185

FROM STANSBERRY & ASSOCIATES INVESTMENT RESEARCH

FROM STANSBERRY & ASSOCIATES INVESTMENT RESEARCH

Published by Stansberry & Associates Investment Research.

Copyright 2014 Stansberry & Associates Investment Research. All Rights Reserved. Any brokers mentioned herein constitute a partial list of available brokers and is for your information only. S&A does not recommend or endorse any brokers, dealers, or financial advisors.

INTRODUCTION

Dear Stansberry & Associates reader,

In the past several years, an incredible amount of Americans have become interested in trading stocks, commodities, and currencies.

I can’t blame them at all.

Twenty years ago, managing your portfolio was simple: Buy a hand-ful of solid companies or send your cash to a great fund manager like Peter Lynch and watch the money pile up over the years.

After all, the years between 1982 and 1999 were the golden years of stock investing.

But this approach has brought nothing but misery for most investors since 2000. Wall Street has proved yet again it can’t be trusted to do anything except go after as many fees and scams as possible.

It pushed overvalued tech stocks in 2000 (while calling them sh*t in private e-mails). It helped Enron and WorldCom take in billions of investor dollars. It pushed risky mortgage securities in 2006. And when the wall of mortgage debt crashed down in 2008, they got their buddies in Washington, D.C. to bail them out with your money.

Given this behavior, I can’t blame folks for wanting to learn how to trade short-term market movements. Done with a solid risk-manage-ment plan, this approach can safely return at least 20% annually.

That’s why we’ve put together the S&A Trader’s Manual.

Our goal with the S&A Trader’s Manual is to provide our readers with the knowledge and tools to help them become smarter, more successful traders.

Inside these pages, you’ll learn how to profit as stocks fall... how to use charts in order to make the safest profits the right way... how to time any market... the two biggest factors in your trading success... the right way to trade along corporate insiders... and the most im-portant thing ever said about trading.

I guarantee if you take the information in the following pages to

heart, you’ll be a vastly better – and richer – trader. And you’ll never be scammed by Wall Street again.

Regards,

Brian HuntEditor in Chief, Stansberry Research

CONTENTS

KNOWLEDGE BASE: HOW TO THINK ABOUT TRADING

The 10 Best Things Ever Said About Trading

The Seven Real Secrets of the World’s Best Investors

This Little-Known Secret Virtually Guarantees You’ll Make Money in the Market

The Magic Words Every Investor/Trader Says Over and Over, All the Time

The Four Dirtiest Words in Trading

The Only Reliable Cycle in the Market

TRADER’S TOOL BOX: SYSTEMS AND STRATEGIES THAT MAKE MILLIONS

Common Sense Guide to Technical Analysis

The Trader’s Best Friend

Don’t Lose Money: The Most Important Law of Lasting Wealth

A Short Guide to Using Stop Losses

The Right Time to Change a Stop Loss

The Art of the Short Sale

The S&A Guide to Options Trading

The Easiest Way to Make Money in a Risky Stock Market

How to Safely Double and Triple the Returns in Your Retire-ment Account

Top Insider Buying Strategies

This Is One of the Best Insider Buying Indicators in the World

1

2

23

41

47

53

55

58

59

84

87

90

92

94

109

119

126

149

151

An Incredibly Powerful Trading Tool You’ve Never Heard Of

Advanced Chart-Reading Course

Time the Market... Any Market

APPENDIX A

Five Books That Can Make You a Millionaire Trader

APPENDIX B

How to Buy Securities and Set Up Your Options Account

153

156

167

169

170

174

175

Knowledge Base: How to Think About Trading

2

S&A Trader’s Manual

Table of Contents

THE 10 BEST THINGS EVER SAID ABOUT TRADINGAND HOW TO USE THEM TO ENSURE

YOUR FINANCIAL FREEDOM

By Brian HuntEditor in Chief, Stansberry Research

Spend much time studying the art of trading, and you’re bound to come across hundreds of quotes about making money in stocks and commodities.

In mid-2009, I took on the challenge to boil down the thousands of pages I’ve read on trading... the hundreds of hours spent talking about it... and the experiences I’ve had since I started trading at 18.

At the risk of being struck down by the trading gods, I think I did a good job of boiling down a century of trading wisdom by selecting just 10 quotes... and supporting each one with a short essay that explains its meaning.

I believe that if you read and internalize each of these 10 quotes, you’ll always win in the stock, bond, and commodity markets.

Good trading,

Brian

Of all the brilliant things Jim Rogers has ever said, I believe this one is head-and-shoulders above the rest.

Rogers is one of the most successful money managers in history. He made so much money investing and trading during the 1970s, he left the conventional side of work to travel and run his own mon-

1. “I just wait until there is money lying in the corner, and all I have to do is go over there and pick it up. I do nothing in

the meantime.” – Jim Rogers

3

KNOWLEDDGE BASE

Table of Contents

ey. You can read more about him in the greatest trading book ever, Market Wizards.

In that short quote above, Rogers nails one of the most important factors to trading and investment success: Don’t spend your time and energy chasing mediocre trades and investment opportunities. Only move when the odds are overwhelmingly in your favor.

If you follow his lead, you’ll probably end up a very successful trad-er. If you don’t, you’ll contribute to the bank accounts of those who do follow his lead.

You see, the average market participant always feels like he has to be “doing something.” He chases all kinds of ideas... takes lots of “fliers”... acts on all kinds of magazine articles, CNBC shows, and hot tips from buddies. He’s always on his phone or computer check-ing quotes. He usually has a bunch of stocks in his portfolio that are down big... but are sure to “come back.”

Not Jim Rogers.

In all his books, interviews, and articles, Rogers makes it clear he spends long stretches of time without having significant money at work in the market. He waits for extraordinary opportunities, where the odds are so far in his favor, the position is like picking up free money. When he doesn’t see any sure things, he simply sits in cash and does nothing.

Now, don’t get me wrong. There are few 100% can’t-lose trades and investments in this world. I’m not encouraging you to find trades that carry no risk of loss. I’m encouraging you to find trades where the odds are heavily stacked in your favor.

Find “extreme” opportunities... where the sentiment toward an asset is shifted to one side... where the valuation is ridiculously expensive or ridiculously cheap... and where the market is moving in the right direction and confirming your thesis. These are the opportunities where you can risk $1 and make $5 or $10.

Only then should you commit a large chunk of capital to an idea.

If you’re not seeing any extremes, it’s best to fight the natural

4

S&A Trader’s Manual

Table of Contents

urge to stay busy and make “this might-could-kinda-work” trades. These trades will just distract you, cause stress, and run up your commission bill.

Most older, rich investors and traders will tell you they made most of their money on five or 10 positions they had tremendous convic-tion in... where it felt like they were simply picking up free money. They’ll tell you the other positions weren’t worth the time it took to put them on.

This is not to say there aren’t a lot of great traders out there who make quick, frequent trades. But folks who can do that are few and far between. Most regular traders don’t have the time or the temper-ament for it.

So be lazy in the market. Don’t worry about sitting on a big pile of cash, waiting for low-risk, high-reward trades. It’s the idea behind “free money” trading. It’s the thinking that built and maintained Jim Rogers’ wealth.

It can do the same for you.

I know... this quote sounds bizarre. But hear me out: It contains an incredible seed of trading knowledge.

Hamilton was one of the first editors of the Wall Street Journal... He was one of the country’s most respected market analysts 80 years ago. And the legendary market advisor Richard Russell still recom-mends reading Hamilton’s book The Stock Market Barometer, once a year.

So what does Hamilton mean by “right too soon”?

Well, many traders and investors have a strong “hero streak” in

2. “Wall Street’s graveyards are filled with men who were right

too soon.” – William Hamilton

5

KNOWLEDDGE BASE

Table of Contents

them. They have a lot of confidence in their ability to value assets and gauge investor sentiment. They love to “see what others don’t,” step into a runaway market, and bet on prices moving the other way.

It’s an exciting way to trade. It’s like being the only guy standing on the beach while a hurricane approaches. Problem is, the hurricane will usually blow you into the next state.

That hurricane hit a lot of traders in late 1999... Tech stocks had ab-solutely soared for five years, many companies were trading for 100 or 200 times earnings, and sentiment was overwhelmingly shifted to one side. It was an extreme situation – the kind you should always be hunting for.

