of capital. To raise the huge sums necessary tofinance large-scale businesses, entities must accept the difficulties inherent inthe separation of ownership and control because there are few individual in-vestors with sufficient personal wealth the expertise and the willingness to bothown and manage a corporate giant. Thus, to finance big businesses it is oftennecessary to have many owners (stockholders) who are willing to relinquishcontrol to hired managers. Now let us consider the characteristics of the cor-porate form of organization that enable it to dominate alternative organiza-tional structures.

First, through the issuance of common stock, a highly transferable security isused as the medium for exchanging ownership interests in the business. The abil-

Chapter 1 • A Financial Model of the Corporation18

1U.S. Bureau of the Census, Statistical Abstract of the United States, 1990, 110th edition, p. 521.

Proprietorships and partnerships havelower organizational costs and tax ad-vantages compared to corporations.

ity of stockholders to sell their shares easily is important if individuals are to bepersuaded to take an ownership interest in a firm over which they have limitedcontrol. Such claimants, as mentioned earlier, can “vote with their feet,” sellingtheir shares when they wish. Moreover, if many stockholders become dissatisfied,then selling pressure, behaving in accordance with the law of supply and demand,will drive down share prices. The supply of such a corporation’s stock availablefor sale on the secondary market will increase while demand for the securities de-creases. This decline in the price of the corporation’s securities indicates to theboard of directors that action needs to be taken. By contrast, partnership andproprietorship ownership interests are less transferable and marketable. For ex-ample, partnerships often require the approval of remaining partners before a dis-sident partner can sell his or her interest to a third party. In the end, many part-ners are stuck with their investment and powerless to change it. Thus the easewith which stock may be bought and sold (its marketability) is a strong advan-tage of the corporation, aiding its ability to raise capital when compared to alter-native business forms.

A second contrasting characteristic is the liability of owners. Sole propri-etors and partners (with the exception of limited partners—see Exhibit 1.5) risknot only their original investments in a business but must stand ready to use theirpersonal resources to meet any shortfall the enterprise experiences in meeting itsfixed obligations. For example, a large legal judgment against a proprietorshipor partnership may lead to the personal bankruptcy of its owners. This is not thecase with the corporate form of organization. Stockholders have limited liability,meaning that they can lose no more than the amount they have invested in thestock. In a corporation, residual claimants cannot be forced to make up short-falls in meeting fixed claims once corporate assets have been fully liquidated.Again, this corporate attribute is especially critical in larger firms with diffuseownership. Few individuals would be willing to expose their resources to risk,without direct control over how those capital contributions are utilized, if theirliability is unlimited.

The last advantage of the corporate form is its conceptually unlimited life.Partnerships depend on a team acting as both owners and managers. Like anyteam, the loss of a key player or players can destroy its effectiveness. In propri-etorships this difficulty is exacerbated because the team consists of one player,the loss of whom completely changes the character of the entity. To replace

Chapter 1 • A Financial Model of the Corporation 19

The corporate form of business orga-nization offers owners limited liabilityand more marketability than do pro-prietorships or partnerships.

TAX ADVANTAGE OF PARTNERSHIPS AND PROPRIETORSHIPS

Assuming a corporate tax rate of 20% and a personal tax rate of 25%, it is clearthat corporations’ owners are at a disadvantage taxwise because their income is subject to double taxation.

PARTNERSHIPS ANDPROPRIETORSHIPS CORPORATIONS

Income before business-level taxes $1000 $1000Income tax rate at the business level 0% 20%Income tax payable at the business level $0 $200Income to owners before personal income taxes $1000 $800Personal income tax rate 25% 25%Personal income taxes owed $250 $200After-tax cash flow to owners $750 $600

EXHIBIT 1.4

players in partnerships or proprietorships, an individual must be sought withthe wealth, expertise, and willingness to be both a manager and an owner. Ifsuch an individual cannot be located, the business must be liquidated. Corpo-rations, on the other hand, are faced with less critical problems of this nature.Replacing lost owners is relatively simple because of marketability of the stock,as already discussed. Loss of key management personnel, although potentiallydifficult, is less of a problem than it is in other organizational forms because thereplacement does not necessarily also need to become a major owner, as a pro-prietorship or partnership requires.

