43

FTTx coverage and capex: worldwide trends and forecasts 2019–2025 FTTx coverage and capex: worldwide trends and forecasts 2019–2025 Stephen Wilson

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

FTTx coverage and capex:

worldwide trends and

forecasts 2019–2025

Stephen Wilson

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

KEY QUESTIONS ANSWERED IN THIS REPORT WHO SHOULD READ THIS REPORT

This report analyses and forecasts coverage (premises passed)

and capex for FTTx architecture and technologies during 2019–

2025. It is based on several sources, including the following.

▪ Analysys Mason’s internal research, including our core

telecoms forecasts, our fixed data traffic forecasts and our

detailed modelling of the costs of technologies and

deployment. Our modelling and assumptions are informed

by professionals in our 16 offices worldwide.

▪ Ongoing engagement with stakeholders in the FTTx market,

including operators and vendors.

2

About this report

▪ How quickly will next-generation access (NGA) coverage grow across

different global regions and individual markets?

▪ Which markets represent the most-promising opportunities for vendors

in terms of NGA coverage expansion?

▪ To what extent can NGA coverage grow in emerging markets across the

globe?

▪ What will be the scale of roll-outs from non-incumbent FTTP operators?

▪ What are the coverage levels of Gigabit-capable broadband?

▪ This report provides strategic planners with detailed and comprehensive

insight into the development of FTTx in comparable markets, allowing

them to understand what level and type of investment is appropriate,

and where opportunities lie.

▪ For equipment vendors, construction businesses and component

suppliers, it shows the scale of opportunity in FTTx.

▪ The model can also serve several other functions beyond the immediate

scope of this report. It can be used to provide the costs of alternative

scenarios, including different mixes of technologies, different demand

profiles in different geotypes, and different completion dates. If you wish

to explore these options, please contact the author.

GEOGRAPHICAL COVERAGE

▪ Western Europe (WE)

▪ Central and Eastern Europe

(CEE)

▪ Middle East and North Africa

(MENA)

▪ Sub-Saharan Africa (SSA)

▪ Emerging Asia–Pacific (EMAP)

▪ Developed Asia–Pacific (DVAP)

▪ North America (NA)

▪ Latin America (LATAM)

CASE STUDIES

▪ Coverage (premises passed)

▪ Capex (network and connection)

▪ Split by architecture/technology:

o FTTC/VDSL or G.fast,

FTTB/VDSL or G.fast, FTTB/LAN

o FTTP (split by incumbent and

alternative operator)

o Cable DOCSIS3.0 or 3.1 (Note:

capex is not provided for cable

DOCSIS3.0 or 3.1).

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

6. Worldwide trends

7. We forecast that 2019 was the peak year for global FTTx capex worldwide

8. FTTP will increase its dominance of the global NGA landscape during the

forecast period

9. FTTP and cable networks are the only viable options for meeting coverage

targets for gigabit-capable broadband

10. Roll-out plans in most countries in Western Europe currently miss the

Gigabit Society’s targets by some margin

11. Much work remains in Central and Eastern Europe in order to meet the

EU’s Gigabit Society’s targets

12. The rate at which FTTP can be built out depends on the existing level of

usable infrastructure, but regulation can help to speed up roll-outs

13. Non-incumbent operators can also rapidly increase FTTP coverage,

particularly if they have access to their own or rented infrastructure

14. There are opportunities for FTTP vendors to benefit from significant

coverage increases in some, but not all, large emerging markets

15. Western Europe

16. We forecast strong levels of investment in FTTP networks in Western

Europe throughout the forecast period

17. Central and Eastern Europe

18. The number of non-incumbent FTTP deployments in rural areas in Central

and Eastern Europe is growing, but not dramatically

19. Middle East and North Africa

20. Government intervention is driving an increase in fibre coverage in the

Middle East and North Africa, and the focus on wholesale access in the

region is increasing

21. Sub-Saharan Africa

22. NGA coverage in Sub-Saharan Africa is constrained by affordability, the

high cost of deployment and the lack of availability of fibre backbone

infrastructure

23. China

24. FTTP coverage is already very high in China and the focus has shifted to

upgrading to next-generation PON

25. Emerging Asia–Pacific

26. The number of FTTP deployments in several countries in the EMAP region

increased in 2019 and this momentum will continue

27. Developed Asia–Pacific

28. Several drivers explain the growth in the number of next-generation PON

deployments in developed Asia–Pacific

29. North America

30. The number of new fibre entrants in North America is far fewer than in

Western Europe

31. Latin America

32. Investment in FTTx networks in LATAM continues to be strong, although

this will slow down during the forecast period

33. Forecast methodology and assumptions

34. Geographical scope: forecasts are provided for 64 countries in 8 regions

35. Definitions

36. We take baseline costs for each technology and then apply several context-

specific variables to determine total capexTop-level breakdown of the

relative costs of FTTx technologies: basic topologies

37. Top-level breakdown of the relative costs of FTTx technologies: basic

topologies

3

Contents [1/2]

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

38. About the author and Analysys Mason

39. About the author

40. Analysys Mason’s consulting and research are uniquely positioned

41. Research from Analysys Mason

42. Consulting from Analysys Mason

4

Contents [2/2]

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Figure 1: FTTx capex, by worldwide region, 2015–2025

Figure 2: NGA coverage by technology, worldwide, 2015–2025

Figure 3: Percentage of premises covered by gigabit-capable networks,

Western Europe, 2019 and 2025

Figure 4: Percentage of premises covered by gigabit-capable networks, Central

and Eastern Europe, 2019 and 2025

Figure 5: Percentage of premises covered by gigabit-capable networks, North

America and developed Asia–Pacific, 2019 and 2025

Figure 6: Incumbent operators’ maximum year-on-year percentage point

increases in FTTP coverage, as a percentage of total premises passed, selected

countries

Figure 7: Incumbent operators’ maximum year-on-year percentage point

increases in FTTP coverage, as a percentage of total premises passed, selected

countries

Figure 8: FTTP coverage of total premises, by selected counties in emerging

markets, 2019 and 2025

Figure 9: NGA coverage by technology, Western Europe, 2017–2025

Figure 10: FTTx capex by technology, Western Europe, 2017–2025

Figure 11: NGA coverage by technology, Central and Eastern Europe, 2017–

2025

Figure 12: FTTx capex by technology, Central and Eastern Europe, 2017–2025

Figure 13: NGA coverage by technology, Middle East and North Africa, 2017–

2025

Figure 14: FTTx capex by technology, Middle East and North Africa, 2017–

2025

Figure 15: NGA coverage by technology, Sub-Saharan Africa, 2017–2025

Figure 16: FTTx capex by technology, Sub-Saharan Africa, 2017–2025

Figure 17: NGA coverage by technology, China, 2017–2025

Figure 18: FTTx capex by technology, China, 2017–2025

Figure 19: NGA coverage by technology, emerging Asia–Pacific excluding China,

2017–2025

Figure 20: FTTx capex by technology, emerging Asia–Pacific excluding China,

2017–2025

Figure 21: NGA coverage by technology, developed Asia–Pacific, 2017–2025

Figure 22: FTTx capex by technology, developed Asia–Pacific, 2017–2025

Figure 23: NGA coverage by technology, North America, 2017–2025

Figure 24: FTTx capex by technology, North America, 2017–2025

Figure 25: NGA coverage by technology, Latin America, 2017–2025

Figure 26: FTTx capex by technology, Latin America, 2017–2025

Figure 27: Countries covered in this report, by region

Figure 28: Definitions used in this report

Figure 29: Capex model outline

Figure 30: Basic overview of FTTx network topologies and elements

5

List of figures

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Contents Worldwide trends

Regional trends

Western Europe

Central and Eastern Europe

Middle East and North Africa

Sub-Saharan Africa

China

Rest of emerging Asia-Pacific

Developed Asia-Pacific

North America

Latin America

Forecast methodology and assumptions

About the author and Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

We estimate that global FTTx capex peaked in 2019.

