20

The car buyers handbook Buying and maintaining a car in NSW M a y 2 0 1 1 F T 2 2 4 www. airtrading.nsw.gov.au

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 1/19

The car buyers

handbookBuying and maintaining a car in NSW

M a y2 0 1 1

F T 2

2

4

www.airtrading.nsw.gov.au

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 2/19

Contents

ISBN 0 7347 6062 0

This publication can be viewed or printed rom the Publications pageo our website at www.airtrading.nsw.gov.au

DisclaimerThis publication is a plain language guide to your rights andresponsibilities. It must not be relied on as legal advice. For moreinormation please reer to the appropriate legislation or seekindependent legal advice.

CopyrightYou may copy, distribute, display, download and otherwise reelydeal with this inormation provided you attribute NSW Fair Trading

as the owner. However, you must obtain permission rom NSW FairTrading i you wish to 1) modiy, 2) charge others or access,3) include in advertising or a product or sale, or 4) obtain prot,rom the inormation.

Important: For ull details, see NSW Fair Trading’s copyright policyat http://www.airtrading.nsw.gov.au/copyright.html or [email protected]

© State o New South Wales through NSW Fair Trading.

Revised May 2011

Introduction 2

What type o car do youwant to buy? 2

1. Where to buy a car 3

Buying rom a car dealership 3

Buying a car privately 3

Buying online 5

2. Organising fnance 6

Loans 6

Balloon repayments 6

Leasing 7

Varying a credit contract 8

Cooling-o period 9

Contracts and deposits 9

3. Importantpre-purchase checks 11

RTA checks 13

Vehicle inspections 13

Space saver tyres 13

Real cost comparison 14

Vehicle inspection guide 16

Warranties 18

Motor Dealer Forms 18

Extended warranties 19

Extended warranty booklet 21Extended warranty checklist 21

4. Negotiating the deal 23

Buying the car 24

Insurance 25

Registration 26

Stamp duty 28

5. Maintenance 29

Service and repairs 29

6. Motor vehicle repairers 31

How Fair Trading can help 32

7. Useul agencies 33

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 3/19

The car buye rs handbook

2

The car buye rs handbook

3

1. Where to buy a carThere are a number o options available in terms o whereyou can buy a car. They each have their advantages anddisadvantages.

Buying rom a car dealership

Buying a car rom a licensed motor vehicle dealershipprovides many advantages. Unlike buying privately, thedealer has an obligation to guarantee that there is nomoney owing on the car. In certain conditions the dealer isobliged by law to provide a warranty. Also the dealer otenallows you to trade in your old car, however you may getmore money i you se ll it privately. Unlike buying rom anauction, you can test drive the car to make sure it has thepower and eatures you require. Most licensed car dealerscan also oer you nance or insurance but you don’t haveto accept it. Shop around and check out the rates oeredby banks, credit unions and nance companies.

Buying a car privately

Buying a car privately involves relying on your own judgement and knowledge. You can arrange or a vehicleinspection at your own cost but there are no statutorywarranties. Also, making sure that the vehicle is notencumbered, stolen or de-registered is the responsibility o

the buyer. Doing a REVS check (see page 11) will help youascertain this. Always ask the seller or, and note down, theinormation listed below:

• the current certicate of registration

• a pink slip which is no more than 42 days old

• proof that the person selling the car is the owner eg. asales receipt or driver’s licence to help identiy the seller

• the registration number

. Important

When planningyour budget, don’torget about stampduty, registrationand transercosts, insurance,maintenance andrepair costs.

IntroductionBuying a new car can be an overwhelming experience withso many considerations. This booklet is designed to assistconsumers through the entire car experience – what typeo car to buy, where and how to purchase, and importantthings to consider while making your decision. The bookletalso suggests a number o steps you can take to protectyoursel and lists various agencies that can assist you alongthe way.

The hard work doesn’t stop once you have purchased acar. Maintaining a car is also a big responsibility and is asimportant as driver saety. An unsae car is as dangerous asan unsae driver. The car buyers handbook suggests ways toapproach maintaining and repairing your vehicle.

What type o car do you want to buy?

The type o car you want to buy depends on your ownpersonal taste and needs, and your budget. A armer mayneed a vehicle that will handle dicult and rugged terrain.A tradesperson may need a vehicle that will transport allo their tools. A university student may need a cheap yetreliable car to get them rom university to work.

Whatever your needs and personal taste, buying a car islike any other serious purchase – deciding on the most you

want to spend will help narrow down the options and makechoosing easier.

Ensure that you can actually aord the car not just therepayments per week/month but other associated costssuch as registration, insurance, car maintenance etc.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 4/19

The car buye rs handbook

4

The car buye rs handbook

5

• the engine number

• the VIN (vehicle identication number) or chassisnumber.

Note: Ensure the inormation shown in the paperworkmatches what is on the actual car.

Buying from the roadside

There are no saeguards with this type o car sale. Thereare no guarantees o title and no warranties supplied. Youcould be stuck with a vehicle that has been poorly repaired

or even written-o. No matter how good the bargain looks,steer well clear o this method o purchasing a car.

Buying from an auction

The benet o buying a car at auction is that you couldpick up a real bargain. The cars come rom situations thatinclude deceased estates and repossessed vehicles. The riskwith buying at auction is that the car is not covered by astatutory warranty and generally you can’t take it or a testdrive. You can arrange an independent vehicle inspection atyour own cost but not on the day o the auction.

Auction houses are responsible or ensuring the cars theysell have no money owing on them. Most auction housesrequire a 10% deposit or $500 at the all o the hammer.

