Fuel Oil Price Risk Management … and perspectives from the financial side Hartley Connett Executive Director, Marketing Mitsui & Co. Energy Risk Management (U.S.A.), Inc. 2007 Fuel Oil & Energy Buyers’ Conference October 31, 2007

Transcript

Fuel Oil Price Risk Management

… and perspectives from the financial side

Hartley ConnettExecutive Director, Marketing

Mitsui & Co. Energy Risk Management (U.S.A.), Inc.

2007 Fuel Oil & Energy Buyers’ Conference October 31, 2007

2

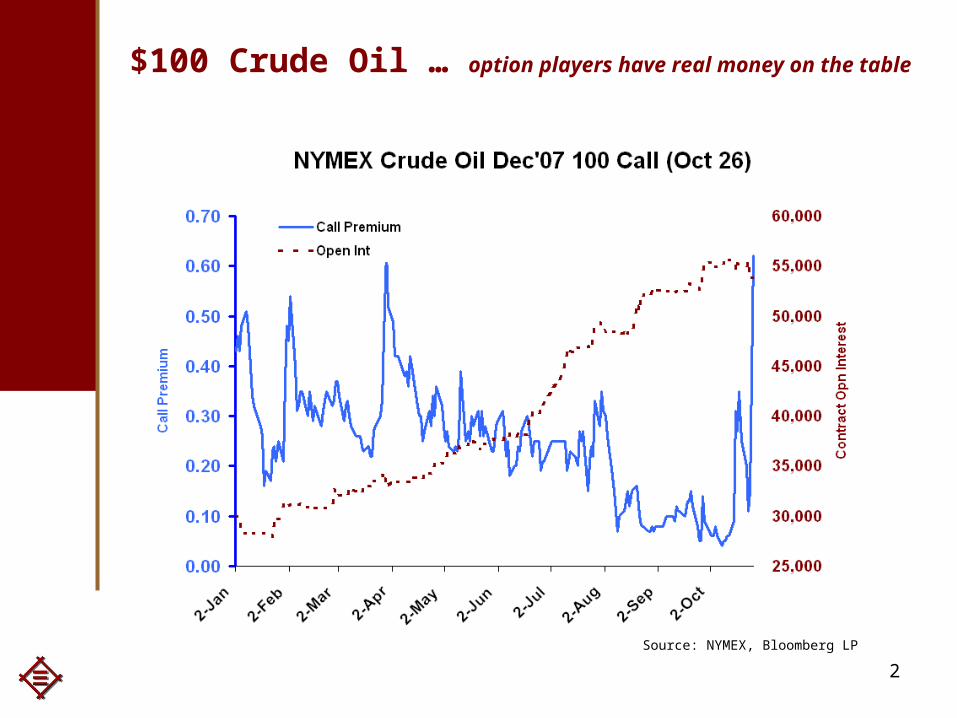

$100 Crude Oil … option players have real money on the table

Source: NYMEX, Bloomberg LP

3

Fundamental Drivers in 2007 Global Security Risk

Iraq and The Middle East

Nigeria

Turkey and PKK (recent)

Global Supply & Demand Balances

Economic Expansion in Asia

OPEC production Cuts

No significant excess capacity outside OPEC

In OPEC, only the Saudis

Weaker US Dollar

US Refining stress

Tokyo Electric Power Co. (more recent)

Asian fuel oil supply constraints develop later in year (more recent)

Lower Russian exports

Iran becomes importer

4

12/29/06 Saddam Hussein Execution

Large short put position on NYMEX

01/23/07 – Proposal to increase SPR to 1.5 billion bbls.

3/20/07 OPEC keeps

level Unchanged

3/22/07 Iran captured 15 British Soldiers

9/01/07 US Inventory

shows much larger than expected

drawdowns

Mid August

Hurricane’s do not materialize in US

5/10/07 Disruptions from

Nigeria

and

Start of US Driving Season

10/28/07 Oil follows Equity Market reaction to Subprime Crisis

7/16/07 TEPCO Outage

2 Q 07 Cushing Stocks Full - Refinery Offline

2007 Timeline: NYMEX Spot WTI

10/15/07Turkey /

PPK

Source: NYMEX, Charts provided by Future Source www.futuresource.com

Recently, New US Sanctions against Iran

5

Consumer Hedging Discussion

3 Simple Themes in a Core Hedging Strategy

Theme 1- Historical Price Distribution… Where are current prices versus historical distribution?

