15

BUILDING BUSINESS BANKING RIGHT FOR EUROPEAN ENTREPRENEURS

| Date post: | 26-Jan-2017 |

| Category: |

Internet |

| Upload: | friends-and-family |

| View: | 4,648 times |

| Download: | 0 times |

BUILDING BUSINESS BANKING RIGHT FOR EUROPEAN ENTREPRENEURS

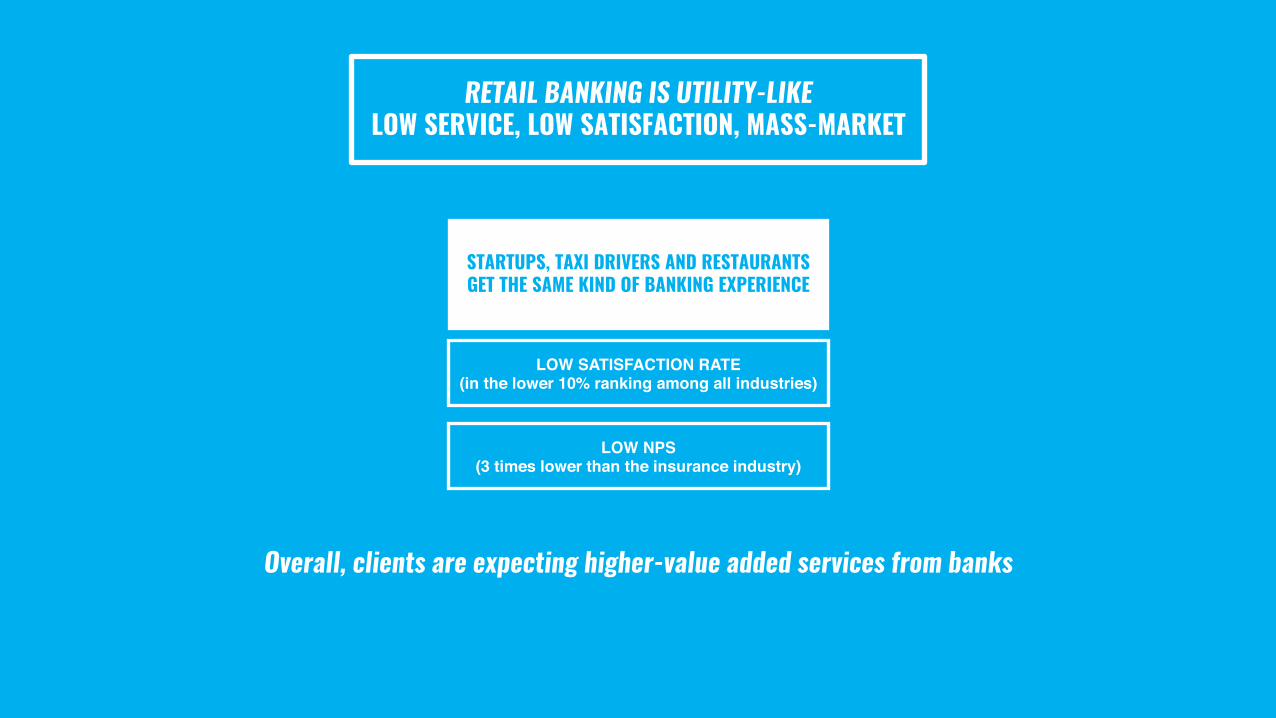

RETAIL BANKING IS UTILITY-LIKELOW SERVICE, LOW SATISFACTION, MASS-MARKET

LOW SATISFACTION RATE (in the lower 10% ranking among all industries)

STARTUPS, TAXI DRIVERS AND RESTAURANTS GET THE SAME KIND OF BANKING EXPERIENCE

LOW NPS(3 times lower than the insurance industry)