Where motor vehicles are sold with number plates attached

to private purchasers they have to have a Saety Inspectionreport (pink slip) issued by an Authorised Inspection Station(AIS). The inspection report must:

• be not more than one month old at the time of auction

• state that the vehicle is t for registration

• be attached to the vehicle at the time it is offered ordisplayed or sale or

• be provided to the purchaser at the time of delivery of the vehicle.

When a vehicle (other than an exempted vehicle eg.commercial) is oered or displayed or sale at auction aForm 9 should be displayed. The Form 9 must state thatthe vehicle is not subject to the warranty provisions o the Motor Dealers Act 1974 and displayed either on thevehicle, adjacent to the auctioneer or at each entrance tothe auction.

Buying from a car market

Car markets bring buyers and sellers together in the oneplace without the need to drive all over town. However, you

are still buying ‘privately’ and thereore need to rely on yourown judgement and knowledge. There will be no guaranteeo title or warranties supplied. They can also be an outletor backyard operators to dispose o sub-standard vehicles,or even possibly stolen vehicles.

If the vehicle is not registered

I the vehicle is not registered you need to take it to anAuthorised Unregistered Vehicle Inspection Station (AUVIS).They will conduct a roadworthiness check and identiy thevehicle or the purpose o registration or the Roads andTrac Authority (RTA) and provide you with a blue slip.

To nd your nearest AUVIS, call 1300 137 302.

Buying online

When buying online you are either buying rom a dealer orbuying privately so ollow the guidelines that apply to thosepurchases. When you purchase goods online rom overseasor another state, NSW consumer protection laws may notapply and may only oer you limited protection. For moreinormation on buying online visit our website.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 5/19

The car buye rs handbook

6

The car buye rs handbook

7

Important

A new car can bequite expensive.It pays to do yourhomework so thatyou know exactlyhow much you canborrow withoutstretching yoursel.

ImportantDuring the termo the lease youare responsible ormaking the leaserepayments and orthe car’s runningand maintenancecosts.

Important

I you are leasing acar or business use,ask your accountant

i tax and GSTbenets apply.

Important

Balloon paymentoptions availableto you may includepaying the amountin ull, re-nancingor rolling over intoanother creditproduct.

2. Organising fnanceOnce you have decided upon your budget, the make andmodel o the car you would like to purchase, it is timeto shop around or the best price. Price can vary romdealership to dealership. Special oers will happen atdierent times through the year and most dealershipswill reduce prices just beore the next year’s models aredelivered.

Many car dealerships will oer ‘nance’ (a loan) to

their customers through a credit provider, but it i s alsoworthwhile shopping around to get the best deal. Banks,credit unions, and other nancial institutions all lend moneyand can be cheaper and more fexible than car dealerships.

All credit transactions that are predominantly orpersonal, domestic, or household use are regulated by theNational Credit Code. I the credit is provided wholly orpredominantly (over 50%) or business purposes, the Actmay not cover you.

Loans

When comparing loans you need to have a goodunderstanding o the terms used in loan contracts. The totalamount you pay to the lender will depend on the amountyou borrow, interest rate charged and the length o time

that you borrow the money (the term o the loan). Lenderswill usually calculate interest charges on a daily basis. Theseinterest charges are usually added to your loan accounteach month.

Balloon repayments

This is a loan where you pay reduced monthly instalmentsor the term o the loan, with a large nal payment (balloonpayment) that clears the debt.

Car dealerships may provide balloon loans that oera guaranteed buy-back price on your vehicle. Makesure you are aware o any conditions attached to thesearrangements. For example, i you buy a car on the basisthat you are promised a buy-back amount or the vehicleater a period o time, you could nd this amount isdependent on actors such as the condition o the vehicleand kilometres travelled.

Leasing

Leasing is another type o nance that may suit people whoregularly trade-in their car. In a lease arrangement wherethere is no obligation to buy the car, the ownership stayswith the lender and the car is returned at the end o thelease term. You can terminate the lease early by returningthe car, but there is a cost involved and this should beexplained in the contract.

When you lease a car the payments are based on thedierence between the car’s sale price and what the car isestimated to be worth at the end o the lease (its residualvalue).

Vehicles leased or business or commercial purposes andnovated leases are not covered by the National Credit Code.

Some leases have conditions that base the residual valueo the vehicle on the distance the vehicle will travel andon its condition. I or some reason the vehicle is not worththe estimated residual value at the end o the lease thenyou may have to make up the price dierence. I you intendto buy a vehicle on a lease agreement, make sure you areaware o any conditions on the vehicle such as mileage andits condition at the end o the lease period.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 6/19

The car buye rs handbook

8

The car buye rs handbook

9

Important

It is commonpractice or dealers

to take a holdingdeposit or the carwhen you sign acontract. Alwaysget a receipt or thismoney.

Important

From 1 July 2010the AustralianSecurities andInvestmentsCommission (ASIC)became the nationalregulator orconsumer credit.

Important

Buyers and dealersmay negotiate anextension or waivethe cooling-o period, howeverit is advisable orconsumers to retainthe cooling-o period to saeguardtheir rights.

Varying a credit contract

I you nd you have problems repaying your loan the lawallows or a variation in a credit contract on the basis o hardship, but the ollowing circumstances must exist:

• your inability to make repayments must be due tounemployment or illness or some other reasonable cause

• you expect that you will be able to make repayments if they are altered

• the situation is only temporary and it should improve inthe near uture.

Contact the lender and try to come to an arrangementto vary the loan contract with them. I you reach anagreement the lender must give you written conrmation o the terms. This could involve reducing the repayments andextending the term o the loan or postponing repaymentsor a period o time or a combination o both.

Where to get help with your credit contract

I you are having diculties coming to an arrangementwith the lender or have a dispute or complaint about yourcredit contract you can get help rom the Credit and DebtHotline – call 1800 808 488.