Theme 2- Forward Curve and Best Value

… Where is the best value along the curve?

Theme 3- Product relationship to Crude Oil

… What are the crackspreads doing?

6

Consumer HedgingTheme 1 ... Where are current prices along the historical continuum?

Theme 1

Prices in 2008 (and beyond) are at the highest portion of the historical distribution curve

Accumulate at the averages, add more aggressively below if opportunity presents.

Current prices are far from the ‘best world’ from a Consumer’s standpoint

For Consumer Hedging, the recommendation is to use Defensive Strategies

7

Hedging Theme 1 – Applicable Strategies

Examples of Defensive Strategies

… Option products are effective.

Caps … ‘price insurance’, plain vanilla, upfront premium in return for upside price protection above a certain price. Weigh Premium Cost versus Opportunity Cost.

Collars … plain vanilla, purchased cap financed by sold floor, typically designed to be costless

Capped Swap … a vanilla swap with an embedded option, provides enhanced (lower) fixed rate swap in return for a maximum upside payout

Capped Collar … enhanced collar (lower floor and/or more valuable initial cap strike) in return for maximum payout above the cap

8

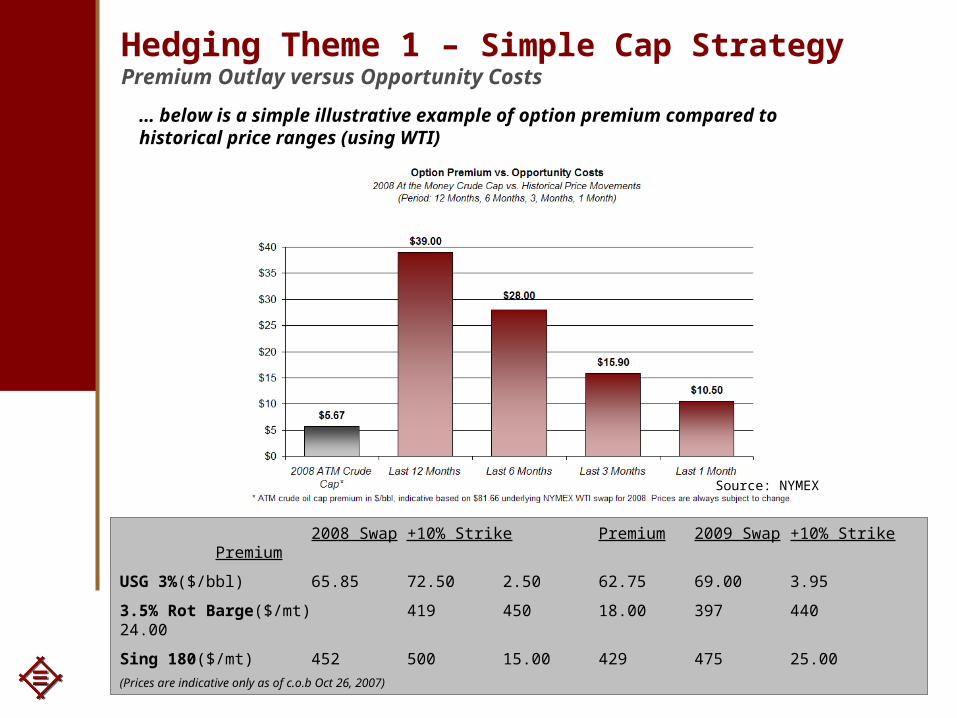

Hedging Theme 1 – Simple Cap Strategy Premium Outlay versus Opportunity Costs

… below is a simple illustrative example of option premium compared to historical price ranges (using WTI)

In backwardated markets, consumers should consider extending tenors to achieve a lower average price ...

Vanilla Swaps

Option products can also be effective …

Hedging with Extendible Structures (option embedded products)

Extendible Swaps

Extendible Capped Swaps

Extendible Collars

Extendible Structures – general explanation

• Consumer obtains an enhanced hedge (fixed swap or collar) for an initial period.

• In return, the consumer grants the counterparty (Mitsui) the right to extend the terms of the initial hedge into a future period (pre-determined at outset).

• The extendible portion can only be exercised 1-time on a pre-determined date, at the preference of the counterparty.

