37

1 2 3 4 5 6 7 8 9 10 11 Q1 Q2

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 1/37

1

2

3

4

5

6

7

8

9

10

11

Q1

Q2

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 2/37

Q3

Q4

12

13

14

15

Q5

Q6

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 3/37

Q7

16

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 4/37

Please Enter Your Student ID Here ------>

Once you have entered your student ID above, you should see data on the "Data" worksheet. The data consists

of a few monthly time series with month-end dates in column B. The series start in January 2003 and end in

December 2008. There is empty space separating year 2008 from earlier data because you will use earlier data

The first time series in column C is the excess return on the market, that is, the market return minus the risk-free rate. Next, the Fama-French factors: SMB (return on small stocks minus return on big stocks) in column D

and HML (return on high book-to-market stocks minus return on low book-to-market stocks) in column E.

Column F consists of the momentum factor UMD (return on up stocks up in the past minus return on stocks

down in the past. Column G provides the risk-free return in each month.

Columns I to K provide monthly returns for three stocks. You can use any blank area of that worksheet for your

calculations. You can also create and edit other worksheets in this spreadsheet or copy the data to another

spreadsheet for your calcuations. Or if you are comfortable with some other statistical page, you can copy the

First you need to determine the characteristics of your stocks based on the data from 2003-2007. That is, you

have to estimate how does the excess return on each stock return varies with the excess return on the market,

the Fama-French factors, and the momentum factor. Here are the steps:

Calculate in some blank column the excess return on your stock by subtracting the risk-free rate (column G)

from your stock's return (column I, J, or K).

Next perform a regression of the excess return on the 4 factors: excess return on market, SMB, HML, and

UMD. For this, you can use Excel's Data Analysis feature.

There are two ways of running regression in Excel. You can use linest function after reading its description in

help. Or you can use data analysis tool. If you use Excel 2007, please go to data tab and look at the rightmost

column for data analysis. If you don't see that, click the Microsoft Office Button (at top left), and then click

Excel Options. Click Add-Ins, and then in the Manage box, select Excel Add-ins. Click Go. In the Add-Ins available

box, select the Analysis ToolPak check box, and then click OK. After you load the Analysis ToolPak, the Data

Analysis command is available in the Analysis group on the Data tab. If you use a version of Excel earlier thanExcel 2007, please go to tools menu to find "Data Analysis." If you don't see data analysis, please choose "Add-

Do not force constant (intercept) term to be zero. You may specify the regression output to be in the same

worksheet or in a new worksheet.

See the "Example" tab for an example of such a regression. You will need to perform three regressions, one for

each stock. Now answer the following questions:

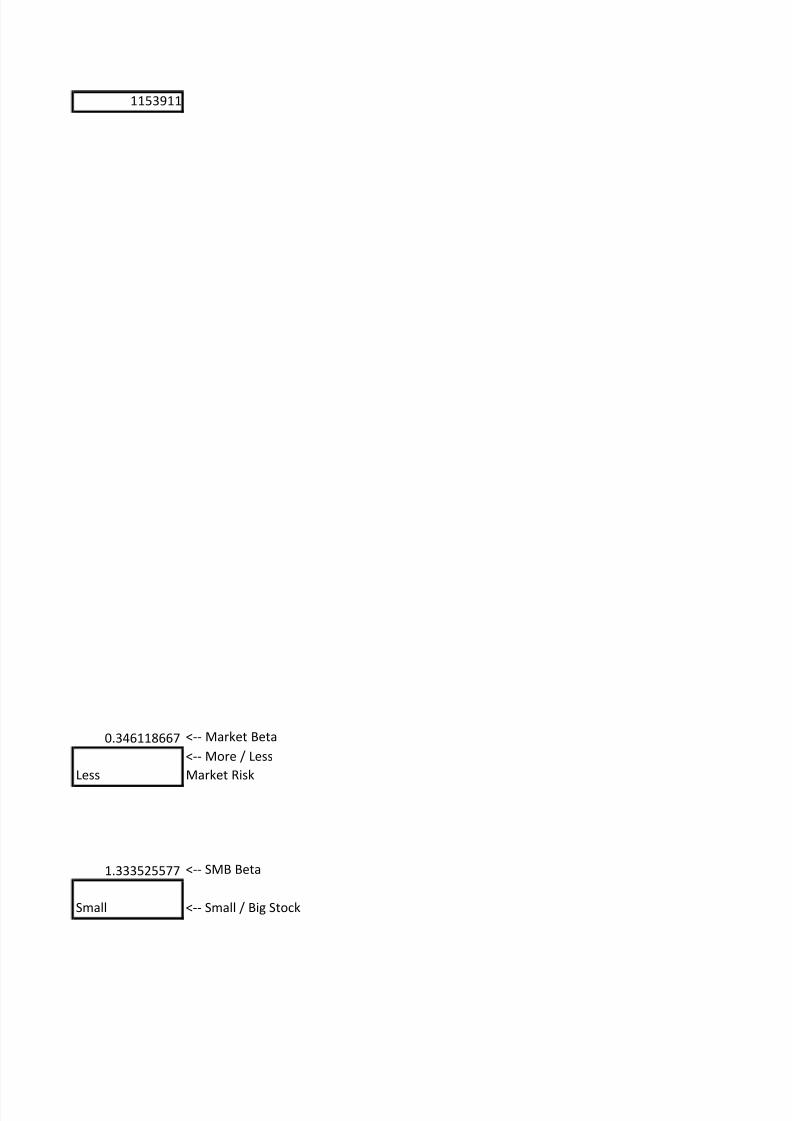

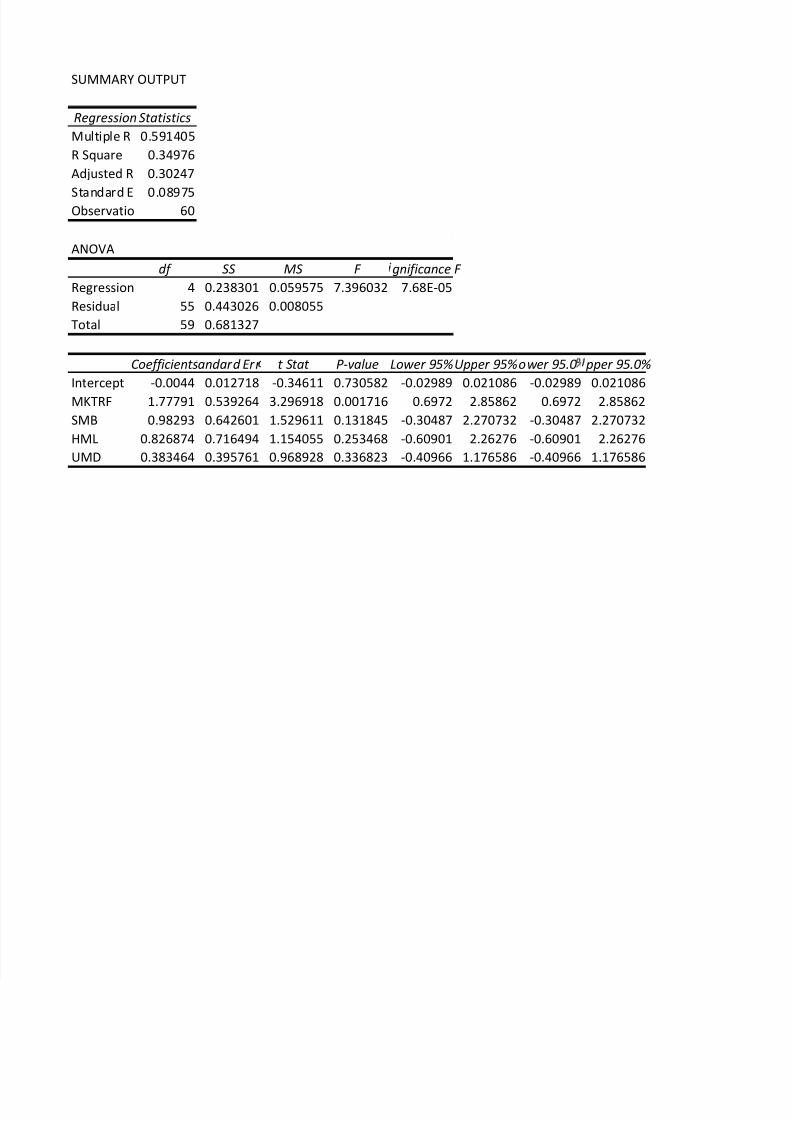

What is WALGREEN CO (WAG)'s market beta? Does it have more market risk or less market risk than an

average stock?

The regression coefficient on SMB factor shows whether the stock acts like a small stock or a big stock and is

called its SMB beta. A positive coefficient suggests that the stock acts more like a small stock than an average

stock while a negative coefficient suggests that the stock acts more like a big stock than an average stock.

What is TIVO INC (TIVO)'s SMB beta? Does it act like a small stock or a big stock?