The Credit and Debt Hotline is an independent andcondential advice and advocacy service or credit and

debt matters.

Cooling-o period

The Motor Dealers Act 1974 provides or a 1 day, waivablecooling-o period or motor cars purchased by a linkedcredit arrangement.

A linked credit arrangement is where you purchase a carrom a dealership and the dealership:

• arranges your loan for the car

or

• supplies application forms for (or a referral to) a credit

provider.

The cooling-o period begins when the contract is enteredinto and generally ends at 5pm on the next day on whichthe dealer carries on business.

During the cooling-o period the purchaser can cancel thecontract by giving a signed, written notice to the dealer. I the contract is cancelled, the purchaser will be liable to paythe dealer $250, or 2% o the purchase price, whichever isthe lesser amount.

Contracts and deposits

I you sign anything at a car dealership, it is probably asale contract. You may also sign a loan application or loancontract on the premises. Contracts are legally enorceable.

Read all the documents careully. Do not sign anythingunless you understand what you are agreeing to and youare certain you will be buying the car.

I you have decided to buy a car but you need to have aloan approved rst, make sure that it is written into thecontract that completing the purchase is conditional on youobtaining the loan. I you have this specied in the contractand you cannot get a loan ater reasonable attempts, youmay be able to cancel the contract and have the depositreturned to you.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 7/19

The car buye rs handbook

10

The car buye rs handbook

11

New laws commenced on 1 July 2010 to deal with unairterms in standard orm consumer contracts. I you think aterm in your contract is unair, you should rst try to resolvethe issue with the trader. I you can’t resolve the issue, thenyou can lodge a complaint with NSW Fair Trading.

Understanding common contract terms

Principal The amount you borrow.

Interest The charge rom the lender or usingits money. This is usually expressedas a yearly rate and called the annualpercentage rate.

Fixed interestrate

This means the rate will remain the sameor a set amount o time. This oers greatercontrol over your nances because therepayment amount will always be thesame. The xed interest rate and the timeperiod it applies to must be stipulated inthe credit contract. Generally you will notbe able to make more than the agreedrepayments (ie. pay the loan o aster).Check the contract careully or anyconditions that apply.

Variableinterest rate

This means the interest rate will move upand down depending on the market.

Split interest

rate

You may be able to choose to split the

type o interest rate that applies to a loan.This occurs in two ways:

• a xed interest rate applies for aset amount o time. When that timeelapses, the rate can be changed to avariable interest rate

• part of the amount borrowed has axed interest rate applied and theremainder amount has a variableinterest rate applied.

3. Important pre-purchase checksThe Personal Property Securities Register (PPSR) will replace

REVS in late 2011. See note on let.

The Register o Encumbered Vehicles (REVS) is a serviceprovided by NSW Fair Trading that can tell you whether or nota vehicle is recorded as encumbered in NSW, ACT, NT, QLD, VICand SA. Encumbered simply means that there could be moneyowing on the car or that the registered owner may not ownthe vehicle outright. I you buy an encumbered vehicle, action

could be taken to repossess it, even though the debt is notyours. Completing a REVS check means you can conrmthis important aspect beore you make a purchase.

You can conduct your own REVS enquiry online 24 hours aday, 7 days a week at www.revs.nsw.gov.au

Call REVS on 13 32 20 8:30am - 5:00pm (weekdays) and9:00am - 2:00 pm (Saturdays).

You can purchase a REVS search certicate (through theinternet or telephone) or a small ee, which will buy youpeace o mind as it provides conrmation o your enquiry andoers legal protection against the vehicle being repossessedby a creditor due to a previous owner’s unpaid debt.

I REVS says the vehicle is recorded as being encumberedand you still wish to proceed with the purchase, REVS cantell you what steps to take.

REVS can also inorm you i the vehicle has been:

• reported to the police as stolen

• recorded as de-registered by the RTA due to outstanding nes

• recorded with the RTA by an insurer as a written-off vehicle

• recorded by Fair Trading as having possible odometerintererence.

Important

REVS does notguarantee theaccuracy o stolenand written-o vehicle inormation.

To check i theregistration is stillvalid, visitwww.rta.nsw.gov.aucall the RTA on13 22 13 or contactyour local motorregistry.

Important

In late 2011, theCommonwealth willcommence its newPersonal PropertySecurities Register(PPSR), which willreplace REVS and allother State vehicle

securities registers.The new PPSR willprovide nationalinormation aboutsecurities over motorvehicles. PPSR contactdetails will be postedon the Fair Tradingand REVS websites.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 8/19

The car buye rs handbook

12

The car buye rs handbook

13

Note: I you buy a late model second-hand car, check withthe manuacturer that the balance o the new car warrantycan be transerred to you and that it has not been cancelledparticularly i the vehicle has been recorded as a repairablewrite-o. Some warranties have conditions that invalidatethe warranty when there has been an accident.

Where the inormation provided by the seller does notmatch, the RTA can also give advice on what to do.

Seven easy steps to ollow when you buy a car privately

1. Ask i any money is owing on the vehicleYes No

2. Get the registration number, engine number, and vehicleID number (VIN) or chassis number rom the vehicle.

Registration number:

Engine no:

VIN/Chassis no:

3. Conrm that the registration number, engine numberand VIN/chassis numbers on the vehicle match those onthe registration papers.

Registration number:

Engine no:

VIN/Chassis no:

4. Call REVS on 13 32 20 or visit www.revs.nsw.gov.au to complete a vehicle search with these numbers.

5. Purchase a REVS Search Certicate to guard againstrepossession.

6. Arrange or the current owner to repay the debt, i oneexists. REVS can tell you how to do this.

7. Complete the transaction beore midnight the next day.

RTA checks

An RTA vehicle history check will tell you i a vehiclehas previously been written o in NSW or interstate, thenumber o previous NSW owners, vehicle usage historyand much more. An RTA registration check will giveyou inormation about a vehicle’s registration and CTPinsurance status. Visit www.rta.nsw.gov.au or moreinormation.