Overall, clients are expecting higher-value added services from banks

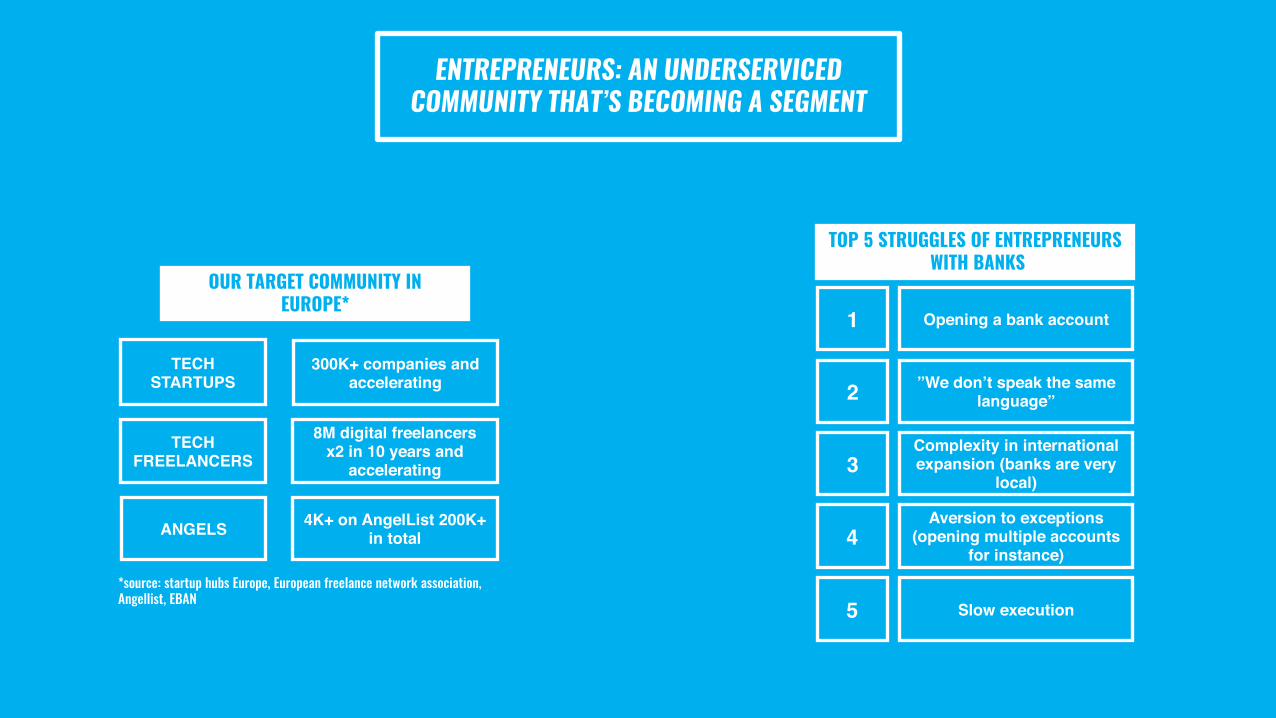

ENTREPRENEURS: AN UNDERSERVICED COMMUNITY THAT’S BECOMING A SEGMENT

TECH STARTUPS

OUR TARGET COMMUNITY IN EUROPE*

300K+ companies and accelerating

TECH FREELANCERS

8M digital freelancersx2 in 10 years and

accelerating

ANGELS 4K+ on AngelList 200K+ in total

*source: startup hubs Europe, European freelance network association, Angellist, EBAN

Opening a bank account

”We don’t speak the same language”

TOP 5 STRUGGLES OF ENTREPRENEURSWITH BANKS

Aversion to exceptions (opening multiple accounts

for instance)

Slow execution

Complexity in international expansion (banks are very

local)