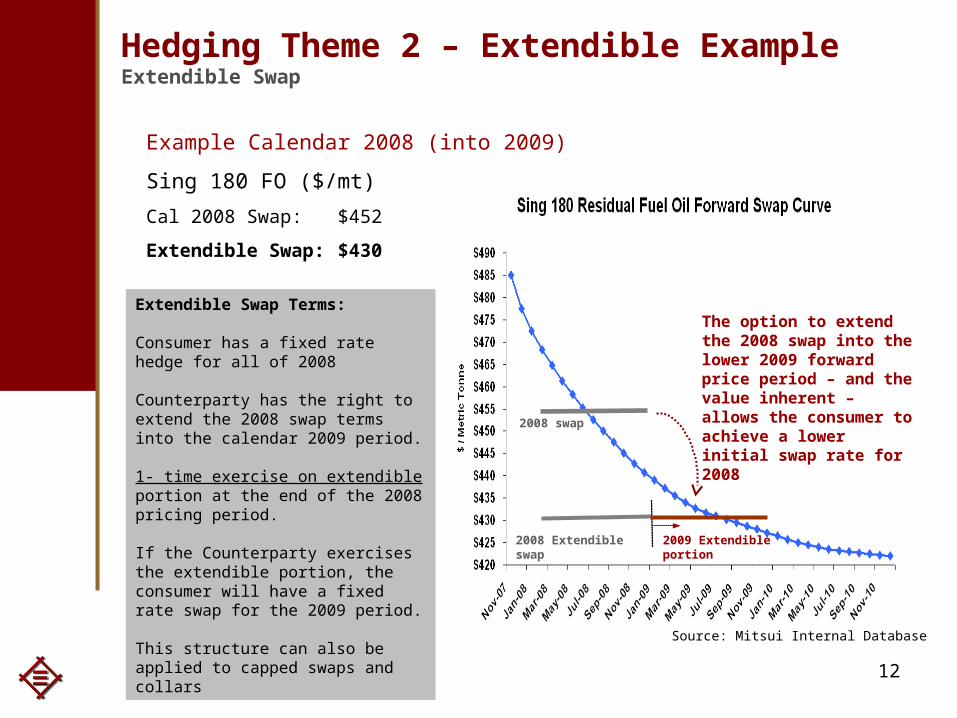

WTI USG 3% ($/bbl) 3.5% Rot Barge($/mt) Sing 180($/mt)

The option to extend the 2008 swap into the lower 2009 forward price period – and the value inherent – allows the consumer to achieve a lower initial swap rate for 2008

Extendible Swap Terms:

Consumer has a fixed rate hedge for all of 2008

Counterparty has the right to extend the 2008 swap terms into the calendar 2009 period.

1- time exercise on extendible portion at the end of the 2008 pricing period.

If the Counterparty exercises the extendible portion, the consumer will have a fixed rate swap for the 2009 period.