Vehicle inspections

Beore purchasing a second-hand car it is important toinspect the vehicle thoroughly. Inspections can help youidentiy problems and assess a car’s value more accurately.They can also provide some room or negotiation on thesale price. There are details that are easy to check yoursel as indicated in the Real cost comparison on page 14.

Space saver tyres

Many new vehicles are now sold without a ull-size sparetyre or with no spare at all.

The most common type is the space saver tyre, which isnarrower than a normal tyre and is thereore lighter andtakes up less space in the boot.

I you have to use a space saver tyre be sure to observe the

manuacturers instructions or its use regarding maximumspeed, tyre pressure, vehicle load, sae travel distances,road holding and stopping distance.

Some cars do not have a spare tyre at all, but have run fattyres, which can still be driven on i punctured. They also arelimited as to the speed o the vehicle and the distance theycan travel when fat, so check the manuacturers instructionscareully. Their convenience must be weighed up against thecost o replacing them, as they cannot be repaired.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 9/19

The car buye rs handbook

14

The car buye rs handbook

15

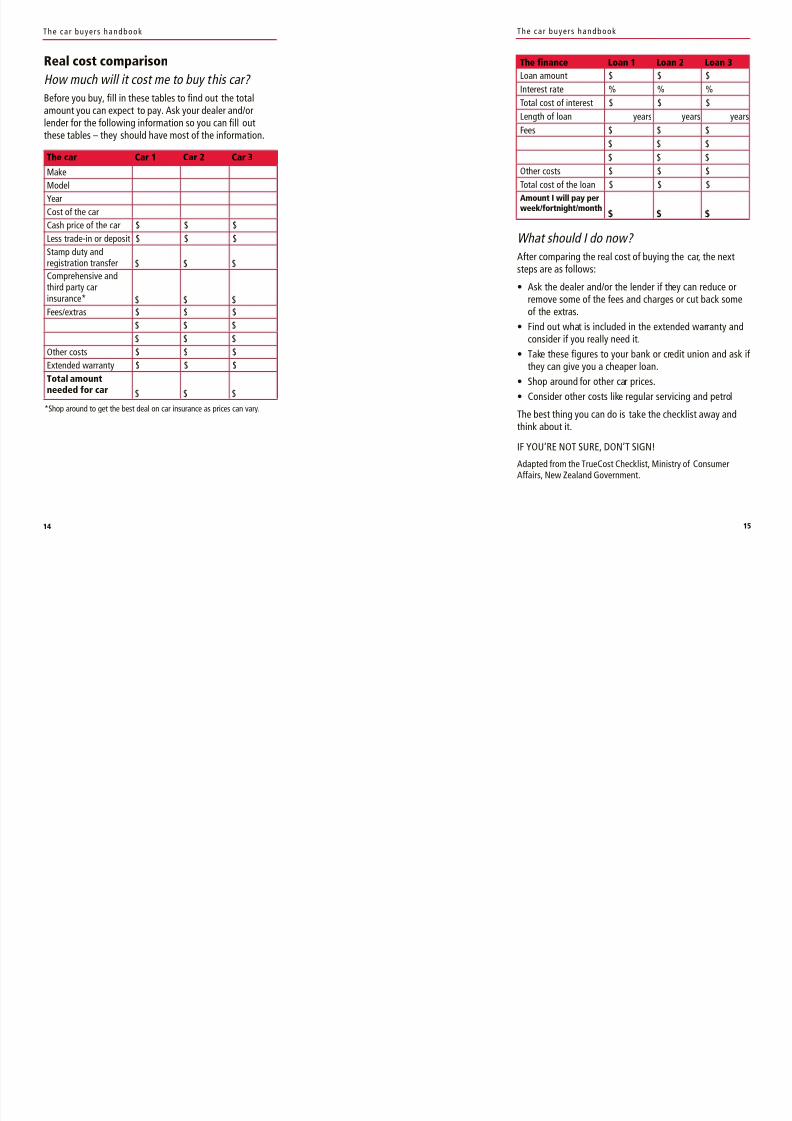

Real cost comparison

How much will it cost me to buy this car?

Beore you buy, ll in these tables to nd out the totalamount you can expect to pay. Ask your dealer and/orlender or the ollowing inormation so you can ll outthese tables – they should have most o the inormation.

The car Car 1 Car 2 Car 3

Make

Model

Year

Cost o the car

Cash price o the car $ $ $

Less trade-in or deposit $ $ $

Stamp duty andregistration transer $ $ $

Comprehensive andthird party carinsurance* $ $ $

Fees/extras $ $ $

$ $ $

$ $ $

Other costs $ $ $

Extended warranty $ $ $

Total amount

needed or car $ $ $

The fnance Loan 1 Loan 2 Loan 3

Loan amount $ $ $

Interest rate % % %

Total cost o interest $ $ $

Length o loan years years years

Fees $ $ $

$ $ $

$ $ $

Other costs $ $ $

Total cost o the loan $ $ $

Amount I will pay perweek/ortnight/month

$ $ $

What should I do now?

Ater comparing the real cost o buying the car, the nextsteps are as ollows:

• Ask the dealer and/or the lender if they can reduce orremove some o the ees and charges or cut back someo the extras.

• Find out what is included in the extended warranty andconsider i you really need it.

• Take these gures to your bank or credit union and ask if they can give you a cheaper loan.

• Shop around for other car prices.

• Consider other costs like regular servicing and petrol

The best thing you can do is take the checklist away andthink about it.