FTTx coverage in China reached 96% of premises at the end of

2019 and there is limited scope to extend the number of new

premises passed in China. As the expansion of network coverage

in China slows, network capex will decline.

Capex in the rest of the EMAP region (excluding China) will peak in

2020. Roll-outs in markets such as India and Indonesia will be a

significant driver of high capex in the early part of the forecast

period. We expect 50% of premises in the rest of EMAP to be

passed with NGA infrastructure by the end of 2025, up from 21%

at the end of 2019. This growth reflects the confidence that has

been generated as a result of robust subscriber take-up of NGA

roll-outs in many emerging markets.

Western Europe’s share of global FTTx capex will grow from 24%

in 2019 to 47% in 2025, driven in part because there is room to

increase FTTP coverage in France, Germany and the UK.

Furthermore, many alternative operators are just starting to roll

out FTTP in Western Europe; this, together with a generally slower

rate of roll-out in the region, means that capex will still be spent

on these deployments, even in 2025. FTTx capex in North

America will remain steady towards the end of the forecast

period, and in 2025, the region will have the second-highest

share of overall global FTTx capex. Developed markets have much

higher FTTP costs per premises passed and connected, which

means they have a greater impact on the global capex figures.

Figure 1: FTTx capex, by worldwide region, 2015–2025

0

10

20

30

40

50

60

70

80

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Ca

pe

x (

US

D b

illio

n)

WE CEE NA DVAP China Rest of EMAP MENA LATAM SSA

Source: Analysys Mason

7

We forecast that 2019 was the peak year for global FTTx capex worldwide

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

We forecast that NGA coverage of premises as a percentage of

overall global premises will rise from 55.2% at the end of 2019 to

65% at the end of 2025.

We have increased our end-of-year 2025 NGA coverage figure by

3.4 percentage points compared with our forecasts from last year,

partly because we are more confident of further NGA roll-outs in

the EMAP region (excluding China). Compared with last year, our

forecasts for NGA coverage in India for the end of 2025 are higher

by around 59 million premises, equivalent to around 2.5% of total

global premises. We have increased our year-end 2025 NGA

coverage figure for Indonesia by around 25 million premises – or

around 1% of the global total.

The percentage of global premises covered by NGA but not by

FTTP will fall from 17.5% at the end of 2019 to 12.4% by the end

of 2025. This reflects the increasing momentum behind FTTC/B

to FTTP migration in Western Europe and North America. Global

FTTC coverage will decline from 11.7% at the end of 2019 to

10.2% at the end of 2025. Challenger FTTP operators, particularly

in Western Europe, will also increase their coverage and move

into the areas previously only covered by FTTC and FTTB.

Nevertheless, we do not expect any decline in the percentage of

cable premises passed because there are no signs of large-scale

migrations of DOCSIS networks to FTTP. DOCSIS 4.0 promises

further increases in capacity, and the ability to use all frequencies

for both downstream and upstream transmission negates the

disadvantages that cable traditionally had with upstream speeds.

Figure 2: NGA coverage by technology, worldwide, 2015–2025

0%

10%

20%

30%

40%

50%

60%

70%

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

NG

A c

ove

rage

of

pre

mis

es

FTTP FTTx, but not FTTP Cable, but not FTTx

Source: Analysys Mason

8

FTTP will increase its dominance of the global NGA landscape during the forecast

period

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Policymakers are placing increasing emphasis on ensuring that

NGA broadband coverage meets the targets set for higher speeds.

Targets set by the European Union’s Gigabit Society state that by

the end of 2025 all households should have access to networks

with download speeds of at least 100Mbit/s, which can be

upgraded to 1Gbit/s.

Cable networks have an important role to play in meeting gigabit

coverage targets.

Cable networks can provide gigabit downstream speeds, but such

speeds are not always made available in current retail offers. In

the USA, Comcast offered gigabit speeds across almost all of its

footprint as of October 2018, thanks to its roll-out of DOCSIS 3.1.

In the larger countries within Western Europe, maximum cable

download speeds of 300–500Mbit/s are common. However,

Vodafone Germany has deployed DOCSIS 3.1 and offers gigabit

speeds. Cable operators in Western Europe that do not offer

gigabit speeds could easily upgrade their networks to do so.

Copper networks will struggle in even the most-favourable of

circumstances to offer gigabit downstream speeds.

It is unclear whether copper networks can offer gigabit

downstream speeds. VDSL35b supervectoring falls far short and

Telekom Deutschland offers maximum download speeds with

VDSL35b of only 250Mbit/s. While aggregate downstream and

upstream speeds of around 1Gbit/s are possible with G.fast,

106MHz downstream speeds would be below 1Gbit/s.

BT’s FTTC-based G.fast roll-out offers download speeds of

300Mbit/s, and Swisscom’s FTTdp G.fast roll-out provides

downstream speeds of 500Mbit/s. Depending on the

circumstances, even G.fast that uses 212MHz may not deliver

gigabit downstream speeds. For example, this may be the case if

operators have to start G.fast at 19MHz because VDSL2 17MHz is

being used in the same binder.

G.mgfast aims to provide aggregate downstream and upstream

bitrates of 10Gbit/s over in-building copper and coaxial cabling by

using frequencies up to 424MHz or 848 MHz The first volume of

the recommendation for the G.mgfast ITU project was scheduled

to be completed in January 2020. However, we exclude G.mgfast

from our gigabit-capable forecasts because standardisation is

incomplete and it is not clear if it is commercially viable.

5G fixed-wireless access may also struggle to meet the criteria of

upgradability to 1Gbit/s speeds.

Given current benchmarks, 5G fixed-wireless in mid-band

spectrum will struggle to go much beyond speeds in the low

hundreds of Mbit/s. There also appears to be limited interest in

5G mmWave deployments in Western Europe currently. The cost

advantage of fixed-wireless roll-outs rapidly erode with mmWave.

which severely limits deployment incentives. In any case, it is not

clear that such roll-outs can achieve 1Gbit/s speeds. Verizon is

using 400MHz of spectrum but still only promises typical

download speeds of 300Mbit/s.

9

FTTP and cable networks are the only viable options for meeting coverage targets

for gigabit-capable broadband

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Current investment plans indicate that most countries in Western

Europe will fall far short of meeting the Gigabit Society’s target to

provide nationwide coverage for networks that can be upgraded

to 1Gbit/s.

By the end of 2019 in most countries in Western Europe,

households with DOCSIS cable coverage accounted for the largest

percentage of all households covered by networks that could be

upgraded to 1Gbit/s. Significantly, the two countries in Western

Europe with the lowest coverage of networks capable of being

upgraded to gigabit speeds are Greece and Italy, both of which

are unusual in that they do not have any DOCSIS cable networks.

Even during the forecast period, DOCSIS cable coverage will

continue to be important in determining the coverage of networks

that can be upgraded to 1Gbit/s. This is partly because

incumbents want to upgrade to FTTP to address competition from

cable operators. Cable operator coverage is focused on major

urban areas and these are also the cheapest areas for FTTP roll-

outs.