This structure can also be applied to capped swaps and collars

Source: Mitsui Internal Database

13

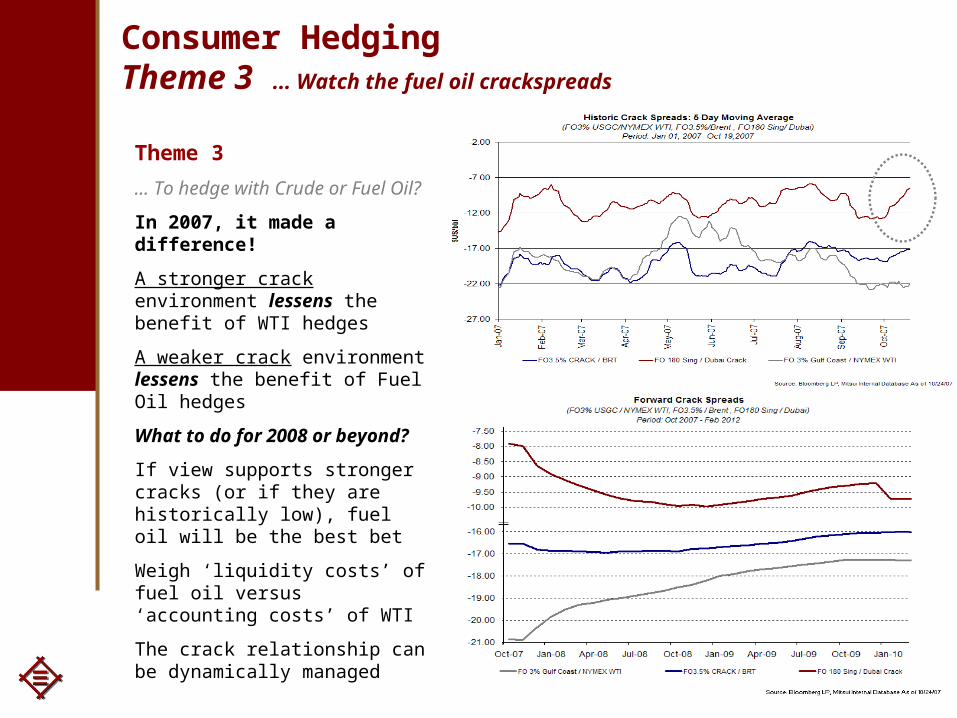

Consumer HedgingTheme 3 ... Watch the fuel oil crackspreads

Theme 3

… To hedge with Crude or Fuel Oil?

In 2007, it made a difference!

A stronger crack environment lessens the benefit of WTI hedges

A weaker crack environment lessens the benefit of Fuel Oil hedges

What to do for 2008 or beyond?

If view supports stronger cracks (or if they are historically low), fuel oil will be the best bet

Weigh ‘liquidity costs’ of fuel oil versus ‘accounting costs’ of WTI

The crack relationship can be dynamically managed

14

Take away; The 3 Core Themes

• Theme 1 - Historical price continuum

Use Defensive Strategies at the Highs, use more aggressive strategies at the historical averages or below

Options can help! … look at premium in context to historical ranges and volatility … being ‘wrong’ premium can be [much] less expensive in the long-run

• Theme 2 - Look for best value along the curve

In backwardated markets, extend tenors to achieve lower average hedge price … extendible strategies work well … lower volatility in forward periods

• Theme 3 - Watch the product-to-crude oil relationships

Refiners do! … can help achieve more effective hedge results ... also a Defensive Strategy

15

Days of Supply of OECD Commercial Oil Stocks

Forecast

44

46

48

50

52

54

56

58

Jan 2002 Jan 2003 Jan 2004 Jan 2005 Jan 2006 Jan 2007 Jan 2008

Days ofsupply

NOTE: Colored band represents the 5-year minimum/maximum range for each month.

Short-Term Energy Outlook, October 2007

The Longer Fundamental OutlookSupportive fundamentals remain in place … adding specific factors to the residual sector

Existing fundamental drivers remain in place for the most part

Adding …

•Global Supply & Demand Imbalance

•Q3 global stock draw

•Implied Days Supply

•US Total Petroleum Inventories heading towards lower end of the historical average

Adding for residual sector …

•Projected global fleet size by 2010 (long-term)

•Longer-term impact of upgrades for refinery coking and hydrocracking units on global RFO supply (long-term)

TOTAL US Petroleum Inventories Exlcuding Crude Oil & SPR

600,000

620,000

640,000

660,000

680,000

700,000

720,000

740,000

760,000

780,000

,000

Bbl

s

5-Yr Max/Min Range 5-Yr Avg 2006 2007

Bottom line … the overall picture remains Bullish.

Source: Bloomberg LP, EIA

16

The from Contango to Backwardation

… supports the theory of a fundamentally tight market

Spot NYMEX with 1st Line vs. 12th Line Crude Spread

Singapore prices are leading the way at the moment

Depleted Russian exports into Singapore

Iranian product out of the market

Pull of product into the Arab Gulf

Europe

Poor demand at moment for Utility spec bbls

Healthier demand for Bunkers

Med

Stronger demand for 1% coming from Mediterranean Utilities

Buying Med 1% / Selling NWE 1%

US

Is 1% FO high vs. Natural Gas?

A trade we see interest in Source: NYMEX, Bloomberg LP

19

The SPR(s) and Crude Oil PricesNot the only factor of course, but a ‘wild card’ going forward

Going forward, SPR policy of the US Administration will deserve attention, as will China’s SPR policy

Source: Bloomberg LP , NYMEX

New YorkTelephone: +1 (212) 878 6750

AsiaTelephone: +44 20 7489 6741

LondonTelephone: +44 20 7489 6741

SydneyTelephone: +61 2 9256 9596

Thank You For Listening

LONDON

SYDNEY

NEW YORK

SINGAPORE

Mitsui & Co. Energy Risk Management, Ltd. Worldwide Locations

TOKYO

Hartley ConnettExecutive Director, MarketingMitsui & Co. Energy Risk Management (USA), Inc.As agent for Mitsui & Co. Energy Risk Management Ltd.200 Park Avenue31st FloorNew York, NY 10166Desk- 212.878.6750Cell- 914.907.7508Fax- [email protected]