IF YOU’RE NOT SURE, DON’T SIGN!

Adapted rom the TrueCost Checklist, Ministry o ConsumerAairs, New Zealand Government.

*Shop around to get the best deal on car insurance as prices can vary.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 10/19

The car buye rs handbook

16

The car buye rs handbook

17

Vehicle inspection guide*Under the hood

Engine numberand VIN number

The numbers shown on the Certicate o Registration must matchthe engine and VIN numbers on the car. Be wary o any signs o intererence such as scratches, grind marks or drill holes. Thesemay indicate illegal tampering with the numbers and the vehicle.

Engineappearance

A build-up o dirt may suggest poor maintenance or mechanicalproblems.

Engine oil Dirty/thick oil and a build-up o sludge in the engine may suggestpoor maintenance. Grey or milky coloured oil may suggest thepresence o water, which would indicate serious problems.

Engine idle The engine should idle smoothly. Listen or irregular running or anyunusual noise such as any knocking or rattling noises.

Oil umes Remove the oil ller cap while the engine is idling. Fumes maysigniy worn piston rings or cylinders. Thick, black smoke comingrom the exhaust can signiy problems as well.

Radiator coolant Should be clean and brightly coloured. Oil in the coolant may indicatea cracked cylinder-head or a leaky gasket.

Radiator coolerfns or core tubes

Check or corrosion or damage.

Battery mountingplatorm/bracket

Check or acid corrosion.

Underneath the car

Tyres (don’t orgetthe spare)

Uneven wear may indicate worn or misaligned steering orsuspension. Check that there is at least 5mm o tread. Check there isa jack and tools.

Oil leaks Check the engine, transmission, axles, brakes, power steering andshock absorbers. A leak in any o these areas could indicate

a problem and could possibly be a danger.Exhaust system Fumes or excessive noise may suggest there is a hole or rust in thepipes or the mufer.

Body o the car

Rust/accidentdamage

Check inside the boot, the foor wells, doors and lower sills or redor other dark stains, dimpled or bubbled paint. Use a sot ridgemagnet to check panels or plastic body ller.

Hail damage Hail damage makes a car dicult to insure. Check the horizontalpanels such as the bonnet, roo and boot lid.

Panel ftment Loose panels may indicate accident damage or that the car hasbeen driven over rough roads.

Doors/boot lid Catches should close rmly and lock. Rubber seals can perish over time.

Paint Look or colour variation, overspraying, dents or ripples. These mayindicate that the car has been in an accident.

Inside the car

Upholstery,carpet

Check or wear and tear.

Seat belts Check that the belts are not rayed or damaged, and that the belts,buckles and adjusters and child restraint anchorage points are ingood condition.

Lights Check that all lights, both inside and outside the car, are working.

I the car is tted with ABS and/or SRS (air bag), check that thedashboard warning light/s illuminate or a short time when theignition is turned on.

Equipment andaccessories

Check air-conditioning, ventilation an, electric windows, soundsystems, horn, windscreen wipers etc. Inoperative items can beexpensive to repair or replace.

Jack and tool kit These items should be in place and in serviceable condition.

Test driving the vehicle

As part o a thorough inspection many people test drive the car. The ollowing are somethings to check when test driving.

Steering Excessive ‘ree travel’ or wandering on straight roads can indicateworn suspension or misaligned steering.

Brakes The car should stop smoothly and in a straight line. The pedalshould not sink to the foor or eel spongy and the steering wheelshould not vibrate.

Exhaust Blue smoke indicates oil is burning.

Engine Should run smoothly (accelerating, decelerating and cruising) and

the water temperature gauge should stay in the sae range. Rattlingor knocking could mean incorrect tuning or excessive wear.

Transmission Gear changes (manual and automatic) should be smooth, withoutany rattles or knocking noises. On ront-wheel drive vehicles, thesenoises could indicate worn constant-velocity joints.

Suspension andbodywork

Listen or rattles when you drive over bumps. It is also wise to havethe car inspected by a reputable mechanic.

Odometer Check that the odometer is working during the test drive. Note thenumber o kilometres travelled which can indicate when a majorservice will be required.

*This inormation was provided by the NRMA and has since been updated by Fair Trading.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 11/19

The car buye rs handbook

18

The car buye rs handbook

19

Warranties

The Motor Dealers Act 1974 requires licensed dealers tox certain deects i they occur in vehicles that they havesold. This is called a statutory warranty. When buying asecond-hand car you can only get a statutory warranty i you buy the car rom a licensed motor dealer.

New cars have a 12 month statutory warranty. However,most manuacturers provide a manuacturers warranty romthe date o sale.

In NSW all second-hand passenger cars that are less than10 years old and have travelled less than 160,000km andare priced under the luxury tax limit have a minimumwarranty o 3 months or 5,000km – whichever comes rst.This is called the standard warranty.

Both the car and any accessories tted to it (such as soundsystems) are covered by the warranty. Supercial damage(such as paint scratches or minor tears in the upholstery)and normal wear and tear are not covered.

Nor does the warranty cover:

• routine services

• tune-ups

• batteries

• tyres (however they must be roadworthy at the time of sale)

• defects that arise from accidents or misuse of the vehicle.

Motor dealer orms

Licensed dealerships are required to put a orm on everysecond-hand vehicle or sale or on display, describing thevehicle. The orm includes the dealer’s name, cash price,engine number, odometer (speedo) reading and importantlywhether a warranty applies. The orm will be either a Form

4, 6 or 8 and it is important to know the dierence, as itaects the warranty.

Form 4 means the car has a standard statutory warrantyas described above.