Any experienced trader was looking to bet the other way. But any trader who actually made the bet was “right too soon.” Take a look...

Even though the Nasdaq was overvalued at the time... even though the rally was long in the tooth... it was a bad move to short with the Nasdaq at 3,500 (circled in red). It was too early. The crazed public drove the index 30% higher over the coming months.

Now, have a look at the blue circle. What’s so special about this area? This was the point at which the market started moving in the “direction of sanity.” This was the point the bubble popped. This

6

S&A Trader’s Manual

Table of Contents

was the market getting started in the direction the bears believed it would. Traders call this “price confirmation.”

Smart traders always wait for a bit of “price confirmation” before they back a trading thesis with big money.

They know the market can run far away from rational fundamental values. They know how easy it is to be “right too soon.” So they wait for the price to move in their direction for five or 10 trading ses-sions... or they wait for the price to break through a moving average.

The point is, they let the market exhaust itself before they step in. So it’s as easy as pushing over an exhausted runner (on the bear side)... or climbing aboard a gently moving freight train (on the bull side).

Wall Street’s graveyards are filled with guys who got killed because they tried to step in front of runaway markets. So keep Hamilton’s words in mind anytime you’re considering being a “hero.” Find mar-ket extremes... then wait to be right.

Jesse Livermore was one of the most respected traders of the 1920s. He built one of America’s largest fortunes at the time with his skills in the stock and commodity markets. The classic book Remi-niscences of a Stock Operator contains his story.

“Sitting tight” was Livermore’s term for not selling when he was up 20%... 50%... or 100% on a position. Sitting tight is the art of not taking quick profits.

You see, most traders and investors get tempted to sell their winners after they see a modest profit... like, say, 33%. They get fidgety. They tell themselves that, “You can’t go broke taking a profit.” They always feel like they should be doing something, so they take action and jump out of the winning trade.

3. “It never was my thinking that made big money for me. It

was always my sitting. Got that? My sitting tight!” – Jesse Livermore

7

KNOWLEDDGE BASE

Table of Contents

This strategy will kill your long-term trading performance.

For instance... I have a friend who bought shares of Brazilian oil company Petrobras in 2003 for around $5 per share. He doubled his money in just over a year... and then sold. Nothing negative hap-pened with the position – he just got fidgety and figured a double was good enough.

It’s a shame my friend didn’t “sit tight,” because Petrobras eventually climbed to $70 per share. He missed the chance to make 14 times his money instead of one times his money. He missed the chance to ride a huge, multi-year trend in oil stocks to its fullest extent.

That’s it. When you are right on a trade – whether it’s tech stocks, biotech stocks, oil, or gold – ride it for all it’s worth. Don’t cut your profits short. Don’t sell until you see a legitimate reason for con-cern... like a decline of more than 15%... or an asset’s refusal to rise on bullish news. One of the best ways to get rich in the stock market is to get in early on a big trend and ride it for years... You can’t ride a trend if you don’t sit tight.

And although we’re concerned with trading here, it’s worth pointing out a key fact about the world’s greatest investor, Warren Buffett... Buffett’s partner, Charlie Munger, claims Buffett’s edge over other investors is that he “sits on his ass and reads a lot.” Buffett spends most of his time sitting. And don’t forget Jim Rogers’ “I just wait until there is money lying in the corner” philosophy.

You see, you can go broke taking profits... if you allow losers to pile up and if you cut profits short. Learning how to sit tight will make sure you let winners pile up instead.

Congratulations.

You found an asset that was extremely cheap... extremely hated...

4. “Never confuse brains with a bull market.”

– Humphrey Neill

8

S&A Trader’s Manual

Table of Contents

and just starting an uptrend.

You took an intelligent position size that limited risk.

You did a great job of sitting tight... of being patient and letting the bull market fully express itself.

You are up 500%. Now... for God’s sake... Don’t confuse brains with a bull market.

This classic quote is attributed to Humphrey Neill. Neill was a stock market expert who literally wrote the book on contrarian investment thinking. It’s called The Art of Contrary Thinking. Neill’s advice will save you a ton of money as a trader.

You see, the natural human tendency after hitting it big in the market is to “puff up” a bit... to brag to friends and family about how you “nailed it.”

Maybe you did some great analysis on the oil market and rode a big move for hundreds of thousands of dollars. Or maybe you found a promising microcap company that turned into a 1,000% winner.

The natural human tendency after doing something great is hubris. And in the stock market, hubris is more dangerous than igno-rance.

In 1999, I thought of myself as a great stock trader. I was 22 years old... and I was sitting on huge gains in tech stocks like JDS Uni-phase, Ariba, and Microsoft. I would buy ‘em, and they’d go up hundreds of percent. I made more money trading stocks that year than I did from my job.

I figured I would be retired and living on a private island by my late 20s. That’s how good I was!

Now mind you, this was during the greatest tech stock bull market in history. The benchmark Nasdaq stock index gained 86% that year. I wasn’t some incredible trader. I simply happened to be buying while the market was soaring. I had confused brains with a bull market.

You can guess what happened next. When the market collapsed, so

9

KNOWLEDDGE BASE

Table of Contents

did my huge tech stock bets. I didn’t use stop losses. I didn’t prac-tice smart position sizing. I lost everything I had gained and then some.

It was expensive market tuition... but it taught me a tremendously valuable lesson.

Rich traders reach a happy medium between confidence and overconfidence. The right balance means having conviction in your beliefs and the courage to act on them... but always treating the market as a dangerous place that can bankrupt you if you don’t use intelligent positions sizes and stop losses.

The wrong balance is being overconfident, taking a huge leveraged position, and refusing to say “uncle” if the market doesn’t move in your direction.

If you’ve made a bundle on a big market move, go ahead and cele-brate a little. Brag to your buddies. Go on a nice vacation.

But take Humphrey Neill’s advice... Remember the lesson of the Inter-net bubble. Don’t believe that just because you were right before, you don’t have to limit risk. Confusing brains with a bull market will result in bankruptcy.

This quote is the financial equivalent of nuclear energy: a source of tremendous power that can be used to drive progress... or to cause complete destruction.

It’s so dangerous, I debated not including this piece.

You see, this idea is one of the keys to making a fortune in the stock market... the idea of being a “pig.”

Stanley Druckenmiller is one of the most successful money man-

5. “When you have tremendous conviction on a trade, you have to go for the jugular. It takes courage to be a pig.”

– Stanley Druckenmiller

10

S&A Trader’s Manual

Table of Contents

agers of all time. He earned an estimated $150 million in 2008. He learned much of what he knows from legendary speculator George Soros. That’s where he learned to be a pig.

There’s an old Wall Street adage that says, “Bears make money, bulls make money, but pigs get slaughtered.” The idea is that you can make money when stocks go down (the bear side) or when they go up (the bull side)... but anyone who behaves like a pig – who gets too greedy – is destined to lose.

Soros and Druckenmiller don’t agree with this line of thinking. They know that to make tremendous returns, you have to back your best ideas with large positions. You have to get greedy when you find an amazing risk-reward situation. Hitting a big trade with a tiny position size just doesn’t generate big returns. You have to be a pig.

But here’s where this idea gets dangerous...

The No. 1 cause of catastrophic losses – the kind of financial blow that will bankrupt someone – is losing a big percentage of a big position.

So why would I encourage you to learn about this weapon of mass financial destruction?

Because used correctly, a large position size in a great idea can make you rich. Because being a pig can make your year, doubling or tripling your account. It can be the difference between making $20,000 or $200,000 on a big trend, like the monster 500% move many gold stocks enjoyed from 2003 to 2008.

Normally, a trader should avoid putting more than 5% of his money into one idea. If you use a stop loss of 20% on a 5% position, you will only lose 1% of your total portfolio if you are wrong.

But occasionally, when trade is close to “slam dunk” territory – when the reward-to-risk ratio is 6, 8, or 10 to 1 – a large position size of 10% or 20% of your portfolio allows you to make huge gains. The way to build superior long-term returns is through your “home run” trades... which must be backed by real money... not a 3% position.