Over the past century advances in technology, more cost-effective means oftransportation and distribution, communications advances, a rising standard ofliving, and the globalization of markets have provided many investment oppor-tunities for corporations, requiring large amounts of capital to finance theirgrowth. Organizations have sought the most efficient means of meeting theseneeds. Many would argue that the advantages of corporate organizational formsoutweigh the disadvantages as firms become large. Witness their dominance.

Corporations and SocietyThe relative efficiency of the corporate form of organization has led to it being thestructure of choice for firms foreseeing attractive growth opportunities. The effi-ciency of corporations has led to criticism as well. Corporations are often por-trayed as cold-hearted in their pursuit of economic gains. They are charged withignoring the communities in which they operate, lacking concern for the welfare oftheir customers, and even ignoring the planet in their relentless pursuit of profits.

Chapter 1 • A Financial Model of the Corporation20

Some key characteristics of the forms of business organization are contrasted for corporations, partnerships, andproprietorships.

CORPORATIONS1,2 PARTNERSHIPS3 PROPRIETORSHIPS

Taxation Twice, once at the busi- Once at the individual Once at the individual ness level, once at the level levelindividual level

Liability Limited to the amount Unlimited Unlimitedinvested

Ownership and control Separated, majority of Partners own and By definition, ownership stockholders are not control the enterprise and control are in the usually managers hands of a single

individualTransferability of Relatively easy through Potentially difficult Potentially difficult

ownership sale of stockAccess to capital Best Moderate Most restrictiveInformation asymmetry Potentially high Relatively low if all Very little, because there is

and agency costs partners are equal no separation of owner- and active ship and control

1S corporations differ in that they are treated much like partnerships. S corporations’ business-level income flows to the individ-ual tax returns without business-level taxation.2Closely held corporations are similar to partnerships except in the area of taxation and liability.3Limited partnerships are managed by a general partner, and limited partners have limited liability. In limited partnerships, therecan be high agency costs because the general partner is acting as the limited partners’ agent. Thus, limited partners are much likestockholders except in the areas of taxation, transferability, and access to capital.

EXHIBIT 1.5

Some critics of corporations charge that the goal of shareholder wealth max-imization is too narrow for the good of society. These critics contend that corpo-rations should act in a socially responsible manner. Although social responsibil-ity has different meanings to different people, circumstances do indeed existwhen the good of society is at odds with the welfare of corporate shareholders.For example, in its manufacturing endeavors a firm may produce externalities,such as air pollution, while the cost of cleaning up this dirty air may be borne notby the corporation but by society. Thus, shareholders receive higher returns associety bears some of the costs of producing the product.

These charges are often true on a case-by-case basis and must be taken seri-ously by all corporations, even nonoffenders, because corporations as legal enti-ties exist at the pleasure of society. Should society see pervasive abuses, it willsurely restrict the freedom of corporations to act.

Businesses, and corporations in particular, are remarkably resilient. Abusesof labor, unethical securities practices, and consumer fraud have led to major leg-islative initiatives during the last century that restricted the freedom of firms. Yetthe competitive drive toward shareholder wealth maximization allowed corpora-tions to meet society’s legal mandates and continue to thrive. It is this goal, com-bined with marketplace competition, which has allowed businesses in our soci-ety to produce ever-higher standards of living. Compare our economy with thosein which other goals have supplanted shareholder wealth maximization. Alterna-tive goals, such as the former Soviet Union’s objectives of universal employmentand equal distribution of wealth, have proven to be socially irresponsible in thesense that resources were not put to their best use. Resulting inefficiencies in suchsocieties have not been beneficial to their members. Therefore, the competitivenature of the financial goal, while sometimes producing socially irresponsiblecorporate behavior, is also largely responsible for the economic well-being oursociety enjoys.

