From PLI’s Online Program The Bank Holding Company Act: How to Handle Business Restrictions #20818 6 EXECUTIVE COMPENSATION GROUP ADVISORY — DISCLOSURE DEVELOPMENTS: EXECUTIVE COMPENSATION Ernest W. Torain, Jr. Vedder Price P.C. Disclaimers and Suggested Refer ences: The outline that follows provides a general overview of retiree medical benefit VEBAs, with specific focus on the VEBAs recently proposed by the Big Three U.S. automakers. The author is by no means an expert on

Transcript

From PLI’s Online ProgramThe Bank Holding Company Act: How to Handle Business Restrictions#20818

that follows provides a general overview of retiree

medical benefit VEBAs, with specific focus on the

VEBAs recently proposed by the Big Three U.S.

automakers. The author is by no means an expert on

THE BANK HOLDING COMPANY ACTTHE BANK HOLDING COMPANY ACT:HOW TO HANDLE BUSINESS RESTRICTIONS

Bradley K. SabelBradley K. SabelShearman & Sterling LLP

January 22, 2009y ,PLI

Th B k H ldi C A t (“BHCA”) G llThe Bank Holding Company Act (“BHCA”) Generally

Summary of previous programSummary of previous programDifference between a bank and a bank holding company (“BHC”)Federal Reserve as “umbrella” supervisor of BHCs and all subsidiaries Limitations on BHC activities in order to separate banking and commerce and to protect bank subsidiary(ies)

Focus of this presentationFocus of this presentationActivity restrictions of the BHCAMeaning of “control” under the BHCA and its significance for BHCs and their investorsinvestorsRestrictions on transactions between banks and their affiliates (Section 23A and the Federal Reserve’s Regulation W, 12 CFR Part 223)