Nevertheless, there will be cases of FTTP roll-outs in more-rural

areas which will extend the coverage of gigabit-capable networks.

FTTP will be rolled out nationwide in Portugal and Spain, which

will enable the Gigabit Society’s targets to be met under current

roll-out plans.

Figure 3: Percentage of premises covered by gigabit-capable

networks, Western Europe, 2019 and 2025

10

Roll-out plans in most countries in Western Europe currently miss the Gigabit

Society’s targets by some margin

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Gre

ece

Ita

ly

UK

Ire

lan

d

Fra

nc

e

Au

str

ia

Ge

rma

ny

Fin

lan

d

De

nm

ark

Icela

nd

Sw

itze

rla

nd

Sp

ain

No

rwa

y

Sw

ed

en

Ne

the

rla

nd

s

Po

rtu

ga

l

Be

lgiu

m

Pe

rce

nta

ge

of

pre

mis

es p

asse

d b

y gig

ab

it-c

ap

ab

le n

etw

ork

s

2019 2025

Source: Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

In Central and Eastern Europe, much work is required to meet the EU’s Gigabit

Society’s targets

In some Western European countries, national broadband plans

will underpin changes to coverage of gigabit-capable broadband

networks between the end of 2019 and the end of 2025. For

example, the Irish National Broadband Plan will help to drive up

gigabit-capable broadband coverage in Ireland from 55% at the

end of 2019 to 95% at the end of 2025.

In most countries in Central and Eastern Europe, only modest

progress will be made towards meeting the Gigabit Society’s

targets. Incumbents in some markets, such as the Baltic countries

and Bulgaria, have focused on expanding NGA coverage with VDSL.

Rural FTTP deployments will be less common, but some are

emerging, for example, in Romania, Estonia, Croatia and Slovenia.

Gigabit-capable broadband coverage in other developed markets

is noteworthy. In the USA and Canada, gigabit cable speeds are

already available and gigabit coverage is therefore high. Fixed

wireless rollouts will be used to extend coverage in Canada but

these networks will not be gigabit capable. In developed Asia–

Pacific, the government-backed UFB FTTP roll-outs in New

Zealand will increase gigabit coverage to 91.6% by the end of

2025. In Australia, the multi-technology mix selected for the NBN

roll-out will mean that gigabit-capable coverage will reach 51.5%

of households at the end of 2025. We are sceptical that copper

technologies will offer gigabit downstream speeds. For example,

in Japan, KDDI’s FTTB-G.fast 106MHz roll-out promises only

aggregate downstream and upstream speeds of 830Mbit/s.

Figure 4: Percentage of premises covered by gigabit-capable

networks, Central and Eastern Europe, 2019 and 2025

0%

20%

40%

60%

80%

100%

Tu

rke

y

Cro

ati

a

Uk

rain

e

Slo

va

kia

Esto

nia

Cze

ch

ia

Po

lan

d

Slo

ve

nia

Se

rbia

La

tvia

Lit

hu

an

ia

Bu

lga

ria

Ru

ssia

Ro

ma

nia

Hu

ng

aryP

erc

en

tage

of

pre

mis

es

pa

sse

d b

y gig

ab

it-

ca

pa

ble

ne

two

rks

2019 2025

Source: Analysys Mason

Figure 5: Percentage of premises covered by gigabit-capable

networks, North America and developed Asia–Pacific, 2019

and 2025

0%

20%

40%

60%

80%

100%

Au

str

alia

Ta

iwa

n

Ne

w Z

ea

lan

d

Jap

an

Ca

na

da

US

A

So

uth

Ko

rea

Sin

ga

po

re

Pe

rce

nta

ge

of

pre

mis

es

pa

sse

d b

y gig

ab

it-

ca

pa

ble

ne

two

rks

2019 2025

Source: Analysys Mason

11

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

The rate at which FTTP can be built out depends on the existing level of usable

infrastructure, but regulation can help to speed up roll-outs

FTTP build run rate is a topical issue in Western Europe. This is

partly due to government pressure, as well as objectives for fibre

broadband coverage. This also reflects the desire of each

country’s incumbent to head off the threat posed by challenger

operators by being the first to deploy FTTP in a particular area. In

Western Europe, Spain’s incumbent accounts for the highest

proportion of premises passed by any regional incumbent in a

single year – at 19.5% in 2014. FTTP coverage in Portugal also

grew by 15.5% in 2015. In the UK, Openreach noted that as of

January 2020 it passed around 26 000 premises per week with

fibre, and is aiming to reach 30 000 premises passed by the end

of March 2020, which equates to just 5% of all UK premises

passed in a single year.

Availability of civil infrastructure for FTTP roll-out

Operators in Spain and Portugal benefited from the availability of

good-quality, usable duct infrastructure. However, not all incumbents

in Western Europe (including in Germany, Belgium, the

Netherlands and Italy) have ducted networks between exchanges

and subscribers’ homes; instead, copper lines are directly buried.

MDU penetration and regulation

In Spain and Portugal, the high penetration of multiple dwelling

units (MDUs) has encouraged the rapid roll-out of FTTP.

Regulations in Spain also require property owners to allow fibre

deployments within the MDU or on the building facade. In the UK,

access to MDUs has been more challenging.

Figure 6: Incumbent operators’ maximum year-on-year

percentage point increases in FTTP coverage, as a percentage

of total premises passed, selected countries

4.0%

7.5%

8.5%

18.4%

19.3%

0% 5% 10% 15% 20% 25%

Openreach, UK, 2019

Orange, France, 2019

Incumbents, Canada, 2018

Meo, Portugal, 2017

Movistar, Spain, 2014

Percentage of premises

Source: Analysys Mason

12

The UK government’s UK Telecommunications Infrastructure

(Leasehold Property) Bill is currently being read in parliament.

This legislation seeks to address concerns that 40% of landlords

do not respond to requests for access to their buildings. The

legislation aims to provide operators with a less-costly and a

more-rapid legal process to use if they do not receive co-operation

from building owners for infrastructure roll-out.

Finally, new build properties in the UK are not currently required

to incorporate gigabit internet connections, but the government

intends to introduce legislation to address this.