Form 6 means the car has a standard warranty, but notor deects listed by the motor dealer as beingexcluded rom warranty. The dealer must list thedeects that are excluded and give an estimate o the costo repairing them. Roadworthiness items (such as tyres orbrakes) cannot be excluded rom warranty. A car displaying

a Form 6 must be sold with a pink slip showing that it isroadworthy.

Form 8 means the car is not covered by warranty.Generally this is because it is older than 10 years, hastravelled more than 160,000km, is a commercial vehicleor priced above the luxury car limit (ie. $57,123). A cardisplaying a Form 8 must be sold with a pink slip showingthat it is roadworthy.

Extended warranties

Some dealers oer an extended warranty or periodsbeyond the standard statutory or manuacturer’s warranty.There are many dierent types o extended warrantiesoered through motor dealerships by insurance companiesor manuacturers. Extended warranties may be insurance ormaintenance policies oered by a third party rather than amanuacturer.

An extended warranty policy is usually a comprehensive10-20 page booklet which is supposed to provide anadditional cover to the standard statutory warranty thatyou get or ree or manuacturer’s warranty or new or usedvehicles. Generally, you have to pay extra or an extendedwarranty. However, some motor dealers may include an

Important

You can only get astatutory warranty

or a second-handcar i it is boughtrom a licensedmotor dealer.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 12/19

The car buye rs handbook

20

The car buye rs handbook

21

extended warranty with a minimum (highly restrictive)cover, in the sale price or oer it ree o charge to make thesale more attractive.

Exclusions and special conditions

Make sure you know exactly what is covered and whatis excluded rom the extended warranty policy and anyspecial conditions that you need ollow or the cover toapply. Some typical extended warranty exclusions are:

• wear and tear

• car modications, including tinting or paint changesoered by the dealer

• consequential damage or defect caused by misuse of thevehicle such as overheating, lack o oil

• specied parts or systems.

Beware, as some extended warranties or new cars do notoer the same cover as the manuacturer’s warranties, suchas oil leaks.

Some common extended warranty conditions andrequirements include:

• a regular service during the whole warranty period ata specied place (or dealer) at your own cost eg. every5,000km/6 months or 10,000km/12 months dependingon the distance the vehicle has travelled

• an excess payment up to $500 per claim depending onthe component ailure

• a service coupon must be stamped and posted within7 days

• a maximum payout limit which may not be sufcient tocomplete the necessary repairs and you may need to paythe gap yoursel.

Extended warranty booklet

Make sure you FULLY read and understand the extendedwarranty booklet and can comply with its terms andconditions or the whole warranty period beore buying it.I you don’t meet any o the extended warranty conditionsyou may not be able to claim on it or your policy may becancelled. Beware o its limitations.

Always confrm all the terms and conditions o theextended warranty in writing, not verbally. Check theseacts in the extended warranty booklet beore you

take out the warranty. You can get this booklet rom thedealer and take it home to consider.

Extended warranty checklist

Warranty provider

Who is the provider o the extended warranty? Is it amanuacturer or an insurance company?

Type o car and usage

Is the extended warranty or a new or used car? Dierentstatutory and manuacturer warranties apply.

Is the car or commercial or private use? The extendedwarranty may not apply to commercial usage.

Period

What is the period o the extended warranty?

Does it start rom the date o purchase?

Does it start when the statutory or manuacturer’s warrantyexpires?

Terms and conditions

Are there any special requirements? eg. regular service every5,000km or 10,000km.

What does the extended warranty cover?

What are the exclusions or restrictions?

Important

I the extendedwarranty is oeredor ‘ree’ or isincluded in thedeal, expect claimlimitations.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 13/19

The car buye rs handbook

22

The car buye rs handbook

23

Can you cancel or transer the extended warranty? It maycost extra.

Is there a cooling-o period? Some policies may have acooling-o period o 21 days. However, you may not get theull reund i you want to cancel the policy and you will haveto do it in writing within the cooling-o period.

Claims

Are there any claim limits?

Are there excess ees or each claim you make?

Where and how do you lodge a claim? You may be restricted

to a particular repairer and number o claims you can make.General

How much does the extended warranty cost?

How long do you plan to keep the car?

Are you planning to move? You may have servicing issues.

Is it really worth the money?

4. Negotiating the dealYou have ound the car and have completed all thenecessary pre-purchase inspections and now you are readyto make an oer. All the research and inspection eortsthat you have put in will provide valuable inormation innegotiating the best price. For example, i an inspectionreveals that you may need to pay or certain repairs, youmay be able to negotiate a lesser price because o it.

I you need to obtain a loan to purchase the car, make sure

you shop around. Many motor dealers are able to oernance but you may get a better deal rom your own bankor credit union.

There is a ‘cooling-o period’ that applies i you purchase acar rom a dealership and the dealership:

• arranges your loan for the car

or

• supplies application forms for, or a referral to, a creditprovider. This is called a linked credit arrangement.

Under these circumstances only, the cooling-o period givesyou 1 day to change your mind. The cooling-o period beginswhen the contract is entered into and generally closes at5pm on the next day that the dealer is open or business.During the cooling-o period the purchaser can cancel the

contract by giving written and signed notice to the dealer.The purchaser will be liable to pay the dealer $250, or 2% o the purchase price, whichever is the lesser amount.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 14/19

The car buye rs handbook

24

The car buye rs handbook

25

Buying the car

Have you completed all the necessary inspections? Makesure that:

• the seller and the name on the registration relate toeach other

• the identication numbers on the car, and those listed onthe registration papers match

• any necessary safety check forms have been provided(such as a pink slip or blue slip)

• a REVS check (page 11) has been satisfactorilycompleted

• a vehicle inspection has been satisfactorily completed

• a price and a means of payment has been agreed uponbetween you and the seller.