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 5/37

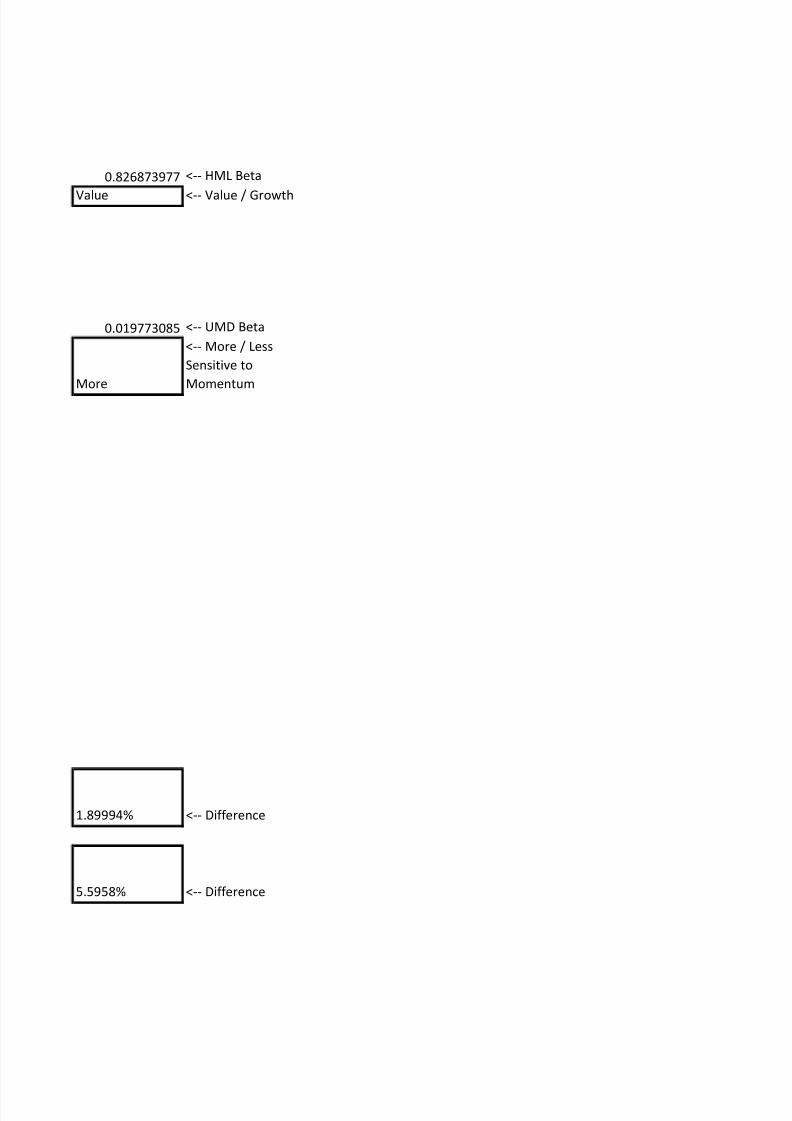

The regression coefficient on HML factor shows whether the stock acts like a value stock with high book-to-

market or a growth stock with low book-to-market ratio and is called its HML beta. A positive coefficient

suggests that the stocks acts more like a value stock than an average stock while a negative coefficient

What is SPSS INC (SPSS)'s HML beta? Does it act like a value stock or a growth stock?

The regression coefficient on UMD factor measures how sensitive the stock's return is to momentum and is

called its momentum beta. A more positive coefficient suggests that the stocks return is more sensitive to

momentum than an average stock while a negative coefficient suggests the stock return is less sensitive to

momentum than an average stock. Sensitivity to momentum means that stock will perform well when

momentum is higher (past winners continue to do well and past losers continue to do poorly) and perform

What is WALGREEN CO (WAG)'s UMD beta? Is it more or less sensitive to momentum than an average stock?

Now, you will test if the regression relation based on data from 2003 to 2007 continues to explain returns in

2008 too. First note that in efficient markets, predicting stock returns is very difficult because the models

predict only the systematic component of return but a significant variation in returns occurs due to

idiosyncratic news which are not incorporated in prediction model. Thus, no model can provide very precise

forecasts. Four factor model is supposed to be one of the better models but even this doesn't work very well at

individual stock level as the model cannot anticipate the events that influence the return of a particular stock.

Since monthly stock returns vary a lot due to idiosyncratic risk, instead of predicting returns in a particular

month, predict average monthly returns for your stocks in 2008. For this, use the regression results and the

average values of the four factors and the risk-free rate in 2008. Note this is not true prediction because we are

First calculate the average monthly value of the four factors and the risk-free rate in 2008 by taking averages of 12 monthly values for each of the columns C to G.

Now calculate predicted average monthly return of a stock by multiplying its market beta with average excess

return on market, multiplying its SMB beta with average SMB value, multiplying HML beta with average HML

value, multiplying UMD beta with average UMD value, adding all four products, adding the intercept from

That is, predicted return = intercept + market beta * average MKTRF + SMB beta * average SMB + HML beta *

average HML + UMD beta * average UMD + average RF

See the "Example" worksheet for an example. Calculate the predicted average monthly return for each stock

and compare it to the actual monthly average return in 2008. Do this for all three stock and answer the

What is the difference between the predicted average monthly return and the actual average monthly return

for WALGREEN CO (WAG)? This captures the size of idiosyncratic component of return. Report only the

magnitude (that is report 0.3456% as 0.3456% and -0.5432% as 0.5432%).

What is the difference between the predicted average monthly return and the actual average monthly return

for TIVO INC (TIVO)? This captures the size of idiosyncratic component of return. Report only the magnitude

(that is report 0.3456% as 0.3456% and -0.5432% as 0.5432%).

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 6/37

What is the difference between the predicted average monthly return and the actual average monthly return

for SPSS INC (SPSS)? This captures the size of idiosyncratic component of return. Report only the magnitude

(that is report 0.3456% as 0.3456% and -0.5432% as 0.5432%).

Save this spreadsheet on a computer and then submit your assignment in Blackboard by uploading this