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

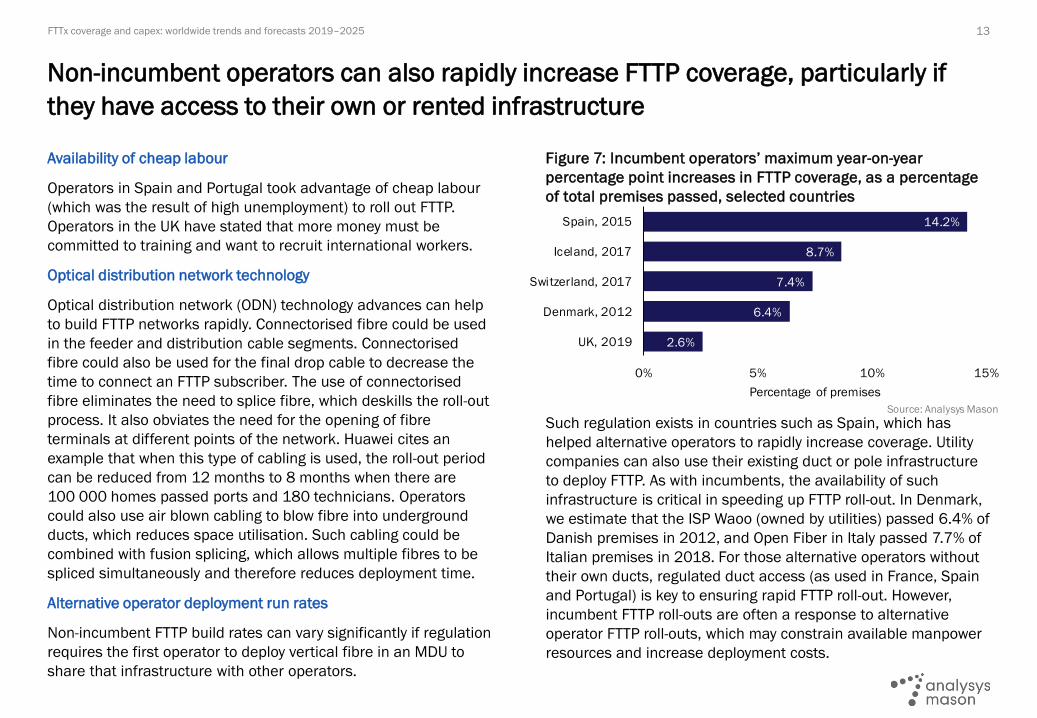

Non-incumbent operators can also rapidly increase FTTP coverage, particularly if

they have access to their own or rented infrastructure

Availability of cheap labour

Operators in Spain and Portugal took advantage of cheap labour

(which was the result of high unemployment) to roll out FTTP.

Operators in the UK have stated that more money must be

committed to training and want to recruit international workers.

Optical distribution network technology

Optical distribution network (ODN) technology advances can help

to build FTTP networks rapidly. Connectorised fibre could be used

in the feeder and distribution cable segments. Connectorised

fibre could also be used for the final drop cable to decrease the

time to connect an FTTP subscriber. The use of connectorised

fibre eliminates the need to splice fibre, which deskills the roll-out

process. It also obviates the need for the opening of fibre

terminals at different points of the network. Huawei cites an

example that when this type of cabling is used, the roll-out period

can be reduced from 12 months to 8 months when there are

100 000 homes passed ports and 180 technicians. Operators

could also use air blown cabling to blow fibre into underground

ducts, which reduces space utilisation. Such cabling could be

combined with fusion splicing, which allows multiple fibres to be

spliced simultaneously and therefore reduces deployment time.

Alternative operator deployment run rates

Non-incumbent FTTP build rates can vary significantly if regulation

requires the first operator to deploy vertical fibre in an MDU to

share that infrastructure with other operators.

Figure 7: Incumbent operators’ maximum year-on-year

percentage point increases in FTTP coverage, as a percentage

of total premises passed, selected countries

2.6%

6.4%

7.4%

8.7%

14.2%

0% 5% 10% 15%

UK, 2019

Denmark, 2012

Switzerland, 2017

Iceland, 2017

Spain, 2015

Percentage of premises

Source: Analysys Mason

13

Such regulation exists in countries such as Spain, which has

helped alternative operators to rapidly increase coverage. Utility

companies can also use their existing duct or pole infrastructure

to deploy FTTP. As with incumbents, the availability of such

infrastructure is critical in speeding up FTTP roll-out. In Denmark,

we estimate that the ISP Waoo (owned by utilities) passed 6.4% of

Danish premises in 2012, and Open Fiber in Italy passed 7.7% of

Italian premises in 2018. For those alternative operators without

their own ducts, regulated duct access (as used in France, Spain

and Portugal) is key to ensuring rapid FTTP roll-out. However,

incumbent FTTP roll-outs are often a response to alternative

operator FTTP roll-outs, which may constrain available manpower

resources and increase deployment costs.

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

There are opportunities for FTTP vendors to benefit from significant coverage

increases in some, but not all, large emerging markets

Total FTTP coverage levels vary significantly between countries in

the world’s largest emerging markets (in terms of population). In

Vietnam, for example, FTTP coverage reached 68.2% at the end of

2019 compared with just 0.2% in Nigeria. The countries in large

emerging markets that today have the highest FTTP coverage

levels, namely Vietnam and China (although it is a matter of

debate whether China is an emerging market), have achieved this

status through state-directed investment. Governments either

fully or partly own fixed incumbents and have set objectives for

increasing fibre coverage.

We expect some levelling up of FTTP coverage levels across the

largest countries in emerging markets during the forecast period.

The drivers for this trend are largely commercial as operators see

opportunities to deliver a rapid return on investment. The threat

of new entrants will also encourage heavy incumbent investment

in some markets. In Indonesia, we expect Telekom Indonesia to

significantly expand its fibre coverage because it has seen much

improved take-up rates for its IndiHome retail proposition. In the

Philippines, the ambitious expansion plans of Converge ICT will

drive FTTP coverage expansion and force incumbent PLDT to roll

out FTTP with increased vigour. There is also considerable interest

from commercial investors in expanding FTTP coverage in Brazil.

There is a trend towards consolidation and expansion among

regional Brazilian FTTP providers and incumbent Oi is investing

heavily in expanding its FTTP coverage as it seeks to secure its

future place in the fixed broadband landscape.

Figure 8: FTTP coverage of total premises by selected counties

in emerging markets, 2019 and 2025

0%

20%

40%

60%

80%

100%

Nig

eri

a

Eg

ypt

Ind

ia

So

uth

Afr

ica

Me

xic

o

Ph

ilip

pin

es

Bra

zil

Ind

on

esia

Vie

tna

m

Pe

rce

nta

ge

of

pre

mis

es

pa

sse

d b

y F

TTP

2019 2025

Source: Analysys Mason

14

However, in other markets, obstacles will prevent significant

expansion of FTTP coverage. In Nigeria and South Africa, fixed

broadband affordability is a significant challenge. In Nigeria, the

availability of broader infrastructure such as backbone and metro

fibre networks will constrain the growth of FTTP coverage. In Sub-

Saharan Africa, right-of-way challenges also limit FTTP roll-outs. In

Mexico, incumbent Telmex has been slow to deploy NGA and we

forecast that it will continue to rely partly on FTTC-VDSL, even by

the end of 2025. This will also be the case in Egypt where the

government owns an 80% share in the incumbent, which has

deployed a nationwide FTTC network and is due to make some

upgrades to FTTP in the forecast period while keeping most of its

FTTC roll-out intact.

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Contents Worldwide trends

Regional trends

Western Europe

Central and Eastern Europe

Middle East and North Africa

Sub-Saharan Africa

China

Rest of emerging Asia-Pacific

Developed Asia-Pacific

North America

Latin America

Forecast methodology and assumptions

About the author and Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

We forecast strong levels of investment in FTTP networks in Western Europe

throughout the forecast period

Fragmentation is the dominant trend for fibre deployments in

Western Europe as new players emerge and mixed ownership

becomes more commonplace.

Across Western Europe, there is a growing emphasis on

wholesale-only FTTP challengers whose backers often include

energy companies such as those in Ireland (SIRO), Iceland

(Gagnaveita), Italy (Open Fiber) and Switzerland (Swiss Fibre Net).

Many of the networks in these countries have been able to attract

sizeable operators as wholesale clients. For example, Open Fiber

has agreements with Vodafone, WIND Tre, Fastweb and Sky Italia,

which bodes well for the overall prospects of the deployment.

There has also been a wave of incumbent FTTP infrastructure

carve-outs. This reflects incumbents’ desires to maximise

wholesale subscriber growth and limit the threat from the new

breed of wholesale-only competitors, while allowing more capex to

be spent on a more-rapid FTTP roll-out.