1

2

3

4

5

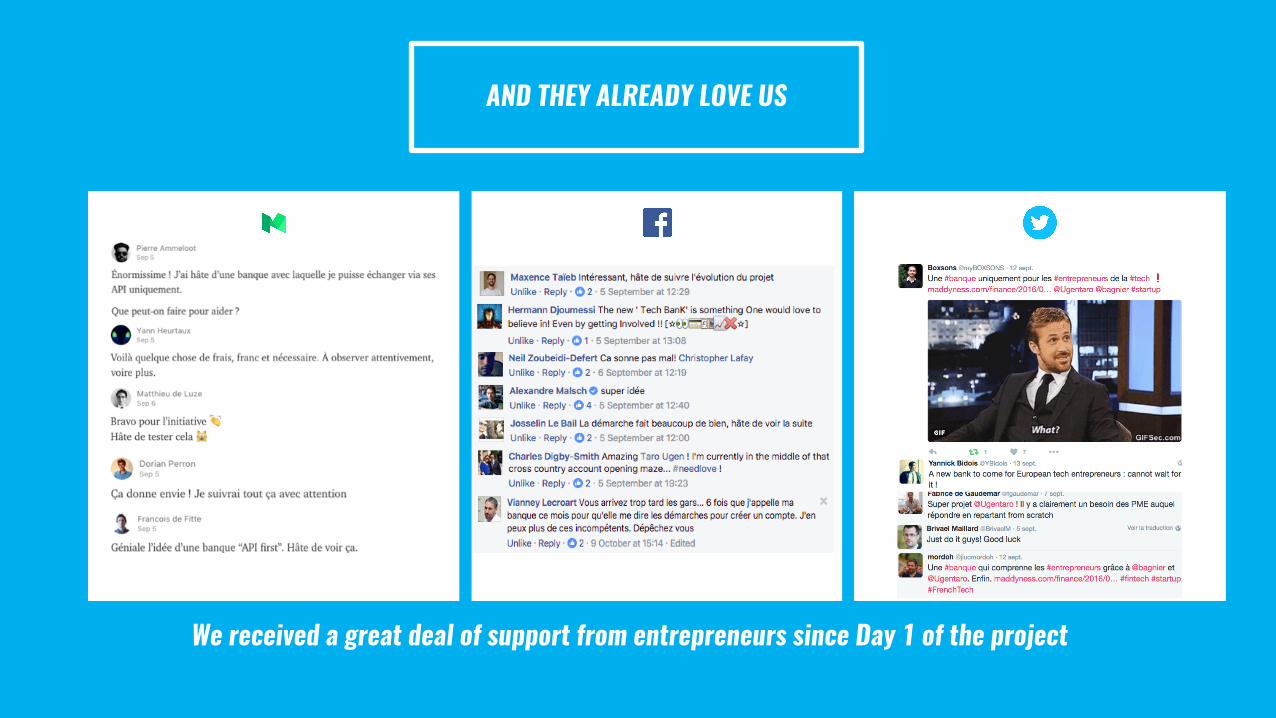

AND THEY ALREADY LOVE US

We received a great deal of support from entrepreneurs since Day 1 of the project

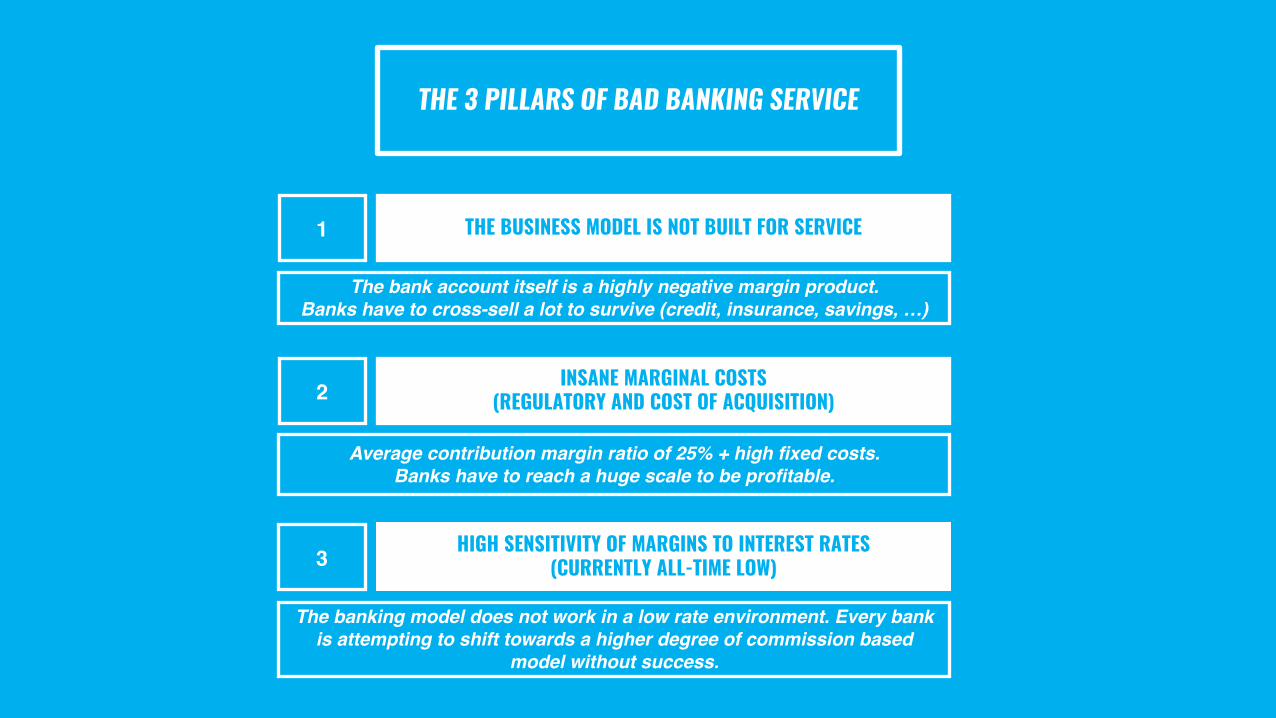

THE 3 PILLARS OF BAD BANKING SERVICE

Average contribution margin ratio of 25% + high fixed costs.Banks have to reach a huge scale to be profitable.

2 INSANE MARGINAL COSTS (REGULATORY AND COST OF ACQUISITION)

The bank account itself is a highly negative margin product. Banks have to cross-sell a lot to survive (credit, insurance, savings, …)

1 THE BUSINESS MODEL IS NOT BUILT FOR SERVICE

The banking model does not work in a low rate environment. Every bank is attempting to shift towards a higher degree of commission based

model without success.