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 7/37

1153911

0.346118667 <-- Market Beta

Less

<-- More / Less

Market Risk

1.333525577 <-- SMB Beta

Small <-- Small / Big Stock

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 8/37

0.826873977 <-- HML Beta

Value <-- Value / Growth

0.019773085 <-- UMD Beta

More

<-- More / Less

Sensitive to

Momentum

1.89994% <-- Difference

5.5958% <-- Difference

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 9/37

3.90244% <-- Difference

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 10/37

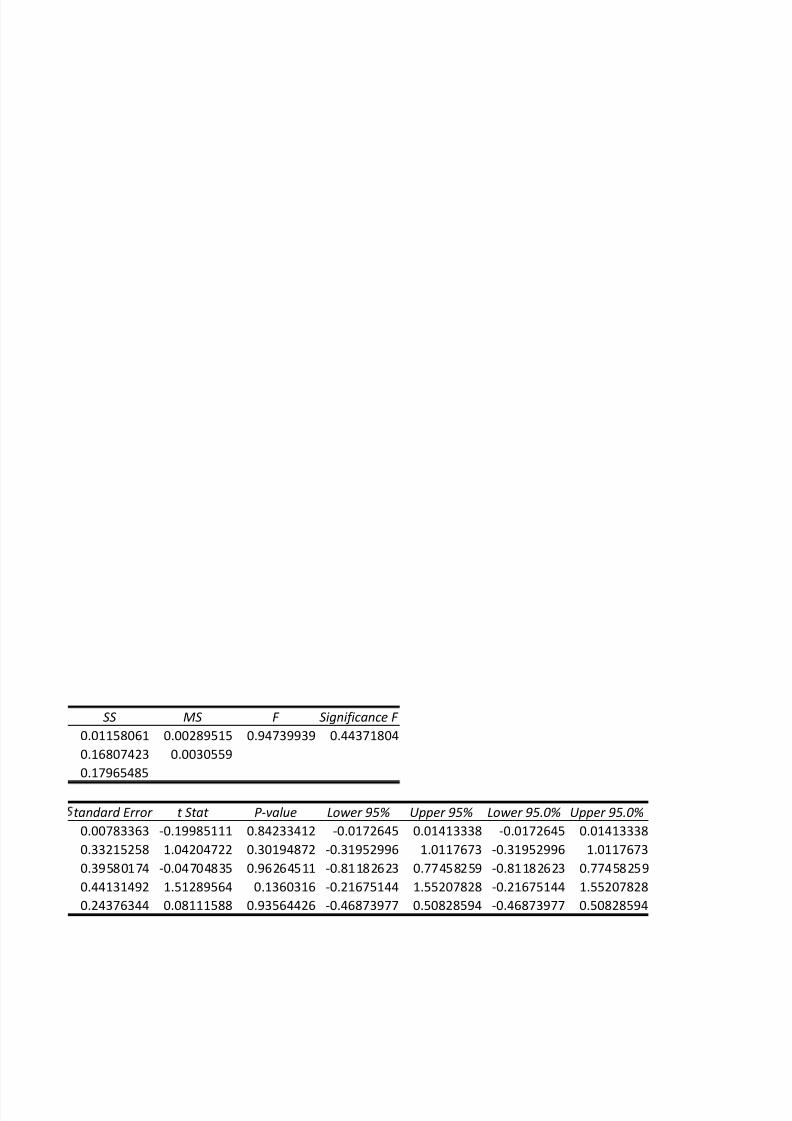

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.25389

R Square 0.06446

Adjusted R -0.00358

Standard E 0.05528Observatio 60

ANOVA

df SS MS F gnificance F

Regression 4 0.011581 0.002895 0.947399 0.443718

Residual 55 0.168074 0.003056

Total 59 0.179655

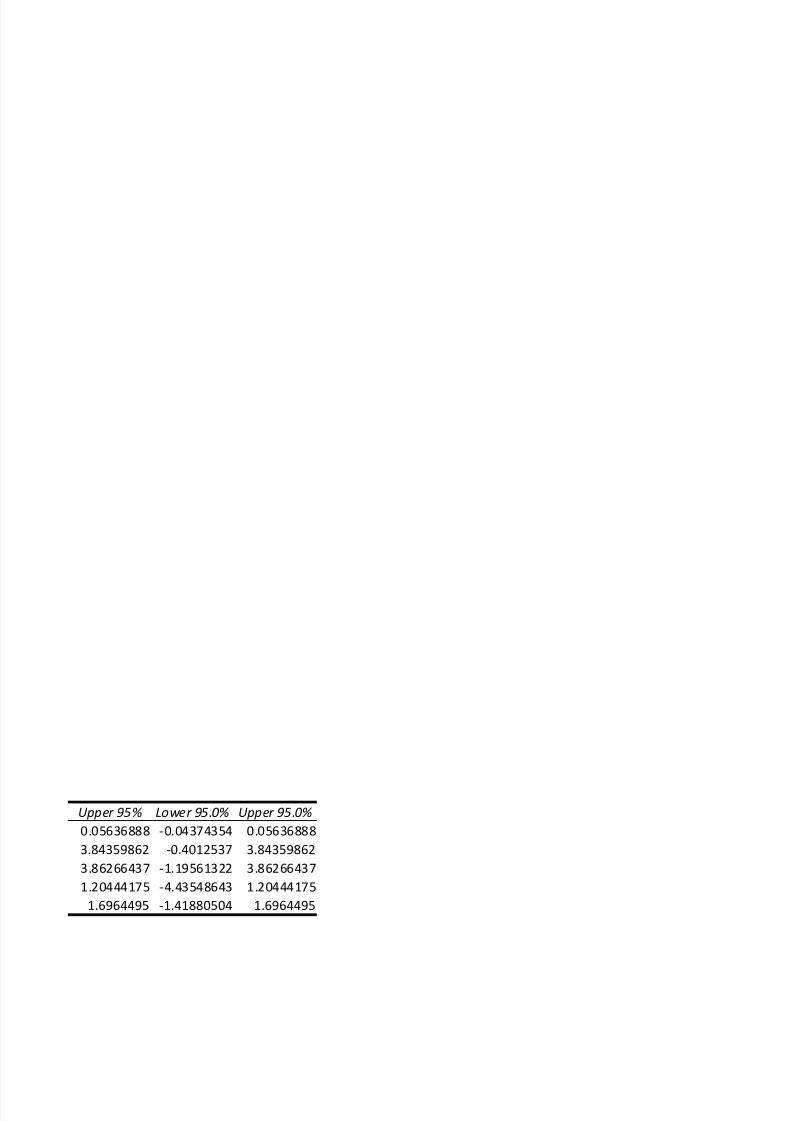

Coefficientsandard Err t Stat P-value Lower 95%Upper 95%ower 95.0 pper 95.0%

Intercept -0.00157 0.007834 -0.19985 0.842334 -0.01726 0.014133 -0.01726 0.014133

MKTRF 0.346119 0.332153 1.042047 0.301949 -0.31953 1.011767 -0.31953 1.011767

SMB -0.01862 0.395802 -0.04705 0.962645 -0.81183 0.774583 -0.81183 0.774583

HML 0.667663 0.441315 1.512896 0.136032 -0.21675 1.552078 -0.21675 1.552078

UMD 0.019773 0.243763 0.081116 0.935644 -0.46874 0.508286 -0.46874 0.508286

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 11/37

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.398899

R Square 0.159121

Adjusted R 0.097966

Standard E 0.176261Observatio 60

ANOVA

df SS MS F gnificance F

Regression 4 0.323347 0.080837 2.601928 0.045774

Residual 55 1.708741 0.031068

Total 59 2.032088

Coefficientsandard Err t Stat P-value Lower 95%Upper 95%ower 95.0 pper 95.0%

Intercept 0.006313 0.024978 0.252733 0.801417 -0.04374 0.056369 -0.04374 0.056369