The momentum behind FTTC-to-FTTP migration is increasing in

Western Europe. In the UK, the threat posed by the new breed of

FTTP challengers explains Openreach’s increased focus on full

fibre. This increased emphasis is also explained by growing

government pressure. One significant exception to this rule is

Germany, where the absence of ducts in the access network

pushes up the costs of full FTTP considerably and helps to explain

the incumbent’s continuing focus on VDSL35b, at least in the

short term.

Figure 9: NGA coverage by technology, Western Europe, 2017–

2025

Figure 10: FTTx capex by technology, Western Europe, 2017–

2025

16

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Pe

rce

nta

ge

of

pre

mis

es p

assse

d

Cable, but not FTTx

FTTx, but not FTTP

FTTP

Source: Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Contents Worldwide trends

Regional trends

Western Europe

Central and Eastern Europe

Middle East and North Africa

Sub-Saharan Africa

China

Rest of emerging Asia-Pacific

Developed Asia-Pacific

North America

Latin America

Forecast methodology and assumptions

About the author and Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

The number of non-incumbent FTTP deployments in rural areas in Central and

Eastern Europe is growing, but not dramatically

The NGA market in CEE has not changed dramatically over the

last year.

Incumbent operators in CEE have shown little additional

inclination to roll out FTTP during the last year. CETIN in Czechia is

an exception to this and the operator plans to roll out FTTP to

1 million premises (or 18% of all premises in the country) in the

next 7 years. Reticence from incumbents to deploy further FTTP is

partly explained by the fact that there may be some moves

towards using 5G fixed-wireless, for instance, in Poland.

There is little ongoing non-incumbent FTTP deployment in major

urban areas. This is because many such areas have long been

covered by FTTB+LAN players and/or cable networks, which

overlap in some cities in individual countries (such as in Warsaw,

Poland). Orange in Romania is an exception: its FTTP deployment

was launched at the end of 2019, perhaps spurred by MNO

Vodafone’s acquisition of Liberty Global’s Romanian cable assets,

which could lead to more pressure on standalone MNOs.

We noted in last year’s forecast report an emphasis on extending

NGA coverage to rural areas, and this continues to be important.

In Slovenia, the RUNE project will cover 233 000 premises

(around 22% of all premises) over the next 3 years. RUNE Group

is also rolling out FTTP in rural Croatia. National broadband plans,

such as those in Poland, can help to drive FTTP coverage in more-

rural areas. In Estonia, electricity company Elektrilevi is rolling out

FTTP in rural areas with some help from public funding.

Figure 11: NGA coverage by technology, Central and Eastern

Europe, 2017–2025

Figure 12: FTTx capex by technology, Central and Eastern

Europe, 2017–2025

18

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Contents Worldwide trends

Regional trends

Western Europe

Central and Eastern Europe

Middle East and North Africa

Sub-Saharan Africa

China

Rest of emerging Asia-Pacific

Developed Asia-Pacific

North America

Latin America

Forecast methodology and assumptions

About the author and Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Government intervention is driving an increase in fibre coverage in the Middle East

and North Africa, and the focus on wholesale access in the region is increasing

The number of networks that offer wholesale access has been

increasing in the MENA region.

FTTP has been deployed nationwide by vertically integrated

incumbents in the United Arab Emirates (UAE) and Qatar, the

most-advanced countries in the Gulf region. Next-generation PON

has not yet been deployed in these countries, and for both

Etisalat in the UAE and Ooredoo in Qatar, the maximum speed

offered is only 1Gbit/s. Despite this, Etisalat in the UAE increased

entry-level FTTP speeds from 20Mbit/s to 250Mbit/s in 2019,

and Ooredoo in Qatar increased its entry-level speeds from

15Mbit/s to 50Mbit/s at the same time.

Investment in FTTP is increasing in other Gulf region and North

African markets. This is often driven by government pressure and,

as a result, more operators are offering wholesale access or are

operating purely as wholesale players. In Bahrain, Batelco has

structurally separated into a retail division and networks division

(BNET) and the National Broadband Network is set to cover 95%

of households with FTTP by the end of 2019. BNET will offer

wholesale access on equal terms to all operators. In Saudi Arabia,

the Saudi Electricity Company has received SAR1.56 billion

(USD0.4 billion) to roll out FTTP to 10% of premises by 2020.

Incumbent STC has also received government funding to deploy

FTTP to 1.3 million premises by the end of 2020. In Egypt,

government-backed incumbent Telecom Egypt is also offering

wholesale access and has largely completed its nationwide FTTC-

VDSL roll-out. It is also deploying FTTP and aims to cover 2 million

premises (7% of all premises).

Figure 13: NGA coverage by technology, Middle East and North

Africa, 2017–2025

Figure 14: FTTx capex by technology, Middle East and North

Africa, 2017–2025

20

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Contents Worldwide trends

Regional trends

Western Europe

Central and Eastern Europe

Middle East and North Africa

Sub-Saharan Africa

China

Rest of emerging Asia-Pacific

Developed Asia-Pacific

North America

Latin America

Forecast methodology and assumptions

About the author and Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

NGA coverage in Sub-Saharan Africa is constrained by affordability, the high cost of

deployment and the lack of availability of fibre backbone infrastructure

We forecast that by the end of 2025, NGA coverage will be well

below 10% of all premises in all countries that we provide

individual forecasts for, with the exception of South Africa.

Challenges remain around the affordability of fixed broadband in

SSA. The proportion of income spent on mobile is much higher in

this region than in other regions and constrains the ability to

spend on fixed broadband. In South Africa, Vumatel is trying to

assuage concerns about affordability by launching prepaid FTTP

offers. These offers reduce the barriers to subscribing by

eliminating installation charges. Vumatel has passed around

600 000 premises and its expansion into lower-income markets

with its prepaid offer could mean that it passes another 700 000

premises, equivalent to around 4% of all premises in the country.

Infrastructure and cost present further challenges in Sub-

Saharan Africa. The absence of fibre backbone infrastructure

hinders the roll-out of FTTP and the cost of such access network

deployments is likely to be higher than in other emerging market

regions. This helps to explain why some operators are moving

towards deploying fixed-wireless access. For example, Airtel in

Nigeria launched 4G fixed-wireless access in more than 130

towns and cities in August 2019. In South Africa, FTTP costs per

home passed and connected are both particularly high. This helps

explain why Rain in South Africa was one of the first operators in

the world to launch 5G fixed-wireless. Right-of-way issues also

severely hinder FTTP roll-outs in the SSA region.

Figure 15: NGA coverage by technology, Sub-Saharan Africa,

2017–2025

Figure 16: FTTx capex by technology, Sub-Saharan Africa,

2017–2025

22

0.0

0.1

0.1

0.2

0.2

0.3

0.3

0.4

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

FTTx c

ap

ex (

US

D b

illio

n)

Other FTTx

FTTP

Source: Analysys Mason

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Pe

rce

nta

ge

of

pre

mis

es p

assse

d

Cable, but not FTTx

FTTx, but not FTTP

FTTP

Source: Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Contents Worldwide trends

Regional trends

Western Europe

Central and Eastern Europe

Middle East and North Africa

Sub-Saharan Africa

China

Rest of emerging Asia-Pacific

Developed Asia-Pacific

North America

Latin America

Forecast methodology and assumptions

About the author and Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

FTTP coverage is already very high in China and the focus has shifted to upgrading

to next-generation PON

There is little scope for further expansion of FTTP coverage in

China. We have therefore not altered our forecast from last year

that 96% of the country’s premises will be passed by the end of

2025.