3 HIGH SENSITIVITY OF MARGINS TO INTEREST RATES (CURRENTLY ALL-TIME LOW)

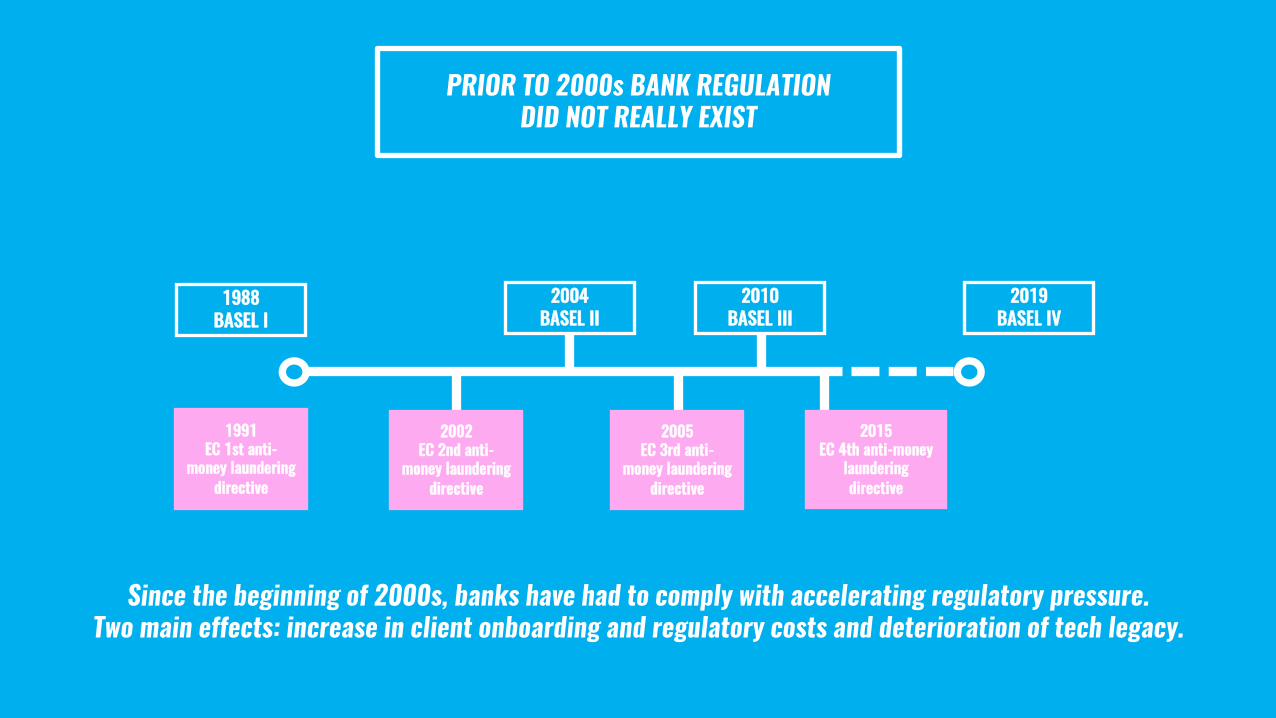

PRIOR TO 2000s BANK REGULATION DID NOT REALLY EXIST

1991EC 1st anti-

money launderingdirective

1988BASEL I

2004 BASEL II

2010BASEL III

2019BASEL IV

2002 EC 2nd anti-

money launderingdirective

2005EC 3rd anti-

money launderingdirective

2015EC 4th anti-money

launderingdirective

Since the beginning of 2000s, banks have had to comply with accelerating regulatory pressure. Two main effects: increase in client onboarding and regulatory costs and deterioration of tech legacy.