NYDOCS01/1193066.1 2

A ti it R t i ti f th BHCAActivity Restrictions of the BHCA

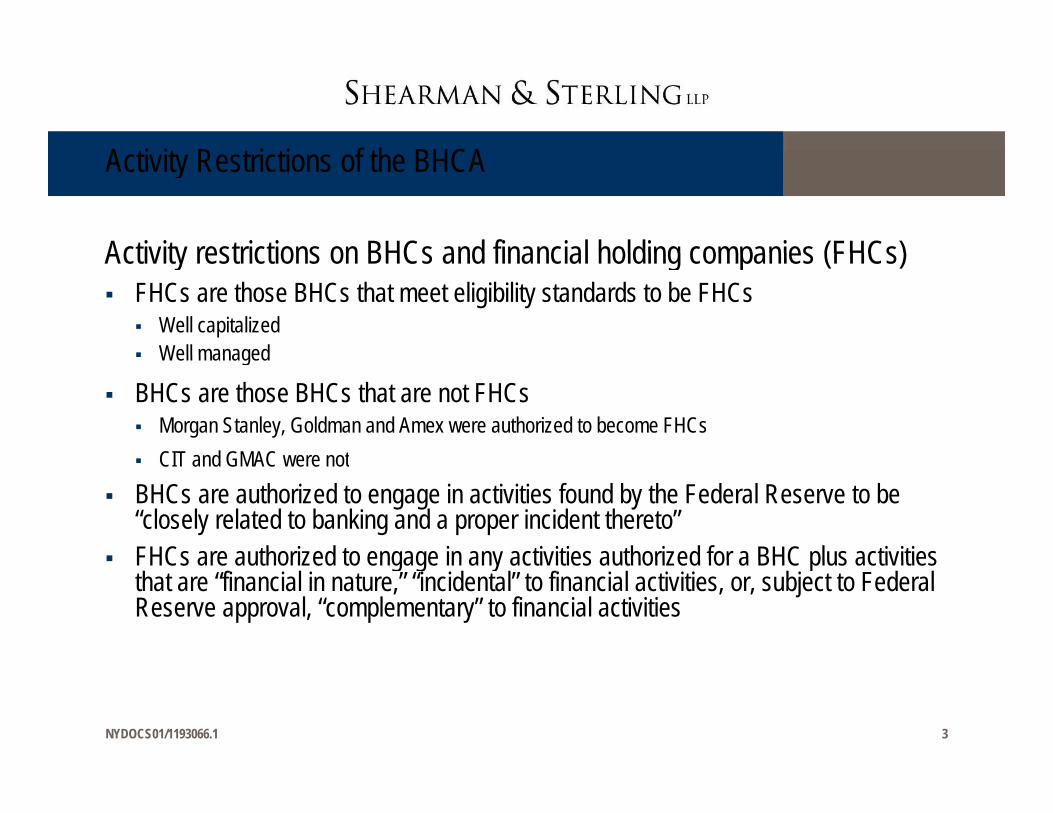

Activity restrictions on BHCs and financial holding companies (FHCs)Activity restrictions on BHCs and financial holding companies (FHCs)FHCs are those BHCs that meet eligibility standards to be FHCs

Well capitalizedWell managedWell managed

BHCs are those BHCs that are not FHCsMorgan Stanley, Goldman and Amex were authorized to become FHCsCIT and GMAC were notCIT and GMAC were not

BHCs are authorized to engage in activities found by the Federal Reserve to be “closely related to banking and a proper incident thereto” FHCs are authorized to engage in any activities authorized for a BHC plus activitiesFHCs are authorized to engage in any activities authorized for a BHC plus activities that are “financial in nature,” “incidental” to financial activities, or, subject to Federal Reserve approval, “complementary” to financial activities