MKTRF 1.721172 1.059071 1.625172 0.109843 -0.40125 3.843599 -0.40125 3.843599

SMB 1.333526 1.262017 1.056662 0.295285 -1.19561 3.862664 -1.19561 3.862664

HML -1.61552 1.407136 -1.14809 0.2559 -4.43549 1.204442 -4.43549 1.204442

UMD 0.138822 0.777242 0.178609 0.858901 -1.41881 1.69645 -1.41881 1.69645

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 12/37

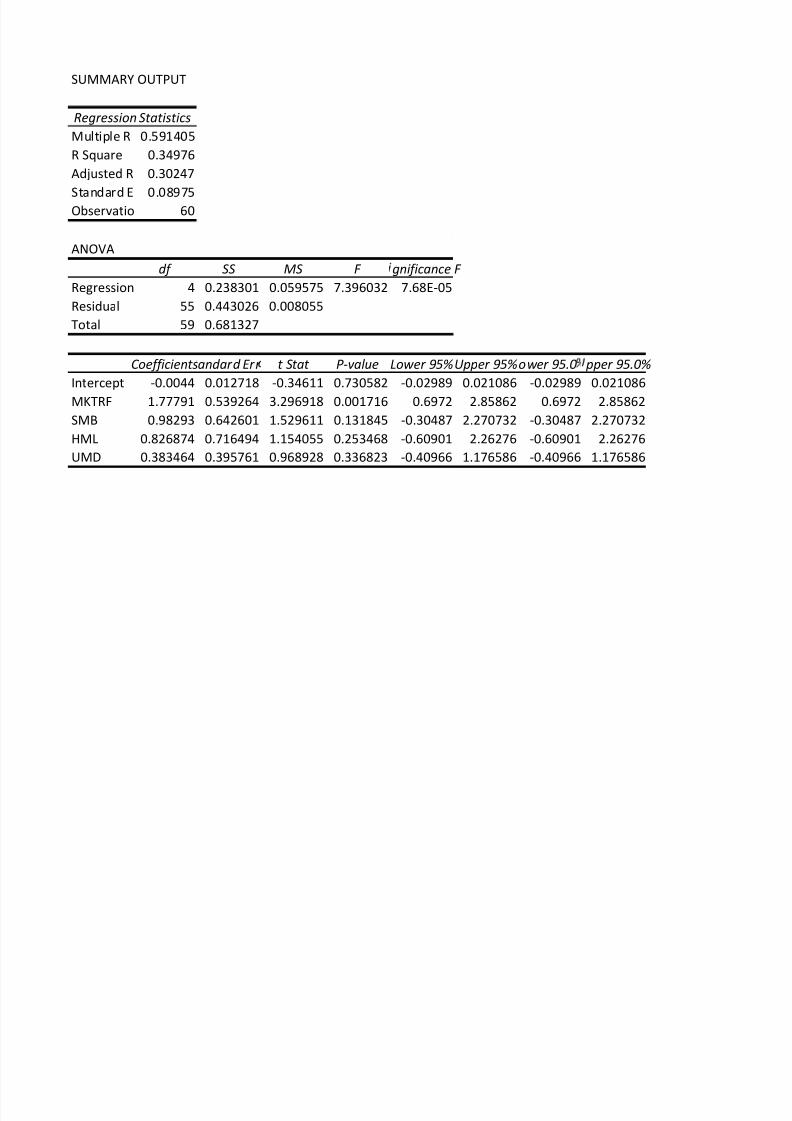

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.591405

R Square 0.34976

Adjusted R 0.30247

Standard E 0.08975Observatio 60

ANOVA

df SS MS F gnificance F

Regression 4 0.238301 0.059575 7.396032 7.68E-05

Residual 55 0.443026 0.008055

Total 59 0.681327

Coefficientsandard Err t Stat P-value Lower 95%Upper 95%ower 95.0 pper 95.0%

Intercept -0.0044 0.012718 -0.34611 0.730582 -0.02989 0.021086 -0.02989 0.021086

MKTRF 1.77791 0.539264 3.296918 0.001716 0.6972 2.85862 0.6972 2.85862

SMB 0.98293 0.642601 1.529611 0.131845 -0.30487 2.270732 -0.30487 2.270732

HML 0.826874 0.716494 1.154055 0.253468 -0.60901 2.26276 -0.60901 2.26276

UMD 0.383464 0.395761 0.968928 0.336823 -0.40966 1.176586 -0.40966 1.176586

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 13/37

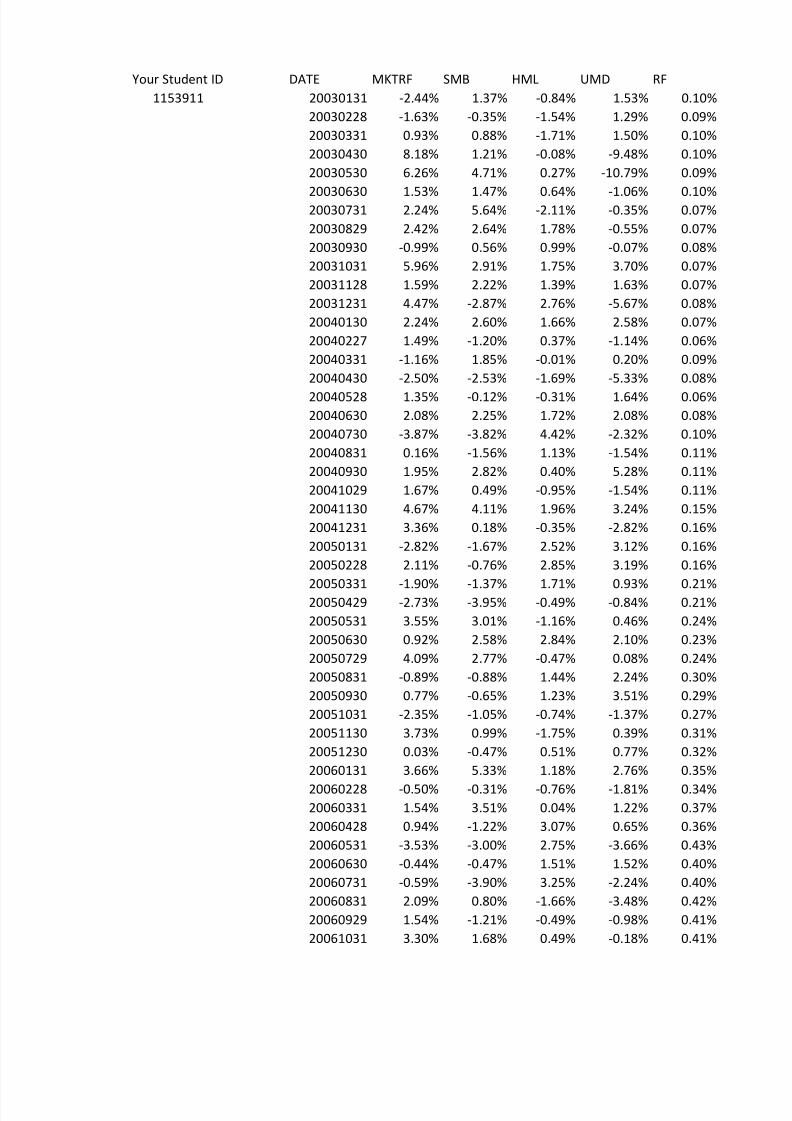

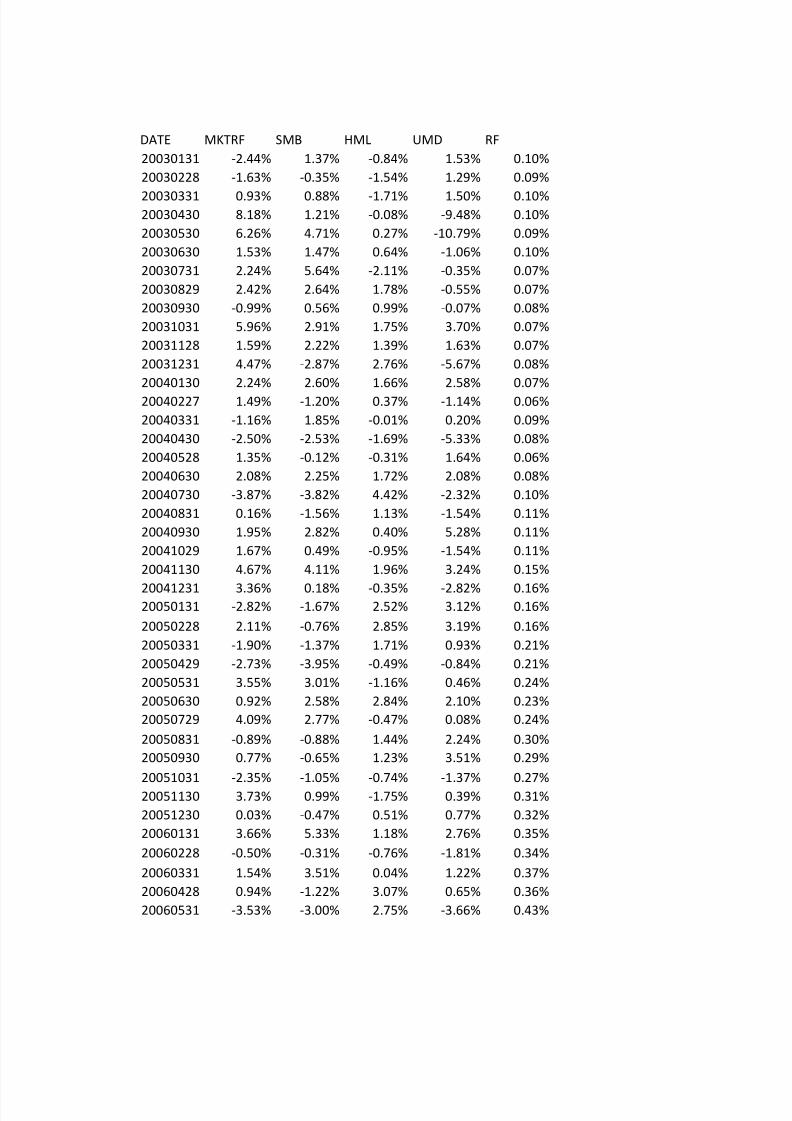

Your Student ID DATE MKTRF SMB HML UMD RF

1153911 20030131 -2.44% 1.37% -0.84% 1.53% 0.10%

20030228 -1.63% -0.35% -1.54% 1.29% 0.09%

20030331 0.93% 0.88% -1.71% 1.50% 0.10%

20030430 8.18% 1.21% -0.08% -9.48% 0.10%

20030530 6.26% 4.71% 0.27% -10.79% 0.09%

20030630 1.53% 1.47% 0.64% -1.06% 0.10%20030731 2.24% 5.64% -2.11% -0.35% 0.07%

20030829 2.42% 2.64% 1.78% -0.55% 0.07%

20030930 -0.99% 0.56% 0.99% -0.07% 0.08%

20031031 5.96% 2.91% 1.75% 3.70% 0.07%

20031128 1.59% 2.22% 1.39% 1.63% 0.07%

20031231 4.47% -2.87% 2.76% -5.67% 0.08%

20040130 2.24% 2.60% 1.66% 2.58% 0.07%

20040227 1.49% -1.20% 0.37% -1.14% 0.06%

20040331 -1.16% 1.85% -0.01% 0.20% 0.09%

20040430 -2.50% -2.53% -1.69% -5.33% 0.08%

20040528 1.35% -0.12% -0.31% 1.64% 0.06%

20040630 2.08% 2.25% 1.72% 2.08% 0.08%

20040730 -3.87% -3.82% 4.42% -2.32% 0.10%

20040831 0.16% -1.56% 1.13% -1.54% 0.11%

20040930 1.95% 2.82% 0.40% 5.28% 0.11%

20041029 1.67% 0.49% -0.95% -1.54% 0.11%

20041130 4.67% 4.11% 1.96% 3.24% 0.15%

20041231 3.36% 0.18% -0.35% -2.82% 0.16%

20050131 -2.82% -1.67% 2.52% 3.12% 0.16%

20050228 2.11% -0.76% 2.85% 3.19% 0.16%

20050331 -1.90% -1.37% 1.71% 0.93% 0.21%20050429 -2.73% -3.95% -0.49% -0.84% 0.21%

20050531 3.55% 3.01% -1.16% 0.46% 0.24%

20050630 0.92% 2.58% 2.84% 2.10% 0.23%

20050729 4.09% 2.77% -0.47% 0.08% 0.24%

20050831 -0.89% -0.88% 1.44% 2.24% 0.30%

20050930 0.77% -0.65% 1.23% 3.51% 0.29%

20051031 -2.35% -1.05% -0.74% -1.37% 0.27%

20051130 3.73% 0.99% -1.75% 0.39% 0.31%

20051230 0.03% -0.47% 0.51% 0.77% 0.32%

20060131 3.66% 5.33% 1.18% 2.76% 0.35%

20060228 -0.50% -0.31% -0.76% -1.81% 0.34%

20060331 1.54% 3.51% 0.04% 1.22% 0.37%

20060428 0.94% -1.22% 3.07% 0.65% 0.36%

20060531 -3.53% -3.00% 2.75% -3.66% 0.43%

20060630 -0.44% -0.47% 1.51% 1.52% 0.40%

20060731 -0.59% -3.90% 3.25% -2.24% 0.40%

20060831 2.09% 0.80% -1.66% -3.48% 0.42%

20060929 1.54% -1.21% -0.49% -0.98% 0.41%

20061031 3.30% 1.68% 0.49% -0.18% 0.41%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 14/37

20061130 1.95% 0.70% 0.39% -1.00% 0.42%

20061229 0.68% -0.93% 2.56% 0.81% 0.40%

20070131 1.50% 0.02% 0.00% 0.22% 0.44%

20070228 -1.78% 1.38% 0.32% -1.32% 0.38%

20070330 0.86% -0.20% 0.31% 2.48% 0.43%

20070430 3.55% -2.06% -1.08% -0.14% 0.44%

20070531 3.48% -0.05% -0.23% -0.33% 0.41%20070629 -1.88% 0.69% -1.07% 0.40% 0.40%

20070731 -3.58% -2.74% -3.01% 2.80% 0.40%

20070831 0.74% -0.09% -2.42% 0.14% 0.42%

20070928 3.77% -2.47% -2.10% 4.64% 0.32%

20071031 2.26% 0.07% -1.97% 4.86% 0.32%

20071130 -5.27% -2.72% -0.88% 0.93% 0.34%

20071231 -0.70% 0.06% -0.02% 6.48% 0.27%

20080131 -6.44% -0.76% 3.13% -7.89% 0.21%

20080229 -2.33% -0.67% 0.04% 6.23% 0.13%

20080331 -1.22% 0.87% 0.26% 4.12% 0.17%

20080430 4.94% -1.60% 0.08% -0.38% 0.17%

20080530 2.21% 2.80% -0.30% 3.19% 0.17%

20080630 -8.03% 0.91% -0.93% 12.45% 0.17%

20080731 -1.46% 3.89% 3.57% -5.11% 0.15%

20080829 0.98% 3.66% 1.65% -3.82% 0.12%

20080930 -9.96% -0.20% 4.37% 0.36% 0.15%

20081031 -18.55% -2.05% -3.14% 7.91% 0.08%

20081128 -8.54% -3.46% -5.09% 7.19% 0.02%20081231 2.06% 4.04% -1.20% -5.04% 0.09%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 15/37

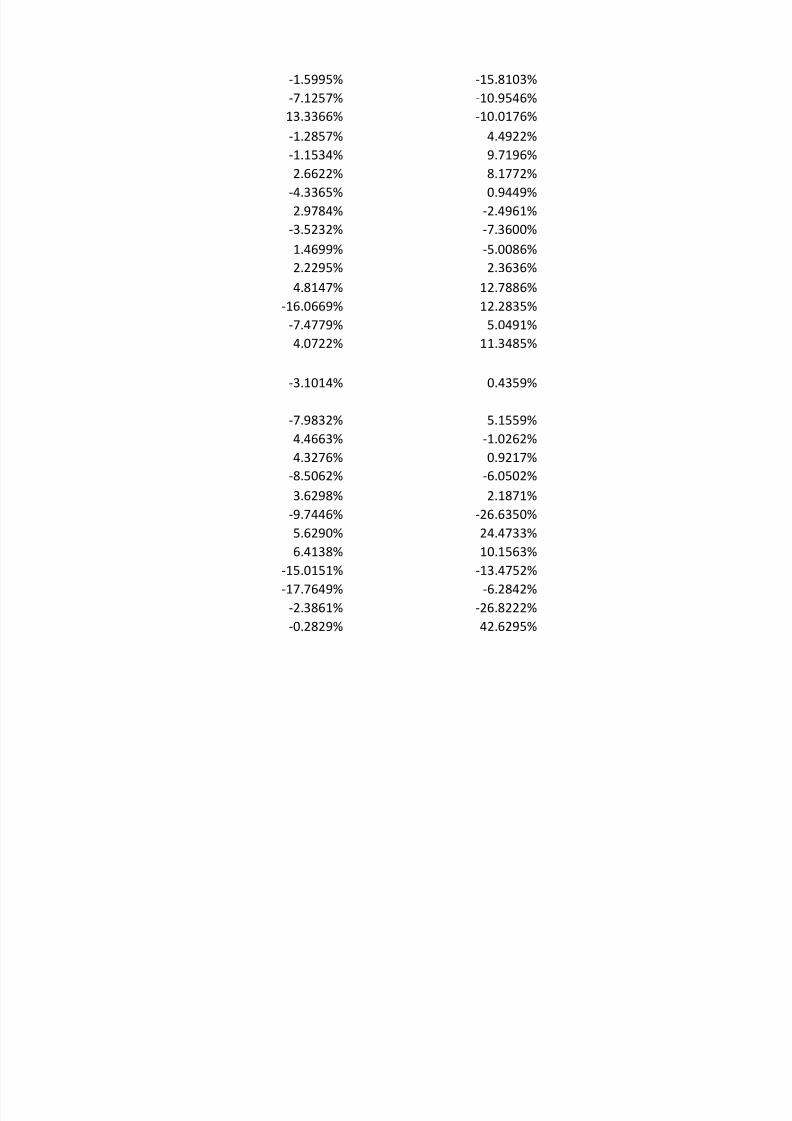

WALGREEN CO (WAG) TIVO INC (TIVO)