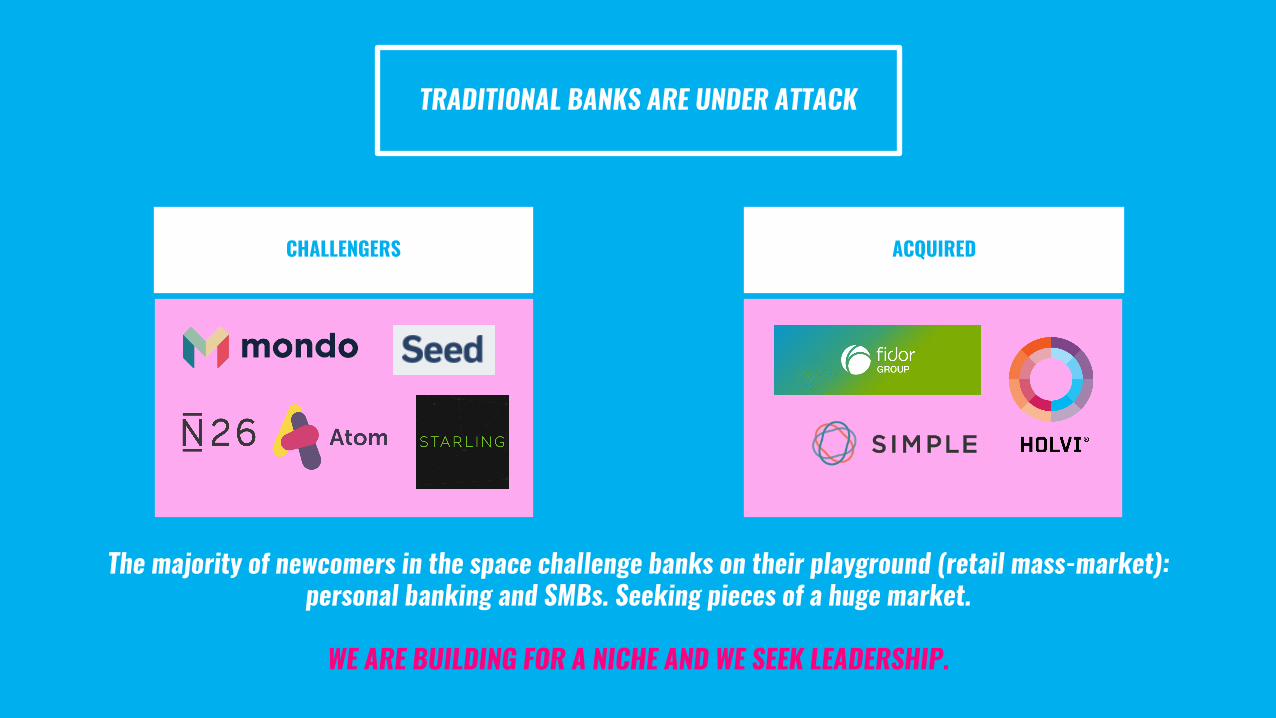

TRADITIONAL BANKS ARE UNDER ATTACK

CHALLENGERS ACQUIRED

The majority of newcomers in the space challenge banks on their playground (retail mass-market): personal banking and SMBs. Seeking pieces of a huge market.

WE ARE BUILDING FOR A NICHE AND WE SEEK LEADERSHIP.