I you have answered ‘yes’ to the above questions and arehappy to proceed with the purchase, you need to do theollowing:

• ask the seller to complete and sign the back of thecerticate o registration. I the vehicle is registered intwo names, both must sign

• ask the seller to give you a receipt that shows:

- your name

- the date you bought the car

- the amount you paid or it- the vehicle’s VIN or chassis number, and engine number

- the seller’s driver’s licence, name and signature

• check that the seller’s signature on the receipt matchesthe signature on the seller’s licence.

Remember that the receipt is the only proo that you nowown the vehicle. The RTA certicate o registration showsonly the person who takes responsibility or the car, it doesnot prove ownership.

Before you drive away

Make sure the seller gives you:

• all keys including those for the ignition, glove box, bootand alarm

• the service books, owner’s manual and log book

• instructions for working and de-activating any alarm

• location of the hidden ignition switch if there is one

• radio security number.

Insurance

Cars are powerul machines that can cause substantialdamage. Even though we may regularly have our carsserviced and drive saely, unortunately accidents occur.Beore you can register your car with the RTA, you mustprove that you have purchased a green slip – otherwiseknown as Compulsory Third Party (CTP) personal injuryinsurance.

The NSW Motor Accidents Authority (MAA) regulates theinsurers who provide green slip insurance. It also undsa large number o injury prevention and rehabilitationprograms or people injured in car accidents.

You purchase a green slip direct rom insurers, not rom theMAA. However, the MAA can provide you with advice onwhere to nd the cheapest green slip. I you are purchasing

a new car, the car dealer will generally have arranged agreen slip or you.

There are many insurers competing or your business, so it’swise to shop around. You might be able to save money byvisiting the green slip calculator at the MAA’s web site,www.maa.nsw.gov.au

Important

Recording the dateyou bought the

car may protectyou against anyoutstanding red lightor speeding camerainringements.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 15/19

The car buye rs handbook

26

The car buye rs handbook

27

Based on the inormation you provide, the calculator willtell you which insurer will sell you a green slip or thecheapest price. I you don’t have access to the internet, youcan call the MAA’s green slip help line on 1300 137 600.

I you cause an accident, your green slip insurance coversmedical costs or:

• your passengers

• other road users, such as drivers, passengers, pedestrians,cyclists, motor cyclists and pillion passengers

• injuries caused through the use of a trailer.

Your green slip insurance does not cover:

• you for your personal injuries if you cause the accident

• damage to property or other vehicles.

There are two other types o insurance available or yourvehicle:

Third party property - which covers you or the damageyour car might cause to someone e lse’s vehicle or property.

Comprehensive - which provides third party propertycover and also covers your car or accidental damage, thetand re.

Registration

Once you have purchased your new or used vehicle, youneed to arrange registration. An unregistered vehicle canincur hety nes, and will leave your car uninsured. I youhave an accident in your unregistered car, you will be liableor any damage caused to people or property.

To establish registration

I there are no number plates attached to the vehicle, or theregistration has been expired or more than 3 months, youwill need to establish the registration o your vehicle.

To do this you must attend a motor registry in person andprovide the ollowing:

• proof of your identity

• the receipt showing that you are the new owner

• current green slip

• safety inspection report, known as a blue slip, from anAuthorised Unregistered Vehicle Inspection Station (AUVIS)

• payment for registration, including stamp duty

• if previously registered interstate, proof of that registration.

To renew an existing registration You can renew your vehicle’s registration at a motorregistry, online at www.rta.nsw.gov.auor by calling13 22 13.

You will need to provide:

• the renewal notice

• current green slip

• if your vehicle is more than 3 years old a safety checkreport (pink slip)

• payment for registration.

Transferring registration

To transer the registration o a vehicle, you must visit amotor registry and provide the ollowing:

• the certicate of registration for your vehicle, completedand signed on the back by the seller

• proof of your identity eg. your driver’s licence

• the receipt showing that you are the new owner

• the transfer fee and stamp duty cost.

You have 14 days to transer the Certicate o Registrationinto your name. Ater this period you will be charged a latetranser ee. Failing to transer the registration can result in

Important

To renew online orover the phone youmust get your pinkslip rom ane-Saety CheckStation andyour green slipprovider must sendyour insurancedetails to the RTAelectronically.

Important

Your green slipwill only coveryou i your vehicleis registered. I you allow yourregistration to lapse,you are personallyliable or any injuriesyou cause in a motorvehicle accident.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 16/19

The car buye rs handbook

28

The car buye rs handbook

29

the RTA cancelling the registration altogether. Your vehiclewill then be unregistered which can result in hety nes andwill leave your car uninsured.

Stamp duty

The Oce o State Revenue (OSR) levies stamp duty whena vehicle is registered in a new name. The RTA collects thestamp duty on OSR’s behal. You will pay stamp duty onthe market value o the vehicle or on the price you paidor the vehicle, whichever is higher. Stamp duty is 3% o the market value o the car, up to $45,000 then 5% on thevalue over $45,000.

For example, the stamp duty or a vehicle with a marketvalue o $50,000 is calculated as ollows:

$45,000 at 3% = $1,350$5,000 at 5% = $250Total stamp duty to be paid = $1,600

(Calculations are provided by RTA and are correct at time o printing. Please check with the OSR or RTA to conrm.)

Important

As long as

the service iscarried out inaccordance withthe manuacturer’sspecications, anylicensed repairercan do it, not justthe dealer romwhom youpurchased the car.

5. MaintenanceA car is a big investment or most people and a largeresponsibility. Car owners should regularly maintain theircars to protect their investment and to keep them sae androadworthy.

Service and repairs

I you have a problem with a new car that is still underwarranty, reer to your warranty and talk to the motordealer who sold you the car. Whether new or second-hand,your car should have come with a log book or owner’shandbook that sets out when the vehicle should be servicedand what maintenance needs to be done.