NYDOCS01/1193066.1 3

A ti iti A th i d f BHCActivities Authorized for BHCs

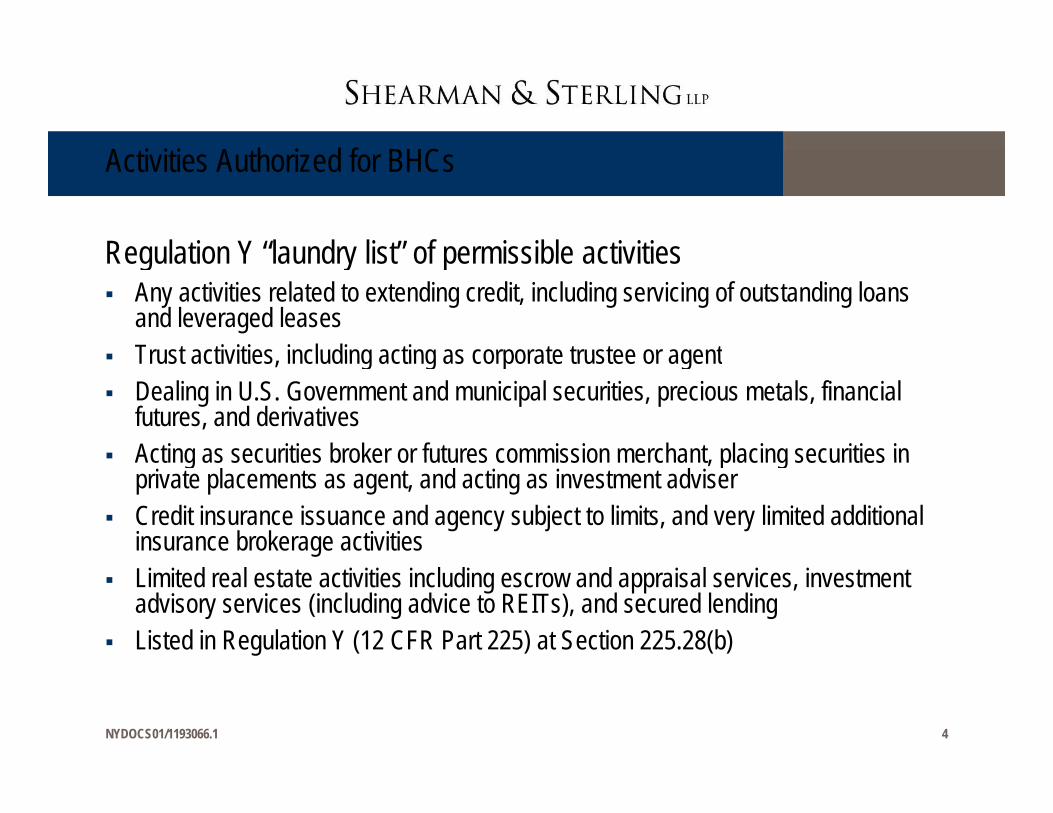

Regulation Y “laundry list” of permissible activitiesRegulation Y laundry list of permissible activitiesAny activities related to extending credit, including servicing of outstanding loans and leveraged leasesTrust activities including acting as corporate trustee or agentTrust activities, including acting as corporate trustee or agentDealing in U.S. Government and municipal securities, precious metals, financial futures, and derivativesActing as securities broker or futures commission merchant placing securities inActing as securities broker or futures commission merchant, placing securities in private placements as agent, and acting as investment adviser Credit insurance issuance and agency subject to limits, and very limited additional insurance brokerage activitiesLimited real estate activities including escrow and appraisal services, investment advisory services (including advice to REITs), and secured lendingListed in Regulation Y (12 CFR Part 225) at Section 225.28(b)

NYDOCS01/1193066.1 4

A ti iti A th i d f BHC ( ’t)Activities Authorized for BHCs (con’t)

Regulation K “laundry list” of permissible activities outside the UnitedRegulation K laundry list of permissible activities outside the United States

Wide range of non-U.S. activities allows BHCs to compete more effectively against non-U S banksnon-U.S. banksIncludes limited amount of underwriting and dealing in non-U.S. equities, limited insurance activities, and travel services (Regulation K, 12 CFR Part 211, at Sections 211.8 and 211.10(a))( ))

Permissible activities of non-U.S. banks inside or outside the United States

Non-U.S. banks generally subject to same Regulation Y list of financial businesses inside the United States as domestic BHCsException allows control of U.S. commercial companies if non-U.S. bank holds them through non U S subsidiaries engaged in same line of business (Section 211 23(f))

NYDOCS01/1193066.1 5

through non-U.S. subsidiaries engaged in same line of business (Section 211.23(f)) Any activity outside the United States is permissible

A ti iti A th i d f BHC ( ’t)Activities Authorized for BHCs (con’t)

Commencing engagement in a permissible activity in the United StatesCommencing engagement in a permissible activity in the United StatesBHCs must obtain prior Fed approval to commence engaging in an activity unless:

BHC and its subsidiary banks are well-capitalized,BHC and its subsidiary banks have satisfactory examination ratings, andBHC and its s bsidiar banks ha e had no o tstanding enforcement actions ithin the pre io sBHC and its subsidiary banks have had no outstanding enforcement actions within the previous 12 months

If BHC does not meet any of these standards, filing of a notice for prior approval is required; approval usually obtained within 12 or 30 days

Acquiring existing company engaged in a permissible activity in the United States BHCs must file a notice for prior Federal Reserve approval

Financial and managerial resources and risk management capabilities of BHC Antitrust and competitive effectsp

Approval usually obtained within 30 days

Commencing activities or acquiring companies outside the United StatesRegulation K provides set of standards and procedures different from Regulation Y (Section 211.9)

NYDOCS01/1193066.1 6

In general, prior Federal Reserve approval required for first non-U.S. investment, entry into a new country, and investments above certain dollar amounts based on BHC’s capital