SummaryIn this chapter several key concepts that underlie finance were introduced. Theseare the blocks on which the bulk of the course is built. The main points of thechapter are, therefore, important enough to merit repetition here:

• The financial balance sheet was used to illustrate the firm’s capital acquisi-tion and investment activities.

• Residual and fixed claims’ characteristics were discussed, including the prior-ity of claims, default and legal recourse, and voting rights.

• The major distinctions between finance and accounting were drawn.• Shareholder wealth maximization was introduced as the financial goal of the

corporation.• Wealth creation was illustrated as corporate investment in any project whose

value is greater than its cost.• A project’s value was discussed as being dependent on the size of expected

cash flows, the riskiness of those cash flows, their timing, and the returnsavailable on alternative investments of similar risk.

• Agency costs and information asymmetry were discussed as impediments tomaximizing shareholder wealth.

• Competing forms of business organization were compared to the corporateform.

Chapter 1 • A Financial Model of the Corporation 21

Acting in a socially responsible man-ner implies doing what’s best for soci-ety even if the action is at odds withshareholder wealth maximization.

• Corporations were noted to exist at society’s pleasure and must be sensitive tosocial concerns. Overall, economic efficiency and well-being may be the mostimportant products of corporations competing to serve their shareholders.

Also covered were characteristics of bonds (coupon payments, par value, etc.),characteristics of stock (dividends, etc.), and assumptions about the way peopletend to behave (rational self-interest). Taken altogether, the topics in Chapter 1have provided an introduction to finance by focusing on the corporation. How-ever, we have yet to look at the environment in which the corporation operates.Chapter 2 discusses how these external factors both challenge corporations andprovide corporations with opportunities. It is in the firm’s products and securi-ties markets that the value of corporate decisions are reflected. Therefore, it isimportant to understand the nature of markets and the impact they have onvalue if future managers hope to be effective in their jobs.

Key Terms

Chapter 1 • A Financial Model of the Corporation22

Questions1. What is the primary goal of financial management?2. Identify at least three characteristics that differ between fixed claims and

residual claims.3. What are the three major distinctions between accounting and finance?4. Identify and discuss the three methods firms have available for raising the

cash used to fund investment projects.5. Identify four factors that determine value.6. Do you think agency cost would tend to increase as information asymmetry

increases between corporate insiders and outsiders? Why?7. Which forms of business organization offer the owners limited liability?8. When McDonald’s began accepting credit cards as payment for their prod-

ucts, the average profit per sale fell because credit card companies charge aservice fee on each charged transaction. If this decision was a good one given

securitiesbondscoupon paymentsface amountpar valuecommon stockdividendsboard of directorsproxyfinancial balance sheettangible and intangible assetsfixed claimsdefaultresidual claimscash flowsspontaneously generated loans trade creditsecondary tradingcorporate governance

maximizing shareholder wealthinformation asymmetryinsidersoutsiderswidely-held corporationseparation of ownership and controlclosely-held corporationsinsider tradingprotective covenantsperquisitesagency costshirkingempire-buildingsole proprietorshipspartnershipslimited partnerslimited liabilitysocial responsibilityexternalities

Chapter 1 • A Financial Model of the Corporation 23

the goal of shareholder wealth maximization, discuss how accepting creditcards could lead to the increase of shareholder wealth despite these fees?

9. If the Disney corporation began producing X-rated movies, the firm wouldrisk destroying its investment in what intangible asset?

10. Do you think that individuals are more socially responsible than corpora-tions? If they are, should corporations contribute some residual cash flows tocharitable causes of the corporation’s choice, or should these cash flows bedistributed to stockholders, who may then make contributions to whom theychoose, if they desire?

11. An investment seems likely to produce cash flows, after all expenses are paid,equal to twice its cost. Does this necessarily mean it’s a good investment?Why or why not? What other factors should be considered?

12. Here is an old joke about limited partnerships: A limited partnership iswhere, at the beginning, the limited partners have the money and the generalpartners have the experience. At the end, the joke goes, the general partnershave the money and the limited partners have the experience. Explain thisjoke in light of the separation of ownership and control, agency costs, andwhat you know about the characteristics of limited partnerships as a form ofbusiness organization.