Someone who isn’t comfortable taking losses and minding their sell

11

KNOWLEDDGE BASE

Table of Contents

discipline should never take large positions sizes. If you can’t cut losers short, you’re playing Russian roulette when you take big posi-tions. It’s only a matter of time before you’re toast. And if you’re not good at recognizing great high-reward/low-risk trades, then please keep your position sizes small.

Only after years of successful trading and mastering stop losses should you even consider a position size greater than 5%.

But if you have extensive experience under your belt, you need to brush off the old Wall Street wisdom and pay attention to filthy rich traders like George Soros and Stanley Druckenmiller. You must make big money on your best high-reward/low-risk trades. You must be a pig.

At some point in his career, every trader will confront the ghost of John Maynard Keynes. The decision he makes then will either ruin him or save him a fortune.

John Maynard Keynes was the most influential economist of the 20th century. His ideas shaped the way the Western world ran its finances after World War II. Keynes was also a brilliant speculator who pulled millions of dollars out of the market.

While I believe some of Keynes’ economic ideas were batty (a sub-ject for another time), his quote above is one of the most important things ever said about trading.

It’s how Keynes’ ghost will forever live in the minds of traders.

You see, Keynes brilliantly cautions traders against shorting a stock or a market that “shouldn’t” be rising... and cautions against buying a stock or a market that “shouldn’t” be falling.

Great traders are always on the lookout for extremes: extremes in

6. “The market can stay irrational longer than you can

stay solvent.” – John Maynard Keynes

12

S&A Trader’s Manual

Table of Contents

sentiment, extremes in valuation, and extremes in momentum. It’s by finding extremes and then betting against the crowd that you set yourself up for big gains in a short time.

But watch out for the problem Keynes warns about: The crowd often gets irrational and stays that way for a long time.

For example, a lot of money managers believed the enormous rise in oil prices starting in early 2007 was an irrational move. When crude oil had risen from $50 to $90 a barrel in early 2008, they knew speculators with lots of borrowed money were behind the move. And they knew oil was selling for at least 50% more than its re-al-world value. So they bet on falling prices.

When oil climbed to $100 a barrel, these money managers knew it was even more irrationally overvalued. Same with $115... and $125... and $135... and you get the idea.

Any trader who stubbornly held on to his short position because he just knew $90 was an “irrational” price suffered the longest summer of his life. He watched that irrational price tick higher and higher like Chinese water torture... and his losses were huge.

Any trader who was short at $90 and hung on was carried out a bro-ken man... He forgot the market can stay irrational longer than any one single person can heavily bet against it and stay solvent.

The market is full of stories like this... Think of the traders who went bankrupt shorting super expensive Nasdaq stocks in 1999... or the famous blow-up of Long Term Capital Management in 1998. Both groups took big positions against markets they felt were behaving irrationally... but those markets just kept on behaving irrationally for a long time.

A corollary to Keynes’ quote is the Jim Rogers line, “Markets often rise higher than you think is possible, and fall deeper than we can imagine.”

You can put the warning from Keynes and Rogers to real-world use by always minding your stop losses. Go ahead and take a contrari-an position at the extremes. But always have an “uncle” point to limit

13

KNOWLEDDGE BASE

Table of Contents

losses in case the crowd keeps pushing prices in a crazy direction.

It’s tough to watch a stock you know inside and out move in a direc-tion that isn’t rooted in reality. But remember... if a stock can trade for an irrational 50 times earnings, it can trade for an irrational 75 times earnings... or 100 times earnings... or as we saw in the Nas-daq bubble days, 200 times earnings.

It’s tough to say uncle on a trade you know has terrific potential. But when you start thinking, “This is an irrational move... I’ll just keep betting against it,” remember Keynes and Rogers. Know that mar-kets can go farther in either direction than you can imagine... and they can keep going longer than you can stay solvent.

Imagine someone rounded up the greatest golfers of all time, sat them down, and asked them how to become a great golfer.

Now imagine that all of them – Arnold Palmer, Ben Hogan, Jack Nicklaus, Tiger Woods, and so on – recommended using the same technique to achieve incredible success. Maybe they tell you to keep your head down or to keep your arm straight. If you wanted to become a great golfer, you’d probably make this technique your main focus.

This sort of thing has been done in the business of trading. You’ll find it in the greatest trading book of all time, Market Wizards. This book is a series of interviews with some of the richest, most suc-cessful traders to ever live. It’s also a series of stories about one trading technique, which Ed Seykota captured in the quote above.

The technique is cutting your losses. Of selling a position if it’s not moving in your favor. It’s the key to turning your trading into a

7. “The elements of good trading are: (1) cutting losses, (2) cutting losses, and (3) cutting losses. If you follow

these three rules, you may have a chance.” – Ed Seykota

14

S&A Trader’s Manual

Table of Contents

lifetime builder of wealth.

Seykota is a legendary “trend following” trader who made himself and his clients millions and millions of dollars. His quote is a lot like the real estate cliché, “location, location, location.” The idea of cut-ting losses is so much more important than everything else, it needs to be repeated three times.

Other legendary traders say the same thing... William O’Neil, the great stock trader and founder of the newspaper Investor’s Busi-ness Daily puts it like this: “Letting losses run is the most serious mistake made by most investors.” The great short-term trader Marty Schwartz puts it like this: “Learn to take losses. The most important thing in making money is not letting your losses get out of hand.”

Now... it’s easy to read all of this great “cut your losers short and let your winners ride” stuff. It’s easy to repeat it to yourself while you’re driving or lying in bed. But for many traders, the execution of this idea is difficult. Many traders just can’t say, “Well, I’m wrong on this one... Time to admit it, protect my capital, and move on.”

If you’re one of these traders, here’s a technique that could mean a lifetime of profitable trading...

Let’s say you’re trading a $50,000 account and having trouble cut-ting losses. When you look at your account statement at the end of the year, you see a series of large losses overwhelming your small winners.

Take a small portion of your total account – maybe $3,000 or $5,000 – and start trading a volatile sector of the market. Small-cap Chinese stocks, biotech stocks, or mining stocks work beautifully here.

Instead of placing your normal-sized position in these stocks, place just $300 or $500 into each trade. Use a stop loss of 10% or 25% on each trade. Make a lot of trades with this small “training account.” When one of these trades goes against you, cut your loss and move on. You’ll lose maybe $50 or $125 per trade.

Make as many of these micro trades as it takes in order to turn loss-cutting into an automatic reaction... just like throwing your arms

15

KNOWLEDDGE BASE

Table of Contents

out for balance when you slip on ice.

Practice loss cutting just like you would practice the piano and you’ll get great at it. You’ll know what the Market Wizards know... and you’ll start acting like them. Wealth will follow.

Back in his day, Nathan Rothschild was like Warren Buffett and Alan Greenspan rolled into one.

Nathan was one of the founding members of the greatest banking dynasty in history. He and his family bankrolled wars, giant gold purchases, governments, and anything else that could pay them interest. Even kings couldn’t match Nathan’s power and influence. He’s considered the man who financed Napoleon’s final defeat at Waterloo in 1815.

Today, many estimate the Rothschild fortune totals billions or even trillions of dollars. (The family has always managed their accounts the right way: so nobody knows how large they are.)

Despite the enormous wealth he accumulated, Nathan is best known by the classic contrarian investment quote above, which is No. 8 in our series of all-time great trading quotes.

“Blood in the streets” has become a cliché, but for good reason: To make extraordinary gains, you must buy an asset near the point of maximum pessimism.

In Nathan’s day, in 19th century Europe, folks had plenty of chances to buy when blood literally soaked city streets and battlefields. The developing nations fought hideous wars at least once a generation. In today’s age of relative peace, however, it’s tougher to follow Na-than’s lead.

8. “Buy when there is blood in the streets.”

– Nathan Rothschild

16

S&A Trader’s Manual

Table of Contents

I can’t tell you to hop on a plane and scout rental properties or stock investments in a war zone. So here’s the main thing to take away from “blood in the streets”... Great investors and traders are like birddogs for news of disaster and despondency. They don’t wince at headlines like “Gambling industry bankrupt,” or “Indian stock market crashes for seventh day in a row.” They get excited.