However, the total FTTP coverage figure obscures the fact that we

forecast that China Mobile will continue to increase its FTTP

coverage: the company planned to reach 70% of households with

fibre by the end of 2017 and we estimate that total non-

incumbent FTTP coverage will reach 90% of premises by the end

of 2025.

We also estimate that upgrades of all legacy FTTx deployments to

FTTP will be complete by the end of 2021. An indication of the

near-completion of the migration to FTTP is that 96% of China

Telecom’s fixed broadband subscribers took FTTP by the end of

2018, compared with 86% 2 years earlier.

There is greater activity around expanding gigabit coverage and

extending next-generation PON deployments. China Mobile has

been deploying 10 GPON in Shanghai and it is estimated that by

the end of 3Q 2019, gigabit broadband coverage had been

extended to all of the administrative districts in the city. China

Telecom also completed a city-wide deployment in Shanghai of 10

GPON in October 2018 for a reported cost of USD144 million. By

mid-2019 China Telecom stated that 180 cities were gigabit-

enabled although this did not represent an increase from the end

of 2018.

Figure 17: NGA coverage by technology, China, 2017–2025

Figure 18: FTTx capex by technology, China, 2017–2025

24

75%

80%

85%

90%

95%

100%

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Pe

rce

nta

ge

of

pre

mis

es p

assse

d

Cable, but not FTTx

FTTx, but not FTTP

FTTP

Source: Analysys Mason

0

2

4

6

8

10

12

14

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

FTTx c

ap

ex (

US

D b

illio

n)

Other FTTx

FTTP

Source: Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Contents Worldwide trends

Regional trends

Western Europe

Central and Eastern Europe

Middle East and North Africa

Sub-Saharan Africa

China

Rest of emerging Asia-Pacific

Developed Asia-Pacific

North America

Latin America

Forecast methodology and assumptions

About the author and Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

The number of FTTP deployments in several countries in the EMAP region increased

in 2019 and this momentum will continue

We have adjusted our forecast figures from last year, and now

forecast that fibre coverage will increase more rapidly in a

number of countries in emerging Asia–Pacific (excluding China).

Telkom Indonesia had already passed 30 million premises with

FTTx at the end of 2018, and we estimate that its FTTP coverage

will reach 62 million premises by the end of 2025, equivalent to

66% of all premises in Indonesia. Strong take-up from existing

deployments and relatively low fibre coverage help to explain the

forecasted increase in coverage.

We have increased our end-of-year 2025 NGA coverage for the

Philippines to 66% (it was 50% in last year’s forecast). This is

because the challenger Converge ICT has received further financial

backing for its ambitious FTTP roll-out plans. Competition from

Converge ICT will also spur incumbent PLDT to deploy more FTTP.

We have also adjusted our forecast upwards for fibre coverage in

Malaysia due to the impact of government funding for fibre roll-

out in the form of the National Fiberisation and Connectivity Plan.

We estimate that NGA coverage will reach 78% of all premises by

the end of 2025. The remaining premises are in rural areas,

where the costs of roll-out are much higher and where 5G fixed-

wireless coverage is an option.

We also expect more-extensive FTTP roll-outs in India compared

with last year. Reliance Jio is aiming to pass 75 million premises

with FTTP by the end of 2022 and 35 million premises in its first

year of operating the network.

Figure 19: NGA coverage by technology, emerging Asia–Pacific

excluding China, 2017–2025

Figure 20: FTTx capex by technology, emerging Asia–Pacific

excluding China, 2017–2025

26

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Pe

rce

nta

ge

of

pre

mis

es p

assse

d

Cable, but not FTTx

FTTx, but not FTTP

FTTP

Source: Analysys Mason

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

FTTx c

ap

ex (

US

D b

illio

nOther FTTx

FTTP

Source: Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Contents Worldwide trends

Regional trends

Western Europe

Central and Eastern Europe

Middle East and North Africa

Sub-Saharan Africa

China

Rest of emerging Asia-Pacific

Developed Asia-Pacific

North America

Latin America

Forecast methodology and assumptions

About the author and Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Several drivers explain the growth in the number of next-generation PON

deployments in developed Asia–Pacific

NGA coverage is already high in most countries in developed

Asia–Pacific; government-backed roll-outs in New Zealand and

Australia are closing the gap with the rest of the region.

In New Zealand and Australia, NGA coverage reached 86% and

91% of all premises, respectively, at the end of 2019. This reflects

strong progress with the UFB initiatives in New Zealand and the

NBN roll-out in Australia.

The number of deployments of next-generation PON deployments

is higher in DVAP than any other region. In Singapore, the

availability of passive FTTP unbundling encouraged active

operators (which are also retailers) to roll out 10GPON (XGPON1)

some years ago in order to remain competitive. This strategy may

be replicated in New Zealand where Vodafone and Vocus have

expressed interest in using PON unbundling offers. In turn, this

has encouraged Chorus to roll out XGSPON from 2020 onwards.

In other markets in DVAP, competition from non-incumbent

infrastructures can encourage next-generation PON deployments.

For example, competition from HKBN was a driver for Hong Kong

incumbent HKT’s early deployment of XGPON1. In South Korea,

operators have had success in boosting ARPU with gigabit offers

and are looking to reproduce this with multi-gigabit access,

enabled by upgrades to next-generation PON technologies

(XGSPON for SK Telecom and 10GEPON for Korea Telecom). In

South Korea and elsewhere, the higher speeds enabled by next-

generation PON technologies can also avert any substitution

threat posed by the launch of 5G.

Figure 21: NGA coverage by technology, developed Asia–Pacific,

2017–2025

Figure 22: FTTx capex by technology, developed Asia–Pacific,

2017–2025

28

0%10%20%30%40%50%60%70%80%90%

100%

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Pe

rce

nta

ge

of

pre

mis

es p

assse

d

Cable, but not FTTx

FTTx, but not FTTP

FTTP

Source: Analysys Mason

0.00.5

1.01.52.02.53.03.54.04.55.0

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

FTTx c

ap

ex (

US

D b

illio

nOther FTTx

FTTP

Source: Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Contents Worldwide trends

Regional trends

Western Europe

Central and Eastern Europe

Middle East and North Africa

Sub-Saharan Africa

China

Rest of emerging Asia-Pacific

Developed Asia-Pacific

North America

Latin America

Forecast methodology and assumptions

About the author and Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

The number of new fibre entrants in North America is far fewer than in Western

Europe

Relatively few announcements have been made in the last year

about new major wireline infrastructure projects in North America.

Incumbent operators in North America have more incentive to use

fixed-wireless to complement fibre than their counterparts in

Europe. In Canada, Bell intends to cover 1 million hard-to-reach

premises (6% of all premises in the country) with 4G fixed-

wireless using spectrum in the 3.5GHz band. In addition, rather

than focusing on using FTTP to expand coverage beyond its

franchise area, Verizon is using 5G mmWave fixed-wireless. Little

progress has been made on this deployment in the last year and

the 5G Home service is still only available in certain areas within

five cities. FTTP costs per home passed and connected are

significantly higher for both Bell and Verizon than is the case for

operators in most of Western Europe, which helps to explain the

choice of fixed-wireless. The high cost of FTTP deployment also

helps to explain why there has been an absence of third wireline

infrastructure deployments to compete with those of incumbents

and near-ubiquitous cable networks.

AT&T is also reducing investment after completing the tranche of

fibre roll-out required by the FCC as part of the approval for

AT&T’s acquisition of pay-TV provider DirecTV.