A th i d A ti iti f FHCAuthorized Activities for FHCs

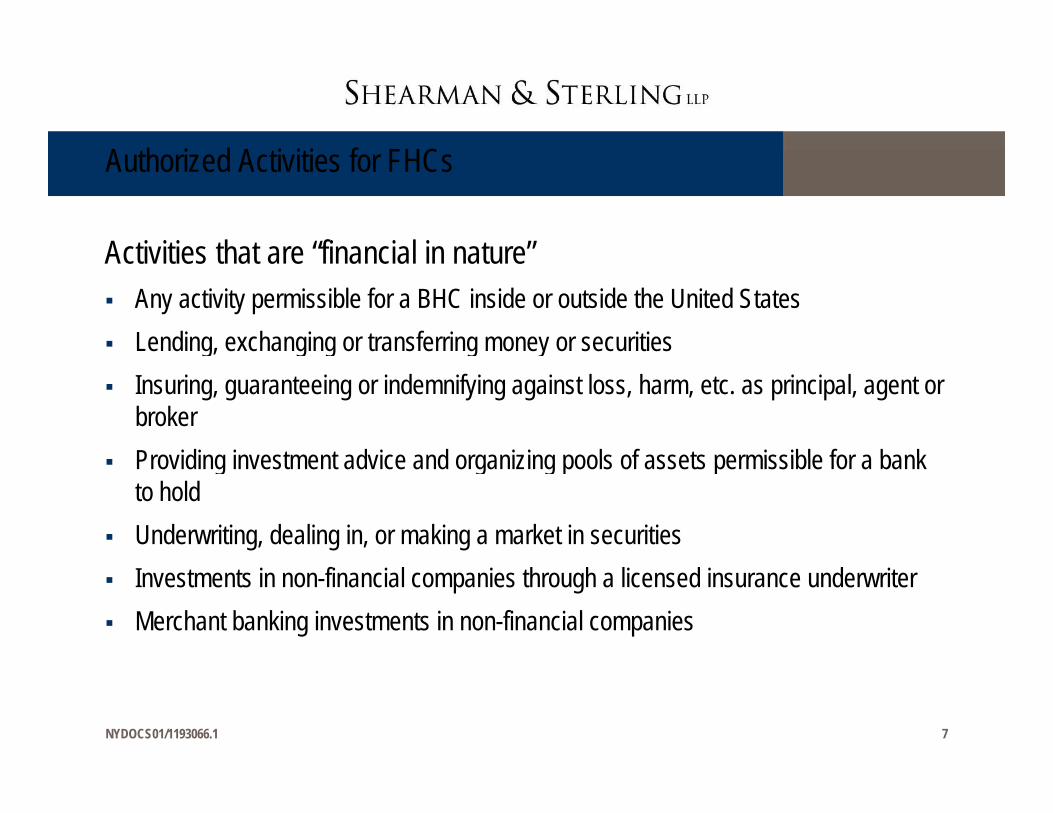

Activities that are “financial in nature”Activities that are financial in natureAny activity permissible for a BHC inside or outside the United StatesLending, exchanging or transferring money or securitiesg g g g yInsuring, guaranteeing or indemnifying against loss, harm, etc. as principal, agent or brokerProviding investment advice and organizing pools of assets permissible for a bankProviding investment advice and organizing pools of assets permissible for a bank to holdUnderwriting, dealing in, or making a market in securitiesInvestments in non-financial companies through a licensed insurance underwriterMerchant banking investments in non-financial companies

NYDOCS01/1193066.1 7

A th i d A ti iti f FHC ( ’t)Authorized Activities for FHCs (con’t)

Activities that are incidental to a financial activityActivities that are incidental to a financial activityFederal Reserve makes determination subject to Treasury Department approvalIntent is to authorize activities not truly financial but so connected with financial activities as to make it convenient to engage in themactivities as to make it convenient to engage in themFederal Reserve has found that acting as a finder by bringing buyers and sellers of any product or service together for transactions that the parties themselves negotiate

Operating a website for this purpose is authorized

Activities that are complementary to a financial activityFederal Reserve makes determinationSpot commodity activities authorized due to connection to commodity derivatives

FHC must request specific authority from Federal ReserveLimits apply based on FHC total capital controls handling of commodities

NYDOCS01/1193066.1 8

Limits apply based on FHC total capital, controls, handling of commoditiesLong-term power contracts and expanded transactions involving power (RBS order March 27, 2008)

A ti iti A th i d f FHC ( ’t)Activities Authorized for FHCs (con’t)