They know desperate situations create incredible values and incred-ible extremes in sentiment. They are always on the hunt for places where “things can’t get any worse”... When things “can’t get any worse,” they can only get better.

It’s only when things can’t get any worse that you can buy world-class businesses for just four or five times annual profits... or safe bonds yielding 18%... or trophy properties for 80% below their highs. And despite what your emotions tell you, dark and gloomy situations have a way of working themselves out.

Note that in March 2009, most folks believed the Great Depression II was in the cards. There was plenty of blood on the balance sheets of bankrupt businesses and homeowners. The average stock climbed 60% in six months after the pessimism blew over. Many stocks climbed 200% and 300%.

So turn your completely normal, knee-jerk reaction to good news on its head. Don’t rush out to buy a stock, a piece of land, or a com-modity based on some bullish headline like “Analysts all agree... crude oil is going higher.” Instead, hunt for headlines like, “Uranium prices sink to historic low... industry desperate for money,” or “Argen-tina suffers currency crisis.” Both of these headlines preceded huge gains in the past decade.

Like many great trading ideas, Nathan’s quote has been “repeated” by other skilled investors: Warren Buffett tells us, “Be greedy when others are fearful and fearful when others are greedy.” Steve Sjugger-ud says, “You make triple-digit gains not when things go from bad to good, but when things go from bad to less bad.” Peter Steidlmayer reminded us that these trades can be hard to make because of fear... but, “The hard trade is the right trade.”

However it’s phrased, the idea behind “blood in the streets” is the

17

KNOWLEDDGE BASE

Table of Contents

9. “The most important rule of trading is to play great

defense, not great offense. Every day I assume every position I have is wrong.”

– Paul Tudor Jones

same: Be on the lookout for desperate, blown-out sectors, com-modities, and countries. This is where you’ll find extraordinary deals. It’s been the surest way to triple-digit profits for hundreds of years.

It will be the surest way for hundreds more.

Tucked near the middle of the greatest book on trading ever pro-duced are 23 pages of pure paranoia.

These 23 pages center on a guy who sees trouble around every corner... a guy obsessed with risk... a guy probably worth over $3 billion... a guy who correctly called the 1987 stock market crash, made over $80 million in the process, and will go down as one of the greatest trading minds of all time.

Pages 117 through 139 of Market Wizards contain an interview with legendary trader Paul Tudor Jones.

For many years, Jones was the picture of the Wall Street big shot. He owned an enormous Chesapeake Bay mansion. He took skiing trips to Switzerland. He married a fashion model. To this day, Jones controls one of the largest hedge funds in the world.

He became so successful because of the idea behind the quote above – the idea that playing great defense is the key to succeeding in the markets. He became so successful by focusing on not losing money... His billions came as a result.

Reading Jones’ interview will take you less than 10 minutes... and it might be the greatest “time put in versus value received” proposition an investor or trader will ever get. You’ll find that for a guy associ-ated with “winning” so much money, Jones constantly talks about losing... he constantly talks about playing great defense.

18

S&A Trader’s Manual

Table of Contents

There’s a comment on defense on nearly every page. In addition to his quote above, he says:

• Don’t focus on making money. Focus on protecting what you have. • I know that to be successful [in trading], I have to be frightened. • I am always thinking about losing money as opposed to making money. • Risk control is the most important thing in trading. • Never play macho man with the market.

Like all great traders, Jones sees his No. 1 job as cutting risk to the bone. You can cut your own risk by always using protective stop losses and intelligent position sizing.

Bottom line: Keep your losses small and your winners large. And never put more than 1% or 2% of your account at risk on a given trade. An amateur trader will often risk 5% to 10% of his account on a trade, which eventually leads to disaster.

Most people lose in the stock market. It’s an incredibly hostile place, where you’re going toe-to-toe with the world’s smartest people.

So I encourage you to buy Market Wizards and read Jones’ interview many times. Repeating his “defense” lines over and over is about the best “daily affirmation” a trader or investor will find.

Playing great defense. Winning by not losing. It’s the system Paul Tudor Jones used to become a billionaire... and it’s the second most important factor in your trading success.

I saved this quote for the final essay in our series of all-time great trading quotes.

10. “The realization that you are responsible for your re-

sults is the key to successful investing. Winners know they are responsible for their results; losers think they

are not.” – Dr. Van K. Tharp

19

KNOWLEDDGE BASE

Table of Contents

It’s the “broccoli” of trading. It’s the one few people want to read.

And that’s a shame, because the idea contained in this quote is far and away the No. 1 factor in your success as a trader or investor.

Most folks who make it through the next 400 words will decide this essay simply doesn’t apply to them. Those people will always lose in the market. They will always lose in life.

And worst of all, they’ll believe those losses are not their fault.

Dr. Van K. Tharp is an investor, trader, and famed trading psycholo-gist. For decades, Tharp has worked with traders to develop winning trading systems and mindsets. His work landed him in the trading classic, Market Wizards. Of all the fancy trading systems and stock strategies Tharp could present as the “Holy Grail” for traders, this is what he chose.

Personal responsibility is the Holy Grail.

For most people, the natural tendency is to find someone – any-one – to blame for their failures. It’s too painful for most people to just come out and admit they screwed up. Since money is such an emotionally charged topic, the “blame game” is especially common in trading.

Folks blame their broker for bad advice. They blame an advisory writer for a stock tip that doesn’t pan out. They blame Wall Street for its rigged game. They blame the government, Jim Cramer, God, conspiracy theories, and anything else you can think of.

They point their finger at everyone except the person in the mirror.

The “finger pointing” mindset is the loser’s mindset, whether you’re talking about sports, work, relationships, or trading. Unfortunately, most people have it. Most people simply will not accept full respon-sibility for their actions... and it suffocates their progress.

When you always accept responsibility for your actions, you set yourself up for a lifetime of progress and betterment. When you acknowledge your errors and discover why you made them, you can take steps to correct them. Blaming someone else for your trading

20

S&A Trader’s Manual

Table of Contents

failures is like ignoring an awful sound from your car’s engine. If you ignore the sound, you’ll eventually find yourself in the middle of nowhere with a car that won’t move.

How does this apply to trading? Let’s say you’ve been taking big losses on your stocks. When you accept that you should have mind-ed your stop losses – but didn’t – then you can make it a point to fix the problem. Or let’s say the stock-picking method you’re using isn’t working. When you accept that it’s your responsibility to decide what’s best for your money – and not the responsibility of a guy on television or a stock broker – you can start looking around for a method that works.

You – and you alone – are responsible for the gains and losses in your trading account. You must take all of the wisdom and strategies accumulated by legends like Paul Tudor Jones and Stanley Druck-enmiller and put them to use.

Van Tharp has spent most of his adult life – decades – working with winning traders and losing traders. This is what he found separates the two. Many of life’s dilemmas are not “black or white” choices. Many of them are different shades of grey. This one is not. You either accept responsibility for your results and learn how to win... or you do not accept responsibility for your results and always lose.

If you’re looking for the Holy Grail of trading, it’s not in a book, stock picking system, Fibonacci series, or a currency advisor. It’s embed-ded in Tharp’s quote. It looks you in the eye every time you look at a mirror.

Trade accordingly.

P.S. I consider Van’s book Trade Your Way to Financial Freedom the second-best book on trading ever written (second to the trading Bi-ble Market Wizards). You can buy it used on Amazon for about $20. Used properly, the return on investment will be in the thousands and millions of percent.

21

KNOWLEDDGE BASE

Table of Contents

Postscript... “Number 11”

While putting this collection together, one incredible quote kept turn-ing up over and over.

I kept meaning to write up a commentary on the quote, only to realize that if I did, it would make the rest of my list a little redundant. It also has so much meaning packed into it, that it would take 20 pages of analysis to do it justice.

If you took all of the previous quotes and threw them into a stew, this is what the lot would taste like.

The quote is from a man most traders consider to be the greatest speculator in history. Here it is:

“It’s not whether you’re right or wrong that’s important, but how much money you make when you’re right and how much you lose when you’re wrong.” – George Soros

George Soros is the man who famously made $1 billion on a single trade by betting against the British Pound in 1992. He took on one of the most powerful governments in the world as the Bank of England fought to support the value of its currency. They say you should nev-er bet against the government. Well, George did, and he won.