-0.6509% -0.7678%

-2.8362% 8.3172%

4.7619% -8.9286%

4.6811% 16.4706%

-0.1053% 51.5152%

-2.2410% 34.3333%-0.5980% -11.0835%

9.0011% 1.3953%

-5.9257% -32.0183%

13.6423% 8.7719%

5.8390% 3.2258%

-1.1682% -11.0577%

-5.0302% 45.2703%

3.3376% -0.6512%

-7.5995% -16.7603%

4.6434% -21.1474%

1.6622% 8.5592%

3.4276% -6.8331%

0.5247% -20.3103%

0.2816% -23.8938%

-1.7010% 53.9535%

0.1675% 1.5861%

6.5269% -29.9628%

0.4976% 24.6284%

11.0503% -31.6865%

0.6395% 0.0000%

3.7123% 28.9277%-3.0617% 8.8975%

5.4169% 19.8934%

1.4336% -1.0370%

4.0661% -6.4371%

-3.0610% -17.6000%

-6.2163% 6.4078%

4.5570% -11.6788%

0.6934% 11.1570%

-3.1086% -4.8327%

-2.2142% 7.6172%

3.8008% 0.7260%

-3.8564% 30.2703%

-2.7823% 14.7994%

-3.0169% -23.7349%

10.4434% 12.9542%

4.3265% -5.8741%

5.8946% 22.5854%

-10.2507% -8.0000%

-1.5995% -15.8103%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 16/37

-7.1257% -10.9546%

13.3366% -10.0176%

-1.2857% 4.4922%

-1.1534% 9.7196%

2.6622% 8.1772%

-4.3365% 0.9449%

2.9784% -2.4961%-3.5232% -7.3600%

1.4699% -5.0086%

2.2295% 2.3636%

4.8147% 12.7886%

-16.0669% 12.2835%

-7.4779% 5.0491%

4.0722% 11.3485%

-7.9832% 5.1559%

4.4663% -1.0262%

4.3276% 0.9217%

-8.5062% -6.0502%

3.6298% 2.1871%

-9.7446% -26.6350%

5.6290% 24.4733%

6.4138% 10.1563%

-15.0151% -13.4752%

-17.7649% -6.2842%

-2.3861% -26.8222%-0.2829% 42.6295%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 17/37

SPSS INC (SPSS)

-23.3738% -0.75% -0.87% -23.47%

1.6791% -2.93% 8.23% 1.59%

3.8532% 4.66% -9.03% 3.75%

9.1873% 4.58% 16.37% 9.09%

25.5664% -0.20% 51.43% 25.48%

6.8943% -2.34% 34.23% 6.79%8.6197% -0.67% -11.15% 8.55%

5.7714% 8.93% 1.33% 5.70%

-11.4900% -6.01% -32.10% -11.57%

8.5359% 13.57% 8.70% 8.47%

5.6800% 5.77% 3.16% 5.61%

-7.5969% -1.25% -11.14% -7.68%

18.0090% -5.10% 45.20% 17.94%

-3.0806% 3.28% -0.71% -3.14%

-10.0245% -7.69% -16.85% -10.11%

-22.7174% 4.56% -21.23% -22.80%

17.0886% 1.60% 8.50% 17.03%

7.9279% 3.35% -6.91% 7.85%

-17.6405% 0.42% -20.41% -17.74%

-6.7568% 0.17% -24.00% -6.87%

-3.4058% -1.81% 53.84% -3.52%

1.3503% 0.06% 1.48% 1.24%

18.3568% 6.38% -30.11% 18.21%

-2.1889% 0.34% 24.47% -2.35%

1.9821% 10.89% -31.85% 1.82%

21.6301% 0.48% -0.16% 21.47%

-10.3608% 3.50% 28.72% -10.57%-7.4756% -3.27% 8.69% -7.69%

8.6389% 5.18% 19.65% 8.40%

9.8970% 1.20% -1.27% 9.67%

2.2384% 3.83% -6.68% 2.00%

10.9980% -3.36% -17.90% 10.70%

10.0917% -6.51% 6.12% 9.80%

-5.0000% 4.29% -11.95% -5.27%

26.6667% 0.38% 10.85% 26.36%

7.0983% -3.43% -5.15% 6.78%

4.2354% -2.56% 7.27% 3.89%

1.2407% 3.46% 0.39% 0.90%

-3.0024% -4.23% 29.90% -3.37%

10.1074% -3.14% 14.44% 9.75%

6.1388% -3.45% -24.16% 5.71%

-13.1351% 10.04% 12.55% -13.54%

-15.8992% 3.93% -6.27% -16.30%

-6.1413% 5.47% 22.17% -6.56%

-1.7343% -10.66% -8.41% -2.14%

10.9908% -2.01% -16.22% 10.58%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 18/37