Commencing engagement in a permissible activity in the United StatesCommencing engagement in a permissible activity in the United StatesNo prior approval to engage in permissible activities de novoNo prior approval to acquire a going concernp pp q g g

Exception: acquisition of a thrift institutionCompliance with Hart-Scott-Rodino requirements and other antitrust requirementsSmall amount of impermissible activities by acquired company permissible with two-year grace period

fto conform

If FHC ceases to be well-capitalized or well-managedPrior Federal Reserve approval required for commencement of engagement in an activity requiring FHC th it ( t j t BHC th it ) t iFHC authority (not just BHC authority) or to acquire any companyFHC required to enter into agreement with Federal Reserve to fix the problem and return to eligibilityFederal Reserve highly unlikely to give approval for commencement or acquisition, on theory that FHC should devote its efforts to returning to eligibility

NYDOCS01/1193066.1 9

g g y

Fi i l b idi iFinancial subsidiaries

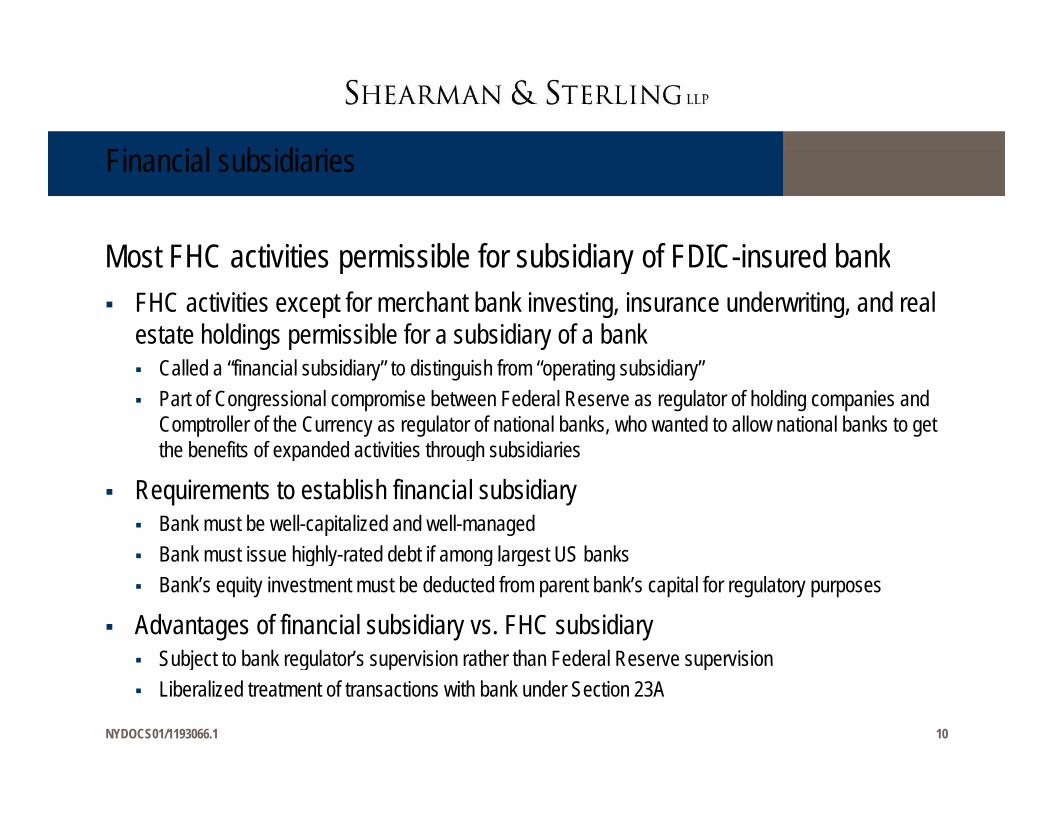

Most FHC activities permissible for subsidiary of FDIC insured bankMost FHC activities permissible for subsidiary of FDIC-insured bankFHC activities except for merchant bank investing, insurance underwriting, and real estate holdings permissible for a subsidiary of a bank