And while many folks dislike George’s brand of politics (viewed as anti-American), there’s no disputing the man is likely the greatest trader to have ever lived. Together with Market Wizard Jim Rogers, Soros founded the Quantum Fund in 1970. They managed the Quantum Fund to a 3,365% return over the next 11 years.

Think about Soros’ quote for a moment...

Let’s take in a few pieces:

“how much money you make when you’re right”

This is the idea behind “being a pig” and committing a good deal of money to your best ideas (No. 7)... the ideas you should only move on when it’s close to “picking money up in the corner” (No. 1)... ideas that are revealed in periods of extreme sentiment and “blood

22

S&A Trader’s Manual

Table of Contents

in the streets” (No. 2). And you can only make big money when you “sit tight” and take advantage of big trends (No. 6) and being hum-ble enough to take your gains by not “confusing brains with a bull market” (No. 4)

Now... let’s go to:

“how much you lose when you’re wrong”

This is the idea behind playing great defense (No. 3) by “cutting loses, cutting loses, cutting loses.” (No. 8)... and not taking losses by fighting an irrational market (No. 9)... and the idea of not trying to be “right too soon,” (No. 5).

George’s quote doesn’t capture No. 10, which is taking personal responsibility for your results. That has more to do with you as a person than trading tactics.

But if you’re looking for that one magic quote to tape near your com-puter, take the advice from the guy many consider to be “the king,” George Soros:

Make a lot of money when you’re right, and lose a little money when you’re wrong.

This is the only way to be a winner in the market.

23

KNOWLEDDGE BASE

Table of Contents

THE SEVEN REAL SECRETS OFTHE WORLD’S BEST INVESTORS

By Porter Stansberryfounder, Stansberry & Associates

My friend Steve Sjuggerud and I were sitting in the main boardroom at the New York Stock Exchange. We’d been invited there by Eduar-do Elsztain, a wildly successful Argentine investor, to ring the open-ing bell of the exchange.

For those of you who don’t know his reputation, Elsztain got his start making a pile of money for George Soros in Argentine stocks in the early 1990s. Then, he began compounding his wealth by buying up distressed real estate in Argentina, becoming the country’s largest landowner.

We were in New York to celebrate his first U.S. real estate deal, a deal that netted the Elsztain group of investors 20% of one of the country’s largest hotel groups for roughly $0.10 on the dollar.

While Elsztain is focused on doing real estate deals, he is still an ac-tive investor in gold and stocks, too. And he has been a subscriber to our letters for many years...

When Elsztain first read Steve Sjuggerud’s True Wealth, he honestly thought someone was leaking his private memos to Sjuggerud.

“Steve, your ideas... your thinking... When I first saw your letter, I honestly thought I had written it myself. I couldn’t believe some-one else was having all of my same thoughts.” When he read True Wealth, he recognized immediately that we shared the same strate-gies and core ideas about investing.

Keep in mind, when I started working with Steve Sjuggerud as a financial analyst in 1996, I hardly knew the difference between a stock and a bond. But after a few years of working 14-hour days, six days a week... and after reading hundreds of books about finance and financial history... I still knew almost nothing. Just enough to be dangerous, really.

24

S&A Trader’s Manual

Table of Contents

I kept at it, though. And through the terrible emerging-market col-lapse of 1998-99 and the tech bear of 2001-02, I finally began to acquire the knowledge and the confidence in my own thinking I needed to make the kind of investment calls I’ve made since then... like buying right at the bottom in October 2002... like calling the top in February 2007... like predicting GM’s bankruptcy... and urging my subscribers to buy stocks in November 2008.

So... how did our thinking and Elsztain’s end up so closely aligned?

Successful investing involves only a few real secrets. Almost all of the world’s best investors use the same basic principles. Nobody teaches these principles. But everyone who stays in the markets long enough and succeeds eventually discovers them on their own.

Our meeting with Elsztain was a vivid reminder of this fact. It’s something I’d taken for granted over the years because I’d seen it so many times. You can put a group of the best investors together anywhere in the world, and nine times out of 10 they will be able to finish each other’s sentences. They’re all looking at the same things. They are all waiting on the same things. And they all see the same opportunities.

Unless I’d lived through dozens of experiences like this, I wouldn’t have believed it. But I know from firsthand experience that it is abso-lutely true: All of the world’s best investors use the same handful of techniques and strategies. And as a result, they frequently end up in the same positions.

In this essay, I’m going to do something I’ve never seen done be-fore. I’m going to teach you these core strategies. The real secrets. And I’m going to show you how to use them – just like I do with my own money.

While this information probably won’t make you a great investor overnight, it will surely improve your results dramatically over time. And if you practice the execution of these strategies, I promise you can make a living as an investor – easily.

All you really need to know is right here.

25

KNOWLEDDGE BASE

Table of Contents

Secret No. 1: You Can Time the Market... You Must Time the Market

Please take a moment to look carefully at this chart.

These are the daily closing prices of the Templeton Russian & East Europe mutual fund (TRF) over a 15-year period. This is one of the oldest and most established emerging-market mutual funds. This is the kind of fund people invest in heavily through 401(k) allocations. It is a closed-end fund. It trades like a corporation – like a regular, publicly listed stock. Sometimes it trades at a premium to its net assets and sometimes at a discount. That attracts traders and spec-ulators.

In this one investment vehicle, we have both sides of the invest-ment world. Typical individual investors (lemmings, if you will) are dripping capital into this fund, month after month, regardless of the premium or discount and oblivious of critical factors in the market-place. Meanwhile, the world’s best investors follow this fund close-ly... waiting. They are like sharks. They know this is one of the most reliably volatile funds in the world... and one of the easiest to trade successfully.

So in this one fund you have a good litmus test to compare the two major philosophies of investing. Should you buy and hold? Should you pour capital into your 401(k) blindly each month? Or should you

26

S&A Trader’s Manual

Table of Contents

time the markets? Should you know the factors that lead funds like TRF to soar to absurd levels and then crash?

Looking at this chart, you easily can see the fund peaked twice in 2006 – once in the spring and again at the end of 2006/beginning of 2007. Both of these times, TRF was trading at such an extremely high premium that we noticed it immediately.

Here’s exactly what we said at the time:

The Templeton Russia Fund (TRF) is about to get crushed again. Stuffed with Russian oil and bank stocks, this ETF is one of the few direct Russia plays in the market... This spring, the premium on TRF hit a whopping 35%. You had to pay $1.35 for every $1 of real value. This huge overvaluation was corrected when emerging mar-kets got obliterated in May. The Russia Fund fared the worst, falling 47% from its peak.

With emerging market speculation heating up again, TRF is trading for a 24% premium right now. If that premium climbs any higher, we predict another obliteration. – Brian Hunt, DailyWealth, December 21, 2006

When we published that note in December 2006, the Templeton Russia & East Europe Fund traded just shy of $95 per share. After falling in nearly a straight line for two years, it was trading for less than $7 per share in March 2009. That’s a decline of more than 90%.

Perhaps more importantly to any long-term, buy-and-hold investor, the decline we foresaw in the fund would have wiped out more than 100% of the accumulated capital gains, assuming you invested as long as 15 years earlier.

Now... I’d like you to look at the chart one more time. Look at what happened to the fund in the first half of 2009. It went nearly straight up.

On April 17, 2009, we told subscribers to buy Russian stocks. In-stead of using TRF, Steve Sjuggerud recommended a nearly identi-cal Scudder Fund, the Central Europe and Russia Fund (CEE). Both went up 150% from their March lows.

27

KNOWLEDDGE BASE

Table of Contents

So if you followed the buy-and-hold strategy in Russian stocks over the last 15 years, you would have made a very small amount of money – or lost money, depending on when you sold your shares. On the other hand, if you applied a few of our secrets, you could have easily traded this fund for more than 100% gains in only a few weeks. And if you watch this fund, you’ll be able to make trades like this three or four times each decade. If you watch other similar funds, you’ll be able to make trades like this once or twice a year.

All you’re looking for are extremes in the premium or the discount to net asset value in closed-end country funds. Barron’s publishes a complete list of these premiums/discounts in every issue.