To keep your car in top condition and to avoid thepossibility o breakdown or expensive repairs in the uture,you should ollow the maintenance schedule. I the car isstill under warranty and you don’t have it serviced to themanuacturer’s maintenance schedule, you may void yourwarranty.

When booking your car in or a service, clearly explain toyour repairer the type o service you require. Dierent costsare associated with the dierent types o services you canhave. I you don’t have a log book or handbook and are notsure what your car needs, ask the repairer to explain what

is involved with each type o service and its associatedcost. I you are still uncertain, it is wise to ollow themanuacturer’s service schedule.

The more inormation you can give to the repairer, the morelikely the diagnosis will be correct and the repair carried outproperly. You may even need to test drive the car with therepairer, or example, i a rattle only occurs at a certain speed.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 17/19

The car buye rs handbook

30

The car buye rs handbook

31

Always ask or a written cost estimate or quote to x theproblem so there are no surprises at the end. It is a goodidea to leave a contact number with the repairer in casethey discover the need or additional work. I you have adeadline, such as picking up the children ater work, tell therepairer so they are aware o the timerame.

Where a repairer spends time carrying out and providinga detailed diagnosis, but you decide not to carry outthe repair, the repairer is entitled to charge a ee or thediagnosis.

6. Motor vehicle repairersIn NSW repairers must be licensed to work on your car. Tohold a licence a repairer must meet criteria laid down bythe State Government licensing authority, which is part o NSW Fair Trading. This includes having specied equipmentin the workshop and employing only certied tradespeopleto carry out repairs.

I you are dissatised with the work conducted on your car,you can do something about it. Follow these steps to seek a

resolution:1. Talk to the repairer and advise that you are not satised

with the work completed. This will give the repairer anopportunity to x the problem to your satisaction.

2. I unresolved, call NSW Fair Trading on 13 32 20.We have Technical Enquiry Ocers, who can provideunbiased advice regarding your issue. You can use theinormation they provide to again attempt a resolutionwith your repairer.

3. I unresolved, send a letter to NSW Fair Tradingcontaining the ollowing inormation:

- your name and address

- your vehicle identication

- the repairer’s name and address

- a summary o the issue

- what you want to settle the matter.

4. A mediator rom Fair Trading will arrange a meeting,usually at the repairer’s workshop, with the repairerand you. The mediator, who is a qualied tradesperson,is impartial, representing neither the consumer northe repairer. I a resolution is reached, the terms o settlement are drawn up by the mediator and providedto each party. I a resolution is not reached, a report iswritten by the mediator and supplied to each party.

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 18/19

The car buye rs handbook

32

The car buye rs handbook

33

7. Useul agenciesMotor Accident Authority (MAA)

Tel: 1300 137 600 (Green slip helpline)Tel: 1300 137 131 (General enquiries)8.30 – 5.30 Mon-Thu8.30 – 5.00 Friwww.maa.nsw.gov.au

Motor Traders Association o NSW (MTA NSW)

Tel: 9213 4222

9.00 – 5.00 Mon-Friwww.mtansw.com.au

Register o Encumbered Vehicles (REVS)

Tel: 13 32 208.30 – 5.00 Mon-Fri9.00 – 2.00 Satwww.revs.nsw.gov.au

Roads and Trafc Authority (RTA)

Tel: 13 22 138.30 – 5.00 Mon-Fri8.30 – 12.00 Satwww.rta.nsw.gov.au

5. You can then take the dispute to the Consumer, Traderand Tenancy Tribunal or a resolution. The mediator’sreport is oten submitted as a type o ‘expert opinion’.

I you believe that the repairer has acted in a dishonest orunair manner you should report it to NSW Fair Trading,who will investigate your complaint. Repairers which areound to have been dishonest or unair or who perormrepair work that is below the usual trade standard can bedisciplined and their repairer’s licence may be suspended orcancelled.

How Fair Trading can helpNSW Fair Trading provides a range o inormation to assistcar buyers. As well as this booklet, our website has acomprehensive section on motor vehicles which can beaccessed at www.airtrading.nsw.gov.au

Fair Trading can also assist with complaints regardingnew and used vehicles, deposits, warranty repairs, salescontracts and misleading conduct by licensed motordealers. Our customer service sta can provide inormationon what to do i you have a problem.

Contact Fair Trading on 13 32 20.

You can also lodge a complaint on our website atwww.airtrading.nsw.gov.au

8/4/2019 FT224 the Car Buyers Handbook

http://slidepdf.com/reader/full/ft224-the-car-buyers-handbook 19/19

For inormation and help on air trading issues call NSW Fair Trading

General enquiries

13 32 20

Language assistance13 14 50

TTY or hearing impaired

1300 723 404

Aboriginal enquiry ofcer

1800 500 330

Consumer, Trader & Tenancy Tribunal1300 135 399

Registry o Co-operatives & Associations

1800 502 042

Or visit a Fair Trading Centre at:• Albury • Armidale • Bathurst • Blacktown • Broken Hill • Coffs Harbour

• Dubbo • Gosford • Goulburn • Grafton • Hurstville • Lismore • Liverpool

• Newcastle • Orange • Parramatta • Penrith • Port Macquarie • Queanbeyan• Sydney • Tamworth • Tweed Heads • Wagga Wagga • Wollongong

Visit our website or details

www.airtrading.nsw.gov.au

13 32 20

NSW Fair Trading1 Fitzwilliam St Parramatta NSW 2150

PO Box 972 Parramatta NSW 2124

9895 0111

![FT224 the Car Buyers Handbook[1]](https://static.documents.pub/doc/80x56/577d34c61a28ab3a6b8ed1e7/ft224-the-car-buyers-handbook1.jpg)