[BUSINESS BANKING FOR HACKERS] OUR EARLY COMMUNITY HAS HELPED US DETERMIN WHAT TO BUILD FIRST

A simple banking product and an API

v

SUSCRIBE IN MINUTES

OPEN AS MANY ACCOUNTS AS YOU NEED AND SET UP RULES FOR EACH OF THEM

OPEN AND MANAGE ACCESS FORYOUR TEAM

ORDER CARDS FOR ALL YOUR TEAM AND MANAGE LIMITS

CONNECT WITH YOUR FAVOURITE PAYMENTS PROVIDER

API: BUILD ANY TYPES OF APPS TO READ DATA AND PUSH PAYMENTS

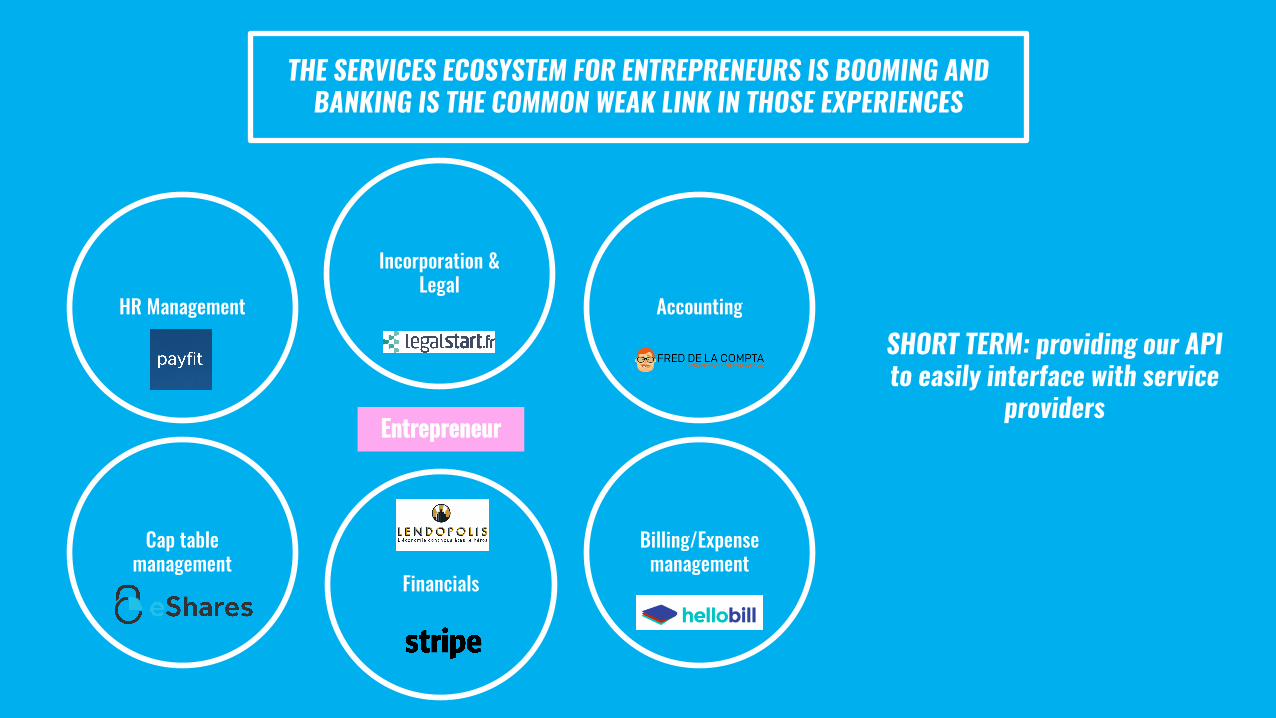

THE SERVICES ECOSYSTEM FOR ENTREPRENEURS IS BOOMING AND BANKING IS THE COMMON WEAK LINK IN THOSE EXPERIENCES

Entrepreneur

Cap table management

Accounting

Billing/Expensemanagement

HR Management

Incorporation & Legal

Financials

SHORT TERM: providing our API to easily interface with service

providers

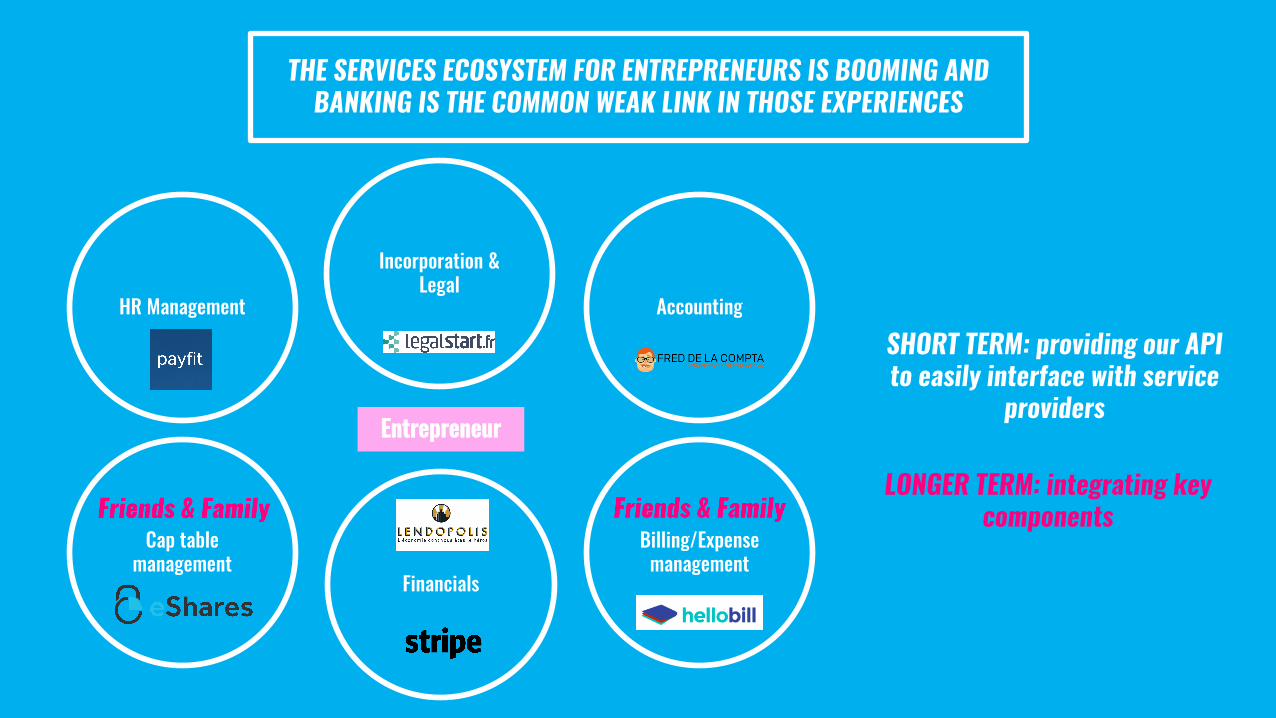