And let me tell you one more thing about this situation. In January 2007, when TRF was widely overvalued and when most individu-al investors were clamoring to buy shares – despite the premium valuation – we checked to see if we could sell the fund short. We knew it was going to collapse and wanted to profit directly as it fell. But we couldn’t. Why not? Because other professionals had already borrowed all of the available shares to short.

In other words, while 401(k) investors were buying and holding a time bomb, Wall Street’s pros were lined up, waiting to take their money.

That’s why we call “buy and hold” “buy and fold.” That’s what hap-pens. People think they’re investors when they buy. But sooner or later, the pain gets so bad and the loss is so big they panic and sell. Wall Street wins.

Why does anyone believe “buy and hold” works?

The mutual-fund industry, which has boomed since the 1980s, used a bunch of faulty academic research to “prove” you couldn’t time the markets. According to these folks, we shouldn’t have been able to do the kind of trading we did with the Templeton Russia & East Europe Fund. They would tell you we didn’t have any real edge against the other investors in the fund. They would tell you we just got “lucky” – despite the fact that we do these kinds of trades year after year.

28

S&A Trader’s Manual

Table of Contents

Why would they promote the idea that you can’t time the markets? Because they get paid based on assets under management. They need you to leave your money with them, good times or bad. No matter what, a mutual-fund manager isn’t going to return your mon-ey and tell you, “Sorry, it’s just not a good time to buy stocks... “So they have to invent a world where it is always a good time to buy stocks.

You undoubtedly know their mantra: buy and hold. But it’s all a lie. It doesn’t work. And even if it did work, few people would be able to apply the strategy because most individual investors do not have the risk tolerance required to actually buy and hold.

Would you have been able to continue buying the Templeton Russia Fund through the collapse of 2008? Not many people could. In-stead, they chase hot sectors and investment fads and buy in at the worst possible time. Then after prices collapse, sooner or later, the pain and fear become unbearable, and they liquidate their invest-ments – usually at the exact bottom.

Believe me, the pros know that’s what individual investors are going to do. That’s how they make their living.

Meanwhile, the big mutual-fund companies spend millions on “buy and hold” advertising each year. They give more millions to academ-ic researchers – all of whom “prove” you can’t time the market. It’s a big lie.

When researchers study actual mutual-fund returns, the results are nothing like the averages you find in the prospectus. The truth is, most people who invest in mutual funds never make more than 5% a year on average because they buy the wrong funds at the wrong times and sell at exactly the wrong times. And anyone who was buying stock mutual funds over the last 15 years most likely lost money overall.

Buy and hold doesn’t work for two reasons: It ignores valuation and sentiment (I’ll explain these two factors next), and it ignores human nature. (Even if buy and hold did work, it would be a less-than-op-timal strategy because, as should be readily apparent to everyone who watches the stock market, the market isn’t as “efficient” as so many academics claim.)

29

KNOWLEDDGE BASE

Table of Contents

The intellectual rationale for buy and hold is the idea that securities prices instantly reflect all the information available. You can’t get an advantage on the market. The best investors can hope to do, there-fore, is to get the market’s average return. And the only sure way to do this is to buy an index fund, year after year, and hold it forever.

This idea – that information is reflected accurately and instantly in the market – is preposterous. In the first place, lots of people trad-ing stocks don’t know what they’re doing. They can’t accurately handicap stock prices because they don’t know the first thing about valuation.

But even more than this, most of what’s important to stock pric-es is unknowable. Nobody knows what the future holds for things like interest rates and economic growth. People’s emotions about these unknowable variables – what we call “sentiment” – make a far bigger impact on stock prices than the latest earnings report. And people’s emotions are anything but rational or efficient.

You can dramatically increase your returns in common stocks if you’re simply more disciplined about when you make major invest-ments. You only want to commit a substantial amount of capital when both valuation and sentiment are in extremely bullish ranges. In short, you want to buy when stocks are cheap and most people are afraid to buy them. Unfortunately, these opportunities don’t arise often in U.S. blue-chip stocks. But you can almost always find these conditions somewhere or in some part of the U.S. market.

Now... let me show you how the pros evaluate valuation and sentiment.

Secrets Nos. 2 and 3: The Investor’s ToolkitValuation Ratios and Sentiment Indicators

The world’s best investors don’t see the market the way you do.

And I mean that literally... They look at the market through different lenses.

Most investors know how to value equities using various valuation ratios – like the price-to-earnings ratio, the price-to-book ratio, or

30

S&A Trader’s Manual

Table of Contents

dividend yields. These valuation studies are important when you’re buying individual stocks. And they can give you some idea of wheth-er or not the market as a whole is attractive. But... there are much better ways to see valuation in the markets.

For example, here’s a 30-year chart of the S&P 500. This is the way you probably look at the market. And when you look at the market this way, it looks pretty expensive. Stocks have been mostly going up for a long time. The big selloffs in the past decade didn’t bring the S&P 500 index back down all that much... or so it seems when you look at a plain chart.

But there’s a much better and more accurate way to view the markets.

The next chart is the S&P 500 again, from the same time period. As you can see, this chart looks nothing like the first one. In this chart you can see the huge mania of the 1990s – where the chart goes nearly straight up. And you can plainly see the big top formed in stocks in the early 2000s. But in this chart, the second top in stocks we saw in 2007 doesn’t exist. It’s like the bull market of 2002-07 never happened.

This chart is the S&P 500, but measured in gold, rather than U.S. dollars. What this chart shows is the value of stocks as compared to gold. Gold is a much better standard of value than the U.S. dollar

31

KNOWLEDDGE BASE

Table of Contents

because it can’t be printed or manipulated as easily as the U.S. dollar.

What this second chart shows is how cheap stocks have really become – something you can’t see on the regular S&P 500 chart because of the effects of inflation.

At the bottom of stock prices in the late 1970s, just one ounce of gold (then at $800) would have bought an entire unit of the Dow Jones Industrial Average. Stocks and gold were trading on a one-to-one basis, based on this measure. At the peak of stock prices in 2000, a unit of the Dow was worth $14,000. And an ounce of gold was only worth $260. To buy the Dow would have cost more than 50 ounces of gold. Obviously, stocks were extremely expensive – 50 times more expensive than they were at the bottom in 1980.

In January 2011, gold was trading around $1,700 an ounce. And the Dow was near 12,000. It took roughly seven ounces of gold to buy the Dow.

Looking at stocks through the lens of gold gives you a much better idea of where we are in terms of sentiment and valuation. Using this gold ratio will help you make much better asset allocation decisions. You want to buy stocks when the ratio of the Dow to the price of gold is low – less than 10. And you want to buy gold when the ratio is high.

32

S&A Trader’s Manual

Table of Contents

Using a chart just like this, my partner Bill Bonner began to tell peo-ple to buy gold and sell stocks in 2000. Using the same chart, I told Doug Casey’s Gold Summit audience in March 2009 to buy stocks instead of gold.

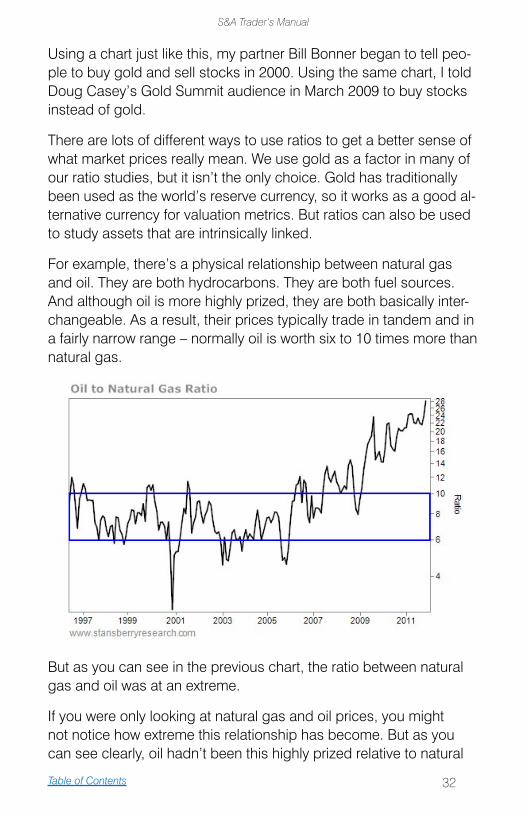

There are lots of different ways to use ratios to get a better sense of what market prices really mean. We use gold as a factor in many of our ratio studies, but it isn’t the only choice. Gold has traditionally been used as the world’s reserve currency, so it works as a good al-ternative currency for valuation metrics. But ratios can also be used to study assets that are intrinsically linked.