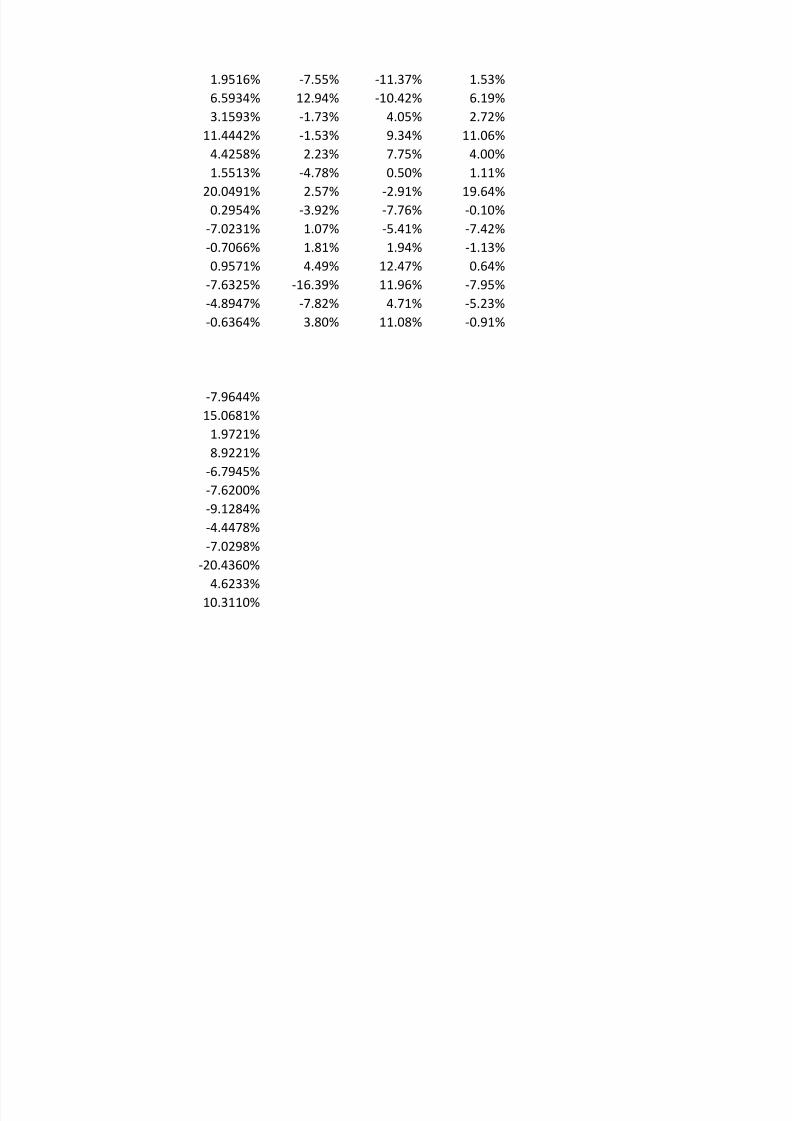

1.9516% -7.55% -11.37% 1.53%

6.5934% 12.94% -10.42% 6.19%

3.1593% -1.73% 4.05% 2.72%

11.4442% -1.53% 9.34% 11.06%

4.4258% 2.23% 7.75% 4.00%

1.5513% -4.78% 0.50% 1.11%

20.0491% 2.57% -2.91% 19.64%0.2954% -3.92% -7.76% -0.10%

-7.0231% 1.07% -5.41% -7.42%

-0.7066% 1.81% 1.94% -1.13%

0.9571% 4.49% 12.47% 0.64%

-7.6325% -16.39% 11.96% -7.95%

-4.8947% -7.82% 4.71% -5.23%

-0.6364% 3.80% 11.08% -0.91%

-7.9644%

15.0681%

1.9721%

8.9221%

-6.7945%

-7.6200%

-9.1284%

-4.4478%

-7.0298%

-20.4360%

4.6233%10.3110%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 19/37

DATE MKTRF SMB HML UMD RF

20030131 -2.44% 1.37% -0.84% 1.53% 0.10%

20030228 -1.63% -0.35% -1.54% 1.29% 0.09%

20030331 0.93% 0.88% -1.71% 1.50% 0.10%20030430 8.18% 1.21% -0.08% -9.48% 0.10%

20030530 6.26% 4.71% 0.27% -10.79% 0.09%

20030630 1.53% 1.47% 0.64% -1.06% 0.10%

20030731 2.24% 5.64% -2.11% -0.35% 0.07%

20030829 2.42% 2.64% 1.78% -0.55% 0.07%

20030930 -0.99% 0.56% 0.99% -0.07% 0.08%

20031031 5.96% 2.91% 1.75% 3.70% 0.07%

20031128 1.59% 2.22% 1.39% 1.63% 0.07%

20031231 4.47% -2.87% 2.76% -5.67% 0.08%

20040130 2.24% 2.60% 1.66% 2.58% 0.07%

20040227 1.49% -1.20% 0.37% -1.14% 0.06%

20040331 -1.16% 1.85% -0.01% 0.20% 0.09%

20040430 -2.50% -2.53% -1.69% -5.33% 0.08%

20040528 1.35% -0.12% -0.31% 1.64% 0.06%

20040630 2.08% 2.25% 1.72% 2.08% 0.08%

20040730 -3.87% -3.82% 4.42% -2.32% 0.10%

20040831 0.16% -1.56% 1.13% -1.54% 0.11%

20040930 1.95% 2.82% 0.40% 5.28% 0.11%

20041029 1.67% 0.49% -0.95% -1.54% 0.11%

20041130 4.67% 4.11% 1.96% 3.24% 0.15%

20041231 3.36% 0.18% -0.35% -2.82% 0.16%20050131 -2.82% -1.67% 2.52% 3.12% 0.16%

20050228 2.11% -0.76% 2.85% 3.19% 0.16%

20050331 -1.90% -1.37% 1.71% 0.93% 0.21%

20050429 -2.73% -3.95% -0.49% -0.84% 0.21%

20050531 3.55% 3.01% -1.16% 0.46% 0.24%

20050630 0.92% 2.58% 2.84% 2.10% 0.23%

20050729 4.09% 2.77% -0.47% 0.08% 0.24%

20050831 -0.89% -0.88% 1.44% 2.24% 0.30%

20050930 0.77% -0.65% 1.23% 3.51% 0.29%

20051031 -2.35% -1.05% -0.74% -1.37% 0.27%

20051130 3.73% 0.99% -1.75% 0.39% 0.31%

20051230 0.03% -0.47% 0.51% 0.77% 0.32%

20060131 3.66% 5.33% 1.18% 2.76% 0.35%

20060228 -0.50% -0.31% -0.76% -1.81% 0.34%

20060331 1.54% 3.51% 0.04% 1.22% 0.37%

20060428 0.94% -1.22% 3.07% 0.65% 0.36%

20060531 -3.53% -3.00% 2.75% -3.66% 0.43%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 20/37

20060630 -0.44% -0.47% 1.51% 1.52% 0.40%

20060731 -0.59% -3.90% 3.25% -2.24% 0.40%

20060831 2.09% 0.80% -1.66% -3.48% 0.42%

20060929 1.54% -1.21% -0.49% -0.98% 0.41%

20061031 3.30% 1.68% 0.49% -0.18% 0.41%

20061130 1.95% 0.70% 0.39% -1.00% 0.42%20061229 0.68% -0.93% 2.56% 0.81% 0.40%

20070131 1.50% 0.02% 0.00% 0.22% 0.44%

20070228 -1.78% 1.38% 0.32% -1.32% 0.38%

20070330 0.86% -0.20% 0.31% 2.48% 0.43%

20070430 3.55% -2.06% -1.08% -0.14% 0.44%

20070531 3.48% -0.05% -0.23% -0.33% 0.41%

20070629 -1.88% 0.69% -1.07% 0.40% 0.40%

20070731 -3.58% -2.74% -3.01% 2.80% 0.40%

20070831 0.74% -0.09% -2.42% 0.14% 0.42%

20070928 3.77% -2.47% -2.10% 4.64% 0.32%

20071031 2.26% 0.07% -1.97% 4.86% 0.32%

20071130 -5.27% -2.72% -0.88% 0.93% 0.34%

20071231 -0.70% 0.06% -0.02% 6.48% 0.27%

-3.86% 0.62% 0.20% 1.60% 0.14%

20080131 -6.44% -0.76% 3.13% -7.89% 0.21%

20080229 -2.33% -0.67% 0.04% 6.23% 0.13%

20080331 -1.22% 0.87% 0.26% 4.12% 0.17%

20080430 4.94% -1.60% 0.08% -0.38% 0.17%

20080530 2.21% 2.80% -0.30% 3.19% 0.17%20080630 -8.03% 0.91% -0.93% 12.45% 0.17%

20080731 -1.46% 3.89% 3.57% -5.11% 0.15%

20080829 0.98% 3.66% 1.65% -3.82% 0.12%

20080930 -9.96% -0.20% 4.37% 0.36% 0.15%

20081031 -18.55% -2.05% -3.14% 7.91% 0.08%

20081128 -8.54% -3.46% -5.09% 7.19% 0.02%

20081231 2.06% 4.04% -1.20% -5.04% 0.09%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 21/37

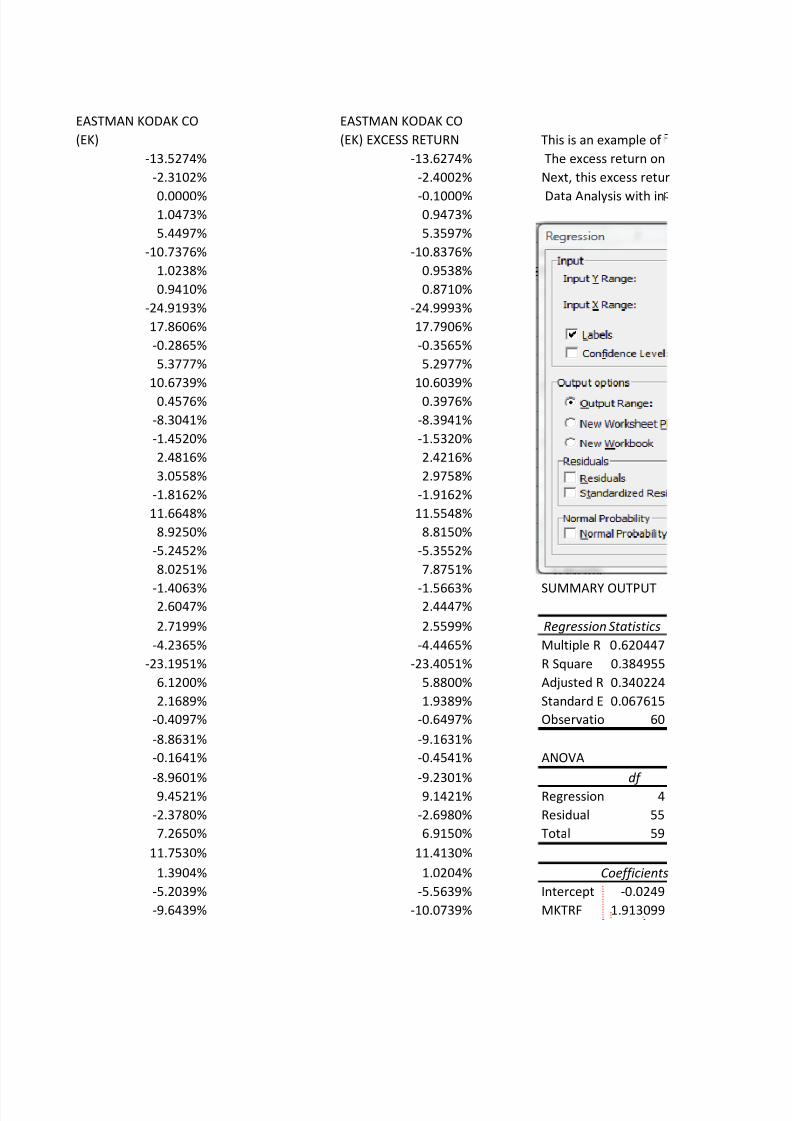

EASTMAN KODAK CO

(EK)

EASTMAN KODAK CO

(EK) EXCESS RETURN This is an example of

-13.5274% -13.6274% The excess return on

-2.3102% -2.4002% Next, this excess retur

0.0000% -0.1000% Data Analysis with in1.0473% 0.9473%

5.4497% 5.3597%

-10.7376% -10.8376%

1.0238% 0.9538%

0.9410% 0.8710%

-24.9193% -24.9993%

17.8606% 17.7906%

-0.2865% -0.3565%

5.3777% 5.2977%

10.6739% 10.6039%

0.4576% 0.3976%

-8.3041% -8.3941%

-1.4520% -1.5320%

2.4816% 2.4216%

3.0558% 2.9758%

-1.8162% -1.9162%

11.6648% 11.5548%

8.9250% 8.8150%

-5.2452% -5.3552%

8.0251% 7.8751%

-1.4063% -1.5663% SUMMARY OUTPUT2.6047% 2.4447%

2.7199% 2.5599% Regression Statistics

-4.2365% -4.4465% Multiple R 0.620447

-23.1951% -23.4051% R Square 0.384955

6.1200% 5.8800% Adjusted R 0.340224

2.1689% 1.9389% Standard E 0.067615

-0.4097% -0.6497% Observatio 60

-8.8631% -9.1631%

-0.1641% -0.4541% ANOVA

-8.9601% -9.2301% df

9.4521% 9.1421% Regression 4

-2.3780% -2.6980% Residual 55

7.2650% 6.9150% Total 59

11.7530% 11.4130%

1.3904% 1.0204% Coefficients

-5.2039% -5.5639% Intercept -0.0249

-9.6439% -10.0739% MKTRF 1.913099

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 22/37

-1.3687% -1.7687% SMB 0.039372

-6.4340% -6.8340% HML 0.201359

-4.4045% -4.8245% UMD 0.464549

5.3126% 4.9026%

10.0446% 9.6346%

6.6393% 6.2193% The market beta is-0.8455% -1.2455% Since market beta is g

0.2326% -0.2074%

-7.6953% -8.0753% The SMB beta is

-5.4881% -5.9181% Since this beta is posit

10.4167% 9.9767% stock but only slightly

2.8101% 2.4001%

9.7397% 9.3397% The HML beta is

-9.2706% -9.6706% Since this beta is posit

5.6238% 5.2038%

0.3375% 0.0175% The UMD beta is

8.0344% 7.7144% Since this beta is posit

-18.0740% -18.4140% stock.