Migration from FTTC-VDSL to FTTP continues in North America. In

Canada, we estimate that FTTC-VDSL covered 45% of all premises

at the end of 2017. This figure had fallen to 33% at the end of

2019 due to overbuilds of FTTC with FTTP conducted by Telus and

Bell.

Figure 23: NGA coverage by technology, North America, 2017–

2025

Figure 24: FTTx capex by technology, North America, 2017–

2025

30

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Pe

rce

nta

ge

of

pre

mis

es p

assse

d

Cable, but not FTTx

FTTx, but not FTTP

FTTP

Source: Analysys Mason

0

2

4

6

8

10

12

14

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

FTTx c

ap

ex (

US

D b

illio

nOther FTTx

FTTP

Source: Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Contents Worldwide trends

Regional trends

Western Europe

Central and Eastern Europe

Middle East and North Africa

Sub-Saharan Africa

China

Rest of emerging Asia-Pacific

Developed Asia-Pacific

North America

Latin America

Forecast methodology and assumptions

About the author and Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Investment in FTTx networks in LATAM continues to be strong, although this will slow

down during the forecast period

We expect that by the end of 2025, total NGA coverage will reach

60–75% of all premises in all the countries in LATAM that we

provide individual forecasts for (with the exception of Uruguay).

Incumbents in the LATAM region continue to announce FTTP

coverage expansion plans. Oi in Brazil is a prominent example of

this: it intends to cover 16 million premises (or 23%) of the

country’s premises by the end of 2021. This roll-out is being

funded partly through Oi’s divestment of non-core assets,

including its Angolan subsidiary. Oi’s deployments of FTTP have

previously lagged behind those of other operators in Brazil and it

has faced a strong threat to its existing broadband business from

Telefónica, cable operator NET Servicos and new fibre entrants.

Investment from non-incumbent operators, typically MNOs or

other third parties, has increased. Examples of this include

Claro’s FTTP deployment in Peru, which adds to the FTTP

deployment of fellow MNO Bitel. These roll-outs are more focused

on underserved inland areas. In Brazil, towerco American Tower

has a partnership with Vivo whereby American Tower will provide

the investment and construct and manage the fibre network and

Vivo will offer services to end users and supply the CPE. In Brazil,

a process of consolidation of smaller regional fibre ISPs is also

ongoing. For example, Vinci Partners is the largest shareholder in

Vero Internet, which has been formed from the consolidation of

eight regional providers in Minas Gerais. Vinci Partners intends to

spend BRL500–750 million (USD109–152 million) – including

the money spent on the acquisitions – in the next 5 years.

Figure 25: NGA coverage by technology, Latin America, 2017–

2025

Figure 26: FTTx capex by technology, Latin America, 2017–

2025

32

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Pe

rce

nta

ge

of

pre

mis

es p

assse

d

Cable, but not FTTx

FTTx, but not FTTP

FTTP

Source: Analysys Mason

0.00.51.01.52.02.53.03.54.04.55.0

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

FTTx c

ap

ex (

US

D b

illio

nOther FTTx

FTTP

Source: Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Contents Worldwide trends

Regional trends

Western Europe

Central and Eastern Europe

Middle East and North Africa

Sub-Saharan Africa

China

Rest of emerging Asia-Pacific

Developed Asia-Pacific

North America

Latin America

Forecast methodology and assumptions

About the author and Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Figure 27: Countries covered in this report, by region

34

Geographical scope: forecasts are provided for 64 countries in 8 regions

EMERGING MARKETS

DEVELOPED MARKETS

North America Western Europe

Developed

Asia–Pacific

Central and

Eastern Europe

▪ Canada

▪ USA▪ Austria

▪ Belgium

▪ Denmark

▪ Finland

▪ France

▪ Germany

▪ Greece

▪ Iceland

▪ Ireland

▪ Italy

▪ Netherlands

▪ Norway

▪ Portugal

▪ Spain

▪ Sweden

▪ Switzerland

▪ UK

▪ Australia

▪ Hong Kong

▪ Japan

▪ New Zealand

▪ Singapore

▪ South Korea

▪ Taiwan

▪ Bulgaria

▪ Croatia

▪ Czech Republic

▪ Estonia

▪ Hungary

▪ Latvia

▪ Lithuania

▪ Poland

▪ Romania

▪ Russia

▪ Serbia

▪ Slovakia

▪ Slovenia

▪ Turkey

▪ Ukraine

The Middle East

and Africa

Emerging

Asia–Pacific

Latin America

▪ Israel

▪ Oman

▪ Qatar

▪ Saudi Arabia

▪ UAE

▪ China

▪ India

▪ Indonesia

▪ Malaysia

▪ Philippines

▪ Thailand

▪ Vietnam

▪ Argentina

▪ Brazil

▪ Chile

▪ Colombia

▪ Mexico

▪ Peru

▪ Uruguay

Sub-Saharan Africa

▪ Ghana

▪ Kenya

▪ Nigeria

▪ South Africa

Source: Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

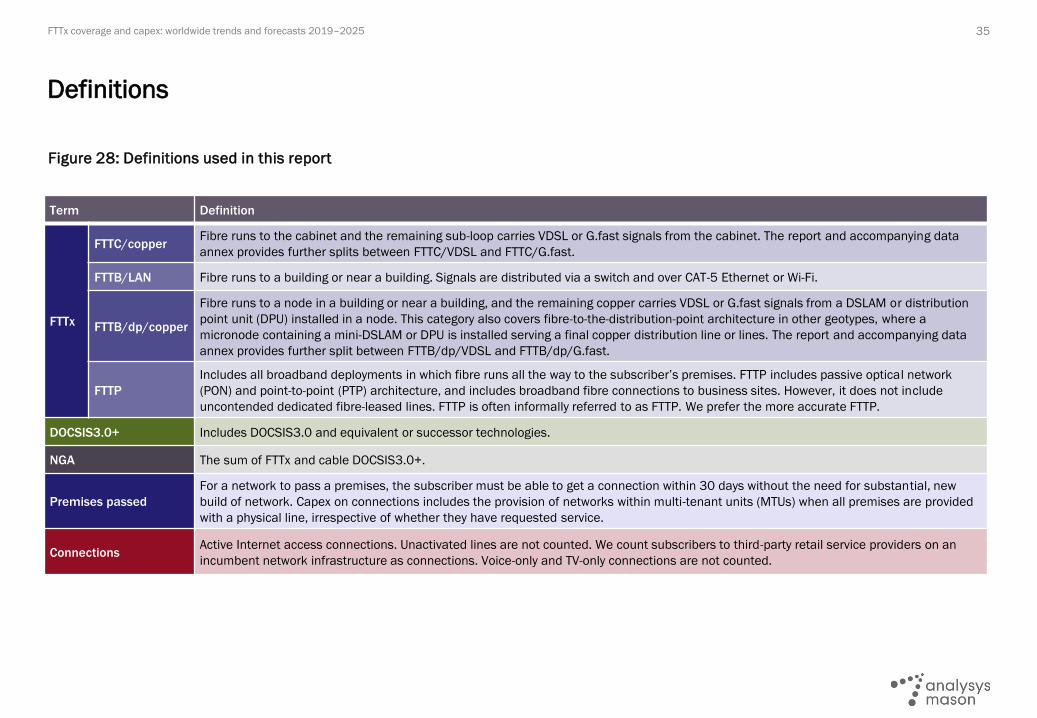

Figure 28: Definitions used in this report

35

Definitions

Term Definition

FTTx

FTTC/copperFibre runs to the cabinet and the remaining sub-loop carries VDSL or G.fast signals from the cabinet. The report and accompanying data

annex provides further splits between FTTC/VDSL and FTTC/G.fast.