For example, there’s a physical relationship between natural gas and oil. They are both hydrocarbons. They are both fuel sources. And although oil is more highly prized, they are both basically inter-changeable. As a result, their prices typically trade in tandem and in a fairly narrow range – normally oil is worth six to 10 times more than natural gas.

But as you can see in the previous chart, the ratio between natural gas and oil was at an extreme.

If you were only looking at natural gas and oil prices, you might not notice how extreme this relationship has become. But as you can see clearly, oil hadn’t been this highly prized relative to natural

33

KNOWLEDDGE BASE

Table of Contents

gas since before 1996. That’s because natural gas production has soared thanks to major new shale discoveries, causing inventories to swell to record levels.

At the time, nobody wanted natural gas. The record-low valuation of natural gas as compared to oil showed that market participants had come to believe natural gas will never be valued at par with oil again. That’s impossible, of course, because as the price of a com-modity falls – especially one as useful as natural gas – consumption rises. Sooner or later, scarcity returns and the price will go back up. But the point is, you want to buy commodities (or other markets) when the valuation ratios tell you people have totally lost faith that prices will ever return to normal.

Look at the chart again. Back in 2001, the price of oil relative to natural gas neared an all-time low. Oil was trading for only about two times more than natural gas. That’s because Enron had rigged the domestic market for natural gas and the global recession had knocked down oil prices.

Nobody knew Enron was rigging the market. But you didn’t need to know: All you had to know was that the relationship between the two fuels was bound to correct back into the six-to-10 range, and the most likely way for that to happen was for the price of oil to go up. This was a great buy indicator for oil. And as you know, oil prices went nearly straight up from 2001 until the summer of 2008.

Now, this chart is telling us the ratio between natural gas and oil was completely out of whack again in 2011. And using a gold ratio chart, we can also see natural gas was about as cheap as it’s been in 15 years.

[Chart on following page]

Natural gas is worth watching closely. And I know every great inves-tor in the world is doing the same thing. I know because I’ve spoken to a handful of them about natural gas. I know because legendary investors have been buying lots of natural gas-related stocks. Final-ly, I’ve been in the markets long enough to know, when you see an anomaly like this, it’s going to attract a lot of capital... At some point, lots of people are going to make a killing in natural gas.

34

S&A Trader’s Manual

Table of Contents

Valuation studies, like the ratios I’ve shown you, can tell you a lot about when prices are attractive. Sentiment tells you when we’re at the bottom of prices. Sentiment, however, covers a wide range of factors. There’s no single best way to judge sentiment; it requires experience... and intuition.

I’ve learned to wait on a lot of factors. My favorite is magazine covers. When you see a market that’s gotten out of whack, like natural gas, you want to see the mainstream press report the false conclusion. I’ll never forget The Economist cover from November of 1998 when oil traded for $7 per barrel. Just two or three years before “Peak Oil” would become the intellectual fad, The Economist asked on its cover if we were “drowning in oil.”

Another great sentiment indicator is suicides. In December 2008, I recommended GDX, a fund of gold stocks. I did so because several of the best-known gold-stock speculators had blown their accounts up spectacularly in the horrible gold bear market of 2008 and then blown their heads off in late October – which, of course, marked the exact bottom of the market for gold-mining stocks. When you hear about speculators committing suicide, you want to be a buyer.

Finally, I recommend you check out www.sentimentrader.com. It is the best sentiment research out there, and the website is run by a friend of ours, Jason Goepfert.

35

KNOWLEDDGE BASE

Table of Contents

There are very few firm rules about using sentiment. Like I told you, it’s mostly a matter of judgment and experience. You have to learn how a market feels when it’s near a bottom or a top. But I know two things for sure about sentiment...

First, you never, ever put on a big trade if the crowd is already in the position. You can’t hope to succeed as an investor if you’re chasing the market. So if the position you want to take is popular or crowd-ed, wait for a better idea to come along.

And second, you can ignore sentiment as an indicator 90% of the time. It’s only really important at the extremes. When markets be-come intensely loved or intensely hated, that’s the time to pay atten-tion to sentiment and trade opposite the crowd.

Secrets Nos. 4 and 5:Trailing Stops and Position Sizing

We have two kinds of customers at my firm, Stansberry & Associ-ates Investment Research: folks who will cut their losses and folks who will not.

And unfortunately, the “will not cut losses” customer is the most common.

Here’s what happens. The prospective subscriber sees one of our advertisements, which are designed to catch your eye with whatever stock or sector we think is going to be hot. This stock or sector is, unfortunately, usually too popular by this point to be a great invest-ment. We’re typically trying to grab the tail end of a trend – which can be very lucrative. But the key to these kinds of trades is one of the few, real secrets to investing: trailing stop losses.

Our new client, however, grew up on a steady diet of “buy and hold.” He believes staying with a stock is a matter of pride and masculinity. He is no quitter. So when we stop out of the story that he originally subscribed to learn about, he doesn’t sell. In fact, he starts writing us e-mails every third day asking why we’re no longer covering his baby. And of course, he buys and buys and buys all the way down.

36

S&A Trader’s Manual

Table of Contents

Now it’s six months later. We’ve been out of the stock – with a decent profit – for so long we’ve forgotten why we liked it in the first place. We’re walking through the exhibits at a conference when Mr. Buy and Hold stops us and demands to know why we’ve cost him $50,000 with our terrible recommendation.

“Do you mean the stock we sold months ago?” we ask.

“Yes, that’s the one... and don’t give me any excuses about stop-ping out. Everyone knows you have to buy and hold if you want to make money in stocks,” the former client says.

For the next several years, we’ll see this poor fellow every now and then. He’ll swear to everyone he meets it is Porter Stansberry’s fault he lost a bundle on that stock, which has now tumbled more than 90%. But the man will say, “I’m still buying because I know it’s coming back.”

The second kind of customer is the one we prefer. He actually takes our advice, which is to determine ahead of time the price you’ll sell any given stock. Some stocks demand more leeway. Some situ-ations require a lot less. But the point is, you don’t let the market convince you to stay with any given investment. The market can be irrational for a lot longer than you can be solvent.

If you are a good investor, you already know: Losses are part of the game. If the losses are small, they don’t matter. If you’re not a good investor, you see every loss as a failure. But small losses aren’t fail-ures. They are victories – victories against big losses. And big loss-es have to be avoided, at all costs. Nobody can survive a big loss.

If I could teach every investor only one secret it would be to cut your losses and let your winners run. If you refuse to do these two things, you will never be successful as an investor. Remember: It is difficult to get everything right in any given trade – valuation, sentiment, timing, position size... When you’ve made a mistake, admit it quickly and move on. When you get everything right, treasure it. Hold on as long as possible.

When we hire new analysts at Stansberry & Associates, the smart-est guys have the hardest time buying into these ideas. Smart guys think they’re smarter than the market. And usually they are. The

37

KNOWLEDDGE BASE

Table of Contents

problem is, you only have to be wrong once to suffer a catastrophic loss. And everyone – and I mean everyone – is wrong at least once every few years. So you have to completely rule out the possibility by being a disciplined investor and cutting your losses. There is no other way.

There’s one more thing you have to know about cutting your losses and that’s Secret No. 5 – position sizing. The secret is simple: You adjust your position size based on the maximum risk you’re taking. You should never put more than 3% of your portfolio at risk and, ideally, you should never lose more than 1% of your portfolio on any trade. So if you’re going to put 5% of your portfolio into a risky stock, you should use a 20% stop loss. If you’re wrong, no problem – you’ve only risked 1% of your portfolio.

If you want to hold a position longer and expect a lot of volatility, you should simply use a smaller position size – all the way down to a 1% position size for stocks that are basically lottery tickets. On the other hand, from time to time, I recommend position sizes up to 25% of your portfolio.