-6.8569% -7.1269%

To predict average m

-8.2798% factors, the riskfree ra

to 76.

-8.9163% -9.1263%

-14.7590% -14.8890% Now calculate the pre

4.0636% 3.8936% the problem as:

1.2450% 1.0750% Predicted Return =

-12.9681% -13.1381% which is obtained fro-5.8094% -5.9794% = -0.0249

1.4553% 1.3053% + 1.913099

10.5874% 10.4674% + 0.039372

-5.0031% -5.1531% + 0.201359

-38.8166% -38.8966% + 0.464549

-17.3581% -17.3781% +

-13.0779% -13.1679%

Finally, the difference

between -8.9325%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 23/37

our-factor analysis using Eastman Kodak stock returns.

Eastman Kodak is calculated in column L as column I minus column G.

n is regressed on the four-factors in columns C to F using

uts as shown below. Regression output follows.

SS MS F gnificance F

0.15738293 0.039346 8.606079 1.82E-05

0.25145194 0.004572

0.40883486

tandard Erro t Stat P-value Lower 95%Upper 95%ower 95.0 pper 95.0%

0.00958164 -2.5983 0.012001 -0.0441 -0.00569 -0.0441 -0.00569

0.40626981 4.708937 1.73E-05 1.098916 2.727282 1.098916 2.727282

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 24/37

0.48412178 0.081327 0.935477 -0.93083 1.009574 -0.93083 1.009574

0.53979087 0.373032 0.710559 -0.88041 1.283124 -0.88041 1.283124

0.29815734 1.558068 0.124953 -0.13297 1.06207 -0.13297 1.06207

1.91309886reater than 1, this stock has more market risk than an average stock.

0.03937241

ive, the stock acts more like a small stock compared to an average

because beta is very close to 0.

0.20135916

ive, the stock acts like a value stock compared to an average stock.

0.46454932

ive, the stock return is more sensitive to momentum than an average

nthly return for 2008, calculate the average monthly values of the four

te, and the stock return. The values in row 63 are averages of rows 65

dicted average monthly return using the equation mentioned in

-8.9325%

the following calculation:

* -3.86%

* 0.62%

* 0.20%

* 1.60%

0.14%

between predicted return and the actual return is the difference

and -8.2798% which is 0.6528%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 25/37

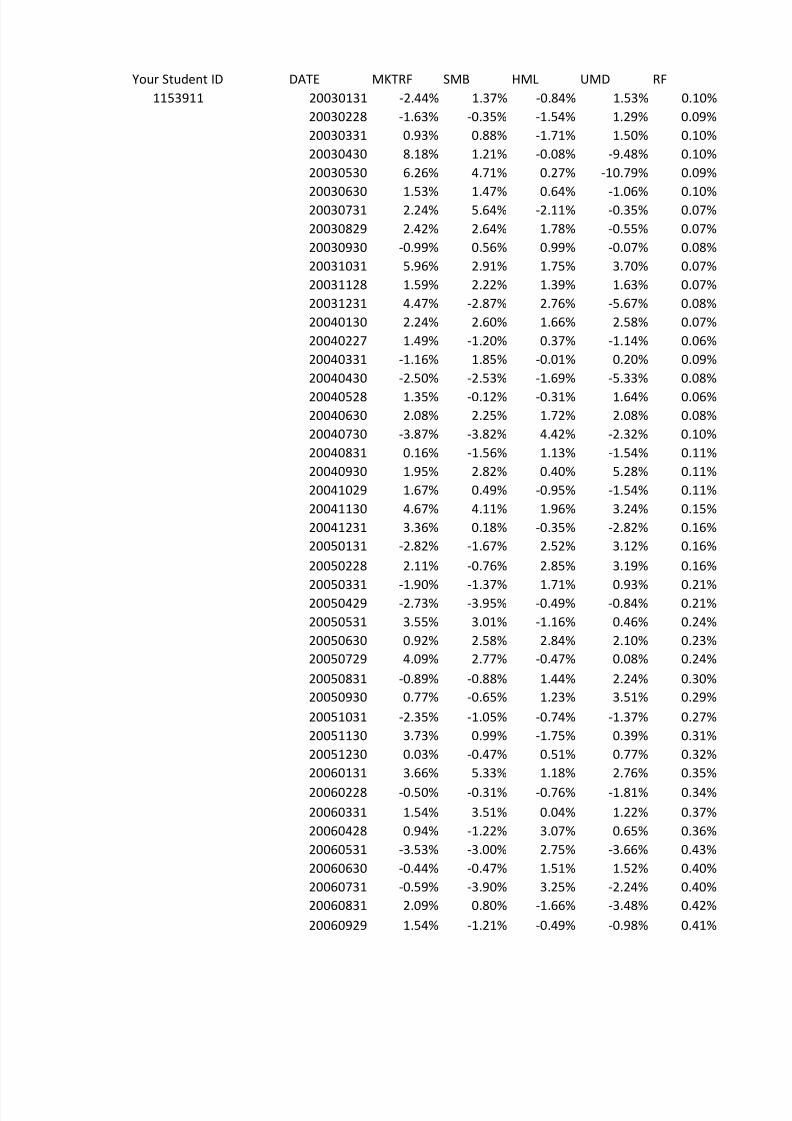

Your Student ID DATE MKTRF SMB HML UMD RF

1153911 20030131 -2.44% 1.37% -0.84% 1.53% 0.10%

20030228 -1.63% -0.35% -1.54% 1.29% 0.09%

20030331 0.93% 0.88% -1.71% 1.50% 0.10%

20030430 8.18% 1.21% -0.08% -9.48% 0.10%

20030530 6.26% 4.71% 0.27% -10.79% 0.09%

20030630 1.53% 1.47% 0.64% -1.06% 0.10%20030731 2.24% 5.64% -2.11% -0.35% 0.07%

20030829 2.42% 2.64% 1.78% -0.55% 0.07%

20030930 -0.99% 0.56% 0.99% -0.07% 0.08%

20031031 5.96% 2.91% 1.75% 3.70% 0.07%

20031128 1.59% 2.22% 1.39% 1.63% 0.07%

20031231 4.47% -2.87% 2.76% -5.67% 0.08%

20040130 2.24% 2.60% 1.66% 2.58% 0.07%

20040227 1.49% -1.20% 0.37% -1.14% 0.06%

20040331 -1.16% 1.85% -0.01% 0.20% 0.09%

20040430 -2.50% -2.53% -1.69% -5.33% 0.08%

20040528 1.35% -0.12% -0.31% 1.64% 0.06%

20040630 2.08% 2.25% 1.72% 2.08% 0.08%

20040730 -3.87% -3.82% 4.42% -2.32% 0.10%

20040831 0.16% -1.56% 1.13% -1.54% 0.11%

20040930 1.95% 2.82% 0.40% 5.28% 0.11%

20041029 1.67% 0.49% -0.95% -1.54% 0.11%

20041130 4.67% 4.11% 1.96% 3.24% 0.15%

20041231 3.36% 0.18% -0.35% -2.82% 0.16%

20050131 -2.82% -1.67% 2.52% 3.12% 0.16%

20050228 2.11% -0.76% 2.85% 3.19% 0.16%

20050331 -1.90% -1.37% 1.71% 0.93% 0.21%20050429 -2.73% -3.95% -0.49% -0.84% 0.21%

20050531 3.55% 3.01% -1.16% 0.46% 0.24%

20050630 0.92% 2.58% 2.84% 2.10% 0.23%

20050729 4.09% 2.77% -0.47% 0.08% 0.24%

20050831 -0.89% -0.88% 1.44% 2.24% 0.30%

20050930 0.77% -0.65% 1.23% 3.51% 0.29%

20051031 -2.35% -1.05% -0.74% -1.37% 0.27%

20051130 3.73% 0.99% -1.75% 0.39% 0.31%

20051230 0.03% -0.47% 0.51% 0.77% 0.32%

20060131 3.66% 5.33% 1.18% 2.76% 0.35%

20060228 -0.50% -0.31% -0.76% -1.81% 0.34%

20060331 1.54% 3.51% 0.04% 1.22% 0.37%

20060428 0.94% -1.22% 3.07% 0.65% 0.36%

20060531 -3.53% -3.00% 2.75% -3.66% 0.43%

20060630 -0.44% -0.47% 1.51% 1.52% 0.40%

20060731 -0.59% -3.90% 3.25% -2.24% 0.40%

20060831 2.09% 0.80% -1.66% -3.48% 0.42%

20060929 1.54% -1.21% -0.49% -0.98% 0.41%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 26/37

20061031 3.30% 1.68% 0.49% -0.18% 0.41%

20061130 1.95% 0.70% 0.39% -1.00% 0.42%

20061229 0.68% -0.93% 2.56% 0.81% 0.40%

20070131 1.50% 0.02% 0.00% 0.22% 0.44%

20070228 -1.78% 1.38% 0.32% -1.32% 0.38%

20070330 0.86% -0.20% 0.31% 2.48% 0.43%

20070430 3.55% -2.06% -1.08% -0.14% 0.44%20070531 3.48% -0.05% -0.23% -0.33% 0.41%