Called a “financial subsidiary” to distinguish from “operating subsidiary”Part of Congressional compromise between Federal Reserve as regulator of holding companies and Comptroller of the Currency as regulator of national banks, who wanted to allow national banks to get the benefits of expanded activities through subsidiariesp g

Requirements to establish financial subsidiaryBank must be well-capitalized and well-managedBank must issue highly-rated debt if among largest US banksBank must issue highly rated debt if among largest US banksBank’s equity investment must be deducted from parent bank’s capital for regulatory purposes

Advantages of financial subsidiary vs. FHC subsidiarySubject to bank regulator’s supervision rather than Federal Reserve supervision

NYDOCS01/1193066.1 10

Subject to bank regulator s supervision rather than Federal Reserve supervisionLiberalized treatment of transactions with bank under Section 23A

“C t l” d th BHCA“Control” under the BHCA

“Control” is important for several purposesControl is important for several purposesAny company that controls a BHC/FHC must itself become a BHC/FHCAny company controlled by a BHC/FHC (a “subsidiary” of the BHC/FHC) is subject y p y y ( y ) jto the activity restrictions of the BHCA

This is true for any company of which a BHC/FHC owns 5% or more of any class of voting stockAny shares held by a company controlled by a BHC/FHC are attributed to the parent and are aggregated for purposes of determining whether parent owns or controls 5% or more of any class of voting stock of another company

Any subsidiary of a FHC/BHC is subject to Federal Reserve examination, supervision and enforcement authoritysupervision and enforcement authority

Many potential targets of a FHC/BHC do not want to become subject to BHCA restrictionsNoncontrolling investment by FHC/BHC is an alternative to avoid subsidiary status

NYDOCS01/1193066.1 11

“C t l” d th BHCA ( ’t)“Control” under the BHCA (con’t)

Statutory definition of “control”Statutory definition of controlOwnership or control of 25% or more of any class of voting stockControl in any manner of a majority of the board of directorsControl in fact as determined by the Federal Reserve after notice and opportunity for a hearing, with burden of proof on Federal Reserve to prove control

“Control in fact” is the issue that has attracted recent attentionControl in fact is the issue that has attracted recent attentionFederal Reserve held hearings on control in the 1960s and 1970sHolding hearings is time-consuming and burdensome for staffFederal Reserve announced policy on control that effectively put burden on BHCs to comply with certain standards in order to avoid a finding of control

Federal Reserve effectively reversed the burden of proof on BHC/FHCsFor those not already subject to BHCA technically the policy does not apply; however to avoid Federal Reserve

NYDOCS01/1193066.1 12

For those not already subject to BHCA, technically the policy does not apply; however, to avoid Federal Reserve action, most parties try to comply and discuss their proposed investment with staff in order to get informal agreement that it will not result in a finding of control

“C t l” d th BHCA ( ’t)“Control” under the BHCA (con’t)

Current policy on noncontrolCurrent policy on noncontrolPrior policy issued originally in 1982 and complicated by later decisionsOriginal rules (Regulation Y at Section 225.143):g ( g )

Total equity (amount of funds invested based on US GAAP balance sheet of target) no greater than 25%Convertible securities treated as voting stock unless subject to restrictions on sale upon conversion, primarily that sales must be in a public distribution with no more than 2 percent sold to any one investorNumber of directors generally no greater than the voting interest would allow except that one director permittedNumber of directors generally no greater than the voting interest would allow except that one director permittedGenerally no covenants to approve major policies, such as annual budgets, major acquisitions, hiring of senior staff and the like, and limited business relationships between the bank and investor

September 2008 revision (press release September 22, 2008 (Section 225.144))Total equity no greater than 33% so long as voting interest no greater than 15%One director permissible, and two directors permissible if proportional to total voting or equity interest, less than 25% of total board seats, and another investor has a larger investment and is subject to the BHCANo covenant to approve major policies, but expression of views to management permitted

NYDOCS01/1193066.1 13

Covenants and business relationships must be limited and effectively require Federal Reserve consultation

“C t l” d th BHCA ( ’t)“Control” under the BHCA (con’t)