13. The great majority of stock trades do not involve newly issued stock. Thismeans that investors are buying and selling these shares among themselvesand no new capital is raised for the corporation from these trades. Yet theprice at which a stock trades is important to the firm. Why?

14. A factory appears on an accounting balance sheet at its historical cost of$1,000,000 (disregarding depreciation). Why might such a factory actuallybe worth $10,000,000 or perhaps only $100,000? Make up an exampleshowing why a factory might appear at a higher figure on the financial bal-ance sheet than on an accounting statement and one example why one mightappear on an FBS at a lower figure.

15. Why might a self-interested citizen rationally vote for a tax increase to builda new high school, although this citizen does not have children (and does notintend to have any)?

16. Are all perquisites non–wealth producing? How might you decide if a perk isan agency cost or a cost-effective LHS investment?

17. If an automobile manufacturer contributed $1 million to public television,but did so anonymously, would this be a socially responsible act? Would it bein the shareholders’ best interest?

18. From Question 17, if the automaker made the same contribution and wasgiven publicity for its generosity, was the donation beneficial to sharehold-ers? How would you decide whether the donation and resulting publicitywere a good investment decision?

19. Suppose corporations are taxed at an 18% rate and individuals are taxed at a 30% rate. Now imagine that a business has income before any taxes of$5,000. Compare the after-tax cash flow to the business owner if the enterprisewere organized as a proprietorship, a partnership, and a corporation. Based onafter-tax cash flows, which form of organization should the owner choose?

20. Referring to Question 19, suppose the firm’s product is fireworks. Whenwould an astute owner choose the corporate form of organization in spite ofits disadvantage based on tax arguments?

21. Suppose a manager announces that the firm he directs is going to expand bypurchasing another company. Why won’t this manager state in the announce-ment that he is making the acquisition as part of his empire-building strategy?

Chapter 1 • A Financial Model of the Corporation24

22. In an economically competitive market, we state in the chapter that competi-tion will correct irrational behavior. How does this work? (Hint: Supposethat people are competing for resources. If they consistently pay too much forthe resource, what will happen? If they try to pay too little for the resource,what will happen?)

23. Describe how a firm might invest in building its reputation. How might thatinvestment pay off, creating wealth for the firm’s owners?

24. How might an individual go about building a good reputation? Could such areputation be economically valuable?

25. Calculate the change in shareholder’s wealth for the following three-minutecorporation.Minute Zero: A project costing $500 is identified that will produce cash

flows of $510 one minute after the investment is made.

Minute One: Sources of capital are identified:• A one-minute loan of $300, bearing an interest rate of 1%

per minute• Stock sold for $200

Minute Two: The $500 of capital is raised and the investment in the proj-ect is made.

Minute Three: (You complete)26. Referring to Question 25, if there were no risk associated with this project,

how much would you pay for the stock at minute two (just after it was issued)?27. Corporations often include in their officers’ pay large amounts of stock. Can

you explain the use of this form of compensation as a method for helping tosolve the agency problem described in the chapter?

28. How could each of the following areas of business administration contributeto shareholder wealth?a. Marketingb. Human resource managementc. Production managementd. Accounting

29. Is employee training an investment? Explain your answer.30. If stock prices act as a report card of management’s wealth-building activi-

ties, what would you expect to happen to the value of firms with ongoingagency problems.

31. In light of your answer to Question 30, do you think it could be a profitablestrategy to take over another company that has engaged in empire building?Explain your answer.

Internet ExerciseFor an interesting example of the value of intangible assets, see the site http://www.submerged-ideas.com, which includes a list of the top prices paid for do-main names. You can register a domain name for $14.99 on the site (and maybemake a million!). Try dreaming up a domain name that you think may have value,then use Google.com or some other search engine to see whether it already exists.Note: The best way to access all of the Web addresses listed in this book is to goto the text’s site at http://hickman.swcollege.com and click on Internet Refer-ences. We will update our links if any addresses mentioned in the book change.