Every few years, an exceptional opportunity will appear in very low-risk stocks. Never put on a trade of this size unless you are certain the position is incredibly safe. If you’re not an expert at evaluating a company’s balance sheet and its earnings prospects, you shouldn’t put on positions of this size – ever. Also, when you put on a jumbo position, you must use a trailing stop loss, which moves your stop point higher as the stock goes up.

Every successful investor uses some combination of stop losses or position-size limits. And yet most individual investors know nothing about these key strategies.

Secret No. 6: Positive Carry

Most individual investors use margin the wrong way – or not at all.

The most common way individual investors use margin is through buying put or call options. They want a big leveraged position, and

38

S&A Trader’s Manual

Table of Contents

they buy their leverage in the options market. They would get better odds in Vegas. Buying leverage in the options market is extremely expensive and unlikely to lead to success over the long term. Most of the great investors I know never buy options. They only sell them.

Why? Positive carry.

“Carry” refers to the cost of borrowing money. When interest rates are low, most institutional traders can get margin loans for between 3% and 4% annually. So to make money with this margin, they don’t have to earn very much. Using conservative strategies – like selling puts on stocks they want to buy anyway, they can easily earn 15%-30% per year.

These kinds of highly leveraged positions (you only have to put up 20% to sell a put) involve some risk. But if you’re good at it, you can make incredible profits. You’re borrowing money at 4% and earning 20% with it. This is “positive carry.”

There are lots of ways to earn positive carry. You can sell option premiums. You can invest in higher-yielding debt obligations, like junk bonds. You can lend money to payday loan venders... The point is most of the great investors I know are always involved in carry trades of some kind. They keep 25%-50% of their capital tied up in these kinds of trades, which will earn them around 20% a year. They only take their money out of these kinds of trades when there’s a really unique and profitable opportunity.

The best way for individual investors to mimic these kinds of carry trades is to use margin accounts to buy high-yield bonds. Even if you’re paying 6% a year for your margin, you should often be able to produce a 10% positive carry.

Don’t use margin to buy speculative positions. Don’t use margin because you’re not disciplined enough to keep a cash reserve. Only use margin when you can calculate that it will enable you to pro-duce a substantial amount of positive carry.

Finally... even if you decide not to engage in carry trades, you should at least pretend that your default cash setting will net you 10% per year. And yes, it’s possible to make 10% a year in liquid positions.

39

KNOWLEDDGE BASE

Table of Contents

I want you to pretend your default setting earns 10% a year because when your downside is positive 10% a year, you be-come far more skeptical about new ideas. And that’s the key. You only want to take on new positions you think are safe, when the valuation and the sentiment is in your favor, and when the upside is so significant it’s worth risking the 10% a year you would make otherwise.

Secret No. 7: Compound Interest

Richard Russell is the dean of the financial newsletter industry. He has been writing Dow Theory Letters since the 1950s. If you’ve never read his famous essay “Rich Man, Poor Man” before, stop right now, go to his website (ww2.dowtheoryletters.com), and click on the link to it. It’s right there on the front page of his web-site.

To explain the power of compound interest, Russell notes that if a 19-year-old put $2,000 each year into his IRA for seven years in a row and then never contributed another penny to his retirement, he’d have $1 million by the age of 65, assuming he earned 10% a year on his account on average. If another investor started saving for retirement at 26 – the same age the first investor stopped con-tributing – and he put $2,000 into his IRA every single year until he was 65, he still wouldn’t catch up to the first guy.

Now lots of folks who see this information think, “Oh, it’s too late for me. I don’t have enough time to compound my wealth.” No, that’s not true. What this presentation really means is that you have to start now. You have to learn to be a saver. You have to make sure your money is earning interest all the time. Most of all, you must realize if you’re borrowing money (without a positive carry), you will never, ever be rich.

Says Russell:

And because the little guy is trying to force the market to do some-thing for him, he’s a guaranteed loser. The little guy doesn’t under-stand values so he constantly overpays. He doesn’t comprehend

40

S&A Trader’s Manual

Table of Contents

the power of compounding, and he doesn’t understand money. He’s never heard the adage, ‘He who understands interest – earns it. He who doesn’t understand interest – pays it.’ The little guy is the typical American, and he’s deeply in debt.

The little guy is in hock up to his ears. As a result, he’s always sweating – sweating to make payments on his house, his refrigera-tor, his car, or his lawn mower. He’s impatient, and he feels perpet-ually put upon. He tells himself that he has to make money – fast. And he dreams of those ‘big, juicy mega-bucks.’ In the end, the little guy wastes his money in the market, or he loses his money gambling, or he dribbles it away on senseless schemes. In short, this ‘money-nerd’ spends his life dashing up the financial down-es-calator.

But here’s the ironic part of it. If, from the beginning, the little guy had adopted a strict policy of never spending more than he made, if he had taken his extra savings and compounded it in intelligent, income-producing securities, then in due time he’d have money coming in daily, weekly, monthly, just like the rich man. The little guy would have become a financial winner, instead of a pathetic loser.

41

KNOWLEDDGE BASE

Table of Contents

THE CRUX INTERVIEW

THIS LITTLE-KNOWN SECRET VIRTUALLY GUARANTEES YOU’LL MAKE

MONEY IN THE MARKET

You can file this interview under “trading ideas you’ve never heard of.”

The trading idea you’ll read about below is something that could immediately turn a struggling trader into a highly profitable one.

This idea has nothing to do with a specific stock or commodity trad-ing system. Instead, it’s a rarely used trading exercise you can use to ensure you’re always making money in the market.

Sharing this secret is Brian Hunt, Editor in Chief of Stansberry & Asso-ciates Investment Research. Brian is a successful private trader, and oversees one of the world’s largest independent financial research firms. He also writes the “Market Notes” column in DailyWealth, one of the most popular daily investment advisories in the world.

Read on for how to perform this valuable trading exercise...

The Crux: Brian... you’re a believer in a rarely used trading strategy that can drastically improve a trader’s performance. Something you call a “position audit.”

Can you talk about this idea, and how our readers can start using this to make more money?

Brian Hunt: Sure... A position audit is something everyone with money in the market should do at least once a year. And if you’re a trader who typically holds positions from two months to two years, you should do this exercise every month.

The exercise is taking a hard look at every position you have – long or short – and asking yourself, “If I wasn’t in this position already, would I take it now?”

If the answer is “no” on any position, sell it immediately.

42

S&A Trader’s Manual

Table of Contents

Crux: So the trader forces himself to be objective with his holdings on a regular basis.

Hunt: Exactly.

You see, lots of investors and traders struggle with admitting mis-takes and taking losses early. Rather than cut losing positions early, they tend to hold onto them and say something like, “it will come back.”

Or just as bad, they ignore the loser. They’ll ignore a loser that is down 20% or 30% until it grows into a giant 60% or 80% loser. And of course, it’s the giant losers that ruin your year... or your trading career.

It’s simple human nature to try to forget your mistakes. Life is easier that way. And in many cases, forgetting painful memories and mis-takes is a good thing.

For example, if an NFL quarterback has a horrible Sunday and throws five interceptions, he’d better get over it quickly... because he’ll need his self-confidence to be effective in the next game.

But with trading, ignoring a mistake is like ignoring cancer. If you catch it early, it’s not going to destroy you. But if you ignore it for months or years, it’s going to be fatal.

Your goal with regular position audits is to force yourself to confront your mistakes... and root them out of your portfolio before they be-come big ones.

Crux: Do you recommend this for trades based on fundamentals or based on technical analysis?

Hunt: Both.

Let’s say you buy company ABC because you think it’s going to come out with a new tech gadget that will sell millions of units. If that gadget comes out, and isn’t a hit – let’s say it only sells 20,000 units – the rea-son for owning that stock doesn’t exist anymore. It’s time to sell.

Or, let’s say you buy a big dominant company, like phone-maker

43

KNOWLEDDGE BASE

Table of Contents

Nokia used to be.

You think to yourself that it’s going to be a good long-term holding. But, if Apple comes along with a game changing product like the iPhone that starts eating into Nokia’s market share, the reason you bought that stock no longer exists. It’s time to sell.

Those are two fundamental examples. Of course, a company has lots of moving parts you have to analyze. I made those examples very simple... but you get the idea.

Crux: Okay, how about a technical example?