Consequences of “control” for venture capital firmsConsequences of control for venture capital firmsFirms desire to invest in banks but not to become subject to BHCA requirementsInvestments complying with noncontrol policy can achieve investment goalsp y g p y g

Corsair investment in NatCityTPG investment in WaMuCerberus and GM investment in GMAC

Cerberus to reduce stake to less than 25%GM to reduce to less than 10%

Investments by various groups in IndyMac successor thrift

Group of venture capital investors generally called “silo” investmentsGroup of venture capital investors generally called silo investmentsEach group can be found not to have control so long as it does not have interlocking relationships or arrangements with the other groupsDiscussions with Federal Reserve staff necessary in order to establish that the policy is being

NYDOCS01/1193066.1 14

complied with

O i f S ti 23A d 23B d R WOverview of Sections 23A and 23B and Reg. W

Statutory BackgroundStatutory BackgroundSection 23A was originally enacted in 1933 as part of the Glass-Steagall Act and was completely revised in 1982; Section 23B was enacted in 1987S ti 23A d 23B b th i t t t b k d th f d l d it iSection 23A and 23B both aim to protect banks and the federal deposit insurance fund. While Section 23A imposes limits on the amounts of extensions of credit and certain other “covered transactions”, Section 23B requires that transactions be at arm’s length and on “market terms”arm s length and on market termsIn October 2002, the Board adopted Regulation W, which was designed to provide guidance to the banking industry with respect to the application of Sections 23A and 23B

NYDOCS01/1193066.1 15

O i f S ti 23A d 23B d R WOverview of Sections 23A and 23B and Reg. W

Section 23ASection 23ASection 23A is often described as simple in concept, but complicated in its application –particularly to large, complex banking organizations participating in modern financial marketsS i 23A k hi i i lSection 23A seeks to achieve its purpose in several ways

Limitations on “covered transactions” with affiliatesRequirement of “safe and sound banking practices”Prohibition from purchasing low quality assets from an affiliateProhibition from purchasing low-quality assets from an affiliateRequirement of a defined amount of collateralThe “Attribution Rule”

Section 23BSection 23B protects a bank by requiring that transactions between the bank and its affiliates occur on market terms

NYDOCS01/1193066.1 16

Section 23B applies this restriction to any “covered transaction” as well as other transactions

O i f S ti 23A d 23B d R WOverview of Sections 23A and 23B and Reg. W

Regulation WRegulation WRegulation W was proposed for several reasons

The new regulatory framework established by the Gramm-Leach-Bliley Act (“GLB Act”) emphasized th i t f S ti 23A d 23Bthe importance of Sections 23A and 23BA comprehensive regulation allows the Board to place together in a single document the various Board interpretations and staff opinions relating to the statute that have been issued over the yearsIt simplifies the task of complying with the statute and ensures that the rules are interpreted p p y g pconsistentlyIt gave an opportunity to comment on Board and staff interpretations of Sections 23A and 23B and to discuss the concerns that were raised over the years

NYDOCS01/1193066.1 17

D fi iti f “Affili t ”Definition of “Affiliate”

General DefinitionGeneral DefinitionGenerally, any subsidiary of a BHC/FHC plus the following is an affiliate:

Any company that is “sponsored and advised” by any bank or bank-affiliateAny investment company registered under the Investment Company Act of 1940 (“ICA”) for which the bank or its affiliate serves as an investment advisoror its affiliate serves as an investment advisor

“Sponsored and advised test”The Board stated that a “sponsored and advised company” is one

that receives investment advice and administrative services on a contractual basis from a member bank,h t t l t d b th b k dwhose trustees or managers are selected by the bank, and

that has a name similar to that of the bank. The Board expressed its expectation that banks treat companies meeting or substantially meeting these three indicia of sponsorship and advice as affiliates under Regulation W.