THE SERVICES ECOSYSTEM FOR ENTREPRENEURS IS BOOMING AND BANKING IS THE COMMON WEAK LINK IN THOSE EXPERIENCES

Entrepreneur

Cap table management

Accounting

Billing/Expensemanagement

HR Management

Incorporation & Legal

Financials

SHORT TERM: providing our API to easily interface with service

providers

LONGER TERM: integrating key components

WE ARE BUILDING FOR GROWTH

NICHE

STRONG FOCUS ON ACCOUNT

PRODUCTS

HOMEMADE SOFTWARE

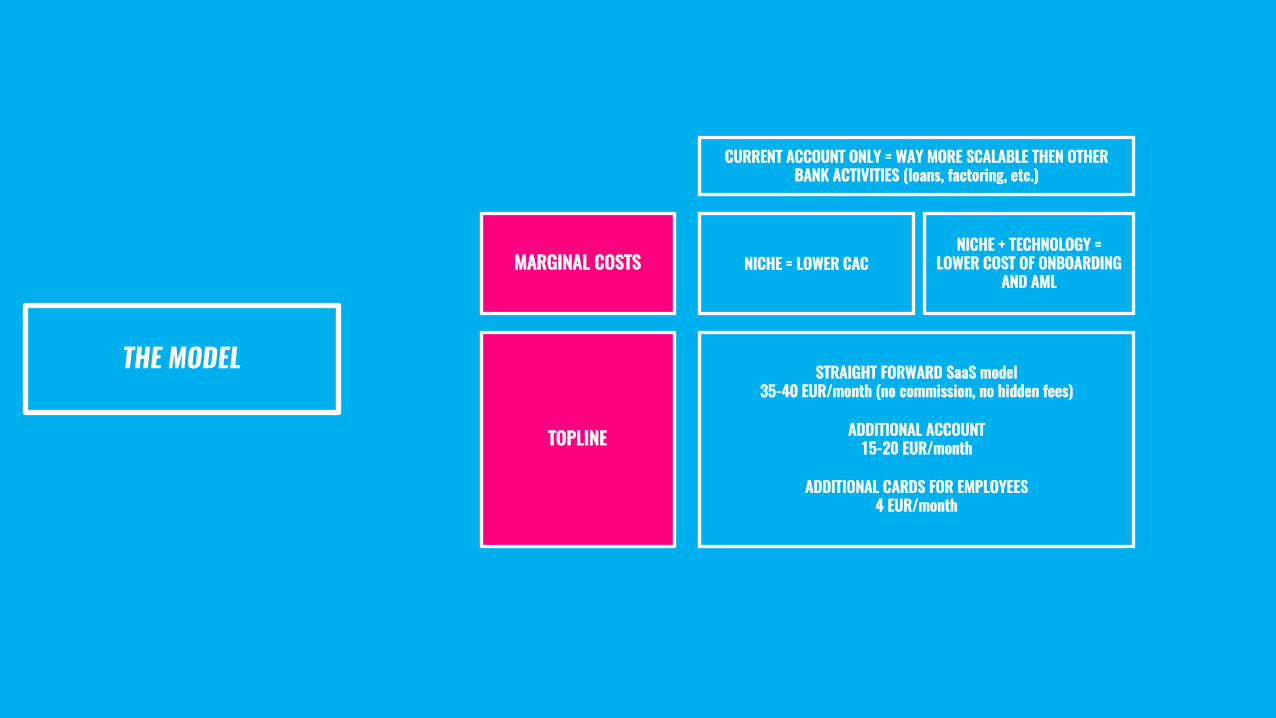

THE MODEL

MARGINAL COSTS NICHE = LOWER CACNICHE + TECHNOLOGY =

LOWER COST OF ONBOARDING AND AML

TOPLINE

STRAIGHT FORWARD SaaS model 35-40 EUR/month (no commission, no hidden fees)

ADDITIONAL ACCOUNT 15-20 EUR/month

ADDITIONAL CARDS FOR EMPLOYEES4 EUR/month

CURRENT ACCOUNT ONLY = WAY MORE SCALABLE THEN OTHER BANK ACTIVITIES (loans, factoring, etc.)