20070629 -1.88% 0.69% -1.07% 0.40% 0.40%

20070731 -3.58% -2.74% -3.01% 2.80% 0.40%

20070831 0.74% -0.09% -2.42% 0.14% 0.42%

20070928 3.77% -2.47% -2.10% 4.64% 0.32%

20071031 2.26% 0.07% -1.97% 4.86% 0.32%

20071130 -5.27% -2.72% -0.88% 0.93% 0.34%

20071231 -0.70% 0.06% -0.02% 6.48% 0.27%

-3.86% 0.62% 0.20% 1.60% 0.14%

20080131 -6.44% -0.76% 3.13% -7.89% 0.21%

20080229 -2.33% -0.67% 0.04% 6.23% 0.13%

20080331 -1.22% 0.87% 0.26% 4.12% 0.17%

20080430 4.94% -1.60% 0.08% -0.38% 0.17%

20080530 2.21% 2.80% -0.30% 3.19% 0.17%

20080630 -8.03% 0.91% -0.93% 12.45% 0.17%

20080731 -1.46% 3.89% 3.57% -5.11% 0.15%

20080829 0.98% 3.66% 1.65% -3.82% 0.12%

20080930 -9.96% -0.20% 4.37% 0.36% 0.15%

20081031 -18.55% -2.05% -3.14% 7.91% 0.08%20081128 -8.54% -3.46% -5.09% 7.19% 0.02%

20081231 2.06% 4.04% -1.20% -5.04% 0.09%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 27/37

WALGREEN CO (WAG) TIVO INC (TIVO)

-0.6509% -0.7678%

-2.8362% 8.3172%

4.7619% -8.9286%

4.6811% 16.4706%

-0.1053% 51.5152%

-2.2410% 34.3333%-0.5980% -11.0835%

9.0011% 1.3953%

-5.9257% -32.0183%

13.6423% 8.7719%

5.8390% 3.2258%

-1.1682% -11.0577%

-5.0302% 45.2703%

3.3376% -0.6512%

-7.5995% -16.7603%

4.6434% -21.1474%

1.6622% 8.5592%

3.4276% -6.8331%

0.5247% -20.3103%

0.2816% -23.8938%

-1.7010% 53.9535%

0.1675% 1.5861%

6.5269% -29.9628%

0.4976% 24.6284%

11.0503% -31.6865%

0.6395% 0.0000%

3.7123% 28.9277%-3.0617% 8.8975%

5.4169% 19.8934%

1.4336% -1.0370%

4.0661% -6.4371%

-3.0610% -17.6000%

-6.2163% 6.4078%

4.5570% -11.6788%

0.6934% 11.1570%

-3.1086% -4.8327%

-2.2142% 7.6172%

3.8008% 0.7260%

-3.8564% 30.2703%

-2.7823% 14.7994%

-3.0169% -23.7349%

10.4434% 12.9542%

4.3265% -5.8741%

5.8946% 22.5854%

-10.2507% -8.0000%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 28/37

-1.5995% -15.8103%

-7.1257% -10.9546%

13.3366% -10.0176%

-1.2857% 4.4922%

-1.1534% 9.7196%

2.6622% 8.1772%

-4.3365% 0.9449%2.9784% -2.4961%

-3.5232% -7.3600%

1.4699% -5.0086%

2.2295% 2.3636%

4.8147% 12.7886%

-16.0669% 12.2835%

-7.4779% 5.0491%

4.0722% 11.3485%

-3.1014% 0.4359%

-7.9832% 5.1559%

4.4663% -1.0262%

4.3276% 0.9217%

-8.5062% -6.0502%

3.6298% 2.1871%

-9.7446% -26.6350%

5.6290% 24.4733%

6.4138% 10.1563%

-15.0151% -13.4752%

-17.7649% -6.2842%-2.3861% -26.8222%

-0.2829% 42.6295%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 29/37

SPSS INC (SPSS)

-23.3738% -0.75%

1.6791% -2.93%

3.8532% 4.66%

9.1873% 4.58%

25.5664% -0.20%

6.8943% -2.34%8.6197% -0.67%

5.7714% 8.93%

-11.4900% -6.01%

8.5359% 13.57%

5.6800% 5.77%

-7.5969% -1.25%

18.0090% -5.10%

-3.0806% 3.28%

-10.0245% -7.69%

-22.7174% 4.56%

17.0886% 1.60%

7.9279% 3.35%

-17.6405% 0.42%

-6.7568% 0.17%

-3.4058% -1.81%

1.3503% 0.06%

18.3568% 6.38%

-2.1889% 0.34% SUMMARY OUTPUT

1.9821% 10.89%

21.6301% 0.48% Regression Statistics

-10.3608% 3.50% Multiple R 0.253890413-7.4756% -3.27% R Square 0.064460342

8.6389% 5.18% Adjusted R Square -0.003578906

9.8970% 1.20% Standard Error 0.055280151

2.2384% 3.83% Observations 60

10.9980% -3.36%

10.0917% -6.51% ANOVA

-5.0000% 4.29% df

26.6667% 0.38% Regression 4

7.0983% -3.43% Residual 55

4.2354% -2.56% Total 59

1.2407% 3.46%

-3.0024% -4.23% Coefficients

10.1074% -3.14% Intercept -0.001565559

6.1388% -3.45% MKTRF 0.346118667

-13.1351% 10.04% SMB -0.01862182

-15.8992% 3.93% HML 0.667663422

-6.1413% 5.47% UMD 0.019773085

-1.7343% -10.66%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 30/37

10.9908% -2.01%

1.9516% -7.55%

6.5934% 12.94%

3.1593% -1.73%

11.4442% -1.53%

4.4258% 2.23%

1.5513% -4.78%20.0491% 2.57%

0.2954% -3.92%

-7.0231% 1.07%

-0.7066% 1.81%

0.9571% 4.49%

-7.6325% -16.39%

-4.8947% -7.82%

-0.6364% 3.80%

-1.8770%

WAG

-7.9644% Predicted return -1.20144%

15.0681% Difference -1.89994%

1.9721%

8.9221% TIVO

-6.7945% Predicted return -5.16008%

-7.6200% Difference 5.59598%

-9.1284%

-4.4478% SPSS

-7.0298% Predicted return -5.77946%

-20.4360% Difference 3.90244%4.6233%

10.3110%

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 31/37

SS MS F Significance F

0.01158061 0.00289515 0.94739939 0.44371804

0.16807423 0.0030559

0.17965485

tandard Error t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%

0.00783363 -0.19985111 0.84233412 -0.0172645 0.01413338 -0.0172645 0.01413338

0.33215258 1.04204722 0.30194872 -0.31952996 1.0117673 -0.31952996 1.0117673

0.39580174 -0.04704835 0.96264511 -0.81182623 0.77458259 -0.81182623 0.77458259

0.44131492 1.51289564 0.1360316 -0.21675144 1.55207828 -0.21675144 1.55207828

0.24376344 0.08111588 0.93564426 -0.46873977 0.50828594 -0.46873977 0.50828594

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 32/37

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 33/37

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.3988992R Square 0.15912057

Adjusted R Sq 0.0979657

Standard Erro 0.17626122

Observations 60

ANOVA

df SS MS F Significance F

Regression 4 0.32334699 0.08083675 2.60192815 0.04577432

Residual 55 1.70874095 0.03106802

Total 59 2.03208795

Coefficients tandard Error t Stat P-value Lower 95%

Intercept 0.00631267 0.02497759 0.25273327 0.80141654 -0.04374354

MKTRF 1.72117246 1.05907123 1.62517158 0.1098434 -0.4012537

SMB 1.33352558 1.26201711 1.05666204 0.29528515 -1.19561322

HML -1.61552234 1.40713627 -1.14809232 0.25589962 -4.43548643

UMD 0.13882223 0.77724175 0.17860882 0.85890117 -1.41880504

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 34/37

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.59140495

R Square 0.34975982

Adjusted R Sq 0.30246962Standard Erro 0.08974975

Observations 60

ANOVA

df SS MS F Significance F

Regression 4 0.23830068 0.05957517 7.39603242 7.684E-05

Residual 55 0.44302596 0.00805502

Total 59 0.68132664

Coefficients tandard Error t Stat P-value Lower 95%

Intercept -0.00440189 0.01271824 -0.34610842 0.73058176 -0.02988981

MKTRF 1.77791001 0.53926427 3.29691789 0.00171636 0.69720028

SMB 0.98293003 0.64260148 1.5296106 0.13184473 -0.3048721

HML 0.82687398 0.71649412 1.15405549 0.25346757 -0.60901233

UMD 0.38346361 0.39576064 0.96892811 0.33682278 -0.40965843

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 35/37

Upper 95% Lower 95.0% Upper 95.0%

0.05636888 -0.04374354 0.05636888

3.84359862 -0.4012537 3.84359862

3.86266437 -1.19561322 3.86266437

1.20444175 -4.43548643 1.20444175

1.6964495 -1.41880504 1.6964495

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 36/37

Upper 95% Lower 95.0% Upper 95.0%

0.02108603 -0.02988981 0.02108603

2.85861975 0.69720028 2.85861975

2.27073216 -0.3048721 2.27073216

2.26276028 -0.60901233 2.26276028

1.17658564 -0.40965843 1.17658564

8/2/2019 Four Factors

http://slidepdf.com/reader/full/four-factors 37/37

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.591405

R Square 0.34976

Adjusted R 0.30247

Standard E 0.08975Observatio 60

ANOVA

df SS MS F gnificance F

Regression 4 0.238301 0.059575 7.396032 7.68E-05

Residual 55 0.443026 0.008055

Total 59 0.681327

Coefficientsandard Err t Stat P-value Lower 95%Upper 95%ower 95.0 pper 95.0%

Intercept -0.0044 0.012718 -0.34611 0.730582 -0.02989 0.021086 -0.02989 0.021086

MKTRF 1.77791 0.539264 3.296918 0.001716 0.6972 2.85862 0.6972 2.85862

SMB 0.98293 0.642601 1.529611 0.131845 -0.30487 2.270732 -0.30487 2.270732

HML 0.826874 0.716494 1.154055 0.253468 -0.60901 2.26276 -0.60901 2.26276

UMD 0.383464 0.395761 0.968928 0.336823 -0.40966 1.176586 -0.40966 1.176586