Also includes any unregistered investment fund if the bank or any affiliate serves as an investmentAlso includes any unregistered investment fund if the bank or any affiliate serves as an investment advisor to the fund and owns more than 5 percent of any class of voting shares.By doing so, many of the following funds are treated as affiliates:

Private equity fundsForeign Investment funds

NYDOCS01/1193066.1 18

Foreign Investment fundsCommodity funds

“C d T ti ”“Covered Transaction”

Definition of “Covered Transaction”Definition of Covered TransactionCovered Transactions under Section 23A and Regulation W include:

A loan or extension of credit to an affiliateA purchase of or investment in securities issued by an affiliateA purchase of, or investment in, securities issued by an affiliateA purchase of assets from an affiliate (including assets subject to a repurchase agreement)The acceptance of securities issued by an affiliate as collateral for a loan or extension of credit to any personThe issuance of a guarantee on behalf of an affiliate

Certain types of transactions to which a bank is a party are exempt fromSection 23A’s restrictions:

Deposits to the credit of an affiliated bank or affiliated foreign bank in the ordinary course of correspondent businessGi i f i di t dit t ffili t ll t d it i d i th di f b iGiving of immediate credit to an affiliate on uncollected items received in the ordinary course of businessPurchases of assets having a “readily identifiable and publicly available market quotation” (the “Market Quotation Exemption”)Transactions secured by obligations issued or fully guaranteed as to principal and interest by the U.S. government or its agencies or by a segregated earmarked deposit account

NYDOCS01/1193066.1 19

its agencies, or by a segregated earmarked deposit account

Li it ti d R t i tiLimitations and Restrictions

Quantitative LimitsQuantitative LimitsSection 23A prohibits a bank from engaging in any “covered transactions” with an affiliate if:

The aggregate amount of the bank’s covered transactions with that affiliate would exceed 10 percent of the capital stock and surplus of the bank (a financial subsidiary of a bank is exempt from this limit); orp p ( y p );The aggregate amount of the bank’s covered transactions with all affiliates would exceed 20 percent of the capital

The 10/20-rule only applies to a new covered transaction. A bank is not required to reduce existing transactions when its capital declines or when a pre existing covered transaction increases intransactions when its capital declines or when a pre-existing covered transaction increases in value

Collateralization RequirementSection 23A and Regulation W require that all extensions of credit to, or on behalf of, affiliates, all guarantees, acceptances and letters of credit issued on behalf of an affiliate and all cross-affiliate netting arrangements (“credit transactions”) be collateralized by an amount of collateralTh t f ll t l i i l f 100 t t 130 t f th l f th dit

NYDOCS01/1193066.1 20

The amount of collateral varies in value from 100 percent to 130 percent of the value of the credit extended depending on the nature of the collateral

Li it ti d R t i ti ( ’t)Limitations and Restrictions (con’t)

The market term requirement in Section 23BThe market term requirement in Section 23BSection 23B generally requires that transactions between a bank and its non-bank affiliates be on terms and under circumstances, including credit standards (the “market term requirements”):term requirements ):

that are substantially the same, or at least as favorable to the bank, as those prevailing at the time for comparable transactions with the involving non-affiliates; orIn the absence of comparable transactions, that in good faith would be offered to, or would apply to,

ffili tnon-affiliates

The market requirement applies not merely to covered transactions pursuant toSection 23A but also to the following transactions:

Any sale of assets by the bank to an affiliateAny sale of assets by the bank to an affiliateAny payment of money or furnishing of services by the bank to an affiliateAny transaction in which an affiliate acts as an agent or broker for the bank or any other person if the bank is participant in the transaction

NYDOCS01/1193066.1 21

Any transaction by the bank with a third party if an affiliate has a financial interest in the third party or if an affiliate is a participant in the transaction

Att ib ti R lAttribution Rule

The RuleThe RuleThe attribution rule of Section 23A states that any transaction by a bank with a third party in which the proceeds of the transaction are paid or transferred by the third party to an affiliate of the bank is treated as though the bank engaged in the transaction directly with the affiliateThe intent of the attribution rule is to prevent evasions of the general rule The attribution rule is the provision that raises the most concerns as it is for major financial institutions with many lines of business almost impossible to comply with