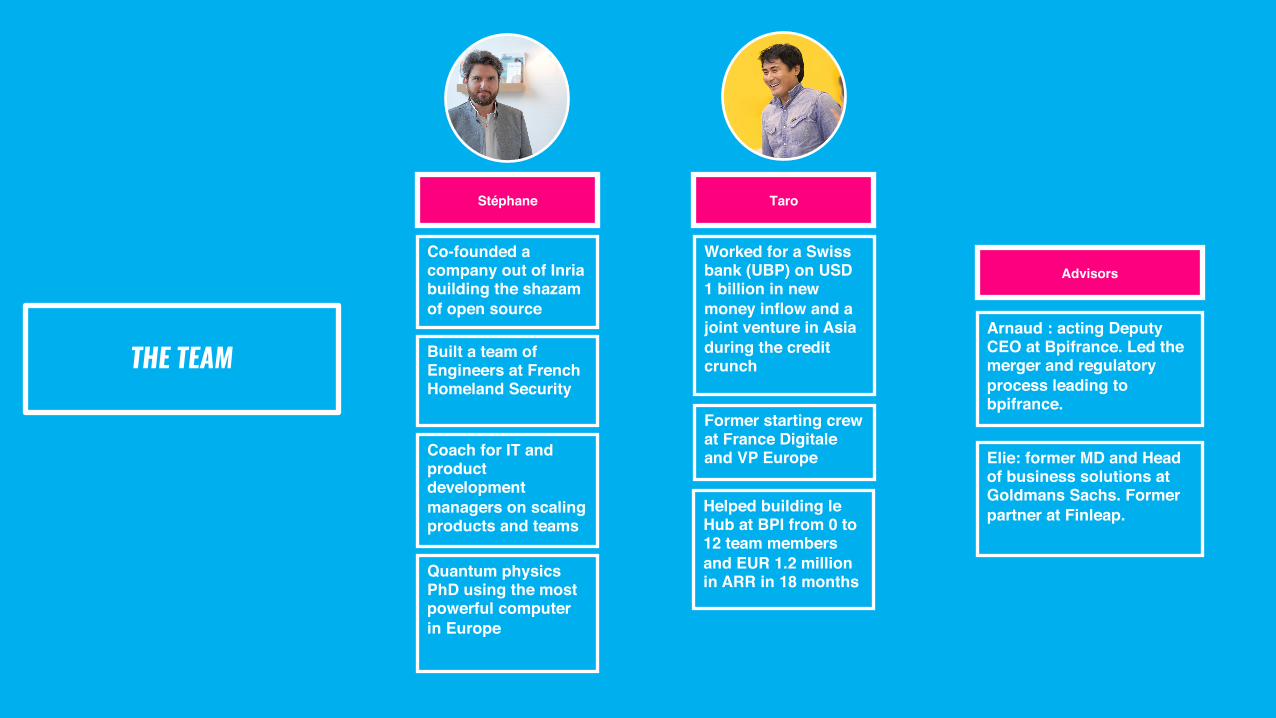

THE TEAM

Taro

Worked for a Swiss bank (UBP) on USD 1 billion in new money inflow and a joint venture in Asia during the credit crunch

Former starting crew at France Digitaleand VP Europe

Helped building le Hub at BPI from 0 to 12 team members and EUR 1.2 million in ARR in 18 months

Stéphane

Built a team of Engineers at French Homeland Security

Co-founded a company out of Inriabuilding the shazamof open source

Quantum physics PhD using the most powerful computer in Europe

Coach for IT and product development managers on scaling products and teams

Advisors

Arnaud : acting Deputy CEO at Bpifrance. Led the merger and regulatory process leading to bpifrance.

Elie: former MD and Head of business solutions at Goldmans Sachs. Former partner at Finleap.

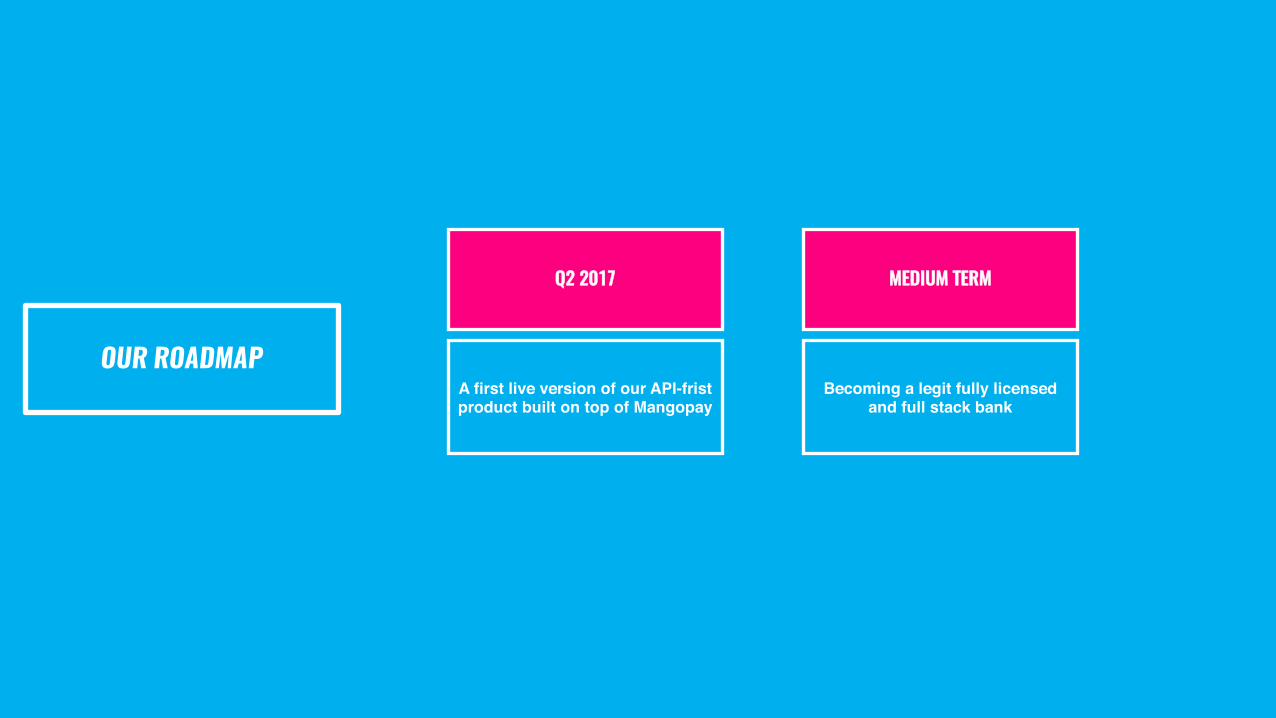

OUR ROADMAP

Q2 2017 MEDIUM TERM

A first live version of our API-fristproduct built on top of Mangopay

Becoming a legit fully licensedand full stack bank

IT’S AMBITIOUSEVERYBODY NEEDS A BANK.

WE ARE BUILDING THE TOP OF MIND BANK FOR THE EUROPEAN TECH INDUSTRY.