FTTB/LAN Fibre runs to a building or near a building. Signals are distributed via a switch and over CAT-5 Ethernet or Wi-Fi.

FTTB/dp/copper

Fibre runs to a node in a building or near a building, and the remaining copper carries VDSL or G.fast signals from a DSLAM or distribution

point unit (DPU) installed in a node. This category also covers fibre-to-the-distribution-point architecture in other geotypes, where a

micronode containing a mini-DSLAM or DPU is installed serving a final copper distribution line or lines. The report and accompanying data

annex provides further split between FTTB/dp/VDSL and FTTB/dp/G.fast.

FTTP

Includes all broadband deployments in which fibre runs all the way to the subscriber’s premises. FTTP includes passive optical network

(PON) and point-to-point (PTP) architecture, and includes broadband fibre connections to business sites. However, it does not include

uncontended dedicated fibre-leased lines. FTTP is often informally referred to as FTTP. We prefer the more accurate FTTP.

DOCSIS3.0+ Includes DOCSIS3.0 and equivalent or successor technologies.

NGA The sum of FTTx and cable DOCSIS3.0+.

Premises passed

For a network to pass a premises, the subscriber must be able to get a connection within 30 days without the need for substantial, new

build of network. Capex on connections includes the provision of networks within multi-tenant units (MTUs) when all premises are provided

with a physical line, irrespective of whether they have requested service.

Connections Active Internet access connections. Unactivated lines are not counted. We count subscribers to third-party retail service providers on an

incumbent network infrastructure as connections. Voice-only and TV-only connections are not counted.

FTTx coverage and capex: worldwide trends and forecasts 2019–2025 36

We take baseline costs for each technology and then apply several context-specific

variables to determine total capex

Source: Analysys Mason

Technology

Baseline

cost to pass

Baseline

cost to

connect

Adjusted for

local costs

Adjusted for

local costs

Adjusted for

geo-type

Adjusted for

cost erosion

Adjusted for

cost erosion

Adjusted for

building type

Forecast

coverage

Forecast

conversion

Adjustment

for overbuild

of previous

NGA

=+Capex per

country per

technology

Active

equipment unit

costs

Passive

equipment unit

costs

Labour and

cost of physical

infrastructure

Based on real

capex

benchmarks

Labour rates

Availability of

physical

infrastructure

Topology of

existing copper

for FTTC (lines

per cabinet)

Likelihood of

vendor

discounts

General unit

cost erosion

Additional costs

such as

vectoring

Labour

efficiencies

over time

(deskilling)

FTTC/VDSL

FTTB/VDSL

FTTB/LAN

FTTP

If an operator

shifts from, for

example,

FTTB/VDSL to

FTTP, then

assume some

costs already

sunk

For FTTP,

separate

calculations

are made for

incumbent and

for other

operators.

Therefore, the

cost of overlaid

networks is

taken into

account

×

×

Figure 29: Capex model outline

▪ Forecast levels of coverage are what we consider to be the most likely outcome based on operators’ plans. Conversion takes into

account macro-economics and inter- and intra-country trends, which we monitor on a quarterly basis. Our capex forecasts are derived

as follows.

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Figure 30: Basic overview of FTTx network topologies and elements

37

Top-level breakdown of the relative costs of FTTx technologies: basic topologies

Source: Analysys Mason

Switch MSANs New modemFibre mostly in

existing duct

Existing

copper

Existing

copper

Switch New modem

Basement MSANs

Outdoor micro-

nodes

Fibre mostly in

existing duct

Existing

copperSplitter/switch

Fibre mostly in

existing duct

OLT Splitter ONUFibre mostly in

existing duct

Fibre mostly in

existing duct

In-building or aerial

fibre

OLT Switch ONUFibre mostly in

existing duct

In-building

or aerial fibre

Fibre mostly in

existing duct

Basement

switch

Fibre CAT 5

or Wi-FiSwitch

Fibre

mostly aerial

Other point

of interconnection

▪ Our assumptions on capital costs are based on a breakdown of network elements for the five main kinds of telco NGA deployment:

FTTC/VDSL, FTTB/VDSL, FTTB/LAN, FTTP/GPON and FTTP/PTP. In each case (except FTTB/LAN), our starting point is a typical urban

exchange serving 12 000 residential subscribers, connecting to 80 cabinets, each serving 150 subscribers, with each cabinet

connecting to distribution points typically serving 10 subscribers. FTTB/LAN costs are simply built on benchmarks because they will

vary greatly.

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Contents Worldwide trends

Regional trends

Western Europe

Central and Eastern Europe

Middle East and North Africa

Sub-Saharan Africa

China

Rest of emerging Asia-Pacific

Developed Asia-Pacific

North America

Latin America

Forecast methodology and assumptions

About the author and Analysys Mason

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

About the author

39

Stephen Wilson (Principal Analyst) is the lead analyst for Analysys Mason’s Fixed Broadband Services research programme. He leads Analysys

Mason’s annual FTTx coverage, capex and conversion forecasts, and other recent areas of focus include examining fixed broadband operators’

home Wi-Fi strategies. Stephen has more than 10 years of experience in the telecoms sector and is a graduate in Philosophy, Politics and

Economics from St Catherine's College, Oxford University.

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

CONSULTING

We deliver tangible benefits to clients across the telecoms

industry:

▪ communications and digital service providers, vendors,

financial and strategic investors, private equity and

infrastructure funds, governments, regulators, broadcasters,

and service and content providers.

Our sector specialists understand the distinct local challenges

facing clients, in addition to the wider effects of global forces.

We are future-focused and help clients understand the challenges

and opportunities that new technology brings.

RESEARCH

Our dedicated team of analysts track and forecast the different

services accessed by consumers and enterprises.

We offer detailed insight into the software, infrastructure and

technology delivering those services.

Clients benefit from regular and timely intelligence, and direct

access to analysts.

Analysys Mason’s consulting services and research portfolio

40

Analysys Mason’s consulting and research are uniquely positioned

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Research from Analysys Mason

41

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

Consulting from Analysys Mason

42

FTTx coverage and capex: worldwide trends and forecasts 2019–2025

PUBLISHED BY ANALYSYS MASON LIMITED IN MARCH 2020

Bush House • North West Wing • Aldwych • London • WC2B 4PJ • UK

Tel: +44 (0)20 7395 9000 • Email: [email protected] • www.analysysmason.com/research • Registered in England and Wales No. 5177472

© Analysys Mason Limited 2020. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means – electronic,

mechanical, photocopying, recording or otherwise – without the prior written permission of the publisher.

Figures and projections contained in this report are based on publicly available information only and are produced by the Research Division of Analysys Mason Limited independently of any

client-specific work within Analysys Mason Limited. The opinions expressed are those of the stated authors only.

Analysys Mason Limited recognises that many terms appearing in this report are proprietary; all such trademarks are acknowledged and every effort has been made to indicate them by the

normal UK publishing practice of capitalisation. However, the presence of a term, in whatever form, does not affect its legal status as a trademark.

Analysys Mason Limited maintains that all reasonable care and skill have been used in the compilation of this publication. However, Analysys Mason Limited shall not be under any liability for

loss or damage (including consequential loss) whatsoever or howsoever arising as a result of the use of this publication by the customer, his servants, agents or any third party.